GOLD: $1325.20 DOWN $8.20 (COMEX TO COMEX CLOSINGS)

Silver: $16.36 UP 6 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1326.50

silver: $16.39

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR 595 FOR 59500 OZ (1.8506 tonnes)

THE COMEX IS OUT OF GOLD

For silver:

APRIL

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 19 for 90,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6738/OFFER $6841: DOWN $1(morning)

Bitcoin: BID/ $6710/offer $6810: DOWN $29 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY AND SHOCKINGLY ROSE BY 8453 contracts from 232,682 RISING TO 241,135 DESPITE YESTERDAY’S 11 CENT FALL IN SILVER PRICING. TODAY WE SET A NEW ALL TIME RECORD FOR SILVER OPEN INTEREST AND EACH AND EVERY TIME, THE PRICE OF SILVER WHEN THE RECORD WAS SET IS LOWER. OBVIOUSLY, WE HAD ZERO COMEX LIQUIDATION. HOWEVER WE ALSO WITNESSED ZERO COMEX SHORT COVERING AND THUS THE REASON FOR THE RAID TODAY..TRYING TO SHAKE SOME OF THE SILVER LEAVES FROM THE SILVER TREE. WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 3962 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 3962 CONTRACTS. WITH THE TRANSFER OF 3962 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3962 CONTRACTS TRANSLATES INTO 19.810 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX AND THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

8994 CONTRACTS (FOR 4 TRADING DAYS TOTAL 8994 CONTRACTS) OR 44.97 MILLION OZ: AVERAGE PER DAY: 2249 CONTRACTS OR 11.243 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 44.97 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.42% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 763.46 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A GIGANTIC (ATMOSPHERIC) SIZED GAIN IN COMEX OI SILVER COMEX OF 8453 DESPITE THE 11 CENT FALL IN SILVER PRICE. WE ALSO HAD ANOTHER STRONG SIZED EFP ISSUANCE OF 3962 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 3962 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A HUMONGOUS 12,415 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 3962 open interest contracts headed for London (EFP’s) TOGETHER WITH AN INCREASE OF 8453 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 11 CENTS AND A CLOSING PRICE OF $16.30 WITH RESPECT TO WEDNESDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.206 BILLION TO BE EXACT or 172% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 241,135 AND AGAIN THIS HAS BEEN SET WITH A STILL LOWER PRICE. THE PREVIOUS RECORD WAS 234,000 CONTRACTS WITH A SILVER PRICE CLOSING OF $17.89.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE OPEN INTEREST IN SILVER 241,135 CONTRACTS (OR 1.207 BILLION OZ/

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOWER PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

In gold, the open interest ROSE BY A CONSIDERABLE SIZED 6569 CONTRACTS UP TO 499,710 ACCOMPANYING THE SMALL SIZED RISE IN PRICE/YESTERDAY’S TRADING ( GAIN OF $2.90). AS WE ENTER THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A RATHER LARGE SIZED 12,098 CONTRACTS : JUNE SAW THE ISSUANCE OF 12,098 CONTRACTS AND ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 499,710. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A HUMONGOUS OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 6569 OI CONTRACTS INCREASED AT THE COMEX AND A STRONG SIZED 12,098 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 18,667 CONTRACTS OR 1,866,700 OZ =58.06 TONNES

YESTERDAY, WE HAD 691 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 39,730 CONTRACTS OR 3,973,000 OZ OR 123.57 TONNES (4 TRADING DAYS AND THUS AVERAGING: 9933 EFP CONTRACTS PER TRADING DAY OR 993,300 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 4 TRADING DAYS IN TONNES: 125.57 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 125.57/2550 x 100% TONNES = 4.92% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2168.07 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUGE SIZED INCREASE IN OI AT THE COMEX DESPITE THE SMALL SIZED GAIN IN PRICE IN GOLD TRADING YESTERDAY ($2.90 GAIN). WE HAD A VERY LARGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12098 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12098 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS NET GAIN IN OPEN INTEREST OF 18,667 contracts ON THE TWO EXCHANGES:

12098 CONTRACTS MOVE TO LONDON AND 6569 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 58.06 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $8.20 : WE HAD TWO ENTRIES IN GOLD TONNAGE AT THE GLD: 1)A WITHDRAWAL OF .29 TONNES TO PAY FOR FEES. AND 2) A DEPOSIT OF 2.06 TONNES

Inventory rests tonight: 854.09 tonnes.

SLV/

WITH SILVER UP 6 CENTS TODAY: NO CHANGES/

/INVENTORY RESTS AT 318.877 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY AN ATMOSPHERIC 8453 CONTRACTS from 232,682 UP TO 241,135 (AND A NEW COMEX RECORD SET TODAY/APRIL 5/2017. THE PREVIOUS RECORD WAS 234,787 SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89). THIS ALL OCCURRED SURPRISINGLY WITH THE FALL IN PRICE OF SILVER (11 CENTS// YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 3962 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD AGAIN ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 8453 CONTRACTS TO THE 3962 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC GAIN OF 12,415 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN APRIL (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 62.075 MILLION OZ!!!

RESULT: A HUMONGOUS SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE FALL IN SILVER PRICING / YESTERDAY (11 CENTS) . BUT WE ALSO HAD ANOTHER VERY GOOD SIZED 3962 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed HOLIDAY /Hang Sang CLOSED HOLIDAY / The Nikkei closed UP 325.87 POINTS OR 1.53%/Australia’s all ordinaires CLOSED UP .41% /Chinese yuan (ONSHORE) closed UP at 6.3033/Oil DOWN to 63.22 dollars per barrel for WTI and 68.00 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED UP AT 6.3033 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2938 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA ON HOLIDAY TODAY/CHINA RETALIATES WITH TARIFFS/LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

ii)The Central Bank of Japan now owns 77% of all ETF’s in Japan on top of just about all of Japanese Government debt.

This is an accident waiting to happen

(courtesy zerohedge)

3 c CHINA

i)Two things to be cognizant of:

- China is already declaring victory in their trade war with the uSA as they correctly state that China has targeted key industries such as autos, chemicals and of course soybeans

- China has hinted that they may wish to lower the value of the USA dollars and that means dumping their huge amount of treasuries.

( zerohedge)

ii)The way China and the uSA are going at each other, there is no way that there is going to be a settlement between them. Trump is now building an army of nations in its war against China

( zerohedge)

4. EUROPEAN AFFAIRS

i)France is a bit of a turmoil with rotating rail strikes. Macron is trying to change the hugely debt ridden public transportation rail operations Citizens of France are worried that he might privatize the rail..and that has set of the protests.

( Mac Slavo/SHFTPlan.com)

ii)The following commentary should make you think that the poisoning of Skripal and his daughter was not of Russian origins:

(courtesy Rob Slane/Blogmire.com)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia is still denied request to join the OPCW investigation into the Skripal poisoning. Very strange.

( zerohedge)

6 .GLOBAL ISSUES

( Bill Blain/Mint Partners)

7. OIL ISSUES

Bahrain discovers a massive 80 billion barrels of oil

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)A thorough presentation of how the gold market is manipulated by central banks and the BIS

( Chris Powell/GATA)

ii)So far this year, China has recorded SGE withdrawals which equal Chinese citizen demand of 534 tonnes (1/4 of the year) It seems that we will again have over 2000 tonnes of gold demanded. When you add India which has over 1000 tonnes of gold demanded, the total of just these two nations equates to over 3000 tonnes when only 2550 tonnes of gold is produced ex China ex Russia. This is why central banks are banging their heads against the wall as they are having difficulty in finding physical metal.

( Lawrie Williams)

10. USA stories which will influence the price of gold/silver

ii)USA news/data

Donald is not going to be happy as the monthly trade deficit widened to $57.6, the largest monthly deficit since the financial crisis. It seems that every country had a surplus when compared to the USA

(courtesy zerohedge)

iii)This is interesting: In March the jobs cuts amounted to 60,357 with health care leading the way. This was a 71% increase from February

(zerohedge/Challenger/Grey/Christmas)

iv)As always, David Stockman tells the truth on the USA economy and where we are headed

( David Stockman/Contra Corner)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:360,630 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 297,094 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY AN ATMOSPHERIC 8453 CONTRACTS FROM 232,682 UP TO 241,135 AND A NEW RECORD OI FOR SILVER, DESPITE OUR 11 CENT FALL IN SILVER PRICING/ YESTERDAY). ALSO,WE WERE ALSO INFORMED THAT WE HAD A FAIR 3962 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 3962. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE SURPRISINGLY AND SHOCKINGLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND SHORT COVERING BUT THAT WAS QUICKLY REMEDIED WITH TODAY’S RAID. WE ALSO HAVE A HUMONGOUS SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE OF APRIL AS WELL AS THE CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 12,415 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 8453 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 3962 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:12,415 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 5 contracts LOWERING TO 337 contracts. We had 0 notices filed upon (CME correction last Thursday night) so in essence we lost 5 contracts or 25,000 additional ounces of silver will NOT stand for delivery in this non active delivery month of April.(AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS)

The next big active delivery month for silver will be May and here the OI GAINED 3377 contracts UP to 152,557. June saw another gain of 33 contracts to stand at 33. The next big delivery month for silver is July and here the OI rose by 4377 contracts up to 52,271.

We had 0 notice(s) filed for NIL OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 5/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

1707 contracts

(170700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

595 notices

59500 OZ

1.8506 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 14 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (595) x 100 oz or 59500 oz, to which we add the difference between the open interest for the front month of APRIL. (1707 contracts) minus the number of notices served upon today (8 x 100 oz per contract) equals 230,200 oz, the number of ounces standing in this active month of APRIL (7.160 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (595 x 100 oz or ounces + {(1707)OI for the front month minus the number of notices served upon today (8 x 100 oz )which equals 230,200 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 286 COMEX OI CONTRACTS OR 28,600 OZ OF GOLD WILL NOT STAND BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

18,378.47

oz

Delaware

Brinks

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

606,231.900 oz

JPMorgan

|

| No of oz served today (contracts) |

0

CONTRACT(S

NIL OZ)

|

| No of oz to be served (notices) |

337 contracts

(1,685,000 oz)

|

| Total monthly oz silver served (contracts) | 19 contracts

(95,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 1 deposits into the customer account

i) Into JPMorgan: 606,231.900 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan deposited into its warehouses (official) today.

total deposits today: 606,231.900 oz

we had 2 withdrawals from the customer account;

i) Out of Delaware: 15,343.770 oz

ii) Out of Brinks: 3037.700 oz

total withdrawals; 18,378.47 oz

we had 0 adjustment

total dealer silver: 58.8561 million

total dealer + customer silver: 263.332 million oz

The total number of notices filed today for the APRIL. contract month is represented by 0 contract(s) FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 19 x 5,000 oz = 95,000 oz to which we add the difference between the open interest for the front month of April. (337) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 19(notices served so far)x 5000 oz + OI for front month of April(337) -number of notices served upon today (0)x 5000 oz equals 1,780,000 oz of silver standing for the April contract month

WE LOST 5 SILVER CONTRACTS OR 25,000 ADDITIONAL OUNCES WILL NOT STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 115,765 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 106058 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 106,058 CONTRACTS EQUATES TO 530 MILLION OZ OR 75.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.52% (APRIL 4/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.62% to NAV (APRIL 4/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.52%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.62%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.58%: NAV 13.65/TRADING 13.29//DISCOUNT 2.58

END

And now the Gold inventory at the GLD/

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 5/2018/ Inventory rests tonight at 854.09 tonnes

*IN LAST 356 TRADING DAYS: 86.95 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 306 TRADING DAYS: A NET 69.35 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 5/2018: NO CHANGES IN SILVER INVENTORY:

Inventory 318.877 million oz

end

6 Month MM GOFO 2.04/ and libor 6 month duration 2.46

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.04%

libor 2.46 FOR 6 MONTHS/

GOLD LENDING RATE: .42%

XXXXXXXX

12 Month MM GOFO

+ 2.48%

LIBOR FOR 12 MONTH DURATION: 2.68

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.20

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Silver Bullion: Should We Be Worried About Silver?

Silver Bullion: Should We Be Worried About Silver?

– Bloomberg’s Mike McGlone silver “set to test the $18 an ounce resistance level”

– LBMA report: volume of silver ounces transferred in February fell by 24%

– Standard Chartered: gold-silver ratio and supply/demand fundamentals favour silver

– Gold/silver ratio at near two-year high on silver’s underperformance

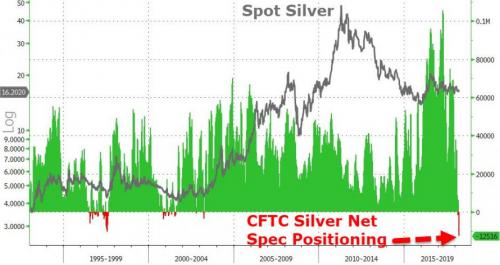

– Silver COT reports remain more bullish than at any time in history

– Silver expected to outperform gold as macro and industrial factors begin to drive price

The silver price has perhaps disappointed many investors of late. Two key institutional metrics released in the last fortnight may have made things worse, however not all is at it seems.

The latest silver COT reports have shown that Managed Money positions are net bearish, the most recent is for the seventh week in a row. Meanwhile an LBMA report this week shows that the volume of silver transferred in February fell by 24%.

Whilst both of these suggest that the silver price might continue to resist further climbs, the contrarian perspective suggests otherwise. Analysis of past COT reports, previous gold/silver ratios and a close look at macro fundamentals should give investors (and those considering buying silver) reassurance that the silver price could be set to make some key moves.

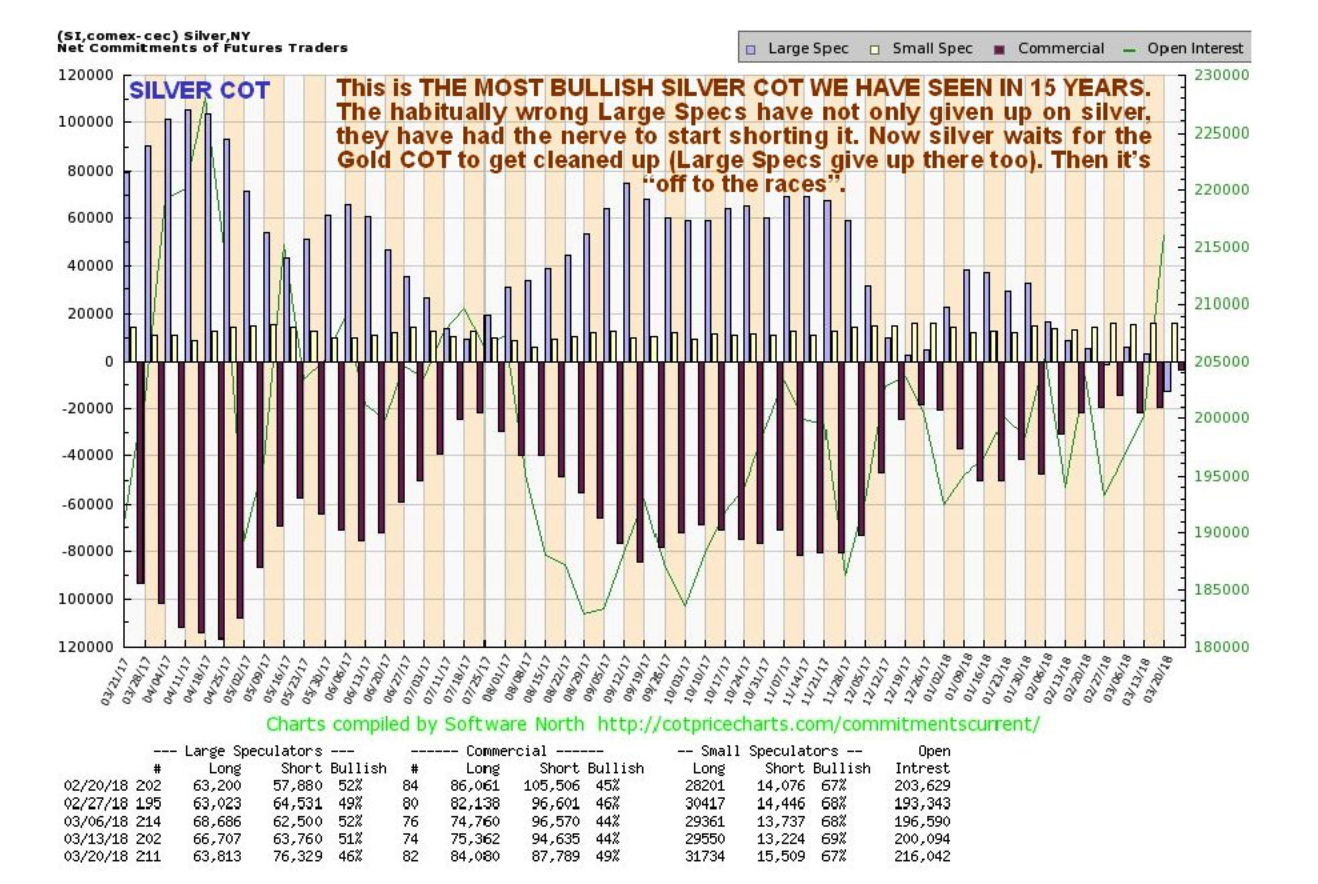

COT report

Last week’s COT data showed Managed Money positions hold are net bearish for the 7th week in a row. This is the longest net negative stretch in over three years (since late 2014).

The March 20 COT report ‘showed an all-time record high Large Speculator NET short position and an all-time record low Commercial NET short position with the Small Specs as the only category still showing a small NET long position.’

As we explained last week, COT data shows that ‘we are close to bottoming and suggests that both gold and silver should make gains in the coming weeks and months. The data showed that the hedge funds and “Managed Money traders,” the “dumb money” speculators now have record short positions in silver.’

At the same time, the large commercials and including large bullion banks such as JP Morgan, the “smart money” and the “inside money” have reduced their shorts dramatically and are now long.

The COT report shows ‘Managed money’ silver specs have their largest short position in at least 28 years and maybe ever. From a contrarian perspective this is very bullish.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Usually we would expect gold and silver to behave similarly when it comes to the futures market as generally the same factors affect both metals. Whilst recent silver COT reports showing large speculators giving up on and even shorting silver is (from a contrarian perspective) extremely bullish, there is a paradox with the gold COTs which are arguably bearish. Many analysts believe this is a positive sign that the silver price is set to climb, but not before falling.

In recent weeks we have commented on the divergence occurring between both gold and silver.

‘What does this mean? One possible explanation is that silver has gotten too cheap relative to gold and needs to be revalued. That could happen in several ways, with both metals rising but silver rising more, or both falling but silver falling less. Or with gold dropping while silver rises, as improbable as that seems.’

In order for the silver price to climb it likely requires a retreat in the gold price before recovering alongside it. In short, the current silver indicators show a short-term weakness followed by a strong rebound.

Bloomberg Intelligence’s Mike McGlone wrote in a recent report “Silver’s 52-week range is the most compressed in 15 years and appears unsustainable…Silver’s extreme compression projects a revisit of 2016’s high. Sustaining below the December low would indicate failure.”

Why should we expect a recovery in the silver price? “Because of the gold price” is clearly not a reasonable enough answer. Standard Chartered said in a recent report that they expect fortunes to turn for silver this year as the weaker dollar and rising inflation expectations will see investors seek out safe havens alongside gold. Many of the factors driving gold will begin to affect silver as well. Additionally silver is both a monetary and industrial metal which means it listens to two tunes when performing.

Gold/silver ratio

This week the gold/silver price ratio has so far remained above 81. This is gold at its most expensive in relation to silver, since the early 1990s. Since the start of the millennium the ratio has been trading in a range of 80 and 47. Silver is extremely undervalued in both the short and long-term.

ICBC’s Marcus Garvey said in a report last week, “Inevitably, given the historical precedent, [the ratio level] has raised the question of whether bullion investors are being presented with a contrarian opportunity to position for a reversal…In the very short-term, we think the answer is yes.”

As in any market and with any asset the ratio could yet head higher, but how much higher must be considered in respect of the key fundamentals. For example, the current breakeven price for the primary silver mining industry is about $15-$16. The current price point is not sustainable.

The gold/silver ratio has never remained at 80 (or above) for very long before decreasing. This suggests that the window of opportunity to stock up on silver is small. According to silver seek there have been three occasions sine 1995 where the ratio registered at or above 80. The average of those days is 47. We have just exceeded the historical average in this latest range.

John Rubino recently explained how investors can use this unusual occurrence to their advantage:

‘gold has recently been rising relative to silver (or silver has been falling relative to gold) with the gold/silver ratio now close to 80, meaning that it takes 80 ounces of silver to buy one ounce of gold. It’s been there two other times in the past decade and both times gold subsequently rose while silver rose a lot more.

Based on this (admittedly short) bit of recent history, an interesting trade might be to short gold and go long silver on the assumption that silver bullion will outperform gold bullion going forward. Or just stack more silver than usual for a while.

With the world’s mines producing only about 10 times as much silver as gold while silver stockpiles are dwarfed by those of gold because so much silver is used and then lost in industrial applications, this might be a trade that works for years rather than months.

Silver: the hardworking metal

Silver’s role as an industrial metal has always been impressive but no more so than since this fourth industrial revolution. It’s importance in both communication and sustainable technologies is worth noting, especially given both industries are set to expand.

In the last five years more than half of all the silver sold worldwide has been bought by industry. Less than 10% of gold is bought by the same sector.

Import figures demonstrate growing demand for silver: China’s silver imports are up 36% year-on-year so far in 2018, while India’s silver imports are up 63%. This is in large part thanks to industrial demand where mobile phone and solar cell use are mopping up supply.

“To go green, to do all the things we want to do as the human race gets off oil and gas, we need a ton of silver,” Keith Neumeyer, CEO of First Majestic Silver Corp

Silver has enormous potential in the field of technology. It is the most electrically conductive known material other than gold. Unsurprisingly gold is far too expensive to use in the majority of areas where silver makes for a viable alternative. As we find more solutions to solve energy and technology issues we will inevitably require more and more silver. Right now there is no obvious substitute for it.

Wider macro factors will drive silver

As John Rubino wrote recently, we should be careful not to look at recent institutional date in a vacuum as there are other factors that will support stronger silver prices:

‘Silver is a whole different story, with speculators going aggressively net short, something very seldom seen, and commercials almost in balance, which is also unusual. Looked at in a vacuum, this is hyper-bullish…between trade wars, massive ongoing government deficits and spiking stock market volatility, the reasons for owning safe haven assets like gold and silver are both multiplying and gaining urgency.’

The latest COT report should not be seen as a bearish sign. This is a strong indicator to accumulate silver before it breaks through this current resistance level and begins to catch up with gold. Gold has outperformed silver in the last year or so most likely thanks to safe-haven demand.

Gold is considered to be a safe play in times such as these, hence silver isn’t keeping pace with it. This is also not helped by the fact that the market perceives silver to be exposed to economic weakness. But this won’t be forever. Inflation will begin to show itself in a less covert manner. As it does so more of the public will realize silver’s second role as a store of value and inflation hedge.

Final note from Mark O’Byrne:

Silver remains very undervalued in the short term and on a long term historical basis. It is also undervalued against gold as seen in the gold silver ratio at over 80:1.

Gold is beginning to receive some interest again from a small minority of retail investors but silver remains the preserve of relatively few contrarian investors. The media and financial press rarely, if ever, covers silver and almost never in a positive manner despite its strong fundamentals.

Yet silver is quite likely in the early stages of a new bull market that will rival or surpass that of the 1970s and thus merits an allocation in investment and pension portfolios.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Related reading

Silver bullion will likely outperform gold bullion going forward

Silver Futures Report and JP Morgan Record Silver Bullion Holding Is Extremely Bullish

Silver’s Positive Fundamentals Due To Strong Demand In Key Growth Industries

News and Commentary

Gold futures pop higher as fresh China tariffs escalate trade-war fear (MarketWatch.com)

Gold hits 1-week high as dollar dips, U.S.-China trade tensions escalate (Reuters.com)

China’s Counterpunch to Trump’s Tariffs Sparks Global Selloff (Bloomberg.com)

Growth in U.S. Service Industries Cools for a Second Month (Bloomberg.com)

U.S. factory orders increase broadly in February (Reuters.com)

Gold Is Heading to $1,400 If Trade War Breaks Out, According to Sprott (Bloomberg.com)

No Exit in Sight for the World Record Holder in Negative Rates (Bloomberg.com)

Three Mini-Bubbles Burst. Is One Of The Big Ones Next? (DollarCollapse.com)

Matt King: This Is The Real Reason Behind The Blow Out In Libor-OIS (ZeroHedge.com)

Goldman Sachs: 20 Years Left of Mineable Gold (ProActiveInvestors.co.uk)

Gold Prices (LBMA AM)

04 Apr: USD 1,343.15, GBP 955.52 & EUR 1,092.79 per ounce

03 Apr: USD 1,336.60, GBP 949.65 & EUR 1,085.99 per ounce

29 Mar: USD 1,323.90, GBP 941.69 & EUR 1,075.80 per ounce

28 Mar: USD 1,341.05, GBP 946.24 & EUR 1,082.23 per ounce

27 Mar: USD 1,350.65, GBP 954.64 & EUR 1,087.41 per ounce

26 Mar: USD 1,348.40, GBP 949.27 & EUR 1,086.95 per ounce

23 Mar: USD 1,342.35, GBP 952.80 & EUR 1,088.65 per ounce

Silver Prices (LBMA)

04 Apr: USD 16.46, GBP 11.72 & EUR 13.40 per ounce

03 Apr: USD 16.52, GBP 11.78 & EUR 13.44 per ounce

29 Mar: USD 16.28, GBP 11.58 & EUR 13.21 per ounce

28 Mar: USD 16.46, GBP 11.63 & EUR 13.28 per ounce

27 Mar: USD 16.64, GBP 11.79 & EUR 13.41 per ounce

26 Mar: USD 16.61, GBP 11.67 & EUR 13.39 per ounce

23 Mar: USD 16.53, GBP 11.70 & EUR 13.39 per ounce

Recent Market Updates

– Martin Luther King Jr. Anniversary: Reminds Us Of Costs Of War To Society and Financial System

– Gold Outperforms Stocks In Q1, 2018

– Brexit, Stagflation Pressures UK High Street

– Gold Is Money While Currencies Today Are “IOU Nothings”

– “Stars Are Slowly Aligning For Gold” – Frisby

– Uncle Sam Issuing $300 Billion In New Debt This Week Alone

– Eurozone Faces Many Threats Including Trade Wars and “Eurozone Time-Bomb” In Italy

– Silver Futures Report and JP Morgan Record Silver Bullion Holding Is Extremely Bullish

– London House Prices Falling Sharply – UK’s Much Needed Wake-Up Call

– Global Trade War Fears See Precious Metals Gain And Stocks Fall

– Gold +1.8%, Silver +2.5% As Fed Increases Rates And Trade War Looms

– Credit Concerns In U.S. Growing As LIBOR OIS Surges to 2009 High

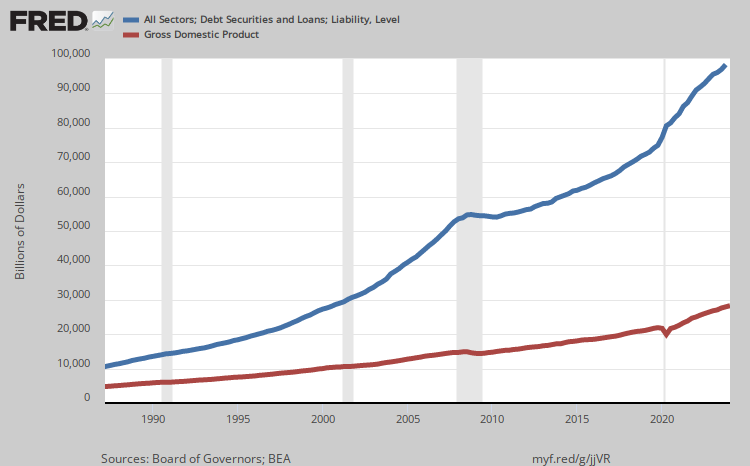

– Four Charts: Debt, Defaults and Bankruptcies To See Higher Gold

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

A thorough presentation of how the gold market is manipulated by central banks and the BIS

(courtesy Chris Powell/GATA)

Chris Powell: Gold market manipulation update, April 2018

Submitted by cpowell on Wed, 2018-04-04 15:23. Section: Documentation

Gold Market Manipulation Update

Remarks by Chris Powell

Secretary/Treasurer, Gold Anti-Trust Action Committee Inc.

Mining Investment Asia Conference

Marina Bay Sands, Singapore

Wednesday, March 28, 2018

Mines and Money Asia Conference

Hong Kong Exhibition and Convention Centre

Wednesday, April 4, 2018

The slides for this presentation are posted here:

http://gata.org/files/GoldMarketManipulationUpdateApril2018Slides_0.pdf

Slide 1 — Title

Since we were here last year some big changes have occurred in the international gold price suppression policy. These changes indicate growing tightness in the gold market — indicate that governments and central banks are having to work harder to keep the price down.

First, the Bank for International Settlements, the association of major central banks, has jumped back into the gold market

GATA consultant Robert Lambourne, who seems to be the only analyst outside government who studies the gold market interventions of the BIS, notes that footnotes in the BIS’ monthly reports show that the bank’s gold, gold swap, and gold derivative positions exploded from zero in March 2016 to 438 tonnes in March 2017 to 525 tonnes last month:

http://www.gata.org/node/18090

http://www.gata.org/node/18022

Slide 2 — BIS / Notes to the financial statements

This page is taken from the BIS annual report issued in June, covering the year ending March 31, 2017. It acknowledges 438 tonnes of gold swaps.

Slide 3 — BIS / Statement of account

This page, from the BIS’ October 2017 statement of account, shows that the BIS’ gold loans rose substantially since March last year.

What exactly is the BIS doing in the gold market and for whom?

In November I brought Lambourne’s analysis to the attention of the BIS press office and asked if his analysis was correct and if the bank could explain exactly what it was doing in the gold market and for whom. The BIS press office replied:

http://www.gata.org/node/17793

“We do not comment on specific accounts and holdings of central banks or of the BIS. Please see our latest annual report for details on gold. Further information can be gleaned from central banks directly.”

But the BIS’ annual reports provide no more substantial information about its activity in the gold market than its monthly reports do. As for obtaining information about gold market activity from BIS member central banks, they are no more forthcoming.

A few years ago GATA sued the Federal Reserve in U.S. District Court in Washington for access to its gold market records. We received very little access, since the court ruled that nearly all the Fed’s gold records are exempt from disclosure. Indeed, the most notable information we got by suing the Fed was the possibly inadvertent admission in writing by a member of the Fed’s Board of Governors, Kevin M. Warsh, that the Fed has gold swap arrangements with foreign banks and will never disclose them.

http://www.gata.org/files/GATAFedResponse-09-17-2009.pdf

Slide 4 — Warsh photo and letter

If the swapping and leasing of gold by central banks is ordinary and innocent activity, why won’t central banks disclose and explain it?

The answer to that question was given by the secret March 1999 report of the staff of the International Monetary Fund, which acknowledged that central banks conceal their gold swaps and leases to facilitate their secret interventions in the gold and currency markets:

http://www.gata.org/node/12016

http://www.gata.org/files/IMFGoldDataMemo–3-10-1999.pdf

Slide 5 — Secret IMF report

* * *

The second biggest development in the gold price suppression scheme since we last gathered here involves the New York Commodities Exchange –

Slide 6 — NYMEX/COMEX building

— where, GATA consultant Harvey Organ reports, thousands of gold futures contracts that have been called for delivery have been moved off the exchange in private transactions called “exchange for physicals,” or EFPs.

One implication of this development is that there isn’t enough gold in Comex warehouses to cover futures deliveries sought in New York and that deliveries have to be moved to London, where transactions are more easily concealed by mechanisms controlled by the London Bullion Market Association, or where long contract holders seeking delivery can be paid privately to postpone delivery.

There may be other explanations for this development, but it is recent and signifies that something big has changed about the gold market in the last year.

* * *

Perhaps not so coincidentally, as gold researcher Ronan Manly of Bullion Star in Singapore disclosed the other day, on April 1 the London Bullion Market Association —

Slide 7 — LBMA building

— will begin delaying its daily gold and silver auction price reports. Recently the auction price reports have been issued 30 minutes after the conclusion of the auctions. As of April 1 the auction price reports will be delayed 14 hours. The LBMA has provided no explanation for this delay, but of course the longer the reports are delayed, the more opportunity there will be to adjust or tamper with them.

Further, Manly discloses, the LBMA has postponed for another year its plan to start reporting individual trades of gold and silver. If something nefarious is going on with those “exchange for physicals” by which Comex futures contracts appear to be transferred to London, the LBMA’s reporting of individual trades might reveal it. Now there will be no reporting by the LBMA of individual gold and silver trades in London for at least another year:

http://www.gata.org/node/18094

* * *

In January this year U.S. authorities charged three foreign banks and eight individuals in “spoofing” of the gold and silver futures markets:

http://www.gata.org/node/18004

https://www.reuters.com/article/us-usa-cftc-arrests/european-banks-pay-4…

Slide 8 — Reuters story on spoofing

* * *

Also in January this year GATA disclosed the discounts that are being given by CME Group futures exchanges to governments and central banks for secretly trading gold and silver futures contracts. It is not widely understood that governments and central banks are secretly trading all futures contracts on U.S. exchanges, for mainstream financial news organizations refuse to report secret interventions in markets by governments:

http://www.gata.org/node/17976

http://www.gata.org/files/CMEGroupCBIP-Q&A-December2017.pdf

Slide 9 — CME Group explainer

* * *

But maybe all you really need to know about gold price suppression could have been surmised from a story on the front page of The Wall Street Journal on August 10 last year:

http://www.gata.org/node/17562

Slide 10 — Wall Street Journal front page

In that story the newspaper quoted four experts on the gold market, all of them associates of the Gold Anti-Trust Action Committee and all of them introduced to the newspaper’s reporter by me.

Slide 11 — Close-up of Wall Street Journal story

Those four experts — gold researcher Ronan Manly, Sprott Asset Management’s John Embry, GoldMoney founder James Turk, and futures market analyst James McShirley — accused the Federal Reserve of being involved with the suppression of the gold price through the surreptitious lending and swapping of central bank gold reserves.

The Wall Street Journal story was a triumph for GATA, even though the Journal declined to mention GATA by name. (The reporter told GATA Chairman Bill Murphy that the newspaper just ran out of space.)

But the story would have been a much greater triumph for us — indeed, it would have been a triumph for free markets — if the newspaper had not decided, in reporting these complaints about surreptitious government intervention in the gold market, to violate the first rule of journalism. That’s the rule about getting and reporting both sides of a story.

The Journal reported: “Some gold bugs — investors bullish on the yellow metal — think the Fed secretly lends it out to suppress prices, partly to protect the dollar’s value. In theory the Fed can feed gold into the market through swaps with other countries.”

So where were the Journal’s questions about this for the Fed and the U.S. Treasury Department? Are the Fed and the Treasury Department involved in keeping the gold price down through surreptitious interventions, or are they not involved?

But the Journal never asked such questions, even though for a year and a half, as I provided the Journal’s reporter with the documents of these interventions, I repeatedly pressed her to put the questions to the Fed and Treasury. I even provided the Journal’s reporter with a video showing New York Federal Reserve Bank President William Dudley refusing to answer a question about gold swaps during his appearance at the Virginia Military Institute on March 31, 2016.

Slide 12 — Still photo from Dudley video

Can we play that video now?

The Dudley video can be viewed here:

https://drive.google.com/file/d/1_igBCLUsgNUx4o-O3LC764QIsaWKBAU6/view

Note the inconsistency in Dudley’s response. First he talks at length about the German Bundesbank’s transactions to repatriate its gold from the New York Fed. Then, asked if the Fed is involved with gold swaps, Dudley says he can’t comment on “individual customer kind of transactions.” But he had just discussed an individual customer’s transactions with the Fed at great length — Germany’s — and the second question, about gold swaps, was not about individual customer transactions at all but simply whether the Fed was in the gold swap business.

Ordinarily news organizations are most interested in questions that high government officials refuse to answer. But mainstream financial news reporters are not interested in questions about secret government interventions in the gold market and secret interventions in markets generally. No, such questions are too sensitive, apparently considered threats to national security.

The best that mainstream financial news organizations can do is just to acknowledge the questions sometimes. Mainstream financial news organizations can never pursue the answers, no matter how easy it would be to do so.

Unfortunately most gold market analysts themselves will not pursue these questions either — at least not yet. GATA will continue working on them.

Will the gold industry itself ever pursue these questions? Will the gold industry ever stand up for itself?

If not, why should anyone invest in an industry that doesn’t care about the suppression of the price of its product?

Slide 13 — Contact and thanks

The documents I have cited today are all posted at GATA’s internet site, GATA.org, most of them in the “documentation” section:

http://www.gata.org/taxonomy/term/21

If you have any trouble locating them or have any questions about GATA’s work, I’ll be glad to hear from you at CPowell@GATA.org.

Thanks for your kind attention.

end

So far this year, China has recorded SGE withdrawals which equal Chinese citizen demand of 534 tonnes (1/4 of the year)

It seems that we will again have over 2000 tonnes of gold demanded. When you add India which has over 1000 tonnes of gold demanded, the total of just these two nations equates to over 3000 tonnes when only 2550 tonnes of gold is produced ex China ex Russia. This is why central banks are banging their heads against the wall as they are having difficulty in finding physical metal.

(courtesy Lawrie Williams)

LAWRIE WILLIAMS: China’s SGE gold withdrawals higher in Q1

China’s Shanghai Gold Exchange has just published its gold withdrawal data for March and so far this year the figure is a little higher than last year, when the full year total was a little over 2,030 tonnes, and 5% up on 2016 Q1 withdrawals when the annual total was just over 1,970 tonnes. Some analysts equate SGE gold withdrawals to total Chinese gold demand, while others may disagree, but the fact remains that the withdrawal figures on an annual basis are far closer to the sum of known Chinese gold imports, plus China’s own gold output, plus a figure for scrap conversion, than other estimates of Chinese gold demand, which tend to be somewhat limited as to what demand categories are included by the analysts in their calculations.

Table: SGE Monthly Gold Withdrawals (Tonnes)

| Month | 2018 | 2017 | 2016 | % change 2017-2018 | % change 2016- 2018 |

| January | 223.58 | 184.41 | 225.08 | +21.2% | -0.7% |

| February* | 118.42 | 148.24 | 107.60 | -20.1% | +10.7% |

| March | 192.61 | 192.25 | 183.24 | +0.2% | +5.1% |

| April | 165.78 | 171.40 | |||

| May | 138.08 | 147.28 | |||

| June | 155.51 | 138.51 | |||

| July | 144.71 | 117.58 | |||

| August | 161.41 | 144.44 | |||

| September | 214.24 | 170.90 | |||

| October | 151.54 | 153.25 | |||

| November | 189.10 | 214.72 | |||

| December | 185.21 | 196.37 | |||

| Year to date | 534.61 | 524.90 | 515.92 | + 1.8% | +3.6% |

| Full Year | 2,030.48 | 1,970.37 |

Source: Shanghai Gold Exchange. Lawrieongold.com

It is encouraging in terms of global gold demand patterns that Q1 SGE gold withdrawals are up on those of the past two years and taking the whole of Q1 that irons out the anomalies surrounding the Chinese New Year holiday period given its variable dates year to year. What will need watching now, given the apparent sharp fall in gold output from the Chinese domestic mines whether this shortfall, estimated by Metals Focus at around 35 tonnes, will be made up in additional SGE withdrawals, or indeed in gold imports, to satisfy what many observers see as strengthening Chinese gold demand this year.

Thus so far this year Chinese gold demand, as represented by SGE withdrawals is holding up well compared with the past two years – indeed is a little higher, but still well down on the record 2015 figure when Q1 withdrawals totalled 625 tonnes and the full year total a massive 2,596 tonnes.

05 Apr 2018

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3033 /shanghai bourse CLOSED / HANG SANG CLOSED

2. Nikkei closed UP 325.87 POINTS OR 1.53%/ /USA: YEN RISES TO 107.08/

3. Europe stocks OPENED DEEPLY IN THE GREEN /USA dollar index RISES TO 90.25/Euro FALLS TO 1.2263

3b Japan 10 year bond yield: RISES TO . +.046/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.08/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 63.22 and Brent: 68.00

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.521%/Italian 10 yr bond yield UP to 1.748% /SPAIN 10 YR BOND YIELD UP TO 1.172%

3j Greek 10 year bond yield FALLS TO : 3.978?????????????????

3k Gold at $1328.75 silver at:16.29 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 15/100 in roubles/dollar) 57.58

3m oil into the 63 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.08 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9618 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1794 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.521%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.8192% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.0568% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures Rise, Global Stocks Rebound As Trade War Fears Ease

Stocks across the globe rose in a continuation of yesterday’s euphoric rally that sent the Dow Jones nearly 1000 points higher from its session lows, as the moderation of trade war rhetoric – despite the tit-for-tat tariff announcements by China and the US – lifted risk sentiment across the board. As a result, whereas yesterday’s market snapshot was a sea of red, this morning it’s green as far as the eye can see.

US TSY yields rose back over 2.80% (just shy of 2.82% as of this moment) as the dollar and commodities strengthened, while safe-haven assets including the yen and gold slipped.

In a dramatic, if low-volume, reversal, which according to many strategists was largely one widespread short squeeze, all major indices recovered from Wednesday’s initial sharp losses after US and China’s tit-for-tat tariff announcements, however fears later apparently were soothed as representatives from China and the U.S. left the door open for a negotiated solution to trade disputes. The improvement in sentiment was helped by comments from White House economic adviser Kudlow who stated that the US measures were a form of trade negotiations and that Trump’s tariffs on China are all proposals, while he added that backchannel talks with China were occurring. Furthermore, the White House noted there will be a couple of months before China tariffs are implemented with the review period ongoing, and some analysts also viewed the impact from proposed tariffs to be

manageable. It is still unclear how – or why – either Trump or Xi will show weakness and concede in the ongoing negotiations.

“I think that the substance of trade restrictions and their real impact will be far less than the headlines,” said Jeffery Becker, CEO of Jennison Associates who summarized the prevailing mood quite well. “U.S. and Chinese cross-border trade has grown significantly over the last decade and economic inter-dependence runs very deep, deeper than the actual trade numbers.”

At the same time, some argue that the global economy is currently running so well that it could even cope with the impact of the proposed tariffs, which cover a fraction of world trade. “We’ve had a few months now where markets have really been going sideways and progressively lower, but at the same time has data really rolled over? The answer is no,” Geoffrey Yu, head of the UK investment office at UBS Wealth Management, said. “The underlying economy is actually chugging along which will increase the scope for upside surprises on the corporate front, on the economic front and at some point markets will have to catch up to that.”

Meanwhile, Federal Reserve officials also chimed in and said it’s premature to fully assess the impact of the trade dispute, which is adding uncertainty to an otherwise bright economic outlook. A board member, Lael Brainard, said trade policy is “certainly something that I take into account, in thinking about risks.”

In any case, S&P futures also advanced after the S&P 500 Index on Wednesday erased a loss to close up 1.2% and were another 0.4% higher this morning, as the VIX slides back under 20.

Despite yesterday’s thundering reversal which from a loss of -2% ended up being a gain of over 1%, the biggest such intraday move since 2011, volatility is clearly back, and as the following Bloomberg chart shows, Wednesday was the 26th move of 1% or more this year, already triple the 2017 total.

One of the culprits of the recent tech wreck, Facebook, erased earlier losses in pre-market trading and was on pace to extend Wednesday’s gains as traders appeared unfazed by company disclosure that data on most of its 2 billion users could have been accessed improperly. According to Bloomberg, “investors are cautiously returning to technology shares after a selloff last month gave momentum to a global equity correction.”

Most of Asia’s major markets rose, even though China, Hong Kong and Taiwan were closed for holidays. Australia’s ASX 200 (+0.5%) and Nikkei 225 (+1.5%) were higher with strength in Australia’s largest weighted financials sector leading the local index, and the Japanese benchmark was among the outperformers as exporters cheered a weaker JPY. Elsewhere, KOSPI (+1.2%) also advanced and Straits Times Index (+2.0%) saw its largest intraday gain in over a year alongside the rising tide across stocks.

Having closed for the day before yesterday’s US short squeeze really kicked in, European stocks have advanced for the first time this week, following global peers higher, amid optimism that the U.S. and China will step back from a full-blown trade war, and boosted by a weaker euro propping up exporters. The Stoxx 600 climbs 1.6% with nearly 90% of its components in the green as mining, tech and autos lead gains.

Among regional benchmarks, Germany’s exporter-heavy DAX Index climbed the most aided by a slump in the Euro. Financials are higher as banks benefit from the US 10y yield rising back above 2.80%. In terms of stock specifics, Telecom Italia (+3.0%) is higher on sources reporting Italian state lender CDP is to purchase a 5% stake in the company. Sophos Group soars 18% after the company said it anticipates full-year reported billings growth toward the top end of the previously guided growth range. Lagging behind, Just Eat (-3.3%) is failing to deliver on the back of a downgrade by JP Morgan.

In global macro, the dollar strengthened while safe-haven assets including the yen slipped. The USDJPY briefly rose above 107 while the USDTRY hit record highs due to concerns of further rate cuts and reports of Deputy PM resigning. BRL is likely to be in focus as Lula appeal is rejected, Brazil ETF rallies in Asian trading. Elsewhere, Australia’s dollar led declines against the greenback after the country’s money-market rate fell for the first time in almost two months.

In fixed income the core has been pressured by general positive tone as curves steepen; Spanish bonds underperform after a poor 30y auction with large tail; France unusually sells toward bottom end of indicative auction range which also weighs.

Ooil prices extended their post-DoE gains (May ’18 crude WTI futures hovering around USD 63.50/bbl) amid the easing of trade war fears. Gold has lost support from safe-haven flows with prices pulling back from one-week highs as the risk tone returns to the market. Copper traded sideways during Asia hours with its largest consumer China shut for the rest of the week due to holidays, while improved market sentiment lifted London copper, which has recouped the losses seen in the previous session. Elsewhere, Shanghai aluminium stocks tumbled for the first time in nine months. Copper futures well supported, spot gold grinds lower.

Market Snapshot

- S&P 500 futures up 0.4% to 2,656.25

- STOXX Europe 600 up 1.5% to 372.66

- MSCI Asia Pacific up 0.6% to 171.90

- MSCI Asia Pacific ex Japan up 0.6% to 560.40

- Nikkei up 1.5% to 21,645.42

- Topix up 1.1% to 1,724.61

- Hang Seng Index down 2.2% to 29,518.69

- Shanghai Composite down 0.2% to 3,131.11

- Sensex up 1.5% to 33,506.31

- Australia S&P/ASX 200 up 0.5% to 5,788.81

- Kospi up 1.2% to 2,437.52

- German 10Y yield rose 1.7 bps to 0.517%

- Euro down 0.1% to $1.2262

- Italian 10Y yield fell 5.2 bps to 1.488%

- Spanish 10Y yield rose 1.6 bps to 1.182%

- Brent futures unchanged at $68.02/bbl

- Gold spot down 0.5% to $1,326.35

- U.S. Dollar Index up 0.1% to 90.24

Top Overnight News

- The U.S. and China indicated they’re willing to negotiate on escalating frictions, helping to ease fears among investors that a tit-for-tat trade dispute could derail the strongest global expansion in years

- White House economic adviser Larry Kudlow stressed U.S. tariffs announced on Chinese goods are still only proposals that might never take effect as the Trump administration sought to tamp down fears of a trade war

- U.S. President Donald Trump said a trade war with China was “lost many years ago” by his predecessors, sounding a defiant tone amid tumult in financial markets a day after his administration slapped tariffs on 1,333 Chinese products

- Barclays Plc’s debt ratings were cut to one level above junk by Moody’s Investors Service, after the U.K. bank separated its investment banking activities from retail operations to comply with new rules

- The most accurate pound forecasters are keeping calm and see the currency climbing more than 8 percent this year

- The U.K. Financial Conduct Authority wants asset managers to disclose more information about how they measure their performance, ramping up pressure on active funds to justify their charges

- Brazil’s Supreme Court has rejected former President Luiz Inacio Lula da Silva’s plea to remain at liberty while appealing a 12-year prison sentence for corruption, paving the way for the imprisonment of the front-runner in October’s elections

- Yellen spoke at a private event 2 months after leaving the Fed; she said she considered inflation to be in check and unlikely to spike, so rates would stay relatively low, according to people familiar

- Nikkei: Kim Jong Un had shown intent to return to 6-party talks on denuclearization when he met with China’s President Xi according to people familiar

- Eurozone Mar. Services PMIs: Spain 56.2 vs 56.1 est; Italy 52.6 vs 53.9 est; France 56.9 vs 56.8 est; Germany 53.9 vs 54.2 est; Markit note salary pressures within Spanish, Italian and German reports

- U.K. Mar. Services PMI: 51.7 vs 54.0 est; bad weather in March a key factor holding back number

Asian stocks traded mostly higher as the region sustained the momentum from Wall St where all major indices recovered from the initial losses seen after US and China’s tit-for-tat tariff announcements, with fears later soothed as the US hinted at a willingness for negotiations. The improvement in sentiment was helped by comments from White House economic adviser Kudlow who stated that the US measures were a form of trade negotiations and that Trump’s tariffs on China are all proposals, while he added that back-channel talks with China were occurring. Furthermore, the White House noted there will be a couple of months before China tariffs are implemented with the review period ongoing, and some analysts also viewed the impact from proposed tariffs to be manageable. As such, ASX 200 (+0.5%) and Nikkei 225 (+1.5%) were higher with strength in Australia’s largest weighted financials sector leading the local index, and the Japanese benchmark was among the outperformers as exporters cheered a weaker JPY. Elsewhere, KOSPI (+1.2%) also advanced and Straits Times Index (+2.0%) saw its largest intraday gain in over a year alongside the rising tide across stocks, while mainland China, Hong Kong and Taiwan remained shut for holidays. Finally, 10yr JGBs were subdued following losses in T-notes and with safe-havens shunned amid the heightened risk appetite, while an enhanced-liquidity auction in the super-long end also kept participants side-lined during early trade and after results showed weaker demand

Top Asian News

- Second-Biggest Pakistan Bank Targets ‘Enormous’ Youth Market

- Japan Seeks Jump in Green Bond Issuance With State Backing

- Singer Stake Looms Over Hyundai’s Plan for Smooth Succession

- Japan’s Foreign Stock Investors Come Back After 11-Week Hiatus

European bourses opened higher with 88% of the Stoxx 600 in the green as it sustained the momentum and risk appetite from Wall St. and Asia. The improvement in sentiment was aided by comments from White House economic adviser Kudlow stating that the US measures were a form of trade negotiations and that Trump’s tariffs on China are all proposals, while he added that backchannel talks with China were occurring. All sectors sit firmly in the green with material and technology names top-performers. Financials are also higher as banks benefit from the US 10y yield rising back above 2.80%. In terms of stock specifics, Telecom Italia (+3.0%) is higher on sources reporting Italian state lender CDP is to purchase a 5% stake in the company. Lagging behind, Just Eat (-3.3%) is failing to deliver on the back of a downgrade by JP Morgan.

Top European News

- Steinhoff Bows to Pressure Over Bonus Payments After Outrage

- Danske Executive Behind Baltic Unit Quits Amid Laundering Probe

- Cassa Depositi May Buy Up to 5% of Telecom Italia: Il Sole

- U.K. Economy Battered by the ‘Beast From the East’ Snowstorm

Commodities:

- DXY: The Index looks a bit more comfortable back above the psychological 90.000 level and with the Greenback firmer vs all G10 peers, bar the Loonie that continues to glean encouragement from broadly constructive NAFTA developments (negotiations said to be progressing well, albeit with some major issues yet to be resolved, and on track for an agreement in principle by mid-April). A truce or rather a time out for talks between the US and China on proposed import tariffs has calmed trade war fears, underpinning the Dollar and risk sentiment in general to the detriment of traditional safe-havens. However, the DXY really needs to reclaim 90.500 and above to maintain momentum vs highs around 90.335 thus far.

- CAD: Bucking the broader trend due to the aforementioned positive NAFTA impulses and back near recent peaks vs the Usd within 1.2780-45 parameters ahead of Canadian (and US) trade data.

- CHF: Also a bit of an outlier among majors with firmer than forecast Swiss CPI data supporting the Franc between 0.9600-30 and 1.1790-1.1805 vs the Usd and Eur respectively, but the Chf still not really trading like a safe-haven amidst market talk of SNB intervention.

- GBP: Another mover on independent factors, or to be precise in the run up to a much weaker than expected UK services PMI, with Cable drifting back from yet another test of 1.4100 resistance/multiple tops to around 1.4035 and Eur/Gbp nudging towards 0.8740.

- EUR: Losing more ground from recent 1.2300+ peaks vs the Usd and seriously probing stops around 1.2250 ahead of more layered bids in the 1.2240-20 area and decent tech support at the upper end of that range.

- JPY: Also extending losses vs the Usd and the headline pair probing a bit higher above 107.00, but not quite challenging offers said to be sitting at 107.20 and 107.30, which could expose stops above the 107.33 level (55 DMA).

In commodities, oil prices extended their post-DoE gains (May ’18 crude WTI futures hovering around USD 63.50/bbl) amid the easing of trade war fears after US officials said they are open to negotiations with China over tariffs. Gold has lost support from safe-haven flows with prices pulling back from one-week highs as the risk tone returns to the market. Copper traded sideways during Asia hours with its largest consumer China shut for the rest of the week due to holidays, while improved market sentiment lifted London copper, which has recouped the losses seen in the previous session. Elsewhere, Shanghai aluminium stocks tumbled for the first time in nine months. Qatar oil energy minister says OPEC and non-OPEC should continue cooperation over oil market.

Looking at the day ahead, in the US, data due include weekly initial jobless claims and the February trade balance reading.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior -4.3%

- 8:30am: Initial Jobless Claims, est. 225,000, prior 215,000; Continuing Claims, est. 1.84m, prior 1.87m

- 8:30am: Trade Balance, est. $56.8b deficit, prior $56.6b deficit

- 9:45am: Bloomberg Consumer Comfort, prior 56.8

DB’s Jim Reid concludes the overnight wrap