EXCHANGE: COMEX

CONTRACT: JUNE 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,489.100000000 USD

INTENT DATE: 06/02/2026 DELIVERY DATE: 06/04/2026

FIRM ORG FIRM NAME ISSUED STOPPED

072 H GOLDMAN 1

099 H DEUTSCHE BANK AG 88

118 H MACQUARIE FUTURES US 1

190 H BMO CAPITAL MARKETS 15

323 C HSBC 47

363 H WELLS FARGO SECURITI 39

555 C BNP PARIBAS SEC CORP 180

661 C JP MORGAN SECURITIES 24

686 C STONEX FINANCIAL INC 1

686 H STONEX FINANCIAL INC 160

800 C MAREX SPEC 30

880 C CITIGROUP 2

905 C ADM 32

TOTAL: 310 310

MONTH TO DATE: 25,345

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2026: 310 CONTRACTs NOTICES FOR 31,000 OZ or 0.9642 TONNES

total notices so far: 25,345 contracts FOR 2,534,500 OZ OR 78.83 TONNES

SILVER NOTICES: 4 NOTICE(S) FILED FOR 20,000 OZ /

total number of notices filed so far this month : 1947 CONTRACTS (NOTICES) for 9.585 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 20,000 OZ//NEW STANDING ADVANCES TO 11.135 MILLION OZ//

SUMMARY OF OUR JUNE 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE..8.980 MILION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 20,000 OZ//NEW STANDING ADVANCES TO: 11.135 MILLION OZ

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT 0.6780 TONNES OF A QUEUE JUMP/NEW STANDING ADVANCES TO 81.598 TONNES

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.6780 TONNES//NEW STANDING ADVANCES TO 81.598 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 25.334 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE 894 CONTRACTS TO AN OI OF 102,804.

EFP ISSUANCE 846 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 846 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 894 CONTRACTS AND ADD TO THE 846 E.FP. ISSUED

WE OBTAIN A MEGA HUGE GAIN OF 1746 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR SMALL GAIN OF $0.25

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 8.700 MILLION PAPER OZ

OCCURRED DESPITE OUR SMALL GAIN IN PRICE.OF $0.25

2.ASIAN AFFAIRS JUNE 3 /2025

SHANGHAI CLOSED UP 8.87 PTS OR 0.22%

HANG SENG CLOSED DOWN 405.11 PTS OR 1.56%

Nikkei CLOSED UP 1742.76 PTS OR 2.41%

//Australia’s all ordinaries CLOSED DOWN 0.02%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7637

/ OFFSHORE CLOSED DOWN AT 6.7752 Oil UP TO 96,29 dollars per barrel for WTI and BRENT UP TO 98.22 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7737) OFFSHORE YUAN TRADING DOWN TO 6.7752 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL 289 CONTRACTS TO 326,052 A NEW ALL TIME LOW OF 326,052 OI SURPASSING THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,052 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD HUGE T.A.S. LIQUIDATION EARLY DURING FRIDAY’S OP =EX TRADING (OTC/LONDON OPTIONS EXPIRY TRADING). IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MAY CONTRACT MONTH!!

THE SMALL SIZED GAIN ON OUR TWO EXCHANGES OCCURRED WITH OUR GAIN IN PRICE IN GOLD (UP $7.45).

WE THUS HAD A SMALL SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 866 CONTRACTS (OR 7.427 TONNES) WITH OUR GAIN IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 1155 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO SO FAR

DETAILS ON OUR NEW JUNE COMEX CONTRACT MONTH//

IN TOTAL WE HAD A SMALL GAIN ON OUR TWO EXCHANGES OF 866 CONTRACTS WITH OUR GAIN IN PRICE ($7.45). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A SMALL SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 764 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 134+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO. WE WILL KNOW IN JUNE WHETHER THEY COVERED ANY OF THEIR SHORTFALL.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES (CME CORRECTED) TO WHICH WE ADD OUR NEXT 0.6780 TONNES OF A QUEUE JUMP//NEW STANDING ADVANCES TO 81.598 TONNES//

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JUNE,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $7.45)

WE HAD SOME T.A.S. SPREADER LIQUIDATION TUESDAY // COMEX SESSION// WITH OUR GAIN IN PRICE , OUR LONG SPECULATORS STILL REMAIN RELENTLESS POURING INTO THE COMEX

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

TUESDAY NIGHT//WEDNESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $7.45

WE HAD A STRONG 1522 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 866 CONTRACTS OR 86,600 OZ OR 2.693 TONNES

MAY DELIVERY MONTH

JUNE 3

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | ENTRIES; 1 ENTRY: 1 i) Into Brinks 643.02 oz 20 kilobars total deposit: 643.02 oz |

| Deposit to the Dealer Inventory in oz | 1 ENTRY i) Into Stonex: 16,005.454 oz total deposit: 16,005.454 oz |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER ENTRY: 0 xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 310 CONTRACTS OR 31,000 OZ 0.9642 TONNES OF GOLD |

| No of oz to be served (notices) | 889 Contracts 88,900 OZ 2.765TONNES |

| Total monthly oz gold served (contracts) so far this month | 25,345 notices 2,534,500 oz 78.83 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

1 ENTRY

i) Into Stonex: 16,005.454 oz

total deposit: 16,005.454 oz

DEPOSITS/CUSTOMER

ENTRY: 0

xxxxxxxxxxxxxxxxxx

comex withdrawal

ENTRIES; 1

ENTRY: 1

i) Into Brinks 643.02 oz

20 kilobars

total deposit: 643.02 oz

adjustments: 2// customer to dealer:

a) Delaware 503.200 oz

b) Manfra 2893.59 oz

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JUNE OI STANDS AT 1199 CONTRACTS HAVING A LOSS OF 323 CONTRACTS.

WE HAD 541 CONTRACTS SERVED ON TUESDAY, SO WE GAINED A STRONG 218 CONTRACTS OR 21,800 OZ. (0.6780 TONNES) EXERCISED A QUEUE JUMP WHERE THEY WILL TAKE PHYSICAL GOLD ON THIS SIDE OF THE POND.

JULY LOST 8 CONTRACTS DOWN TO 3220 CONTRACTS.

AUGUST GAINED 221 CONTRACTS UP TO AN OI OF 262,894

.

We had 310 contracts filed for today representing 31,000oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 310 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 24 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (25,345) to which we add the difference between the open interest for the front month of JUNE1199 CONTRACTS) minus the number of notices served upon today 310 x 100 oz per contract) equals 2,623,400 OZ OR (81.598Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (25,345) to which we add the difference between the open interest for the front month of JUNE( 1199 CONTRACTS) minus the number of notices served upon today 310 x 100 oz per contract) equals 2,623,400 OZ OR (81.598 Tonnes of gold)

new total of gold standing in JUNE becomes 80.936 TONNES//

TOTAL COMEX GOLD STANDING FOR JUNE 81.598 TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS ACTIVE DELIVERY MONTH OF JUNE.

confirmed volume TUESDAY confirmed 110,192// extremely poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,871,884.743 oz 58.22 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,871,884.743 tonnes oz 58.22 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 28,328,195.901oz

TOTAL REGISTERED GOLD 15,299,634.698 tonnes (475.882 tonnes)

TOTAL OF ALL ELIGIBLE GOLD 13,028,561.203 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,427,750 oz ((REG GOLD- PLEDGED GOLD)=

417.659 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JUNE DELIVERY MONTH

JUNE 3

JUNE DELIVERY MONTH

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 ENTRY |

| Deposits to the Dealer Inventory | 0 entries |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT DEPOSIT ENTRIES/CUSTOMER ACCOUNT 1 entries i) Into HSBC 600,056.052 oz total deposit: 600,056.052 oz |

| No of oz served today (contracts) | 4 CONTRACT(S) (20,000 OZ) |

| No of oz to be served (notices) | 310 Contract (1.555 MILLIONoz) |

| Total monthly oz silver served (contracts) | 1917 contracts 9.585 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

1 entries

i) Into HSBC 600,056.052 oz

total deposit: 600,056.052 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

0 ENTRIES

adjustments 1 dealer to customer

i) CNT 51,849.05 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 84.534 MILLION OZ//.TOTAL REG + ELIGIBLE. 319.278 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE /2026 OI: 314 OPEN INTEREST CONTRACTS FOR A LOSS OF 66 CONTRACTS.

WE HAD 70 NOTICES SERVED ON TUESDAY SO WE GAINED 4 CONTRACTS OR AN ADDITIONAL 20,000 OZ WILL STAND AS A QUEUE JUMP AT THE SILVER COMEX.

JULY SAW A LOSS OF 233 CONTRACTS DOWN TO 70,509 CONTRACTS.

AUGUST SAW A GAIN OF 43 CONTRACTS UP TO 775…

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 4 or 20,000 oz

CONFIRMED volume TUESDAY; 39,414// poor volume

XXX

AND NOW JUNE. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 1917 X5,000 oz = 9.585 MILLION oz

to which we add the difference between the open interest for the front month of JUNE( 314) AND the number of notices served upon today (4 )x (5000 oz)

Thus the standings for silver for the JUNE 2026 contract month: (1917 )Notices served so far) x 5000 oz + OI for the front month of JUNE (314) minus number of notices served upon today (4)x 5000 oz equals silver standing for the JUNE..contract month equating to 11.135 MILLION OZ.+

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 84.534 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/319.278 million: 43.85

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JUNE 3 /2026/WITH GOLD DOWN $51.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.856 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.000 TONNES

JUNE 2 /2026/WITH GOLD UP $7.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.712 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.856 TONNES

JUNE 1 /2026/WITH GOLD DOWN $79.30 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 29 /2026/WITH GOLD UP $59.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

GLD INVENTORY: 1028.000 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JUNE 3 WITH SILVER DOWN $2.55: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.432 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

CLOSING INVENTORY 483.423 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD..

Is silver about to explode higher?

Silver appears to be catching a bid. It raises a question: if copper is at all-time highs, why not silver? As an illiquid trade, silver often leads gold higher as well.

| Alasdair MacleodJun 3∙Paid |

Bullet points:

· Global silver supply is tightening, because 56% of mine supply comes from copper and nickel ores whose processing requires sulphuric acid, which is not easily sourced due to the Hormuz closure and China’s withdrawing from exporting it.

· Copper and nickel prices are hitting record highs suggesting that silver should as well.

· Industrial demand is increasing, driven by a number of factors, adding perhaps 10% or more to The Silver Institute’s estimates of industrial demand, increasing the supply deficit. The industrial shortage is increasing significantly.

· China is severely restricting silver exports and has become a net buyer in record quantities.

· Speculative interest in London and New York paper markets is at the lowest level in over a decade, leading to poor liquidity and potentially another bear squeeze.

The current setup

There are a few indications that something is afoot in silver even though speculative interest in both gold and silver is almost absent. This tells us that selling is almost exhausted and the speculators’ next action will be to buy.

It’s not just silver. Gold’s open interest on Comex has also collapsed to levels not seen for nearly 20 years:

Open interest in both metals is now lower than at the bottom of the 2011-15 bear market in gold. But today they are trading in fundamentally different conditions, leading the wider commodity world to higher price levels.

Silver’s industrial demand is accelerating

As the best electrical and thermal conductor, silver outperforms copper giving it a starring role not just in photovoltaics and electric vehicles but in all electronic circuitry. The AI revolution is leading to a massive expansion of data centres, which is almost certainly underestimated in the most recent Silver Institute forecasts. Furthermore, electric vehicle sales are being given a further boost by the oil crisis, as is demand for photovoltaics.

Metals Focus produced its estimates for the Silver Institute before the war against Iran, and the data centre expansion theme was probably less developed. Furthermore, silver demand for missiles and other defence applications has increased significantly as the US, NATO, and Israel are desperately trying to replace their depleted stocks.

Clearly, the MF/SI estimate of industrial demand in 2026 at 639.6 million ounces is now too low, probably by as much as 10% or more. It is the surge in advanced technical applications, particularly in the field of defence which has led the US to declare silver as a critical mineral, signalling a policy of government accumulation which must be urgent. Indeed, any nation accumulating copper will be accumulating silver for similar reasons. Where copper goes, so must silver. But as the chart below shows, they have followed different paths recently.

Should silver be significantly below its January highs and particularly left behind since April when copper began its current run from $5.35 to $6.43 while silver struggled to rise from $70 to the current $75?

Both metals share many applications, particularly with respect to advanced technologies. The US is thought to be stockpiling copper under its 2026 Project Vault, a $12 billion public-private strategic critical minerals reserve modelled partly on the Strategic Petroleum Reserve. Now declared a critical mineral, silver is definitely on the US buying list.

The other copper stockpiling nation is China. It is now stockpiling silver as well and created the tightness in western markets which led to the lease rate in London last October soaring to 40% as buyers of forward paper demanded delivery. It was that event which led to silver rising from $50 to over $120 on 29th January.

In the first three months of this year most of which saw a fall in silver’s price, China imported 1,626 tonnes (52.28 moz). Her domestic production last year was 3,400 tonnes, and over the decades has also accumulated significant above-ground stocks, though these strategic holding details are not publicly available.

Now that China has been aggressively importing silver and severely restricting exports under licence against a background of maintaining her strategic above-ground stocks, it is hard to escape the conclusion that China has abandoned efforts to suppress the price and instead is prepared to put the squeeze on other nations’ industrial demand. This is almost certainly true along with restrictions on rare earth exports for the US, more so given that the US has only recently declared silver as a critical mineral for its 2026 Project Vault.

Non-ferrous ore is now over 70% of new silver supply

Over 70% of mined silver is a byproduct of operations targeting other metals, with copper accounting for 27% and lead/zinc a further 29% totalling 456 moz. Both copper and zinc require sulphuric acid for leaching, though less is used in the case of lead ore, which is another source. The reason this is relevant is that 60% of the world’s sulphuric acid is primarily a downstream product from oil refining. The closure of the Straits of Hormuz has disrupted sulphur and sulphuric acid availability. And China, which was the world’s greatest single export source, has stopped exporting it entirely to preserve her own stocks.

The price of sulphur has doubled since the start of the war against Iran and so has that of sulphuric acid. This has effectively tightened copper supply, contributing to bullish sentiment for copper. The reduction of copper and zinc supply from the same factors should have the same or even greater impact on the price of silver, because over 50% of silver is a byproduct from these ores and unlike copper and nickel supply was already in growing deficit relative to demand.

Investment demand

So far, the silver story has been entirely about industrial demand. Since silver’s peak price on 29th January, there has been relatively minor liquidation of silver ETFs in US and European markets. But overall, investor sentiment in G7 nations never really got going last year, and is still subdued. Silver stands-for-delivery on Comex totalling 104 moz since the price peak appear to be entirely due to industrial demand.

Because investors see silver primarily as a precious or monetary metal, investment sentiment is tied to gold. Silver tends to rise and fall at twice gold’s pace, so it is regarded as a secondary play on the gold price. And with respect to gold, Comex’s ultra-low open interest confirms that US investors have almost no involvement there as well.

In this report we have detailed how industrial demand accounts for all silver supply, and then some. Clearly, should gold begin another bull run, investment demand for silver will increase with it, exacerbating the shortage of physical metal. We can be sure that industrial users are not profit-takers if prices begin to be driven by investors and might even begin to panic buy to secure inventory.

This article posed the question: Is silver about to explode higher? Signs of the silver price being more resilient in recent trading sessions than that of gold suggest that in current thin markets there are ready buyers when silver is offered. Furthermore, Comex open interest has increased 24.6 million ounces in the last month, while still at very low levels. Clearly, silver is searching for a bottom and when it is in, not only will it catch up with copper and zinc, which is also hitting new highs, but the panic to buy by both users and then investors promises to trigger another dramatic bear squeeze on the establishment shorts.

3. CHRIS POWELL AND HIS GATA DISPATCHES

4.ANDREW MAGUIRE LIVE FROM THE VAULT 274 and 273

MUST VIEWl ANDREW’S NEWEST PODCAST

5. COMMODITY REPORT//RICE

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 8.87 PTS OR 0.22%

HANG SENG CLOSED DOWN 405.11 PTS OR 1.56%

Nikkei CLOSED UP 1742.76 PTS OR 2.41%

//Australia’s all ordinaries CLOSED DOWN 0.02%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7637

/ OFFSHORE CLOSED DOWN AT 6.7752 Oil UP TO 96,29 dollars per barrel for WTI and BRENT UP TO 98.22 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7737) OFFSHORE YUAN TRADING DOWN TO 6.7752 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7732

OFFSHORE YUAN: DOWN TO 6.7752

1.HANG SANG CLOSED DOWN 405.11 PTS OR 1.56%

2. Nikkei closed UP 1742.76 PTS OR 2.61%

WEST TEXAS INTERMEDIATE OIL UP TO 96.29

BRENT; 98.22

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 99.34/// EURO FALLS TO 1.1613 DOWN 9 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.634 UP 4 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.68… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.853 UP 1 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN( 6.7737 AND OFFSHORE: DOWN AT 6.7752

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +3.0113// Italian 10 Yr bond yield UP to 3.747// SPAIN 10 YR BOND YIELD UP TO 3.443%

3i Greek 10 year bond yield UP TO 3.679%

3j Gold at $4456.30 //Silver at: 74.20 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 11/ 100 roubles/72.93

3m oil (WTI) into the 96 dollar handle for WTI and 98 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.68 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.634% UP 4 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.853 UP 1 PTS..: USA/SF this 0.7844 as the Swiss Franc . Euro vs SF: 0.9167

USA 10 YR BOND YIELD: 4.485 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.990 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.076 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 45.96 UP 3 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.9040 UP 6 PTS

30 YR UK BOND YIELD: 5.592 UP 5 BASIS PTS

10 YR CANADA BOND YIELD: 3.415 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.075 DOWN 1 BASIS PTS.

Futures Drop, Yields And Oil Rise On Latest Middle East Hostilities

Wednesday, Jun 03, 2026 – 08:24 AM

US equity futures are mixed as oil prices, bond yields, and USD move higher in response to the latest overnight attacks in the Middle East with no public progress on a deal. As reported previously, the US struck Iran’s Qeshm Island, which was then met with retaliatory Iranian strikes on US bases in Kuwait; explosions were also reported in Saudi Arabia, and air sirens were set off in the UAE. US Centcom said that the Iranian drone attacks were “successfully defeated.” As of 8:00am ET, S&P futures were down 0.1% but off session lows: absent the now daily gamma squeeze, the S&P is poised to halt a nine-day rally; Nasdaq futures rose 0.2% with semis bid premarket led by MRVL, INTC, AVGO, and AMD as Mag7 names are weaker. Some pockets of tech exuberance are seen in the US pre-market with Marvell adding 12% to Tuesday’s near 33% surge. Tech enthusiasm was once again on display in Asia with the MSCI APAC index hitting yet another record high. Mag7 have been used as a funding trade to buy Semis and to make room for deals, according to JPM. Cyclicals ex-Energy are lagging Defensives. Brent rose 2.3% to top $98 a barrel. The yield on 10-year Treasuries climbed four basis points to 4.48% as crude prices stoked concerns about inflationary pressures; the yield curve is bear flattening with yields up 3-4bp as USD is poised for its strongest week since mid-May. Data calendar includes May ADP employment change (8:15am), S&P Global US services PMI (9:45am), and April factory orders and May ISM services index (10am). Fed speaker slate includes Barr (9am) and Logan (4pm), and Beige Book is slated for 2pm release.

In premarket trading, Magnificent Seven are mixed (Meta +0.6%, Apple -0.2%, Alphabet -0.7%, Amazon -0.05%, Nvidia +0.3%, Microsoft +0.2%, Tesla -0.7%)

- Cognyte Software (CGNT) slumps 21% after the Israeli company posted disappointing first quarter earnings.

- GameStop (GME) is up 13% after the video game retailer reported net sales for the first quarter of $835.3 million, marking a 14% increase from the year prior. The company also said its board approved a discretionary $2 billion share repurchase authorization.

- Iren Ltd. shares rise in premarket trading after it signed a transmission connection agreement to support a planned 800-megawatt data center campus in Bundey, South Australia.

- Macy’s (M) climbs 3% after the department-store operator boosted its adjusted earnings per share forecast for the full year.

- Marvell Technology (MRVL) gains 10%, putting the stock on track to extend Tuesday’s 33% rally, after Nvidia CEO Jensen Huang predicted that the semiconductor and networking company would be the next business to hit a $1 trillion valuation.

- Medtronic (MDT) rises 2% after posting fourth quarter revenue that beat expectations.

- Palo Alto Networks (PANW) falls 2% after the security software company reported results following a 61% year-to-date rally.

- Sherwin-Williams (SHW) climbs 3% after the company and Nippon Paint abandoned efforts to acquire the Dutch paintmaker Akzo Nobel.

- Sprinklr (CXM) falls 3% after the software company trimmed its full-year revenue outlook.

In other news, SpaceX plans to set the terms of its IPO offering as early as Wednesday afternoon, ahead of what’s expected to be the biggest ever listing. Reuters later reported that SpaceX aims to sell 555.6 million shares at $135 apiece. Uber set usage caps on some AI-powered tools used by its staff. The move, meant to manage costs after the company blew through its AI budget, may be a concern for investors tracking the explosive growth in the industry. GitLab is cutting about 14% of its workforce and exiting 22 countries as part of a restructuring aimed at streamlining operations and sharpening execution. Google must make changes to its AI-generated search summaries after the UK’s antitrust watchdog ordered it to give publishers more control over how their content is used.

US stocks struggled to build on record gains as growing strains on the ceasefire between the US and Iran sent oil prices higher for a third straight day and lifted bond yields. The cautious mood in markets follows flare-ups in the Middle East that are testing a fragile truce between Washington and Tehran, with US forces intercepting ballistic missiles and drones aimed at neighboring countries and striking an Iranian command center in response.

The mitigating factor is higher SoH throughput; According to JPM EM Strategy, energy export volume have risen to ~3.6mm bpd over the last 2 days with the 7dma ~2.5mm bpd and refined chemical throughput now >50% of pre-conflict levels. The OECD flags global growth downside risk from a prolonged US / Iran Conflict while hiking its inflation estimates.

Trump said the US was continuing to work with Iran on a deal. Tehran has agreed it won’t have a nuclear weapon and the parties’ leaders “probably will meet at some point,” Trump said. Traders are watching whether the S&P 500 can extend its winning streak to the longest in more than three decades. A narrow rally has seen technology stocks, and chipmakers in particular, leave the rest of the market far behind.

“I don’t think this is the top, there’s still room to run,” said Amanda Lyons, head of research at Energy Group Capital. “The fuel is just quietly shifting from earnings to excitement; that’s fine on the way up, it only matters when the music stops.”

The S&P 500 may have just matched its best winning streak since 1995, but that run included five days in a row when decliners outnumbered advancers. The pattern, which was snapped on Tuesday, is described as a “breadth paradox,” by BTIG technician Jonathan Krinsky. Yet over the past three years, periods of weak breadth failed to alter the overall picture, Bloomberg notes.

Investors are also awaiting SpaceX’s disclosure of the terms of its initial public offering that is set to be by far the largest in history. Reuters reported that Elon Musk’s rocket launch, satellite and AI company aims to sell more than 550 million shares at $135 apiece for a $75 billion IPO. The share sale forms part of a pipeline of potential offerings from high-profile tech companies in the coming months. AI rivals OpenAI and Anthropic PBC look to forge ahead with listings of their own, while Alphabet Inc. revealed plans for a record $80 billion equity offering on Monday.

“The IPO wave is a strong confidence indicator for markets,” said Nataliia Lipikhina, head of EMEA equity strategy at JPMorgan Private Bank. “We think there is enough capacity in the market to absorb them, and the renewed issuance pipeline is additive to the broader market story.”

Private credit is back in focus, with Partners Group limiting withdrawals at one of its evergreen private equity funds amid heightened redemption pressure. It’s a sign the investor anxiety that hit private credit vehicles may be spilling over to asset classes within private markets. It follows Cliffwater’s flagship private credit fund capping redemptions at 5% in the second quarter after investors looked to pull about 17% of shares.

In political news, Republican Steve Hilton and Democrat Xavier Becerra surged to the top of California’s crowded gubernatorial primary. Meanwhile, the US is proposing tariffs of 10% on imports from the EU as Trump looks to rebuild the tariff wall struck down by the US Supreme Court. China, India, Japan, South Korea, Brazil and Switzerland would be subject to a 12.5% levy. Fed Chair Kevin Warsh is said to have hired conservative policy analysts Paul Winfree and Daniel Heil as temporary advisers.

Bitcoin’s selloff extended into Wednesday after Strategy’s sale of a tiny portion of its massive cryptocurrency stockpile rattled sentiment and widened the token’s divergence from record-setting technology shares.

Turning to earnings, Broadcom will offer investors another snapshot into AI spending when it reports after the close, with Bloomberg Intelligence expecting accelerating revenue from XPU chips and growing demand for networking.

European equities continue to lag global peers with the Stoxx 600 down 0.4% as higher energy prices weigh on sentiment. Here are the biggest movers Wednesday:

- Inditex shares advanced 5.6%, the third-best performance on the Stoxx 600 Retail Index, after the Zara owner reported earnings that analyst calls “reassuring,” while a strong start to 2Q has been aided by calendar effects

- B&M shares rose as much as 16%, the largest intraday gain on record, after the discount retailer reported earnings that beat consensus expectations

- Boohoo shares rose as much as 16%, trading at a 12-week high, after the online retailer returned to growth following a rise in gross merchandise value in the first quarter, with much stronger growth delivered in May

- Douglas gained as much as 7.9%, the most since Aug. 2025, as Berenberg initiates the stock with a buy rating, saying the German beauty retailer offers a compelling risk-reward based on its single-digit adjusted P/E valuation and double-digit free cash flow yields

- Sodexo shares gained as much as 3.6% to trade at a seven-month high after Barclays lifted its price target by almost 10% and said upcoming third-quarter results can provide a positive short-term catalyst for the food services company

- Howden Joinery Group’s shares rose as much as 5.2%, the most in almost two months, after it agreed to acquire the parent company of Ultima Furniture Systems, which trades as DIY Kitchens, for an enterprise value of £390 million

- Akzo Nobel shares fell as much as 22%, their steepest drop on record, after Nippon Paint and Sherwin-Williams abandoned efforts to acquire the Dutch paintmaker

- Partners Group fell as much as 13% to the lowest in more than six years as the alternative investment manager caps withdrawals from one of its evergreen private equity funds amid heightened redemption pressure

- Norwegian Air shares slide as much as 9%, the most in over a year, after Danske Bank cut its recommendation on the airline to sell from hold, saying proprietary fare data indicate demand for its routes is weaker than expected

- Clas Ohlson fell as much as 11%, the most since December, after the Swedish home improvement retailer reported its latest earnings and presented new financial targets

- DiscoverIE shares fell as much as 7% after earnings broadly met expectations but failed to extend a rally that had lifted the electronics manufacturer more than 50% over the past two months

- Ninety One fell as much as 8.2% in London, to its lowest intraday level since April after the asset management firm reported net flows for the full year that missed the average analyst estimate

Asian stocks rose to yet another record, with Japan leading gains as optimism over the region’s growing role in the artificial-intelligence ecosystem boosted tech shares. The MSCI Asia Pacific Index climbed as much as 0.9%, heading for a fourth day of gains. Japan’s Nikkei also surged to an all-time high as investors piled into chip and technology shares following a surge in US equities. Taiwan’s benchmark was the second-biggest gainer in the region. Markets in South Korea and Thailand were shut for a public holiday. Meanwhile, Indonesian stocks were the biggest losers as oil prices extended their advance to a third day. The Jakarta Composite Index plunged to its lowest level in five years and the rupiah hit a record low in another stark reminder of the multi-faceted challenges confronting Southeast Asia’s biggest economy. Investors who continue to buy into the AI trade are increasingly bullish on the region, with several Asian semiconductor shares rising. In particular, Japan’s AI industry is offering renewed appeal due to its lower cyclical risk compared with Taiwan’s and South Korea’s markets, according to Barclays Plc.

“Korea is a memory trade. Taiwan is a foundry trade. Japan is an economy trade, with an AI kicker,” Barclays global chairman of research Ajay Rajadhyaksha wrote in a note. “That distinction matters enormously if the memory cycle turns.”

In FX, USD/JPY touched 160 before remarks from PM Takaichi briefly guided the pair lower. Subsequent comments from BOJ Governor failed to support the yen.

In rates, treasury futures sit near day’s lows into the early US session amid deeper losses in European bonds as rising oil prices put upside pressure on yields globally. Oil is higher for a third straight day as strikes between the US and Iran cloud outlook for a peace agreement. US yields are 3bp-4bp higher on the day with curve spreads little changed; 10-year is near 4.48%, 3.5bp cheaper with bunds and gilts in the sector lagging by an additional 0.5bp and 1bp. US session includes ADP employment change and ISM services index, both for May, and April factory orders.

In commodities, brent crude is up 2.6% near session highs, and on a $98/bbl handle amid a lack of a breakthrough in US-Iran negotiations and Iran launching missile and drone strikes at multiple US sites. Spot gold and silver are on the backfoot, with respective losses of 1% and 1.2%.Bitcoin is off its worst levels but has extended its recent slide, down 1.2%.

US economic data calendar includes May ADP employment change (8:15am), S&P Global US services PMI (9:45am), and April factory orders and May ISM services index (10am). Fed speaker slate includes Barr (9am) and Logan (4pm), and Beige Book is slated for 2pm release.

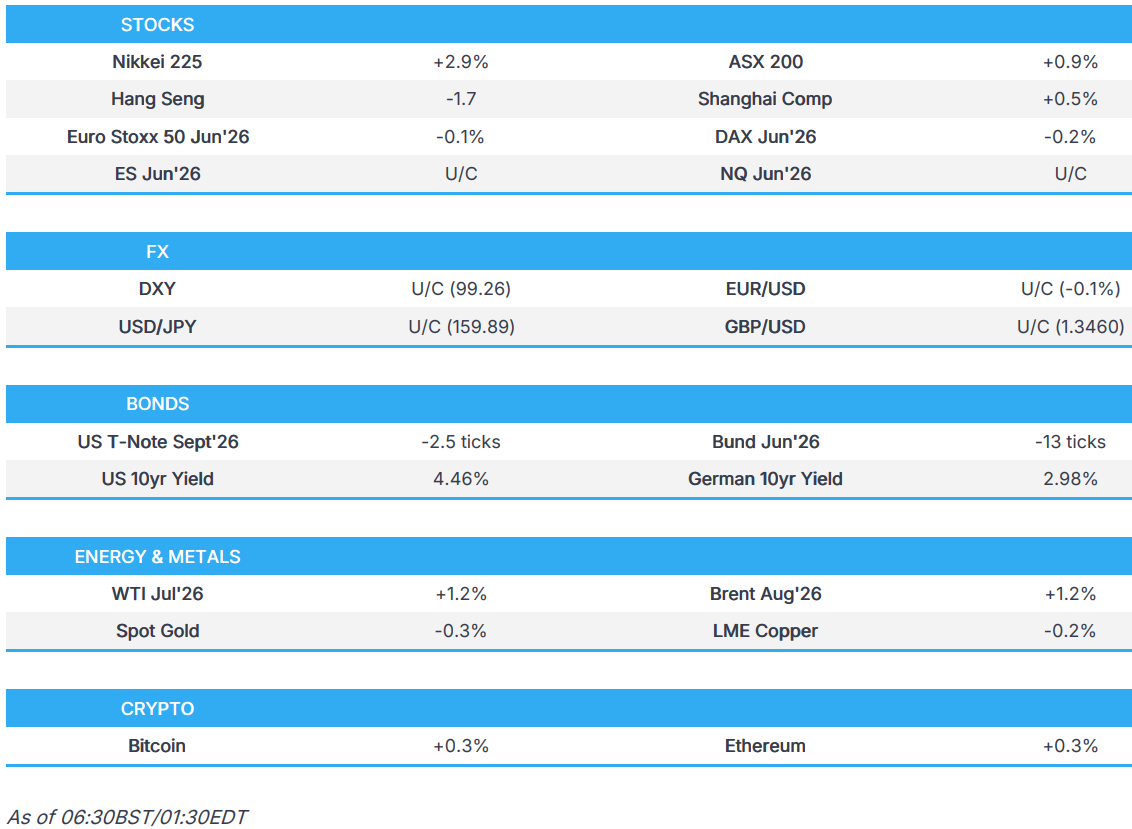

Market Snapshot

Top Overnight News

- Iran launched missiles at Kuwait — where one person was killed, according to the country’s foreign ministry — and Bahrain, as the US conducted new strikes on Qeshm Island. These came after the US military said it struck an oil tanker heading for an Iranian port. President Donald Trump has ruled out the prospect of “boots on the ground now.” CNN

- Trump said he swore at Benjamin Netanyahu in a call this week as the president tried to deescalate fighting in Lebanon and keep peace talks with Iran on track. The president also said in an interview on the Pod Force One podcast that Iran has agreed it won’t have a nuclear weapon. BBG

- Donald Trump is moving to rebuild his tariff wall, with the US proposing duties of at least 10% on imports from major trading partners including the EU, Canada and Mexico following a forced-labor probe. Products from China, Japan, Brazil and several other economies would face a higher 12.5% rate. BBG

- Even as the piles of capital secured have grown ever larger, the ability to deploy it in the artificial intelligence race has become less certain. Supply-chain backlogs, permitting fights and availability of power supplies are among the issues that have caused the construction of data centers to fall behind targeted timelines, with the gap growing wider in recent months. WSJ

- Nvidia’s Jensen Huang outlined the “insane” returns offered by AI during an address to wealthy family offices that sought to dispel lingering concerns around the big spending that’s accompanied the boom. BBG

- US Acting Attorney General Blanche confirmed the Trump administration is not moving forward with the weaponisation fund.

- US Senate Democrats are reportedly privately urging GOP leaders to pressure President Trump to withdraw his appointment of Pulte as acting director of national intelligence, threatening to tank a bipartisan FISA deal if Trump refuses: Punchbowl

- Federal Reserve Chairman Kevin Warsh has tapped two outside associates (Paul Winfree and Daniel Heil) to advise him while he settles into the job, one of whom previously helped write a conservative blueprint that recommended a radical restructuring of the central bank. WSJ

- Federal Reserve watchers expect Kevin Warsh to begin revamping the central bank’s rate guidance as soon as this month, as the newly appointed chair embarks on a sweeping overhaul of the institution. Several former top officials said that they expected Warsh, whom President Donald Trump swore in to succeed Jay Powell as Fed chair in May, to begin rolling back the central bank’s “forward guidance” on interest rates as soon as the mid-June Federal Open Market Committee meeting. FT

- China’s services activity jumped in May, according to a private survey, a positive sign amid still weak consumer sentiment as price shocks from the conflict in the Middle East ripple through economies. The RatingDog China services purchasing managers’ index rose to 54.4 from 52.6 in April. BBG

- India is considering tax cuts for foreign bond investors to attract more overseas capital, people familiar said. The cabinet is expected to today weigh a significant reduction in taxes paid by global funds on Indian debt, including eliminating or cutting the current 20% levy on interest income. BBG

Iran War News

- Explosions were heard near Qeshm Island in Iran on Wednesday morning.

- Kuwait’s Army announced its air defences were intercepting hostile missile and drone attacks, while reports noted that two US bases were targeted in Kuwait, with explosions in the Ali al-Salem and Arifjan bases where US soldiers are stationed. Furthermore, air raid sirens sounded in the UAE and Saudi Arabia, with explosions also reported in Saudi Arabia, while explosions were heard in Qamishli, Syria, and earlier reports noted multiple explosions in the centre of Iraqi Kurdistan with the headquarters of anti-Iranian separatist groups targeted.

- IRGC said the US attacked Qeshm Island, and in response, Iran carried out precise and intensive missile strikes on US bases in Kuwait, while it warned further US aggression will be met with a seismic, crushing and decisive response.

- IRGC said the headquarters of the US 5th Fleet in Bahrain was attacked by missiles and drones from the IRGC Aerospace Force, while it targeted a US-affiliated vessel named Panaya with missiles and clarified the recent attack was in retaliation for the US targeting an IRGC communications tower in the south of Qeshm Island.

- US CENTCOM said Iran launched several ballistic missiles towards neighbours and that forces successfully defeated multiple Iranian missiles, while US forces had conducted strikes on Qeshm Island in response to attempted attacks by Iran. CENTCOM stated that forces shot down three one-way attack drones launched by Iran toward civilian mariners that were rightfully transiting regional waters, and US forces also conducted self-defence strikes on an Iranian military ground control station on Qeshm Island. Furthermore, it denied IRGC claims that Iran struck the 5th Fleet HQ in Bahrain and a US airbase in the region, and stated that all Iranian attacks on US forces failed.

- US CENTCOM says forces disabled a Botswana-flagged unladen oil tanker that was attempting to sail toward an Iranian port on the Arabian Gulf on June 2nd. Says: US aircraft disabled the vessel by firing a Hellfire missile into the ship’s engine room, preventing the tanker from reaching Iran.

- US President Trump is pushing Iran to make firmer nuclear commitments and wants nuclear concessions in writing from Iran, according to ABC News.

- US Secretary of State Rubio said that Iran has mined large segments of the Hormuz Strait. Rubio stated that nuclear negotiations with Iran were highly complicated and technical, which would therefore take time, while he added that the war with Iran had made interactions with Tehran more complicated, but also commented that the “war in Iran is over”.

- Iran’s Foreign Ministry condemned the US attacks on Iranian tanker and Qeshm island. The Foreign Ministry “notes the direct and clear responsibility of the rulers of Kuwait and Bahrain for last night’s aggressive acts.”

- Hardline Iranian lawmaker called for stronger military response to US strikes, Al Jazeera reported.

- Kuwait’s General Civil Aviation Authority said an emergency plan at Kuwait International Airport was activated after Terminal 1 was targeted by Iranian drones and missiles.

- Hezbollah attacked an Israeli command post in southern Lebanon with a drone strike, which wounded eight Israeli soldiers, according to SNN.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly gained as the region took its cue from Wall St, where the S&P 500, Dow and Nasdaq 100 printed fresh record highs, which has helped regional bourses shrug off the geopolitical escalation, in which the US struck Qeshm Island, and Iran targeted US bases in neighbouring countries. ASX 200 was led by outperformance in materials, mining and resources sectors, but with gains capped as tech, telecoms and defensives lagged, while participants also digested weaker-than-expected GDP data. Nikkei 225 took inspiration from US peers and printed a fresh all-time high after climbing above 68,000 for the first time. Hang Seng and Shanghai Comp were mixed, with the Hong Kong benchmark dragged lower by profit-taking following recent earnings and mixed fortunes among the key tech stocks, while the mainland found support from the better-than-expected Chinese RatingDog Services PMI data.

Top Asian News

- Japanese PM Takaichi said FX policy is important to support the economy and trades including speculation have a big impact on markets. She further stated that they are prepared to take appropriate measures in the FX market at any time if needed while deepening international cooperation, including with the US, on FX.

- Japanese Finance Minister Katayama said they are prepared to respond appropriately on forex as needed, while she won’t comment on specific FX levels.

European bourses (STOXX 600 -0.4%) start Wednesday’s session with modest losses due to the introduction of new levies on US imports related to its 301 investigations. A 10% tariff has been applied to imports from Canada, Mexico, the EU, Taiwan and the UK, while some countries, including China and Japan, have received a higher 12.5% levy. European sectors highlight a negative bias. Financial Services (-1.7%) and Autos (-1.6%) are the laggards, with Chemicals (-1.1%) rounding out the bottom three. At the top end lies Retail (+1.8%), the sole sector printing decent gains, helped by gains in Inditex (+3.9%) after the Co. reported Q1 earnings that came in line with expectations, while sales in May rose 11.5%.

Top European News

- UK S&P Global Composite PMI Final (May) 49.7 vs. Exp. 48.5 (Prev. 52.6).

- UK S&P Global Services PMI Final (May) 49.3 vs. Exp. 47.9 (Prev. 52.7).

- EU S&P Global Composite PMI Final (May) 48.5 vs. Exp. 47.5 (Prev. 48.8).

- EU S&P Global Services PMI Final (May) 47.7 vs. Exp. 46.4 (Prev. 47.6).

- German S&P Global Composite PMI Final (May) 48.8 vs. Exp. 48.6 (Prev. 48.4).

- German S&P Global Services PMI Final (May) 48.1 vs. Exp. 47.8 (Prev. 46.9).

- French S&P Global Composite PMI Final (May) 44.9 vs. Exp. 43.5 (Prev. 47.6).

- French S&P Global Services PMI Final (May) 44.3 vs. Exp. 42.9 (Prev. 46.5).

- Italian S&P Global Composite PMI (May) 50.4 (Prev. 50.5).

- Italian S&P Global Services PMI (May) 49.4 vs. Exp. 49.1 (Prev. 49.8).

- Spanish S&P Global Composite PMI (May) 50.2 (Prev. 48.7).

- Spanish S&P Global Services PMI (May) 50.1 vs. Exp. 48.

FX

- G10s are mostly lower against the Buck (DXY +0.1%) as flare-ups continue in the Middle East. Since the close on Tuesday, the US struck Iran’s Qeshm Island, which was then met with retaliatory Iranian strikes on US bases in Kuwait, and explosions were also reported in Saudi Arabia, and air sirens were set off in the UAE.

- The Dollar crept higher overnight in tandem with oil/yields, and now looks towards the 99.40 mark in DXY (session high 99.40). Tuesday saw firm JOLTS jobs data which rose to the highest level since May 2024. Today sees the release of ADP’s monthly employment figure, expected to rise to 110/120k depending on which consensus you look at.

- JPY is the best G10 performer after sharp strength seen among comments from Japanese PM Takaichi and BoJ Governor Ueda. At around 08:30 BST, Japanese PM Takaichi said: “prepared to take appropriate measures in the FX market”. USD/JPY moved sharply lower from 159.91 to a trough of 159.55 within three minutes. The move pared around 20 pips, then around an hour later, comments from BoJ Governor Ueda resumed Yen strength. Ueda said the “BoJ’s basic stance is to continue raising the policy rate”, helping the pair mark a fresh session low of 159.36, though ultimately proving fleeting and returning to pre-Ueda levels. USD/JPY -0.1% at 159.80, a moving target at the time of writing.

- Antipodeans are the worst G10 performers. Aussie fares a little better than the Bird despite soft growth data overnight, which contracted at a faster rate than anticipated on a quarterly basis. AUD/USD (-0.3%) immediately fell around 8 pips, pared the move, then resumed lower as the Buck picked up. AUD/NZD +0.3%.

Fixed Income

- Global fixed benchmarks are broadly lower as the complex takes leads from the strength in energy prices, after yet another US-Iran flare-up. In brief, the US struck Iran’s Qeshm Island, which was then met with retaliatory Iranian strikes on US bases in Kuwait; explosions were also reported in Saudi Arabia, and air sirens were set off in the UAE.

- USTs (-5+ ticks) are lower this morning and trade at the lower end of a 109-15+ to 109-24+ range. And unsurprisingly, yields are firmer across the curve, with mild outperformance in the short end. Much of the action recently has been dictated by geopolitical developments, but attention this week will turn back to domestic data. Thus far, ISM Manufacturing topped expectations, whilst Prices Paid slipped from the prior (though still remains elevated); on the jobs front, JOLTS Job Openings topped expectations. Both are factors which play into the hands of the hawkish members at the Fed. Attention today now shifts to ADP, ISM Services and then the NFP report to end the week.