GOLD: $1196.00 DOWN $6.95 (COMEX TO COMEX CLOSINGS)

Silver: $14.11 DOWN 11 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold $1193.60

silver: $14.07

For comex gold:

SEPT/

And now Sept:

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 56 NOTICE(S) FOR 5600 OZ

Total number of notices filed so far for Sept: 607 for 60700 (1.8880 tonnes)

For silver:

Sept

146 NOTICE(S) FILED TODAY FOR

730,000 OZ/

Total number of notices filed so far this month: 5869 for 29,345,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6478/OFFER $6480: DOWN $12(morning)

Bitcoin: BID/ $6535/offer $6537: UP $51(CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1209.82

NY price at the same time:$1204.50

PREMIUM TO NY SPOT: $5.32

XX

Second gold fix early this morning: $ 1210.15

USA gold at the exact same time:$1204.80

PREMIUM TO NY SPOT: $5.35

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A SMALL 526 CONTRACTS FROM 206,803 DOWN TO 206,277 WITH YESTERDAY’S 2 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE MOVED FURTHER FROM LAST MONTH’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

12 EFP’S FOR SEPT. 738 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 750 CONTRACTS. WITH THE TRANSFER OF 750 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 750 EFP CONTRACTS TRANSLATES INTO 3.75MILLION OZ ACCOMPANYING:

1.THE 2 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND NOW 30.720 MILLION OZ STANDING SO FAR IN SEPT.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

19,621 CONTRACTS (FOR 9 TRADING DAYS TOTAL 19,621 CONTRACTS) OR 98.105 MILLION OZ: (AVERAGE PER DAY: 2180 CONTRACTS OR 10.900 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 98,105 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 14.01% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,135.93 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 526 WITH THE 2 CENT FALL IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 750 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A SMALL SIZED: 224 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 750 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A DECREASE OF 526 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 2 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.22 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND NOW IN SEPTEMBER AN INITIAL MONSTROUS 30.720 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.031 MILLION OZ TO BE EXACT or 147% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 146 NOTICE(S) FOR 730,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244.,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. AND NOW SEPT: AN INITIAL HUGE 30.720 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 4156 CONTRACTS UP TO 475,646 DESPITE THE LOSS IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A FALL IN PRICE OF $2.65). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7755 CONTRACTS:

OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 7755 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 475,646. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN VERY STRONG SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,911 CONTRACTS: 4156 OI CONTRACTS INCREASED AT THE COMEX AND 7755 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 11,911 CONTRACTS OR 1,191100 OZ = 437.04 TONNES. AND ALL OF THIS HUGE DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $2.65???

YESTERDAY, WE HAD 8969 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 75092 CONTRACTS OR 7,509,200 OZ OR 233.56 TONNES (9 TRADING DAYS AND THUS AVERAGING: 8343 EFP CONTRACTS PER TRADING DAY OR 834,300 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAYS IN TONNES: 233.56 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 233.56/2550 x 100% TONNES = 9.15% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,430.48* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 4156 DESPITE THE LOSS IN PRICING ($2.65 THAT GOLD UNDERTOOK YESTERDAY) // . WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7755 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7755 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG GAIN OF 11,911 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7755 CONTRACTS MOVE TO LONDON AND 4156 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 37.04 TONNES). ..AND ALL OF THIS HUGE DEMAND OCCURRED WITH A FALL OF $2.65 IN YESTERDAY’S TRADING AT THE COMEX??.

we had: 56 notice(s) filed upon for 5600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $6.95 TODAY: /

ANOTHER BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.65 TONNES OF GOLD FROM THE GLD.

/GLD INVENTORY 742.53 TONNES

Inventory rests tonight: 742.53 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 11 CENTS TODAY

WE HAD NO CHANGES FOR SILVER :

/INVENTORY RESTS AT 334.973 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 526 CONTRACTS from 206,803 DOWN TO 206,277 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST MONTH AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

12 EFP CONTRACTS FOR SEPTEMBER, 738 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 750 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 526 CONTRACTS TO THE 750 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 224 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 1.120 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. AND NOW A HUGE 30.720 MILLION OZ INITIALLY STAND FOR SILVER IN SEPTEMBER….

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 2 CENT PRICING FALL THAT SILVER UNDERTOOK IN PRICING YESTERDAY. BUT WE ALSO HAD A SMALL SIZED 750 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i) FRIDAY MORNING/ THURSDAY NIGHT: Shanghai closed DOWN 4.93 POINTS OR 0.18% /Hang Sang CLOSED UP 272.35 POINTS OR 1.20%/ / The Nikkei closed UP 271.92 POINTS OR 1.01%/Australia’s all ordinaires CLOSED UP 0.58% /Chinese yuan (ONSHORE) closed UP at 6.8523 AS POBC STOPS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER/Oil DOWN to 68.93 dollars per barrel for WTI and 78.22 for Brent. Stocks in Europe OPENED GREEN //. ONSHORE YUAN CLOSED UP AT 6.8523 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8475: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS NOT DOING TOO GOOD : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)Last night, we witnessed 3 major reports out of China and all signalling a slowdown in their local economy:

i. Fixed investment missed..and that is the biggest driver for the Chinese economy

2. industrial output just met estimates

3.retail sales rose by 9.0% barely beating estimates.

( zerohedge)

ii)Well that did not last long. Trump does not wait for the Chinese response as he now proceeds with $200 billion more in Chinese tariffs. Talks are still continuing…stocks tumble.

( zerohedge)

4/EUROPEAN AFFAIRS

We brought you the story about the problems at Estonia’s Danske bank. It is now getting really serious as the uSA is investigating money laundering fraud

There are two key points in this commentary:

- Deutsche ban and Citibank may be complicit in this scheme

- the fact that the uSA is involved in this investigation and the threat that Danske will not be allowed to receive treasuries and thus dollars, may throw this bank into a death spiral

very important read.

( zerohedge)

ii)UK

Mark Carney is throwing out false warnings that a “no Brexit” deal would lead to chaos and a crisis as bad as 2008

( zerohedge)

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY

I would like to be a fly on the fall when Erdogan’s has a family get together: He has just stated that his patience has limits. Down goes the Lira

( zerohedge)

ii)Russia

This is a surprise: Russia surprises the markets with its first rate hike since 2014 and that sent the rouble higher. Russia has been increasing its gold purchases.

( zerohedge)

6. GLOBAL ISSUES

i)First it was Morgan Stanley and now Soc Generale gives its latest global economic outlook and they are warning about storm clouds gathering as the next recession looms big

( Soc Generale)

ii)A super Bellwether on the global economy: shipping rates have collapsed because the total number of freight items have collapsed. The global economy is faltering

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Argentina

The Argentinian Peso closes at a record low of 39.80 peso to the dollar as the IMF withholds the next 3 billion bailout tranche. Macri made a deal with the devil (IMF) and they will pay for it

( zerohedge)

9. PHYSICAL MARKETS

i)Our good friend Andrew Maguire has a great interview today with Kingworldnews…how the PetroYuan scheme orchestrated by China will destroy the paper centric west… This is a must read..

( Kingworldnews/Andrew Maguire)

ii)An excellent commentary from GATA sec. Steer who states that metal price suppression is really aimed at all commodities trying to contain their price and keep the dollar scheme healthy. However the tariff/trade war is putting a huge dent in this scheme.

(courtesy Ed Steer/GATA))

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

MARKET TRADING

after initial weakness overnight, the dollar strengthens but also the 10 yield rises above 3.00%. The higher the rate, the more trouble for our emerging nations

(courtesy zerohedge)

a)The markets do not like this: retail sales miss badly as auto spending slides. the economy is faltering

( zerohedge)

b)Industrial production surges but almost all of the gain came from utilities as air conditioners were going full blast throughout the USA in August due to the heat wave. Interestingly enough manufacturing another key component was down

( zerohedge)

c)Soft data, U. of Michigan sentiment soars as economic optimism hits a 14 year high.

Major flooding and it will get worse: the authorities believe that the damage will be in excess of 30 billion dollars

( zerohedge)

2 Florence huge damage/ tonight/

(zerohedge)

c)Catastrophe bondholders are now panicking because their insurer’s model failed to predict Hurricane Florence and the devastating cost to repair.

( zerohedge)

iv)SWAMP STORIES

a) 1,Manafort agrees to a plea deal. However we do not know if he will spill any beans or he is just does not want to spend any more money as it will not make a difference

( zerohedge)

a) 2.This may not be good for Trump as part of the deal is a “cooperation agreement”. What does Manafort know with respect to Trump

( zerohedge)

b)What on earth is this world coming to?; Kavanaugh categorically and unequivocally” denies sexual misconduct claim and the White House and 65 women who knew him then stated that he was always honourable when dealing with the opposite sex

( zerohedge)

Let us head over to the comex:

The next active delivery month after August for silver is September and here the OI FELL by 34 contracts DOWN to 421.

We had 83 notices filed on yesterday so we gained 49 contracts or 245,000 ADDITIONAL oz will stand at the comex as these guys refused a fiat bonus as well as a London based forwards. For the past 17 months starting in April 2017, we have been witnessing on a constant basis queue jumping as the commercials seek physical silver immediately after first day notice. After a little holiday this week, queue jumping resumes in earnest in the silver pits

October GAINED 17 contracts to stand at 578. November saw a gain of 3 contracts to stand at 70.

ON FIRST DAY NOTICE FOR THE SEPT/2017 SILVER CONTRACT MONTH: 20.515 MILLION OZ STOOD FOR DELIVERY AND BY MONTH’S END: A HUGE 32.875 MILLION OZ WAS THE FINAL STANDING AS WE WERE WELL INTO THE PHENOMENON OF QUEUE JUMPING IN SILVER. THUS WE ARE WAY AHEAD OF LAST YEAR AS ALREADY WE HAVE 30.720 MILLION OZ OF SILVER INITIALLY STAND. WE WILL NO DOUBT PASS LAST YEAR’S TOTAL OF 32.875 MILLION OZ ONCE SEPTEMBER ENDS AS THE BANKS SCRAMBLE FOR PHYSICAL SILVER.

our large speculators

those large specs who have been long in gold pitched (transferred) 1395 contracts from their long side

those large specs who have been short in gold covered (transferred) 73092 contracts from their short side

our commercials

those commercials who have been long in gold added 460 contract to their long side

those commercials who have been short in gold added 6972 contracts from their short side

our small speculators

those small specs that have been long in gold pitched (transferred) 1303 contracts from their long side’

those small specs who have been short in gold pitched (transferred) 1908 contracts from their short side

and now the silver COT

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 81,095 | 108,498 | 18,339 | 78,140 | 65,766 | |

| -1,966 | -3,537 | 1,350 | -3,281 | -1,042 | |

| Traders | |||||

| 108 | 74 | 46 | 42 | 31 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 208,969 | Long | Short | |

| 31,395 | 16,366 | 177,574 | 192,603 | ||

| 475 | -193 | -3,422 | -3,897 | -3,229 | |

| non reportable positions | Positions as of: | 173 | 131 | ||

| Tuesday, September 11, 2018 | |||||

our large speculators

those large specs that have been long in silver pitched (transferred) 1966 contracts from their long side

those large specs that have been short in silver pitched (transferred) 3537 contracts from their short side

our commercials

those commercials who have been long in silver pitched (transferred) 3281 contracts from their long side

those commercials who have been short in silver pitched (covered) 1042 contracts from their short side

our small speculators

those small specs who have been long in silver added 475 contracts to their long side

those small specs who have been short in silver added 193 contracts to their short side

conclusions; do not waste your precious time reading this garbage.

end

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

This Week’s Golden Nuggets – BOE Warns Of UK House Price Crash

News, Market Updates, Charts and Videos You May Have Missed

Here is our Friday digest of the important news, market updates, charts and videos we were informed by this week.

We felt it important to do a video update which considers the risks that Brexit poses to the London property market. This is a very real risk that has not been assessed in the British and Irish media.

Our timing was good and the Bank of England must have been listening to us! Yesterday, Bank of England governor Mark Carney confirmed that there are real risks to UK property investors and the UK economy, when he warned that a “no- deal Brexit” would likely result in economic chaos and a UK house price correction or crash of some 35%.

In a stark warning to the British government, Mark Carney told ministers that the impact of a no-deal Brexit could be as “catastrophic” as the 2008 financial crisis.

Needless to say this would result in a very serious recession indeed in the UK and would have consequences for the Irish economy, EU economies and other over-valued property markets – one of which is in Dublin, Ireland.

Enjoy and have a nice weekend!

Video This Week

Market Updates and News This Week

Video: BREXIT To Contribute To London Property Bubble Bursting

Australia’s Banking System May Be The “Bloody Big Butterfly” Which Triggers Next “Financial Storm”

Biggest Driver of 2008 Financial Crisis Has Only Got Worse – Ten Years Since Lehman

London Property: Here Comes the Crash

Protestors hold signs behind Richard Fuld, Chairman and Chief Executive of Lehman Brothers Holdings after its collapse led to the last global financial crisis. REUTERS/Jonathan Ernst/File Photo

Protestors hold signs behind Richard Fuld, Chairman and Chief Executive of Lehman Brothers Holdings after its collapse led to the last global financial crisis. REUTERS/Jonathan Ernst/File Photo

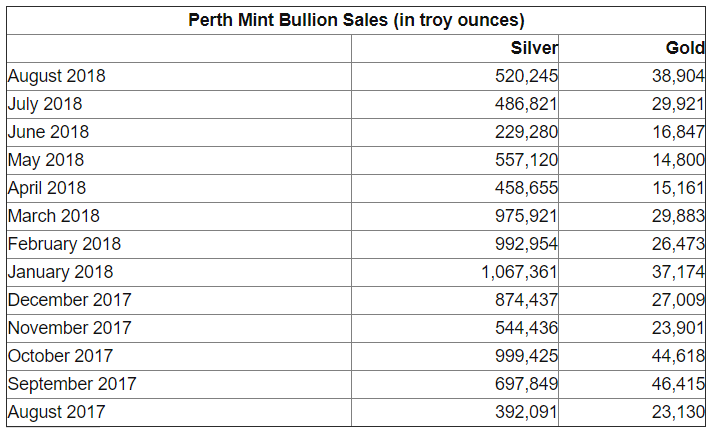

Perth Mint Gold Bullion Sales Rally in August to Ten-Month High

China to Continue Driving Global Silver Market Forward

Putin Says Russia and China Will Reduce Use of Dollar in Trade

New Zealand Is The Doomsday Escape Plan For Super Rich of Silicon Valley

Charts This Week

London median, Islington, Wandsworth & Southwark prices. Must See Interactive Graphic Piece From Bloomberg News

Source: Australian Financial Review

Source: @CharlieBillelo

Source: SilverInstitute.org

~

~

Source: CoinNews.net

Source: Bloomberg

News and Commentary

Perth Mint Gold Bullion Sales Rally in August to Ten-Month High (CoinNews.net)

Gold prices settle lower in pullback from 2-week high (MarketWatch.com)

Gold gains as dollar dips on soft US data (CNBC.com)

Head of Russian bank warns customers they may not get dollars back (Bloomberg.com)

Gundlach: US Economy And Stocks Could Be “Burnt Out” (AdvisorPerspectives.com)

Ten years on: was it right to bail out the banks? (MoneyWeek.com)

Here’s what J.P. Morgan says could cause the next financial crisis (MarketWatch.com)

Precious Metals Price Suppression Aimed At Commodities (DaveJanda.com)

Paper Gold Market Is Screaming “Short Squeeze” (DollarCollapse.com)

This Is About To Trigger A Major Short Squeeze In The Gold & Silver Markets (KingWorldNews.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

13 Sep: USD 1,206.65, GBP 924.41 & EUR 1,038.68 per ounce

12 Sep: USD 1,197.80, GBP 919.07 & EUR 1,033.10 per ounce

11 Sep: USD 1,194.00, GBP 915.92 & EUR 1,028.75 per ounce

10 Sep: USD 1,195.80, GBP 923.28 & EUR 1,032.45 per ounce

07 Sep: USD 1,200.75, GBP 928.30 & EUR 1,031.32 per ounce

06 Sep: USD 1,204.30, GBP 931.65 & EUR 1,035.82 per ounce

Silver Prices (LBMA)

13 Sep: USD 14.23, GBP 10.90 & EUR 12.24 per ounce

12 Sep: USD 14.16, GBP 10.90 & EUR 12.22 per ounce

11 Sep: USD 14.13, GBP 10.85 & EUR 12.19 per ounce

10 Sep: USD 14.22, GBP 10.99 & EUR 12.28 per ounce

07 Sep: USD 14.19, GBP 10.90 & EUR 12.20 per ounce

06 Sep: USD 14.27, GBP 11.03 & EUR 12.27 per ounce

Recent Market Updates

– Video: BREXIT To Contribute To London Property Bubble Bursting

– Australia’s Banking System May Be The “Bloody Big Butterfly” Which Triggers Next “Financial Storm”

– Ten Years Since Lehman: Biggest Driver of 2008 Financial Crisis Has Only Got Worse

– London Property: Here Comes the Crash

– This Week’s Golden Nuggets

– Gold Remains An “Excellent Way to Hedge” for Longer Term – BNP Interview

– Video: Gold Surges To Record Highs In Emerging Market Currencies – New Highs In USD, EUR, GBP In the Coming Months?

– September Is The Best Month For Gold and Worst Month For Stocks

– Pound Investors Face Months of Volatility Into Brexit Endgame

– This Week’s Golden Nuggets

– Video: “Financial War” Deepens as Russia Buys Gold and Dollar Hegemony At Risk – Rickards on CNN

– Will Indebted Nations Globally Follow Venezuela Into Hyperinflation?

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

An excellent commentary from GATA sec. Steer who states that metal price suppression is really aimed at all commodities trying to contain their price and keep the dollar scheme healthy. However the tariff/trade war is putting a huge dent in this scheme.

(courtesy Ed Steer/GATA))

Metals price suppression aims at all commodities,

GATA’s Ed Steer says

Submitted by cpowell on Thu, 2018-09-13 14:36. Section: Daily Dispatches

10:41a ET Thursday, September 13, 2018

Dear Friend of GATA and Gold:

GATA Board of Directors member Ed Steer, publisher of Ed Steer’s daily Gold and Silver Digest letter, was interviewed this week by talk show host Dave Janda of WAAM-AM1600 in Ann Arbor, Michigan, and explained how the monetary metals price suppression scheme of governments and central banks is part of their longstanding policy to suppress all commodity prices and protect government currencies, particularly the U.S. dollar. This policy, Steer notes, is imperialistic exploitation of developing, commodity-producing countries.

But, Steer adds, the U.S. government’s increasing weaponization of the dollar in foreign policy is starting to alienate the world and bust the scheme apart.

The interview is 25 minutes long and can be heard here:

https://davejanda.com/audio/EdSteer090918.mp3

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

-END-

for your interest….is Barrick an agent of China?

(courtesy Chris Powell/GATA

(GATA) Is Barrick still central banking’s agent in the gold market?

Submitted by cpowell on 03:08PM ET Friday, September 14, 2018. Section: Daily Dispatches

11:24a ET Friday, September 14, 2018

Dear Friend of GATA and Gold:

The report from today’s South China Morning Post that is appended is interesting for a couple of reasons.

First, it shows that a big gold-mining company owned by the Chinese government continues to invest heavily in new mines — now with another three quarters of a billion dollars — “confident that an upward trend in gold prices will emerge within the next 12 months.”

Second, it highlights another connection between the Chinese government and Barrick Gold, their joint ownership of the second-largest gold mine in South America, the Veladero mine in Argentina.

A particularly intriguing connection between the Chinese government and Barrick was brought to your attention by GATA the other day via a report in the Financial Times. The newspaper noted that the Chinese government has appointed a committee to advise it on relations with the United States and financial and economic reforms and the committee will be co-chaired by the chairman of Barrick Gold, John Thornton, a former Goldman Sachs executive. The committee’s members, which include leading Wall Street bankers, have been invited to Beijing in two days:

http://www.gata.org/node/18485

In federal court in New Orleans in 2003 Barrick admitted that, with its borrowing and leasing of central bank gold, it had become the agent of central banks in regulating the price of the monetary metal:

Soon after that admission, which came during a lawsuit charging the company with rigging the gold market, Barrick announced that it would discontinue leasing gold. But the mining company’s growing closeness with the Chinese government implies that China not only considers gold crucial to the world financial system but also wants gold mining intermediaries in the West.

Is Barrick still helping central banks manage the gold market?

There might be some interesting financial journalism to undertake here upon Thornton’s return from Beijing. Can gold investors continue to count on gold market reporters and analysts to refrain from asking gold mining executives the most important questions?

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Our good friend Andrew Maguire has a great interview today with Kingworldnews…how the PetroYuan scheme orchestrated by China will destroy the paper centric west… This is a must read..

(courtesy Kingworldnews/Andrew Maguire)

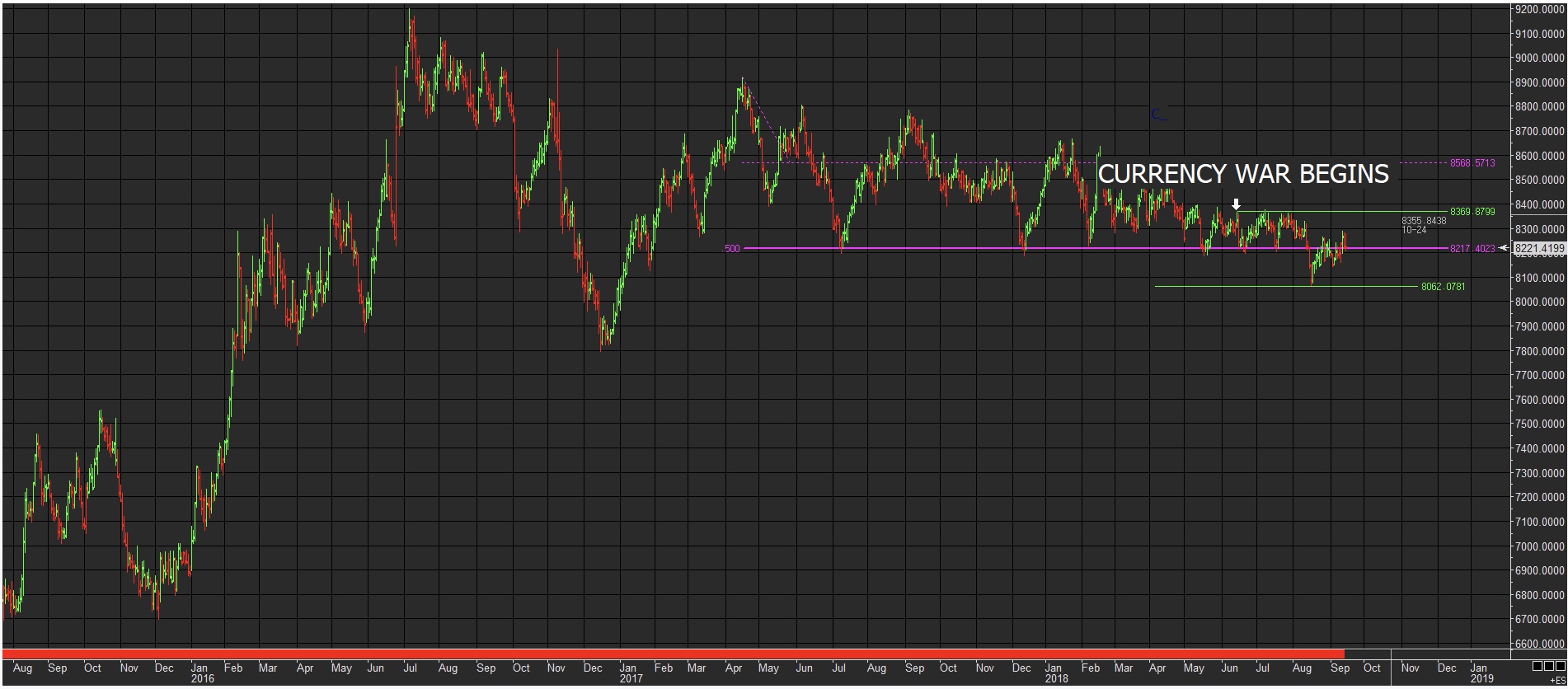

Andrew Maguire – Forget Trade War, China Is Positioning

To Crush The US In The Currency War And Russia Is A

Golden Ally

Today London whistleblower and metals trader Andrew Maguire told KWN to forget the trade war because China is positioning to crush the US in the currency war and Russia is a golden ally.

China Positioning To Win The Currency War

September 14 (King World News) – Andrew Maguire:“This week we evidenced another escalation in the US/China trade war, which in mid-June had already morphed into a dangerous currency war. However, this week the tables began to turn. But to assess what is changing we have to look at the general market which dutifully accepts at face value what the mainstream media tells them.

It is a fact that China has a massive bilateral trade surplus, so it cannot go head-to-head with the US in a trade war. However, a currency war is a completely different animal

“China is playing the long game and has already put all the components in place to internationalize the yuan and to displace US dollar hegemony with a gold-backed currency. It takes two to tango in a currency war and China is strategically playing the US into its own hands and using gold to do it.

China Counterattacking US By Vacuuming Gold Out Of London

As far as the trade war is concerned, a tit-for-tat devaluation of the Yuan has 1/1 offset the imposed US tariffs, which by design has brought down the commodity sector. However, during this devaluation process, the most important takeaway is that China has maintained the CNY/Gold peg within a very tight range to commodity exporting countries.How is China doing this? The answer is two-fold. The 95% correlated algo driven synthetic marketplace has seen gold and silver prices in dollar terms collapse. But into this US dollar price discount, China has been sucking 400oz. bars from London by swapping US dollars for cheap bullion.

And maintaining the CNY/Gold peg in a very tight range has enabled China to provide price stability to those countries it is buying/exchanging oil in yuan to bypass the US dollar. Short-term currency war pain aside, the 80/20 rule applies. China is focused on providing yuan to the major oil producing countries such as Russia and Iran through the Shanghai Oil Futures Exchange, commonly known as the Petro Yuan contract. Oil producers can lock in a stable yuan/oil price that is instantly convertible to gold.This has been carefully maintained by China.

Pull up a Yuan/gold chart and you will evidence a very tight CNY/gold trading range, with multiple PBOC interventions supporting CNY gold prices at 8214 — with a very tight managed band since the trade war entered a currency war stage in mid-June (see chart below).

China Positioning To Win The Currency War

Though this entire trade war is evolving into an escalating currency war, we have seen US dollar gold prices crash 11.2% (at the recent lows), while CNY/gold during this same period has been managed in a tight 2.0% range.

China Aggressively Attacking US Hegemony

Long before the US/China trade war escalated into a full-blown currency war, the dollar was already under threat as China had already reopened the gold window. The Shanghai Gold Exchange (SGE) is the conduit to exchange gold in yuan, and the SGE supply of physical gold is gold that is continuing to be dishoarded from the West (the UK US, BIS). China pays in yuan, which in turn increases supply of yuan, and converts it to gold sourced out of the West. This is a clear enveloping horn attack on US hegemony and is moving the West toward its own demise.

END

___________________________________________________________________________________________________________________________________________________________________________________

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8523/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER //OFFSHORE YUAN: 6.8475 /shanghai bourse CLOSED DOWN 4.93 POINTS OR 0.18% /HANG SANG CLOSED UP 271.92 POINTS OR 1.01%

2. Nikkei closed UP 273.35 POINTS OR 1.20%/USA: YEN FALLS TO 111.88/

3. Europe stocks OPENED IN THE GREEN

/USA dollar index FALLS TO 94.47/Euro RISES TO 1.1697

3b Japan 10 year bond yield: RISES. +.12/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.88/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 68.93 and Brent: 78.22

3f Gold UP/JAPANESE Yen UP/ CHINESE YUAN: ON SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.450%/Italian 10 yr bond yield UP to 2.97% /SPAIN 10 YR BOND YIELD UP TO 1.48%

3j Greek 10 year bond yield RISES TO : 4.09

3k Gold at $1204.50 silver at:14.18 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 58 /100 in roubles/dollar) 67.72

3m oil into the 68 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.97DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9645 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1278 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.45%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.99% early this morning. Thirty year rate at 3.12%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.1195

Dollar Suffers Biggest Weekly Drop Since February,

Pushing Global Markets Higher

The dollar headed for its worst weekly loss since February following slowing inflation data out of the US and amid bets that other major central banks will start to normalize monetary policies, helping global stocks extend their lead as the MSCI All-Country World Index gained 0.3%.

The bout of dollar weakness helped the MSCI Asia Pacific index extend its rebound from the worst run of losses in 16 years, while stocks in Europe gained along with S&P500 futures as renewed prospects for U.S.-China trade talks and a desperate rate hike action by Turkey (which again prompted Erdogan’s angry rebuke) to support its currency, fostered a positive mood.

In Europe, the Stoxx 600 Index increased 0.2% to the highest in more than a week; Germany’s DAX Index jumped 0.4% also to a one week high, and leading the way in European equities, driven by Infineon, which benefited from broad-based IT sector strength after yesterday’s outperformance in the US. The SMI was the laggard and weighed on by Roche’s announcement of a “moderate” sales growth in 2019.

Asia’s cheer was limited however, as China shares again underperformed after overnight’s Chinese economic data dump showed that fixed-asset investment fell dropped to 5.3%, missing expectations and hitting a new record low, even as retail sales surprised modestly to the upside.

The yuan stayed lower as the PBOC added net 150 billion of repo liquidity; the Shanghai Composite closed down 0.2%, and just off the lowest print since the bursting of the 2014/2015 stock bubble.

Offsetting China’s weakness, markets in Japan, South Korea and Hong Kong climbed as Asian equities ended the week on a high after enduring the longest daily losing streak since 2002.

Emerging-market stocks and currencies extended a rally following Turkey’s larger-than-expected rate increase, the kiwi outperformed on a manufacturing uptick, the yen reversed early weakness after Abe’s policy exit comment, saying QE can’t last forever; India’s rupee gained from recent record low prints while India’s 10-year yield falls five basis points to 8.08% on slower inflation.

In G-10 FX, the euro rose to its strongest level versus the dollar in more than two weeks amid improving risk appetite and dollar weakness after soft U.S. inflation data on Thursday, and after the ECB said it expects to phase out new bond purchases by the end of the year. The Bloomberg Dollar Spot Index headed for its worst weekly performance since mid-February as the U.S. curve flattened and euro-area stocks rose.

“The rally in the euro post the ECB meeting and the easing of trade tensions are weakening the dollar,” said David Forrester, FX strategist at Credit Agricole CIB in Hong Kong. “The soft U.S. CPI overnight is also holding the dollar back”

Elsewhere, the krona led losses among G-10 peers as Swedish inflation missed estimates, while emerging-market currencies extended their recent advance. The British pound headed for a six-week high and gilts fell after Bank of England Governor Mark Carney told lawmakers that a no-deal Brexit would see interest rates rise rather than fall.

10-year Treasuries dropped, with the yield rising above 2.98%.

One day after central bank “Super Thursday”, the Russian Central Bank also surprised markets when it hiked its key rate Sep 7.50% vs. Exp. 7.25% (Prev. 7.25%). The bank said they will consider the necessity of further rate hikes taking into account inflation and economic dynamics against the forecast. They added the increase of key rates will help maintain real interest rates on deposits in the positive territory, which will support the attractiveness of savings and the balanced growth in consumption.

Investors will be happy to close the busy week on a positive note, following numerous, often conflicting reports, including cooling U.S. inflation to central-bank meetings in Europe, the U.K. and Turkey. And while the Russian central bank unexpectedly hiked rates moments ago to 7.50% with most expecting an unchanged 7.25% print, all eyes will be on American retail sales.

Speaking to Bloomberg, Robert Shiller said that while U.S. equities are now “highly priced,” they could still go “a lot higher,” and adding that “the U.S. is just doing great right now in terms of the strength of the economy and the stock market,” with Trump’s tax cuts and deregulation moves helping stoke sentiment. Of course, sooner or later the hangover from the sugar high will come…

In geopolitical news, North Korea said US sanctions over cyber-attack is a smear campaign against North Korea and that the US is misleading as if North Korea were behind the Sony hack, while it warned that sanctions could impact implementation of US agreement.

Elsewhere:

- Italian Deputy Finance Minister Castelli states that the nation’s citizen’s income will commence on Jan 1st 2019 and will be a minimum of EUR 7880mln.

- Mexico NAFTA negotiator Smith Ramos said it is ideal to keep NAFTA trilateral, but they remain prepared to proceed with a bilateral deal with US.

- Former Trump campaign manager Manafort was reported to have agreed a plea deal with Special Counsel Mueller although reports noted it was unclear if he is agreeing to cooperate with prosecutors or is conceding to a guilty plea, while sources later stated that a Manafort plea deal with Special Counsel Mueller is close but not there yet.

- Turkish President Erdogan said they have faced a “heinous” attack against Turkey after US statements, the rise in TRY above 7 was an economic assassination attempt. He added that in 15 years the inflation target of the central bank was

never correct and that we will see the results of central bank independence after the rate hike

The oil market is languishing around yesterday’s lows after the previous sessions losses of over 2%. Brent and WTI are both set for gains of over 1.5% this week, as weather reports remain in focus, with Hurricane Florence set to make landfall in North Carolina today. In the metals scope, gold is currently benefitting from a softer USD and is currently up 0.5% on the day. LME copper has remained stable around two week highs as traders remain wary of trade talks, after US President Trump said the US “are under no pressure to make a deal with China, they are under pressure to make a deal with us” in Thursday’s session.

Market Snapshot

- S&P 500 futures up 0.2% to 2,909.75

- STOXX Europe 600 up 0.2% to 377.10

- German 10Y yield rose 0.7 bps to 0.43%

- Euro up 0.2% to $1.1709

- Brent Futures up 0.3% to $78.39/bbl

- Italian 10Y yield unchanged at 2.589%

- Spanish 10Y yield rose 0.7 bps to 1.476%

- MXAP up 1.2% to 162.17

- MXAPJ up 1.2% to 520.16

- Nikkei up 1.2% to 23,094.67

- Topix up 1.1% to 1,728.61

- Hang Seng Index up 1% to 27,286.41

- Shanghai Composite down 0.2% to 2,681.64

- Sensex up 0.8% to 38,015.35

- Australia S&P/ASX 200 up 0.6% to 6,165.33

- Kospi up 1.4% to 2,318.25

- Gold spot up 0.4% to $1,206.63

- U.S. Dollar Index down 0.1% to 94.46

Top Overnight News

- Hurricane Florence is swirling closer to the U.S. East Coast, battering the Carolinas with water and wind and threatening to unleash widespread destruction. The North Carolina coast was subject to life-threatening storm surge and heavy rain at around 4 a.m. local time

- BOE Governor Mark Carney gave a stark warning of the dangers of a no-deal Brexit that could see mortgage rates raised even as economic output and house prices tumble. At a meeting with the U.K. Cabinet, he said crashing out without an agreement could lead to a fall in the pound and higher tariffs, pushing inflation higher, people familiar with the matter said

- Italian Finance Minister Giovanni Tria’s political future is shaky; he’s being squeezed between investor demands to uphold EU rules and the extravagant spending plans of his fractious coalition, as budget time approaches.

- Turkish President Recep Tayyip Erdogan resumed his criticism of the nation’s central bank a day after it announced the biggest rate hike of his rule. “It’s currently my phase of patience, but there is a limit to this patience,” Erdogan said on Friday

- China’se conomic momentum weakened in August, with a slowdown in investment overshadowing solid retail sales and industrial production data

- Turkish companies and households bought up to $2b of foreign currency following Thursday’s central bank decision, according to Istanbul-based currency traders who declined to be named

- From a Swiss perspective it would certainly be ideal if other jurisdictions would normalize monetary policy, Swiss National Bank President Thomas Jordan said

- U.S. President Donald Trump swaggered ahead of a possible new round of tariffs talks with China, boasting he has the upper hand in the burgeoning trade war and feels “no pressure” to resolve the feud

- A date has not yet been set for the next round of U.S.-Japan trade talks, but Japan is aiming for late September, Economic Revitalization Minster Toshimitsu Motegi said

- Bank of Japan’s newly introduced forward guidance was drafted with overseas investors in mind, reflecting an effort to avoid any sharp reaction in the yen and stocks, according to people familiar with discussions at the central bank

Asian equity markets traded mostly higher as the region took impetus from the US where the S&P 500 notched a 4th consecutive gain and the Nasdaq outperformed as tech rebounded with a vengeance. ASX 200 (+0.6%) and Nikkei 225 (+0.9%) were higher in which miners led the broad gains in Australia, while Japanese exporters benefitted from a weaker currency which lifted the benchmark index to above the 23,000 level. Elsewhere, Hang Seng (+0.8%) and Shanghai Comp. (-0.1%) were both initially positive after continued liquidity efforts by the PBoC, although sentiment in the mainland eventually waned as amid weakness in Shenzhen and as participants digested mixed data in which Industrial Production printed in-line with expectations and Retail Sales beat, while Fixed Assets Investments growth declined to a fresh multi-year low. In addition, recent Trump comments also spurred some apprehension after he commented the US are under no pressure to make a deal with China and that it is China which is pressured to reach an agreement. Finally, 10yr JGBs are uneventful with demand for safe-havens dampened by the positive risk appetite in Japan, but with downside also capped amid the BoJ’s presence in the market for JPY 700bln of maturities in the short-end to belly.

Top Asian News

- Philippine Finance Chief Spurns Calls for Early Rate Hike

- China’s Choices Narrowed by Debt as Trump Threatens Economy

- Hong Kong Highly Likely to Issue Typhoon Signal 8 Sunday

- He Was at Trump Tower. He Says He’s No Spy. Now He’s Suing

- Glencore Returns to Japan Coal Talks Scuppered by High Prices

European equities have started the day on the front foot. The DAX is leading the way in the equities space, driven by Infineon, who are benefitting from broad-based IT sector strength after yesterday’s outperformance in the US. The SMI is currently the laggard and weighed on by Roche’s announcement of a “moderate” sales growth in 2019. UK homebuilders are struggling after comments from BoE’s Carney stating that UK home prices could fall by over 35% if there is a “no-deal” Brexit. Investec announced the demerger of their asset management business, and are currently leading the gains in the Stoxx 600.

Top European News

- Hong Kong Tycoon Li Is Said to Weigh U.K. Infrastructure IPO

- Investec Spins Off Asset-Management Unit as Founders Depart

- Buy Amer as Market Overly Pessimistic on M&A: Everbright SHK

- Miners Rebound From Bear Market Levels on Trade-Talks Optimism

In currencies, it was another downturn in the index and for the Greenback overall, partly on a further reflection post-benign US CPI, but also or perhaps mainly due to relative strength in rival currencies. The DXY remains below 94.500 and not far from recent lows, with more data on the horizon via retail sales, ip and business inventories before preliminary Michigan sentiment for September. G10 – All majors are ahead vs the Usd, bar the Loonie that continues to trade around the 1.3000 handle awaiting more NAFTA news. The Kiwi has overtaken its Aussie peer with some independent impetus overnight from firmer NZ manufacturing PMI growth to extend gains towards 0.6600, while Aud/Usd continues to look heavy above 0.7200. Elsewhere, Cable and Eur/Usd appear more comfortable on 1.3100 and 1.1700 handles respectively, amidst largely positive Brexit vibes at the UK-EU level if not on the domestic front, with the former eyeing 1.3150 and latter filling a chunk of bids/stops at 1.1715 before fading ahead of the 1.1734 August peak and strong chart resistance at 1.1750. Usd/Jpy continues to trade against the broad trend, but has retreated from 112.00+ highs to sub-111.88 Fib levels again, as 112.15 technical resistance held firm. EM – Try back in focus with another attempt to probe post-CBRT peaks around 6.0000 vs the Usd thwarted by more rhetoric from Turkish President Erdogan aimed at the US again, but also reiterating his stern opposition to higher rates. The Lira duly weakened in response, as has become an all too familiar pattern, but is off worst levels with some tangible support from data showing a narrower than forecast current account deficit. Elsewhere, the Rub is hedging bets around 68.4700 vs the Usd ahead of the CBR policy decision that is widely expected to be a ‘hawkish hold’.

In commodities, the oil market is languishing around yesterday’s lows after the previous sessions losses of over 2%,. Brent and WTI are both set for gains of over 1.5% this week, as weather reports remain in focus, with Hurricane Florence set to make landfall in North Carolina today. In the metals scope, gold is currently benefitting from a softer USD and is currently up 0.5% on the day. LME copper has remained stable around two week highs as traders remain wary of trade talks, after US President Trump said the US “are under no pressure to make a deal with China, they are under pressure to make a deal with us” in Thursday’s session.

Looking at the day ahead, the main highlight is probably the August retail sales report which is expected to show a +0.5% mom ex auto and gas print and +0.4% control group reading. Also due is the August import price index reading, August industrial production, July business inventories and finally a first look at the September University of Michigan consumer sentiment print. Away from that, the BoE’s Carney is due to speak again today, this time in Dublin at 11am BST while the ECB’s Nowotny also speaks this morning on a panel in Vienna. In the afternoon the Fed’s Evans (2pm BST) and Rosengren (3pm BST) are scheduled to make remarks.

US Event Calendar

- 8:30am: Retail Sales Advance MoM, est. 0.4%, prior 0.5%; Retail Sales Ex Auto MoM, est. 0.5%, prior 0.6%

- 8:30am: Import Price Index MoM, est. -0.2%, prior 0.0%; Export Price Index MoM, est. 0.0%, prior -0.5%

- 9:15am: Industrial Production MoM, est. 0.3%, prior 0.1%; Capacity Utilization, est. 78.2%, prior 78.1%

- 10am: Business Inventories, est. 0.55%, prior 0.1%

- 10am: U. of Mich. Sentiment, est. 96.6, prior 96.2; Current Conditions, prior 110.3; Expectations, prior 87.1

DB’s Jim Reid concludes the overnight wrap

Ten years ago tomorrow will be the anniversary of the Lehman default and I think that the biggest proof that we’re still in the long shadow of the GFC is the fact that around 25% of the global economy still operates under negative policy rates.

So it was apt in this anniversary week that yesterday saw an ECB that continued to flag that rates will be on hold in negative territory through next summer at least. Their policy meeting was pretty much as expected. Further details below but in reading Mark Wall’s review last night ( link ) what struck me from his analysis is that the recent revival in wage inflation in Europe is looking sustained. Although good news, if this continues life gets a bit more complicated for the ECB if an internal crisis hits (e.g. Italy) because they may not have the cover of ultralow inflation to intervene as aggressively as they have done in the past. Anyway, a story for another day, especially as US CPI disappointed yesterday.

Before that the biggest story of an eventful day was the larger than expected rate hike out of Turkey which saw the Lira trade in an 8.52% intraday range (closed +4.32%) which was pretty impressive as the range throughout the whole of September prior to yesterday was ‘only’ 6.69%. The 625bp hike in the one week repo rate to 24% completely smashed the consensus expectation for 21% and in fact was also higher than forecasts predicted by 21 of the 22 surveyed in Bloomberg. The overnight and late liquidity window lending rate were also hiked by 625bps to 25.5% and 27% respectively which meant the Bank kept the symmetric corridor framework while the CBT also announced the Bank’s decision to start funding banks again from the one-week repo rate, as opposed to overnight lending facilities, which therefore means the effective rate will reach 24%. For our Turkey Chief Economist, Kubilay Ozturk, yesterday’s move was in his view a strong signal about the authorities’ determination to address the ongoing currency and confidence crisis before it turns into something costlier. The path for macro stabilization has kicked off but with plenty of potential headwinds still ahead and an economy that is deteriorating sharply due to these actions.

However, for yesterday this was seen as overwhelmingly positive, especially after President Erdogan’s comments earlier in the session caused the Lira to depreciate as much as -3.20%. Erdogan instituted a decree that will force most Turkish entities to stop using foreign currencies to lend or borrow. The measure could de-incentivize dollarization over the medium term, but since it was paired with market unfriendly-comments, e.g. repetition of Erdogan’s assertion that higher interest rates cause inflation, the market took it negatively. After its steep depreciation, the Lira then rallied after the rate hikes to close 7.55% off the intraday lows.

The second big surprise of the day came with the August CPI report in the US where, at an unrounded +0.0818% mom, the core reading came in with decent daylight under the +0.20% consensus. As a result, the annual rate dipped two-tenths to +2.2% yoy and back to levels last seen in May. The details revealed that a big drop in apparel inflation – the largest since the 1940s – was a big contributor to the soft print while medical services inflation also fell by the second most since 1975. As a result, the 3-month and 6-month annualised readings are now down to +1.96% and +1.88% respectively. Our economist believe one-offs can explain some of the softness but not all of it. One to watch going forward.

Markets generally liked the news flow yesterday with the S&P 500 closing +0.53% while the NASDAQ and DOW climbed +0.75% and +0.57% respectively. Apple (+2.42%) rose after its refreshed product launch and I’m still undecided as to whether I’m going to join the online queue at 8.01am this morning!! Elsewhere the VIX (-0.77pts) closed back under 13 for the first time since last month. The Dollar index closed down a reasonably modest -0.30% while 10y Treasury yields finished 0.9bps higher at 2.972% after trading as low as 2.943% post-CPI. In Europe equity markets underperformed (Stoxx600 -0.15%) and Italy lagged (-0.56%) while bonds finished broadly flat to a couple basis points higher. EM FX did rally to the tune of +0.60% helped by that move in TRY (+4.32%).

This morning in Asia markets are for the most part feeding off that positive tone on Wall Street last night. The Nikkei (+0.95%), Hang Seng (+0.81%), Kospi (+1.23%) and ASX (+0.64%) are all firmer although bourses in China are more flat to slightly down. That follows the latest August activity indicators in China which were slightly mixed. Retail sales printed at a slightly better than expected +9.0% yoy (vs. +8.8% expected), industrial production was in line at +6.1% yoy although fixed asset investment did miss (+5.3% yoy vs. +5.6% expected).

Staying with China, Reuters has reported that China will not “surrender” to the US demands on trade talks according to a state paper released today. This follows President Trump’s tweet yesterday (more on that shortly) so it appears that China are digging their heels in somewhat.

Back to the ECB. It wasn’t really a huge game changer especially in light of the surprises above. We got confirmation that QE will be phased out in the final quarter of this year albeit still “subject to incoming data”. So keeping some optionality. Rates guidance was also left unchanged while the main takeaway from Draghi was the acknowledgment of risks from emerging markets, financial market volatility and the trade war. Italy was addressed but only insofar as “waiting for the facts” while, as expected, the council made modest downward revisions to growth and core inflation – although interestingly there was mention of wages picking up (see Mark Wall’s piece). Even the emerging market risk was caveated with the mention that the spillover hasn’t been substantial. Nothing particularly ground-breaking then.

The award for the least exciting event of the day yesterday meanwhile went to the BoE. As expected there was no change in policy following a unanimous 9-0 vote to keep rates on hold. The Bank was more hawkish on growth for this year (Q3 to +0.5% qoq from +0.4%) while comments around consumer spending were upbeat. However this was balanced by obvious signs of caution on the committee related to Brexit and also mentions of a deteriorating global environment. So fairly unexciting. Sterling finished +0.49% but was unchanged through much of the BoE with the rally coming post the US CPI report.

Staying with the UK, yesterday we got confirmation that the UK had pledged to provide the relevant info needed to solve the Irish border impasse. EU negotiators had asked for data on the volume of goods that flow from Northern Island to the UK, and they will apparently seek a solution to the issue that does not result in a hard border within the UK. Not groundbreaking news, but a potential signal that the two sides are making progress toward a November deal.

In terms of other news to highlight, the US is working on new Russia sanctions as a response to the nerve-agent attack in the UK earlier this year. The ruble, despite some support from higher oil prices, has depreciated 15.55% this year, the fifth worst performance among major emerging market currencies, partially due to geopolitical pressures.

Back to economic data, nothing was as significant as the CPI print. Still, last week’s US initial jobless claims were at 204,000, down marginally to a fresh 35+ year low. The US Treasury’s August budget deficit printed slightly wider than expected at -$214.1. This year’s cumulative budget deficit is now the widest since 2011, and the evolving fiscal situation will be one to watch. On the Fedspeak front, Atlanta Fed President Bostic broadly confirmed his existing views. He supports gradual rate hikes moving forward and views the risks to the outlook as balanced. Finally, in a tweet, President Trump hinted that the next round of tariffs on imports from China could come soon, saying that “we will soon be taking in Billions in Tariffs”. The S&P 500 did fall -0.17% on the tweet (though it later more than retraced the move) and the offshore Yuan depreciated 0.29% immediately following the tweet. The Yuan eventually retraced a bit to close 0.10% weaker.

As for the day ahead, well it might be comparatively less packed compared to Thursday but there’s still some potentially interesting data releases to watch. This morning in Europe we’ll get the July trade balance for the euro area while in the US this afternoon the main highlight is probably the August retail sales report which is expected to show a +0.5% mom ex auto and gas print and +0.4% control group reading. Also due is the August import price index reading, August industrial

production, July business inventories and finally a first look at the September University of Michigan consumer sentiment print. Away from that, the BoE’s Carney is due to speak again today, this time in Dublin at 11am BST while the ECB’s Nowotny also speaks this morning on a panel in Vienna. In the afternoon the Fed’s Evans (2pm BST) and Rosengren (3pm BST) are scheduled to make remarks.

3. ASIAN AFFAIRS

i) FRIDAY MORNING/ THURSDAY NIGHT: Shanghai closed DOWN 4.93 POINTS OR 0.18% /Hang Sang CLOSED UP 272.35 POINTS OR 1.20%/ / The Nikkei closed UP 271.92 POINTS OR 1.01%/Australia’s all ordinaires CLOSED UP 0.58% /Chinese yuan (ONSHORE) closed UP at 6.8523 AS POBC STOPS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER/Oil DOWN to 68.93 dollars per barrel for WTI and 78.22 for Brent. Stocks in Europe OPENED GREEN //. ONSHORE YUAN CLOSED UP AT 6.8523 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8475: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS NOT DOING TOO GOOD : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

Last night, we witnessed 3 major reports out of China and all signalling a slowdown in their local economy:

i. Fixed investment missed..and that is the biggest driver for the Chinese economy

2. industrial output just met estimates

3.retail sales rose by 9.0% barely beating estimates.

(courtesy zerohedge)

Chinese Data Dump Shows Continued Slowdown In Local Economy

One month after China’s latest data dump disappointed across the board, moments ago the National Bureau of Statistics, released the latest Retail sales, Industrial output and Fixed investment data, which was a modest improvement with 1 beat, 1 meet, and 1 miss as follows:

- China Jan.-Aug. Fixed Investment Miss; Rises 5.3% Y/Y; Est. 5.6%

- China Aug. Industrial Output Meet: Rises 6.1% Y/Y; Est. 6.1%

- China Aug. Retail Sales Beat: Rise 9.0% Y/Y; Est. 8.8%

While the rebound in retail sales was welcome (if modest) after several months of missing analyst expectations, China’s fixed investment – historically the biggest driver behind the economy – rose at the lowest pace on record.

On the positive side, property investment continues to be strong:

- China Jan.-Aug. Property Dev. Investment Rises 10.1%

- China Jan.-July Property Dev. Investment Rises 10.2% Y/Y

This was offset by another drop in car sales, while jewelry demand rose 14.1%.

While some have praised the beat in retail sales, recall that over the weekend Goldman showed the wide divergence between public (strong) and private (weak) consumption data, suggesting that Beijing is goalseeking yet another data set in addition to GDP.

That said, the latest drop in fixed investment – potentially a consequence of the trade war with the US and China’s own shadow deleveraging – will probably mean more pressure on the government to push growth, meaning more fiscal stimulus. In fact, the record low fixed investment suggests that contrary to the trade war rhetoric, China’s growth woes are homegrown, not just the trade tensions. And, as we have discussed previously, the ongoing sharp decline in investment spending by local governments due to develeraging campaign may be to blame.

Commenting on the data, Tring Nguyen of Natixis, summarized that “retail sales up but fixed asset investment down again. Not great news for growth expectations & growth is increasingly more dependent on consumption. So what is the reaction from the government? More pump priming? The worse the data, the more the easing?”

Trinh@Trinhnomics#China : Retail sales up by fixed asset investment down again. Not great news for growth expectations & growth is increasingly more dependent on consumption. So what is the reaction from the government?

More pump priming? The worse the data, the more the easing?

Meanwhile, as Bloomberg also notes, an August jump in local government bond sales from a year ago may be a signal that China’s infrastructure projects are kicking off again to support a wilting economy which has been hit by the twin risks of trade wars and deleveraging.

- The data dump release was accompanied by the usual propaganda from the NBS in Beijing which claimed that:

- There is no stagflation or stagflation-like conditions in China

- China’s infrastructure investment may stabilize in the next few months

- China fixed-asset investment may stabilize

- China household debts remain at reasonable level

- Effects of China pro- growth measures are showing up

- China inflation pressure remains moderate