GOLD: $1336.40 DOWN $ 10.20 (COMEX TO COMEX CLOSINGS)

Silver: $17.14 DOWN 11 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1336.20

silver: $17.12

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:8 NOTICE(S) FOR 800 OZ.

TOTAL NOTICES SO FAR 673 FOR 67300 OZ (2.0933 tonnes)

THE COMEX IS OUT OF GOLD

For silver:

APRIL

1 NOTICE(S) FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 461 for 2,305,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8470/OFFER $8570: up $249(morning)

Bitcoin: BID/ $8367/offer 8567: UP $245 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1349.03

NY price at the same time: 1343.00

PREMIUM TO NY SPOT: $6.03

ss

Second gold fix early this morning: 1350.86

USA gold at the exact same time: 1342.00

PREMIUM TO NY SPOT: $8.86

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A SMALL 254 CONTRACTS FROM 221,659 RISING TO 221,913 ACCOMPANYING YESTERDAY’S SMALL 3 CENT GAIN IN SILVER PRICING. AFTER A STRING OF 6 CONSECUTIVE DAYS OF DROPS IN OPEN INTEREST, WE NOW HAVE THREE CONSECUTIVE OI GAINS. . WE WERE AGAIN NOTIFIED THAT WE HAD AN HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 4245 EFP’S FOR MAY , 273 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL SKY BOUND ISSUANCE OF 4518 CONTRACTS AND IT IS THE HIGHEST EVER ISSUED AS FAR AS I HAVE BEEN RECORDING THESE ENTRIES!!!. WITH THE TRANSFER OF 4518 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 4518 EFP CONTRACTS TRANSLATES INTO 23.86 MILLION OZ ACCOMPANYING 1.THE RISE IN SILVER PRICE AT THE COMEX AND 2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

53,141 CONTRACTS (FOR 15 TRADING DAYS TOTAL 53,141 CONTRACTS) OR 265.705 MILLION OZ: AVERAGE PER DAY: 3,542 CONTRACTS OR 17.7136 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 265.705 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 37.95% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 983.835 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A TINY SIZED GAIN IN COMEX OI SILVER COMEX OF 254 WITH THE TINY 3 CENT GAIN IN SILVER PRICE. THE CME NOTIFIED US THAT WE HAD AN HUMONGOUS SIZED EFP ISSUANCE OF 4518 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA 4245 EFP’S WERE ISSUED FOR THE MONTH OF MAY, AND 273 EFP CONTRACTS FOR JULY, FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A STRONG 4772 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 4518 open interest contracts headed for London (EFP’s) TOGETHER WITH AN INCREASE OF 254 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE TINY RISE IN PRICE OF SILVER OF 3 CENTS AND A CLOSING PRICE OF $17.25 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by WELL OVER 1 BILLION oz i.e. 1.109 BILLION TO BE EXACT or 159% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest ROSE BY 1532 CONTRACTS UP TO 519,453 DESPITE THE FALL IN PRICE/YESTERDAY’S TRADING ( DROP OF $4.25). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 15,381 CONTRACTS : JUNE SAW THE ISSUANCE OF 15,381 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 522,173. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 1532 OI CONTRACTS INCREASED AT THE COMEX AND AN HUMONGOUS SIZED 15,381 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 16,913 CONTRACTS OR 1,691,300 OZ = 52.60 TONNES.

YESTERDAY, WE HAD 11075 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 164,736 CONTRACTS OR 16,473,600 OZ OR 512.37 TONNES (15 TRADING DAYS AND THUS AVERAGING: 10,982 EFP CONTRACTS PER TRADING DAY OR 1,098,200 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 15 TRADING DAYS IN TONNES: 512.37 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 512.37/2550 x 100% TONNES = 20.09% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2,556.88 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: AN INCREASE IN OI AT THE COMEX OF 1532 DESPITE THE FALL IN PRICE // GOLD TRADING YESTERDAY ($4.25 DROP). WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 15,381 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 15,381 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS SIZED NET GAIN OF 16,913 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

15,381 CONTRACTS MOVE TO LONDON AND 1532 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 52.60 TONNES).

we had: 8 notice(s) filed upon for 800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $10.20 : WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/

Inventory rests tonight: 865.89 tonnes.

SLV/

WITH SILVER DOWN 11 CENTS TODAY: ANOTHER HUGE CHANGE/ A WITHDRAWAL OF 1.130 MILLION OZ/

/INVENTORY RESTS AT 316.711 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A TINY 254 CONTRACTS from 221,659 UP TO 221,913 (AND CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AFTER 6 CONSECUTIVE DAYS OF LOSSES. WE HAVE HAD THREE CONSECUTIVE DAYS OF COMEX SILVER GAINS. NOT ONLY THAT BUT OUR BANKERS ALSO USED THEIR EMERGENCY PROCEDURE TO ISSUE A HUMONGOUS 4245 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), AND 273 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 4518 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 254 CONTRACTS TO THE 4518 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 4772 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 23.860 MILLION OZ!!! AND THIS OCCURRED WITH A TINY RISE IN PRICE OF 3 CENTS. THE BANKERS ARE CAPITULATING AS THEY DESPERATELY TRY AND PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES. YESTERDAY THEY THREW ALL OF THEIR PAPER MUSCLE (WHICH IS INFINITE) PLUS THE KITCHEN SINK TRYING TO CONTAIN SILVER BUT TO NO AVAIL.

RESULT: A TINY SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE RISE IN SILVER PRICING / YESTERDAY (3 CENTS/) . BUT WE ALSO HAD ANOTHER HUMONGOUS SIZED 4518 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed DOWN 45.83 POINTS OR 1.47% /Hang Sang CLOSED DOWN 290.11 POINTS OR 0.94% / The Nikkei closed DOWN 28.94 POINTS OR 0.13%/Australia’s all ordinaires CLOSED DOWN .20% /Chinese yuan (ONSHORE) closed DOWN at 6.2924/Oil UP to 69.08 dollars per barrel for WTI and 74.33 for Brent. Stocks in Europe OPENED MIXED. ONSHORE YUAN CLOSED DOWN AT 6.2924 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.2843/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING A LITTLE WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

3 c CHINA

The ban on high tech chips will be deadly to China and they plan to hit back against the ZTE ban

( zerohedge)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

i)first oil for yuan for gold

( zerohedge)

ii)Trump now targets production cuts in OPEC as he claims that oil prices are artificially high. Saudi Arabia responds that there is no such thing as artificial oil prices.

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

This ought to be fun: Turkey wishes to repatriate all of its gold held at the FRBNY: 591 tonnes

( zerohedge)

10. USA stories which will influence the price of gold/silver

i)Early morning trading

( zerohedge)

ii)A huge fine: over one billion dollars is believed to be the amount of the settlement on the “risk management” case with respect to Wells Fargo with transgressions against its own depositors. The case was laid by the Financial Protection Bureau.

( zerohedge)

iii)SWAMP STORIES

Nunes, Gowdy and Goodlatte go nuclear:

( zerohedge)

b)Comey memos are now probed by the Dept of Justice as some were classified

(courtesy zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:288,108 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 352,060 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A TINY 254 CONTRACTS FROM 221,659 UP TO 221,913 (AND CLOSER TO THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) WITH THE 3 CENT RISE IN SILVER PRICING. WE ALSO WERE ALSO INFORMED THAT WE HAD A HUMONGOUS 4245 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS, AND 273 EFP CONTRACTS ISSUED FOR JULY AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 4518. ON A NET BASIS WE GAINED 4518 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 254 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 4518 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 4772 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 81 contracts FALLING TO 22 contracts. We had 81 notices filed upon so in essence we GAINED 0 contracts or ZERO additional ounces of silver will stand for delivery in this non active delivery month of April .

The next big active delivery month for silver will be May and here the OI LOST 4578 contracts DOWN to 94,860. June saw a GAIN of 32 contract to stand at 359. The next big delivery month for silver is July and here the OI ROSE by 4216 contracts UP to 88,403.

We had 1 notice(s) filed for 5,000 OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 20/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

257.20 OZ

Manfra

8 kilobars)

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

8 notice(s)

800 OZ

|

| No of oz to be served (notices) |

826 contracts

(82,600 oz)

|

| Total monthly oz gold served (contracts) so far this month |

673 notices

67300 OZ

2.0933 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 8 contract(s) of which 8 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (673) x 100 oz or 67300 oz, to which we add the difference between the open interest for the front month of APRIL. (834 contracts) minus the number of notices served upon today (8 x 100 oz per contract) equals 149,900 oz, the number of ounces standing in this active month of APRIL (4.6625 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (673 x 100 oz or ounces + {(834)OI for the front month minus the number of notices served upon today (8 x 100 oz )which equals 149,900 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 80 COMEX OI CONTRACTS OR 8000 OZ OF GOLD WILL NOT STAND BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 73 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

628,375.170 oz

JPMORGAN

CNT

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

599,587.455 oz

CNT

|

| No of oz served today (contracts) |

1

CONTRACT(S)

(5,000 OZ)

|

| No of oz to be served (notices) |

21 contracts

(105,000 oz)

|

| Total monthly oz silver served (contracts) | 461 contracts

(2,305,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 1 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) INTO CNT: 599,587.455 OZ

total deposits today: 599,587.455 oz

we had 2 withdrawals from the customer account;

i) out of JPMorgan; 598,011.000 oz

ii) Out of CNT: 30,364.170 oz

total withdrawals; 628,375.17- oz

accumulation in last 4 days for JPMorgan silver withdrawals,015,515.95 oz

JPMorgan has withdrawn silver on each of these last 4 days.

why is JPMorgan withdrawing so much silver?

we had 1 adjustment

i) Out of Scotia: 198,561.870 oz was withdrawn from the customer and this landed into the dealer account of Scotia

total dealer silver: 62.576 million

total dealer + customer silver: 261.698 million oz

The total number of notices filed today for the APRIL. contract month is represented by 1 contract(s) FOR 5,000 oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 461 x 5,000 oz = 2,305,000 oz to which we add the difference between the open interest for the front month of April. (22) and the number of notices served upon today (1 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 461(notices served so far)x 5000 oz + OI for front month of April(22) -number of notices served upon today (1)x 5000 oz equals 2,410,000 oz of silver standing for the April contract month

WE GAINED 0 SILVER CONTRACT OR 0 ADDITIONAL OUNCES WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

CRIMINALS!!

ESTIMATED VOLUME FOR TODAY: 125,940 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 172,838 CONTRACTS (my goodness)

YESTERDAY’S CONFIRMED VOLUME OF 172,838 CONTRACTS EQUATES TO 864 MILLION OZ OR 123.45% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.10% (APRIL 20/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.55% to NAV (APRIL 20/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.10%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.55%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.19%: NAV 14.03/TRADING 13.72//DISCOUNT 2.19.

END

And now the Gold inventory at the GLD/

APRIL 20/WITH GOLD DOWN $10.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 869.89 TONNES

APRIL 19/WITH GOLD DOWN $4.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 869.89 TONNES/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.89 TONNES

APRIL 17/WITH GOLD DOWN $1.00 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 16/WITH GOLD UP$2.80/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 13/WITH GOLD UP $6.15, A HUGE DEPOSIT OF 5.90 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 865.89 TONNES

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

APRIL 10/WITH GOLD UP $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 20/2018/ Inventory rests tonight at 865.89 tonnes

*IN LAST 366 TRADING DAYS: 75.15 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 316 TRADING DAYS: A NET 81.15 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 20/WITH SILVER DOWN 11 CENTS: ANOTHER HUGE CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.13 MILLION OZ//SLV RESTS TONIGHT AT 316.711 MILLION OZ/

APRIL 19/WITH SILVER UP 3 CENTS TODAY: WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.355 MILLION OZ/ MAKES ABSOLUTELY NO SENSE!!/INVENTORY RESTS AT 317.841 MILLION OZ

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 17/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

April 16/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 13/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ.

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 10/WITH GOLD UP 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 20/2018: A BIG CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.130 MILLION OZ WITH SILVER ON A TEAR THESE PAST FEW DAYS????

Inventory 316.711 million oz

end

6 Month MM GOFO 2.07/ and libor 6 month duration 2.51

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.07%

libor 2.51 FOR 6 MONTHS/

GOLD LENDING RATE: .44%

XXXXXXXX

12 Month MM GOFO

+ 2.76%

LIBOR FOR 12 MONTH DURATION: 2.49

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.27

end

And now for your weekly useless COT report

First Gold COT

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 237,288 | 74,219 | 52,500 | 173,535 | 358,797 | 463,323 | 485,516 |

| Change from Prior Reporting Period | ||||||

| 2,831 | -4,866 | -261 | 6,739 | 16,349 | 9,309 | 11,222 |

| Traders | ||||||

| 191 | 74 | 75 | 46 | 57 | 271 | 175 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 46,906 | 24,713 | 510,229 | ||||

| 1,332 | -581 | 10,641 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, April 17, 2018 | |||||

Our large speculators

those large speculators that have been long in gold added 2831 contracts to their long side

those large speculators that have been short in gold added 4866 contracts to their short side.

Our Commercials

those commercials that have been long in gold added 6739 contacts to their long side

those commercials that have been short in gold added a whopping 16,349 contracts to their short side

(and on top of this, they transferred a monstrous total of EFPs to London)

Our small speculators

our small specs that have been long in gold added 1332 contracts to their long side

our small specs that have been short in gold covered (transferred) 581 contracts from their short side

AND NOW SILVER COT

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 66,609 | 66,696 | 40,261 | 76,300 | 93,255 | |

| 1,576 | -13,170 | -5,917 | -7,040 | 5,337 | |

| Traders | |||||

| 107 | 60 | 61 | 40 | 40 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 214,297 | Long | Short | |

| 31,127 | 14,085 | 183,170 | 200,212 | ||

| -1,497 | 872 | -12,878 | -11,381 | -13,750 | |

| non reportable positions | Positions as of: | 178 | 136 | ||

Our large speculators

those large specs that have been long in silver added 1576 contracts to their long side

those large specs that have been short in silver covered (transferred) a massive 13,170 contacts from their short side.

Our Commercials

those commercials that have been long in silver pitched (transferred) a huge 7040 contracts from their long side.

those commercials that have been short in silver added 5337 contract from their short side.

Our small speculators

those small specs that have been long in silver pitched (transferred) 1497 contracts from their long side.

those small specs that have been short in silver added 872 contracts to their short side.

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Daily Market Update

New All Time Record Highs For Gold In 2019

– New all time record highs for gold in 2019

– ‘Powerful bull market’ will likely send gold to $5,000 to $10,000

– If USD & Treasuries keep falling, stocks may decline at ‘moment’s notice’

– Traditional portfolio of stocks and bonds will not protect investors

– “Gold will replace bonds as the go-to hedge”

by Brian Delaney of Secure Investments

Gold is gaining momentum after a 5-year consolidation and is set to challenge the 2011 highs some time next year. Once gold clears $2,000, a powerful bull market should drive the gold price meaningfully higher.

Gold has been an unloved asset class for years but that is about to change. I am expecting a bear market in equities and rising yields as a consequence of years of central bank QE.

A traditional portfolio of stocks and bonds will not protect investors during the next downturn. I expect gold will replace bonds as the go-to hedge.

Ultimately, I think gold will reach $5,000/oz-$10,000/oz, as a multi-year bear market in equities and the USD unfolds (along with a USD currency crisis), but let’s get to $2,000/oz first.

Should gold continue on its bullish trajectory, the gold (and silver) miners will explode higher.

$XAU is an index of gold and silver mining companies, and are they on sale today, following a catastrophic collapse from 2011 to 2016. Miners are cheaper today than they were all the way back in 2000 when the gold bull market began (and gold was trading at $250/oz). Many gold and silver mining companies are now breaking out from multi-year base formations.

Fortunes will be made in this sector over the next 5-10 years.

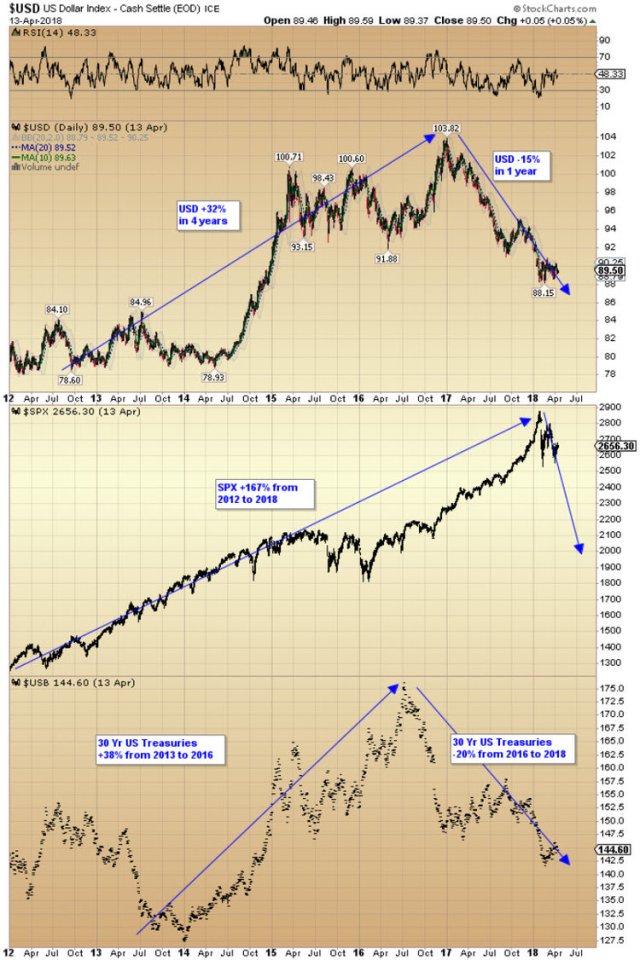

Last Friday, I reviewed the performance of US equities, bonds and USD in the run up to the 1987 stock market crash to see if there are any similarities to today’s markets.

From 1981 to 1986, US equities and bonds went on a tear. The S&P 500 rallied +237% from 1982 to 1987, while bonds surged +84% higher. The USD ran up +68% and then collapsed -42%. The combination of an overvalued stock market, overly bullish investor sentiment, a collapsing currency and automatic trading programmes in place at the time resulted in the panic now known as Black Monday.

Today, stocks are more expensive, debt levels are much higher across the board and interest rates are much lower too. The US stock market has rallied +167% from 2012 to 2018. US Treasuries added almost +40% from 2013 to 2016 before falling -20% over the last two years. The USD added +32% from 2013 to 2017 before declining -15% over the last 15 months.

Investors with a bullish bias should be rooting for both US Treasuries and USD to stabilize. If the USD and Treasuries continue to fall, the stock market will surely follow and the decline could accelerate at a moment’s notice.

Silver has been in a trading range for over four years and is now preparing to launch higher. More volatile than gold, silver is also considered a precious metal and the upside potential from here is significant. Silver cleared $17 yesterday. I think $18 and $20 will fall shortly as the next leg of the precious metals bull market gets underway. Just as I expect gold to break out to new all time highs next year above $2,000/oz, silver has a good chance of doing the same.

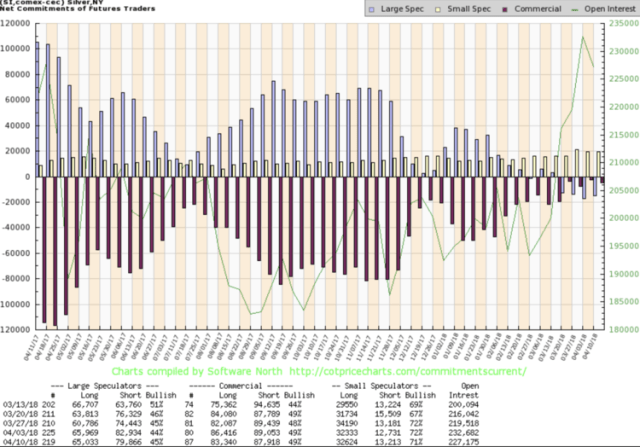

The latest Commitment of Traders report is also favouring a sharp move higher in silver prices. The Commercial Traders (smart money, purple bars) who are always short the metal to hedge silver producer production, are holding their smallest short position in years.

Meanwhile, the Large Speculator position (blue bars) is now short silver for the first time in years. The scene is set for a rocket launch in silver prices.

by Brian Delaney, CFA of Secure Investments

Recent Market Updates

– Palladium Surges 17% In 9 Days On Russian Supply Concerns

– Silver Remains Good Value On Positive Supply And Demand Factors

– London House Prices See Fastest Quarterly Fall Since 2009 Crisis

– Global Debt Bubble Hits New All Time High – One Quadrillion Reasons To Buy Gold

– Oil Surges Over 8%, Gold and Silver Marginally Higher, Stocks Gain In Volatile Week

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube above

News and Commentary

Gold prices inch down as global political tensions ease (Reuters.com)

U.S. Leading Economic Index Rises In Line With Estimates In March (Nasdaq.com)

Commodities Rally as Metals Surge; Bonds Slide (Bloomberg.com)

Philly Fed manufacturing index points to continued growth in April (MarketWatch.com)

U.S. weekly jobless claims dip in latest week (Reuters.com)

Don’t Wait Too Long to Leave the Party (DailyReckoning.com)

Russia And Iran Complete First Oil-For-Goods Transfer, Extend Agreement For A Year (ZeroHedge.com)

More Signs Of Inflation: Home Prices Jump Again And “$3 Gas Is Coming” (GoldSeek.com)

Sweden’s Very Own Bitcoin. What Could Possibly Go Wrong? (Bloomberg.com)

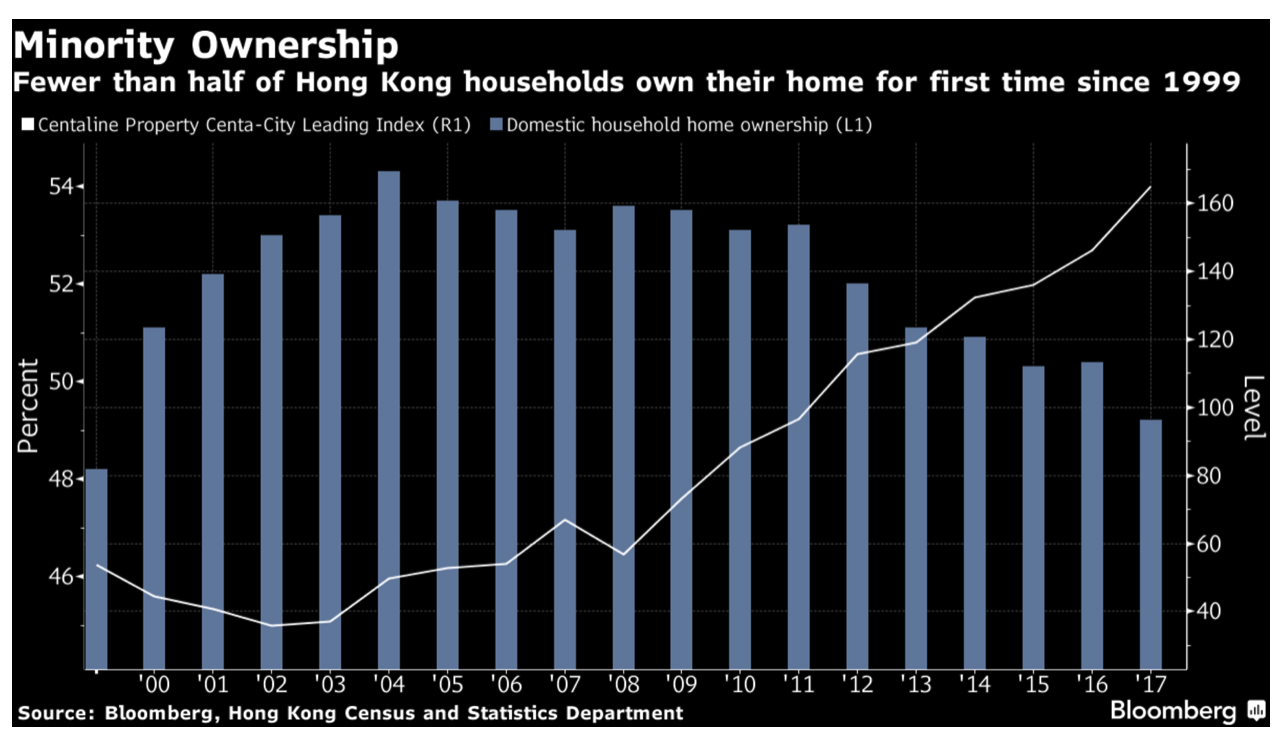

Hong Kong Home Owners Now a Minority as Prices Keep on Rising (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

19 Apr: USD 1,347.90, GBP 950.54 & EUR 1,090.59 per ounce

18 Apr: USD 1,346.55, GBP 949.59 & EUR 1,088.95 per ounce

17 Apr: USD 1,342.95, GBP 937.24 & EUR 1,084.57 per ounce

16 Apr: USD 1,344.40, GBP 941.21 & EUR 1,087.62 per ounce

13 Apr: USD 1,340.75, GBP 938.93 & EUR 1,087.35 per ounce

12 Apr: USD 1,345.90, GBP 951.01 & EUR 1,090.99 per ounce

Silver Prices (LBMA)

19 Apr: USD 17.20, GBP 12.09 & EUR 13.91 per ounce

18 Apr: USD 16.95, GBP 11.93 & EUR 13.70 per ounce

17 Apr: USD 16.63, GBP 11.60 & EUR 13.44 per ounce

16 Apr: USD 16.60, GBP 11.61 & EUR 13.42 per ounce

13 Apr: USD 16.51, GBP 11.57 & EUR 13.40 per ounce

12 Apr: USD 16.66, GBP 11.74 & EUR 13.50 per ounce

Recent Market Updates

– Palladium Bullion Surges 17% In 9 Days On Russian Supply Concerns

– Silver Bullion Remains Good Value On Positive Supply And Demand Factors

– London House Prices See Fastest Quarterly Fall Since 2009 Crisis

– Global Debt Bubble Hits New All Time High – One Quadrillion Reasons To Buy Gold

– Oil Surges Over 8%, Gold and Silver Marginally Higher, Stocks Gain In Volatile Week

– EU and Euro Exposed To Risks Including Trade Wars and War With Russia In Middle East

– Trump Tweets Russia “Get Ready” For Missiles In Syria – Gold, Oil Rise and Stocks Fall

– Private: EU and Euro Exposed To Trade Wars, Energy Dependence, Anti-EU and Anti-Euro Movements

– Trump Making ‘Major Decisions’ on Syria, Iran and Russia Response ‘Very Quickly’

– Gold Out Performs Stocks In 2018 and This Century By Ratio Of Two To One

– Jamie Dimon Warns Of Potential ‘Market Panic’

– Silver Bullion: Should We Be Worried About Silver?

– Martin Luther King Jr. Anniversary: Reminds Us Of Costs Of War To Society and Financial System

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

first oil for yuan for gold

(courtesy zerohedge)

Russia And Iran Complete First Oil-For-Goods Transfer, Extend Agreement For A Year

Nearly four years after Iran and Russia first agreed to an oil-for-goods swap agreement worth billions of dollars, RT is reporting that the first delivery of Iranian crude oil to Russia under the program has been completed,and the two sides are angling to extend the deal, possible for another five years.

“The agreement is effective; it has been extended for the year, but in general, we think it should be extended for five years,” said Russian Energy Ministry Aleksandr Novak.

As we reported more than three years ago,the $20 billion agreement was initially signed in April 2014 when Iran was facing Western sanctions over its nuclear program (they have since been lifted thanks to the Iran deal, but will likely soon be reimposed).

When the sanctions against Tehran were lifted in 2016, Novak said the deal was no longer necessary. However, Novak said in March 2017 that the plan was back on the table with Russia buying 100,000 barrels per day from Iran and selling the country $45 billion worth of goods.Another agreement was later signed in late May.

Current Iranian oil supplies under the program amount to five million tons per year. The first delivery was made in November 2017 and totaled one million tons.

Russia and Iran have also discussed cooperation in energy, electricity, nuclear energy, gas and oil, as well as cooperation in the field of railways, industry, and agriculture. Novak said in February that Russia’s state trading enterprise Promsirieimport has been authorized by the government to carry out the purchase of Iran’s oil through the oil-for-goods program under study by both countries

The oil-for-goods swaps are expected to boost trade between the two countries (while conveniently circumventing the petrodollar system). The nations have also signed six provisional agreements to collaborate on “strategic” energy deals worth up to $30 billion.

Presidential aide Yuri Ushakov said earlier this month that Russian investment in Iranian oil and gas fields could total more than $50 billion.

And in a sign of closer cooperation to come, Ushakov said Iran is weighing whether to enter the Russia-led Eurasian Economic Union – a move that could come within months. A free-trade zone deal would be expected to “trigger further development of our bilateral trade and expansion of investment cooperation.”

end

This ought to be fun: Turkey wishes to repatriate all of its gold held at the FRBNY: 591 tonnes

(courtesy zerohedge)

Turkey Will Repatriate All Gold From The US In Attempt To Ditch The Dollar

After Venezuela, Germany, Austria and the Netherlands prudently repatriated a substantial portion (if not all) of their physical gold held at the NY Fed or other western central banks in recent years, this morning Turkey also announced that it has decided to repatriate all its gold stored in the US Federal Reserve and deliver it to the Istanbul Stock Exchange, according to reports in Turkey’s Yeni Safak. It won’t be the first time Turkey has asked the NY Fed to ship the country’s gold back: in recent years, Turkey repatriated 220 tons of gold from abroad, of which 28.7 tons was brought back from the US last year.

According to the latest IMF data, Turkey’s gold reserves are estimated at 591 tons, worth just over $23 billion. This makes Ankara the 11th largest gold holder, behind the Netherlands and ahead of India.

Turkey’s gold repatriation come at a sensitive time for Turkey’s currency, the lira, which has been pounded, and plunged to all time lows against both the dollar and the euro despite runaway, double-digit inflation in Turkey, as the central bank is seemingly afraid of President Recep Tayyip Erdogan, and refuses to raise rates.

Meanwhile, Erdogan has taken a tough stance against the US currency, criticized dollar loans and saying that international loans should be given in gold instead.

“Why do we make all loans in dollars? Let’s use another currency. I suggest that the loans should be made based on gold,” Erdoğan said during a speech at the Global Entrepreneurship Congress in Istanbul on April 16, according to Hurriyet.

In what some saw an appeal for a gold standard by the Turkish president, Erdogan added that “with the dollar the world is always under exchange rate pressure. We should save states and nations from this exchange rate pressure. Gold has never been a tool of oppression throughout history.”

Well, now that Turkey will soon have all of its gold on the ground, Erdogan will be able to launch a gold-backed currency if he so desires. Unfortunately, all signs point to the gold being repatriated only so it can be raided, pillaged and promptly deposited in offshore vaults by members of the ruling oligarchy.

As noted above, Turkey has been one of several countries which have moved their gold from the world’s biggest, and most secure gold vault, that located 95 feet below sea level at 33 Liberty Street in Manhattan, also known as the New York Fed.

The repatriation wave began in 2012, when Venezuela announced it was withdrawing all of its 160 tons of gold at the NY Fed, valued at around $9 billion. Germany’s Bundesbank then demanded 300 tons be returned, with the Fed saying it would take seven years to do so; a scrambling Germany was able to complete the process 3 years ahead of schedule. The Netherlands has also repatriated 122.5 tons of gold.

As a result, according to the latest Fed data, the amount of physical gold stored at the NY Fed has dropped to the lowest on record, or 7.819 thousand tons, following a withdrawal scramble that started in 2014 and continued until the end of 2016. After a 15 month hiatus, withdrawals resumed in 2018, with 15.5 tons of gold repatriated in January and February.

“The central banks started the repatriation already a few years ago, meaning before we had Brexit, Catalonia, Trump, AFD or the rising tensions between the Politburo in Brussels and the nations of Eastern Europe,” said Claudio Grass of Precious Metal Advisory in Switzerland.

According to him, the world is becoming less centralized. “If we follow this trend, it should be obvious that the next step should be an even bigger break up into smaller units than the nation state. With such geopolitical fragmentation comes also the decentralization of power.”

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN 6.2924 /shanghai bourse CLOSED DOWN 45.83 POINTS OR 1.47% / HANG SANG CLOSED DOWN 290.11 POINTS OR 0.94%

2. Nikkei closed DOWN 28.94 POINTS OR 0.13%/ /USA: YEN RISES TO 107.58/

3. Europe stocks OPENED MIXED /USA dollar index RISES TO 90.16/Euro FALLS TO 1.2307

3b Japan 10 year bond yield: RISES TO . +.060/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.58/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 68.10 and Brent: 73.72

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.593%/Italian 10 yr bond yield UP to 1.780% /SPAIN 10 YR BOND YIELD UP TO 1.285%

3j Greek 10 year bond yield RISES TO : 4.051?????????????????

3k Gold at $1341.40 silver at:17.14 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 44/100 in roubles/dollar) 61.40

3m oil into the 68 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.58 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9734 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1982 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.593%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.9099% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.1015% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Stocks Struggle As Surging Dollar Snaps Commodity Rally

World stocks, as tracked by the MSCI All-Country Index, struggled on Friday, dipping in early trading but were set for a second week of gains after a solid start to the the global Q1 earnings season, even as a rally in commodity prices fizzled pressured by the recent dollar spike.

U.S. equity index futures are modestly in the red, alongside Asian markets, where technology shares came under pressure after yesterday’s unexpected Taiwan Semi warning, which saw the world’s biggest semiconductor foundry cut its revenue target to the low end of forecasts and blamed softer demand for smartphones

European stocks initially inched lower as traders assessed earnings results from companies including Reckitt Benckiser Group Plc and Ericsson AB, pushing the Stoxx Europe 600 Index slides 0.2%. However, since then Euro stocks erased all earlier losses as the Euro slumped, boosting exporters while the telecom sector outperformed after gains by Telia. The Stoxx Europe 600 Index rose 0.1% to session high with 11 of 19 industry groups advancing, telecom up 1.2% as Telia rallies following strong earnings.

Reckitt Benckiser falls after the company posted like-for-like sales for the first quarter that missed estimates, while Ericsson soars after posting results that were stronger than analysts had expected. ASM International heads for the worst performance on the Stoxx 600 after the semiconductor equipment maker’s results were seen as signaling a touch start to the year.

“Our base case is that investor focus will shift back to economic growth as some of the current uncertainties ease,” UBS strategists wrote in a note to clients. “In our base case we do not expect current tensions between NATO and Russia to escalate further than issues in the past, such as Crimea, and expect the trade dispute between the U.S. and China to be negotiated without escalating to a trade war.”

Outside of the EU, the Swiss National Bank said it was “not in a hurry” to adjust policy despite the franc touching a milestone low of EURCHF 1.20, according to President Thomas Jordan. American sanctions on Russian oligarchs have had the effect the Trump administration wanted, Treasury Secretary Steven Mnuchin said. Both aluminum and nickel fall back after Thursday’s gains.

U.S. equity-index futures nudged lower were off session lows, and just barely in the red.

Elsewhere, it has been a quiet, data-less, morning. USD is bid, EUR is under pressure and the Citi FX desk anticipates a move back up to the 90.55 area for the DXY Index – but we remain firmly within the same range. Commodities and risk-correlated currencies are suffering the most. There is a general USD bid out there this morning, which emerged out of leveraged London account and has been linked to a few factors – positions feel as though they are being lightened up ahead of the weekend, EUR is under pressure.

Thursday’s treasury yield spike moderated overnight, and yields were little changed around 2.90%, though they remained on track for the biggest weekly surge since early February.

Discussions this morning have revolved around the BoE, after Carney’s surprise comments overnight shook the general assumption that a May hike was on the way; as a result U.K. shares outperformed as the pound weakened also aided by reports of disagreements in Brexit talks on the Irish border. Short Sterling reds and greens open higher by 7-8 ticks, gilt curve steepens while according to Bloomberg, money-market pricing for a Bank of England interest-rate hike in May fell below 50% compared with about 80% on Thursday.

Gilts surged and the pound slid a fourth day, set for its longest run of losses this month, as leveraged names have been unwinding longs in the past two days and macro accounts also seen on the offer after Carney’s remarks. However, returning some normalcy, in a speech on Friday, BOE policy maker Michael Saunders backed further rate increases.

Elsewhere the yen slid to a one-week low of 107.73 per dollar as appetite for haven assets kept declining amid receding geopolitical and trade risks and as rising U.S. yields boosted dollar demand. The Indian rupee weakened to the lowest level since March 2017 despite minutes from the country’s central bank meeting showing an unexpected hawkish tilt. Oil prices drifted.

Meanwhile, yesterday’s big story – the surge in commodities – took a back seat even as WTI crude extended its advance to a three-year high, but the rally in metals market stuttered, driving the Bloomberg Commodity Index lower for a second day. Bond market breakevens showed an increase in expectations for U.S. inflation after the recent torrid gains in metals from aluminum to nickel. Trade remains in focus with the U.S. Treasury Department considering using an emergency law to curb Chinese investments in sensitive technologies.

Spot gold was down 0.2% at $1,342.56 an ounce even as the recent cryptocurrency surge continued on Friday.

In other overnight news, Fed’s Mester (Voter, Hawk) said further rate hikes are appropriate in 2018 and 2019, adding gradual hikes would help avert overheating and financial stability risks. Across the pond, BoE’s Saunders (Hawk) said UK no longer needs as much stimulus as before, due to little slack and rising cost pressures. Adding that pace of further rate hikes are likely to be “gradual” not “glacial”. Saunders says significance of data points is questionable due to weather and history of upward revisions.

Elsewhere, the EU rejected Theresa May’s Brexit Irish border solution as doubts grow over whether UK can leave customs union. Continuing the neverending Brexit saga, EU’s Barnier says at least 75% of the Brexit draft deal has been agreed on, the remaining 25% includes serious issues such as Ireland, “no way” to cherry-pick a deal.

Coming up in the NY session, the focus is on the Canadian March CPI print where expectations are looking for a 0.4%MoM. After that, Eurozone consumer confidence for April may generate some interest, but there’s a really sunny Friday feeling to proceedings thus far. Baker Hughes, GE, Honeywell, State Street and Waste Management are among companies due to report earnings.

Bulletin Headline Summary from RanSquawk

- FTSE the outperforming bourse following Carney’s comments reducing hike expectations

- Oil stable near multi year highs as OPEC JMMC meets

- Looking ahead, highlights include Canadian CPI, Fed’s Evans and Williams

Market Snapshot

- S&P 500 futures down 0.1% to 2,691.25

- STOXX Europe 600 down 0.2% to 381.19

- MSCI Asia Pacific down 0.8% to 174.03

- MSCI Asia Pacific ex Japan down 1.2% to 567.61

- Nikkei down 0.1% to 22,162.24

- Topix up 0.05% to 1,751.13

- Hang Seng Index down 0.9% to 30,418.33

- Shanghai Composite down 1.5% to 3,071.54

- Sensex down 0.2% to 34,375.71

- Australia S&P/ASX 200 down 0.2% to 5,868.78

- Kospi down 0.4% to 2,476.33

- German 10Y yield unchanged at 0.6%

- Euro down 0.1% to $1.2328

- Italian 10Y yield rose 6.4 bps to 1.527%

- Spanish 10Y yield rose 1.5 bps to 1.299%

- Brent futures up 0.1% to $73.84/bbl

- Gold spot down 0.3% to $1,341.03

- U.S. Dollar Index up 0.2% to 90.14

Top Overnight News

- Trump praised James Comey for his honorable conduct during the 2016 presidential campaign, sought out his loyalty, and asked the FBI director to let go of an investigation into his former national security adviser, according to memos Comey wrote to document private conversations

- Treasury is considering using an emergency law to curb Chinese investments in sensitive technologies as the Trump administration looks to punish China for what it sees as violations of intellectual-property rights

- Labour Party has given its clearest signal yet that it will join forces with rebel Tories in an attempt to defeat May on Brexit, threatening a political crisis that may bring down her government

- Swiss National Bank is “not in a hurry” to adjust policy President Jordan said despite the franc breaking through the 1.20-per-euro mark for the first time since early 2015

- U.S. Deputy Attorney General Rosenstein told President Trump last week he isn’t a target of any part of Special Counsel Robert Mueller’s investigation, according to several people familiar with the matter

- European Union officials are set to reject a potential U.K. solution to the crucial issue of what happens to the Irish border after Brexit, deepening the stalemate in negotiations

- U.K’s Brexit payments to the EU may exceed the 39b pound ($55b) ceiling of the Treasury’s estimate, the government auditor said

- Keir Starmer, chief Brexit spokesman of the opposition Labour party, indicated in an interview with Bloomberg that his party could join forces with rebels from PM Theresa May’s Conservatives in an attempt to defeat the government on a vote on staying in the EU customs union

- In a further escalation of rhetoric over trade, China accused the U.S. of throwing its weight around, saying it advocates principles of fairness but isn’t living up to them

Asia stocks traded lower after the subdued tone rolled over from Wall St where all major indices finished in the red, amid tech woes after semiconductor giant TSMC downgraded its revenue forecasts on concerns of softer smartphone demand. ASX 200 (-0.2%) and Nikkei 225 (-0.1%) opened negative although losses were mostly pared as the Energy sector remained afloat in Australia and with the Japanese benchmark finding some relief from a weaker JPY. Elsewhere, Taiwan’s Taiex (-1.7%) is the laggard as TSMC slumped following the weak revenue outlook, while Hang Seng (-0.9%) and Shanghai Comp. (-1.5%) were lacklustre after the PBoC skipped open market operations and as trade tensions lingered. Finally, 10yr JGBs were subdued as yields tracked their US counterparts higher, although the downside to JGBs was also limited amid the BoJ’s presence in the market for JPY 710bln in the belly to super-long end and with the amounts of the Rinban announcement unchanged.

Top Asian News

- India Is Said to Tell U.S. It Doesn’t Manipulate the Rupee

- India’s Central Bank Makes Surprising Tilt Toward Rate Hike

- Ex-Barclays Quants Move to Old House by Sea to Try to Do Good

In Europe, approaching the week’s end equity bourses are marginally higher (Eurostoxx +0.1%), with positivity noted in the FTSE (+0.5%), following lowered expectation of a UK rate hike, and a weaker GBP. The telecom sector is currently outperforming (+1.1%) driven by Telia’s strong earnings results. The sector underperformer is currently energy (-0.4%), driven by falling oil prices. Significant individual stock news was noted in Shire (-4.5%) with Allergan pulling out of the acquisition deal leading to underperformance, Pfizer and Abbvie, however, are said to be suitors. Earning outperformance was noted at Ericsson (+16%), and underperformance at Reckitt Benckiser (-5.8%)

Top European News

- U.K. Money-Market Pricing for May BOE Rate Hike Falls Below 50%

- Benettons Are Said to Plan Wireless Tower Champion With Cellnex

- FdR Offers to Buy Remaining Stake in Landlord Beni Stabili

- Billionaire Rokke Likely to Return to Oil Rigs With Odfjell

In FX, DXY is back on the 90.000 handle, but again largely on the back of the travails of others in the G10 fold, and the index still needs to establish a firm foothold above the big figure to mount a serious challenge of nearest upside resistance levels ahead of 91.000. Note, 90.362, 90.600 and 90.900 have all been tested, but rejected, and more recently 90.273. GBP: 3 UK data misses (albeit with some parts of the latest jobs and earnings report relatively strong) put a serious dent in Sterling’s seasonal advance, but ‘confirmation’ from BoE Governor Carney that this week’s disappointing releases could keep the MPC on hold in May has thrown a real spanner in the works, as Cable looks in danger of losing grip of 1.4000 and Eur/Gbp approaches 0.8800. Technical support around 1.4020 holding in for now, and remaining (some might say foolhardy) Pound longs/bulls have received a reprieve from broadly hawkish comments from Saunders, that leaves a hike at the next meeting in the balance. EUR/JPY/CHF: All softer vs the Dollar, though within recent/familiar ranges on the wide, as Eur/Usd meanders between 1.2290-1.2390, Usd/Jpy sits in the middle of 107.35-75 parameters and Usd/Chf is even more tightly bound from 0.9705-30. However, for those unsure on Thursday Eur/Chf clearly crossed the 1.2000 line earlier amidst more SNB assurances that policy is not about to change even though the Franc is less highly valued.

In commodities, oil was lower on European equity close on Thursday, and currently trading flat on the day with WTI at USD 68.38 and Brent at USD 73.85. This comes as some profit taking is being seen following a touch on over 2 year highs. OPEC specifically we have heard from various oil ministers speaking at the OPEC JMMC meeting, as well as comments from Russia’s Novak saying OPEC and Non-OPEC countries could ease output reductions as soon as 2018, but no move was noted on this. Gold tracking lower for the day, currently down -0.3%, largely due to a strengthening USD. Saudi energy minister Falih says there is a need to strengthen OPEC and Non-OPEC cooperation beyond the current agreement as this is critical to restore market confidence. Russia says it is committed to OPEC/Non-OPEC supply cut agreement until the end of the year; according to sources.

Looking at the day ahead now and March PPI in Germany and April consumer confidence for the Euro area are the highlights. There are no key data releases in the US. The Fed’s Evans and BOE’s Saunders are due to speak. General Electric is due to report earnings.highlights.

US Event Calendar

- No economic events scheduled

- Riksbank’s Ingves, Jansson at IMF, World Bank Spring Meetings

- 9:40am: Fed’s Evans Speaks on the Economy and Monetary Policy

- 11am: Riksbank’s Ingves Gives Speech in Washington

DB’s Jim Reid concludes the overnight wrap

Yesterday was the hottest April day in London since 1949. We saw 29.1 degrees. If my eyes are anything to go by it was also the worst day for birch pollen since about 1524. I’m currently overdosing on my hay fever tablets. I’m hoping that one of the side effects is fast growing hair. Anyway the sudden heatwave has also coincided with a sudden boost in the rising yield and inflation story. This story – which we thought would be the main 2018 theme – has been overtaken by events over the last two months. However is it back to being front and centre now?

Indeed we’ve come a long way very quickly. As we started last week WTI Oil was trading at $62 and 10 year Treasuries at around 2.78%. 10 days later and yesterday oil peaked at $69.5 (currently $68.3) and Treasuries ended at 2.911% yesterday. Oil is at the highest since December 2014 and US 10yrs are within 4bps of their mid-February highs which in turn were the highs since late 2013/early 2014. As an aside we haven’t been above 3.05% since 2011. For the record, 10 year Bund yields were also around 3% back then as opposed to the still moribund (pardon the pun) 0.598% close yesterday which was nearly 7bps higher on the day. Meanwhile US 10 year breakevens marked a fresh high since July 2014 while the 2s10s and 5s30s steepened 3.7bp and 1.4bp respectively.

Interestingly the probability (according to Bloomberg) of four Fed rates hikes in 2018 is now at the highest of the year – at around 33% – from 18% at the start of last week. A reminder that DB has long felt 4 rates hikes (one done) this year and 4 next year are likely.

As discussed above Oil has certainly played its part in the recent move but other commodities have also contributed. For metals (although yesterday was a down day – see below), the big driver appears to be the sanctions imposed on Russia’s Rusal (the largest aluminium supplier outside of China) by the US which has seen a significant volume of metals (namely aluminium) removed from the market. Tariffs talk has also contributed and LME Aluminium is up 24.0% in April alone. At the same time our commodities strategists noted that this has come at a time when China’s primary supply growth in Aluminium is set to decelerate sharply this year on a combination of limited new capacity and cost pressures.

For Oil, the story is more one of fundamentals with OPEC highlighting that high inventories, which had weighed on the market for the last few years, have now been largely wiped out, helping to rebalance the market. The demand side of the equation is also said to have improved of late in the lead up to the northern hemisphere summer. It’s worth noting that OPEC energy ministers have been meeting over the last 36 hours. Watch out for any headlines.

In addition our Chinese economists have recently upgraded their near-term GDP forecasts (link) which seems to be a little off consensus and if correct we could be seeing evidence of this better growth outlook in the recent commodities rally.

In terms of supporting data, the prices paid component of yesterday’s Philly Fed was at the highest since May 2008 and this would have been collated before the latest commodity price surge. DB’s Alan Ruskin showed a graph suggesting that at these levels and with the usual lead time, this is consistent with core YoY US CPI close to 3% by H2 2019.

This morning markets in Asia are trading lower with the Nikkei (-0.05%), ASX200 (-0.24%), Kospi (-0.35%), Hang Seng (-0.42%) and Shanghai Comp. (-1.20%) all down as we type. Datawise, Japan’s headline and core March CPI (ex-food) were both in line at 1.1% yoy and 0.9% yoy respectively. Elsewhere, Bloomberg noted the US Treasury Department is considering using an emergency law that would allow President Trump to block Chinese related investments in sensitive technologies.

Now recapping other markets performance from yesterday. The S&P initially traded down c1%, impacted by tech and consumer staple stocks as the world’s largest contract chipmaker (Taiwan Semiconductor) cut its 2Q revenue forecasts by c10% while Philip Morris dropped a stunning -15.6% post its results. Eventually, the index pared back losses to close -0.57%, in part as Bloomberg reported that Deputy Attorney General Rosenstein told President Trump last week that he is not a target of any part of the Special Counsel Mueller’s investigations.

Elsewhere, the Nasdaq (-0.78%) and Dow (-0.34%) trended lower while the Stoxx 600 edged up +0.02%. The VIX rose for the second straight day to 15.96 (+2.3%). In the UK, the BOE Governor Carney has reiterated that Britain should prepare “for a few interest rates over the next few years” and that a rate hike this year was “likely”, but he seemed to dampen down the expectation for a May hike by noting that there was also “other meetings” this year. The Euro and Sterling ended -0.23% and -0.82% lower respectively, while the USD dollar index rose for the third straight day (+0.35%). In commodities, precious metals were little changed (Gold -0.29%; Silver +0.32%) while other base metals retreated, in part as Bloomberg reported Russia may provide support to Rusal given the current US sanctions on the firm (Copper -0.73%; Zinc -0.86%; Aluminium -1.86%).

Turning to the four Fed speakers overnight on inflation and financial stability. Ms Mester who is a voter this year said she “doesn’t expect inflation to pick up sharply” and that “further (gradual) increases in interest rates will be appropriate this year and next”, in part to allow inflation to move back up to the 2% target. Elsewhere, Ms Brainard noted that while economic activity has improved, “we cannot afford to be complacent”. She added that the current level of bank capital is a “sign of strength” but she is “reluctant” to see big banks reducing their capital buffers and voiced her support for a lift in the counter-cyclical buffers on banks from 0% currently. Following on, Mr Rosengren noted that the US fiscal and monetary policy are poorly positioned to respond to economic stresses, in part as higher level of government debt to GDP may limit the ability of authorities to offset a financial or economic shock. Finally on trade, the soon to be retiring Mr Dudley said “we’re watching (the trade negotiations) very, very closely”, in part as it could deliver a good outcome, “but it could also go on a much less favourable way”.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the April Philly Fed index edged up 0.9pts mom and was above market at 23.2 (vs. 21 expected) while the March Conference board leading index was in line at 0.3% mom. Elsewhere, the weekly initial jobless claims (232k vs. 230k expected) and continuing claims (1,863k vs. 1,845k expected) were slightly above expectations. Back home, the UK’s March core retail sales fell more than expected at -0.5% mom (vs. -0.4% expected), with the weakness partly due to harsh weather during the quarter. My has that changed now!!!

Looking at the day ahead now and March PPI in Germany and April consumer confidence for the Euro area are the highlights. There are no key data releases in the US. The Fed’s Evans and BOE’s Saunders are due to speak. General Electric is due to report earnings.highlights.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed DOWN 45.83 POINTS OR 1.47% /Hang Sang CLOSED DOWN 290.11 POINTS OR 0.94% / The Nikkei closed DOWN 28.94 POINTS OR 0.13%/Australia’s all ordinaires CLOSED DOWN .20% /Chinese yuan (ONSHORE) closed DOWN at 6.2924/Oil UP to 69.08 dollars per barrel for WTI and 74.33 for Brent. Stocks in Europe OPENED MIXED. ONSHORE YUAN CLOSED DOWN AT 6.2924 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.2843/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING A LITTLE WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea

3 b JAPAN AFFAIRS

end

c) REPORT ON CHINA/HONG KONG

The ban on high tech chips will be deadly to China and they plan to hit back against the ZTE ban

(courtesy zerohedge)

China Hits Back Against ZTE Ban Amid Rising Tide Of Anti-American Sentiment

China is taking active measures against a major escalation in the brewing trade-war with the United States, and “won’t allow the U.S. to use chips as a stick against it”, following Monday’s ban of American component sales to Chinese smartphone manufacturer ZTE, reported the country’s state-owned nationalist tabloid Global Times.

“The Trump administration is helping us Chinese make such a decision,” the paper said, “thanking” Trump for forcing China to take measures that eliminate China’s reliance on US technologies.

Trump’s latest trade war salvo appears to have unleashed a tide of patriotic backlash in China’s cyberspace. A photograph showing ZTE’s 76-year-old founder Hou Weigui with senior executives at a mainland airport about to catch a flight to the United States prompted a torrent of messages of support: “Trying so hard, bearing so much, all to fight for China’s interest – how touching!” said one popular comment that played on a comparison with a late Qing dynasty official, Li Hongzhang, a chief negotiator in the first Sino-Japanese war.

Curiously, a bifurcation in sentiment promptly emerged, and while sympathy for ZTE swept across Chinese social media, most official domestic newspapers have chosen to cast the blame for the telecom equipment maker’s troubles on China’s heavy reliance on foreign semiconductors. In one widely circulated photograph online, an unidentified restaurant erected a banner with patriotic slogans calling for solidarity and offering ZTE employees free meals.

“If it were not because of ZTE’s strength and ability to represent China, it would not have been punished like this,” the banner said according to Reuters.

Another Global Times article said the move against ZTE was a strong push for China to strengthen its domestic chip industry. China’s semiconductor-related imports from the United States last year came to $11 billion.

At this rate, it’s only a matter of time until – in a rerun of China’s territorial and trade spat with Japan from 2011/2012 – China’s populist press urges the local population to avoid all US imports, including iPhones, leading to an even steeper deterioration in the US trade deficit with Beijing.

* * *

Meanwhile, away from the media reaction, in response to the ban China is looking to supercharge the growth of its already aggressive push into domestic semiconductor manufacturing, two people with direct knowledge of the plans tell Reuters.

On Monday, we reported that the White House has banned American companies from selling components to Chinese telecom-equipment manufacturing giant Zhongxing Telecommunications Equipment (ZTE) for seven years, accusing the company of lying during a settlement negotiation.

Previously, the Department of Commerce determined that ZTE had made false statements to the Bureau of Industry and Security during 2016 settlement negotiations and during its 2017 probationary period. As a reminder, China’s No.2 telecoms equipment maker pleaded guilty in March 2017 of illegally shipping U.S. technologies to banned countries including Iran. ZTE also paid nearly $900 million in fines and penalties, and an additional $300 million that could be imposed in the future.

The seven-year ban on U.S. firms selling parts to ZTE comes at a time when the two countries have threatened each other with tens of billions of dollars in tariffs in recent weeks, fanning worries of a full blown trade war. –Reuters

The ban could be catastrophic for ZTE, the fourth-largest smartphone vendor in the United States, as it is estimated to rely on U.S. firms for nearly a third of crucial components such as chips in its products.

In response, Reuters reports that Senior Chinese officials have been holding meetings with industry bodies, regulators and the country’s influential chip fund, about accelerating already aggressive plans for the sector. The discussions underscore China’s growing concerns over its reliance on imported technology from companies such as Intel and Qualcomm – which would be at risk as tensions flare between Washington and Beijing. An escalation here could also jeopardize China’s ambitions to become an technological peer and equivalent of the US (largely by reverse-engineering the latest US technologies). As a result, “in the last few days senior Chinese officials have met to discuss plans to speed up the development of the chip industry” Reuters reported.

A second person with knowledge of the talks said senior officials had met with key ministries, as well as the National Integrated Circuitry Investment Fund, “this week” to discuss speeding up plans due to recent trade tensions. –Reuters

China has made the semiconductor industry a key priority as part of its “Made in China 2025” initiative aimed at reducing dependence on foreign technology imports. The plan calls for at least 40% of all Chinese smartphones to contain domestically manufactured chips – which the government is plowing billions of dollars into.

Analysts say money is now “raining down” from Beijing and state-backed funds to support the chip market, while the country’s state chip fund, known as the “Big Fund”, raised an estimated $32 billion in a new round of financing last month. –Reuters