GOLD CLOSED UP $63.95 TO $4062.95

SILVER CLOSED UP $1.18 TO $58.81

GOLD $4052.00 3:30 PM)

SILVER: 58.73 3;30 PM)

JULY 14

EXCHANGE: COMEX

CONTRACT: JULY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,997.000000000 USD

INTENT DATE: 07/13/2026 DELIVERY DATE: 07/15/2026

FIRM ORG FIRM NAME ISSUED STOPPED

092 C DEUTSCHE BANK 245

099 H DEUTSCHE BANK AG 196

118 C MACQUARIE FUTURES US 271

357 C WEDBUSH SECURITIES 1

363 H WELLS FARGO SECURITI 6

555 C BNP PARIBAS SEC CORP 198

661 C JP MORGAN SECURITIES 10

732 C RBC CAP MARKETS 2

905 C ADM 27

TOTAL: 478 478

MO

GOLD: NUMBER OF NOTICES FILED FOR JULY/2026: 478 CONTRACTs NOTICES FOR 47,800 OZ or 1.4867 TONNES

total notices so far: 10,253 contracts FOR 1,025,300 OZ OR 31.891 TONNES

SILVER NOTICES: 141 NOTICE(S) FILED FOR 0.705 MILLION OZ /

total number of notices filed so far this month : 6089 CONTRACTS (NOTICES) for 30.445 million oz

GLD AND SLV

GLD

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF XX CONTRACTS OR XXX OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

JUNE INITIAL STANDING FOR SILVER:10.935 MILLION OZ TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 10,000 OZ//NEW STANDING ADVANCES TO 12.970 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 20 CONTRACTS FOR 100,000 OZ//NEW STANDING ADVANCES TO 13.070 MILLION OZ. (IN EXCHANGE FOR RISK THE BUYER ASSUMES THE RISK AND ONLY A CENTRAL BANK WOULD TAKE THAT RISK. THE BUYER IS PROBABLY THE CENTRAL BANK OF INDIA.)

JULY INITIAL STANDING: 37.110 MILLION OZ FOLLOWED BY A STRONG 508 CONTRACT QUEUE JUMP OR 2.540 MILLION OZ WHERE DELIVERY WILL OCCUR ON THIS SIDE OF THE POND//STANDING ADVANCES TO 39.015 MILLION OZ///

SUMMARY OF OUR JULY 2026 COMEX CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 59.79 MILLION OZ

JUNE. 64.065 MILLION OZ//FINAL AND FAIR SIZED THIS MONTH.

JULY: 20.750 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

JUNE: INITIAL AMOUNT OF SILVER WILLING TO STAND: 10.935 MILLION OZ PLUS OUR NEXT QUEUE JUMP OF 10,000 OZ//NEW STANDING ADVANCES TO 12.960 MILLION OZ TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 20 CONTRACTS FOR 100,000 OZ//NEW STANDING ADVANCES TO 13.070 MILLION OZ

JULY : INITIAL STANDING: 37.110 MILLION OZ FOLLOWED BY TODAY’S STRONG 2.540 MILLION QUEUE JUMP //STANDING THUS ADVANCES TO 39.015 MILLION OZ//

GOLD//OUTLINE

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

JUNE; INITIAL AMOUNT OF GOLD WILLING TO STAND; 64.496 TONNES.(CME CORRECTED) TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER OF 0.0186 TONNES/NEW STANDING REDUCES TO 127.03 TONNES

JULY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 23.306 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 1.764 TONNES//NEW STANDING ADVANCES TO 31.953 TONNES

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER JUMP OF 0.0186 TONNES//NEW STANDING REDUCES TO 127.03 TONNES//FINAL

JULY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 23.306 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 1.764 TONNES//NEW STANDING FOR GOLD ADVANCES TO 31.015 TONNES.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 118.430 TONNES

JUNE: 142.053 TONNES

JULY: 47.586 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A FAIR SIZED 185 CONTRACTS TO AN OI OF 105,087

EFP ISSUANCE 63 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 63 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 185 CONTRACTS AND ADD TO THE 63 E.FP. ISSUED

WE OBTAIN A FAIR GAIN OF 248 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS OF $2.07

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 1.24 MILLION PAPER OZ

OCCURRED DESPITE OUR LOSS IN PRICE.OF $2.07

2.ASIAN AFFAIRS JULY 14 /2025

SHANGHAI CLOSED UP 53.33 PTS OR 1.36%

HANG SENG CLOSED UP 150.00 PTS OR 0.62%

Nikkei CLOSED UP 507.27 PTS OR 0.75%

//Australia’s all ordinaries CLOSED DOWN 0.10%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7802

/ OFFSHORE CLOSED DOWN AT 6.7820 Oil UP TO 80.07 dollars per barrel for WTI and BRENT UP TO 85.38 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7804) OFFSHORE YUAN TRADING DOWN TO 6.7820 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR 2124 CONTRACTS TO 379,756 STILL WELL ABOVE ITS NEW LOW OF 326,052 OI SET JUNE 3, CLOSE TO THE PREVIOUS ALL TIME LOW OF 345,705 SET (MAY 28) AND CLOSE TO THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27.. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 326,052 //JUNE 3 2026 WITH GOLD AT AN EXTREMELY HIGH $4,450.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD HUGE T.A.S. LIQUIDATION DURING MONDAY’S COMEX TRADING//RAID. IT SEEMS THAT MANY OF THE SPECULATORS THAT HAVE NOW CONTINUED AGAIN TO GO MASSIVELY ON THE SHORT SIDE WITH BANKERS ON THE LONG SIDE WILL BE OBLITERATED TODAY WHEN THE LONGS TENDERED FOR DELIVERY:

CENTRAL BANKS TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS JULY CONTRACT MONTH!!

THE FAIR SIZED GAIN ON OUR TWO EXCHANGES (3,860 CONTRACTS) OCCURRED DESPITE OUR LOSS IN PRICE IN GOLD (DOWN $105.20)

WE THUS HAD A FAIR SIZED GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 3860 CONTRACTS (OR 12.00 TONNES) DESPITE OUR LOSS IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 1736 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIDAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH JUNE AND JULY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

JUNE: 0 IN GOLD. THUS FOR THE ENTIRE MONTH IN GOLD ZERO NOTICES WERE FILED.

JULY 0

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO JUNE/JULY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 146+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

JUNE: ZERO

JULY 0

DETAILS ON OUR NEW JULY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR GAIN ON OUR TWO EXCHANGES OF 3860 CONTRACTS DESPITE OUR LOSS IN PRICE ($105.50). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE/JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A MEGA MEGA HUGE SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED THIS MONSTER 12,635 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IF HISTORY SERVES US WELL, EXPECT 1 MORE OF THESE ISSUANCES ON CONSECUTIVE DAYS WHICH COMMENCED LAST THURSDAY AND THESE ISSUANCES WILL END THIS COMING WEDNESDAY

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

JUNE: ZERO FOR THE MONTH

JULY: ZERO SO FAR

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 146+ TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

JUNE: INITIAL AMOUNT OF GOLD WILLING TO STAND: 64.496 TONNES TO WHICH WE SUBTRACT AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON OF 0.0186 TONNES//NEW STANDING REDUCES TO 127.03 TONNES// TOTAL QUEUE JUMPING FOR THE MONTH FINALIZES AT 62.4217 TONNES OR AVERAGING 3.285 TONNES PER DAY IN JUNE.

JULY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 749,300 OZ OR 23.306 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.6352 TONNES//NEW STANDING ADVANCES TO 30.4167 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING JULY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $105.50)

WE HAD HUGE T.A.S. SPREADER LIQUIDATION MONDAY // COMEX SESSION// WITH OUR STRONG LOSS IN PRICE , OUR SPECULATORS STILL WENT MASSIVELY TO THE SHORT SIDE LED BY THE NOSE BY OUR HIGH FREQUENCY MOMENTUM PLAYERS WITH CENTRAL BANKERS TAKING THE LONG SIDE.

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING //TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $105.20

WE HAD 142 CONTRACTS ADDED TO OI AT THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES: 3860 CONTRACTS OR 386,000 OZ (12.00 TONNES)

JULY DELIVERY MONTH

JULY 14

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER//gold ENTRIES: 0 xxxxxxxxxxxxxxxx |

| No of oz served (contracts) today | 478 CONTRACTS OR 47800 OZ 1.4867 TONNES OF GOLD |

| No of oz to be served (notices) | 20 Contracts 2000 OZ 0.0622 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,253 notices 1,025,300 OZ 31.891 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

DEPOSITS/CUSTOMER

ENTRIES: 0

xxxxxxxxxxxxxxxxxx

comex withdrawal

0 ENTRIES

adjustments: 0//

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF JULY OI STANDS AT 1855 CONTRACTS HAVING A GAIN OF 258 CONTRACTS. WE HAD A GAIN IN OZ STANDING OF 548 CONTRACTS FOR 54,800 OZ OR 1.764 TONNES, ANOTHER QUEUE JUMP AS CENTRAL BANKS CONTINUE TO TAKE PHYSICAL GOLD OUT OF THE COMEX!!

AUGUST LOST 10,120 CONTRACTS TO AN OI OF 237,453

SEPTEMBER LOST 365 CONTRACTS DOWN TO AN OI OF 1532.

.

We had 478 contracts filed for today representing 47,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 10 notices issued from their client or customer account. The total of all issuance by all participants equate to 478 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY. /2026. contract month, we take the total number of notices filed so far for the month (10,253) to which we add the difference between the open interest for the front month of JULY (498 CONTRACTS) minus the number of notices served upon today 478 x 100 oz per contract) equals 1,027,300 OZ OR (31.953 Tonnes of gold)

THUS: INITIAL total number of gold ounces standing for JULY. /2026. contract month, we take the total number of notices filed so far for the month (10,253) to which we add the difference between the open interest for the front month of JULY( 498) contracts minus the number of notices served upon today 478 x 100 oz per contract) equals 1,027,300 OZ OR (31.953 Tonnes of gold)

Yesterday’s standing: 30.4167 tonnes//today: 31.953 tonnes// (queue jump = 1.764 tonnes

new total of gold standing in JULY becomes 31/953 TONNES//

TOTAL COMEX GOLD STANDING FOR JULY 31.953TONNES TONNES WHICH IS NOW REALLY HUGE FOR THIS NON ACTIVE DELIVERY MONTH OF JULY.

confirmed volume MONDAY confirmed 204,285/ FAIR// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,857,755.696 oz 57.78 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,857,755.696 tonnes oz 57.78 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 27,102,993.599oz

TOTAL REGISTERED GOLD 14,760,603.861 tonnes (459.116tonnes)

TOTAL OF ALL ELIGIBLE GOLD 12,342,289.738 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 12,902,848 oz ((REG GOLD- PLEDGED GOLD)=

401.33 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

JULY DELIVERY MONTH

JULY 14

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries i) Out of Asahi 551.640.500 OZ total withdrawal: 551,640.500 oz |

| Deposits to the Dealer Inventory | ENTRY:1 i) Into Asahi: 210,376.140 oz total deposit 210,376.140 oz |

| Deposits to the Customer Inventory | ENTRY:1 i) Into CNT 599,709.790 oz total deposit: 599,709.790 oz |

| No of oz served today (contracts) | 141 CONTRACT(S) ( 0.675 MILLION OZ) |

| No of oz to be served (notices) | 1714 Contracts (8.570 MILLION oz) |

| Total monthly oz silver served (contracts) | 6089 contracts 30.445 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

ENTRY:1

i) Into Asahi: 210,376.140 oz

total deposit 210,376.140 oz

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRY:1

i) Into CNT 599,709.790 oz

total deposit: 599,709.790 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

1 entries

i) Out of Asahi 551.640.500 OZ

total withdrawal: 551,640.500 oz

adjustments :0

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 95.114 MILLION OZ//.TOTAL REG + ELIGIBLE. 328.048 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF JULY /2026 OI: 1855 OPEN INTEREST CONTRACTS FOR A GAIN OF 258 CONTRACTS.

STANDING FOR SILVER TODAY IS REPRESENTED BY 39.015 MILLION OZ. YESTERDAY’S STANDING: 36.475 MILLION OZ. THUS WE GAINED 508 CONTRACTS OR AN ADDITIONAL 2.54 MILLION OZ WILL STAND ON THIS SIDE OF THE POND.

AUGUST SAW A GAIN OF 3 CONTRACTS UP TO 2080…

SEPTEMBER SAW A LOSS OF 638 CONTRACTS DOWN TO AN OI OF 80,672 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 141 or 0.705 MILLION oz

CONFIRMED volume MONDAY; 41,525// extremely poor//

XXX

AND NOW JULY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 6089 X5,000 oz = 30.445 MILLION oz.

We now take the total number of oz standing today and subtract the total standing yesterday and we have a GAIN of 508 contracts for 2.540 MILLION oz and this represents a queue jump where these guys will take delivery on this side of the pond.

YESTERDAY: 36.475 MILLION OZ//STOOD FOR DELIVERY// TODAY 39.015 MILLION OZ//que jump is thus: 2.54 MILLION oz

Thus the standings for silver for the JULY 2026 contract month: (6089 )Notices served so far) x 5000 oz + OI for the front month of JULY ( 1855) minus number of notices served upon today (141)x 5000 oz equals silver standing for the JULY..contract month equating to 39.015 MILLION OZ. ( a very strong delivery month)

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 95.114 million oz of registered silver

JPMorgan as a percentage of total silver: 137.898/328.048million: 42.11%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

JULY 14/2026/WITH GOLD UP $63.45 /NO CHANGES IN GOLD AT THE GLD : / //:/INVENTORY RESTS AT 1002.510 TONNES

JULY 13/2026/WITH GOLD DOWN $105.20 /HUGE CHANGES IN GOLD AT THE GLD : A WITHDRAWAL 0F 3.108 TONNES OF GOLD OUT OF THE GLD/ //:/INVENTORY RESTS AT 1002.510 TONNES

JULY 10/2026/WITH GOLD DOWN $27.25 /HUGE CHANGES IN GOLD AT THE GLD : A DEPOSIT 0F 3.138TONNES OF GOLD INTO THE GLD/ //:/INVENTORY RESTS AT 1005.618 TONNES

JULY 9/2026/WITH GOLD UP $58.60 /SMALL CHANGES IN GOLD AT THE GLD : A WITHDRAWAL OF 0.28 TONNES OF GOLD FROM THE GLD/ //:/INVENTORY RESTS AT 1002.510 TONNES

JULY 8/2026/WITH GOLD DOWN $73.30 /NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1002.79 TONNES

JULY 7/2026/WITH GOLD DOWN $28.05 /HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.42 TONNES OUT INTO THE GLD/ ./ //:/INVENTORY RESTS AT 1002.79 TONNES

JULY 6 /2026/WITH GOLD DOWN $19.55 /HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.954 TONNES OUT OF THE GLD/ ./ //:/INVENTORY RESTS AT 1001.366 TONNES

JULY 3 /2026/WITH GOLD UP $62.95 /NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JULY 2 /2026/WITH GOLD UP $44,05 /NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JULY 1 /2026/WITH GOLD UP $42.95 /NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JUNE 30 /2026/WITH GOLD UP $2.85 /NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JUNE 29 /2026/WITH GOLD DOWN $58.30 /HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 8.223 TONNES OF GOLD FROM THE GLD // ./ //:/INVENTORY RESTS AT 1005.077 TONNES

JUNE 26 /2026/WITH GOLD UP $49.10 /HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 4.287 TONNES OF GOLD FROM THE GLD // ./ //:/INVENTORY RESTS AT 1013.350 TONNES

JUNE 25 /2026/WITH GOLD UP $42.70 /NO CHANGES IN GOLD AT THE GLD: // ./ //:/INVENTORY RESTS AT 1017.637 TONNES

JUNE 24 /2026/WITH GOLD DOWN $141.55 /HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.563 TONNES OF GOLD OUT OF THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1017.637 TONNES

JUNE 19 /2026/WITH GOLD UP $36.85 /HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 7.421 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1020.49 TONNES

JUNE 18 /2026/WITH GOLD DOWN $135.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.856 TONNES OF GOLD INTO THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1013.069 TONNES

JUNE 17 /2026/WITH GOLD UP $20.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.427 TONNES OF GOLD FROM THE GLD/./ //// ./ //:/INVENTORY RESTS AT 1012.213 TONNES

JUNE 16 /2026/WITH GOLD UP $4.45 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 15 /2026/WITH GOLD UP $111.10 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 12 /2026/WITH GOLD UP $123.30 TODAY/NO CHANGES IN GOLD AT THE GLD: //// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 11 /2026/WITH GOLD DOWN $15.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.855 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1013.640 TONNES

JUNE 10 /2026/WITH GOLD DOWN $153.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.426 TONNES OF GOLD FROM THE GLD//// ./ //:/INVENTORY RESTS AT 1016.495 TONNES

JUNE 9 /2026/WITH GOLD DOWN $75.60 TODAY/NO CHANGES IN GOLD AT THE GLD:// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 8 /2026/WITH GOLD DOWN $3.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 6.936 TONNES OF GOLD FROM THE GLD// ./ //:/INVENTORY RESTS AT 1019.921 TONNES

JUNE 5 /2026/WITH GOLD DOWN $134;85 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1026.857 TONNES

GLD INVENTORY: 1002.51 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

JULY 14 WITH SILVER UP $1.18: :HUGE CHANGES IN INVENTORY AT THE SLV/ A WITHDRAWAL OF 543,000 OZ FROM THE SLV// :INVENTORY RESTS AT 477,587 MILLION OZ

JULY 13 WITH SILVER DOWN $2.07: :NO CHANGES IN INVENTORY AT THE SLV/ :INVENTORY RESTS AT 478.130 MILLION OZ

JULY 10 WITH SILVER DOWN $0.67: :SMALL CHANGES IN INVENTORY AT THE SLV A WITHDRAWAL OF 0.904 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 478.130 MILLION OZ

JULY 9 WITH SILVER UP $2.64: :SMALL CHANGES IN INVENTORY AT THE SLV A WITHDRAWAL OF 0.497 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 479.531 MILLION OZ

JULY 8 WITH SILVER DOWN $2.70: :HUGE CHANGES IN INVENTORY AT THE SLV A DEPOSIT OF 0.497 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 479.531 MILLION OZ

JULY 7 WITH SILVER DOWN $1.36: :HUGE CHANGES IN INVENTORY AT THE SLV A WITHDRAWAL OF 1.266 MILLION OZ OUT OF THE SLV/ :INVENTORY RESTS AT 479.034 MILLION OZ

JULY 6 WITH SILVER DOWN $0.51: :HUGE CHANGES IN INVENTORY AT THE SLV A DEPOSIT OF 940,000 OZ INTO THE SLV/ :INVENTORY RESTS AT 480.300 MILLION OZ

JULY 3 WITH SILVER UP $1.81: :SMALL CHANGES IN INVENTORY AT THE SLV A DEPOSIT OF 940,000 OZ INTO THE SLV.// :INVENTORY RESTS AT 479.360 MILLION OZ

JULY 2 WITH SILVER UP $0.58: : NO CHANGES IN INVENTORY AT THE SLV// :INVENTORY RESTS AT 479.360 MILLION OZ

JULY 1 WITH SILVER UP $0.48: : SMALL CHANGES IN INVENTORY AT THE SLV A DEPOSIT OF 0.233 MILLION OZ OUT OF THE SLV/./ // :INVENTORY RESTS AT 479.360 MILLION OZ

JUNE 30 WITH SILVER UP $1.35: : HUGE CHANGES IN INVENTORY AT THE SLV A WITHDRAWAL OF 1.447 MILLION OZ OUT OF THE SLV/./ // :INVENTORY RESTS AT 479.127 MILLION OZ

JUNE 29 WITH SILVER DOWN $1.08: : HUGE CHANGES IN INVENTORY AT THJE SLV A WITHDRAWAL OF 1.402 MILLION OZ OUT OF THE SLV/./ // :INVENTORY RESTS AT 480.574 MILLION OZ

JUNE 26 WITH SILVER UP $0.86: : HUGE CHANGES IN INVENTORY AT THJE SLV A DEPOSIT OF 2.352 MILLION OZ INTO THE SLV/./ // :INVENTORY RESTS AT 481.976 MILLION OZ

JUNE 25 WITH SILVER UP $0.69: : SMALL CHANGES IN INVENTORY AT THJE SLV A WITHDRAWAL OF 769,000 OUT OF THE SLV/./ // :INVENTORY RESTS AT 479.624 MILLION OZ

JUNE 24 WITH SILVER DOWN $4.18: : SMALL CHANGES IN INVENTORY AT THJE SLV A DEPOSIT OF 93,000 MILLION OZ INTO THE SLV/./ // :INVENTORY RESTS AT 480.393 MILLION OZ

JUNE 19 WITH SILVER UP $1.11: : NO CHANGES IN INVENTORY AT THJE SLV/./ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 18 WITH SILVER DOWN $4.80: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: HUGE CHANGES IN INVENTORY A WITHDRAWAL OF 1.086 MILLION OZ FROM THE SLV././ // :INVENTORY RESTS AT 480.302 MILLION OZ

JUNE 17 WITH SILVER UP $0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: NO CHANGE IN INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 16 WITH SILVER DOWN $0.13: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.362 MILLION OZ INTO THE SLV /./ // :INVENTORY RESTS AT 481.388 MILLION OZ

JUNE 15 WITH SILVER UP $3.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.357 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 481.026 MILLION OZ

JUNE 12 WITH SILVER UP $3.34: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.769 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 482.383 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.12: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.226 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.152 MILLION OZ

JUNE 10 WITH SILVER DOWN $0.50: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.909 MILLION OZ OUT THE SLV /./ // :INVENTORY RESTS AT 483.378 MILLION OZ

JUNE 9 WITH SILVER DOWN $3.35: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.407 MILLION OZ INTO INTO THE SLV /./ // :INVENTORY RESTS AT 484.287 MILLION OZ

JUNE 8 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 543,000 OZ FROM THE SLV /./ // :INVENTORY RESTS AT 482.880 MILLION OZ

JUNE 5 WITH SILVER DOWN $4.86: NO CHANGES IN SILVER INVENTORY AT THE SLV /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 4 WITH SILVER UP $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.432 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 3 WITH SILVER DOWN $2.55: NO CHANGES IN SILVER INVENTORY AT THE SLV >> /./ // :INVENTORY RESTS AT 483.423 MILLION OZ

JUNE 2 WITH SILVER UP $0.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV >> A WITHDRAWAL OF 1.2222 MILLION OZ FROM THE SLV/./ // :INVENTORY RESTS AT 484.855 MILLION OZ

JUNE 1 WITH SILVER DOWN $0.52: HUGE CHANGES IN SILVER INVENTORY AT THE SLVA WITHDRAWAL OF 1.9 MILLION OZ FORM THE SLV/./ // :INVENTORY RESTS AT 486.077 MILLION OZ

MAY 29 WITH SILVER DOWN $0.03: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

CLOSING INVENTORY 477.587 MILLION OZ OF SILVER

GOLD COMMENTARIES:

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD.\

3. CHRIS POWELL AND HIS GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT; 279 AND 278

China Pulls Gold Revaluation Trigger

by Kinesis Money

Thursday, Jul 02, 2026 – 11:19

In this week’s Live from the Vault, Andrew Maguire reveals how China is clearing the path to take control of global gold price setting, as the PBOC drains Western gold reserves and builds the infrastructure to challenge London and New York’s pricing grip.

With central banks racing to repatriate their gold, June imports into China set to break all records, the London whistleblower outlines why he believes a US Treasury gold revaluation is no longer a distant possibility – but an approaching reality.

MUST VIEW

China takes control of gold pricing this month, Maguire tells LFTV

Submitted by admin on Thu, 2026-07-02 14:59 Section: Daily Dispatches

3:02p ET Thursday, July 2, 2025

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire today tells Kinesis Money’s “Live from the Vault” program that “central bank gold wars have spilled into the daylight” and events in China suggest that an upheaval in the gold market is targeted for July 24.

“The Fed’s 60-year gold short is running out of road,” with central bank repatriations of gold putting impossible pressure on the Fed, since adequate real metal isn’t available, Maguire says.

The recent pounding of derivative gold prices in London and New York by the Fed was meant to produce the “death cross” on gold charts, Maguire says, but has been construed by central banks not as a sell signal but as a buy signal.

China, Maguire says, has been taking three to five tonnes of metal out of London and New York every day and now has the infrastructure in place to take control of gold pricing away from London and New York. As a result, he adds, the Chinese yuan, heavily anchored by gold, will challenge the dollar as a reserve currency.

END

5. COMMODITY REPORT/HELIUM…

China’s Helium Export Ban Raises New Risks For Global Supply Chains

Tuesday, Jul 14, 2026 – 01:05 PM

Authored by Michael Zhuang via The Epoch Times,

China has imposed a temporary ban on helium exports, adding fresh uncertainty to global supplies of a gas essential to semiconductor manufacturing, aerospace, medical equipment, and other high-tech industries. The first pilot helium production facility in Europe, located in Saint-Parize-le-Châtel, France, on Sept. 11, 2024. FREDERIC MOREAU/Hans Lucas via AFP/Getty Images

The first pilot helium production facility in Europe, located in Saint-Parize-le-Châtel, France, on Sept. 11, 2024. FREDERIC MOREAU/Hans Lucas via AFP/Getty Images

The July 10 announcement by China’s Ministry of Commerce and General Administration of Customs comes as Beijing faces mounting pressure on its own helium supplies following disruptions to imports from Qatar and Russia.

Analysts who spoke to The Epoch Times say the move appears primarily aimed at safeguarding China’s domestic supply rather than directly targeting the United States. However, since Chinese companies have increasingly served as intermediaries for Russian helium exports, the restriction could further disrupt global supply chains, particularly in Europe.

Beijing Announces Temporary Export Ban

The Chinese regime said the export restriction was imposed under the country’s Foreign Trade Law. It took effect immediately. The regime did not specify how long the temporary measure would remain in place.

Helium is a colorless, odorless, non-toxic inert gas extracted as a byproduct of natural gas processing. Since it cannot be manufactured or replenished, it is considered a strategic resource.

The gas plays a critical role in semiconductor production, where it is used for wafer cooling, plasma etching, chemical vapor deposition, atomic layer deposition, photolithography support, and leak detection. It is also widely used in medical imaging, aerospace, scientific research, and advanced manufacturing.

Despite expanding domestic production, China still relies heavily on imported helium.

According to industry data from China Fortune Securities, approximately 84 percent of China’s helium supply is dependent on foreign imports, with natural gas producers Qatar and Russia accounting together for nearly half of global helium production. The United States is the world’s largest helium producer, producing more than 40 percent of global production.

China sources roughly 46 percent of its helium imports from Qatar and about 35 percent from Russia. But these import channels have come under increasing pressure this year.

According to a report on Chinese news portal Sina, maritime routes carrying Qatari helium through the Persian Gulf were disrupted amid the Iran war. In April, Russia announced temporary export controls on helium through the end of 2027, reducing export quotas to Asia to roughly 40 percent of 2025 levels. The China Liquefied Natural Gas Association estimated that those developments have created a helium supply shortfall exceeding 60 percent for China.

Cheng Cheng-ping, a professor of finance at Taiwan’s National Yunlin University of Science and Technology, told The Epoch Times that Beijing’s decision appears to be driven largely by domestic supply concerns rather than geopolitical retaliation.

“The timing suggests this is primarily an act of self-preservation,” he said. “It is different from previous export controls on rare earths, which were more directly aimed at the United States.”

Beijing has been working to expand China’s domestic semiconductor industry while reducing reliance on advanced chips restricted by U.S. export controls.

“China is engaged in intense competition with the United States in high-end industries but remains behind technologically,” Cheng said. “Restricting exports allows it to retain more resources to support its own advanced manufacturing.”

Shen Ming-shih, a research fellow at Taiwan’s Institute for National Defense and Security Research, told The Epoch Times that several factors likely influenced the decision, but domestic industrial demand appears to be the primary consideration.

“The Chinese Communist Party (CCP) can still import helium from Russia for now,” Shen said. “But if Russian supplies tighten further through 2027 while imports from other sources remain constrained, China’s own helium resources will become increasingly scarce.”

China’s Role as a Russian Helium Middleman

While the export restrictions may help preserve domestic supplies, they could also tighten international markets because Chinese companies have become important intermediaries in the global helium trade.

According to a June report by U.K.-based industry intelligence firm Gasworld, Western sanctions have largely prevented Russia from exporting helium directly to Europe. Instead, Chinese companies have been importing Russian helium at relatively low prices – often in volumes exceeding China’s own domestic consumption – and re-exporting part of those shipments to overseas markets, including Europe.

Russian helium exports to China averaged 38 million cubic feet per month in 2025, a 60 percent increase from the previous year, according to the report. Shipments reached 71 million cubic feet in December alone.

China’s export ban could further tighten global helium supplies because of the country’s growing role as a redistribution hub for Russian helium.

Cheng said the United States is unlikely to be significantly affected because of its own supplies.

According to the U.S. Geological Survey, the United States accounted for 44 percent of global helium production in 2024, followed by Qatar at 34 percent, Russia at 9 percent, and Algeria at 6 percent.

“The impact will be much greater for Europe and other countries that previously relied on Russian or Qatari helium but increasingly obtained those supplies through China,” Cheng said.

With Russian exports constrained by sanctions and Middle Eastern supplies facing periodic disruptions, China has gained considerable leverage as an intermediary, he said.

“By restricting exports now, China is increasing risks across the global supply chain,” Cheng said.

He added that Beijing has previously leveraged its position in global supply chains to exert pressure on agricultural imports from Australia, Brazil, and Taiwan.

“Now, helium has become another example,” Cheng said. “China is only an intermediary, but it is using that position as a tool to influence markets and supply chains. Companies trading with authoritarian regimes need to factor these risks into their supply-chain planning.”

Shen said the ultimate impact of the export restrictions will depend on how heavily individual countries rely on Chinese helium exports and whether they can secure alternative suppliers.

European countries may experience greater short-term disruptions, he said, but the move could also encourage importers to diversify their sources and reduce dependence on China.

Tang Bing, Luo Ya, and Reuters contributed to this report

END.

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 53.33 PTS OR 1.36%

HANG SENG CLOSED UP 150.00 PTS OR 0.62%

Nikkei CLOSED UP 507.27 PTS OR 0.75%

//Australia’s all ordinaries CLOSED DOWN 0.10%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.7802

/ OFFSHORE CLOSED DOWN AT 6.7820 Oil UP TO 80.07 dollars per barrel for WTI and BRENT UP TO 85.38 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING DOWN (6.7804) OFFSHORE YUAN TRADING DOWN TO 6.7820 ONSHORE YUAN TRADING ABOVE LEVEL OF OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ONSHORE YUAN: CLOSED DOWN AT 6.7804

OFFSHORE YUAN: DOWN TO 6.7820

1.HANG SANG CLOSED UP 150.00 PTS OR 0.62%

2. Nikkei closed UP 507.27 PTS OR 0.75%

WEST TEXAS INTERMEDIATE OIL UP TO 80.07

BRENT; 85.38

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 101.03/// EURO RISES TO 1.1386 UP 3 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +2.703 DOWN 8 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA CROSS NOW AT 162.07… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.809 DOWN 11 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN( 6.7804) AND OFFSHORE: DOWN AT 6.7820

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA. CENTRAL BANK OF JAPAN WILL NO LONGER DO QE.

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt. GOVERMENT ASKED JAPAN PENSION FUNDS AND INSURANCE FUNDS TO BUY MORE JAPANESE BONDS AND REPATRIATE ALL FOREIGN BONDS.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EU German 10yr bund YIELD UP TO +3.1058/ Italian 10 Yr bond yield UP to 3.930/ SPAIN 10 YR BOND YIELD UP TO 3.602%

3i Greek 10 year bond yield UP TO 3.809%

3j Gold at $4026.00 //Silver at: 58.03 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 24/ 100 roubles/76.86

3m oil (WTI) into the 80 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 162.07 // 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.703% DOWN 8 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS TO BE REPATRIATED.//JAPAN 30 YR: 3.735 DOWN 16 PTS..: USA/SF this 0.8147 as the Swiss Franc . Euro vs SF: 0.9277

USA 10 YR BOND YIELD: 4.630 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 5.106 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.290 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 47.04 UP 4 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD AND USA DOLLAR RESERVES.

10 YR UK BOND YIELD: 5.0032 UP 6 PTS

30 YR UK BOND YIELD: 5.706 UP 4 BASIS PTS

10 YR CANADA BOND YIELD: 3.565 UP 5 BASIS PTS

5 YR CANADA BOND YIELD: 3.190 UP 6 BASIS PTS.

Futures Mixed Ahead Of CPI And Warsh Testimony, As IBM Sinks, Bank Earnings Fizzle

Tuesday, Jul 14, 2026 – 08:24 AM

US stocks are struggling for direction as traders waited to buy the dip on a busy day that kicked off with Wall Street earnings whichwith JPM, BofA, Goldman, Citi and Wells all reporting. Kevin Warsh’s testimony before Congress and CPI data are due later. As of 8:00am ET, S&P 500 futures fell 0.2% with Nasdaq 100 contracts up 0.6%, set for a rebound from the selloff in AI-linked names yesterday and defying declines elsewhere. In premarket trading, IBM crashed 20% – the most since 1987 – after unexpectedly preannouncing a big revenue miss; elsewhere, semiconductors are leading after Korea’s Kospi staged a powerful rebound from session lows while SK Hynix saw a 10% swing in Korea trading; Mag7 is mixed, and the AI theme is bid. WTI crude traded around $80/bbl and Brent above $86/bbl (both off session highs) as the ceasefire / MoU appear to be voided with both sides claiming control of the SoH. Both Disc and Staples are lower, perhaps reflecting some consumer fears. Energy / Mats are bid on the Middle East, Fins are bid into earnings, Industrials are higher with the AI theme with HC mixed. Higher oil prices lifted odds of a July US rate hike in place, with swap markets signaling a nearly 40% chance of a hike when the Fed meets later this month. The yield on two-year UK gilts touched the highest level since May. Treasuries edged higher and the dollar fell. Traders will closely watch the CPI data, especially after the Fed’s Waller, a former dove, said Monday that a hike is on the table if inflation stays hot and as bond market volatility saw a double-digit jump. The recent fall in gasoline prices likely helped drag down the CPI print, which may notch its first monthly decline since the onset of the pandemic in 2020. The macro focus is on CPI plus the consumer / GDP read-through from GSIBs. The data calendar includes weekly ADP employment change (8:15am), June CPI (8:30am) and May TIC flows (4pm), Fed calendar includes Warsh’s testimony on its Semi-Annual Monetary Policy Report before the House Financial Services at 10am. Also scheduled to speak are Governor Barr (12:40pm), Chicago Fed’s Goolsbee (1pm) and Governors Cook (1:30pm) and Bowman (2:55pm).

In premarket trading, Mag 7 stocks are mixed: Apple is down 0.7% after being cut to underweight at KeyBanc, which expects weaker device demand and service revenue growth in the US (Nvidia +1.2%, Tesla +0.3%, Amazon -0.4%, Alphabet -0.5%, Microsoft -2.8%, Meta Platforms -1.1%).

- IBM (IBM) sinks 19% after reporting preliminary quarterly sales results that missed analysts estimates, with Chief Executive Officer Arvind Krishna saying customers were holding back spending.

- Software and IT/professional services stocks are broadly lower after IBM’s preliminary revenue for the second quarter fell short of the consensus estimate. Microsoft falls 2.8%, Intuit drops 5% and Adobe declines 4.8%

- CoStar Group (CSGP) falls 5% after the real estate analytics firm named Robin Rossmann as the company’s next CFO. Rossmann will succeed Christian Lown, who is stepping down to pursue an opportunity outside the company’s industry.

- Goldman Sachs Group (GS) climbs 1.3% after posting $7.42 billion for a quarter with record-breaking stock-trading results, driven by financing and taking profit in arranging bets.

- JPMorgan (JPM) falls 2% after the lender said it sees full year adjusted expenses at about $107.5 billion, previously seeing about $105 billion.

- O-I Glass (OI) slips 3% after BofA cut its rating to underperform from buy, saying relative upside for the shares may lag due to volume weakness in glass packaging.

- Trex (TREX) climbs 3% after the decking manufacturer’s second-quarter net sales forecast beat the average analyst estimate.

In other AI related developments Nvidia and Mitsubishi Heavy Industries are looking to tie up on AI data center technologies, Nikkei reported, and Samsung is said to be in early discussions for a potential US share sale. Memory and chip stocks remain the core equity theme after investors poured $21 billion into ETFs last week, according to JPMorgan. In other corporate news, Brown-Forman President/CEO Lawson Whiting is set to step down once a successor is named. BP said it expects to write down another $1 billion from energy transition assets in the second quarter, as the British major continues the painstaking work of re-orientating itself toward its core oil and gas business. Apple falls in premarket trading after being cut to underweight from sector weight at KeyBanc, which expects weaker device demand and service revenue growth in the US.

Today’s event-filled calendar began with a mixed reaction to Goldman Sachs, JPMorgan, Bank of America, Wells Fargo and Citigroup, as the banks were already priced to perfection, and despite blowout earnings, their stocks mostly dipped in premarket trading. June CPI data is expected to show some relief after inflation accelerated rapidly from March through May. Federal Reserve Chair Warsh is scheduled to testify before House members hours later.

“Geopolitics on the margin is a negative, but the oil price has not spiked dramatically,” said Richard Flax, chief investment officer at Moneyfarm. “I expect Warsh will give a sort of data-driven speech rather than say too much about forward guidance. For us, it’s more about the inflation data.”

Warsh would probably prefer not to present this week’s Humphrey-Hawkins testimony, but “Congress isn’t inclined to let Warsh off the hook,” writes Bloomberg Senior US Economist Andrew Sacher, who outlines what to expect from Warsh’s appearances.

In an escalation of the standoff between the US and Iran over the Strait of Hormuz, President Donald Trump reinstated the blockade of Iranian ships transiting the waterway and demanded a 20% reimbursement for all other cargo. US forces also completed another round of strikes against the Islamic Republic.

“We know the market can sustain far higher oil prices and US stocks keep rising,” said Alpesh Patel, managing partner at RootBridge Capital. “The only thing that matters is any indication rates are going to rise.”

Global investors buying stocks aggressively should consider reducing exposure with investor sentiment getting extremely bullish, according to the latest BofA Global Fund Manager Survey, with positioning on US equities now at its highest level since December 2024 at a net 24% overweight, cash levels “uber-low” at 3.6%, and BofA’s Bull & Bear Indicator now at the extreme bull reading of 9.

Overnight, China exports climbed 27% from a year earlier, exporting a record $412 billion worth of goods in June, blowing past all forecasts and turbocharged by a global investment supercycle in AI.

In a sign of confidence that the artificial-intelligence buildout will keep on fueling demand for chips, people familiar said Samsung Electronics is exploring a potential offering of ADR, similar to SK Hynix, in hopes of top ticking the memory bubble. Semiconductor stocks bounced in early US trading after Monday’s rout. “This suggests that the Nasdaq could break its short-term negative correlation with the oil price, and rise alongside energy prices if this continues,” wrote Kathleen Brooks, research director at XTB.

In Europe, the Stoxx 600 slid 0.4%, having dodged the weakness in tech stocks on Monday, is falling 0.6% with a drag from the media, travel and consumer sectors. Ericsson AB’s shares fell as much as 10% after warning that margins in its main networks business will come under pressure. Here are the biggest movers Tuesday:

- Mycronic shares gain as much as 14% to hit a record high as earnings from the Swedish electronics equipment group beat forecasts. DNB described the report as “impressive”

- BP shares surged as much as 3.3% to touch a one-month high as Jefferies noted that the oil major’s net debt estimates for the second quarter had undershot expectations

- Allegro climbs as much as 6.5% to highest since 2022 after the Polish e-commerce company reported strong preliminary 1H results and indicated it may raise its full-year outlook

- Salzgitter shares rise as much as 7.4% as Jefferies upgrades its rating on the steel producer to buy from hold, citing benefits from EU steel quotas

- Hapag-Lloyd shares rise as much as 8.2% in Frankfurt after the German container shipper boosted its Ebitda forecast for the year

- Genus shares rise as much as 14%, the most in about six months, after the animal genetics specialist said it now sees full-year profit ahead of market expectations

- Ericsson shares fall as much as 10% after the Swedish mobile networks and technology group said margins for its key Networks division will come under pressure in the second half of 2026, overshadowing otherwise in-line figures

- IntegraFin shares fall as much as 5.4%, the most in nearly two months, as the investment platform sees third-quarter flows come in slightly below some analysts’ expectations

- Norske Skog falls as much as 18%, the most since February 2025, after the Norwegian paper and forestry firm reported its latest earnings, which included misses on total operating income and Ebitda

- Norion Bank falls as much as 13%, the most since February, after the Swedish banking group reported weak second-quarter earnings. SB1 Markets points to an underlying miss in net interest income and higher costs

Asian stocks reversed earlier losses as South Korean memory chipmakers rebounded in late trading. The MSCI Asia Pacific Index gained 0.4% after falling as much as 1.6% earlier in the session. Samsung was the biggest boost to the index amid news the company was in early discussion for a potential share sale in the US. SK Hynix also erased an early plunge, helping to lift the Kospi gauge. The movements in Korea’s memory chip stocks underscore the extreme volatility gripping some of the world’s biggest beneficiaries of the artificial intelligence boom. Japan’s Topix rose as investors looked for opportunities in non-tech sectors that have lagged the broader market. Taiwan’s Taiex index dropped 1.4% to its lowest in more than two weeks.

The “recent volatility indicates you are starting to build two camps — one remains very optimistic, whereas you have a growing group that question the sustainability,” said Mattias Martinsson, chief investment officer at Tundra Fonder AB. “That creates a tug of war, from day to day, which has very little to do with geopolitical events. For today the optimists have the upper hand.”

In rates, treasuries are little changed after retreating from session highs reached as oil extended its climb, with investors awaiting testimony by Fed Chair Kevin Warsh and June CPI report. US 10-year yield near 4.62% outperforms bunds and gilts in the sector by 2bp and 4bp following retreat from 4.634%, highest since May 20; curve spreads are also little changed. 2- and 5-year tenors reached new YTD yield highs. Around 11bp of Fed tightening is priced in for the July policy meeting following Monday’s increase on hawkish comments from Fed Governor Christopher Waller. Money markets see at least one Bank of England and one European Central Bank rate hike this year, while leaning strongly toward a second in December. IG dollar issuance slate empty so far. Monday saw a combined $6.7 billion priced as issuers paid about 2.7 basis points in new issue concessions on deals that were 5.5 times covered.

In FX, the Bloomberg Dollar Spot Index is down by 0.2% and moves across currency markets remain relatively muted.

In commodities, Brent extended its gain to $86/barrel on the new US blockade of Hormuz is driving more rate-hike bets from traders and rippling across the short-end of European bond markets. WTI crude oil futures are up about 3%, off session highs reached as the truce between the US and Iran collapsed following fresh attacks on shipping in the Strait of Hormuz. Gold is gaining to move back above $4,000/oz.

The US economic data calendar includes weekly ADP employment change (8:15am), June CPI (8:30am) and May TIC flows (4pm), Fed calendar includes Warsh’s testimony on its Semi-Annual Monetary Policy Report before the House Financial Services at 10am. Also scheduled to speak are Governor Barr (12:40pm), Chicago Fed’s Goolsbee (1pm) and Governors Cook (1:30pm) and Bowman (2:55pm)

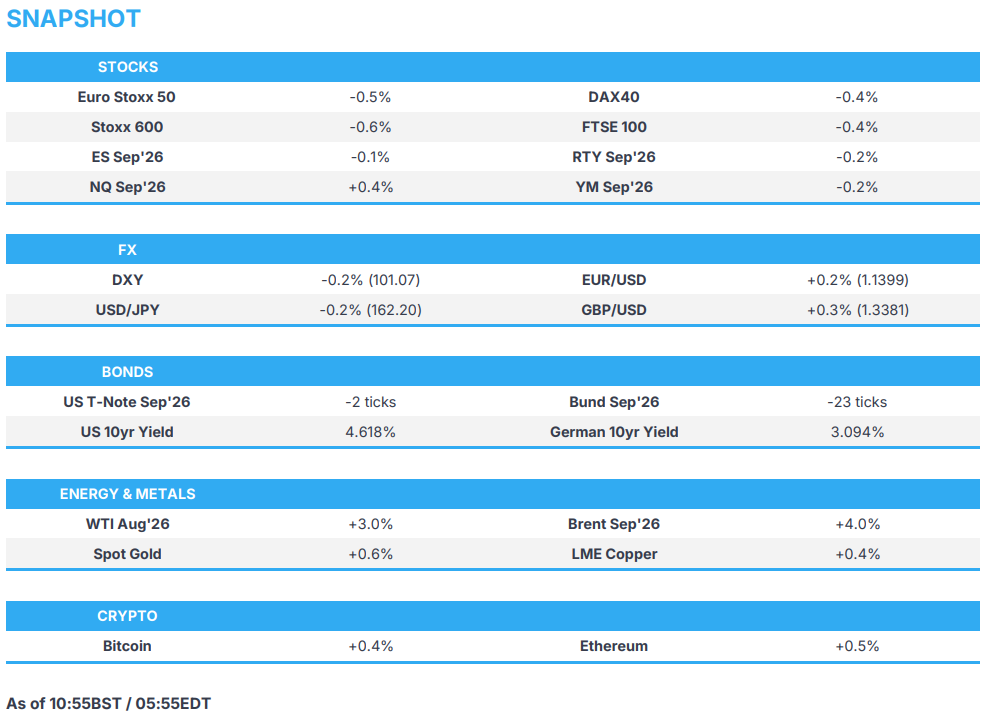

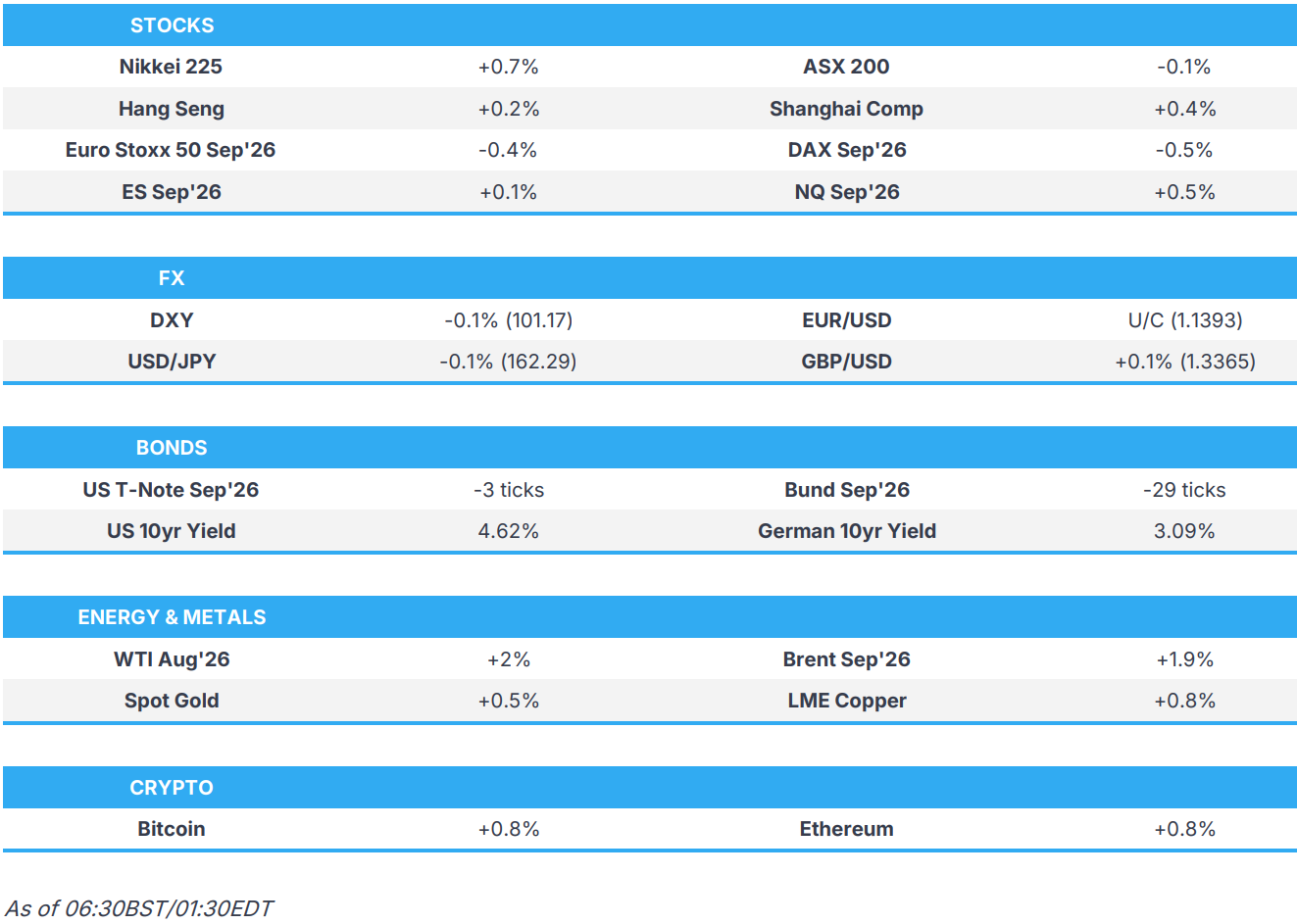

Market Snapshot

Top Overnight News

- President Donald Trump formally notified lawmakers this weekend that the nation is once again at war with Iran, giving his administration another 60-day clock to use the military in the region without congressional approval. Politico

- Brent topped $86 as Donald Trump said he would reinstate a blockade of Iranian ships transiting the Strait of Hormuz at 4 p.m. ET today. BBG

- For decades, OPEC influenced the market by how much oil it produced. But China, the largest importer, is demonstrating its remarkable power over prices. Typically the world’s largest oil importer, China slashed purchases this spring, reducing demand so much that it prevented oil prices from soaring even higher earlier in the war. WSJ

- Trump plans to back a Russia sanctions bill championed by late Senator Lindsey Graham, a person familiar said. His support would be a major win for Ukraine’s push to punish buyers of Moscow oil and gas. BBG

- China’s exports surged in June, buoyed by orders for chips to fuel the global AI boom and automobiles, deepening producers’ reliance on overseas buyers as policymakers in the world’s No. 2 economy continue to grapple with how to boost demand at home. The stronger-than-expected trade performance keeps China on track to post a surplus topping $1 trillion for a second straight year, with factories sustaining sales despite slowing growth in major economies and trade frictions with Washington. RTRS

- Japanese policymakers on Tuesday flagged the possibility of changes to the asset allocation of the nation’s giant state pension funds, though they offered no clues on the timing or scale of any shift. RTRS

- Over the past year, the Trump administration has made deals to acquire equity stakes in more than two dozen firms, an unusual practice that extended the government’s influence over industries including semis, nuclear energy, minerals, and quantum computers and steel. AI execs are increasingly wondering if they will be next. NYT

- Gov. Kathy Hochul is banning large data-center construction for up to a year, making New York the latest state to confront the rollout of sites powering the artificial-intelligence boom. The move responds to concerns over power costs, water supplies and community impacts as states consider limits on AI infrastructure’s effects on electricity grids and utility bills. WSJ

- As Warsh prepares to face Congress, traders now see a US rate hike later this month as a coin toss. Money-market pricing suggests traders boosted their wagers for a July increase to almost 50% after yesterday’s strikes on Iran. BBG

- US House will vote today on merging the SAVE America Act with a national security and State Department funding bill: Fox

- Trump said they’re looking into whether Cuba is storing Iranian drones, while he added that they will take care of it if Cuba has Iranian drones.

- CPI Preview: Goldaman expects a 0.17% increase in June core CPI (vs. +0.3% consensus), corresponding to a year-over-year rate of +2.76% (vs. +2.9% consensus). The bank expects a 0.11% decline in headline CPI (vs. -0.1% consensus), reflecting lower energy prices. The forecast is consistent with a 0.24% increase in core PCE in June, reflecting another large increase in its financial services component.

A more detailed look at global markets courtesy of Newsquawk