GOLD: NUMBER OF NOTICES FILED FOR MAY/2026: 137 CONTRACTs NOTICES FOR 13,700 OZ or 0.4261 TONNES

total notices so far: 3463 contracts FOR 346,300 OZ OR 10.7713 TONNES

SILVER NOTICES: 69 NOTICE(S) FILED FOR 0.345 MILLION OZ /

total number of notices filed so far this month : 4998 CONTRACTS (NOTICES) for 24.990 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY OUR NEXT QUEUE JUMP OF 22 CONTRACTS FOR 110,000 OZ/NEW STANDING ADVANCES TO 30.540 MILLION OZ/.//

SUMMARY OF OUR MAY 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 8.705 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 22 CONTRACTS/110,000 OZ//NEW STANDING ADVANCES TO 30.540 MILLION OZ//

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 278 CONTRACT QUEUE JUMP FOR 27800 OZ/ (0.8646 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 118 CONTRACTS OR 11800 OZ (.3670 TONNES)/STANDING NOW ADVANCES TO 13.399 TONNES OF GOLD.

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 118 CONTRACTS/11800 OZ// 0.3670 TONNES//NEW STANDING IS NOW ADVANCES TO 13.399 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 23.235 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONG

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE 2104 CONTRACTS TO AN OI OF 99,036 ADVANCING A BIT FROM ITS ALL TIME LOW SET MAY 1.

EFP ISSUANCE 600 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 600 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2104 CONTRACTS AND ADD TO THE 600 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 2704 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $3.75

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 13.752 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $3.75

2.ASIAN AFFAIRS MAY 7 /2025

SHANGHAI CLOSED UP 19.92 PTS OR 0.48%

HANG SENG CLOSED UP 412.50 PTS OR 1.51%

Nikkei CLOSED UP 3,449.38 PTS OR 5.80%

//Australia’s all ordinaries CLOSED DOWN 0.10%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.8019

/ OFFSHORE CLOSED UP AT 6.7991 Oil DOWN TO 93.13 dollars per barrel for WTI and BRENT DOWN TO 99.13 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING UP (6.8019) OFFSHORE YUAN TRADING UP TO 6.7991 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG 3771 CONTRACTS DOWN TO AN OI OF 371,703 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET LATE LAST MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD ZERO T.A.S. LIQUIDATION DURING WEDNESDAY’S TRADING. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT ALSO SOME SPECULATORS STILL GOING TO THE SHORT SIDE WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS APRIL CONTRACT MONTH!!

THE STRONG SIZED GAIN ON OUR TWO EXCHANGES OCCURRED WITH OUR GAIN IN PRICE IN GOLD (UP $124.70).

WE THUS HAD A STRONG GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 6046 CONTRACTS (OR 18.80 TONNES) WITH OUR GAIN IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.EQUATING TO 2275 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF ZERO CONTRACTS FOR RISK ISSUANCE IN GOLD TOTALLING 0 CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK YESTERDAY MAY 7. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: ONE ISSUANCE SO FAR FOR 109 CONTRACTS OR 10,900 OZ OR 0.3390 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: ONE ISSUANCE SO FAR FOR 109 CONTRACTS, 10900 OZ OR 0.3390 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

DETAILS ON OUR NEW MAY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 6046 CONTRACTS WITH OUR GAIN IN PRICE ($124.70). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A STRONGER SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 2788 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT IS NOW IN FULL FORCE DURING LAST WEEK DURING LONDON COMEX AND LBMA/OTC OPTION EXPIRY WEEK!! (INITIAL MAY CONTRACT MONTH)

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS FIRST ISSUANCE FOR 0.3390 TONNES ISSUED YESTERDAY MAY 6.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 11,800 OZ (.3670 TONNES) TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 10,900 OZ OR 0.3390 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 13.399 TONNESS

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING MAY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $124.70)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION // COMEX SESSION// WITH OUR GAIN IN PRICE , OUR LONG SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI //

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $124.70

WE HAD 3975 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 6046 CONTRACTS OR 604,600 OZ OR 18.80 TONNES

INITIAL GOLD COMEX

MAY DELIVERY MONTH

MAY 7 2026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 1 i) BRINKS 32.151 oz (1 kilobar) total withdrawal: 32.151 oz or .0009 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 137 CONTRACTS OR 13700 OZ 0.4261 TONNES OF GOLD |

| No of oz to be served (notices) | 736 Contracts 73,600 OZ 2.289TONNES |

| Total monthly oz gold served (contracts) so far this month | 3463 notices 346,300 oz 10.7713 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 1

ENTRIES; 1

i) BRINKS 32.151 oz

(1 kilobar)

total withdrawal: 32.151 oz or 0009 tonnes

xxxx

adjustments: 0

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF MAY OI STANDS AT 873 CONTRACTS HAVING A LOSS OF 15 CONTRACTS.

WE HAD 133 CONTRACT SERVED ON WEDNESDAY SO WE GAINED ANOTHER STRONG 118 CONTRACTS OR 11800 OZ (0.3270 TONNES) UNDEREWENT A QUEUE JUMP TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI LOST BY 2979 CONTRACTS DOWN TO AN OI OF 253,356

JULY GAINED 82CONTRACTS UP TO AN OI OF 1081.

We had 137 contracts filed for today representing 13,700oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 137 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 41 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (3,463) to which we add the difference between the open interest for the front month of MAY (873 CONTRACTS) minus the number of notices served upon today 137 x 100 oz per contract) equals 419,900 OZ OR (13.060 Tonnes of gold) to which we add our first exchange for risk issuance for 10,900 oz or 0.3390 tonnes//new standing for gold/May again advances to 13.399 tonnes.

THUS: INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (3,463) to which we add the difference between the open interest for the front month of MAY(873 CONTRACTS) minus the number of notices served upon today 137 x 100 oz per contract) equals 419,900 OZ OR (13.060 Tonnes of gold) plus we must add our first exchange for risk issuance of 10,900 oz or 0.3390 tonnes/new standing advances to 13.399 tonness

new total of gold standing in MAY ADVANCES TO 13.399 TONNES//

TOTAL COMEX GOLD STANDING FOR MAY 13.399 TONNES TONNES WHICH IS NOW STRONG FOR THIS NORMALLY NON ACTIVE DELIVERY MONTH OF MAY.

confirmed volume WEDNESDAY confirmed 186,921 poor many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

the number provided do not match from yesterday!!!

total pledged gold: 1,964,079.919 oz 61.091 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,964,079.919 tonnes oz 61.091 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 29,127,882.874oz

TOTAL REGISTERED GOLD 15,827,899.555 OZ 492.314 tonnes

TOTAL OF ALL ELIGIBLE GOLD 13,3040.982.720 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,863,800 oz ((REG GOLD- PLEDGED GOLD)=

431.22 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

MAY DELIVERY MONTH

MAY 7

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 entries |

| Deposits to the Dealer Inventory | 0 entries xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 0 ENTRIES |

| No of oz served today (contracts) | 69 CONTRACT(S) (0.345 MILLION OZ |

| No of oz to be served (notices) | 1110Contracts (5.550 MILLION oz) |

| Total monthly oz silver served (contracts) | 4998 contracts 24.990 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

0 entries

the comex is being drained of silver

adjustments:1

a) Manfra: dealer to customer; 296,986.874 oz

WEDNESDAY volume: 59,420 oz// AWFUL

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 79.838 MILLION OZ//.TOTAL REG + ELIGIBLE. 312.752 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2026 OI: 1179 OPEN INTEREST CONTRACTS FOR A LOSS OF 123 CONTRACTS. WE HAD 145 CONTRACTS SERVED UPON ON WEDNESDAY SO WE GAINED 22 CONTRACTS OR 110,000 OZ WHERE THESE BOYS WILL TRY THEIR LUCK TRYING TO TAKE SILVER DELIVERY OVER AT THE COMEX RATHER THAN TROTTING OVER TO LONDON.

JUNE SAW A GAIN OF 287 CONTRACTS UP TO 2458 OI CONTRACTS

JULY SAW A GAIN OF 1835 CONTRACTS UP TO 74,373 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 69 or 345,000 oz

CONFIRMED volume WEDNESDAY; 59,420 poor

AND NOW MAY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 4998 X5,000 oz = 24.998 MILLION oz

to which we add the difference between the open interest for the front month of MAY (1179) AND the number of notices served upon today (69 )x (5000 oz)

Thus the standings for silver for the MAY 2026 contract month: (4998 )Notices served so far) x 5000 oz + OI for the front month of MAY (1179) minus number of notices served upon today (69)x 5000 oz equals silver standing for the MAY..contract month equating to 30.540 MILLION OZ.+

NEW STANDING ADVANCES T0: 30.540 MILLION OZ WHICH IS STILL PRETTY GOOD FOR THIS ACTIVE DELIVERY MONTH OF MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 79.838 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/312.752 million: 44.83

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAY 7 /2026/WITH GOLD UP $15.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.853 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1033.197TONNES

MAY 6 /2026/WITH GOLD UP $124.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.718 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1034.05TONNES

MAY 5 /2026/WITH GOLD UP $33.75 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 4 /2026/WITH GOLD DOWN $106.65 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 1 /2026/WITH GOLD UP $13.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.427 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1035.768 TONNES

APRIL 30/2026/WITH GOLD UP $19.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.142 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1039.195 TONNES

APRIL 29/2026/WITH GOLD DOWN $45.70 TODAY/NO CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 28/2026/WITH GOLD DOWN $85.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

APRIL 1/2026/WITH GOLD UP $134.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.143 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1047.276 TONNES

MAR 31/2026/WITH GOLD UP $119.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.429 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1046.133 TONNES

MAR 30/2026/WITH GOLD UP $33.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.143 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1049.562

MAR 27/2026/WITH GOLD UP $103.55 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.285 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.705

MAR 26/2026/WITH GOLD DOWN $213.05 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.580 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.42

MAR 25/2026/WITH GOLD UP $155.30 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.300 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1053.000

MAR 24/2026/WITH GOLD DOWN $7.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.286 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1052.705

MAR 23/2026/WITH GOLD DOWN $165.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 5.149 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1056.991

MAR 20/2026/WITH GOLD DOWN $39,55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1062.135

MAR 19/2026/WITH GOLD DOWN $XXX TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 2.57 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1066.99

MAR 18/2026/WITH GOLD DOWN $111.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1069.564 TONNES

MAR 17/2026/WITH GOLD UP $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 0.857 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.708 TONNES

GLD INVENTORY: 1033.197 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

MAY 7 WITH SILVER UP $2.26: NO CHANGES IN SILVER INVENTORY AT THE SLV: / // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 6 WITH SILVER UP $3.75: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.724 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 5 WITH SILVER UP $0.21: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 4 WITH SILVER DOWN $3.05: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 1 WITH SILVER UP $2.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.905 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 484.338 MILLION OZ

APRIL 30 WITH SILVER UP $2.03: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.991 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 485.243MILLION OZ

APRIL 29 WITH SILVER DOWN $1.95: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 28 WITH SILVER DOWN $2.05: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

APRIL 1 WITH SILVER UP $1.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND WITHDRAWAL OF 0.453 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 491.079 MILLION OZ

MAR 31 WITH SILVER UP $4.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.893 MILLION OZ FROM THE SLV // :INVENTORY RESTS AT 491.532 MILLION OZ

MAR 30 WITH SILVER UP $0.74: NO CHANGES IN SILVER INVENTORY AT THE SLV: // :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 27 WITH SILVER UP $1.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV// :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 26 WITH SILVER DOWN $4.75: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 25 WITH SILVER UP $3.25: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 24 WITH SILVER DOWN $0.15: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT DEPOSIT OF 10.505 MILLION OZ INTO THE SLV :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 23 WITH SILVER UP $0.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// NO CHANGE IN INVENTORY/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 20 WITH SILVER DOWN $1.92: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.490 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 19 WITH SILVER DOWN $6.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.9444 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 490.761 MILLION OZ

MAR 18 WITH SILVER DOWN $2.36: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 1.087 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 494.792 MILLION OZ.

MAR 17 WITH SILVER DOWN $0.89: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 493.705 MILLION OZ.

CLOSING INVENTORY 484.130 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

JESSE COLUMBO\

JOHN RUBINO

3.CHRIS POWELL AND HIS GATA DISPATCHES:

4.ANDREW MAGUIRE LIVE FROM THE VAULT 270 and 269

LONDON PAUL//MUST VIEW

5. COMMODITY REPORT/JET FUEL

UK Jet Fuel Rationing Risks Emerge As Goldman Warns Of “Extreme Physical Tightness”

Thursday, May 07, 2026 – 05:45 AM

Brent crude futures briefly tumbled below $100 a barrel on Wednesday morning after an Axios report indicated the Trump administration and Tehran were working toward a one-page memorandum of understanding to end the war and reopen the Strait of Hormuz.

Still, any near-term peace deal would not immediately normalize the badly fractured global energy supply chains. Crude products markets remain physically tight, and the damage from months of disrupted tanker flows will take time to unwind. Some countries may already be entering a critical point, with jet fuel and diesel inventories at risk of being drawn down to dangerously low levels in the months ahead.

Goldman analysts, led by Michele Della Vigna, warned about diesel and jet fuel availability in Europe ahead of the summer months, noting that “extreme physical tightness in summer/early autumn” is a scenario they are forecasting.

“We believe jet fuel prices in Europe will need to remain elevated to redirect cargoes from other regions, covering 50% of the shortfall in disrupted volumes from the Middle East through Hormuz and from Asian exporters no longer exporting to Europe,” Della Vigna told clients.

Della Vigna, the head of EMEA natural resources research at Goldman, pointed out that “some countries (the UK in particular) could end up with extremely low inventories, and it’s possible that rationing measures would be put in place to slow inventory draw.”

Readers have been well informed about the looming jet fuel crisis set to hit Europe this summer (read here & here & here & here), as well as JPMorgan’s March take on how the energy crisis is spreading across regions (read here).

As we detailed on Tuesday, President Trump’s push to reopen the Hormuz chokepoint at the start of the week likely reflects the beginning of a one-month countdown to accelerated energy chaos if the critical waterway is not reopened. The risk is no longer confined to crude markets. Prolonged disruption through Hormuz is spreading into refined-product supply chains, with Europe’s jet fuel and diesel inventories facing the brunt of physical tightness heading into summer and early autumn.

Della Vigna estimated that Europe faces a gross jet fuel loss of about 500,000 barrels a day from Gulf-area exporters and Asian tankers transiting Hormuz, and assumes that half of that shortfall can be offset by redirected U.S. and West African energy flows, leaving a net loss of approximately 250,000 barrels a day. For diesel, he assumes the full 220,000 barrels-a-day loss is absorbed by European stocks.

Exhibit 3: We estimate a gross jet fuel loss of c.500 kb/d from Middle East Gulf and Asian exporters and we show the sensitivity to different % of exports subtitutions coming from other regions

He singled out the UK as having the highest-risk jet fuel market because it is Europe’s largest net importer of jet fuel, at about 195,000 barrels a day, and lacks proper reserves. He warned that UK commercial stocks could fall below 10 days of cover by midsummer, raising the risk of rationing, which in turn would impact commercial flights.

Della Vigna continued:

Under our commodities teams’ base case (Gulf normalization in June), we see European jet fuel inventories – on commercial stocks alone, excluding government emergency reserves – falling to the IEA’s critical 23-day shortage threshold by end-May and breaching it in June, slightly more aggressive than the IEA’s own assessment as we account for the disruption of Asian-origin cargoes transiting the Strait.

Under an adverse scenario (normalization delayed to July), stocks could be depleted entirely by year-end (Exhibit 1). Diesel faces a more gradual erosion given lower ME import dependence.

At the country level, the UK appears most at risk of rationing (Exhibit 4), with commercial stocks falling below 10 days of cover by mid-summer given high starting import dependence and no government reserves. Net exporters such as the Netherlands and Greece are more insulated but would still be affected through higher prices.

Exhibit 1: Jet Fuel is the tightest oil product market

Exhibit 4: For jet fuel, the UK is most at risk with low inventories and high reliance on imports

To offset losses, Europe has drawn in more jet fuel and barrels from Nigeria’s Dangote refinery, but Della Vigna said prices will need to remain elevated to redirect even more tankers to the energy-stricken continent.

Bloomberg’s Javier Blas notes, “US refiners are going gangbusters trying to solve the global jet-fuel shortage (and to cash in record high margins).”

On the topic of airlines, he said carriers on the continent have already slashed summer capacity by low single digits, while Middle East schedules have been reduced by high double digits through late June.

Exhibit 8: Low single-digit capacity cuts on EU short-haul post conflict

Exhibit 9: Similar cuts on Transatlantic capacity

It’s clear Europe has a jet fuel problem. And this won’t be solved by Brussels’ weird obsession with ‘green’ energy.

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 19.92 PTS OR 0.48%

HANG SENG CLOSED UP 412.50 PTS OR 1.51%

Nikkei CLOSED UP 3,449.38 PTS OR 5.80%

//Australia’s all ordinaries CLOSED DOWN 0.10%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.8019

/ OFFSHORE CLOSED UP AT 6.7991 Oil DOWN TO 93.13 dollars per barrel for WTI and BRENT DOWN TO 99.13 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING UP (6.8019) OFFSHORE YUAN TRADING UP TO 6.7991 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 6.8019

OFFSHORE YUAN: UP TO 6.7991

1.HANG SANG CLOSED UP 412.50 PTS OR 1.57%

2. Nikkei closed

WEST TEXAS INTERMEDIATE OIL DOWN TO 93.22

BRENT; 99.13

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX DOWN TO 97,70/// EURO RISES TO 1.1772 UP 23 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +2.486 DOWN 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.37… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.738 UP 2 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP( 6.8019 AND OFFSHORE: UP AT 6.7991

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.9890 Italian 10 Yr bond yield DOWN to 3.736// SPAIN 10 YR BOND YIELD DOWN TO 3.413%

3i Greek 10 year bond yield DOWN TO 3.670%

3j Gold at $4734.20 //Silver at: 80.41 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 3/ 100 roubles/75.17

3m oil (WTI) into the 93 dollar handle for WTI and 99 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.32 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.488% DOWN 2 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.738 UP 2 PTS..: USA/SF this 0.7774 as the Swiss Franc . Euro vs SF: 0.9157

USA 10 YR BOND YIELD: 4.335 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.927 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.843 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.25 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 4.9320 DOWN 2 PTS

30 YR UK BOND YIELD: 5.620 DOWN 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.497 DOWN 2 BASIS PTS

5 YR CANADA BOND YIELD: 3.152 DOWN 1 BASIS PTS.

1a New York Opening report

“Semi-Irrational Chase” Sends Futures To Another Record High, Oil Drops On Iran Optimism

by Tyler Durden

Thursday, May 07, 2026 – 08:27 AM

The global market meltup is rolling on. US stock futures inch higher, but are off session highs, with oil falling for a third straight day as traders waited for updates on a potential US-Iran peace deal that would reopen oil flows through the Strait of Hormuz. As of 8:00am ET, S&P and Nasdaq futures were 0.1% higher, after the benchmarks notched back-to-back record highs. In premarket trading, most Mag 7 stocks were higher although Arm Holdings dropped 8% after the chip company reported weak fourth-quarter royalty revenue, hurt by sluggishness in the smartphone industry; the company warned about weaker demand for lower-end phones due to higher memory cost. Whirlpool plunged 18% after the household appliance manufacturer cut its revenue forecast for the full year, missing the average analyst estimate. Overseas indexes are also rising, bolstered by stocks tied to artificial intelligence. Japan’s Nikkei 225 was a particular standout, climbing 5.6% after an 18% rally in Softbank shares. Brent traded near $99 a barrel, extending a 12% slump in the two prior sessions on mounting confidence that an agreement in the Middle East is within reach. The dollar headed for its worst week in a month. Global bonds continued their advance as inflationary pressures receded. Today’s US economic data calendar slate includes 1Q preliminary nonfarm productivity and jobless claims (8:30am), March construction spending (10am), April New York Fed 1-year inflation expectations (11am) and March consumer credit (3pm). Fed speaker slate includes Hammack (10am, 2:05pm), Daly (12:30pm), Kashkari (1pm) and Williams (3:30pm)

In premarket trading, Mag 7 stocks are mostly higher (Tesla +1.7%, Alphabet +1.1%, Nvidia +0.1%, Microsoft +0.7%, Amazon +0.3, Meta Platforms +0.02%, Apple -0.1%).

- Albemarle (ALB) climbs 6% after the chemical producer reported net sales for the first quarter that beat the average analyst estimate.

- Arm Holdings ADRs (ARM) drop 8% after the chip company reported weak fourth-quarter royalty revenue, hurt by sluggishness in the smartphone industry. Daiwa’s analyst notes that there was weaker demand for lower-end phones due to higher memory cost.

- Celsius Holdings (CELH) rises 4% after the energy drink maker’s first quarter adjusted Ebitda and revenue beat consensus estimate.

- Coherent (COHR) drops 3% as analysts note that the optical communications company’s gross margins underwhelmed.

- DoorDash (DASH) jumps 10% after the delivery firm gave a forecast for order value in the current period that topped analyst estimates, signaling healthy consumer demand for its services in the US and international markets.

- Fluence Energy (FLNC) jumps 31% after the company reported a narrower-than-estimated second-quarter adjusted Ebitda loss. Additionally, Fluence maintained its 2026 total revenue forecast, which has a midpoint above the average analyst estimate.

- Fortinet (FTNT) gains 15% after the cybersecurity company forecast earnings that beat the average analyst estimate. The company also boosted its full-year revenue outlook. Analysts note particular strength at its hardware business.

- Fastly (FSLY) slumps 25% after the software company reported first-quarter earnings, a report that wasn’t strong enough to extend a rally that has lifted shares nearly 300% off a February low.

- McDonald’s (MCD) gains 3% after the fast-food chain said bigger orders bolstered results in the US in the first quarter.

- Sezzle (SEZL) climbs 15% after the financial technology company raised its total revenue growth forecast for the full year.

- Shake Shack (SHAK) falls 18% after the burger chain reported revenue for the first quarter that missed the average analyst estimate.

- Warby Parker (WRBY) gains 7% after the the eyeglass company reported net revenue for the first quarter that beat the average analyst estimate.

- Whirlpool (WHR) is down 18% after the household appliance manufacturer cut its revenue forecast for the full year, missing the average analyst estimate.

- Zoetis (ZTS) falls 10% after the animal health firm cut its adjusted earnings per share guidance for the full year.

Elsewhere in AI, Anthropic signed an agreement with Elon Musk’s SpaceX to access computing resources from a large SpaceX data center. Anthropic’s CEO said his company is “working as quickly as possible” to secure more computing resources after experiencing “80x growth” in annualized revenue and usage in 1Q.

An ongoing slide in oil prices is helping to lift investors’ mood, with Brent crude futures trading below $100 a barrel this morning. The U.S. and Iran are getting closer to restarting talks to end the war and reopen the Strait of Hormuz, with discussions possibly resuming as early as next week in Islamabad. While the US is waiting on Iran to respond to its proposal which sent stocks surging yesterday, and it’s unclear whether they’ll accept. But stocks have largely focused on a solid earnings season and the tech trade anyway. The inverse relationship between stocks and oil prices is “long gone,” wrote Bloomberg Opinion columnist John Authers. The resumption of shipments through Hormuz would also reduce risks around the economic impact of the war. US Treasury yields are retreating for a third straight session alongside the dollar, which is now trading lower than when the war began.

“Even though there is not yet a final peace agreement, markets are clearly pricing in a meaningful step forward toward a resolution,” said Francisco Simón, head of investment strategy at Santander Asset Management. “The key point is that this reduces the probability of the most negative scenarios, particularly those involving a more prolonged shock to global growth.”

That said, there are clear signs of mania: the SOX chip index is now up more than 60% this year – a parabolic move that suggests “we are in semi-irrational chase mode,” Goldman Delta-One head Richard Privorotsky warns. Meanwhile, in a sign the entire market has become one giant gamma squeeze, the S&P traded a record $2.6 trillion notional of calls yesterday..

… with almost 60% of every SPX option yesterday traded a call.

There are a few signs of the rally broadening out, with the S&P 500 equal-weight index closing at a record for the first time since late February. But there’s really just one trade in town, with the SOX hitting new records almost daily. “Until supply normalizes, the market can continue to justify increasingly large numbers across the ecosystem, although the obvious risks are building,” Goldman partner Privorotsky wrote in a note.

The global chip euphoria helped South Korea’s stock market to overtake Canada’s, and is boosting niche firms around the world, with Sweden’s Silex Microsystems having the strongest first day of trading for a sizable European IPO in almost five years. Still, there may be a limit — after more than doubling in value this year, ARM shares fell after it warned of sluggishness in the smartphone industry.

In eco data, planned job cuts continued to mount in the tech sector last month, even as overall private-sector layoff announcements receded, according to Challenger data. And consumer sentiment remains closely watched. Costco’s April comparable sales rose 11.6%, aided by 3.2% gas-price inflation. Whirlpool cut its revenue forecast, noting North American industry demand reached recession-level lows.

The Trump administration has begun paying out refunds for the $166 billion in global tariffs that the US Supreme Court declared unlawful earlier this year. The FCC said that an inquiry the commission launched into the rising cost of watching sports on TV may not lead to any regulatory action. In hedge funds, SPX Capital is undergoing a major restructuring, with senior partners departing and a rethink of operations that will include shutting its London office. Point72 is creating a new fundamental stock-picking unit led by Hong Kong-based star portfolio manager James Lau.

With earnings season gradually drawing to a close, of the 411 S&P 500 companies to have reported so far this earnings season, 84% have beaten analysts’ forecasts, while 11% have missed

In Europe, the Stoxx 600 is down 0.2% after erasing an earlier gain.Uutilities and food beverage shares led declines while luxury, travel and leisure stocks are among the best performers. Here are the biggest movers Thursday:

- Luxury stocks are among Europe’s best performers on Thursday, with strong Chinese consumer data adding to hopes for a turnaround that’s already been fueled by optimism about a peace deal in the Iran war

- Stora Enso gains as much as 5.4%, the most in a month, following a first-quarter Ebit beat from the paper, packaging and forestry company

- Tenaris falls as much as 7.1%, the most since July last year, after the Italian pipeline and steel-pipe manufacturer reported its latest earnings

- Maersk falls as much as 5.3%, the most since March, after the Danish shipping giant reported its latest earnings and reaffirmed its full-year guidance, with the latter being a small negative for analysts as consensus already sits at the upper end of the guided range

- Orsted shares drop 2.4% after the Danish wind farm operator reported 1Q Ebitda that beat the average analyst estimate, while after-tax profit missed. Analysts at Jefferies and JP Morgan point to rising interest rates and higher-than-expected taxes for the miss

- Siemens Healthineers drops as much as 5.7%, the most in six months, after the German medical equipment maker cut its comparable sales forecast for the full year and lowered the upper end of the guidance range for adjusted EPS

- GN Store Nord shares fall as much as 8.7%, the most in three months, after the Danish communication solutions company reported what Jefferies described as a “weakish” quarter

- Vestas shares see choppy trading as the Danish wind-turbine maker reported first-quarter EBIT before special items that beat the average analyst estimate, though Morgan Stanley flagged weakness in services

Earlier, Asian stocks rose to a record high, supported by a catchup rally in Japanese shares and optimism that the US and Iran are nearing a deal to end their war. The MSCI Asia Pacific Index climbed as much as 2.3% after gaining 2.4% in the previous session. TSMC, SoftBank Group and SK Hynix provided the biggest boost to the advance. Japan led gains in the region as trading resumed after a long holiday. Shares in Taiwan and Hong Kong also outperformed. Tech shares continued to draw investor interest, with the MSCI Asia Pacific Information Technology Index gaining as much as 3.4% to a record.

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The Norwegian krone outperforms, rising 0.9% against the greenback after the Norges Bank hiked interest rates. Most economists had them on hold. The Riksbank did stand pat.

In rates, treasuries hold small gains into early US session, supported by lower oil prices and European bond rally. Brent crude oil holds below $100 a barrel, extending Wednesday’s nearly 8% slump, as investors weigh latest attempts by US and Iran to reach a peace agreement. US yields are 2bp-3bp richer on the day with curve spreads narrowly mixed; 10-year, lower by 2bp near 4.33%, slightly outperforms German and UK counterparts. European government bonds also edge up. Gilts are also in focus with UK local elections underway. US session includes weekly jobless claims and several Fed speakers. IG dollar issuance slate includes a couple of deals. Three names priced $14.5 billion Wednesday, led by Eli Lilly’s $9b eight-part offering. On average, issuers paid negative concessions on deals that were 3.7 times oversubscribed.

In commodities, brent crude futures fall another 2% to around $99 a barrel as the US waits on Iran to respond to its proposal to reopen the Strait of Hormuz and end the war. Precious metals gain with spot silver up 4%. Bitcoin falls.

Today’s US economic data calendar slate includes 1Q preliminary nonfarm productivity and jobless claims (8:30am), March construction spending (10am), April New York Fed 1-year inflation expectations (11am) and March consumer credit (3pm). Fed speaker slate includes Hammack (10am, 2:05pm), Daly (12:30pm), Kashkari (1pm) and Williams (3:30pm)

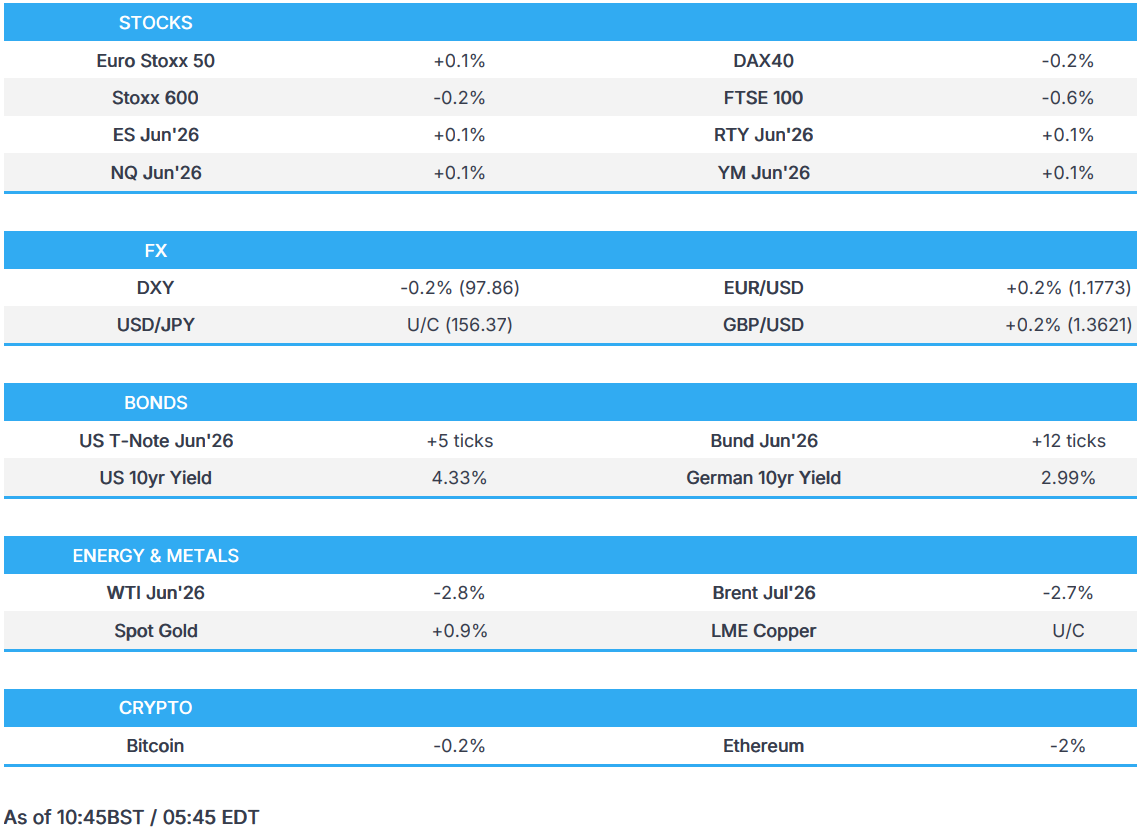

Market snapshot

- S&P 500 mini +0.1%

- Nasdaq 100 mini +0.1%

- Russell 2000 mini +0.1%

- Stoxx Europe 600 -0.2%,

- DAX little changed,

- CAC 40 little changed

- 10-year Treasury yield -2 basis points at 4.33%

- VIX +0.1 points at 17.48

- Bloomberg Dollar Index -0.1% at 1187.37,

- euro +0.2% at $1.1768

- WTI crude -2.6% at $92.6/barrel

Top Overnight News

- The U.S.-Iran war had created a “new wake-up call” for global trade, Maersk CEO Vincent Clerc told CNBC on Thursday, warning that the impact could worsen in the coming months. “And there is so much we can do on reducing costs, but there is a lot we need to do on passing on these costs to customers, because it’s such a massive cost increase that we can’t shoulder it.” CNBC

- Privately, President Trump’s advisers are increasingly worried that Republicans will pay a political price for the rising fuel costs, according to people familiar with the matter. Many of those advisers are eager to end the war in hopes that prices will begin moderating before November’s midterm elections. WSJ

- Hungry to sell, UAE slips hidden oil tankers through Strait of Hormuz: RTRS

- The jet fuel shock triggered by the Iran war has been a bigger crisis for the global airline industry than the Covid-19 pandemic, according to one of Asia’s biggest carriers AirAsia. FT

- Japan probably spent around $30 billion since its currency intervention on April 30, according to a Bloomberg analysis. Their top FX official Atsushi Mimura signaled authorities are prepared to respond on all fronts to speculative moves. BBG

- Chinese households increased their pace of spending over the recent Labor Day extended holiday weekend, with a 14.3% jump in consumer sales from the same holiday last year. The increase is seen as an encouraging sign for the world’s second-largest economy, but household spending over holidays can be volatile, and big-ticket purchases remain subdued. BBG

- China asked its biggest banks to pause new yuan loans to five US-sanctioned refiners tied to Iranian oil, people familiar said. BBG

- The US and China are considering launching official discussions on AI when US President Trump visits China next week. With the proposed recurring conversations, risks from unexpected AI model behaviour, autonomous military systems, and attacks by non-state actors using open source tools will be addressed: WSJ

- Norway’s central bank unexpectedly hiked rates (from 4% to 4.25% – the Street was expecting rates to stay unchanged) due to upward inflation pressures. BBG

- BOE officials are privately concerned UK economic data may be sending false signals, complicating rate-setting, people familiar said. BBG

- Federal Reserve officials said on Wednesday the ongoing U.S.-backed war with Iran is raising the risk of a sustained inflation shock, with continued high oil prices and developing concerns about problems with global supply chains. BBG

Iran News

- Al Arabiya reported that “the coming hours will witness a breakthrough for the situation of the ships stuck in the strait”, spurring pressure in the crude complex.

- Iran is expected to provide its reply to the US proposal for ending the war to mediators on Thursday, according to CNN, citing a regional source.

- US President Trump could turn to military action without an agreement with Iran ahead of the China trip, according to Axios, citing US officials.

- Iran is expected to provide its reply to mediators on Thursday, CNN reported citing a regional source.

- “Arabic sources: Reaching understandings regarding easing the siege in exchange for the gradual opening of the Strait of Hormuz “, Al Arabiya reported; “The coming hours will witness a breakthrough for the situation of the ships stuck in the strait”.

- Pakistani Foreign Ministry spokesperson said, “We do not talk about war and instead talk about dialogue and diplomacy. However, if any aggression similar to what we saw last year, we will respond; Pakistan will respond just as it did”, Mallick posted.

- Pakistani Foreign Ministry Spokesperson said “We have not yet received a response from Iran regarding the US amendments”, Al Jazeera reported.

- “Pakistani source to Al Arabiya said Iran may hand over its response to the US proposal to the Pakistani mediator today”, Al Arabiya. “No arrangements for any direct meetings between the Iranians and the Americans so far.”. “Contacts with the Iranians are ongoing and there are no obstacles hindering continued”. “Discussions are ongoing regarding the status of the Strait of Hormuz, and reaching understandings is still possible”.

- Pakistani Foreign Ministry said “We expect an urgent agreement between Iran and the United States”, Al Araby reported.

- “Israel was informed that Iran has agreed to transfer its stockpile of 60% enriched uranium to a third country that remains unknown”, Sky News Arabia reported citing Israeli Channel 12.

- Pakistani Foreign Ministry spokesperson, on US-Iran agreement, said “we would expect an agreement sooner rather than later”, Pakistani journalist Mallick posted. “We will welcome any settlement wherever that takes place, if it takes place in Islamabad, it would be an honour and privilege.”.

- The proposed agreement between the US and Iran may limit the IDF’s action in Lebanon, Israeli press reported citing an Israeli official.

- US President Trump, on Iran, said it will all work out very quickly.

- IDF said it has intercepted suspicious aerial target launched from Lebanon towards Israel following sirens that sounded in Manara, Margaliot and Kiryat Shmona.

- Lebanon’s PM Salam said it is not seeking normalisation with Israel and it is too early to discuss any possible meeting with Israeli PM Netanyahu.

- Iran has issued a message to commercial vessels in the Strait of Hormuz, saying Iran’s port is fully prepared to provide general maritime services and support to the vessels, IRNA reported.

- US President Trump could turn to military action without an Iran agreement ahead of the China trip, Axios reported citing US officials.

- US President Trump’s reversal on his plan to help ships go through the Strait of Hormuz came after Saudi Arabia suspended the US’s ability to use its bases and airspace to carry out Project Freedom, NBC reported citing US officials.

- IRGC Navy Political Affairs Official said we will impose our control over the Strait of Hormuz, and any attack will be met with a plan beyond the enemy’s calculations, Al Jazeera reported.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded broadly in the green, as a continuation of gains seen stateside as hopes of an end of the US-Iran conflict spurred risk-on flows. ASX 200 continued its rebound and is set for 2 consecutive days of gains. Miners were the biggest gainers while Energy names slumped. Shares of Tabcorp have nose-dived after the Co. stated that AUSTRAC has commenced an enforcement investigation with serious concerns over money laundering and terrorism financing risks. Nikkei 225 returned from its holiday with the need to catch up to the gains seen in equities while it was closed. As a result, the Nikkei surged to new ATHs and extended above the 63,000 handle, driven by tech majors SoftBank and Ibiden. KOSPI underperformed its APAC peers, as it consolidated following its surge beyond the 7,000 handle. SK Securities raised its PT for Samsung Electronics and SK Hynix to a price that is 88% and 87% higher, respectively, than their current price, reaffirming the tech strength. Shanghai Comp. and Hang Seng gained despite a lack of single-stock news. Continuing on the chip theme, Montage has overtaken CATL as the most expensive dual-listed stock in Hong Kong relative to its mainland shares

Top Asian News

- Philippine’s Economic Minister said controlling inflation, even if it will cost growth, is not necessarily bad.

- China’s top diplomat Wang Yi met with a delegation led by Steve Daines on Thursday, Xinhua reported.

- South Korea’s government is to invest KRW 30bln in a project aimed at establishing an AI data platform for autonomous vessels, Yonhap reported.

- Indonesia’s Planning Minister said the 2027 government working plan is set with GDP growth target in a range of 5.9-7.5%.

- Hong Kong Financial Secretary Chan announces plans to promote the use of the CNY in commodity pricing.

- China rural banks have reportedly cut its deposit rates, with further cuts expected.

- Japan’s Top FX Diplomat Mimura does not comment on FX intervention but said FX is being closely watched and are in daily contact with US authorities. IMF’s classification of free floating regime does not restrict frequency of intervention. Will not comment on FX levels. Too early to comment on US Treasury Secretary Bessent’s upcoming visit.

- US Treasury Bessent is to meet with Japanese PM Takaichi, Finance Minister Katayama and BoJ Governor Ueda for 3 days, starting Monday 11th, to discuss the weak yen, Nikkei reported.

European bourses are broadly modestly firmer, attempting to build on the hefty gains seen in the prior session. Geopolitics remains the key focus this morning, with Iran expected to provide its reply to the US proposal for ending the war to mediators on Thursday, CNN reported. Sentiment in early morning trade was lifted after Al Arabiya reported that “the coming hours will witness a breakthrough for the situation of the ships stuck in the strait”. European sectors are mixed. Travel & Leisure takes the top spot, joined closely by Consumer Products and then Autos. Sectors which have broadly benefited from the risk-tone and/or lower energy prices. Elsewhere, Utilities is found right at the foot of the pile, joined closely by Telecoms. In terms of key movers: Henkel (+3.9%, sales topped exp.), Rheinmetall (-3.1%, missed on Q1 EPS, but reaffirmed outlook), Telecom Italia (+3.2%, revenue +1.4% amidst strong Brazil growth), Shell (-1.7%, EPS and Rev. topped expectations whilst announcing a USD 3bln buyback), Flutter (-3.6%, cut guidance despite reporting higher Q1 revenue).

Top European News