GOLD CLOSED CLOSED DOWN $141.55 TO $3990.10

SILVER CLOSED DOWN $4.18 TO $57.70

WE HAVE NOW ENTERED OPTIONS EXPIRY WEEK: COMEX OP EX EXPIRES ON THIS THURSDAY. LONDON/OTIC LBMA OPTIONS EXPIRY ON FIRST DAY NOTICE THIS COMING TUESDAY.

ACCESS MARKET

GOLD $3981.75 3:30 PM)

SILVER: 56.67 3;30 PM)

Bitcoin morning price:$62,606 UP 289 DOLLARS (MANY SWITCHING TO PHYSICAL GOLD)

Bitcoin: afternoon price: $59,664 DOWN 2653 DOLLARS

Platinum price closed DOWN 98.00 to $1567.50

Palladium price; DOWN $81.00 TO $1159.00

JUNE 24

EXCHANGE: COMEX

CONTRACT: JUNE 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,129.900000000 USD

INTENT DATE: 06/23/2026 DELIVERY DATE: 06/25/2026

FIRM ORG FIRM NAME ISSUED STOPPED

092 C DEUTSCHE BANK 101

099 H DEUTSCHE BANK AG 48

363 H WELLS FARGO SECURITI 18

661 C JP MORGAN SECURITIES 120

686 C STONEX FINANCIAL INC 55

737 C ADVANTAGE FUTURES 4

905 C ADM 3

991 H CME 7

TOTAL: 178 178

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2026: 178 CONTRACTs NOTICES FOR 17,800 OZ or 0.5536 TONNES

total notices so far: 38,352 contracts FOR 3,835,200 OZ OR 119.290 TONNES

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000 OZ /

total number of notices filed so far this month : 2424 CONTRACTS (NOTICES) for 12.120 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF XX CONTRACTS OR XXX OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 45,000 OZ//NEW STANDING ADVANCES TO 12.180 MILLION OZ//

SUMMARY OF OUR JUNE 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE. 58.790 MILION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 745,000 OZ//NEW STANDING ADVANCES TO 12.180 MILLION OZ

GOLD//OUTLINE

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT 2.9548 TONNES OF A QUEUE JUMP/NEW STANDING ADVANCES TO 118.799 TONNES

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.5318 TONNES//NEW STANDING ADVANCES TO 119.331 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 106.071 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A SMALL 186 CONTRACTS TO AN OI OF 108,944

EFP ISSUANCE 1880 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1880 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 186 CONTRACTS AND ADD TO THE 1880 E.FP. ISSUED

WE OBTAIN A HUGE GAIN OF 2066 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS OF $3.67

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 10.330 MILLION PAPER OZ

OCCURRED DESPITE OUR LOSS IN PRICE.OF $3.67

2.ASIAN AFFAIRS JUNE 24 /2025

SHANGHAI CLOSED UP 4.56 PTS OR 0.11%

HANG SENG CLOSED UP 75.90 PTS OR 0.33%

Nikkei CLOSED DOWN 613.41 PTS OR 0.88%

//Australia’s all ordinaries CLOSED UP 0.05%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.8109

/ OFFSHORE CLOSED DOWN AT 6.8147 Oil DOWN TO 71.66 dollars per barrel for WTI and BRENT UP TO 75.18 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.8109) OFFSHORE YUAN TRADING DOWN TO 6.8147 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR 1507 CONTRACTS TO 352,167 WELL ABOVE ITS NEW LOW OF 326,052 OI SET JUNE 3, CLOSE TO THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND CLOSE TO THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,052 //JUNE 3 2026 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD HUGE T.A.S. LIQUIDATION DURING TUESDAY’S COMEX TRADING JUNE 23!!. IT SEEMS THAT MANY OF THE SPECULATORS HAVE NOW CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT WITH THE BANKERS NOW PROVIDING THE PAPER,AND CENTRAL BANKS DOING THEIR QUEUE JUMPING IN AN INCREASING MANNER

CENTRAL BANKS TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS JUNE CONTRACT MONTH!!

THE FAIR SIZED GAIN ON OUR TWO EXCHANGES (2497 CONTRACTS) OCCURRED WITH OUR LOSS IN PRICE IN GOLD (DOWN $52.85)

WE THUS HAD A FAIR SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 2497 CONTRACTS (OR 2.706 TONNES) DESPITE OUR LOSS IN PRICE, AS WE WERE INFORMED OF A SMALL CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 990 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIDAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH JUNE

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

JUNE: 0 SO FAR!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO JUNE:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 146+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO SO FAR

DETAILS ON OUR NEW JUNE COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR GAIN ON OUR TWO EXCHANGES OF 2497 CONTRACTS DESPITE OUR LOSS IN PRICE ($36.85). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A SMALL SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1008 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

JUNE: ZERO SO FAR.

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 146+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO. WE WILL KNOW IN JUNE WHETHER THEY COVERED ANY OF THEIR SHORTFALL.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.5318 TONNES//NEW STANDING ADVANCES TO 119.331 TONNES// TOTAL QUEUE JUMPING FOR THE MONTH; 54.7026 TONNES OR AVERAGING 3.2178 TONNES PER DAY IN JUNE.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JUNE,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $36.45)

WE HAD HUGE T.A.S. SPREADER LIQUIDATION TUESDAY // COMEX SESSION// WITH OUR LOSS IN PRICE , OUR SPECULATORS WENT MASSIVELY TO THE SHORT SIDE LED BY THE NOSE BY OUR HIGH FREQUENCY MOMENTUM PLAYERS WITH CENTRAL BANKERS TAKING THE LONG SIDE. THE SPECS WILL BE ANNIHILATED ONCE OPTIONS EXPIRY ENDS.

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

TUESDAY NIGHT//WEDNESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING //WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $52.85

WE HAD 1492 CONTRACTS ADDED THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES: 2497 CONTRACTS OR 249,700 OZ (2.706 TONNES)

JUNE DELIVERY MONTH

JUNE 24

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 ENTRIES i) Out of Asahi 72,725.346 oz (2262 kilobars) ot 2.262 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER//gold ENTRIES: 0 xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 178 CONTRACTS OR 17,800 OZ 0.5536 TONNES OF GOLD |

| No of oz to be served (notices) | 13 Contracts 1,300 OZ 0.040 TONNES |

| Total monthly oz gold served (contracts) so far this month | 38,352 notices 3,835,200 OZ 119.290 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

ENTRIES: 0

xxxxxxxxxxxxxxxxxx

comex withdrawal

1 ENTRIES

i) Out of Asahi 72,725.346 oz

(2262 kilobars)

ot 2.262 tonnes

3,325 tonnes

adjustments: 2//customer to dealer accounts

a) Brinks 5500.000 oz

b) JPMorgan 14,467.950 oz

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JUNE OI STANDS AT 191 CONTRACTS HAVING A LOSS OF 785 CONTRACTS.

WE HAD 956 CONTRACTS SERVED ON TUESDAY, SO WE GAINED 171 CONTRACTS OR 17,100 OZ. (0.5318 TONNES) EXERCISED A QUEUE JUMP WHERE THEY WILL TAKE PHYSICAL GOLD ON THIS SIDE OF THE POND. THIS IS NO DOUBT CENTRAL BANKS STANDING FOR PHYSICAL GOLD.

JULY LOST 14 CONTRACTS DOWN TO 7188 CONTRACTS.

AUGUST LOST 1167 CONTRACTS TO AN OI OF 270,241

.

We had 178 contracts filed for today representing 17,800oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 178 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 120 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (38,352) to which we add the difference between the open interest for the front month of JUNE(191 CONTRACTS) minus the number of notices served upon today 178 x 100 oz per contract) equals 3,836,500 OZ OR (119.331 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (38,352) to which we add the difference between the open interest for the front month of JUNE( 191 CONTRACTS) minus the number of notices served upon today 178 x 100 oz per contract) equals 3,836,500 OZ OR (119.331Tonnes of gold)

new total of gold standing in JUNE becomes 119.331 TONNES//

TOTAL COMEX GOLD STANDING FOR JUNE 119331 TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS ACTIVE DELIVERY MONTH OF JUNE.

confirmed volume TUESDAY confirmed 132,732// poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,708,373.370 oz 53.137 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,708,373.370 tonnes oz 53.137 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 27,809,901.511 oz

TOTAL REGISTERED GOLD 15,005,344.441 tonnes (466.72 tonnes)

TOTAL OF ALL ELIGIBLE GOLD 12,804,557.020 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,296,971oz ((REG GOLD- PLEDGED GOLD)=

413.359 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JUNE DELIVERY MONTH

JUNE 24

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries i) Out of CNT 70,034.680 oz |

| Deposits to the Dealer Inventory | 0 entries |

| Deposits to the Customer Inventory | 0 entries |

| No of oz served today (contracts) | 14 CONTRACT(S) (70,000 OZ) |

| No of oz to be served (notices) | 12 Contract (60,000 oz) |

| Total monthly oz silver served (contracts) | 2423 contracts 12.115 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRIES

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRY:0

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

1 entries

1 ENTRIES

1 entries

i) Out of CNT 70,034.680 oz

total withdrawal 70,034.680 oz

adjustments 1

dealer to customer:

Brinks 33.157.800 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 87.320 MILLION OZ//.TOTAL REG + ELIGIBLE. 322.792 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE /2026 OI: 13 OPEN INTEREST CONTRACTS FOR A LOSS OF 5 CONTRACTS.

WE HAD 14 NOTICES SERVED ON TUESDAY SO WE GAINED 9 CONTRACTS OR AN ADDITIONAL 45,000 OZ WILL STAND AS A QUEUE JUMP AT THE SILVER COMEX.

JULY SAW A LOSS OF 4024 CONTRACTS DOWN TO 29,141 CONTRACTS.

AUGUST SAW A GAIN 0F 121 CONTRACTS UP TO 1338…

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 or 5,000 OZ oz

CONFIRMED volume TUESDAY; 98,481// EXCELLENT

XXX

AND NOW JUNE. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 2424 X5,000 oz = 12.120 MILLION oz

to which we add the difference between the open interest for the front month of JUNE(13) AND the number of notices served upon today (1 )x (5000 oz)

Thus the standings for silver for the JUNE 2026 contract month: (2424 )Notices served so far) x 5000 oz + OI for the front month of JUNE ( 13) minus number of notices served upon today (1)x 5000 oz equals silver standing for the JUNE..contract month equating to 12.180 MILLION OZ.+

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 87.320 million oz of registered silver

JPMorgan as a percentage of total silver: 138.479/322.79 million: 42.72%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JUNE 24 /2026/WITH GOLD DOWN $141.55 /HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.563 TONNES OF GOLD OUT OF THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1017.637 TONNES

JUNE 19 /2026/WITH GOLD UP $36.85 /HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 7.421 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1020.49 TONNES

JUNE 18 /2026/WITH GOLD DOWN $135.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.856 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1013.069 TONNES

JUNE 17 /2026/WITH GOLD UP $20.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.427 TONNES OF GOLD FROM THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1012.213 TONNES

JUNE 16 /2026/WITH GOLD UP $4.45 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 15 /2026/WITH GOLD UP $111.10 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 12 /2026/WITH GOLD UP $123.30 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 11 /2026/WITH GOLD DOWN $15.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.855 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 10 /2026/WITH GOLD DOWN $153.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.426 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1016.495 TONNES

JUNE 9 /2026/WITH GOLD DOWN $75.60 TODAY/NO CHANGES IN GOLD AT THE GLD:// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 8 /2026/WITH GOLD DOWN $3.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 6.936 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 5 /2026/WITH GOLD DOWN $134;85 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 4 /2026/WITH GOLD UP $39.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.143 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 3 /2026/WITH GOLD DOWN $51.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.856 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.000 TONNES

JUNE 2 /2026/WITH GOLD UP $7.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.712 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.856 TONNES

JUNE 1 /2026/WITH GOLD DOWN $79.30 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 29 /2026/WITH GOLD UP $59.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

GLD INVENTORY: 1017.637 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JUNE 24 WITH SILVER DOWN $4.18: : SMALL CHANGES IN INVENTORY AT THJE SLV A DEPOSIT OF 93,000 MILLION OZ INTO THE SLV/./ // :INVENTORY RESTS AT 480.393 MILLION OZ

JUNE 19 WITH SILVER UP $1.11: : NO CHANGES IN INVENTORY AT THJE SLV/./ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 18 WITH SILVER DOWN $4.80: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: HUGE CHANGES IN INVENTORY A WITHDRAWAL OF 1.086 MILLION OZ FROM THE SLV././ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 17 WITH SILVER UP $0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: NO CHANGE IN INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 16 WITH SILVER DOWN $0.13: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.362 MILLION OZ INTO THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 15 WITH SILVER UP $3.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.357 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 481.026 MILLION OZ

JUNE 12 WITH SILVER UP $3.34: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.769 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 482.383 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.12: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.226 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.152 MILLION OZ

JUNE 10 WITH SILVER DOWN $0.50: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.909 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.378 MILLION OZ

JUNE 9 WITH SILVER DOWN $3.35: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.407 MILLION OZ INTO INTO THE SLV /./ // :INVENTORY RESTS AT 484.287 MILLION OZ

JUNE 8 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 543,000 OZ FROM THE SLV /./ // :INVENTORY RESTS AT 482.880 MILLION OZ

JUNE 5 WITH SILVER DOWN $4.86: NO CHANGES IN SILVER INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 4 WITH SILVER UP $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.432 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 3 WITH SILVER DOWN $2.55: NO CHANGES IN SILVER INVENTORY AT THE SLV >> /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

CLOSING INVENTORY 480.393 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD.

3. CHRIS POWELL AND HIS GATA DISPATCHES

Stefan Gleason: RIP, Alan Greenspan, the schizophrenic gold bug

Submitted by admin on Mon, 2026-06-22 21:58 Section: Daily Dispatches

By Stefan Gleason

Money Metals Exchange, Eagle, Idaho

Monday, June 22, 2026

Chairman Alan Greenspan has now passed from the scene at the age of 100.

Greenspan parlayed his sound-money bonafides into the top post at America’s central bank and the stewardship of the world’s dominant fiat currency. In betrayal of his own stated free-market principles, Greenspan spent nearly two decades at the Fed pumping up financial markets with easy money, backstopping Wall Street, and enabling runaway government spending commitments.

Today the “Maestro” of central banking leaves behind a complicated legacy.

He was celebrated by the financial establishment as a master economic steward. Yet many of the financial distortions, asset bubbles, and debt excesses that characterize the modern economy can be traced to policies implemented during his tenure.

The irony is that in his later years Greenspan increasingly sounded like one of his longtime critics. …

… For the remainder of the commentary:

END

Hong Kong draws large gold bars ahead of clearing mechanism launch

Submitted by admin on Mon, 2026-06-22 10:20 Section: Daily Dispatches

By Yihui Xie

Bloomberg News

Monday, June 22, 2028

At least four of the 11 banks participating in Hong Kong’s new gold clearing system are importing large bullion bars in preparation for the mechanism’s planned launch in July.

Traders are receiving orders from some of the clearing banks to move 400-ounce gold bars into the city, according to people familiar with the matter. The bars meet the London Good Delivery industry standard, said the people, who asked not to be named because they are not authorized to speak to media.

The 400-ounce bars are typically traded by banks and sovereign entities in London, the largest bullion trading hub, but are less common in the Asian market, which is dominated by much smaller kilobars. The banks need to build up inventories to allow for physical delivery when clearing begins next month, some of the people said. …

… For the remainder of the report:

END

Guinea’s president bans raw gold exports

Submitted by admin on Sun, 2026-06-21 20:01 Section: Daily Dispatches

By Ougna Camara

Bloomberg News

Sunday, June 21, 2026

Guinean President Mamadi Doumbouya announced a ban on raw gold exports, in an effort to boost local processing of the metal and help the domestic economy.

Doumbouya made the announcement during a meeting with industrial and artisanal gold producers as well as gold-buying offices operating in the West African nation.

“Guinea has the second-largest gold reserves in West Africa, but its gold leaves the country daily in its raw state to be processed, certified, and sold elsewhere,” Doumbouya said during the meeting, which was subsequently broadcast on state-owned Radio Television Guineenne.

“I am putting an end to that starting today,” he said. “Guinea will now require its gold to be processed within its own borders. Raw gold will no longer leave Guinea.” …

Doumbouya said gold will only be exported after being refined into ingots at a newly built facility in Conakry, the capital. …

… For the remainder of the report:

4. ANDREW MAGUIRE/LIVE FROM THE VAULT; 277

Maguire and Hemke say gold ‘correction’ is over and expect revaluation

Submitted by admin on Mon, 2026-06-22 11:56 Section: Daily Dispatches

11:56a ET Monday, June 22, 2025

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire and the TF Metals Report’s Craig Hemke, in conversation on this week’s edition of Kinesis Money’s “Live from the Vault” program, agree that gold’s “correction” is over and speculate how a U.S. Treasury revaluation of the monetary metal to a much higher price may come about soon.

The program is 57 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

5. COMMODITY REPORT//GOLD

Gold Is the Nuclear Option for a $127 Trillion Debt Crisis

![]()

by ITM Trading

Tuesday, Jun 23, 2026 – 12:41

Taylor Kenney walks through the arithmetic nobody in Washington wants done out loud. Take the $40 trillion debt everyone admits to, divide by the 261 million ounces the Treasury claims to hold, and a “gold revaluation” pencils out at $153,000 an ounce. Now add the $88.4 trillion in unfunded Social Security and Medicare promises buried in the government’s own 2025 financial report (a figure that somehow ballooned $10.1 trillion in a single year), and the real number creeps toward $486,000.

Meanwhile $846 trillion in derivatives sits stacked on top of it all, and every government on earth is borrowing like the house is already on fire.

They keep insisting there’s no crisis. So why does everyone in charge act like there is?

About ITM Trading: ITM Trading has spent nearly 30 years helping clients prepare for monetary resets, inflation, and systemic risk using physical gold and silver. We focus on education, historical context, and strategies designed to protect wealth when trust in the system breaks down.

end

GOLD TRADING TODAY

Hawkish Warsh Hammers Barbarous Relic: Gold Crashes Back Below $4000 As Rate-Hike Odds Rise

Wednesday, Jun 24, 2026 – 09:40 AM

Gold plunged back below $4,000 an ounce for the first time since November 2025 this morning, as a resurgent dollar and the prospect of higher interest rates bring bullion’s three-year bull market to a halt (now down 30% from its January highs).

The precious metal has posted double-digit gains for each of the last three years, more than doubling in price as central banks, money managers and retail investors all piled into the trade.

That rally ran out of steam in late January, shortly after the precious metal hit an all-time-high near $5,600 an ounce.

Chief among the factors that weighed on bullion’s performance was the outbreak of the US-Iran war.

Higher energy prices have fueled inflation and increased the likelihood of rate hikes, making bullion less attractive relative to yield-bearing assets like Treasuries.

Additionally, during the early period of the war, Gold reserves were used as a ‘piggy bank’ by Emerging Market nations to fund the huge increase in costs to procure energy (and manage currency runs).

Although oil prices are now falling as the US and Iran are negotiate a permanent peace deal, new Fed Chair Kevin Warsh surprised markets with a hawkish tone at his first rate-setting meeting last week, putting more downward pressure on the metal.

“The primary driver behind gold’s recent decline has been a significant repricing of interest-rate expectations,” Ewa Manthey, commodities strategist at ING Groep NV wrote in a note Wednesday.

Additionally, the debasement trade, a strategy favoring assets such as gold and Bitcoin over currencies vulnerable to inflationary, fiscal and monetary excess, has been losing momentum since President Trump nominated Kevin Warsh to lead the Fed.

Warsh’s statement that price stability is his overriding priority and his reputation as an inflation hawk have introduced doubts about the direction he would take, causing some investors to hedge their bets and leading to a decline in the debasement trade.

“Anyone who thinks that he is some kind of a stooge that’s been put in there to cut interest rates regardless of inflation is going to really, really be disappointed with Kevin Warsh,” said Gavyn Davies, co-founder and chairman of Fulcrum Asset Management and a former chief economist at Goldman Sachs.

“He’s not that kind of chair.”

The debasement trade – broadly defined as a strategy favoring assets such as gold and Bitcoin over currencies vulnerable to inflationary, fiscal and monetary excess like the dollar – had been one of the defining market narratives of the past two years.

“If the Fed has got the hiking bias, it’s really hard to play the debasement card,” Meera Chandan, JPMorgan’s co-head of global foreign-exchange strategy, said in an interview.

In the US, surging government borrowing and inflation running above target for more than half a decade fueled concerns that the greenback’s purchasing power would erode.

“What people were worried about was the inflation target, the Fed’s credibility and its independence,” said Jonathan Owen, a portfolio manager at TwentyFour Asset Management.

“I think those concerns were largely put to rest.”

All of which has helped push the dollar up to its highest since May 2025 (around the Nov 2025 highs)

As Bloomberg’s Jack Ryan and Yihui Xie report, several major banks have cut their gold forecasts in the last week.

Though revised targets imply prices will gain from current levels, Wall Street analysts are markedly less bullish than before.

Goldman Sachs axed $500 from a forecast that now sees bullion ending the year at $4,900 an ounce, while Deutsche Bank AG cut its fourth-quarter estimate by 17%.

It seems that Specs have thrown in the towel on the barbarous relic…

As the gold price has caught down to ETF holdings.

As Deutsche Bank wrote in a note, continued sales from gold-backed ETFs showed that the usual support for the metal is “notably absent,”

Meanwhile in China, the metal’s onshore discount to Comex prices in New York suggests imports will not be a support for the market, the bank’s analysts said.

But Goldman noted that gold ETF holdings that have undershot their federal funds rate-implied level

Still, one bright spot for bullion is the continued strength of central-bank demand.

“The one pillar which remains strong is central bank demand, and we expect this to be the case for some time to come,” Deutsche Bank wrote.

The monetary institutions added to their holdings at the fastest pace in more than a year in the first quarter, and survey data indicates they intend to buy more.

END

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 4.56 PTS OR 0.11%

HANG SENG CLOSED UP 75.90 PTS OR 0.33%

Nikkei CLOSED DOWN 613.41 PTS OR 0.88%

//Australia’s all ordinaries CLOSED UP 0.05%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.8109

/ OFFSHORE CLOSED DOWN AT 6.8147 Oil DOWN TO 71.66 dollars per barrel for WTI and BRENT UP TO 75.18 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.8109) OFFSHORE YUAN TRADING DOWN TO 6.8147 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.8109

OFFSHORE YUAN: DOWN TO 6.8147

1.HANG SANG CLOSED UP 75.90 PTS OR 0.33%

2. Nikkei closed DOWN 613.41 PTS OR 0.88%

WEST TEXAS INTERMEDIATE OIL DOWN TO 71.66

BRENT; 75.18

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 101/42/// EURO FALLS TO 1.1344 DOWN 35 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.669 DOWN 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA CROSS NOW AT 161.67… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.876 UP 4 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN( 6.8109) AND OFFSHORE: DOWN AT 6.8147

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.8950/ Italian 10 Yr bond yield DOWN to 3.631/ SPAIN 10 YR BOND YIELD DOWN TO 3.367%

3i Greek 10 year bond yield DOWN TO 3.583%

3j Gold at $4040.65 //Silver at: 59.30 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 46/ 100 roubles/74.96

3m oil (WTI) into the 71 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 161.67 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.669% DOWN 2 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.876 UP 4 PTS..: USA/SF this 0.8124 as the Swiss Franc . Euro vs SF: 0.9215

USA 10 YR BOND YIELD: 4.476 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.922 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.199 DOWN 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 46.50 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.7314 DOWN 3 PTS

30 YR UK BOND YIELD: 5.438 DOWN 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.416 DOWN 2 BASIS PTS

5 YR CANADA BOND YIELD: 3.041 DOWN 2 BASIS PTS.

Futures Rebound From “Chip-Wreck” Ahead Of Critical Micron Earnings

Wednesday, Jun 24, 2026 – 08:25 AM

US stocks are set for a rebound with equity futures higher as Semis and Tech stage a partial recovery from yesterday’s “Chip-Wreck” as KOSPI retraced about 20% of its losses ahead of earnings from the single-biggest contributor to US outperformance this year: Micron’s third-quarter numbers are an even bigger deal than usual, following Tuesday’s shakeout of an overcrowded AI trade that’s has been priced for perfection. As of 8:00am ET, S&P 500 futures are 0.3% higher with Nasdaq 100 contracts up 0.5%. In premarket trading, equities are boosted by a bid for Semis (MU +3.6% with earnings tonight) with most of Mag7 higher. Within Cyclicals, Discretionary and Industrials are the standouts as Energy / Fins are mostly lower. Cyclicals poised to lead Defensives with Momentum factor flat. Bond yields are lower 1-2bp as the yield curve flattens, pushing 10Y yields ; USD remains bid even as real yields decline. DXY set a new 52-wk high today. Cmdty remain under pressure dragged by the Energy complex and weakness in Metals. Today’s macro data focus is on Home Sales ahead of tomorrow’s update on GDP, PCE, Personal Income / Spending, Cap / Durable Goods, and weekly Claims.

In premarket trading, Alphabet (GOOGL) is up 0.5% after news the Google parent will replace Verizon in the Dow Jones Industrial Average. Verizon (VZ) is down 0.5%. Other Mag 7 stocks are mostly higher (Nvidia +0.6%, Tesla +0.6%, Meta +0.1%, Apple +0.6%, Microsoft -0.5%, Amazon -0.2%)

- Cerebras Systems (CBRS) falls 14% premarket after the newly public chipmaker gave an annual sales forecast that disappointed investors looking for it to take a bigger slice of the AI data center market.

- FedEx (FDX) is down 7% after the parcel delivery company posted its first earnings report since completing the spin off of its freight unit earlier this month. Results seem to have fallen short of investor expectations after a strong run-up in the first half of the year: the company cited margin pressure and global trade uncertainty in its outlook.

- FuelCell Energy (FCEL) rises 16% after the company said it reached an agreement with Fit Energy to supply 380 megawatts of clean on-site power for data centers using FuelCell Energy’s technology.

- Hertz (HTZ) slumps 16% after providing an update. The company also filed to offer $100m of stock.

- Twilio Inc. (TWLO) rises 3% as Goldman Sachs rates the software company buy with a Street-high $300 price target, citing AI tailwinds.

- Wendy’s (WEN) rises 23% as the stock climbed the ranks in Stocktwits and Reddit’s widely followed wallstreetbets forum.

In other company news, Qualcomm is hosting a highly anticipated investor day in New York. CEO Cristiano Amon and executives are using the event to outline the company’s next phase of growth and diversification strategy. And Nike is hiring David Denton as its next CFO, who is poised to leave Pfizer in August. SpaceX shares are fluctuating, after it sold $25 billion of investment-grade bonds.

While yesterday’s market action was wild for some chip stocks, there was no sense of over-reaction or panic across the market, according to Goldman traders. They said that on a 1 to 10 scale of overall activity level on their trading floor, the session was a 5, despite broad selling by long only and hedge funds. They also say that top-of-book liquidity remains shallow, exacerbating price action.

The recent swings are sharpening the focus on Micron, one of the biggest beneficiaries of roaring demand for chipmakers that stand to gain from the billions of dollars being plowed into AI infrastructure. The stock is up more than 260% in 2026 even after dropping 13% on Tuesday, and has been a leader of the rebound from the S&P 500’s war-driven lows. Today’s main event, the Micron earnings print, follows four of the six major market-moving events on June’s calendar: the CPI print, the SpaceX IPO, the US-Iran MoU, and Warsh’s first Fed meeting. The bar is high, positioning crowded and the semi/memory complex is nervous.

“The main problem for Micron is not Micron itself, but the expectations for its third-quarter earnings,” said Joachim Klement, head of strategy at Panmure Liberum. “Even if Micron has a stellar quarter and gives solid guidance, it may not be enough to fulfill lofty expectations.”

Traders warned of possible further swings in tech stocks if Micron’s earnings and outlook fail to meet sky-high expectations.

“For high-performing companies that reflect the dynamics of a sector, market expectations naturally rise,” said Guillermo Hernández Sampere, head of trading at MPPM. “From a rational standpoint, these are difficult to meet, and disappointments become apparent in the stock’s price performance.”

Evidence of the vast amounts of capital flowing into the buildout of AI infrastructure and its supply chain was again on display as South Korea’s SK Hynix Inc. announced it was looking to raise $29 billion in a US listing. The offering would add to the recent wave of AI-related funding secured through stock issuances, after SpaceX held the largest initial public offering in history earlier this month and Alphabet Inc. planned a $85 billion capital raise.

The sixth and final major market event on the docket this month comes on Thursday, with this week’s marquee economic release, the core PCE. Bloomberg Economics expects that a hot PCE reading will likely reinforce the hawkish tilt by the Fed at its meeting earlier this month.

Building on the AI funding theme, SK Hynix Inc. is planning to raise 45.45 trillion won ($29.4 billion) in a landmark US listing. That could put it among the top five share sales of all time, comparable with Saudi Aramco’s then-record 2019 initial public offering.

In geopolitics, oil oil is down for an eighth day in nine and back at about $72 barrel, with Brent dropping below $75 for the first time since the start of the war, as crude continues to price for lower geopolitical risk, higher supply and increasing traffic through the Strait of Hormuz. Separately, Trump is meeting defense industry executives later to talk about picking up the pace of weapon production. Lower crude prices pushed the cost of diesel in the US below $5 a gallon for the first time since mid-March.

Private credit also remains in focus as a $7 billion fund run by Morgan Stanley caps investor withdrawals at 5%, allowing less than half of the redemptions shareholders requested in the second quarter.

Europe’s Stoxx 600 index is little changed and Germany’s DAX is lagging following a big drop for defense company Rheinmetall. Asian stocks slid amid a selloff in the region’s leading chipmaker TSMC and other technology names over concerns about the sustainability of demand for AI-linked shares and their valuations. The MSCI Asia Pacific Index dropped as much as 1.2%, before paring most of the losses. Taiwan and Indonesia led the region’s decline, while Japan also underperformed. Indonesia’s stock benchmark fell as much as 3.7% after MSCI Inc. again decided to postpone its review on the country’s equities, saying it needs more time to see whether recently announced transparency reforms are effective. Sectors to Watch

- Chinese semiconductor stocks rally as momentum in AI‑related investments lingered, while the news about TSMC lifting prices further lifts sentiment.

- Australia’s software-heavy technology sector rises as investors rotate out of Asian chipmakers amid valuation concerns that triggered a selloff in AI-linked shares.

- India’s software exporters are steadily losing their sway on the country’s stock market as concerns over artificial intelligence-led disruption trigger a prolonged selloff in the sector.

- Chinese shipping stocks gain after more vessels transit the Strait of Hormuz with tracking signals switched on, signaling rising confidence in the vital energy chokepoint.

- Chinese healthcare stocks advance after Citi says the sector’s current valuations fail to reflect improving fundamentals and resilient order books.

- Citigroup says this year’s 6.18 campaign was the quietest in the past 16 years, which does not bode well for June retail sales data and suggests downside risks to second-quarter earnings estimates for JD and Alibaba.

In FX, the dollar continued to benefit from haven demand as risk sentiment remained fragile. Advancing 0.3%, the greenback headed for its longest winning streak in more than a month and cemented its highest level of the year. Meanwhile, the euro has fallen to the lowest since May 2025

In rates, treasuries rose modestly as inflation worries eased, with the 10-year yield falling two basis points to 4.48% supported by similar gains for European bonds during the London session, as oil prices extend their recent slide with tankers openly crossing the Strait of Hormuz. US long-end yields are about 2bp lower with shorter maturities little changed, flattening 2s10s and 5s30s spreads by almost 2bp. 10-year is about 1bp lower near 4.47%, UK counterpart by an additional 1bp. Treasury auction cycle continues with $70 billion 5-year note; Tuesday’s 2-year sale stopped through by 0.3bp. WI 5-year yield near 4.265% is ~8bp cheaper than last month’s auction, which tailed by 0.1bp. The dollar issuance slate includes three names so far. SpaceX led a $30b, four-offering calendar on Tuesday. Issuers paid about 11bp in new issue concessions on deals that were 2.9 times covered. Focal points of US session include 5-year note auction at 1pm New York time.

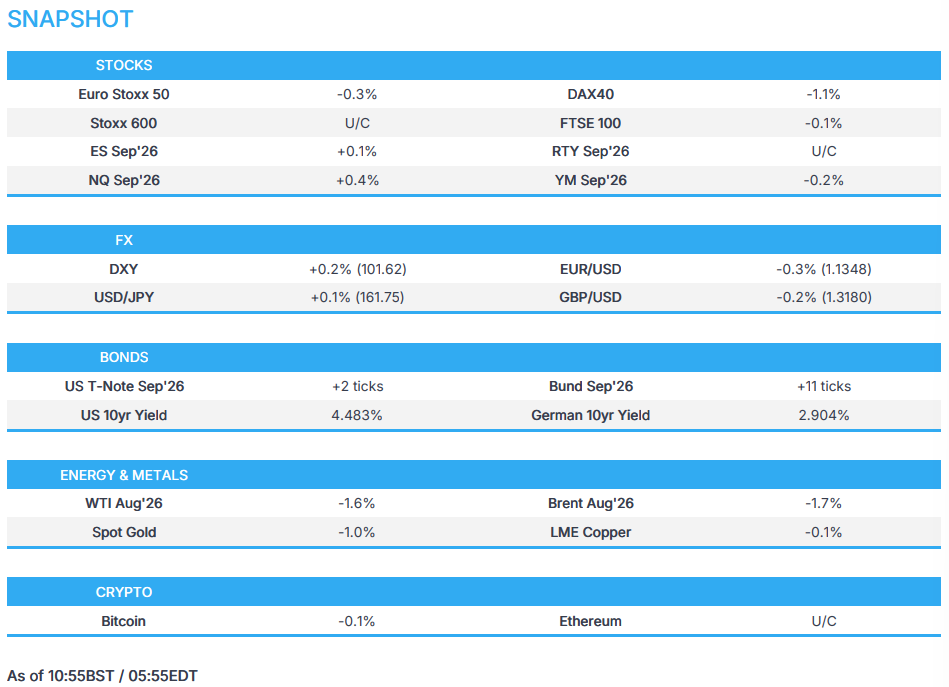

In commodities, WTI crude oil futures are down around 2% near session lows as the US and Iran signal progress toward ending the war, weighing on energy prices. Brent fell below $75 for the first time since the war started. Gold slipped as the stronger dollar made bullion priced in the US currency more expensive.

US economic data calendar includes 1Q current account balance (8:30am) and May new home sales (10am). Fed speaker slate includes Governor Lisa Cook at 2pm

Market Snapshot

Top Overnight News

- Qatar’s prime minister said establishing a hotline between the US and Iran is essential to prevent rogue actors impeding the reopening of the Strait of Hormuz, as he predicted that the Gulf state would resume normal liquefied natural gas production “within a few weeks”. FT

- The US Senate voted 50-48 to pass a resolution to halt the Iran war unless US President Trump gets approval from Congress. However, the White House said Congress resolutions on Iran are non-binding and won’t be sent to President Trump, while Trump criticised the Senate passage of the Iran war powers resolution, which he claimed provides aid and comfort for the enemy.

- Treasury Secretary Bessent said inflation will return to the target, and he is confident Fed Chair Warsh will optimize the path for the economy. Bessent also stated that the US housing issue is a conundrum affected by rate-lock owners, and will take lower rates and more supply, predicting inflation will ease as talks with Iran continue and gas prices fall. BBG

- Congress on Tuesday passed its most-ambitious housing legislation since the 1980s, a package of more than 50 provisions aimed at making it easier to build homes and make housing more affordable. The House passed the bill 358-32 with broad bipartisan support a day after the Senate voted 85-5 to approve the measure. President Trump is expected to sign it into law as soon as Wednesday. WSJ

- Leveraged ETFs tracking Samsung Electronics or SK Hynix probably sold a combined $6 billion of the Korean chipmakers’ shares yesterday to maintain their ratios, underscoring how such products are amplifying market moves. BBG

- The BoJ sees the risk of inflation exceeding its 2% target and will conduct additional interest-rate hikes appropriately, Governor Kazuo Ueda said in speech Wednesday that reiterated policymakers’ recent messaging. BBG

- Australia’s consumer price growth eased in May amid cooling fuel prices, but underlying inflation continued to strengthen as businesses passed on higher costs resulting from the Middle East conflict. WSJ

- Extreme temperatures in Western Europe triggered widespread school and transit disruptions across the UK and France. The failure of two transformers in Brittany, probably due to the heat, left 68,000 people without electricity, while the UK’s grid operator issued a rare summer power-supply warning. BBG

- Venezuela is set to reveal a $240bn debt pile, much higher than previously thought, as the country embarks on the biggest sovereign restructuring in history following the US removal of Nicolás Maduro. The country is on track to reveal borrowings that are significantly larger than market estimates of $150bn to $200bn when it lifts the veil for creditors on the state of its finances in the coming weeks. FT

- SK Hynix plans to raise up to $29.4 billion in a landmark US listing to increase its capacity to meet memory chip demand. At that size, the deal would be among the top five share sales of all time. BBG

A more detailed look at global markets courtesy of Newsquawk

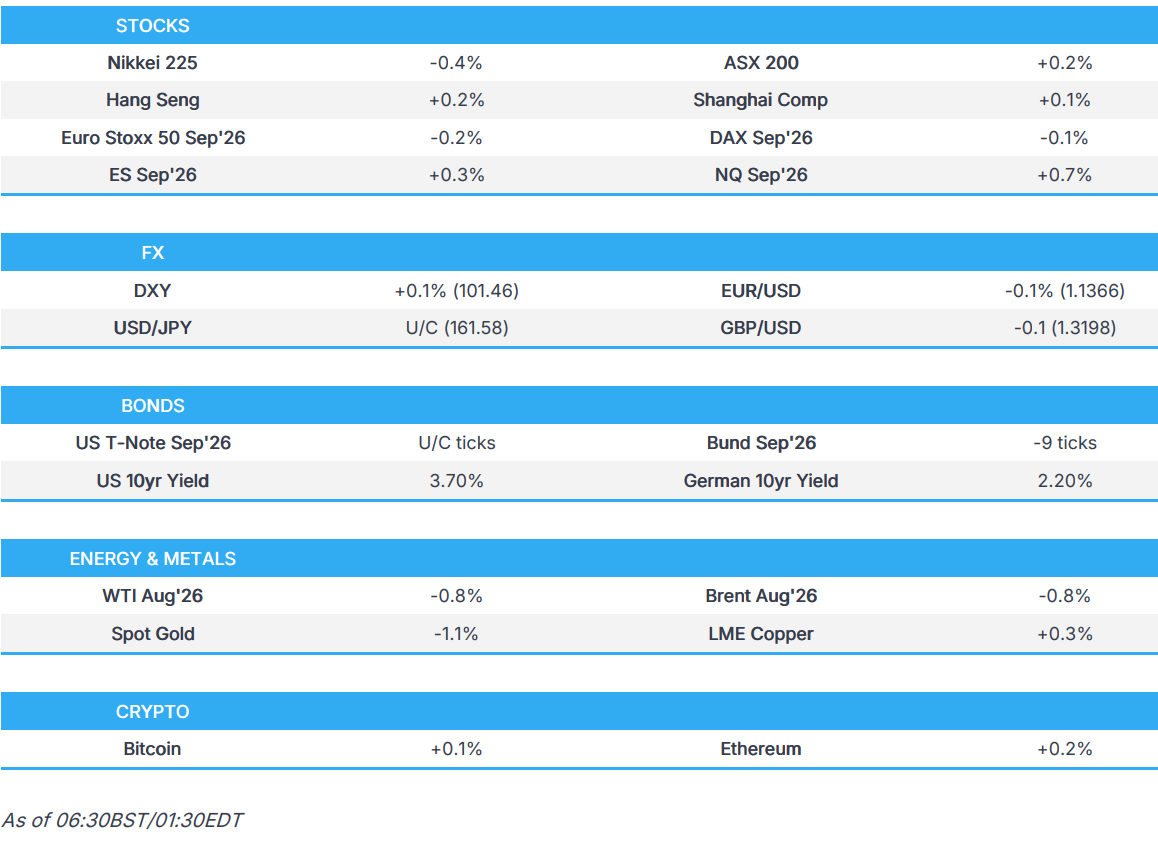

APAC stocks saw mixed price action as the initial rebound from the prior day’s tech-driven sell-off gradually waned in the absence of any fresh major catalysts. ASX 200 traded rangebound as strength in tech and defensives was counterbalanced by losses in mining and energy following the recent declines in underlying commodity prices, while inflation data was mixed and would likely have little bearing on monetary policy. Nikkei 225 failed to sustain early gains and dipped back beneath the 70,000 level, while Services PPI data printed in line with forecasts and the BoJ Summary of Opinions showed members continued to advocate for further rate increases. Hang Seng and Shanghai Comp were indecisive as the attention turned to the WEF in Dalian, where Premier Li said China’s economy shows resilience and maintains sound momentum. He stated China remains committed to opening up and will continue to accelerate the large-scale application of new technologies.

Top Asian News

- Japan is reportedly looking at ways to streamline the management of its USD 1.3tln FX reserves to increase returns and help state finances, Reuters reported.

- A draft proposal of 1% consumption tax was presented and will reportedly be implemented from April 2027, FNN reported. The proposal faces significant resistance from opposition parties, with DPP representative Furukawa stating they have no intention of cooperating, leaving the prospect of a June agreement uncertain.

- Chinese Premier Li said China’s economy shows resilience and maintains sound momentum, while he noted four key words for the economy including stability, innovation, dynamism and integration. Li also stated that China remains committed to opening up, as well as noted that China’s AI sector sees explosive growth, and they will continue to accelerate the large-scale application of new technologies.

European bourses (STOXX 600 U/C) start Wednesday’s trade broadly lower, with the AEX (+0.3%) outperforming as tech names steady from Tuesday’s selloff. Germany’s DAX 40 (-0.9%) is the clear underperformer, as Rheinmetall weighs on the index. The FT reported that Germany will scrap plans to build Rheinmetall’s F126 frigates and instead purchase 8 Meko A-200 frigates from TKMS. Rheinmetall (-14%) has taken a hit following this news, while TKMS (+9.4%) benefits. European sectors print a mixed picture. Real Estate (+2.2%) is the clear outperformer, with Food, Beverages & Tobacco (+1.1%) and Consumer Products (+1.2%) rounding out the top 3. Media (-1.3%), Construction (-0.7%) and Energy (-0.6%) are the sector laggards.

Top European News

- UK MP Jones said that while he has the 81 seats required to run, he will not contest against Burnham for Labour leadership, Sky News reported. Jones further said he thinks traders “can be content” with Burnham as PM and added that he thinks there is room to “borrow a little more”, and things (referring to investment) can be done differently, without “broad brush” borrowing and spending.

- Germany confirmed earlier reports that it will abandon plans to build 6 Rheinmetall (RHM GY) F126 frigates, and instead intends to buy 8 smaller Meko A-200 frigates from TKMS (TKMS GY).

FX

- G10s are weaker against the Buck as the risk-off mood continues into Micron earnings this evening. Antipodeans lag, as the Aussie digests mixed CPI, JPY fluctuates either side of unchanged, and EMs are getting hit.

- Markets are reluctant to buy the dip in equities after losses on Tuesday. As such, the Buck continues to firm as the preferred haven, with USD outperformance vs Scandis and Antipodeans with liquidity lower. Traditional havens fare better against the Buck, JPY steady at the lower end of its recent ranges, while CHF continues its downward trend. For US-specifics, the highlight of the session will be the Fed Bank Stress Test Report alongside Micron earnings – both due after the close. DXY trades at the upper end of its 101.35-101.68 range, higher by 0.2%.

- Aussie data was mixed, CPI in May cooled below expectations, and the trimmed mean firming in line with most forecasts to 0.4% M/M and 3.6% Y/Y. The report noted housing was the main inflation pressure point, and Westpac analysis notes price pressures are broadening, particularly within services. As such, with the recent energy related prices pressures set to linger, the RBA will be keenly monitoring signs of sticky inflation with the bank widely expected to have concluded tightening. AUD faring better than Kiwi (AUD/NZD +0.1%), but lower against the Buck as the mixed data does not provide a bias towards any future easing/tightening; Labour market data ahead.

- EUR and GBP are lacklustre and tracking the firmer Buck. Domestic catalysts light for both regions, though some continued incrementally optimistic updates from a likely incoming Burnham premiership which has helped GBP. EUR/GBP trades a whisker away from the 200 week moving average @ 0.8602 which is also the session low. For the EUR, recent Governing Council commentary remains hawkish, though nothing deviating too much from the Statement at June’s meeting.

- Barclays sees a moderate dollar-buying by month-end against most majors, with a weak sign on USDJPY.

Fixed Income

- Global fixed income benchmarks are slightly firmer, as energy prices continue to pull back and investors seemingly return to see bonds as a haven following the recent tech sell-off.

- USTs (+2 ticks) return to gains after pulling back from a 109-17+ top in Tuesday’s session, currently trading at the top end of a 109-09+ to 109-15 range. The US data docket is light today, ahead of Thursday’s busy day (PCE, GDP, initial jobless claims, durable goods). On the supply front, the US is to sell USD 70bln 5-year notes. The auction benefits from a combination of higher outright yields, reduced geopolitical uncertainty and a more hawkish Federal Reserve. The key question will be whether the improved backdrop can bring direct bidders back into the sector while maintaining the strong indirect demand seen at the previous auction.