GOLD CLOSED CLOSED DOWN $52.45 TO $4131.65

SILVER CLOSED DOWN $3.67 TO $61.98

WE HAVE NOW ENTERED OPTIONS EXPIRY WEEK: COMEX OP EX EXPIRES ON THIS THURSDAY. LONDON/OTIC LBMA OPTIONS EXPIRY ON FIRST DAY NOTICE THIS COMING TUESDAY.

ACCESS MARKET

GOLD $4120.50 3:30 PM)

SILVER: 61.66 3;30 PM)

Bitcoin morning price:$62,316 DOWN 2029 DOLLARS (MANY SWITCHING TO PHYSICAL GOLD)

Bitcoin: afternoon price: $62,317 DOWN 2030 DOLLARS

Platinum price closing DOWN $2.00 TO $1666.50

Palladium price; DOWN $24.00 TO $1240.50

JUNE 23

EXCHANGE: COMEX

CONTRACT: JUNE 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,181.900000000 USD

INTENT DATE: 06/22/2026 DELIVERY DATE: 06/24/2026

FIRM ORG FIRM NAME ISSUED STOPPED

092 C DEUTSCHE BANK 200

099 H DEUTSCHE BANK AG 94

152 C DORMAN TRADING, LLC 1

357 C WEDBUSH SECURITIES 1

363 H WELLS FARGO SECURITI 35

435 H SCOTIA CAPITAL (USA) 734

661 C JP MORGAN SECURITIES 315

732 C RBC CAP MARKETS 506

737 C ADVANTAGE FUTURES 19

905 C ADM 1

991 H CME 6

TOTAL: 956 956

MONTH TO DATE: 38,174

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2026: 956 CONTRACTs NOTICES FOR 95,600 OZ or 2.97356 TONNES

total notices so far: 38,154 contracts FOR 3,815,400 OZ OR 115 TONNES

SILVER NOTICES: 14 NOTICE(S) FILED FOR 70,000 OZ /

total number of notices filed so far this month : 2423 CONTRACTS (NOTICES) for 12.115 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF XX CONTRACTS OR XXX OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 70,000 OZ//NEW STANDING ADVANCES TO 12.135 MILLION OZ//

SUMMARY OF OUR JUNE 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE. 49.390 MILION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 70,000 OZ//NEW STANDING ADVANCES TO 12.135 MILLION OZ

GOLD//OUTLINE

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT 2.9548 TONNES OF A QUEUE JUMP/NEW STANDING ADVANCES TO 118.799 TONNES

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 2.9548 TONNES//NEW STANDING ADVANCES TO 118.799 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 102.992 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A SMALL 278 CONTRACTS TO AN OI OF 108,758.

EFP ISSUANCE 2015 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 2015 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 134 CONTRACTS AND ADD TO THE 2015 E.FP. ISSUED

WE OBTAIN A HUGE GAIN OF 1880 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $1.11

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 9.440 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $1.11

2.ASIAN AFFAIRS JUNE 23 /2025

SHANGHAI CLOSED DOWN 58.84 PTS OR 1.37%

HANG SENG CLOSED DOWN 432/24 PTS OR 1.82%

Nikkei CLOSED DOWN 2505.96 PTS OR 3.46%

//Australia’s all ordinaries CLOSED DOWN 0.92%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7850

/ OFFSHORE CLOSED DOWN AT 6.7883 Oil DOWN TO 73.79 dollars per barrel for WTI and BRENT UP TO 77.86 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7850) OFFSHORE YUAN TRADING DOWN TO 6.7883 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG 7408 CONTRACTS TO 350,660 WELL ABOVE ITS NEW LOW OF 326,052 OI SET JUNE 3, CLOSE TO THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND CLOSE TO THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,052 //JUNE 3 2026 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD NO T.A.S. LIQUIDATION DURING MONDAY’S COMEX TRADING JUNE 22!!. IT SEEMS THAT MANY OF THE SPECULATORS HAVE NOW CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT WITH THE BANKERS NOW PROVIDING THE PAPER,AND CENTRAL BANKS DOING THEIR QUEUE JUMPING IN AN INCREASING MANNER

CENTRAL BANKS TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS JUNE CONTRACT MONTH!!

THE STRONG SIZED GAIN ON OUR TWO EXCHANGES (9628 CONTRACTS) OCCURRED WITH OUR GAIN IN PRICE IN GOLD (DOWN $36.85)

WE THUS HAD A STRONG SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 9628 CONTRACTS (OR 29.940 TONNES) WITH OUR GAIN IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 2220 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIDAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH JUNE

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

JUNE: 0 SO FAR!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO JUNE:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 146+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO SO FAR

DETAILS ON OUR NEW JUNE COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG GAIN ON OUR TWO EXCHANGES OF 9628 CONTRACTS WITH OUR GAIN IN PRICE ($36.85). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A SMALL SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 889 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

JUNE: ZERO SO FAR.

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 146+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO. WE WILL KNOW IN JUNE WHETHER THEY COVERED ANY OF THEIR SHORTFALL.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 2.9548 TONNES//NEW STANDING ADVANCES TO 118.799 TONNES// TOTAL QUEUE JUMPING FOR THE MONTH; 54.1708 TONNES OR AVERAGING 3.419 TONNES PER DAY IN JUNE.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JUNE,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $135.40)

WE HAD NO T.A.S. SPREADER LIQUIDATION MONDAY // COMEX SESSION// WITH OUR GAIN IN PRICE , OUR SPECULATORS WENT TO THE SHORT SIDE LED BY THE NOSE BY OUR HIGH FREQUENCY MOMENTUM PLAYERS WITH CENTRAL BANKERS TAKING THE LONG SIDE. THE SPECS WILL BE ANNIHILATED.

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING //TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $36.85

WE HAD 107 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES: 9628 CONTRACTS OR 962,800 OZ (29.940 TONNES)

JUNE DELIVERY MONTH

JUNE 23

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 ENTRIES i) Out of JPMorgan: 106,902.075 oz (3325 kilobars) total withdrawal 106,902.075 oz 3.325 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER//gold ENTRIES: 1 i) Into Delaware: 1209.173 oz total deposit: 1209.173 oz xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 956 CONTRACTS OR 95,600 OZ 2.97386 TONNES OF GOLD |

| No of oz to be served (notices) | 20 Contracts 2000 OZ 0.06222 TONNES |

| Total monthly oz gold served (contracts) so far this month | 38,124 notices 3,721,800 oz 118.7390 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

ENTRIES: 1

i) Into Delaware: 1209.173 oz

total deposit: 1209.173 oz

xxxxxxxxxxxxxxxxxx

comex withdrawal

1 ENTRIES

i) Out of JPMorgan: 106,902.075 oz

(3325 kilobars)

total withdrawal 106,902.075 oz

3,325 tonnes

adjustments: 0//

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JUNE OI STANDS AT 976 CONTRACTS HAVING A GAIN OF 322 CONTRACTS.

WE HAD 628 CONTRACTS SERVED ON MONDAY, SO WE GAINED 950 CONTRACTS OR 95,000 OZ. (2.9548 TONNES) EXERCISED A QUEUE JUMP WHERE THEY WILL TAKE PHYSICAL GOLD ON THIS SIDE OF THE POND. THIS IS NO DOUBT CENTRAL BANKS STANDING FOR PHYSICAL GOLD.

JULY GAINED 1252 CONTRACTS UP TO 7002 CONTRACTS.

AUGUST GAINED 4420 CONTRACTS TO AN OI OF 269,074

.

We had 956 contracts filed for today representing 95,600oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 956 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 315 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (38,174) to which we add the difference between the open interest for the front month of JUNE(976 CONTRACTS) minus the number of notices served upon today 956 x 100 oz per contract) equals 3,819,400 OZ OR (118.799 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (38,174) to which we add the difference between the open interest for the front month of JUNE( XXX CONTRACTS) minus the number of notices served upon today 956 x 100 oz per contract) equals 3,819,400 OZ OR (118.799Tonnes of gold)

new total of gold standing in JUNE becomes 118.799 TONNES//

TOTAL COMEX GOLD STANDING FOR JUNE 118.799 TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS ACTIVE DELIVERY MONTH OF JUNE.

confirmed volume MONDAY confirmed 198,220// poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,693,905.420 oz 52.687 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,693.905.420 tonnes oz 52.687 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 27,882,226.857 oz

TOTAL REGISTERED GOLD 14,985,376.491 tonnes (466.108 tonnes)

TOTAL OF ALL ELIGIBLE GOLD 12,897,250.366 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,290,262oz ((REG GOLD- PLEDGED GOLD)=

413.382 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JUNE DELIVERY MONTH

JUNE 23

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 entries |

| Deposits to the Dealer Inventory | 0 entries |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT TWO ENTRIES i) Into Asahi 297,117.700 oz ii) Into CNT 599,473.810 oz total deposit: 896,591.510 oz ONE ENTRY i)Into Asahi: 602,315,390 oz total deposit: 602,315.330 oz |

| No of oz served today (contracts) | 14 CONTRACT(S) (70,000 OZ) |

| No of oz to be served (notices) | 4 Contract (20,000 oz) |

| Total monthly oz silver served (contracts) | 2423 contracts 12.115 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRIES

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRY:2

TWO ENTRIES

TWO ENTRIES

i) Into Asahi 297,117.700 oz

ii) Into CNT 599,473.810 oz

total deposit: 896,591.510 oz

i)Into Asahi: 602,315,390 oz

total deposit: 602,315.330 o

total deposit 605,069.076 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

0 entries

adjustments 1

dealer to customer:

Brinks 33.157.800 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 86.213 MILLION OZ//.TOTAL REG + ELIGIBLE. 322,822 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE /2026 OI: 18 OPEN INTEREST CONTRACTS FOR A GAIN OF 12 CONTRACTS.

WE HAD 2 NOTICES SERVED ON MONDAY SO WE GAINED 14 CONTRACTS OR AN ADDITIONAL 70,000 OZ WILL STAND AS A QUEUE JUMP AT THE SILVER COMEX.

JULY SAW A LOSS OF 6095 CONTRACTS DOWN TO 33.165 CONTRACTS.

AUGUST SAW A GAIN 0F 230 CONTRACTS UP TO 1212…

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 14 or 70,000 OZ oz

CONFIRMED volume MONDAY; 93,353// EXCELLENT

XXX

AND NOW JUNE. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 2423 X5,000 oz = 12.114 MILLION oz

to which we add the difference between the open interest for the front month of JUNE(18) AND the number of notices served upon today (14 )x (5000 oz)

Thus the standings for silver for the JUNE 2026 contract month: (2423 )Notices served so far) x 5000 oz + OI for the front month of JUNE ( 18) minus number of notices served upon today (14)x 5000 oz equals silver standing for the JUNE..contract month equating to 12.135 MILLION OZ.+

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 86.213 million oz of registered silver

JPMorgan as a percentage of total silver: 138.479/322.82 million: 42.72%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JUNE 23 /2026/WITH GOLD DOWN $52;75 /HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.71 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1022.20 TONNES

JUNE 19 /2026/WITH GOLD UP $36.85 /HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 7.421 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1020.49 TONNES

JUNE 18 /2026/WITH GOLD DOWN $135.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.856 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1013.069 TONNES

JUNE 17 /2026/WITH GOLD UP $20.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.427 TONNES OF GOLD FROM THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1012.213 TONNES

JUNE 16 /2026/WITH GOLD UP $4.45 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 15 /2026/WITH GOLD UP $111.10 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 12 /2026/WITH GOLD UP $123.30 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 11 /2026/WITH GOLD DOWN $15.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.855 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 10 /2026/WITH GOLD DOWN $153.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.426 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1016.495 TONNES

JUNE 9 /2026/WITH GOLD DOWN $75.60 TODAY/NO CHANGES IN GOLD AT THE GLD:// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 8 /2026/WITH GOLD DOWN $3.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 6.936 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 5 /2026/WITH GOLD DOWN $134;85 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 4 /2026/WITH GOLD UP $39.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.143 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 3 /2026/WITH GOLD DOWN $51.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.856 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.000 TONNES

JUNE 2 /2026/WITH GOLD UP $7.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.712 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.856 TONNES

JUNE 1 /2026/WITH GOLD DOWN $79.30 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 29 /2026/WITH GOLD UP $59.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

GLD INVENTORY: 1022.20 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JUNE 123 WITH SILVER DOWN $3.67: : HUGE CHANGES IN INVENTORY AT THJE SLV A DEPOSIT OF 2.714 MILLION OZ INTO THE SLV/./ // :INVENTORY RESTS AT 483.016 MILLION OZ

JUNE 19 WITH SILVER UP $1.11: : NO CHANGES IN INVENTORY AT THJE SLV/./ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 18 WITH SILVER DOWN $4.80: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: HUGE CHANGES IN INVENTORY A WITHDRAWAL OF 1.086 MILLION OZ FROM THE SLV././ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 17 WITH SILVER UP $0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: NO CHANGE IN INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 16 WITH SILVER DOWN $0.13: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.362 MILLION OZ INTO THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 15 WITH SILVER UP $3.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.357 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 481.026 MILLION OZ

JUNE 12 WITH SILVER UP $3.34: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.769 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 482.383 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.12: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.226 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.152 MILLION OZ

JUNE 10 WITH SILVER DOWN $0.50: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.909 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.378 MILLION OZ

JUNE 9 WITH SILVER DOWN $3.35: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.407 MILLION OZ INTO INTO THE SLV /./ // :INVENTORY RESTS AT 484.287 MILLION OZ

JUNE 8 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 543,000 OZ FROM THE SLV /./ // :INVENTORY RESTS AT 482.880 MILLION OZ

JUNE 5 WITH SILVER DOWN $4.86: NO CHANGES IN SILVER INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 4 WITH SILVER UP $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.432 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 3 WITH SILVER DOWN $2.55: NO CHANGES IN SILVER INVENTORY AT THE SLV >> /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

CLOSING INVENTORY 480.302 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD.

The Burnham shoe-in

Andy Burnham is obviously a smart political operator, having engineered his prime ministership without even being challenged. But will he succeed where Starmer failed?

| Alasdair MacleodJun 23∙Paid |

Inevitably, unless it is for pure pursuit of power, people seek high office “to make a difference”. Either way, it involves increased government spending. For Burnham, it’s been such a rush that initially he favoured one thing, such as refusing to be constrained by bond markets, before retracting his opinion when someone pointed out to him the dangers. Instead, he now says that he will be bound by current treasury fiscal rules.

In an attempt to bolster his economic credibility, he has appointed three eminent economists as advisers: Andy Haldane, Richard Hughes, and Lord O’Neill. Haldane is sound, Hughes is anodyne, and O’Neill is an ex-Goldman Sachs macroeconomist with Keynesian leanings. Their advice is likely to be inconsistent, and if I was Haldane, I would distance myself from this circus act.

The chart below sums up Burnham’s problem. He will have great difficulty funding an O’Neill stimulus.

According to an article in today’s Daily Telegraph by Adam Smith (yes, that is his name and as a Tory MP he was a former Chief Secretary to the Treasury) O’Neill is pushing the line that “Britain needs to be much bolder to invest”. Put another way, O’Neill is displaying his Keynesian statist credentials. And as a fellow Mancunian with an impeccable macroeconomic pedigree, there can be no doubt that this is the line Burnham is inclined to take.

This brings us back to the observation that as prime minister he will want to make a difference, which for statists is always more spending, taxing those with wealth to give, and the suppression of free markets.

The international threat

While the UK media is totally absorbed by the leadership crisis, a greater threat to Burnham’s plans whatever they may be comes from abroad. Pretty much all G7 nations face similar problems centred on intractable government deficits and excessive debt-to-GDPs. A crisis in anyone of them, odds-on being Japan, will have a major impact on UK bond markets. Sanae Takaichi, the prime minister, is following O’Neill’s spending policies with a fiscal supplementary budget. It will be interesting to see how that turns out, but so far it is fuelling a developing bond and currency crisis that is likely to lead to Japan’s institutions withdrawing from international capital markets with knock-on consequences for the other G7s including the UK.

It would be a mistake to dismiss the fragility of all G7 economies, made particularly more so by the needless war against Iran. For the avoidance of doubt, Iran won hands down and has the upper hand in negotiations. Israel is panicking and disruptive, while the US electorate, believing Trumpian propaganda, is yet to take the consequences seriously. But you don’t need to have an enormous brain to understand that G7 economies will slump and budget deficits soar. In addition to all G7 currencies being expanded by the increasing disparity between government revenue and welfare obligations, the temptation to follow the O’Neill/Takaichi Keynesian remedy of supporting bankrupted zombies without limit will prove irresistible.

The additional credit in the form of base money will be printed, undermining their purchasing powers. The comparison with the October-1973 oil crisis is stark in its message for today.

Of course, Burnham will be able to blame his woes on “events”. But the greatest failure of the British economy in recent history will be on his watch.

END

3. CHRIS POWELL AND HIS GATA DISPATCHES

Help us in the struggle for free and transparent markets in the monetary metals

Submitted by admin on Mon, 2026-06-22 12:18 Section: Daily Dispatches

12:19p ET Monday, June 22, 2026

Dear Friend of GATA and Gold (and Silver):

The last year has been dramatic for the monetary metals. Sharp increases in price, indicative of short squeezes, have been offset by counterintuitive downward smashes even as a major war has broken out while another has intensified. News reports and analysis have emphasized the role of some central banks as major longs in the gold and silver markets but not the continuing role of other central banks on the short side in defense of their currencies and particularly the U.S. dollar.

The Gold Anti-Trust Action Committee long has focused on the monetary metals markets — not just the public activity but also the surreptitious activity, which is usually more influential. We have alerted investors, elected officials, financial journalists, and even central banks themselves to many things they would not have known otherwise. By exposing the government-engineered short position in gold and celebrating the virtues of the monetary metals, including their protection of individual liberty, GATA has spurred demand for the metals and the shares of gold and silver mining companies.

…

We sometimes have been able to break through the blackout that many mainstream financial news organizations have imposed on the gold and silver manipulation issue, as we broke through a few weeks ago with this report in Canada’s Financial Post:

We have detailed and publicized the monthly interventions against gold undertaken by the Bank for International Settlements on behalf of their central bank members, interventions that seem to correlate with smashes in the gold price:

We have spread the word at financial conferences around the world —

— and through many programs on YouTube, like this one:

We have maintained and updated our master compendium of the documentation that confirms gold price suppression policy, a compendium that is the only such work in the world:

And with daily dispatches we have kept our supporters informed about important developments in gold and silver:

If you’re not already on our dispatch list, please subscribe. It’s free:

But the struggle for free and transparent markets in the monetary metals and for limited and accountable government everywhere is not yet won, even as it can be won if enough people around the world support the cause. We need your help to continue. We get no support from the World Gold Council, which has a huge budget financed by large mining companies and which should be doing the work we have been doing but is too timid to challenge the enemies of free and transparent markets and sometimes seems aligned with them.

We’re still up against enormous undemocratic financial and political power. So please consider supporting GATA financially:

Donations of $500 or more will entitle the donor to a beautiful 1-ounce silver round commemorating GATA’s work:

https://www.gata.org/sites/default/files/GATA-silver-round-front.png

We very much need your help now.

With good wishes.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4. ANDREW MAGUIRE/LIVE FROM THE VAULT; 277

LAST WEEK 276

5. COMMODITY REPORT//GOLD/ZERO HEDGE

China Gold Imports Soar To Two Year High, As Hong Kong Gold Bar Imports Surge Ahead Of Clearing System Launch

Monday, Jun 22, 2026 – 06:50 PM

China’s monthly gold imports reached their highest in more than two years in May, showing the world’s biggest buyer’s appetite for bullion remained resilient as prices remained under pressure; the number prompted some to scratch their heads as to where all this gold is going in light of tepid official central bank purchases, coupled with the lowest gold withdrawals from the Shanghai Gold Exchange since the covid outbreak.

As Bloomberg reports, imports were around 163 tons last month, the highest since March 2024, according to customs data released on Saturday. Volumes for the first five months of 2026 were about 692 tons, up by about 76% from a year earlier.

Chinese demand for physical bullion bars, as well as metal linked to gold accumulation plans (low-barrier products that allow investors to buy gold incrementally), have been among the main drivers of the surge, said Song Jiangzhen, a researcher at the Guangzhou Southern Gold Market Academy.

China also started implementing a new import licensing regime for gold from June 1, with certain banks facing fewer restrictions. But the change may have prompted some banks to use up their existing quotas before the new system began, Song said.

Curiously, in its latest official monthly update, China’s central banb, the People’s Bank of China (PBoC) only increased its gold reserves by nearly 10 tonnes last month, its 19th consecutive month of bullion purchases. The State Administration of Foreign Exchange (SAFE) announced on Sunday that China’s official gold reserves rose by 320,000 troy ounces or 9.95 tonnes in May to a total of 74.96 million troy ounces or 2331.52 tonnes.

China’s total foreign exchange reserves rose to $3.4422 trillion at the end of May, increasing by $31.7 billion or 0.93% from April. This is the highest level for China’s FX reserves since November 2015; they have remained above $3.3 trillion for the past 10 months.

SAFE attributed the growth of reserves to a number of factors, including a firmer US Dollar Index and rising global asset prices, adding that China’s sound economic momentum has underpinned the stability of its reserves.

Experts have noted that China’s rising foreign exchange reserves are closely linked to the country’s export performance. China’s total foreign trade in the first four months of 2026 rose to $2.39 trillion, an increase of 14.9% year-on-year, with exports rising by 11.3% percent to $1.37 trillion and imports rising 20% percent to $1.01 trillion, according to the latest data from China’s General Administration of Customs

According to the latest central bank gold purchase tracker from Goldman, of the 59 tonnes of gold purchased by central bank in April, China’s PBOC was estimated to have bought 24 tonnes of gold, or well below the recent pace of imports which are about 5x greater. While the pace of central bank gold purchases has moderated to ~50 tonnes/month on a 3-month (seasonally adjusted) and 12-month moving average basis, Goldman views the ongoing diversification trend as structural.

Goldman remains bullish on gold, with continued central bank diversification the main structural driver of the bank’s constructive base case for gold prices, contributing 9% to its forecast for appreciation by Dec26. As we highlighted last week, a recent World Gold Council survey supports Goldman’s optimistic view: a record 45% of the 76 central banks surveyed between February and May expect to increase their own gold reserves over the next 12 months, while ~90% expect global reserves to rise with the remainder expecting broadly stable holdings. As a result, Goldman assumes continued central bank accumulation of 50t/month in 2026 and 40t/month in 2027.

Meanwhile, as Kitco notes, China’s domestic gold market has shown definite signs of cooling in recent weeks.

“Amid heightened market uncertainty, gold ETFs have seen an overall reduction in assets under management, with several funds experiencing significant net outflows,” noted a report from Gelonghui Finance. “As of June 3, 14 gold ETFs recorded combined net outflows exceeding RMB 10 billion [$1.48 billion] over the past month.”

“The previously widely accepted investment view of ‘buying on dips amid falling gold prices’ has started to face divergence under current volatile market conditions,” they added.

Gold prices have retreated by about a quarter from the record highs reached in January, weighed down by EM selling (most notably Turkey in the early days of the Iran war), and global inflation fears amid the war in the Middle East which have pushed the US dollar sharply higher. While strong buying from Chinese consumers was a key catalyst for the January frenzy, domestic demand has since moderated, but without a major slump.

Adding to the mathematical mystery, the latest numbers from the Shanghai Gold Exchange (SGE) showed that gold withdrawals in May totaled only 63.5 tonnes – the lowest level since February of 2020 during the first wave of the COVID-19 outbreak, and around half of what they were in March of this year. Industry professionals told Gelonghui Finance that “while short-term gold price volatility may persist, the core rationale supporting gold’s strategic allocation value remains intact over the medium to long term.”

In other words, there appears to be a gap between near record imports, tepid official central bank demand, and muted gold withdrawals from the SGE.

This is not a new development: as we documented previously, China is well known for indicating just modest central bank purchases, even as total Chinese purchases of gold on the London OTC market are orders of magnitude higher.

Separately, Bloomberg also reported that at least four of the 11 banks participating in Hong Kong’s new gold clearing system are importing large bullion bars in preparation for the mechanism’s planned launch in July.

Traders are receiving orders from some of the clearing banks to move 400-ounce gold bars into the city, Bloomberg reported citing people familiar with the matter. The bars meet the London Good Delivery industry standard.

The 400-ounce bars are typically traded by banks and sovereign entities in London, the world’s largest bullion trading hub, but are less common in the Asian market, which is dominated by much smaller kilobars. The banks need to build up inventories to allow for physical delivery when clearing begins next month.

By launching its gold clearing system, Hong Kong is securing first-mover advantage in a push to become Asia’s preeminent hub for bullion trading. Last week, Singapore announced its own plans to launch a clearing mechanism by the end of the year.

Both cities are aiming to capitalize on strong demand in Asia, where many investors remain bullish about the long-term prospects for the precious metal as an alternative store of wealth despite the recent drop in price as the war in the Middle East fanned concerns around inflation and higher interest rates.

In an emailed response to questions, a spokesperson for the government agency behind the system, known as the Financial Services and the Treasury Bureau, said the clearing company had been “working closely with the market to formulate the framework and rules of the clearing system” and that preparatory work had entered its final stage.

Eleven banks are on the board of the Hong Kong Precious Metals Central Clearing Company. Some of these lenders will become clearing banks from the launch, whereas others will take longer to build up their bullion capacity. While Hong Kong plans to start by using the London Good Delivery standard, its future plans are still to be decided, the people said.

In Singapore, the clearing system will be aligned with the London Good Delivery framework for large bars, as well as delivery and settlement standards for kilobars adopted by major exchanges in Chicago and Shanghai.

END

COMMODITY: RARE EARTHS

MP Materials’ Lawsuit Against USA Rare Earth Highlights Battle For America’s Future In Minerals

Tuesday, Jun 23, 2026 – 12:30 PM

USA Rare Earth has dismissed a lawsuit filed by MP Materials, calling the claims “completely without merit” and arguing the case is an attempt to slow its growth. The company said it will deny all allegations that it improperly obtained confidential information from a former MP employee, according to Bloomberg.

The dispute underscores intensifying competition in the U.S. rare-earth sector, where both companies are racing to build domestic mining, processing, and magnet-production capabilities. USA Rare Earth said MP is trying to impede its progress as it develops the Round Top deposit in Texas and a magnet facility in Oklahoma.

Bloomberg writes that MP sued last month, alleging a coordinated effort by USA Rare Earth to recruit MP employees and misuse proprietary information. The lawsuit also questioned the viability of USA Rare Earth’s projects. MP declined to comment on the latest filing.

The clash comes as billions of dollars flow into the U.S. rare-earth industry amid efforts to reduce reliance on China, which continues to dominate global supply chains for the critical minerals.

Rare earth minerals have become increasingly important to the United States because they are essential components in advanced technologies, including electric vehicles, semiconductors, robotics, aerospace systems, and military equipment. Materials such as neodymium, praseodymium, dysprosium, and terbium are critical for manufacturing high-performance magnets used in everything from fighter jets and missile guidance systems to wind turbines and data centers.

The strategic importance of rare earths has grown as the U.S. seeks to reduce its dependence on China, which currently dominates global rare earth mining, processing, and magnet production. Supply chain disruptions and export restrictions have heightened concerns among policymakers and industry leaders, prompting significant investments in domestic mining, processing, and manufacturing capabilities. Companies such as MP Materials and USA Rare Earth are at the forefront of efforts to establish a secure and resilient American rare earth supply chain.

Under the Trump administration, rare earth minerals have become a central component of broader efforts to strengthen U.S. energy security, industrial competitiveness, and national defense. Recent policy initiatives and government support have accelerated domestic rare earth development, reflecting a growing consensus that securing access to these critical minerals is essential for maintaining America’s technological leadership and reducing strategic vulnerabilities.

END

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 56.84 PTS OR 1.37%

HANG SENG CLOSED DOWN 432/24 PTS OR 1.82%

Nikkei CLOSED DOWN 2505.96 PTS OR 3.46%

//Australia’s all ordinaries CLOSED DOWN 0.92%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7850

/ OFFSHORE CLOSED DOWN AT 6.7883 Oil DOWN TO 73.79 dollars per barrel for WTI and BRENT UP TO 77.86 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7850) OFFSHORE YUAN TRADING DOWN TO 6.7883 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.7850

OFFSHORE YUAN: DOWN TO 6.7883

1.HANG SANG CLOSED DOWN 432.24 PTS OR 1.82%

2. Nikkei closed DOWN 2505.96 PTS OR 3.46%

WEST TEXAS INTERMEDIATE OIL DOWN TO 73.79

BRENT; 77.86

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 100.98/// EURO FALLS TO 1.13999 DOWN 27 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.684 UP 1/10 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA CROSS NOW AT 161.47… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.849 DOWN 2 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN( 6.7850) AND OFFSHORE: DOWN AT 6.7883

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.9643// Italian 10 Yr bond yield DOWN to 3.637// SPAIN 10 YR BOND YIELD DOWN TO 3.384%

3i Greek 10 year bond yield DOWN TO 3.584%

3j Gold at $4118 //Silver at: 62.08 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 42/ 100 roubles/74.66

3m oil (WTI) into the 73 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 161.728 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.684% UP 1/10 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.849 DOWN 2 PTS..: USA/SF this 0.8100 as the Swiss Franc . Euro vs SF: 0.9235

USA 10 YR BOND YIELD: 4.487 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.940 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.196 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 46.48 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.7738 DOWN 6 PTS

30 YR UK BOND YIELD: 5.475 DOWN 6 BASIS PTS

10 YR CANADA BOND YIELD: 3.438 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 3.055 DOWN 3 BASIS PTS.

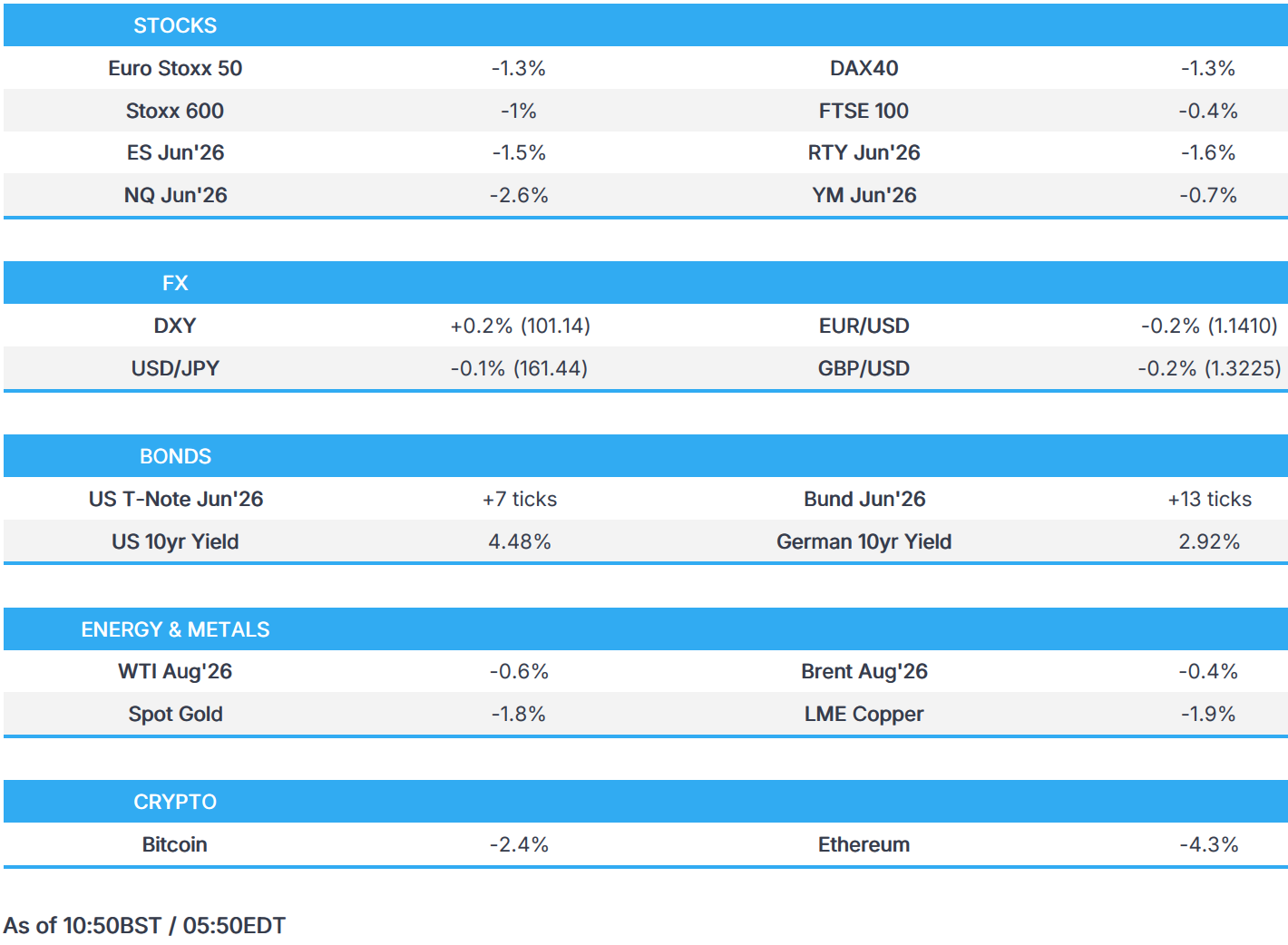

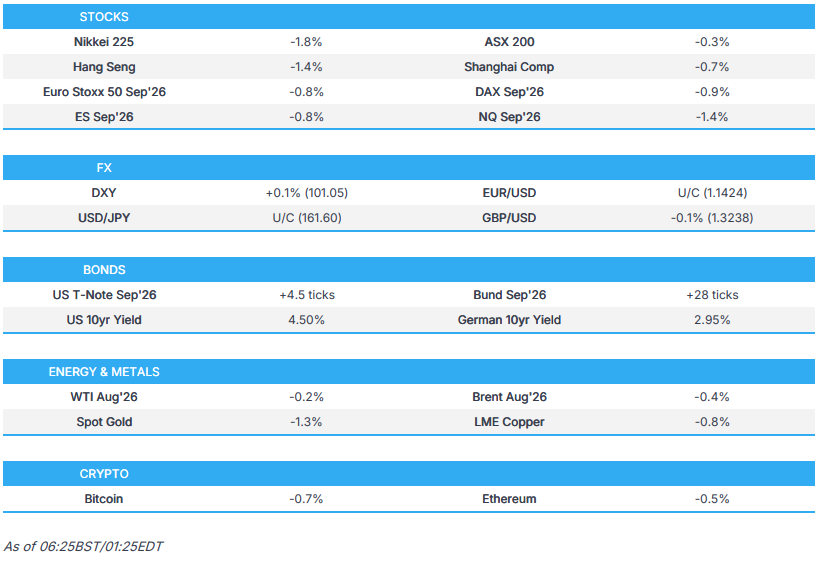

Futures Slide As Tech Tumbles, Korea Crashes

Tuesday, Jun 23, 2026 – 07:59 AM

US equity futures are sharply lower as a Semis/South Korea-induced selloff has spread globally slamming tech stocks and pushing SpaceX 3% lower and below its first day of trading price of $150. Nasdaq stocks lead sentiment and early trading lower with AI cost concerns back in focus, as Bloomberg notes that traders are pointing to a South Korean media report we first highlighted at 8pm last night, saying SK Hynix is slowing expansion of AI memory chip production and shifting emphasis to commodity DRAM. As of 8:00am S&P futures were -1.3%, and Nasdaq futures tumbled 2.7%, both near session lows. In premarket trading, Intel and Micron led a broader decline among chipmakers while SpaceX fell 4.3%, below its $150 initial trade price. Chinese equities in Hong Kong entered a bear market. Mag7s are dragging the indices lower with MSFT / telecom the safety valve. In Seoul, chip giants SK Hynix Inc. and Samsung Electronics Co. slumped more than 10%. According to JPM, today’s sell-off “may reflect anxiety into MU’s print on Weds as well as the levered ETF mkt structure.” Bonds are operating as a safety haven as the yield curve bull steepens, and USD is bid. Commodities are seeing further declines in Energy as US / Iran discussions continue and precious metals are getting hit due to USD (gold) and AI / Tech (silver). Ags are mixed. Today’s macro data focus is on Flash PMIs, ADP’s weekly employment print, and regional Fed activity indicators.

In premarket trading, chipmakers, memory stocks and other AI-related firms slide during the broader selloff. Decliners include Micron (MU -7%), Intel (INTC -6%), AMD (AMD -6%) and CoreWeave (CRWV -5%).

- Nvidia leads most of the Magnificent Seven group lower (Nvidia -2%, Tesla -2%, Meta -0.6%, Microsoft +1%, Apple -0.3%, Amazon -0.6%, Alphabet -2%,)

- Avis Budget (CAR) climbs 4% as the rental car company entered into a settlement agreement with Pentwater Capital Management and affiliated persons to resolve a lawsuit seeking recovery of short-swing profits, the company said in a filing.

- Best Buy (BBY) falls 3% after the company said Matt Bilunas will step down as CFO and depart the retailer at the end of July after 20 years, including seven years as CFO.

- Edgewell Personal Care (EPC) rises 9% after people familiar with the matter said the maker of Schick razors has rejected an unsolicited takeover offer from private equity firm Yellow Wood Partners.

- IBM (IBM) gains 4% as JPMorgan upgrades to overweight and as the company announced it has joined the OpenAI Daybreak Cyber Partner Program.

- Primoris Services (PRIM) sinks 35% after the infrastructure construction company cut its adjusted earnings guidance for the full year.

In other corporate news, Oracle reduced its workforce by 21,000 employees in the past 12 months, a wider scale than previously known, including those whose jobs were eliminated by the use of AI. SoftBank’s founder said there’s little merit to building data centers in space, while acknowledging that AI competition is intensifying.

In an ugly session that started with a rout in South Korea, the Kospi finished down 10% while Nasdaq 100 contracts lose 2.5% and are struggling to find a floor. European stocks are not immune with the Stoxx 600 down 1%. Other assets have been caught up in the equity selloff with spot silver down over 4% and Bitcoin dropping 3%. Memory stocks, many of which are riding triple-digit gains this year, recorded some of the steepest losses. SpaceX was poised to fall below its first-day opening price of $150.

In Seoul, chip giants SK Hynix Inc. and Samsung Electronics Co. slumped more than 10%. Intel Corp. and Micron Technology Inc. led a broader decline among chipmakers in US premarket trading, while SpaceX fell 4.3%. Chinese equities in Hong Kong entered a bear market.

BofA equity derivative strategists said the Nasdaq 100’s heavy concentration in technology stocks has fueled its outperformance versus the S&P 500 in both returns and volatility. That’s pushed the Nasdaq’s Bubble Risk Indicator (BRI) closer to a key level which often signals elevated near-term tail risks. Meanwhile, already jittery tech sentiment and volatility could turn on a dime after Micron’s earnings tomorrow. The chipmaker has been the largest contributor to S&P 500 gains this year, while technology stocks make up each of the index’s 10 biggest drivers of returns.

“Some of the recent performance in stocks has been highly speculative, fueled by a passion from retail investors for short-term gains,” Mark Dowding, chief investment officer for fixed income at RBC BlueBay Asset Management, told Bloomberg TV. “We may not like it this morning, but actually it’s healthy behavior.

The market selloff “is largely a blip, but it is tapping a real and more fundamental anxiety,” said Amanda Lyons, head of research at Energy Group Capital. “The blip part: it is a single piece of local trade press, landing into a jumpy tape and a day before a nervous Micron print, on a trade that is about as crowded and as priced-for-perfection as anything in the market.

One regular buyer of stocks, the corporates themselves, are exiting for the time being. Goldman’s Vani Ranganath estimates approximately 65% of companies have entered their blackout window ahead of 2Q results.

For the AI trade, attention is now shifting to Micron’s quarterly results on Wednesday after the stock rallied more than 300% since January.

“The real test is Micron,” said Amanda Lyons, head of research at Energy Group Capital. “I would watch the rate of change in pricing and any change to capex or bit-supply guidance far more closely than the headline beat or miss.”

Fed’s Goolsbee said he remains concerned about inflation and questioned whether all the factors driving prices up are temporary. US Trade Representative Jamieson Greer kicked off talks with Indian officials this week as both sides stepped up efforts to resolve the remaining differences holding up an interim trade agreement.

In other assets, currency traders are on high alert for intervention after further weakness in the yen. Gold slides, with Deutsche Bank following Goldman in cutting price forecasts for the metal.

European equities fell sharply at the open on Tuesday: the Stoxx 600 falls 1.1% to 632.10, with mining and technology shares leading declines while health care and food beverage stocks are the biggest outperformers. Here are the biggest movers Tuesday:

- Porsche shares rise as much as 1.8%, erasing early declines after the German luxury carmaker confirmed its forecast for the 2026 financial year

- Basic resources stocks are falling the most in the Stoxx Europe 600, with the sector index down as much as 4.6%, as metals fell across the board on inflationary concerns and progress of peace talks

- Hermes shares fall as much as 2.9%, extending its drop to 11% over the past three sessions, after HSBC downgraded its rating on the Birkin bag maker to hold from buy

- Epiroc drops as much as 5.6%, the most in three months, as UBS downgrades the Swedish mining-equipment maker to sell from neutral and says its valuation “has gone too far”

- Signify plunges as much as 18% after the Dutch lighting manufacturer announced new medium-term targets and an updated dividend policy that analysts say would mean big cuts to shareholder payouts

- Telecom Plus shares plunge as much as 33%, sending shares to their lowest level since 2012. The company’s new five-year plan will see it invest with the ambition of improving growth and the quality of earning

- Dometic declines as much as 11%, the most since March, with Danske Bank cautioning its upcoming 2Q report will be held back by tough US markets for its RV and marine divisions

Earlier in the session, Asian stocks fell reversing the previous session’s gains as a selloff in technology shares weighed on regional markets. The MSCI Asia Pacific Index dropped as much as 3.6%, with SK Hynix and Samsung Electronics among the biggest drags. Most of the region’s major markets were in the red, led by declines in South Korea, Japan and China. A sub-gauge of information technology shares slid as much as 6.1%, after rallying 2.3% on Monday. South Korean stocks tumbled 10% from a record high as investors dumped chip heavyweights on concerns that the rally has become overstretched, prompting the local exchange to briefly halt program selling. Japanese equities slipped as some AI-related stocks fell following a selloff in US tech megacaps.

“I think our Asian markets are tracking a rotation already underway in the US rather than a fresh risk-off move,” said Billy Leung, an investment strategist at Global X Management. “Hyperscalers have been leading the pullback on AI capex concerns and negative cash flow concerns.”

In FX, the Bloomberg Dollar Spot Index gains 0.2% although the yen takes top place among the G-10 currencies, climbing a few pips against the greenback. The Aussie dollar is the weakest, falling 0.7%.

In rates, treasuries are richer across the curve with gains led by front-end and belly, as oil steadies and stock futures slump after a selloff in Korean chipmakers stoked concerns about the artificial intelligence trade. US yields richer by as much as 4bp across front-end and belly with 2s10s and 5s30s spreads steeper by 1bp and 3bp on the day; 10-year is around 4.48%, 3bp richer on the day with bunds and gilts in the sector outperforming by around 1bp: German and UK 10-year yields falling 3 basis points each. SpaceX shares fell to the lowest level since their first day of trading ahead of a potential jumbo investment-grade bond sale that could be announced Tuesday. Focal points of US session also include June preliminary PMIs and a 2-year note auction. This week’s Treasury auctions begin at 1pm New York time with $69 billion 2-year note sale, to be followed by 5- and 7-year notes Wednesday and Thursday; WI 2-year yield near 4.20% is ~13bp cheaper than the May auction, which stopped on the screws.

In commodities, Brent crude futures fall 1% to around $77 a barrel. Other assets have been caught up in the equity selloff with spot silver down over 4% and Bitcoin dropping 3%.

Today’s US economic data calendar includes weekly ADP employment change (8:15am), June Philadelphia Fed non-manufacturing activity (8:30am), June preliminary S&P Global US manufacturing and services PMIs (9:45am) and Richmond Fed manufacturing and business conditions indexes (10am). Fed speaker slate empty for the session.

Market Snapshot

Top Overnight News

- Korea’s KOSPI plummeted 9.99%, its steepest drop in more than three months, on Tuesday as overseas investors sold chipmakers following regulatory signals that the sector’s rally had gotten overheated. RTRS

- South Korea’s retail investors are ploughing profits from a world-beating stock market into an overheated property sector, confounding government efforts to cool real estate demand. FT

- Iran said $12 billion of its frozen funds were set to be released as part of ongoing talks with the US, with the two sides broadly signaling progress in negotiations to formally end their war. BBG

- The Trump administration and Qatar have warned the EU that it faces a gas supply crunch that would force up prices unless Brussels rewrites planned rules on methane emissions. BBG