GOLD: $1273.95 DOWN $9.15

Silver: $16.43 DOWN 13 cents

Closing access prices:

Gold $1275.30

silver: $16.43

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1292.28 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1284.75

PREMIUM FIRST FIX: $7.53

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1290.66

NY GOLD PRICE AT THE EXACT SAME TIME: $1284.10

Premium of Shanghai 2nd fix/NY:$6.56

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1282.15

NY PRICING AT THE EXACT SAME TIME: $1281.90

LONDON SECOND GOLD FIX 10 AM: $1280.20

NY PRICING AT THE EXACT SAME TIME. 1280.00

For comex gold:

DECEMBER/

NUMBER OF NOTICES FILED TODAY FOR DECBER CONTRACT: 2309 NOTICE(S) FOR 230,900 OZ.

TOTAL NOTICES SO FAR: 2309 FOR 230,900 OZ (7.181 TONNES)

For silver:

DECEMBER

3994 NOTICE(S) FILED TODAY FOR

19,970,000 OZ/

Total number of notices filed so far this month: 3994 for 19,970,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $9808/OFFER $9868, DOWN $5 (morning)

BITCOIN : BID $9854 OFFER: $9914 // UP $39 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY ROSE BY A CONSIDERABLE 3254 contracts from 186,272 RISING TO 189,526 DESPITE YESTERDAY’S TRADING WHICH SAW SILVER PLUMMET 32 CENTS AND NOW WELL BELOW THE HUGE $17.25 SILVER RESISTANCE. WE HAD SURPRISINGLY NO COMEX LIQUIDATION. HOWEVER WE WERE ALSO NOTIFIED THAT WE HAD ANOTHER LARGE NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE : 0 DECEMBER EFP’S WERE ISSUED ALONG WITH 5700 EFP’S FOR MARCH FOR A TOTAL ISSUANCE OF 5700 CONTRACTS. I GUESS WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED 820 EFP’S FOR SILVER ISSUED.

RESULT: A GOOD SIZED RISE IN OI COMEX DESPITE THE DROP IN SILVER PRICE OF 32 CENTS. HOWEVER WE HAD ALL OF OUR COMEX LONGS WHICH EXITED OUT OF THE SILVER COMEX TRANSFERRED THEIR OI TO LONDON THROUGH THE EFP ROUTE: FROM THE CME DATA 5700 EFP’S WERE ISSUED TODAY FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. IN ESSENCE THE DEMAND FOR SILVER PHYSICAL INTENSIFIES GREATLY. WE REALLY GAINED 8954 OI CONTRACTS i.e. 5700 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 3254 OI COMEX CONTRACTS.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.949 BILLION TO BE EXACT or 135% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 3994 NOTICE(S) FOR 19,970,000 OZ OF SILVER

In gold, the open interest COLLAPSED AGAIN IN SIMILAR FASHION TO WHICH WE HAVE WITNESSED DURING THE PAST TWO YEARS AS WE APPROACH AN ACTIVE DELIVERY MONTH LIKE THIS ONE, I.E. DECEMBER. THE TOTAL OI FELL BY ANOTHER 14,574 CONTRACTS DOWN TO 489,236 WITH THE HUGE FALL IN PRICE OF GOLD YESTERDAY ($12.30). HOWEVER THE TOTAL NUMBER OF GOLD EFP’S ISSUED TODAY TOTALED ANOTHER 20,559 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 600 CONTRACTS AND FEB SAW THE ISSUANCE OF 19,959 CONTRACTS. (EMERGENCY??) The new OI for the gold complex rests at 490,015. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE WITNESS THE HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE AMOUNT OF GOLD OUNCES STANDING FOR DECEMBER. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO ACCPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND ON TOP OF THAT IT IS TAKING A FURTHER 13 WEEKS TO OBTAIN PHYSICAL FROM THE POINT WHEN FORWARDS BECOME DUE. IN ESSENCE WE HAD A NET GAIN OF 5989 OI CONTRACTS: 14,574 OI CONTRACTS LOST AT THE COMEX OI BUT OF THAT TOTAL 20,559 OI CONTRACTS NAVIGATED OVER TO LONDON. AS I REPORTED YESTERDAY: “THE CME HAS BEEN VERY TARDY IN THEIR REPORTING OF EFP ISSUANCE. MY BET IS THAT WITH TOMORROW’S READING WE WILL HAVE A SURPLUS OF 22,000++ OI NAVIGATING TO LONDON.” I WAS CLOSE: 20,559 MOVED ACROSS. THESE GUYS ARE CROOKS. THEY ARE IMMEDIATELY REMOVING OPEN INTEREST NUMBERS BUT DELAYING RELEASE OF EFP’S

YESTERDAY, WE HAD 13,058 EFP’S ISSUED.

Result: A HUGE SIZED DECREASE IN OI WITH THE HUGE SIZED FALL IN PRICE IN GOLD YESTERDAY ($12.30). WE HAD AN LARGE NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 20,559. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE REACHED THE HUGE DELIVERY MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 20,559 EFP CONTRACTS ISSUED, WE HAD A NET GAIN OPEN INTEREST OF 5989 contracts:

20,359 CONTRACTS MOVE TO LONDON AND 14,574 CONTRACTS REMOVED FROM THE COMEX.

we had: 2309 notice(s) filed upon for 230,900 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Today, no changes in gold inventory at the GLD/

Inventory rests tonight: 839.55 tonnes.

SLV

TODAY WE HAD NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVENTORY RESTS AT 317.130 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver SURPRISINGLY ROSE BY 3254 contracts from 186,272 UP TO 189,526 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE LOSS IN PRICE OF SILVER PRICE (A FALL OF 32 CENTS ). HOWEVER, OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER HUGE 5700 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS). EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAVE NOW REACHED FIRST DAY NOTICE. AS I STATED YESTERDAY: “THIS IS THE SCENE WHERE IN THE PAST WE DID SEE MASSIVE COMEX OI CONTRACTION ALTHOUGH IT WAS MORE PRONOUNCED IN GOLD THAN WITH SILVER.” IF YOU COMPARE GOLD TO SILVER ONE CAN SEE THE DIFFERENCE: GOLD HAS A MUCH GREATER TRANSFER IN EFP’S THAN SILVER. TODAY WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. IF WE ADD THE OI GAIN AT THE COMEX (3528 CONTRACTS) TO THE 5700 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A NET GAIN OF A MASSIVE 8954 OPEN INTEREST CONTRACTS, ON TOP OF THE HUGE AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN DECEMBER (SEE BELOW)

RESULT: A LARGE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 32 CENT FALL IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 5770 EFP’S ISSUED.. TRANSFERRING OUR COMEX LONGS OVER TO LONDON . TOGETHER WITH THE HUGE AMOUNT OF SILVER OUNCES STANDING FOR DECEMBER, DEMAND FOR PHYSICAL SILVER IS STRONG.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed DOWN 20.67 points or .62% /Hang Sang CLOSED DOWN 446.48 pts or 1.51% / The Nikkei closed UP 127.76 POINTS OR 0.57%/Australia’s all ordinaires CLOSED DOWN 0.64%/Chinese yuan (ONSHORE) closed DOWN at 6.6150/Oil DOWN to 57.85 dollars per barrel for WTI and 63.27 for Brent. Stocks in Europe OPENED GREEN . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6150. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.6210 //ONSHORE YUAN WEAKER AGAINST THE DOLLAR/OFF SHORE WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT HAPPY TODAY.(MARKETS VERY WEAK)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

South Korea received good news that its Industrial Production instead of rising 3% this month plunged 5.9% year/year. Their stock market rallied big on the news..

( zerohedge)

ii)This is what scares me the most; an EMP attack:

( Michael Snyder)

iii)Pictures of that North Korean ICBM capable of striking the USA

( zero hedge)

b) REPORT ON JAPAN

3 c CHINA

Chinese and USA economic dialogue goes nowhere and there are no plans to revive talks. Trump is still adamant at the huge trade imbalances between the two countries. Nothing will happen with these stalled talks unless Trump initiates huge tariffs..then things will change.

( zerohedge)

4. EUROPEAN AFFAIRS

It looks like Frankfurt will be the big winner once England leaves the EU. Twenty skyscrapers are now being built to meet with this new “BREXIT demand”

( zerohedge)

ii)Despite an improvement in the unemployment rate, the EU cannot get their inflation expectations up to 2%. It rose from 1.5% to 1.6%

iii)This says it all: the ECB will have a tough time raising rates as sovereigns cannot afford the higher rates as will create a systemic mess:

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)As promised to you, trader Zarrab confirms that Erdogan approved the “secret Iran gold” trade. This violated USA sanctions. The Turkish lira tumbles

( zerohedge)

ii)Saudi Arabia/Yemen

Saudi Arabia intercepts a ballistic missile fired from Yemen onto its shores

(courtesy zero hedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

a deal looks questionable in oil as WTI slumps

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)A terrific presentation from Chris Powell to the Mines and Money Conference in London. He outlines beautifully the massive manipulation in the gold market by central banks and the central bank to the central banks: the BIS

( Chris Powell/GATA)

ii)Chaos in the Bitcoin market: Last night it flash crashed down to $8500 then rebounds back to $9800. The biggest USA exchange Coinbase is off line.

(zerohedge)

iii)Your are going to find the following commentary pretty powerful as Stewart Dougherty describes the manipulation of gold by the elitists and how this allowed the entry of cryptocurrencies into our economy. This will eventually lead to the defeat of the “Deep State”. We are going to provide it to you in two parts.

a must read..

( Stewart Dougherty)

10. USA stories which will influence the price of gold/silver

i)National Chicago manufacturing PMI (soft data) drops from a 6 year high with new orders slowing down

( Chicago PMI/zerohedge)

ii)An extremely important commentary from James Rickards on 3 important dates for the Fed

ii b)PCE up a tick but still well below its mandate:( zerohedge)

iii)Markets are not going to like this: Trump is set to replace Tillerson with Mike Pompeo( zerohedge)

iv)He probably is correct: Bitcoin is the poster boy for an unhinged financial system

Let us head over to the comex:

The total gold comex open interest FELL BY A WHOPPING 14,574 CONTRACTS DOWN to an OI level of 489,236 WITH THE HUGE SIZED FALL IN THE PRICE OF GOLD ($12.30 LOSS WITH RESPECT TO YESTERDAY’S TRADING). IN ACTUAL FACT WE DID NOT HAVE ANY GOLD LIQUIDATION. WE HAD ANOTHER LARGE COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 600 EFPS WERE ISSUED FOR DECEMBER (THE NEED FOR IMMEDIATE GOLD) AND 19,959 EMERGENCY EFP’S WERE ISSUED FOR FEBRUARY FOR A TOTAL OF 20,559 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. THE CONSTANT BANKER RAIDS CONTINUE AS THEY TRY TO GET OUR “MATHEMATICAL PAPER LONGS” IN GOLD TO LIQUIDATE THEIR POSITIONS AT THE COMEX. SO FAR IT HAS NOT SUCCEEDED (AS THEY MORPH INTO LONDON FORWARDS) AND THUS THE CONTINUAL RAID TODAY AS THE CROOKS TRY AND EXTRICATE FIAT DOLLARS FROM OUR STUPID LONG OPTION HOLDERS IN BOTH GOLD AND SILVER. THE CME HAS BEEN VERY TARDY IN THEIR REPORTING OF EFP’S CONTRACTS AFTER A COMEX OI MORPHS INTO AN EFP WHICH WAS THE REASON FOR MY 2ND LETTER TO THE CFTC. AS I STATED YESTERDAY:”LET US SEE IF WE OBTAIN IN EXCESS OF 22,000 EFP’S ISSUED FOR TOMORROW” AND “YOU CAN IMAGINE THE BOOK WORK THAT THESE CROOKS MUST UNDERGO TRYING TO KEEP EVERYTHING STRAIGHT.” I WAS CLOSE: 20,559 MIGRATED OVER TO LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 5989 OI CONTRACTS IN THAT 20,559 LONGS WERE TRANSFERRED AS LONGS TO LONDON AS A FORWARD AND WE LOST 14,574 COMEX CONTRACTS. NET GAIN: 5989 contracts. TOMORROW WE SHOULD SE MORE EFP’S DECLARED AS TRANSFERS.

Result: a HUGE DECREASE IN COMEX OPEN INTEREST WITH THE HUGE SIZED LOSS IN THE PRICE OF GOLD ($12.30.) WE HAD NO REAL GOLD LIQUIDATION. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 5989 OI CONTRACTS…WITH A PROBABLE FURTHER ADDITION IN EFP TOMORROW.

.

We have now entered the active contract month of DECEMBER. The open interest for the front month of December stands at a whopping 11,908 contracts. And thus by definition, the amount of gold initially standing for delivery for December is 1,190,800 oz or 37.03 tonnes. Interestingly enough there is only 20 tonnes of registered or for sale gold at the comex.

January saw its open interest GAIN OF 171 contracts UP to 1919. FEBRUARY saw a gain of 5735 contacts up to 377,828.

We had 2,309 notice(s) filed upon today for 230900 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 329,732

FINAL NUMBERS CONFIRMED FOR FRIDAY: 450,210

comex gold volumes are increasing dramatically

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI SURPRISINGLY ROSE BY 3254 CONTRACTS FROM 186,272 UP TO 189,526 DESPITE YESTERDAY’S 17 CENT LOSS IN PRICE. HOWEVER WE DID HAVE ANOTHER STRONG 5700 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (ZERO FOR DECEMBER) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON.THE TOTAL EFP’S ISSUED: 5700. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD NO LONG SILVER COMEX LIQUIDATION AS DEMAND FOR PHYSICAL SILVER REMAINS STRONG ESPECIALLY AS WE WITNESS A HUGE AMOUNT OF SILVER OUNCES STANDING FOR METAL IN DECEMBER. IT SEEMS THAT ALL OF OUR LOST SILVER COMEX OI CONTRACTS MIGRATED OVER TO THE PHYSICAL HUB OF OUR PRECIOUS METALS, LONDON. ON A NET BASIS WE GAINED 8954 OPEN INTEREST CONTRACTS: 3254 CONTRACTS ADDED THE COMEX WITH THE ADDITION OF 5700 OI CONTRACTS NAVIGATING OVER TO LONDON.

We are now in the big active delivery month of December and here the OI fell by 7126 contracts down to 6508. And thus by definition, the initial amount of silver ounces standing for metal at the comex in December is as follows;

6508 contracts x 5000 oz per contract = 32,540,000 oz. This is huge!!

The January contract month fell by 36 contracts down to 1671. The March contract gained 9883 contracts up to 146,152.

We had 3994 notice(s) filed initially for 19,970,000 oz for the DECEMBER. 2017 contract

INITIAL standings for DECEMBER

Nov 30/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil

oz

|

| No of oz served (contracts) today |

2309 notice(s)

230,900 OZ

|

| No of oz to be served (notices) |

9599 contracts

(959,900 oz)

|

| Total monthly oz gold served (contracts) so far this month |

2309 notices

230,900 oz

7.181 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 0 customer deposit(s):

total customer deposits nil oz

We had 0 customer withdrawal(s)

Total customer withdrawals: nil oz

we had 1 adjustment(s)

Out of HSBC: 259,525.345 oz was adjusted out of the customer account and this landed into the dealer account of HSBC. It seems that HSBC is being called upon to deliver upon our longs

For DECEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2309 contract(s) of which 1039 notices were stopped (received) by j.P. Morgan dealer and 74 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the DECEMBER. contract month, we take the total number of notices filed so far for the month (2309) x 100 oz or 230,900 oz, to which we add the difference between the open interest for the front month of DEC. (11,908 contracts) minus the number of notices served upon today (2309 x 100 oz per contract) equals 1,199,800 oz, the number of ounces standing in this active month of DECEMBER

Thus the INITIAL standings for gold for the DECEMBER contract month:

No of notices served (2309) x 100 oz or ounces + {(11,908)OI for the front month minus the number of notices served upon today (2309) x 100 oz which equals 1,190,800 oz standing in this active delivery month of DECEMBER (37.03 tonnes). INTERESTINGLY THERE IS ONLY 20 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

LAST YEAR WE SAW CONSIDERABLE GOLD LEAVE THE COMEX THROUGH EFP’S. LET US SEE WHAT HAPPENS THROUGHOUT DECEMBER IF CONTRACTS MIGRATE OVER TO LONDON.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR DECEMBER, THE INITIAL GOLD STANDING: 39.038 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 29.791 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 922,639.946 or 28.69 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 8,914,844.991 or 277.28 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 77 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

609,176.378 oz

CNT

|

| Deposits to the Dealer Inventory |

581,723.413

oz

Brinks

I-D

|

| Deposits to the Customer Inventory |

1,109,440.708 oz

Brinks

Malca

|

| No of oz served today (contracts) |

3994 CONTRACT(S)

(19,970,000OZ)

|

| No of oz to be served (notices) |

2,514 contract

(12,570,000 oz)

|

| Total monthly oz silver served (contracts) | 3994 contracts

(19,970,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

today, we had 2 deposit(s) into the dealer account:

i) Into Brinks: 556,757.49 oz

ii) Into International Delaware: 24,975.923

total dealer deposit: n581,723.413 oz

we had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 1 customer withdrawal(s):

i) Out of CNT: 609,176.378 oz

TOTAL CUSTOMER WITHDRAWAL 609,176.378 oz

We had 2 Customer deposit(s):

i) Into Brinks 500,264.33 oz

ii) Into Malca: 609,176.378

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: 1109,440.708 oz

we had 3 adjustment(s)

i) From Brinks: 623,912.910 oz was adjusted out of the customer account and this landed into the dealer account of Brinks

ii) Out of CNT: 1,228,903.808 oz was adjusted out of the customer account and this landed into the dealer account

iii) out of customer: Delaware: 1129.80 oz removed/accounting error.

The total number of notices filed today for the DECEMBER. contract month is represented by 3994 contract(s) FOR 19,970,000 oz. To calculate the number of silver ounces that will stand for delivery in DECEMBER., we take the total number of notices filed for the month so far at 3994 x 5,000 oz = 19,970,0000 oz to which we add the difference between the open interest for the front month of DEC. (6508) and the number of notices served upon today (3994 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the DECEMBER contract month: 3994 (notices served so far)x 5000 oz + OI for front month of DECEMBER(6508) -number of notices served upon today (3994)x 5000 oz equals 32,540,000 oz of silver standing for the DECEMBER contract month. This is EXCELLENT for this active delivery month of November.

IT SURE LOOKS LIKE THE BANKERS WERE READY FOR SILVER DELIVERIES AS REGISTERED OI FOR SILVER IS 53 MILLION OZ. (REGISTERED = FOR SALE SALE BY BANKERS)

WE MUST NOW WAIT TO SEE IF WE ARE GOING TO HAVE CONTINUAL QUEUE JUMPING IN SILVER. THIS STARTED IN EARNEST ON MAY 1/2017 AND CONTINUED IN FULL BLAST EVEN TO TODAY. THIS IS ANOTHER INDICATOR OF PHYSICAL METAL SHORTAGE TOGETHER WITH THE HIGH TRANSFER OF EFP’S TO LONDON AS WELL AS THE MASSIVE AMOUNT OF SILVER STANDING FOR DECEMBER: DEMAND FOR SILVER INTENSIFIES.

ON FIRST DAY NOTICE FOR THE DECEMBER 2016 CONTRACT WE HAD 15.282 MILLION OZ STAND.

THE FINAL STANDING: 19.900 MILLION OZ AS QUEUE JUMPING INTENSIFIED.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 86,725

CONFIRMED VOLUME FOR YESTERDAY: 140,570 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 140,570 CONTRACTS EQUATES TO 703 MILLION OZ OR 100% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 55.852 million

Total number of dealer and customer silver: 235.904 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 2.3 percent to NAV usa funds and Negative 2.3% to NAV for Cdn funds!!!!

Percentage of fund in gold 62.9%

Percentage of fund in silver:36.8%

cash .+.3%( Nov 30/2017)

2. Sprott silver fund (PSLV): NAV FALLS TO -0.42% (Nov 30 /2017)

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.54% to NAV (Nov 30/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -0.42%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.54%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Nov 30/no change in gold inventory at the GLD. Inventory rests at 839.55 tonnes

Nov 29/a withdrawal of 2.66 tonnes at the GLD/Inventory rests at 839.55 tonnes

NOV 28/ no change in gold inventory at the GLD/inventory rests at 842.21 tonnes

Nov 27 Strange!! we gold up by $6.40 today, we had a good sized withdrawal of 1.18 tonnes from the GLD. Here is something that is also strange: we have had exactly 1.18 tonnes of gold withdrawn from the comex on 5 separate occasions in the past 30 days..explanation?

Nov 24/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 22/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 21/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

NOV 20/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 17/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

Nov 16./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.39 TONNES

Nov 15./no change in gold inventory at the GLD/inventory rests at 843.09 tonnes

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

NOV 6/ a tiny withdrawal of .29 tonnes to pay for fees etc/inventory rests at 845.75 tonnes

Nov 3/no change in gold inventory at the GLD/Inventory rests at 846.04 tonnes

NOV 2/STRANGE!!! WE HAD ANOTHER WITHDRAWAL OF 3.55 TONNES FROM THE GLD DESPITE GOLD’S RISE OF $6.60 YESTERDAY AND $1.55 TODAY/INVENTORY RESTS AT 846.04 TONNES

Nov 1/a withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 849.59 tonnes

OCT 31/no change in gold inventory at the GLD/Inventory rests at 850.77 tonnes

Oct 30/STRANGE WITH GOLD UP THESE PAST TWO TRADING DAYS, THE GLD HAS A WITHDRAWAL OF 1.18 TONNES FROM ITS INVENTORY/INVENTORY RESTS AT 850.77 TONES

Oct 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 26./A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 25/NO CHANGE (SO FAR) IN GOLD INVENTORY/INVENTORY RESTS AT 853.13 TONNES

Oct 24./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

OCT 23./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 853.13 TONNES

OCT 20/NO CHANGE IN GOLD INVENTORY AT THE GLD/ INVENTORY REMAINS AT 853.13 TONNES

oCT 19/NO CHANGE/853.13 TONNES

Oct 18 /no change in gold inventory at the GLD/ inventory rests at 853.13 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Nov 30/2017/ Inventory rests tonight at 839.55 tonnes

*IN LAST 283 TRADING DAYS: 101.40 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 218 TRADING DAYS: A NET 55.88 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 24.77 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Nov 30/no changes in silver inventory despite the huge drop in price/inventory rests at 317.130 million oz

Nov 29/no changes in silver inventory at the SLV/Inventory rests at 317.130 million oz/strange!! at drop of 32 cents and no change in inventory?

Nov 28/no change in silver inventory at the SLV/Inventory rests at 317.130 million oz.

Nov 27/NO CHANGE IN SILVER INVENTORY DESPITE A ZERO GAIN IN PRICE /QUITE OPPOSITE TO GOLD WHICH SAW 1.18 TONNES OF GOLD WITHDRAWN DESPITE A RISE IN PRICE OF $6.40

Nov 24/A WITHDRAWAL OF 944,000 OZ OF SILVER FROM THE SLV//INVENTORY RESTS AT 317.130 MILLION OZ

Nov 22/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz.

Nov 21/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

NOV 20/no change in silver inventory at the SLV/inventory rests at 318.074 million oz

Nov 17/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

Nov 16./NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ/

Nov 15./no change in silver inventory at the SLV/inventory rests at 318.074 tones

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

NOV 6/no change in silver inventory at the SLV/Inventory rests at 319.018 million oz/

Nov 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 319.018 MILLION OZ.

NOV 2/A TINY LOSS OF 137,000 OZ BUT THAT WAS TO PAY FOR FEES LIKE INSURANCE AND STORAGE/INVENTORY RESTS AT 319.018 MILLION OZ/

Nov 1/STRANGE! WITH SILVER’S HUGE 48 CENT GAIN WE HAD NO GAIN IN INVENTORY AT THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 31/no change in silver inventory at the SLV/Inventory rests at 319.155 million oz

Oct 30/STRANGE!WITH SILVER UP THESE PAST TWO TRADING DAYS, WE HAD A HUGE WITHDRAWAL OF 1.133 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 27/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ/

Oct 25/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 24/no change in inventory at the SLV/inventory rests at 320.288 million oz/

oCT 23./STRANGE!!WITH SILVER RISING TODAY WE HAD A HUGE WITHDRAWAL OF 1.039 MILLION OZ/inventory rests at 320.288 million oz/

OCT 20NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.327 MILLION OZ

oCT 19/INVENTORY LOWERS TO 321.327 MILLION OZ

Oct 18 no change in silver inventory at the SLV/inventory rest at 322.271 million oz

Nov 30/2017:

Inventory 317.130 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.60%

12 Month MM GOFO

+ 1.84%

30 day trend

end

Major gold/silver trading/commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Goldcore:

Low Cost Gold In The Age Of QE, AI, Trump and War

‘Fear and Loathing In the Age of QE … AI’ is a presentation given at Mining Investment London earlier this week.

Stephen Flood, CEO of GoldCore presentation (28 minutes) was well received at the conference which is a strategic mining and investment conference for leaders in the mining and investment sectors, bringing together attendees from 20 countries.

Key topics in the video:

– A bullion dealers view on ‘What will drive the markets in 2018?’

– QE, inflation, Fed rates, debt bomb, China, populism, EU cohesion, Brexit, digital disruption, cashless society, demographics, Trump (war), Artificial intelligence (AI)

– Solve global debt crisis with humongous amount of debt!?

– Inflation – U.S. health insurance has increased 13% per annum since

– How Artificial Intelligence (AI) is the “big one,” likely be massively disruptive

– Trump: ‘No respect, no capacity, no strategy’

– Brexit and EU – ‘Poor outlook’ for Europe and euro doomed?

– “We are getting older and getting fatter” … “less useful & less fair”

– “We live in uncertain times … there is no map”

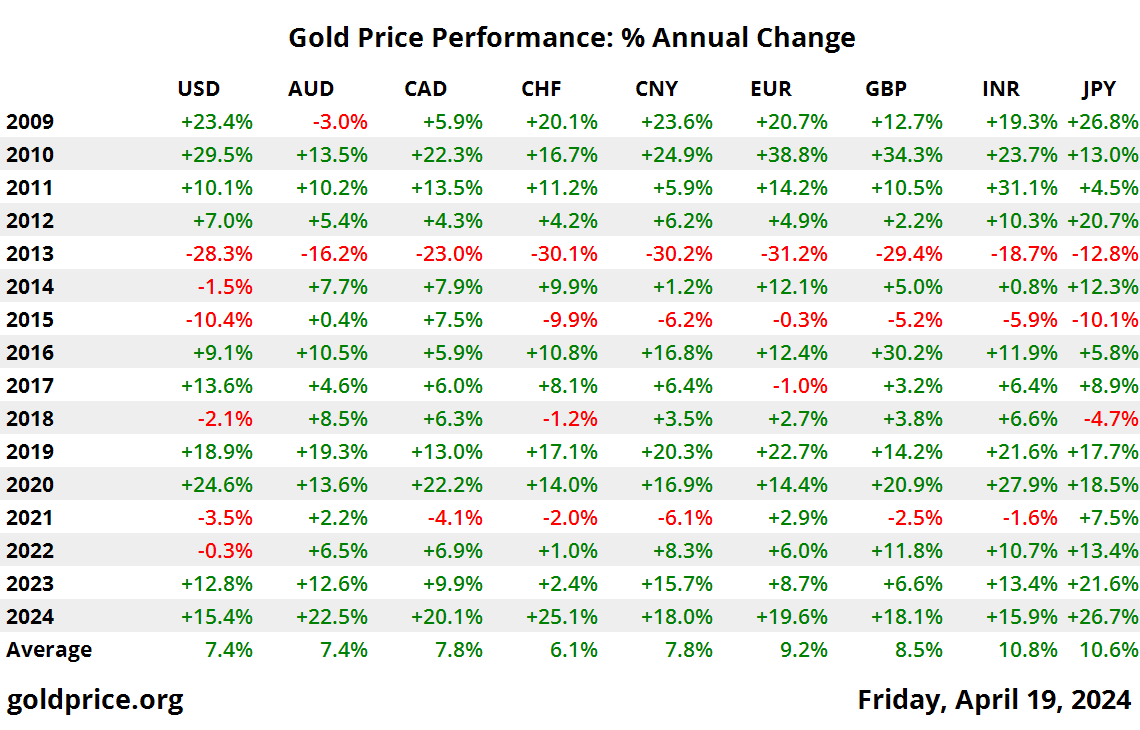

– Gold’s excellent c.10% per annum performance over long term (see table)

– Low cost gold = Low “utility” gold

– Avoid “single point of failure”

‘Fear and Loathing In the Age of QE … AI’ can be watched on Youtube here

Related Videos

GoldNomics – Cash or Gold Bullion?

Why Silver Bullion Is Set To Soar – GoldCore Interview

Gold Bullion Stored In Singapore Is Safest – Marc Faber

Russia Seen More Likely to Sell Dollar Rather Than Gold

Talking Gold with CNN’s Richard Quest

News and Commentary

Gold holds near one-week low as dollar firms (Reuters.com)

Tech Stock Slide Spreads to Asia; Korean Won Drops (Bloomberg.com)

U.S. Stocks Dragged Down by Tech Rout; Bonds Fall (Bloomberg.com)

Goldman Says the Bitcoin Haters Just Don’t Get It (Bloomberg.com)

Fidelity restores online account access after resolving technical issue (CNBC.com)

Source: Bloomberg

Goldman Warns That Market Valuations Are at Their Highest Since 1900 (Bloomberg.com)

Bitcoin Tops $11,000 – Bundesbank Sees No Bubble, Stiglitz Says “Should Be Outlawed” (ZeroHedge.com)

Own Bitcoin – But Invest No More Than You Can Afford To Lose (StansBerryChurcHouse.com)

What to do if you’ve missed out on the bitcoin super-bubble (MoneyWeek.com)

Gold Slammed On Massive Volume To Key Technical Support On GDP Beat (ZeroHedge.com)

Gold Prices (LBMA AM)

30 Nov: USD 1,282.15, GBP 952.64 & EUR 1,084.06 per ounce

29 Nov: USD 1,294.85, GBP 965.70 & EUR 1,092.46 per ounce

28 Nov: USD 1,293.90, GBP 972.75 & EUR 1,088.95 per ounce

27 Nov: USD 1,294.70, GBP 969.73 & EUR 1,084.83 per ounce

24 Nov: USD 1,289.15, GBP 967.89 & EUR 1,086.37 per ounce

23 Nov: USD 1,290.15, GBP 969.93 & EUR 1,089.40 per ounce

22 Nov: USD 1,283.95, GBP 969.25 & EUR 1,092.51 per ounce

Silver Prices (LBMA)

30 Nov: USD 16.57, GBP 12.32 & EUR 14.00 per ounce

29 Nov: USD 16.90, GBP 12.60 & EUR 14.26 per ounce

28 Nov: USD 17.07, GBP 12.84 & EUR 14.36 per ounce

27 Nov: USD 17.10, GBP 12.81 & EUR 14.32 per ounce

24 Nov: USD 17.05, GBP 12.80 & EUR 14.38 per ounce

23 Nov: USD 17.10, GBP 12.84 & EUR 14.43 per ounce

22 Nov: USD 16.97, GBP 12.81 & EUR 14.44 per ounce

Recent Market Updates

– Own Gold Bullion To “Support National Security” – Russian Central Bank

– Bitcoin $10,000 – Huge Volatility of Cryptocurrencies and Risky Fiat Making Gold Attractive

– Financial Advice from Dr Wayne Dyer

– Buy Gold As Fed Shows Uncertainty And Concern Over Financial ‘Imbalances’

– Brexit Budget – Grim Outlook As UK Economy Downgraded

– Geopolitical Risk Highest “In Four Decades” – Gold Demand in Germany and Globally to Remain Robust

– Gold Versus Bitcoin: The Pro-Gold Argument Takes Shape

– Money and Markets Infographic Shows Silver Most Undervalued Asset

– Is New Fed Chief A “Swamp Critter Extraordinaire”?

– Deepening Crisis In Hyper-inflationary Venezuela and Zimbabwe

– UK Debt Crisis Is Here – Consumer Spending, Employment and Sterling Fall While Inflation Takes Off

– Protect Your Savings With Gold: ECB Propose End To Deposit Protection

– Internet Shutdowns Show Physical Gold Is Ultimate Protection

end

GOLD TRADING TODAY:

Makes no sense!! with the dollar being pummeled why did gold falter. Simple: criminal banker manipulation.

(courtesy zerohedge)

Gold Tumbles Below Key Technical Support As 5Y Yields Spike To Six-Year Highs

For the second day in a row, precious metals are being pounded as gold joins silver back below its 200-day moving-average…

Knocking gold back to 3-week lows…

All of which is odd given the chaos in the dollar… Two days of collapse in gold as the dollar goes nowhere…

And Treasury yields are surging – woith 5Y back at its highest since April 2011…

end

A terrific presentation from Chris Powell to the Mines and Money Conference in London. He outlines beautifully the massive manipulation in the gold market by central banks and the central bank to the central banks: the BIS

(courtesy Chris Powell/GATA)

Chris Powell: London update on gold market manipulation

Submitted by cpowell on Wed, 2017-11-29 13:28. Section: Documentation

Remarks by Chris Powell

Secretary/Treasurer, Gold Anti-Trust Action Committee Inc.

Mines and Money London

Business Design Center, London

Wednesday, November 29, 2017

* * *

The slides for this presentation are posted here:

http://gata.org/files/GATA-Powell-Mines&MoneyLondonSlides-11-29-2017.pdf

* * *

SLIDE 1

All you really need to know about gold could have been surmised from a story on the front page of The Wall Street Journal on August 10:

http://www.gata.org/node/17562

SLIDE 2

In that story the newspaper quoted four experts on the gold market, all of them associates of the Gold Anti-Trust Action Committee and all of them introduced to the newspaper’s reporter by me.

SLIDE 3

Those four experts — gold researcher Ronan Manly, Sprott Asset Management’s John Embry, GoldMoney founder James Turk, and futures market analyst James McShirley — accused the Federal Reserve of being involved with the suppression of the gold price through the surreptitious lending and swapping of central bank gold reserves.

The Wall Street Journal story was a triumph for GATA, even though the Journal declined to mention GATA by name. (The reporter told GATA Chairman Bill Murphy that the newspaper just ran out of space.)

But the story would have been a much greater triumph for us – indeed, it would have been a triumph for free markets — if the newspaper had not decided, in reporting these complaints about surreptitious government intervention in the gold market, to violate the first rule of journalism. That’s the rule about getting both sides of a story.

The Journal reported: “Some gold bugs — investors bullish on the yellow metal — think the Fed secretly lends it out to suppress prices, partly to protect the dollar’s value. In theory, the Fed can feed gold into the market through swaps with other countries.”

So where were the Journal’s questions about this for the Fed and the Treasury Department? Are the Fed and the Treasury Department involved in keeping the gold price down through surreptitious interventions, or are they not involved?

But the Journal never asked such questions, even though for a year and a half, as I provided the Journal’s reporter with the documents of these interventions, I repeatedly pressed her to put the questions to the Fed and Treasury Department. I even provided the Journal’s reporter with a video showing New York Federal Reserve Bank President William Dudley refusing to answer a question about gold swaps during his appearance at the Virginia Military Institute on March 31, 2016:

http://www.gata.org/node/16341

https://www.youtube.com/watch?v=p0JYoJ_rKxQ

Ordinarily news organizations are most interested in questions that high government officials refuse to answer. But mainstream financial news reporters are not interested in questions about secret government intervention in the gold market and secret interventions in markets generally. No, such questions are too sensitive, considered matters of national security.

The best that mainstream financial news organizations can do is just to acknowledge the questions sometimes. Mainstream financial news organizations can never pursue the answers, no matter how easy it would be to do so.

Unfortunately most gold market analysts themselves will not pursue these questions either — at least not yet. GATA will continue working on them.

But market manipulation issues have kept coming close to the surface during the last year.

Last month GATA consultant Robert Lambourne, who studies the gold activity of the Bank for International Settlements, reported that gold swaps undertaken by the BIS have exploded from zero a year and a half ago to about 570 tonnes as of last month:

http://www.gata.org/node/17790

The increase in the BIS’ gold swaps is revealed in the footnotes of the bank’s latest annual report and its statement of account for this October.

This page is taken from the BIS annual report issued in June, covering the year ending March 31. It acknowledges 438 tonnes of gold swaps:

SLIDE 4

This page, from the BIS’ October statement of account, shows that gold loans have risen substantially since March.

SLIDE 5

Lambourne says there is reason to believe that the swaps undertaken by the BIS in the last year and a half were undertaken just as the gold price showed signs of breaking upward.

The BIS is the primary gold broker for its central bank members and does all sorts of gold business for them. This business is acknowledged in the bowels of the BIS’ internet site:

http://www.bis.org/banking/finserv.htm

SLIDE 6

Contrary to what some people would have you believe, central bank gold reserves don’t just sit quietly in their vaults all day. They are mobilized every day, often with the help of the BIS, not just through sales and leases but also through issuance of the various kinds of derivatives listed on the screen.

Indeed, when the BIS thinks that only its central bank members and potential members are listening, it even advertises that its services include secret interventions in the gold market.

This advertisement was part of the BIS presentation that was made to potential central bank members during a conference at BIS headquarters in Basel, Switzerland, in June 2008.

http://www.gata.org/node/11012

SLIDE 7

What exactly is the BIS doing in the gold market, for whom is it making its transactions, and what are their objectives?

Two weeks ago I put that question to the bank’s press office. I sent the bank’s press office Lambourne’s analysis of the bank’s gold transactions and asked if he was right or wrong and, if he was wrong, how so. I added: “Could you also please tell me the BIS’ purpose and objectives with these gold swaps and with the bank’s involvement in the gold and gold derivatives markets generally?”

The following day I received a curt and unsigned reply from the bank. The press office wrote: “We do not comment on specific accounts / holdings of central banks or of the BIS. Please see our latest annual report for details on gold. Further information can be gleaned from central banks directly.”

Ironically, on the same day the BIS’ press office told me to drop dead, the bank’s research director, Hyun Song Shin, attended a conference at the European Central Bank in Frankfurt, Germany, giving a speech titled “Can Central Banks Talk Too Much?”:

http://www.gata.org/node/17802

SLIDE 8

Shin told the ECB conference: “If central banks talk more to influence market prices, they should listen less to the signals emanating from those same markets. Otherwise, they could find themselves in an echo chamber of their own making, acting on market signals that are echoes of their own pronouncements.

“On the other hand,” Shin continued, “talking less is hardly a viable option. Central bank actions matter too much for the lives of ordinary people to turn the clock back to an era when silence was golden. Accountability demands that central banks make clear the basis for their actions.”

Accountability in central banking? That’s a laugh, especially in regard to gold.

All you need to know about the supposed accountability of central banking is conveyed by the secret March 1999 report of the staff of the International Monetary Fund to the fund’s executive board.

http://www.gata.org/node/12016

SLIDE 9

The report told the board that central banks conceal their gold swaps and leases to facilitate their surreptitious interventions in the gold and currency markets. That is, central banks conceal their gold swaps and leases to defeat accountability.

The BIS is a powerful organization but most of its power comes from the refusal of mainstream financial news organizations and gold market analysts to ask the bank to explain what it does in the gold market and then to report the bank’s refusal to explain.

Confirmations of gold and silver market rigging below the central bank level have poured in during the last year.

In December last year Deutsche Bank agreed to pay $60 million to settle a class-action anti-trust lawsuit’s complaints that it had manipulated the gold market. In October last year Deutsche Bank agreed to pay another $38 million to settle a similar complaint that it had manipulated the silver market. Perhaps more importantly, Deutsche Bank agreed to provide the plaintiffs with evidence against the banks it admitted conspiring with:

http://www.gata.org/node/16964

SLIDE 10

Unfortunately the discovery and deposition procedures in the class-action anti-trust lawsuits against Deutsche Bank have been put on hold at the request of the U.S. Justice Department, which purports to be undertaking its own investigation of the bank. More likely the Justice Department is just trying to delay exposure of the U.S. government’s own involvement with the market rigging.

http://www.gata.org/node/17157

In June a former metals trader for Deutsche Bank pleaded guilty in federal court in Chicago to using “spoofing” techniques to manipulate the futures markets for gold, silver, platinum, and palladium. The former trader for Deutsche Bank also admitted front-running customer orders.

http://www.gata.org/node/17407

In May gold researcher Ronan Manly, reviewing records at the Bank of England, discovered minutes showing that Western central bankers conspired in the early 1980s to suppress the gold price in exchange for continued cheap oil exports from the Middle East. These Bank of England minutes are confirmation of the long-held belief in gold circles that gold price suppression originates in part from the desire of Middle Eastern oil exporters to be able to exchange their oil for better money than U.S. dollars, money that can’t be devalued so easily:

http://www.gata.org/node/17386

SLIDE 11

Reviewing those Bank of England records, Manly also discovered that Western central banks conspired in 1979 to create a second London gold pool to control the metal’s price:

http://www.gata.org/node/17372

SLIDE 12

In May GoldMoney Vice President John Butler discovered still another U.S. State Department memorandum detailing U.S. government policy to drive gold out of the world financial system in favor of the U.S. dollar and the Special Drawing Rights issued by the International Monetary Fund, which then was under U.S. government control.

http://www.gata.org/node/17361

SLIDE 13

The memo was written in 1974 by Deputy Assistant Secretary of State Sidney Weintraub for Secretary of State Henry Kissinger and the Treasury Department’s undersecretary for monetary affairs, Paul Volcker, who of course went on to become chairman of the Federal Reserve.

Weintraub wrote: “To encourage and facilitate the eventual demonetization of gold, our position is to keep the present gold price, maintain the present Bretton Woods agreement ban against official gold purchases at above the official price, and encourage the gradual disposition of monetary gold through sales in the private market.”

In April the British Broadcasting Co.’s “Panorama” program obtained and broadcast a recording of a conversation between two officials of Barclays bank that implicated the Bank of England in the infamous rigging of the London Interbank Offered Rate, the LIBOR interest rate.

http://www.gata.org/node/17303

SLIDE 14

In the recording a senior Barclays manager, Mark Dearlove, instructs the bank’s LIBOR rate submitter, Peter Johnson, to lower the rates Barclays is submitting.

Dearlove tells Johnson: “We’ve had some very serious pressure from the UK government and the Bank of England about pushing our LIBORs lower.”

Johnson objects, saying that this would mean breaking the rules for setting LIBOR, which required Barclays to submit rates based only on the cost of borrowing cash. Johnson asks: “So I’ll push them below a realistic level of where I think I can get money?”

His boss Dearlove replies: “We’ve got the Bank of England, all sorts of people involved in the whole thing. … I am as reluctant as you are. … These guys have just turned around and said just do it.”

In January the TF Metals Report discovered in the Wikileaks archive of State Department diplomatic cables a cable sent in December 1974 from the U.S. embassy in London to the State Department in Washington. The cable shows that the U.S. government had just gotten assurances from London bullion banks that the imminent creation of a gold futures market in the United States would cause so much volatility in the gold price that ordinary investors would be driven out of gold:

http://www.gata.org/node/17081

SLIDE 15

In GATA’s view there are four crucial questions about the gold price. I urge you to put these questions to those who speak about gold at this conference. I also urge you to put them to the executives of companies that mine the monetary metals.

SLIDE 16

1) Are governments and central banks active in the monetary metals markets or not?

2) Are the documents compiled by GATA from government archives and other official sources asserting such activity genuine or forgeries?

3) If governments and central banks are active in the monetary metals markets, is it just for fun or is it for policy purposes?

SLIDE 17

4) If such activity by governments and central banks is for policy purposes, do those purposes involve the traditional objectives of defeating an independent world currency that competes with government currencies and interferes with government control of interest rates and, indeed, interferes with control of the entire economy and society itself?

In GATA’s view there are good arguments for investing in the monetary metals and the companies that mine them. But investors need to know what they’re getting into, what they’re up against, and what they can do to improve the prospects for their investments and for the restoration of free markets.

Remember, as author and fund manager Jim Rickards said on CNBC a few years ago: “When you own gold you’re fighting every central bank in the world.”

So if we want free and transparent markets and limited and accountable government, we just have to beat the bastards.

The documents and events I have reviewed today are mainly those that have been unearthed or developed during the past year. There is much more documentation of the central bank gold price suppression scheme at GATA’s internet site:

http://www.gata.org/taxonomy/term/21

A good summary of the scheme is posted in “The Basics” section of the GATA site:

http://www.gata.org/node/14839

You can find GATA on the internet at GATA.org, where you can sign up for our daily e-mail dispatches and, if you’re inclined to help us, make contributions that are federally tax-deductible in the United States. We really could use your help. Of course I’ll be glad to hear from you by e-mail at CPowell@GATA.org.

SLIDE 18

Thanks for your kind attention.

end

Chaos in the Bitcoin market: Last night it flash crashed down to $8500 then rebounds back to $9800. The biggest USA exchange Coinbase is off line.

Bitcoin Flash-Crashes To $8,500, Then Rebounds As Biggest US Exchange Breaks

Chaos: Bitcoin bounced back $1500 from the lows, rising as high as $10,400 from nearly $2000 lower just an hour earlier, before trading in a range around $10,000.

* * *

Update: The crash is continuing with Bitcoin now collapsing below $9000…

Ethereum and Litecoin are also under pressure.

Numerous exchanges and trading platforms are suffering outages.

* * *

Having soared in the last 24-48 hours to as high as $11,395 this moring, Bitcoin has just tumbled back below $10,000…

While a notable pump and dump, this drop is a mere 13% (following an 8% drop overnight after initially breaking $10,000).

There is some chatter than Bitcoin flash-crashed to as low as $9130 on Coinbase…

Remember on November 8th to 10th, Bitcoin crashed 30% amid rumors of its death.

image courtesy of CoinTelegraph

And as we noted previously, Bitcoin crashes at least once every quarter…

Amid a record day for traffic, Coinbase website is down once again…

end

Your are going to find the following commentary pretty powerful as Stewart Dougherty describes the manipulation of gold by the elitists and how this allowed the entry of cryptocurrencies into our economy. This will eventually lead to the defeat of the “Deep State”. We are going to provide it to you in two parts.

a must read..

(courtesy Stewart Dougherty)

The War on Gold Intensifies: It Betrays The Elitists’ Panic And Coming Defeat – Part 1

IRD is honored to present another guest post from Stewart Dougherty

Dictatorship (noun): Definition #3: absolute power or authority (Websters);

Def. #2: absolute, imperious or overbearing power or control (Random House);

Def. #3: Absolute or despotic control or power (American Heritage);

Def. #3: Absolute or supreme power or authority (Collins English Dictionary);

Def. #1: A type of government where absolute sovereignty is allotted

to an individual or small clique (Wikipedia).

“If you know the enemy and know yourself, you need not fear the result of a hundred battles. If you know yourself but not the enemy, for every victory gained, you will also suffer a defeat. If you know neither the enemy nor yourself, you will succumb in every battle.” Sun Tzu, The Art of War

In recent weeks, the War on Gold, which is a subset of the broader War on Human Freedom, has sharply intensified, with massive, multi-billion dollar naked short price raids now being launched on a weekly and even daily basis by the criminal, state-sponsored price manipulators. This escalation proves the supreme importance to the Deep State financial elite of the maintenance of their gold price dictatorship, which is a vital component of their long term, systemic campaign of financial plunder.

The elitists have no problems whatsoever with stratospheric stock and bond prices; 5,000 year low interest rates; $450 million Da Vinci’s; $250 million private homes; $50,000,000 annual salaries for circus masters, whose role in keeping the masses distracted and dumb is vital; $1.9 million Aston Martins; $100,000 Air Jordan sneakers, or any of the other prices that have now gone into outer space.

But there is one thing they will not accept: an honest, free market price for gold. Because while all debauchery under the sun is permitted and encouraged in the Castle of Fraud and Corruption they have constructed and in which they revel, one thing is strictly prohibited: the utterance of truth. Being monetary truth when free to speak, gold is their deadliest enemy. Therefore, it is silenced, in the same way truth tellers are silenced in all dictatorships.

The vast majority of people, aside from a small, enlightened minority who refuse to poison their minds by ingesting mainstream media (MSM) fake news, propaganda and brainwashing, do not yet realize what they are up against in the wars that have been declared against them, and are therefore at serious risk. For those who wish to survive the wars, there has never been a greater need to know the enemy and know yourself.

As the gold price war becomes manic, so has the MSM’s anti-gold propaganda campaign, with their attempts to smear gold now a clinical obsession.

In a prime example of their over-the-top anti-gold propaganda, on 10 November 2017, the Financial Times, a long-time Deep State bullhorn and puppet, ran an article entitled, “Gold is the new cocaine for money launderers.” In this screed, the author beat the dead horse of the NTR Metals gold import scheme. This operation, whose total dollar yield was an infinitesimal fraction of the massive sums stolen by the financial Deep Statists in their forty year gold price manipulation crime, was already the subject of an over-dramatized Bloomberg Businessweek propaganda piece published on 9 March 2017, entitled “How to Become an International Gold Smuggler.” Apparently, the MSM is running so short of new material with which to try to demonize gold, that it is now forced to recycle old, stale non-stories to keep the smear machine going.

In the article, the MSM propagandist states such things as: 2017 has seen, according to his one time Goldman Sachs source, a “dramatic crash in [physical gold coin] demand,” that interest in gold coins is linked to “political conservatism, or anarcho-libertarianism” and “end of the world right wing sentiments,” that gold has been implicated in a “conspiracy to commit money laundering,” that gold is “financed by people in the narcotics trade,” that it comes from “illegal mines and drug dealers in Peru, Bolivia and Ecuador,” that “the federal authorities assume the NTR Metals [case] represented only a fraction of illegally sourced and financed gold,” that therefore the US attorney is broadly investigating the gold industry, that gold is “produced by exploited workers,” that “crude [gold] extraction techniques create serious and lasting environmental damage,” that gold plays an important part in “tax evasion,” that it is related to American gun sales, which the author abhors; that “drug dealers [use] gold imports as a way of laundering their proceeds,” and that “they came to realize that illegal gold [is] an intrinsically better business” than drug dealing; to name but a few of the aspersions cast against gold in the short article. As we can see, when it comes to their smear jobs, the MSM flings at the wall all the mud it can fit in its hands, hoping that some of it might stick.

As is always the case with the MSM’s consistently negative, biased and dishonest reporting on gold, no mention was made in the article of the Deep State financial elite’s criminal gold price manipulation fraud that has been perpetrated non-stop for nearly forty years and that has resulted in a massive, $1,000,000,000,000.00+ theft from its victims. This is because the MSM is the Deep State’s in-house public relations agency, whose job is to whitewash the elitists’ crimes, no matter how egregious they are.

But buried in the article was an important clue that the Deep Statists are concerned they are losing the War on Gold, which we will further explore later in the article. It turns out that the Deep Statists’ paranoia about and rage toward gold might be entirely justified, because more than ever in the past 37 years, gold is poised to tell the world what it knows, and this will absolutely annihilate them.

Many people are completely baffled as to why, with so many serious fiscal, financial, monetary, economic, social, and geopolitical problems in the world, the Deep Statists remain so mono-maniacally fixated on demagogically denigrating gold and controlling its price.

The answer is that the Deep Statists cannot, under any circumstances, allow the price of gold to replicate the surging price of Bitcoin and other cryptocurrencies. If the gold price genie were to get out of the bottle, becoming international news in the process no matter how much the MSM might try to suppress it, it would spur a gold buying stampede that would cause a flood of money to pour out of bank accounts and into physical precious metals. $325+ billion worldwide now resides in cryptocurrencies, a highly specialized and complex product class. In the right set of circumstances, many multiples of that amount could incrementally flow into gold, a simple product that has been innately understood for millennia by human beings all over the globe.

Already fragile, the banking system cannot withstand a large scale withdrawal of funds. Being finite and in short supply, incremental demand for physical gold would result in immediate and sustained price gains, creating a positive feedback loop in the market place. As people watched the price go up, more and more of them would want to jump on the band wagon and participate in the gains, which is exactly what has happened in the cryptocurrency market.

If interest in gold goes mainstream, then basic supply fundamentals indicate the price would have to rise by thousands of dollars per ounce to even approach what might be considered overbought and/or bubble territory. Which is exactly what has happened to Bitcoin, whose price has exploded to over $10,500 as of today, 29 November 2017.

In the United States, the latest Federal Reserve Board tally of Household and Non-profit Organization (much of which is private) wealth totals $96.2 trillion. If a miniature, 1% sliver of this amount, $962 billion, attempted to find its way into the physical gold market, it would represent incremental demand, at $1,300 per ounce, of 740 million ounces. Not even a small fraction of this incremental demand would be available in the physical gold market at this time, given that it already operates at a supply / demand equilibrium. The gold price would have to surge in order to flush out supplies from current gold owners, whose hands have proven to be, and are likely to remain strong. We believe it would take years for incremental demand of this magnitude to be filled, even at much higher prices. Please keep in mind that this example relates to the United States, alone; there are additional, vast stores of private wealth all over the world, all of which would almost certainly be activated in unison by a run to gold.

With the right spark, the same viral, Social Media-enhanced demand that has come to cryptocurrencies could come to gold. The Deep Statists know it, and the ghostly whites of their eyes now glow eerily and blinkingly across the dark battlefield of Liberty, in the senseless war they provoked and are going to lose.

While there are now hundreds of cryptocurrencies, physical gold is physical gold, and cannot be replicated or conjured out of nothing. There will be no endless stream of new ICOs for genuine, physical gold, because gold is what it is and always will be. This means that funds flowing into gold will be forced into the one and only physical gold market that already exhibits tight, inflexible supply. This further means that the upward price pressure on gold could become volcanic if a run starts.

A steadily increasing number of people will want to get in on the “new Bitcoin,” a bizarre paradox given that gold is as old as time, and will soon realize that gold possesses virtues Bitcoin does not, given that it is real, not digital and abstract; that owners can personally possess and store it in physical form; that it will survive any kind of electric grid or Internet disruption that might occur; that it cannot ever be hacked; that it is the epitome of private, quiet wealth; that it is actually quite beautiful to behold; and that it was not and cannot be made by man, only by God, who does not appear to have any interest in making any more of it.

To date, in order to prevent a surge in physical gold demand from happening, the Deep Statists have created various forms of transparently fake gold, such as electronic gold futures, options and non-auditable ETFs and EFPs. These fake gold products have siphoned funds away from real, physical gold, which cannot be created out of the nothing the way the imposter electronic gold products can be. Increasingly, people are learning that there are no substitutes for physical gold.

More, we find it interesting that while there have been certain highly publicized condemnations of cryptocurrencies, such as J. P. Morgan Chase CEO Jamie Dimon’s comment that Bitcoin is a “fraud,” the financial authorities in the west have done little to nothing to shut down the crypto market. They seem to be just fine with $10,500 Bitcoin, but will stop at nothing to prevent $1,300 gold. Today’s (29 November) market action is a case in point.

The reason is that monetary elitists fully approve of cryptocurrencies, because this the new form of fiat currency the western banks intend to issue. Mass adoption of cryptocurrencies is the necessary forerunner to the elimination of cash, a well-known and important agenda for the financial elite. By issuing their own cryptocurrencies, and/or co-opting Bitcoin and other private cryptos via regulation and edict, central bankers can continue their tradition of controlling the money supply. A population that has learned the value of owning and become adept at trading physical gold would prevent central banks from continuing to use fiat currencies as economic, political and societal control mechanisms. It should be no surprise that they loathe gold so much; in its honesty and integrity, it is the exact antithesis of everything they stand for, are, and do.

Some people argue, “Even if people run to gold, their funds will still remain within the banking system, so the bankers aren’t worried about this happening.” In our opinion, this is wrong.

Fiat currency used to buy precious metals will move from personal and business bank accounts, to gold dealer accounts, to gold wholesaler accounts; and then to a variety of sovereign mint, gold precious metals refiner, gold miner and other gold supplier accounts, a large percentage of which are international.

A bank that hosts a deposit account used to purchase physical gold has no assurance whatsoever that the buyer’s funds will transfer into another personal or business account managed by it. In all likelihood, the funds will disappear from the host bank and not return. Ultimately, the likelihood is also high that a portion of the funds, potentially significant, will disappear from the country’s banking system altogether, given the global nature of gold mining, refining, minting and fabrication. Therefore, bankers regard a run to gold as a severe, direct threat to them, which is why they do everything in their power to discredit it and crush its price. They are attempting to prevent a run on their banks.

Over the past several years, the Deep Statists have gone to extraordinary lengths to internationally legalize bank “bail-ins.” They did not do this casually, by accident, or for fun; they did it because they know that when the system fails, a time-bomb guaranteed to detonate given the system’s very design, they will be able to make an unprecedented fortune by expropriating customers’ deposits via the elaborate bail-in mechanism they have engineered. They will use the phony pretext of “rescuing” and “resetting” the financial system for the public good to justify this action. If, before they spring the bail-in trap, depositors have already withdrawn their funds to purchase physical precious metals held outside the banking system, those funds will no longer be available for bail-in looting. The bankers cannot steal bank balances that have disappeared.

The cryptocurrency phenomenon, now an international sensation, has stunned them into the awareness that people all over the world have a deep, abiding, instinctive desire to own honest money of limited supply that will serve as a reliable store of value, and that cannot be hyper-inflated into oblivion for the private gain of plunderers and profiteers, the chief problem with corrupt, endlessly counterfeited fiat currencies controlled by self-interested, opportunistic, predatory central bankers and their controllers, the Deep State financial elite.

Due to the length of this article, we have divided it into two parts. This ends Part 1. In Part 2, which is already written and will be released in a few days, we will share with you important clues indicating the Deep State’s concerns about losing the War on Gold, despite the unprecedented intensification of their attacks. We will also discuss how the United States Federal Reserve is outright warning that new threats to financial and economic stability are on the horizon.

Stewart Dougherty is the creator of Inferential Analytics, a forecasting method that applies to events proprietary, time-tested principles of human instinct, desire and action. In his view, forecasting methods not fundamentally based upon principles of human action are unlikely to be reliable over time. He is a graduate of Tufts University (BA) and Harvard Business School (MBA). He developed expertise in strategic analysis and planning during a 35+ year business career, has traveled to and conducted research in over 25 countries and has refined Inferential Analytics into a reliable predictive instrument over a period of 17+ years

END

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN AT 6.6150/shanghai bourse CLOSED DOWN AT 20.67 POINTS .62% / HANG SANG CLOSED DOWN 446.48 POINTS OR 1.51%

2. Nikkei closed UP 127.76 POINTS OR 0.57% /USA: YEN RISES TO 112.33

3. Europe stocks OPENED GREEN /USA dollar index RISES TO 93.39/Euro FALLS TO 1.1839

3b Japan 10 year bond yield: RISES TO . +.039/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.33/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 57.85 and Brent: 63.27

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.376%/Italian 10 yr bond yield UP to 1.771% /SPAIN 10 YR BOND YIELD UP TO 1.474%

3j Greek 10 year bond yield RISES TO : 5.46???

3k Gold at $1281.30 silver at:16.51: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 19/100 in roubles/dollar) 58.48

3m oil into the 57 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED DEVALUATION SOUTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.33 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9871 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1682 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.371%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.382% early this morning. Thirty year rate at 2.823% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Dow Hits Record 24,000, Europe Jumps As Euphoria Returns After Tech Rout

Despite a Wednesday dive in high-flying U.S. tech stocks on worries their boom may have peaked following a MS downgrade, which pressured Asian stocks leading to a slide in Hong Kong and South Korean share, on Thursday morning the dip buyers have emerged and both European stocks and US equity futures are once again solidly in the green as yesterday’s tech selloff is quickly forgotten. Confirming that algos have moved on, US stock-index futures climbed briskly (ES +0.3%), and Dow futures were above 24,000 with Europe green across the board as signs of progress on the tax reform plan led some investors to shift to positions that are seen benefiting from lower corporate tax.

Following a lackluster Wednesday session, and some mixed results in Asia, Europe’s Stoxx 600 has advancds to session’s high, up 0.6%, as defensive sectors including telecommunications, utilities and real estate outperform more cyclical sectors like construction, financial services and technology, with the FTSE 100 once again lagging (-0.3%) as the firmer GBP continues to hamper the index. Despite opening relatively flat, European bourses have drifted higher amid the declines seen in EUR with little else in the way of fresh fundamental catalysts to guide price action. All sectors trade in positive territory with the exception of energy names in the wake of yesterday’s sell-off in oil prices.

Germany’s Dax and France’s CAC 40 both inched up for a third day, though London’s FTSE was back in the red as hopes of a breakthrough in Brexit negotiations pushed the pound higher again.

Earlier, Hong Kong and South Korean-listed shares tumbled, while Japanese stocks gained. Asia stock markets were mostly negative as the tech-sell off on Wall St. dampened sentiment in the region and overshadowed better than expected Chinese PMI data. ASX 200 (-0.7%) was pressured by its largest weighted Financial sector after the announcement of a royal commission inquiry into the industry, while Nikkei 225 (+0.6%) recovered from opening losses as JPY weakness provided support. Elsewhere, KOSPI (-1.5%) weakened as the BoK delivered a widely anticipated 25bps rate hike and Chinese markets were also subdued with the Hang Seng (-1.5%) reeling on tech weakness, although losses in the Shanghai Comp. (-0.6%) were somewhat stemmed by encouraging Chinese Official PMI data.

In global FX and macro, the Bloomberg Dollar Spot Index was higher a fourth day, its longest winning run since August, before key U.S. data releases including personal income, spending, deflator, initial claims, and Chicago PMI; the pound held on to Asia session gains as Brexit talks seemed on track to soon enter phase 2, the hardest part of the negotiations. As noted earlier, the euro reversed gains after inflation in the currency bloc missed estimates, while the 10-year bund yield fell from a two-week high; equities were mixed amid profit taking in EMFX and month-end flows in G-10 currencies. Some other key FX observations, from Bloomberg:

- The pound was the only G-10 currency to strengthen against the dollar on Thursday after news that Ireland and the U.K. were close to a border deal

- EUR/USD set a fresh session low after annual euro-zone flash CPI rose 1.5% in November versus an estimated 1.6% rise

- Kiwi dropped after business confidence fell to the lowest level since 2009

- The yen fell to a one-week low on the back of a rally in Japanese stocks and as better-than- expected U.S. economic data sapped haven demand

- Norway’s krone slid to a nine-year low against the euro, with low liquidity exaggerating the move, after retail sales unexpectedly contracted 0.2% m/m in October versus an estimated 0.7% rise

Weighing on tech were concerns, sparked by a Morgan Stanley report

earlier this week, that the “super-cycle” in memory chip demand looks

likely to peak soon. Yesterday, shares of Amazon.com, Apple, Alphabet

and Facebook fell between 2 percent and 4 percent. Among the year’s

other high fliers, Netflix slid 5.5 percent while Asia’s bellwether

Samsung slumped 4.3 percent to two-month lows, also on some Morgan

Stanley skepticism.

“I‘m not sure one would say it’s a bubble (in tech stocks),” said Andrew Milligan, head of investment strategy at Standard Life. “By and large the companies are generating either good profits or the potential for good profit growth”. But “Tech is a sector unto itself… it’s utterly a view about barriers to entry.”

Still, the Nasdaq index remains up 26.8% so far this year, roughly 7% points above gains in the MSCI world index. “It is true that if you look at the world’s semiconductor sales on chart, their year-on-year growth appears to be peaking out,” said Hiroshi Watanabe, an economist at Sony Financial Holdings. “But if you look at what’s driving demand, it’s not just smart phones and actually a lot of things.”

In the US, Senate Republicans voted 52-48 to begin debate on their sweeping tax-overhaul bill, touching off a process that could produce an up-or-down vote before the end of this week. Outgoing Federal Reserve Chair Janet Yellen said Wednesday the central bank would welcome and support a faster expansion of the economy stemming from changes in the tax code, provided it was the right kind of growth. Other notable US events overnight: