GOLD CLOSED UP $49.10 TO $4081.90

SILVER CLOSED UP $0.86 TO $59.25

LONDON/OTIC LBMA OPTIONS EXPIRY ON FIRST DAY NOTICE THIS COMING TUESDAY.

ACCESS MARKET

GOLD $4067.10 3:30 PM)

SILVER: 58.97 3;30 PM)

Bitcoin morning price:$59,483 UP 269 DOLLARS (MANY SWITCHING TO PHYSICAL GOLD)

Bitcoin: afternoon price: $59,824 UP 610 DOLLARS

Platinum price closed UP 25.50 to $1634.50

Palladium price; UP $20.00 TO $1214.00

JUNE 26

EXCHANGE: COMEX

CONTRACT: JUNE 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,030.500000000 USD

INTENT DATE: 06/25/2026 DELIVERY DATE: 06/29/2026

FIRM ORG FIRM NAME ISSUED STOPPED

092 C DEUTSCHE BANK 142

099 H DEUTSCHE BANK AG 17

363 H WELLS FARGO SECURITI 84

624 H BOFA SECURITIES 1993

657 H MORGAN STANLEY 10

661 C JP MORGAN SECURITIES 1000 200

709 C BARCLAYS 873

732 C RBC CAP MARKETS 117

737 C ADVANTAGE FUTURES 4

TOTAL: 2,220 2,220

MONTH TO DATE: 40,834

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2026: 2,220 CONTRACTs NOTICES FOR 222,000 OZ or 6.905 TONNES

total notices so far: 40,854 contracts FOR 4,085,400 OZ OR 127.010 TONNES

SILVER NOTICES: 118 NOTICE(S) FILED FOR 590,000 OZ /

total number of notices filed so far this month : 2592 CONTRACTS (NOTICES) for 12.960 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF XX CONTRACTS OR XXX OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0 OZ//NEW STANDING ADVANCES TO 12.960 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 20 CONTRACTS FOR 100,000 OZ//NEW STANDING ADVANCES TO 23.060 MILLION OZ. IN EXCHANGE FOR RISK THE BUYER ASSUMES THE RISK AND ONLY A CENTRAL BANK WOULD TAKE THAT RISK. THE BUYER IS PROBABLY THE CENTRAL BANK OF INDIA.

SUMMARY OF OUR JUNE 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE. 61.065 MILION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 0 OZ//NEW STANDING ADVANCES TO 12.960 MILLION OZ TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 20 CONTRACTS FOR 100,000 OZ//NEW STANDING ADVANCES TO 13.060 MILLION OZ

GOLD//OUTLINE

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT 6/926 TONNES OF A QUEUE JUMP/NEW STANDING ADVANCES TO 127.1104 TONNES

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 6/926 TONNES//NEW STANDING ADVANCES TO 127/1104 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 125/68 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE 1170 CONTRACTS TO AN OI OF 103,803

EFP ISSUANCE 254 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 254 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1170 CONTRACTS AND ADD TO THE 254 E.FP. ISSUED

WE OBTAIN A HUGE LOSS OF 816 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN OF $0.69

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.580 MILLION PAPER OZ

OCCURRED DESPITE OUR GAIN IN PRICE.OF $0.69

2.ASIAN AFFAIRS JUNE 26 /2025

SHANGHAI CLOSED DOWN 93.02 PTS OR 2.26%

HANG SENG CLOSED DOWN 405.05 PTS OR 1.76%

Nikkei CLOSED DOWN 2958.34 PTS OR 4.09%

//Australia’s all ordinaries CLOSED UP 0.07%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7982

/ OFFSHORE CLOSED UP AT 6.8038 Oil UP TO 69.75 dollars per barrel for WTI and BRENT UP TO 72.83 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING UP (6.7982) OFFSHORE YUAN TRADING UP TO 6.8038 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR 2844 CONTRACTS TO 360,560 WELL ABOVE ITS NEW LOW OF 326,052 OI SET JUNE 3, CLOSE TO THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND CLOSE TO THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,052 //JUNE 3 2026 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD HUGE T.A.S. LIQUIDATION DURING WEDNESDAY’S MASSIVE COMEX TRADING//RAID JUNE 24!!. BUT ZERO LIQUIDATION ON THURSDAY. IT SEEMS THAT MANY OF THE SPECULATORS THAT HAVE NOW CONTINUED AGAIN TO GO MASSIVELY ON THE SHORT SIDE WITH BANKERS ON THE LONG SIDE WERE OBLITERATED WHEN THE LONGS TENDERED FOR DELIVERY:

CENTRAL BANKS TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS JUNE CONTRACT MONTH!! AND THE HUGE MASSIVE QUEUE JUMP FOR TODAY. LAST NIGHT I SENT MANY OF YOU THE HUGE NUMBER OF NOTICES FILED FOR TODAY.

THE STRONG SIZED GAIN ON OUR TWO EXCHANGES (5004 CONTRACTS) OCCURRED WITH OUR GAIN IN PRICE IN GOLD (UP $42.70)

WE THUS HAD A STRONG SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 5004 CONTRACTS (OR 15.56 TONNES) WITH OUR GAIN IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 2160 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIDAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH JUNE

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

JUNE: 0 SO FAR IN GOLD

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO JUNE:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 146+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO SO FAR

DETAILS ON OUR NEW JUNE COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG GAIN ON OUR TWO EXCHANGES OF 5004 CONTRACTS WITH OUR GAIN IN PRICE ($42.70). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A STRONGER SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1208 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

JUNE: ZERO SO FAR.

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 146+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO. WE WILL KNOW IN JUNE WHETHER THEY COVERED ANY OF THEIR SHORTFALL.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 6.926 TONNES//NEW STANDING ADVANCES TO 127.1104 TONNES// TOTAL QUEUE JUMPING FOR THE MONTH; 62.4217 TONNES OR AVERAGING 3.285 TONNES PER DAY IN JUNE.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JUNE,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $42.70)

WE HAD HUGE T.A.S. SPREADER LIQUIDATION THURSDAY // COMEX SESSION// WITH OUR GAIN IN PRICE , OUR SPECULATORS STILL WENT MASSIVELY TO THE SHORT SIDE LED BY THE NOSE BY OUR HIGH FREQUENCY MOMENTUM PLAYERS WITH CENTRAL BANKERS TAKING THE LONG SIDE. THE SPECS WERE ANNIHILATED ON THURSDAY AND THEY WILL AGAIN BE WHACKED ON FRIDAY.

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

THURSDAY NIGHT//FRIDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING //FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $42.70

WE HAD 459 CONTRACTS REMOVED THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES: 5004 CONTRACTS OR 500, 400 OZ (15.56 TONNES)

JUNE DELIVERY MONTH

JUNE 26

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 2 ENTRIES i) Out of JPMorgan: 96,442.359 oz ii) Out of Manfra: 35,754.697 os total withdrawal 132,496.556 oz 4.12 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER//gold ENTRIES: 0 xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 2220 CONTRACTS OR 222,000 OZ 6.905 TONNES OF GOLD |

| No of oz to be served (notices) | 12 Contracts 1200 OZ 0.0373 TONNES |

| Total monthly oz gold served (contracts) so far this month | 40,834 notices 4,083,400 OZ 127.01 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

ENTRIES: 0

xxxxxxxxxxxxxxxxxx

comex withdrawal

2 ENTRIES

i) Out of JPMorgan: 96,442.359 oz

ii) Out of Manfra: 35,754.697 os

total withdrawal 132,496.556 oz

4.12 tonnes

adjustments: 2// dealer to customer account

a)Asahi: 49,219.118 oz

b) HSBC 105,393.389 oz

total oz leaving dealer to customer: 154,603.517 oz or 4.80 tonnes

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JUNE OI STANDS AT 2233 CONTRACTS HAVING A GAIN OF 1965 CONTRACTS.

WE HAD 262 CONTRACTS SERVED ON THURSDAY, SO WE GAINED A HUMONGOUS 2227 CONTRACTS OR 222,700 OZ. (6.926 TONNES) EXERCISED A QUEUE JUMP WHERE THEY WILL TAKE PHYSICAL GOLD ON THIS SIDE OF THE POND. THIS IS NO DOUBT CENTRAL BANKS STANDING FOR PHYSICAL GOLD.

JULY GAINED 214 CONTRACTS UP TO 7686 CONTRACTS.

AUGUST LOST 1586 CONTRACTS TO AN OI OF 271,983

.

We had 2220 contracts filed for today representing 222,000oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 1000 notices issued from their client or customer account. The total of all issuance by all participants equate to 22200 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 100 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (40,854) to which we add the difference between the open interest for the front month of JUNE (2233 CONTRACTS) minus the number of notices served upon today 2,220 x 100 oz per contract) equals 4,086,600 OZ OR (120.125 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JUNE. /2026. contract month, we take the total number of notices filed so far for the month (40,834) to which we add the difference between the open interest for the front month of JUNE( 2233 CONTRACTS) minus the number of notices served upon today 22,200 x 100 oz per contract) equals 4,086,600 OZ OR (127.1104 Tonnes of gold)

new total of gold standing in JUNE becomes 127.1104 TONNES//

TOTAL COMEX GOLD STANDING FOR JUNE 127.1104 TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS ACTIVE DELIVERY MONTH OF JUNE.

confirmed volume THURSDAY confirmed 172,699/ poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,708,373.370 oz 53.137 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,708,373.370 tonnes oz 53.137 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 27,677,372.805 oz

TOTAL REGISTERED GOLD 14,783,609.646 tonnes (459.832tonnes)

TOTAL OF ALL ELIGIBLE GOLD 12,893,763.159 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,075,256oz ((REG GOLD- PLEDGED GOLD)=

406.649 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JUNE DELIVERY MONTH

JUNE 26

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries i) Out of Delaware 2972.810 oz total withdrawal: 2972.810 oz |

| Deposits to the Dealer Inventory | 0 entries |

| Deposits to the Customer Inventory | 1 entries 1 entries i) Into Delaware 1067.147 oz total deposit 1067.147 oz |

| No of oz served today (contracts) | 118 CONTRACT(S) (590,000 OZ) |

| No of oz to be served (notices) | 0 Contracts (0, oz) |

| Total monthly oz silver served (contracts) | 2592 contracts 12.960 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRIES

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRY:1

1 entries

i) Into Delaware 1067.147 oz

total deposit 1067.147 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

1 entries

) Out of Delaware 2972.810 oz

total withdrawal: 2972.810 oz

adjustments 1

dealer to customer:

delaware 70,323.224 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 87.126 MILLION OZ//.TOTAL REG + ELIGIBLE. 323,393 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE /2026 OI: 118 OPEN INTEREST CONTRACTS FOR A GAIN OF 49 CONTRACTS.

WE HAD 50 NOTICE(S) SERVED ON THURSDAY SO WE GAINED 99 CONTRACTS OR AN ADDITIONAL 495,000 OZ WILL STAND AS A QUEUE JUMP AT THE SILVER COMEX.

JULY SAW A LOSS OF 8,432 CONTRACTS DOWN TO 14,657 CONTRACTS. JULY BECOMES THE FRONT MONTH. WE HAVE 2 MOR READING DAYS BEFORE FIRST DAY NOTICE. WE SHOULD HAVE AROUND 30 MILLION OZ STANDING FOR SILVER AT THE COMEX..

AUGUST SAW A GAIN 0F 84 CONTRACTS UP TO 1519…

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 118 or 590,000 OZ oz

CONFIRMED volume THURSDAY; 122,595// enormous//spec shorts caught

XXX

AND NOW JUNE. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 2592 X5,000 oz = 12.960 MILLION oz

to which we add the difference between the open interest for the front month of JUNE(118) AND the number of notices served upon today (118 )x (5000 oz)

Thus the standings for silver for the JUNE 2026 contract month: (2592 )Notices served so far) x 5000 oz + OI for the front month of JUNE ( 118) minus number of notices served upon today (118)x 5000 oz equals silver standing for the JUNE..contract month equating to 12.960 MILLION OZ.+ to which we add our first exchange for risk of 20 contracts for 100,000 oz//standing thus increases to 13.060 MILLION OZ!!

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 87.126 million oz of registered silver

JPMorgan as a percentage of total silver: 138.479/323.393 million: 42.67%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JUNE 26 /2026/WITH GOLD UP $49.10 /HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 4.287 TONNES OF GOLD FROM THE GLD // ./ //:/INVENTORY RESTS AT 1013.350 TONNES

JUNE 25 /2026/WITH GOLD UP $42.70 /NO CHANGES IN GOLD AT THE GLD: // ./ //:/INVENTORY RESTS AT 1017.637 TONNES

JUNE 24 /2026/WITH GOLD DOWN $141.55 /HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.563 TONNES OF GOLD OUT OF THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1017.637 TONNES

JUNE 19 /2026/WITH GOLD UP $36.85 /HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 7.421 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1020.49 TONNES

JUNE 18 /2026/WITH GOLD DOWN $135.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.856 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1013.069 TONNES

JUNE 17 /2026/WITH GOLD UP $20.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.427 TONNES OF GOLD FROM THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1012.213 TONNES

JUNE 16 /2026/WITH GOLD UP $4.45 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 15 /2026/WITH GOLD UP $111.10 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 12 /2026/WITH GOLD UP $123.30 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 11 /2026/WITH GOLD DOWN $15.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.855 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 10 /2026/WITH GOLD DOWN $153.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.426 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1016.495 TONNES

JUNE 9 /2026/WITH GOLD DOWN $75.60 TODAY/NO CHANGES IN GOLD AT THE GLD:// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 8 /2026/WITH GOLD DOWN $3.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 6.936 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 5 /2026/WITH GOLD DOWN $134;85 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 4 /2026/WITH GOLD UP $39.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.143 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 3 /2026/WITH GOLD DOWN $51.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.856 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.000 TONNES

JUNE 2 /2026/WITH GOLD UP $7.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.712 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.856 TONNES

JUNE 1 /2026/WITH GOLD DOWN $79.30 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 29 /2026/WITH GOLD UP $59.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

GLD INVENTORY: 1013.350 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JUNE 26 WITH SILVER UP $0.86: : HUGE CHANGES IN INVENTORY AT THJE SLV A DEPOSIT OF 2.352 MILLION OZ INTO THE SLV/./ // :INVENTORY RESTS AT 481.976 MILLION OZ

JUNE 25 WITH SILVER UP $0.69: : SMALL CHANGES IN INVENTORY AT THJE SLV A WITHDRAWAL OF 769,000 OUT OF THE SLV/./ // :INVENTORY RESTS AT 479.624 MILLION OZ

JUNE 24 WITH SILVER DOWN $4.18: : SMALL CHANGES IN INVENTORY AT THJE SLV A DEPOSIT OF 93,000 MILLION OZ INTO THE SLV/./ // :INVENTORY RESTS AT 480.393 MILLION OZ

JUNE 19 WITH SILVER UP $1.11: : NO CHANGES IN INVENTORY AT THJE SLV/./ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 18 WITH SILVER DOWN $4.80: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: HUGE CHANGES IN INVENTORY A WITHDRAWAL OF 1.086 MILLION OZ FROM THE SLV././ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 17 WITH SILVER UP $0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: NO CHANGE IN INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 16 WITH SILVER DOWN $0.13: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.362 MILLION OZ INTO THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 15 WITH SILVER UP $3.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.357 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 481.026 MILLION OZ

JUNE 12 WITH SILVER UP $3.34: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.769 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 482.383 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.12: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.226 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.152 MILLION OZ

JUNE 10 WITH SILVER DOWN $0.50: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.909 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.378 MILLION OZ

JUNE 9 WITH SILVER DOWN $3.35: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.407 MILLION OZ INTO INTO THE SLV /./ // :INVENTORY RESTS AT 484.287 MILLION OZ

JUNE 8 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 543,000 OZ FROM THE SLV /./ // :INVENTORY RESTS AT 482.880 MILLION OZ

JUNE 5 WITH SILVER DOWN $4.86: NO CHANGES IN SILVER INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 4 WITH SILVER UP $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.432 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 3 WITH SILVER DOWN $2.55: NO CHANGES IN SILVER INVENTORY AT THE SLV >> /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

CLOSING INVENTORY 481.976 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD.\

Last growl of the PM bear?

We are into contract expiry on Comex again. Silver’s active July contract settles on Monday. Option expiry was yesterday. Are we now about to see gold and silver prices recover?

| Alasdair MacleodJun 26∙Paid |

It has been a long slog lower with silver more than halving from the 29th of January spike and gold losing over $1,500. It should be the paper markets’ get-out-of-jail card, and they have certainly managed to reduce their liabilities. The cost has been enabling China to pick up large quantities of physical gold — 692 tonnes — and ridding herself of about $26bn up to May this year so far. And she has accumulated 1,626 tonnes of silver in Q1 2026, increasing to an estimated 2,000-2,500 tonnes to date.

In effect, the cost of Western book-squaring has been a loss of large quantities of bullion. And now China’s major banks are giving notice to their trading customers to close their speculative positions in gold and silver — more on this below.

In this wrap-up week for July contracts on Comex, gold declined to $4,050 this morning in European trade, down $160 from last week’s close, having traded as low as $3,960 yesterday. Silver at $58.30 was down $6.40 over the same time scale. Since 1st January, silver is down 18% and gold is down by 6.5%.

The influence of contract expiry in silver is illustrated by the surge in volume on Comex:

In the last week, open interest has contracted by 4,882 contracts representing 24,410,000 ounces. It marks a long period of declining open interest to the lowest levels for more than two decades:

For establishment market makers and bullion bank traders, it has been a remarkable record of risk containment. From July 2025, these actors in the swap category have managed to reduce their net shorts from 82,217 contracts to 25,706 contracts currently. But the swaps are still short of an average of $784bn at current valuations. Their only redemption has been producer hedging increasing their shorts by 16,000 contracts in the last year.

The story in gold is similar. The next chart of gold’s open interest on Comex makes this point:

In summary, both gold and silver for deferred settlement are as oversold as it gets. It is the point at which investors bent on accumulating wealth measured in their fiat currencies have been selling out, while the establishment is buying — in the case of market makers seeing which way the winds are blowing and trying to contain their prospective losses.

Asians, led by China’s government, see things differently. They don’t want our paper, whether that be a market promise to deliver or fiat currencies as liabilities of G7 central banks. Some 448 tonnes of gold and 5,928 tonnes of silver have been stood for delivery on Comex this year so far, despite the discouragement of falling prices. They understand that real money has no counterparty risk, and that is gold. Fluctuations in paper values are irrelevant. Customs returns tell us that China encashed paper dollars for 692 tonnes of gold by end-May and presumably continued to do so in June.

China realises that she must bring gold trading for her yuan closer to home and beyond the control of the US and other G7 governments. It would be naïve of us to think that China won’t apply similar methods, but from her actions it is clear that she intends to use gold to secure the value of her own currency by turning it into a gold substitute. She can do that at a time of her choosing, but when she does the entire fiat currency system will be exposed as a sham and face collapse.

It appears that the word is out to China’s large banks. China Construction Bank is closing its customer trading facilities for gold and silver on the Shanghai Gold Exchange from July 24th and ICBC made a similar announcement for the same date: “It would close agency personal auction trading through mobile banking, online banking. After the closure the closing selling and delivery operations of customers holding positions will be restricted.”

Coupled with Chinese banks reducing transaction fees to 0.2% on their customers’ gold accumulation accounts, these moves are clearly aimed at reducing speculation and encouraging accumulation. The common date of 24th July suggests an event is in the wings. What that will be we can only guess.

Timing is of the essence. If she acts too soon China will be blamed for creating all our woes. She might decide to wait until it is obvious that she acts to protect herself from the collapse in our fiat currencies, which are entirely our responsibility. It seems unlikely that 24th July will see the yuan fixed to gold. Could it be a revelation of how many tonnes China has actually accumulated off-balance-sheet over the last 40 years, as a first step to a yuan gold standard?

Whatever it is, the message from China’s establishment banks to its customers is: Don’t be short!

3. CHRIS POWELL AND HIS GATA DISPATCHES

ANDREW MAGUIRE MENTIONED IN THIS VIDEO….

Mining entrepreneur Sprott surveys the damage and the anomalous fundamentals

Submitted by admin on Thu, 2026-06-25 23:48 Section: Daily Dispatches

11:48p ET Thursday, June 25, 2025

Dear Friend of GATA and Gold (and Silver):

In a discussion this week with the TF Metals Report’s Craig Hemke for the Sprott Money channel at YouTube, mining entrepreneur Eric Sprott surveyed the recent smashes in the gold and silver markets, indications of and potential mechanisms for market manipulation, the migration of gold and silver from the West to Asia, the spectacular indebtedness of the U.S. government, the likely overvaluation of enterprises involved with artificial intelligence, and the anomaly of falling gold and silver prices amid fundamentals that seem overwhelmingly favorable for the monetary metals.

Sprott still thinks those fundamentals will prevail even as the recent volatility has been distressing.

The discussion is 45 minutes long and can be viewed here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. ANDREW MAGUIRE/LIVE FROM THE VAULT; 277

Maguire and Hemke say gold ‘correction’ is over and expect revaluation

Submitted by admin on Mon, 2026-06-22 11:56 Section: Daily Dispatches

11:56a ET Monday, June 22, 2025

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire and the TF Metals Report’s Craig Hemke, in conversation on this week’s edition of Kinesis Money’s “Live from the Vault” program, agree that gold’s “correction” is over and speculate how a U.S. Treasury revaluation of the monetary metal to a much higher price may come about soon.

The program is 57 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

5. COMMODITY REPORT//BITCOIN

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 93.02 PTS OR 2.26%

HANG SENG CLOSED DOWN 405.05 PTS OR 1.76%

Nikkei CLOSED DOWN 2958.34 PTS OR 4.09%

//Australia’s all ordinaries CLOSED UP 0.07%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7982

/ OFFSHORE CLOSED UP AT 6.8038 Oil UP TO 69.75 dollars per barrel for WTI and BRENT UP TO 72.83 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING UP (6.7982) OFFSHORE YUAN TRADING UP TO 6.8038 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.7982

OFFSHORE YUAN: UP TO 6.8038

1.HANG SANG CLOSED DOWN 405.05 PTS OR 1.76%

2. Nikkei closed DOWN 2959.34 PTS OR 4.09%

WEST TEXAS INTERMEDIATE OIL UP TO 69.78

BRENT; 72.83

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 101.00/// EURO RISES TO 1.1404 UP 42 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +2.600 DOWN 3 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA CROSS NOW AT 161.63… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.800 DOWN 4 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP( 6.7982) AND OFFSHORE: UP AT 6.8038

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.8468/ Italian 10 Yr bond yield DOWN to 3.592/ SPAIN 10 YR BOND YIELD DOWN TO 3.338%

3i Greek 10 year bond yield UP TO 3.531%

3j Gold at $4052.65 //Silver at: 58.36 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 76/ 100 roubles/77.61

3m oil (WTI) into the 69 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 161.63 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.600% DOWN 3 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.800 DOWN 3 PTS..: USA/SF this 0.8084 as the Swiss Franc . Euro vs SF: 0.9219

USA 10 YR BOND YIELD: 4.371 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.858 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.088 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 46.63 UP 11 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.7050 UP 1 PTS

30 YR UK BOND YIELD: 5.419 UP 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.385 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.013 UP 1 BASIS PTS.

Futures Drop, Chips Resume Slide As OpenAI IPO Delay Dents Sentiment

Friday, Jun 26, 2026 – 08:31 AM

Futures point to a lower start for cash trading on the last day of the week, as tech stocks dragged global indexes lower following renewed selling in chipmakers, while a report that OpenAI could postpone plans to go public also weighed on sentiment. The volatility reflects a valuation test, profit‑taking and flow-driven positioning, according to Christian Stocker, equity strategist at UniCredit, who suggests it’s a “temporary correction within a still-intact long-term AI growth trend.” As of 8:00am ET, Nasdaq 100 futures slid 1.1%, while those on the S&P 500 fell 0.4%. In premarket trading, semiconductor names, including Micron and optical stocks were broadly lower following news of OpenAI’s IPO delay; the “chip paying” hyperscalers showing moderate gains as the equilibrium seems to shift away from chip stocks. A selloff in Korean chip giants Samsung Electronics and SK Hynix triggered a second trading suspension in Seoul within days. Oil resumed its slide, failing to lift stocks but offering a fillip to bonds. Bond yields declined further led by the front-end of the curve: 2y is down 3.5bp; USD is lower. Oil fell -2.74 this morning to $69.18. US economic data calendar includes May goods trade balance, retail and wholesale inventories (8:30am), June final University of Michigan sentiment (10am) and Kansas City Fed services activity (11am). Fed speaker slate includes Minneapolis Fed’s Kashkari at 11:30am

In premarket trading, Mag 7 are mixed: Microsoft is the is a top gainer as investors rotate into software stocks from hardwar (Microsoft +0.8%, Apple +0.5%, Amazon unchanged, Meta Platforms +0.3%, Alphabet -0.7%, Nvidia -1%, Tesla -1.1%).

- Semiconductor stocks are broadly lower amid investor concerns over the staying power of chip demand given price increases seen across Apple and Xbox products. A potential delay to OpenAI’s IPO, as reported by the New York Times, also dampened risk sentiment.

- ON Semiconductor (ON) slides 14% after the chipmaker agreed to an all-stock deal to buy Synaptics. Analysts worry that buying a business that’s exposed to smart devices and the consumer market may distract a push to supply for AI data centers. Synaptics (SYNA) is up 4.2%.

- Rocket Lab (RKLB) gains about 1% after the space firm said NASA selected it to provide three Electron launches for two missions, PolSIR and TSIS-2, from early 2027.

- Tango Therapeutics (TNGX) climbs 5% after Jefferies upgraded the drug developer to buy citing durability of its experimental therapy to treat pancreatic cancer.

- Wise (WSE) climbs 5% after the financial technology firm announced it will begin a new buyback program and reported results for the full year which analysts say were in line with expectations.

In other corporate news, EV maker Polestar will exit the US after the Commerce Department banned the company due to a rule prohibiting Chinese software in cars, according to the WSJ. And Volkswagen is looking to cut tens of thousands of additional jobs and may shutter factories in a push to be more competitive, Manager Magazin reported.

Markets are capping a volatile week in which shifting sentiment around the once-relentless tech trade whipsawed stocks, with traders parsing everything from spending plans to corporate earnings. Investors pulled money from US equities for the first time in three months, with record withdrawals from tech.

Friday’s bout of weakness came as price increases in products from Apple Inc. and Microsoft Corp. triggered fears about the staying power of chip demand. A New York Times report that OpenAI could delay its initial public offering until 2027 also brought into focus how volatility could affect the sector. In Japan, OpenAI backer SoftBank Group Corp. tumbled following the NYT report, sending the Nikkei 225 down 4.2%. The tech sector led declines in Europe as well, with the Stoxx 600 on course for its worst performance since the middle of May.

“Technology remains a crowded trade, positioning is relatively tight, and that makes the sector more sensitive to negative news flow or sharp moves in individual names,” said Francisco Simon, European head of strategy at Santander Asset Management.

AI valuations relative to the rest of the S&P 500 have fallen to their lowest levels since the Iran war, with AI stocks now trading at just a 15% P/E premium to ex-AI stocks, notes Bloomberg. The case for the AI trade remains intact, but the risk of getting it wrong has risen considerably with leverage, crowding and dispersion in focus.

Investors say the roller-coaster week shows that while the case for the AI-trade is still strong, the days of everything going up in a straight line appear to be over. While there hasn’t been panic selling, the cracks are real, and extreme investor positioning means the easy days could be a thing of the past.

The most sensible strategy “is to maintain well-diversified portfolios across geographies, styles, sizes, companies, and sectors,” said David Manso, chief investment officer at CaixaBank AM. “In a couple of weeks, the earnings season will kick off, and leading indicators are pointing in the right direction. We expect corporate results to become a positive catalyst.”

Also in AI, the Pentagon has revised its doctrine on how the US military picks its targets in battle, opening the way for AI to make critical wartime decisions in the future.

In politics, New York City’s Rent Guidelines Board voted to freeze some apartment rents, handing Mayor Mamdani a major political victory. Commerce Secretary Lutnick intervened to delay the opening of a new bridge between the US and Canada and is pressing to renegotiate the deal for a larger share of toll revenue.

The Stoxx 600 is down by 0.6%, with energy and technology equities leading declines, while food beverage and personal care drug stocks are the biggest outperformers. Here are the biggest movers Friday:

- Wise shares climb as much as 8.2% after the financial technology firm announced it will begin a new buyback program and reported results for the full year which analysts say were in line with expectations

- Pandora shares rise as much as 5.1% after BofA upgraded the stock to buy from underperform, saying it has a “clear catalyst path ahead as main pressures subside and LFL [like-for-like sales] stabilizes”

- Barratt Redrow and Bellway climb after Berenberg upgrades both stocks to buy, saying depressed valuations, strong balance sheets and attractive capital returns create selective opportunities in UK housebuilders despite a downbeat market outlook

- Koninklijke KPN shares rise as much as 2.5% after the Dutch telecoms firm was upgraded at Citi, as analysts said there is an opportunity for investors to increase their holding in a “quality stock” following a recent pullback

- Technology shares declined in Europe, following Asia peers lower, after Apple slumped Thursday following price increases on its products. A report that OpenAI may delay its IPO also weighed on sentiment

- Zalando shares fall as much as 11% after the German Financial Supervisory Authority BaFin opened a probe into the online fashion retailer’s 2025 report over suspected violations of accounting rules

- Accor shares drop as much as 2.8%, pulling back from an all-time high after the hotelier was downgraded at Jefferies. Analysts believe any potential recovery in the Middle East is already priced in

- INWIT shares slip as much as 2.1% after a downgrade to neutral from buy at Goldman Sachs, which sees “heightened operating and structural uncertainty” for the Italian telecoms company’s investment case

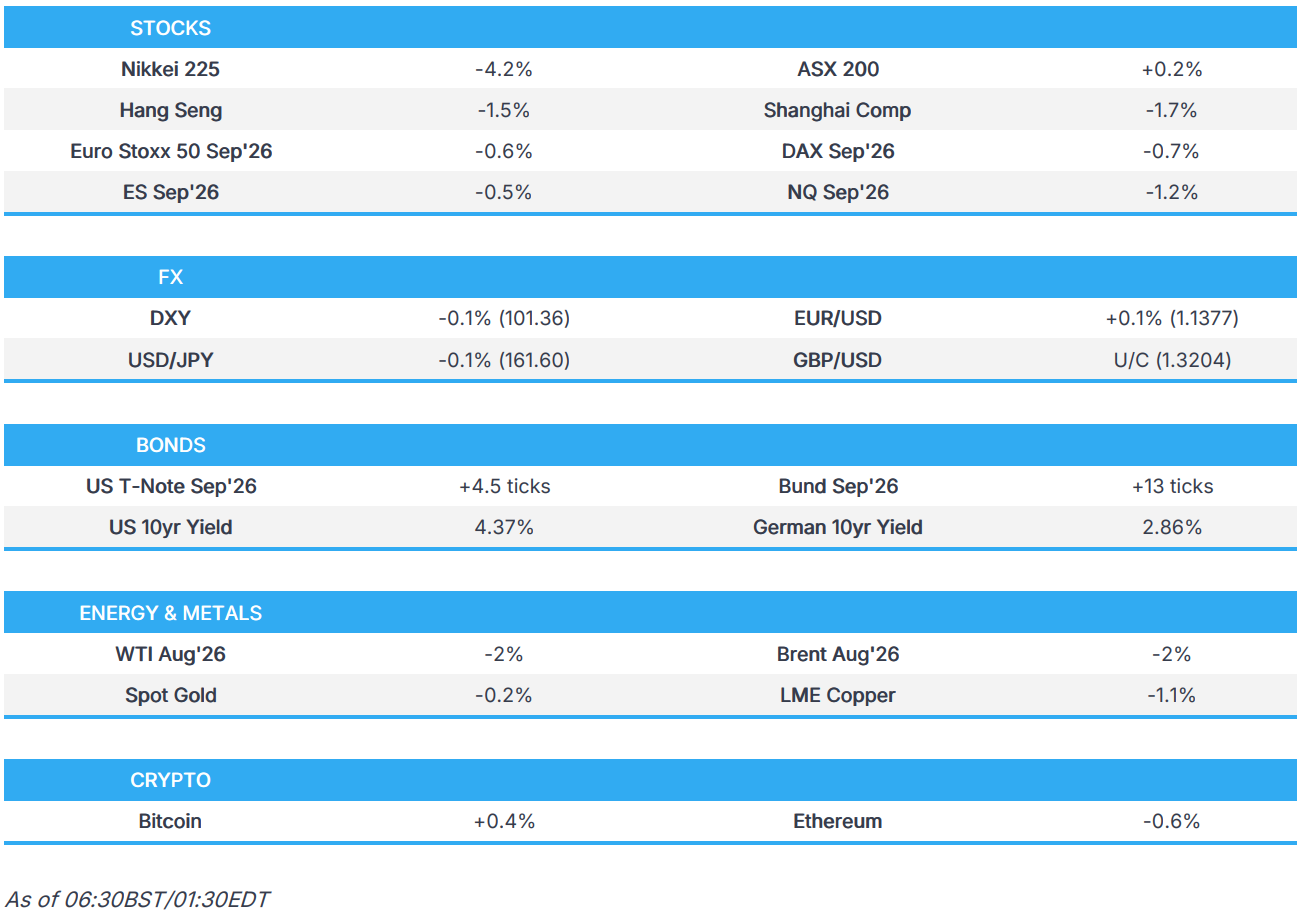

Asian stocks resumed their decline after a brief reprieve the prior day, as concerns about the sustainability of recent tech gains weighed on sentiment. Trading in Asian stocks has remained volatile, with investors torn between whether the rally in technology shares is stretched or backed by confidence in continued AI-driven growth. In the end, tech stocks dragged Asia lower, with the Kospi falling 5.8% and the Nikkei 225 dropping 4.2%. The MSCI Asia Pacific Index dropped as much as 3.6%, with Samsung Electronics, SK Hynix and TSMC weighing most on the gauge. South Korea, Japan and Taiwan led declines. For the week, the index has fallen more than 4%, on track for its worst showing since early March. The selloff comes after Apple said it raised prices to offset cost hikes caused by an unprecedented shortage of memory chips, dragging supplier shares across the region lower. For some, it underscored just how vulnerable the chip rally — which has lifted benchmarks to repeated highs — has become.

“After recent performance, it’s not difficult to expect some consolidation,” said Kieran Calder, head of Asia equity research at Union Bancaire Privee. Apple price hikes highlighted “memory shortage impact on consumer electronics prices and part of the inflation narrative.”

In FX, the Bloomberg Dollar Spot Index down by 0.1% and the euro back to testing $1.14, while sterling has climbed back above $1.32. The Norwegian krone is underperforming among major currencies on the slide in oil prices.

In rates, a falling oil price is lifting short-end bonds across Europe and the US, with a pullback in bets on central bank rate hikes. US two-year yields falling by four basis points and outperforming moves in the same direction in Europe and the UK.

treasury futures hold gains led by front-end tenors, extending Thursday’s yield-curve steepening move, as oil prices resume their slide toward pre-war levels and short-term rate products price in less Fed tightening in the coming months. 2-year yields are lower by 3bp-4bp, long-end tenors by less than 1bp, steepening 2s10s curve by 1.5bp, 5s30s by 3bp; 10-year, down 2bp near 4.375%, outperforms bunds and gilts in the sector by around 1bp. IG dollar issuance slate empty so far. At least two borrowers stood down Thursday as three priced a combined $5.4 billion, paying about 5bps in new issue concessions on deals that were 3 times oversubscribed.

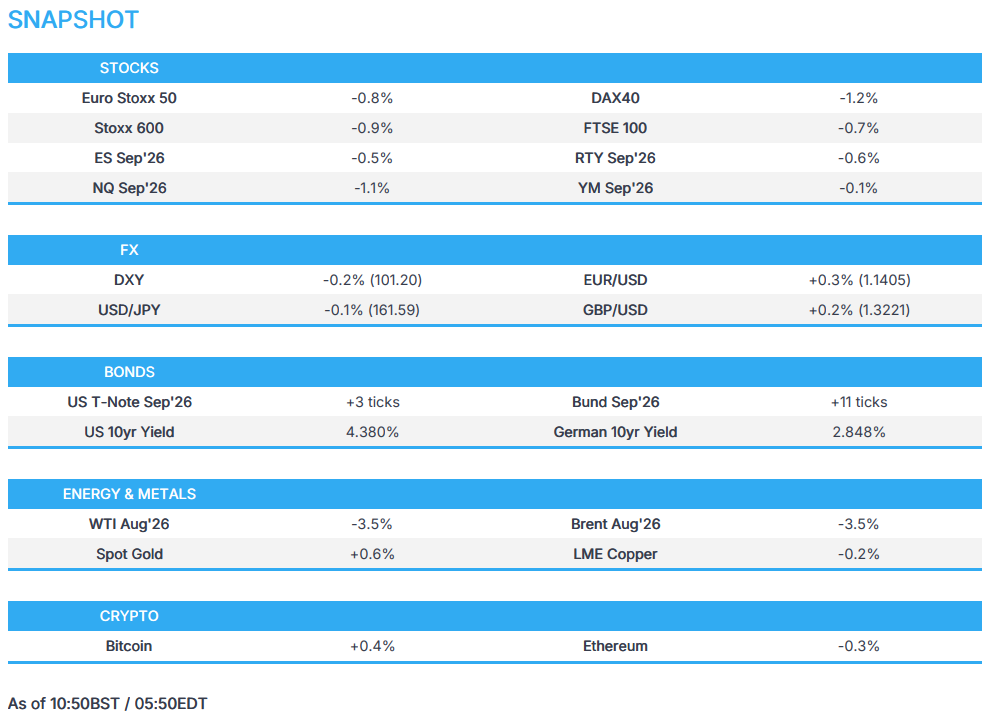

In commodities, Brent is sliding by nearly 4% and below $73/barrel and WTI futures are sinking toward $69/barrel and headed for biggest weekly drop in a month after transits through the Strait of Hormuz accelerated; Gold little changed but holding above $4,000/oz.

US economic data calendar includes May advance goods trade balance, May retail and wholesale inventories (8:30am), June final University of Michigan sentiment (10am) and Kansas City Fed services activity (11am). Fed speaker slate includes Minneapolis Fed’s Kashkari at 11:30am

Market Snapshot

Top Overnight News

- Iranian Deputy Foreign Minister said the safe passage through the Strait of Hormuz without consideration of Iran’s sovereignty is not guaranteed. This follows an Iranian strike on a Singapore-flagged cargo ship after failing to follow the set route: RTRS

- Traffic through Strait of Hormuz slows after attack on ship: RTRS

- US Chip Stocks Decline on Worries Over Memory Prices, OpenAI IPO: BBG

- US President Trump said we have a new market coming up called Iran and added that Iran wants to make a deal with us very badly and thinks they will make a deal.

- Venezuela Seeks Survivors as Quakes Death Toll Hits 235; Quake Crisis to Test Legitimacy of Rodriguez Regime: BBG

- OpenAI Leans Toward Holding Up I.P.O. Until Next Year: NYT

- SpaceX Plans New Starlink Mobile Service for US Consumers: FT

- US President Trump’s administration asked OpenAI to restrict the launch of its next model, GPT-5.6, to only a small set of government-approved partners before a wider release due to security concerns: Axios.

- Russian hawks urge Putin to escalate war, drop US talks as Ukraine strikes deep: RTRS

- Volkswagen weighs up to 100,000 job cuts and four plant closures in overhaul: RTRS

- On immigration, Supreme Court accedes to Trump’s restrictive agenda: RTRS

- Wall Street Realizes It Needs More Than Money to Counter Mamdani: WSJ

- Representatives Gottheimer (D) and Moolenaar (R) are reportedly introducing legislation that would allow US cloud companies to report suspected foreign misuse of advanced AI computing: Axios

- Novak Djokovic Joins General Atlantic in His Wall Street Debut: BBG

- BofA’s weekly flow report notes USD 25.5bln out of cash, USD 5.0bln out of stocks, USD 16.6bln into bonds, USD 0.5bln out of gold. Bull & Bear Indicator fell to 9.1 (prev. 9.2)

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were pressured following the choppy performance stateside, where markets were indecisive amid two-way trade in tech, a recent data deluge and a rebound in oil. The overnight deterioration in risk sentiment coincided with renewed selling in tech after Apple raised prices of some products by nearly 20% and with OpenAI leaning towards delaying its IPO until next year. ASX 200 was rangebound with the index cushioned as the underperformance in tech, telecoms and healthcare was partially offset by resilience in some defensive stocks. Nikkei 225 suffered heavy losses as tech stocks dominated the list of worst performers, with SoftBank down by a double-digit percentage owing to its large exposure to AI and semiconductors. KOSPI remained volatile with the slump triggering a sidecar and eventual circuit breaker alongside notable declines in both Samsung Electronics and SK Hynix. Hang Seng and Shanghai Comp conformed to the sell-off across the region amid the tech rout

Top Asian News

- China sharpened tools for retaliating against foreign sanctions with Beijing preparing a new law that would add to its ability to punish foreign companies and individuals deemed to harm Chinese interests, according to WSJ.

- PBoC has requested that some commercial banks increase lending in June amid ongoing weak credit demand, according to reports.

European bourses (STOXX 600 -0.9%) are entirely in the red in the last session of the week, driven by another day of losses in South Korea (SK Hynix -8.4%, Samsung -5.3%). Some analysts are citing Apple’s price hikes on products due to memory chip shortages as a catalyst for the recent sell-off, raising concerns that rising component costs could curb demand for devices. An analyst at Javelin Wealth Management also said the recent gains for chipmakers could come at the expense of product manufacturers. The losses in South Korean giants have weighed on European chip names (Infineon -3.1%, ASML -1.0%) and indices composed of technology companies (DAX 40 -0.8%, AEX -0.6%). European sectors highlight a negative bias. Optimised Personal Care (+0.8%), Food, Beverages & Tobacco (+0.6%) and Utilities top the sector pile. Energy (-1.5%) is the underperformer again, with Technology (-1.4%) and Financial Services (-1.1%) also lagging.

Top European News

- The Times’ Swinford reported that it is likely to be a two-horse race between Ed Miliband and Shabana Mahmood for chancellor, with allies of Streeting say they do not think he will get the job.

FX

- USD finds itself under modest pressure. DXY at a 101.18 base, but well clear of the 100.76 WTD low, with the index set to see the week out around the middle of its range. In brief, a tale of two halves for the index which began the week on the front foot before reversing after Thursday’s data deluge and continuing to slip since.

- EUR outperforms as a result of the continued USD pressure. No real move to the ECB CES, which showed a moderation in the 12-month price view and an uptick in the growth view. The growth revision is not enough to provide comfortable space for further tightening, and equally the price moderation is not sufficient to take another move off the table. Nonetheless, the price moderation does add to the post-PMI & Lagarde dovish tilt we have seen in recent days.

- In more detail, EUR/USD has breached 1.14 to the upside. Picking up gradually across the morning, as the US data on Thursday has and continues to permit an unwinding of some of the yield differential moves we have seen in recent days, with the Fed more-hawkish and ECB mixed but net less-hawkish, particularly from Lagarde as referenced. However, while it has hit a 1.1407 peak, EUR remains in the red on the week and continuing the near unbroken downward trend of the last seven weeks.

- Elsewhere, G10s generally are slightly firmer against the USD. With GBP the next-best behind EUR, comfortably above 1.3200 and flat/firmer WTD, but again, still towards post June policy announcement lows, as BoE expectations coalesce around the on hold for the foreseeable narrative, despite the hawkish dissenters.

- CAD, JPY and CHF all faring around equally. Of those, USD/JPY participants remain on watch for potential intervention risk, particularly as Japanese authorities tend to target Friday’s and go with the market move rather than fighting it. USD/JPY just above a 161.53 base, and while the JPY is firmer today the bearish trend remains near-enough unbroken at a weekly level over the last month and a half.

- Today is spot month/quarter-end. As a reminder, Barclays model was neutral overall for the USD against all majors, formed of a moderate USD buying signal on the month-end, but countered by a strong USD sell signal for quarter-end

Commodities

- The US-Iran situation remains complex. It was reported that the IRGC attacked a Singapore-flagged cargo ship, after it attempted to traverse through the Strait through a route not designated by the Iranians. This led the UN to pause its evacuation plans for ships around the Strait. Despite the attack, Bloomberg data continues to indicate that ships continue to traverse through the Hormuz, highlighting that traffic continues to flow in “both directions”.

- On the Lebanon front. The US-mediated Lebanon-Israel talks were expected to conclude on Wednesday, but were then extended into today. Israeli sources have suggested that there has been some progress, but no deal has been reached thus far. The negotiations focus on the withdrawal of Israeli troops from southern Lebanon; there may be a chance that Israel will only withdraw from areas where operations have already been concluded, and continue such action in other parts of the region. Therefore, the risk is that Iran is not satisfied by the outcome of the talks, and potentially restart closures of the Strait.

- Crude benchmarks are in the red, with WTI (-3.5%) and Brent (-3.4%) holding at the bottom end of their respective USD 68.98-71.86/bbl and USD 72.14-75.13/bbl ranges. Despite the flare-up on the Strait in the prior session and the continued lack of progress between Lebanon and Israel, crude prices continue to slip. It is the case that as long as ships continue to traverse the Strait, other friction points can be ignored… at least in the short term.

- Spot gold (+0.2%) is ever so slightly firmer this morning, but continues to remain near recent troughs. Today, the yellow-metal holds just above the USD 4k/oz mark, and within a USD 3,982-4,039/oz range. Elsewhere, base metals are broadly slightly lower this morning, with 3M LME copper currently off by c. 0.6%. It currently holds around USD 13.25k/t and within a USD 13,088.3-13,281/t range.

- Saudi Aramco reopened the Ras Tanura oil loading operations after a prolonged halt, with two supertankers loading oil at Ras Tanura on Friday, while another is awaiting loading, according to shipping data.

- Several Japanese-related vessels passed through the Strait of Hormuz as part of IMO evacuation plans, which have since been suspended following the attack on a cargo ship, according to Mainichi.

- China’s MOFCOM released a list of non-state Chinese companies eligible for oil imports.

- Kazakhstan cut the gas production at the Karachaganak gas field after Ukraine drone attacks on Russia’s Orenburg gas processing plant. Raw gas from the field is usually delivered to the Orenburg plant.

- Kazakhstan Energy Minister said we may consider fuel exports to Russia if there is an official request.

- Russia is considering a short-term ban on diesel exports for a few months, TASS reported.

Central Banks

- Fed’s Goolsbee (2027 voter) said it is difficult to determine whether inflation pressures are persistent or temporary, while noting inflation is moving in the wrong direction, and some of that is being driven by one-off factors. He added that inflation remains more concerning on the services side and that spending based on expected future gains makes him concerned about potential inflationary pressures. Goolsbee also said there are some signs of improvement in services inflation, but it remains well above where it needs to be, as well as stated that core inflation it is still too high and trending in the wrong direction, while services-driven core CPI is more concerning than inflation driven by goods or oil-related items. Furthermore, he stated that wages are not a particularly good leading indicator for inflation and that inflation could rise before wages do, adding that inflation needs to be monitored closely.

Geopolitics