GOLD: NUMBER OF NOTICES FILED FOR JUNE/2026: 541 CONTRACTs NOTICES FOR 54,100 OZ or 1.6822 TONNES

total notices so far: 25,035 contracts FOR 2,503,500 OZ OR 77.869 TONNES

SILVER NOTICES: 70 NOTICE(S) FILED FOR 0.350 MILLION OZ /

total number of notices filed so far this month : 1943 CONTRACTS (NOTICES) for 9.565 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ (CME CORRECTED) TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 160,000 OZ//NEW STANDING ADVANCES TO 11.115 MILLION OZ//

SUMMARY OF OUR JUNE 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE..4.750 MILION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 0.160 MILLION OZ//NEW STANDING ADVANCES TO: 11.115 MILLION OZ

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT 0.1213 TONNES OF A QUEUE JUMP/NEW STANDING ADVANCES TO 80.936 TONNES

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.1213 TONNES//NEW STANDING ADVANCES TO 80.936 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 21.7451 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE 1884 CONTRACTS TO AN OI OF 101,915.

EFP ISSUANCE 450 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 440 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1884 CONTRACTS AND ADD TO THE 450 E.FP. ISSUED

WE OBTAIN A MEGA HUGE GAIN OF 2334 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WDESPITE OUR LOSS OF $0.52

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 11.670 MILLION PAPER OZ

OCCURRED DESPITE OUR LOSS IN PRICE.OF $0.52

2.ASIAN AFFAIRS JUNE 2 /2025

SHANGHAI CLOSED UP 17.36 PTS OR 0.43%

HANG SENG CLOSED UP 616.32 PTS OR 2.43%

Nikkei CLOSED UP 17.36 PTS OR 0.43%

//Australia’s all ordinaries CLOSED UP 0.75%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7611

/ OFFSHORE CLOSED UP AT 6.7627 Oil DOWN TO 90.81 dollars per barrel for WTI and BRENT DOWN TO 93.36 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN// WITH YUAN TRADING UP (6.7611) OFFSHORE YUAN TRADING UP TO 6.7627 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL 240 CONTRACTS TO 326,341 AND NOW IT BECOMES THE ALL TIME LOW OF 326,341 OI SURPASSING THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,341 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD HUGE T.A.S. LIQUIDATION EARLY DURING FRIDAY’S OP =EX TRADING (OTC/LONDON OPTIONS EXPIRY TRADING). IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MAY CONTRACT MONTH!!

THE STRONG SIZED GAIN ON OUR TWO EXCHANGES OCCURRED DESPITE OUR LOSS IN PRICE IN GOLD (DOWN $79.30).

WE THUS HAD A FAIR SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 2015 CONTRACTS (OR 6.267 TONNES) DESPITE OUR LOSS IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 2255 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO SO FAR

DETAILS ON OUR NEW JUNE COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR GAIN ON OUR TWO EXCHANGES OF 2015 CONTRACTS DESPITE OUR LOSS IN PRICE ($79.30). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A SMALL SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 834 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 106+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO. WE WILL KNOW IN JUNE WHETHER THEY COVERED ANY OF THEIR SHORTFALL.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES (CME CORRECTED) TO WHICH WE ADD OUR NEXT 0.1213 TONNES OF A QUEUE JUMP//NEW STANDING ADVANCES TO 80.936 TONNES//

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JUNE,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $79.30)

WE HAD HUGE T.A.S. SPREADER LIQUIDATION MONDAY // COMEX SESSION// WITH OUR LOSS IN PRICE , OUR LONG SPECULATORS STILL REMAIN RELENTLESS POURING INTO THE COMEX

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $79.30

WE HAD A STRONG 676 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 2015 CONTRACTS OR 201500 OZ OR 6.267 TONNES

MAY DELIVERY MONTH

JUNE 2

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 3 i) Out of Brinks 64.302 oz 2 kilobars ii) Out of Loomis: 2025.513 oz (63 kilobars) iii) Out of Manfra: 96.263 oz (3 kilobars) total withdrawal: 2196.268 oz (68 kilobars) or .068 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRY i) Into Manfra: 32,151.000 oz 1000 kilobars total deposit: 32,151.000 oz 1000 kilobars or 1 tonnne xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 541 CONTRACTS OR 54,100 OZ 1.6827 TONNES OF GOLD |

| No of oz to be served (notices) | 986 Contracts 98,600 OZ 3.066TONNES |

| Total monthly oz gold served (contracts) so far this month | 25,035 notices 2,503,500 oz 77.869 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

ENTRY: 1

i) Into Manfra: 32,151.000 oz

1000 kilobars

total deposit: 32,151.000 oz

1000 kilobars or 1 tonnne

xxxxxxxxxxxxxxxxxx

comex withdrawal

ENTRIES; 3

3 CUSTOMER WITHDRAWAL ENTRIES

i) Out of Brinks 64.302 oz

2 kilobars

ii) Out of Loomis: 2025.513 oz

(63 kilobars)

iii) Out of Manfra: 96.263 oz

(3 kilobars)

total withdrawal: 2196.268 oz

(68 kilobars)

or

.068 tonnes

adjustments: 5 all dealer to customer account

Brinks: 62,350.867 oz dealer to customer account

HSBC 82,852.140 oz dealer to customer account

JPMorgan: 32,000.709 oz dealer to customer account

Loomis: 4726.177 oz

Manfra 02,757.240 oz

net gold leaving the dealer accounts: 205,667.155 oz (6.39 tonnes)

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JUNE OI STANDS AT 1527 CONTRACTS HAVING A LOSS OF 835 CONTRACTS.

WE HAD 874 CONTRACTS SERVED ON MONDAY, SO WE GAINED 39 CONTRACTS FOR 3900 OZ. (0.1273 TONNES).

JULY LOST 33 CONTRACTS DOWN TO 3228 CONTRACTS.

AUGUST LOST 127 CONTRACTS UP TO AN OI OF 262,673

.

We had 541 contracts filed for today representing 54,100oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 181 notices issued from their client or customer account. The total of all issuance by all participants equate to 541 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 73 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (25,035) to which we add the difference between the open interest for the front month of JUNE 1527 CONTRACTS) minus the number of notices served upon today 541 x 100 oz per contract) equals 2,602,100 OZ OR (80.936Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (25,035) to which we add the difference between the open interest for the front month of JUNE( 1527 CONTRACTS) minus the number of notices served upon today 541 x 100 oz per contract) equals 2,602,100 OZ OR (80.936 Tonnes of gold)

new total of gold standing in JUNE becomes 80.936 TONNES//

TOTAL COMEX GOLD STANDING FOR JUNE 80.936 TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS ACTIVE DELIVERY MONTH OF JUNE.

confirmed volume MONDAY confirmed 128,603// extremely poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,867,352.114 oz 58.08 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,867,352.114 tonnes oz 59.74 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 28,312m833.447oz

TOTAL REGISTERED GOLD 15,280,232.454 tonnes (475.279 tonnes)

TOTAL OF ALL ELIGIBLE GOLD 13,032,601.013 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,412,880 oz ((REG GOLD- PLEDGED GOLD)=

417.196 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JUNE DELIVERY MONTH

JUNE 2

JUNE DELIVERY MONTH

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | ONE ENTRY i) Out of Asahi: 405,665.800 oz total withdrawal: 405,665.800 oz |

| Deposits to the Dealer Inventory | 1 entries i) Into the dealer STONEX: 14,933.990 oz total deposit 14,993.990 oz |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT DEPOSIT ENTRIES/CUSTOMER ACCOUNT 3 entries i)Into Asahi 561,738.800 OZ ii) Into Loomis 600,257,130 oz iii) Into Manfra: 300,369.575 oz total deposit 1,462,365.505 oz |

| No of oz served today (contracts) | 70 CONTRACT(S) (0.350 MILLION OZ OZ |

| No of oz to be served (notices) | 310 Contract (1.555 MILLIONoz) |

| Total monthly oz silver served (contracts) | 2913 contracts 9.565 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

i) Into the dealer STONEX: 14,933.990 oz

total deposit 14,993.990 oz

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

3 ENTRIES

i)Into Asahi 561,738.800 OZ

ii) Into Loomis 600,257,130 oz

iii) Into Manfra: 300,369.575 oz

total deposit 1,462,365.505 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

1 ENTRIES

ONE ENTRY

i) Out of Asahi: 405,665.800 oz

total withdrawal: 405,665.800 o

adjustments 1 dealer to customer

i) Asahi: 405,665.800 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 84.586 MILLION OZ//.TOTAL REG + ELIGIBLE. 318.678 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF JUNE /2026 OI: 380 OPEN INTEREST CONTRACTS FOR A LOSS OF 118 CONTRACTS.

WE HAD 150 NOTICES SERVED ON MONDAY SO WE GAINED 32 CONTRACTS OR AN ADDITIONAL 160,000 OZ WILL STAND AS A QUEUE JUMP AT THE SILVER COMEX.

JULY SAW A LOSS OF 288 CONTRACTS DOWN TO 70,742 CONTRACTS.

AUGUST SAW A GAIN OF 50 CONTRACTS UP TO 735…

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 70 or 0.350 MILLION oz

CONFIRMED volume MONDAY; 46,471// poor volume

XXX

AND NOW JUNE. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 1913 X5,000 oz = 9.565 MILLION oz

to which we add the difference between the open interest for the front month of JUNE( 380) AND the number of notices served upon today (70 )x (5000 oz)

Thus the standings for silver for the JUNE 2026 contract month: (1913 )Notices served so far) x 5000 oz + OI for the front month of JUNE (380) minus number of notices served upon today (70)x 5000 oz equals silver standing for the JUNE..contract month equating to 11.115 MILLION OZ.+

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 84.586 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/318.678 million: 43.91

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JUNE 2 /2026/WITH GOLD UP $7.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.712 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.856 TONNES

JUNE 1 /2026/WITH GOLD DOWN $79.30 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 29 /2026/WITH GOLD UP $59.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

GLD INVENTORY: 1028,856 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

CLOSING INVENTORY 484.855 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD..

3. CHRIS POWELL AND HIS GATA DISPATCHES

4.ANDREW MAGUIRE LIVE FROM THE VAULT 274 and 273

MUST VIEWl ANDREW’S NEWEST PODCAST

5. COMMODITY REPORT//RICE

The Cost Of The Grain That Feeds Half The World Just Posted Biggest Monthly Surge Since 2008

Tuesday, Jun 02, 2026 – 04:15 AM

Asian rice prices logged their biggest monthly gain in nearly two decades in May, as a Gulf energy shock collides with an expected El Niño event later this year. The spike adds to the mounting risks of a broader food price shock that could emerge as soon as six months from now.

Any time rice prices spike, it is a major concern because the grain feeds more than half the world’s population, estimated at 3.5 to 4 billion people.

Thailand white rice, a regional Asian benchmark, surged 20% in May, the largest monthly increase in data going back to 2008, according to Bloomberg. Chicago rice futures rose 15% last month.

Seasonality:

BMI analyst Bin Hui Ong warned that an expected El Niño event later this year will unleash adverse weather conditions across major rice-growing belts in Asia, including hotter, drier conditions. She noted this adds further upside to rice prices in the months ahead.

It is not just the threat of a severe El Niño event on analysts’ radars. There are also continued elevated diesel and fertilizer costs tied to disruptions around the Strait of Hormuz. This will further weigh on rice production yields across import-reliant Asia.

Rice farming is already highly fertilizer-intensive, while irrigation systems often depend on diesel-powered pumps.

In Vietnam’s Vinh Long province, a farmer told Bloomberg that he plans to skip one of his usual three annual crops due to rising input costs and extreme heat.

Fertilizer prices in Thailand, Cambodia, and the Philippines have soared by nearly 50% since late February, according to the International Rice Research Institute.

The Philippines has warned that a strong El Niño could cut rice production by up to 700,000 tons, or 3.5% of its annual production target.

Already, the United Nations Food and Agriculture Organization’s FAO Food Price Index, which tracks monthly changes in the international prices of a basket of globally traded food commodities, is trending upward and risks a further leg higher.

Alexandra Prokopenko, a fellow at the Carnegie Russia Eurasia Center, warned in mid-March that disruptions to the Strait of Hormuz would spark shortages of energy and fertilizers, translating into higher food prices in “six to nine months from now.”

Related:

- We Are 6 Months From Global Food Shortages Because Farmers Are Facing A Quadruple Whammy Crisis

- Everyone Talks About The Cost Of Gasoline… Soon Everyone Will Be Talking About The Cost Of Food

Last month, ZeroHedge Debates held a roundtable to ask: How bad will the food inflation mess get?

View here:

Visual Capitalist’s Dorothy Neufeld outlined where food inflation is expected to hit the hardest, on a country-by-country level, this year (see report)

END

COMMODITY: COPPER:

HSBC Warns Of Commodity “Super-Squeeze” As Goldman Hikes Copper Forecasts

Tuesday, Jun 02, 2026 – 02:45 PM

Copper is inching closer to its mid-May all-time high of $14,153 a ton on the London Metal Exchange, trading around $13,832 on Tuesday morning, as Goldman raised its year-end price targets and HSBC warned that commodities face a “super-squeeze” with the Hormuz maritime chokepoint still largely shuttered in early June.

Let’s begin with HSBC analysts, who wrote in a note to clients that “metal prices are generally in an upswing, driven by supply disruptions for some commodities due to the Middle East conflict and strong structural demand.”

They warned that commodities were facing a “super-squeeze” with the Strait of Hormuz still blocked.

HSBC’s note comes after Goldman analysts led by Aurelia Waltham told clients Monday that the core issue with copper markets right now is supply:

- Year-to-date data does suggest that supply recovery from previous disruption events has trailed our expectations. Accordingly, we lower our 2026 global mine supply forecast by 350kt, equivalent to ~1.5% of global mine supply, including ~200kt less from Grasberg (Indonesia) and Kamoa-Kakula (DRC) combined, with neither returning to full capacity until 2028.

At the same time, she said stronger-than-expected US copper imports in the first half of 2026 are tightening the ex-US market:

- Furthermore, US copper imports in H1 2026 have exceeded our previous forecast, tightening the ex-US balance. As a result, we now expect US inventory to build by 900kt in 2026 (vs. 550kt previously), even as our base case remains that no copper tariff will be announced this year.

The combination of soft mine supply, US stockpiling, tariff uncertainty, and long-term demand tied to AI buildout and grid-upgrade themes prompted Waltham to upgrade her end-of-year 2026 and 2027 copper price forecasts:

- We raise our end-2026/average 2027 LME copper forecasts to $13,735/$13,800 from $12,465/$12,150 previously (vs. forwards at $13,630/$13,610).

She mapped out three price scenarios for copper:

1. Strait of Hormuz Remains Closed for Longer: While we would expect limited impact on the global copper balance as the demand hit from lower economic growth is largely offset by lower copper supply due to sulfur shortages, a substantial pullback in global risk appetite could push the LME price down to its fundamental support level at ~$12,600 in H2 2026, before resuming an upward trend.

2. US Copper Tariff Announced for January 2027: If a US copper tariff is announced prospectively in June 2026, to start in January 2027, we would expect US copper imports to accelerate in H2 2026 (vs. our base case of a slowdown in imports), tightening the ex-US balance and raising prices to over $14,000 in H2 2026. However, we would expect prices to retreat in 2027 as imports stop once the tariff is imposed.

3. Announcement of No Copper Tariff: A definitive decision against the tariff would reduce the size of our ex-US deficit forecast in 2026 and push the ex-US market back into surplus in 2027 as imports fall to a negligible level. In this scenario, we would expect the price to fall to an average of $12,800/t in 2027.

Mapped out here:

Professional subscribers can read the full copper note here at our new Marketdesk.ai portal

With Hormuz still all but shuttered and only a 22% chance that the critical waterway reopens by the end of June, according to a Polymarket bet, it would take many months, if not quarters, to normalize shipping flows. This indicates that the commodities cycle will likely remain bullish into early summer.

END

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 17.36 PTS OR 0.43%

HANG SENG CLOSED UP 616.32 PTS OR 2.43%

Nikkei CLOSED UP 17.36 PTS OR 0.43%

//Australia’s all ordinaries CLOSED UP 0.75%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7611

/ OFFSHORE CLOSED UP AT 6.7627 Oil DOWN TO 90.81 dollars per barrel for WTI and BRENT DOWN TO 93.36 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN// WITH YUAN TRADING UP (6.7611) OFFSHORE YUAN TRADING UP TO 6.7627 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 6.7611

OFFSHORE YUAN: UP TO 6.7627

1.HANG SANG CLOSED UP 616.32 PTS OR 2.43%

2. Nikkei closed UP 17.36 PTS OR 0.43%

WEST TEXAS INTERMEDIATE OIL DOWN TO 90.81

BRENT; 93.36

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 99.05/// EURO RISES TO 1.1647 UP 12 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +2.570 DOWN11 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.69… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.843 DOWN 7 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP( 6.7611 AND OFFSHORE: UP AT 6.7627

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.9509// Italian 10 Yr bond yield DOWN to 3.670// SPAIN 10 YR BOND YIELD DOWN TO 3.363%

3i Greek 10 year bond yield DOWN TO 3.606%

3j Gold at $4536.00 //Silver at: 76.85 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 61/ 100 roubles/72.56

3m oil (WTI) into the 90 dollar handle for WTI and 93 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.69 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.570% DOWN 11 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.843 DOWN 7 PTS..: USA/SF this 0.7845 as the Swiss Franc . Euro vs SF: 0.9142

USA 10 YR BOND YIELD: 4.4311 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.9530 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.021 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.93 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.8480 DOWN 6 PTS

30 YR UK BOND YIELD: 5.540 DOWN 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.427 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.081 UP 3 BASIS PTS.

1a New York Opening report

US Futures Dip As Questions Mount Over Relentless Tech Rally, Lack Of Peace Progress

Tuesday, Jun 02, 2026 – 08:22 AM

Futs are weaker but well off their overnight lows as the US is set to lag its global peers; according to JPM investors will need to watch to see if there is a beginning of a larger rotation similar to Jan-Feb or perhaps a slight pullback following the US’s multi-week run. As of 8:00am ET, S&P futures are down 0.2% after the artificial-intelligence trade fueled the S&P 500’s longest winning streak in more than a year, with investors gauging prospects for an end to the war in the Middle East. Nasdaq futures down a fraction after clocking yet more records on Monday (driven by a surge in Software stocks), as traders digest a barrage of AI news overnight while a growing number of traders urge caution on market positioning and the technical setup. Im premarket trading the story remains Tech with HPE / MRVL both up ~25% and AVGO +6.5%, NVDA +1.8%. Industrials, Materials, and Utilities the standout sectors. Technology stocks led gains in Asia overnight and are doing the same in Europe where the Stoxx 600 climbs 0.7%. Overnight macro news was quiet, and broader risk sentiment has also been helped by Brent crude futures falling 1.6% to around $93 a barrel. Treasuries advance, pushing US 10-year yields down 2 bps to 4.44%.Oil / Energy prices are declining along with Ags as Metals are bid led by aluminum, copper, and precious. US economic data calendar includes April JOLTS job openings at 10am; Fed speaker slate includes Hammack (8:30am) and Goolsbee (11pm).

In premarket trading, Mag 7 are mixed with Alphabet down 2.7% after raising $80 billion through a package of equity offerings, including a deeply discounted private placement with Berkshire Hathaway and a $40bn ATM ovvering (Nvidia +1.5%, Meta +0.5%, Tesla flat, Apple -0.1%, Amazon -1.6%, Microsoft -2.6%)

- Shares of semiconductor companies are rallying as investors continue to rotate into the sector, seeing strong long-term growth potential related to artificial intelligence.

- Credo Technology Group (CRDO) falls 3% after the communications equipment company reported fourth-quarter results that beat expectations but weren’t strong enough to extend recent strength.

- Fulcrum Therapeutics (FULC) plunges 50% after the company discontinued its pociredir program for treatment of sickle cell disease and initiated a strategic review.

- Generac (GNRC) is up 9% after the company signed a global agreement to supply backup power generators to a leading hyperscale data center operator.

- Hewlett Packard Enterprise (HPE) rallies 25% after the company gave an outlook for annual sales that topped estimates, citing massive growth in AI-fueled demand for its servers and networking.

- Intuit (INTU) is down 5% after Goldman downgraded its rating on the maker of tax-preparation software to sell, the only negative rating among 32 analysts tracked by Bloomberg.

- Marvell Technology (MRVL) rises 22% after Nvidia’s Jensen Huang called the firm the “next trillion dollar company.”

- Microchip Technology (MCHP) gains 7% after the chipmaker says its data center solutions unit generated $302.7m in revenue in calendar year 2025, with about $500m expected for this year.

- NU Holdings (NU) falls 5% after the company announced a CFO transition, hiring Visa Inc.’s Rob Livingston to succeed Guilherme Lago.

- Praxis Precision Medicines (PRAX) falls 10% after the company said said vormatrigine did not meet its primary endpoint of percent change in monthly seizure frequency in the Phase 2/3 study.

In corporate news, Abivax shares plunged after cancer cases in a crucial clinical trial for an experimental bowel disease drug threw the French biotech’s future into question. Morgan Stanley risks being drawn into a probe over Bolloré’s disposal of an allegedly corrupt €5.7 billion ($6.6 billion) asset.

In AI developments, Arm may achieve its target of $15 billion in sales of its own chips earlier than anticipated, according to its CEO. SK Hynix plans to double its memory chip wafer capacity to help ease the memory chip crunch. HPE delivered a sizable beat and raise after-hours on the back of growing AI-fueled demand for its servers and networks. Alphabet unveiled an $80 billion equity raise to fund AI spending. And Tencent shares surged after a report it’s set to launch WeChat AI agent.

Traders are juggling unprecedented euphoria around the economic potential of AI and a war that has brought about a historic disruption in oil markets. Uncertainty about how close a deal may be means investors must consider that crude prices could retreat dramatically or scale to the highest levels in years. Downside risks are also growing as US large-cap positioning continued to grind higher last week, led by persistent new risk flows to both the S&P 500 and Nasdaq 100, according to Citigroup strategists. “How much more concentration can investors handle” is the question posed by Bloomberg strategists, noting that re-risking has been unusually quick and narrow.

“Triggers that could force an unwind include hawkish Fed repricing, structural rebalancing risks surrounding a prominent SpaceX IPO, or a momentum rotation out of over-allocated Tech into Cyclicals,” notes Andrew Kent at Kyte. At these current levels, the forward three-month return profile for the S&P 500 exhibits “a clear fat left tail, signaling a significantly higher probability of a >5% correction,” Kent adds.

In the latest example of the vast amounts of capital being pumped into AI infrastructure, Alphabet Inc. said it is raising $80 billion through equity offerings. The announcement came hours after Anthropic PBC filed draft paperwork for a possible blockbuster initial public offering.

“We may be approaching the point where optimism around the long-term positive impact of the AI buildout is going to crash against a wall of higher yields, higher inflation and lower growth,” said Stephan Kemper, chief investment strategist at BNP Paribas Wealth Management.

The next part of the tech trade to experience FOMO-driven chasing looks to be software stocks. In the past two sessions, theSoftware Sector ETF IGV has experienced the familiar “vol-up/spot-up” pattern as investors have bought call options to chase upside. That’s seen the call skew invert and the volatility spread vs S&P 500 reach extremes again.

With all attention constantly focused on AI rather than macro jobs data, the set-up into US non-farm payrolls data suggests a muted reaction to the reading on Friday. Through the lens of S&P 500 options, Barclays derivatives strategists note the current NFP-related implied move of 55 bps is significantly lower than the past one-year average realized move.

“US data, such as the ISM manufacturing print we just had, still keeps the Fed/inflation debate alive and limits the scope for a dovish rates repricing, especially if oil remains volatile,” said Alessandro Gabellone, fixed-income analyst at Bank Degroof Petercam. Tuesday’s figures on US job openings will likely add to the series of favorable labor-market data releases for April. High-frequency data suggest total openings inched up, particularly in the second half of the month, according to Bloomberg.

In other assets, commodities are in a “super-squeeze,” rather than “super-cycle” that will worsen if the Strait of Hormuz remains effectively shut, according to HSBC analysts. Bitcoin dipped below $70,000 as Strategy’s rare sale of the token continues to weigh on fragile sentiment.

In hedge fund news, famed short seller Andrew Left faces the possibility of 25 years behind bars after being found guilty of using disingenuous social media posts to manipulate stocks, in a landmark case that threatens to chill a broader trading strategy loathed by corporate executives.

Technology stocks led gains in Europe where the Stoxx 600 climbs 0.7%. Here are the biggest movers Tuesday:

- STMicro shares soared as much as 10% to the highest since 2000, after the chipmaker raised its data center revenue forecast for this year to about $1 billion

- Alzchem shares rose as much as 13% to a record high as the German maker of chemicals used for ammunition and muscle enhancement announces that defense firm CSG has been increasing its stake

- Hiab rallied as much as 7.9%, adding to its 5.6% advance on Monday, as analysts raise their price targets on the Finnish cargo-handling firm, lauding yesterday’s announcement that it’s buying refuse collection vehicle manufacturer Labrie Environmental Group

- Deutsche Post shares rose as much as 3.6% to their highest level in over four years after Kepler Cheuvreux upgraded its rating to buy. The broker cites strength in a key metric, weight transported

- Entain shares rose as much as 4.6%, extending Monday’s gains after MGM Resorts confirmed it received a takeover offer from People Inc

- IntegraFin Holdings gained as much as 6.1%, the most since mid-December, after Shore Capital upgrades the investment platform provider to buy from hold in a note, saying it’s “an excellent business, properly undervalued”

- Abivax shares plunged as much as 32%, the most in a decade, after the French biotech company reported cancer cases in a crucial clinical trial for its experimental inflammatory bowel disease drug

- British American Tobacco shares fell as much as 3.8%, extending a seven-day losing streak, as a trading update showed continued downtrading from consumers is hurting margins, overshadowing the firm’s maintained guidance and growth in new, smoke-free categories

- Avolta shares dropped as much as 5.9% to CHF45, after holder Richemont sold its stake in the Basel, Switzerland-based travel retail store operator for CHF45.35 per share

- Paragon Banking Group shares fell as much as 7.6% to the lowest in nearly two months after first-half impairments prove unexpectedly big

- GB Group slumped as much as 17%, the most since April 2025, after the identity verification and fraud prevention company announced additional investments to accelerate growth, which will impact short-term numbers

Asian stocks rebounded from early losses to extend their run of record‑setting gains, lifted by falling crude prices and gains in chipmakers and other technology shares. The MSCI Asia Pacific Index rose 0.6% in afternoon trading, heading for a record, after being down as much as 1% Tuesday. Tencent Holdings, Samsung Electronics and TSMC were among the top gainers, underscoring investors’ continued enthusiasm for artificial intelligence-related shares. Hong Kong and China led the region’s gains, while Japan fell. Investors eyeing major Chinese technology firms in Hong Kong helped revive the Asia benchmark, following a report of Tencent’s progress in launching an AI agent on WeChat and Meituan’s narrower quarterly losses. A gauge tracking these companies rose 4.7%. Indian information technology stocks also gained, after Nvidia CEO Jensen Huang rebuffed concerns that the software industry is at risk of being disrupted by more advanced AI tools.

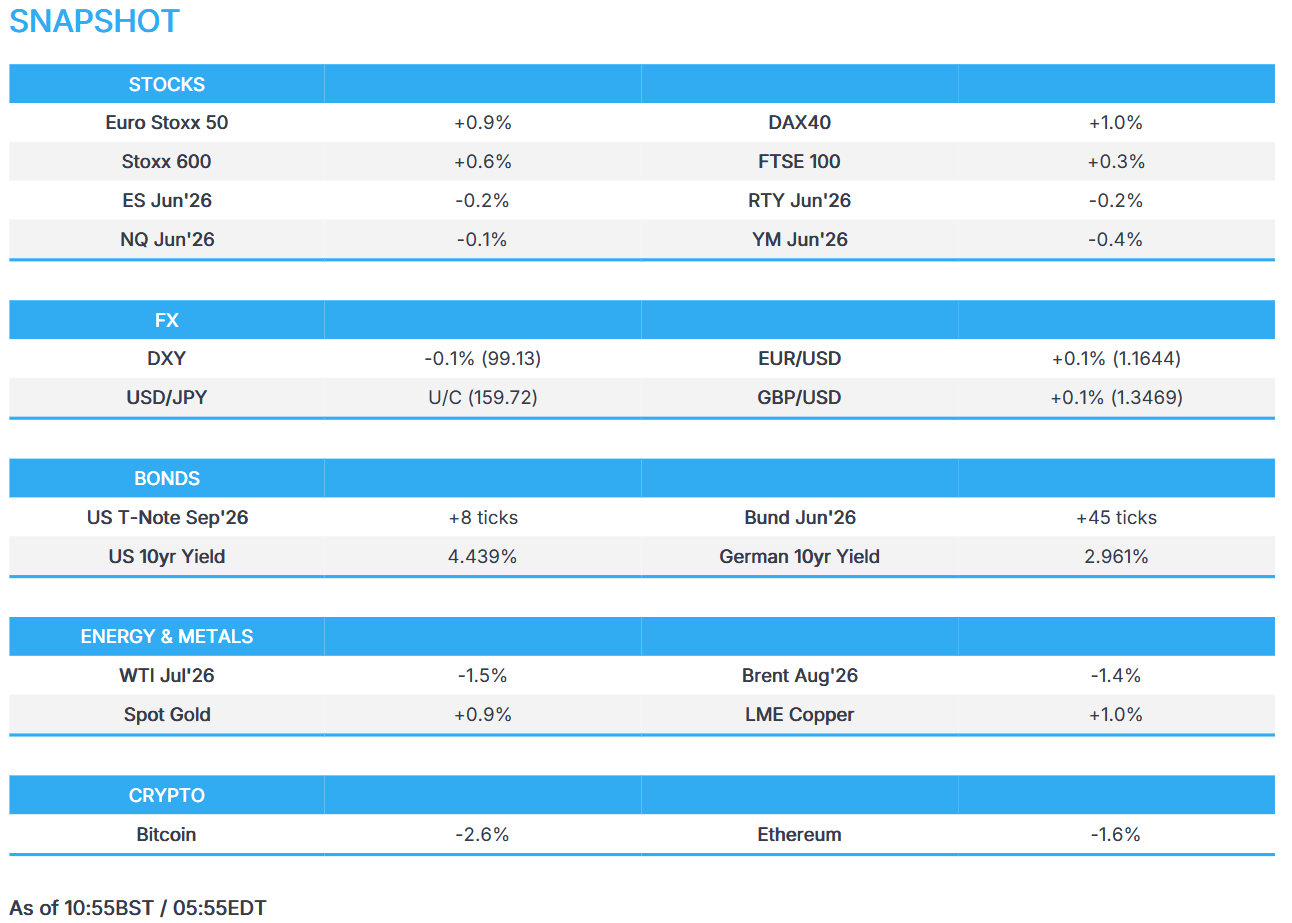

In FX, the Bloomberg Dollar Spot Index edged 0.1% lower and oil prices eased as President Donald Trump said he is still optimistic the US can reach an interim peace deal with Iran soon, even after the Islamic Republic threatened to suspend talks. AUD/USD gained 0.3% to 0.7182 after Reserve Bank of Australia monetary policy board member Ian Harper said strong action is needed if inflation expectations become unanchored,USD/JPY ticked up less than 0.1% to 159.73. EUR/USD rose 0.2% to 1.1650

In rates, treasuries advance, pushing US 10-year yields down 2 bps to 4.44% supported by a wider rally across European bonds as oil unwinds a portion of Monday’s gains on optimism around the prospects of a US-Iran peace deal flagged by President Donald Trump. US yields richer by 2bp to 3bp across the curve with belly marginally outperforming, richening the 2s5s30s fly by ~1bp on the day. US 10-year yields trade around 4.425%, richer by 3bp on the day with bunds and gilts outperforming by 2.5bp and 4.5bp in the sector. European government bonds outperform with UK and German 10-year borrowing costs falling 5-6 bps each. Labor market in focus for the US session with JOLTS job openings data due, ahead of ADP employment and the May jobs report later this week.

In commodities, WTI crude oil futures are down 1.3% near session lows. Precious metals advance, with spot silver adding 2% and gold trading around $4,525. Bitcoin falls below $70,000 for the first time since April.

US economic data calendar includes April JOLTS job openings at 10am; Fed speaker slate includes Hammack (8:30am) and Goolsbee (11pm).

Market Snapshot

Top Overnight News

- Lebanon announced a partial ceasefire between Hezbollah and Israel on Monday in what would amount to a limited de-escalation of a conflict that has killed thousands of people and inflamed the broader U.S.-Israeli war with Iran. RTRS

- The fighting in Lebanon had become a major sticking point in end-of-war talks as Iran considers the conflict a violation of the U.S.-Iran ceasefire. Trump received briefings in recent weeks that the Israel-Hezbollah conflict was one of the key reasons why Iran remained unwilling to make a deal with the U.S., Trump administration officials said. WSJ

- The Trump administration on Monday proposed a 25 percent tariff on a broad range of Brazilian imports, concluding after a trade investigation that Brazil had engaged in unfair practices that imposed burdens on American businesses. NYT

- The White House will cut tariffs on agricultural equipment, such as combines and harvesters, to 15% from 25% on June 8. A lower 10% duty rate may apply if the equipment contains at least 85% US steel or aluminum. BBG

- Gold has overtaken US government bonds as the world’s top reserve asset following years of relentless buying by central banks and a historic rally that has seen prices nearly double over the past two years. FT

- SK Hynix plans to double its memory chip wafer capacity over the coming half-decade to ease a global shortage of a key AI component. BBG

- Former BOJ board member Sayuri Shirai said the central bank may hold rates steady this month because underlying inflation pressures haven’t strengthened that much. BBG

- The US is discussing whether to deploy nuclear weapons in additional European Nato states, in a move intended to reassure allies that reduced conventional military support does not weaken security guarantees. FT

- NVDA CEO Jensen Huang said on Tuesday the company has enough supply to accommodate robust growth in central processing units (CPUs) and graphics processing units (GPUs) as it rides an AI boom. The company, considered a barometer for the AI market’s health as its semiconductors are used in virtually every major data center in the world, acknowledged, however, that supply constraints remain a concern. RTRS

Iran War

- US President Trump told ABC News he thinks he will have an agreement with Iran to extend the ceasefire and reopen the Strait of Hormuz over the next week, while he also stated that a peace agreement with Iran could be better than a military victory. Trump also stated that it’s not simple for both sides, but they’re getting what they need to get and that he still has to get a few more points.

- US President Trump said he had a very productive call with Israeli PM Netanyahu and that there will be no troops going to Beirut, while he added that Hezbollah agreed that all shooting will stop.

- US President Trump reportedly lashed out at Israeli PM Netanyahu over Israel’s escalation in Lebanon in an expletive-laden call on Monday, according to Axios, citing two US officials and a source briefed on the call.

- Iran’s final text is still being discussed in Tehran and no response has been sent yet, Mehr News reported citing sources.

- Iranian Parliament Speaker Ghalibaf said talks will halt if Israeli actions persist in Lebanon, and warned that Iran will confront Israel if atrocities in Lebanon continue.

- A senior Iranian official said a renewed war with US ‘inevitable’, Arab News reported citing state TV.

- Iran’s IRGC reported targeting a US-owned commercial vessel with a cruise missile, according to Al Jazeera.

- Iran’s IRGC said 24 ships passed through the Strait of Hormuz in the last 24 hours after obtaining permission from Iran, Nour News reported.

- “A number of vessel owners are saying that they are no longer receiving IRGC threats via the radio, which wasn’t the case a few weeks back. But still the confidence level in crossing is low”, Kpler’s Bakr posted.

- Lebanon officials said Hezbollah and Israel agreed to the US proposal for mutual cessation of hostilities. Israel will stop strikes on Beirut southern suburbs under the proposed agreement, Press TV reported.

- Israeli airstrikes target sites in southern Lebanon, Sky News Arabia reported.

- Source close to Yemen’s Houthis emphasised they will not allow Lebanon to be attacked and Hezbollah to fight alone, according to SNN.

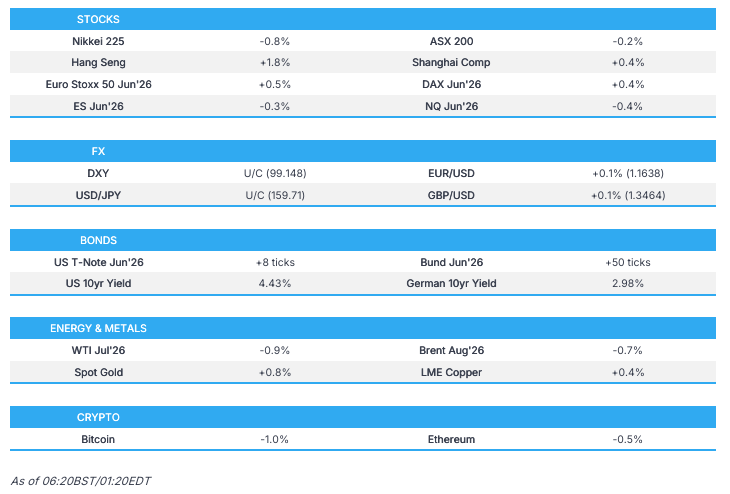

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed following the choppy performance stateside, where the major indices ultimately finished mostly higher amid tech strength and mixed geopolitical updates. ASX 200 was subdued amid weakness in real estate, financials and defensives, while sentiment was also not helped by a slew of mostly weaker-than-expected data releases. Nikkei 225 slipped after printing a new all-time high at the open with very few fresh catalysts from Japan, and as the recent mixed geopolitical headlines provide an opportunity to book profits. Hang Seng and Shanghai Comp conformed to the mixed picture with the mainland flat, while the Hong Kong benchmark was led higher by strength in the big tech names, with Meituan underpinned post-earnings, while Tencent, Alibaba, Lenovo, Kuaishou, SMIC and JD were all among the top performers.

Top Asian News

- Japanese Finance Minister Katayama refrained from commenting on FX intervention and current FX levels, while she said volatility in oil markets remain and prepared to take appropriate action. Closely coordinating with the US on Forex, and both sides are closely monitoring markets.

- South Korean Inflation Rate YoY (May) Y/Y 3.1% (Prev. 2.6%).

- South Korean Inflation Rate MoM (May) M/M 0.5% (Prev. 0.5%).

European bourses (STOXX 600 +0.7%) start Tuesday’s trade with broad gains after raised hopes of an imminent US-Iran deal. US President Trump said negotiations with Tehran were continuing and signalled expectations of a deal to extend the ceasefire and reopen Hormuz “over the next week”. Furthermore, Trump also claimed Israel and Hezbollah had agreed to stop shooting, which further weighed on energy prices and boosted the global risk tone. European sectors highlight the positive bias. Technology (+2.7%) tops the sector pile, with Basic Resources (+2.2%) following closely behind as metals surge amid worries of a tighter global supply. Energy (-0.7%), Healthcare (-0.6%) and Food, Beverages & Tobacco (-0.4%) are the only sectors printing modest losses.

Top European News

- EU is weighing fiscal flexibility for energy costs, while the proposal would allow countries budgetary leeway to cushion energy costs, according to Bloomberg.

- US is in talks to expand nuclear weapon deployments in Europe, according to FT.

- UK Labour leader candidate Andy Burnham said he rules out an early General Election if he is elected to replace PM Starmer, Bloomberg reported citing his spokesperson.

- UK’s Ofgem is seeking views on draft guidance to support proportionate supply chain security risk management in the downstream gas and electricity sector.

FX

- G10s are mixed but mostly stronger against the Buck as energy benchmarks pull back alongside more constructive Gulf headlines.

- The Buck trades a touch lower after pressure seen in the early European morning attempted to push the Dollar index to the 99.00 level. Markets are generally more risk-on after headlines overnight were more constructive than those seen on Monday. See 08:20 BST headline for geopolitical specifics. US domestic newsflow has been light. Today sees the release of JOLTS job openings. The figure is expected to be broadly unchanged from the March figure. DXY trades 0.1% lower within a 99.05-9922 range.

- EUR is a touch firmer against the weaker Buck in a reaction you would expect to see in response to the recent geopolitical headlines. The EZ Inflation report held a hawkish skew, with the energy component and Services jumping. The single currency was little moved on the report, given it ultimately plays in favour of a hike in June, which is ultimately fully priced in.

- JPY is incrementally lower vs the USD. Japan saw strong demand at its 10yr auction overnight, where demand rose beyond the 12-month average despite the BoJ slated to hike rates in two weeks. JPY saw modest strength on the results, though it proved fleeting with USD/JPY rangebound given the various fiscal/Terms of Trade headwinds. In a note this morning, ING wrote “The risk of new intervention does look a bit underpriced, considering Japanese authorities have remained rather hawkish with their intervention narrative.” Katayama was on the wires overnight, she said: “Closely coordinating with the US on FX.”

Fixed Income

- Global fixed benchmarks are stronger across the board, facilitated by a pullback in energy prices after some positive-leaning geopolitical newsflow. In brief, President Trump suggested that talks with Iran are continuing at a rapid pace, adding that he thinks an agreement will be made with Iran to extend the ceasefire over the next week.

- As for price action, USTs benefit from the lower energy prices this morning, with gains of c. 8 ticks at pixel time; currently holds at the upper end of a 109-22 to 109-30 range (vs Monday’s trough of 109-09+). From a yield perspective, rates at the belly of the curve are underperforming vs short-dated rates, signalling that traders remain uncertain about near-term geopolitical progress. The 10yr (4.43%) now resides back towards recent troughs, and another leg lower could see a test of the low from 12 May at 4.41%. Focus ahead turns to US JOLTS.

- Bunds (+50 ticks) and Gilts (+60 ticks) also extend higher, following the geopolitical risk tone. For the EZ specifically, a hawkish inflation report out of the EZ (Services at 3.5% from 3.00%, and Core Y/Y topped expectations), led to some mild pressure in German paper.

- JGBs (+92 ticks) are outperforming vs peer, boosted by the geopolitical tone and a solid 10yr Japanese auction. Whilst the b/c and avg. yield were not so good, the lowest accepted price fell to 98.01 (prev. 98.86), indicating some solid demand for the paper. The 10yr knee-jerked higher following the sale, before then gradually moving higher as other investors also bought debt. As it stands, the 10yr (2.57%) now resides at levels not seen since 13 May 2026.

- Germany sells EUR 3.857bln vs exp. EUR 5bln 2.50% 2028 Schatz: b/c 1.58x (prev. 1.4x), average yield 2.59% (prev. 2.70%), retention 22.86% (prev. 22.8%).

- UK sells GBP 3.25bln 4.625% 2037 Green Gilt: b/c 3.63x, average yield 4.975%, tail 0.2bps.

- Japan sells JPY 1.98tln 10yr JGBs, b/c 3.53x (prev. 3.90x, 12-month avg. 3.35x), average yield 2.649% (prev. 2.540%).

Central Banks

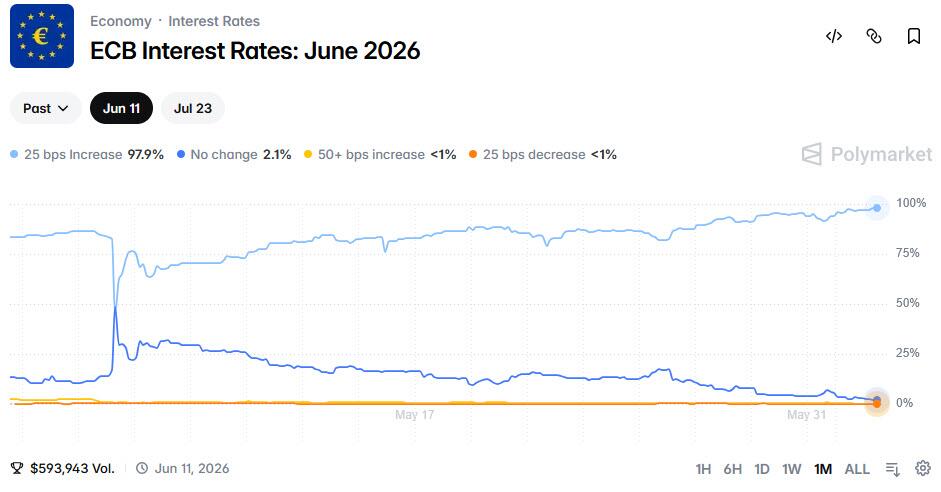

- ECB’s Rehn says a June rate move would be an insurance hike and that inflation expectations remain unanchored.

- ECB’s Simkus said consumer short-term inflation expectations are similar to 2022 and that it is important to react in a timely manner to inflation.

- Rabobank maintains its forecast for a 25bps ECB rate hike next week; expects the ECB to raise rates by another 25bps, likely in September.

- RBA’s Harper said stronger than expected domestic demand and re-emergence of capacity constraints have widened the output gap again, and markets are now anticipating that the bank would have to address this, while he added that persistent inflation is a genuine concern and market measures of inflation have gone up, which is a worry.

- Nikkei reported that the BoJ is continuing to call for a June hike, though the government is opting for a “wait-and-see” approach given the risks of risking inflation and a weaker JPY.

- BoJ summary of meeting with investors: one participant said the need for further tapering of bond purchases is not high; participant said there is no need for further tapering of bond buying. One participant said the BoJ should act nimbly, such as conducting emergency bond-buying operations as needed when the bond market destabilises.

Commodities

- Crude futures are subdued this European morning as the complex takes a breather from yesterday’s surge, with upside capped by constructive comments from US President Trump. To recap, US President Trump said talks with Iran were continuing at a rapid pace and that he believes an agreement to extend the ceasefire and reopen the Strait of Hormuz could be reached within the next week. That being said, it was reported this morning that Iran’s final text is still being discussed in Tehran and no response has been sent yet; Mehr News reported, citing sources. Meanwhile, a senior Iranian official said renewed war with the US is ‘inevitable’, Arab News reported, citing state TV. Elsewhere, Lebanon emerged as a major issue, with Iran warning that continued Israeli actions could impact negotiations.

- WTI and Brent front-month futures trade softer by some 2% and 1.8% respectively, at the time of writing after the benchmarks settled higher by USD 4.80/bbl and USD 3.86/bbl, respectively, on Monday. Benchmarks have held a negative bias throughout the European morning. WTI Jul resides towards the bottom end of a USD 90.15-92.65/bbl range, Brent Aug trades in a USD 90.66-92.85/bbl range. Dutch TTF trades -2.5% within the recent EUR 47-48/MWh range.

- Spot gold is slightly firmer as the USD remains subdued by oil prices, with the yellow metal in a USD 4,463-4,541/oz range, within yesterday’s USD 4,447-4,546/oz range. Spot silver similarly rebounds but tops yesterday’s high (USD 76.29/oz) to currently trade towards the top end of a USD 74.48-76.93/oz range.

- Base metals are firmer across the board amid the softer USD and softer oil prices, coupled with a firm performance across Chinese markets overnight. 3M LME copper resides in a narrow USD 13,821.53-13,992.22/t range at the time of writing.

- The IEA’s oil division chief said oil supplies from the US, Brazil, Argentina and Venezuela have exceeded expectations, but output from the Americas can only marginally offset supplies lost East of Suez.

- UAE’s ADNOC executive said China’s demand is starting to come back, and “teapot” refineries are showing appetite.

Trade/Tariffs