EXCHANGE: COMEX

CONTRACT: MAY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,506.300000000 USD

INTENT DATE: 05/19/2026 DELIVERY DATE: 05/21/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 21

118 C MACQUARIE FUTURES US 4

363 H WELLS FARGO SECURITI 709

555 C BNP PARIBAS SEC CORP 715

657 H MORGAN STANLEY 5

661 C JP MORGAN SECURITIES 118

732 C RBC CAP MARKETS 104

905 C ADM 40

TOTAL: 858 858

MONTH TO DATE: 5,554

GOLD: NUMBER OF NOTICES FILED FOR MAY/2026: 858 CONTRACTs NOTICES FOR 85,800 OZ or 2.644 TONNES

total notices so far: 5554 contracts FOR 555,400 OZ OR 17.275 TONNES

SILVER NOTICES:16 NOTICE(S) FILED FOR .080 MILLION OZ /

total number of notices filed so far this month : 5644 CONTRACTS (NOTICES) for 28.220 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY OUR SMALL 3 CONTRACT EXCHANGE FOR PHYSICAL TRANSFER JUMP TO LONDONO FOR 0.015 MILLION OZ/NEW STANDING REDUCES TO 32.560 MILLION OZ/.//

SUMMARY OF OUR MAY 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 50.405 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.560 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX.

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 278 CONTRACT QUEUE JUMP FOR 27800 OZ/ (0.8646 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 861 CONTRACTS OR 86,100 OZ (2.6750 TONNES) TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK ISSUANCES FOR 11.676 TONNES/STANDING NOW ADVANCES TO 30.932 TONNES OF GOLD.

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 861 CONTRACTS/86100 OZ// 2.6750 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK 3 OCCASIONS: 11.676 TONNES///NEW STANDING NOW ADVANCES TO 30.932 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 71.937 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE 1201 CONTRACTS TO AN OI OF 100,751.

EFP ISSUANCE 246 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 246 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1199 CONTRACTS AND ADD TO THE 246 E.FP. ISSUED

WE OBTAIN A MEGA STRONG LOSS OF 955 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR HUGE LOSS OF $2.39

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.775 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $2.39

2.ASIAN AFFAIRS MAY 20 /2025

SHANGHAI CLOSED DOWN 7.35 PTS OR 0.18%

HANG SENG CLOSED DOWN 146.73 PTS OR 0.37%

Nikkei CLOSED DOWN 8-8/59 PTS OR 1.34%

//Australia’s all ordinaries CLOSED DOWN .56%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.8047

/ OFFSHORE CLOSED DOWN AT 6.8059 Oil DOWN TO 102.79 dollars per barrel for WTI and BRENT DOWN TO 109.23 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN (6.8047) OFFSHORE YUAN TRADING DOWN TO 6.8059 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A TINY 35 CONTRACTS UP TO AN OI OF 379,325 CONTRACTS (OI) , HAVING ADVANCED FROM OUR NEW LOW OI SET LATE LAST MONTH AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,700.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD CONSIDERABLE T.A.S. LIQUIDATION DURING TUESDAY’S TRADING. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MAY CONTRACT MONTH!!

THE STRONG SIZED GAIN ON OUR TWO EXCHANGES OCCURRED DESPITE OUR LOSS IN PRICE IN GOLD (DOWN $46.50).

WE THUS HAD A STRONG SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 3387 CONTRACTS (OR 10.53 TONNES) DESPITE OUR LOSS IN PRICE, AS WE WERE INFORMED OF A STRONG CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 3422 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A ZERO CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD.YESTERDAY, BY FAR HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: THREE ISSUANCES SO FAR FOR 3754 CONTRACTS OR 375,400OZ OR 11.676 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: THREE ISSUANCES SO FAR FOR 3754 CONTRACTS, 375,400 OZ OR 11.676 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

DETAILS ON OUR NEW MAY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG GAIN ON OUR TWO EXCHANGES OF 3387 CONTRACTS DESPITE OUR LOSS IN PRICE ($46.50). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS FINALLY A FAIR SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1455 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT IS NOW IN FULL FORCE WITH TODAY’S RAID AND CAPITULATION ON OUR PRECIOUS METALS.

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 3RD ISSUANCE FOR 11.676 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 13.676 TONNES ISSUED MAY 6 ,MAY 12 AND MAY 18.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 86100 OZ (2.6780 TONNES) TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK ISSUANCE FOR 375,400 OZ OR 11.676 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 30.932 TONNESS

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING MAY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $46.50)

WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION TUESDAY // COMEX SESSION// WITH OUR LOSS IN PRICE , OUR LONG SPECULATORS STILL REMAIN RELENTLESS POURING INTO THE COMEX

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

TUESDAY NIGHT//WEDNESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $46.50

WE HAD A 5466 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 3387 CONTRACTS OR 338,700 OZ OR 10;534 TONNES

MAY DELIVERY MONTH

MAY 20 2026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 2 i) LOOMIS 32,151.000 oz 1000 kilobars) ii) Out of Manfra: 32.151.000 oz 1 KILOBAR total: 32,183.151 oz (1001 kilobars) 1.001 TONNE |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 858 CONTRACTS OR 85,800 OZ 2.644 TONNES OF GOLD |

| No of oz to be served (notices) | 637 Contracts 63,700 OZ 1.981 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5554 notices 555,400 oz 17.275 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxx

comex withdrawals:

ENTRIES; 2

i) LOOMIS 32,151.000 oz

1000 kilobars)

ii) Out of Manfra: 32.151.000 oz 1 KILOBAR

total: 32,183.151 oz (1001 kilobars)

1.001 TONNE

adjustments: 2//CUSTOMER TO DEALER;

a) Brinks customer to dealer: 482.265 oz

b) customer to dealer; Delaware 1500.281 oz

total adjusted out of eligible into dealer acct: 1982.546 oz

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF MAY OI STANDS AT 1495 CONTRACTS HAVING A GAIN OF 829 CONTRACTS.

WE HAD 32 CONTRACTS SERVED ON TUESDAY SO WE GAINED A HUGE 861 CONTRACTS OR 86,100 OZ (2.6780 TONNES)

UNDERWENT A HUGE QUEUE JUMP WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND.

.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI FELL BY 6646 CONTRACTS DOWN TO AN OI OF 185,951. JUNE BECOMES THE NEW FRONT MONTH.

JULY LOST 40 CONTRACTS DOWN TO AN OI OF 1687.

We had 858 contracts filed for today representing 85,800oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 858 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 118 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (5,554) to which we add the difference between the open interest for the front month of MAY (1495 CONTRACTS) minus the number of notices served upon today 858 x 100 oz per contract) equals 619,100 OZ OR (19.256 Tonnes of gold) to which we add our THREE exchange for risk issuance for 375,400 oz or 11.676 tonnes//new standing for gold/May again advances to 30.932 tonnes.

THUS: INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (5,554) to which we add the difference between the open interest for the front month of MAY( 1495 CONTRACTS) minus the number of notices served upon today 858 x 100 oz per contract) equals 619,100 OZ OR (19.256 Tonnes of gold) plus we must add our THREE exchange for risk issuances of 375,400 oz or 11.676 tonnes/new standing advances to 30.932 tonness

new total of gold standing in MAY ADVANCES TO 30.932 TONNES//

TOTAL COMEX GOLD STANDING FOR MAY 30.932 TONNES TONNES WHICH IS NOW STRONG FOR THIS NORMALLY NON ACTIVE DELIVERY MONTH OF MAY.

confirmed volume TUESDAY confirmed 170,688// fair// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

the number provided do not match from yesterday!!!

total pledged gold: 1,911,131.257 oz 59.44 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,911,131.257 tonnes oz 59.44 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 28,681,513.821oz

TOTAL REGISTERED GOLD 15,707,330.162 OZ 488.563 tonnes

TOTAL OF ALL ELIGIBLE GOLD 12,974,183.659 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,796.199 oz ((REG GOLD- PLEDGED GOLD)=

429.11 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

MAY DELIVERY MONTH

MAY 20

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries i) Out of Loomis: 640,,863.900 oz ii Out of Delaware: 993.3000 oz total withdrawal: 641,857.300 oz |

| Deposits to the Dealer Inventory | 1 entries i) Into Stonex; 49,163.830 oz total deposit 49,163.830 oz |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT DEPOSIT ENTRIES/CUSTOMER ACCOUNT 2 ENTRIES i) Into Loomis: 600,238.950 oz ii) Into Manfra: 18,974.367 total deposit 619,213.317 oz |

| No of oz served today (contracts) | 16 CONTRACT(S) (0.080 MILLION OZ |

| No of oz to be served (notices) | 868 Contracts (4.340 MILLION oz) |

| Total monthly oz silver served (contracts) | 5,644 contracts 28.220 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

1 entries

1 entries

i) Into Stonex; 49,163.830 oz

total deposit 49,163.830 oz

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

2 ENTRIES

i) Into Loomis: 600,238.950 oz

ii) Into Manfra: 18,974.367

total deposit 619,213.317 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

2 entries

i) Out of Loomis: 640,,863.900 oz

ii Out of Delaware: 993.3000 oz

total withdrawal: 641,857.300 oz

adjustments 1 customer to dealer

a) Delaware 100,961.685 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 81.669 MILLION OZ//.TOTAL REG + ELIGIBLE. 315.857 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2026 OI: 884 OPEN INTEREST CONTRACTS FOR A LOSS OF 126 CONTRACTS. WE HAD 123 CONTRACTS SERVED UPON ON TUESDAY SO WE LOST 3 CONTRACT OR 0.015 MILLION OZ UNDERWENT AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE THEY WILL TAKE DELIVERY OVER ON THAT SIDE OF THE POND. IT SHOWS THAT THERE IS NO REAL PHYSICAL SILVER OVER HERE TO BE DELIVERED UPON.

JUNE SAW A GAIN OF 35 CONTRACTS UP TO 2900 OI CONTRACTS

JULY SAW A LOSS OF 1100 CONTRACTS DOWN TO 72,470 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 16 or 0.080 MILLION oz

CONFIRMED volume TUESDAY; 53,122 fair

AND NOW MAY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 5644 X5,000 oz = 28.220 MILLION oz

to which we add the difference between the open interest for the front month of MAY (884) AND the number of notices served upon today (16 )x (5000 oz)

Thus the standings for silver for the MAY 2026 contract month: (5,644 )Notices served so far) x 5000 oz + OI for the front month of MAY (884) minus number of notices served upon today (16)x 5000 oz equals silver standing for the MAY..contract month equating to 32.560 MILLION OZ.+

NEW STANDING REDUCES T0: 32.560 MILLION OZ WHICH IS STILL PRETTY GOOD FOR THIS ACTIVE DELIVERY MONTH OF MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 81.669 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/315.857 million: 44.39

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAY 20 /2026/WITH GOLD UP $26.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.999 TONNES OF GOLD OUT OF THE GLD./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 19 /2026/WITH GOLD DOWN $46.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.57 TONNES OF GOLD INTO THE GLD./ //:/INVENTORY RESTS AT 1038.85 TONNES

MAY 18 /2026/WITH GOLD DOWN $4.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 15 /2026/WITH GOLD DOWN $118.70 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 14 /2026/WITH GOLD DOWN $20.95 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 13 /2026/WITH GOLD UP $18.75 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 12 /2026/WITH GOLD DOWN $38.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.285 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 11 /2026/WITH GOLD DOWN $2.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.515 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.995 TONNES

MAY 8 /2026/WITH GOLD UP $22.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.283 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.480TONNES

MAY 7 /2026/WITH GOLD UP $15.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.853 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1033.197TONNES

MAY 6 /2026/WITH GOLD UP $124.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.718 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1034.05TONNES

MAY 5 /2026/WITH GOLD UP $33.75 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 4 /2026/WITH GOLD DOWN $106.65 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 1 /2026/WITH GOLD UP $13.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.427 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1035.768 TONNES

APRIL 30/2026/WITH GOLD UP $19.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.142 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1039.195 TONNES

APRIL 29/2026/WITH GOLD DOWN $45.70 TODAY/NO CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 28/2026/WITH GOLD DOWN $85.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

GLD INVENTORY: 1036.851 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

MAY 20 WITH SILVER UP $1.27: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 19 WITH SILVER DOWN $2.39: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.086 MILLION OZ OUT OF THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 18 WITH SILVER DOWN $0.09: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 15 WITH SILVER DOWN $7.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.9000 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 14 WITH SILVER DOWN $3,79: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.448 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 487.524 MILLION OZ

MAY 13 WITH SILVER UP $3,62: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.086 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 486.087 MILLION OZ

MAY 12 WITH SILVER DOWN $0.48: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.176 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 484.990 MILLION OZ

MAY 11 WITH SILVER UP $5.10: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.995 MILLION OZ OF SILVER PUT OF THE SLV// / // :INVENTORY RESTS AT 483.814 MILLION OZ

MAY 8 WITH SILVER UP $1.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.689 MILLION OZ OF SILVER INTO THE SLV// / // :INVENTORY RESTS AT 484.809 MILLION OZ

MAY 7 WITH SILVER UP $2.26: NO CHANGES IN SILVER INVENTORY AT THE SLV: / // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 6 WITH SILVER UP $3.75: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.724 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 5 WITH SILVER UP $0.21: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 4 WITH SILVER DOWN $3.05: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 1 WITH SILVER UP $2.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.905 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 484.338 MILLION OZ

APRIL 30 WITH SILVER UP $2.03: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.991 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 485.243MILLION OZ

APRIL 29 WITH SILVER DOWN $1.95: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 28 WITH SILVER DOWN $2.05: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

CLOSING INVENTORY 488.338 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

Bond yields and gold

Higher bond yields are undermining gold and silver. We examine why, and what are the consequences.

| Alasdair MacleodMay 20∙Paid |

Brien Lundin (@Brien_Lundin) posted this chart on X, which explains much about why gold, and also silver, have weakened recently. In recent months, the negative correlation with US Treasury yields has been very close.

This prompts the question as to why this should be so. Obviously, it reflects changes in the spread between gold’s lease rate and rising bond yields. This is a legacy of the last four decades, when the propaganda struggle to establish the dollar as money replacing gold gradually succeeded.

At least, this was the belief that gradually held sway. If the gold standard was no more than a barbarous relic and gold was little more than a pet rock, of course the dollar was king. Never mind that the dollar was a fiat currency, an imaginary money created by the US government’s central bank.

So long as participants in financial markets believe this tosh, then clearly a rise in dollar interest rates will act to make non-yielding gold less valuable. In other words, we can see why it is that when rates rise, gold weakens. But it is an effect always constrained to a period of perceived currency stability in domestic markets. Not only do US markets default to this error, but markets in thrall to the dollar, such as London and elsewhere fall for it as well.

A large part of it stems from the financialisation of economies stemming from London’s Big-Bang in the mid-80s, when gold was used as the basis of a carry trade investing in US T-bills. Gold was sold for T-bills, fixing interest rate differentials as drivers of price in collective minds.

The relationship between gold and the dollar of the 1970s and instances of heightened inflation and bond yields were quickly forgotten. At the beginning of that decade, the Fed’s funds rate was 3.7% and gold $35. In 1981, the fund’s rate was 19% and gold hit $850. In other words, there was a positive correlation between the two.

Why the difference?

Clearly, a negative correlation between dollar rates and the dollar gold price can exist only when in general terms inflation is not seen to be a significant concern. It can be expected to rise and fall under the general control of the monetary authorities: at least in the sense that it won’t run away. This tells us that while the inflation outlook is changing for the worse, financial markets in the West take the collective view that it will be just a temporary blip.

Lundin’s chart tracks the relationship only since late-March and shows a closely negative relationship between the 10-year Treasury note and the gold price. The same chart from the beginning of January tells a different story.

There were times when the negative correlation occurred, but gold still managed a substantial rise between April 2025 and late-February when the net change in the bond yield was about 10 basis points. It appears that the negative correlation has been good only in parts.

Context is everything. Until the US decided to wage war on Iran, investors expected interest rates to decline in 2026, hopes reflected in bond yields declining over most of 2025. But inflation remained above the Fed’s target, and central banks were buying gold, not impressed by relative yield arguments.

We now face a different environment, for which markets have yet to adjust. There is little doubt that instead of interest rate cuts in 2026, we should now expect them to rise. This is beginning to be reflected in higher bond yields, but the full implications are not yet reflected in gold. Higher inflation is in fact a loss of currency purchasing power. The calculation becomes one of assessing that loss potential against the bond yield which compensates for that risk. At 4.6% on the 10-year maturity, is the compensation for loss of the dollar’s purchasing power sufficient?

We can all have our opinions, but the indications are growing that it is not sufficient and that we will see higher bond yields. If the assumption is that the higher yields will not destabilise government finances, then doubtless gold will be sold or marked down accordingly. But if there is a likelihood of significantly higher inflation, a slump, or government funding facing a debt trap, then the risk will be in the bond, not in gold, which emerges as a safe haven.

It is often the case in a currency decline that foreigners take a different view from domestic users. It is clear from all commentary that domestic users of the dollar see minimal danger to the value of their currency. They are just beginning to suspect that interest declines are now on hold and that increases are a remote but increasing possibility. The same can be said for domestic users of yen, euros, and sterling.

Foreign insiders appear to take the opposite view. While domestic users of G7 currencies are yet to be alarmed and are sellers of gold and silver, they are being bought by foreign central banks and sovereign wealth funds, as well as investing institutions and citizens who are selling down their holdings of these currencies. While America sells, China and others buy, until there’s none left.

In March alone, China and India imported 561 tonnes of silver through London, which in turn imported 601 tonnes from the US, while the price fell from over $90 to under $70.

The risk they see should not be ignored. They see the end of the dollar-based fiat currency system. That will happen anyway as the imagination that currencies are money faces reality — as always happens eventually.

The hit to the dollar’s purchasing power from the war against Iran and the closure of the Strait of Hormuz is turbocharging its decline, bringing forward its extinction. That’s what the Asian hegemons see as clear as daylight but is yet to become apparent to the inward-looking American investment community.

4.ANDREW MAGUIRE LIVE FROM THE VAULT 272 and 271

Ted Oakley//272

MUST VIEW…

5. COMMODITY REPORT/GOLD

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 7.35 PTS OR 0.18%

HANG SENG CLOSED DOWN 146.73 PTS OR 0.37%

Nikkei CLOSED DOWN 8-8/59 PTS OR 1.34%

//Australia’s all ordinaries CLOSED DOWN .56%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.8047

/ OFFSHORE CLOSED DOWN AT 6.8059 Oil DOWN TO 102.79 dollars per barrel for WTI and BRENT DOWN TO 109.23 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN (6.8047) OFFSHORE YUAN TRADING DOWN TO 6.8059 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.8047

OFFSHORE YUAN: DOWN TO 6.8057

1.HANG SANG CLOSED DOWN 146.73 PTS OR 0.53%

2. Nikkei closed DOWN 808.59 PTS OR 1.34%

WEST TEXAS INTERMEDIATE OIL DOWN TO 102.78

BRENT; 109.23

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 99.93/// EURO FALLS TO 1.1593 DOWN 14 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +2.763 DOWN 3 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.03… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 4.062 DOWN 9 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN( 6.8047 AND OFFSHORE: UP AT 6.8059

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +3.1631// Italian 10 Yr bond yield DOWN to 3.920// SPAIN 10 YR BOND YIELD DOWN TO 3.592%

3i Greek 10 year bond yield DOWN TO 3.837%

3j Gold at $4485.85 //Silver at: 75/37 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 6/ 100 roubles/71.26

3m oil (WTI) into the 102 dollar handle for WTI and 109 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.03 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.762% DOWN 3 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 4.062 DOWN 9 PTS..: USA/SF this 0.7902 as the Swiss Franc . Euro vs SF: 0.9163

USA 10 YR BOND YIELD: 4.648 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 5.168 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.095 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.60 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 5.0490 DOWN 8 PTS

30 YR UK BOND YIELD: 5.725 DOWN 7 BASIS PTS

10 YR CANADA BOND YIELD: 3.704 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.351 UP 0 BASIS PTS.

1a New York Opening report

Futures Rise Ahead Of Critical Nvidia Earnings As Oil, Bond Yields Drop

Wednesday, May 20, 2026 – 07:51 AM

US equity futures are higher led by tech as the selloff in bonds eased and traders awaited earnings from Nvidia after the close. As of 7:30am ET, S&P futures are up 0.3% while Nasdaq futs rose 0.7% showing optimism heading into the release and overlooking weakness in tech during APAC trade. In premarket trading, NVDA is up 1.8% in premarket trading, as semis see a strong bid with Mag7 names almost all higher. Cyclicals ex-Energy are rallying led by Industrials with Defensives lagging and Staples down. European stocks have edged higher alongside a pullback in energy prices, which saw Brent briefly slip onto a $108/bbl handle. Today is all about NVDA but Fed Minutes this afternoon may provide color on the dissenters from the previous Fed Day. Bond yields in the US and Europe retreated from multiyear highs as traders pared back aggressive bets on interest-rate hikes this year. US yields are 1-3bp lower across the curve, the 10Y dropping to 4.64% from yesterday’s high of 4.69%, as the USD sees a mild bid. Brent fell 1.8% toward $109 a barrel with the broader energy complex drops as JPM flags 6.6mm bbls of oil crossing the SoH over the last 24 hours; Precious Metals are also bid with Ags seeing weakness. Tomorrow’s macro releases include Flash PMIs and jobless data.

In premarket trading, Nvidia is outperforming fellow Magnificent Seven stocks, rising 1.8%, ahead of its much-anticipated first-quarter results report after the market closes. Fellow chip stocks are also gaining (Tesla +1%, Alphabet +0.3%, Amazon +0.2%, Meta Platforms +0.2%, Apple -0.2%, Microsoft -0.4%)

- 8×8 (EGHT) jumps 17% after the software company reported fourth-quarter results that beat expectations.

- Cava Group Inc. (CAVA) is up 7.1%. The company raised its annual sales outlook after diners flocked to its restaurants in the first quarter, defying the crunch in consumer budgets that has weighed on the industry.

- Keysight Technologies (KEYS) is up 2.3% after the measurement instruments company reported second-quarter results that beat expectations and gave a third-quarter forecast that is above the analyst consensus.

- Toll Brothers (TOL) rises 2.3% after the luxury homebuilder reported second-quarter profit that beat analysts’ estimates and raised its full-year guidance.

In other corporate news, Goldman Sachs is said to have the leading role on the cover of SpaceX’s IPO, with Morgan Stanley also listed as a lead bank. SpaceX expects to proceed with its acquisition of Cursor 30 days after the company begins trading publicly, and if the deal doesn’t go through, SpaceX would pay Cursor a $10 billion breakup fee in cash, BBG reported. Early AI tools are boosting productivity as much as 30%, said JPMorgan, while Standard Chartered’s CEO has sought to reassure staff after a backlash to his remarks on using artificial intelligence to replace “lower-value human capital.” Softbank’s $60 billion bet on OpenAI, and growing unease over Masayoshi Son’s devotion to Sam Altman is today’s The Big Take.

Futures are higher in early trading as investors digest a backdrop of surging rates volatility, heavily crowded semis exposure and euphoric – and outright manic bubble in the case of Korea – positioning, while some of the most aggressive AI momentum trades globally show signs of strain, even as stocks broadly ignore the historic rout taking place in the bond market, sending 30Y yields to 19 year highs.

A potential strike at Samsung and the words of Jensen Huang are two catalysts in the next 24 hours to keep traders on edge.

The impending strike at Samsung could add to concerns around supply being able to meet burgeoning demand for AI memory chips in the face of already surging memory prices, at a time inflation is coming for the overcrowded AI trade.

Nvidia will give a much-anticipated update on the state of the AI economy when it reports after the close. While sales are estimated to have grown 80%, investors will be more focused on what Nvidia has to say about ramping up production and fending off competitors.

Options traders are pricing an implied move of about 5.5% for Nvidia shares in either direction following the results. With the report coming at a time when the roaring rally in chipmakers is coming off the boil, well-received earnings could give the sector fresh momentum and help drive global indexes even higher into superbubble territory.

“The semiconductor rally has stalled, but really is just in a holding pattern until Nvidia reports,” said Joachim Klement, head of strategy at Panmure Liberum. “Nvidia can, for now, keep its beat-and-raise machine going, which will reignite the rally in semiconductors.”

Today we also get the minutes of the April 28–29 FOMC meeting which should show that support for removing the easing bias from the statement extended beyond the three dissenters. The minutes should reinforce the market view that the easing cycle is on an extended hold, according to Bloomberg Economics. Fed’s Paulson said she favored holding interest rates steady and conditioned lower borrowing costs on making sustained progress on inflation.

President Donald Trump threatened to resume strikes on Iran in the coming days as part of the push for a deal to end the war, after he said he had just called off a US attack. Alexandre Drabowicz, chief investment officer at Indosuez Wealth Management, said he wouldn’t be surprised if Trump’s next steps take into account where interest rates are headed, given the current yield levels. “We’re in the thick of the danger zone,” he said.

“Stagflation risk has gone up significantly,” said Justin Onuekwusi, chief investment officer at St. James’s Place. “When we’re talking about increased inflation and falling growth, in that environment, most asset classes will struggle, including bonds.”

In politics, the Republican-led US Senate signaled mounting opposition to continuing the Iran war in a procedural vote Tuesday, reflecting deepening political unease over a conflict that is taking a financial toll on Americans. Trump signed an executive order directing regulators to issue guidance on banking services to undocumented migrants, in a move that could tighten access to the financial system.

Retail is in focus before the market opens, with Target and TJX set to report. Visits to Target stores during the first quarter were up 5.1% from the year prior, marking the chain’s first positive visit growth in more than a year, according to data from Placer.ai. The firm also notes traffic in April rose 5.5% from the previous year.

European stocks edge higher alongside a pullback in energy prices, which saw Brent briefly slip onto a $108/bbl handle. Stock market operator Euronext is among the biggest gainers, while credit checking firm Experian fell on its latest earnings. Here are the biggest movers Wednesday:

- Euronext shares gain 7.1%, most since July 2023, after the stock market operator reported what analysts say are strong 1Q earnings, driven by better revenues and costs, with the equity markets division as the main standout

- CSG shares rise as much as 12%, the most since January, after the defense company reported results analysts called strong, saying the market should be relieved after the recent selloff

- Marks & Spencer shares rise as much as 5.5% after the retailer reported a milder drop in adjusted pretax profit than anticipated during FY26, having grappled with a costly cyberattack during the year

- RS Group shares rise as much as 10%, the most since November 2024, after the distributor of electrical and industrial products announced a £100m share buyback and pointed to improving momentum across its major markets

- Playtech shares gain as much as 5.1% after the gaming software maker said it delivered an “excellent trading performance” over the first four months of the year, according to a statement ahead of its annual general meeting

- Ypsomed shares jump as much as 14%, the most since April 2025, after the Swiss maker of injection systems reported better-than-expected financial results and provided guidance that pleased investors

- Severn Trent shares rise as much as 4.9% after the UK water company reported earnings ahead of expectations in FY26 and upgraded its outlook for FY28; peer United Utilities is up 1.3%%, while smaller rival Pennon is trading 1% higher

- Experian shares drop for the first day in five, falling as much as 6%, as the credit checking company’s full-year guidance proves slightly lower than analysts expected

- Orkla falls as much as 8.9% after the Norwegian consumer goods group reported earnings which fell short of expectations. DNB Carnegie sees a “mixed” report, flagging an adjusted Ebit miss and increased margin pressure

- Rusta falls as much as 8.6%, the most since September, after SEB cut its recommendation on the Swedish retailer to hold from buy, saying the stock’s valuation discount has disappeared after a strong rally

- B&M falls as much as 3.9% as Goodbody cut its rating on the European budget retailer to hold from buy. The broker sees tepid earnings as the UK macroeconomic climate deteriorates and poor weather weighs on sales

Earlier in the session, Asian equities fell for a fourth straight session, heading for their longest losing streak in nearly two months as chip stocks dropped and bonds sold off on inflation concerns. The MSCI Asia Pacific Index declined as much as 1.3%, with Samsung and TSMC among the the biggest drags. Samsung shares slumped after its labor union said it will go on strike Thursday, a development that pushed the Korean benchmark Kospi lower. Most markets in the region were down, led by Kospi’s 3% decline. Concerns that the US-Iran war may stretch on have lifted global inflation expectations, pushing yields higher. The higher cost of capital may hinder the fast expansion of Asian stocks that have ridden artificial intelligence tailwinds to grow earnings. Stocks also fell in Japan, China, Hong Kong and Australia.

In FX, the greenback has given back some ground after dollar gains pushed EUR/USD to its lowest level since April 7. JPY remains rangebound amid the threat of intervention, with Yen fundamentals still bearish (Supplementary Budget/Energy). Demand at the overnight JGB auction was weak and saw some pressure in JGBs but no real follow-through to the FX space. USD/JPY is unchanged and testing 159.00 to the downside at the time of writing. GBP is a little weaker after soft April inflation data trimmed bets on BoE hikes. GBP/USD moved lower by c. 15pips post-data, now above pre-release levels as it attempts to regain a 1.34 handle. EUR/GBP moved higher by 10pips post-data, a move which swiftly pared amid resistance at 0.8670 and recent energy-related moves. (See 08:40 BST headline for more). EUR is also a touch weaker and seemingly moving lower in tandem with USD strength. EUR/USD -0.1%, the pair delved as low as 1.1583 before attempting to return back to a 1.16 handle, where it has traded throughout the week so far.

US Treasuries yields continue to test levels reminiscent of unnerving times. A sustained selloff in Asia and Europe on Tuesday continued through the US morning until a small relief bid emerged in the afternoon. Still, 30y yield ended the day hovering around 5.17% – the highest level since 2007. 10y yields have pushed past the 4.50% mark that has typically served as a reentry point from oversold territory and are inching closer to 4.75%. Global inflationary concerns, a Middle East crisis and a lack of conviction has led to a perfect storm of stop outs and compounding bearish momentum. The lack of thematic dip buying is likely summed up by sentiment that things look cheap but could look even cheaper. 2s5s10s – something the desk highlighted a few sessions ago – has dramatically cheapened 10bp over the past few days. Wednesday’s 20y auction will be a key gauge on the market’s appetite for long-end duration at these levels. The elevated rate environment is bad news for risk assets in a world where debt-fueled capex is high, and this US administration has used tools to indirectly affect dip buying in duration before

This morning treasuries hold gains amid a bigger curve-steepening rally in gilts after UK inflation gauge slowed more than economists estimated. US yields are 2bp-3bp lower on the day, with 5s30s curve steeper by more than 1bp; 10-year is down 2.7bp near session low 4.64%, with UK 10-year lower by more than 8bp, Germany’s by more than 3bp. UK front-end yields remain around 10bp richer on the day heading into the US session, which includes a 20-year bond auction poised to draw the highest yield since October 2023. July WTI crude oil futures, down around 2.5%, also support Treasuries. UK yields are 7bp to 10bp lower on the day with 2s10s and 5s30s curves steeper by about 1.5bp; following the UK inflation data, swaps-implied chance of a BOE rate hike in June ebbed to less than 20%, compared with about 50% at one point last week

Treasury auctions resume with $16 billion 20-year new issue at 1pm New York time. WI 20-year yield near 5.17% is ~29bp cheaper than last month’s auction; a $19 billion 10-year TIPS reopening is ahead Thursday. IG dollar issuance slate includes a couple of offerings. Twelve borrowers raised almost $15 billion on Tuesday with issuers paying, on average, 4.8bp in new issue concessions on deals that were 3.9 times covered

Economic data slate empty for the session. Fed speaker slate includes Barr (9:15am), and minutes of FOMC’s April 28-29 meeting are slated for 2pm release

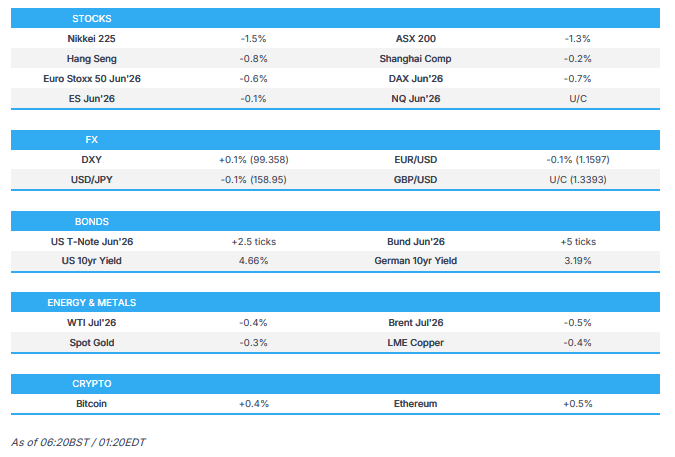

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.5%

- Russell 2000 mini +0.2%

- Stoxx Europe 600 +0.2%

- DAX +0.2%

- CAC 40 +0.3%

- 10-year Treasury yield -3 basis points at 4.64%

- VIX little changed at 18.03

- Bloomberg Dollar Index little changed at 1204.72

- euro -0.1% at $1.1591

- WTI crude -1.5% at $102.59/barrel

Top overnight news

- The Trump administration is planning to tell NATO allies this week that it will shrink the pool of military capabilities that the U.S. would have available to assist the alliance’s European nations in a major crisis, three sources familiar with the matter said. BBG

- Two giant Chinese tankers laden with around 4 million barrels of oil exited the strait on Wednesday, the latest signal that Iran is willing to ease its blockade for countries it considers friendly. Iran had announced last week, while Trump was in Beijing for a summit, that it had reached an agreement to ease rules for Chinese ships. RTRS

- India is preparing to send vessels through the Strait of Hormuz to load energy cargoes from Middle East suppliers, the first time since the Iran conflict began. BBG

- Xi Jinping called for “a comprehensive ceasefire” in the Middle East as he opened talks with Vladimir Putin in Beijing. BBG

- US President Trump signed a fintech Executive Order to protect the US financial system from illicit activity, while it was reported that the White House plans to release an Executive Order on cybersecurity and AI safety as soon as this week, which seeks early government access to advanced models.

- Indonesia’s central bank snapped a long-running pause as it delivered its first rate hike in over two years to guard against inflation and steady the rupiah. Bank Indonesia on Wednesday raised its benchmark seven-day reverse repo rate by 50 basis points to 5.25%, coming off the sidelines after holding steady since it eased policy settings in September last year. The move surprised markets. WSJ

- British inflation cooled by more than expected in April but the slowdown did little to mask a tough outlook for households, with global costs from the Iran war set to hit them harder later this year. Consumer prices rose by an annual 2.8%, down from March’s annual inflation rate of 3.3%, official data showed, helped by smaller increases in household energy and other regulated utility bills than in April 2025, and by measures to lower energy bills introduced by finance minister Rachel Reeves. RTRS

- The EU finalized the text of its long-delayed US trade deal after months of negotiations, clearing a major hurdle to ratifying the pact before President Donald Trump’s threatened deadline to impose higher tariffs. The EU agreed to scrap tariffs on US industrial goods in exchange for a 15% cap on EU export levies. BBG

- Japan’s 20-year bond auction drew strong demand, helping calm a recent selloff in longer-dated JGBs. PM Sanae Takaichi said an extra budget would avoid large bond sales. BBG

- China banned Nvidia’s US export-friendly RTX 5090D V2 gaming chip last Friday. FT

A more detailed look at global markets courtesy of Newsquawk

APAC stocks declined following the weak handover from the US, with sentiment dampened amid headwinds from a higher yield environment and the uncertain geopolitical backdrop. ASX 200 retreated with the declines led by underperformance in the mining and materials sectors, while a lack of data and firmer yields contributed to the uninspired mood. Nikkei 225 fell beneath the 60,000 level with notable pressure in machine tool and electrical equipment manufacturers, while recent comments from Japan’s Finance Minister, and current FX levels were seen to stoke intervention risks. Hang Seng and Shanghai Comp conformed to the downbeat sentiment amid bond and inflation woes, with the declines in Hong Kong led by mining, solar and property stocks, while there was a lack of surprises from the PBoC announcement to maintain the benchmark Loan Prime Rates for the 12th consecutive month.

Top Asian News

- Chinese President Xi met Russian President Putin in Beijing and said that relations have reached their current level due to deepened political mutual trust and strategic cooperation, while Putin said ties between Russia and China support broader international stability. Furthermore, China and Russia plan to deepen continuous strategic coordination, and Putin invited Chinese President Xi Jinping to travel to Russia next year, while Xi told Putin that the world faces the risk of regressing into a “law of the jungle.”

- Japanese PM Takaichi said she is not currently at a stage where she can comment on the possible size of the extra budget. She further said that plans to protect people’s lives and businesses while curbing issuance of deficit-financing bonds as much as possible.

European bourses (STOXX 600 +0.2%) were initially incrementally lower, but now display a more positive picture. On the trade front, the EU finalised the text of its US trade deal, in which the bloc would remove levies on US industrial goods in exchange for a 15% tariff ceiling on EU exports. Next steps are for the Parliament and EU countries to vote to ratify the text. The AEX (+0.4%) hovers around the U/C mark, with chip majors ASML (+3.2%) and BESI (+2.3%) supporting the index, while the FTSE 100 (-0.1%) sees little support following the cooler-than-expected UK inflation print. European sectors trade mixed. Basic Resources tops the sector pile as it manages to claw back some of Tuesday’s losses. Energy and Technology round out the top three sectors. To the downside, Media, Retail and Food, Beverages & Tobacco underperforms. UK supermarkets (Tesco -1.6%, Sainsburys -1.4%) have came under pressure after reports by the FT stated that the UK Treasury is pushing large supermarkets to introduce voluntary price caps on key groceries in return for lifting some regulations.

Top European News

- UK Inflation Rate MoM (Apr) M/M 0.7% vs. Exp. 0.9% (Prev. 0.7%, Low. 0.8%, High. 1.3%).

- UK Inflation Rate YoY (Apr) Y/Y 2.8% vs. Exp. 3% (Prev. 3.3%, Low. 2.8%, High. 3.4%); Services 3.2% (prev. 4.5%). ONS: “There was a notable fall in annual inflation led by lower electricity and gas prices. This was due to the government’s energy bill support package reducing variable and fixed tariffs, along with lower global wholesale energy prices before the conflict in the Middle East, which fed through to the reduction in the Ofgem cap.”

- UK Core Inflation Rate MoM (Apr) M/M 0.7% (Prev. 0.4%).

- UK Core Inflation Rate YoY (Apr) Y/Y 2.5% vs. Exp. 2.6% (Prev. 3.1%, Low. 2.5%, High. 3.2%).

FX

- USD continues driving higher amid the continued unconstructive oil/yield environment with oil either side of USD 110/bbl and yields still elevated, albeit lower on the day. US/Iran news overnight was light, and nothing pertinent this morning, but the running commentary remains hostile. The Buck will remain attentive to Gulf developments, alongside expected hawkish FOMC minutes this evening, and NVIDIA earnings after the US close. DXY +0.1%, is now above all significant DMAs, with the 50DMA closest at 99.00.

- JPY remains rangebound amid the threat of intervention, with Yen fundamentals still bearish (Supplementary Budget/Energy). Demand at the overnight JGB auction was weak and saw some pressure in JGBs but no real follow-through to the FX space. USD/JPY is unchanged and testing 159.00 to the downside at the time of writing.