GOLD: $1323.40 UP $2.25

Silver: $16.60 UP 21 CENTS

Closing access prices:

Gold $1323.75

silver: $16.61

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1326.55 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1318.45

PREMIUM FIRST FIX: $8.10

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1329.10

NY GOLD PRICE AT THE EXACT SAME TIME: $1318.85

PREMIUM SECOND FIX /NY:$10.25

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1319.35

NY PRICING AT THE EXACT SAME TIME: $1319.50

LONDON SECOND GOLD FIX 10 AM: $1320.60

NY PRICING AT THE EXACT SAME TIME. $1320.85

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR:4 FOR 400 OZ

For silver:

MARCH

173 NOTICE(S) FILED TODAY FOR

865,000 OZ/

Total number of notices filed so far this month: 4727 for 23,635,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8907/OFFER $8,977: DOWN $348(morning)

Bitcoin: BID/ $8947/offer $9017: DOWN $308 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A FAIR SIZED 796 contracts from 195,724 RISING TO 196,520 DESPITE YESTERDAY’S TINY 1 CENT FALL IN SILVER PRICING. WE OBVIOUSLY HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 2693 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 2693 CONTRACTS. WITH THE TRANSFER OF 2693 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2693 CONTRACTS TRANSLATES INTO 13.43 MILLION OZ WITH THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

18,356 CONTRACTS (FOR 7 TRADING DAYS TOTAL 18,356 CONTRACTS OR 91.780 MILLION OZ: AVERAGE PER DAY: 2622 CONTRACTS OR 13.111 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 91.780 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 13.11% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 584.255 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A SMALL SIZED GAIN IN COMEX OI SILVER COMEX OF 796 DESPITE THE TINY 1 CENT FALL IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 2693 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 2693 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 3489 OI CONTRACTS i.e. 2693 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 796 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 1 CENT AND A CLOSING PRICE OF $16.49 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.982 BILLION TO BE EXACT or 140% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 173 NOTICE(S) FOR 865,000 OZ OF SILVER

*** note in gold. last last night, the CME released EFP’s for yesterday and today and I reversed them ie. the EFP for today is 7473 and yesterday 7106. I will not change and it will not make a difference when the two are added.

In gold, the open interest FELL BY A STRONG 10,663 CONTRACTS DOWN TO 497,387 WITH THE CONSIDERABLE FALL IN PRICE YESTERDAY ($5.45) HOWEVER FOR TODAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN GOOD SIZED 7106 CONTRACTS THE ISSUANCE OF, APRIL SAW THE ISSUANCE OF 7106 CONTRACTS , JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 497,387. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A HUGE LOSS OI CONTRACTS: 10,663 OI CONTRACTS DECREASED AT THE COMEX AND A GOOD SIZED 7106 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI LOSS: 3557 CONTRACTS OR 355,700 OZ =11.06 TONNES

YESTERDAY, WE HAD 7473 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 68,796 CONTRACTS OR 6,879,600 OZ OR 213.96 TONNES (7 TRADING DAYS AND THUS AVERAGING: 9828 EFP CONTRACTS PER TRADING DAY OR 982,800 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 5 TRADING DAYS IN TONNES: 213.96 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 213.96/2550 x 100% TONNES = 8.39% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1464.33 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A HUGE SIZED DECREASE IN OI AT THE COMEX WITH THE CONSIDERABLE FALL IN PRICE IN GOLD TRADING YESTERDAY ($5.45). HOWEVER, WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7106 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7106 EFP CONTRACTS ISSUED, WE HAD A NET LOSS IN OPEN INTEREST OF 3557 contracts ON THE TWO EXCHANGES:

7106 CONTRACTS MOVE TO LONDON AND 10,663 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 11.063 TONNES).

we had: 0 notice(s) filed upon for nil oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $2.25 : NO CHANGES IN GOLD INVENTORY AT THE GLD /

Inventory rests tonight: 833.73 tonnes.

SLV/

WITH SILVER UP 21 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 318.069 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 796 contracts from 195724 UP TO 196,520 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE TINY FALL IN PRICE OF SILVER (1 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 2686 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 796 CONTRACTS TO THE 2693 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 3484 OPEN INTEREST CONTRACTS WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 17.420 MILLION OZ!!!

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE TINY FALL OF 1 CENT IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD SIZED 2693 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)FRIDAY MORNING/LATE THURSDAY NIGHT: Shanghai closed UP 18.76 POINTS OR 0.57% /Hang Sang CLOSED UP 341.69 POINTS OR 1.11% / The Nikkei closed UP 101.13 POINTS OR 0.47%/Australia’s all ordinaires CLOSED UP 0.37%/Chinese yuan (ONSHORE) closed UP at 6.3365/Oil DOWN to 60.58 dollars per barrel for WTI and 64.25 for Brent. Stocks in Europe OPENED RED EXCEPT PARIS CAC . ONSHORE YUAN CLOSED DOWN AT 6.3365 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3360 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (STRONGER CURRENCY GOOD CHINESE MARKETS/BUT TRUMP TARIFFS INITIATED/ )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

Not so fast! Before Trump is to meet North Korea must take “concrete actions”

let us see what Kim Jung Un does

(zerohedge)

b) REPORT ON JAPAN

i)Tepco now admits that its ICE WALL is failing. Radiation is leaking through the water

( zerohedge)

ii)Bank of Japan leaves policy stance unchanged. After September, they will be the last one standing per QE

( zerohedge)

3 c CHINA

i)Hong Kong:

We have been highlighting this story to you for the past few weeks as the Hong Kong dollar is floundering. House prices are sky high. The problem is citizens are buying dollars with the higher yield than Hong Kong yields and that is putting pressure on their Hong Kong dollar

(courtesy zerohedge)

( zerohedge)

4. EUROPEAN AFFAIRS

i)Britain

It now seems that Britain’s largest charity Oxfam is a fraud with massive public money disappearing

( G Meotti/Gatestone Institute)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

This does not look good for New Zealand as their chief guarantor of properties,CBL collapsed. Now Deposit power has also collapsed putting 10,000 homes at risk

( MishShedlock/Mishtalk)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Ronan Manly is seeing what I am seeing: delays in reporting. He comments that the LBMA will delay reporting on the gold and silver price auction

Manly writes: “It must be obvious to everyone that the LBMA and its bullion bank members do not want the transparency that gold and silver trade reporting would provide. Otherwise they would not have spent four years on a project that any individual investment bank could start and complete within less than three months.”

( RonanManly/Bullionstar)

ii)A very good commentary today from Hugo Salinas Price who collectedly states that if the uSA seeks to remove its trade deficits with the rest of the world, then it will no longer be the reserve currency of the world. He concludes that the only replacement will be gold.

( Hugo Salinas Price)

10. USA stories which will influence the price of gold/silver

Trading:/jobs report

i)an extremely strong economy with February payrolls adding 313,000 jobs. But Wall Street looks for hourly earnings and they disappointed. The need wage growth to stimulate their version of inflation

( zerohedge)

ii)Initial reaction: stocks rise, bond yields rise (dangerous) with the mixed payroll report

( zerohedge)

iib)Now treasury yields have risen above 2.90% and this is the danger zone for stocks

iii)Broad strength everywhere including retail

v)here is another retail casualty: Claires as they are to file for bankruptcy protection..another Amazon victim( zerohedge)

vi)SWAMPVILLE

Have fun with this: Former porn star Stormy Daniels is hit with a restraining order over the Trump affair talk

( zerohedge)

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 372,548 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 291,956 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A SMALL 796 CONTRACTS FROM 195,724 UP TO 196,520 DESPITE YESTERDAY’S 1 CENT FALL IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD 2693 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 2693. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION BUT WE ALSO HAD A HUGE SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 3489 SILVER OPEN INTEREST CONTRACTS 796 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 2693 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:3489 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month LOST 19 contracts FALLING TO 639 contracts. We had 30 contracts filed upon yesterday, so we GAINED 11 contracts or an additional 85,000 will stand in this active delivery month of March.(AS SOMEBODY IS IN GREAT NEED OF PHYSICAL SILVER)

April LOST 8 contracts FALLING TO 430 .

The next big active delivery month for silver will be May and here the OI LOST 805 contracts DOWN to 145,080

We had 173 notice(s) filed for 850,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 9/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

964 oz

Scotia

30 kilobars

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

0 notice(s)

400 OZ

|

| No of oz to be served (notices) |

560 contracts

(56,000 oz)

|

| Total monthly oz gold served (contracts) so far this month |

4 notices

400 oz

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (4) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (560 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 56,400 oz, the number of ounces standing in this nonactive month of MARCH (1.7542 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (4 x 100 oz or ounces + {(560)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 56400 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 43 CONTRACTS OR AN ADDITIONAL 4300 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 18 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

20,003.330 oz

Delaware

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

595,976.175 oz

Scotia

CNT

|

| No of oz served today (contracts) |

173

CONTRACT(S

(865,000 OZ)

|

| No of oz to be served (notices) |

466 contracts

(2,330,000 oz)

|

| Total monthly oz silver served (contracts) | 4727 contracts

(23,635,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total inventory deposits/withdrawals/ into dealer: nil oz

we had 2 deposits into the customer account

i) into CNT 16,611.445 oz

ii) Into Scotia: 579,364.730 oz

ii) JPMorgan: zero

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 135 million oz of total silver inventory or 54% of all official comex silver.

JPMorgan did not add any silver into its warehouses (official) today.

total deposits today: 595,976.175 oz

we had 1 withdrawals from the customer account;

i) Out of Delaware 20,003.330 oz

total withdrawals; 20,003.330 oz

we had 1 adjustments

i) Out of CNT: 827,327.06 oz was adjusted out of the customer and this landed into the dealer account of CNT

total dealer silver: 59.419 million

total dealer + customer silver: 252.893 million oz

The total number of notices filed today for the March. contract month is represented by 173 contract(s) FOR 865,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 4727 x 5,000 oz = 23,635,000 oz to which we add the difference between the open interest for the front month of Mar. (639) and the number of notices served upon today (173 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 4727(notices served so far)x 5000 oz + OI for front month of March(639) -number of notices served upon today (173)x 5000 oz equals 25,965,000 oz of silver standing for the March contract month.

We GAINED an additional 11 contracts or 55,000 additional silver oz will stand for delivery at the comex as somebody was in urgent need of physical silver.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 94,067 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 73,029 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 73,029 CONTRACTS EQUATES TO 365 MILLION OZ OR 52.1% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.13% (MARCH 9/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.52% to NAV (March 9/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.13%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.52%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -3.07%: NAV 13.70/TRADING 13.27//DISCOUNT 3.07.

END

And now the Gold inventory at the GLD/

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 9/2018/ Inventory rests tonight at 833.73 tonnes

*IN LAST 339 TRADING DAYS: 107,41 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 269 TRADING DAYS: A NET 48.89 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 315.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

MARCH 9/2018: NO CHANGES TO SILVER INVENTORY/

Inventory 318.069 million oz

end

6 Month MM GOFO 2.00/ and libor 6 month duration 2.24

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.97%

libor 2.26 FOR 6 MONTHS/

GOLD LENDING RATE: .29%

XXXXXXXX

12 Month MM GOFO

+ 2.36%

LIBOR FOR 12 MONTH DURATION: 2.53

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.17

GOLD LENDING RATES FALLING TO APPROACH ZERO AS PHYSICAL GOLD IS SCARCE/GOFO RATES RISING

end

At 3:30 pm we receive a COT report which has no real value due to the huge exit of EFP contracts morphing to forwards over in London.

However for the sake of completeness I will provide them for you but please do not ask me what they mean because quite frankly I do not know

Gold COT

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 245,587 | 61,764 | 62,811 | 153,421 | 358,324 | 461,819 | 482,899 |

| Change from Prior Reporting Period | ||||||

| -6,394 | -11,499 | -9,206 | -8,106 | -2,999 | -23,706 | -23,704 |

| Traders | ||||||

| 183 | 79 | 86 | 50 | 62 | 267 | 196 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 46,281 | 25,201 | 508,100 | ||||

| -1,054 | -1,056 | -24,760 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, March | |||||

our large speculators

those large specs who have been long in gold pitched (transferred through EFP) 6,394 contracts

those large specs who have been short in gold covered a huge 11,499 contracts from their short side(maybe transferred their liability to London).

our commercials

those commercials who have been long in gold pitched (transferred) a net 8106 contracts from their long side

those commercials who have been short in gold covered (transferred liability to London) a net 2999 contracts from their short side.

our small speculators

those small specs who have been long in gold pitched (transferred) 1054 contracts from their long side

those small specs who have been short in gold covered (transferred) 1056 contracts from their short side.

Conclusion:

i can only think of one word: fraud

And now for our silver COT

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 68,686 | 62,500 | 23,783 | 74,760 | 96,570 | |

| 5,663 | -2,031 | 6,018 | -7,378 | -31 | |

| Traders | |||||

| 112 | 55 | 47 | 40 | 36 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 196,590 | Long | Short | |

| 29,361 | 13,737 | 167,229 | 182,853 | ||

| -1,056 | -709 | 3,247 | 4,303 | 3,956 | |

| non reportable positions | Positions as of: | 172 | |||

our large speculators

strange!! those large speculators who have been long in silver added a net 5663 contracts even after receiving a huge number of EFP contracts.

those large specs who have been short in silver covered (transferred) 2999 contracts from their short side

our commercials

those commercials who have been long in silver pitched (transferred) a huge 7378 contracts from their long side

those commercials who have been short in silver covered (transferred) 31 contracts from their short side.

our small speculators

those small specs who have been long in silver pitched (transferred) 1056 contracts from their long side

those small specs who have been short in silver covered (transferred) 709 contracts from their short side.

Conclusion: same as gold/ Fraud

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

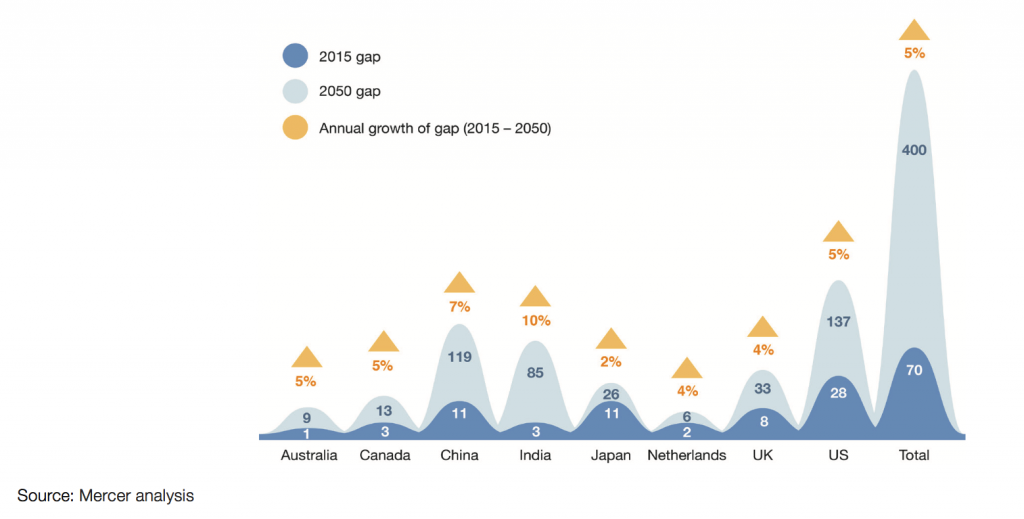

Women’s Pension Crisis Highlights Dangers To Savers

Women’s Pension Crisis Highlights Dangers To Savers

– International Women’s Day highlights the underreported UK Women’s pension crisis

– 2.66 million affected by UK government’s change to state pension act

– Women’s pension crisis is one of many in the UK, where there is a £710bn deficit for prospective retirees

– Changes by government highlights the counterparty risks pensions are exposed to

– Global problem as pensions gap of developed countries growing by $28B per day

– Savers and investors should look to invest in gold as part of their pensions

Imagine contributing to a pension throughout your working life only to be told that you won’t receive it when you expect to. When you receive this information it comes with just a few years’ notice. There is little time to make alternative pension arrangements. You have a choice: either continue to work until your pension comes in, or live on very little in the meantime.

This is a reality over 2.6 million women in the UK currently face. Those born in the 1950s have been told by the British government that their retirement ages have been increased from 60 to 65 years of age. This change means they will not receive their state pensions when they originally expected to. This is part of a move to bring men and women’s retirements to the same level.

Put that way, this looks to be a good move. Particularly when one considers the demands for women to be treated equally to men. But when a change is made in this way it is about anything but equality.

The decision by the UK government to delay paying pensions to women of a certain birthdate has resulted in one of the biggest pension crises in the UK, yet it is the least reported and discussed.

Pensions crises is something the country is rapidly getting used to. As well as the 2.6 million women affected by the UK’s Pensions Act there are the many thousands of men and women affected by private pension disasters that amount to over £710bn in deficits.

Each of these issues highlight the high exposure pensions have to counterparty risk. Millions of individuals believe they have safely contributed to a retirement pot only for the government to tell them they have to wait even longer for it or that the company they trusted to support their pension has gone bust.

UK’s pension inequality is economic inequality

Yesterday it was International Women’s Day (IWD) and on Sunday many of us around the world will be celebrating Mother’s Day. Both days are there to recognise the achievements and sacrifices of women. IWD is also there to raise attention to the plights of billions of women across the globe. Many are disadvantaged through economic, political, sexual and other means. Campaigns run throughout the year to help them but IWD is a day to really bring the spotlight to them.

Few in the West realise that IWD has an important place in the UK. We still have major problems with sex trafficking, domestic abuse and discrimination against minorities.

One of the least reported areas in the economic discrimination of women. I’m not talking about gender pay gap, the lack of female CEOs or maternity leave. In this specific instance I’m talking about the female pension crisis that has left over a two million women in a huge financial limbo.

Women Against State Pension Inequality (WASPI) explain how this has happened:

The 1995 Conservative Government’s Pension Act included plans to increase women’s SPA (State Pension Age) to 65, the same as men’s. WASPI agrees with equalisation, but does not agree with the unfair way the changes were implemented – with little or no personal notice (1995/2011 Pension Acts), faster than promised (2011 Pension Act), and no time to make alternative plans. Retirement plans have been shattered with devastating consequences.

WASPI has been campaigning for a long-time to have the changes brought in in a more economically viable manner, so that women can afford their retirements or at least have time to make alternative arrangements. They estimate those suffering as a result of the changes could be higher than the 2.6 million reported by the UK government.

In early February 2018 the government rejected WASPI’s proposals for a fairer transition period, claiming it would “represent a loss of over £70bn to the public purse.” This was a burden pensions minister Guy Opperman said he was not prepared to pass onto ‘young people’.

What about the burden of those women who have not been given enough notice regarding their retirement age? i News, spoke to one WASPI campaigner about the hardships now facing many women in their later 50s and early 60s:

“I was 58 when I got a letter saying my state pension age was going up from 65 to 66. It was a shock because I thought I was getting my state pension at 60.” Ms Eachus says some of the women she has helped have been in serious financial hardship, while others had no idea their pension age had risen. “At Christmas, we sent food and toiletry parcels to women in their sixties who are struggling. We shouldn’t have to do that. Women are having to sell their homes. One of the women I spoke to was sleeping on someone’s sofa. Some are too embarrassed to tell their family.”

In a study carried out by former pensions minister Rachel Reeves on the 2011 Act it found out of 416,000 women considered, 80,000 lost up to £8,000 because of the changes in the 2011 Act. 48,000 lost out on as much as £12,000 thanks to their new state pension age. This study did not take into account the Acts of 1995 and 2007 which stripped other 1950s born women of thousands more.

MP Frank Field, in 2006, estimated there were some women who were as much as £40,000 out of pocket, due to the changes. Those who have to continue working to the retirement age are not expected to receive more as a result of their increased economic contribution through National Insurance payments.

Economic inequality goes beyond women’s pension crisis

A report released yesterday by The Living Wage Foundation and the Fawcett Society revealed the true dangers women are economically exposed to.

A quarter of all women workers in the UK earn less than the living wage. Three out of five working women only have enough savings to last a month if they lost their job.

In short, the pension poverty of women is not set to improve. This, combined with the overall pension crisis in the UK makes for a dire future.

As of September 2017 £710 billion was the estimated, terrifying size of the UK pensions deficit. Ageing populations, low birth rates and dire monetary policy means that over 27 million people in the UK will not be receiving adequate pensions once they retire.

A 2017 report looked at both public and corporate pensions. It was the government and public pensions that were the most unhealthy, accounting for 75% of the under funding.

In November 2017, the OECD warned that the UK’s defined benefit workplace pension plans (final salary schemes) as ‘persistently underfunded’ and the state pension as seriously lacking.

It’s not much better in the corporate pensions sector of the US and UK where the WEF estimates there are over $4 trillion in liabilities.

This year the biggest pension news in the UK has come courtesy of the Carillion crisis, estimated to have left a £900 million debt pile and 30,000 pensions at risk. This was yet another example of mismanagement and lack of consideration for workers.

Everyone future retiree is exposed to these issues. They emphasise the importance of saving for retirement and ensuring your pension is both funded and properly diversified.

Men and women alike are heading for pension inequality

Here in the UK there is some growing resentment about campaigns such as IWD, many believe it is sexist. A frequently asked question on Twitter yesterday was ‘Well, when’s International Men’s Day’, suggesting men were sidelined for the female cause. International Men’s Day is November 19th and it was conceived in 1991.

In the UK (and many Western countries) there is an assumption that women’s rights campaigns have been successful and we should be happy with where we are now. The problem is that women of a certain age have been discriminated against.

For a funny reason whenever there is a pension crisis in the UK as we have seen recently with Carillion or BHS to name few, the government rallies around to find a solution. When it is a government-led crisis then they (and the media) are suspiciously quiet and unhelpful.

The pension crisis is not exclusive to women, but it is the only one that has come about due to discrimination by the government. It is a terrifying example of how the government has the power to not only provide but to also takeaway. The UK government very much holds the financial fate of these women in its hands, with very little acknowledgement of the consequences.

This example shows that when it comes to pensions that are managed by counterparties there is little control on the part of the savers. Governments and businesses have the power to decimate a lifetime of contributions in a matter of moments.

In a recent study the World Economic Forum declared a Western pension crisis. They said one of the few ways it could be managed was for individuals to ‘take responsibility to manage [their] pensions’.

It is vital that individuals take responsibility for their pensions. You must ask questions about it as soon as possible.

Particularly, you should ask if you can invest in gold as part of your pension. Internationally, the trend for doing this is extremely low which is surprising given the role it has played in preserving and growing pension wealth.

Dr. Constantin Gurdgiev, formerly an adviser to GoldCore, says the following about the importance of having gold in your pension:

“Gold is a long-term risk management asset, not a speculative one.

As such it should be analysed and treated predominantly in the context of its role as a part of a properly structured, risk-balanced and diversified portfolio spanning the full life-cycle of the investment and pension horizon for individual investors and those with pensions.

Whether they be SIPPs in the UK or IRAs in the USA.”

Gold in a SPIPP or IRA is not held hostage to a change in government policy or a CEOs reckless spending of company finances. It is there to act as a safe haven against such events.

Investors in the UK and Ireland, the US, the EU can invest in gold bullion in their pension, through self-administered pension funds.

UK investors can invest in gold bullion through their Self-Invested Personal Pensions (SIPPs), Irish investors can invest in gold in Small Self Administered Schemes (SSAS) and US investors can invest in gold in their Individual Retirement Accounts (IRAs).

The pension crisis is a multi-trillion dollar/pound crisis. It is not going to go away. Adding gold to your pension is a key way to protect yourself against the economic inequality facing many future retirees.

Related reading

Pension Crisis And Deficit of £2.6 Billion At Carillion To Impact UK Pensions

UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold

UK Pensions and Debt Time Bomb: £1 Trillion Crisis Looms

News and Commentary

Stocks in Japan, South Korea surge on news of Trump-Kim meeting (MarketWatch.com)

Stocks Rise in Asia on Trump-Kim Summit; Yen Drops (Bloomberg.com)

Gold dips as dollar firms amid hopes for easing U.S.-N.Korea tensions (Reuters.com)

Stocks, Bonds Rise as Trump Signs Off on Tariffs (Bloomberg.com)

U.S. Household Debt Rose Last Quarter at Fastest Rate Since 2007 (Bloomberg.com)

Image source: Bloomberg

Reuters exclusive: Five banks open up trillion-dollar gold club (Reuters.com)

Trump’s Historic Bet on Kim Summit Shatters Decades of Orthodoxy (Bloomberg.com)

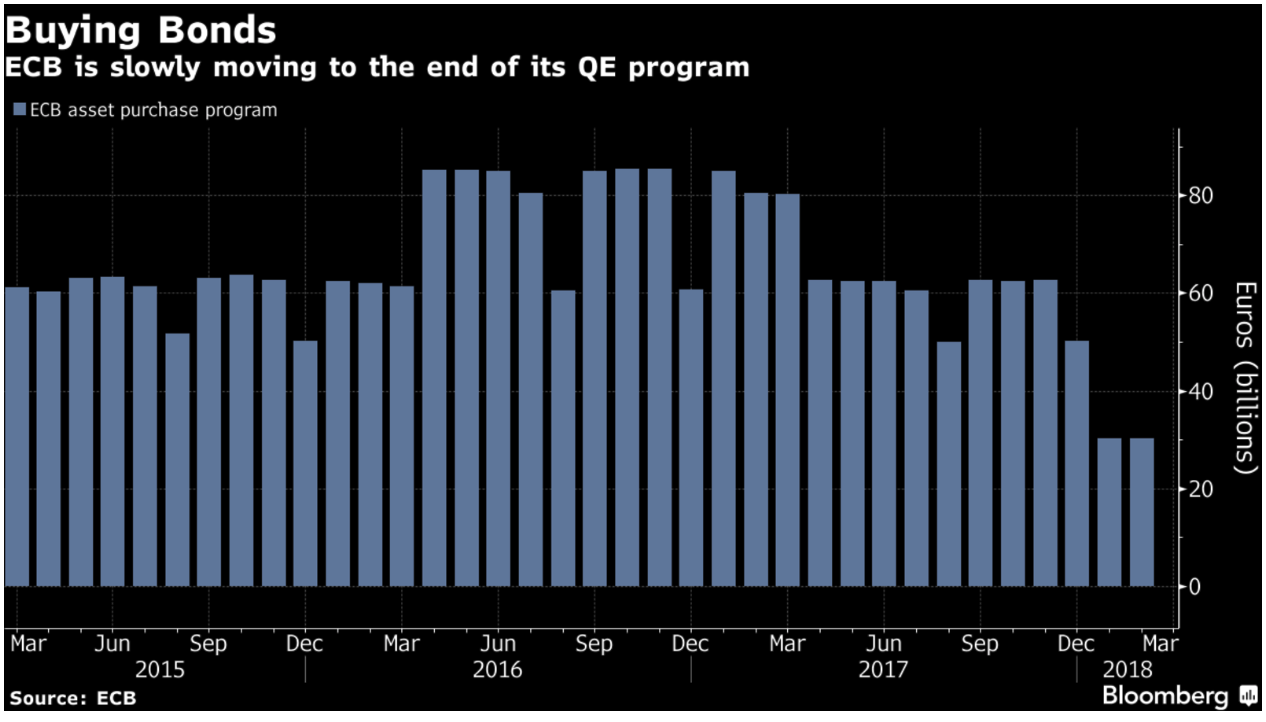

ECB Assumes Final QE Push Totaling 30 Billion Euros (Bloomberg.com)

Hungarian National Bank Decides to Bring Gold Reserves Back Home (HungaryToday.hu)

Gold Prices (LBMA AM)

09 Mar: USD 1,319.35, GBP 955.21 & EUR 1,072.50 per ounce

08 Mar: USD 1,325.40, GBP 955.08 & EUR 1,070.39 per ounce

07 Mar: USD 1,332.50, GBP 960.07 & EUR 1,071.86 per ounce

06 Mar: USD 1,324.95, GBP 957.01 & EUR 1,074.00 per ounce

05 Mar: USD 1,326.30, GBP 958.78 & EUR 1,075.63 per ounce

02 Mar: USD 1,316.75, GBP 955.70 & EUR 1,071.04 per ounce

01 Mar: USD 1,311.25, GBP 953.80 & EUR 1,075.75 per ounce

Silver Prices (LBMA)

09 Mar: USD 16.49, GBP 11.92 & EUR 13.40 per ounce

08 Mar: USD 16.48, GBP 11.89 & EUR 13.31 per ounce

07 Mar: USD 16.65, GBP 12.01 & EUR 13.42 per ounce

06 Mar: USD 16.62, GBP 11.96 & EUR 13.41 per ounce

05 Mar: USD 16.51, GBP 11.95 & EUR 13.42 per ounce

02 Mar: USD 16.45, GBP 11.92 & EUR 13.36 per ounce

01 Mar: USD 16.32, GBP 11.87 & EUR 13.39 per ounce

Recent Market Updates

– London Property Sees Brave Bet By Norway As Foxtons Profits Plunge

– Gold Does Not Fear Interest Rate Hikes

– RaboDirect Closing – Gold May Protect From Irish Banks Going “Belly Up Again” – Finuncane

– Silver bullion will likely outperform gold bullion going forward

– Gold $10,000? Goldnomics Podcast Quotations and Transcript

– Trump Risks Trade and Currency Wars – Protectionism and Economic War Loom

– Four Key Themes To Drive Gold Prices In 2018 – World Gold Council

– Is The Gold Price Going To $10,000? (Goldnomics Podcast 3)

– Gold Corridor From Dubai to China Sought By China

– Digital Gold Provide the Benefits Of Physical Gold?

– Weekly Briefing: Currency Wars – ECB Warns Re Trump, Russia and Turkey Buy Gold and BOE Bitcoin Warning

– Russian Central Bank Buys Gold – 600,000 Ounces Or 18.7 Tons In January As Venezuela Launches ‘Petro Gold’

– Bitcoin or British Pound ‘Pretty Much Failed’ As Currency?

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end.

THE FOLLOWING CAME FROM KOOS JANSEN:

YOU WILL NOTE THAT FOR THE FIRST TIME EVER CHINA EXPORTED GOLD TO LONDON.

THE QUESTION IS WHY?

I ASKED MY GOOD FRIEND REG HOWE FOR HIS THOUGHTS ON THIS AND WE AGREE THAT THERE ARE TWO POSSIBILITIES: 1) THAT THERE IS EXTREME SHORTAGE IN LONDON AND A MAJOR BANK COULD NOT DELIVER UPON ALONG OVER THERE.. CHINA WOULD BE ASKING FOR A BIG QUID PRO QUO FOR PROVIDING THE NECESSARY PHYSICAL. (IT MAKES SENSE IN THE FACT THAT GOLD IS IN BACKWARDATION IN LONDON)

2. TO HELP IN THE FACILITATION OF THE NEW OIL FOR YUAN FOR GOLD NEW FORMAT OR SOME FUTURE MEASURE THAT CHINA WILL REQUIRE OR AT LEAST BENEFIT FROM ADDITION PHYSICAL LIQUIDITY IN LONODN..

REGARDLESS, IT SHOWS SCARCITY OVER THERE.

FROM REG HOWE TO ME:

“Have read speculation that it may have to do with the mechanics of settling the new oil and gold contracts in physical. More generally, I would guess it’s one of two things: (1) Chinese help in containing some serious stress in the gold market due to lack of physical, e.g., some central bank or major bullion bank unable to deliver, in which case there is likely a big quid pro quo; or (2) a positioning to facilitate some (other) future measure by China that will require or at least benefit from additional physical liquidity in London. In any event, seems to be more evidence of severe shortage of physical in London, otherwise they would just buy it there at today’s suppressed prices.”

END

Ronan Manly is seeing what I am seeing: delays in reporting. He comments that the LBMA will delay reporting on the gold and silver price auction

Manly writes: “It must be obvious to everyone that the LBMA and its bullion bank members do not want the transparency that gold and silver trade reporting would provide. Otherwise they would not have spent four years on a project that any individual investment bank could start and complete within less than three months.”

(courtesy RonanManly/Bullionstar)

Ronan Manly: LBMA stalls daily gold and silver price auction fix reports

Submitted by cpowell on Thu, 2018-03-08 17:00. Section: Daily Dispatches

12:02p ET Thursday, March 8, 2018

Dear Friend of GATA and Gold:

The London Bullion Market Association, gold researcher Ronan Manly discloses today, has stopped providing timely reports of the daily gold and silver auction price fixes and has against postponed its plans to publish trade data about the monetary metals.

Manly writes: “It must be obvious to everyone that the LBMA and its bullion bank members do not want the transparency that gold and silver trade reporting would provide. Otherwise they would not have spent four years on a project that any individual investment bank could start and complete within less than three months.”

Manly’s report is headlined “LBMA Alchemy and the London Gold and Silver Markets: 2 Steps Back” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/lbma-alchemy-london-gold-m…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A very good commentary today from Hugo Salinas Price who correctedly states that if the uSA seeks to remove its trade deficits with the rest of the world, then it will no longer be the reserve currency of the world. He concludes that the only replacement will be gold.

(courtesy Hugo Salinas Price)

Hugo Salinas Price: Without trade deficits, U.S. dollar can’t be world reserve currency

Submitted by cpowell on Thu, 2018-03-08 18:04. Section: Daily Dispatches

1:04p ET Thursday, March 8, 2018

Dear Friend of GATA and Gold:

Hugo Salinas Price, president of the Mexican Civic Association for Silver, remarking on President Trump’s tariffs and potential trade war to eliminate the trade deficits of the United States, notes today that no country can issue the world reserve currency without running trade deficits to spread its currency throughout the world.

Salinas Price writes: “So the exorbitant privilege of the United States, the production of the world’s fundamental currency — which allows it to purchase anything in any amount, in any place, at any price — produces automatically the fundamental need of foreign countries to undersell U.S. producers.”

If the dollar is no longer to be the world reserve currency, Salinas Price concludes, the only replacement will be gold.

His analysis is headlined “Bad Karma Brings Bad Consequences for Those Who Practice It” and it’s posted at the silver association’s internet site here:

http://plata.com.mx/enUS/More/346?idioma=2

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3365 /shanghai bourse CLOSED UP 18.76 POINTS OR 0.57% / HANG SANG CLOSED UP 341.69 POINTS OR 1.11%

2. Nikkei closed UP 101.13 POINTS OR 0.47% /USA: YEN RISESS TO 106.82/

3. Europe stocks OPENED DEEPLY IN THE RED /USA dollar index RISES TO 90.255/Euro FALLS TO 1.2298

3b Japan 10 year bond yield: FALLS TO . +.053/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.82/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 60.58 and Brent: 64.25

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.648%/Italian 10 yr bond yield DOWN to 1.989% /SPAIN 10 YR BOND YIELD DOWN TO 1.422%

3j Greek 10 year bond yield FALLS TO : 4.183?????????????????

3k Gold at $1318.25 silver at:16.45 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 15/100 in roubles/dollar) 56.95

3m oil into the 60 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.82 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9511 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1696 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.648%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.877% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.1457% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures Tread Water Ahead Of “Average Hourly Earnings” Report

After a barrage of breaking, surprise headlines and geopolitical developments, markets fall back to the familiar rhythm of trading the monthly payrolls (+205K exp), or rather, the far more important average hourly earnings (+2.8% Y/Y exp.) report. This morning, global shares hit a one-week high before easing a touch, as caution ahead of jobs data, and a potential disappointment in wage inflation outweighed a potential breakthrough in nuclear tensions over the Korean peninsula.

As a result, futures are somewhat mixed, with Asia trading higher, while Europe started off on the back foot but has recovered losses. The MSCI All-Country World index was 0.1% higher and set for a weekly gain of almost 2%.

As is traditionally the case ahead of payrolls, S&P futures have hugged the flatline.

Gains came mostly from Asian stocks which staged sharp rallies after U.S. President Donald Trump said he was prepared to meet North Korea’s Kim Jong Un, potentially marking a major breakthrough in nuclear tensions between the two countries. The summit news overshadowed a warning from China that it will take “strong” measures to counter U.S. trade tariffs.

“While it is easy to be cynical, one can’t help feeling these talks could well go the same way as previous attempts. But nonetheless it will be interesting to see how this one plays out,” said Michael Hewson, chief markets analyst at CMC Markets.

Commenting on Trump’s two main announcement this week, one desk had the following interestinh commentary:

President Trump must be delighted that his policies are paying off. His bellicose tweets have brought North Korea to the negotiating table and his use of cold war steel tariffs is effectively an invitation for trading partners to make him their best offer in order to secured tariff exemption. A weaker dollar is clearly part of Trump’s protectionist agenda as well and we believe investors will be looking to sell into any near-term dollar rallies.

As previewed, the market now will focus onto today’s employment report in the US. The consensus is for a 205k February payrolls number, which follows 200k in January. The unemployment rate is expected to dip to 4.0% from 4.1%. But it’s the average hourly earnings print which is the bigger component focus for the market right now given the obsession with inflation. The market forecasts a +0.2% mom print (which should lower than annual rate by one-tenth to +2.8% yoy, driven by base effects).

Going into payrolls, Asian stocks were higher across the board after the lead from US where Trump confirmed aluminium and steel tariffs, but exempted NAFTA partners and was also said to be open to providing relief for allies. In addition, Asia-Pac risk appetite was further bolstered by geopolitical developments in which the South Korean National Security Office chief announced that North Korean Leader Kim is committed to denuclearization and will refrain from conducting further tests, with President Trump and North Korea’s Kim to meet by May.

Overnight, in its latest announcement, the BoJ kept monetary policy unchanged as expected with NIRP held at -0.1% and 10yr JGB yield target at around 0%. The decision was made by 8-1 vote with board member Kataoka the sold dissenter, who called for the BoJ to buy JGBs so 10yr yields or longer drop further and repeated that the BoJ should clarify it will ease further if domestic factors delay reaching price target. At the post-meeting press conference, Governor Kuroda faced a barrage of questions about the so-called exit from the current monetary easing scheme, but according to Goldman, the governor damped expectations for the exit for the foreseeable future. In fact, Goldman adds, and we agree, that it will be difficult for the BOJ to normalize interest rates before the impact of the next consumption tax hike, slated for October 2019, has run its course, given the weakness of upward pricing pressures and the strong intentions of the government.

Australia’s ASX 200 (+0.3%) and Nikkei 225 (+0.5%) were positive but with upside capped by a subdued commodities sector and weakness across steel names on Trump tariffs, while KOSPI (+1.0%) outperformed on the further appeasement in the Korean peninsula. Not helping the growth narrative was China’s CPI which came in blistering hot, surging 2.9%, or the most in 5 years. Elsewhere, Hang Seng (+1.1%) was underpinned amid the broad positivity in the region, while the Shanghai Composite (+0.6%) somewhat lagged after PBoC inaction led to a net weekly drain of CNY 240bln.

Also overnight, outgoing PBOC Governor Zhou Xiaochuan said market-access reforms should be accelerated and that the world’s second-largest economy “can be bolder in opening up”; Deputy Governor Yi Gang said stable progress will be made on capital-account convertibility.

Other key Chinese data:

- Chinese CPI (Feb) Y/Y 2.9% vs. Exp. 2.5% (Prev. 1.5%); highest in over 4 years. (Newswires)

- Chinese PPI (Feb) Y/Y 3.7% vs. Exp. 3.8% (Prev. 4.3%)

- Chinese New Yuan Loans (CNY)(Feb) 839B vs. Exp. 900B (Prev. 2900B). (Newswires)

- Chinese Aggregate Financing (CNY)(Feb) 1.17tln vs. Exp. 1.07tln (Prev. 3.06tln)

- Chinese Money Supply M2 (Feb) Y/Y 8.8% vs. Exp. 8.7% (Prev. 8.6%)

Chinese commodities were hit hard by the jump in inflation and trade war announcement, with iron ore plunging 5%, now down 14% from February peak; steel rebar futures -7.8% this week in Shanghai, on course for biggest slump in a year.

DCE Iron Ore

European equities erased earlier losses before edging higher, chasing gains in the U.S. and Asia as the U.S. non-farm payrolls report draws near. Automakers remain underperformers as trade-related concerns linger. The Stoxx Europe 600 Index was fractionally higher (+0.1%) and heading for a weekly advance of 2.6%. GVC Holdings is one of the best performers on the gauge after the company said it made a strong start to 2018. Lagardere drags media shares to the worst industry group performance after posting weaker-than-expected full-year results. German Jan. ind. production fell 0.1% m/m; est. +0.6% m/m. U.K. February retail sales drop as BDO sees more ‘casualties.’

In global macro, the overnight narrative was dominated by the yen and the Norwegian krone, with the USDJPY jumping after Trump agreed to meet Kim Jong Un in an unprecedented summit; meanwhile, Norway’s headline inflation print beat every single estimate and came in higher than the central bank’s newly reduced target, providing fodder to krone bulls. The EUR/USD dropped below 1.2300, while MXN and CAD among the strongest major currencies after Mexico and Canada’s tariff exemption. Asia’s emerging currencies were mixed as concern over U.S. metals tariffs and possible retaliation from other nations was offset by news of the first ever meeting between the leaders of the U.S. and North Korea.

Meanwhile, few investors sought the safety of Treasuries ahead of February’s non-farm payrolls data. Treasury yields rise across the curve, led by 7Y-10Y sector. Core euro-area bonds extend losses as traders build concession ahead of large supply next week.

In the commodities complex, WTI and Brent crude futures remain in close proximity to yesterday’s lows with energy newsflow relatively light ahead of today’s Baker Hughes rig count. In metals markets, spot gold remains modestly softer after yesterday’s sell-off with prices suffering from an apparent easing in geopolitical tensions. Chinese steel futures were pushed to their lowest level since November as domestic producers call on the Chinese government to increase its efforts in retaliating to Trump’s tariff plans whilst sentiment also hampered for copper prices which were seen at their lowest level since September 2017.

Expected data include non-farm payrolls, unemployment and wholesale inventories. Big Lots and American Woodmark are among companies reporting earnings. The Fed’s Evans (1.40pm, 3.45pm and 5.45pm GMT) and Rosengren (5.40pm GMT) are both expected to speak on monetary policy and the outlook following the report so that’s worth also keeping an eye on.

Market Snapshot

- S&P 500 futures little changed at 2,744.25

- STOXX Europe 600 up 0.1% to 376.93

- MXAP up 0.3% to 175.49

- MXAPJ up 0.6% to 579.41

- Nikkei up 0.5% to 21,469.20

- Topix up 0.3% to 1,715.48

- Hang Seng Index up 1.1% to 30,996.21

- Shanghai Composite up 0.6% to 3,307.17

- Sensex down 0.3% to 33,266.66

- Australia S&P/ASX 200 up 0.3% to 5,963.23

- Kospi up 1.1% to 2,459.45

- German 10Y yield rose 2.0 bps to 0.648%

- Euro up 0.02% to $1.2314

- Italian 10Y yield rose 4.1 bps to 1.728%

- Spanish 10Y yield rose 2.0 bps to 1.428%

- Brent futures up 0.6% to $63.96/bbl

- Gold spot down 0.2% to $1,319.11

- U.S. Dollar Index little changed at 90.23

Top Overnight News

- Trump hailed “great progress” in talks with North Korea. While a South Korean official said the meeting would take place by May, the White House indicated no timing has been set

- U.S. slapped a 25% tariff on steel imports and 10% on aluminum on Thursday. The U.S. excluded Mexico and Canada, a concession that will remain in place as long as they reach agreement on a new North American Free Trade Agreement that meets U.S. satisfaction

- People’s Bank of China Governor Zhou Xiaochuan said market-access reforms should be accelerated and that the world’s second-largest economy “can be bolder in opening up”; Deputy Governor Yi Gang said stable progress will be made on capital- account convertibility.

- Data released Friday showed Chinese consumer inflation climbed 2.9% in February, beating a forecast of 2.5%

- President Donald Trump and the Republican Party are being forced to put their political muscle into the race for a Pennsylvania House seat that should be theirs for the taking; it would be an embarrassing defeat for the president and yet another sign of a weakened GOP heading into the November midterm elections that will decide control of Congress

- U.K. officials don’t expect to clinch a Brexit deal until two months before exit day, in March 2019, increasing the chances of chaos for executives and lawmakers

- While news on the tariff exemption and Korean talks were seen as positive, analysts and investors said they’re waiting on follow-through actions on the summit and possible trade measures from other countries

- The Bank of Japan stayed the course with its monetary stimulus

- U.K. officials don’t expect to clinch a Brexit deal by the end of the year and privately think January is the real deadline to get an accord in time for exit day, according to people familiar with the negotiations

Asian stocks were higher across the board after the positive lead from US where on one hand President Trump confirmed aluminium and steel tariffs, but exempted NAFTA partners and was also said to be open to providing relief for allies. In addition, Asia-Pac risk appetite was further bolstered by geopolitical developments in which the South Korean National Security Office chief announced that North Korean Leader Kim is committed to denuclearization and will refrain from conducting further tests, with President Trump and North Korea’s Kim to meet by May. ASX 200 (+0.3%) and Nikkei 225 (+0.5%) were positive but with upside capped by a subdued commodities sector and weakness across steel names on Trump tariffs, while KOSPI (+1.0%) outperformed on the further appeasement in the Korean peninsula. Elsewhere, Hang Seng (+1.1%) was underpinned amid the broad positivity in the region, while Shanghai Comp. (+0.6%) somewhat lagged after PBoC inaction led to a net weekly drain of CNY 240bln, while participants also digested US tariffs alongside mixed Chinese lending and inflation data. Finally, 10yr JGBs were flat with markets focused on riskier assets and after an uneventful BoJ announcement. The PBoC skipped open market operations for a net weekly drain of CNY 240bln vs. last week’s CNY 120bln net injection.

Overnight, outgoing PBoC Governor Zhou said China’s economy will be less reliant on quantitative stimulus and that China may reduce reliance on money supply to boost growth. Responding to Trump’s tariffs, China Mofcom said it firmly opposes US trade measures and urged the US to withdraw tariffs on steel and aluminium, while it added it will take strong measures to safeguard its own interests.

Other Chinese data:

- Chinese CPI (Feb) Y/Y 2.9% vs. Exp. 2.5% (Prev. 1.5%); highest in over 4 years. (Newswires)

- Chinese PPI (Feb) Y/Y 3.7% vs. Exp. 3.8% (Prev. 4.3%)

- Chinese New Yuan Loans (CNY)(Feb) 839B vs. Exp. 900B (Prev. 2900B). (Newswires)

- Chinese Aggregate Financing (CNY)(Feb) 1.17tln vs. Exp. 1.07tln (Prev. 3.06tln)

- Chinese Money Supply M2 (Feb) Y/Y 8.8% vs. Exp. 8.7% (Prev. 8.6%)

The BoJ kept monetary policy unchanged as expected with NIRP held at -0.1% and 10yr JGB yield target at around 0%. The decision was made by 8-1 vote with board member Kataoka the dissenter, who called for the BoJ to buy JGBs so 10yr yields or longer drop further and repeated that the BoJ should clarify it will ease further if domestic factors delay reaching price target.

Top Asian News

- HNA Unloads More Land in Hong Kong as Selling Spree Picks Up

- Indonesia Orders Coal Price Cut to Shield Power Producers

- Diabetes Drug Developer Hua Is Said to Pick Hong Kong for IPO

- BOJ Keeps Stimulus Unchanged Ahead of New Term for Kuroda

- China Looks to Claw Back $1.4 Trillion in Lost Tech Listings

European bourses have seen a tame start to the session as is often the case during pre-NFP trade (Eurostoxx 50 -0.2%) with EU stocks not joining in on the gains seen overnight that came amid potential reprieve for US allies on the tariff front and a de-escalation of geopolitical tensions. Sector specific performance has been relatively broad-based thus far with some slight underperformance in material names following price action seen overnight in the metals complex. In terms of individual movers, GVC (+3.1%) leads the Stoxx 600 following their latest earnings report with Lagardere the laggard (-6.4%) after their earnings statement was met with a cold reception by the market.

Top European News

- U.K. Industry Output Jumps Amid Oil Rebound, Record Factory Run

- German Economic Momentum Moderates as Production, Exports Slip

- Czech Inflation Dips Under Target as Central Bank Halts on Rates

- Rotate Out of European Tech and Into Financials, UBS Says

In FX, USD majors are broadly split down the middle as the safer-havens underperform on latest US-NK developments and further signs that President Trump is willing to approach import tariffs on a country by country basis. Usd/Jpy has now broken free from its recent 106.00 anchor to the upside, above 106.50 and through the 20 DMA around 106.75-80, but could be contained by hefty option expiries within a new 106.50-107.00 range (1.2 bn and 3.8 bn respectively), with the upper end not just more alluring due to the size of interest at the strike, but also perhaps compelling if US jobs data is strong (wages especially). Usd/Chf is testing 0.9500, while Eur/Usd is trading either side of the 1.2300 handle and remaining lower after Thursday’s sharp reversal from initial postECB/Draghi presser peaks. In terms of tech analysis, 1.2334 seems to be capping the upside (21 DMA), while support is seen down at 1.2245 and there is also big expiry interest in close proximity with 1.8 bn running off at 1.2300 and 2.3 bn at 1.2350. The Loonie is amongst the G10 outperformers and back below 1.2900 vs the Greenback after Canada (and Mexico) got an indefinite exemption from steel and aluminium taxes pending NAFTA negotiations. However, today’s employment report offers plenty of scope for independent impetus and there are some decent option expiries that could come into play around 1.2815-25 (1.1 bn) and 1.3000 (1.6 bn). Elsewhere, Eur/Nok dropped (to sub-9.600) on stronger than expected Norwegian inflation data, with headline CPI above the new 2% target level just ahead of next week’s policy meeting. Looking at the Dollar Index, yesterday’s close above the 21 DMA at 89.820 bodes well for further recovery gains and a breach of the topside from the current circa 90.100-300 range.

In commodities, WTI and Brent crude futures remain in close proximity to yesterday’s lows with energy newsflow

relatively light ahead of today’s Baker Hughes rig count. In metals markets, spot gold remains modestly softer after yesterday’s sell-off with prices suffering from an apparent easing in geopolitical tensions. Chinese steel futures were pushed to their lowest level since November as domestic producers call on the Chinese government to increase its efforts in retaliating to Trump’s tariff plans whilst sentiment also hampered for copper prices which were seen at their lowest level since September 2017

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 205,000, prior 200,000

- Unemployment Rate, est. 4.0%, prior 4.1%

- Average Hourly Earnings MoM, est. 0.2%, prior 0.3%

- Average Hourly Earnings YoY, est. 2.8%, prior 2.9%

- Average Weekly Hours All Employees, est. 34.4, prior 34.3

- Labor Force Participation Rate, est. 62.7%, prior 62.7%

- 10:00am: Wholesale Trade Sales MoM, prior 1.2%; Wholesale Inventories MoM, est. 0.7%, prior 0.7%

Central Banks:

- 8:40am: Fed’s Evans live TV interview

- 10:45am: Fed’s Evans live TV interview

- 12:40pm: Fed’s Rosengren Speaks on Outlook

- 12:45pm: Fed’s Evans Speaks on Monetary Policy

DB’s Jim Reid concludes the overnight wrap

I spent the last night before holidays at a big DB macro dinner with most people fixated about rates, inflation, and risks to the dollar weakness view. The risks to growth due to a China slowdown did come up a few times as well which it hadn’t as much at previous similar events I’ve been at. Usually at these dinners there tends to be quite consensual themes running through the core of it. However there didn’t seem to be high conviction last night. It’s seems a combination of the vol shock, the subsequent recovery, confusion about whether yields have peaked for now and Trump’s tariff plan have left conviction low.

Before the dinner, Deutsche Bank held its 8th annual Global Bank Capital Forum in London. Every year, it brings together major investors, issuers and senior regulators to discuss the latest market and regulatory developments in banking. This year, the event was attended by 120 investors and 70 representatives of banks from Europe, North America and APAC. The keynote address was delivered by William Coen, Secretary General of the Basel Committee on Banking Supervision, and the closing speech was given by Stanley Fischer, Vice Chairman of the Federal Reserve in 2014-2017.

Moving on to today, it’s the 9th anniversary of the closing low for the S&P 500 from the GFC. How time flies. In the PDF today we show our usual performance review chart for this period. There’s also some accompanying text further down the page to mark this occasion. Today is also payrolls day and in particular we’ll get the next instalment of the averagely hourly earnings saga that last month created mayhem in financial markets (full preview below). Ahead of that we’ve just had news of the BoJ policy meeting where members voted 8-1 to keep its yield curve settings and asset purchases unchanged while the statement reiterated that inflation expectations have been “more or less unchanged”. We shall hopefully learn more from Governor Kuroda’s press conference at 3:30pm local time which is just before our note goes to print.

The other big news this morning – that could lead to lower geopolitical risks – is that the US and North Korean leaders may meet for the first time after the South Korean National Security Council Chief Chung Eui-yong said North Korean leader Kim Jong Un “expressed his eagerness to meet President Trump as soon as possible”, while Trump said he would meet Kim “by May to achieve permanent denuclearization” by the North. In Asia, markets have pared back larger gains but remain higher with the Nikkei (+0.48%), Kospi (+0.92%), Hang Seng (+0.87%) and China’s CSI 300 (+0.55%) all up. Elsewhere, China’s departing PBOC Governor Zhou noted that “when we’re pursuing quality-oriented (economic) growth, we’ll depend less heavily on the credit-base growth model”. Datawise, China’s February CPI was above market at 2.9% yoy (vs. 2.5% expected) while the PPI moderated further to 3.7% yoy (vs. 3.8% expected).

The BoJ this morning follows a market moving ECB meeting yesterday where hawkish language was spun dovishly by Draghi in the press conference leading to a big round trip for the Euro and Government bonds. In terms of language, the most significant development yesterday was the ECB dropping the pledge to increase the asset purchase programme if needed following the policy meeting. Specifically the March statement removed the sentence “if the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the asset purchase programme (APP) in terms of size and/or duration”. While a change to the easing guidance was expected, the complete removal rather than toning down or change in reaction function was a bit more of a surprise to markets.

To be fair the press conference wasn’t hugely eventful but markets reacted in a way which suggested a more dovish Draghi. When questioned on the dropping of the pledge to increase stimulus Draghi said that it was long overdue (a way of perhaps downplaying the language) and also unanimous across the council. He confirmed that the removal reflects the fact that stimulus is an “unlikely contingency now” and emphasised the improved economic backdrop now compared to 2016 when guidance was initially tinkered. Away from that, there wasn’t much change in staff economic forecasts. For growth, GDP was revised up one-tenth to 2.4% for 2018 and left unchanged in 2019 and 2020 at 1.9% and 1.7% respectively. For inflation, CPI was left unchanged in 2018 at 1.4%, revised down one-tenth in 2019 to 1.4% and left unchanged in 2020 at 1.7%. Unsurprisingly the recent escalation in tariffs and protectionist rhetoric was bought up with Draghi saying that “we are convinced that disputes should be discussed and resolved in a multilateral framework and unilateral decisions are dangerous”. He also confirmed that the ECB would assess the response of the exchange rate on the tariff discussion”.

The price action through the press conference is a little challenging to explain but clearly Draghi’s words and tone had a massive impact on changing the interpretation of the hawkish initial announcement. Indeed euro and bond yields first rose while equities sold-off however by the time Draghi was finished speaking much of those moves had fully reversed, before accelerating further in that direction into the European close. By the end of play, the euro had weakened -0.80% with a post meeting high to low range between 1.2298 and 1.2446. 10y Bunds finished 2.8bps lower at 0.625% with a post ECB range between 0.6236% and 0.700%. The ranges on BTPs and Spanish Bonds were 9bps and 8bps respectively. That weaker euro helped the likes of the Stoxx 600 and DAX to +1.05% and +0.90% respectively, as it gained from being broadly unchanged before Draghi spoke.