EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,718.700000000 USD

INTENT DATE: 05/11/2026 DELIVERY DATE: 05/13/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 5

118 C MACQUARIE FUTURES US 1

523 C INTERACTIVE BROKERS 1

555 C BNP PARIBAS SEC CORP 17

657 H MORGAN STANLEY 20

661 C JP MORGAN SECURITIES 13

709 C BARCLAYS 15

TOTAL: 36 36

MONTH TO DATE: 3,790

GOLD: NUMBER OF NOTICES FILED FOR MAY/2026: 36 CONTRACTs NOTICES FOR 3600 OZ or 0.1119 TONNES

total notices so far: 3790 contracts FOR 379,000 OZ OR 11.788 TONNES

SILVER NOTICES: 260 NOTICE(S) FILED FOR 1.300 MILLION OZ /

total number of notices filed so far this month : 5373 CONTRACTS (NOTICES) for 26.365 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY OUR HUGE QUEUE JUMP OF 265 CONTRACTS FOR 1.325 MILLION OZ/NEW STANDING ADVANCES TO 31.180 MILLION OZ/.//

SUMMARY OF OUR MAY 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 26.055 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 265 CONTRACTS/1.325 OZ//NEW STANDING ADVANCES TO 31.180 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THE MAY DELIVERY MONTH)

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 278 CONTRACT QUEUE JUMP FOR 27800 OZ/ (0.8646 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 35 CONTRACTS OR 3500 OZ (.1088 TONNES) TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES FOR .4353 TONNES/STANDING NOW ADVANCES TO 14.4073 TONNES OF GOLD.

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 35 CONTRACTS/3500 OZ// 0.0963 TONNES/ TOTAL EXCHANGE FOR RISK: 004353 TONNES///NEW STANDING IS NOW ADVANCES TO 14.4073 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 34.215 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA MEGA STRONG 4461 CONTRACTS TO AN OI OF 104,418 ADVANCING A FROM ITS ALL TIME LOW SET MAY 1.

EFP ISSUANCE 2195 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 2195 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 4461 CONTRACTS AND ADD TO THE 2195 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 6656 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $5.10

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 33.28 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $5.10

2.ASIAN AFFAIRS MAY 12 /2025

SHANGHAI CLOSED DOWN 10.73 PTS OR 0.25%

HANG SENG CLOSED DOWN 58.93 PTS OR 0.22%

Nikkei CLOSED UP 274.12 PTS OR 0.44%

//Australia’s all ordinaries CLOSED DOWN 0.79%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7948

/ OFFSHORE CLOSED UP AT 6.7947 Oil UP TO 101.60 dollars per barrel for WTI and BRENT UP TO 107.15 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP (6.7948) OFFSHORE YUAN TRADING UP TO 6.7947 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR 2998 CONTRACTS UP TO AN OI OF 374,344 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET LATE LAST MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD ZERO T.A.S. LIQUIDATION DURING MONDAY’S TRADING. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT ALSO SOME SPECULATORS STILL GOING TO THE SHORT SIDE WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MAY CONTRACT MONTH!!

THE STRONG SIZED GAIN ON OUR TWO EXCHANGES OCCURRED DESPITE OUR SMALL LOSS IN PRICE IN GOLD (DOWN $2.80).

WE THUS HAD A STRONG SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 5,023 CONTRACTS (OR 15.632 TONNES) DESPITE OUR LOSS IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.EQUATING TO 2028 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A SMALL CONTRACT FOR RISK ISSUANCE IN GOLD TOTALLING 13 CONTRACTS FOR 1300 OZ OR 0.0963 TONNES OF GOLD. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK ON MAY 7, SO THIS IS OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: TWO ISSUANCES SO FAR FOR 140 CONTRACTS OR 14,000OZ OR 0.4353 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: TWO ISSUANCES SO FAR FOR 140 CONTRACTS, 14,000 OZ OR 0.4353 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

DETAILS ON OUR NEW MAY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 5,023 CONTRACTS DESPITE OUR LOSS IN PRICE ($2.80). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A HUGE SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 14,367 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT IS NOW IN FULL FORCE WITH TODAY’S RAID ON OUR PRECIOUS METALS.

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 2ND ISSUANCE FOR 0.0963 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 0.4353 TONNES ISSUED MAY 6 AND MAY 12.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 6300 OZ (.1959 TONNES) TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 14,000 OZ OR 0.4353 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 14.4073 TONNESS

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING MAY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $2.80)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION MONDAY // COMEX SESSION// DESPITE OUR LOSS IN PRICE , OUR LONG SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI //

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $2.80

WE HAD 2339 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 5023 CONTRACTS OR 502,300 OZ OR 15.682 TONNES

INITIAL GOLD COMEX

MAY DELIVERY MONTH

MAY 12 2026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 1 i) Brinks: 64,302.000 oz (2000 kilobars) 2.0 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 36 CONTRACTS OR 3600 OZ 0.1119 TONNES OF GOLD |

| No of oz to be served (notices) | 702 Contracts 70200 OZ 2.1835 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3790 notices 379,000 oz 11.788 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 1

ENTRIES; 1

i) Brinks: 64,302.000 oz

(2000 kilobars)

2.0 tonnes

xxxx

adjustments: 1

Brinks: 1929.06 oz customer to dealer

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF MAY OI STANDS AT 738 CONTRACTS HAVING A LOSS OF 37 CONTRACTS.

WE HAD 72 CONTRACTS SERVED ON MONDAY SO WE GAINED ANOTHER STRONG 35 CONTRACTS OR 3500 OZ (0.1088 TONNES) UNDERWENT A QUEUE JUMP TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI LOST BY 3946 CONTRACTS DOWN TO AN OI OF 228,067

JULY GAINED 21 CONTRACTS UP TO AN OI OF 1124.

We had 36 contracts filed for today representing 3600oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 36 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 13 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (3,790) to which we add the difference between the open interest for the front month of MAY (738 CONTRACTS) minus the number of notices served upon today 36 x 100 oz per contract) equals 449,200 OZ OR (13.972 Tonnes of gold) to which we add our TWO exchange for risk issuance for 14,000 oz or 0.4353 tonnes//new standing for gold/May again advances to 14.4073 tonnes.

THUS: INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (3,790) to which we add the difference between the open interest for the front month of MAY( XXX CONTRACTS) minus the number of notices served upon today 36 x 100 oz per contract) equals 449.200 OZ OR (13.972 Tonnes of gold) plus we must add our TWO exchange for risk issuances of 14,000 oz or 0.4353 tonnes/new standing advances to 14.4073 tonness

new total of gold standing in MAY ADVANCES TO 14.4073 TONNES//

TOTAL COMEX GOLD STANDING FOR MAY 14.4073 TONNES TONNES WHICH IS NOW STRONG FOR THIS NORMALLY NON ACTIVE DELIVERY MONTH OF MAY.

confirmed volume MONDAY confirmed 183,673// poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

the number provided do not match from yesterday!!!

total pledged gold: 1,885,243.095 oz 58.63 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,885,243.095 tonnes oz 58.63 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 29,014,384.041oz

TOTAL REGISTERED GOLD 15,829,828.615OZ 492.355 tonnes

TOTAL OF ALL ELIGIBLE GOLD 13,184,555.426 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,944,585 oz ((REG GOLD- PLEDGED GOLD)=

433.74 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

MAY DELIVERY MONTH

MAY 12

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries i) CNT : 51,734.220 oz total withdrawal: 51,734.220 oz |

| Deposits to the Dealer Inventory | 0 entries |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 1 ENTRIES i) Into Asahi: 1,132,194.900 oz total deposit 1,132,194.900 oz |

| No of oz served today (contracts) | 260 CONTRACT(S) (1.3000 MILLION OZ |

| No of oz to be served (notices) | 963 Contracts (4.815 MILLION oz) |

| Total monthly oz silver served (contracts) | 5273 contracts 26.365 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

i) Into Asahi: 1,132,194.900 oz

total deposit 1,132,194.900 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

one entry:

i) CNT : 51,734.220 oz

total withdrawal: 51,734.220 oz

adjustments:3 customer to dealer

a) Brinks 73,888.100 oz

b) Delaware: 4,759.700oz

c) Manfra: 5,887.980 oz

MONDAY volume: 79,193 oz// good

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 79.968 MILLION OZ//.TOTAL REG + ELIGIBLE. 313.197 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2026 OI: 1223 OPEN INTEREST CONTRACTS FOR A GAIN OF 259 CONTRACTS. WE HAD 6 CONTRACTS SERVED UPON ON MONDAY SO WE GAINED A HUGE 265 CONTRACTS OR 1.325 MILLION OZ AS THESE BOYS ENTERTAINED A MASSIVE QUEUE JUMP WHERE THEY WILL TRY THEIR LUCK AND TAKE DELIVERY ON THIS SIDE OF THE POND.

JUNE SAW A GAIN OF 71 CONTRACTS UP TO 2702 OI CONTRACTS

JULY SAW A GAIN OF 3163 CONTRACTS UP TO 78,171 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 260 or 1.3000 MILLION oz

CONFIRMED volume MONDAY; 79,193 good

AND NOW MAY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 5273 X5,000 oz = 26.365 MILLION oz

to which we add the difference between the open interest for the front month of MAY (1223) AND the number of notices served upon today (260 )x (5000 oz)

Thus the standings for silver for the MAY 2026 contract month: (5273 )Notices served so far) x 5000 oz + OI for the front month of MAY (1223) minus number of notices served upon today (260)x 5000 oz equals silver standing for the MAY..contract month equating to 31.180 MILLION OZ.+

NEW STANDING ADVANCES T0: 31.180 MILLION OZ WHICH IS STILL PRETTY GOOD FOR THIS ACTIVE DELIVERY MONTH OF MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 79.968 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/313.197 million: 44.72

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAY 12 /2026/WITH GOLD DOWN $38.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.285 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 11 /2026/WITH GOLD DOWN $2.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.515 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.995 TONNES

MAY 8 /2026/WITH GOLD UP $22.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.283 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.480TONNES

MAY 7 /2026/WITH GOLD UP $15.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.853 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1033.197TONNES

MAY 6 /2026/WITH GOLD UP $124.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.718 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1034.05TONNES

MAY 5 /2026/WITH GOLD UP $33.75 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 4 /2026/WITH GOLD DOWN $106.65 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 1 /2026/WITH GOLD UP $13.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.427 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1035.768 TONNES

APRIL 30/2026/WITH GOLD UP $19.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.142 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1039.195 TONNES

APRIL 29/2026/WITH GOLD DOWN $45.70 TODAY/NO CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 28/2026/WITH GOLD DOWN $85.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

APRIL 1/2026/WITH GOLD UP $134.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.143 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1047.276 TONNES

MAR 31/2026/WITH GOLD UP $119.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.429 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1046.133 TONNES

MAR 30/2026/WITH GOLD UP $33.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.143 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1049.562

MAR 27/2026/WITH GOLD UP $103.55 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.285 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.705

MAR 26/2026/WITH GOLD DOWN $213.05 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.580 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.42

MAR 25/2026/WITH GOLD UP $155.30 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.300 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1053.000

MAR 24/2026/WITH GOLD DOWN $7.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.286 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1052.705

MAR 23/2026/WITH GOLD DOWN $165.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 5.149 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1056.991

MAR 20/2026/WITH GOLD DOWN $39,55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1062.135

MAR 19/2026/WITH GOLD DOWN $XXX TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 2.57 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1066.99

MAR 18/2026/WITH GOLD DOWN $111.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1069.564 TONNES

MAR 17/2026/WITH GOLD UP $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 0.857 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.708 TONNES

GLD INVENTORY: 1033.995 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

MAY 12 WITH SILVER DOWN $0.48: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.176 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 484.990 MILLION OZ

MAY 11 WITH SILVER UP $5.10: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.995 MILLION OZ OF SILVER PUT OF THE SLV// / // :INVENTORY RESTS AT 483.814 MILLION OZ

MAY 8 WITH SILVER UP $1.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.689 MILLION OZ OF SILVER INTO THE SLV// / // :INVENTORY RESTS AT 484.809 MILLION OZ

MAY 7 WITH SILVER UP $2.26: NO CHANGES IN SILVER INVENTORY AT THE SLV: / // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 6 WITH SILVER UP $3.75: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.724 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 5 WITH SILVER UP $0.21: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 4 WITH SILVER DOWN $3.05: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 1 WITH SILVER UP $2.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.905 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 484.338 MILLION OZ

APRIL 30 WITH SILVER UP $2.03: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.991 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 485.243MILLION OZ

APRIL 29 WITH SILVER DOWN $1.95: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 28 WITH SILVER DOWN $2.05: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

APRIL 1 WITH SILVER UP $1.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND WITHDRAWAL OF 0.453 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 491.079 MILLION OZ

MAR 31 WITH SILVER UP $4.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.893 MILLION OZ FROM THE SLV // :INVENTORY RESTS AT 491.532 MILLION OZ

MAR 30 WITH SILVER UP $0.74: NO CHANGES IN SILVER INVENTORY AT THE SLV: // :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 27 WITH SILVER UP $1.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV// :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 26 WITH SILVER DOWN $4.75: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 25 WITH SILVER UP $3.25: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 24 WITH SILVER DOWN $0.15: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT DEPOSIT OF 10.505 MILLION OZ INTO THE SLV :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 23 WITH SILVER UP $0.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// NO CHANGE IN INVENTORY/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 20 WITH SILVER DOWN $1.92: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.490 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 19 WITH SILVER DOWN $6.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.9444 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 490.761 MILLION OZ

MAR 18 WITH SILVER DOWN $2.36: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 1.087 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 494.792 MILLION OZ.

MAR 17 WITH SILVER DOWN $0.89: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 493.705 MILLION OZ.

CLOSING INVENTORY 484.990 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

JESSE COLUMBO\

This is a post from Jesse Colombo’s The Bubble Bubble Report—a bestselling newsletter focusing on precious metals investing and global economic risks. We specialize in detailed reports and analyses.

Gold Is Ready for Liftoff

Gold is on the cusp of breaking out of its recent channel pattern while investor sentiment is overly pessimistic, a combination that sets the stage for a sharp upward move.

| Jesse ColomboMay 11∙Paid |

In my updates over the past week, I’ve been showing how silver was on the verge of a major breakout following its sharp correction since late January, and that scenario is now playing out, with silver up 7.39% in Monday trading and COMEX futures closing at $86.80. In today’s update, I want to turn to gold, which appears poised to follow in silver’s footsteps and move higher, though several key hurdles still need to be cleared, which I’ll outline in this analysis.

I want to start by showing the chart of silver and its clean breakout from the triangle pattern that formed over the past few months:

Interestingly, gold’s chart shows a setup similar to silver’s, though instead of a triangle, a channel pattern formed during the correction of the past several months. In Monday’s trading, gold began breaking out of this channel, which is an encouraging sign, though I would like to see a stronger follow-through for full confirmation, which is likely to play out over the next few trading sessions.

Once gold has fully broken out of its channel, I’m watching two additional major hurdles: the $4,800 to $5,000 resistance zone and $5,400 to $5,600. Breakouts above horizontal resistance levels and zones tend to be more reliable than those above diagonal trendlines like the top of the channel, so I would like to see these zones cleared for added confirmation.

To learn more about support and resistance zones, I recommend reading my two-part tutorial on the topic (Part 1 and Part 2).

I would like to see gold close decisively above each resistance zone, and with each successive breakout, the odds of the next powerful leg higher will increase significantly. The final breakout above the $5,400 to $5,600, which formed at the late-January peak, is the most important, as it would signal that gold has once again entered blue-sky territory and that the correction of the past few months is fully behind it.

A look at gold’s weekly log-scale chart puts the channel pattern of the past few months into clearer perspective. Channel like this typically act as continuation patterns within a bull market, so breakouts from them usually lead to much further gains.

As a reminder, I believe gold is only about two years into a secular bull market that should last at least a full decade, ultimately driving prices to at least $15,000 to $20,000 per ounce (learn more).

As I’ve explained in my updates, gold’s correction over the past few months was necessary to flush out excessive bullish speculative sentiment and overbought conditions, and now that it is no longer overbought, it is in a much healthier position for the bull market to resume.

The indicator used in the chart below to assess whether gold is overbought is the Relative Strength Index (RSI), which is the one I rely on when analyzing longer-term charts, such as those on the weekly timeframe.

In addition to analyzing price charts, I place strong emphasis on monitoring investor sentiment and its proxies, interpreting them from a contrarian perspective. When the crowd or “dumb money” becomes overly pessimistic, it is typically a bullish signal, and when it becomes overly optimistic, it is usually a bearish one.

One such proxy for investor sentiment is the physical gold holdings of the world’s most popular gold exchange-traded fund (ETF), the SPDR Gold Shares (GLD). As the chart below shows, during gold’s correction in recent months, GLD experienced heavy outflows totaling 2.16 million troy ounces, or 67.18 metric tonnes of gold.

In case you are unfamiliar with the mechanics, when investors sell shares of the SPDR Gold Shares (GLD), the fund must reduce its physical gold holdings by a commensurate amount. I view these recent outflows as irrational and foolish behavior because nothing has changed fundamentally for gold and it remains in a powerful secular bull market, but there are many Nervous Nellies and fair-weather friends out there who threw in the towel, thinking the bull market is dead—they will deeply regret that rash decision.

As I mentioned, I’m a big believer in sentiment indicators, and as someone with a large online presence focused on precious metals, I’m in a unique position to gauge investor sentiment through traffic, views, engagement, and even newsletter revenue.

Since the precious metals correction began a few months ago, this newsletter’s annual revenue has declined from a peak of roughly $656,000 to about $530,000, a drop of around 19%. What’s fascinating is that the revenue chart almost perfectly mirrors GLD’s gold holdings, which is no coincidence, as both serve as proxies for sentiment.

Together, they show that many investors foolishly threw in the towel on precious metals in recent months, believing the bull market was over. The good news is that, from a contrarian perspective, this is bullish, as it indicates that excessive optimism has largely been flushed out.

I share this for informational and encouragement purposes, not to seek sympathy—revenue is still up a remarkable sevenfold from a year ago, and it was zero when I started in September 2024. I believe the next leg higher in precious metals should also lead to the next leg higher in revenue. Thanks again for your continued support!

While American retail investors (the “dumb money”) have quickly soured on gold, the “smart money,” such as China’s central bank, has continued buying. Gold holdings at the People’s Bank of China rose by 260,000 troy ounces, or 8.1 tonnes, in April, the largest increase since December 2024.

Another bullish scenario I’m watching is the U.S. Dollar Index, which is very close to breaking down from its two-decade-old rising channel pattern. Assuming that occurs, a secular bear market in the dollar will begin, kicking the precious metals and commodities bull market into overdrive.

There are many reasons a secular bear market in the dollar is likely, including its overvaluation, U.S. federal debt recently surpassing 100% of GDP, and the renewed expansion of the money supply.

Next, let’s take a look at the gold mining sector using the VanEck Gold Miners ETF (GDX) as a proxy. A successful bullish breakout in gold would also be very bullish for gold miners. In addition to the key levels I’m watching in gold mentioned earlier, I am closely monitoring the $100 to $104 and $112 to $116 resistance zones in GDX to determine whether the next leg of the bull market in gold mining stocks has begun.

As a reminder, I am very bullish on gold and silver miners, in addition to the metals themselves, as I explained in this report.

I’m also monitoring the $130 to $135 and $150 to $155 resistance zones in the VanEck Junior Gold Miners ETF (GDXJ), which I use as a proxy for the junior gold mining sector:

As with gold itself, investor sentiment toward gold miners is extremely depressed, which is exactly what contrarians like myself want to see, as it typically precedes bullish moves. The chart below shows the Gold Miners Bullish Percent Index, which measures overbought and oversold conditions in the gold mining sector.

The last time this index reached such low levels was in late 2023 and early 2024, just before the major bull market in gold and gold mining stocks began, making this a particularly compelling and encouraging setup to watch.

To conclude, gold is on the cusp of breaking out from the channel pattern that formed over the past several months, and I’m looking for strong follow-through in the coming trading sessions. The correction has flushed out virtually all excessive bullish sentiment, and pessimism now pervades the sector, conditions that often precede powerful advances. I view this as an excellent opportunity to accumulate more gold and gold miners before the long-term bull market resumes its upward trajectory.

If you enjoyed today’s update, I recommend checking out my other related reports:

- Here’s When I’ll Sell My Gold & Silver

- Gold & Silver Volatility Has Plunged

- Encouraging Signs in Silver

- Past Oil Bull Markets Have Been Bullish for Precious Metals

- Goldman & Wells Fargo Maintain Bullish Outlook on Gold

- The Bullish Case For Gold & Silver Miners

- U.S. Debt Exceeds 100% of GDP

- The Money Supply is Surging

- Gold Isn’t Going Up, Your Money Is Just Losing Value

- The Dollar Is Not Out of the Woods

Disclaimer: the information provided in The Bubble Bubble Report and related content is for informational and educational purposes only and should not be construed as investment, financial, or trading advice. Nothing in this publication constitutes a recommendation, solicitation, or offer to buy or sell any securities, commodities, or financial instruments.

All investments carry risk, and past performance is not indicative of future results. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions. The author and publisher disclaim any liability for financial losses or damages incurred as a result of reliance on the information provided.

JOHN RUBINO

3.CHRIS POWELL AND HIS GATA DISPATCHES:

Brien Lundin: Silver rings the bell

Submitted by admin on Mon, 2026-05-11 14:10 Section: Daily Dispatches

By Brien Lundin

Gold Newsletter / Golden Opportunities, Metairie, Louisiana

Monday, May 11, 2026

Something very interesting is happening in the metals and mining market.

As you know, the winds of war have been driving every asset market. Stocks, bonds and commodities (including gold and silver) have risen along with hopes for peace, while oil and the dollar have fallen when those hopes emerge.

…

.And of course the opposite has occurred whenever those hopes have been dashed.

But something important changed last week. …

… For the remainder of the commentary:

https://goldnewsletter.com/go051126/

END

India’s leader urges people to stop buying gold as Asia scrambles for energy

Submitted by admin on Sun, 2026-05-10 22:25 Section: Daily Dispatches

From the Australian Broadcasting Corp., Sydney

Sunday, May 10, 2026

Indian Prime Minister Narendra Modi has appealed to the country’s 1.4 billion people to work from home, avoid travel, and stop buying gold, as the Iran war continues to send energy costs soaring.

Modi today called for a return to work-from-home arrangements and online meetings, measures adopted during the COVID-19 pandemic.

He also urged people to use public transport and carpool wherever possible.

Last month he said there was no proposal to raise pump prices for diesel and gasoline, leaving it among the countries yet to raise prices despite the global surge.

Mr Modi asked citizens to cut non-essential travel, calling for collective restraint to help protect India’s economy during the deepening energy crisis.

He urged people to avoid buying gold, which India spends heavily on for weddings.

He has pushed for the adoption of electric vehicles and asked farmers to halve their use of chemical fertilisers and for families to reduce cooking oil consumption, describing that move as both healthy and patriotic. …

… For the remainder of the report:

END

Trump muses vacantly again about whether gold remains in Fort Knox

Submitted by admin on Sun, 2026-05-10 15:04 Section: Daily Dispatches

No mention of leases, swaps, and other market interventions … and no follow-up questions.

* * *

Trump Still Wants to Visit Fort Knox to Confirm Gold Has Not Been Stolen

By Ryan King

New York Post

Sunday, May 10, 2026

President Trump believes this is his golden opportunity.

The president revealed that he’s still eager to crack open Fort Knox and personally ensure that the nation’s gold reserve — valued at nearly $700 billion — is still in the highly secure bullion depository following an uproar about it last yea

“We wanted to go and knock on the door of Fort Knox — a very thick door — and to see whether or not we have any gold in there,” Trump told “Full Measure with Sharyl Attkisson” in an interview that dropped today.

Last year former Department of Government Efficiency (DOGE) boss Elon Musk reacted to a social media user’s suggestion that he should inspect the country’s gold reserves. …

… For the remainder of the report:

4.ANDREW MAGUIRE LIVE FROM THE VAULT 271 and 270

MUST VIEW…

LONDON PAUL//MUST VIEW

5. COMMODITY REPORT/URANIUM CAMECO

Uranium – Cameco Guidance Hanging by a Thread, Implications for Market Purchases

by Asymmetric Research

Monday, May 11, 2026 – 13:05

Cameco’s flagship McArthur River mine and Key Lake mill are cut off. The Smoothstone River Bridge — their primary supply route — has collapsed. The firm has so far not changed guidance, but has noted possible risks. We think guidance is holding by the thread, and the spot market implications could be significant. We evaluate them here.

The bridge suffered extensive damage from recent flooding.

Bridge collapse shows extensive damage

Source: CBC

Traffic from the other flagship operation, Cigar Lake, remains unaffected for now. While McArthur River and Cigar Lake are only c50km apart by air, they use completely different road routes. But they are both in the same flood prone region. We would not overlook the risk of knock-on effects at Cigar Lake if poor weather conditions persisted. There are other bridges on that route too, and their condition is uncertain.

Path to Recovery

There are two avenues in our view that Cameco could take to resume traffic from McArthur / Key Lake, but the first looks the most realistic to us:

- Most Likely: Pre-engineered bridge can be deployed rapidly and used while a new bridge is built. These can usually be installed within about two weeks once water levels stabilise. Allowing for ramp-up time at the mine and mill, we expect full resolution around 25 June as a Base case, 45 days from now. This temporary bridge should then hold until a permanent fix is completed (which could take 1-2 years).

- Alternative route: Cameco to obtain an emergency overweight permit. Cameco’s vehicles are too heavy legally for the existing alternate route under normal rules. The issue in our view is that route too would involve the use of other bridges, and the flooding may put them at risk too – they need to be structurally sound to withstand heavy vehicle traffic on them.

Implications for Guidance and Spot Purchases

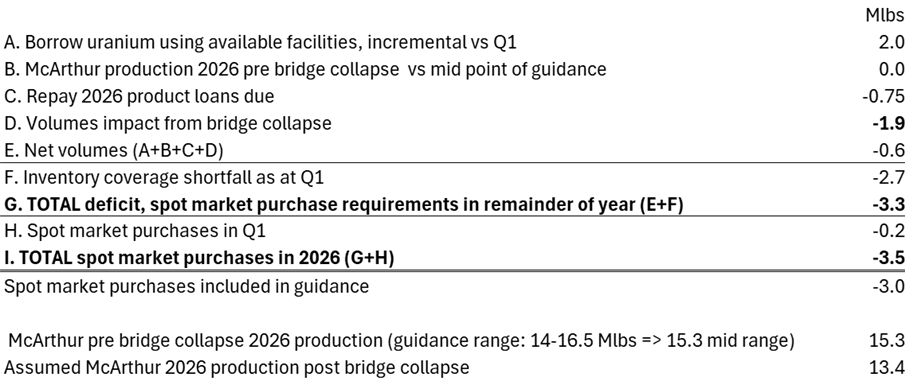

Assuming this fully resolves at our Base case, on 25 June, then McArthur / Key Lake would likely end the year with production at 13.4Mlbs – a tad below Cameco’s low range of guidance (14–16.5Mlbs) – assuming the central case was at the mid-guidance target pre bridge collapse. Assuming zero impact at Cigar Lake, which is also our Base case, then group production guidance (at 100%) could equivalently land at 31Mlbs (vs implicit guidance at 31.5–34.5Mlbs and 33Mlbs at mid-range).

As discussed in our note last week, the issue is that Cameco’s inventory coverage is already very low at 4.4 months of production as at Q1. Taking this level back to what Cameco used to see as a reasonable inventory coverage of around six months of production would suggest a current inventory deficit of c2.7Mlbs.

Assuming Cameco could borrow 2Mlbs of incremental uranium now vs Q1, and that it must pay off the 0.75Mlbs uranium loan it took in Q1 maturing this year, then our 45-day Base case resolution would require 3.5Mlbs of spot market purchases this year vs guidance at 3.0Mlbs. So, guidance on our Base case is on a very thin edge.

We would be surprised to see Cameco able to borrow more than 2Mlbs incremental vs Q1. We would argue that a general tightening credit market could finally make product loans less accessible and flexible than they have previously been. A more limited access to product loans would mean filling the supply gap through more spot market buying.

Our Base Case Estimate of Cameco 2026E Spot Market Purchases (Assuming 45-day McArthur disruption + 2 Mlbs incremental borrowing), Mlbs

Source: Asymmetric Research estimates, Cameco

As an idea on sensitivity, if instead, 1) the McArthur disruption takes say 3 months to resolve, and 2) assuming McArthur pre-bridge collapse was to achieve the lower end of the guidance production range (14Mlbs), and 3) still have access to 2Mlbs of incremental borrow; then Cameco would need to resort to spot market buying for c6.5Mlbs this year. A big number.

[…]

This article was originally published on Asymmetric Research. Continue reading the full analysis — including our sensitivity tables, spot market purchase estimates and highest-conviction uranium positions — at asymmetricresearch.substack.com

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

END

JET FUEL…

Jet Fuel Shortage Deepens Pressure On Global Airlines

Tuesday, May 12, 2026 – 07:20 AM

Via City AM,

- Heathrow’s April passenger numbers fell 5% to 6.7 million, with Middle East traffic down 50%.

- Transfer traffic rose 10% as travellers rerouted through Heathrow to Asia and Oceania.

- Airlines are facing mounting pressure from jet fuel shortages and higher oil prices.

Fewer passengers were heading to Heathrow Airport in April as the war in the Middle East keeps travellers grounded.

Passenger numbers at Europe’s biggest airport fell by five per cent in April to 6.7m with the blame being attributed to the “ongoing impact of the Middle East conflict”.

For those heading to that particular region, Heathrow saw a whopping 50 per cent drop in volumes.

Still, in the year-to-date (Jan–Apr) traffic maintained modest growth at 1.2 per cent.

Transfer demand grew ten per cent in April, as travellers rerouted through Heathrow to reach Asia and Oceania, helping offset losses in direct Middle Eastern travel.

Travel to Asia remained a major growth driver, with a 5.6 per cent increase in April and a 10.6 per cent increase year-to-date.

“We know passengers want certainty when planning their hard-earned summer holidays, so we are supporting Government and airlines as they work through their plans to get passengers on their journeys,” Thomas Woldbye, Heathrow’s top boss, said.

Jet fuel crisis ‘worse’ than Covid

Growing anxieties around the jet fuel shortage caused by the Iran war have rocked the travel industry.

Tony Fernandes, chief executive of Air Asia, said last week: “I thought I’d seen it all with Covid […] but having seen jet fuel go up almost three times — this is much worse.”

It comes after supplies for jet fuel have tumbled to their lowest level since records began, as the war blocks crucial shipping lanes for fuel.

Spirit Airlines – a US-based low-cost airline – last week collapsed under mounting pressure caused by surging oil prices. The firm had failed to secure a $500m lifeline from the Trump administration, leaving it to go out of business and cancel all flights.

Researchers at Allianz Trade warned the UK is among the most “structurally exposed” to jet fuel shortages.

Meanwhile, transport secretary Heidi Alexander has loosened “use it or lose it” rules in a bid to soften the pressures facing airlines.

Woldbye said: “While we have seen some short-term disruption linked to the Middle East conflict, demand for travel remains strong with current fuel supplies stable.”

END

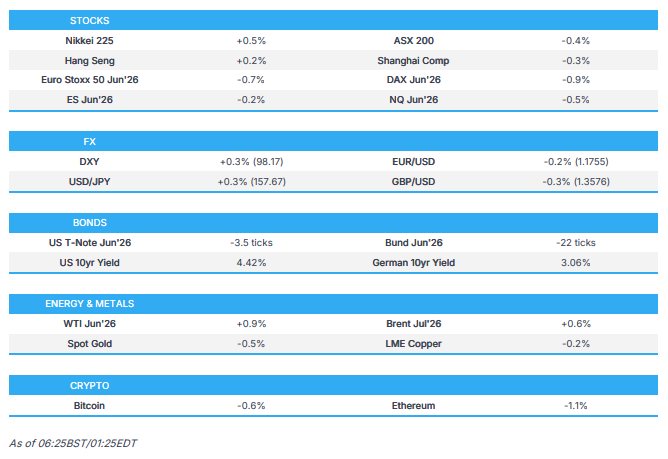

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 10.73 PTS OR 0.25%

HANG SENG CLOSED DOWN 58.93 PTS OR 0.22%

Nikkei CLOSED UP 274.12 PTS OR 0.44%

//Australia’s all ordinaries CLOSED DOWN 0.79%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7948

/ OFFSHORE CLOSED UP AT 6.7947 Oil UP TO 101.60 dollars per barrel for WTI and BRENT UP TO 107.15 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP (6.7948) OFFSHORE YUAN TRADING UP TO 6.7947 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 6.7948

OFFSHORE YUAN: UP TO 6.7947

1.HANG SANG CLOSED DOWN 58.93 PTS OR 0.22%

2. Nikkei closed UP 274.12 PTS OR 0.44%

WEST TEXAS INTERMEDIATE OIL UP TO 101.60

BRENT; 107,15

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 98.15/// EURO FALLS TO 1.1747 DOWN 32 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.540 UP 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.61… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.815 UP 4 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP( 6.7948 AND OFFSHORE: UP AT 6.7947

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +3.0931// Italian 10 Yr bond yield UP to 3.868// SPAIN 10 YR BOND YIELD UP TO 3.519%

3i Greek 10 year bond yield UP TO 3.766%

3j Gold at $4701.30 //Silver at: 84.11 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 33/ 100 roubles/73.96

3m oil (WTI) into the 101 dollar handle for WTI and 107 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.61 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.540% UP 2 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.815 UP 4 PTS..: USA/SF this 0.7807 as the Swiss Franc . Euro vs SF: 0.9172

USA 10 YR BOND YIELD: 4.432 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 5.001 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.973 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.40 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 5.120 UP 12 PTS

30 YR UK BOND YIELD: 5.792 UP 12 BASIS PTS

10 YR CANADA BOND YIELD: 3.539 UP 7 BASIS PTS

5 YR CANADA BOND YIELD: 3.191 UP 7 BASIS PTS.

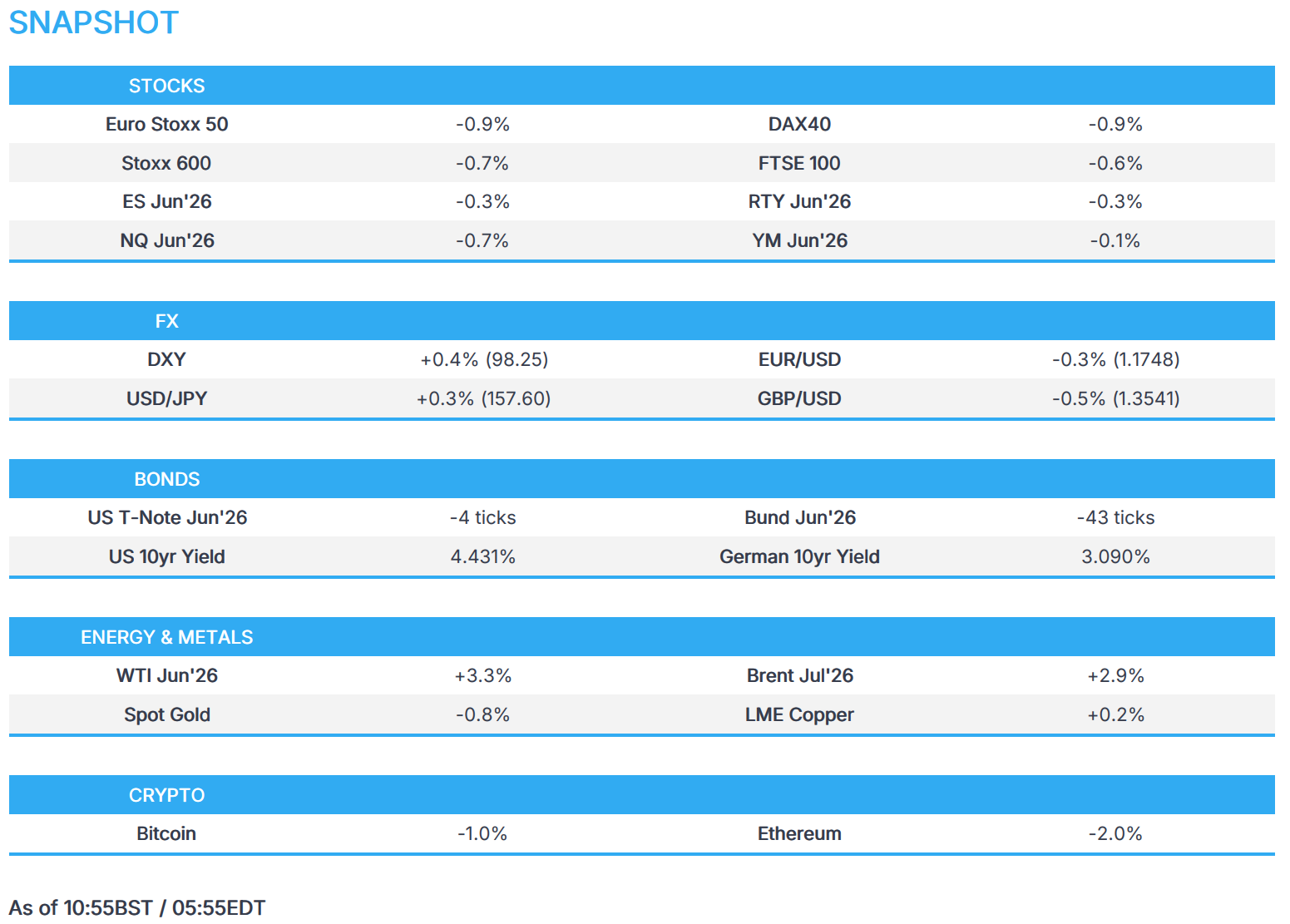

1a New York Opening report

Stocks Fall, Oil And Rates Rise As Inflation “Roars Back”

by Tyler Durden

Tuesday, May 12, 2026 – 09:21 AM

US equity futures and bonds were lower as oil climbed, with a key inflation report showing the impacts of higher energy and supply disruptions stemming from the war in Iran. Stocks are poised to fall from all-time highs after the core CPI rose more than expected in April. As of 9:15am S&P futures ewere down 0.2% and Nasdaq futures dropped 0.7% as a slide in chipmakers and big tech names dragged down the market in early US hours. In premarket trading, all Mag 7 stocks were lower. Treasury two-year yields hovered near the highest since March. Tech’s underperformance followers a weaker APAC session with KOSPI’s biggest loss since early April after the govt hintedf at a potential tax on AI profits dubbed a ‘Citizen Dividend’; the index finished off its lows pointing to the dip buying potential of Semis as the market takes advantage of any price discount. US crude rose to around $101. Gold weaker and sitting just below $4,700/oz. Economic data slate includes weekly ADP employment change (8:15am), April CPI (8:30am) and federal budget balance (2pm). Fed speaker slate includes Chicago Fed’s Goolsbee (9:10am, 1pm), and NY Fed releases quarterly report on household debt and credit at 11am

In premarket trading, Mag 7 names are all lower (Tesla -1.5%, Alphabet -0.9%, Amazon -0.8%, Nvidia -0.8%, Microsoft -0.6%, Meta -0.5%, Apple -0.4%)

- AST SpaceMobile (ASTS) falls 11% after the satellite internet company reported revenue for the first quarter that missed the average analyst estimate. The firm also had a wider loss than forecast.

- GameStop (GME) slips 3% after eBay Inc. rejected a $56 billion takeover offer from the company.

- GitLab (GTLB) is down 11% after the software company announced plans to cut jobs and make operational changes. Raymond James says efforts to retool the business while cutting staff may be challenging, while RBC says guidance for in-line 1Q results suggests no upside versus prior beats.

- Harmonic (HLIT) rises 15% after the communications equipment company reported first-quarter results that beat expectations and gave an outlook that is seen as strong, underlining positive momentum.

- Harrow (HROW) slumps 10% after the eyecare pharmaceutical firm posted an adjusted Ebitda loss for the quarter, disappointing analysts who’d forecasted a profit. The company also reported revenue for the first quarter that fell short of the average analyst estimate.

- Hims & Hers Health (HIMS) slides 15% after the telehealth firm projected 2Q Ebitda that missed consensus estimate, a result of higher costs as it transitions to branded products.

- IHeartMedia (IHRT) slips 4% after the media entertainment and radio broadcasting firm provided a disappointing forecast adjusted Ebitda for the second quarter.

- Microvast Holdings Inc. (MVST) sinks 40% after the battery firm reported first-quarter revenue that fell short of the average analyst estimate.

- PACS Group (PACS) soars 22% after the nursing home operator boosted its adjusted Ebitda guidance for the full year, following better-than-expected results for the first quarter. Truist views the quarter results as a strong start to the year.

- Plug Power (PLUG) is up 7% after the hydrogen producer’s first-quarter net revenue beat the average analyst estimate, with analysts attributing the growth to large customers such as Amazon and Walmart.

- Power Solutions International (PSIX) drops 31% after the engine and power systems manufacturer reported first-quarter revenue and income that fell short of analyst estimates and declined to give full-year guidance, citing variability in order timing and market conditions.

- Quantum Computing Inc. (QUBT) jumps 24% after the application software developer reported revenue for the first quarter that beat the average analyst estimate.

- Venture Global (VG) rises 8% after the liquefied natural gas company reported first-quarter earnings per share that beat the average analyst estimate and announced new deals with TotalEnergies and Vitol.

- Webtoon (WBTN) slumps 10% after the storytelling technology platform gave a revenue forecast for the second quarter that missed the average analyst estimate.

- Wendy’s (WEN) shares jump 23% as the Financial Times reports that Nelson Peltz’s Trian Fund Management is seeking investor backing for a bid to take the burger chain operator private.

- ZoomInfo Technologies (GTM) slides 36% after the software company reduced its full-year forecast for adjusted operating income. The company also announced a restructuring program that will cut about 600 jobs.

In other corporate news, JPMorgan has seen balances within its prime-brokerage business soar to a record as clients look to seize on recent market volatility. Amazon.com has begun the sale of its first Swiss franc bonds as it looks to raise a record six-part deal in the currency.

Wall Street traders left stocks and bonds lower as oil climbed, with today’s CPI report showing the impacts of higher energy and supply disruptions stemming from the war in Iran, resulting in hoter than expected core CPI prices: CPI rose 3.8% from a year earlier, marking the fastest pace since 2023. From a month earlier, prices were up 0.6%, while core prices rose 2.8%, higher than the 2.7% expected.

“Inflation is roaring back largely driven by stubbornly high oil prices,” said Skyler Weinand at Regan Capital. “As a result, we expect the Federal Reserve to be on hold through the summer on interest rates.”

Given that inflation is heading in the wrong direction and the labor market is holding up, it’s very unlikely that the Fed will be able to lower interest rates any time soon, according to Chris Zaccarelli at Northlight Asset Management.