JUNE 17/THE REAL M. OF U. PUBLISHED: TRUMP THREATENS THAT IF THE FINAL DEAL IS NOT TO HIS LIKING HE WILL BOMB AGAIN: GOLD CLOSED UP $20.80 TO $4361.15 WITH SILVER UP $0.79//PLATINUM WAS DOWN $21.60 TO $1796.90 WITH PALLADIUM ALSO DOWN $4.50 TO $1360.00//GOLD COMMENTARY TONIGHT COURTESY OF ALASDAIR MACLEOD//EUROPEAN REPORTS FROM UK AND FRANCE//ISRAEL/USA VS IRAN UPDATES/ISRAEL TBN//HEZBOLLAH UPDATES/COVID VACCINE INJURY REPORT: MARK CRISPIN MILLER AND DR PAUL ALEXANDER//LAST 24 HOURS COURTESY OF MIKE EVERY OF RABOBANK//OIL ISSUES DISCUSSED/USA DATA RELEASES ON HOUSING ETC//USA ECONOMIC REPORTS//KING NEWS/SWAMP STORIES FOR YOU TONIGHT//GREG HUNTER INTERVIEWS STEVE QUAYLE//

Bitcoin morning price:$64,891 DOWN 632 DOLLARS (MANY SWITCHING TO PHYSICAL GOLD)

Bitcoin: afternoon price: $64,420 DOWN 1103 DOLLARS

Platinum price closing DOWN $21.60 TO $1795.90

Palladium price; DOWN $4.50 TO $1360.00

JUNE 17

JUNE COMEX MONTH

JPMORGAN STOPPED: 0/93

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2026: 93 CONTRACTs NOTICES FOR 9300 OZ or 0.2892 TONNES

total notices so far: 35,456 contracts FOR 3,545,600 OZ OR 110.180 TONNES

JUNE 17

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 2 NOTICE(S) FILED FOR 10,000 OZ /

total number of notices filed so far this month : 2395 CONTRACTS (NOTICES) for 11.975 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $20.80 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/// HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.427 TONNES FROM THE GLD

INVENTORY RESTS AT 1013.640 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.79 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: NO CHANGES IN SILV INVENTORY//// : INVENTORY RESTS AT THE SLV AT 481.388 MILLION OZ//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 481.388 MILLION

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 393 CONTRACTS TO AN OI OF 107,721 A LOT HIGHER FROM ITS NEW RECORD LOW OF 95,999 SET MAY 1/2026. THE RECORD HIGH OI FOR SILVER IS 244,710, SET FEB 25/2020, AND THIS FAIR GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0.13 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. ON THE FIRST OF MAY, WE REACHED OUR RECORD LOW OI OF 95,999 SURPASSING EVERY DAY NEW OI LOWS SET DURING THE LAST WEEK OF APRIL 2026.

NOW ON A NET BASIS OUR SPECULATORS HAVE REVERTED BACK TO GOING LONG. THE FRBNY ON A NET BASIS IS PROVIDING THE NECESSARY PAPER TO OUR LONGS ALONG WITH SOME BULLION BANKS AND THEN A HUGE NUMBERS OF LONGS ,OUR CENTRAL BANKERS, TAKE THE LONG SIDE AND TENDER FOR PHYSICAL AT 4 PM EACH NIGHT. BECAUSE OF THE HUGE SHORTFALL IN PHYSICAL SILVER IN LONDON THERE IS A LOTTERY TO SEE WHO GETS ANY OF THE PHYSICAL SILVER AVAILABLE THAT WHICH THEY ARE OBLIGATED TO DELIVER. THEY WAIT PATIENTLY FOR THEIR PHYSICAL METAL AND IF NOBODY GETS ANY THEY THEN COME BACK THE NEXT DAY AND SO ON. THIS IS IN LONDON, THE HOME OF PHYSICAL SILVER!! THE FACT THAT WE ARE WITNESSING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON HIGHLIGHTS THE FACT THAT THE COMEX IS OUT OF SILVER AS WELL.

WE ARE FINALLY MOVING TO A MUCH HIGHER BASE IN SILVER PRICING AT MAJOR SUPPORT LEVEL OF $70.00. SHORTLY WE WILL AGAIN ATTEMPT TO BREAK

WE HAVE A SMALL LOSS OF 393 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A ZERO SIZED SIZED 0 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE , WE HAD NO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO TUESDAY TRADING// WE HAD A HUGE SIZED 829 CONTRACT T.A.S. ISSUANCE!! / THEY DESPERATELY AGAIN TODAY TRYING TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $100.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON TUESDAY WITH SILVER’S FALL IN PRICE

THE PRICE STILL FINISHED BELOW THE MAGIC NUMBER OF $70.00 SILVER SPOT PRICE BUT STILL BELOW THE $100.00 MARK CLOSING AT $71.05 DOWN $0.13. WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS A HUGE SIZED 829 T.A.S. CONTRACTS !!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING ABOVE THE 100.00 DOLLAR MARK!! AND NOW THE HUGE SUPPORT LEVEL OF 70 DOLLARS IS BROKEN!!.MAMMOTH SIZE T.A.S ISSUANCES ARE BECOMING THE NORM AT THE COMEX NOW!!

THERE IS NO NEXT LINE IN THE SAND ONCE THE 100.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A ZERO SIZED 0 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 829 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE.

IN ESSENCE WE HAD A FAIR SIZED LOSS OF 393 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.13. WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION WILL BE REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE STICKY SPECULATOR LONGS STILL REMAIN STOIC

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE.

THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, THROUGHOUT MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT/WEDNESDAY MORNING: A HUGE SIZED 829 CONTRACTS. DESPITE MANY COMPLAINTS THAT THESE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS).

THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS AS ONE UNIT, BUT SELL THE SHORT SIDE FIRST AND THEN LIQUIDATE THE LONG SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF XX CONTRACTS OR XXX OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 10,000 OZ//NEW STANDING ADVANCES TO 12.025 MILLION OZ//

SUMMARY OF OUR JUNE 2026 COMEX CONTRACT MONTH:

WE HAD:

/ SMALL COMEX LOSS+// ZERO SIZED 0 EFP ISSUANCE CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 829 CONTRACTS

xx I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 109 SILVER CONTRACT//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE.. ACCUMULATION

TOTAL CONTRACTS for 13 DAY(S), total 7020 contracts: OR 35.100 MILLION OZ (540 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 35.100 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE. 35.100 MILION OZ

RESULT: WE HAD A SMALL DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 284 CONTRACTS WITH OUR LOSS IN PRICE OF $0.13 IN SILVER PRICING AT THE COMEX// TUESDAY,. THE CME NOTIFIED US THAT WE HAD A 0 SIZED CONTRACT EFP ISSUANCE OF 0 CONTRACTS ISSUED FOR JULY, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS).

INITIAL STANDING: 10.935 MILLION OZ PLUS 10,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 12.025 MILLION OZ

LAST 14 MONTHS OF SILVER DELIVERIES

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 10,000 OZ//NEW STANDING ADVANCES TO: 12.025 MILLION OZ

THE NEW TAS ISSUANCE FOR TODAY (829) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!

WE HAD 2 NOTICE(S) FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY BANKERS

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 46 OI CONTRACTS DOWN TO 339,330 OI AND THIS OI STILL SURPASSES BY A CONSIDERABLE MARGIN THE ALL TIME LOW AT 326,052 SET JUNE3/2026 AND THIS OI IS MUCH FURTHER FROM THE RECORD HIGH (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE HAVE NOW ADVANCED PAST THE PREVIOUS ALL TIME LOWS OF 357,136 SET APRIL 2/.2026AND 354,581 SET AT THE END OF APRIL 2026. WE ARE STILL QUITE A WAY FROM OUR TWO DECADES OLD: 390,000 CONTRACTS LOW SET IN THE YEAR OF 2001 WITH TRADING FOR GOLD AT $260.00. THUS DURING EARLY APRIL WE HAD AN ALL TIME LOW OI IN COMEX (354,531) BUT WITH AN EXTREMELY HIGH PRICE OF GOLD. IN MAY: RECORD LOW OI OF 326,052 WITH A GOLD PRICE OF $4,460 THE SHORT RATS ARE ABANDONING THE COMEX SHIP, NOBODY WANT TO PLAY IN THIS CROOKED CASINO!! (AND THIS CORRELATES WITH SILVER’S LOW OI OF 107,471 CONTRACTS WITH A MUCH HIGHER SILVER PRICE BASE//$75.00)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 281 CONTRACTS //.

WE HAD A SMALL LOSS IN COMEX OI (46 CONTRACTS) . THIS SMALL LOSS IN OI OCCURRED WITH OUR GAIN IN PRICE OF $4.45 //,TUESDAY///.

LAST 13 MONTHS OF GOLD DELIVERIES: (MAY 2025 THROUGH TO /MAY 2026)

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT 0.2270 TONNES OF A QUEUE JUMP/NEW STANDING ADVANCES TO 110.429 TONNES

E.F.P. ISSUANCE/FOR OPENING JUNE. GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 450 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 339,330 SURPASSING THE PREVIOUS ALL TIME LOW OF 326,052 SET JUNE 3 AND RISING FROM OUR PREVIOUS RECORD LOW//MAY 28.2026 WE HAVE THUS RECORD LOW COMEX OI WITH A HIGH PRICE OF GOLD

SILVER ALSO HAS AN ULTRA SMALL SIZED AND EXTREMELY LOW COMEX OI OF 107,721 CONTRACTS// RISING FROM PREVIOUS ALL TIME LOWS SET DURING THE MONTH OF APRIL AND MAY FIRST.

IN ESSENCE WE HAVE A SMALL GAIN IN TOTAL CONTRACTS IN COMEX GOLD ON THE TWO EXCHANGES OF 404 CONTRACTS WITH 46 CONTRACTS DECREASED AT THE COMEX// AND A SMALL SIZED 450 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON.

THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 404 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALLER SIZED BUT CRIMINAL 753 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON

GOLD PRICE ON TUESDAY ROSE BY $4.45

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT (450 ) ACCOMPANYING THE SMALL LOSS IN COMEX OI OF 46 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES 404 CONTRACTS!! WITH THE GAIN IN PRICE.

WE HAVE 1) NOW REVERTED TO OUR FORMAT OF BANKER (FRBNY) GOING ON THE SHORT SIDE AND HUGE NUMBERS OF NEWBIE SPECULATORS GOING TO THE LONG SIDE. IT WAS OUR SHORT SPECULATORS THAT WE BRUTALIZED ON THURSDAY WHEN OUR CENTRAL BANKS TENDERED FOR PHYSICAL GOLD WITH THEIR NEWLY BOUGHT GOLD FROM THE SPECS. THE SPECS ARE STILL SCRAMBLING LOOKING FOR PHYSICAL GOLD TO DELIVER TO OUR LONG CENTRAL BANKS.

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2270TONNES//NEW STANDING ADVANCES TO 110.429 TONNES

3) LITTLE IF ANY T.A.S. LIQUIDATION IN THE COMEX SESSION AND SOME GOVT LIQUIDATION // WITH A STRONG GAIN OF EQUITY SHARES/JUNE16 HAVING 1)A $4.40 COMEX PRICE GAIN AND WE HAD 2) SPEC PILING HUGELY ON THE LONG SIDE// +3. EASTERN CENTRAL BANKERS ALSO PILING INTO THE LONG SIDE. WE HAD A SMALL GAIN OF 404 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A STRONG AMOUNT OF GOLD WILL STAND FOR DELIVERY IN JUNE. (110.429 TONNES). THE SHORT SPECS BAILED ON THURSDAY AND FRIDAY//, CENTRAL BANKERS TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4)A SMALL SIZED COMEX OI LOSS 5) V) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD(450) AND 6. A SMALL T.A.S. ISSUANCE (753) FOR RAID PURPOSES.!!!

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 26,607 CONTRACTS OR 2,660,700 OZ OR 82.758 TONNES IN 13 TRADING DAY(S) AND THUS AVERAGING: 2179 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN13 TRADING DAY(S) IN TONNES: 82.758 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2025, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 82.758 TONNES DIVIDED BY 3550 x 100% TONNES = 2.33% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2023 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2024: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES

2025: AND NOW 2026

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 82.758 TONNES

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SOIS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A SMALL 393 CONTRACTS TO AN OI OF 107,721.

EFP ISSUANCE 0 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 0 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 393 CONTRACTS AND ADD TO THE 0 E.FP. ISSUED

WE OBTAIN A FAIR LOSS OF393 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $0.13

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 1.905 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $0.13

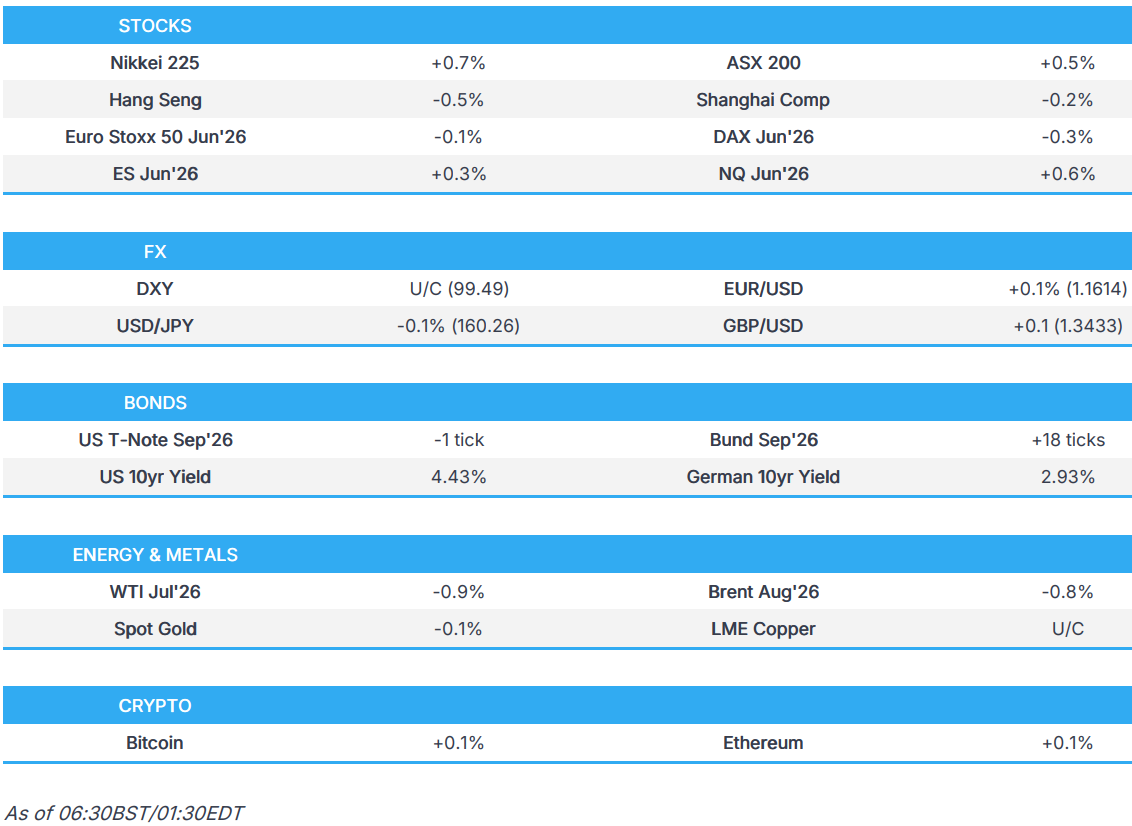

2.ASIAN AFFAIRS JUNE 17 /2025

SHANGHAI CLOSED UP 16.18 PTS OR 0.40%

HANG SENG CLOSED DOWN 181.79 PTS OR 0.74%

Nikkei CLOSED UP 575.50 PTS OR 0.83%

//Australia’s all ordinaries CLOSED UP 0.84%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7588

/ OFFSHORE CLOSED DOWN AT 6.7593 Oil DOWN TO 76.23 dollars per barrel for WTI and BRENT DOWN TO 76.23Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7588) OFFSHORE YUAN TRADING DOWN TO 6.7593 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL 46 CONTRACTS TO 339,330 RISING FROM ITS NEW LOW OF 326,052 OI SET JUNE 3, SURPASSING THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,052 //JUNE 3 2026 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD NO T.A.S. LIQUIDATION DURING TUESDAY’S TRADING JUNE 16!!. IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE SHORT SIDE BUT WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL.

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS JUNE CONTRACT MONTH!!

THE SMALL SIZED GAIN ON OUR TWO EXCHANGES OCCURRED WITH OUR GAIN IN PRICE IN GOLD (UP $4.45)

WE THUS HAD A SMALL SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 440 CONTRACTS (OR 2.037 TONNES) WITH OUR GAIN IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 450 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIDAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 146+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO SO FAR

DETAILS ON OUR NEW JUNE COMEX CONTRACT MONTH//

IN TOTAL WE HAD A SMALL GAIN ON OUR TWO EXCHANGES OF 404 CONTRACTS WITH OUR GAIN IN PRICE($4.45). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A FAIR SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 753 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

JUNE: ZERO SO FAR.

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 146+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO. WE WILL KNOW IN JUNE WHETHER THEY COVERED ANY OF THEIR SHORTFALL.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2270 TONNES//NEW STANDING ADVANCES TO 110.429 TONNES// TOTAL QUEUE JUMPING FOR THE MONTH; 45.802 TONNES OR AVERAGING 3.530 TONNES PER DAY IN JUNE.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JUNE,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $4.45)

WE HAD NO T.A.S. SPREADER LIQUIDATION TUESDAY // COMEX SESSION// WITH OUR GAIN IN PRICE , OUR LONG SPECULATORS STILL REMAIN RELENTLESS POURING INTO THE COMEX

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

TUESDAY NIGHT//WEDNESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $4.45

WE HAD 251 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES: 404 CONTRACTS OR 40400 OZ (2.020 TONNES)

Total monthly oz gold served (contracts) so far this month

35,456 notices 3,545,600 oz 110.180 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

ENTRIES: 0

xxxxxxxxxxxxxxxxxx

comex withdrawal

1 ENTRIES

1 ENTRIES

i) Brinks: 3,408.006 oz (106 kilobars)

total withdrawal 3,408.006 oz

adjustments: 2// dealer to customer

a) Asahi: 60,080.003 oz

b) Brinks 133,008.687 oz

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JUNE OI STANDS AT 140 CONTRACTS HAVING A LOSS OF 1360 CONTRACTS.

WE HAD 1433 CONTRACTS SERVED ON TUESDAY, SO WE GAINED 73 CONTRACTS OR 7300 OZ. (0.2270 TONNES) EXERCISED A QUEUE JUMP WHERE THEY WILL TAKE PHYSICAL GOLD ON THIS SIDE OF THE POND. THIS IS NO DOUBT CENTRAL BANKS STANDING FOR PHYSICAL GOLD.

JULY GAINED 1386 CONTRACTS UP TO 4629 CONTRACTS.

AUGUST DOWN 30 CONTRACTS UP TO AN OI OF 263,688

.

We had 93 contracts filed for today representing 9,300oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 2 notices issued from their client or customer account. The total of all issuance by all participants equate to 93 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (35,456) to which we add the difference between the open interest for the front month of JUNE(140 CONTRACTS) minus the number of notices served upon today 93 x 100 oz per contract) equals 3,550,300 OZ OR (110.429 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (35,456) to which we add the difference between the open interest for the front month of JUNE( 140 CONTRACTS) minus the number of notices served upon today 93 x 100 oz per contract) equals 3,550,300 OZ OR (110.429Tonnes of gold)

new total of gold standing in JUNE becomes 110.429 TONNES//

TOTAL COMEX GOLD STANDING FOR JUNE 110.429 TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS ACTIVE DELIVERY MONTH OF JUNE.

confirmed volume TUESDAY confirmed 99,679// poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,730,178.612 oz 53.816 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,730,178.612 tonnes oz 53.816 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 27,935,912.745oz

TOTAL REGISTERED GOLD 15,229,363.439 tonnes (473.697 tonnes)

TOTAL OF ALL ELIGIBLE GOLD 12,706,549.306 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,499,185oz ((REG GOLD- PLEDGED GOLD)=

419.887 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JUNE DELIVERY MONTH

JUNE 17

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

4 entries Out of: a) Asahi: 32,042.930 oz b) Delaware 1067.147 oz c) JPMorgan 599,422.306 oz d) Maanfrea 99,249.620 oz

total withdrawal: 731,781.997 oz

Deposits to the Dealer Inventory

0 entries

Deposits to the Customer Inventory

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ONE ENTRY

i) Into HSBC 605,069.076 oz

total deposit: 605,069.076. oz

No of oz served today (contracts)

212 CONTRACT(S) (1.060 MILLION OZ)

No of oz to be served (notices)

10 Contract (50,000 oz)

Total monthly oz silver served (contracts)

2393 contracts 11.965 MILLION oz

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRIES

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRY:1

ONE ENTRY

i)Into HSBC 605,069.076 oz

total deposit 605,069.076 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

4 entries

i) Out of

a) Asahi: 32,042.930 oz

b) Delaware 1067.147 oz

c) JPMorgan 599,422.306 oz

d) Manfrea 99,249.620 oz

total withdrawal: 731,781.997 oz

adjustments 0

0

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 86.273 MILLION OZ//.TOTAL REG + ELIGIBLE. 321.082 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE /2026 OI: 12 OPEN INTEREST CONTRACTS FOR A LOSS OF 210 CONTRACTS.

WE HAD 212 NOTICES SERVED ON TUESDAY SO WE GAINED 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL STAND AS A QUEUE JUMP AT THE SILVER COMEX.

JULY SAW A LOSS OF 2179 CONTRACTS DOWN TO 43,299 CONTRACTS.

AUGUST SAW A GAIN 0F 78 CONTRACTS UP TO 938…

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2 or 10,000 OZ oz

CONFIRMED volume TUESDAY; 47,817// fair

XXX

AND NOW JUNE. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 2395 X5,000 oz = 11.975 MILLION oz

to which we add the difference between the open interest for the front month of JUNE(12) AND the number of notices served upon today (2 )x (5000 oz)

Thus the standings for silver for the JUNE 2026 contract month: (2395 )Notices served so far) x 5000 oz + OI for the front month of JUNE ( 12) minus number of notices served upon today (2)x 5000 oz equals silver standing for the JUNE..contract month equating to 12.025 MILLION OZ.+

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 86.273 million oz of registered silver

JPMorgan as a percentage of total silver: 139.079/321.159 million: 43.30%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JUNE 17 /2026/WITH GOLD UP $20.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.427 TONNES OF GOLD FROM THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1012.213 TONNES

JUNE 16 /2026/WITH GOLD UP $4.45 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 15 /2026/WITH GOLD UP $111.10 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 12 /2026/WITH GOLD UP $123.30 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 11 /2026/WITH GOLD DOWN $15.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.855 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 10 /2026/WITH GOLD DOWN $153.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.426 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1016.495 TONNES

JUNE 9 /2026/WITH GOLD DOWN $75.60 TODAY/NO CHANGES IN GOLD AT THE GLD:// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 8 /2026/WITH GOLD DOWN $3.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 6.936 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 5 /2026/WITH GOLD DOWN $134;85 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 4 /2026/WITH GOLD UP $39.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.143 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 3 /2026/WITH GOLD DOWN $51.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.856 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.000 TONNES

JUNE 2 /2026/WITH GOLD UP $7.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.712 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.856 TONNES

JUNE 1 /2026/WITH GOLD DOWN $79.30 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 29 /2026/WITH GOLD UP $59.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

GLD INVENTORY: 1012/213 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JUNE 17 WITH SILVER UP $0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: NO CHANGE IN INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 16 WITH SILVER DOWN $0.13: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.362 MILLION OZ INTO THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 15 WITH SILVER UP $3.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.357 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 481.026 MILLION OZ

JUNE 12 WITH SILVER UP $3.34: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.769 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 482.383 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.12: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.226 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.152 MILLION OZ

JUNE 10 WITH SILVER DOWN $0.50: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.909 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.378 MILLION OZ

JUNE 9 WITH SILVER DOWN $3.35: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.407 MILLION OZ INTO INTO THE SLV /./ // :INVENTORY RESTS AT 484.287 MILLION OZ

JUNE 8 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 543,000 OZ FROM THE SLV /./ // :INVENTORY RESTS AT 482.880 MILLION OZ

JUNE 5 WITH SILVER DOWN $4.86: NO CHANGES IN SILVER INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 4 WITH SILVER UP $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.432 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 3 WITH SILVER DOWN $2.55: NO CHANGES IN SILVER INVENTORY AT THE SLV >> /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

While Western investors are dithering and selling gold and silver for fear they might go lower, China is buying up all available bullion. Record export earnings make it inevitable.

Today, China’s export surpluses are larger than ever giving the PBOC an unwanted dollar headache. She has little need for other G7 currencies and their debt, so they can only be sold for precious metals. This is confirmed in the gold and silver import statistics for China in what we know of them in 2026 so far.

It was a problem anticipated by the post-Mao administration as they planned their way into capitalism, unleashing enormous economic development coupled with a high consumer saving mentality. Ever since then, China has had the problem of excess dollars, and it is still growing. But the Communist Party understood from the outset the danger of being hostage to a rival national currency.

Back in 1983, China’s Communist Party appointed the People’s Bank (PBOC) with sole responsibility for buying and selling gold and silver. It was logical, because the PBOC was also the monopoly dealer in foreign exchange. And while I’ve told the story many times about how the PBOC accumulated an estimated 20,000 tonnes of gold before setting up the Shanghai Gold Exchange in 2002 and permitted the public to buy gold from then on, the silver story has been neglected. But it is a tandem operation. I shall release an analysis of China’s silver policy in a separate article.

Gold mining developed deliberately with China becoming the largest mining nation almost from scratch. From only 50 tonnes in the early 1980s, rising to 100 tonnes in the early ’90s and overtaking South Africa in 2007, China has mined an estimated 10,200 tonnes by the start of this year. Virtually no gold leaves China, so what the Chinese mine and buy is locked away from global markets.

Estimates of gold imports since 2002 vary widely between 15,000-25,000 tonnes. Deliveries from SGE vaults post-2002 into public hands total over 28,000 tonnes, some of which will have been scrapped and resubmitted to the government for refining.

However, this does not include gold designated as monetary. If the PBOC buys gold from another central bank, or books it as monetary, it goes unrecorded in China’s import figures. Investor uncertainty in Europe and North America doesn’t faze the Chinese either, who continue to sell dollars in favour of gold, having bought an estimated 473 tonnes of non-monetary gold so far this year to end-April. That’s a run-rate of nearly 1,500 tonnes annualised, selling nearly $70 billion so far.

Most of the gold delivered to the public is turned into jewellery. Though some is recast into bars and coin, gold categorised for investment is increasingly being acquired through gold accumulation accounts offered by China’s banks that run alongside deposit accounts. These are designed to be available even for small savers, who can open an account for as little as ¥500 ($75).

Periodically, banks have been forced to suspend this facility for lack of physical gold to cover these growing commitments.

This brings us to the topic of household savings, which are about 30% of GDP or $6,300 billion equivalent, added every year to the estimated $21,000 billion of savings in bank deposits. The mobilisation of just a small part of household saving deposits into gold almost certainly leads the banks to buy any available bullion in London and New York.

Furthermore, with both Hong Kong and Singapore expanding their gold and silver trading facilities, the relevance of London and New York as price setters is diminishing, and probably rapidly.

Conclusion

Market commentators in North America and Europe appear to be ignorant of the dynamics driving China’s continuing thirst for gold. The pace at which dollars and other G7 currencies are being dumped for gold is increasing and is becoming a serious problem for the entire fiat currency system based on the US dollar.

There comes a point where the drain of physical bullion liquidity will unexpectedly drive prices higher, and probably rapidly. It risks being self-feeding by unlocking massive Chinese saver demand.

In general terms, it is correct to view gold’s value measured in commodities and wholesale prices as being stable. But as a consequence of trade and savings imbalances between China and G7 nations, there is a building propensity for selling dollars and their currencies for physical gold, destroying their credibility as credit.

It starts with central banks and sovereign wealth funds predominantly in China and Asia, and spreads to wider populations in those countries before the domestic users of those currencies understand the threat. We can now see these dynamics playing out in China in plain sight. It marks the start of the final rejection of the dollar-based fiat currency system.

.

3. CHRIS POWELL AND HIS GATA DISPATCHES

5. COMMODITY REPORT//ALUMINIUM/SULFUR

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 16.18 PTS OR 0.40%

HANG SENG CLOSED DOWN 181.79 PTS OR 0.74%

Nikkei CLOSED UP 575.50 PTS OR 0.83%

//Australia’s all ordinaries CLOSED UP 0.84%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7588

/ OFFSHORE CLOSED DOWN AT 6.7593 Oil DOWN TO 76.23 dollars per barrel for WTI and BRENT DOWN TO 76.23Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7588) OFFSHORE YUAN TRADING DOWN TO 6.7593 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7588

OFFSHORE YUAN: DOWN TO 6.7593

1.HANG SANG CLOSED DOWN 181.79 PTS OR 0.74%

2. Nikkei closed UP 575.50 PTS OR 0.83%

WEST TEXAS INTERMEDIATE OIL DOWN TO 76.23

BRENT; 79.00

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 99.37/// EURO FALLS TO 1.1598 DOWN 11 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.606 DOWN 3 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA CROSS NOW AT 160.219… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.748 DOWN 3 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN( 6.7588 AND OFFSHORE: DOWN AT 6.7593

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.9219// Italian 10 Yr bond yield DOWN to 3.640// SPAIN 10 YR BOND YIELD DOWN TO 3.342%

3i Greek 10 year bond yield DOWN TO 3.581%

3j Gold at $4328.00 //Silver at: 69.87 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 61/ 100 roubles/73.11

3m oil (WTI) into the 76 dollar handle for WTI and 79 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 160.219 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.606% DOWN 3 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.748 DOWN 2 PTS..: USA/SF this 0.7921 as the Swiss Franc . Euro vs SF: 0.9186

USA 10 YR BOND YIELD: 4.428 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.936 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.052 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 46.32 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.7393 DOWN 5 PTS

30 YR UK BOND YIELD: 5.4555 DOWN 4 BASIS PTS

10 YR CANADA BOND YIELD: 3.379 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.019 DOWN 1 BASIS PTS.

1a New York Opening report

1b) European opening report

US equity futures gain, GBP weaker after cooler than exp. CPI, USD benefits into FOMC – Newsquawk US Market Open

Wednesday, Jun 17, 2026 – 06:25 AM

An informed source told Tasnim that Bloomberg’s alleged text of the US-Iran MoU is not accurate, but that the finalised text will be published after the signing on Friday. However, it was initially stated that it would not be published.

US equity futures gain steadily; Germany’s DAX 40 underperforms, weighed by BMW’s guidance cut.

DXY flat, G10s mixed; SEK softer despite Riksbank forecasts of a greater chance of a rate hike.

Fixed income muted, while gilts outperform following cooler-than-expected CPI; Fed announcement ahead.

Energy benchmarks contained in narrow ranges, as the focus remains on the US-Iran MoU signing.

Looking ahead, highlights include US Retail Sales (May), Atlanta Fed GDP (Q2), New Zealand GDP (Q1), Fed Policy Announcement, BCB Policy Announcement, Speakers including ECB’s Lagarde & Fed’s Warsh.

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

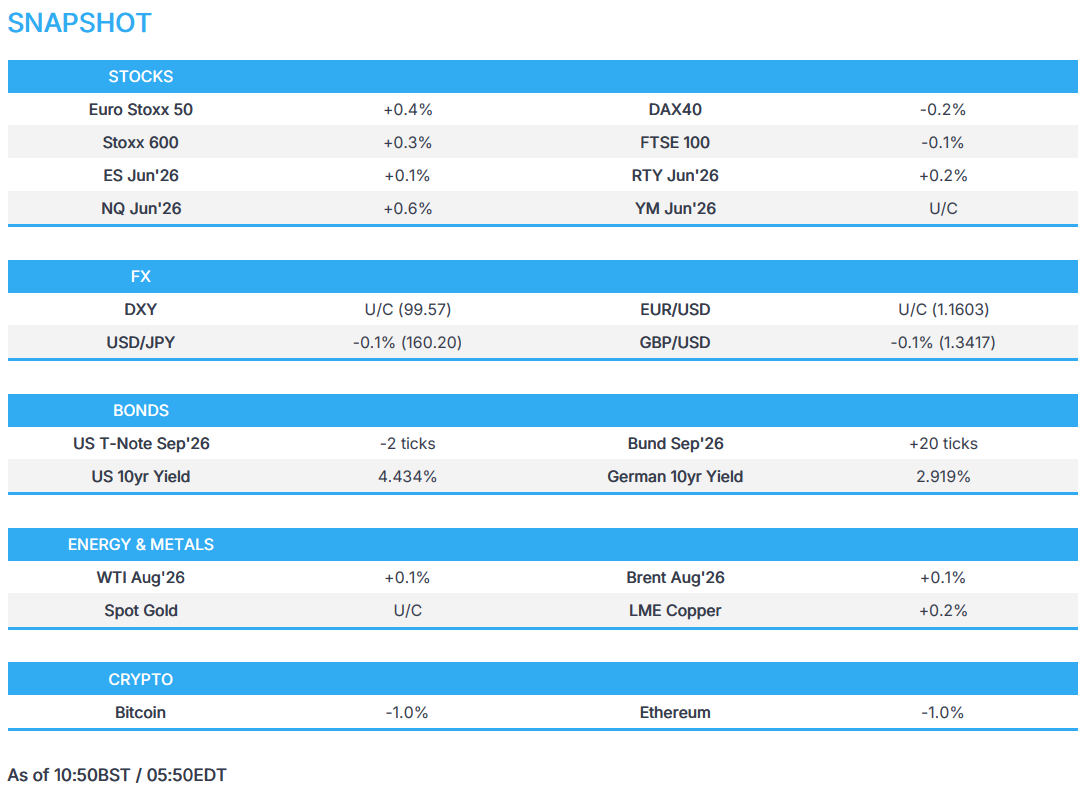

European bourses (STOXX 600 +0.3%) start Wednesday’s trade mixed, with outperformance in the AEX (+0.7%) while the DAX 40 (-0.2%) lags after BMW cut guidance. Geopolitical newsflow has been light thus far as markets await for the official MoU signing on Friday.

European sectors also lack a clear bias. Technology (+1.2%) and Banks (+0.8%) top the sector pile. Autos (-2.1%) is the worst-performing sector this morning, primarily driven by updated guidance from BMW. The Co. cut its operating auto margin to 1-3% (prev. 4-6%) and said it would intensify cost-cutting, with a negative one-off in the H2’26. Analysts at Deutsche Bank and Jefferies both said the outlook cut was significantly larger than expected, which has resulted in the Co.’s shares slumping as much as 11%. This has dragged peers lower with it (Volkswagen -2.4%, Mercedes-Benz -3.0%)

US equity futures are muted, except for the NQ (+0.6%). Intel (+4.1%) announced that its 18A manufacturing process has entered risk (i.e. early) production, with the chipmaker seeing strong demand for its central processors.

DXY is on a modestly firmer footing after softening on Monday alongside a decline in yields and lower oil prices. Focus today is overwhelmingly on Warsh’s first FOMC meeting as chair, where the committee is widely expected to keep the federal funds rate unchanged at 3.50-3.75%. Within the meeting, attention will be on language surrounding the easing bias, and the dot plots, which ING believes a removal of the bias alongside a cut to the 2026 dot plot, would support the Buck. Alongside these points, Warsh’s communication will be closely monitored. (Full Fed preview in the Newsquawk Research suite). DXY lacks direction, trading unchanged and supported just above 99.50.

GBP is a touch lower. In short, a cooler than expected UK CPI print, which falls beneath BoE forecasts on both a headline and core basis, services were also cooler than BoE forecast, but in line/hotter than analyst forecasts, depending on which data vendor is cited. GBP weakened post-data; Cable fell as much as 20 pips to a 1.3408 trough before paring modestly. The pair dipped below its 200DMA at 1.3418.

Two-way action seen in SEK, which is modestly softer post-announcement despite the forecasts implying a greater chance of a 2026 hike. Pressure that is a function of the fact that the forecasts and statement are based on information up to the 11th of June, as such the fall in energy benchmarks seen in the last few sessions on the US-Iran MOU progress is not accounted for, and therefore the hawkish tilt to the policy forecast is likely to be unwound in the next meeting, if the MOU holds and the energy retreat sticks and/or extends. We may get more details from Governor Thedeen at 10:00BST, and the Minutes on the 24th of June.

FIXED INCOME

Global fixed benchmarks are mixed, with USTs a couple of ticks lower whilst Bunds and Gilts gain; the latter outperforms after the UK’s inflation held steady in May. Geopolitical updates have been lacking today, with all eyes on the US-Iran deal signing on Friday. However, Iran’s Tasnim, citing a source, suggested that the text will not be published after the signing on Friday. Though, this was later corrected and it will be released.

USTs (-2 ticks) hold within a 109-26+ to 109-30+ range. Markets are ultimately on tenterhooks ahead of the Fed policy announcement, which will see the debut of Kevin Warsh as Chair. Policy rates are expected to remain unchanged, so focus will be on whether the easing bias will be removed from the statement. Dot plots are seen to show higher inflation and a more cautious policy path, with the new Chair interestingly not expected to publish a personal dot plot. At the presser, traders will eye whether he attempts to push a dovish agenda and how he contrasts to his fellow board members. From a yield point, Warsh will be eyed for any hints to his thinking on the Fed balance sheet; should markets be guided to faster unwinding of the Fed’s balance sheet, a steeper curve could be expected.

Bunds (+20 ticks) trade firmer this morning, continuing recent price action. Domestically, the release of the ECB Wage Tracker had little impact on German paper, where the 2026 quarterly figure rose slightly from the prior. Focus ahead turns to the EZ Final Inflation metrics for May, which are expected to remain unrevised. From a yield perspective, the German 10yr has now slipped below the 3.00% mark (current 2.93%), and now approaching levels not seen since early April.

Gilts (+57 ticks) outperform vs peers following the region’s inflation report. In brief, a cooler-than-expected print on both a headline and core basis. A series that reduces the odds of a hawkish surprise at the June BoE. However, the as-expected/slightly-hotter (depending on the consensus provider) services figure will be a point of concern for policymakers and may well be enough to keep some dissenters in play, even given the significant energy benchmark moderation in recent days. The report will not have any impact on the policy decision at Thursday’s meeting (BoE to hold), but could push the vote split a bit more dovish vs consensus; analysts saw a range between 8-1 to 6-3 before the inflation print and recent energy moderation on US-Iran progress.

Germany sells EUR 2.107bln vs exp. EUR 2.5bln 3.40% 2047 and 1.80% 2053 Bund.

Australia sells AUD 300mln 4.75% June 2054 bonds b/c 2.46, avg yield 5.3040%.

COMMODITIES

Crude futures are essentially incrementally firmer, hovering at 3-month lows, as markets await the US-Iran MoU signing in Switzerland. Details of the deal remain light; however, Reuters did shine some light on a point of the draft MoU: the rehabilitation and economic development of Iran. The report stated that a USD 300bln private fund is being designed to trigger investment into Iran. The report added that commitments have already exceeded USD 150bln across 5 regions, while the fund will not contain US government money or grants.

Energy benchmarks are relatively contained. WTI Aug’26 oscillates in a USD 74.09-76.06 range while Brent Aug’26 rotates in a 77.75-79.57/bbl band.

Spot gold has come off slightly ahead of the FOMC meeting, in which a hold is expected. Focus will lie in the press conference, in which Fed Chair Warsh is delivering his first post-policy conference in his new role. The yellow metal currently trades at the lower end of its narrow USD 4318-4350/oz range.

3M LME Copper flips either side of the USD 13.8k/t handle as market risk is subdued.

US Private Inventory Data (bbls): Crude -8.3mln (exp. -4.5mln), Distillates -0.5mln (exp. -0.2mln), Gasoline +2.5mln (exp. -1.4mln), Cushing -1.5mln.

IEA OMR (Jun): World oil demand falling by 1.1mln BPD in 2026 on the Iran War (prev. forecast 420k BPD fall); sees total world oil supply 920k BPD lower than demand in 2026 (prev. forecast 1.7mln BPD lower).

TotalEnergies (TTE FP) says its Saudi Arabian refinery was hit by three drones but is still only running at 70% and “probably” will not be repaired until early 2027.

Tanker Trackers reported that two Iranian supertankers carrying a total of 3.8mln barrels of crude oil passed through the US blockade.

Two US Senate Democrats are calling for US Energy Secretary Wright to abandon efforts to build a West Coast SPR, CNN reported. Democrats warned that establishing it this fiscal year would flout the law and usurp congressional authority.

TRADE/TARIFFS

The US delayed the blacklisting of China’s DeepSeek and over 100 Chinese firms deemed national security risks, to avoid escalating tensions with Beijing, according to sources cited by Reuters.

NOTABLE EUROPEAN DATA RECAP

UK Inflation Rate YoY (May) Y/Y 2.8% vs. Exp. 3% (Prev. 2.8%); Services 3.7% (exp. 3.7%, prev. 3.2%).

UK Inflation Rate MoM (May) M/M 0.2% (Prev. 0.7%).

UK Core Inflation Rate YoY (May) Y/Y 2.6% vs. Exp. 2.7% (Prev. 2.5%, Low. 2.6%, High. 3.0%).

UK Core Inflation Rate MoM (May) M/M 0.3% (Prev. 0.7%).

EU Inflation Rate YoY Final (May) Y/Y 3.2% vs. Exp. 3.2% (Prev. 3%, Low. 3.2%, High. 3.2%).

EU Inflation Rate MoM Final (May) M/M 0.1% vs. Exp. 0.1% (Prev. 1%, Low. 0.1%, High. 0.1%).

EU Core Inflation Rate YoY Final (May) Y/Y 2.6% vs. Exp. 2.5% (Prev. 2.2%).

The Riksbank left rates unchanged at 1.75%, as expected, stating probability of a hike in 2026 has increased relative to the March assessment. The Bank stated that the range of potential outcomes for what can happen going forward is wide and the Riksbank is highly prepared to adjust monetary policy.

NOTABLE US HEADLINES

US admin officials weighed how to structure government stakes in major AI companies, according to Semafor. Treasury Secretary Bessent favoured using equity in AI firms to seed Trump Accounts.