GOLD: $1202.95 DOWN $2.65 (COMEX TO COMEX CLOSINGS)

Silver: $14.22 DOWN 2 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold $1201.95

silver: $14.19

For comex gold:

SEPT/

And now Sept:

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 0 NOTICE(S) FOR NIL OZ

Total number of notices filed so far for Sept: 551 for 55100 (1.7138 tonnes)

For silver:

Sept

83 NOTICE(S) FILED TODAY FOR

415,000 OZ/

Total number of notices filed so far this month: 5723 for 28,615,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6407/OFFER $6492: UP $111(morning)

Bitcoin: BID/ $6388/offer $6474: UP $92(CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1209.73

NY price at the same time:$1204.50

PREMIUM TO NY SPOT: $5.23

XX

Second gold fix early this morning: $ 1209.13

USA gold at the exact same time:$1204.80

PREMIUM TO NY SPOT: $4.33

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE 2166 CONTRACTS FROM 208,969 DOWN TO 206,803 DESPITE YESTERDAY’S 9 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE MOVED FURTHER FROM LAST MONTH’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

24 EFP’S FOR SEPT. 496 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 520 CONTRACTS. WITH THE TRANSFER OF 520 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1217 EFP CONTRACTS TRANSLATES INTO 2.600MILLION OZ ACCOMPANYING:

1.THE 9 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND NOW 30.475 MILLION OZ STANDING SO FAR IN SEPT.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

18,871 CONTRACTS (FOR 8 TRADING DAYS TOTAL 18,871 CONTRACTS) OR 94.355 MILLION OZ: (AVERAGE PER DAY: 2358 CONTRACTS OR 11.794 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 94,355 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 13.47% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,132.18 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2166 DESPITE THE 9 CENT RISE IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 520 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A CONSIDERABLE SIZED: 1646 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 520 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A DECREASE OF 2166 OI COMEX CONTRACTS. AND ALL OF THIS LACK OF DEMAND HAPPENED WITH A 9 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.24 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND NOW IN SEPTEMBER AN INITIAL MONSTROUS 30.475 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.034 MILLION OZ TO BE EXACT or 148% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 83 NOTICE(S) FOR 415,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244.,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. AND NOW SEPT: AN INITIAL HUGE 30.475 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 2040 CONTRACTS UP TO 471,490 WITH THE GAIN IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A RISE IN PRICE OF $8.00). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8969 CONTRACTS:

OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 8969 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 471,490. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN VERY STRONG SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,009 CONTRACTS: 2040 OI CONTRACTS INCREASED AT THE COMEX AND 8969 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 11,009 CONTRACTS OR 1,100,900 OZ = 34.24 TONNES. AND ALL OF THIS HUGE DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $8.00

YESTERDAY, WE HAD 8670 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 67,337 CONTRACTS OR 6,733,700 OZ OR 209.44 TONNES (8 TRADING DAYS AND THUS AVERAGING: 8417 EFP CONTRACTS PER TRADING DAY OR 841,700 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAYS IN TONNES: 209.44 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 209.44/2550 x 100% TONNES = 8.21% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,406.36* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 2040 WITH THE GAIN IN PRICING ($3.00 THAT GOLD UNDERTOOK YESTERDAY) // . WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8969 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8969 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 11,009 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8969 CONTRACTS MOVE TO LONDON AND 2040 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 34.24 TONNES). ..AND THIS HUGE DEMAND OCCURRED WITH A RISE OF $8.00 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $2.65 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/GLD INVENTORY 745.18 TONNES

Inventory rests tonight: 745.18 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 2 CENTS TODAY

WE HAD A HUGE CHANGES FOR SILVER : A DEPOSIT OF 1.316 MILLION OZ INTO THE SLV INVENTORY

/INVENTORY RESTS AT 334.973 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 2166 CONTRACTS from 208,969 DOWN TO 206,803 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST MONTH AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

24 EFP CONTRACTS FOR SEPTEMBER, 496 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 520 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2166 CONTRACTS TO THE 520 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET LOSS OF 1646 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 8.230 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. AND NOW A HUGE 30.475 MILLION OZ INITIALLY STAND FOR SILVER IN SEPTEMBER….

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 9 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING YESTERDAY. BUT WE ALSO HAD A SMALL SIZED 520 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i) THURSDAY MORNING/ WEDNESDAY NIGHT: Shanghai closed UP 30.47 POINTS OR 1.15% /Hang Sang CLOSED UP 669.45 POINTS OR 2.54%/ / The Nikkei closed UP 216.71 POINTS OR 0.96%/Australia’s all ordinaires CLOSED DOWN 0.70% /Chinese yuan (ONSHORE) closed DOWN at 6.8668 AS POBC STOPS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER/Oil DOWN to 69.44 dollars per barrel for WTI and 79.17 for Brent. Stocks in Europe OPENED GREEN //. ONSHORE YUAN CLOSED UP AT 6.8468 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8429: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS NOT DOING TOO GOOD : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

i)UK

Bank of England keeps rates unchanged and this was widely expected

( zerohedge)

ii)EU/ECB

iii)UK/RUSSIA/SKRIPAL POISONING

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY/ EARLY THIS MORNING:

TURKISH lira crashes to 6.55 after Erdogan attacks his central bank hours before a rate decision. Must be fun in his household as the chief central banker is his son in law

( zerohedge)

ii)Our Turkish Central banker, the son in law of Erdogan, is certainly going to have lots of scorn in his household as he raised interest rates rise by a massive 625 basis points to 24%. That will certainly kill off most of their businesses inside Turkey

iii)We have been highlighting to you the ambitions of Erdogan over the past year. Several authors have stated that Turkey is deficient in energy and the Turkish leader will encroach on other sovereign territories to secure their much needed oil and gas. This is why they covet the Cyprus big gas field discovered by the Israelis over 4-5 years ago. The Israelis will protect the Cypriots.

( zerohedge)

v)Iran/Turkey

vi)Russia/USA

The USA will introduce more severe sanctions on Russia over the Skripal case. This time it will be aimed at the venerable banks

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Argentina

Argentina’s annual inflation rate just hit 34.4% with the Peso hitting an all time low of 39.55 to the dollar

(courtesy Gillespie/Bloomberg)

9. PHYSICAL MARKETS

i)the drunkard Juncker vows to turn the euro into a reserve currency. Wishful thinking

( GATA/London’s Financial Times)

ii)Craig Hemke of Sprott Money suggests the data is not to bullish for paper gold and silver

( Craig Hemke/Sprott/GATA)

iii)These guys come up with a novel thought that gold and silver are under valued

(courtesy USAgold/GATA)

iv)Interesting: the head of a Russian bank, VTB, stated that because of the USA sanctions customers may not get dollars back from their dollar account

( Bloomberg/GATA)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

MARKET TRADING

Consumer prices supposedly have been contained at 2.7% vs expectations of a 2.8% rise. However services are still very much inflationary. Even hour earnings are on the rise and this in very inflationary!! The dollar tanks, yields tank

(courtesy zerohedge)

b)Goldman Sachs warns of a huge 6 trillion dollars in losses in a global trade war.

( Goldman Sachs/zerohedge)

c)Even though the storm has been reduced to a category 2, Florence is expected to crate huge damage in excess of 30 billion dollars

(courtesy zerohedge)

d)That did not last long: Trump states that contrary to Mnuchin, the USA is under no pressure to make a deal with China

(courtesy zerohedge)

e)A detailed look at the August budget deficit which just hit a huge 222 billion dollars for the month, the highest deficit of recorded history. Spending advanced by a whopping 433 billion dollars

(your detailed August budgetary deficit/zerohedge)

iv)SWAMP STORIES

please give me a break!!

(courtesy zerohedge)

b)From the King report and special thanks from Chris Powell for sending this to us:

( King report

Let us head over to the comex:

The next active delivery month after August for silver is September and here the OI FELL by 7 contracts DOWN to 455.

We had 15 notices filed on yesterday so we gained 8 contracts or 40,000 ADDITIONAL oz will stand at the comex as these guys refused a fiat bonus as well as a London based forwards. For the past 17 months starting in April 2017, we have been witnessing on a constant basis queue jumping as the commercials seek physical silver immediately after first day notice. After a little holiday,queue jumping in the silver pits resumed in earnest today.

October lost 21 contracts to stand at 561. November saw a gain of 26 contracts to stand at 67.

ON FIRST DAY NOTICE FOR THE SEPT/2017 SILVER CONTRACT MONTH: 20.515 MILLION OZ STOOD FOR DELIVERY AND BY MONTH’S END: A HUGE 32.875 MILLION OZ WAS THE FINAL STANDING AS WE WERE WELL INTO THE PHENOMENON OF QUEUE JUMPING IN SILVER. THUS WE ARE WAY AHEAD OF LAST YEAR AS ALREADY WE HAVE 30.475 MILLION OZ OF SILVER INITIALLY STAND. WE WILL NO DOUBT PASS LAST YEAR’S TOTAL OF 32.875 MILLION OZ ONCE SEPTEMBER ENDS AS THE BANKS SCRAMBLE FOR PHYSICAL SILVER.

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Video: BREXIT To Contribute To London Property Bubble Bursting

Video: BREXIT To Contribute To London Property Bubble Bursting

– Brexit in conjunction with severe price unaffordability, rising interest rates and global economic uncertainty is leading to sharp price falls in London home prices

– London home prices have fallen five months in a row with property prices more than 7% lower in 12 months in some areas

– The Economist has done research which suggests that London house prices are 50% overvalued and Dublin house prices are 25% overvalued

– The Economist believes that there are many cities with properly bubbles vulnerable to sharp corrections due to rising interest rates and geopolitical uncertainty and unaffordability

– Reuters poll of housing market analysts and experts predicted that London house prices will continue to fall in 2018 and 2019, with a one-in-three chance of a house price crash

Watch Full Video and Subscribe On YouTube

News and Commentary

Juncker vows to turn euro into reserve currency to rival petro-dollar (Politico.eu)

Gold near 1-wk highs as Sino-U.S. trade talk hopes hurt dollar (Reuters.com)

The Fed is trying to finally get back to ‘normal’ after the crisis (CNBC.com)

As Trump embraces more tariffs, U.S. business readies public fight (Reuters.com)

U.S. producer prices post first drop in one-and-a-half years (Bloomberg.com)

Source: SilverInstitute.org

Euro Has the Power to Challenge the Dollar (Bloomberg.com)

Gundlach Says Dollar’s Next Move May Be Downward (Bloomberg.com)

Here’s why one analyst just made a ‘rare’ call to buy some gold (MarketWatch.com)

China to Continue Driving Global Silver Market Forward (SilverInstitute.org)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

12 Sep: USD 1,197.80, GBP 919.07 & EUR 1,033.10 per ounce

11 Sep: USD 1,194.00, GBP 915.92 & EUR 1,028.75 per ounce

10 Sep: USD 1,195.80, GBP 923.28 & EUR 1,032.45 per ounce

07 Sep: USD 1,200.75, GBP 928.30 & EUR 1,031.32 per ounce

06 Sep: USD 1,204.30, GBP 931.65 & EUR 1,035.82 per ounce

05 Sep: USD 1,194.70, GBP 932.46 & EUR 1,031.74 per ounce

Silver Prices (LBMA)

12 Sep: USD 14.16, GBP 10.90 & EUR 12.22 per ounce

11 Sep: USD 14.13, GBP 10.85 & EUR 12.19 per ounce

10 Sep: USD 14.22, GBP 10.99 & EUR 12.28 per ounce

07 Sep: USD 14.19, GBP 10.90 & EUR 12.20 per ounce

06 Sep: USD 14.27, GBP 11.03 & EUR 12.27 per ounce

05 Sep: USD 14.17, GBP 11.05 & EUR 12.22 per ounce

Recent Market Updates

– Australia’s Banking System May Be The “Bloody Big Butterfly” Which Triggers Next “Financial Storm”

– Ten Years Since Lehman: Biggest Driver of 2008 Financial Crisis Has Only Got Worse

– London Property: Here Comes the Crash

– This Week’s Golden Nuggets

– Gold Remains An “Excellent Way to Hedge” for Longer Term – BNP Interview

– Video: Gold Surges To Record Highs In Emerging Market Currencies – New Highs In USD, EUR, GBP In the Coming Months?

– September Is The Best Month For Gold and Worst Month For Stocks

– Pound Investors Face Months of Volatility Into Brexit Endgame

– This Week’s Golden Nuggets

– Video: “Financial War” Deepens as Russia Buys Gold and Dollar Hegemony At Risk – Rickards on CNN

– Will Indebted Nations Globally Follow Venezuela Into Hyperinflation?

– End Of Dollar Hegemony May Happen Soon and Badly Impact Indebted America

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

the drunkard Juncker vows to turn the euro into a reserve currency. Wishful thinking

(courtesy GATA/London’s Financial Times)

Juncker vows to turn euro into reserve currency to rival dollar

Submitted by cpowell on Wed, 2018-09-12 14:05. Section: Daily Dispatches

By Mehreen Khan and Jim Brunsden

Financial Times, London

Wednesday, September 12, 2018

Jean-Claude Juncker has vowed to turn the euro into a global reserve currency that could rival the dollar as part of the European Union’s drive to reduce its financial dependence on the United States.

In his last “State of the Union” speech to members of the European Parliament in Strasbourg today, the president of the European Commission said it was an “aberration” that the EU paid for more than 80 percent of its energy imports in U.S. dollars despite only 2 percent of imports coming from the U.S.

Most of the dollar-denominated imports are from Russia and the Gulf states.

“We will have to change that. The euro must become the active instrument of a new sovereign Europe,” said Mr. Juncker, whose five-year tenure as commission president is due to end next year.

…

… For the remainder of the report:

https://www.ft.com/content/7358f396-b66d-11e8-bbc3-ccd7de085ffe

END

Craig Hemke of Sprott Money suggests the data is not to bullish for paper gold and silver

(courtesy Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: Trader data not so

bullish for gold, silver

Submitted by cpowell on Wed, 2018-09-12 19:24. Section: Daily Dispatches

3:27p ET Wednesday, September 12, 2018

Dear Friend of GATA and Gold:

Trader positioning data in gold and silver futures in the United States is not as bullish as the prevailing analysis describes, the TF Metals Report’s Craig Hemke writes today at Sprott Money. Particularly, Hemke writes, nothing in the data shows that JPMorganChase & Co., the big player in the monetary metals markets, has gone long in the monetary metals.

Hemke’s commentary is headlined “What Is a Bank and What Is a Commercial?” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/what-is-a-bank-and-what-is-a-commercial…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

These guys come up with a novel thought that gold and silver are under valued

(courtesy USAgold/GATA)

USAGold’s News & Views September newsletter is up

Submitted by cpowell on Wed, 2018-09-12 20:04. Section: Daily Dispatches

4:08p ET Wednesday, September 12, 2018

Dear Friend of GATA and Gold:

USAGold’s News & Views newsletter for September features an essay by Thorsten Polleit of the Degussa Market Report arguing that gold is undervalued at the moment, as well as a digest of other gold-related news and commentary. It’s posted in the clear at USAGold here:

http://www.usagold.com/publications/NewsViewsSEPT2018.html

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Interesting: the head of a Russian bank, VTB, stated that because of the USA sanctions customers may not get dollars back from their dollar account

(courtesy Bloomberg/GATA)

Head of Russian bank warns customers they may not get dollars back

Submitted by cpowell on Wed, 2018-09-12 22:29. Section: Daily Dispatches

By Annmarie Hordern and Jake Rudnitsky

Bloomberg News

Wednesday, September 12, 2018

Russians with bank accounts in dollars may find they can only make withdrawals in other currencies if new sanctions proposed by U.S. lawmakers take effect.

“I am sure that all the clients of all banks should receive their money back. That’s the principal approach,” VTB Group Chief Executive Officer Andrey Kostin said today. “How, in which currency, is a different story.

The U.S. Senate is considering punishing the Kremlin for alleged election meddling, including a fresh raft of measures dubbed the “bill from hell.” This could bar Americans from buying new issues of Russian sovereign debt and ban Russia’s largest state banks, such as VTB, from using dollars.

Kostin’s comments are an indication to markets that policy makers and businesses are bracing for the worst, and could focus investors’ attention on the possible fallout from sanctions, according to Liza Ermolenko, an economist at Barclays Capital in London. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-09-12/russians-may-have-to-…

end

A good commentary on how physical gold accumulations will kill the petrodollar

(courtesy Stefan Gleason)

Gold accumulations could checkmate the petrodollar

September 13, 2018

by: Stefan Gleason*

President Donald Trump’s administration is playing a game of high-stakes international chess with Russia, Iran, Turkey, China, and other countries viewed as adversaries in trade and geopolitics.

It’s not necessarily the case that tariffs, sanctions, and blustering will result in a hot war. More likely, escalating strife between the U.S. and a bloc of much more populous adversaries will push them to unite more closely to undermine and ultimately dethrone King Dollar.

The U.S. has long been the grandmaster – the dominant player on the geopolitical board – owing largely to its unique reserve currency status.

Quite simply, the U.S. dollar is the go-to currency for world trade. Oil and gold are traded in dollars. Manufactured goods on the international market are traded in dollars. All other currencies are measured against the dollar.

Nations Anxiously Moving to Dollar Alternatives

But all that is in the process of changing. As Washington, D.C.’s international adversaries pursue contra-dollar alliances, it could soon be checkmate for King Dollar.

President Trump recently touted tariffs designed to punish Turkey. The tariffs triggered the biggest financial crisis Turkey has seen in decades.

That may well have been the intended consequence. But the unintended consequence is that Turkey is now being pushed to form stronger economic ties with Iran… which in turn is forming stronger ties with Russia… which in turn is forming stronger ties with China.

The countries being targeted with tariffs and sanctions have a much larger combined GDP and a combined population that is multiples of the United States.’ What if a contra-dollar bloc formed that was determined to isolate the U.S. from the world financial system?

Russian Deputy Foreign Minister Sergei Ryabkov recently told International Affairs, “The time has come when we need to go from words to actions and get rid of the dollar as a means of mutual settlements and look for other alternatives.”

Foreign Gold Buying Is Ramping Up

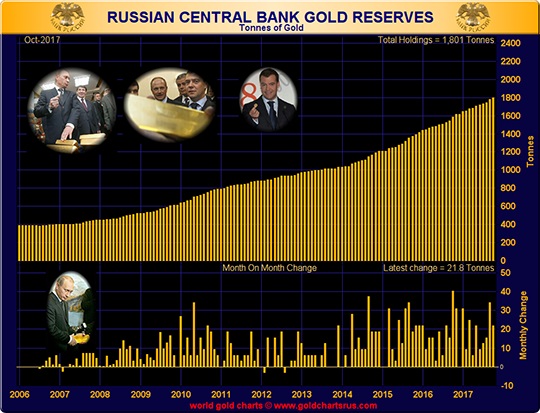

One of those alternatives is gold. The Central Bank of Russia is ramping up its gold buying and reducing its holdings of U.S. Treasuries. In recent years, in fact, Russia has been the largest official buyer of gold – followed closely by China.

Earlier this year, the Shanghai International Energy Exchange launched a futures contract for crude oil priced in Chinese yuan. Now Chinese and other international traders can trade the world’s most important energy commodity in a liquid market without using U.S. dollars.

China has also launched a pilot program to purchase oil from Russia and Angola (two of its top suppliers) using yuan. It’s another gambit in the currency war being fought by major powers that have been targeted by the U.S. administration for punishment.

Those calls turned out to be premature. The petro-dollar lived to fight another decade, boosted the perception of the U.S. dollar as a safe haven during the financial crisis and later by the shale oil fracking boom that saw North American oil production surge.

Whether this method of production is sustainable at current oil prices remains to be seen. What’s not sustainable is the U.S. government (officially $21 trillion in debt) being able to extend itself militarily and through punitive economic measures to prop up the petro-dollar.

According to Gal Luft of the Institute for the Analysis of Global Security, “The main front where the future of the dollar will be decided is the global commodity market, especially the $1.7 trillion oil market.”

The Dollar’s Dominance in Global Transactions May End on Trump’s Watch

If China wants to buy oil from Saudi Arabia in yuan, from Russia in rubles or from Iran in gold, then OPEC nations and other major energy exporters will surely figure out how to accommodate their biggest customers.

Whether a new global standard emerges or multiple competing standards rise in tandem, the dollar’s multi-decade run as the world’s dominant transactional currency could end on Trump’s watch.

The trend in the value of the dollar versus other fiat currencies and gold is another question.

China doesn’t actually want the greenback to go down versus its yuan – at least not at this point in the currency wars.

The one alternative currency that stands to benefit as the major national currencies battle each other is gold. It’s the only monetary asset that has proven to be resilient against all economic and geopolitical threats.

*Stefan Gleason is President of Money Metals Exchange, the national precious metals company named 2015 “Dealer of the Year” in the United States by an independent global ratings group.

-END-

___________________________________________________________________________________________________________________________________________________________________________________

Your earlyTHURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8468/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER //OFFSHORE YUAN: 6.8429 /shanghai bourse CLOSED UP 30.47 POINTS OR 1.15% /HANG SANG CLOSED UP 669.45 POINTS OR 2.54%

2. Nikkei closed UP 216.71 POINTS OR 0.96%/USA: YEN FALLS TO 111.55/

3. Europe stocks OPENED IN THE GREEN EXCEPT LONDON

/USA dollar index RISES TO 94.86/Euro RISES TO 1.1633

3b Japan 10 year bond yield: FALLS. +.11/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.29/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 69.44 and Brent: 79.17

3f GoldUP/JAPANESE Yen DOWN/ CHINESE YUAN: ON SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.420%/Italian 10 yr bond yield UP to 2.95% /SPAIN 10 YR BOND YIELD UP TO 1.46%

3j Greek 10 year bond yield FALLS TO : 4.03

3k Gold at $1206.10 silver at:14.22 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 78 /100 in roubles/dollar) 68.22

3m oil into the 69 dollar handle for WTI and 79 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.55DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9789 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1272 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.42%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.98% early this morning. Thirty year rate at 3.12%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.1751

Global Stocks Rise Ahead Of Central Bank Barrage,

Inflation Data

Global trade was front and center again, after the Trump administration proposed another round of trade talks with Beijing before slapping China with $200BN in tariffs in the absence of key concessions from Beijing, while traders were on edge ahead of a slew of central bank announcements and critical CPI data in the US.

One day after Apple’s latest iPhone unveiling disappointed shareholders who sold AAPL stock and pressured tech stocks, world markets calmed and MSCI’s All World index was set for a fourth straight day of gains with S&P futures slightly higher after Asian shares jumped ending a 10 day losing streak, the longest in 16 years, on renewed hopes of fresh trade negotiations between the US and China.

Shanghai, Tokyo, Jakarta stocks all gained around 1% following Wednesday’s sharp drop in the dollar, while Hong Kong’s Hang Seng finished up 1.8%, while China’s yuan also edged higher in the currency markets even if the Shanghai Composite barely budged amid ongoing skepticism inside Ground Zero, China, that talk this time will be different.

Initially, Europe also moved higher, led by automakers with gains between 0.2% and 0.6% for German, French, Italian and Spanish shares offsetting a weaker FTSE in London which was hit by weaker oil and tobacco stocks. However, Europe’s Stoxx 600 index erased gains of as much as 0.3% as the Turkish lira plunged after country’s President Recep Tayyip Erdogan attacked the central bank for continuously missing inflation targets and saying the CBRT “should cut this high interest rate”, just hours before rate decision.

European shares have remained especially sensitive to rising EM risks, especially in Turkey, as exporters and banks have exposure to developing nations. Meanwhile, The euro edged lower and the pound was steady ahead of central bank announcements which are not expected to deliver any major surprises.

Staying in Europe there was some more Italian drama, after La Stampa reported that Italian Finance Minister Giovanni Tria called Prime Minister Giuseppe Conte to discuss the struggle over the 2019 budget and threatened to resign. The FTSE MIB was trying to bounce back after a 17% drop in the past four months, while Italian bonds declined for a third day after the nation’s latest debt auction drew weaker demand.

Meanwhile, as previewed earlier, as part of today’s ECB announcement, the biggest “surprise” will likely be that growth forecasts are tweaked lower, even as the central bank keeps its guidance on interest rates which will stay at record lows “at least through the summer” of next year. According to Bloomberg, given the highly negative sentiment toward the banks – the sector index SX7P is down more than 20% since a peak in January, trades below book value and at 9.3x expected earnings which is its lowest P/E ratio in two years, with a dividend yield of 5% – risk seems to be on the upside for the sector heading into Draghi’s press conference.

Over in the US, index futures all pointed to a slightly firmer open.

In FX, the dollar nudged higher after a weaker than expected PPI report which saw producer prices drop for the first time in 18 months, undermined the case for a faster pace of policy tightening by the Federal Reserve. The latest CPI data is due out at 8:30am today.

The euro hovered around $1.1624 having gained around 0.6 percent so far this week. The yen weakened 0.2 percent to 111.47 per dollar on the soothing trade noises. Sterling held near a six-week high of $1.3087 as Brexit-supporting lawmakers in British Prime Minister Theresa May’s party publicly pledged support for her to stay in power.

Treasuries edged lower while Italy’s bonds under-performed other European sovereign debt as speculation swirled around the fate of the country’s finance minister.

Elsewhere, emerging-market shares and currencies climbed helped by the recent weakness in the dollar, with South Africa’s rand leading the pack. Crude oil pared two days of gains made on the outlook for tighter supply. The potential impact on commodities from Hurricane Florence faded with lower wind speeds. Meanwhile copper held above $6,000 in London as metals broadly keep Wednesday’s gains on optimism around an easing in the US-China trade war.

Market Snapshot

- S&P 500 futures up 0.09% to 2,891.00

- STOXX Europe 600 up 0.2% to 377.96

- MXAP up 0.9% to 160.29

- MXAPJ up 0.9% to 512.81

- Nikkei up 1% to 22,821.32

- Topix up 1.1% to 1,710.02

- Hang Seng Index up 2.5% to 27,014.49

- Shanghai Composite up 1.2% to 2,686.58

- Sensex up 0.8% to 37,717.96

- Australia S&P/ASX 200 down 0.8% to 6,128.72

- Kospi up 0.1% to 2,286.23

- German 10Y yield rose 0.5 bps to 0.416%

- Euro down 0.06% to $1.1619

- Brent Futures down 0.9% to $79.03/bbl

- Italian 10Y yield rose 0.8 bps to 2.589%

- Spanish 10Y yield rose 0.2 bps to 1.465%

- Brent Futures down 0.9% to $79.03/bbl

- Gold spot down 0.03% to $1,205.82

- U.S. Dollar Index up 0.1% to 94.92

Top Overnight News

- U.S. government has proposed another round of trade talks with Beijing to avoid further escalation in Donald Trump’s trade war with China, the president’s top economic adviser said

- If ECB President Mario Draghi intends to plow on with the plan to phase out asset purchases starting next month, then he’ll need to explain why the confidence of policy makers remains intact: decision day guide

- Hurricane Florence weakened on its course to the U.S. East Coast, but is still big enough to deliver a rainy punch and threaten a huge swath of the Carolinas coastline

- Italian bonds declined for a third day amid reports that Finance Minister Giovanni Tria threatened to quit over the country’s budget negotiations and the nation’s latest debt auction drew weaker demand

- The ECB said banks have selected the euro short-term rate, or Ester, as their preferred replacement for Eonia, a gauge of how much they charge each other for loans

- Erdogan published an executive decree that forces contracts between two entities in Turkey to be made in liras rather than foreign currencies

- Australian employment jumped by more than twice economists’ estimates in August, while the jobless rate remained unchanged as more people sought jobs

- Bank of Japan will keep policy unchanged next week, according to all economists surveyed by Bloomberg. A majority point to the central bank staying on hold until after a sales- tax increase next year

- The EU is gambling on U.K. Prime Minister Theresa May making concessions on the Irish border to pave the way for a Brexit deal in November and are starting to redraft the language on the so-called Irish “backstop” in an attempt to make it more acceptable to Britain

- Pro-Brexit members of May’s Conservative Party are running out of patience with her refusal to ditch her so-called Chequers proposals and will launch a formal leadership challenge against her if she does not do so in the next three weeks

Asian equity markets were positive with sentiment underpinned by hopes of a de-escalation of the trade dispute after the US invited China for trade talks which was seen to be an effort to get negotiations back on track. This lifted most the regional bourses with Nikkei 225 (+0.9%) also euphoric on better than expected Machine Orders which grew at the fastest pace since January 2016, while ASX 200 (-0.8%) bucked the trend as financials were dampened after further unscrupulous practices were revealed at banking royal commission. Elsewhere, Hang Seng (+2.5%) and Shanghai Comp. (+1.2%) were firmer with sentiment boosted by the more encouraging trade-related headlines and after the PBoC upped its liquidity efforts, while participants also digested lending data in which New Yuan Loans missed estimates although Aggregate Financing, which is the broadest measure for China’s credit growth, topped forecasts. Finally, JGBs were flat as focus centred on the region’s riskier assets, while stronger demand at today’s 5yr auction also failed to underpin prices of the 10yr.

Top Asian News

- Nobel Prize Winner’s Microlender Enters Japan to Fight Poverty

- Sri Lanka Says Has Been Acting to Counter Currency, Eco Risks

- Korea Sovereign Fund Exits Investment With Paul Singer’s Elliott

- China Welcomes U.S. Invitation for Trade Talk: Commerce Ministry

Equities are mixed, with trading tentative ahead of the BoE, ECB and CRBT rate decisions later on in the day. Major moves have been confined to equity specific stories, with Michelin’s guidance reaffirmation leading the CAC to the top of the bourse pile. Despite FTSE heavyweights RBS (announcement of a special dividend) and Glencore (base metal strength) outperforming, the FTSE is leading the losses in the index space, with SSE close to the foot of the bourse after a broker downgrade.

The IT sector is the marked sector outperformer with semiconductor names benefiting from AMD’s outperformance in the US session.

Top European News

- European Autos Outperform on Possible New Round of Trade Talks

- Italy Bonds Dip on Report Tria Offered to Quit on Budget Discord

- Reports of Tria Resignation Unfounded: Finance Ministry Official

In FX, the DXY index and broad Dollar are softer post-US initiatives to resume formal trade discussions with China, but off lows and relatively side-lined ahead of US inflation data later. The DXY is attempting to nudge back up towards 95.000 from 94.767 at worst, as Usd/G10 pairings consolidate before Thursday’s headline events. AUD – The major outperformer and beneficiary of planned mediation on tariffs between Washington and Beijing, but still labouring on approaches or rebounds to 0.7200, even with the extra incentive of upbeat Aussie data overnight (August payrolls easily exceeded consensus and largely due to full time jobs). Note also, Aud/Usd flanked by hefty option expiry interest at 0.7220-30 (1 bn) and 0.7140-50 (1.1 bn). JPY – Back to the bottom of the G10 pile on the aforementioned de-escalation of global protectionism tensions, and significantly stronger than expected Japanese machinery orders, with reported domestic offers at 111.50 revisited ahead of larger supply said to be lurking between 111.60-70, plus large option expiries between 111.50-65 (2.1 bn) in the mix. EM – The Lira looks all set to grab the limelight at midday with anticipation/hype running rife for the CBRT rate decision amidst extremely wide-ranging estimates about the extent and manner of the flagged policy stance change. For the benchmark 1 week repo, forecasts span from unchanged to as much as +725 bp, while others suggest that the Bank may be more creative/subtle/restricted and tweak other official rates/corridors instead. Usd/Try poised around the middle of a 6.3385-3905 band in the run-up, while the Rand continues its impressive rebound towards 14.8000 vs the Usd on the softer Dollar overall, and with some independent encouragement from Moody’s downplaying the threat of an SA ratings downgrade.

In commodities, oil is slipping after IEA’s monthly report which reported an increased level of production by OPEC to offset falling Iranian production, and weather premiums are being unwound as Florence has weakened abit more, but is still life-threatening storm surge and rainfall is still expected. Brent futures are now hovering above USD 79.00/bbl after breaking USD 80.00/bbl in Wednesday’s trade. This is discounting the potential support offered to the fossil fuel by the closure of oil production facilities in the eastern part of the South China Sea before two typhoons hit the area. In the metals scope, gold is essentially unmoved ahead of this Thursdays Central Bank flurry, with low volumes seen as investors hold off trading the yellow metal. Shanghai copper (+2.3%) has seen its largest one-day gain in 3 months off the back of restored US-China trade talks, with nickel (+2.6%) and zinc (+2.6%) also benefiting from the improved risk tone. IEA Monthly Report: maintains their global oil demand growth forecast for 2018 and 2019 at 1.4mln bpd and 1.5mln bpd respectively. Said that the global oil market is tightening up. The Brent price range of USD 70-80bbl seen since April could be tested. OPEC crude output stands at a 9-month high of 32.63mln bpd in August.

The day ahead will be dominated by the ECB, BoE, CBT and US CPI but there are other data releases to highlight including the final August CPI revisions in Germany and France, Argentina CPI for August, and the latest weekly jobless claims and August monthly budget statement in the US. Worth flagging also is the IMF conference on sovereign debt including opening remarks from Lagarde, as well as scheduled speeches from the Fed’s Quarles (at 3pm BST) and Bostic (at 6pm BST). We’ve not mentioned the BoE but DB agrees with consensus that no changes to policy are likely. Officials may mention the recent softening in economic data and could comment on ongoing Brexit negotiations, but it shouldn’t be market moving.

US Event Calendar

- 8:30am: US CPI MoM, est. 0.3%, prior 0.2%; CPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%

- US CPI YoY, est. 2.8%, prior 2.9%; CPI Ex Food and Energy YoY, est. 2.4%, prior 2.4%

- 8:30am: Real Avg Weekly Earnings YoY, prior 0.11%; Real Avg Hourly Earning YoY, prior -0.2%

- 8:30am: Initial Jobless Claims, est. 210,000, prior 203,000; Continuing Claims, est. 1.71m, prior 1.71m

- 9:45am: Bloomberg Consumer Comfort, prior 58

- 2pm: Monthly Budget Statement, est. $187.0b deficit, prior $107.7b deficit

DB’s Jim Reid concludes the overnight wrap

There’s the potential for today to be the most exciting day of the week. Indeed, we’ve got the ECB, CBT and BoE meetings as well as a US CPI report all within the space of an hour and a half (from 12pm to 1.30pm for those wanting to get an upper hand on lunch orders).

Of these the ECB, CBT and US CPI are much more likely to be market moving than the BoE. Briefly previewing these, first up is the ECB where our economists’ expectation ( link ) is that we’ll get a confirmation that QE net purchases will be phased out in the final quarter of this year. As a reminder, the ECB included a caveat which gave it optionality of sorts depending on incoming data, but given that the inflation outlook hasn’t weakened since June then there’s little reason to think that there’s been a “major deviation” that could cause the ECB to change its tune. Meanwhile, relative to the most recent consensus expectations, our colleagues note that the June staff forecasts look in line to marginally too optimistic so there’s a moderate risk that the staff revise forecasts slightly lower (around a tenth lower for CPI and GDP). On this it’s worth noting the Bloomberg article doing the rounds yesterday which suggested we would see lower GDP forecasts from the ECB today. Also worth watching out for is President Draghi’s response to Italy. It’s hard to see him approaching any questions from reporters with anything but a straight bat but the market will no doubt be closely watching.

As for Turkey, well the market is expecting the CBT to hike the one-week repo rate to 325bps to 21% although the range among economists on Bloomberg is anywhere from no change to 725bps of hikes. So it could be an interesting meeting. Our economists in Turkey expect ( link ) the CBT hike to 22% while also returning back to full funding from the policy rate. They note that this would translate into 275bps of effective tightening as the marginal lending rate for local banks would move to 22% from 19.25% currently at the overnight facility. Despite rallying yesterday (+1.35%), the Lira is still down -40.19% YTD so clearly the market is crying out for some policy stability to help stem the rout. The question though is how much tightening is needed.

Elsewhere, the consensus for US CPI this afternoon is another +0.2% mom core print for August – the 35th month in a row with such a forecast – which should be enough to keep the annual reading at +2.4% yoy. Our US economists actually expect the latter to round down to +2.3%, however the three and six month annualized changes should firm to +2.45% and +2.12% respectively so it should continue to ensure that the Fed remain resolute in their tightening mode. Last Friday’s strong AHE print and Tuesday’s JOLTS data signalled that inflationary wage pressures should continue, so the inflation pulse does seem to still be on the up for the US right now.

Going into Super Thursday markets in Asia appear to be in a much more upbeat mood which seems to reflect the news that broke yesterday suggesting that US Treasury Secretary Mnuchin had reached out to China to propose a new round of trade talks. Economic Advisor to the White House Larry Kudlow has since confirmed this overnight. The Nikkei (+0.84%) and Hang Seng (+1.40%) are leading gains on the back of that while the Shanghai Comp (+0.14%) and Kospi (+0.18%), although off their highs, are also up. Futures are more or less flat in the US while bonds are more mixed but the overall scope of moves is fairly modest. Looking back to yesterday, equities spent much of day grappling between a tumbling tech sector, another sharp leg higher for oil prices and that story suggesting that the US will propose a new round of trade talks with China. After diving between gains and losses, by the close of play last night the S&P 500 finished +0.04% with energy stocks up +0.51% while the NASDAQ fell -0.23% and wiped out around half of Tuesday’s gain. Apple closed -1.25% (with the stock trading mostly flat after the new iPhone release) and the NYFANG index ended +0.05%. Credit markets continued their recent strength, with the CDX IG index tightening 1bp to 57.5bps – its lowest level since March. CDS has outperformed cash notably of late.

The MSCI EM index traded up +0.12%, gaining for the only second session in the last eleven trading days. The EM currency index rallied +0.80% after the positive trade headlines regarding new US-China discussions. Meanwhile WTI Oil (+1.62%) turned in its second consecutive >1.5% session yesterday and Brent hit $80/bbl for the first time since May with rising concerns about supply including the impact of Hurricane Florence driving price action. Demand looks healthy too, with US data showing a drawdown in crude oil inventories of 5.3 million versus expectations for a 1.6 million barrel drawdown. Bonds largely ignored the oil and trade headlines though, with Treasuries finishing 1.3bps lower and yields in Europe down a similar amount. BTPs (+0.6bps) underperformed for the second day, albeit modestly, following a later-denied Ansa news story about the 5SM Party asking for €10bn for its citizen income proposal or otherwise Finance Minister Tria’s resignation.

Ahead of today’s US CPI, yesterday’s headline PPI data for August initially looked like a slight inflation miss but at closer inspection it was much more of a wash. Indeed the headline number came in at -0.1% mom (vs. +0.2% expected) largely due to the trade component, causing the annual reading to fall to +2.8% yoy from +3.3%. However the healthcare component was a solid +0.18% mom (implying a decent read-through to PCE) and we also saw the ex-food, energy and trade reading rising one-tenth to +2.9% yoy.

We also had speeches from two FOMC members yesterday, though neither signalled a substantive change in policy views. Fed Governor Brainard recommitted to the gradual pace of rate hikes, cited financial stability as a potential concern, and mentioned emerging markets, the yield curve, and the stilllow level of r-star as potential problems moving forward. St. Louis Fed President Bullard reiterated his dovish view that rates are already near neutral, or even already restrictive, given the slope of the yield curve and the level of market-based measures of inflation expectations. Brainard is nearer the centre of the committee and her speech probably better reflects the median FOMC view, but Bullard’s comments remind us that some issues will continue to be debated on the FOMC.

The day ahead will likely be dominated by the four events we highlighted further up (ECB, BoE, CBT and US CPI) but there are other data releases to highlight including the final August CPI revisions in Germany and France, Argentina CPI for August, and the latest weekly jobless claims and August monthly budget statement in the US. Worth flagging also is the IMF conference on sovereign debt including opening remarks from Lagarde, as well as scheduled speeches from the Fed’s Quarles (at 3pm BST) and Bostic (at 6pm BST). We’ve not mentioned the BoE but DB agrees with consensus that no changes to policy are likely. Officials may mention the recent softening in economic data and could comment on ongoing Brexit negotiations, but it shouldn’t be market moving.

3. ASIAN AFFAIRS

i) THURSDAY MORNING/ WEDNESDAY NIGHT: Shanghai closed UP 30.47 POINTS OR 1.15% /Hang Sang CLOSED UP 669.45 POINTS OR 2.54%/ / The Nikkei closed UP 216.71 POINTS OR 0.96%/Australia’s all ordinaires CLOSED DOWN 0.70% /Chinese yuan (ONSHORE) closed DOWN at 6.8668 AS POBC STOPS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER/Oil DOWN to 69.44 dollars per barrel for WTI and 79.17 for Brent. Stocks in Europe OPENED GREEN //. ONSHORE YUAN CLOSED UP AT 6.8468 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8429: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS NOT DOING TOO GOOD : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

4.EUROPEAN AFFAIRS

UK

Bank of England keeps rates unchanged and this was widely expected

(courtesy zerohedge)

Bank of England Keeps Rates Unchanged In Widely Expected Decision

While far less exciting than today’s Turkish rate announcement which saw the central bank hike the 1 week repo rate by 625bps to 24%, the BOE decided to keep rates unchanged at 0.75% as expected in a unanimous 9-0 vote.

Bank of England

✔@bankofengland

MPC voted unanimously to maintain #BankRate at 0.75%

In a relatively upbeat statement, the BOE said that economic activity had been better than expected, and raised its Q3 GDP estimate to 0.5% from the August estimate of 0.4% noting the very limited degree of slack remaining in the economy, and predicting that a small margin of excess demand was projected to emerge by late 2019 and build thereafter, feeding through into higher growth in domestic costs than has been seen over recent years.

As also expected, the BOE repeated its view that any future rate hikes “are likely to be at a gradual and limited” over the next few years as inflation to its 2% target. The central bank also discussed the global economy, noting that it “still appears to be growing at above-trend rates, although recent developments are likely to have increased downside risks around global growth to some degree. ”

In emerging market economies, indicators of growth have continued to soften and financial conditions have tightened further, in some cases markedly. Recent announcements of further protectionist measures by the United States and China, if implemented, could have a somewhat more negative impact on global growth than was anticipated at the time of the August Report.

In the minutes accompanying the decision, the MPC said it saw more indications of uncertainty over Brexit withdrawal process than a month ago, especially financial markets.

The central bank also noted that ongoing tightening of monetary policy is likely appropriate if economy grows as expected, and that any rate rises are to be gradual and limited.

It noted that recent developments have increased downward risks to above trend global economic growth, especially for EMs.

The central bank highlighted recent protectionist measures by the US and China and said these could have a somewhat more negative effect on growth than expected in August, if implemented Sees Q3 growth of 0.5% QQ (prev. 0.4%)

The market is pricing in the next rate hike for May.

In response to the widely expected announcement, cable has done nothing and was virtually unchanged.

Euro Surges As Draghi Forecasts “Significantly Stronger Core Inflation”

While the ECB indeed trimmed its GDP outlook for 2018 and 2019 as previewed previously, cutting 2018 and 2019 GDP from 2.1% and 1.9% to 2.0% and 1.8%, respectively, and mirroring the recent reversal in the Citi Eurozone surprise index…

… the market ignored this and instead focused on Mario Draghi’s assessment that the expansion is “still solid” while noting that “uncertainty around the inflation outlook is receding.”

Commenting on inflation, Draghi said that while “measures of underlying inflation remain generally muted” he countered that “domestic cost pressures are strengthening, broadening” as “uncertainty around inflation outlook is receding” and expects “underlying inflation to pick up toward end of year, rise gradually in medium term.”

Subsequently, Draghi also said that the ECB projects “significantly stronger core inflation.”

The mood was boosted by Draghi’s comments on, saying that while “we have to wait and see” so far, all the major Italian ministers and the PM have said they will respect the EU’s budgetary requirements, and there has been no contagion out of Italy to Europe yet.

This, together with the latest miss in US inflation as CPI missed across the board one day after PPI posted its first contraction since January 2017 which slammed the dollar, turned out to be a “perfect storm” for EUR shorts, and forced a broad squeeze in the heavily shorted currency while dollar longs were forced to unwind positions.

As a result, the EURUSD jumped +0.5%, setting a session high of 1.1688 with the pair briefly rising above 100-DMA but stalling ahead of technical resistance at 1.1690.

Skripal Suspects Appear For First Time In Shocking Interview: We Are “Framed Tourists”

The same day the US announced it plans a second round of “very severe” sanctions on Russia over the use of a nerve agent in connection to the West’s allegations surrounding the Skripal poisoning, the alleged perpetrators of the poison attack have appeared on RT News for an exclusive interview with RT’s Editor-in-Chief Margarita Simonyan.

Suffice it to say the whole strange Skripal saga just got a lot more bizarre. The pair told Simonyan in the televised interview that they had nothing to do with it, but were very excited to visit the famous Salisbury cathedral as mere sightseers and were in the Salisbury town briefly on two consecutive days, but that they are not GRU agents or Russian spies.

“Our friends had been suggesting for a long time that we visit this wonderful town,” they said, and explained that after the short visit, their“whole lives were turned upside down” as they suddenly became “framed tourists” caught up in the Skripal cause after being falsely accused by UK authorities.

The pair sat stone-faced throughout the interview and delivered brief, concise answers to RT’s questions, while consistently claiming to have been visiting Britain as tourists, but while also acknowledging it was indeed them that appeared in CCTV footage published by the UK authorities.

“Salisbury? A wonderful town?” RT’s Margarita Simonyan asked. “Yes,” Petrov answered tersely. “It is a tourist town,” Boshirov offered. “There’s a famous cathedral there… It is famous not just in Europe, but in the whole world. It’s famous for its 123-metre spire, it’s famous for its clock, the first one [of its kind] ever created in the world, which is still working.”

Upon the start of the interview wherein the two confirm their true identities as Alexander Petrov and Ruslan Boshirov to RT’s Simonyan, the interview proceeds:

SIMONYAN: The guys we all saw in those videos from London and Salisbury, wearing those jackets and trainers, it’s you?

PETROV: Yes, it’s us.

SIMONYAN: What were you doing there?

PETROV: Our friends have been suggesting for quite a long time that we visit this wonderful city.

SIMONYAN: Salisbury? A wonderful city?

PETROV: Yes.

SIMONYAN: What makes it so wonderful?

BOSHIROV: It’s a tourist city. They have a famous cathedral there, Salisbury Cathedral. It’s famous throughout Europe and, in fact, throughout the world, I think. It’s famous for its 123-meter spire. It’s famous for its clock. It’s one of the oldest working clocks in the world.

Petrov then explains that the pair planned to visit famous tourist sites in London and in and around Salisbury, but parts of their trip were cut short because of heavy snowfall and inclement weather.

RT

✔@RT_com

Framed tourists?

FULL INTERVIEW: 5GMT on http://RT.com#Skripalhttps://on.rt.com/9e8t

The pair say they only spent three days total in England, due their decision to cut it short, but were in Salisbury for some of that time, on two consecutive days:

SIMONYAN: So, you travelled to Salisbury to see the clock?

PETROV: No, initially we planned to go to London and have some fun there. This time, it wasn’t a business trip. Our plan was to spend some time in London and then to visit Salisbury. Of course, we wanted to do it all in one day. But when we got there, our plane couldn’t land on its first approach. That’s because of all the havoc they had with transport in the UK on March 2 and 3. There was heavy snowfall, nearly all the cities were paralyzed. We were unable to go anywhere.

BOSHIROV: It was in all the news. Railroads didn’t work on March 2 and 3. Motorways were closed. Police cars and ambulances blocked off highways. There was no traffic at all – no trains, nothing. Why is it that nobody talks about any of this?

SIMONYAN: Can you give a time line? Minute-by-minute, or at least hour-by-hour, or as much as you can remember. You arrived in the UK – like you said, to have some fun and to see the cathedral, to see some clock in Salisbury. Can you tell us what you did in the UK? You spent two days there, right?

PETROV: Actually, three.

SIMONYAN: OK, three. What did you do for those three days?

PETROV: We arrived on March 2. We went to the train station to check the schedule, to see where we could go.

BOSHIROV: The initial plan was to go there for a day. Just take a look and return the same day.

PETROV: To Salisbury, that is. One day in Salisbury is enough. There’s not much you can do there.

BOSHIROV: It’s a regular city. A regular tourist city.

SIMONYAN: OK, I get that. That was your plan. But what did you actually do? You arrived. There was heavy snowfall. No trains, nothing. So, what did you do?

PETROV: No, we arrived in Salisbury on March 3. We wanted to walk around the city but since the whole city was covered with snow, we spent only 30 minutes there. We were all wet.

In comments that will likely be able to be easily proven or disproven, he followed with: “There are no pictures. The media, television – nobody talks about the fact that the transport system was paralyzed that day. It was impossible to get anywhere because of the snow. We were drenched up to our knees.”

In Salisbury, Petrov continued, the two intended “to see Stonehenge, Old Sarum, and the Cathedral of the Blessed Virgin Mary. But it didn’t work out because of the slush.” But they blame the harsh conditions for quickly canceling their plans and “transport collapse”, and they returned the train station after their initial arrival in the town via train from London.

SIMONYAN: All right. You went for a walk for 30 minutes, you got wet. What next?

PETROV: We travelled there to see Stonehenge, Old Sarum, and the Cathedral of the Blessed Virgin Mary. But it didn’t work out because of the slush. The whole city was covered with slush. We got wet, so we went back to the train station and took the first train to go back. We spent about 40 minutes in a coffee shop at the train station.

BOSHIROV: Drinking coffee. A hot drink because we were drenched.

PETROV: Maybe a little over an hour. That’s because of large intervals between trains. I think this was because of the snowfall. We went back to London and continued with our journey.

BOSHIROV: We walked around London…

SIMONYAN: So, you only spent an hour in Salisbury?

PETROV: On March 3? Yes. That’s because it was impossible to get anywhere.

SIMONYAN: What about the next day?

PETROV: On March 4, we went back there, because the snow melted in London, it was warm.