GOLD: $1346.40 DOWN $ 4.25 (COMEX TO COMEX CLOSINGS)

Silver: $17.25 UP 3 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1345.75

silver: $17.26

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR 665 FOR 66500 OZ (2.068 tonnes)

THE COMEX IS OUT OF GOLD

For silver:

APRIL

81 NOTICE(S) FILED TODAY FOR

405,000 OZ/

Total number of notices filed so far this month: 460 for 2,300,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8039/OFFER $8139: up $32(morning)

Bitcoin: BID/ $8199/offer 8299: UP $80 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1355.45

NY price at the same time: 1349.20

PREMIUM TO NY SPOT: $6.25

Second gold fix early this morning: 1354.11

USA gold at the exact same time: 1351.30

PREMIUM TO NY SPOT: $2.81

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A STRONG 7362 CONTRACTS FROM 214,297 RISING TO 221,659 ACCOMPANYING YESTERDAY’S GOOD 44 CENT GAIN IN SILVER PRICING. AFTER A STRING OF 6 CONSECUTIVE DAYS OF DROPS IN OPEN INTEREST, WE NOW HAVE TWO CONSECUTIVE OI GAINS. . WE WERE AGAIN NOTIFIED THAT WE HAD AN ATMOSPHERIC SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 9532 EFP’S FOR MAY , 100 CONTRACTS FOR JUNE, 170 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL SKY BOUND ISSUANCE OF 9802 CONTRACTS AND IT IS THE HIGHEST EVER ISSUED AS FAR AS I HAVE BEEN RECORDING THESE ENTRIES!!!. WITH THE TRANSFER OF 9802 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 9802 EFP CONTRACTS TRANSLATES INTO 49.01 MILLION OZ ACCOMPANYING 1.THE RISE IN SILVER PRICE AT THE COMEX AND 2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

48,623 CONTRACTS (FOR 14 TRADING DAYS TOTAL 48,623 CONTRACTS) OR 243.115 MILLION OZ: AVERAGE PER DAY: 3,473 CONTRACTS OR 17.3653 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 243.115 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 34.73% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 961.245 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A HUGE SIZED GAIN IN COMEX OI SILVER COMEX OF 7362 WITH THE 44 CENT GAIN IN SILVER PRICE. THE CME NOTIFIED US THAT WE HAD AN ATMOSPHERIC AND RECORD SIZED EFP ISSUANCE OF 9802 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA 9532 EFP’S WERE ISSUED FOR THE MONTH OF MAY, 100 EFP’S FOR JUNE AND 170 EFP CONTRACTS FOR JULY, FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A WHOPPING 17,513 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 9802 open interest contracts headed for London (EFP’s) TOGETHER WITH AN INCREASE OF 7362 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE STRONG RISE IN PRICE OF SILVER OF 44 CENTS AND A CLOSING PRICE OF $17.22 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH. THE BANKERS USED ALL OF THEIR PAPER MUSCLE AND THE KITCHEN SINK TO PREVENT SILVER FROM FLYING INTO THE 18 DOLLAR COLUMN.

In ounces AT THE COMEX, the OI is still represented by WELL OVER 1 BILLION oz i.e. 1.108 BILLION TO BE EXACT or 158% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 81 NOTICE(S) FOR 405,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest ROSE BY AN STRONG SIZED 7692 CONTRACTS UP TO 517,921 WITH THE RISE IN PRICE/YESTERDAY’S TRADING ( RISE OF $3.65). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 11075 CONTRACTS : JUNE SAW THE ISSUANCE OF 11075 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 517,921. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 7692 OI CONTRACTS INCREASED AT THE COMEX AND AN STRONG SIZED 11,075 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 18,767 CONTRACTS OR 1,876,700 OZ = 58.37 TONNES.

YESTERDAY, WE HAD 7535 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 149,355 CONTRACTS OR 14,935,500 OZ OR 464.55 TONNES (14 TRADING DAYS AND THUS AVERAGING: 10,668 EFP CONTRACTS PER TRADING DAY OR 1,066,800 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 14 TRADING DAYS IN TONNES: 464.55 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 464.55/2550 x 100% TONNES = 18.21% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2,509.04 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 7692 ACCOMPANYING THE RISE IN PRICE // GOLD TRADING YESTERDAY ($3.65 RISE). WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11075 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,075 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS SIZED NET GAIN OF 18,767 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11075 CONTRACTS MOVE TO LONDON AND 7692 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 58.37 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $4.25 : WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/

Inventory rests tonight: 865.89 tonnes.

SLV/

WITH SILVER UP 3 CENTS TODAY: A HUGE CHANGE/ A WITHDRAWAL OF 2.355 MILLION OZ/

/INVENTORY RESTS AT 317.841 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUGE 7362 CONTRACTS from 214,297 UP TO 221,659 (AND CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AFTER 6 CONSECUTIVE DAYS OF LOSSES. WE HAVE HAD TWO CONSECUTIVE DAYS OF COMEX SILVER GAINS. NOT ONLY THAT BUT OUR BANKERS ALSO USED THEIR EMERGENCY PROCEDURE TO ISSUE AN ATMOSPHERIC 9532 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), 100 EFP ISSUANCE FOR JUNE AND 170 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 9802 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 7711 CONTRACTS TO THE 9802 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 17,164 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 85.820 MILLION OZ!!! AND THIS OCCURRED WITH A RISE IN PRICE OF 44 CENTS. THE BANKERS ARE CAPITULATING AS THEY DESPERATELY TRY AND PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES. YESTERDAY THEY THREW ALL OF THEIR PAPER MUSCLE (WHICH IS INFINITE) PLUS THE KITCHEN SINK TRYING TO CONTAIN SILVER

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE RISE IN SILVER PRICING / YESTERDAY (44 CENTS/) . BUT WE ALSO HAD ANOTHER HUMONGOUS SIZED 9802 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed UP 25.98 POINTS OR 0.84% /Hang Sang CLOSED UP 424.19 POINTS OR 1.40% / The Nikkei closed UP 32.98 POINTS OR 0.15%/Australia’s all ordinaires CLOSED UP .34% /Chinese yuan (ONSHORE) closed UP at 6.2766/Oil UP to 69.08 dollars per barrel for WTI and 74.33 for Brent. Stocks in Europe OPENED MIXED. ONSHORE YUAN CLOSED UP AT 6.2766 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2701 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING A LITTLE STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

i)We have been reporting on numbers from Germany and they all seem to be flashing the yellow sign that a recession is coming to this behemoth export nation

( Mish Shedlock/Mishtalk)

ii)Bill Blain talks about his fears on the markets this morning

( Bill Blain/Mint Partners)

iii)Now I fully understand what is going on with the Swiss franc. It has been falling pretty badly against the Euro. Jordan actually likes that. What we have here is another casualty with respect to the Russian sanctions as Russian investments in Switzerland may have exposure so they are getting out of Dodge…thus the fall in the Swiss Franc

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

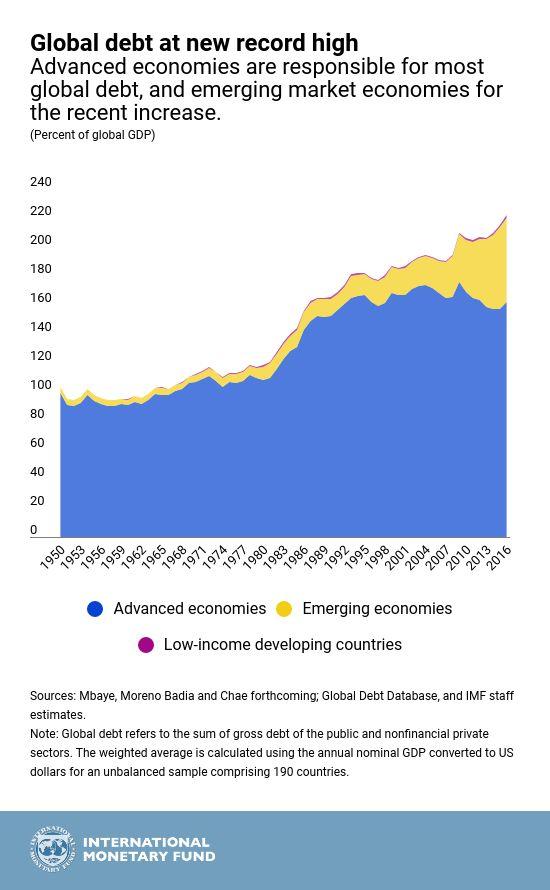

i)the IMF sounds the alarm bell on excessive debt issuance

( Chris Giles/London’s Financial times)

ii)With huge dollar shortages it was a no brainer for Iran to switch to euros for official reporting currency. It is not going to help them

( Reuters/GATA)

iii)With famed geologist Keith Barron roaming the mountains of Ecuador, he reports that the government there has a new, realistic and practical approach to companies wishing to exploit the countries mineral riches

( Keith Barron/news.vice.com/GATA)

iv)This is a difficult one! There is no question that in silver the crooks goaded the speculators in a considerable short position. The reason that the bankers were doing this is that they feared that silver was in dramatic short supply in London. Bars are arriving only with 2018 year stamped on them as the physical supply is rapidly disappearing. Maybe your reason for a short squeeze as the commercials will desperately try and extricate themselves from this mess

( John Rubino/DollarCollapse)

thus the reason for aluminium rising on the markets..very inflationary

( zero hedge)

vi)why we reached peak silver/trouble at a few silver mines

( Lawrie Williams)

10. USA stories which will influence the price of gold/silver

i)Today’s morning trading:

This is not good: with the Dow and Nasdaq tumbling, treasury yield undergo the unexpected: yields are rising because of inflation/stagflation fears

( zerohedge)

ii)Today’s morning data:

Soft data Philly Fed states that prices paid hits a 7 yr high and that signals inflation but no growth or in other words staglation

( zerohedge)

iii)The Amazon effect: Bezos reports over 100 million paid prime members

( zerohedge)

iv)Trump is hopeful that he will leave the meeting with Kim Jong Un happy. But if the meeting is not fruitful then more sanctions on North Korea. Trump will win on this one!! North Korea is hopelessly bankrupt.

v)SWAMP STORIES

a)Oh this is getting good: Comey calls McCabe a liar and the rhetoric between the two intensifies. Sit back and enjoy the popcorn

( zerohedge)

c)My goodness!! that did not last long. The Dept of Justice caves and will hand over the 7 memos and now we will get to see why Rosenstein needed a special prosecutor who became Mueller( zerohedge

d)Rosenstein tells Trump that he is not a target of Mueller’s probe. I highly doubt that…Rosenstein is lying

( zerohedge)

e)TRUMP EYEING GIULIANI TO JOIN IS LEGAL TEAM

( zerohedge)

f)The Inspector General Horowitz refers McCabe for 4 counts of criminal charges of lying to the FBI, to the Inspector general and to the Dept of Justice

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:321,666 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 322,031 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY 7362 CONTRACTS FROM 214,000 UP TO 222,008 (AND CLOSER TO THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) WITH THE 44 CENT RISE IN SILVER PRICING. WE ALSO WERE ALSO INFORMED THAT WE HAD A HUMONGOUS 9532 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS, 100 EFP’S ISSUED FOR JUNE, AND 114 EFP CONTRACTS ISSUED FOR JULY AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 9802. ON A NET BASIS WE GAINED 17,164 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 7362 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 9802 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 17,164 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month GAINED 7 contracts RISING TO 103 contracts. We had 0 notices filed upon so in essence we GAINED 7 contracts or 35,000 additional ounces of silver will stand for delivery in this non active delivery month of April AS SOMEBODY NEEDED SOME SILVER TODAY.

The next big active delivery month for silver will be May and here the OI GAINED 3465 contracts UP to 99,458. June saw a GAIN of 231 contract to stand at 327. The next big delivery month for silver is July and here the OI ROSE by 3177 contracts UP to 84,192.

We had 81 notice(s) filed for 405,000 OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 19/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

803.75 OZ

Manfra

(25 kilobars)

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

914 contracts

(91,400 oz)

|

| Total monthly oz gold served (contracts) so far this month |

665 notices

66,500 OZ

2.068 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to02 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (665) x 100 oz or 66500 oz, to which we add the difference between the open interest for the front month of APRIL. (914 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 157,900 oz, the number of ounces standing in this active month of APRIL (4.911 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (665 x 100 oz or ounces + {(914)OI for the front month minus the number of notices served upon today (2 x 100 oz )which equals 157,900 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 24 COMEX OI CONTRACTS OR 2400 OZ OF GOLD WILL NOT STAND BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

1,267,370.360 oz

JPMORGAN

Scotia

|

| Deposits to the Dealer Inventory |

397,312.06

oz

BRINKS

|

| Deposits to the Customer Inventory |

9530.510 oz

SCOTIA

|

| No of oz served today (contracts) |

81

CONTRACT(S

(405,000 OZ)

|

| No of oz to be served (notices) |

22 contracts

(110,000 oz)

|

| Total monthly oz silver served (contracts) | 460 contracts

(2,300,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 1 inventory movement at the dealer side of things

i) Into dealer Brinks; 397,312.06 oz

total dealer deposits: 397,312.06 oz

we had 1 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) INTO SCOTIA: 9530.510 OZ

total deposits today: 9530.510 oz

we had 1 withdrawals from the customer account;

i) out of JPMorgan; 605,120.500 oz

total withdrawals; 605,120.500 oz

accumulation in last 3 days for JPMorgan silver withdrawal:2,417,143.5 oz

why is JPMorgan withdrawing so much silver?

we had 1 adjustment

i) out of Scotia; 616.561.743 oz was adjusted out of the customer account of Scotia and this landed into the dealer account of Scotia

total dealer silver: 62.377 million

total dealer + customer silver: 261.727 million oz

The total number of notices filed today for the APRIL. contract month is represented by 81 contract(s) FOR 405,000 oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 460 x 5,000 oz = 2,300,000 oz to which we add the difference between the open interest for the front month of April. (103) and the number of notices served upon today (81 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 460(notices served so far)x 5000 oz + OI for front month of April(103) -number of notices served upon today (81)x 5000 oz equals 2,410,000 oz of silver standing for the April contract month

WE GAINED 7 SILVER CONTRACT OR 3500 ADDITIONAL OUNCES WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 161,759 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 226,854 CONTRACTS (my goodness)

YESTERDAY’S CONFIRMED VOLUME OF 226,554 CONTRACTS EQUATES TO 1,132 MILLION OZ OR 161.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER (in other words: 1.132 billion oz)

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.10% (APRIL 19/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.55% to NAV (APRIL 19/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.10%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.55%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.19%: NAV 14.03/TRADING 13.72//DISCOUNT 2.19.

END

And now the Gold inventory at the GLD/

APRIL 19/WITH GOLD DOWN $4.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.89 TONNES/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.89 TONNES

APRIL 17/WITH GOLD DOWN $1.00 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 16/WITH GOLD UP$2.80/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 13/WITH GOLD UP $6.15, A HUGE DEPOSIT OF 5.90 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 865.89 TONNES

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

APRIL 10/WITH GOLD UP $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 18/2018/ Inventory rests tonight at 865.89 tonnes

*IN LAST 365 TRADING DAYS: 75.15 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 315 TRADING DAYS: A NET 81.15 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 19/WITH SILVER UP 3 CENTS TODAY: WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.355 MILLION OZ/ MAKES ABSOLUTELY NO SENSE!!/INVENTORY RESTS AT 317.841 MILLION OZ

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 17/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

April 16/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 13/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ.

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 10/WITH GOLD UP 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 19/2018: A BIG CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 2.355 MILLION OZ WITH SILVER ON A TEAR THESE PAST FEW DAYS????

Inventory 317.841 million oz

end

6 Month MM GOFO 2.09/ and libor 6 month duration 2.50

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.09%

libor 2.50 FOR 6 MONTHS/

GOLD LENDING RATE: .41%

XXXXXXXX

12 Month MM GOFO

+ 2.75%

LIBOR FOR 12 MONTH DURATION: 2.51

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.24

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

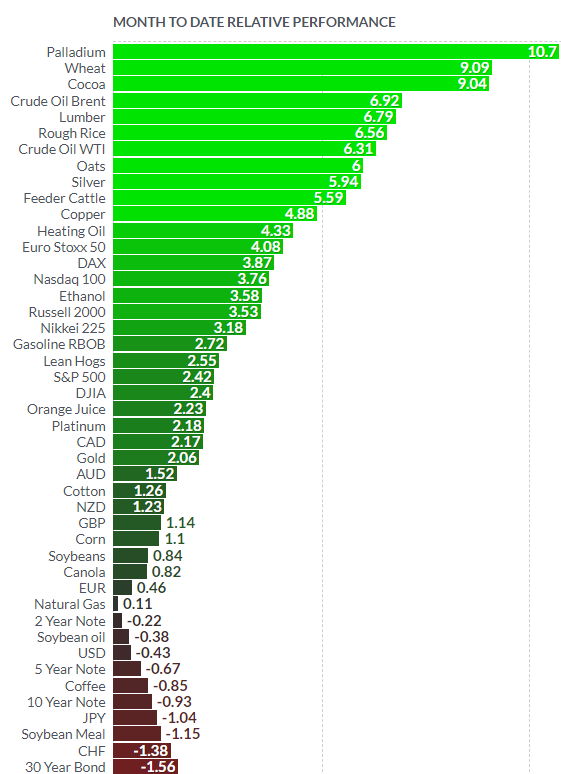

Palladium Bullion Surges 17% In 9 Days On Russian Supply Concerns

Palladium bullion has surged a massive 17% in just nine trading days. From $895/oz on Friday April 6th to over $1,052/oz today (April 19th). The price surge is due to palladium being due a bounce after falling in the first quarter and now due to Russian supply concerns.

In a volatile month, precious metals and commodities have been the clear winners so far, with palladium having the greatest gains of all – up 10.7% in April (see table below).

Source: Finviz

Palladium has surged on concerns about supply from Russia which is the world’s largest producer of palladium with various estimates of its contribution to total global palladium production ranging from 40% to 50%.

Russia and increasingly unstable South Africa control more than three-quarters of the world’s palladium supply, according to Johnson Matthey. Global palladium demand outstripped supply by 23 tonnes (25.4 tons) in 2017, so depleted stocks of this very rare and finite metal were already running low. Palladium is a key component in the global car industry and this will cause difficulties for international car manufacturers.

Palladium lease rates are moving higher in London which suggests a shortage of palladium. Some believe, including precious metals analyst David Jensen, that Russia saved the London palladium futures market (paper/ electronic market) in 2001 when physical palladium was in very short supply and lease rates exploded.

Given the increasing tensions of today and the trade and financial war being waged on powerful Russian individuals including Putin and on Russia itself, ‘the Bear’ is less likely to be as forgiving and accommodating today.

Palladium in USD 20 Years – Macrotrends.net

Were Russia to restrict the supply of palladium due to the bombing of Syria against its will or indeed due to the latest round of sanctions, palladium prices will see even greater gains.

Most of the commodities complex has surged this month due to concerns about war in the Middle East and a trade, economic and actual war between Russia and the U.S. The more aggressive latest round of U.S. sanctions from the Trump administration has jolted a broad range of Russia-related assets including natural gas, oil, base metals and indeed precious metals such as palladium.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Stocks have remained buoyant so far but the dollar and U.S. bonds have seen selling pressure. The long term fiscal outlook for Trump’s America is increasingly precarious with $1 trillion plus budget deficits being projected for the foreseeable future.

This makes the dollar vulnerable in the medium and long term and underlines the case for owning the precious metals of gold, silver, platinum and palladium. Larger allocations to gold are merited, then silver and investors should consider very small allocations to platinum and palladium.

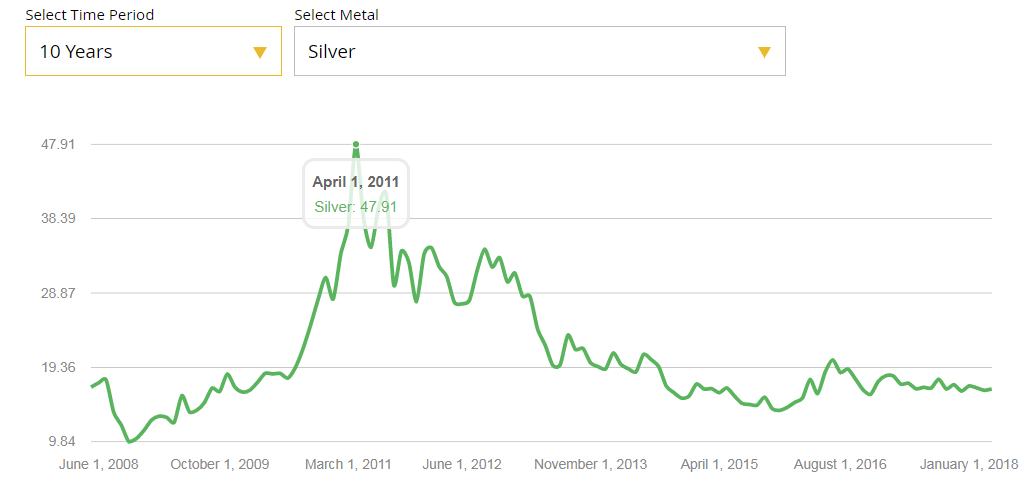

The increasingly bullish fundamentals of the global silver bullion market were shown by usyesterday (see chart below). The fundamentals of very depressed silver are arguably even better than palladium. Palladium is not far from all time record nominal highs (see chart above) while silver at just over $17/oz languishes some 65% below its record highs of near $50/oz in April 2011.

Silver is arguably the cheapest and best value asset in the ‘inflated assets’ world of today. Due to the very positive supply demand fundamentals for silver including increasing investment demand from the “prudent smart money”, expect silver to see similar sharp gains once it has a weekly close and breaks out above $18.50/oz.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

News and Commentary

Gold scores its highest finish in a week (MarketWatch.com)

Gold advances on technical buying, light safe haven demand (Reuters.com)

Fed’s Beige Book finds widespread concerns about new and proposed trade tariffs (MarketWatch.com)

Stocks Rise on Earnings, Oil as Treasuries Decline (Bloomberg.com)

World Top 20 Silver producers 2017 (SharpsPixley.com)

India Is Facing a Risky Cash Crunch (Bloomberg.com)

Metals Gripped by Turmoil (Bloomberg.com)

IMF sounds alarm on excessive global borrowing (FT.com)

The Federal Reserve Has Done A Great Job Destroying The Middle Class (ZeroHedge.com)

IMF Warns “United States Stands Out” (ZeroHedge.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

18 Apr: USD 1,346.55, GBP 949.59 & EUR 1,088.95 per ounce

17 Apr: USD 1,342.95, GBP 937.24 & EUR 1,084.57 per ounce

16 Apr: USD 1,344.40, GBP 941.21 & EUR 1,087.62 per ounce

13 Apr: USD 1,340.75, GBP 938.93 & EUR 1,087.35 per ounce

12 Apr: USD 1,345.90, GBP 951.01 & EUR 1,090.99 per ounce

11 Apr: USD 1,345.20, GBP 947.96 & EUR 1,087.86 per ounce

10 Apr: USD 1,335.95, GBP 942.25 & EUR 1,083.46 per ounce

Silver Prices (LBMA)

18 Apr: USD 16.95, GBP 11.93 & EUR 13.70 per ounce

17 Apr: USD 16.63, GBP 11.60 & EUR 13.44 per ounce

16 Apr: USD 16.60, GBP 11.61 & EUR 13.42 per ounce

13 Apr: USD 16.51, GBP 11.57 & EUR 13.40 per ounce

12 Apr: USD 16.66, GBP 11.74 & EUR 13.50 per ounce

11 Apr: USD 16.57, GBP 11.67 & EUR 13.39 per ounce

10 Apr: USD 16.49, GBP 11.65 & EUR 13.38 per ounce

Recent Market Updates

– Silver Bullion Remains Good Value On Positive Supply And Demand Factors

– London House Prices See Fastest Quarterly Fall Since 2009 Crisis

– Global Debt Bubble Hits New All Time High – One Quadrillion Reasons To Buy Gold

– Oil Surges Over 8%, Gold and Silver Marginally Higher, Stocks Gain In Volatile Week

– EU and Euro Exposed To Risks Including Trade Wars and War With Russia In Middle East

– Trump Tweets Russia “Get Ready” For Missiles In Syria – Gold, Oil Rise and Stocks Fall

– Private: EU and Euro Exposed To Trade Wars, Energy Dependence, Anti-EU and Anti-Euro Movements

– Trump Making ‘Major Decisions’ on Syria, Iran and Russia Response ‘Very Quickly’

– Gold Out Performs Stocks In 2018 and This Century By Ratio Of Two To One

– Jamie Dimon Warns Of Potential ‘Market Panic’

– Silver Bullion: Should We Be Worried About Silver?

– Martin Luther King Jr. Anniversary: Reminds Us Of Costs Of War To Society and Financial System

– Gold Outperforms Stocks In Q1, 2018

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

the IMF sounds the alarm bell on excessive debt issuance

(courtesy Chris Giles/London’s Financial times)

IMF sounds alarm on excessive global borrowing

Submitted by cpowell on Wed, 2018-04-18 14:07. Section: Daily Dispatches

By Chris Giles

Financial Times, London

Wednesday, April 18, 2018

WASHINGTON — The International Monetary Fund today sounded the alarm on excessive global borrowing, warning that with a total of $164 trillion owed, the world’s public and private sectors are deeper in debt than at the height of the financial crisis a decade ago.

Global debt is now more than twice the size of the value of goods and services produced every year and at 225 percent of global gross domestic product it is now 12 percentage points higher than at its previous peak in 2009.

The fund said there was now an urgent need to reduce the burden of debt in both the private and public sectors to improve the resilience of the global economy and provide greater firefighting capability if things went wrong. …

… For the remainder of the report:

https://www.ft.com/content/d4bf2984-42d2-11e8-93cf-67ac3a6482fd

END

With huge dollar shortages it was a no brainer for Iran to switch to euros for official reporting currency. It is not going to help them

(courtesy Reuters/GATA)

Iran switches from dollar to euro as official reporting currency

Submitted by cpowell on Thu, 2018-04-19 01:08. Section: Daily Dispatches

From Reuters

Wednesday, April 18, 2018

LONDON — Iran will start reporting foreign currency amounts in euros rather than U.S. dollars, state media said today as part of the country’s effort to reduce its reliance on the U.S. currency due to political tension with Washington.

The new policy could encourage government bodies and firms linked to the state to increase their use of the euro at the expense of the dollar.

Central bank governor Valiollah Seif said last week that Supreme Leader Ayatollah Ali Khamenei had welcomed his suggestion of replacing the dollar with the euro in foreign trade, as the “dollar has no place in our transactions today.”

Tehran has been trying for years to move away from the dollar, although much of the country’s international trade is still conducted in dollars and ordinary Iranians use them for travel and savings. …

… For the remainder of the report:

https://www.reuters.com/article/us-iran-currency-euro/iran-switches-from

END

With famed geologist Keith Barron roaming the mountains of Ecuador, he reports that the government there has a new, realistic and practical approach to companies wishing to exploit the countries mineral riches

(courtesy Keith Barron/news.vice.com/GATA)

Ecuador is getting realistic and practical about exploiting its mineral wealth

Submitted by cpowell on Thu, 2018-04-19 01:38. Section: Daily Dispatches

9:42p ET Wednesday, April 18, 2018

Dear Friend of GATA and Gold:

The VICE newsmagazine on HBO television has just done a documentary about geologist and mining entrepreneur Keith Barron’s return to Ecuador as CEO of Aurania Resources, and it suggests that the country and its people have taken a new, realistic, and practical approach to exploiting their mineral riches.

An excerpt from the documentary, headlined “Meet the Real-Life Indiana Jones Hunting for Gold in the Amazon,” is posted at VICE News here:

https://news.vice.com/en_us/article/d35kmj/meet-the-real-life-indiana-jo…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

This is a difficult one! There is no question that in silver the crooks goaded the speculators in a considerable short position. The reason that the bankers were doing this is that they feared that silver was in dramatic short supply in London. Bars are arriving only with 2018 year stamped on them as the physical supply is rapidly disappearing.

Maybe your reason for a short squeeze as the commercials will desperately try and extricate themselves from this mess

(courtesy John Rubino/DollarCollapse)

Is This The Long-Awaited Silver Short Squeeze?

Authored by John Rubino via DollarCollapse.com,

Silver’s popping this week…

Which is what people following the futures market action have been expecting for several months now. Speculators – usually wrong at big turning points and almost always at least slightly net long silver – have suddenly gone net short.

This is almost unprecedented, and implies that a short squeeze – in which speculators are forced to cover their short bets by buying silver futures, thus forcing the price sharply higher – is a real possibility.

What does this mean going forward? Based on the extremes in the paper market the incipient short squeeze has a little longer to run. The next COT report comes out on Friday and will show where the speculators were on Tuesday. We can infer from today’s action that since Tuesday they will have closed a lot of shorts, which means we’ll have to wait for the following Friday’s report to know how many.

Longer term, this is the kind of attention-getting action that puts an asset back on the radar screens of non-true-believers. As hard as it is for us gold-bugs to imagine, the vast majority of people aren’t watching precious metals and have no idea why silver matters.

They do, however, notice when the price of something jumps.

So if this short squeeze has legs and generates some headlines, it could pull in enough momentum chasing money to create a positive feedback loop in which rising prices beget more rising prices.

People will then try to figure out why this is happening, which will expose silver’s extremely positive fundamentals – tiny available supply, falling mine production, rising demand from technology and other industrial uses, and a tendency to soar in times of monetary stress – thus expanding the pool of fundamental investors.

Let gold finally break through that damn $1,360 resistance and it’s off to the races. (Here’s a free gold investing guide.)

But of course – as fans of precious metals have to readily admit – we’ve been waiting for (and sometimes predicting) stuff like this for years. So this latest flash of light might be yet another freight train heading our way. But one of these days what should happen will happen, and $100 silver will make up for a lot of angst.

end

The sanctions by Trump on Rusal is having a devastating effect on them and on the industry. Rusal cannot source badly needed alumina to manufacture aluminium products. Rusal is seeking China’s help who is also got problems with a potential tariff on Chinese aluminium

thus the reason for aluminium rising on the markets..very inflationary

(courtesy zero hedge)

Russian Aluminum Giant Seeks Rescue From US Sanctions In China

One week ago, when we first discussed the upcoming surge in commodity prices – especially aluminum and nickel – following Trump’s latest Russian sanctions, which in turn sent the stock and bond prices of Russian aluminum giant Rusal crashing amid fears the company would be unable to access capital markets now that it has become “radioactive” to western banks, we suggested that it do the next logical thing: “seek funding in China” or approach Beijing as a market that is exempt from US sanctions: after all, China itself has a ravenous demand for the product.

As it turns out, that’s precisely what the company – owned by Russian oligarch Oleg Deripaska -has done.

According to Bloomberg, officials from Rusal, the world’s second largest aluminum producer, met Chinese companies and traders this week to discuss the possibility of buying alumina and selling aluminum in China.

Still, China’s response was lukewarm: after all, Beijing itself is locked in an escalating trade war with the US and the last thing it wants is to infuriate the moustached neocons in the Trump administration by allowing Russian companies to skirt US sanctions.

Rusal’s delegation in China, which includes senior marketing and sales representatives, is discussing potential options but hasn’t reached any sort of agreement and may not do so, according to the people, who asked not to be identified because the matter is private. Chinese officials were cautious about any sort of deal because of the risk of contravening sanctions, the people said.

Furthermore, in addition to finding capital and buyers for its product, Rusal is looking for alternative sources of alumina, the raw material for aluminum, as sanctions block its normal supplies.

At the same time, the company’s asking traders whether it can boost sales of the refined metal in ingot form in China, as its usual customers are cut off. Rusal’s press office declined to comment.

And while Beijing may be able to quietly provide Rusal with funding, China may not be the “all-in” savior Rusal is seeking. As a reminder, the world’s biggest aluminum producer has already been cutting excess capacity, and has been exporting, and in some cases dumping, huge volumes of aluminum products it doesn’t need domestically and exchange warehouses are brimming with record stockpiles. What’s more, its own aluminum industry is being targeted by U.S. trade tariffs.

“It’s understandable that Rusal is looking for a solution from China as the country is the world’s biggest market of the metal,” said Wan Ling, an analyst at CRU Group in Beijing. “We’ll see major concerns from the Chinese side amid the current sensitivity in the global trade environment.”

Meanwhile, the most likely outcome is that as US sanctions persist, Russia’s aluminum output will remain in limbo, which will cripple European procurement, as the continent is Rusal’s biggest buyer…

while sending global supply chain for aluminum – which is used in everything from planes made by Boeing to Ford trucks to Campbell soup to Budweiser beer cans – in disarray.

And since Rusal supplies about 6% of the world’s aluminum or about 17% of production outside China, and operates mines, smelters and refineries from Ireland to Jamaica, the impact of recent sanctions has sent aluminum prices soaring to the highest since 2011.

Meanwhile, as the world refuses to accept Rusal’s product, the Russian aluminum giant is said to be stockpiling large quantities of aluminum at one of its plants in Siberia, according to Reuters.With the firm’s own storage space filling up with unsold aluminum, Rusal executives in Sayanogorsk, in southern Siberia, have had to rent out additional space to accommodate the surplus stock, one of the sources told Reuters.

“Aluminum sales have broken down. And now the surplus aluminum is being warehoused in production areas of the factory itself,” said someone who works on the grounds of one of Rusal’s two plants in Sayanogorsk

Several people connected to Rusal said that Oleg Deripaska, the company’s main shareholder who along with the company was included on a U.S. sanctions blacklist, visited Sayanogorsk this week for a closed-door meeting with staff.

Reuters spoke to a contractor at the Sayanogorsk plants who said the stockpiled ingots, stacked on pallets, were building up fast. He said two days’ worth of production would fill up a five-car train, but already a week had gone by with aluminum piling up.

“Can you imagine a week?” he said. “There’s a hell of a lot there, a hell of a lot. It’s being stockpiled, it’s not being shipped.”

An electrician working for Rusal said the ingots were being squeezed into all available space.

“The storage is not quite full,” said the electrician, who spoke on condition of anonymity to discuss internal company affairs. “Something is still being loaded all the same, some stuff is being shipped.”

* * *

To be sure, the Russian company will hardly give up without a fight: on Tuesday its Hong-Kong traded shares, which had lost more than 60% since the sanctions were announced last week, surged nearly 30% to HK$1.81 on speculation Trump will stop, and maybe roll back sanctions. But until that happens, Rusal is likely to target sales in alternative markets across the Middle East, Turkey and China to make up for lost exports to western markets, Morgan Stanley analysts said.

Finally there is the other wildcard: inflation. As noted above, aluminum and nickel have been driven to multi-year highs as the turmoil unleashed by U.S. sanctions spreads. On Thursday, aluminum surged to the highest level since 2011, trading at $2,668.50 a ton; Goldman forecasts prices could surge to $3,000 in the near term as the impact overwhelms the market and as no new suppliers can ramp up production to take over Rusal’s market share.

end

why we reached peak silver/trouble at a few silver mines

(courtesy Lawrie Williams)

LAWRIE WILLIAMS: World Top 20 Silver producers 2017

The latest analysis from GFMS for global silver supply and demand points to a 4% drop in new mined production last year. This was put down largely to years of Capex reductions in combination with supply disruptions, particularly in the Americas. The consultancy is looking for something of a supply recovery in the current year.

Particularly big falls were seen in Guatemala in 2017 with the suspension from July of mining at Tahoe Resources’ very large Escobal property, one of the world’s largest silver mines, due to an ongoing dispute with elements of the local population. Virtually on its own Escobal had propelled Guatemala into 11th place among the world’s silver producing nations in 2016, but the production shutdown in the latter part of 2017 dropped it back into 15th place last year and unless the dispute is soon settled and Tahoe allowed to mine again, Guatemala will disappear altogether from next year’s top 20 listing.

Other significant silver production falls were seen in the U.S. where an ongoing dispute at Hecla’s Lucky Friday mine continues and in Chile, where most silver is produced as a byproduct of copper mining, and in Australia as a result of sharply reduced output at the country’s largest silver mine, Cannington, due to lower grades and lower throughput caused by an underground fire in April. Mining rates are expected to recover in the current year following the commissioning of the new crusher and the resumption of mining activities on a high grade stoping section. Adding to the Australian losses, a substantial production decrease was also seen at the big Mount Isa silver/base metals operation, where output fell due to scheduled maintenance at its smelter.

Argentina also saw a fall in output. Production at Puna, a newly formed joint venture between SSR Mining’s Pirquitas and Golden Arrow Resources’ Chinchillas, fell by 4.2 million ounces (132 tonnes) as mining activities at the San Miguel open pit ceased in January 2017. As a result, lower grade stockpiles were processed throughout the year. However Yamana’s Cerro Moro silver/gold mine is due to come on stream about now and should add around 3.8 million ounces (117 tonnes) of silver to this year’s total.

| Table: World’s biggest silver producing nations 2016/2017 (tonnes) | |||||

| Rank | Country |

2017 output |

2016 Output |

% Change |

|

| 1 | Mexico |

6,106 |

5,795 |

+5% |

|

| 2 | Peru |

4,588 |

4,625 |

-1% |

|

| 3 | China |

3,502 |

3,571 |

-2% |

|

| 4 | Russia |

1,306 |

1,449 |

-10% |

|

| 5 | Chile |

1,260 |

1,493 |

-19% |

|

| 6 | Bolivia |

1,244 |

1,353 |

-8% |

|

| 7 | Poland |

1,229 |

1,197 |

+3% |

|

| 8 | Australia |

1,101 |

1,353 |

-19% |

|

| 9 | USA |

1,048 |

1,151 |

-9% |

|

| 10 | Argentina |

796 |

927 |

-14% |

|

| 11 | Kazakhstan |

591 |

554 |

+7% |

|

| 12 | India |

526 |

435 |

+21% |

|

| 13 | Sweden |

482 |

510 |

-5% |

|

| 14 | Canada |

395 |

404 |

-2% |

|

| 15 | Guatemala |

361 |

837 |

-57% |

|

| 16 | Indonesia |

358 |

348 |

+3% |

|

| 17 | Morocco |

339 |

317 |

+7% |

|

| 18 | Turkey |

171 |

174 |

-2% |

|

| 19 | Armenia |

156 |

149 |

+4% |

|

| 20 | Iran |

112 |

112 |

– |

|

| Rest of World |

834 |

880 |

-5% |

||

| Global Total |

26,503 |

27,638 |

-4% |

||

Source: GFMS, Lawrieongold.com

Note: Differences in % figures and global tonne totals shown due to rounding of more detailed stats.

The big output positives in 2017 were in production in Mexico. India and Kazakhstan. In the former, silver output rose by around 10.1 million ounces (311 tonnes), or 5%, led by higher production at San Julián and Peñasquito. Fresnillo’s San Julián operation, which was commissioned in Q3 2016, accounted for the majority of the growth in the country, producing a total of 10.5 million ounces (328 tonnes) and in combination these increases offset production losses elsewhere, particularly in the primary gold mining sector. San Julian commissioned its Phase 2 during the second half of the year which should result in further production growth in 2018.

India, which is a big silver consumer too for its jewellery sector, processed higher silver grades and ore volumes at Hindustan Zinc’s operations. Similarly, further gains were noted in the zinc sector in Kazakhstan, with silver production from Kazzinc’s assets higher by 28%, or 1.3 million ounces (30 tonnes). Kazakhstan continues to step up efforts to promote its domestic precious metals refining capacity, treating mine doré and scrap from several international sources, most notably from Russian mines.

There were output falls in China where the silver mining sector was also subjected to stricter environmental controls, and also a decline in byproduct output from the lead/zinc mining sector. Russia, the world’s fourth largest producer, also saw a substantial output fall extending the losses reported in the previous year.

Looking ahead to the current year, though, GFMS is anticipating something of a pick-up in mined production of silver with mining rates returning to normal and output from gold and primary silver mines in the Americas increasing. At the country level, GFMS estimates that Mexican production will post the largest gain and grow by as much as 6 million ounces (187 tonnes) led by Fresnillo. Higher grades at Cannington in Australia will also provide support to the global balance and it also expects to see some growth from the copper sector in Peru.

The big unknown remains Guatemala should the Escobal shutdown be reversed. That decision remains with the courts and the country is not seen as being particularly mining-friendly, despite the positive economic advantages that might result from a resumption of production at one of the world’s largest, and potentially most profitable, silver mines.

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.2766 /shanghai bourse CLOSED UP 25.98 POINTS OR 0.83% / HANG SANG CLOSED UP 424.19 POINTS OR 1.40%

2. Nikkei closed UP 32.98 POINTS OR 0.15%/ /USA: YEN RISES TO 107.41/

3. Europe stocks OPENED MIXED /USA dollar index RISES TO 89.65/Euro FALLS TO 1.2371

3b Japan 10 year bond yield: RISES TO . +.043/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.41/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 69.08 and Brent: 74.33

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.531%/Italian 10 yr bond yield UP to 1.750% /SPAIN 10 YR BOND YIELD UP TO 1.248%

3j Greek 10 year bond yield RISES TO : 4.019?????????????????

3k Gold at $1349.60 silver at:17.26 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 9/100 in roubles/dollar) 60.95

3m oil into the 69 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.41 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9682 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1978 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.531%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.8913% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.0852% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stock Rally Fizzles As Commodity Buying Frenzy Takes Over

After yesterday’s disappointing close for US stocks, which saw the Dow close down thanks to IBM’s 7.5% plunge and after some early upside VIX manipulation, ending a 3-day upside streak and the S&P closing just barely in the green, U.S. futures are in the red this morning, after Asian shares rose and European equities were little changed.

Having traded in a narrow range, S&P futures are near session lows, just fractionally back over 2,700.

European stocks similarly struggled for traction following two days of increases and in the wake of a mixed bag of corporate earnings, even after shares in Asia rose following gains from the prior day. The Eurostoxx remains roughly flat with FTSE as the outperforming index (+0.2% due to FX effects) and SMI (-0.07%) the underperformer amid domestic earnings. In large cap stocks news, ABB beat EBITDA expectations (+4.9%) pushing industrials to be the sector outperformer whilst Novartis (-1.9%) dragged down healthcare. Nestle (+0.3%) falling in line with expectations, Unilever (-1.9%) disappointed and Pernod Ricard (-0.9%) announcing an earnings beat.

Earlier in Asia, miners rose amid the commodity rally, with Australia’s ASX 200 (+0.3%) lifted by commodity names as miners outperformed amid strength in metals prices, which also boosted BHP shares despite a disappointing quarterly iron ore production update. The Nikkei 225 (+0.2%) was also led higher by metal stocks and in tandem with a weaker currency, while China’s benchmark index rebounded above a key level, driven by an advance in material shares. Hong Kong stocks rose for a second day, led by oil producers and financial institutions. The Shanghai Composite Index rose 0.8% to 3,117.38, rising above the 3,100 level, amid speculation the government is once again in the market.; blue-chip energy stocks in Hong Kong also cheered the higher oil prices and with sentiment also helped by another firm liquidity operation by the PBoC.

But if the overnight action in equities was muted, it was very different story in commodities where a buying frenzy has been unleashed as the U.S. sanctions against Rusal reverberated in metals markets, sending aluminum and nickel to multi-year highs on Wednesday.

Nickel jumped the most in 6.5 years on talk Nornickel – the world’s second-biggest producer of the metal – could be targeted. Aluminum prices also reached their highest since 2011, its raw material alumina touched an all-time peak, while iron ore leapt 5 percent. Such increases, if sustained, could fuel inflationary pressures and investors hedged by selling sovereign bonds.

In any case, it was set to be the strongest day for the commodity complex in eight months as Brent crude futures climbed past $74 a barrel after a near 3% jump overnight, one day after Dennis Gartman said he had gone short gold. The surge came on a Reuters report that OPEC’s new price hawk Saudi Arabia would be happy for crude to rise to $80 or even $100, a sign Riyadh will seek no changes to a supply-cutting deal even though the agreement’s original target is now within sight. “The Saudis and their colleagues in OPEC need higher oil for their fiscal positions and the Kingdom is on a bold – and costly – reform program,” Greg McKenna, chief market strategist at CFD, told Reuters.

On Thursday, metals extended their stellar gains, driving another rally in Bloomberg’s commodity index (BCOM), which is now back to levels seen in late 2015, as investors continue to fret about how Russian sanctions will impact the market.

In currency markets, the U.S. dollar remained rangebound with its index a fraction firmer at 89.669. It gained a touch on the yen to 107.46 yen, but stayed short of recent peaks at 107.78. Meanwhile, the Swiss franc has kept traders chained to their desks given its ongoing struggle to stay off the historic 1.20 handle versus the euro – which was so famously breached in early 2015 when the SNB ended its peg to the euro…

… as the USD gains traction after another set of U.K. data comes in lower than forecast. The EURCHF got as high as 1.1999 in the session in what appears to have been an algo attempt to trigger stops, before immediately sliding following a counterattack by other algos.

The USDJPY rose as the Japan-U.S. summit so far hasn’t stoked concerns of heightening trade tensions, helping to improve risk sentiment while a weak outcome at a 20-year JGB debt sale sent Japanese bonds lower. Elsewhere, the sterling dropped a third day, dragging the euro lower amid relatively low volumes in the currency market. The strength in commodity prices helped the Australian dollar easily weather unexpectedly soft jobs data, with employment rising by a meager 4,900 in March, and the AUD turned higher amid the commodity rally.

Government bonds retreated amid an upbeat global growth outlook, allowing U.S. curve flattening to take a breather. 10-year Treasury yields climbed to 2.89% after leaping on Wednesday in the wake of the Federal Reserve’s Beige Book report, which showed a solid outlook for the economy despite trade concerns. Still, optimism over expansion has been tested by the flattening yield curve, though there’s also been some respite for traders as geopolitical tensions showed signs of dissipating. European bonds played catch up, and yields in the region jumped.

In other news, overnight Fed president Quarles (Voter, Neutral) said he does not view current yield curve flattening as a signal for a recession. Separately the Fed’s Rosengren (Non-voter, Hawkish) suggests US lacks buffers for next downturn. Meanwhile, RBNZ Governor Orr says expects very benign inflation ahead, adds doggedly determined to aim for inflation at 2%.

Data include jobless claims and Philadelphia Fed Business Outlook. Bank of New York Mellon, BB&T, Blackstone, Danaher, Philip Morris, and P&G are among companies reporting earnings

Bulletin Headline Summary from RanSquawk

- Equity markets mostly flat as macro effects subside, focus turns toward earnings

- UK Retail sales falls below expectations pulling cable below the 1.42 level

- Looking ahead, highlights include US weekly jobs, Philly Fed and a slew of central bank speakers

Top Overnight News

- Abe acknowledged that the U.S. is interested in a bilateral deal but said that Japan’s position remains that the multilateral Trans-Pacific Partnership “is the best for both of the countries.” Trump said he’d rejoin TPP if offered ‘a deal I can’t refuse.’

- Russia’s central bank deviated from its standard practice and used off-market conversion of ruble revenue into foreign currency for a wealth fund to avoid adding to volatility gripping the currency, according to S&P Global Ratings

- Hong Kong rates reach 2008 high after HKMA spends $6.5b on intervention to support the local dollar since the currency hit the weak end of its trading band a week ago for the first time since 2005. The HKMA’s purchases have been orderly and outflows aren’t too big, Deputy Chief Executive Howard Lee said on Thursday

- President Donald Trump is methodically laying the groundwork for a landmark meeting with North Korean leader Kim Jong Un with the meeting increasingly likely to occur by early June

- JPMorgan is said to plan on moving “far greater” numbers of staff and traders to Paris than the 60-80 bankers previously known, AFP reports

- Australian employment rose less than forecast in March and the previous month’s gain was revised to a decline, suggesting the central bank will keep interest rates on hold

- Hong Kong rates reach 2008 high after HKMA spends $6.5b on intervention to support local dollar. HKMA said the size of the outflows isn’t too big

- To Citigroup, the chances are slim the U.S. enters a recession anytime soon. Fed officials feel the same way. Yet both camps agree that an inverted Treasuries yield curve would be an ominous sign for growth

Market Snapshot

- S&P 500 futures down 0.1% to 2,706.50

- STOXX Europe 600 down 0.03% to 381.76

- MXAP up 0.5% to 175.49

- MXAPJ up 0.9% to 574.75

- Nikkei up 0.2% to 22,191.18

- Topix up 0.03% to 1,750.18

- Hang Seng Index up 1.4% to 30,708.44

- Shanghai Composite up 0.8% to 3,117.38

- Sensex up 0.2% to 34,397.84

- Australia S&P/ASX 200 up 0.3% to 5,881.00

- Kospi up 0.3% to 2,486.10

- German 10Y yield rose 2.9 bps to 0.56%

- Euro down 0.05% to $1.2368

- Italian 10Y yield fell 4.2 bps to 1.463%

- Spanish 10Y yield rose 3.9 bps to 1.256%

- Brent futures up 0.9% to $74.13/bbl

- Gold spot up 0.2% to $1,351.80

- U.S. Dollar Index up 0.1% to 89.70

Asian stocks were higher across the board following the mostly positive lead from Wall St, where earnings remained in focus and the energy sector outperformed after crude rallied over 3% to its highest since 2014. ASX 200 (+0.3%) was lifted by commodity names as miners outperformed amid strength in metals prices, which also boosted BHP shares despite a disappointing quarterly iron ore production update. Nikkei 225 (+0.2%) was also led higher by metal stocks and in tandem with a weaker currency, while Hang Seng (+1.4%) and Shanghai Comp. (+0.8%) conformed to the commodity-led gains with the blue-chip energy stocks in Hong Kong cheering the higher oil prices and with sentiment also helped by another firm liquidity operation by the PBoC. Finally, 10yr JGBs were subdued as upside in riskier assets sapped safe-haven demand, and with price action also kept tame by mixed 20yr auction results which showed reduced demand but higher accepted prices. The PBoC injected CNY 190bln via 7-day reverse repos. US President Trump said will shrink the US trade deficit with Japan and hopefully a balance will be reached, while he later stated that they are negotiating a one-on-one trade deal with Japan. There were also comments from Japanese PM Abe that he agreed with US President Trump to begin discussions on fair, free and reciprocal trade, while he also commented that TPP is the best trade deal for both Japan and US

Top Asia News

- Hong Kong Rates Reach 2008 High After $6.5 Billion Intervention

- China Asks Qualcomm For More Remedies to Win NXP Approval

- Itochu to Pay $1.1 Billion for Majority Stake in FamilyMart

- World’s Most Unloved Stocks Pummeled Further by Rate- Hike Fears

Equities have seen the narrative subside from macro effects and move toward individual stock news as the Eurostoxx remains roughly flat (-0.05%), with FTSE as the outperforming index (+0.2% due to FX effects) and SMI (-0.07%) the underperformer amid domestic earnings. Large cap stocks news are as follows, with ABB beating EBITDA expectations (+4.9%) pushing industrials to be the sector outperformer whilst Novartis (-1.9%) have dragged down healthcare. Nestle (+0.3%) falling in line with expectations, Unilever (-1.9%) who were disappointing and Pernod Ricard (-0.9%) announcing an earnings beat. In the M&A scope, Merck (+0.5%) confirmed their decision to offload their consumer unit to P&G for around EUR 3.4bln

Top European News

- Debenhams Stock Sinks as Retailer Loses CFO and Warns on Profit

- Novartis Names Amgen’s John Tsai to Oversee Drug Development

- U.K. Retail Sales Fall More Than Forecast Amid Snow Chaos

- Spanish Mayor Offers to Help Gibraltar Insurers Get Round Brexit

In FX, the DXY remains contained in a relatively tight range around 89.500, and mostly firmer for choice, but narrowly mixed vs G10 counterparts. The commodity currencies are gleaning support from underlying price gains, while comments from China’s SAFE contending that the Dollar may decline further as other global economies catch up has also aided EMs to recoup more recent losses. GBP: Sterling’s April winning streak has hit another potential obstacle in the shape of much weaker than expected UK retail sales data, and Cable has fallen back below the 1.4200 handle as a result to re-test and marginally breach lows seen in wake of Wednesday’s CPI miss. Market contacts report sell-stops through 1.4170, but there has been limited follow-through so far with Gbp/Usd finding buyers around 1.4160 and Eur/Gbp capped just ahead of 0.8740. AUD: A marginal outperformer as broad risk appetite and extended rallies in oil/metals more than offset a disappointing Aussie jobs report overnight, but Aud/Usd is still finding the atmosphere above 0.7800 tough to reside in, with some key chart resistance levels also keeping the pair in check (200 DMA at 0.7817 and a 0.7831 Fib. EUR/JPY: Both sticking rigidly to recent ranges, with key chart levels restraining price action alongside hefty and some mega option expiries. Eur/Usd looks bid below 1.2350 and offered on treks above 1.2400, while Usd/Jpy has been supported just under 107.00 and mostly resistant around 107.50-55.

In commodities, WTI (+0.8%) and Brent (+1%) remain close to highs that were last seen in 2014 amid reports yesterday Saudi Arabia would favour crude prices to rise US 80/bbl, or even USD 100/bbl. The upside is also followed the DoE inventory report which mirrored the API release and showed drawdowns across all product components. In the metals bloc, gold is trading softer amid pressure from a slightly firmer dollar, whilst Dalian iron ore rose almost 7% overnight, and Nickel soared 9% to a three-year high amid Russian sanction by the US on major Russian aluminium producer Rusal. Nickel has now risen over 16% in the last two sessions, whilst the Shanghai Futures Exchange cut intra-day transaction fees for nickel futures contracts for May to CNY 6 from current CNY 30. OPEC and Non-OPEC committee are said to have seen stockpiles nearly cleared

Looking at the day ahead now, the most notable data due in Europe is the February current account balance reading for the Euro area and March retail sales data for the UK. In the US we’ll get the latest weekly initial jobless claims reading, March leading index and April Philly Fed business outlook print. The Fed’s Brainard, Quarles and Mester as well as the BoE’s Cunliffe and Brazier are due to speak. Worth noting also is talks between Germany’s Merkel and France’s Macron with EU reforms and trade conflicts with the US expected to be high on the agenda.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 230,000, prior 233,000; Continuing Claims, est. 1.85m, prior 1.87m

- 8:30am: Philadelphia Fed Business Outlook, est. 21, prior 22.3

- 9:45am: Bloomberg Economic Expectations, prior 56; Consumer Comfort, prior 58

- 10am: Leading Index, est. 0.3%, prior 0.6%

Central Banks

- 8am: Fed’s Brainard Speaks on Regulatory Reform

- 9:30am: Fed’s Quarles Testifies on Supervision Before Senate Panel

- 6:45pm: Fed’s Mester Speaks on Economic Outlook and Policy

DB’s Jim Reid concludes the overnight wrap

With Spring finally deciding to make a long overdue appearance here in London, it feels like the dark clouds full of trade spats, tech tantrums and geopolitics have cleared, at least temporarily for markets, leaving the last few days feeling much more 2017-esque compared to some of the volatility swings that had become all too commonplace in 2018 so far. Indeed stronger equities, tighter credit spreads, lower volatility across the board and flatter yield curves seem to have come back to the forefront.

On the former, despite stalling a bit into the close last night, equity markets generally made headway yesterday with the S&P 500 (+0.08%), Nasdaq (+0.19%) and Stoxx 600 (+0.29%) all closing up on the back of an energy-sector driven boost and a smattering of decent earnings reports including Morgan Stanley. The Dow (-0.16%) did lag a bit however following the IBM results. Still, relative to the intraday lows back on April 2nd the S&P 500 and Dow are now up over +6% while the Nasdaq is up over +7%. The Stoxx 600 is also up nearly +5% from the lows on April 4th. At the same time the VIX – which was marginally higher yesterday – is down 10pts over the same time horizon.