JULY 1//GOLD CLOSED UP $42.95 TO $4068.40/SILVER CLOSED UP $0.48 TO $60.00//PLATINUM CLOSED UP $30.00 TO $1591.00//PALLADIUM CLOSED UP $92.00 TO $1282.50//GOLD COMMENTARY TONIGHT COURTESY OF ALASDAIR MACLEOD//EUROPEAN NEWS FROM THE UK AND HOLLAND PLUS A BIG UN STORY//ISRAEL, USA VS IRAN UPDATES//ISRAEL TBN/HEZBOLLAH UPDATES/RUSSIA VS UKRAINE/ VACCINE INJURY REPORT//OIL REPORTS//USA DATA RELEASES//USA ECONOMIC REPORTS/ KING NEWS/ GREG HUNTER INTERVIEWS WARREN WESTON..finalized/complete

092 C DEUTSCHE BANK 250 099 H DEUTSCHE BANK AG 1029 118 C MACQUARIE FUTURES US 31 167 C MAREX 1 363 H WELLS FARGO SECURITI 324 555 C BNP PARIBAS SEC CORP 53 661 C JP MORGAN SECURITIES 1875 128 686 C STONEX FINANCIAL INC 17 16 709 C BARCLAYS 59 732 C RBC CAP MARKETS 516 737 C ADVANTAGE FUTURES 20 16 905 C ADM 9

TOTAL: 2,172 2,172 MONTH TO DATE: 7,880

JPMORGAN STOPPED: 128/2172

GOLD: NUMBER OF NOTICES FILED FOR JULY/2026: 2172 CONTRACTs NOTICES FOR 217,200 OZ or 6.755 TONNES

total notices so far: 7880 contracts FOR 788,000 OZ OR 24.510 TONNES

JUNE 30

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 301 NOTICE(S) FILED FOR 1.505 MILLION OZ /

total number of notices filed so far this month : 5076 CONTRACTS (NOTICES) for 25.380 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $42.95 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/// NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1005.077 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.48 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: SMALL CHANGES IN SILV INVENTORY: A DEPOSIT OF 0.233 MILLION OZ OZ OUT OF THE SLV /// : INVENTORY RESTS AT THE SLV AT 479.360 MILLION OZ//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 480.574 MILLION OZ

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA MEGA HUGE SIZED 3531 CONTRACTS TO AN OI OF 104,423 STILL A LOT HIGHER FROM ITS NEW RECORD LOW OF 95,999 SET MAY 1/2026. THE RECORD HIGH OI FOR SILVER IS 244,710, SET FEB 25/2020, AND THIS HUGE LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE GAIN OF $1.35 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. ON THE FIRST OF MAY, WE REACHED OUR RECORD LOW OI OF 95,999 SURPASSING EVERY DAY NEW OI LOWS SET DURING THE LAST WEEK OF APRIL 2026.

NOW ON A NET BASIS OUR SPECULATORS HAVE REVERTED BACK TO GOING SHORT. THE FRBNY ON A NET BASIS IS PROVIDING THE NECESSARY PAPER TO OUR LONG BANKERS AND THEN TENDER FOR PHYSICAL AT 4 PM EACH NIGHT. BECAUSE OF THE HUGE SHORTFALL IN PHYSICAL SILVER IN LONDON THERE IS A LOTTERY TO SEE WHO GETS ANY OF THE PHYSICAL SILVER AVAILABLE THAT WHICH THEY ARE OBLIGATED TO DELIVER. THEY WAIT PATIENTLY FOR THEIR PHYSICAL METAL AND IF NOBODY GETS ANY THEY THEN COME BACK THE NEXT DAY AND SO ON. THIS IS IN LONDON, THE HOME OF PHYSICAL SILVER!! THE FACT THAT WE ARE WITNESSING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON HIGHLIGHTS THE FACT THAT THE COMEX IS OUT OF SILVER AS WELL.

WE ARE NOW MOVING TO A MUCH LOWER BASE IN SILVER PRICING BREAKING MAJOR SUPPORT LEVEL OF $70.00. SHORTLY WE WILL REVERT BACK TO NUMBERS GREATER THAN 70 DOLLARS PER OZ.

WE HAVE A MEGA MEGA HUGE LOSS OF 2841 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A STRONG SIZED SIZED 690 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE , WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO TUESDAY TRADING// WE HAD A HUMONGOUS SIZED 1182 CONTRACT T.A.S. ISSUANCE!! / THEY DESPERATELY AGAIN TODAY TRYING TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $100.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON TUESDAY WITH SILVER’S GAIN IN PRICE

THE PRICE STILL FINISHED BELOW THE MAGIC NUMBER OF $70.00 SILVER SPOT PRICE BUT STILL BELOW THE $100.00 MARK CLOSING AT $59.52 UP $1.35. WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS A HUMONGOUS SIZED 1182 T.A.S. CONTRACTS !!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING ABOVE THE 100.00 DOLLAR MARK!! AND NOW THE HUGE SUPPORT LEVEL OF 70 DOLLARS HAS BEEN BROKEN// //.MAMMOTH SIZE T.A.S ISSUANCES ARE BECOMING THE NORM AT THE COMEX NOW!!

THERE IS NO NEXT LINE IN THE SAND ONCE THE 100.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A STRONG SIZED 690 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUMONGOUS SIZED 1182 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE.

IN ESSENCE WE HAD A MEGA MEGA HUGE SIZED LOSS OF 2841 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR GAIN IN PRICE OF $1.08. WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION WILL BE REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE STICKY SPECULATOR LONGS STILL REMAIN STOIC

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE.

THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, THROUGHOUT MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT/WEDNESDAY MORNING: A HUMONGOUS SIZED 1182 CONTRACTS. DESPITE MANY COMPLAINTS THAT THESE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS).

THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS AS ONE UNIT, BUT SELL THE SHORT SIDE FIRST AND THEN LIQUIDATE THE LONG SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF XX CONTRACTS OR XXX OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 10,000 OZ//NEW STANDING ADVANCES TO 12.970 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 20 CONTRACTS FOR 100,000 OZ//NEW STANDING ADVANCES TO 13.070 MILLION OZ. (IN EXCHANGE FOR RISK THE BUYER ASSUMES THE RISK AND ONLY A CENTRAL BANK WOULD TAKE THAT RISK. THE BUYER IS PROBABLY THE CENTRAL BANK OF INDIA.)

JULY INITIAL STANDING: 37.110 MILLION OZ FOLLOWED BY A HUGE 295 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE OR 1.475 MILLION OZ WHERE DELIVERY WILL OCCUR IN LONDON. THUS STANDING REDUCES TO 35.540 MILLION OZ//

SUMMARY OF OUR JUNE 2026 COMEX CONTRACT MONTH:

WE HAD:

/ HUGE COMEX LOSS+// STRONG SIZED EFP ISSUANCE CONTRACTS AT 690 CONTRACTS (/ VI) A HUMONGOUS NUMBER OF T.A.S. CONTRACT ISSUANCE 1182 CONTRACTS

xx I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 83 SILVER CONTRACT//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY.. ACCUMULATION

TOTAL CONTRACTS for 1 DAY(S), total 690 contracts: OR 3.450 MILLION OZ (690 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 3.450 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE. 64.065 MILLION OZ//FINAL AND FAIR SIZED THIS MONTH.

JULY: 3.450 MILLION OZ

RESULT: WE HAD A HUGE DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3531 CONTRACTS DESPITE OUR HUGE GAIN IN PRICE OF $1.35 IN SILVER PRICING AT THE COMEX// TUESDAY,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED CONTRACT EFP ISSUANCE OF 690 CONTRACTS ISSUED FOR SEPT, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS).

INITIAL STANDING: 37.110 MILLION OZ FOLLOWED BY TODAY’S HUGE 1.475 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON: STANDING THUS REDUCES TO 35.540 MILLION OZ//

LAST 14 MONTHS OF SILVER DELIVERIES

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 10,000 OZ//NEW STANDING ADVANCES TO 12.960 MILLION OZ TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 20 CONTRACTS FOR 100,000 OZ//NEW STANDING ADVANCES TO 13.070 MILLION OZ

JULY : INITIAL STANDING: 37.110 MILLION OZ FOLLOWED BY TODAY’S HUGE 1.475 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON//STANDING THUS REDUCES TO 35.540 MILLION OZ//

THE NEW TAS ISSUANCE FOR TODAY (1182) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING LIKE TODAY.

WE HAD 301 NOTICE(S) FILED TODAY FOR 1.505 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY BANKERS

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A TINY SIZED 226 OI CONTRACTS UP TO 365,048 OI AND THIS OI STILL SURPASSES BY A CONSIDERABLE MARGIN THE ALL TIME LOW AT 326,052 SET JUNE3/2026 AND THIS OI IS MUCH FURTHER FROM THE RECORD HIGH (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE HAVE NOW ADVANCED PAST THE PREVIOUS ALL TIME LOWS OF 357,136 SET APRIL 2/.2026AND 354,581 SET AT THE END OF APRIL 2026. WE ARE STILL QUITE A WAY FROM OUR TWO DECADES OLD: 390,000 CONTRACTS LOW SET IN THE YEAR OF 2001 WITH TRADING FOR GOLD AT $260.00. THUS DURING EARLY APRIL WE HAD AN ALL TIME LOW OI IN COMEX (354,531) BUT WITH AN EXTREMELY HIGH PRICE OF GOLD. IN MAY: RECORD LOW OI OF 326,052 WITH A GOLD PRICE OF $4,460 THE SHORT RATS ARE ABANDONING THE COMEX SHIP, NOBODY WANT TO PLAY IN THIS CROOKED CASINO!! (AND THIS CORRELATES WITH SILVER’S LOW OI OF 104,154 CONTRACTS WITH A MUCH HIGHER SILVER PRICE BASE//$58.00)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED XXX CONTRACTS //.

WE HAD A SMALL LOSS IN COMEX OI (226 CONTRACTS) . THIS LOSS IN OI OCCURRED DESPITE OUR GAIN IN PRICE OF $2.85 //,TUESDAY

DAY///.

LAST 14 MONTHS OF GOLD DELIVERIES: (MAY 2025 THROUGH TO /MAY 2026)

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER OF 0.0186 TONNES/NEW STANDING REDUCES TO 127.03 TONNES

JULY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 23.306 TONNES TO WHICH WE ADD OUR FIRST QUEUE JUMP OF 1.2846 TONNES//NEW STANDING ADVANCES TO 24.5909 TONNES

E.F.P. ISSUANCE/FOR OPENING JUNE. GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 730 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 365,048 SURPASSING THE PREVIOUS ALL TIME LOW OF 326,052 SET JUNE 3 AND RISING FROM OUR PREVIOUS RECORD LOW//MAY 28.2026 WE HAVE THUS RECORD LOW COMEX OI WITH A HIGH PRICE OF GOLD

SILVER ALSO HAS AN ULTRA SMALL SIZED AND EXTREMELY LOW COMEX OI OF 104,427 CONTRACTS// STILL ABOVE FROM PREVIOUS ALL TIME LOWS SET DURING THE MONTH OF APRIL AND MAY FIRST.

IN ESSENCE WE HAVE A SMALL GAIN IN TOTAL CONTRACTS IN COMEX GOLD ON THE TWO EXCHANGES OF 504 CONTRACTS WITH 226 CONTRACTS DECREASED AT THE COMEX// AND A SMALL SIZED 730 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON.

THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 504 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A LOT STRONGER SIZED AND CRIMINAL 1740 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON LIKE TODAY.

GOLD PRICE ON TUESDAY ROSE BY $2.85

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT (730 ) ACCOMPANYING THE SMALL LOSS IN COMEX OI OF 220 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES 504 CONTRACTS!! DESPITE THE GAIN IN PRICE.

WE HAVE 1) NOW REVERTED TO OUR FORMAT OF BANKER (FRBNY) GOING ON THE LONG SIDE AND HUGE NUMBERS OF NEWBIE SPECULATORS GOING TO THE SHORT SIDE LED BY THE NOSE BY OUR HIGH FREQUENCY TRADERS.. IT WAS OUR SHORT SPECULATORS THAT WILL BE BRUTALIZED WHEN OUR CENTRAL BANKS TENDER FOR PHYSICAL GOLD WITH THEIR NEWLY BOUGHT GOLD FROM THE SPECS THIS MORNING. THE SPECS WILL BE SCRAMBLING LOOKING FOR PHYSICAL GOLD TO DELIVER TO OUR LONG CENTRAL BANKS.

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER JUMP OF 0.0186 TONNES//NEW STANDING REDUCES TO 127.03 TONNES//FINAL

JULY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 23.306 TONNES OF GOLD TO WHICH WE ADD OUR FIRST QUEUE JUMP OF 1.2846 TONNES//NEW STANDING FOR GOLD ADVANCES TO 24.5909 TONNES.

3) HUGE T.A.S. LIQUIDATION IN THE COMEX SESSION AND SOME GOVT LIQUIDATION // WITH A STRONG GAIN OF EQUITY SHARES/JUNE30 HAVING 1)A $2.80 COMEX PRICE GAIN AND WE HAD 2) SPEC PILING HUGELY ON THE SHORT SIDE// +3. EASTERN CENTRAL BANKERS ALSO PILING INTO THE LONG SIDE. WE HAD A SMALL GAIN OF 504 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A STRONG AMOUNT OF GOLD WILL STAND FOR DELIVERY IN JULY. (24.5909 TONNES). THE SHORT SPECS CONTINUED TO PILE INTO THE SHORT SIDE.//, CENTRAL BANKERS THE LONG SIDE AND THEY THEN TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4)A SMALL SIZED COMEX OI LOSS 5) V) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD(730) AND 6. A STRONG T.A.S. ISSUANCE (1740) FOR RAID PURPOSES.!!!

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 730 CONTRACTS OR 73000 OZ OR 2.2395 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 730 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN1 TRADING DAY(S) IN TONNES: 2.2395 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2025, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 2.2395 TONNES DIVIDED BY 3550 x 100% TONNES = 0.06197% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2023 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2024: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES

2025: AND NOW 2026

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 142.053 TONNES

JULY: 2.2395 TONNES

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA MEGA HUGE 3531 CONTRACTS TO AN OI OF 104,427

EFP ISSUANCE 690 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 690 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3,531 CONTRACTS AND ADD TO THE 690 E.FP. ISSUED

WE OBTAIN A HUGE LOSS OF 2841 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN OF $1.35

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 14.205 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $1.35

2.ASIAN AFFAIRS JULY 1 /2025

SHANGHAI CLOSED UP 18.05 PTS OR 0.44%

HANG SENG CLOSED HOLIDAY

Nikkei CLOSED UP 423.68 PTS OR 0.60%

//Australia’s all ordinaries CLOSED DOWN 0.86%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7939

/ OFFSHORE CLOSED DOWN AT 6.7998 Oil DOWN TO 69.40 dollars per barrel for WTI and BRENT DOWN TO 72.87 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7939) OFFSHORE YUAN TRADING DOWN TO 6.7998 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL 226 CONTRACTS TO 365,048 STILL WELL ABOVE ITS NEW LOW OF 326,052 OI SET JUNE 3, CLOSE TO THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND CLOSE TO THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,052 //JUNE 3 2026 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD HUGE T.A.S. LIQUIDATION DURING TUESDAY’S MASSIVE COMEX TRADING// ATTEMPTED RAID JUNE 30 IT SEEMS THAT MANY OF THE SPECULATORS THAT HAVE NOW CONTINUED AGAIN TO GO MASSIVELY ON THE SHORT SIDE WITH BANKERS ON THE LONG SIDE WILL BE OBLITERATED TODAY WHEN THE LONGS TENDERED FOR DELIVERY:

CENTRAL BANKS TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS JULY CONTRACT MONTH!!

THE SMALL SIZED GAIN ON OUR TWO EXCHANGES (504 CONTRACTS) OCCURRED WITH OUR GAIN IN PRICE IN GOLD (UP $2.85)

WE THUS HAD A SMALL SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 504 CONTRACTS (OR 1.567 TONNES) WITH OUR SMALL GAIN IN PRICE, AS WE WERE INFORMED OF A SMALL CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 730 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIDAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH JUNE

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

JUNE: 0 IN GOLD. THUS FOR THE ENTIRE MONTH IN GOLD ZERO NOTICES WERE FILED.

JULY 0

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO JUNE:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 146+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO

JULY 0

DETAILS ON OUR NEW JUNE COMEX CONTRACT MONTH//

IN TOTAL WE HAD A SMALL GAIN ON OUR TWO EXCHANGES OF 504 CONTRACTS WITH OUR GAIN IN PRICE($2.85). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A MUCH STRONGER SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1740 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

JUNE: ZERO FOR THE MONTH

JULY: ZERO SO FAR

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 146+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO. WE WILL KNOW IN JUNE WHETHER THEY COVERED ANY OF THEIR SHORTFALL.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE SUBTRACT AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON OF 0.0186 TONNES//NEW STANDING REDUCES TO 127.03 TONNES// TOTAL QUEUE JUMPING FOR THE MONTH FINALIZES AT 62.4217 TONNES OR AVERAGING 3.285 TONNES PER DAY IN JUNE.

JULY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 749,300 OZ OR 23.306 TONNES OF GOLD TO WHICH WE ADD OUR FIRST QUEUE JUMP OF 1.2646 TONNES//NEW STANDING ADVANCES TO 24.5906 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JUNE,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $58.30)

WE HAD HUGE T.A.S. SPREADER LIQUIDATION TUESDAY // COMEX SESSION// DESPITE OUR SMALL GAIN IN PRICE , OUR SPECULATORS STILL WENT MASSIVELY TO THE SHORT SIDE LED BY THE NOSE BY OUR HIGH FREQUENCY MOMENTUM PLAYERS WITH CENTRAL BANKERS TAKING THE LONG SIDE. THE SPECS WERE ANNIHILATED ON THURSDAY AND FRIDAY.

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

TUESDAY NIGHT//WEDNESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING //WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $2.85

WE HAD XXX CONTRACTS REMOVED AT THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES: 504 CONTRACTS OR 50,400 OZ (1.567 TONNES)

Total monthly oz gold served (contracts) so far this month

7880 notices 788,000 OZ

24.510 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 1

0 ENTRY

DEPOSITS/CUSTOMER

ENTRIES: 0

xxxxxxxxxxxxxxxxxx

comex withdrawal

0 ENTRIES

adjustments: 2// DEALER TO CUSTOMER

a) LOOMIS 1446.795 OZ

b) Malca: 990.196 oz

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JULY OI STANDS AT 2198 CONTRACTS HAVING A LOSS OF 5295 CONTRACTS. WE HAD 5708 NOTICES FILED ON TUESDAY SO WE GAINED 413 CONTRACTS OR 41,300 OZ. WE THUS HAD A STRONG QUEUE JUMP OF 1.2846 TONNES.

AUGUST GAINED 1467 CONTRACTS TO AN OI OF 276,056

SEPTEMBER GAINED 257 CONTRACTS UP TO AN OI OF 1253.

.

We had 2172 contracts filed for today representing 217,200oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 1875 notices issued from their client or customer account. The total of all issuance by all participants equate to 2172 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 128 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY. /2026. contract month, we take the total number of notices filed so far for the month (7880) to which we add the difference between the open interest for the front month of JULY (2198 CONTRACTS) minus the number of notices served upon today 2172 x 100 oz per contract) equals 790,600 OZ OR (24.5909 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JULY. /2026. contract month, we take the total number of notices filed so far for the month (7880) to which we add the difference between the open interest for the front month of JULY( XXX CONTRACTS) minus the number of notices served upon today 2172 x 100 oz per contract) equals 790,600 OZ OR (24.5906 Tonnes of gold)

new total of gold standing in JULY becomes 24.5906 TONNES//

TOTAL COMEX GOLD STANDING FOR JULY 24.5906TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS NON ACTIVE DELIVERY MONTH OF JULY.

confirmed volume TUESDAY confirmed 140,727/ poor// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,864,701.391 oz 58.000 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,864,701.391 tonnes oz 58.000 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 27,559.820.207 oz

TOTAL REGISTERED GOLD 14,826,009.194 tonnes (461.15tonnes)

TOTAL OF ALL ELIGIBLE GOLD 12,731,374.072 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 12,961,308oz ((REG GOLD- PLEDGED GOLD)=

403.151 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JULY DELIVERY MONTH

JULY 1

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

0 entries

Deposits to the Dealer Inventory

0 entries

Deposits to the Customer Inventory

0 entries

No of oz served today (contracts)

301 CONTRACT(S) ( 1.505MILLION OZ)

No of oz to be served (notices)

2032 Contracts (10.160 MILLION oz)

Total monthly oz silver served (contracts)

5076 contracts 25.380 MILLION oz

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRY:0

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

0 entries

adjustments 1; ALL CUSTOMER ACCT TO DEALER ACCT

a) Asahi: 406,348.770 oz

c) Delaware: 120,507.438 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 93.010 MILLION OZ//.TOTAL REG + ELIGIBLE. 322.536 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JULY /2026 OI: 2333 OPEN INTEREST CONTRACTS FOR A LOSS OF 5070 CONTRACTS. WE HAD 4775 CONTRACTS SERVED ON TUESDAY SO WE LOST 295 CONTRACTS OR A HUGE 1.475 MILLION OZ UNDERWENT AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE THEY WILL TAKE DELIVERY OVER ON THAT SIDE OF THE POND.

AUGUST SAW A LOSS OF 64 CONTRACTS UP TO 1887…

SEPTEMBER SAW A GAIN OF 1399 CONTRACTS UP TO AN OI OF 81,518 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 301 or 1.505 MILLION oz

CONFIRMED volume TUESDAY; 52,756// poor//

XXX

AND NOW JUNE. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 5076 X5,000 oz = 25.380 MILLION oz

to which we add the difference between the open interest for the front month of JULY(2333) AND the number of notices served upon today (301 )x (5000 oz)

Thus the standings for silver for the JULY 2026 contract month: (5076 )Notices served so far) x 5000 oz + OI for the front month of JULY ( 2333) minus number of notices served upon today (301)x 5000 oz equals silver standing for the JULY..contract month equating to 35.540 MILLION OZ. (still a very strong delivery month)

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 93.010 million oz of registered silver

JPMorgan as a percentage of total silver: 137.898/322.536 million: 42.75%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JULY 1 /2026/WITH GOLD UP $42.95 /NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JUNE 30 /2026/WITH GOLD UP $2.85 /NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JUNE 29 /2026/WITH GOLD DOWN $58.30 /HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 8.223 TONNES OF GOLD FROM THE GLD // ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JUNE 26 /2026/WITH GOLD UP $49.10 /HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 4.287 TONNES OF GOLD FROM THE GLD // ./ //:/INVENTORY RESTS AT 1013.350 TONNES

JUNE 25 /2026/WITH GOLD UP $42.70 /NO CHANGES IN GOLD AT THE GLD: // ./ //:/INVENTORY RESTS AT 1017.637 TONNES

JUNE 24 /2026/WITH GOLD DOWN $141.55 /HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.563 TONNES OF GOLD OUT OF THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1017.637 TONNES

JUNE 19 /2026/WITH GOLD UP $36.85 /HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 7.421 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1020.49 TONNES

JUNE 18 /2026/WITH GOLD DOWN $135.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.856 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1013.069 TONNES

JUNE 17 /2026/WITH GOLD UP $20.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.427 TONNES OF GOLD FROM THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1012.213 TONNES

JUNE 16 /2026/WITH GOLD UP $4.45 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 15 /2026/WITH GOLD UP $111.10 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 12 /2026/WITH GOLD UP $123.30 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 11 /2026/WITH GOLD DOWN $15.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.855 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 10 /2026/WITH GOLD DOWN $153.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.426 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1016.495 TONNES

JUNE 9 /2026/WITH GOLD DOWN $75.60 TODAY/NO CHANGES IN GOLD AT THE GLD:// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 8 /2026/WITH GOLD DOWN $3.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 6.936 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 5 /2026/WITH GOLD DOWN $134;85 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 4 /2026/WITH GOLD UP $39.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.143 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1026.857 TONNES

JUNE 3 /2026/WITH GOLD DOWN $51.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.856 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.000 TONNES

JUNE 2 /2026/WITH GOLD UP $7.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.712 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1028.856 TONNES

JUNE 1 /2026/WITH GOLD DOWN $79.30 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 29 /2026/WITH GOLD UP $59.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD ./ //:/INVENTORY RESTS AT 1032.568 TONNES

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

GLD INVENTORY: 1005.077 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JULY 1 WITH SILVER UP $0.48: : SMAL CHANGES IN INVENTORY AT THE SLV A DEPOSIT OF 0.233 MILLION OZ OUT OF THE SLV/./ // :INVENTORY RESTS AT 479.360 MILLION OZ

JUNE 30 WITH SILVER UP $1.35: : HUGE CHANGES IN INVENTORY AT THE SLV A WITHDRAWAL OF 1.447 MILLION OZ OUT OF THE SLV/./ // :INVENTORY RESTS AT 479.127 MILLION OZ

JUNE 29 WITH SILVER DOWN $1.08: : HUGE CHANGES IN INVENTORY AT THJE SLV A WITHDRAWAL OF 1.402 MILLION OZ OUT OF THE SLV/./ // :INVENTORY RESTS AT 480.574 MILLION OZ

JUNE 26 WITH SILVER UP $0.86: : HUGE CHANGES IN INVENTORY AT THJE SLV A DEPOSIT OF 2.352 MILLION OZ INTO THE SLV/./ // :INVENTORY RESTS AT 481.976 MILLION OZ

JUNE 25 WITH SILVER UP $0.69: : SMALL CHANGES IN INVENTORY AT THJE SLV A WITHDRAWAL OF 769,000 OUT OF THE SLV/./ // :INVENTORY RESTS AT 479.624 MILLION OZ

JUNE 24 WITH SILVER DOWN $4.18: : SMALL CHANGES IN INVENTORY AT THJE SLV A DEPOSIT OF 93,000 MILLION OZ INTO THE SLV/./ // :INVENTORY RESTS AT 480.393 MILLION OZ

JUNE 19 WITH SILVER UP $1.11: : NO CHANGES IN INVENTORY AT THJE SLV/./ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 18 WITH SILVER DOWN $4.80: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: HUGE CHANGES IN INVENTORY A WITHDRAWAL OF 1.086 MILLION OZ FROM THE SLV././ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 17 WITH SILVER UP $0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: NO CHANGE IN INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 16 WITH SILVER DOWN $0.13: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.362 MILLION OZ INTO THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 15 WITH SILVER UP $3.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.357 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 481.026 MILLION OZ

JUNE 12 WITH SILVER UP $3.34: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.769 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 482.383 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.12: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.226 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.152 MILLION OZ

JUNE 10 WITH SILVER DOWN $0.50: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.909 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.378 MILLION OZ

JUNE 9 WITH SILVER DOWN $3.35: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.407 MILLION OZ INTO INTO THE SLV /./ // :INVENTORY RESTS AT 484.287 MILLION OZ

JUNE 8 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 543,000 OZ FROM THE SLV /./ // :INVENTORY RESTS AT 482.880 MILLION OZ

JUNE 5 WITH SILVER DOWN $4.86: NO CHANGES IN SILVER INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 4 WITH SILVER UP $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.432 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 3 WITH SILVER DOWN $2.55: NO CHANGES IN SILVER INVENTORY AT THE SLV >> /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

The UK’s next prime minister, Andy Burnham, was schooled in old fashioned socialism, hobnobbing with London’s Labour elite since leaving university, first becoming an MP in 2001. This King of the North stuff is just an act.

While politics is always about image, it is particularly so with socialists. They promote themselves as representing the downtrodden masses at the expense of evil capitalists. But it always turns out to be impossible to improve on capitalism, for one simple fact which was exposed in the socialist calculation debate triggered by Ludwig von Mises’s 1920 article pointing out the impossibility of economic calculation in the socialist state.

MacleodFinance Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Mises demonstrated that Marxist dogma about the state owning and distributing the means of production was nonsense, because the economic calculations to make the division of labour work for society’s benefit could only be made by businesses in free markets. The less the intervention from the state, the more effective the economic delivery and progress both become. Socialism travels in the opposite direction.

You only had to compare the free market success of Hong Kong with communist mainland China under Chairman Mao. John Cowperthwaite was instrumental in Hong Kong’s recovery from the economic and monetary ruins left by the Japanese army and is a story well told. He oversaw this recovery by refusing to intervene, kept the state small, and kept taxes low.

Contrast that with China’s misery under Mao which led to an estimated 40 to 70 million deaths attributable to his communist policies. Same ethnic people, just different politics.

The truth about communism, which is simply a severe form of socialism was fully revealed when the Berlin Wall fell, and the corruption in Eastern European states was revealed. Honecker, Jaruzelski, Husak, Kadar, Zhivkov, and Ceausescu — all Warsaw Pact leaders living high on the hog while their populations were suppressed and starved. It is a characteristic of socialism that while it fails, those deemed “more equal than others” become increasingly divorced from economic reality and personally corrupt. Hark! Did someone say Brussels?

Over fifty years ago, there was another King of the North called T. Dan Smith aka Mr Newcastle, leader of that city’s council, who along with bent architect John Poulson and another council leader Andrew Cunningham in nearby County Durham were jailed for corruption. Mini-Honeckers and Ceausescus all of them.

I recall discussing this with an acquaintance back in the seventies. He was in the business of developing car parks in city centres, negotiating with planning departments and Labour councillors all the time. He was clear that the further left a councillor, the easier he was to bribe. His cynical observation appears to be confirmed by the facts.

Imagine you have a social conscious and become a socialist politician. You rapidly find that everything you do suffers from unintended consequences, but lobbyists come to you simply because you have power. Dinners, visits to the races, fact-finding missions and conferences in luxury resorts all paid for, and finally some deals on the side are quietly offered. The chances are your head is turned. The Brussels elite which doesn’t even have to face a plebiscite is a supreme example of a socialist political class which in terms of luxury and indulgence gives the Warsaw Pact leaders a close run for their money.

Burnham and his appointees may or may not succumb to the most obvious forms of bribery, but when things don’t pan out too well, almost certainly he will follow Starmer for the photo opportunities, the dinners, and all the other trappings of NATO, EU, and G7 meetings whose attendees meet to simply reassure themselves of their importance.

Importance abroad offsets impotence at home. Nothing changes, because socialism doesn’t deliver. As Mises correctly observed, there’s no such thing as economic calculation in a socialist state. Formally the most powerful nation in the world, Britain under socialism is now becoming a third world country. It is extraordinary that no one seems to think that the problem is too much government and regulation. Instead, the solution is to double down: more government, more regulation, more taxes, more Burnhams. Any complainer is an enemy of the state and his right to a contrary opinion is vigorously denied.

3. CHRIS POWELL AND HIS GATA DISPATCHES

GREAT FOR GOLD

For first time, more central banks plan to shrink dollar holdings, survey finds

Submitted by admin on Tue, 2026-06-30 13:37 Section: Daily Dispatches

By Libby George Reuters Tuesday, June 30, 2026

LONDON — More of the world’s central banks plan to cut dollar allocations than increase them in the coming decade as political risks associated with the U.S. currency rise, an OMFIF survey of public investors released on Tuesday showed.

It is the first time the survey, carried out by the Official Monetary and Financial Institutions Forum, has found such a shift away from the dollar.

The findings dovetail with a global debate about the U.S. dollar’s role as the primary reserve currency that has been stoked by U.S. policy uncertainty and heightened geopolitical risks.

The London-based thinktank set up in 2010 also found an eagerness among the 90 central banks, public pension funds and sovereign funds surveyed to significantly increase the use of AI from current levels. …

Submitted by admin on Mon, 2026-06-29 17:39 Section: Daily Dispatches

By Brien Lundin Gold Newsletter / Golden Opportunities Monday, June 29, 2026

While the headlines continue to validate my skepticism regarding any peace deal with Iran, metals bulls might be justified in feeling singled out for punishment today.

Because while the rest of the “risk assets” are up, gold and silver are taking it on their respective chins, with both metals down about 1.5% as I write.

The good news, such that it is, is that gold has remained above the key $4,000 line, after rising back above it late last week. …

All this points to the simple fact that Western investors have all but given up on gold. And because Western markets continue to set the price, well … you’ve seen the charts.

Now here’s where it gets interesting.

While the West is setting the gold price, China has been taking it. …

END

The U.S. Mint gold coin that broke the circle

Submitted by admin on Sun, 2026-06-28 12:20 Section: Daily Dispatches

From Coin Week, Silver Springs, Florida Sunday, June 28, 2026

The 1915-S Panama-Pacific $50 Octagonal gold coin did something no other legal-tender United States coin had done.

It broke the circle.

For more than a century this massive gold commemorative stood alone as the only non-round legal-tender coin ever issued by the United States Mint. That distinction now feels more important than ever.

On July 16, 2026, the Mint will release its Freedom Ringing–Liberty Bell gold coins and Silver Medal for the Semiquincentennial. Those new Liberty Bell-shaped gold coins will finally add a modern chapter to a story that began in San Francisco in 1915.

However, the original remains the original.

The 1915-S Panama-Pacific $50 Octagonal still carries the drama of the Gold Rush, the triumph of the Panama Canal, and the rebirth of a city that refused to stay broken. …

Maguire and Hemke say gold ‘correction’ is over and expect revaluation

Submitted by admin on Mon, 2026-06-22 11:56 Section: Daily Dispatches

11:56a ET Monday, June 22, 2025

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire and the TF Metals Report’s Craig Hemke, in conversation on this week’s edition of Kinesis Money’s “Live from the Vault” program, agree that gold’s “correction” is over and speculate how a U.S. Treasury revaluation of the monetary metal to a much higher price may come about soon.

The program is 57 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

5. COMMODITY REPORT//GOLD

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 18.05 PTS OR 0.44%

HANG SENG CLOSED HOLIDAY

Nikkei CLOSED UP 423.68 PTS OR 0.60%

//Australia’s all ordinaries CLOSED DOWN 0.86%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7939

/ OFFSHORE CLOSED DOWN AT 6.7998 Oil DOWN TO 69.40 dollars per barrel for WTI and BRENT DOWN TO 72.87 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7939) OFFSHORE YUAN TRADING DOWN TO 6.7998 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.7939

OFFSHORE YUAN: DOWN TO 6.7998

1.HANG SANG CLOSED HOLIDAY

2. Nikkei closed UP 423.68 PTS OR 0.60%

WEST TEXAS INTERMEDIATE OIL DOWN TO 69.40

BRENT; 72.82

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 101.10/// EURO FALLS TO 1.1399 DOWN 13 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +2.704 UP 1 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA CROSS NOW AT 162.67… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.964 UP 0 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN( 6.7939) AND OFFSHORE: DOWN AT 6.7998

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EU German 10yr bund YIELD UP TO +2.9355/ Italian 10 Yr bond yield UP to 3.634/ SPAIN 10 YR BOND YIELD UP TO 3.378%

3i Greek 10 year bond yield UP TO 3.5171%

3j Gold at $3976.95 //Silver at: 57.66 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 90/ 100 roubles/77.72

3m oil (WTI) into the 69 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 162.67 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.704% UP 1 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.964 UP 0 PTS..: USA/SF this 0.8100 as the Swiss Franc . Euro vs SF: 0.9234

USA 10 YR BOND YIELD: 4.467 UP 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.960 UP 6 BASIS PTS/

USA 2 YR BOND YIELD: 4.176 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 46.68 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 4.8145 UP 5 PTS

30 YR UK BOND YIELD: 5.541 UP 7 BASIS PTS

10 YR CANADA BOND YIELD: 3.382 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.0150 UP 2 BASIS PTS.

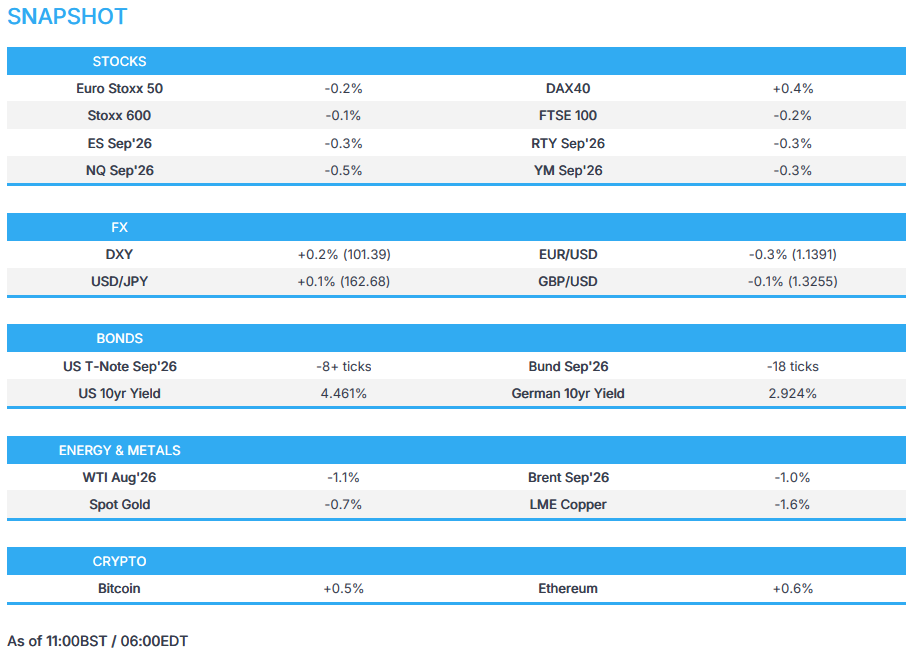

1a New York Opening report

Futures Fall To Start Now Quarter With Warsh Sintra Comments On Deck

Wednesday, Jul 01, 2026 – 08:35 AM

US equity futures point to a softer start to the third quarter as investors await a fresh batch of economic data and the first major overseas appearance by Fed Chair Kevin Warsh. As of 8:20am ET, S&P futures are down 0.2%, off session lows, while Nasdaq futures are down 0.6: techs lags following NDX’s 3.9% gain over the last 2 days; in premarket trading, chipmakers, which did much of the heavy lifting as investors piled into AI beneficiaries, were weaker with Mag7s mostly lower. Nike dropped 2% following a cautious outlook. Software names including Microsoft gained. Cyclicals are under pressure with HC and Staples leading a Defensives bid. Overnight the US removed Anthropic’s foreign access restrictions. Bond yields are flat to down 1bp, and USD is bid as positive progress is reported in US / Iran talk. In commodities, crude prices are lower as distillates rise; WTI futures are down about 0.8% following the biggest quarterly drop since the pandemic.Metals are under pressure, with Ags bid as the group has been the recent outperformer. US economic data calendar includes June ADP employment change (8:15am), June final S&P Global manufacturing PMI (9:45am) and June ISM manufacturing (10am).

In premarket trading, Microsoft outperforms Magnificent 7 peers in premarket trading. Business Insider reports that the company is planning to announce job cuts, impacting thousands of roles, citing people it didn’t identify. Shares are up 1.7%. Other Mag 7 stocks are mixed early Wednesday (Alphabet -0.4%, Nvidia -0.6%, Apple -0.09%, Tesla -0.4%, Amazon +0.9%, Meta Platforms +0.3%). Here are some of the biggest US movers today:

Abbott Lab (ABT) shares are up 0.03% in premarket trading after Baird initiated coverage of the stock with an outperform rating, saying a clearer path to upside for the medical device maker is “beginning to emerge.”

Alcoa Corp. (AA) is down 5.0% after the mining company agreed to buy South32 Ltd.’s bauxite, alumina and aluminum assets in a deal worth as much as $5.6 billion. Morgan Stanley expects a negative reaction on the transaction multiple and limited visibility on synergies.

Bloom Energy (BE) shares rise 8.3% in premarket trading on Wednesday after the company expanded its partnership with Brookfield from $5 billion to $25 billion to help grow the fuel cell partnership globally.

Dow Inc. shares are down 0.7% in premarket trading, after RBC Capital Markets downgraded the chemical company to sector perform from outperform. Mizuho cut its price target to $35 from $43.

FMC shares rise 7.0% after the company said Tessenderlo Group will make a strategic minority equity investment of about $400 million at $13.30 per share. Shares in Tessenderlo gain 3.4% in Brussels.