GOLD $4550.00 3:30 PM)

ZERO GOLD

GOLD: NUMBER OF NOTICES FILED FOR MAY/2026: 0 CONTRACTs NOTICES FOR NIL OZ or 0.0 TONNES

total notices so far: 4067 contracts FOR 406,700 OZ OR 12.650 TONNES

SILVER NOTICES: 29 NOTICE(S) FILED FOR .145 MILLION OZ /

total number of notices filed so far this month : 5473 CONTRACTS (NOTICES) for 27.365 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY OUR SMALL QUEUE JUMP OF 32 CONTRACTS FOR 0.160 MILLION OZ/NEW STANDING ADVANCES TO 32.135 MILLION OZ/.//

SUMMARY OF OUR MAY 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 36.495 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 32 CONTRACTS/0.160 MILLION OZ//NEW STANDING ADVANCES TO 32.135 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON EARLY DURING THE MAY DELIVERY MONTH)

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 278 CONTRACT QUEUE JUMP FOR 27800 OZ/ (0.8646 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER OF 2 CONTRACTS OR 200 OZ (0.00622 TONNES) TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES FOR .4353 TONNES/STANDING NOW REDUCES TO 15.0575 TONNES OF GOLD.

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER OF 2 CONTRACTS/200 OZ// 0.00622 TONNES/ TOTAL EXCHANGE FOR RISK: 00.4353 TONNES///NEW STANDING NOW REDUCES TO 15.0575 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 46/753 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA MEGA STRONG 2369 CONTRACTS TO AN OI OF 104,516.

EFP ISSUANCE 240 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 240 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2369 CONTRACTS AND ADD TO THE 240 E.FP. ISSUED

WE OBTAIN A MEGA MEGA SIZED LOSS OF 2129 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $3.79

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 10.645 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $3.79

2.ASIAN AFFAIRS MAY 15 /2025

SHANGHAI CLOSED DOWN 42.75 PTS OR 1.02%

HANG SENG CLOSED DOWN 426.31 PTS OR 1.62%

Nikkei CLOSED DOWN 1101.05 PTS OR 1.76%

//Australia’s all ordinaries CLOSED DOWN 0.85%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.8035

/ OFFSHORE CLOSED DOWN AT 6.8060 Oil UP TO 104.75 dollars per barrel for WTI and BRENT UP TO 109.10 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING DOWN (6.8035) OFFSHORE YUAN TRADING UP TO 6.8060 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR 2877 CONTRACTS DOWN TO AN OI OF 384,401 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET LATE LAST MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD CONSIDERABLE T.A.S. LIQUIDATION DURING THURSDAY’S TRADING. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT ALSO SOME SPECULATORS STILL GOING TO THE SHORT SIDE WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MAY CONTRACT MONTH!!

THE FAIR SIZED LOSS ON OUR TWO EXCHANGES OCCURRED DESPITE OUR LOSS IN PRICE IN GOLD (DOWN $20.95).

WE THUS HAD A FAIR SIZED LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1813 CONTRACTS (OR 9.065 TONNES) WITH OUR LOSS IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.EQUATING TO 1024 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A ZERO CONTRACT FOR RISK ISSUANCE IN GOLD TOTALLING 0 CONTRACTS FOR 0 OZ OR 0.000 TONNES OF GOLD. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK ON MAY 7, SO THIS IS OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: TWO ISSUANCES SO FAR FOR 140 CONTRACTS OR 14,000OZ OR 0.4353 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: TWO ISSUANCES SO FAR FOR 140 CONTRACTS, 14,000 OZ OR 0.4353 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

DETAILS ON OUR NEW MAY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 1813 CONTRACTS WITH OUR LOSS IN PRICE ($20.95). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS FINALLY A SMALL SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 802T.A.S CONTRACTS THUS ENDING THE STREAK OF 5 HUGE ISSUANCES.. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT IS NOW IN FULL FORCE WITH TODAY’S RAID AND CAPITUALTION ON OUR PRECIOUS METALS.

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 2ND ISSUANCE FOR 0.0963 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 0.4353 TONNES ISSUED MAY 6 AND MAY 12.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER TO LONDON OF 200 OZ (.00622 TONNES) TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 14,000 OZ OR 0.4353 TONNES////NEW TOTALS STANDING FOR GOLD REDUCES TO 15/0575 TONNESS

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING MAY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $20.95)

WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION THURSDAY // COMEX SESSION// WITH OUR LOSS IN PRICE , OUR LONG SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI //SPREADER LIQUIDATION FOR TODAY,, FRIDAY WILL BE ENORMOUS WHICH I WILL REPORT ON FOR MONDAY.

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

THURSDAY NIGHT//FRIDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $20.95

WE HAD A RECORD 19,393 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES : 1813 CONTRACTS OR 181,300 OZ OR 9.065 TONNES

MAY DELIVERY MONTH

MAY 15 2026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 0 |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 0 CONTRACTS OR 0 OZ 0.0 TONNES OF GOLD |

| No of oz to be served (notices) | 634 Contracts 63,400 OZ 1.972 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4067 notices 406700 oz 12.650 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 0

xxxx

adjustments: 0

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF MAY OI STANDS AT 634 CONTRACTS HAVING A LOSS OF 211 CONTRACTS.

WE HAD 209 CONTRACTS SERVED ON THURSDAY SO WE LOST 2 CONTRACTS OR 200 OZ WERE TRANSFERRED VIA AN EXCHANGE FOR PHYSICAL TRANSFER WHERE THEY WILL TAKE DELIVERY OVER IN LONDON (0.00622 TONNES)

.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI FELL BY 2119 CONTRACTS UP TO AN OI OF 210,983

JULY GAINED 93 CONTRACTS UP TO AN OI OF 1208.

We had 0 contracts filed for today representing 0oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (4,067) to which we add the difference between the open interest for the front month of MAY (634 CONTRACTS) minus the number of notices served upon today 0 x 100 oz per contract) equals 470,100 OZ OR (14.622 Tonnes of gold) to which we add our TWO exchange for risk issuance for 14,000 oz or 0.4353 tonnes//new standing for gold/May again advances to 15.0633 tonnes.

THUS: INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (4,067) to which we add the difference between the open interest for the front month of MAY( 634 CONTRACTS) minus the number of notices served upon today 0 x 100 oz per contract) equals 470,100 OZ OR (14.622 Tonnes of gold) plus we must add our TWO exchange for risk issuances of 14,000 oz or 0.4353 tonnes/new standing advances to 15.0575 tonness

new total of gold standing in MAY ADVANCES TO 15.0575 TONNES//

TOTAL COMEX GOLD STANDING FOR MAY 15.0575 TONNES TONNES WHICH IS NOW STRONG FOR THIS NORMALLY NON ACTIVE DELIVERY MONTH OF MAY.

confirmed volume FRIDAY confirmed 124,192// poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

the number provided do not match from yesterday!!!

total pledged gold: 1,907,747.506 oz 59.34 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,907,747.506 tonnes oz 59.34 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 28,717,998.972oz

TOTAL REGISTERED GOLD 15,701,327.881OZ 488.3772 tonnes

TOTAL OF ALL ELIGIBLE GOLD 13,076,671.091 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,793,580 oz ((REG GOLD- PLEDGED GOLD)=

429.03 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

MAY DELIVERY MONTH

MAY 15

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 entries |

| Deposits to the Dealer Inventory | 0 entries |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 0 ENTRIES |

| No of oz served today (contracts) | 112 CONTRACT(S) (0.560 MILLION OZ |

| No of oz to be served (notices) | 954 Contracts (4.770 MILLION oz) |

| Total monthly oz silver served (contracts) | 5,444 contracts 27.200 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

1 entries

i) Into Stonex: 501,435.700 oz

total deposit 501,435.700 oz

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

3 ENTRIES

i) Into Asahi: 602,163.302 oz

ii) Into CNT 600,003.600 oz

iii) Into Delaware: 15,022.117

total deposit 1,217,189.059 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

one entry:

i) Stonex: 714,393.560 oz

total withdrawal: 714,393.560 oz

adjustments 1

a) Loomis: customer to dealer: 401,366.360 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 80.827 MILLION OZ//.TOTAL REG + ELIGIBLE. 315,101 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2026 OI: 983 OPEN INTEREST CONTRACTS FOR A LOSS OF 80 CONTRACTS. WE HAD 112 CONTRACTS SERVED UPON ON THURSDAY SO WE GAINED 32 CONTRACTS OR 0.160 MILLION OZ AS THESE BOYS ENTERTAINED A STRONG QUEUE JUMP WHERE THEY WILL TRY THEIR LUCK AND TAKE DELIVERY ON THIS SIDE OF THE POND.

JUNE SAW A GAIN OF 52 CONTRACTS UP TO 2964 OI CONTRACTS

JULY SAW A LOSS OF 2645 CONTRACTS DOWN TO 75,979 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 29 or 0.145 MILLION oz

CONFIRMED volume THURSDAY; 62,577 good

AND NOW MAY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 5473 X5,000 oz = 27.365 MILLION oz

to which we add the difference between the open interest for the front month of MAY (983) AND the number of notices served upon today (29 )x (5000 oz)

Thus the standings for silver for the MAY 2026 contract month: (5,473 )Notices served so far) x 5000 oz + OI for the front month of MAY (983) minus number of notices served upon today (29)x 5000 oz equals silver standing for the MAY..contract month equating to 32.135 MILLION OZ.+

NEW STANDING ADVANCES T0: 32.135 MILLION OZ WHICH IS STILL PRETTY GOOD FOR THIS ACTIVE DELIVERY MONTH OF MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 80.827 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/315.101 million: 44.49

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAY 15 /2026/WITH GOLD DOWN $118.70 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 14 /2026/WITH GOLD DOWN $20.95 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 13 /2026/WITH GOLD UP $18.75 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 12 /2026/WITH GOLD DOWN $38.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.285 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 11 /2026/WITH GOLD DOWN $2.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.515 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.995 TONNES

MAY 8 /2026/WITH GOLD UP $22.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.283 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.480TONNES

MAY 7 /2026/WITH GOLD UP $15.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.853 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1033.197TONNES

MAY 6 /2026/WITH GOLD UP $124.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.718 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1034.05TONNES

MAY 5 /2026/WITH GOLD UP $33.75 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 4 /2026/WITH GOLD DOWN $106.65 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 1 /2026/WITH GOLD UP $13.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.427 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1035.768 TONNES

APRIL 30/2026/WITH GOLD UP $19.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.142 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1039.195 TONNES

APRIL 29/2026/WITH GOLD DOWN $45.70 TODAY/NO CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 28/2026/WITH GOLD DOWN $85.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

GLD INVENTORY: 1033.995 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

MAY 15 WITH SILVER DOWN $7.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.9000 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 14 WITH SILVER DOWN $3,79: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.448 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 487.524 MILLION OZ

MAY 13 WITH SILVER UP $3,62: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.086 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 486.087 MILLION OZ

MAY 12 WITH SILVER DOWN $0.48: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.176 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 484.990 MILLION OZ

MAY 11 WITH SILVER UP $5.10: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.995 MILLION OZ OF SILVER PUT OF THE SLV// / // :INVENTORY RESTS AT 483.814 MILLION OZ

MAY 8 WITH SILVER UP $1.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.689 MILLION OZ OF SILVER INTO THE SLV// / // :INVENTORY RESTS AT 484.809 MILLION OZ

MAY 7 WITH SILVER UP $2.26: NO CHANGES IN SILVER INVENTORY AT THE SLV: / // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 6 WITH SILVER UP $3.75: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.724 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 5 WITH SILVER UP $0.21: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 4 WITH SILVER DOWN $3.05: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 1 WITH SILVER UP $2.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.905 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 484.338 MILLION OZ

APRIL 30 WITH SILVER UP $2.03: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.991 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 485.243MILLION OZ

APRIL 29 WITH SILVER DOWN $1.95: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 28 WITH SILVER DOWN $2.05: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

CLOSING INVENTORY 489.424 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

Inflation undermines all asset values

The febrile condition of all asset markets headed by rising G7 bond yields is leading to uncertainty for gold and silver prices. One last sell-off is a golden opportunity for stackers.

| Alasdair MacleodMay 15∙Paid |

For the first half of this week, gold and particularly silver prices rose before being hammered yesterday and this morning. In overnight Asian trade, gold was $4,582, down $95 from last Friday’s close, and silver at $79.20 was down $1.00. A 16,556 jump in gold’s preliminary open interest on Comex yesterday suggests active shorting by hedge funds, while open interest in silver declined by 2,270 confirming that it was gold/$ pair traders in action.

While preliminary open interest figures see some revision before being final, this selling when gold’s contract is already oversold is consistent with a final sell-off. The swaps, being mainly market makers and bullion bank trading desks which take the short side will be delighted, because they know from the quality of buying both in New York and London that they must try to achieve and maintain level books.

This sudden bearishness on the part of hedge fund traders is linked to this week’s inflation shock, with April’s accelerating to 3.8% from March’s 3.3% driven mainly by energy costs. That this should prove a shock is an indictment of sleepy markets, but traders have now been alerted to the severe consequences of oil prices rising and US reserves depleting.

Bond yields are rising in sympathy, as the chart of the US 10-year treasury note shows:

The yield is rising to test and potentially break out above the post-covid rise in yields (the upper pecked line). The long-term chart puts this in context. When yields break higher, they have the potential to at least double from current levels:

Other G7 bonds have already broken through their yield ceilings, notably Japan, the UK, Germany, and France. Canada and Italy have some way to go but like the US are also on the rise. Longer maturities are already leading the way, with the US long bond yield already testing post-covid new highs.

Clearly, measures of inflation will go significantly higher in the coming months, so bond yields in all G7 currencies will rise considerably. And as the long-term chart above of the US T-note shows it will signal a significant destruction of bond and other financial asset values.

If markets expected some relief from Trump’s visit to China this week, they will be badly let down. Cutting through the media commentary, it is clear that China may be non-confrontational, but nor will it intervene to resolve the Persian Gulf crisis. That leaves the prospect of either a continuing stalemate or an escalation by the US. Both options are globally destructive economically, ensuring a combination of a global slump and significantly higher inflation.

Meanwhile, the equity bubble continues to inflate, led by AI stocks and bitcoin which are correlating. The value divergence with bonds is already stretched to a record extent as our last chart shows:

Now that bond yields are moving higher, the equity crash will be even more spectacular when it comes, probably in a matter of weeks or even days. Sell in May and go away has never been more appropriate.

For gold and silver bugs, these are the conditions which vindicates their bullishness. They will be buying into dips such as this in the knowledge that price uncertainty is increasingly short-term. A collapse in currency purchasing power is always reflected in higher gold, silver, and commodity prices. And this time, there are inescapable debt traps to boot.

JESSE COLUMBO\

JOHN RUBINO

3.CHRIS POWELL AND HIS GATA DISPATCHES:

Alasdair Macleod: Inflation undermines all asset values

Submitted by admin on Fri, 2026-05-15 14:01 Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Friday, May 15, 2026

The febrile condition of all asset markets headed by rising G7 bond yields is leading to uncertainty for gold and silver prices. One last sell-off is a golden opportunity for stackers.

For the first half of this week, gold and particularly silver prices rose before being hammered yesterday and this morning. In overnight Asian trade, gold was $4582, down $95 from last Friday’s close, and silver at $79.20 was down $1.00. A 16,556 jump in gold’s preliminary open interest on Comex yesterday suggests active shorting by hedge funds, while open interest in silver declined by 2,270 confirming that it was gold/$ pair traders in action.

While preliminary open interest figures see some revision before being final, this selling when gold’s contract is already oversold is consistent with a final sell-off. The swaps, being mainly market makers and bullion bank trading desks which take the short side will be delighted, because they know from the quality of buying both in New York and London that they must try to achieve and maintain level books. …

… For the remainder of the analysis:

END

Billionaire Sprott put 98% of his $3 billion fortune into gold and silver and says gold is headed to $10,000

Submitted by admin on Thu, 2026-05-14 17:13 Section: Daily Dispatches

By Godwin Oluponmile

Forbes, New York

via AP MoneyWise, New York

Gold has had one of the greatest two-year runs in its history and the man who saw it coming says it’s just getting started.

Eric Sprott, 81, was at his vacation rental in San Jose, Costa Rica, in late January when Forbes checked in with him. This was right around the same time that silver had hit its all-time high of $100 an ounce, and Sprott wasn’t impressed.

…“I’m not a geologist. I know nothing about rocks, but I know about numbers. … If the reward’s a big reward I can afford to lose,” he told Forbes. “I think the prices are going much higher. I think silver can easily go to $200, even $300. I think gold could go to $10,000.”

Days later silver dropped to $76 and gold had pulled back below $5,000, but Sprott was still unfazed.

Such equanimity is easier when you’ve spent four decades being right about precious metals. Eric Sprott doesn’t claim to be a geologist, even after decades of success in the mining sector. When asked how he finds the next billion-dollar play, he keeps it simple: “Numbers took me there — numbers. You don’t have to be a geologist.” …

… For the remainder of the report:

https://finance.yahoo.com/markets/commodities/articles/billionaire-eric-sprott-put-98-141500805.htm

END

Equinox Gold bids C$7 billion for Orla Mining to create Canada’s second-largest gold producer

Submitted by admin on Wed, 2026-05-13 13:05 Section: Daily Dispatches

By Andrew Willis

The Globe and Mail, Toronto

Wednesday, May 13, 2026

Equinox Gold Corp. is bidding to join the ranks of North America’s largest gold producers with an all-stock, C$7 billion offer for Orla Mining Ltd. pitched with zero takeover premium.

Two of Orla’s largest shareholders, financier Pierre Lassonde and Fairfax Financial Holdings Ltd., and the company’s executives and directors pledged to vote their 20% holding in favour of the Equinox offer.

“Today is an incredibly exciting day for both Equinox and Orla shareholders as we announce a business combination that creates a senior North American gold producer,” Equinox chief executive officer Darren Hall said. …

… For the remainder of the report:

END

Ross Norman: India panics and burns the golden lifeboat

Submitted by admin on Wed, 2026-05-13 09:39 Section: Daily Dispatches

By Ross Norman

Metals Daily, London

Wednesday, May 13, 2026

The word I’m looking for is “contronym” — a term that can mean its own opposite — and it may be an apt description of gold right now. News that India has raised import duties on gold and silver from 6% to 15% is bullish and bearish at the same time.

We are now seeing second-order consequences of the Iran war manifest. India is particularly exposed to energy costs from what used to be called the Middle East, a region increasingly framed as East Asia — literally a matter of perspective, but I digress.

India is interesting because there are many layers to the motivations for owning gold: weddings, festivals, reliable savings, culture and fashion, and conspicuous displays of wealth. At its core, however, gold is an asset of last resort — and Indians know that.

So when the government takes an action like this — effectively burning the lifeboats to keep warm — you know there is a real problem. There is a whiff of a real panic about this … and that makes it good and bad for gold simultaneously. …

… For the remainder of the commentary:

4.ANDREW MAGUIRE LIVE FROM THE VAULT 272 and 271

Ted Oakley//272

MUST VIEW…

5. COMMODITY REPORT/GOLD AGNICO EAGLE

Agnico Eagle investing $14 billion in Northern Ontario mines

Ontario touts its fast permitting regime as a calling card to attract mining investment

Agnico Eagle, the world’s second largest gold miner, is making a landmark investment of $14 billion in its operations and assets in northeastern Ontario over the next five years.

Ammar Al-Joundi, Agnico’s president-CEO, made the announcement at George Brown College in Toronto May 13, an event hosted by the Ontario government to promote its mining-friendly policies.

Of that $14 billion, Al-Joundi said $12 billion is earmarked for across-the-board spending on its mining operations, development and exploration programs on its Ontario properties.

Agnico Eagle operates mainly in the gold-rich Abitibi region of the northeast, where its massive Detour Lake open pit is situated near the Quebec border, northeast of Cochrane, and in Kirkland Lake, where the historic Massaca mine complex has been running for more than 90 years.

In lauding Agnico as “the gold standard” in the industry, provincial Energy and Mines Minister Stephen Lecce called the investment “one of the largest to date” in the province’s history and shows strong support for the government’s new permitting regime.

Lecce said Agnico’s spending plans are the direct result of the Ford government’s red tape-cutting mandate to “move with speed” to get mines into production faster by overhauling the permitting system through its One Project, One Process. It’s all designed to promote Ontario as a world-leading jurisdiction for mining investment, he said.

“What this planned $14-billion investment represents is hope for our economy,” said Lecce, “and a message that we can do big things at scale, we move with speed, we can unlock resources responsibly, and we can lift our economy and sovereignty together.”

Al-Joundi didn’t dig into the details on how that entire $14-billion package will be spent on specific individual items or improvements, but he did say $2 billion is allocated for its major underground expansion at Detour Lake and on its Upper Beaver mine project, outside Larder Lake, scheduled to enter production by 2030.

On the job-creation front, Al-Joundi said the company expects these investments will generate roughly 1,500 new jobs, thereby boosting its Ontario workforce to 5,500.

Al-Joundi said this major investment is a reflection of the “confidence we have in Ontario” as a stable and global significant mining jurisdiction.

With other mines in Quebec, Nunavut, Australia and Finland, Northern Ontario, he said, remains important to Agnico, accounting for 30 per cent of its global production.

“Companies like Agnico Eagle can make investments anywhere in the world. We’ve chosen to be in Ontario for almost 70 years now and chosen to invest heavily and to continue to invest heavily in this province because we know Ontario is a place we can make long-term investments.”

Al-Joundi paid credit to Lecce and the ministry for making Ontario “an attractive place to invest” by improving the predictability of outcomes for mining investments and through coordinated efforts and partnerships with government, Indigenous and local stakeholders.

He emphasized the immense economic impact the mining sector can have in Northern communities through spending and jobs.

In 2025, he said Agnico contributed more than $5 billion to local economies, employed 4,100, and spent $2 billion in local goods and services, including $625 million with Indigenous-owned businesses.

“This is one company of many in the mining space in Ontario. This is a big and important industry.”

Ian Howcroft, CEO of Skills Ontario, called Agnico’s investment “wonderful news” for Ontario and its future workforce, calling the company a key partner in the organization’s efforts to promote skilled trades and technology careers, and deliver programming around the province.

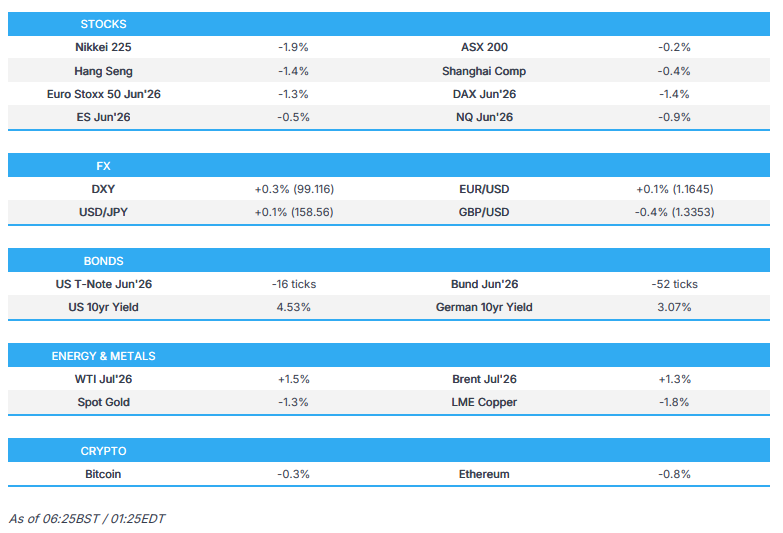

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 42.75 PTS OR 1.02%

HANG SENG CLOSED DOWN 426.31 PTS OR 1.62%

Nikkei CLOSED DOWN 1101.05 PTS OR 1.76%

//Australia’s all ordinaries CLOSED DOWN 0.85%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.8035

/ OFFSHORE CLOSED DOWN AT 6.8060 Oil UP TO 104.75 dollars per barrel for WTI and BRENT UP TO 109.10 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING DOWN (6.8035) OFFSHORE YUAN TRADING UP TO 6.8060 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.8035

OFFSHORE YUAN: UP TO 6.8060

1.HANG SANG CLOSED DOWN 426.31 PTS OR 1.62%

2. Nikkei closed DOWN 1101.05 PTS OR 1.76%

WEST TEXAS INTERMEDIATE OIL UP TO 104.75

BRENT; 109.10

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 99.08/// EURO FALLS TO 1.1635 DOWN 27 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.718 UP 9 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 158.46… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 4.080 UP 16 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN( 6.89035 AND OFFSHORE: DOWN AT 6.8060

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +3.1073// Italian 10 Yr bond yield UP to 3.877// SPAIN 10 YR BOND YIELD UP TO 3.533%

3i Greek 10 year bond yield UP TO 3.783%

3j Gold at $4561.30 //Silver at: 78.56 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 28/ 100 roubles/72.96

3m oil (WTI) into the 104 dollar handle for WTI and 109 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 158.46 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.718% UP 9 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 4.080 UP 16 PTS..: USA/SF this 0.7854 as the Swiss Franc . Euro vs SF: 0.9139

USA 10 YR BOND YIELD: 4.544 UP 9 BASIS PTS…

USA 30 YR BOND YIELD: 5.096 UP 8 BASIS PTS/

USA 2 YR BOND YIELD: 4..069 UP 8 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.55 UP 11 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 5.1220 UP 13 PTS

30 YR UK BOND YIELD: 5.7840 UP 14 BASIS PTS

10 YR CANADA BOND YIELD: 3.570 DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 3.235 UP 1 BASIS PTS.

1a New York Opening report

Futures Tumble As Reality Returns And Yields, Oil And Dollar Soar

Friday, May 15, 2026 – 08:43 AM

Bond yields, oil and the dollar are surging this morning as US futures tumble from all-time highs, with Tech underperforming driven by a series of factors including i) surging energy prices on lack of Iran war progress, ii) elevated positioning into options expiry; iii) Central bank repricing, iv) Tech sell-off driven by higher yields, and v) strikes at Samsung Electronics. The combination of stronger consumption and higher inflation is also a factor today. As of 8:00am ET, S&P futures are down 1.0% and Nasdaq futures slide 1.4% with the momentum brigade of Semis and Memory dumping (that bastion of the memory trade, Korea, sold off last night, its worst day since early March). The losses point to a bleak end to a week in which chipmakers led a narrow rally despite steadily rising yields and the absence of a US-Iran deal. Cyclicals ex-Energy are, unsurprisingly, seeing material underperformance to Defensives. Bond yields are up 4-7bps as the Dollar looks to complete its first 5-day win steak since March. In commodities, Energy is leading with Brent rising 2.3% to above $108 a barrel. Helima Croft, global head of commodity strategy at RBC Capital Markets, said an expectation that the Strait of Hormuz would reopen within the next month was “magical thinking.” Precious metals tumble on dollar strength. Today’s macro data releases are all B-grade, including Empire Mfg, Industrial / Mfg Production, and Capacity Utilization; none are market-moving.

In premarket trading, Mag 7 stocks are mostly lower: Microsoft (MSFT) rises 0.7% after Pershing Square Chief Executive Officer Bill Ackman said he’s taken a new stake in the compan ( Alphabet -1.6%, Amazon -1.5%, Apple -1.2%, Nvidia -2%, Meta -0.7%, Tesla -1.9%)

- Dexcom (DXCM) rises 3% after the diabetes device maker gave long-term growth outlook at its investor day that impressed analysts. Separately, activist investor Elliott Investment Management took a stake in the company and struck a settlement that will put two independent directors on the board.

- Dlocal (DLO) falls 8% after the emerging markets payment services provider reported first-quarter results that missed expectations in terms of net income and earnings.

- Figma (FIG) rises 10% after the creative software platform reported first-quarter results that beat expectations and raised its full-year forecast. Analysts said the report eased concerns about AI-related disruption.

- Gemini Space Station (GEMI) gains 21% after the fintech firm announced that Winklevoss Capital Fund has made a $100 million strategic investment in the company, at a price of $14 per share.

- Globant (GLOB) climbs 5% after the IT services company reported first-quarter results that beat expectations.

- Magnum Ice Cream (MICC) US-listed shares rise 12% after Reuters reported that private equity firms including Blackstone and Clayton Dubilier & Rice are exploring potential bids for the company.

- NU Holdings Ltd. (NU) falls 3% after the Brazil-based financial institution reported the cost of credit climbing 72% in the first quarter from the same period a year earlier.

- Papa John’s (PZZA) gains 6% after Reuters reported investment firm Irth Capital is working with the pizza chain’s largest US franchisee, who controls around 10% of its domestic restaurants, to take the company private. Reuters cited three sources which it did not identify.

In other corporate news, Kioxia said it would list its shares in the US as it reaps the benefits of a global memory chip shortage that’s ratcheted up prices of the vital component. OpenAI CFO said the ChatGPT maker may raise more capital, as the company races to secure computing power to meet surging AI demand.

A broad selloff in bond markets dragged stocks lower, bringing a sudden halt to the artificial intelligence-fueled equity rally that has pushed the S&P 500 from one record high to the next. The sentiment reversal reflects some profit taking after recent gains, and a lack of concrete progress between Trump and Xi beyond cordial niceties. Also Fed Chair Powell’s term comes to an end today, just as the 10-year Treasury hit 4.5% for the first time overnight since June, prompting a swoon in equity futures.

With a summit between President Donald Trump and China’s Xi Jinping ending without any path to resume flows through Hormuz, the impasse between the US and Iran is moving back into focus. Traders will now watch the next steps the two countries take after more than two months of war.

“There’s no question that momentum has been so aggressive on the upside that the risk of a correction is there,” Paul Skinner of Wellington Management told Bloomberg TV. “With a background of bond markets looking unsettled, with the problem of inflation, with the Strait of Hormuz not having a solution out of that Summit, I think there definitely is some volatility to come.”

Brent crude rose 2.3% to above $108 a barrel. Helima Croft, global head of commodity strategy at RBC Capital Markets, said an expectation that the Strait of Hormuz would reopen within the next month was “magical thinking.”

“There seems to be an emerging consensus that the Strait of Hormuz will reopen in June because the cost of continued closure will be too high,” she wrote. “We are very skeptical. The optimistic scenario seems predicated on the tenuous assumption that there is a relatively easy policy lever that can be pulled.”

In central bank news, the Governor Barr pushed back against proposals to shrink the Fed’s balance sheet, describing them as wrong and a threat to financial stability. The Fed’s Williams said there’s no reason to raise or cut rates right now.

Meanwhile, the turmoil in UK markets is showing no sign of ending as investors price in the possibility of more expansive fiscal policy under a potential successor to Prime Minister Keir Starmer. Manchester Mayor Andy Burnham secured a pathway for a future challenge, unsettling investors who were rattled last year by his comments that the country was “in hock” to bond markets. The prospect of a seventh prime minister in 10 years “is not a record of which any nation would be proud,” said Russ Mould, investment director at AJ Bell. “It is contributing to how the UK has the highest 10-year bond yield in the G7.”

Growing price pressures and a series of key dates next month are setting up the stock market for profit taking, according to Bank of America strategists. Michael Hartnett cited the next OPEC gathering, the start of the World Cup, the Group of Seven summit and the first Federal Reserve FOMC meeting under Kevin Warsh as catalysts. US inflation is on course to exceed 5% by November’s midterm elections unless the 0.4% monthly gains of the past half year slow rapidly. A scenario where inflation climbs above 4% is “where risk assets get twitchy,” Hartnett said. “Bull capitulation into stocks and tech likely fully complete in next few weeks, early June ripe for taking some off table.”

One thing that Xi has that Trump wants is low interest rates, notes BofA’s Michael Hartnett. The strategist had previously said if the 30-year Treasury yield severely breached the 5% threshold, “the door to doom starts to open.” The jury is still out on whether Powell did enough to bring inflation back to target, notes Anna Wong in a Bloomberg Eco Essential Read. The problem is that if macro – and bond yields- actually matters again, then the S&P is about 1000 points too high.

Elsewhere, BofA strategists noted that US large-cap stock funds attracted their largest inflows in five weeks at $24.4 billion, in the week to May 13, citing EPFR Global data. Discussions around positioning and momentum continue at pace. Momentum in large caps is on a tear, with the factor up more than 30% on a long/short basis this year, tracking one of the strongest six-month stretches in more than two decades.

Given the Nasdaq 100’s run-up, it’s worth taking note that the rarely seen “spot up/vol-up” correlation is evident in options. It’s part of the FOMO trade as traders, especially the retail cohort, chase upside through long calls. In a sign of how heated price action has become, the poster child of the AI melt-up, South Korea’s Kospi, touched the 8,000 level before reversing and sinking 7%. All sectors in the benchmark were sharply lower.

In geopolitics, US Trade Representative Jamieson Greer said he anticipates that China would commit to billions in American agricultural purchases. The CIA Director visited Cuba for talks with top leaders as the US grows frustrated over a lack of progress in economic and political change. California Governor Gavin Newsom is proposing a new tax on cloud-based software sales to raise revenue for the state.

European stocks are following their Asian counterparts lower as oil prices rise on concerns that the Strait of Hormuz will remain shut for longer. Miners fall the most while the health care subindex is the leading performer. Stoxx 600 falls 1.2% to 608.54. Here are some of the biggest movers on Friday:

- Technoprobe shares rally as much as 39%, the most on record, after the Italian company raised its revenue and margin guidance for 2027 and said it expected to hit those revised targets a year early, indicating soaring demand for its semiconductor probe cards.

- Dino Jumps shares jump as much as 18%, the most on record, after the retailer beat first-quarter earnings estimates, with an acceleration in like-for-like sales growth that outpaced competitors. The results should improve sentiment toward the stock, which has fallen nearly 50% over the past 12 months.

- Syensqo shares rally as much as 12%, its biggest gain in over 13 months, after the chemicals company reported Ebitda ahead of expectations in the first quarter. Citi said the beat and the improving order book are reassuring investors.

- Salvatore Ferragamo shares fall as much as 19% after the luxury goods maker reported first-quarter revenue below analyst estimates. Analysts said Europe remained the weakest region because of the company’s reliance on wholesale, while North America posted strong growth. Ongoing conflict in the Middle East remains a key risk to Ferragamo’s turnaround.

- Grafton shares drop as much as 3.8% to trade at a 13-month low, after Citi said tougher trading conditions will weigh on consensus estimates for the building supplies company. Analysts said weakness in the UK is being offset by growth in other regions.

- European miners are heavily underperforming on Friday, as copper continues to retreat from the record-high close seen earlier this week. Accelerating US inflation reduced the chance of rate cuts and a stronger dollar make the red metal more expensive for many buyers. Gold is also falling.

The tech sector fueled losses in Europe and Asia too, with the Stoxx 600 falling 1.4%. South Korea’s high-flying Kospi index tumbled 6.1% as investors cashed out of Samsung Electronics Co. and SK Hynix Inc. Nvidia Corp. slid 2.1% in premarket trading after a seven-day streak of gains. Asian equities slid the most since March as higher oil prices fueled concerns over inflation, with heavyweight Korean chip stocks leading the declines after a dizzying rally. The MSCI Asia Pacific Index lost 2.2%, snapping a five-week winning streak. Samsung Electronics and SK Hynix, which contributed to much of Kospi’s roughly 80% rally this year, each dropped over 6% on Friday. Almost all national benchmarks in the region traded lower as Brent crude headed for its biggest weekly advance in three, with efforts to end the Iran war in limbo and the crucial Strait of Hormuz staying effectively closed. President Donald Trump made conflicting remarks on Hormuz, telling Fox News the US doesn’t need the waterway open, and then later saying “we want the straits open” while sitting alongside Chinese leader Xi Jinping in Beijing.

Japan’s government bond yields marched higher across the curve in the latest sign that elevated oil prices are raising inflation concerns across global debt markets. Meanwhile, India’s state-run refiners raised fuel prices for the first time in four years.

In FX, the US dollar has been the main beneficiary, looking to complete its first 5-day win steak since March, after a jump in oil prices reignited inflation concerns and sparked a selloff across global bond markets. The Bloomberg Dollar Spot Index is up 0.3% to its highest level this month.

In rates, bonds fell across the Americas, Europe and Asia as doubts grew over whether oil supplies from the Middle East will normalize anytime soon. Scorching wholesale inflation data in Japan offered a fresh warning of price pressures building throughout the global economy. Treasuries broadly hold losses seen in early Asia session as oil pushes higher with the Strait of Hormuz still effectively closed and efforts to end the war in limbo. Yields are off session highs however leading into the early US session as oil gains unwind slightly. Yields remain cheaper by 2bp to 6bp across the curve in a bear steepening move. US 10-year yields trade near session highs around 4.55%, and highest since May. Front-end outperforms slightly, steepening the US 2s10s and 5s30s spreads by 3bp and 2.5bp on the day. Gilts lag, with UK yields trading cheaper by 9bp to 14bp across the curve.While around 14bp of easing is priced by December, or about 55% of a 25bp move, Fed-dated OIS swaps price 25bp of rate hikes by the April policy meeting next year. In UK, political pressure also in play for gilts along with gains in oil, adding to underperformance, after Manchester Mayor Andy Burnham secured a pathway to potentially challenge Keir Starmer for the prime minister’s job. Wider losses seen across gilts, where long-end trades cheaper by 14bp on the day.

Japan’s government bond yields marched higher across the curve to effectively what are new record highs for the modern era, in the latest sign that elevated oil prices are raising inflation concerns across global debt markets. Meanwhile, India’s state-run refiners raised fuel prices for the first time in four years.

In commodities, Brent crude futures earlier topped $109 a barrel after representatives for Iran bemoaned contradictory US messages, and the The decline in Treasuries has pushed US 10-year yields up 6 bps to 4.54%. Metals are broadly lower with spot silver dropping 6%.

Economic data slate includes May Empire manufacturing (8:30am) and April industrial production (9:15am). Fed speaker slate empty for the session.

Market Snapshot

- S&P 500 mini -1.1%

- Nasdaq 100 mini -1.6%

- Russell 2000 mini -1.2%

- Stoxx Europe 600 -1.4%

- DAX -1.7%

- CAC 40 -1.4%

- 10-year Treasury yield +6 basis points at 4.54%

- VIX +1.5 points at 18.79

- Bloomberg Dollar Index +0.4% at 1202.79

- euro -0.4% at $1.1622

- WTI crude +3.7% at $104.88/barrel

Top Overnight News

- US President Donald Trump left China on Friday with no major breakthroughs on trade or tangible help from Beijing to end the Iran war, despite two days spent heaping praise on his host, Xi Jinping. RTRS

- An underappreciated surplus of crude oil, sloshing around storage tanks and aboard ships, cushioned the global economy when the Persian Gulf closed 2½ months ago. That excess supply is now dwindling at a record pace, with oil executives and analysts predicting that a harsh reckoning is set to upend the relative calm in energy markets. Acute shortages of key fuels and soaring prices could emerge within weeks if the Strait of Hormuz remains shut. WSJ

- President Donald Trump said the US objective of recovering highly enriched uranium from Iran was “more for public relations than it is for anything else,” while reiterating his commitment to removing the nuclear material. BBG

- Iran has allowed some Chinese vessels to pass through the Strait of Hormuz following diplomatic overtures from China’s government, semiofficial Iranian news agencies reported on Thursday. WSJ

- The UAE will double its capacity to export crude oil bypassing the Strait of Hormuz by next year, as it seeks to reduce reliance on the shipping chokepoint. WSJ

- UK borrowing costs hit their highest level since 2008 on Friday and the pound dipped as traders priced in a greater likelihood that Andy Burnham would challenge Sir Keir Starmer for the Labour leadership. The 10-year bond yield rose as much as 0.15 percentage points to 5.15 per cent, as the price of the debt fell, taking the UK’s benchmark borrowing costs above a post-2008 high set earlier this week. FT