GOLD: $1220.70 DOWN $4.00 (COMEX TO COMEX CLOSINGS)

Silver: $14.16 DOWN 17 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1222.40

silver: $14.19

For comex gold and silver:

DEC

NUMBER OF NOTICES FILED TODAY FOR DEC CONTRACT: 2083 NOTICE(S) FOR 208300 OZ

Total number of notices filed so far for DEC: 219 for 208,300 OZ (6.479 TONNES)

FOR NOVEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1463 NOTICE(S) FILED TODAY FOR 7,315000 OZ/

Total number of notices filed so far this month: 1463 for 7,315,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4327: DOWN 272

Bitcoin: FINAL EVENING TRADE: $4327 down $272

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A STRONG SIZED 5559 CONTRACTS FROM 190,258 DOWN TO 184,699 DESPITE YESTERDAY’S TINY 2 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1677 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1677 CONTRACTS. WITH THE TRANSFER OF 1677 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1677 EFP CONTRACTS TRANSLATES INTO 8.385 MILLION OZ ACCOMPANYING:

1.THE 2 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

, FOR AUGUST: 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

NOW 17.355 INITIALLY STAND FOR DECEMBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF NOV: 49,435 CONTRACTS (FOR 21 TRADING DAYS TOTAL 49,435 CONTRACTS) OR 247.18 MILLION OZ: (AVERAGE PER DAY: 2354 CONTRACTS OR 11.77 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF NOV: 247.18 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 35.28% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,676.90 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

ACCUMULATION FOR NOVEMBER /2018: 247.18 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5559 DESPITE THE TINY 2 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A VERY GOOD SIZED EFP ISSUANCE OF 1677 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A HUGE SIZED: 3882 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1677 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 5559 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 2 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.33 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .9240 BILLION OZ TO BE EXACT or 132% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DEC MONTH/ THEY FILED AT THE COMEX: 1463 NOTICE(S) FOR 7,315000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./AND NOW DEC. AT 17.535 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY AN ATMOSPHERIC SIZED 27,963 CONTRACTS DOWN TO 390,899 DESPITE THE GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $1.30//.YESTERDAY’S TRADING) AS THESE GUYS JOINED SILVER IN THE ROUTINE MIGRATION OVER TO ETF’S AS WE APPROACH AN ACTIVE DELIVERY MONTH.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN ATMOSPHERIC SIZED 16,141 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 16,141 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 390,899. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,822 CONTRACTS: 27,963 OI CONTRACTS DECREASED AT THE COMEX AND 16,141 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS: 11,822 CONTRACTS OR 1,182,200 OZ = 36.77 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.30

YESTERDAY, WE HAD 14521 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV : 179,955 CONTRACTS OR 17,775,500 OZ OR 552.88 TONNES (21 TRADING DAYS AND THUS AVERAGING: 8569 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY IN TONNES: 552.88 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 552.88/2550 x 100% TONNES = 21.68% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,764.39 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018: 552.88 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED DECREASE IN OI AT THE COMEX OF 27,963 DESPITE THE GAIN IN PRICING ($1.30) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 16,141 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 16,141 EFP CONTRACTS ISSUED, WE HAD A HUGE LOSS OF 10,708 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

16,141 CONTRACTS MOVE TO LONDON AND 27,963 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 36.77 TONNES). ..AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A GAIN OF $1.30 IN YESTERDAY’S TRADING AT THE COMEX

we had: 2083 notice(s) filed upon for 208,300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.00 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD/

/GLD INVENTORY 761.74 TONNES

Inventory rests tonight: 761.74 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 17 CENTS TODAY

A BIG CHANGES IN SILVER INVENTORY AT THE SLV

A WITHDRAWAL OF 1.22 MILLION OZ FROM THE SLV

/INVENTORY RESTS AT 321.686 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A GIGANTIC 5559 CONTRACTS from 190,258 DOWN TO 184,699 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1677 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1677 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 5413 CONTRACTS TO THE 1677 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE NET LOSS OF 3882 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 19.41 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. AND NOW 17.705 MILLION OZ STANDING IN DECEMBER.

RESULT: A HUGE DECREASE IN SILVER OI AT THE COMEX DESPITE THE 2 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 1677 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 20.75 POINTS OR 0.81% //Hang Sang CLOSED UP 55.72 POINTS OR 0.21% //The Nikkei closed UP 88.46 OR 0.40%/ Australia’s all ordinaires CLOSED DOWN 1.48% /Chinese yuan (ONSHORE) closed DOWN at 6.9465 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil DOWN to 50.58 dollars per barrel for WTI and 58.11 for Brent. Stocks inEurope OPENED RED//. ONSHORE YUAN CLOSED UP AT 6.9465AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9407: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)China’s economy is falling apart. The all important PMI (manufacturing and service) falls to exactly 50.00 which means it is basically in contraction. Remember that China is the engine for global growth. What China is telling us is that the global economy has been faltering for the past few months

( zerohedge)

4/EUROPEAN AFFAIRS

i)GREAT BRITAIN/EU

An excellent article explaining to us the ins and outs of the upcoming vote in the uK parliament on Brexit. The best scenario will be for May to cancel the debate and tell the EU they need a better deal as the one before the table is awful

(courtesy Macleod/GoldMoney.com)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Russia/UKRAINE

The situation between Russian and the Ukraine is getting worse by the minute. It is good that Putin is showing restraint. The Ukraine bans Russian men from the country but Russia will not reciprocate

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

Russia is comfortable with prices at 50 dollars or below but not the USA as the huge junk debt of oil drillers will certainly weigh on them

( zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)GE tumbling again and close to its previous low of $6.66

(courtesy zerohedge)

b)Snyder points out 3 things which happened just before the 2008 crisis is happening now

( Michael Snyder)

d)A powerful 7.2 earthquake whacks Anchorage Alaska( zerohedge)

e)A good one from Peter Tchir of Academy Securities as to what to expect with tomorrows showdown with Xi

f)You will recall that all of the upper echelon of Goldman Sachs participated in the fraud that caused Malaysia to lose considerable dollars in a fraud. We now have a former Dept of Justice official who accepted bribes from Low, one of the key architects of the scam who worked diligently close to our Goldman Sachs former CEO Blankfein and others..this may bring down Goldman Sachs..

iv)SWAMP STORIES

Let us head over to the comex:

We are now in the non active delivery month of DECEMBER and here we now have 3507 notices INITIALLY standing for silver.

Thus by definition: the initial amount of silver standing IN DECEMBER is as follows:

3507 notices x 5000 oz per contract = 17.535 million oz. (last yr initial standing 19.47 million oz)

After December we have the non active January contract month and here we saw a GAIN of 51 contracts up to 1988 contracts. March, the next big delivery month after December saw a gain of 8929 contracts up to 150,360

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

i) Into Brinks: 823170.240 oz

Ireland’s Mr Gold Reveals Nuggets Of Wisdom For When The Next Crash Comes

Ireland’s Mr Gold Reveals Nuggets Of Wisdom For When The Next Crash Comes

Editors note: I am not sure what to make of being called “Ireland’s Mr Gold” but I suppose you could be called worse. For me, my fellow founder Stephen and our excellent team, it has never been about gold itself, but rather it has been about the benefit that gold provides to our clients, their families, their companies and the wider society.

This benefit is not just in terms of hedging, financial insurance and owning a proven safe haven asset but also in terms of the peace of mind that gold provides those who hold it in the safest ways possible.

Credit: Associated Newspapers (Ireland) Limited, t/a dmg Media Ireland

Our mission statement since 2003 has been ‘To protect and grow our client’s wealth with the provision of physical gold in the safest ways possible.’ With 16,000 clients in 140 countries, many of whom store gold with us in some of the safest vaults in the world, I am happy that we have achieved that.

Simply put, physical gold is about financial freedom and financial security in an uncertain world.

In the volatile world of today, gold has never been more important. Investors and pension owners who re-balance portfolios in the coming days and weeks will be handsomely rewarded in 2019 and in the coming years. They will sleep better at night too and not be worried about the latest Brexit shenanigans or Trump tweet!

Mark O’Byrne is Ireland’s Mr Gold. The founder of GoldCore has just launched a gold storage facility in Dublin, where he says we should all stock up on gold bars to help survive a looming economic meltdown.

Not everyone is listening but he’s not surprised – they didn’t the last time either.

Why buy gold?

The wise old Wall Street adage was that one should have 10% of one’s wealth in physical gold and hope that it does not work.

The implication is that if gold rises sharply in price, it usually means that stocks, bonds, property, and indeed one’s business may be losing value.

This was seen in the last crisis and has been seen throughout history.

Are we really heading for economic meltdown?

We may be. More likely is another financial crisis akin to the one seen on 2007 to 2012, and that was pretty brutal. We believe geopolitical risks, including the risks of cyber terrorism, terrorism and war, are underestimated by investors.

Do you ever feel like the apocryphal guy with the placard saying ‘The end is nigh’ who gets taken for granted?

A small bit. It can be a lonely place and it does not make you popular, especially in some of the media who have a strong ‘economic recovery’ narrative. I was early calling the global financial crisis as we were warning subscribers and clients in 2005 about the coming banking and property crisis.

However, we are not Armageddonists and do not believe the end of the world is nigh. Otherwise, we would be selling canned beans and nuclear bunkers!

How has gold been doing lately? It is down about 1.6% in euro terms this year but has actually done reasonably well since 2014, despite the surge in stock and bond markets.

Editors Note: We are bearish on gold in the short term but bullish on it’s prospects in Q1, 2019. The set up for gold is getting better and better, particularly due to the uncertain economic outlook and gold looks set for a strong 2019.

You advocate buying real gold. But how much does it cost to store?

Our average lump sum investment is €30,000 and that would cost 1% per annum to store in ultra-secure, institutional-grade vaults.

Can investors visit their gold – maybe stroke it, while cackling fiendishly about the looming economic Armageddon that will make them a fortune?

Ha! They cannot do this in the Dublin vaults due to security requirements but they can in our Zurich vaults, which remain our most popular storage location.

Gold is a diversification – a hedge and financial insurance. Actually, they hope the price does not [shoot upwards] as if it does it generally means the rest of their investments – their pensions, savings, bank deposits etc – will likely have fallen in value.

What about yourself? Are you a spender or a saver?

I’m a saver but I allow myself to spend on good food, holidays and family.

Are you into bling?

Not a big fan of jewellery at all: most of it is a rip-off as the mark-ups are massive (200% to 400%) and there is VAT on jewellery. This is in marked contrast to gold bars, which can be bought for 3%+ (premium) and no VAT in the UK and EU due to the EU Gold Directive.

Are you wearing any gold jewellery at all?

My wedding ring is a silver ring that I really liked and picked out and my wife bought me it in a gift store in Dingle. It cost €40 but has some interesting insignia symbolising the history of Ireland.

Best/worst investments?

Best investment is in ongoing education and personal development including a recent course with Dr Joe Dispenza.

Health is wealth!

Favourite film?

(Apart from Goldfinger!) True Romance! Love the song in that movie too.

How did it go for you in the financial crash?

As we expected, it went well. Irish people began investing in gold for the first time and we were very busy with that and with UK and international clients.

How do you buy stuff? Cash? Credit card? Gold sovereigns?

I am DIVERSIFIED. Cash, credit cards and a ‘real gold’ card, which I can use to buy things with actual gold stored in a vault in Zurich. With gold at €1,070 per oz, three pints costs 0.0015 of an ounce of gold.

Three things you’d do as finance minister?

1. Repatriate whatever Irish national gold reserves we still have and mandate that 10% of the national pension fund be allocated to gold and that it be stored in institutional grade vaults in Ireland.

2. Introduce a flat income tax of about 25% and increase taxes on consumption (especially on luxuries like jewellery, shoes, handbags, sports cars etc).

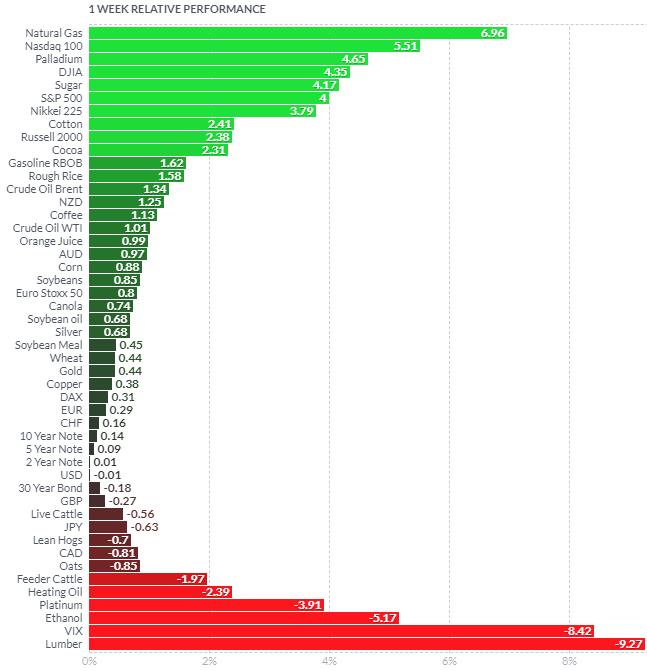

Gold and silver traded sideways this week as stock markets saw what appears to be a short covering rally and a “dead cat bounce.”

Of note was natural gas surging again and lumber collapsing nearly 10% in the week due to concerns about the US housing market …

Source: Finviz.com

Source: Finviz.com

News and Commentary

Gold prices flat ahead of Trump-Xi meet at G20 summit (Reuters.com)

U.S. pending home sales drop in October (Reuters.com)

US weekly jobless claims rise to 6-month high (CNBC.com)

Deutsche Bank Raided in Laundering Probe Going Into 2018 (Bloomberg.com)

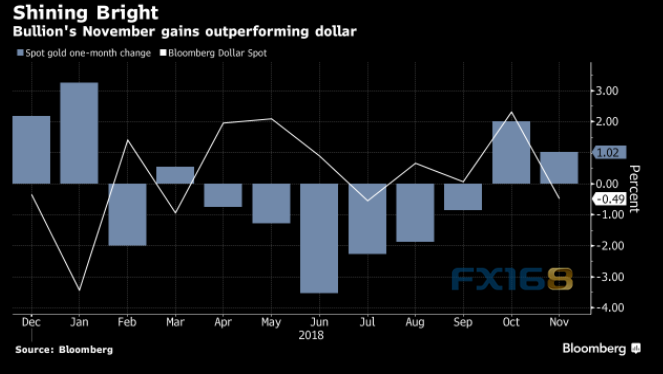

Gold’s set up is getting better and better and it looks set for a strong 2019 (Finance.com)

Source: Bloomberg

What is the optimal weight for gold in a portfolio? (Papers.com)

The $15 Billion Money Pit Dragging GE Down (Bloomberg.com)

The Cost Of Insurance Is About To Jump (DollarCollapse.com)

Refusals to answer should be enough to settle the gold-rigging issue (GATA.org)

Bubbles and Hot Potatoes – Hussman (HussmanFunds.com)

Key passages from the Fed minutes (MarketWatch.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

29 Nov: USD 1,226.25, GBP 960.03 & EUR 1,077.87 per ounce

28 Nov: USD 1,213.20, GBP 949.69 & EUR 1,074.77 per ounce

27 Nov: USD 1,225.05, GBP 959.70 & EUR 1,082.21 per ounce

26 Nov: USD 1,226.65, GBP 954.58 & EUR 1,079.33 per ounce

23 Nov: USD 1,222.15, GBP 951.69 & EUR 1,075.13 per ounce

22 Nov: USD 1,228.25, GBP 950.42 & EUR 1,074.72 per ounce

21 Nov: USD 1,224.00, GBP 957.29 & EUR 1,075.04 per ounce

Silver Prices (LBMA)

29 Nov: USD 14.26, GBP 11.17 & EUR 12.55 per ounce

28 Nov: USD 14.15, GBP 11.06 & EUR 12.54 per ounce

27 Nov: USD 14.28, GBP 11.20 & EUR 12.61 per ounce

26 Nov: USD 14.38, GBP 11.18 & EUR 12.65 per ounce

23 Nov: USD 14.26, GBP 11.12 & EUR 12.56 per ounce

22 Nov: USD 14.52, GBP 11.26 & EUR 12.72 per ounce

21 Nov: USD 14.42, GBP 11.26 & EUR 12.65 per ounce

Recent Market Updates

– BREXIT May Lead to UK Property Crash and Depression

– General Motors And General Electric Highlight The Ponzi Scheme That Is The US Economy

– A Worldwide Debt Default Is A Real Possibility

– Risk of Lower Lows in Gold Remains Prior to Spectacular Rally to Follow

– Gold and Silver Hold Firm as Stocks and Oil Lower in to US Holiday Weekend

– Is Brexit a Massive Threat to Globalisation?

– Stock Markets Remains Extremely Overvalued – Hussman

– Stocks are Now in ‘Complete Bitcoin Territory,’ Asset Manager Says

– Brexit’s Safe Haven Is a Dangerous Place

– Gold and Silver Rise As Stocks Fall On Valuation Concerns, Italy and Brexit Risks

– Pound Falls 2.5% Against Gold as UK Government in Turmoil Over Brexit

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

__

end

________________________________________

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.9465/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER NOW ON //OFFSHORE YUAN: 6.9407 /shanghai bourse CLOSED UP 20.75 POINTS OR 0.81%

. HANG SANG CLOSED UP 55.72 POINTS OR 0.21%

2. Nikkei closed UP 88.46 POINTS OR 0.40%

3. Europe stocks OPENED ALL RED

/USA dollar index RISES TO 96.96/Euro FALLS TO 1.1366

3b Japan 10 year bond yield: RISES TO. +.09/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.52/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 50.58 and Brent: 59.11

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.31%/Italian 10 yr bond yield DOWN to 3.20% /SPAIN 10 YR BOND YIELD UP TO 1.51%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.89: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.27

3k Gold at $1222.10 silver at:14.25 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 60/100 in roubles/dollar) 66.86

3m oil into the 50 dollar handle for WTI and 59 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.52DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9979 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1314 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.31%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.01% early this morning. Thirty year rate at 3.31%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.1702

Nervous Traders Drag US Futures, World Stocks Lower

Ahead Of G-20

US equity futures, European and Asian stocks all dropped as nervous investors looked ahead skeptically to a much anticipated meeting between the American and Chinese presidents that could decide the course of the trade war. US Treasury yields dropped and the dollar gained amid a flutter of risk-off sentiment across the globe.

The G20 Summit kicks off today in Buenos Aires, and while the main event will be the Trump-Xi “dinner of the decade” on Saturday, headline risk is high for the entire event. Market participants have every reason to be nervous: heading into the meeting neither side has expressed a willingness to make concession, making the outcome highly uncertain.

Ahead of his Saturday meeting with Xi, Trump said Thursday he’s very close to “doing something” with China as officials work on the contours of a deal that may delay ramping up tariffs on the Asian country in January. Any sign of a trade truce could take the edge off a rampant greenback and boost risk assets including emerging-market currencies and stocks. Goldman Sachs, however, said an escalation of tensions is the most likely outcome. Citi agrees and notes that even a positive statement will likely be faded promptly by markets because as Citi notes, “any material break in the trade war impasse is difficult to achieve, and so any positive response on Monday may ultimately be short-lived.”

US equity futures were down 0.5%, following weakness in Europe where the Stoxx Europe 600 Index dropped to session lows, falling as much as 0.6% and trimming its weekly gains following a raft of disappointing macro data. Revised data showed Italy’s economy contracted 0.1% q/q in 3Q; German Oct. adjusted retail sales dropped -0.3% m/m; missing estimates of +0.4%. Euro-area inflation slipped to 2% in November from a year earlier, matching estimates, while the core reading unexpectedly dropped to 1%.

Germany’s DAX (-0.6%) felt the burden of falling auto names after Daimler (-2.7%) was downgraded to sell at HSBC, in turn moving the likes of Volkswagen (-1.1%) and BMW (-1.8%) lower in sympathy. Sector wise, consumer discretionary (weighed by auto names) lags, closely followed by financials as Morgan Stanley downgraded the EU banking sector, while Deutsche bank (-3.0%) shares hit an all time low as the bank feels the brunt of a double whammy from the aforementioned downgrade alongside a second day of raids amid the money laundering probe. Italian PM Conte and Economy Minister Tria are studying cutting the 2019 deficit/GDP target to around 2% in order to reach a deal with the EU; according to a paper.

In the latest Brexit news, UK PM May said Britain will be a more divided country if Parliament votes against her Brexit deal, while she also urged MPs to think about delivering on Brexit vote and answered that she is focused on December 11th vote when asked if she has a plan B if her deal is not approved by Parliament. The number of Conservative MPs who have spoken out against Theresa May’s Brexit deal hit 100 as critics said her two-week charm offensive is failing.

Earlier in the session, Asian stocks traded mixed amid a cautious global risk tone with shares gaining in Tokyo, slipping in Seoul and slumping in Sydney, while rebounding in Shanghai and Hong Kong ahead of the US-China showdown at the G20 and as participants digested disappointing Chinese PMI data. ASX 200 (-1.6%) and Nikkei 225 (+0.4%) initially followed suit to the lacklustre lead from their counterparts stateside with Australia the underperformer on broad weakness in which nearly all sectors declined, while Japanese exporters were hampered by recent flows into the JPY before staging a late recovery. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (+0.8%) were initially indecisive due to trade uncertainty amid a ‘hot and cold’ stance by US President Trump who stated he is close to doing something on trade with China but is unsure if he wants to, while reports noted that White House Trade Adviser and ‘China hawk’ Navarro is back on the guest list for the Trump-Xi dinner tomorrow evening. Furthermore, the latest Chinese PMI data left much to be desired as both Official Manufacturing and Non-Manufacturing PMIs missed expectations with the former at its lowest since June 2016. The indices closed higher on the day, however.

- Chinese Manufacturing PMI (Nov) 50.0 vs. Exp. 50.2 (Prev. 50.2)

- Chinese Non-Manufacturing PMI (Nov) 53.4 vs. Exp. 53.8 (Prev. 53.9)

- Chinese Composite PMI (Nov) 52.8 (Prev. 53.1)

Also overnight, Japan reported the latest inflation data, which was slightly weaker on the margin with Tokyo CPI missing expectations;

- Japanese Tokyo CPI (Nov) Y/Y 0.8% vs. Exp. 1.1% (Prev. 1.5%).

- Japanese Tokyo CPI Ex. Fresh Food (Nov) Y/Y 1.0% vs. Exp. 1.0% (Prev. 1.0%)

The Bank of Korea hiked the 7 Day Repo Rate by 25bps to 1.75% as expected, while it stated that sluggish employment eased somewhat and that exports will sustain favourable movements, but that it sees investments slowing. BoK Governor Lee said the rate decision was not unanimous as 2 board members voted to maintain rates, while Lee also commented that the policy rate is still not at neutral and that he is not worried much about capital outflows due to further Fed rate hikes.

In FX, the dollar rebounded sharply from yesterday’s losses, rising against most G-10 peers in a muted trading session; Treasury yields edged lower while the yen was steady as investors refrained from taking risks ahead of this weekend’s meeting between U.S. President Donald Trump and China’s Xi Jinping. The euro slipped to a day low, holding below the 1.14 handle, after London came into the market. The Norwegian krone crept lower after oil prices resumed their slump, while retail sales contracted in October, missing estimates and unemployment rose in November; DNB finds it likely that Norges Bank will adjust down its rate path in December. The pound remained under pressure, drifting downward as U.K. Prime Minister Theresa May continued efforts to win backers for her Brexit deal. Emerging-market equities and currencies dipped.

Finally, Korea’s won held on to this week’s losses as Friday’s interest rate increase did little to assuage concern surrounding the economy.

WTI crude was dragged back under $51 a barrel, on track for the biggest monthly drop in a decade. The euro weakened after data showed inflation in the common-currency region easing.

Looking at this weekend’s key event, Guggenheim’s Scott Minerd told Bloomberg TV that “I wouldn’t be surprised at the end of this weekend if the U.S. and China didn’t announce a concord that basically sat down a path to help resolve the trade frictions. I don’t think that out of the meeting there’s going to come much substance, but there will be a sort of set of principles that will be established to start the process of bringing an end to the trade war.”

WTI (-1.4%) and Brent (-1.0%) lost the USD 51/bbl and USD 60/bbl handles respectively with sentiment deteriorating as the G20 Summit goes underway, where participants will be looking out for leaks in regard to any potential supply change discussed by key policy makers. Meanwhile, ahead of the Dec 6th OPEC meeting, Russian Energy Ministry stated that OPEC and non-OPEC producers are comfortable with the current oil price, while the country’s Energy Minister Novak said Russia plans to maintain the average oil output level until year-end. Note: yesterday he said Russia proposes an output cut for next year.

In the metals complex, gold (-0.2%) erodes post-Powell gains and remains in the November range of USD 1200-1240/oz as the yellow metal mirrors the rising USD, with traders noting a clean break above the top of the range could result in further bullish action. Copper (-0.3%) trade lower amid the cautious risk tone ahead of the Trump-Xi G20 showdown, with moves to the downside exacerbated by the disappointing Chinese manufacturing PMIs overnight. Elsewhere, Shanghai aluminium prices declined to their lowest level in over two years to print their third consecutive monthly decline amid oversupply fused with downbeat Chinese PMIs

Economic data include MNI Chicago Business Barometer.

Market Snapshot

- S&P 500 futures down 0.4% to 2,734.00

- STOXX Europe 600 down 0.5% to 356.33

- MSCI Asia down 0.2% to 153.44

- MSCI Asia ex Japan down 0.4% to 490.93

- Nikkei up 0.4% to 22,351.06

- Topix up 0.5% to 1,667.45

- Hang Seng Index up 0.2% to 26,506.75

- Shanghai Composite up 0.8% to 2,588.19

- Sensex up 0.05% to 36,186.77

- Australia S&P/ASX 200 down 1.6% to 5,667.16

- Kospi down 0.8% to 2,096.86

- German 10Y yield fell 0.9 bps to 0.312%

- Euro down 0.2% to $1.1374

- Brent Futures down 1.1% to $58.88/bbl

- Italian 10Y yield fell 5.1 bps to 2.837%

- Spanish 10Y yield fell 0.2 bps to 1.506%

- Brent futures down 1.1% to $58.88/bbl

- Gold spot down 0.2% to $1,221.86

- U.S. Dollar Index up 0.2% to 97.00

Top Overnight News

- Federal Reserve officials have stepped off a predictable path of interest-rate increases and are signaling to investors a hard truth about relying on increasingly contradictory economic data: There are no easy answers anymore.

- Waning year-end demand for the U.S. currency is leading to a decline in dollar-funding costs for Japanese and European investors

- Gold may be turning the corner as prices head for the first back-to-back monthly gain since January, holdings in exchange-traded funds expand, and investors reappraise the metal’s prospects in 2019 amid speculation the Federal Reserve will pause its tightening cycle

- The sequence in which the ECB will take its next policy moves “has pretty much been communicated. It’s more about the timing of the various elements,” Estonian central banker Ardo Hansson says in interview with Financial Times

- The first official reading of China’s economy in November showed the manufacturing PMI on the brink of contraction. New export orders contracted for a sixth month while the non-manufacturing gauge, reflecting activity in the construction and services sectors, expanded but at a slower pace

Asian stocks traded mixed amid a cautious global risk tone ahead of the US-China showdown at the G20 and as participants digested disappointing Chinese PMI data. ASX 200 (-1.6%) and Nikkei 225 (+0.4%) initially followed suit to the lacklustre lead from their counterparts stateside with Australia the underperformer on broad weakness in which nearly all sectors declined, while Japanese exporters were hampered by recent flows into the JPY before staging a late recovery. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (+0.8%) were initially indecisive due to trade uncertainty amid a ‘hot and cold’ stance by US President Trump who stated he is close to doing something on trade with China but is unsure if he wants to, while reports noted that White House Trade Adviser and ‘China hawk’ Navarro is back on the guest list for the Trump-Xi dinner tomorrow evening. Furthermore, the latest Chinese PMI data left much to be desired as both Official Manufacturing and Non-Manufacturing PMIs missed expectations with the former at its lowest since June 2016. The indices closed higher on the day, however. Finally, 10yr JGB traded lacklustre after having failed to benefit from the risk averse tone in Japan and BoJ’s presence in the bond market, as prices marginally pulled back from recent gains which had seen long-term yields hit their lowest levels since the beginning of August.

Top Asian News

- China’s Worsening Economy Adds Pressure on Xi Heading to G-20

- BOJ Governor Kuroda’s Latest Pay Raise Falls Short

- Meitu Sinks on Concern Data Privacy Warning Will Worsen Losses

- Evergrande Leads China Developer Rally; Rhb Cites Policy Hopes

Major European indices are lower across the board (Eurostoxx 50 -0.3%) after the region gave up opening gains amid trade jitters heading the US-Sino showdown at the G20 Summit. UK’s FTSE 100 (-0.7%) underperforms peers as heavyweight miners are pressured by the price action in the base metals complex, while Germany’s DAX (-0.6%) feels the burden of falling auto names after Daimler (-2.7%) was downgraded to sell at HSBC, in turn moving the likes of Volkswagen (-1.1%) and BMW (-1.8%) lower in sympathy. Sector wise, consumer discretionary (weighed by auto names) lags, closely followed by financials as Morgan Stanley downgraded the EU banking sector, while Deutsche bank (-3.0%) shares hit an all time low as the bank feels the brunt of a double whammy from the aforementioned downgrade alongside a second day of raids amid the money laundering probe. In terms of stock specifics, Altice (+8.0%) rose to the top of the Stoxx 600 (-0.5%) after the company sold its 49.9% stake in SFR GTTH for EUR 1.8bln, while Faurecia (-7.1%) is the worst performer in Europe amid a downgrade.

Top European News

- Bayer Gains as Analysts Applaud Surprise Measures: Street Wrap

- The London Housing Market Is Worse Than It Looks. Here’s Why

- Italian Jobless Rate Jumps With More Reentering Labor Market

- SocGen Seeks to Tap African Growth and Shrug Off Europe Woes

- Europe Auto Stocks Drop as China, Trade Prompt PT Cuts at HSBC

In FX, the Greenback remains off pre-Powell highs in wake of the latest FOMC minutes that effectively affirm a shift in the approach towards forward guidance that may start in December after a final rate hike this year, with less pre-set indications and more flexibility to take on board incoming data. However, the Buck is ahead vs all G10 counterparts bar the Kiwi that is benefiting from favourable cross-winds, with the index edging just over 97.000 again. EUR – The single currency has been more volatile than most ahead of the looming G20 Summit and month end, with more spikes vs the Pound through 0.8900 around fixes due to ongoing/residual RHS interest, but another failure at 1.1400 vs the Usd on round number offers and option expiry flows as circa 1.6 bn roll off between the big figure and 1.1410 at the NY cut. Moreover, some Usd12.6 bn SOMA-related Dollar demand coincides with the final trading day of November, and this usually weighs most heavily on Eur/Usd vs potential bids at 1.1350 where another 1.6bn expiries reside. AUD/CAD – Also underperforming vs the Greenback, with the Aud bearing the brunt of a weaker than forecast Chinese manufacturing PMI overnight ahead of the Trump-Xi meeting on Saturday, and struggling top keep hold of 0.7300 as the Aud/Nzd cross pivots 1.0650 and the Kiwi remains within striking distance of its 200 DMA (0.6870). Meanwhile, the Loonie is back below 1.3300 as crude prices resume their slide amidst reports from Russia suggesting that OPEC+ are content with current levels, which have also piled more pressure on the Rub for obvious reasons.

In commodities, WTI (-1.4%) and Brent (-1.0%) lost the USD 51/bbl and USD 60/bbl handles respectively with sentiment deteriorating as the G20 Summit goes underway, where participants will be looking out for leaks in regard to any potential supply change discussed by key policy makers. Meanwhile, ahead of the Dec 6th OPEC meeting, Russian Energy Ministry stated that OPEC and non-OPEC producers are comfortable with the current oil price, while the country’s Energy Minister Novak said Russia plans to maintain the average oil output level until year-end. Note: yesterday he said Russia proposes an output cut for next year. In the metals complex, gold (-0.2%) erodes post-Powell gains and remains in the November range of USD 1200-1240/oz as the yellow metal mirrors the rising USD, with traders noting a clean break above the top of the range could result in further bullish action. Copper (-0.3%) trade lower amid the cautious risk tone ahead of the Trump-Xi G20 showdown, with moves to the downside exacerbated by the disappointing Chinese manufacturing PMIs overnight. Elsewhere, Shanghai aluminium prices declined to their lowest level in over two years to print their third consecutive monthly decline amid oversupply fused with downbeat Chinese PMIs.

US Event Calendar

- 9am: Fed’s Williams Speaks on Global Economy at G30 in New York

- 9:45am: Chicago Purchasing Manager, est. 58.5, prior 58.4

DB’s Jim Reid concludes the overnight wrap

As I peer into the distance toward s snow-covered mountain tops, the last day of November is now upon us and all of a sudden we’re into the final countdown to year-end, my Xmas ski trip, and thus the likelihood of getting reacquainted with my knee surgeon sometime early next year. We noted at the start of this week that there are still a few big events for markets to get past before we can call it a year and the first of those starts today and continues into the weekend with the G20 meeting in Buenos Aires. The G20 overall is a sideshow to the main event, which is the meeting between US President Trump and Chinese President Xi Jingping. Will the two leaders strike a truce and thus a grand bargain on trade or will talks hit another snag? It would take a brave man to predict the outcome and it does feel like messages have been fairly mixed in recent days despite some optimism from the US side, especially from Trump’s economic advisor Kudlow, that a deal can be made. Yesterday, the Wall Street Journal reported that the two sides are approaching a deal, possibly to include suspension of any new US tariffs through next spring in exchange for discussions and the lifting of restrictions on US agriculture and energy exports. On the other hand, the President told the very same newspaper earlier this week that it is “highly unlikely” that the next tranche of tariffs, set to take effect on Jan 1, will be delayed. Yesterday’s Reuters headline quoting Trump as saying that he is “close to doing something with China, but he doesn’t know if he wants to do it” perhaps sums up the state of play nicely. Interestingly, the South China Morning Post reported that the White House trade policy adviser, Peter Navarro – who is a known China hawk – is now scheduled to attend the dinner between Trump and Xi having initially been left out. US Trade Representative Lighthizer is still due to attend.

So all to play for and something for everyone in the pre-show headlines. As for timing, the meeting between Trump and Xi is due to take place Saturday evening at some point over dinner, however the exact timing is uncertain. Another potentially interesting meeting on the agenda was that between Trump and Russian President Putin. However, after the Kremlin confirmed yesterday that the meeting was to go ahead tomorrow, President Trump instead said that he had cancelled the meeting, tweeting yesterday that his decision was “based on the fact that the ships and sailors have not been returned to Ukraine from Russia”.

In any case, the tensions between Russia and the Ukraine should also be a focal point along with the trade war, while the presence of the Saudi Crown Prince could also be another talking point. The event has no shortage of AListers however with Japan’s Abe, Germany’s Merkel, France’s Macron, UK’s May, EC’s Juncker, EU’s Tusk, Italy’s Conte, and Turkey’s Erdogan among the leaders attending so there’s the potential for plenty of newsflow this weekend.

As for markets, well the strong three-day winning run for US equities came to an end last night with the S&P 500 (-0.22%), DOW (-0.11%) and NASDAQ (-0.25%) all finishing slightly in the red. As has been the trend recently, tech led the decliners with the NYSE FANG index down -1.13% with Apple (-0.77%) down for the sixth time in the last eight sessions. It was hard to know if the slight riskoff was some pessimism ahead of the G20 or reaction to the news that Trump’s former lawyer Michael Cohen had pleaded guilty to a new federal charge and also agreed to cooperate with Robert Mueller. Prior to this, Europe had opened strongly, benefiting from the dovish Powell halo effect, though ultimately the moves faded. The STOXX 600 pared gains of as much as +0.75% to close +0.20% and the DAX erased gains of +0.93% to close flat.

This morning in Asia markets are off to a mixed start with the Nikkei (+0.33%), Hang Seng (+0.69%) and Shanghai Comp (+0.23%) all up while the Kospi (-0.26%) is down. In terms of overnight data, China’s official November composite PMI continued to soften at 52.8 (vs. 53.1 last month) as both manufacturing (50.0 vs. 50.2 expected) and non-manufacturing PMIs (at 53.4 vs. 53.8 expected) missed expectations. In the details of the manufacturing PMI, new export orders (at 47.0) printed below 50 for the 6th month in a row with new orders also continuing to soften sequentially with the current reading at 50.4 (vs. 50.8 in last month and 53.8 back in May). Japan’s preliminary October industrial production stood at +2.9% mom (vs. +1.2% mom expected) – the highest since January 2015.

Elsewhere, futures on S&P 500 (-0.17%) are pointing towards a slightly softer start. The BoJ is also set to release its monthly bond-buying plan for December at 5:00 pm Tokyo time (8:00 am BST) today which is likely to be closely watched for any possible tweaks as the BoJ tries to boost trading in JGBs. The minutes from the November FOMC meeting were released yesterday evening, but didn’t change the debate much, especially when compared to the market-moving comments from Chair Powell earlier this week. The minutes said that many Committee members may want to change the “further gradual increases” language in the policy statement to something that “places greater emphasis on the evaluation of incoming data.” This confirms the renewed emphasis on data dependency that Powell and Clarida pushed this week. The minutes also signaled that a technical adjustment to the rate setting framework would likely be needed at the December meeting, i.e. raising the IOER rate only 20bps rather than the full 25bps in order to keep the effective federal funds rate near the middle of the target range.

There were several notable landmarks in markets elsewhere yesterday. The first was the 10-year Treasury briefly passing below 3% – touching an intraday low of 2.995% – for first time since September 18th and WTI oil passing below $50 – hitting a low of $49.41 – for the first time since October 9th last year. To be fair both rebounded off the lows. Ten-year Treasuries ended the day at 3.026% (still down -3.3bps on the day) while WTI made a full reversal to finish the session back above $51 (+2.11%), which is roughly where it’s trading this morning. That rebound appeared to be helped by a Reuters report suggesting that both Russia and Saudi Arabia were discussing the details behind a cut in production.

The rally for Treasuries was given an added boost by yesterday’s data in the US. The highlight was the soft core PCE print for October (+0.1024% vs. +0.2% expected) which resulted in the annual rate falling by one-tenth from an already downwardly-revised +1.94% yoy to +1.77% yoy, the lowest since February. On the back of a dovish Powell on Wednesday, that data was perhaps more fuel to the fire for the dovish camp and could drive more talk of a pause in the Fed’s tightening cycle. It’s worth noting that the healthcare component of the data was soft and that there could be some seasonality in this data so that is something to keep in mind.

The other interesting data point in the US yesterday was the weekly initial jobless claims print, which jumped 10k to 234k (vs. 220k expected) and the highest in six months. The four-week moving average is now at 223k and the highest since July. There was some talk that the Thanksgiving Holiday may have had an impact on the data, however a persistent uptick in the jobless claims data would definitely be food for thought looking ahead. So worth setting a calendar reminder for this print over the next two Thursdays after a long period where the number has been no more than a mild distraction to lunch or breakfast depending on where you are in the world.

Over in Italy, the Government and the European Commission continued to trade barbs, with Conte saying that they “are not indifferent to the reaction of financial markets [but] we can’t back away from the core promises we made to Italians.” There still seems to be movement toward a budget deficit of 2.2% of GDP rather than 2.4%, but Commission VP Dombrovskis said that would be an insufficient cut. Italian Deputy Premier Salvini said that the Italian government is not considering lowering the budget deficit below 2.2% while adding that “if there is a saving we won’t leave the money there unspent, we will invest it for other spending.” Still, the Italian press reported that the EU could give Italy more time before instigating the Excessive Deficit Procedure, i.e. delaying the decision till February 2019. This helped BTPs rally -5.2bps despite tepid demand as the Treasury auctioned 4.25 billion euros of debt across the 10- and 5-year tenors.

On Brexit, we didn’t get a lot of new information yesterday but the pound nevertheless traded -0.35% weaker versus the dollar. EU Chief Negotiator Barnier said that discussions are over and that the current Withdrawal Agreement is the only possible Brexit deal. DUP Leader Foster reiterated her opposition to the deal, saying that there exists a better option. It’s hard to square those two views, which explains where there is so much uncertainty ahead of next month’s Parliamentary vote. Interesting it looks like we’ll have a live televised debate with May Vs Corbyn on primetime TV on Sunday 9th December. The problem is that May has agreed to have it on the BBC whereas Corbyn is leaning towards ITV as he didn’t want it to clash with the finale of “I’m a celebrity get me out of here”. It rather sums up the process at the moment. Overnight, on her way to the G-20 summit, UK PM May said that national divisions over Brexit will widen if lawmakers fail to back her plans in the parliamentary vote next month while adding that there are no alternatives to her current deal as she ruled out another referendum and said Britain won’t be in a Customs Union with the EU and dismissed the Norway option. She also reiterated that she won’t resign in the event of her Brexit deal getting rejected by the UK Parliament.

Coming back to inflation, there was also some disappointment in the German HICP reading which came in at a below market +0.1% mom (vs. +0.2% expected) – and so pushing the annual rate down two tenths to +2.2% yoy. A reminder that we get the broader Euro Area reading today in addition to country level reports from France and Italy.

Apart from the inflation and jobless claims prints, the US also released personal income and personal spending data, which both surprised to the upside and supported the narrative of continued labour market strength for now. Income rose +0.5% mom, the fastest pace since January, while spending rose +0.6%, fastest since March. The housing market continued to show signs of slowing, as home sales fell -2.6% mom, their sixth consecutive decline. That’s the longest such streak since 2014.

In terms of the day ahead, as mentioned at the top the G20 Leaders Summit officially gets underway and continues into the weekend, so expect headlines throughout. As for data, shortly after this hits your emails this morning we’ll get November Nationwide house price data in the UK and October German retail sales numbers. Not long after that we get the preliminary November CPI reading for France before the aforementioned Euro Area reading. In the US the only release scheduled is the November Chicago PMI, which is expected to largely hold steady around October’s level. Away from the data we’re finishing the week with two more ECB speakers, with Mersch and Coeure speaking at separate events. Finally the Fed’s Williams will speak this afternoon on the “Global Economy” at an event in New York.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 20.75 POINTS OR 0.81% //Hang Sang CLOSED UP 55.72 POINTS OR 0.21% //The Nikkei closed UP 88.46 OR 0.40%/ Australia’s all ordinaires CLOSED DOWN 1.48% /Chinese yuan (ONSHORE) closed DOWN at 6.9465 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil DOWN to 50.58 dollars per barrel for WTI and 58.11 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED UP AT 6.9465AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9407: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

China’s economy is falling apart. The all important PMI (manufacturing and service) falls to exactly 50.00 which means it is basically in contraction. Remember that China is the engine for global growth. What China is telling us is that the global economy has been faltering for the past few months

(courtesy zerohedge)

China PMI Plunges To 29-Month Lows, Nears Economic Contraction

Despite stepping up fiscal and monetary support in recent months, China PMI tumbled to 50 in November – right at the cusp of economic contraction – the weakest prints since June 2016.

Against expectations of an unchanged 50.2 print, China Manufacturing PMI fell to 50.0 in November (and non-manufacturing PMI slipped to 53.4 from 53.9).

This weakness comes following a string of measures including personal tax cuts and plans to provide credit support for private firms to obtain equity and bond financing, and confirms early indicators signaling weakening on the external front. Among China’s major trading partners, the U.S. and Euro flash PMIs are expected to come in flat. South Korea’s export growth – a barometer for Asia’s exports – decelerated to 5.7% year on year in the first 20 days of November from 26% during the same period in October.

The Composite PMI is the weakest in at least two years, tracking lower with Eurozone and US in November…

Global synchronized un-recovery?

Miscalculation: China Building More Nuclear Subs Than Pentagon Estimated, Report

Some of America’s most influential think tanks and the Pentagon have likely underestimated the number of Chinese nuclear submarines under construction, a new report suggests.

Satellite imagery of the Bohai Shipyard and Longpo Naval Facility taken by Planet Labs shows that “China does not yet have a credible sea-based deterrent,” Catherine Dill of the James Martin Center for Nonproliferation Studies at the Middlebury Institute of International Studies at Monterey told Defense One. Two of China’s four Jin-class submarines “appear to not be in operation and are undergoing maintenance or repairs at the Bohai shipyard, suggesting to us that credibility is still in question.”

Defense One said that contradicts the US Defense Department’s 2018 China Military Report and the Center for Strategic and International Studies’ (CSIS) report, which had stated that China had four operational Jin-class subs.

The report said there is one additional submarine under construction that the Pentagon missed.

Jeffrey Lewis, a colleague of Dill, discovered that China had one more nuclear submarine in development than previously believed. He observed a total of five submarine hulls in production, three at Longpo and two at the Bohai shipyard, indicating that China’s modernization efforts are ahead of schedule to meeting its goal of eight.

“China is continuing to modernize its nuclear weapons program, broadly,” Dill said. “There’s a big emphasis on the SSBN program because all of their deliverable nuclear weapons are on land-based systems. Expanding into these SSBNs gives China more flexibly and credibility.”

The Bohai Chinese Naval port, displaying two Jin-class subs, taken on Nov. 16, courtesy of Planet Labs

The Bohai Chinese Naval port, displaying two Jin-class subs, taken on Nov. 16, courtesy of Planet Labs The Longpo Chinese naval facility displaying multiple Jin-class subs, take on Nov 16, courtesy of Planet LabsShe added, “These observations would not have been possible without the high cadence of the Planet imagery, which gave us 244 days of exploitable imagery to monitor from July 2017 to November 2018.”

The Longpo Chinese naval facility displaying multiple Jin-class subs, take on Nov 16, courtesy of Planet LabsShe added, “These observations would not have been possible without the high cadence of the Planet imagery, which gave us 244 days of exploitable imagery to monitor from July 2017 to November 2018.”

By comparison, the US nuclear-armed submarine fleet features 14 Ohio-class subs, which are comparable in size to China’s Jin-class sub and Russia’s Borey-class.

Boston College Geopolitical Professor Robert Ross, an expert on Chinese defense and security policy, released a new report entitled “The End of US Naval Dominance in Asia,” it warns that at the current rate of modernization by China, US Navy’s global dominance could be displaced sometime in the mid/late 2020s.

“The rapid rise of the Chinese Navy has challenged US maritime dominance throughout East Asian waters,” Ross writes. “The US, though, has not been able to fund a robust shipbuilding plan that could maintain the regional security order and compete effectively with China’s naval build-up.”

“The resulting transformation of the balance of power has led to fundamental changes in US acquisitions and defense strategy. Nonetheless, the US has yet to come to terms with its diminished influence in East Asia.”

Ross provides documentation that shows China is well on its way to deploying a naval fleet that could rival the US, but increasingly more modern.

Sometime around 2038, roughly two decades from now, China will surpass the US in military spending, and become the world’s dominant superpower not only in population and economic growth – China is set to overtake the US economy by no later than 2032 – but in military strength and global influence as well.

While it might not seem like much when American think tanks and the Pentagon underestimated the number of Chinese nuclear submarines in development, it could otherwise show how unprepared the West is for a rising China.

4.EUROPEAN AFFAIRS

GREAT BRITAIN/EU

An excellent article explaining to us the ins and outs of the upcoming vote in the uK parliament on Brexit. The best scenario will be for May to cancel the debate and tell the EU they need a better deal as the one before the table is awful

(courtesy Macleod/GoldMoney.com)

‘No Deal’ Brexit: Bad For Britain, Catastrophic For EU

Authored by Alasdair Macleod via GoldMoney.com,

The deal has been agreed, subject to Parliament. Mrs May now has the uphill task of selling the deal to MPs. The overwhelming majority who have expressed an opinion including both Remainers and Brexiteers have condemned it. As has President Trump. She will be praying for no further asides from him at the G20 in Buenos Aires.

The vote is scheduled for 11 December, after a five-day debate. The Government’s tactic is to rely on Mrs May’s deal being the only one on offer, the alternative being the supposed abyss of a no-deal. The risk to this strategy is that Brexiteers expose the choice as being false and that Mrs May should go back to Brussels and renegotiate. The EU stands ready to reaffirm they will not accept any other deal to cut off this option.

The Treasury and the Bank of England have cranked up their economic and financial models again to forecast maximum disruption in the event Parliament fails to support Mrs May’s deal. However, in the Commons, the Treasury backed off from its responsibility for its post-Brexit forecasts, saying it was based on analysis involving a wide range of government departments. One is left wondering why the Treasury Secretary felt unable to give it his wholehearted support.

The Bank of England has been less delicate in its approach, by claiming we are all doomed. The result after only one day of airing its forecast is a loss of public credibility for the Bank and particularly for Mark Carney, its Governor.

The frighteners extend to a hodgepodge of claims of many things vital to life and employment, put together by government quangos. Shortages of medicines, transport disruption, chemicals for water purification and many more are all documented in eighty different official papers. The deceit is to assume these supplies are provided at an inter-governmental level, and not by profit-seeking businesses, which would surely do everything in their power to secure continuing sales. The Port of Calais is expected to cut off its nose despite its face and turn away traffic.

This line of propaganda seems to be an irresistible line of attack for the Government, accustomed to frightening the populous into a preferred course of action. This is despite the failure of this tactic ahead of the Brexit referendum, when the public decided it was a stinking rat.

What is the deal, and why the fuss?

Britain leaves the EU on 29 March next year and under Mrs May’s plan enters an implementation period when there is no change in current trade arrangements, until at least 1 January 2020. After that, if the trade agreement is not in place (highly unlikely – it takes years to get the EU to agree to trade deals), Britain can either extend the implementation period for a time, or the backstop on the Irish border will be implemented.

The backstop ensures the Irish border would remain open to EU trade, as it is today, until a trade agreement is finally agreed and implemented. Until then, either the whole of the UK continues to be in the customs union, or Northern Ireland alone remains in it, effectively putting a border down the Irish Sea. The backstop, if it is implemented, can only be turned off “when we have fulfilled our commitments on the Irish Border.”

The agreement states that both the EU and the UK will use best endeavours to reach a trade agreement. But given it can be blocked by EU member countries which are not a party to the agreement, this reassurance must be worthless. Even before the ink was dry, Spain forced concessions on Gibraltar, and President Macron of France made it clear France would withhold its consent to a trade agreement if French fishing vessels were denied fishing rights in British waters.

The problem with the agreement is that by not agreeing, EU member states can ensure, in the words of Boris Johnson, Britain remains a vassal state. Worse than that, with this agreement it is a zombie state, a walking-dead captive of the customs union.

Even the Remainers don’t like it, because it is as plain as a pikestaff that Britain is in a far worse position with this agreement than it would be remaining in the EU. It is chained to the customs union with no influence over the regulations imposed upon it. Accordingly, Remainers of all parties are united in the call for a second referendum, which they hope will reverse the first, allowing Britain to remain as a full member of the EU. But to concede a second referendum would be unprecedented, and also an admission of failure by the government. Furthermore, it would take months to go through Parliament, time which it does not have. With no practical alternative, many prominent Remainers are expected to vote against the agreement.

For the Brexiteers, it is already an admission of failure, particularly since the Prime Minister always refused to consider a Plan B. Britain has agreed unconditionally to pay the EU £39bn as the divorce settlement and will continue to pay into Brussels the annual tribute of roughly £9bn until the new trade terms are agreed and implemented (which could be never). While the agreement generally limits the European Court of Justice’s powers to adjudicate on trade and related matters, it means Britain does not have control over future trade arrangements during implementation and backstop periods, and it will be impossible for Britain to strike her own trade deals until that time has passed. Hence President Trump’s remarks.

We have confirmation it is Hotel California: you can check out but never leave. The deal is so unpopular that already the media are saying it will never get through Parliament. The Daily Telegraphhas aggregated various sources of information to estimate 221 MPs will vote for it and 418 against. But much can change in a short fortnight.

Let us look at it from Downing Street’s point of view, to try to understand the Government’s strategy. 96 Conservative MPs have said they will vote against, out of a parliamentary party of 314 (excluding Speaker Bercow). The Democratic Unionist Party, with ten MPs who provide the Conservatives with their slim Commons majority, have also vowed to vote against it. The Labour Party with 257 MPs have said they will vote against it, but there are perhaps 60 Labour rebels. The Scottish National Party has 35 MPs, who will also vote against it. Liberal Democrats, with 12 are probably against it, but may not be united on the threat of no deal.

That leaves 216 Conservatives likely to support the Government (including 94 Ministers), perhaps 240 after the whips have done their work. 74 MPs from the other parties are then required, at least 60 of which must be Labour MPs. It is worth recalling that 64 Labour MPs defied the Labour whip over an amendment tabled to remain in the customs union last December, close to the number of Labour MPs required to rebel this time for Mrs May to win the vote. And that’s assuming Labour isn’t persuaded to abstain, which would guarantee Mrs May gets it passed by a comfortable margin.

Clearly, the key to success is Labour’s intentions, which is why Downing Street is wooing their MPs. However, two weeks ahead of the vote, talk of a heavy defeat for the government looks, on Downing Street’s likely assessment, wide of the mark.

All this assumes Labour will resist the temptation to topple Mrs May and create havoc for the Tories. That is a big assumption, because it is definitely in Labour’s interest to defeat the government to see what opportunities might arise. Consequently, while the Downing Street assessment may turn out to be too optimistic, the Brexit camp cannot afford to be complacent.

Brexiteer tactics

The Brexiteers will concentrate on mustering as much support as possible to reject the proposed agreement. They already have the ten DUP members on side, and 96 Conservatives who have said they will vote against. They need to work on the other 218 Conservative MPs, of which 94 are ministers, leaving a pool of 124 possible votes.

It would help their case enormously if more Brexit-supporting ministers resigned from the government ahead of the vote, so they are likely to be privately encouraged to do so. This would benefit the Brexit cause by fatally undermining the Government’s claim that the agreement is in the spirit of Brexit.