GOLD: $1224.70 UP $1.30 (COMEX TO COMEX CLOSINGS)

Silver: $14.33 DOWN 2 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1224.25

silver: $14.31

Today the CME reports a massive amount of liquidation in the both gold and silver as per total open interest, but not in the front month of December. Unless something drastic happens with tomorrow’s reading, we should have a huge amount of gold and silver standing.

I receive the initial amount of gold and silver standing at around 10: 00 pm tonight and I will put the numbers in this spot to give you the idea of what has been served upon in first day notice.

11 PM TONIGHT: NOV 29.2018

HUGE NUMBER OF GOLD NOTICES FILED: 2083 NOTICES FOR 208300 OZ OR 6.479 TONNES ALREADY SERVED UPON FOR GOLD. IT WILL BE INTERESTING AS THEY ONLY HAVE 4 TONNES OF REGISTERED GOLD.

HUGE NUMBER OF SILVER NOTICES FILED: 1463 NOTICES FOR 7.315,000 OZ

‘

WE NOW AWAIT TO SEE HOW MANY LONGS ARE STANDING FOR DELIVERY IN BOTH GOLD/SILVER

For comex gold and silver:

NOV

NUMBER OF NOTICES FILED TODAY FOR NOV CONTRACT: 1 NOTICE(S) FOR 300 OZ

Total number of notices filed so far for NOV: 219 for 21900 OZ (0.6811 TONNES)

FOR NOVEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1 NOTICE(S) FILED TODAY FOR 5,000 OZ/

Total number of notices filed so far this month: 1488 for 7,440,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4407: up 125

Bitcoin: FINAL EVENING TRADE: $4327 down $46

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A HUMONGOUS SIZED 9525 CONTRACTS FROM 199,783 DOWN TO 190,258 DESPITE YESTERDAY’S 23 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 1323 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1323 CONTRACTS. WITH THE TRANSFER OF 1323 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1323 EFP CONTRACTS TRANSLATES INTO 6.615 MILLION OZ ACCOMPANYING:

1.THE 23 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. 2,520,000 OZ STANDING IN OCTOBER. AND NOW SO FAR A HUGE 7,440,000 OZ STANDING FOR NOVEMBER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF NOV: 47,758 CONTRACTS (FOR 20 TRADING DAYS TOTAL 47,758 CONTRACTS) OR 238.79 MILLION OZ: (AVERAGE PER DAY: 2388 CONTRACTS OR 11.94 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF NOV: 238.79 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 34.11% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,650.42 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 9525 DESPITE THE 23 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A VERY GOOD SIZED EFP ISSUANCE OF 1323 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A HUGE SIZED: 8208 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1323 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 9525 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 23 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.35 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH IN SEPTEMBER A FINAL MONSTROUS 39.05 MILLION OZ OF SILVER STANDING FOR DELIVERY, WITH HUGE DELIVERIES OF OVER 2 MILLION OZ IN OCTOBER (A NON DELIVERY MONTH) AND NOW 7.440 MILLION OZ IN NOVEMBER….... NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .9525 BILLION OZ TO BE EXACT or 136% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz AND NOW NOV AT 7.440 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY AN ATMOSPHERIC SIZED 23,939 CONTRACTS DOWN TO 418,862 DESPITE THE GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $9.45//.YESTERDAY’S TRADING) AS THESE GUYS JOINED SILVER IN THE ROUTINE MIGRATION OVER TO ETF’S AS WE APPROACH AN ACTIVE DELIVERY MONTH.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN ATMOSPHERIC SIZED 14,521 CONTRACTS:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 14,521 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 418,862. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9418 CONTRACTS: 23,939 OI CONTRACTS DECREASED AT THE COMEX AND 14,521 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS: 9418 CONTRACTS OR 941,800 OZ = 29.29 TONNES. AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $9.45???

YESTERDAY, WE HAD 18,710 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV : 163.814 CONTRACTS OR 16,381,400 OZ OR 509.53 TONNES (20 TRADING DAYS AND THUS AVERAGING: 8190 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY IN TONNES: 509.53 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 509.53/2550 x 100% TONNES = 19.98% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,716.76 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018:

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED DECREASE IN OI AT THE COMEX OF 23,939 DESPITE THE GAIN IN PRICING ($9.45) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 14,521 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 14,521 EFP CONTRACTS ISSUED, WE HAD A HUGE LOSS OF 9418 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

14,521 CONTRACTS MOVE TO LONDON AND 23,939 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 29.29 TONNES). ..AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A GAIN OF $9.45 IN YESTERDAY’S TRADING AT THE COMEX

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $1.30 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD/

/GLD INVENTORY 761.74 TONNES

Inventory rests tonight: 761.74 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 2 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 322.906 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A GIGANTIC 9525 CONTRACTS from 199,783 DOWN TO 190,258 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

1323 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1323 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 9525 CONTRACTS TO THE 1323 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE NET LOSS OF 7896 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 41.04 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., AND NOW 7.440 MILLION OZ STANDING IN NOVEMBER.

RESULT: A HUGE DECREASE IN SILVER OI AT THE COMEX DESPITE THE 23 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 1323 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 34.29 POINTS OR 1.32% //Hang Sang CLOSED DOWN 231.53 POINTS OR 0.87% //The Nikkei closed UP 85.38 OR 0.39%/ Australia’s all ordinaires CLOSED UP .64% /Chinese yuan (ONSHORE) closed DOWN at 6.9439 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil DOWN to 50.93 dollars per barrel for WTI and 57.87 for Brent. Stocks in Europe OPENED GREEN EXCEPT SPAIN//. ONSHORE YUAN CLOSED UP AT 6.9439AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9375: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)Your most important commentary of the day: Snider comments correctly that dollars outside the USA system (eurodollars) has collapsed in numbers probably due to the USA higher interest rate policy and its huge deficits are sucking in dollars from around the world. That has created problems for our emerging markets and also most importantly China which has needed foreign investments to grease their economy. Now that dollars are leaving, the CNY is falling in value and we now have a risk of citizens moving their dollars (which are hidden) out to Switzerland or other safe havens. This is setting up a huge deflationary problem for the world as the yuan will spike greater than 7.5 or 8.0 to one USA dollars and with that, China will flood with world with cheap goods and this will idle European and other shops as they simple could not compete.

a must read..

(courtesy Snider/Alhambra Partners)

4/EUROPEAN AFFAIRS

i)Germany

Our good friends over at Deutsche bank, the world’s largest derivative player are not happy campers today. They have been raided by German police at their Frankfurt headquarters.

( zerohedge)

ii)Germany now doubles the payout to migrants if they agree to leave the country

iii)EU

iv)Bill Blain explains the strange Pimco deal where it buys the entire 3 billion euros of debt offered by Italy’s largest banks Unicredit. In a nutshell Pimco is betting that Brussels must support Italy despite the country’s anger at now allowing a budgetary deficit of 2.4%. Pimco is stating that the ECB must buy Italian bonds ad infinitum

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

i)Oil spikes a little after a report that Russia accepts the need for oil cuts

( zerohedge)

ii)Natural Gas prices fall to an average price of 25 MTMu and in some place, natural gas is just given away for free and some at a negative price ie. the user receives money for taking the product off the producer’s hands

iii)Gas prices slide to its lowest level on huge shale production

( zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

The boys juice the markets on a report that both China and the uSA are exploring ways to make a deal to ease tensions

( Wall Street Journal/zerohedge)

ii)Market data/

a)Good data today for the USA. Both Income and spending data surges in October but also inflation

( zerohedge)

b)Seems that the jobless numbers turned on a dime: they soared to 8 month highs..as something is seriously wrong in the USA economy.

c)Housing is a major component of GDP. Today the second leg on the housing report shows pending home sales plunging.

( zerohedge)

d)The libor 3 month rate has been rising steadily for months. Today is surged a monstrous 3 full points to 2.738. As we have pointed out to you on several occasions this kills the dollar funding operations in the emerging markets and in China. The big question now is: who will be buying the huge 1.8 trillion USA debt.

(courtesy zerohedge)

a)The pitiful shake of the USA social security. They state that they will run out of money by 2034. It will be probably much earlier

( SovereignMan.com)

b)Brandon Smith is one smart cookie: He basically is stating that the Trump/Fed will orchestrate a market crash and that will help our banking elites to pick up assets at pennies on the dollar

d)A terrific and short commentary from Graham Summers as he correctly laid out what happened yesterday and it is very bad. The market reacted by going up 600 points but the USA dollar hardly moved and the 10 yr bond also hardly budged. The dollar should have been hit by 1.5% and the 10 yr bond rate should have plummeted. It did not as the global picture is in trouble financially.

iv)SWAMP STORIES

Let us head over to the comex:

We are now in the non active delivery month of NOVEMBER and here we now have 1 notices standing for a GAIN of 1 contact. We had 0 notices served upon yesterday so we gained 1 contract or an additional 5,000 oz will stand for delivery as these longs refused to morph into London based forwards as well as not accepting a fiat bonus for their efforts.

After November, we have a December contract and here we LOST 18,497 contracts DOWN to 17,745. January saw a GAIN of 97 contracts up to 1937 contracts. March, the next big delivery month after December saw a gain of 8478 contracts up to 141,431

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON NOV 27. 2017 WE HAD STILL 14,121 (1 day before first day notice) OPEN INTEREST CONTRACTS LEFT TO BE SERVED UPON AND THIS COMPARES TO TODAY: 17,745 CONTRACTS (1 days before first day notice)

IT ALSO LIKES LIKE WE ARE GOING TO HAVE A DANDY AMOUNT OF SILVER STANDING FOR DELIVERY AT THE COMEX.

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

i) Into Brinks: 504,144.890 oz

BREXIT May Lead to UK Property Crash and Depression

– Brexit no-deal would lead to “worst crash since 1930s”

– Gold rose 0.6% in dollars and 1.2% in pounds today

– UK economy could contract by 8%, house prices fall 30%, sterling fall 25% warns Bank of England

– Sterling collapse would push Irish economy into recession

– Carney’s doomsday scenario sees the crippling of UK finances, the pound crashing and inflation soaring

– BOE accused of “Project Fear” and attempt to scare UK parliament to vote against Brexit deal

Market Performance – 1 Day (Finviz)

via Times UK:

Britain would be plunged into its deepest recession since the 1930s under a disorderly no-deal Brexit, the Bank of England warned yesterday.

House prices could fall by 30 per cent, interest rates rise to 5.5 per cent and the economy shrink by 8 per cent — a greater contraction than after the 2008 financial crisis — its worst-case scenario showed.

Ben Broadbent, one of the Bank’s deputy governors, said that this would be worse than any crisis since “we went back on gold” and the economy subsequently crashed in 1930. In the 2008 financial crisis the British economy shrank by 6.3 per cent.

The Bank gave its assessment hours after a Whitehall analysis suggested that the economy would shrink under all versions of Brexit.

Editors Note: While the BOE’s latest warnings are alarmist, we concur with Mark Carney’s advice to “hope for the best but to prepare for the worst” by re-balancing investment and pension portfolios and owning physical gold.

News and Commentary

Gold gains as US dollar weakens after cautious Fed speech (MoneyControl.com)

Gold Rises on Slipping Dollar On Dovish Fed (Investing.com)

Did Fed’s Powell ‘light the fuse’ for a year-end rally? (MarketWatch.com)

Fed’s Powell, in apparent dovish shift, says rates near neutral (Reuters.com)

Fed warns ‘particularly large’ plunge in asset prices is possible if risks materialize (CNBC.com)

Source: SRSRocco

Brexit: Dire warnings about the cost of a no-deal are mounting (BloombergQuint.com)

Macro Deceleration Getting Confirmed By How 10-Year T-Yield Behaves (Hedgopia.com)

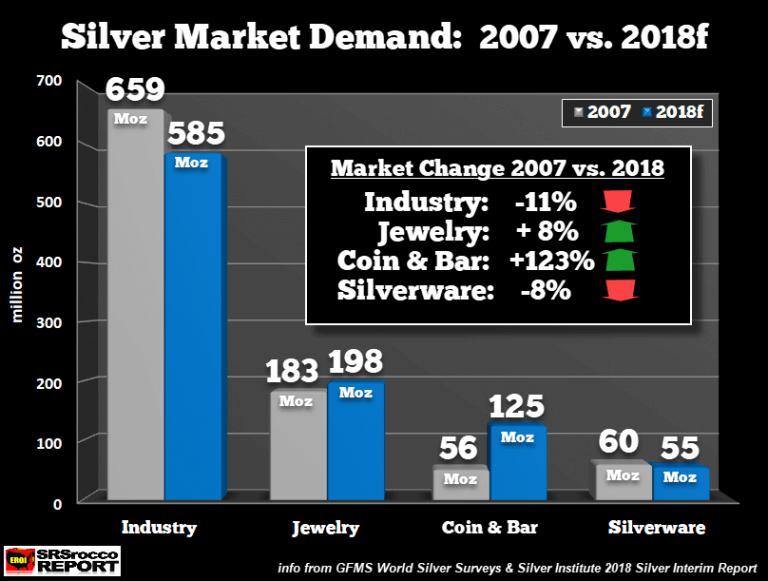

Invest Demand: Still Largest Growth Sector In Silver Market (SRSRoccoReport.com)

Peak Misery: “Everything is Failing” (SevenFigurePublishing.com)

Deutsche Bank Shares Slide As Police Raid Frankfurt Headquarters (ZeroHedge.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

28 Nov: USD 1,213.20, GBP 949.69 & EUR 1,074.77 per ounce

27 Nov: USD 1,225.05, GBP 959.70 & EUR 1,082.21 per ounce

26 Nov: USD 1,226.65, GBP 954.58 & EUR 1,079.33 per ounce

23 Nov: USD 1,222.15, GBP 951.69 & EUR 1,075.13 per ounce

22 Nov: USD 1,228.25, GBP 950.42 & EUR 1,074.72 per ounce

21 Nov: USD 1,224.00, GBP 957.29 & EUR 1,075.04 per ounce

20 Nov: USD 1,223.10, GBP 951.45 & EUR 1,069.97 per ounce

Silver Prices (LBMA)

28 Nov: USD 14.15, GBP 11.06 & EUR 12.54 per ounce

27 Nov: USD 14.28, GBP 11.20 & EUR 12.61 per ounce

26 Nov: USD 14.38, GBP 11.18 & EUR 12.65 per ounce

23 Nov: USD 14.26, GBP 11.12 & EUR 12.56 per ounce

22 Nov: USD 14.52, GBP 11.26 & EUR 12.72 per ounce

21 Nov: USD 14.42, GBP 11.26 & EUR 12.65 per ounce

20 Nov: USD 14.44, GBP 11.24 & EUR 12.63 per ounce

Recent Market Updates

– General Motors And General Electric Highlight The Ponzi Scheme That Is The US Economy

– A Worldwide Debt Default Is A Real Possibility

– Risk of Lower Lows in Gold Remains Prior to Spectacular Rally to Follow

– Gold and Silver Hold Firm as Stocks and Oil Lower in to US Holiday Weekend

– Is Brexit a Massive Threat to Globalisation?

– Stock Markets Remains Extremely Overvalued – Hussman

– Stocks are Now in ‘Complete Bitcoin Territory,’ Asset Manager Says

– Brexit’s Safe Haven Is a Dangerous Place

– Gold and Silver Rise As Stocks Fall On Valuation Concerns, Italy and Brexit Risks

– Pound Falls 2.5% Against Gold as UK Government in Turmoil Over Brexit

– GoldCore Capitalising On Brexit With Dublin Gold Vault

Refusals to answer should be enough to settle the gold-rigging issue

Submitted by cpowell on Thu, 2018-11-29 03:37. Section: Daily Dispatches

10:55p ET Wednesday, November 29, 2018

Dear Friend of GATA and Gold:

Questions are asked to get answers, but refusals to answer may be enough to permit conclusions to be drawn and thus in effect constitute answers as well.

With all these recent refusals to answer, who really cannot believe that governments and central banks long have been manipulating the gold market so they might control the currency markets and thereby defeat all markets?

Consider the following.

* * *

By letter on July 27 this year U.S. Rep. Alex X. Mooney, R-West Virginia, put many critical questions to Treasury Secretary Steven Mnuchin and Federal Reserve Chairman Jerome Powell:

Among the questions:

— Given the recent tight correlation between the gold price and the value of the Chinese yuan, has China been rigging a market purportedly protected by antitrust law in the United States?

…

What is U.S. government policy toward gold? Does it remain, as U.S. government archives show it to have been at least since the 1970s, to drive gold out of the world financial system?

— Is the U.S. government trading in gold or gold derivatives through the Treasury Department’s Exchange Stabilization Fund, other government agencies, or other intermediaries?

— How does the Federal Reserve reconcile the written statement of Fed Governor Kevin M. Warsh in 2009 that the Fed has secret gold swap arrangements with foreign banks with the assertion by Fed Chairman Powell in July this year that the Fed has had no involvement with gold swaps?

— Has any audit sought to identify any encumbrances on monetary metals owned by the U.S. government?

Four months have passed and Mooney’s letter has gone unanswered and even unacknowledged by the Fed and Treasury.

* * *

By letter in July GATA asked the U.S. Commodity Futures Trading Commission to examine the recent correlation of the gold price and the valuation of the Chinese yuan:

We asked the commission:

— How does the CFTC allow a foreign government or entity to control the price of this important commodity and currency by trading in U.S. markets?

— Is market manipulation by a foreign power happening with the authorization of the U.S. government?

Four months have passed and the commission has not answered or even acknowledged the letter.

* * *

By letter in September GATA asked the CFTC if the commission has jurisdiction over market rigging by the U.S. government itself or whether such market rigging is authorized by federal law, such as the Gold Reserve Act of 1934, which established the Exchange Stabilization Fund:

http://www.gata.org/node/18512

Two months have passed without an acknowledgment from the commission.

* * *

On July 2 your secretary/treasurer e-mailed the public relations department at JPMorganChase & Co. about the bank’s involvement in the monetary metals markets, which occasionally has been controversial. The message read:

“In April 2012 Blythe Masters, then chief of the bank’s commodities desk, told CNBC that the bank had no position of its own in the monetary metals markets and was trading only for clients:

https://www.youtube.com/watch?v=gc9Me4qFZYo

“Can you tell me if this remains the case and if the bank’s clients in trading the monetary metals markets include governments and central banks?”

Five months have passed without an acknowledgment from JPMorganChase.

* * *

A year ago GATA e-mailed the press office of the Bank for International Settlements in Basel, Switzerland, the gold broker for most central banks, asking for an explanation of what the bank does in the gold market, for whom the bank does it, and for what purposes:

The bank promptly replied but did not answer the question. The bank wrote: “We do not comment on specific accounts / holdings of central banks or of the BIS. Please see our latest annual report for details on gold. Further information can be gleaned from central banks directly.”

But GATA did not ask the BIS to “comment on specific accounts / holdings of central banks or the BIS itself.” We asked the BIS for an explanation of what the bank does in the gold market generally and why. Further, there is precious little information about gold in the BIS’ annual report and most of the bank’s members conceal their trading of gold and gold derivatives.

Indeed, a secret March 1999 report by the staff of the International Monetary Fund, obtained by GATA, says central banks conceal their gold loans and swaps precisely to facilitate their surreptitious interventions in the gold and currency markets:

http://www.gata.org/node/12016

* * *

Eight days ago the London Bullion Market Association issued a report purporting to disclose the weekly volume of gold trading by its members. Bloomberg News headlined its story about the report this way: “London Gold Market Comes Clean”:

https://www.bloomberg.com/news/articles/2018-11-20/london-gold-market-co…

But Bullion Star’s gold market analyst Ronan Manly, whose research through the years has exposed much about the LBMA, didn’t believe that the association had “come clean” about anything. Manly found the LBMA’s data report suspicious in part because it seemed to omit trading by central banks through LBMA members:

http://www.gata.org/node/18630

So your secretary/treasurer e-mailed the LBMA press office and LBMA Chief Executive Ruth Crowell, calling Manly’s analysis to their attention and putting a question to them: “In the interest of the transparency the LBMA says it is pursuing, please tell me whether central bank trading data has been removed or omitted from the information you have just reported.”

The LBMA has not responded.

* * *

Quite without any help from governments and central banks, GATA has extensively documented what is actually their longstanding policy to suppress and control the gold price to defend their control of the world and prevent free and transparent markets from developing. Various admissions and confirmations are summarized here —

http://www.gata.org/node/14839

— and more can be found here:

http://www.gata.org/taxonomy/term/21

GATA invites skeptics to dispute these admissions and confirmations specifically, rather than to dismiss them generally. GATA invites skeptics to try putting their own questions along these lines to governments, central banks, and their agents like the LBMA and to report any answers and refusals to answer.

Of course mainstream financial news organizations could settle this issue quickly and easily by examining the documentation, pressing a few questions of their own, and reporting what they found. Indeed, the refusal of those news organizations to attempt critical journalism in regard to central banking is central banking’s greatest power, power greater even than their power to create and allocate infinite money in secret. For central banking operates so much in secret precisely because its policies work mainly by deception, and exposure would defeat them.

GATA long has been delivering its documentation to many financial news organizations around the world, with little result. But our friends can help by sharing our work, particularly with financial journalists who report about manipulated markets without addressing manipulation, and by sharing our work with elected officials and asking them to investigate as Representative Mooney is doing.

GATA aims to keep at it but fighting all the money and power in the world on behalf of free and transparent markets, limited and accountable government, and equality among the nations is no picnic. Don’t think you can’t do anything here. You can, and GATA needs the help.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

__

Berlin has no plan on how to get €50bn in German gold back from US

Published time: 29 Nov, 2018

Berlin has no plan on how to get €50bn in German gold back from US

© Global Look Press / Christian Ohde

For decades, the Bundesbank, Germany’s central bank and custodian of the country’s gold, has been storing over 1,200 tons of the precious metal worth nearly €50 billion in the New York vaults of the US Federal Reserve.

After a public outcry in Germany in 2013, authorities started the repatriation program, aimed at returning the country’s gold reserves, which have been stored outside of the country since the Cold War. Berlin intended to get at least half of the country’s gold from the US and France by 2020. The government had initially planned to complete the program within a five-year period, but the US Federal Reserve renegotiated the process to a seven-year timeline.

The country reportedly managed to ship only five tons of its gold in 2013 due to logistical difficulties. The following year, Germany repatriated 120 tons of the precious metal – 35 tons from Paris and 85 tons from New York. Some 110.5 tons were brought back from Paris and 99.5 tons from New York in 2015. Two years ago, the country repatriated total of 200 tons.

So far, the Fed has denied the German financial regulator access to the vast deposits that are literally being held hostage overseas. Thus, the Bundesbank has had no opportunity to audit the reserves that belong to Germany.

Various theories circulated about Germany’s foreign gold reserves, with some experts questioning whether it is still there or if it has been used by foreign central banks. However, the German government doesn’t seem very worried about the issue.

“I haven’t heard that it is now becoming a hot topic, but in case it is, you should contact the Bundesbank. They would give you information about the current state of affairs and plans on this issue,” German Finance Ministry spokesman Dennis Kolberg told RT Deutsch during the weekly news conference.

“The Bundesbank has already spoken on this issue, so I can only refer to them,” the official said, when asked if the government has any plans to address the matter of the country’s gold being kept abroad.https://www.rt.com/business/445133-germany-access- gold-us-fed/

Video Link

https://www.rt.com/business/445133-germany-access-gold- us-fed

end

________________________________________

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.9439/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER NOW ON //OFFSHORE YUAN: 6.9375 /shanghai bourse CLOSED DOWN 34.29 POINTS OR 1.32%

. HANG SANG CLOSED DOWN 231.53 POINTS OR 0.87%

2. Nikkei closed UP 85.38 POINTS OR 0.39%

3. Europe stocks OPENED ALL GREEN EXCEPT SPAIN

/USA dollar index RISES TO 96.82/Euro RISES TO 1.1374

3b Japan 10 year bond yield: FALL TO. +.08/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.28/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 50.93 and Brent: 47.87

3f Gold UP/JAPANESE Yen UPCHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.33%/Italian 10 yr bond yield DOWN to 3.23% /SPAIN 10 YR BOND YIELD UP TO 1.51%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.90: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.27

3k Gold at $1226.10 silver at:14.32 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 13/100 in roubles/dollar) 67.26

3m oil into the 50 dollar handle for WTI and 57 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.28DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9937 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1314 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.33%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.02% early this morning. Thirty year rate at 3.31%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.14

S&P Futures Slide, 10Y Yield Hits 3%, Oil Tumbles

Under $50

After yesterday’s furious Powell-inspired rally, the overnight kneejerk reaction has been muted, with US equity futures giving up some of yesterday’s gains while Europe’s Stoxx 600 Index faded earlier gains following a mostly upbeat Asia session.

After 10Y Treasuries surprisingly barely moved following yesterday’s Powell speech, the benchmark yield finally saw a more pronounced move on Thursday morning, extending its decline after the Fed Chairman fueled speculation the central bank may pause interest rate increases next year…

… while the greenback drifted in a tight range following Wednesday’s drop, it rebounded from session lows and was roughly unchanged.

In the wake of Powell’s “dovish” comments that Fed Funds are “just below” estimates of the neutral rate (vs. “a long way” in October), hinting at a potential slowdown in the hiking cycle, the DXY gave up the 97.000 level and witnessed its steepest one-day percentage decline this month so far, to 96.622 at one stage. However, the USD has pared some losses with month-end and SOMA demand still in play, while some rival currencies also suffer further weakness. Looking ahead, FOMC Minutes are due to be published later todayalthough with the market now pricing in just one rate hike in 2019 (from more than less than two months ago), it is unlikely that any further dovish news is possible.

At the same time, European bonds rose, and even though demand for five-year Italian debt at an auction fell to the lowest since June. Italy’s five-year bond yield dipped 4 bps to 2.36 percent and the closely-watched spread over Germany was at 294 bps. Italian debt has rallied this week as the government said it was ready to compromise with the European Union on its budget deficit target. German bonds extended gains after inflation data from the German state of Saxony and Treasury.

European shares gave up early gains of as much as 0.7%, with the Stoxx 600 Europe Index trading up just 0.2% as of 1:02pm CET, dragged lower by the real estate shares which remains the worst performer sector in the index, while tech shares trim gains of as much as 2%. Deutsche Bank dropped more than 3% after prosecutors said its headquarters were being searched in a money laundering probe.

Material names are also seeing support this morning, in-fitting with price action in the metals scope with gains seen in Antofagasta (+4.9%), Glencore (+1.8%), Rio Tinto (+1.1%); upside in mining names and a softer GBP has pushed the FTSE 100 (+0.8%) towards the top of the leaderboard.

Earlier in the session Asian stocks were broadly higher, with MSCI’s broadest index of Asia-Pacific shares outside Japan rose 0.6 percent, although the Shanghai Composite Index dropped 1 percent. Gains were tempered by investor jitters before trade talks between U.S. President Donald Trump and Chinese President Xi Jinping on Saturday, during the G20 summit in Argentina.

The euro erased an earlier advance after a raft of weak economic data, while emerging-market equities rose to the highest level since early October and developing-nation currencies strengthened. The dollar held steady even as the U.S. 10-year note yield fell below 3% for the first time in two months. The euro failed to sustain early gains amid mixed regional German inflation prints, while the pound led losses in G-10 as PM Theresa May said the U.K. should be ready for no deal if Dec. 11 Parliament vote rejects her Brexit plan. Fed’s hike path stays in focus with several speeches by policy makers and minutes from latest meeting due Thursday.

With Powell now out of the way, the market is looking for any signals on trade from a meeting between the U.S. and Chinese presidents that will take place at the Group of 20 summit in Buenos Aires this weekend.

“The next catalyst will be the G-20 meeting between Trump and Xi; we believe risk assets will tactically trade in the green following a tariff cease-fire,” said Eleanor Creagh, a strategist at Saxo Capital Markets in Sydney. “A tradable risk bounce on a paper deal at G-20 will be unlikely to reverse sentiment structurally as the underlying U.S.-China relationship is still deteriorating.”

Elsewhere, West Texas oil tumbled below $50 a barrel for the first time in more than a year as Russia signaled little urgency to commit to supply cuts and traders fretted that OPEC won’t act decisively to clear a resurgent surplus in the global crude market while U.S. crude stockpiles continue to grow.

Oil futures tumbled as much as 1.8% in New York to $49.41 a barrel, the lowest since early October 2017. Brent for January settlement, which expires Friday, fell as much as 2.1% to $57.50 a barrel on London’s ICE Futures Europe exchange. The global benchmark traded at an $8.23 premium to WTI. The more-active February contract lost as much as 2.2 percent.

While Putin praised Saudi Crown Prince Mohammed Bin Salman and said Moscow is ready to cooperate further, he said crude around $60 a barrel is “balanced and fair” and well above the level needed to to keep his government’s budget in surplus. “Putin is fine with $60, but this time next week we will be well below that if there is no deal,” said Warren Patterson, commodity strategist at ING. “I think we are going to have to see the Saudis actively reduce flows to the U.S.”

As noted yesterday, US crude stockpiles rose by 3.58 million barrels last week in the longest run of gains since November 2015, according to the Energy information Administration. The build was higher than the 1-million-barrel gain predicted in a Bloomberg survey, overshadowing a surprise draw in gasoline inventories.

“Oil has moved into our bear case scenario,” Norbert Ruecker, head of macro and commodity research at Julius Baer Group told Bloomberg. “Today’s price levels imply that the petro-nations will maintain their output hikes or that the world economy is about to slow down significantly.”

Gold has rebounded from two-week lows, as the dollar fell following comments from Fed Chairman Powell saying that the policy rate is just below the estimated neutral range. China’s steel prices have dropped following a two day gain largely due to ample supply and lean demand in markets, with iron ore now rising following Monday’s sell off. Additionally, spot Palladium has hit a record high of USD 1186.30/oz.

In geopolitical news, US Secretary of State Pompeo said he is very hopeful for a new meeting with North Korean officials to discuss denuclearization, while there were separate reports that US requested that North Korea change its chief negotiator. The US Senate voted 63-37 to advance a bill that would end US participation in Saudi Arabia-backed war in Yemen which paves way for additional vote next week, although White House has previously noted it would veto the bill if passed. Russia are to construct a missile early-warning radar station in Crimea in 2019, according to Interfax.

Expected data include personal income and jobless claims. Dollar Tree, TD Bank, HP Inc., VMware, and Workday are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.3% to 2,732.00

- STOXX Europe 600 up 0.7% to 359.89

- MXAP up 0.7% to 153.87

- MXAPJ up 0.6% to 493.83

- Nikkei up 0.4% to 22,262.60

- Topix up 0.4% to 1,659.47

- Hang Seng Index down 0.9% to 26,451.03

- Shanghai Composite down 1.3% to 2,567.44

- Sensex up 1.3% to 36,186.13

- Australia S&P/ASX 200 up 0.6% to 5,758.42

- Kospi up 0.3% to 2,114.10

- German 10Y yield fell 2.4 bps to 0.325%

- Euro up 0.07% to $1.1374

- Italian 10Y yield fell 3.2 bps to 2.888%

- Spanish 10Y yield fell 2.4 bps to 1.519%

- Brent futures down 1.3% to $58/bbl

- Gold spot up 0.4% to $1,226.36

- U.S. Dollar Index up 0.1% to 96.86

Top Overnight News

- Deutsche Bank AG’s premises including its headquarters in Frankfurt were being searched by prosecutors on Thursday in a money laundering probe, prosecutors said in a statement. In an emailed statement, Deutsche Bank confirmed that police are investigating at several German locations in relation to Panama Papers, and said it is fully cooperating with authorities.

- President Vladimir Putin said crude around $60 a barrel is “absolutely fine” just days before talks on oil policy with Saudi Arabia

- The Swiss economy unexpectedly shrank in the third quarter by 0.2%, blighted by a drop in exports and weak domestic demand.

- Benchmark Treasury yields fell below 3% for the first time since September and stocks climbed in Europe and Asia after a dovish tone from the Federal Reserve chairman boosted markets ahead of this weekend’s G-20 gathering.

- U.K. Prime Minister warned the country to prepare for a no-deal Brexit if her deal fails to be approved by the House of Commons on Dec. 11. Sterling fell sharply following the comment, down as much as 0.5% to day’s low of 1.2758.

- Federal Reserve Chairman Jerome Powell opened the door for a potential pullback in projected interest-rate hikes for 2019 following a widely expected increase in December. In what was seen as a shift in tone from remarks last month, Powell said Wednesday that the Fed’s series of rate increases had brought policy to “just below” the range of estimates of neutral

- U.K. consumer confidence slumped to the lowest in a year as the country copes with the economic uncertainty of Brexit. The index compiled by YouGov and the Centre for Economics and Business Research fell in November and remains “notably below” where it was before the 2016 referendum to leave the European Union

- Chinese President Xi Jinping said the global economy is at a turning point as he prepares for a critical meeting with Donald Trump this weekend. Xi said the world has to decide whether to continue working to support the global trading system. Failure to do so will lead to new barriers emerging between nations

- President Donald Trump raised the prospect of slapping a 25 percent tariff on imported cars and ordered a review of China’s retaliatory auto tariffs against the U.S

Asian stocks traded mostly positive after risk appetite was ignited by Fed Chair Powell’s dovish comments which spurred hopes the Fed may begin to slow down on its hiking cycle and helped US stocks notch their biggest daily gain since March. ASX 200 (+0.6%) and Nikkei 225 (+0.4%) were underpinned from the open but with gains capped amid lingering trade uncertainty and inconclusive capex data for Australia, as well as mixed Japanese retail sales and a decline in USD/JPY. Hang Seng (-0.8%) and Shanghai Comp. (-1.3%) both initially conformed to the positive tone but then stalled amid tariff threats with Chinese President Xi’s offer of an olive branch to the US somewhat falling on deaf ears, as USTR Lighthizer said China has yet to offer meaningful proposals and suggested that the US are seeking to match China’s tariffs on autos. Finally, 10yr JGBs were marginally higher as they nursed the prior day’s losses after having found support around the 151.00 level and although today’s mixed 2yr auction results failed to spur a reaction, prices continued to gain as the strength in the regional stock markets moderated.

Top Asian News

- China Is Said to Plan Major Purge of $176 Billion Loan Market

- HNA Is Said to Widen Sales Push, Marketing More Than 90 Assets

- Singaporean Regulators Widen Noble Group Probe to Auditor EY

- South Korea-Japan Spat Deepens Over Mitsubishi Forced Labor Case

- China Bond Defaults Surpass 100 Billion Yuan for 1st Time

European equities (Eurostoxx 50 +0.3%) piggybacked on the optimism seen on Wall St and during the Asia-Pac session as perceived dovish rhetoric by Fed Chair Powell continues to guide markets. Initial reports via WiWo that European Commissioner Oettinger expected US auto tariffs before Christmas resulted in downside to European equities, especially German autos, though DAX (+0.2%) saw a rebound after these comments were denied by the European Commission. Sectors are mixed with IT names the outperformer following gains seen yesterday during US hours which has prompted upside in chip-makers such as Wirecard (+3.3%), STMicrolectronics (+2.5%) and Infineon (+2.2%). Material names are also seeing support this morning, in-fitting with price action in the metals scope with gains seen in Antofagasta (+4.9%), Glencore (+1.8%), Rio Tinto (+1.1%); upside in mining names and a softer GBP has pushed the FTSE 100 (+0.8%) towards the top of the leaderboard. To the downside, energy names lag their peers with WTI and Brent crude unable to halt recent declines. In terms of stock specifics, once again, Deutsche Bank (-3.3%) have found themselves in the centre of further controversy with their offices raided earlier this morning in a money laundering probe involving two members of staff. Elsewhere, Intu Properties’ (-35%) shares have slumped to a record low this morning after reports that a consortium led by their Deputy Chairman has abandoned their plans to buy the Co.

Top European News

- Euro-Area Economic Confidence Falls, Complicating ECB’s Mission

- Swiss, Swedish Economies Shrink as Trade Slump Hits Europe

- Mother and Son Lose $16 Billion in 2018 as Continental Sinks

- Eurofins Finance Chief Says Company Has No Liquidity Problem

In FX, in the wake of Powell’s “dovish” comments that Fed Funds are “just below” estimates of the neutral rate (vs. “a long way” in October), hinting at a potential slowdown in the hiking cycle, the DXY gave up the 97.000 level and witnessed its steepest one-day percentage decline this month so far, to 96.622 at one stage. However, the USD has pared some losses with month-end and SOMA demand still in play, while some rival currencies also suffer further weakness. Looking aheadd, FOMC Minutes are due to be published later today. GBP,EUR – Major G10 underperformer with ongoing Brexit bickering and meaningful vote concerns driving Cable below 1.2800 with a low print of 1.2759 (vs. highs of 1.2850, with offers seen between 1.2855-65) , while Sterling also fell victim to cross positioning for month end as EUR/GBP climbed above the key psychological 0.8900 level, before the single currency came under renewed pressure on latest auto tariff headlines as press reported that EU Commissioner Oettinger expects US auto tariffs before Christmas. This pushed EUR/USD to fresh session lows of 1.1350 and bringing into play options around 1.1340-50 (3.2bln) and 1.1360-65 (1.35bln). Note, the EUR did not really react to mixed German state CPIs but did respect a key fib just ahead of 1.1400 (1.1394). Looking ahead German national CPIs are due at 13.00GMT. AUD – In contrast the AUD has showed some resilience despite lower than expected capital expenditures with the antipodean staying afloat above 0.7300. JPY – The major beneficiary of the post-Powell Dollar weakness as USD/JPY fell through 114.00, 113.50 and currently rests around 113.40. In terms of technicals, the next level to the downside is at 113.17 (tenkan line), looking ahead, Tokyo CPIs are due to be released later today. TRY – The clear EM outperformer with the currency breaching 5.1500 (and temporarily rallying through a key fib at 5.1562) vs. the buck as the move was exacerbated by the drop below 5.2000 in the wake of a significan improvement in Turkish economic confidence index and falling oil prices (as Turkey is a large net importer).

In commodities, Brent (-1.3%) and WTI (-1.0%) have moved lower recently, which may have been exacerbated by reports that 7k WTI contracts were dropped at the same time. Overnight oil prices had moved higher, despite a greater than expected build shown in EIA weekly crude stocks of 3.577mln vs. Exp. 0.769mln, with prices boosted by a stronger dollar in addition markets are looking optimistically to this weeks G20 meeting to improve global demand. Gold has rebounded from two-week lows, as the dollar fell following comments from Fed Chairman Powell saying that the policy rate is just below the estimated neutral range. China’s steel prices have dropped following a two day gain largely due to ample supply and lean demand in markets, with iron ore now rising following Monday’s sell off. Additionally, spot Palladium has hit a record high of USD 1186.30/oz.

Looking at the day ahead, much of the focus should be on the various inflation reports. In Germany we’ll get the preliminary November CPI report this afternoon where the consensus expects a small one-tenth decline to +2.3% yoy. Shortly following that we get the October PCE report in the US where the expectation is also for a modest one-tenth decline to +1.9% yoy. Alongside that data we’ll also get October personal income and spending reports in the US, followed later on by the latest weekly initial jobless claims reading, October pending home sales and the November FOMC minutes. Also due out in Europe is Q3 GDP in France, October money and credit aggregates data in the UK and November confidence indicators for the Euro Area. A busy week for central bank speak rolls on with Guindos and Angeloni speaking on behalf of the ECB, while over at the Fed Mester, Evans, Harker, Kashkari, Kaplan and Rosengren are all participating in a Boston Fed Conference on “Collaboration for Inclusive Economic Development”. Also due today is a 5y and 10y BTP auction which will be worth watching in light of recent weak retail BTP demand. Finally, G-20 finance ministers will attend a working dinner in Buenos Aires tonight before the main event kicks off tomorrow

US Event Calendar

- 8:30am: Powell Greets Students at 15th Annual College Fed Challenge

- 8:30am: Personal Income, est. 0.4%, prior 0.2%

- 8:30am: Personal Spending, est. 0.4%, prior 0.4%; Real Personal Spending, est. 0.2%, prior 0.3%

- 8:30am: PCE Deflator MoM, est. 0.2%, prior 0.1%; PCE Deflator YoY, est. 2.07%, prior 2.0%

- 8:30am: PCE Core MoM, est. 0.2%, prior 0.2%; PCE Core YoY, est. 1.9%, prior 2.0%

- 8:30am: Initial Jobless Claims, est. 220,000, prior 224,000; Continuing Claims, est. 1.66m, prior 1.67m

- 9:45am: Bloomberg Consumer Comfort, prior 61.3

- 10am: Pending Home Sales MoM, est. 0.5%, prior 0.5%; NSA YoY, est. -2.8%, prior -3.4%

- 2pm: FOMC Meeting Minutes

- 2pm: Five Fed Presidents Participate in Conference at Boston Fed

- 3:05pm: Fed’s Kaplan Speaks at Boston Fed Conference

DB’s Jim Reid concludes the overnight wrap

As an analyst the one main currency you have is credibility. If your analysis is found suspect or biased then it’s likely the damage to your reputation will be permanent and career in ruins. I fear that after the deluge of criticism I received after yesterday’s EMR I may have crossed that line. So today I offer an unconditional apology and ask that readers give me a second chance. Maybe I was wrong when I said that “Last Christmas” by Wham is the best ever festive song.

We did also wonder yesterday whether the Santa Claus rally was underway, and in response Fed Chair Powell donned his best Father Christmas outfit and gave the market a mighty “ho, ho, ho.” His speech released at 12 EST / 5pm London time was the game changer as the S&P 500 jumped +0.79% (from only just about up on the day) immediately after he mentioned that rates now were “just below” neutral, and the index ultimately carried on the rally and closed +2.30% the best day since March and the second best this year. This comment was a notable shift from his language on October 3, when he said “we’re a long way from neutral at this point.” Obviously this is very important as the closer that Powell thinks rates are to neutral, the sooner he may be comfortable pausing the hiking cycle. He also noted that the impacts of policy “may take a year or more to be fully realized.” While that’s pretty typical language from a Fed Chair, it is notable in the current context, since it could portend a pause once rates reach neutral. Finally, he also said that “we will be paying very close attention to what incoming economic and financial data are telling us,” committing more forcefully to data dependency than the Fed have for a while. Given recent softness in inflation data and the tightening in financial conditions, this would also argue in favour of a less hawkish rate path.

All markets reacted to Powell’s comments and in rates we immediately priced a more dovish Fed, removing 4bps of hikes from the 2019 rate path. The market continues to expect a hike at this December’s FOMC meeting, but now prices in only 31.5bps of additional hikes over the course of next year, compared to the Fed’s median expectation for 75bps at last count. Two-year Treasury yields fell -2.0bps, and while 10-year yields closed close to flat (+0.4bps), real yields fell -2.7bps (inflation breakevens rose +3.1bps). Elsewhere the dollar depreciated -0.55%, as emerging market currencies gained +0.71% and EM equities advanced +2.39%. Other US equities also rallied, with the DOW, NASDAQ, and NYFANG indexes up +2.50%, +2.95%, and +2.90% respectively. That caps the third session in a row of US equity gains, with the DOW gaining +4.45% over that period, the best such streak since June 2016.

This morning in Asia, markets are largely trading higher with the Nikkei (+0.69%), Shanghai Comp (+0.28%) and Kospi (+0.47%) all up while Hang Seng (-0.04%) is trading flattish. However, most markets are trading off their highs as the overnight rhetoric between the US and China seems to be weighing on sentiment (more on this below). Elsewhere, futures on the S&P 500 (-0.19%) are pointing towards a slightly softer start and Crude oil prices (WTI +1.01% and Brent +0.75%) are up this morning.

Ahead of the meeting between the US President Trump and China’s President Xi Jingping on the sidelines of the G20 summit, the South China Morning Post reported that the Chinese President is likely to offer the US a deal comprising of an offer to provide greater market access to US companies and fewer subsidies to the state enterprises along with better protection for intellectual property. However, the source said that the Chinese offer could be a oneshot deal and that if the US refuses to accept the deal at the meeting then there is a possibility that there will be no deal and “we have to see who can bear the economic pain longer.” In the meantime, President Trump raised the prospect of slapping a 25% tariff on imported cars and ordered a review of China’s retaliatory auto tariffs against the US, likely in response to the General Motors announcement of plant closures in the US. The US Trade Representative Robert Lighthizer also said that China has not offered any meaningful proposals yet ahead of the G20 meeting while adding that China’s policies on auto tariffs are ‘egregious’ and the US will examine tools to equalize tariffs on autos as instructed by President Trump. So the stakes are getting higher ahead of the weekend.

Back to yesterday and prior to Powell, markets in Europe largely limped to the finish following a mostly unspectacular session. The STOXX 600 and the CAC both closed flat, while the DAX fell -0.09%. An index of euro-denominated HY bond spreads widened +1.8bps to match its recent high – the widest level since June 2016. The euro had been trading flat versus the dollar until Powell, after which it rallied +0.70%.

A busy week for the Fed continues with the November FOMC minutes this evening. Some of the interest level has probably been taken out of them given we’ve had Clarida and Powell speak in the last two days however we should still learn a good deal more about the Committee’s discussion of its operating framework and potential for another technical adjustment to the IOER at the December 19 meeting.

Here in the UK, both the BoE and the government yesterday published their various Brexit scenarios with the former also releasing the latest annual bank stress tests – which all banks passed. For the hard Brexit scenarios, look away now if you’re a recent UK homeowner. The BoE warned that at the bearish end with a “disorderly” scenario, GDP would contract -8% within a year, while house prices would fall by -30%, commercial property prices fall -48% and Sterling fall -25% to below parity with the dollar. So we UK homeowners will see our property down over 50% in dollar terms!! Inflation would also accelerate to 6.5% and the base rate to rise to 5.5%. In a scenario in which the UK retains a “Close Economic Partnership” with the EU, including comprehensive arrangements for free trade in goods and some trade in business and financial services, then GDP would be between 1.25% and 3.75% lower over a 5 year forecast relative to where it would have been without the vote. Note a lot of these forecasts assume notable BoE rate hikes to combat higher inflation. Such a hawkish policy response is a bit hard to envision, given the BoE responded to the initial Brexit vote by easing policy aggressively, nevermind the weaker pound and higher inflation outlook. So these forecasts are highly, highly uncertain.

As for the government report, at the most bearish end, assuming no deal and zero EEA migration, UK GDP would be as much as 10.7% lower over 15 years. While there wasn’t an exact modelled representation of the deal agreed with the EU, a halfway point between May’s ideal plan and a regular free-trade arrangement would see GDP as much as 3.9% lower than it would have been assuming no migration and 2.1% lower with migration. When it was all said and done Sterling was trading close to flat on the releases, but it was subsequently caught in the Powell-driven dollar selloff and ultimately rallied +0.64% versus the greenback.

Staying with Europe, there were a few interesting headlines out of the ECB worth noting yesterday. Quoting Euro Area officials, Bloomberg reported that the ECB expects to confirm the end of net asset purchases next month, and also that the central bank sees no need to announce a replacement for TLTRO2 at present. The story also hinted at the possibility of clarifying what the “extended period” means with regards to fully reinvesting maturing bonds after the end of net purchases. So this would suggest that next month’s meeting is likely to be squarely focused on the QE and reinvestment decisions. Our European economists’ baseline view is that it is highly unlikely that the ECB extends QE, the Governing Council reiterates the broad narrative of above-trend growth and confidence in inflation normalisation, and that there is eventually a replacement for TLTRO2 to avoid a disorderly deleveraging. Indeed, the team don’t rule out a hint in that direction from Draghi in next month’s press conference.

Later in the day, the expected new Chief Economist of the ECB, Philip Lane, confirmed that a rate increase will be data dependent in the second half of 2019, and also that the ECB is starting to see more heat in the labour market. These weren’t particularly ground-breaking comments, but Lane’s rhetoric will be important to watch going forward given his expected new position within the ECB. As for markets, after yields bottomed out early in the session, bonds mostly weakened with the improved sentiment. Bunds retraced gains of -1.7bps to close flat.

The BTP curve was a lot more mixed by comparison with the short end selling off (two-year +3.4bps) with the belly stronger (10-year -3.3bps). There wasn’t a great deal of new information to feed off however with headlines remaining fairly contradictory. Finance Minister Tria told the Senate that “we need to clarify to our partners in Europe that the aim of the budget is to tackle concrete problems, and certainly not to organise an affront to Europe or organise an exit from the euro.” Meanwhile, Italian PM Conte was reported as saying that the Government had not decided on a new deficit target for 2019, but also that the Government would do anything necessary to find an agreement with the EU.

In other markets, oil prices were sharply lower once more with WTI and Brent ending the day -2.39% and -2.44% respectively. Despite headlines that both Saudi Arabia and Nigeria were confident about OPEC succeeding in stabilizing prices, Russian President Putin poured cold water on the prospects for a deal.

He said that Brent prices around $60 per barrel are “absolutely fine” for his country, suggesting limited motivation to make an output cap deal at December 6’s OPEC meeting. Later in the session, US crude oil inventories rose more than expected, increasing by 3.6 million barrels. That’s the 10th consecutive weekly inventory build, the longest such streak in three years.

As for the economic data that was out yesterday, there weren’t any great surprises from the releases in the US. There was no change to the second estimate of Q3 GDP in the US at 3.5% qoq saar with downward revisions to consumer spending offset by upward revisions to fixed investment and inventories. Notably, the details showed that corporate profits during the quarter grew at 10.3% yoy which is the strongest pace since Q2 2012 while the core PCE was downgraded by 10bps to 1.49% annualized – enough to move the year over year rate down slightly to 1.96% albeit still close enough to target. Meanwhile the October advance goods trade deficit was confirmed as widening to $77.2bn from $76.3bn, and a bit more than expected. Wholesale inventories rose a greater than expected +0.7% mom (vs. +0.4% expected) during October, new home sales fell unexpectedly (-8.9% mom vs. +4.0% expected) and the Richmond Fed manufacturing index slipped 1pt this month to +14.

Looking at the day ahead, much of the focus should be on the various inflation reports. In Germany we’ll get the preliminary November CPI report this afternoon where the consensus expects a small one-tenth decline to +2.3% yoy. Shortly following that we get the October PCE report in the US where the expectation is also for a modest one-tenth decline to +1.9% yoy. Alongside that data we’ll also get October personal income and spending reports in the US, followed later on by the latest weekly initial jobless claims reading, October pending home sales and the November FOMC minutes. Also due out in Europe is Q3 GDP in France, October money and credit aggregates data in the UK and November confidence indicators for the Euro Area. A busy week for central bank speak rolls on with Guindos and Angeloni speaking on behalf of the ECB, while over at the Fed Mester, Evans, Harker, Kashkari, Kaplan and Rosengren are all participating in a Boston Fed Conference on “Collaboration for Inclusive Economic Development”. Also due today is a 5y and 10y BTP auction which will be worth watching in light of recent weak retail BTP demand. Finally, G-20 finance ministers will attend a working dinner in Buenos Aires tonight before the main event kicks off tomorrow

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 34.29 POINTS OR 1.32% //Hang Sang CLOSED DOWN 231.53 POINTS OR 0.87% //The Nikkei closed UP 85.38 OR 0.39%/ Australia’s all ordinaires CLOSED UP .64% /Chinese yuan (ONSHORE) closed DOWN at 6.9439 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil DOWN to 50.93 dollars per barrel for WTI and 57.87 for Brent. Stocks inEurope OPENED GREEN EXCEPT SPAIN//. ONSHORE YUAN CLOSED UP AT 6.9439AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9375: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

Your most important commentary of the day: Snider comments correctly that dollars outside the USA system (eurodollars) has collapsed in numbers probably due to the USA higher interest rate policy and its huge deficits are sucking in dollars from around the world. That has created problems for our emerging markets and also most importantly China which has needed foreign investments to grease their economy. Now that dollars are leaving, the CNY is falling in value and we now have a risk of citizens moving their dollars (which are hidden) out to Switzerland or other safe havens. This is setting up a huge deflationary problem for the world as the yuan will spike greater than 7.5 or 8.0 to one USA dollars and with that, China will flood with world with cheap goods and this will idle European and other shops as they simple could not compete.

a must read..

(courtesy Snider/Alhambra Partners)

“They Warned Us” – We Haven’t Seen Anything Like This Since The

Darkest Days Of 2015/16

Authored by Jeffrey Snider via Alhambra Investment Partners,

We can add this to the list of all the things going wrong in October. If it felt like a wave of renewed deflation built up and swept over markets and the global economy, it’s because that’s just what had happened. I don’t think it random coincidence the WTI curve went contango and oil prices globally crashed when they did. Golden Weeks in China are always interesting, especially on the reopen.

There are two facts as they pertain to China in 2018. The first is the nation’s clear monetary trouble. The second is why it has (re)emerged.

The statistics for the first part were pretty grim last month, accounting for much of why October was such a major global mess. The People’s Bank of China has been forced into cutting back on monetary growth in base measures all year. This all changed in January, the same time the global economy began to come crashing back down from its low-level reflation in 2017.

Without foreign assets, eurodollars, flowing onto its balance sheet on the asset side the central bank can only restrict growth on the money (liability) side. Factoring the cash needs for the central government, the result has been an increasing squeeze on the RMB base. This includes, ominously, actual cash in circulation.

In October, currency issue expanded by just 2.6% year-over-year. That brings the 6-month average down to 2.7%, which is the lowest average (not counting New Year January/February distortions) in all of the published PBOC data. They’ve just about turned off the literal printing press in China.