EXCHANGE: COMEX

CONTRACT: JULY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,068.300000000 USD

INTENT DATE: 07/01/2026 DELIVERY DATE: 07/06/2026

FIRM ORG FIRM NAME ISSUED STOPPED

092 C DEUTSCHE BANK 100

099 H DEUTSCHE BANK AG 36

363 H WELLS FARGO SECURITI 517

555 C BNP PARIBAS SEC CORP 488

661 C JP MORGAN SECURITIES 108

686 C STONEX FINANCIAL INC 21

709 C BARCLAYS 1

732 C RBC CAP MARKETS 23

737 C ADVANTAGE FUTURES 16

905 C ADM 2

TOTAL: 656 656

MONTH

GOLD: NUMBER OF NOTICES FILED FOR JULY/2026: 656 CONTRACTs NOTICES FOR 65,600 OZ or 2.0404 TONNES

total notices so far: 8536 contracts FOR 853,600 OZ OR 26.5505 TONNES

SILVER NOTICES: 100 NOTICE(S) FILED FOR 0.500 MILLION OZ /

total number of notices filed so far this month : 5176 CONTRACTS (NOTICES) for 25.880 million oz

GLD AND SILV

GLD

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF XX CONTRACTS OR XXX OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 10,000 OZ//NEW STANDING ADVANCES TO 12.970 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 20 CONTRACTS FOR 100,000 OZ//NEW STANDING ADVANCES TO 13.070 MILLION OZ. (IN EXCHANGE FOR RISK THE BUYER ASSUMES THE RISK AND ONLY A CENTRAL BANK WOULD TAKE THAT RISK. THE BUYER IS PROBABLY THE CENTRAL BANK OF INDIA.)

JULY INITIAL STANDING: 37.110 MILLION OZ FOLLOWED BY A SMALL 13 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE OR 0.054 MILLION OZ WHERE DELIVERY WILL OCCUR IN LONDON. THUS STANDING REDUCES TO 35.475 MILLION OZ//

SUMMARY OF OUR JUNE 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE. 64.065 MILLION OZ//FINAL AND FAIR SIZED THIS MONTH.

JULY: 8.775 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 10,000 OZ//NEW STANDING ADVANCES TO 12.960 MILLION OZ TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 20 CONTRACTS FOR 100,000 OZ//NEW STANDING ADVANCES TO 13.070 MILLION OZ

JULY : INITIAL STANDING: 37.110 MILLION OZ FOLLOWED BY TODAY’S SMALL 0.065 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON//STANDING THUS REDUCES TO 35.475 MILLION OZ//

GOLD//OUTLINE

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER OF 0.0186 TONNES/NEW STANDING REDUCES TO 127.03 TONNES

JULY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 23.306 TONNES TO WHICH WE ADD OUR FIRST QUEUE JUMP OF 2.0596 TONNES//NEW STANDING ADVANCES TO 26.650 TONNES

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER JUMP OF 0.0186 TONNES//NEW STANDING REDUCES TO 127.03 TONNES//FINAL

JULY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 23.306 TONNES OF GOLD TO WHICH WE ADD OUR FIRST QUEUE JUMP OF 2.0596 TONNES//NEW STANDING FOR GOLD ADVANCES TO 26.650 TONNES.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 142.053 TONNES

JULY: 15.300 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA MEGA HUGE 3226 CONTRACTS TO AN OI OF 105,734

EFP ISSUANCE 1065 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1065 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3,485 CONTRACTS AND ADD TO THE 1065 E.FP. ISSUED

WE OBTAIN A HUGE LOSS OF 2161 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN OF $0.48

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 10.805 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.48

2.ASIAN AFFAIRS JULY 2 /2025

SHANGHAI CLOSED DOWN 83.56 PTS OR 2.03%

HANG SENG CLOSED UP 174.01 PTS OR 0.71%

Nikkei CLOSED DOWN 1643.96 PTS OR 2,13%

//Australia’s all ordinaries CLOSED UP 0.76%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7891

/ OFFSHORE CLOSED UP AT 6.7935 Oil DOWN TO 67.63 dollars per barrel for WTI and BRENT DOWN TO 70.49 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN// WITH YUAN TRADING UP (6.7891) OFFSHORE YUAN TRADING UP TO 6.7935 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR 2456 CONTRACTS TO 367,083 STILL WELL ABOVE ITS NEW LOW OF 326,052 OI SET JUNE 3, CLOSE TO THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND CLOSE TO THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,052 //JUNE 3 2026 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD HUGE T.A.S. LIQUIDATION DURING WEDNESDAY’S MASSIVE COMEX TRADING// ATTEMPTED RAID JUNE 30 IT SEEMS THAT MANY OF THE SPECULATORS THAT HAVE NOW CONTINUED AGAIN TO GO MASSIVELY ON THE SHORT SIDE WITH BANKERS ON THE LONG SIDE WILL BE OBLITERATED TODAY WHEN THE LONGS TENDERED FOR DELIVERY:

CENTRAL BANKS TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS JULY CONTRACT MONTH!!

THE FAIR SIZED GAIN ON OUR TWO EXCHANGES (1733 CONTRACTS) OCCURRED WITH OUR GAIN IN PRICE IN GOLD (UP $41.95)

WE THUS HAD A FAIR SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1773 CONTRACTS (OR 5.3903 TONNES) WITH OUR STRONG GAIN IN PRICE, AS WE WERE INFORMED OF A HUGE CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 4,189 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIDAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH JUNE

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

JUNE: 0 IN GOLD. THUS FOR THE ENTIRE MONTH IN GOLD ZERO NOTICES WERE FILED.

JULY 0

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO JUNE:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 146+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO

JULY 0

DETAILS ON OUR NEW JUNE COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR GAIN ON OUR TWO EXCHANGES OF 1733 CONTRACTS WITH OUR GAIN IN PRICE ($41.95). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE/JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A MUCH STRONGER SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1643 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

JUNE: ZERO FOR THE MONTH

JULY: ZERO SO FAR

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 146+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE SUBTRACT AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON OF 0.0186 TONNES//NEW STANDING REDUCES TO 127.03 TONNES// TOTAL QUEUE JUMPING FOR THE MONTH FINALIZES AT 62.4217 TONNES OR AVERAGING 3.285 TONNES PER DAY IN JUNE.

JULY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 749,300 OZ OR 23.306 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 2.0596 TONNES//NEW STANDING ADVANCES TO 26.650 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JULY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $41.95)

WE HAD HUGE T.A.S. SPREADER LIQUIDATION WEDNESDAY // COMEX SESSION// DESPITE OUR SMALL GAIN IN PRICE , OUR SPECULATORS STILL WENT MASSIVELY TO THE SHORT SIDE LED BY THE NOSE BY OUR HIGH FREQUENCY MOMENTUM PLAYERS WITH CENTRAL BANKERS TAKING THE LONG SIDE. THE SPECS WERE ANNIHILATED ON THURSDAY AND FRIDAY.

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING //THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $41.95

WE HAD 291 CONTRACTS ADDED AT THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES: 1733 CONTRACTS OR 173,300 OZ (5.3903 TONNES)

JULY DELIVERY MONTH

JULY 2

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 2 ENTRIES i) Out of Asahi: 100,998.442 oz ii) HSBC 32,151.000 oz (1000 kilobars) total withdrawal: 133,149.442 oz or 4.1415 tonnes |

| Deposit to the Dealer Inventory in oz | |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER//gold ENTRIES: 1 i) Into Manfra: 34,281.742 oz total deposit: 34,281.742 oz xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 656 CONTRACTS OR 65,600 OZ 2.0404 TONNES OF GOLD |

| No of oz to be served (notices) | 32 Contracts 3200 OZ 0.099 TONNES |

| Total monthly oz gold served (contracts) so far this month | 8536 notices 853,600 OZ 26.5505 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 1

0 ENTRY

DEPOSITS/CUSTOMER

ENTRIES: 1

i) Into Manfra: 34,281.742 oz

total deposit: 34,281.742 oz

xxxxxxxxxxxxxxxxxx

comex withdrawal

2 ENTRIES

i) Out of Asahi: 100,998.442 oz

ii) HSBC 32,151.000 oz

(1000 kilobars)

total withdrawal: 133,149.442 oz or 4.1415 tonnes

adjustments: 0//

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JULY OI STANDS AT 688 CONTRACTS HAVING A LOSS OF 1510 CONTRACTS. WE HAD 2172 NOTICES FILED ON WEDNESDAY SO WE GAINED 662 CONTRACTS OR 66,200 OZ(2.0596 TONNES). WE THUS HAD A STRONG QUEUE JUMP WHERE A CENTRAL BANK WILL TAKE IMMEDIATE DELIVERY OF GOLD ON A T PLUS ONE BASIS

AUGUST LOST 680 CONTRACTS TO AN OI OF 274,334

SEPTEMBER GAINED 353 CONTRACTS UP TO AN OI OF 1606.

.

We had 656 contracts filed for today representing 65,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 656 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 108 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY. /2026. contract month, we take the total number of notices filed so far for the month (8536) to which we add the difference between the open interest for the front month of JULY (688 CONTRACTS) minus the number of notices served upon today 656 x 100 oz per contract) equals 856,000 OZ OR (26.650 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JULY. /2026. contract month, we take the total number of notices filed so far for the month (8536) to which we add the difference between the open interest for the front month of JULY( 688 CONTRACTS) minus the number of notices served upon today 656 x 100 oz per contract) equals 856,800 OZ OR (26.650 Tonnes of gold)

new total of gold standing in JULY becomes 26.650 TONNES//

TOTAL COMEX GOLD STANDING FOR JULY 26.650TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS NON ACTIVE DELIVERY MONTH OF JULY.

confirmed volume THURSDAY confirmed 167,595/ FAIR// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,882,101.381 oz 58.541 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,882,101.381 tonnes oz 58.541 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 27,460,952.557 oz

TOTAL REGISTERED GOLD 14,826,009.194 tonnes (461.15tonnes)

TOTAL OF ALL ELIGIBLE GOLD 12,634,943.363 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 12,943,908 oz ((REG GOLD- PLEDGED GOLD)=

402.609 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JULY DELIVERY MONTH

JULY 2

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 entries |

| Deposits to the Dealer Inventory | 0 entries |

| Deposits to the Customer Inventory | 2 entries i) Into Loomis: 600,875.730 oz ii) Into Manfra: 23,867.675 oz total deposit: 624,744.365 oz |

| No of oz served today (contracts) | 100 CONTRACT(S) ( 0.500 MILLION OZ) |

| No of oz to be served (notices) | 1919 Contracts (9.595 MILLION oz) |

| Total monthly oz silver served (contracts) | 5176 contracts 25.880 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRY:2

2 entries

i) Into Loomis: 600,875.730 oz

ii) Into Manfra: 23,867.675 oz

total deposit: 624,744.365 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

0 entries

adjustments 1; DEALER ACCT TO CUSTOMER ACCT

a) Asahi: 133,753,200 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 92.876 MILLION OZ//.TOTAL REG + ELIGIBLE. 323.161 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JULY /2026 OI: 2019 OPEN INTEREST CONTRACTS FOR A LOSS OF 5087 CONTRACTS. WE HAD 5074 CONTRACTS SERVED ON WEDNESDAY SO WE LOST 13 CONTRACTS OR A HUGE 0.065 MILLION OZ UNDERWENT AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE THEY WILL TAKE DELIVERY OVER ON THAT SIDE OF THE POND.

AUGUST SAW A LOSS OF 61 CONTRACTS UP TO 1948…

SEPTEMBER SAW A GAIN OF 784 CONTRACTS UP TO AN OI OF 82,163 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 100 or 0.500 MILLION oz

CONFIRMED volume THURSDAY; 53,357// poor//

XXX

AND NOW JULY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 5176 X5,000 oz = 25.880 MILLION oz

to which we add the difference between the open interest for the front month of JULY(2019) AND the number of notices served upon today (100 )x (5000 oz)

Thus the standings for silver for the JULY 2026 contract month: (5176 )Notices served so far) x 5000 oz + OI for the front month of JULY ( 2019) minus number of notices served upon today (100)x 5000 oz equals silver standing for the JULY..contract month equating to 35.475 MILLION OZ. (still a very strong delivery month)

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 92.976 million oz of registered silver

JPMorgan as a percentage of total silver: 137.898/323.161 million: 42.71%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JULY 2 /2026/WITH GOLD UP $44,05 /NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JULY 1 /2026/WITH GOLD UP $42.95 /NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JUNE 30 /2026/WITH GOLD UP $2.85 /NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JUNE 29 /2026/WITH GOLD DOWN $58.30 /HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 8.223 TONNES OF GOLD FROM THE GLD // ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JUNE 26 /2026/WITH GOLD UP $49.10 /HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 4.287 TONNES OF GOLD FROM THE GLD // ./ //:/INVENTORY RESTS AT 1013.350 TONNES

JUNE 25 /2026/WITH GOLD UP $42.70 /NO CHANGES IN GOLD AT THE GLD: // ./ //:/INVENTORY RESTS AT 1017.637 TONNES

JUNE 24 /2026/WITH GOLD DOWN $141.55 /HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.563 TONNES OF GOLD OUT OF THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1017.637 TONNES

JUNE 19 /2026/WITH GOLD UP $36.85 /HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 7.421 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1020.49 TONNES

JUNE 18 /2026/WITH GOLD DOWN $135.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.856 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1013.069 TONNES

JUNE 17 /2026/WITH GOLD UP $20.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.427 TONNES OF GOLD FROM THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1012.213 TONNES

JUNE 16 /2026/WITH GOLD UP $4.45 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 15 /2026/WITH GOLD UP $111.10 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 12 /2026/WITH GOLD UP $123.30 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 11 /2026/WITH GOLD DOWN $15.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.855 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 10 /2026/WITH GOLD DOWN $153.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.426 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1016.495 TONNES

JUNE 9 /2026/WITH GOLD DOWN $75.60 TODAY/NO CHANGES IN GOLD AT THE GLD:// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 8 /2026/WITH GOLD DOWN $3.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 6.936 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 5 /2026/WITH GOLD DOWN $134;85 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 4 /2026/WITH GOLD UP $39.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.143 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 3 /2026/WITH GOLD DOWN $51.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.856 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.000 TONNES

JUNE 2 /2026/WITH GOLD UP $7.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.712 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.856 TONNES

JUNE 1 /2026/WITH GOLD DOWN $79.30 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 29 /2026/WITH GOLD UP $59.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

GLD INVENTORY: 1005.077 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JULY 2 WITH SILVER UP $0.58: : NO CHANGES IN INVENTORY AT THE SLV// :INVENTORY RESTS AT 479.360 MILLION OZ

JULY 1 WITH SILVER UP $0.48: : SMALL CHANGES IN INVENTORY AT THE SLV A DEPOSIT OF 0.233 MILLION OZ OUT OF THE SLV/./ // :INVENTORY RESTS AT 479.360 MILLION OZ

JUNE 30 WITH SILVER UP $1.35: : HUGE CHANGES IN INVENTORY AT THE SLV A WITHDRAWAL OF 1.447 MILLION OZ OUT OF THE SLV/./ // :INVENTORY RESTS AT 479.127 MILLION OZ

JUNE 29 WITH SILVER DOWN $1.08: : HUGE CHANGES IN INVENTORY AT THJE SLV A WITHDRAWAL OF 1.402 MILLION OZ OUT OF THE SLV/./ // :INVENTORY RESTS AT 480.574 MILLION OZ

JUNE 26 WITH SILVER UP $0.86: : HUGE CHANGES IN INVENTORY AT THJE SLV A DEPOSIT OF 2.352 MILLION OZ INTO THE SLV/./ // :INVENTORY RESTS AT 481.976 MILLION OZ

JUNE 25 WITH SILVER UP $0.69: : SMALL CHANGES IN INVENTORY AT THJE SLV A WITHDRAWAL OF 769,000 OUT OF THE SLV/./ // :INVENTORY RESTS AT 479.624 MILLION OZ

JUNE 24 WITH SILVER DOWN $4.18: : SMALL CHANGES IN INVENTORY AT THJE SLV A DEPOSIT OF 93,000 MILLION OZ INTO THE SLV/./ // :INVENTORY RESTS AT 480.393 MILLION OZ

JUNE 19 WITH SILVER UP $1.11: : NO CHANGES IN INVENTORY AT THJE SLV/./ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 18 WITH SILVER DOWN $4.80: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: HUGE CHANGES IN INVENTORY A WITHDRAWAL OF 1.086 MILLION OZ FROM THE SLV././ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 17 WITH SILVER UP $0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: NO CHANGE IN INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 16 WITH SILVER DOWN $0.13: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.362 MILLION OZ INTO THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 15 WITH SILVER UP $3.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.357 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 481.026 MILLION OZ

JUNE 12 WITH SILVER UP $3.34: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.769 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 482.383 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.12: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.226 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.152 MILLION OZ

JUNE 10 WITH SILVER DOWN $0.50: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.909 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.378 MILLION OZ

JUNE 9 WITH SILVER DOWN $3.35: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.407 MILLION OZ INTO INTO THE SLV /./ // :INVENTORY RESTS AT 484.287 MILLION OZ

JUNE 8 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 543,000 OZ FROM THE SLV /./ // :INVENTORY RESTS AT 482.880 MILLION OZ

JUNE 5 WITH SILVER DOWN $4.86: NO CHANGES IN SILVER INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 4 WITH SILVER UP $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.432 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 3 WITH SILVER DOWN $2.55: NO CHANGES IN SILVER INVENTORY AT THE SLV >> /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

CLOSING INVENTORY 479.360 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD.\

3. CHRIS POWELL AND HIS GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT; 279 AND 278

MUST VIEW

Maguire and Hemke say gold ‘correction’ is over and expect revaluation

Submitted by admin on Mon, 2026-06-22 11:56 Section: Daily Dispatches

11:56a ET Monday, June 22, 2025

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire and the TF Metals Report’s Craig Hemke, in conversation on this week’s edition of Kinesis Money’s “Live from the Vault” program, agree that gold’s “correction” is over and speculate how a U.S. Treasury revaluation of the monetary metal to a much higher price may come about soon.

The program is 57 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

5. COMMODITY REPORT//COPPER

Copper Demand Surges, But Supply Deficit Is Hard To Solve, Expert Says

Wednesday, Jul 01, 2026 – 05:50 PM

Authored by Mary Prenon via The Epoch Times,

The ongoing artificial intelligence (AI) boom underscores a harder-to-resolve supply issue for copper, according to veteran natural resource investor Rick Rule.

Speaking recently with Siyamak Khorrami, host of EpochTV’s “Market Insider,” Rule said the increasingly energy-intensive lives people around the world are living have pushed up demand for copper. With companies and countries investing heavily in AI, future demand for the red metal will be “staggering,” he said.

At the same time, the world, especially the United States, doesn’t have enough copper development projects “in the pipeline,” Rule said, making a copper shortage and higher prices inevitable.

Growing Supply Deficit

According to the International Copper Study Group, global refined copper consumption rose to 28.2 million metric tons in 2025 from 25.8 million metric tons in 2022, while production increased to 28.6 million metric tons from 25.2 million metric tons over the same period. This represents a supply surplus of 400,000 metric tons.

However, given the essential role copper plays in electrification, digitalization, and technologies such as AI, data centers, electric vehicles, and defense, a January S&P Global study predicts that demand for the metal will rise to 42 million metric tons by 2040. The study also estimates that, without “meaningful supply expansion,” there could be a copper shortfall of about 10 million metric tons by then.

Copper prices have risen significantly. Copper futures on the New York Mercantile Exchange settled at $6.20 per pound on June 28, nearly doubling from their post-pandemic low of $3.23 per pound, reached on July 11, 2022.

The situation is more challenging for the United States. The country is a net copper importer, producing less than half of the refined copper it consumes. According to the United States Geological Survey, a scientific agency under the Department of the Interior, America produced 850,000 metric tons of refined copper in 2025 while consuming 2.2 million metric tons, resulting in a deficit of more than 1 million metric tons.

The United States is expected to remain a net importer of copper through 2040, with imported refined copper projected to account for about 70 percent of consumption, according to a June 23 SEC filing citing Wood Mackenzie data.

In November 2025, the Department of the Interior added copper to the U.S. Geological Survey’s critical minerals list.

Underinvestment

“In copper, we have been systemically underinvested in exploration, in construction, in development, and we’ve been doing so for 30 years,” Rule told Khorrami.

“This is a capital-intensive, long-term business. There is nothing we can do right now—nothing, not one thing—that will prevent a supply shortage within five years.”

Source: U.S. Geological Survey, Mineral Commodity Summaries 2025—Copper

Rule said developing a new copper mine is a very long process, taking about 10 years to explore and find a mine, three years to drill, three more years “in a good country” to secure a permit and funding, and two years to build—about 18 years in total.

“The difficulty is that people weren’t doing enough of this 18 years ago,” he said.

Wood Mackenzie estimated in a 2021 analysis that the world copper industry had committed around $120 billion in capital spending to maintain production at the time, offsetting the impact of grade decline and depletion.

“Nonetheless, without additional substantial investment, production will decline from 2024 onwards. Coupled with demand growth, this decline in output will lead to a theoretical shortfall of around [16 million metric tons] by 2040,” the analysis states. To close the copper supply shortfall, the analysis said, the industry would need about $325 billion in additional investment.

“The industry is looking right down the barrel at an incredible capital spend to merely maintain current production levels, never mind increase it to meet the demands of rural electrification in the third world, data centers, electric vehicles, the electrification of everything,” Rule said.

“If you believe the numbers that people like Google and Amazon are putting out in terms of their data center demands, we will need to produce more copper between 2026 and 2050—24 short years—than has been mined in the history of mankind,” he said.

Rule said the industry has entered a copper construction cycle.

“For a long time, when copper was languishing at $3 a pound, the industry didn’t make enough money to build new mines; $6 a pound is not a bad incentive price.”

Permitting Hurdles

However, he said there are currently few construction-ready projects due to decades of underinvestment in mineral exploration. In the United States, he added, the permitting process is a major hurdle for these projects to move forward.

For example, Rule said the Resolution Copper project, jointly owned by Australian mining giants Rio Tinto and BHP and located in Arizona, is a high-quality copper deposit and well-located, but has been waiting more than a decade for a permit.

According to Rio Tinto’s website, if developed, the Resolution Copper project could be one of the largest copper mines in the United States, having the potential to supply up to one-quarter of the U.S. copper demand.

After decades of exploration, the Resolution deposit was officially discovered in 1995, according to the Department of Agriculture. It started the permitting process in 2013 and released its independent Final Environmental Impact Statement in 2019, entering a new phase of public consultation, according to a Rio Tinto press release. The company said in a March release that it had completed a key land exchange advancing the project toward development.

“All of this points to the fact that we’re going to have to get used to higher copper prices,” Rule said.

END

SILVER/MEL FISHER ATOCHA

(I HAVE MYSELF A 8 REAL SILVER PIECE FROM THE ATOCHA/DATED 1622)

Treasure Hunters Recover $100K Silver Bar From Legendary 1622 Shipwreck

by Tyler Durden

Thursday, Jul 02, 2026 – 05:45 AMTreasure hunters searching the waters off the Florida Keys have uncovered a 22-pound silver bar believed to have come from the wreck of the Spanish galleon Nuestra Señora de Atocha, according to a new report from SlashGear.

The artifact, estimated to be worth about $100,000, is the first silver bar recovered from the legendary wreck site in nearly three decades. It was discovered by divers working with Mel Fisher’s Shipwreck Expeditions during a routine recovery mission.

The Atocha was part of a Spanish treasure fleet that was destroyed by a powerful hurricane in September 1622 while returning to Europe. Loaded with silver, gold, and other valuables collected from Spain’s colonies in the Americas, the ship went down in relatively shallow water, taking nearly its entire crew with it and scattering its cargo across the ocean floor.

The report says that the wreck remained one of history’s great lost treasures until famed salvager Mel Fisher finally located its main debris field in 1985 after a 16-year search. That breakthrough yielded hundreds of millions of dollars in treasure, but archaeologists and recovery teams have continued to uncover new artifacts from the sprawling debris field ever since.

Experts believe the site is still far from exhausted. Mel Fisher’s organization estimates that more than $120 million worth of silver, copper ingots, bronze cannons, and other cargo may still remain buried beneath the seabed, waiting to be uncovered by future expeditions.

The latest recovery also serves as a reminder that some of history’s greatest discoveries don’t happen all at once. Centuries of shifting sand, storms, and changing ocean currents continue to expose artifacts that were hidden for generations, giving modern explorers fresh opportunities to recover pieces of one of the world’s most famous shipwrecks.

While the silver bar’s estimated value is impressive on its own, discoveries like this are about more than money. Each recovered artifact helps historians better understand the scale of Spain’s colonial trade network, the enormous wealth transported across the Atlantic, and the risks that came with moving treasure by sea during the Age of Exploration.

END

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 83.56 PTS OR 2.03%

HANG SENG CLOSED UP 174.01 PTS OR 0.71%

Nikkei CLOSED DOWN 1643.96 PTS OR 2,13%

//Australia’s all ordinaries CLOSED UP 0.76%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7891

/ OFFSHORE CLOSED UP AT 6.7935 Oil DOWN TO 67.63 dollars per barrel for WTI and BRENT DOWN TO 70.49 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN// WITH YUAN TRADING UP (6.7891) OFFSHORE YUAN TRADING UP TO 6.7935 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.7891

OFFSHORE YUAN: UP TO 6.7935

1.HANG SANG CLOSED UP 174.01 PTS OR 0.71%

2. Nikkei closed DOWN 1643.96 PTS OR 2.73%

WEST TEXAS INTERMEDIATE OIL DOWN TO 67.63

BRENT; 70.49

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 100.82/// EURO RISES TO 1.1410 UP 33 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.772 UP 7 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA CROSS NOW AT 161,35… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 4.034 UP 7 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP( 6.7891) AND OFFSHORE: UP AT 6.7935

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EU German 10yr bund YIELD UP TO +2.9668/ Italian 10 Yr bond yield UP to 3.727/ SPAIN 10 YR BOND YIELD UP TO 3.418%

3i Greek 10 year bond yield UP TO 3.610%

3j Gold at $4063.80 //Silver at: 59.66 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 51/ 100 roubles/78.01

3m oil (WTI) into the 67 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 161.35 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.772% UP 7 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 4.034 UP 7 PTS..: USA/SF this 0.8057 as the Swiss Franc . Euro vs SF: 0.9182

USA 10 YR BOND YIELD: 4.493 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.9133 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.170 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 46.70 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.8133 UP 1 PTS

30 YR UK BOND YIELD: 5.544 UP 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.448 UP 7 BASIS PTS

5 YR CANADA BOND YIELD: 3.071 UP 6 BASIS PTS.

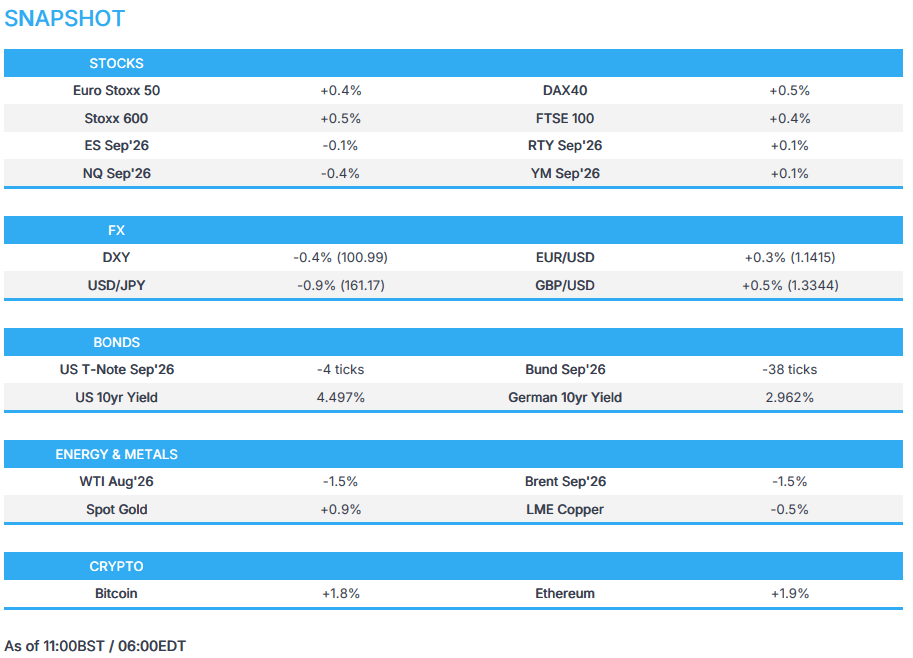

1b European opening report

DXY slips below 101.00, weighed on by possible JPY intervention; US jobs report awaits – Newsquawk US Market Open

Thursday, Jul 02, 2026 – 06:37 AM

- Qatar and Pakistan mediators concluded separate meetings with US and Iranian negotiators in Doha, highlighting positive progress on issues related to the Islamabad MoU.

- US equity futures trade mixed, with the NQ weighed by tech selling in South Korean stocks.

- DXY slips below the 101.00 handle, as the JPY strengthens on possible intervention.

- Fixed income benchmarks trade on the softer side heading into the US jobs report; NFP expected at 110K.

- Crude benchmarks continue to trade lower, Brent -1.5%.

- Looking ahead, highlights include US Jobs Report (Jun), Initial Jobless Claims, Speakers including ECB’s Cipollone, BoE’s Mann and Fed’s Daly.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.5%) initially started Thursday’s trade on a softer footing but have climbed off their lows, with all indices in the green, outside of the AEX (-0.3%). Sentiment overnight was on the softer side, following another tech selloff in South Korean stocks (Samsung -9.1%, SK Hynix -14.6%) after Meta plans to sell excess AI compute to build a cloud business, raising questions over excess in AI capacity. However, with Europe lacking the big AI giants, this seems to support the Euro area.

- European sectors point to a positive bias. Optimised Personal Care (+2.1%) tops the sector pile, followed by Food, Beverages & Tobacco (+2.0%) and Health Care (+1.5%). As expected, Technology (-1.9%) is the clear sector laggard and the only sector in the red.

- US equity futures are softer across the board, with the NQ lagging as it gets weighed on by the tech selloff in Asia. Losses have extended into chip names (NVDA -0.8% / AMD -1.3%) and memory (SanDisk -3%, Micron -1.7%).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY trades lower this morning, and trades at the bottom end of a 100.95 to 101.43 range. Pressure which comes after the lack of hawkish remarks from Fed Chair Warsh at Wednesday’s policy panel, and with the move further exacerbated by a hefty move in the JPY this morning.

- On that front, this morning saw large and immediate selling pressure in USD/JPY, where the pair fell from 162.20 to a trough of 161.12. The pair then pared back about a third of that move, stabilising around 161.80, before then taking another beating towards the session low of 160.89 – now trading at levels not seen since 18 June.

- Given the sheer size of the move lower, it does appear to be the case that this is potentially intervention, rather than a rate check. Details of whether they enacted a form of intervention will be released in the monthly release, which is released on the last business day of every month.

- The move comes after Reuters reported that Japan would abandon its habit of warning the markets of intervention. The aim of this is to squeeze speculators and increase the cost of betting against the JPY.

- The potential intervention comes ahead of today’s NFP report; a USD positive report could see some of the “potential intervention” move be pared back. To preview the report in brief, US non-farm payrolls for June are expected to print 110K (prev. 172K), with the unemployment rate seen unchanged at 4.3%.

- Other G10s are stronger against the USD this morning. JPY unsurprisingly outperforms, followed by the GBP and CHF. For the latter, Switzerland reported in-line/cooler-than-expected inflation metrics, which broadly play in favour of keeping rates on hold for the foreseeable future.

FIXED INCOME

- Global fixed income benchmarks trade on a softer footing ahead of the US payrolls data while Germany announces a new set of reforms.

- USTs (-3 ticks) are lower by a handful of ticks, trading just shy of Wednesday’s low of 109-12+. Looking ahead to the June jobs report; NFP expected at 110K (prev. 172K), unemployment to hold steady at 4.3%, average hourly earnings Y/Y expected at 3.5% (prev. 3.4%). In terms of technical levels, downside levels include 109-16 (prior week’s low), 108-27 (key support level) and 108-10 (worst low seen due to Iran conflict). 110-00+ is the key level to the upside.

- Bunds (-38 ticks), unlike USTs, have extended on Wednesday’s trough, currently trading at the lower end of its 126.78-127.06 range. German Chancellor Merz’s coalition unveiled a package of reforms earlier, which included EUR 10bln in annual tax relief for lower-income earners, changes to the pension system and building more affordable housing. The overall aim is to restore competitiveness in Europe’s biggest economy. Although the move lower in German debt has not been excessive, it could be a potential reason for the downside in German debt, as it brings growth back into the economy.

- OATs (-34 ticks) follow their German counterpart. In the upcoming months, French debt will be more in focus as the Presidential elections near. Political uncertainty continues to remain. More recently, the Green Party announced that it would put forward a motion of no confidence over the government’s handling of the recent heat wave. However, this attempt to bring down PM Lecornuʼs government is likely to fail without the support of other opposition parties. The preference for German debt over OATs is clearly shown in the spread, currently trading at 75bps, up from the 58bps seen at the start of June.

- The UK sells GBP 3.25bln 4.625% 2037 Green Gilt: b/c 3.31x (prev. 3.63x), average yield 4.934% (prev. 4.975%), tail 0.2bps (prev. 0.2bps).

- France sells EUR 14.0bln vs exp. EUR 12.5-14bln 1.25% 2036, 3.70% 2036, 4.50% 2041 and 4.10% 2046 OAT.

- Spain sells EUR 5.958bln vs exp. EUR 5-6bln 2.60% 2031, 3.25% 2034 and 3.40% 2036 Bono and EUR 0.695bln vs exp. EUR 0.25-0.75bln 1.15% 2036 I/L Bono.

- Japan sells JPY 1.96tln 10yr JGBs, b/c 3.13x (prev. 3.53x), average yield 2.729% (prev. 2.649%).

COMMODITIES

- Crude benchmarks are on the backfoot, after mediators suggested positive progress was made in the US-Iran indirect conversation. Conversely, gas benchmarks continue to rise with Dutch TTF above EUR 44/MWh as the European forecast points to renewed heat.

- Brent down to a USD 70.38/bbl base, though it has reverted back towards the USD 71.00/bbl but remains in the red. The mentioned base is the lowest print since the end of February, when USD 70.20/bbl printed for the September contract. ,

- For today, US NFP will dominate the macro narrative, with a full Newsquawk preview available. Specifically for energy, we await any further update from the US-Iran talks, and while the mediator-led exchange has now concluded, we could still see updates as the parties agreed to continue talks over the “coming period”.

- Spot gold at a USD 4080/oz peak. In a recovery from the move below USD 4k/oz seen in the last two sessions. Upside today is a function of a weaker USD and relatively steady UST action. As above, impetus will come from the US NFP report.

- Base peers are under pressure, despite the constructive European risk tone and the mentioned USD pressure. As the complex follows the downbeat performance seen in mainland China overnight, and despite Hong Kong seeing strength on its holiday return.

- US President Trump posted that oil prices are plummeting fast and gas prices at the pump are dropping too, but not as fast as they should be, while he announced the Freedom Fuel Network will be lowering gas prices at 25 “FREEDOM FUEL” stations across the Greater Philadelphia Area.

- Venezuela’s oil production was expected to recover to 1.1mln-1.2mln BPD by the end of Q2 2026 as the US expands export authorisations, allowing more companies to transport and market Venezuelan crude

- Saudi Aramco has reportedly increased its exports from the Ras Tanura port and have shifted to spot sales, according to sources.

- Hengli Petrochemical has reportedly cancelled its recent purchases of West African and Middle East oil purchases and also cut refinery operations, according to Reuters sources.

- Dubai spot crude’s discount to swaps widened to more than USD 4.00/bbl, the largest gap since May 2020, according to Refinitiv data.

- UBS cuts its end-2026 gold forecast to USD 5k/oz, due to elevated interest rates.

TRADE/TARIFFS

- China’s MOFCOM said China and the EU agreed to up to two annual ministerial trade talks and have invited EU’s Trade Commissioner Sefcovic to visit in the Fall.

NOTABLE EUROPEAN HEADLINES

- Germany’s ruling coalition unveiled a package of reforms, including EUR 10bln in annual tax relief for lower-income earners, changes to the pension system and building more affordable housing.

- Germany’s VDMA reported May industrial orders -1% Y/Y, driven by weak domestic demand and a general decline across the EZ.

NOTABLE EUROPEAN DATA RECAP

- Swiss Inflation Rate YoY (Jun) Y/Y 0.5% vs. Exp. 0.5% (Prev. 0.6%, Low. 0.3%, High. 0.6%).

- Swiss Inflation Rate MoM (Jun) M/M 0% vs. Exp. 0.1% (Prev. 0.2%).

NOTABLE US HEADLINES

- The Trump administration is reportedly ready to launch “Trump Accounts” next week, but not allow firms to host children’s savings accounts on their own systems, Semafor reported citing sources.

- OpenAI has discussed giving a 5% to the US government as the AI startup seeks to clear political obstacles by securing financial buy-in from the Trump administration, according to FT.

GEOPOLITICS

MIDDLE EAST

- US official said the US is hopeful that Iran will come to the table to negotiate seriously, but is prepared to walk away if they do not, according to a New York Post reporter on X

- US has informed Iran that changing the status quo around the Strait of Hormuz would be a violation of the current understanding and would be unacceptable, according to Al Arabiya sources.

- Iran said it will respond to US interventions in the Strait of Hormuz, Fars reported.

- Qatar’s Foreign Ministry said Qatar and Pakistan mediators concluded separate meetings with US and Iranian negotiators in Doha, while it added that positive progress was made on issues related to the Islamabad MoU. It also stated that the parties agreed to continue discussion over the coming period, with the next meeting to be scheduled at the earliest possible time following the funeral processions of the former Iranian supreme leader.

- Iranian Parliament Speaker Ghalibaf said the claim that inspectors of the IAEA have access to the sites that were bombed is false, while he added that under no circumstances will access be granted to sites that were bombed and damaged.

- Iran’s Deputy Foreign Minister Gharibabadi said Doha talks focused on US violations of the MoU and frozen assets. Gharibabadi separately commented that the Strait of Hormuz is defined under Iran’s command, not CENTCOM, as well as stated that regional security is ensured by the end of interference and the departure of the US from the region, respect for the sovereignty of countries and acceptance of new geopolitical realities, not under the military umbrella of the US.

- Senior source told Al-Hadath that Iran is allowed to purchase American agricultural products using a portion of its frozen funds, but noted that no cash payments are to be dispersed to Iran

- Lebanon’s PM said negotiations with Israel lack a deal framework, and the government seeks a timeline for Israel’s withdrawal and insists on exclusive state control of weapons

- Israeli drones struck Al-Dir in southern Lebanon and Israeli shelling was also reported on the outskirts of Quneitra in Syria, while Israeli forces conducted night raids in Jenin and Ramallah, in the West Bank.

RUSSIA-UKRAINE

- Russian Armed Forces said it hit a Kyiv plant that produces control systems for specific missiles, RIA reported.

- Russian Defence Ministry said it shot down 327 Ukrainian drones overnight.

- Air defence systems were reportedly repelling a Russian drone attack on Kyiv, while it was separately reported that multiple explosions were heard in Ukraine’s capital which was under ballistic missile attack.

- Ukrainian military said it has struck the Kstovo oil refinery in Russia.

OTHER

- China warned two Japanese Coast Guard survey vessels to stop conducting maritime surveys in the disputed East China Sea, prompting Japan to lodge a formal diplomatic protest.

CRYPTO

- Bitcoin extends further above USD 60k and briefly extended above USD 61k, currently trading at the top end of its USD 59.52k-61.12k range.

APAC TRADE

- APAC stocks were mixed but with the major indices predominantly in the red following the tech-related losses on Wall St, while participants also brace for the incoming Non-Farm Payrolls report in a holiday-shortened trading week stateside.

- ASX 200 was rangebound as strength in the top-weighted financial sector was offset by losses in the utilities, tech, energy and consumer sectors, while sentiment was also not helped by weak Australian trade data.

- Nikkei 225 retreated at the open amid tech selling and recent upside in yields, although the index then staged a partial rebound, before selling resumed later in the session.

- KOSPI slumped amid the pressure in memory chip stocks, and triggered a sidecar in early trade.

- Hang Seng and Shanghai Comp traded mixed with the mainland conforming to the broad risk-off mood, while the Hong Kong benchmark bucked the trend amid strength in local tech, biopharmaceutical and auto names on return from the holiday closure.

NOTABLE ASIA-PAC HEADLINES

- Japan’s Government Panellist Nagahama said that the BoJ should raise rates once every six months; this would not hurt domestic investment.

NOTABLE APAC DATA RECAP

- Australian Trade Balance (May) -3.0B vs. Exp. 2.3B (Prev. 1.8B).

- Australian Exports MM (May) -6.9% (Prev. 7.2%).

- Australian Imports MoM (May) M/M 2.6% (Prev. 0.8%).

- South Korean Inflation Rate YoY (Jun) Y/Y 3.2% vs. Exp. 3.2% (Prev. 3.1%).

- South Korean Inflation Rate MoM (Jun) M/M 0.1% vs. Exp. 0.1% (Prev. 0.5%).

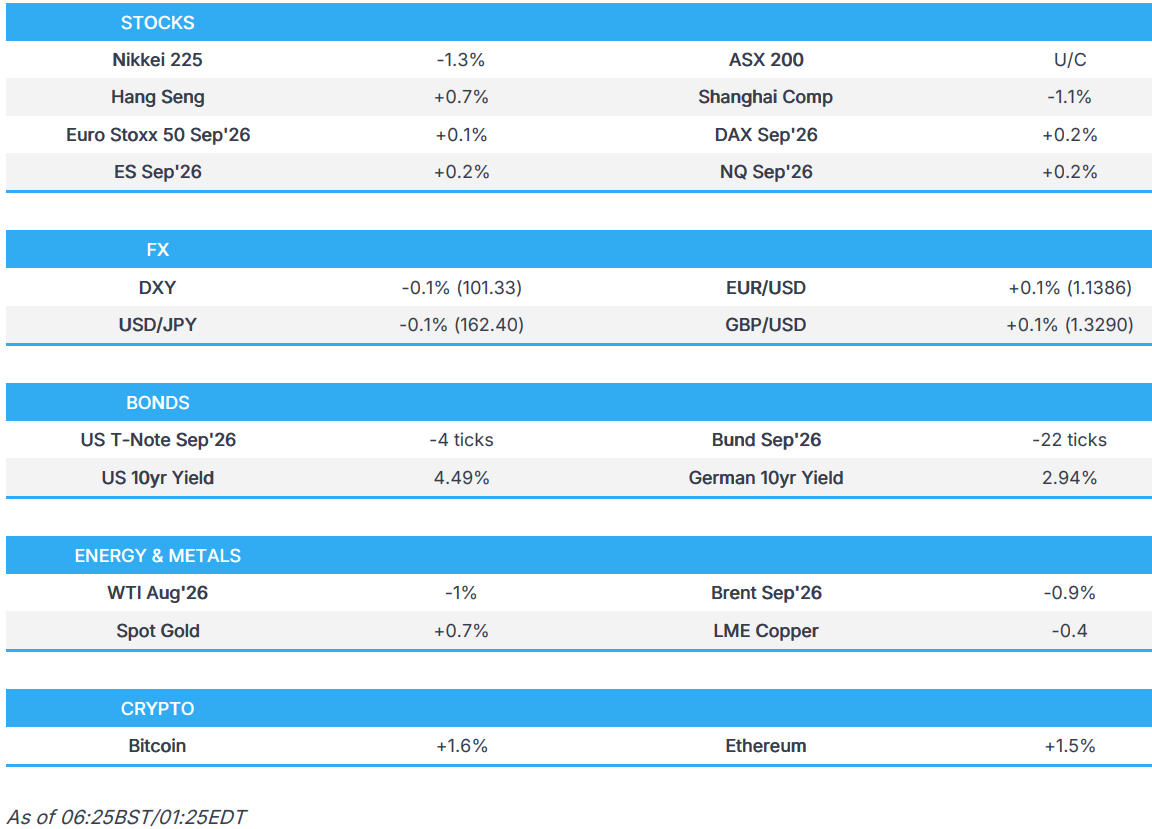

1c) Asian opening report

EU equities futures point to a slightly firmer open; DXY muted ahead of the US jobs report – Newsquawk EU Market Open

Thursday, Jul 02, 2026 – 01:59 AM

- US and Iran talks in Doha focused on management of the Strait of Hormuz and the terms of a 60-day MoU aimed at a comprehensive nuclear deal, Axios reported.

- Qatari and Pakistani mediators suggested that positive progress was made, and stated that both parties agreed to continue discussion over the coming period; Brent -0.9%.

- USTR said the US had not agreed to renew the USMCA in its current form and would continue engaging with Canada and Mexico to address shortcomings in the agreement and bilateral trade deficits.

- APAC stocks were mixed; European equity futures are indicative of a slightly firmer open.

- DXY is a little lower, with price action tentative ahead of today’s NFP report.

- Looking ahead, highlights include Swiss Inflation (Jun), EU Unemployment Rate (May), US Jobs Report (Jun), Initial Jobless Claims, Speakers including ECB’s Elderson & Cipollone, BoE’s Mann, Fed’s Daly, Supply from Spain, France & UK.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US and Iranian negotiators resumed talks in Doha focused on management of the Strait of Hormuz and the terms of a 60-day MoU aimed at a comprehensive nuclear deal, according to Axios’s Barak Ravid. While a temporary one-week de-escalation agreement remained in place, US officials warned the administration remained prepared to respond militarily to any further Iranian aggression, noting that President Trump had previously requested briefings on military options.

- US official said the US is hopeful that Iran will come to the table to negotiate seriously, but is prepared to walk away if they do not, according to a New York Post reporter on X

- Qatar’s Foreign Ministry said Qatar and Pakistan mediators concluded separate meetings with US and Iranian negotiators in Doha, while it added that positive progress was made on issues related to the Islamabad MoU. It also stated that the parties agreed to continue discussion over the coming period, with the next meeting to be scheduled at the earliest possible time following the funeral processions of the former Iranian supreme leader.

- Iranian Parliament Speaker Ghalibaf said the claim that inspectors of the IAEA have access to the sites that were bombed is false, while he added that under no circumstances will access be granted to sites that were bombed and damaged.