JUNE 18/ANOTHER RAID: GOLD CLOSED DOWN $135.20 TO $4225.95//SILVER CLOSED DOWN $4.80 TO $66.00//PLATINUM CLOSED DOWN $90.40 TO $1705.50 WITH PALADIUM DOWN $70.60 TO $1290.00//COMMODITY REPORT TONIGHT ON RARE EARTHS//EUROPEAN REPORTS FROM THE ECB POLAND AND GERMANY//ISRAEL/USA VS IRAN UPDATES/ISRAEL TBN/./HEZBOLLAH VS ISRAEL UPDATES//COMMENTARIES TONIGHT FROM MIKE EVERY AND PHIL MAREY/TRUE ORIGINS OF THE COVID VIRUS EXPLAINED//USA DATA RELEASES/USA ECONOMIC REPORTS// KING NEWS//

099 H DEUTSCHE BANK AG 4 152 C DORMAN TRADING, LLC 5 363 H WELLS FARGO SECURITI 42 435 H SCOTIA CAPITAL (USA) 467 555 C BNP PARIBAS SEC CORP 2 661 C JP MORGAN SECURITIES 825 566 709 C BARCLAYS 208 737 C ADVANTAGE FUTURES 101 3 905 C ADM 29 991 H CME 16

TOTAL: 1,134 1,134 MONTH TO DATE: 36,590

JPMORGAN STOPPED: 566/1134

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2026: 1134 CONTRACTs NOTICES FOR 113,400 OZ or 3.527 TONNES

total notices so far: 36,590 contracts FOR 3,659,000 OZ OR 113.810 TONNES

JUNE 18

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 12 NOTICE(S) FILED FOR 60,000 OZ /

total number of notices filed so far this month : 2407 CONTRACTS (NOTICES) for 12.035 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $135.20 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/// HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.856 TONNES INTO THE GLD

INVENTORY RESTS AT 1013.069 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $4.80 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: HUGE CHANGES IN SILV INVENTORY A WITHDRAWAL OF 1.086 MILLION OZ FROM THE SLV////// : INVENTORY RESTS AT THE SLV AT 480.302 MILLION OZ//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 480.302 MILLION

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 280 CONTRACTS TO AN OI OF 108.001 A LOT HIGHER FROM ITS NEW RECORD LOW OF 95,999 SET MAY 1/2026. THE RECORD HIGH OI FOR SILVER IS 244,710, SET FEB 25/2020, AND THIS FAIR GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.79 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. ON THE FIRST OF MAY, WE REACHED OUR RECORD LOW OI OF 95,999 SURPASSING EVERY DAY NEW OI LOWS SET DURING THE LAST WEEK OF APRIL 2026.

NOW ON A NET BASIS OUR SPECULATORS HAVE REVERTED BACK TO GOING LONG. THE FRBNY ON A NET BASIS IS PROVIDING THE NECESSARY PAPER TO OUR LONGS ALONG WITH SOME BULLION BANKS AND THEN A HUGE NUMBERS OF LONGS ,OUR CENTRAL BANKERS, TAKE THE LONG SIDE AND TENDER FOR PHYSICAL AT 4 PM EACH NIGHT. BECAUSE OF THE HUGE SHORTFALL IN PHYSICAL SILVER IN LONDON THERE IS A LOTTERY TO SEE WHO GETS ANY OF THE PHYSICAL SILVER AVAILABLE THAT WHICH THEY ARE OBLIGATED TO DELIVER. THEY WAIT PATIENTLY FOR THEIR PHYSICAL METAL AND IF NOBODY GETS ANY THEY THEN COME BACK THE NEXT DAY AND SO ON. THIS IS IN LONDON, THE HOME OF PHYSICAL SILVER!! THE FACT THAT WE ARE WITNESSING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON HIGHLIGHTS THE FACT THAT THE COMEX IS OUT OF SILVER AS WELL.

WE ARE FINALLY MOVING TO A MUCH HIGHER BASE IN SILVER PRICING AT MAJOR SUPPORT LEVEL OF $70.00. SHORTLY WE WILL AGAIN ATTEMPT TO BREAK

WE HAVE A STRONG GAIN OF 940 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A VERY STRONG SIZED SIZED 660 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE , WE HAD NO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO WEDNESDAY TRADING// WE HAD A STRONG SIZED 454 CONTRACT T.A.S. ISSUANCE!! / THEY DESPERATELY AGAIN TODAY TRYING TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $100.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON TUESDAY WITH SILVER’S FALL IN PRICE

THE PRICE STILL FINISHED BELOW THE MAGIC NUMBER OF $70.00 SILVER SPOT PRICE BUT STILL BELOW THE $100.00 MARK CLOSING AT $71.84 UP $0.79. WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS A STRONG SIZED 454 T.A.S. CONTRACTS !!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING ABOVE THE 100.00 DOLLAR MARK!! AND NOW THE HUGE SUPPORT LEVEL OF 70 DOLLARS HAS NOW SUPPORT LEVEL//.MAMMOTH SIZE T.A.S ISSUANCES ARE BECOMING THE NORM AT THE COMEX NOW!!

THERE IS NO NEXT LINE IN THE SAND ONCE THE 100.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A ZERO SIZED 0 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG SIZED 454 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE.

IN ESSENCE WE HAD A HUGE SIZED GAIN OF 940 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.79. WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION WILL BE REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE STICKY SPECULATOR LONGS STILL REMAIN STOIC

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE.

THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, THROUGHOUT MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A STRONG SIZED 456 CONTRACTS. DESPITE MANY COMPLAINTS THAT THESE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS).

THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS AS ONE UNIT, BUT SELL THE SHORT SIDE FIRST AND THEN LIQUIDATE THE LONG SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF XX CONTRACTS OR XXX OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 40,000 OZ//NEW STANDING ADVANCES TO 12.065 MILLION OZ//

SUMMARY OF OUR JUNE 2026 COMEX CONTRACT MONTH:

WE HAD:

/ TINY COMEX GAIN+// HUGE SIZED EFP ISSUANCE CONTRACTS AT 660 CONTRACTS (/ VI) A STRONG NUMBER OF T.A.S. CONTRACT ISSUANCE 454 CONTRACTS

xx I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED 221 SILVER CONTRACT//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE.. ACCUMULATION

TOTAL CONTRACTS for 14 DAY(S), total 7680 contracts: OR 38.400 MILLION OZ (548 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 38.400 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE. 38.400 MILION OZ

RESULT: WE HAD A SMALL INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 280 CONTRACTS WITH OUR GAIN IN PRICE OF $0.79 IN SILVER PRICING AT THE COMEX// WEDNESDAY,. THE CME NOTIFIED US THAT WE HAD A 454 STRONG SIZED CONTRACT EFP ISSUANCE OF 454 CONTRACTS ISSUED FOR JULY, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS).

INITIAL STANDING: 10.935 MILLION OZ PLUS 40,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 12.065 MILLION OZ

LAST 14 MONTHS OF SILVER DELIVERIES

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 40,000 OZ//NEW STANDING ADVANCES TO: 12.065 MILLION OZ

THE NEW TAS ISSUANCE FOR TODAY (454) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!

WE HAD 12 NOTICE(S) FILED TODAY FOR 60,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY BANKERS

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1385 OI CONTRACTS UP TO 337,945 OI AND THIS OI STILL SURPASSES BY A CONSIDERABLE MARGIN THE ALL TIME LOW AT 326,052 SET JUNE3/2026 AND THIS OI IS MUCH FURTHER FROM THE RECORD HIGH (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE HAVE NOW ADVANCED PAST THE PREVIOUS ALL TIME LOWS OF 357,136 SET APRIL 2/.2026AND 354,581 SET AT THE END OF APRIL 2026. WE ARE STILL QUITE A WAY FROM OUR TWO DECADES OLD: 390,000 CONTRACTS LOW SET IN THE YEAR OF 2001 WITH TRADING FOR GOLD AT $260.00. THUS DURING EARLY APRIL WE HAD AN ALL TIME LOW OI IN COMEX (354,531) BUT WITH AN EXTREMELY HIGH PRICE OF GOLD. IN MAY: RECORD LOW OI OF 326,052 WITH A GOLD PRICE OF $4,460 THE SHORT RATS ARE ABANDONING THE COMEX SHIP, NOBODY WANT TO PLAY IN THIS CROOKED CASINO!! (AND THIS CORRELATES WITH SILVER’S LOW OI OF 107,471 CONTRACTS WITH A MUCH HIGHER SILVER PRICE BASE//$75.00)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1705 CONTRACTS //.

WE HAD A FAIR LOSS IN COMEX OI (1385 CONTRACTS) . THIS LOSS IN OI OCCURRED WITH OUR GAIN IN PRICE OF $26.80 //,WEDNESDAY///.

LAST 13 MONTHS OF GOLD DELIVERIES: (MAY 2025 THROUGH TO /MAY 2026)

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT 3.486 TONNES OF A QUEUE JUMP/NEW STANDING ADVANCES TO 113.916 TONNES

E.F.P. ISSUANCE/FOR OPENING JUNE. GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3025 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 337,945 SURPASSING THE PREVIOUS ALL TIME LOW OF 326,052 SET JUNE 3 AND RISING FROM OUR PREVIOUS RECORD LOW//MAY 28.2026 WE HAVE THUS RECORD LOW COMEX OI WITH A HIGH PRICE OF GOLD

SILVER ALSO HAS AN ULTRA SMALL SIZED AND EXTREMELY LOW COMEX OI OF 108.001 CONTRACTS// RISING FROM PREVIOUS ALL TIME LOWS SET DURING THE MONTH OF APRIL AND MAY FIRST.

IN ESSENCE WE HAVE A FAIR GAIN IN TOTAL CONTRACTS IN COMEX GOLD ON THE TWO EXCHANGES OF 1640 CONTRACTS WITH 1385 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 3025 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON.

THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1640 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALLER SIZED BUT CRIMINAL 777 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON

GOLD PRICE ON TUESDAY ROSE BY $28/60

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT (3025 ) ACCOMPANYING THE FAIR LOSS IN COMEX OI OF 1385 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES 1640 CONTRACTS!! WITH THE GAIN IN PRICE.

WE HAVE 1) NOW REVERTED TO OUR FORMAT OF BANKER (FRBNY) GOING ON THE SHORT SIDE AND HUGE NUMBERS OF NEWBIE SPECULATORS GOING TO THE LONG SIDE. IT WAS OUR SHORT SPECULATORS THAT WE BRUTALIZED LAST THURSDAY WHEN OUR CENTRAL BANKS TENDERED FOR PHYSICAL GOLD WITH THEIR NEWLY BOUGHT GOLD FROM THE SPECS. THE SPECS ARE STILL SCRAMBLING LOOKING FOR PHYSICAL GOLD TO DELIVER TO OUR LONG CENTRAL BANKS.

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 3/486TONNES//NEW STANDING ADVANCES TO 113.916 TONNES

3) LITTLE IF ANY T.A.S. LIQUIDATION IN THE COMEX SESSION AND SOME GOVT LIQUIDATION // WITH A STRONG LOSS OF EQUITY SHARES/JUNE17 HAVING 1)A $28.60 COMEX PRICE GAIN AND WE HAD 2) SPEC PILING HUGELY ON THE LONG SIDE// +3. EASTERN CENTRAL BANKERS ALSO PILING INTO THE LONG SIDE. WE HAD A FAIR GAIN OF 1640 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A STRONG AMOUNT OF GOLD WILL STAND FOR DELIVERY IN JUNE. (113.916 TONNES). THE SHORT SPECS BAILED ON THURSDAY AND FRIDAY//, CENTRAL BANKERS TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4)A FAIR SIZED COMEX OI LOSS 5) V) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD(3025) AND 6. A SMALL T.A.S. ISSUANCE (777) FOR RAID PURPOSES.!!!

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 29,632 CONTRACTS OR 2,963,200 OZ OR 92.167 TONNES IN 14 TRADING DAY(S) AND THUS AVERAGING: 2116 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN14 TRADING DAY(S) IN TONNES: 92.167 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2025, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 92.167 TONNES DIVIDED BY 3550 x 100% TONNES = 2.59% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2023 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2024: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES

2025: AND NOW 2026

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 92.167 TONNES

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SOIS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A FAIR 280 CONTRACTS TO AN OI OF 108,001.

EFP ISSUANCE 660 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 660 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 280 CONTRACTS AND ADD TO THE 660 E.FP. ISSUED

WE OBTAIN A HUGE GAIN OF940 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $0.79

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.700 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.79

2.ASIAN AFFAIRS JUNE 18 /2025

SHANGHAI CLOSED DOWN 17.59 PTS OR 0.43%

HANG SENG CLOSED DOWN 387.35 PTS OR 1.59%

Nikkei CLOSED UP 1,223.75 PTS OR 1.78%

//Australia’s all ordinaries CLOSED DOWN 0.19%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7698

/ OFFSHORE CLOSED DOWN AT 6.7738 Oil UP TO 75.39 dollars per barrel for WTI and BRENT DOWN TO 78.80Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7698) OFFSHORE YUAN TRADING DOWN TO 6.7738 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR 1285 CONTRACTS TO 337,945 STILL ABOVE ITS NEW LOW OF 326,052 OI SET JUNE 3, SURPASSING THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,052 //JUNE 3 2026 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD NO T.A.S. LIQUIDATION DURING WEDNESDAY’S COMEX TRADING JUNE 17!!. IT SEEMS THAT MANY OF THE SPECULATORS HAVE NOW CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT WITH THE BANKERS NOW PROVIDING THE PAPER,AND CENTRAL BANKS DOING THEIR QUEUE JUMPING IN AN INCREASING MANNER

CENTRAL BANKS TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS JUNE CONTRACT MONTH!!

THE FAIR SIZED GAIN ON OUR TWO EXCHANGES (1640 CONTRACTS) OCCURRED WITH OUR GAIN IN PRICE IN GOLD (UP $26.80)

WE THUS HAD A FAIR SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1640 CONTRACTS (OR 5.01 TONNES) WITH OUR GAIN IN PRICE, AS WE WERE INFORMED OF A STRONG CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 3025 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIDAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH JUNE

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

JUNE: 0 SO FAR!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO JUNE:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 146+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO SO FAR

DETAILS ON OUR NEW JUNE COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR GAIN ON OUR TWO EXCHANGES OF 1640 CONTRACTS WITH OUR GAIN IN PRICE($26.80). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A FAIR SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 777 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

JUNE: ZERO SO FAR.

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 146+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO. WE WILL KNOW IN JUNE WHETHER THEY COVERED ANY OF THEIR SHORTFALL.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 3.486 TONNES//NEW STANDING ADVANCES TO 113.916 TONNES// TOTAL QUEUE JUMPING FOR THE MONTH; 49.291 TONNES OR AVERAGING 3.520 TONNES PER DAY IN JUNE.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JUNE,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $26.80)

WE HAD NO T.A.S. SPREADER LIQUIDATION WEDNESDAY // COMEX SESSION//(BUT SOME AFTER FOMC ANNOUNCMENT) WITH OUR GAIN IN PRICE , OUR LONG SPECULATORS STILL REMAIN RELENTLESS POURING INTO THE COMEX

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $26.80

WE HAD 1705 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES: 1640 CONTRACTS OR 164,000 OZ (5/01 TONNES)

Total monthly oz gold served (contracts) so far this month

36,590 notices 3,659,000 oz 113.810 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

ENTRIES: 1

Into Manfra: 63,499.109 oz

total deposit: 63,499.109 oz

xxxxxxxxxxxxxxxxxx

comex withdrawal

1 ENTRIES

1 ENTRIES

i) Loomis: 643.02 oz (20 kilobars)

total withdrawal 643.02 oz

adjustments: 4// dealer to customer

a) Brinks 90,609.516 oz

b) JPMorgan; 14,467.908 oz

c) Loomis: 4,203.200 oz

d) Manfra: 38,980.172 oz

total dealer to customer 148,260.856 oz

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JUNE OI STANDS AT 1168 CONTRACTS HAVING A GAIN OF 1028 CONTRACTS.

WE HAD 93 CONTRACTS SERVED ON WEDNESDAY, SO WE GAINED 1121 CONTRACTS OR 112,100 OZ. (3.486 TONNES) EXERCISED A QUEUE JUMP WHERE THEY WILL TAKE PHYSICAL GOLD ON THIS SIDE OF THE POND. THIS IS NO DOUBT CENTRAL BANKS STANDING FOR PHYSICAL GOLD.

JULY GAINED 683 CONTRACTS UP TO 5312 CONTRACTS.

AUGUST DOWN 3744 CONTRACTS TO AN OI OF 259,941

.

We had 1134 contracts filed for today representing 113,00oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 825 notices issued from their client or customer account. The total of all issuance by all participants equate to 1134 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 566 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (36,590) to which we add the difference between the open interest for the front month of JUNE(1168 CONTRACTS) minus the number of notices served upon today 1134 x 100 oz per contract) equals 3,662,400 OZ OR (113.916 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (36,590) to which we add the difference between the open interest for the front month of JUNE( 1168 CONTRACTS) minus the number of notices served upon today 1134 x 100 oz per contract) equals 3,550,300 OZ OR (113.916Tonnes of gold)

new total of gold standing in JUNE becomes 113.916 TONNES//

TOTAL COMEX GOLD STANDING FOR JUNE 113.916 TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS ACTIVE DELIVERY MONTH OF JUNE.

confirmed volume WEDNESDAY confirmed 99,679// poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,692,905.420 oz 52.656 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,692,905.420 tonnes oz 52.656 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 27,998,768.924oz

TOTAL REGISTERED GOLD 15,081,102.583 tonnes (469.085 tonnes)

TOTAL OF ALL ELIGIBLE GOLD 12,917,866.251 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,388,197oz ((REG GOLD- PLEDGED GOLD)=

416.429 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JUNE DELIVERY MONTH

JUNE 18

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1 entries

Out of:

a) Manfra: 320,110.517 oz

total withdrawal: 320,110.517 oz

Deposits to the Dealer Inventory

0 entries

Deposits to the Customer Inventory

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ONE ENTRY

ONE ENTRY

i)Into Asahi: 602,433.300 oz total deposit: 602,433.300 oz oz

No of oz served today (contracts)

12 CONTRACT(S) (60,000 OZ)

No of oz to be served (notices)

6 Contract (30,000 oz)

Total monthly oz silver served (contracts)

2407 contracts 12.035 MILLION oz

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRIES

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRY:1

ONE ENTRY

i)Into Asahi: 602,433.300 oz

total deposit: 602,433.300 oz oz

total deposit 605,069.076 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

Out of:

a) Manfra: 320,110.517 oz

total withdrawal: 320,110.517 oz

adjustments 2

i) dealer to customer: CNT 77,547.650 oz

ii) customer to dealer Manfra: 05,431.718 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 86.246 MILLION OZ//.TOTAL REG + ELIGIBLE. 321.345 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE /2026 OI: 18 OPEN INTEREST CONTRACTS FOR A GAIN OF 6 CONTRACTS.

WE HAD 2 NOTICES SERVED ON WEDNESDAY SO WE GAINED 8 CONTRACTS OR AN ADDITIONAL 40,000 OZ WILL STAND AS A QUEUE JUMP AT THE SILVER COMEX.

JULY SAW A LOSS OF 2698 CONTRACTS DOWN TO 40,601 CONTRACTS.

AUGUST SAW A GAIN 0F 31 CONTRACTS UP TO 969…

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 12 or 60,000 OZ oz

CONFIRMED volume WEDNESDAY; 47,817// fair

XXX

AND NOW JUNE. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 2407 X5,000 oz = 12.035 MILLION oz

to which we add the difference between the open interest for the front month of JUNE(18) AND the number of notices served upon today (12 )x (5000 oz)

Thus the standings for silver for the JUNE 2026 contract month: (2407 )Notices served so far) x 5000 oz + OI for the front month of JUNE ( 18) minus number of notices served upon today (12)x 5000 oz equals silver standing for the JUNE..contract month equating to 12.065 MILLION OZ.+

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 86.246 million oz of registered silver

JPMorgan as a percentage of total silver: 138.474/321.315 million: 43.30%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JUNE 18 /2026/WITH GOLD DOWN $135.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.856 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1013.069 TONNES

JUNE 17 /2026/WITH GOLD UP $20.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.427 TONNES OF GOLD FROM THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1012.213 TONNES

JUNE 16 /2026/WITH GOLD UP $4.45 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 15 /2026/WITH GOLD UP $111.10 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 12 /2026/WITH GOLD UP $123.30 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 11 /2026/WITH GOLD DOWN $15.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.855 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 10 /2026/WITH GOLD DOWN $153.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.426 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1016.495 TONNES

JUNE 9 /2026/WITH GOLD DOWN $75.60 TODAY/NO CHANGES IN GOLD AT THE GLD:// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 8 /2026/WITH GOLD DOWN $3.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 6.936 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 5 /2026/WITH GOLD DOWN $134;85 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 4 /2026/WITH GOLD UP $39.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.143 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 3 /2026/WITH GOLD DOWN $51.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.856 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.000 TONNES

JUNE 2 /2026/WITH GOLD UP $7.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.712 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.856 TONNES

JUNE 1 /2026/WITH GOLD DOWN $79.30 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 29 /2026/WITH GOLD UP $59.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

GLD INVENTORY: 1013.069 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JUNE 18 WITH SILVER DOWN $4.80: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: HUGE CHANGES IN INVENTORY A WITHDRAWAL OF 1.086 MILLION OZ FROM THE SLV././ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 17 WITH SILVER UP $0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: NO CHANGE IN INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 16 WITH SILVER DOWN $0.13: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.362 MILLION OZ INTO THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 15 WITH SILVER UP $3.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.357 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 481.026 MILLION OZ

JUNE 12 WITH SILVER UP $3.34: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.769 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 482.383 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.12: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.226 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.152 MILLION OZ

JUNE 10 WITH SILVER DOWN $0.50: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.909 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.378 MILLION OZ

JUNE 9 WITH SILVER DOWN $3.35: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.407 MILLION OZ INTO INTO THE SLV /./ // :INVENTORY RESTS AT 484.287 MILLION OZ

JUNE 8 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 543,000 OZ FROM THE SLV /./ // :INVENTORY RESTS AT 482.880 MILLION OZ

JUNE 5 WITH SILVER DOWN $4.86: NO CHANGES IN SILVER INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 4 WITH SILVER UP $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.432 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 3 WITH SILVER DOWN $2.55: NO CHANGES IN SILVER INVENTORY AT THE SLV >> /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

CLOSING INVENTORY 480.802 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD.

3. CHRIS POWELL AND HIS GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT; 277

LAST WEEK 276

5. COMMODITY REPORT//ALUMINIUM/rare earths

Rare Earth Stocks Pop After G7 Unveils Plan To Reduce Dependence On China For Critical Minerals

Wednesday, Jun 17, 2026 – 06:00 PM

Rare earth stocks spiked on Wednesday after G7 leaders agreed to strengthen coordination on critical minerals as they seek to reduce dependence on China-dominated supply chains, according to a new report from Reuters.

Without naming China directly, the group set a goal of limiting reliance on any single external supplier of rare earths and permanent magnets to less than 60% by 2030, with a longer-term target of 50%.

Reuters reports that to support that effort, the G7 plans to align critical mineral stockpiling strategies, beginning with lithium and nickel, and establish a new platform for policy coordination, data sharing, market monitoring, and crisis response. The platform will work closely with the International Energy Agency, which will provide analysis and early warnings of supply disruptions and market distortions.

The group also pledged to support investment across the entire critical minerals supply chain—from mining and processing to manufacturing—through development finance institutions, export credit agencies, and private-sector partnerships. Since the start of 2026, governments have announced 195 related projects totaling €64 billion ($74 billion) in investment.

Neha Mukherjee, research manager at consultancy Benchmark Mineral Intelligence commented: “The G7 statement is an important signal of intent, but the pace of diversification will ultimately depend on whether policy support translates into investment across the midstream and downstream parts of the value chain.”

Despite the commitments, analysts note that diversification will be difficult, particularly because China controls about 90% of global processed rare earth and permanent magnet production. The G7 is also exploring measures such as joint procurement, subsidies, quotas, and price-support mechanisms, while expanding domestic stockpiles and increasing recycling capacity to make recycled materials a significant share of critical mineral consumption by 2030.

END

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 17.59 PTS OR 0.43%

HANG SENG CLOSED DOWN 387.35 PTS OR 1.59%

Nikkei CLOSED UP 1,223.75 PTS OR 1.78%

//Australia’s all ordinaries CLOSED DOWN 0.19%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7698

/ OFFSHORE CLOSED DOWN AT 6.7738 Oil UP TO 75.39 dollars per barrel for WTI and BRENT DOWN TO 78.80Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7698) OFFSHORE YUAN TRADING DOWN TO 6.7738 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7698

OFFSHORE YUAN: DOWN TO 6.7738

1.HANG SANG CLOSED DOWN 387.35 PTS OR 1.59%

2. Nikkei closed UP 1223.75 PTS OR 1.78%

WEST TEXAS INTERMEDIATE OIL UP TO 75.39

BRENT; 78.80

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 100.50/// EURO FALLS TO 1.1404 DOWN 43 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.616 UP 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA CROSS NOW AT 160.890… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.767 UP 2 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN( 6.7693 AND OFFSHORE: DOWN AT 6.7738

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.9422// Italian 10 Yr bond yield UP to 3.656// SPAIN 10 YR BOND YIELD UP TO 3.367%

3i Greek 10 year bond yield UP TO 3.604%

3j Gold at $4250.65 //Silver at: 67.56 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 61/ 100 roubles/73.51

3m oil (WTI) into the 75 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 160.89 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.616% UP 2 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.769 UP 2 PTS..: USA/SF this 0.8036 as the Swiss Franc . Euro vs SF: 0.9213

USA 10 YR BOND YIELD: 4.454 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.875 DOWN 5 BASIS PTS/

USA 2 YR BOND YIELD: 4.198 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 46.45 UP 13 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.7840 UP 3 PTS

30 YR UK BOND YIELD: 5.4780 UP 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.411 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.092 UP 8 BASIS PTS.

1a New York Opening report

Futures Rise, Oil Drops As Market Prices In Iran Deal For Yet Another Day

Thursday, Jun 18, 2026 – 08:28 AM

Futures rebounded from the post-FOMC selloff, and oil prices fell as Trump signed the Iran MOU two days early to end the war in the Middle East (in the symbolic Palace of Versailles of all place) and some energy shipments began to transit the Strait of Hormuz. As usual, tech led the parade higher. As of 8:00am ET, S&P futures were up 0.6%, but off overnight session highs, partly unwinding a more than 1% decline after Kevin Warsh signaled the Fed may have to raise interest rates this year to contain inflation; Nasdaq gained 1.3%; pre-market all Mag 7 are higher led by AMZN (+1.2%), META (+1.1%) and NVDA (+1.1%), reversing some of yesterday’s losses. Intel shares jumped more than 8% in premarket trading after Trump said the firm struck a chipmaking deal with Apple (a rehash of previous news but to this Pavolvian market, everything seems to be brand new). Overnight, the biggest headline was that the US/Iran MOU was officially in effect (final deal within 60 days, waiver for Iran to export oil, a $300bn reconstruction fund, terminating all types of sanction, per Axios). Bond yields are lower led by the long-end of the curve as 2y is still anchored by Fed commentary yesterday; 2y and 10y are -1bp and -4bp lower, respectively, the 10Y trading at 4.46%. The USD continues to climb with the DXY adding 53bp this morning. Brent slid 1.4% to around $78.50 a barrel and touched its lowest level since the start of the war while WTI fell -2.6% to $74.78; precious metals are largely flat this morning. US economic data calendar includes weekly jobless claims, June Philadelphia Fed business outlook (8:30am), May Leading Index (10am) and April TIC flows (4pm)

In premarket trading Mag 7 stocks are mostly higher (Nvidia +1%, Meta +0.5%, Tesla +0.3%, Amazon +0.2%, Microsoft -0.2%, Alphabet -0.5%).

Apple Inc. (AAPL) is up 0.6% after CEO Tim Cook told the Wall Street Journal that the iPhone maker plans to raise prices on its products to offset the increasing costs of memory and storage chips.

SpaceX (SPCX) falls 1.7%, set to extend the previous session’s drop, as it wraps up its first week as a public company following a record-breaking listing.

Accenture (ACN) tumbles 11% after the IT services company gave a revenue forecast for the fourth quarter that fell short of Wall Street’s expectations.

Albemarle Corp. (ALB) is up 1.8% after Citi raised its recommendation to buy from neutral on expected higher lithium prices.

Enphase Energy (ENPH) rises 4.1% after Barclays raised the recommendation on the company to equal-weight from underweight, citing its push into selling solid-state transformers to data centers.

Hive (HIVE) is up 15% after its subsidiary BUZZ High Performance Computing announced a partnership with Bell Canada, Cohere and Hypertec to build AI infrastructure in Canada.

Iren Ltd. (IREN) gains 3.3% as Jefferies initiated coverage of the Bitcoin miner and data center operator with a recommendation of buy on artificial intelligence data center demand.

Pfizer (PFE) is down 1.6% after the drugmaker said Chief Financial Officer Dave Denton will step down and leave the company on Aug. 15 for a professional opportunity in consumer goods outside the pharmaceutical industry.

Rumble (RUM) jumps 15% after the online video network platform said it plans to operate two core business units: video platform Rumble and cloud and AI-infrastructure business Quake AI, formerly Northern Data.

Four big June events are now in the rear view mirror — the first FOMC of the Warsh era, an Iran deal, the SpaceX’s IPO, and the first CPI print over 4% in 3 years. And yet, nothing appears able to dent the ongoing market meltup which is driven entirely by massive debt-funded capex spending into a handful of chip stocks.

Ahead of the last trading day of the week for US markets, the peace deal is reducing the risk of further energy-supply disruptions. Stocks have largely shrugged off the turmoil and continued to notch record highs on the back of relentless enthusiasm for AI. Equity markets have come through the tests posed by the debut of SpaceX, Kevin Warsh’s first meeting as Fed chair and the US-Iran peace deal fairly unscathed, said Raphael Thuin, head of capital market strategies at Tikehau.

“With the MOU now signed, there’s reason to believe that we may be close to or past peak inflation,” Thuin said. “The market will be able to concentrate on earnings again, like for Micron next week.”

Bond investors, however, face the prospect of lingering risks that may keep the higher-for-longer rates narrative intact. Even though US gasoline prices have dipped below $4 a gallon for the first time since March, energy costs have only been one factor in keeping inflation stubbornly above the Fed’s target.

US gasoline prices dipped below $4 a gallon for the first time since March, providing relief to consumers after global supply disruption sent fuel costs soaring. In contrast, inflation pressures are likely to hit people in the pocket if they want to buy a new iPhone later this year, with Apple’s Tim Cook telling the Wall Street Journal that the company plans to raise prices to offset surging memory and storage chip costs

Despite lower oil prices, front-end Treasury yields remained at their highest level since February 2025, with traders cementing bets for a September US rate hike. In the UK, the yield on two-year gilts jumped six basis points to 4.2%, while the Bank of England kept guidance that it “stands ready to act” on inflation and left its key rate unchanged. The dollar extended gains.

A quick look back at the Fed decision: Wednesday’s Fed decision marked the fourth consecutive meeting in which policymakers left rates unchanged. Officials described economic growth as “solid” and highlighted strong productivity gains and capital investment, while making clear that inflation has become a greater concern than labor-market weakness. Warsh has been critical of over-communication and poor forecasting by the Fed, and the new regime is moving away from explicit forward guidance – investors can no longer rely on central bank signals and will have to price in policy uncertainty. The S&P 500 has historically faced challenges following changes in leadership at the Fed.

“Half the committee is expecting rate hikes this year, which is a real shot across the bow at the market,” said Bob Michele, chief investment officer and global head of fixed income at JPMorgan Asset Management. “I think they’re getting ready for rate hikes.”

As for SpaceX, the company is seemingly sucking retail investors back into equities, flows into US equity ETFs have risen rapidly, notching the second highest-ever monthly flow, Bloomberg notes. Based on the price target of an initiation of coverage by Arete analyst Andrew Beale, SpaceX gets an implied $5.3 trillion valuation by end of 2027.

European stocks are missing out on the rally, with the Stoxx 600 down by 0.4%, dragged lower by the mining and autos sectors. Here are the biggest movers Thursday:

Edenred shares soar as much 18%, hitting their highest level since early November, after the payment solutions firm confirmed it has been approached by investment funds in the wake of a report of takeover interest from BC Partners

Generali shares rose as much as 3.3%, the most in 14 months, after newspaper Il Sole 24 Ore reported that UniCredit has informally proposed exchanging a 10% stake held by the Del Vecchio family holding Delfin in the insurer with its own shares

Oxford Instruments rises as much as 4.4% as Peel Hunt upgrades to buy from add and installs a new Street-high price target, based on durability of growth and scope for further operating leverage

Man Group shares rise as much as 3.4% to the highest since 2011 as BNP Paribas analysts upgrade their rating on the hedge fund manager to outperform from neutral and raise their target price

Informa shares rise as much as 3% as Morgan Stanley said the company has navigated the first five months of its financial year well, with strong results from its Live B2B Events and Academic Markets units

SSP advances as much as 5.1%, to the highest in eight weeks, after Davy initiates on the airport-focused food and beverage outlet operator with an outperform recommendation and 225p price target

Skistar climbs as much as 11%, the most since March 2025, after reporting third-quarter results which DNB Carnegie says show good cost mitigation and decent future pre-bookings

Tesco shares fall as much as 3.7% to their lowest level in two weeks after the UK’s biggest supermarket reported earnings which missed analyst expectations for like-for-like sales

Carrefour drops as much as 6.6% as JPMorgan places the French supermarket operator on a negative catalyst watch, saying first-half results on July 23 “might turn out to be a downgrade event”

Earlier in the session, Asian stocks rose as oil prices eased after President Donald Trump signed an interim peace deal with Iran to reopen the Strait of Hormuz. The MSCI Asia Pacific Index climbed as much as 0.8% to set an intraday record, boosted by gains in tech names including SK Hynix and Samsung Electronics. South Korea led advances in the region, with shares also rising in Taiwan and Japan. Crude prices continued to fall after Trump said a memorandum of understanding with Iran has taken effect, helping to ease inflation concerns for energy importing countries and offsetting hawkish signals from the Federal Reserve. A gauge of tech shares in Asia rose to a new high.Elsewhere in Asia, central banks in Indonesia and the Philippines — two economies hit hard by the sharp increase in global oil prices following the Iran war — both hiked their policy rates on Thursday. Indonesian stocks held losses, while Philippine shares pared gains.

In FX, the Bloomberg Dollar Spot Index reverses an earlier decline, sending the euro below $1.15. The BOE, Switzerland, and Norway’s central banks all held rates.

In rates, treasuries curve-flattening sparked by Wednesday’s hawkish Fed meeting extends as 2-year rises back toward highest levels since February 2025 — and within 25bp of the 10-year — while 30-year is more than 6bp lower on the day. Treasury 2-year is more than 2bps cheaper on the day while 10-year is nearly 3bp richer near 4.46% after touching 4.44% during London morning. US 2s10s and 5s30s spreads are 5bp and 6bp tighter respectively, after narrowing 8bp and 11bp to multi-month lows Wednesday. UK front-end underperforms, holding losses after Bank of England held interest rates at 3.75% as it said the recent fall in oil prices was “encouraging.” UK 2-year, 6bp cheaper on the day, had muted reaction to Bank of England policy announcement decided by 7-2 vote.

In commodities, WTI crude oil futures are down 2%, off session lows after Iranian President Masoud Pezeshkian released details on the text of the memorandum of understanding ending US attacks. Brent slid 1.4% to around $78.50 a barrel and touched its lowest level since the start of the war as three laden oil vessels controlled by Saudi Arabia’s state tanker giant switched on their signals in the Gulf of Oman after being stuck inside the Persian Gulf since the conflict began.

US economic data calendar includes weekly jobless claims, June Philadelphia Fed business outlook (8:30am), May Leading Index (10am) and April TIC flows (4pm)

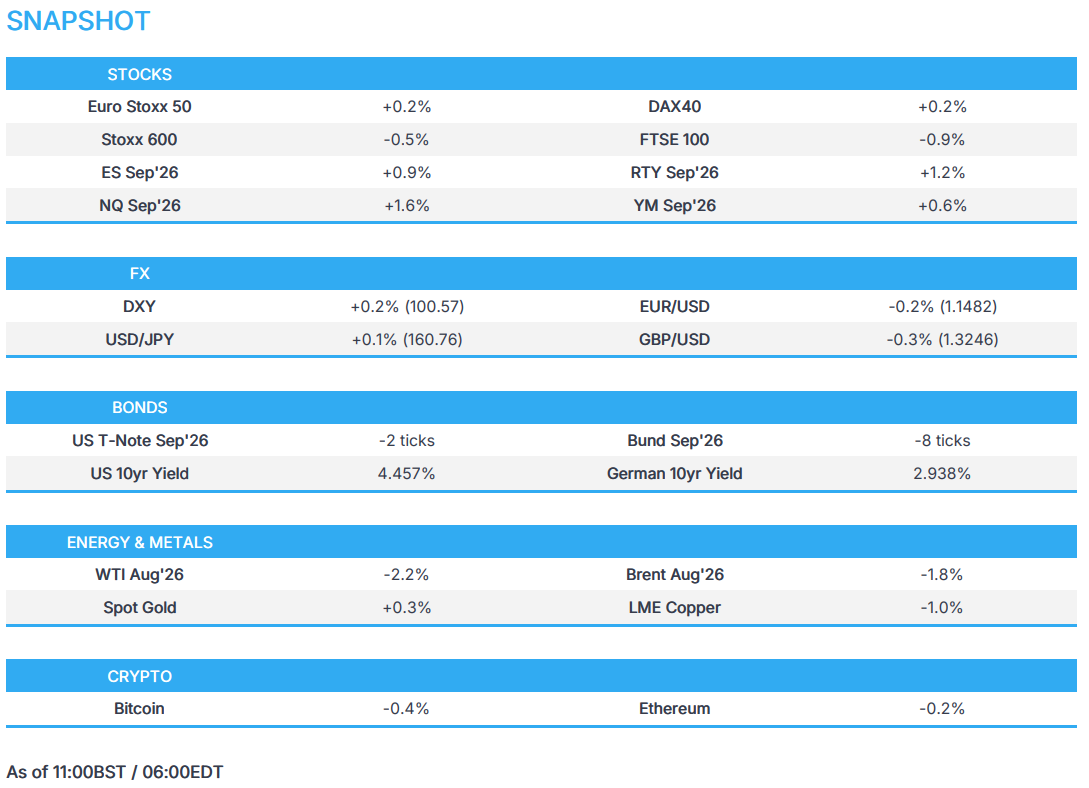

Market Snapshot

Top Overnight News

An impending wave of oil that’s been trapped inside the Strait of Hormuz is set to be unleashed on Asia, suddenly swamping a region that had managed to make up for lost supply in recent weeks. BBG

The average price of U.S. gasoline fell below $4 a gallon on Thursday for the first time in months, after Iran and the United States signed a preliminary agreement to cease hostilities for 60 days and reopen the Strait of Hormuz. The national average for a gallon of regular gasoline fell to a fraction of a penny below $4, down from $4.03 the day before, according to the AAA motor club. NYT