EXCHANGE: COMEX

CONTRACT: MAY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,552.500000000 USD

INTENT DATE: 05/18/2026 DELIVERY DATE: 05/20/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 1

555 C BNP PARIBAS SEC CORP 20

661 C JP MORGAN SECURITIES 11

905 C ADM 32

TOTAL: 32 32

MONTH TO DATE: 4,696

GOLD: NUMBER OF NOTICES FILED FOR MAY/2026: 32 CONTRACTs NOTICES FOR 3,200 OZ or 0.0995 TONNES

total notices so far: 4696 contracts FOR 469,600 OZ OR 14.6065 TONNES

SILVER NOTICES:123 NOTICE(S) FILED FOR .615 MILLION OZ /

total number of notices filed so far this month : 5628 CONTRACTS (NOTICES) for 28.140 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY OUR STRONG 89 CONTRACT QUEUE JUMP FOR 0.455 MILLION OZ/NEW STANDING ADVANCES TO 32.575 MILLION OZ/.//

SUMMARY OF OUR MAY 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 49.175 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 445,000 OZ//NEW STANDING ADVANCES TO 32.575 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON EARLY DURING THE MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX.

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 278 CONTRACT QUEUE JUMP FOR 27800 OZ/ (0.8646 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 32 CONTRACTS OR 3200 OZ (0.0995 TONNES) TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK ISSUANCES FOR 11.676 TONNES/STANDING NOW ADVANCES TO 28.245 TONNES OF GOLD.

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 32 CONTRACTS/3200 OZ// 0.0995 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK 3 OCCASIONS: 11.676 TONNES///NEW STANDING NOW ADVANCES TO 28.248 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 61.29 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A STRONG 900 CONTRACTS TO AN OI OF 101,952.

EFP ISSUANCE 453 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 453 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 900 CONTRACTS AND ADD TO THE 453 E.FP. ISSUED

WE OBTAIN A STRONG LOSS OF447 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $0.09

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 2/235 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $0.09

2.ASIAN AFFAIRS MAY 19 /2025

SHANGHAI CLOSED UP 38.01 PTS OR 0.92%

HANG SENG CLOSED UP 122.67 PTS OR 0.48%

Nikkei CLOSED DOWN 75.45 PTS OR 0.12%

//Australia’s all ordinaries CLOSED UP .40%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.8035

/ OFFSHORE CLOSED DOWN AT 6.8064 Oil UP TO 108.03 dollars per barrel for WTI and BRENT UP TO 110.32 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN (6.8035) OFFSHORE YUAN TRADING DOWN TO 6.8064 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL 440 CONTRACTS UP TO AN OI OF 379,360 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET LATE LAST MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD ZERO T.A.S. LIQUIDATION DURING MONDAY’S TRADING. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MAY CONTRACT MONTH!!

THE SMALL SIZED GAIN ON OUR TWO EXCHANGES OCCURRED WITH OUR LOSS IN PRICE IN GOLD (DOWN $4.90).

WE THUS HAD A SMALL SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 635 CONTRACTS (OR 1.975 TONNES) DESPITE OUR LOSS IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 1075 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A ZERO CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD.YESTERDAY, BY FAR HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: THREE ISSUANCES SO FAR FOR 3754 CONTRACTS OR 375,400OZ OR 11.676 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: THREE ISSUANCES SO FAR FOR 3754 CONTRACTS, 375,400 OZ OR 11.676 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

DETAILS ON OUR NEW MAY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A SMALL GAIN ON OUR TWO EXCHANGES OF 635 CONTRACTS DESPITE OUR LOSS IN PRICE ($4.90). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS FINALLY A SMALL SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 656 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT IS NOW IN FULL FORCE WITH TODAY’S RAID AND CAPITULATION ON OUR PRECIOUS METALS.

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 3RD ISSUANCE FOR 11.676 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 13.676 TONNES ISSUED MAY 6 ,MAY 12 AND MAY 18.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 3200 OZ (0.0995 TONNES) TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK ISSUANCE FOR 375,400 OZ OR 11.676 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 28.248 TONNESS

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING MAY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $4.90)

WE HAD NO T.A.S. SPREADER LIQUIDATION MONDAY // COMEX SESSION// WITH OUR LOSS IN PRICE , OUR LONG SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $4.90

WE HAD A 10,882 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 635 CONTRACTS OR 63,500 OZ OR 1.975 TONNES

MAY DELIVERY MONTH

MAY 19 2026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 2 i) HSBC 32,118.849 oz 1000 kilobars) ii) Out of Manfra: 32,151.000 oz total: 64,302.000 oz (2000 kilobars) |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 32 CONTRACTS OR 3200 OZ 0.0995 TONNES OF GOLD |

| No of oz to be served (notices) | 634 Contracts 63,400 OZ 1.972 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4696 notices 469,600 oz 14.6065 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 2

i) HSBC 32,118.849 oz

1000 kilobars)

ii) Out of Manfra: 32,151.000 oz

total: 64,302.000 oz (2000 kilobars)

adjustments: 1

customer to dealer; Delaware 4019.735 oz

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF MAY OI STANDS AT 666 CONTRACTS HAVING A LOSS OF 565 CONTRACTS.

WE HAD 597 CONTRACTS SERVED ON MONDAY SO WE GAINED 32 CONTRACTS OR 3200 OZ (0.0995 TONNES)

UNDERWENT A SMALL QUEUE JUMP WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND.

.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI FELL BY 8864 CONTRACTS DOWN TO AN OI OF 192,597

JULY GAINED 490 CONTRACTS UP TO AN OI OF 1727.

We had 32 contracts filed for today representing 3200oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 32 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 11 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (4,696) to which we add the difference between the open interest for the front month of MAY (666 CONTRACTS) minus the number of notices served upon today 32 x 100 oz per contract) equals 532,800 OZ OR (16.572 Tonnes of gold) to which we add our THREE exchange for risk issuance for 375,400 oz or 11.676 tonnes//new standing for gold/May again advances to 28.248 tonnes.

THUS: INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (4,696) to which we add the difference between the open interest for the front month of MAY( 616 CONTRACTS) minus the number of notices served upon today 32 x 100 oz per contract) equals 532,800 OZ OR (16.578 Tonnes of gold) plus we must add our THREE exchange for risk issuances of 375,400 oz or 11.676 tonnes/new standing advances to 28.248 tonness

new total of gold standing in MAY ADVANCES TO 28.248 TONNES//

TOTAL COMEX GOLD STANDING FOR MAY 28.248 TONNES TONNES WHICH IS NOW STRONG FOR THIS NORMALLY NON ACTIVE DELIVERY MONTH OF MAY.

confirmed volume FRIDAY confirmed 188,390// fair// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

the number provided do not match from yesterday!!!

total pledged gold: 1,900,154,312 oz 59.10 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,900.154.312 tonnes oz 59.10 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 28,713,696.972oz

TOTAL REGISTERED GOLD 15,705,347 OZ 488.502 tonnes

TOTAL OF ALL ELIGIBLE GOLD 13,008,349.350 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,805,193 oz ((REG GOLD- PLEDGED GOLD)=

429.39 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

MAY DELIVERY MONTH

MAY 19

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries i) Out of Loomis: 300,494.800 oz ii_ Out of Delaware: 19,923.967 oz total withdrawal 320,418.767 oz |

| Deposits to the Dealer Inventory | 1 entries i) Into Stonex; 49,163.830 oz total deposit 49,163.830 oz |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT DEPOSIT ENTRIES/CUSTOMER ACCOUNT 1 ENTRIES i) Into Asahi 560,372.200 oz total deposit 560,372.200 oz |

| No of oz served today (contracts) | 123 CONTRACT(S) (0.615 MILLION OZ |

| No of oz to be served (notices) | 887 Contracts (4.435 MILLION oz) |

| Total monthly oz silver served (contracts) | 5,628 contracts 28.140 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

1 entries

1 entries

i) Into Stonex; 49,163.830 oz

total deposit 49,163.830 oz

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

i) Into Asahi 560,372.200 oz

total deposit 560,372.200 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

2 entries

i) Out of Loomis: 300,494.800 oz

ii_ Out of Delaware: 19,923.967 oz

total withdrawal 320,418.767 oz

adjustments 2 customer to dealer

a) Brinks: customer to dealer: 89,663.430 oz

b) Manfra: customer to dealer 80,224.300 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 81.565 MILLION OZ//.TOTAL REG + ELIGIBLE. 315.880 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2026 OI: 1010 OPEN INTEREST CONTRACTS FOR A GAIN OF 57 CONTRACTS. WE HAD 32 CONTRACTS SERVED UPON ON MONDAY SO WE GAINED 89 CONTRACT OR 0.445 MILLION OZ UNDERWENT A STRONG QUEUE JUMP WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND.

JUNE SAW A LOSS OF 196 CONTRACTS DOWN TO 2865 OI CONTRACTS

JULY SAW A LOSS OF 880 CONTRACTS DOWN TO 73,570 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 123 or 0.615 MILLION oz

CONFIRMED volume MONDAY; 63,818 fair

AND NOW MAY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 5628 X5,000 oz = 28.140 MILLION oz

to which we add the difference between the open interest for the front month of MAY (1010) AND the number of notices served upon today (123 )x (5000 oz)

Thus the standings for silver for the MAY 2026 contract month: (5,628 )Notices served so far) x 5000 oz + OI for the front month of MAY (1010) minus number of notices served upon today (123)x 5000 oz equals silver standing for the MAY..contract month equating to 32.575 MILLION OZ.+

NEW STANDING ADVANCES T0: 32.575 MILLION OZ WHICH IS STILL PRETTY GOOD FOR THIS ACTIVE DELIVERY MONTH OF MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 81.565 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/315.880 million: 44.33

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAY 19 /2026/WITH GOLD DOWN $46.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.57 TONNES OF GOLD INTO THE GLD./ //:/INVENTORY RESTS AT 1038.85 TONNES

MAY 18 /2026/WITH GOLD DOWN $4.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 15 /2026/WITH GOLD DOWN $118.70 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 14 /2026/WITH GOLD DOWN $20.95 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 13 /2026/WITH GOLD UP $18.75 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 12 /2026/WITH GOLD DOWN $38.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.285 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 11 /2026/WITH GOLD DOWN $2.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.515 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.995 TONNES

MAY 8 /2026/WITH GOLD UP $22.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.283 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.480TONNES

MAY 7 /2026/WITH GOLD UP $15.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.853 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1033.197TONNES

MAY 6 /2026/WITH GOLD UP $124.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.718 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1034.05TONNES

MAY 5 /2026/WITH GOLD UP $33.75 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 4 /2026/WITH GOLD DOWN $106.65 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 1 /2026/WITH GOLD UP $13.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.427 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1035.768 TONNES

APRIL 30/2026/WITH GOLD UP $19.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.142 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1039.195 TONNES

APRIL 29/2026/WITH GOLD DOWN $45.70 TODAY/NO CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 28/2026/WITH GOLD DOWN $85.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

GLD INVENTORY: 1038.85 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

MAY 19 WITH SILVER DOWN $2.39: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.086 MILLION OZ OUT OF THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 18 WITH SILVER DOWN $0.09: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 15 WITH SILVER DOWN $7.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.9000 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 14 WITH SILVER DOWN $3,79: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.448 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 487.524 MILLION OZ

MAY 13 WITH SILVER UP $3,62: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.086 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 486.087 MILLION OZ

MAY 12 WITH SILVER DOWN $0.48: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.176 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 484.990 MILLION OZ

MAY 11 WITH SILVER UP $5.10: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.995 MILLION OZ OF SILVER PUT OF THE SLV// / // :INVENTORY RESTS AT 483.814 MILLION OZ

MAY 8 WITH SILVER UP $1.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.689 MILLION OZ OF SILVER INTO THE SLV// / // :INVENTORY RESTS AT 484.809 MILLION OZ

MAY 7 WITH SILVER UP $2.26: NO CHANGES IN SILVER INVENTORY AT THE SLV: / // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 6 WITH SILVER UP $3.75: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.724 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 5 WITH SILVER UP $0.21: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 4 WITH SILVER DOWN $3.05: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 1 WITH SILVER UP $2.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.905 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 484.338 MILLION OZ

APRIL 30 WITH SILVER UP $2.03: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.991 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 485.243MILLION OZ

APRIL 29 WITH SILVER DOWN $1.95: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 28 WITH SILVER DOWN $2.05: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

CLOSING INVENTORY 488.338 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

4.ANDREW MAGUIRE LIVE FROM THE VAULT 272 and 271

Ted Oakley//272

MUST VIEW…

5. COMMODITY REPORT/GOLD

AGNICO EAGLE/HOPE BAY

Hope Bay approved at 400,000 production for a minimum of 11 years. Going underground!!

AgnicoEagle – AGNICO EAGLE APPROVES HOPE BAY INVESTMENT DECISION; STRONG ECONOMIC RETURNS WITH EXPECTED ANNUAL GOLD PRODUCTION OF OVER 400,000 OUNCES

TORONTO, May 19, 2026 /CNW/ – Agnico Eagle Mines Limited (NYSE: AEM) (TSX: AEM) (“Agnico Eagle” or the “Company”) is pleased to report a positive investment decision for its Hope Bay project, located in Nunavut, Canada. Following significant exploration success in recent years, the Company has completed a preliminary economic assessment (the “2026 Study”) which contemplates an underground mining operation supported by a 6,000 tonnes per day (“tpd”) processing facility with estimated annual gold production of between 400,000 and 435,000 ounces. The 2026 Study outlines an initial mine life of 11 years, with substantial upside potential from regional exploration across the highly prospective 80-kilometre greenstone belt extending south from the Doris mine to the Boston deposit, where the Company continues to pursue an aggressive exploration program.

“We are incredibly proud of our team for transforming Hope Bay from a vision into one of Canada’s most important new mines in just five years. With expected annual production of over 400,000 ounces and total cash costs below $1,000 per ounce, based on only half the declared mineral resources drilled, Hope Bay has the potential to evolve into a long-life, district-scale mining camp for decades to come,” said Ammar Al-Joundi, Agnico Eagle’s President and Chief Executive Officer. “The construction and redevelopment of Hope Bay will support the long‑term sustainability of our Nunavut operating platform at between 800,000 ounces and one million ounces of annual gold production and represents the first major milestone toward delivering our targeted 20% to 30% production growth over the next decade. We are also proud that this investment will contribute to the economic development of Northern Canada and enable meaningful, long‑term economic participation for Indigenous organizations and partners, including the Kitikmeot Inuit Association,” added Mr. Al-Joundi.

Highlights from the 2026 Study include:

- Development of the next large-scale gold mine in Nunavut

- Large and high-quality mineral resource base of 5.79 million ounces of gold (31.97 million tonnes grading 5.63 grams per tonne (“g/t”) gold) in the measured and indicated category and 3.33 million ounces of gold (17.33 million tonnes grading 5.97 g/t gold) in the inferred category

- An initial 11‑year mine life which incorporates only approximately 55% of measured and indicated mineral resources and 48% of inferred mineral resources, highlighting substantial upside potential. With continued infill and expansion drilling, the Hope Bay project demonstrates strong prospects to extend mine life and further grow its production profile

- Startup plan contemplates three mining fronts (Doris at the Doris deposit; and Madrid and Patch 7 at the Madrid deposit) supported by a conventional 6,000 tpd milling facility

- Average annual steady state gold production of approximately 435,000 ounces and an average of approximately 408,000 ounces over the full initial 11-year mine life

- Attractive economics with meaningful upside leverage

- Initial development capital expenditures1 are estimated at approximately $2.4 billion, including reconstruction of the processing facility, addition of a 37 megawatt diesel generator power plant, mobile equipment, upgrades to the tailings facility and approximately 33 kilometres in underground development, positioning the operation for multi-decade potential

- Cost structure is below the Company’s current peer-leading cost profile, with projected average total cash costs per ounce2 and all in sustaining costs (“AISC”) per ounce2 of approximately $958 and $1,214, respectively, using current gold prices of $4,500 per ounce and a C$/US$ exchange rate of 1.36

- In this initial phase, the Hope Bay project is expected to generate an after-tax internal rate of return (“IRR”) of approximately 26% based on the same assumptions

- Significant exploration upside is expected to extend mine life through mineral resource conversion and expansion drilling at the Doris and Madrid deposits in the short-term and the potential addition of Boston as a satellite deposit in the medium- to long-term

- Project significantly de-risked and execution-ready

- Detailed engineering is approximately 62% complete, providing a high level of confidence in the capital cost estimate and execution plan

- Significant surface infrastructure upgrades completed, including enhancements to port facilities, camp infrastructure and water management systems, supporting the ramp-up of construction activities

- Leveraging the Company’s nearly 20 years of proven expertise in Arctic mine construction and operations

- Key underground access points are advanced, including the Naartok East exploration ramp and the Patch 7 exploration portal and ramp

- Continued aggressive exploration program planned in the coming years across the broader Hope Bay property

“Over nearly 20 years, we have consistently created value through the drill bit across our Nunavut assets. At Hope Bay, the discovery of the new mineralized zone at Patch 7 was transformative, with high‑grade and thick mineralized intercepts defining a new mining area within the Madrid deposit. This success reflects the strength and agility of our exploration team, which quickly identified this high‑potential opportunity following the acquisition of the project and delivered results through an aggressive and well‑executed exploration program over the last five years,” said Guy Gosselin, Agnico Eagle’s Executive Vice President, Exploration. “Patch 7 underscores the significant exploration upside of the Hope Bay greenstone belt, and we remain highly encouraged by the opportunity to continue growing mineral resources both at depth and laterally at Doris and Madrid in the near term, at the Boston deposit in the medium-to long-term and continue to unlock further value across the highly prospective 80‑kilometre belt,” added Mr. Gosselin.

- Significant exploration potential to grow underground mineral resources

- The 2026 Study is based on a mineral resource estimate which relies on a drill database cut-off of August 28, 2025. The Company has since drilled more than 130 holes totalling over 100,000 metres at Hope Bay to the end of April 2026 in an ongoing exploration program. Recent exploration results show the potential to significantly expand the underground mineral resource between Suluk and Patch 7, to the south of Patch 7 towards Patch 14, and at depth

- Over the next three years, as part of the Company’s exploration budget, more than $100 million in exploration spending is planned at Hope Bay, primarily focused on conversion and expansion drilling of the current underground mineral resource. Work in 2026 includes continued testing and extension of the Patch 7 zone and the resumption of diamond drilling at Boston

- Continue to enhance value through optimization studies and regional exploration focus

- The Boston deposit is located approximately 50 kilometres south of the Madrid deposit and hosts approximately 1.01 million ounces of gold in indicated mineral resources (5.48 million tonnes grading 5.72 g/t gold) and 0.47 million ounces of gold in inferred mineral resources (2.85 million tonnes grading 5.14 g/t gold). It contains some of the highest-grade intersections identified at Hope Bay to date and remains open in all directions. Resuming exploration efforts at Boston aims to test known gold mineralization in the southern portion of the Hope Bay greenstone belt, exploring the gap between Madrid and Boston where fertile rocks and structures are expected to potentially increase economic mineralization

- Ongoing district‑scale exploration across Hope Bay’s extensive land position will focus on satellite targets and the highly prospective corridor between the Madrid and Boston deposits. This area, which lies along the same greenstone belt and major deformation zones, has seen only limited shallow drilling historically and is expected to be a core focus of the Company’s exploration strategy in the coming years, alongside continued advancement of the Boston deposit. Regional work will also incorporate geophysics, geochemistry, and modern exploration techniques to refine targeting and support the identification of additional deposits across the belt

- END

NICKEL

SUPPLY FEARS

Nickel Jumps As Indonesian Output Cut Stokes Supply Fears

Tuesday, May 19, 2026 – 12:05 PM

Nickel prices on the London Metal Exchange surged as much as 2.6% to $19,050 a ton after Shanghai Metals Market said upwards of 15% of high-grade nickel pig iron capacity at Indonesia’s Weda Bay Industrial Park will undergo rotational maintenance in the coming months, according to Bloomberg.

Indonesia’s Weda Bay Industrial Park is one of the most important nickel-processing hubs in the world and serves a large cluster of smelters that produce nickel pig iron, a key input for stainless steel production.

Indonesia dominates global nickel supply, producing 2.6 million metric tons of nickel in 2025 out of a global total of 3.9 million tons, accounting for roughly two-thirds of global mine production.

So, the earlier news from SMM indicating a 10% to 15% reduction in NPI output from Weda Bay Industrial Park in the coming months, building on existing NPI reductions in March and April due to lower ore supplies and high costs, has easily sparked supply concerns on the LME …

Nickel is extremely valuable and a critical industrial metal in the era of electrification and data center buildouts:

- Stainless steel, by far the largest demand center, where nickel improves corrosion resistance, strength, and heat tolerance.

- EV and energy-storage batteries, especially nickel-rich lithium-ion chemistries that increase energy density and driving range.

- Aerospace and military superalloys, including jet-engine turbine blades and high-temperature gas turbines.

- Industrial alloys, plating, and catalysts, used across machinery, chemicals, and corrosion-resistant equipment.

Let’s not forget that sulfuric acid prices have surged amid the Hormuz disruption. This industrial chemical is used in nickel production, especially in Indonesia’s battery-grade nickel supply chain.

The line in the sand for LME nickel futures is $20,000.\

END

GOLD

China, debt, gold: What’s happening under the surface

by Monetary Metals

Monday, May 18, 2026 – 14:51

In this episode, Joseph Solis-Mullen joins us for a sweeping conversation on China’s economy, America’s debt spiral, and the growing global appeal of gold.

From ghost cities and financial repression to reserve currencies and demographic decline, Joseph cuts through the headlines to explain what’s really happening beneath the surface of both the Chinese and U.S. systems.

We explore why China may not want to replace the dollar, how government debt quietly reshapes everyday life, and why both governments and citizens are increasingly turning to gold as a trusted store of value in an era of mounting uncertainty.

Watch the episode now.

Follow Monetary Metals on X: @Monetary_Metals

Follow Jeff Snider on X: @solis_mullen

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 38.01 PTS OR 0.92%

HANG SENG CLOSED UP 122.67 PTS OR 0.48%

Nikkei CLOSED DOWN 75.45 PTS OR 0.12%

//Australia’s all ordinaries CLOSED UP .40%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.8035

/ OFFSHORE CLOSED DOWN AT 6.8064 Oil UP TO 108.03 dollars per barrel for WTI and BRENT UP TO 110.32 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN (6.8035) OFFSHORE YUAN TRADING DOWN TO 6.8064 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.8035

OFFSHORE YUAN: DOWN TO 6.8064

1.HANG SANG CLOSED UP 122.67 PTS OR 0.48%

2. Nikkei closed DOWN 75.45 PTS OR 0.12%

WEST TEXAS INTERMEDIATE OIL UP TO 108.03

BRENT; 110.32

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 99.09/// EURO FALLS TO 1.1631 DOWN 24 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.792 UP 5 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.06… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 4.149 UP 5 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP( 6.8003 AND OFFSHORE: UP AT 6.8053

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +3.1502// Italian 10 Yr bond yield DOWN to 3.9090// SPAIN 10 YR BOND YIELD DOWN TO 3.525%

3i Greek 10 year bond yield DOWN TO 3.820%

3j Gold at $4544.30 //Silver at: 76.07 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 98/ 100 roubles/71.46

3m oil (WTI) into the 108 dollar handle for WTI and 110 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.06 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.792% UP 5 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 4.149 UP 5 PTS..: USA/SF this 0.7856 as the Swiss Franc . Euro vs SF: 0.9137

USA 10 YR BOND YIELD: 4.604 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 5.140 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.061 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.58 UP 0 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 5.0740 DOWN 5 PTS

30 YR UK BOND YIELD: 5.727 DOWN 4 BASIS PTS

10 YR CANADA BOND YIELD: 3.693 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 3.351 UP 0 BASIS PTS.

1a New York Opening report

Futures Fall As Momentum Cracks Grow With Yields And Oil Higher

Tuesday, May 19, 2026 – 07:58 AM

US equity futures are lower, set for a 3rd drop in a row, as traders waited for futile signs of progress toward a peace deal in the Middle East. and as tech and small cap stocks reacted adversely to higher bond yields around the globe, but nowhere more so than in Japan, where many tenors are trading at record lows, as the wheels have fully come off the clown bus, aka the Bank of Japan. As of 7:30am ET, Nasdaq 100 futures slid 0.8% as a retreat in tech shares pulled stocks lower in the US and Asia; S&P futures were down 0.4%, putting the benchmark on course for its longest losing streak since March. In premarket trading, semis/memory names remain under pressure; GOOGL and MSFT outperformed their Mag 7 peers, with Nvidia’s earnings looming as the next major test for the AI trade. Sandisk slipped again as the selloff in memory stocks continued. Financials and Staples are two of the bright spots despite Defensives generally leading Cyclicals. South Korea’s Kospi – ground zero of the global memory momentum bubble – led losses in Asia as the momentum trade cracks (with foreign investors pulling money for a 9th straight day). Europe’s Stoxx 600 rose 0.7% as media and financial services outperformed: the continent’s outperformance may be the market expressing the view that the next rotation is underway. The USD traded near session highs, reversing a modest drop earlier, which helped send 10Y yields to session highs around 4.62%. Oil reversed overnight losses to trade at session highs while. Commodities are mixed after Trump said he is delaying Iranian attacks due to GCC requests to find a deal. Today’s macro data focus is on weekly ADP and Pending Home Sales. Given bond yields, the Goldilocks zone for ADP has narrowed: too high and inflation concerns flare and too low and the narrative shifts to stagflation.

In premarket trading, Mag 7 stocks are mostly lower as Alphabet and Microsoft outperformed their Mag 7 peers, with Nvidia’s earnings looming as the next major test for the AI trade. Sandisk Corp. slipped as the selloff in memory stocks continued. (Alphabet +0.5, Microsoft +1, Meta -0.3, Amazon -0.7%, Apple -0.6%, Nvidia -0.7%, Tesla -1%).

- Agilysys (AGYS) is up 15% after the hospitality software company reported its fourth-quarter results.

- Hyperliquid Strategies (PURR) rises 12% as the Securities and Exchange Commission is said to ready plans for trading crypto versions of stocks.

- XP (XP) falls 5.9% after the Brazilian asset management company reported first-quarter earnings that missed estimates. Revenues from fixed-income products sold to retail clients were especially weak, analysts said, weighed down by elevated interest rates.

- Agilysys (AGYS) rises 20% after the hospitality software company posted quarterly results that topped estimates.

- Amer Sports (AS) rises 4% after it raised full-year guidance and first-quarter results beat estimates, buoyed by demand for Salomon shoes.

- Hyperliquid Strategies (PURR) rises 12% as the Securities and Exchange Commission is said to ready plans for trading crypto versions of stocks.

- Relay Therapeutics (RLAY) rises 14% after the drug developer gave initial clinical data from a mid-stage trial to treat vascular anomalies. TD Cowen calls the data “best case scenario.”

- Stubhub (STUB) rises 4% as Guggenheim Securities upgrades to buy from neutral citing upside to 2026 numbers.

- XP (XP) falls 4% after the Brazilian asset management company reported first-quarter earnings that missed estimates. Revenues from fixed-income products sold to retail clients were especially weak, analysts said, weighed down by elevated interest rates.

In other corporate news, Clear Street is cutting jobs and replacing its CEO, as the Wall Street brokerage firm pivots after abandoning a plan to go public earlier this year. Google agreed to create an AI cloud business with Blackstone, aiming to compete with companies like CoreWeave in a burgeoning market. A jury rejected Elon Musk’s claims that OpenAI betrayed its mission to benefit the public by morphing into a for-profit business, finding that he waited too long to sue the company. Meanwhile, the “Muskonomy” imminently gets a second stock with the SpaceX IPO and that could create problems for Tesla, as explored in the latest Tech Watch column.

The AI/momentum rally is faltering after powering global equities to record highs in the face of rising bond yields and elevated crude prices. As noted last night, the two-day drop in high beta momentum was the biggest since 2022.

The recent boom in pockets of the market such as semiconductors and non-profitable tech has traders wondering if the next move is buy the dip or sustained rotation into other places. At the same time, lagging sectors such as healthcare are catching up after underperforming over the past few weeks.

Meanwhile, asset allocators increased their equity exposure to stocks by the most on record to a net 50% overweight from 13% last month, and are now most overweight stocks since January 2022, Bank of America’s Global Fund Manager Survey shows. The most crowded trade, referenced by 73% of respondents, is long semiconductors, followed by long Mag-7 (14%) and long oil (6%).

JPMorgan Market Intelligence desk expects any pullback to be short-lived, dips will likely be bought on the strength in macro and micro, the return of retail investors, the perceived restart of corporate buybacks, and a generally positive take on impending market catalysts.

“The performance of the semis has been parabolic, so it’s not surprising there’s some profit-taking,” said Roger Lee, head of equity strategy at Cavendish. “Maybe there is also an element of the returning doubts over the monetization of AI.”

Hedging costs appear to be picking up, with normalized skews on the major indexes increasing from last week’s trough, which saw Nasdaq 100 sentiment the most bullish in more than a year.

Speaking of AI, so far the only tangible benefit is scapegoating it for mass layoffs: the recent trend of job cuts on the back of “AI efficiencies” continues to make headlines. Meta is reassigning 7,000 workers to new jobs related to AI, according to an internal memo, part of a broad corporate restructuring that includes planned staff reductions later this week. Standard Chartered said it would cut corporate functions roles by more than 15% by 2030 and scale practical uses of AI to streamline processes.

And then there is the war in iran. “Investors are desperate for the Middle East conflict to end as that should, in theory, help to bring down oil prices, dampen talk of rate hikes, and switch the conversation back to economic growth,” said Dan Coatsworth, head of markets at AJ Bell. “For now, the conflict rumbles on and investors remain slightly cautious.”

After oil-driven inflation drove bond yields steadily higher since the start of the war in the Middle East, traders are now zeroing in on 5.5% as the next key level for 30-year Treasuries, according to Citigroup Inc. strategist Jim McCormick.

“I see markets underpricing the risk of a Fed rate hike starting this year,” he said. Swap traders are currently leaning toward a 25 basis point increase in December, with a move fully priced for March next year.

Nicolas Bickel, group head of investment for private banking at Edmond de Rothschild, told Bloomberg TV he wouldn’t be surprised to see 10-year US yields at 5%. The rate rose three basis points to 4.62% on Tuesday. “If we have higher inflation and growth stays steady, it will not be an issue,” he said.

In political news, Trump announced his administration is adding more than 600 generic medications to its direct-to-consumer drug sales website TrumpRx alongside billionaire Mark Cuban. The SEC is poised to roll out a plan for trading digital versions of securities that could reshape the landscape of the American stock market as it continues to loosen the rules for free-wheeling crypto markets.

In Europe, the Stoxx 600 is thus far avoiding declines and is up by 0.7%, led by media, financial services and retail stocks. Most sectors advance, with the basic resources subindex the only significant decliner. Here are the biggest movers Tuesday:

- Evolution gains as much as 13%, the most since Oct. 2024, after the Swedish online gambling company approved a €2 billion share buyback program. Analysts say the size of the buyback program is a welcome signal of confidence

- IG Group shares rise as much as 9.8% to a new high after first-quarter revenue beat analysts’ forecasts and the online trading company lifted its full-year guidance

- Intrum gains as much as 18% after UBS upgraded the Swedish credit services group to buy from neutral, saying the announcement of a fully-underwritten capital increase is a “clear inflection point for the equity story”

- Lagercrantz gains as much as 8.5% to a record high after the Swedish industrial group reported earnings ahead of estimates. DNB Carnegie describes the update as very solid, citing a high pace of acquisitions during the year

- Currys shares gain as much as 12% after a trading update and are now in positive territory for the year. Analysts welcomed a third consecutive upgrade to pretax profit guidance

- Hansa Biopharma gains as much as 30% after the company sold the exclusive development and commercialization rights to Idefirix in the EU, UK, Switzerland, Norway, Liechtenstein, Iceland and the Middle East and North Africa regions

- Vallourec falls as much as 11%, the most since July 2024, after ArcelorMittal sold shares in the French tubular solutions company at a discount. Morgan Stanley calls the news a surprise

- Grieg Seafood falls as much as 8.1%, the most in a month, after the Norwegian fisheries firm posted weak results and trimmed full-year forecasts, which analysts expect will cause consensus estimates to be slashed

- Boxer declined as much as 5.8% after Pick n Pay Stores raised 4.7 billion rand by selling 57.3 million ordinary shares of the retailer — representing 12.5% of Boxer’s total issued shares — through an accelerated bookbuild offering

- Forterra shares slip as much as 7.9% to the lowest since November 2023 after the UK brickmaker reported soft trading and gave cautious commentary for FY26

- Nanobiotix shares drop as much as 9.5%, falling for a third day after hitting a record last week. That trimmed the French biotechnology company’s rally since the FDA accepted a streamlined trial design in early May for its experimental cancer drug

Asian stocks dropped for a third session as a lack of clarity over an Iran peace deal and elevated global bond yields weighed on risk sentiment. The MSCI Asia Pacific Index fell as much as 0.9%, heading for its longest losing streak since March. South Korea’s Kospi Index was one of the worst performers, tumbling more than 3% as rising bond yields dulled the appeal of growth stocks like chipmakers. Risk appetite remained muted even after President Donald Trump said he was holding off on fresh strikes on Iran, as investors focused on elevated oil prices that have fanned inflation concerns. Those worries are keeping bond yields higher for longer, offsetting optimism over the benefits of the artificial intelligence boom. “Global bond yields moving higher are sending a clear reality check: sustained high energy prices could bring tighter monetary conditions sooner rather than later,” according to Tim Waterer, chief market analyst at KCM Trade.

Over the past five years, the MSCI Asia Pacific Index has fallen in 16 of the 19 weeks when the US 10-year Treasury yield rose by 20 basis points or more, losing an average 1.6%, according to data compiled by Bloomberg. Last week fit that pattern. Indonesian shares were on track for a sixth session of declines as speculation mounted that the government will centralize commodity exports to control capital flows and shore up a plunging currency. Meanwhile, benchmarks in mainland China, Hong Kong and Australia rose. Chipmakers Samsung Electronics Co., SK Hynix Inc. and Taiwan Semiconductor Manufacturing Co. were among the biggest drags on the regional gauge. In Japan, the broader benchmark Topix index rebounded, led by banks after stronger-than-expected GDP data fueled speculation the central bank could raise interest rates again.

In FX, the Bloomberg Dollar Spot Index is up 0.3%, while the Aussie is the underperformer after RBA minutes.

In rates, Treasuries are weaker with 10-year yields up two basis points following similar price action in bunds while gilts outperform after lower-than-forecast UK April jobs figures. US 10-year yield near 4.61% (vs session high 4.62%) underperforms UK counterpart by almost 5bp; US 30-year near 5.15% is also about 1bp off day’s high. US yields are 2bp-3bp cheaper across a slightly flatter curve; Fed-OIS contracts price in around 16 basis points of tightening by year-end and fully price in a hike by the March policy meeting. UK bonds are outperforming in Europe after soft labour market data. Ten-year gilt yields are down four basis points and bets on Bank of England rate hikes have been pulled back. G dollar issuance slate includes five deals already; Monday saw Merck’s $6 billion bond sale lead eight borrowers pricing a combined $12.2 billion of new debt. Kennametal, Mobility Global and Xylem are candidates for Tuesday after holding market exercises Monday. Treasury auctions this week include $16 billion 20-year bonds (Wednesday) and $19 billion 10-year TIPS reopening (Thursday). Focal points of US session include comments by Fed Governor Waller at 8am New York time and potential for another large corporate new-issue calendar.

In commodities, oil prices have reversed overnight losses with Brent sitting a little above $110 after Trump said he’d called off a strike on Iran following an appeal by Persian Gulf allies

Economic data slate includes ADP weekly employment change (8:15am) and April pending home sales (10am). Fed speaker slate includes Waller (8am) and Paulson (7pm).

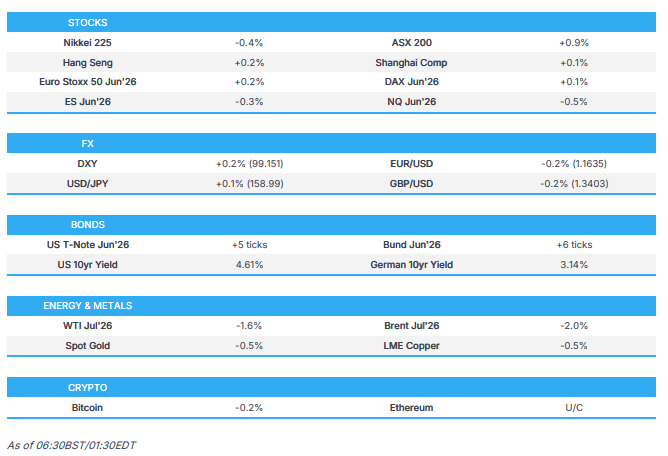

Market Snapshot

- S&P 500 mini -0.3%

- Nasdaq 100 mini -0.6%

- Russell 2000 mini -0.4%

- Stoxx Europe 600 +0.8%

- DAX +1.3%

- CAC 40 +0.9%

- 10-year Treasury yield +2 basis points at 4.61%

- VIX +0.3 points at 18.15

- Bloomberg Dollar Index +0.3% at 1203.27

- euro -0.3% at $1.1616

- WTI crude -1.1% at $107.5/barrel

Top Overnight News

- President Trump said he would hold off on a planned U.S. attack on Iran at the request of Gulf leaders to make room for negotiations with Tehran over a prospective deal to end the war. The White House didn’t provide additional details about the planned attack. Several Gulf officials from some of the countries Trump mentioned said they were not aware of the imminent plan to attack Iran he described. WSJ

- Trump said ‘hopefully, maybe forever’ regarding the decision to delay the Iran attack, while he added that they will probably be satisfied if they can make a deal where Iran doesn’t get a nuclear weapon. Trump also stated that countries requested to put off the attack on Iran briefly and asked if an attack on Iran could be delayed 2-3 days: Truth Social

- US officials told the NYT that Iran has taken advantage of the ceasefire to re-expose dozens of bombed ballistic missile sites, move mobile missile launchers, and adjust its tactics in anticipation of a possible resumption of attacks, according to Amichai Stein.

- Vladimir Putin arrives in Beijing for talks with Xi Jinping as the Iran war offers Russia an opportunity to deepen energy links with China. Putin and Xi are due to meet tomorrow. BBG

- Soaring borrowing costs could trigger a “correction” in the stock market, highlighting a growing disconnect between exuberant equities and bonds battered by worries over high inflation. FT

- Financial market turbulence could force the Bank of Japan to go slow on the unwinding of its massive debt holdings, giving anxious bond investors some relief as surging yields lay bare worsening fiscal strains and inflation pressures. RTRS

- Japan’s economy grew much faster than expected at the start of the year, supporting the case for further Bank of Japan interest-rate hikes, though the outlook remains highly uncertain due to the Middle East conflict. Japan’s economy grew 2.1% on an annualized basis in the first quarter, exceeding economists’ forecast for a 1.7% increase. BBG