GOLD: $1233.95 UP $13,25 (COMEX TO COMEX CLOSINGS)

Silver: $14.45 UP 29 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1230.50

silver: $14.38

For comex gold and silver:

DEC

NUMBER OF NOTICES FILED TODAY FOR DEC CONTRACT: 1529 NOTICE(S) FOR 152,900 OZ (4.755 tonnes)

Total number of notices filed so far for DEC: 3612 for 361,200 OZ (11.234 TONNES)

FOR DECEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1050 NOTICE(S) FILED TODAY FOR 5,250,000 OZ/

Total number of notices filed so far this month: 2513 for 12,555,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4144: DOWN 111

Bitcoin: FINAL EVENING TRADE: $4013 down $269

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY SIZED 134 CONTRACTS FROM 184,693 UP TO 184,565 DESPITE FRIDAY’S 17 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1994 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1944 CONTRACTS. WITH THE TRANSFER OF 1944 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1944 EFP CONTRACTS TRANSLATES INTO 9.97 MILLION OZ ACCOMPANYING:

1.THE 17 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

NOW 18.560 INITIALLY STAND FOR DECEMBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DEC: 1994 CONTRACTS (FOR 1 TRADING DAYS TOTAL 1994 CONTRACTS) OR 9.97 MILLION OZ: (AVERAGE PER DAY: 1994 CONTRACTS OR 9.97 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 9.97 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.42% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,686.87 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

ACCUMULATION FOR NOVEMBER /2018: 247.18 MILLION OZ

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 134 DESPITE THE 17 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A VERY GOOD SIZED EFP ISSUANCE OF 1994 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1860 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1994 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 134 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 17 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.16 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .9220 BILLION OZ TO BE EXACT or 131% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DEC MONTH/ THEY FILED AT THE COMEX: 1050 NOTICE(S) FOR 5,250000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./AND NOW DEC. AT 18.560 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY GOOD SIZED 1989 CONTRACTS DOWN TO 388,910 WITH THE LOSS IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $4.00//.YESTERDAY’S TRADING) AS THESE GUYS JOINED SILVER IN THE ROUTINE MIGRATION OVER TO ETF’S AS WE APPROACH AN ACTIVE DELIVERY MONTH.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9038 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 9038 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 388,910. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7049 CONTRACTS: 1989 OI CONTRACTS DECREASED AT THE COMEX AND 9038 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 7049 CONTRACTS OR 704,900 OZ = 21.92 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $4.00

FRIDAY, WE HAD 16141 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC : 9038 CONTRACTS OR 903800 OZ OR 28.11 TONNES (1 TRADING DAYS AND THUS AVERAGING: 9038 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY IN TONNES: 28.11 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 28.11/2550 x 100% TONNES = 1.10% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,792.50 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018: 552.88 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED DECREASE IN OI AT THE COMEX OF 1989 WITH THE LOSS IN PRICING ($4.00) THAT GOLD UNDERTOOK FRIDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9038 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9038 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 6569 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9038 CONTRACTS MOVE TO LONDON AND 1989 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 21.92 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $4.00 IN FRIDAY’S TRADING AT THE COMEX

we had: 1529 notice(s) filed upon for 152,900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $13.25 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD/

/GLD INVENTORY 761.74 TONNES

Inventory rests tonight: 761.74 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 29 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 321.686 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY 134 CONTRACTS from 184693 UP TO 184,565 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1994 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1944 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 134 CONTRACTS TO THE 1994 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1860 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.30 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. AND NOW 17.705 MILLION OZ STANDING IN DECEMBER.

RESULT: A TINY DECREASE IN SILVER OI AT THE COMEX DESPITE THE 17 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// FRIDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 1994 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 66.61 POINTS OR 2.57% //Hang Sang CLOSED UP 675.29 POINTS OR 2.55% //The Nikkei closed UP 223.70 OR 1.00%/ Australia’s all ordinaires CLOSED UP 1.86% /Chinese yuan (ONSHORE) closed UP at 6.8897 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 52.90 dollars per barrel for WTI and 61.41 for Brent. Stocks in Europe OPENED GREEN //. ONSHORE YUAN CLOSED UP AT 6.8897AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8853: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)Markets are expected to roar, Monday but nothing substantive was agreed at the Xi/Trump meeting on Saturday. Basically there is a truce for 90 for 90 days in which trump will not raise tariffs of 200 billion dollars worth of Chinese goods. In return China will buy a huge portion of the autumn harvest of soybeans. The main points from the USA going into the meeting were not addressed:

- subsidies for state own enterprises

- stealing of USA technology

- forced transfer of technology when USA enters into a joint venture with China.

- China agrees to crack down on the huge fentanyl exports to the west.

ii)Peter Tchir gives his take on the “deal” with China..basically it was a nothing burger.

( Tchir/Academy Securities)

iii)Goldman Sachs pours cold water on the trade war truce as it does not deal with the most importance issues. They give the chance of a comprehensive deal in 3 months at 20%

4/EUROPEAN AFFAIRS

i)GREAT BRITAIN/EU

Amazing: most Brits realize that the divorce from the EU is a bad deal for the uK. Probably the best deal would be for a Norway plus sort of deal with the UK joining the EEC as well as some sort of pre arranged customs union. Theresa May has ruled that out

( mish Shedlock/Mish talk)

ii)WOW@@ Theresa May is caught in a massive lie as she refuses to publish the complete legal analysis done on the agreement she signed. She left two two major points which would have destroyed Great Britain

1, it is quite likely that Britain could not sign trade deals with Europe or others

2. Great Britain could not set subsidies on agriculture something that Europe could do..plus others major points.

she has been caught in a massive lie

( Mish Shedlock/Mishtalk.

iii)FRANCE

Throughout the weekend, France burns as Macron is thinking about a state of emergency. Huge “yellow vest protests.

( zerohedge)

iv)France’s meltdown as a country and Macron’s disdain for his countrymen

v)According to Bloomberg’s Msika, France’s riots are a far bigger problem than Brexit or Italy( zerohedge)

vi)ITALY

Seems that the EU has had enough of USA hegemony: they are proposing widespread de dollarization initiatives

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

IRAN/USA

Iran has tested a medium ranged ballistic missile capable of carrying multiple warheads. The range: anywhere in the middle east as well as parts of Europe.

Trump will not be happy with this

( zerohedge)

6. GLOBAL ISSUES

Alasdair Macleod discusses the background noise on the G20 financial war and possible outcomes:

( Alasdair Macleod)

7. OIL ISSUES

Tom Luongo discusses the new Israeli pipeline which will travel underneath the Mediterranean, supply gas to Cyprus and then onto Italy. The problem is the deep cost. Germany and Russia are OK with this as the the Norstream nO 2 is much cheaper. Germany is happy to receive the cheaper gas and let Italy have the more expensive East Med pipeline gas.

( Tom Luongo)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

iii)Interesting: The Venezuelan opposition leaders urge the Bank of England not to give its gold back to Maduro who will confiscate it( Associated Press/GATA)

iv)Lots of talk about gold but no hint on manipulation

( GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

last night trading from China/futures New York:

(zerohedge)

then this morning

(zerohedge)

then this afternoon

(zerohedge)

ii)Market data/

Bad Omen worsens: yield curve inverts for the first time since 2007:

very ominous: the 3 yr yield overtakes the 5 yr yield.

also ominous: the 2 yr yield is one basis pts above the 5 yr

(zerohedge)

a)Is the Dallas housing market trying to tell us something? The Wall Street Journal has now called the housing boom is coming to an end…and it starts in Dallas…

( zerohedge)

ii)New home sales collapse and remember that home sales are a big part of the GDP

(courtesy Layman/IRD)

iii)Looks like Ford is doing exactly what GM is doing and the are said to announce 25,000 job cuts of which many will occur in the money losing venture over in Europe.(courtesy zerohedge

iv)SWAMP STORIES

Let us head over to the comex:

We are now in the non active delivery month of DECEMBER and here in this front month of December we now have 2239 contracts standing for a loss of 1268 oz. We had 1463 contracts stand for delivery on Friday so we gained 195 contracts or an additional 9755,000 oz will stand for delivery as these guys refused to morph into London based forwards as well as negating to accept a fiat bonus. We continue where we left off last month as queue jumping in silver is the norm for at least 20 months.

After December we have the non active January contract month and here we saw a LOSS of 5 contracts up to 1983 contracts. February saw its initial 13 contract gain to stand at 13. March, the next big delivery month after December saw a gain of 399 contracts up to 150,759

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

Deutsche Bank May Cause The Next Global Crisis

By Greg Hunter’s USAWatchdog.com

The International Monetary Fund (IMF) previously deemed Deutsche Bank as the most systemically dangerous bank in the world.

Professor of Economics and Law, William Black, knows why and contends:

“Deutsche Bank (DB) poses as what is called a ‘National Champion’ bank and the largest bank by far in Germany,but it’s actually the largest criminal enterprise in Germany. This is quite a statement because VW is such a massive fraud…

It is insane that we allow Deutsche Bank to go from fraud to fraud to fraud…

They cheat on everything else you can possibly imagine and, typically, they are getting caught, which is also not a very good sign in terms of their competence even as thieves. Even in the United States, there has been reluctance to crack down on Deutsche Bank…

When the New York Commissioner tried to crack down, the Office of the Comptroller of the Currency, the premier banking regulator, actually sought to impede that. He disparaged the New York folks and said there really wasn’t that big of problems and such, and all of that proved to be lies.”

Deutsche Bank was raided by German regulators last week on more allegations of fraud and money laundering.

DB is the epitome of “Too Big To Fail.”

So, it will never be allowed to fail, and regulators will not be allowed to regulate them properly. Professor Black says, “Why you should care is Deutsche Bank impedes effective regulation everywhere and because God only knows the next thing they are going to do…”

“This is going to continue until something dramatic changes. Eventually, they can cause the next crisis…

There will be a bailout in these circumstances, but that could help trigger another economic crisis. When the largest bank in the third largest economy in the world is completely dysfunctional, then the German economy is more likely to go into recession as well. That is one of the potential sources of the next recession, and you can see lots of people warning that there are signs that a serious recession is pretty likely relatively soon. Relatively could be two years.”

Professor Black, who was a top regulator in the S&L crisis, says,

“The whole system weakens itself because it gets caught in this big lie that says we have to pretend that Deutsche Bank is a bank instead of a criminal enterprise.”

In closing, Professor Black says,

“I am going to give you the advice you get after the recession before the recession. Pay off your debt, all that you can. Do not keep borrowing except in certain circumstances like you are going to buy a home, and it is prudent purchase. Buy a car when you can buy it with cash whenever possible…and always try to be a net saver.”

Join Greg Hunter of USAWatchdog.comas he goes One-on-One with Dr. William Black, Professor of Economics and Law at University of Missouri Kansas City.

via ZeroHedge

News and Commentary

Gold posts a second straight monthly gain (MarketWatch.com)

Asia-Pacific stocks jump on U.S.-China trade truce (MarketWatch.com)

G20 sealed landmark deal on WTO reform by ducking ‘taboo words’ (Reuters.com)

Fed Chair Jerome Powell survives a critical week, faces bigger tests (CNBC.com)

Trump hails trade deal with China as one of the largest ever made (CNBC.com)

NYSE and Nasdaq to close Wednesday for Bush mourning day (FNLondon.com)

Source: Bloomberg

Here’s the silver lining in traders’ outlook for gold (MarketWatch.com)

The Mythical Problem of Finding ‘The Right Gold Price’ (Forbes.com)

This Scholar Says the Government Should Buy Stocks When They Plunge (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

30 Nov: USD 1,220.45, GBP 956.95 & EUR 1,073.75 per ounce

29 Nov: USD 1,226.25, GBP 960.03 & EUR 1,077.87 per ounce

28 Nov: USD 1,213.20, GBP 949.69 & EUR 1,074.77 per ounce

27 Nov: USD 1,225.05, GBP 959.70 & EUR 1,082.21 per ounce

26 Nov: USD 1,226.65, GBP 954.58 & EUR 1,079.33 per ounce

23 Nov: USD 1,222.15, GBP 951.69 & EUR 1,075.13 per ounce

Silver Prices (LBMA)

30 Nov: USD 14.24, GBP 11.16 & EUR 12.52 per ounce

29 Nov: USD 14.26, GBP 11.17 & EUR 12.55 per ounce

28 Nov: USD 14.15, GBP 11.06 & EUR 12.54 per ounce

27 Nov: USD 14.28, GBP 11.20 & EUR 12.61 per ounce

26 Nov: USD 14.38, GBP 11.18 & EUR 12.65 per ounce

23 Nov: USD 14.26, GBP 11.12 & EUR 12.56 per ounce

Recent Market Updates

– Deutsche Bank May Cause The Next Global Crisis

– Ireland’s Mr Gold Reveals Nuggets Of Wisdom For When The Next Crash Comes

– BREXIT May Lead to UK Property Crash and Depression

– General Motors And General Electric Highlight The Ponzi Scheme That Is The US Economy

– A Worldwide Debt Default Is A Real Possibility

– Risk of Lower Lows in Gold Remains Prior to Spectacular Rally to Follow

– Gold and Silver Hold Firm as Stocks and Oil Lower in to US Holiday Weekend

– Is Brexit a Massive Threat to Globalisation?

– Stock Markets Remains Extremely Overvalued – Hussman

– Stocks are Now in ‘Complete Bitcoin Territory,’ Asset Manager Says

– Brexit’s Safe Haven Is a Dangerous Place

– Gold and Silver Rise As Stocks Fall On Valuation Concerns, Italy and Brexit Risks

– Pound Falls 2.5% Against Gold as UK Government in Turmoil Over Brexit

New York Sun: ‘A much bigger problem than China’

Submitted by cpowell on Sat, 2018-12-01 02:17. Section: Daily Dispatches

From the New York Sun

Friday, November 30, 018

Before enplaning for the G20 meeting at Argentina, President Trump gave an eye-opening interview to the Wall Street Journal. The focus was trade, tariffs, and Communist China. Toward the end the Journal’s reporter, Bob Davis, asked Mr. Trump about the Federal Reserve chairman, Jay Powell. Responded Mr. Trump: “I think the Fed right now is a much bigger problem than China.”

What a remarkable thing for the — or any — president to say enroute to a sit-down dinner with the Chinese party boss (Messrs. Trump and Xi seem set to sup Saturday), and we, for one, were delighted to hear the president make the point. It’s not that the Sun is dug in one way or another on interest rates, even if Mr. Trump is irked at the Fed chairman for raising them. It’s that it opens up the monetary debate.

… For the remainder of the commentary:

https://www.nysun.com/editorials/a-much-bigger-problem-than-china/90479/

END

Interesting: The Venezuelan opposition leaders urge the Bank of England not to give its gold back to Maduro who will confiscate it

(courtesy Associated Press/GATA)

Venezuelan opposition leaders urge Bank of England not to give gold to Maduro

Submitted by cpowell on Sat, 2018-12-01 02:34. Section: Daily Dispatches

From the Associated Press

via Tacoma News-Tribune, Tacoma, Washington

Friday, November 30, 2018

CARACAS, Venezuela — A pair of Venezuelan opposition leaders today urged the Bank of England not to hand over $550 million worth of gold sought by President Nicolas Maduro, saying officials in the South American country would either steal the gold or use it to finance its dictatorial government.

In a letter to the bank, former National Assembly president Julio Borges and opposition party leader Carlos Vecchio said Maduro’s socialist administration would pocket the last 14 tons of the Venezuelan gold in the bank’s vaults or use it to illegally imprison and kill its opponents.

It reminded the bank that the United States, United Kingdom, and many European countries consider Maduro’s government illegitimate following his re-election this year in what was widely considered a fraudulent vote. …

… For the remainder of the report:

https://www.thenewstribune.com/news/business/article222445475.html

END

Bullion star gold market charts look bullish

(Bullionstar/GATA)

Bullion Star’s gold market charts for November look bullish

Submitted by cpowell on Sat, 2018-12-01 02:43. Section: Daily Dispatches

9:45p ET Friday, November 30, 2018

Dear Friend of GATA and Gold:

Bullion Star’s gold market charts for November seem bullish, with strong accumulation in China, Russia, and Switzerland, even as the London gold “market” seems to be mostly unallocated paper. The charts and accompanying commentary are posted at Bullion Star here:

https://www.bullionstar.com/blogs/gold-market-charts/gold-market-charts-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Bloomberg rationalizes that governments must control the world’s financial markets..good grief..

(courtesy Bloomberg)

Bloomberg rationalizes government’s commandeering

the financial markets

Submitted by cpowell on Sat, 2018-12-01 02:57. Section: Daily Dispatches

This Scholar Says the Government Should Buy Stocks When They Plunge

By Peter Coy

Bloomberg / Business Week, New York

Friday, November 30, 2018

Last week my Bloomberg colleague Moxy Ying in Hong Kong wrote a fascinating QuickTake headlined, “When Stocks Crash, China Turns to its ‘National Team.'”She explained that government-related entities in China, known informally as the national team, step in to buy shares of mainland-based companies on a large scale to stop market routs. “Worry not, Chinese stockholders, the ‘national team’ is here to (try to) save the day,” she wrote.

…

Economist Roger E.A. Farmer thinks other nations need to emulate China, and even go beyond it. He has been banging this drum for years, as I have written in previous stories. Now he thinks it’s bound to happen. After I emailed him Moxy Ying’s story, he wrote back, “Asset price stabilization policies are coming to a central bank near you. It’s just a question of when.”

Added Farmer: “My best guess is that it will take another stock market crash” to induce governments to actively stabilize their stock markets. “That crash will happen, most likely within the next five years,” he added, “but its timing is unpredictable.” …

… For the remainder of the commentary:

https://www.bloomberg.com/news/articles/2018-11-28/this-scholar-says-the…

END

Lots of talk about gold but no hint on manipulation

(courtesy GATA)

Lots of talk about gold but only a hint about manipulation

Submitted by cpowell on Sat, 2018-12-01 23:02. Section: Daily Dispatches

6:04p ET Saturday, December 1, 2018

Dear Friend of GATA and Gold:

A tiny bit of progress in the struggle to expose gold market manipulation by central banks can be found today at Forbes, where asset manager and economist Nathan Lewis contemplates mechanisms for restoring a gold standard.

In an essay headlined “The Mythical Problem of Finding ‘The Right Gold Price'” —

https://www.forbes.com/sites/nathanlewis/2018/12/01/the-mythical-problem…

— Lewis writes that in recent years “central banks have engaged in other kinds of macroeconomic manipulation (negative interest rates!) to a degree never before seen. Probably they have done some heavy-handed bullying of the gold market itself.”

…

\But there’s nothing to be cheery about over at Barron’s, which, in a report headlined “Is It Time to Hold Gold?” —

https://www.barrons.com/articles/the-case-for-gold-pro-and-con-154361074…

— asks James Grant of Grant’s Interest Rate Observer to outline the reasons for gold as an investment and fund manager Daniel Wiener to outline the reasons against it.

Grant notes that as money without counterparty risk, gold may compare favorably with government currencies that pay little interest. But Grant offers no argument against Wiener’s observation that the gold price in recent years has not been keeping up with inflation.

Of course a response to that criticism is always available from GATA’s research —

http://www.gata.org/node/14839

http://www.gata.org/taxonomy/term/21

— which details the constant and usually surreptitious intervention by central banks against gold, particularly through the creation of a vast imaginary supply of the monetary metal in the futures markets.

But this weekend it seems that no one will get closer to that point than Lewis’ timid hint at Forbes.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

__

end

________________________________________

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8897/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8853 /shanghai bourse CLOSED UP 66.61 POINTS OR 2.57%

. HANG SANG CLOSED UP 675.29 POINTS OR 2.55%

2. Nikkei closed UP 223.70 POINTS OR 1.000%

3. Europe stocks OPENED ALL GREEN

/USA dollar index RISES TO 967.06/Euro RISES TO 1.1329

3b Japan 10 year bond yield: RISES TO. +.09/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.52/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.90 and Brent: 61.94

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.32%/Italian 10 yr bond yield DOWN to 3.15% /SPAIN 10 YR BOND YIELD UP TO 1.50%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.83: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.21

3k Gold at $1230.10 silver at:14.45 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 60/100 in roubles/dollar) 66.86

3m oil into the 52 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.58DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9990 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1324 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.32%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.03% early this morning. Thirty year rate at 3.33%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2430

World Stocks, US Futures, Crude Soar As Trump, Xi Deliver Early Christmas Rally

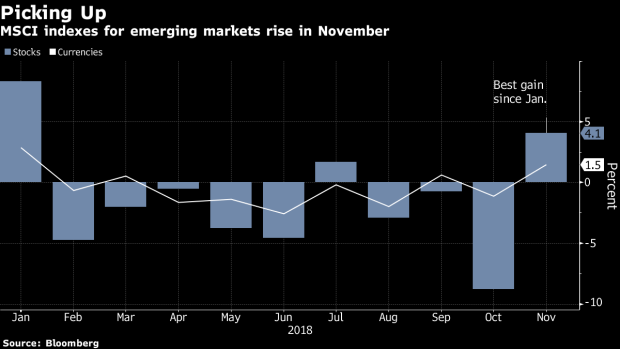

The Grinch may have stolen Thanksgiving profits, but Christmas came early for markets with world stocks rising over one percent and pushing emerging currencies higher against the dollar, as S&P futures jumped as much as 2%…

… and the Shanghai Composite soared 2.9% after the U.S. and China agreed to halt new tariffs for 90 days. Commodities spiked and the dollar rebounded from session lows. The MSCI’s all-country world index rose 0.9% in its sixth straight day of gains and hit its highest level since Nov. 9 while emerging equities rose 2.1% and were set for their strongest day in a month.

The gains came after China and the United States agreed during a Saturday dinner at the G-20 in Argentina to halt additional tariffs on each other. The deal prevents their trade war escalating as the two sides try to bridge differences with fresh talks aimed at reaching a deal within 90 days. If no deal is reached, Trump warned that the US will resume escalation, and hike tariffs to 25% from 10%.

“We have a deal. That’s wonderful news for global financial markets and signaling the start for a year-end rally in risky assets,” said Bernd Berg global macro strategist at Woodman Asset Management. “We are going to see a rally in emerging market and U.S equities, EM currencies and China-related assets like Australia. I expect the rally to last until year-end.”

Oil soared 4% higher after dipping below $50 briefly last Friday, jolted by efforts across the globe to support prices as Saudi Arabia and Russia extended their pact to keep production low (although without providing details ahead of this week’s OPEC+ meeting, while Canada’s largest producing province ordered unprecedented supply cuts. Optimism was dented slightly after Qatar said it was quitting OPEC, just as the group prepares to meet this week.

The risk-on mood initially drove the U.S. dollar as much as 0.4% lower against a basket of currencies before trimming some losses. The greenback was already under some pressure from the recent shift in the Fed’s policy communication to a slightly more dovish stance. Comments by Federal Reserve Chair Jerome Powell were interpreted by markets as hinting at a slower pace of rate hikes.

Emerging currencies were among the main beneficiaries of dollar weakness, with an MSCI index up 0.6 percent. It was led by China’s yuan which rose one percent for its biggest daily gain since Feb. 2016.

The euro pared a gain after data showing manufacturing activity slowed, with factory growth stumbling again in November, as business confidence remains the weakest in 6 years.

“Such positive sentiment won’t fade very soon … (the 90-day) period is not short, it’s long enough to soothe market sentiment,” trader at a foreign bank in Shanghai told Reuters.

Powell was scheduled to testify on Wednesday to a congressional Joint Economic Committee but his hearing is expected to be postponed to Thursday because major exchanges will be closed on Wednesday in honor of former U.S. President George H.W. Bush, who died on Saturday.

While some have speculated that the trade war truce would bring back more hikes on the table, others disagreed: Florian Hense, economist at Berenberg, said the market rally would not bring a return to a more hawkish Fed stance. “We would need to see some rebound in economic activity to lift expectations of more rate hikes,” he said.

Maybe not: in a Bloomberg TV interview, Fed Vice Chairman Richard Clarida said the US economy is in “good shape” and the outlook is “very solid” as the central bank is focused on meeting its dual mandate. He added that the concept of a “Powell Put” isn’t a useful concept, noting that the Fed could operate somewhat above 2% inflation goal.

More importantly, Clarida said that the dot plot of Fed interest-rate forecasts “is not going anywhere”, though it may evolve.

* * *

Back to markets, where Asian shares kicked off the gains, with Chinese mainland markets rising more than 2.5% while Japan’s Nikkei gained as much as 1.3% to a six-week high.

European equities followed Asia’s response higher with miners and automakers leading gains in the Stoxx Europe 600 Index after President Donald Trump said in a late-night tweet that China agreed to “reduce and remove” tariffs on imported American-made cars. The tweet sent the Dax 2.5% higher as auto stocks were set for best day in 2-1/2 yrs on Sino-US trade truce. Just before midnight on Sunday, Trump tweeted that China had agreed to remove car import tariffs, even though in a briefing in Beijing a few hours later China’s foreign ministry spokesman Geng Shuang declined to comment on any car tariff changes.

Donald J. Trump

✔@realDonaldTrump

China has agreed to reduce and remove tariffs on cars coming into China from the U.S. Currently the tariff is 40%.

Trump gave no other details in his late-night tweet, which came shortly after he agreed with Xi to a truce in the trade war during a meeting at the Group of 20 summit in Argentina. Shares of German carmakers Daimler AG and BMW AG rallied Monday morning after the U.S. trade deal with China. Trump’s comments, if ratified, would also hand automakers like Tesla a potential reprieve after higher levies hit sales in the world’s biggest car market.

In EMs, South Africa’s stock market was on course for its best day in four years, while Russian stocks climbed with the ruble as oil-production curbs spurred the biggest jump in Brent crude in two years. The peso advanced after a report that the new government was ready to re-purchase bonds issued to build Mexico’s City new airport.

Meanwhile, in rates, ten-year Treasury yields rose back above 3 percent; the Australian curve bear steepens with 10-year yield three basis points firmer. Mexican peso rallies 1.3%, rand 1.1% stronger; won rose to its strongest since October. Germany’s 10-year government bond, the benchmark for the euro area, was set for its biggest one-day yield jump in a month, rising four basis points to a high of 0.347%. Yields on riskier southern European bonds fell across the board, with Italian yields sliding as much as 10 bps to new two-month lows.

As noted above, WTI (+4.1%) and Brent (+3.9%) were both stronger following the positive US-China trade news and reports that Russia and Saudi Arabia are agreeing to extend the OPEC+ agreement; although no production cut figure has been announced so far. Additionally, Qatar, which produces approximately 600,000 BPD of oil, has announced that they are withdrawing from OPEC as of January with this being in-line with their long-term plan. Separately, Canada’s Alberta province is to reportedly mandate a 9% oil output reduction, which amounts to 325,000 BPD, in order to ease a supply glut with this to come into effect from January.

Gold (+0.7%) was firmer, albeit off of a 3-week high of USD 1232.30/oz reached earlier in the session; after gaining support from the dollar being weighed on by positive US-China trade news from the G20 summit. Steel and copper prices have also benefited from the positive trade news, with Chinese rebar steel increasing by its 7% exchange-set trading; with copper’s London benchmark prices nearing a two-month high. Elsewhere in commodities, Chicago soybeans rally as much as 3.2%. Base metals gain with LME copper up 2%; Dalian iron ore 3.4% stronger.

In other news, Italian PM Conte stated they are examining several options for a budget deal with the EU in which a solution could be made within days. Later it was reported, that Italian PM Conte is reportedly preparing for a deficit of 1.9%-2.0%, while Italian Deputy PMs Salvini and Di Maio are said to be ready to accept new target, according to Messaggero. Italy’s Deputy PM Salvini says that the EU cannot ask for a 1.9% target.

In the latest Brexit developments, UK PM May was reportedly under renewed pressure as the DUP threatened to abandon support for her in a confidence vote if she failed to get her Brexit deal approved in Parliament. May’s chief Brexit adviser Oliver Robbins secretly warned her the PM that customs backstop is a “bad outcome” for the UK which will see regulatory checks in the Irish Sea and put security co-operation at risk, according to the Telegraph. UK Secretary of State for Environment, Food and Rural Affairs Gove, has told Conservative rebels that there was a “real risk” of a second Brexit referendum if they don’t back PM May’s deal with Brussels.

In geopolitical news, South Korean President Moon and US President Trump agreed to revive momentum regarding negotiations for North Korea denuclearization. In related news, South Korean President Moon said a visit by North Korean Leader Kim to Seoul is still open and possible this year, while US President Trump is said to be targeting a summit with North Korean leader early 2019.

Expected data include manufacturing PMI and construction spending. Finisar, Coupa Software, RH and Smartsheet are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 1.7% to 2,805.50

- STOXX Europe 600 up 1.8% to 363.80

- MXAP up 1.9% to 156.55

- MXAPJ up 2.3% to 502.97

- Nikkei up 1% to 22,574.76

- Topix up 1.3% to 1,689.05

- Hang Seng Index up 2.6% to 27,182.04

- Shanghai Composite up 2.6% to 2,654.80

- Sensex up 0.05% to 36,210.60

- Australia S&P/ASX 200 up 1.8% to 5,771.16

- Kospi up 1.7% to 2,131.93

- Brent futures up 5.3% to $61.79/bbl

- Gold spot up 0.8% to $1,230.66

- U.S. Dollar Index down 0.5% to 96.84

- German 10Y yield rose 1.1 bps to 0.324%

- Euro up 0.4% to $1.1362

- Italian 10Y yield rose 0.9 bps to 2.846%

- Spanish 10Y yield fell 1.1 bps to 1.491%

Top Overnight News

- U.S. President Donald Trump said China has agreed to “reduce and remove” tariffs on American cars from 40 percent currently. He gave no other details in the late-night tweet, which came shortly after he agreed with President Xi Jinping to halt the imposition of new tariffs for 90 days as the world’s two largest economies negotiate a lasting agreement. In a briefing in Beijing a few hours later, China’s foreign ministry spokesman Geng Shuang declined to comment on any car tariff changes

- Oil rebounded from the biggest monthly loss in a decade after Russia and Saudi Arabia agreed to extend their deal to manage the crude market into 2019 and Canada’s largest producing province ordered an unprecedented output cut

- Leaders of the world’s largest economies agreed the global system of rules that’s underpinned trade for decades is flawed, in a post-summit statement Saturday that the White House quickly claimed as a win for Donald Trump’s protectionist agenda

- U.K. Prime Minister Theresa May faces yet another grueling battle this week as members of Parliament sink their teeth into her Brexit deal ahead of a crucial vote. On Monday, politicians on all sides will ratchet up the pressure on May to justify the terms she’s agreed to with the European Union by demanding she publish the government’s internal legal advice underpinning the accord

- France’s “Yellow Vest” anti-government demonstrations intensified Saturday. More than 400 people were arrested and at least 133 injured after rioters in Paris burned cars, looted stores and restaurants, and sprayed graffiti on the Arc de Triomphe. Emmanuel Macron convened an emergency cabinet meeting amid demands to alter his environmental and budget policies

- As the Brexit deadline approaches, about 50 banks and other financial institutions are having or have had talks with the Dutch central bank about setting up shop in the Netherlands

- The compromise to safeguard the euro is set to underwhelm supporters of the sweeping vision of an integrated and assertive Europe set out by French President Emmanuel Macron last year as the banking union, bailout plans and euro budget are all bogged down

Asian equity markets were higher across the board with global risk appetite boosted following the US-China trade truce at the G20. News of the tariff ceasefire spurred a rally in US equity futures in which the Emini S&P and DJIA futures reclaimed the 2800 and 26000 levels respectively, with the blue-chip index up nearly 500 points. ASX 200 (+1.8%) and Nikkei 225 (+1.1%) advanced with Australia led by commodity-related sectors as energy benefitted from the positive trade developments and Russia-Saudi agreement to extend the OPEC+ accord, while the JPY-risk dynamic was very much in play for Tokyo trade. Elsewhere, Hang Seng (+2.4%) and Shanghai Comp. (+2.6%) outperformed on the easing of trade tensions, with sentiment also supported by better than expected Chinese Caixin Manufacturing PMI and after the CFFEX relaxed domestic stock index futures trading conditions. Finally, 10yr JGBs initially saw a bout of weakness at the open amid the heightened risk appetite, although prices later recovered amid the BoJ’s presence in the market for JPY 800bln of JGBs with maturities of up to 5yrs.

Top Asian News

- Trump’s Auto Tariff Tweet Boosts Stocks, Leaves Beijing Silent

- Goldman Sachs-Funded Group Bids A$2.4 Billion for GrainCorp

- Macau Casinos Rise as J.P. Morgan Calls November Beat Impressive

- Saudi Prince Finds Both Friends and Disapproval at G-20 Summit

- India Is Said to Seek Seizure of IL&FS Officials’ Properties

European equities (Eurostoxx 50 +1.8%) trade with firm gains as markets react to the fallout of the G20 summit which saw US President Trump and Chinese President Xi Jinping agree to delay hiking tariffs on USD 200bln of Chinese goods to 25% for 90 days to allow for trade discussions between the two nations. In terms of sector specifics, mining names have been the main beneficiary from the trade optimism thus far with price action in metals markets giving a lift to Antofagasta (+8.0%), Arcelormittal (+6.6%), Anglo American (+6.3%), Glenore (+6.5%) and many more. Elsewhere, luxury names are also seeing some reprieve from the US-China developments with the sector previously hampered by tensions between the two nations; as such, Swatch (+6.1%), Kering (+5.5%), LVMH (+4.3%) and Burberry (+3.3%) all trade with firm gains. Auto names are also seen higher amid the spillover from US President Trump tweeting that China has agreed to reduce and remove tariffs on cars coming into China from the US which are currently at 40%; BMW (+6.1%), Daimler (+6.2%), Volkswagen (+3.9%). Finally, tech names have also been supported by the weekend’s developments with tech a key focus for negotiations, subsequently, STMicroelectronics (+7.3%), Infineon (+5.8%) and Wirecard (+4.4%) are also near the top of the Stoxx 600 leaderboard.

Top European News

- U.K. Manufacturing Growth Recovers From 27-Month Low in November

- Spanish Establishment Suffers Another Fracture in Andalusia

- Sewing’s Options Dwindle as Fresh Scandals Hit Deutsche Bank

- Albert Frere, Belgian Billionaire Investor, Dies at 92

- $80 Billion Locked in a ‘Golden Cage’ in Austria May Be Set Free

FX: DXY, CNY, JPY – An optimistic end to the G20 summit with Trump and Xi agreeing on a 90-day tariffs ceasefire until a trade deal can be negotiated (with sticking points such as IP remaining). As such DXY fell to lows of 96.710 vs. last week’s low of 96.622, though the index is nursing losses in an attempt to take another jab at 97.000. USD/CNY fell below the key 6.90 level despite a higher USD/CNY fix by the PBOC overnight, while JPY unwound some risk premium with USD/JPY stopping just shy of 114.00, but the headline pair supported just ahead of a downside tech-level (Tenken at 113.34).

- AUD, NZD, CAD – Major high-beta beneficiaries in the aftermath of the G20, with AUD/USD within striking distance of 0.7400 (where 1.365bln in option expiries lie) ahead of its 200DMA at 0.7418, while the Kiwi holds above 0.6900, marginally hampered by weaker than expected Q3 terms of trade and softer export volumes. Meanwhile, CAD also takes advantage of the rising oil prices after Russia and KSA extended their OPEC+ pact, on top of the tactical 325k BPD production cut at Canada’s Alberta refinery. USD/CAD currently sub-1.3200 but off post-G20 lows of 1.3160.

- GBP, EUR – Little reaction in the pound and the single currency following mixed manufacturing PMIs with Cable back down below 1.2750 (after having breached its 10DMA at 1.2800 where stops were reportedly tripped) and through the Raab-low at 1.2724 to test bids ahead of 1.2700, while EUR/USD couldn’t sustain gains to 1.1400 before retreating through 1.1350 and towards 1.1300. Note, the single currency was supported earlier on Italian press reports that PM Conte is said to be preparing for a deficit/GDP target in the range of 1.9%-2.0%, with the Deputy PMs apparently ready to accept the new target but has eased back in wake of the ECB’s announcement of Capital Key changes, including a perhaps surprisingly lower Italian ratio. In terms of option expiries, EUR/USD sees 1.32bln around 1.1380-90 ahead of reported offers at 1.1400.

- EM – TRY back in focus with softer than expected Turkish CPI helping the Lira retest recent highs around 5.1500 vs. the buck at one stage, but unable to breach resistance as the USD stage a broad comeback.

In commodities, WTI (+4.1%) and Brent (+3.9%) are both stronger following the positive US-China trade news and reports that Russia and Saudi Arabia are agreeing to extend the OPEC+ agreement; although no production cut figure has been announced so far. Additionally, Qatar, which produces approximately 600,000 BPD of oil, has announced that they are withdrawing from OPEC as of January with this being in-line with their long-term plan. Separately, Canada’s Alberta province is to reportedly mandate a 9% oil output reduction, which amounts to 325,000 BPD, in order to ease a supply glut with this to come into effect from January. Gold (+0.7%) is firmer, albeit off of a 3-week high of USD 1232.30/oz reached earlier in the session; after gaining support from the dollar being weighed on by positive US-China trade news from the G20 summit. Steel and copper prices have also benefited from the positive trade news, with Chinese rebar steel increasing by its 7% exchange-set trading; with copper’s London benchmark prices nearing a two-month high.

US Event Calendar

- 6:30am: Fed Vice Chairman Clarida Interviewed on Bloomberg TV & Radio

- 8am: Fed’s Quarles speaks at Council on Foreign Relations in NYC

- 9:15am: Williams Speaks at a NY Fed Conference on Treasury Market

- 9:45am: Markit US Manufacturing PMI, est. 55.4, prior 55.4

- 10am: Construction Spending MoM, est. 0.35%, prior 0.0%

- 10am: ISM Manufacturing, est. 57.5, prior 57.7

- 10:30am: Brainard Gives Keynote at NY Fed’s Treasury Market Conference

- 1pm: Fed’s Kaplan Speaks at Community Forum in Laredo, Texas

- Wards Total Vehicle Sales, est. 17.2m, prior 17.5m

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 66.61 POINTS OR 2.57% //Hang Sang CLOSED UP 675.29 POINTS OR 2.55% //The Nikkei closed UP 223.70 OR 1.00%/ Australia’s all ordinaires CLOSED UP 1.86% /Chinese yuan (ONSHORE) closed UP at 6.8897 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 52.90 dollars per barrel for WTI and 61.41 for Brent. Stocks inEurope OPENED GREEN //. ONSHORE YUAN CLOSED UP AT 6.8897AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8853: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

Markets are expected to roar, Monday but nothing substantive was agreed at the Xi/Trump meeting on Saturday. Basically there is a truce for 90 for 90 days in which trump will not raise tariffs of 200 billion dollars worth of Chinese goods. In return China will buy a huge portion of the autumn harvest of soybeans. The main points from the USA going into the meeting were not addressed:

- subsidies for state own enterprises

- stealing of USA technology

- forced transfer of technology when USA enters into a joint venture with China.

- China agrees to crack down on the huge fentanyl exports to the west.

“I’ll Eat My Hat If This Means Anything Substantive”:

Why The Trump-Xi Truce Achieves Little

The most important, and much-anticipated dinner date between Trump and Xi in years, which concluded amid loud applause and brief celebrations by both sides, ended in a three-month truce to the ongoing trade war between the two superpowers, with the US agreeing to postpone a planned tariff hike on January 1 and to keep the rate on existing tariffs at 10% for another 90 days in return for greater purchases of American goods.

While the arrangement provides breathing space to both leaders as they face slumping stock markets and economic warning signs, and will likely result in a brief jump in the market in the coming days, the two sides failed to make any tangible progress on the fundamental divide and core issues separating the world’s biggest economies.

“You blink first!”… “No, you blink first.”As Bloomberg recaps this morning, “negotiations have long been stuck over U.S. demands for deep structural reforms such as stopping forced technology transfers, enforcing intellectual property rights and ending state subsidies for strategic industries – all of which China sees as an American strategy to thwart its rise as a global power.” It is on these most thorny of issues that there was no real progress during the Trump-Xi dinner.

“You blink first!”… “No, you blink first.”As Bloomberg recaps this morning, “negotiations have long been stuck over U.S. demands for deep structural reforms such as stopping forced technology transfers, enforcing intellectual property rights and ending state subsidies for strategic industries – all of which China sees as an American strategy to thwart its rise as a global power.” It is on these most thorny of issues that there was no real progress during the Trump-Xi dinner.

In fact, as Michael Every, head of Asia financial markets at Rabobank said overnight, “I will eat my hat if this means anything substantive” as “neither side is fully ready for the war, but neither side will budge.”

Despite the lack of material progress on the fundamental divide, the market will cheer that the deal helps to alleviate immediate concerns that trade tensions would further stoke geopolitical tensions, a prospect that has raised worries of a new Cold War. The White House emphasized that Xi agreed to continue pushing for a nuclear-free North Korea, while Beijing said Trump would respect the One-China policy regarding relations with Taiwan — one of the biggest potential flashpoints between the nations.

More importantly, the summit showed that both sides could be pragmatic when needed, and refuted Goldman’s bearish forecast that more escalation would be the immediate conclusion.

Here’s the breakdown:

Xi won at least another three months before punitive tariffs on $200 billion in goods rise to 25 percent, allowing Chinese policy makers more time to offset the blow as growth slows. That said, all Xi got was a reprieve, because as SCMP editor Chungyan Chow writes, “Xi Jinping hasn’t really defused the Trump bomb. He just bought 3 month breathing space. Interesting to see what will happen next before the Chinese national congress sessions in March.”

Chungyan Chow

✔@ChungyanChow

Xi Jinping hasn’t really defused the Trump bomb. He just bought 3 month breathing space. Interesting to see what will happen next before the Chinese national congress sessions in March. https://sc.mp/04uq5

Trump and Xi agree trade war truce and no extra tariffs, Chinese officials say

US and Chinese presidents agree to trade truce, Chinese officials confirm.

scmp.com

Trump, meanwhile, got China to buy more American agricultural, energy and industrial goods while still maintaining the leverage of a tariff increase to pressure Xi into making greater concessions on structural issues. China also pledged action to clamp down on the synthetic opioid fentanyl, and Trump said Xi was open to approving a possible $44 billion deal for Qualcomm Inc. to purchase NXP Semiconductors NV if the companies are still interested.

So what does the truce achieve?

With less than a month left in the year, the one most likely outcome is the greenlight of a strong Santa Rally, both in the US and China, where overnight the China Financial Futures Exchange sent a strong hint to investors to get back in the market by cutting margin requirements for stock index trading to 10% for the CSI300 and SSE50 and 15% for the CSI500, the first such cut since Sept. 2017.

Global Times

✔@globaltimesnews

From Monday, CSI 300, SSE 50 index futures trading margin requirements will be adjusted to 10%, 15% for CSI 500, China Financial Futures Exchange said on Sunday.

“The presidents want the markets to enjoy Santa rallies first,” Junheng Li, the founder of the China-focused research company JL Warren Capital told Bloomberg. “And when February comes we can start worrying again.”

“This is a strongly market positive result for the short term, since over the past few days markets have been nursing hopes that a tariffs pause of this kind would happen,” Evercore ISI head of political analysis Terry Haines wrote in a note. “But it is not a ceasefire as some already are touting.”

The bottom line as Michael Pillsbury, a senior fellow at the Hudson Institute, said, “Neither side got their maximum demands and it’s not the first time in U.S.-China relations that both sides claim victory. Both sides avoided the worst-case scenario.”

* * *

In addition to traders, another immediate beneficiary from the truce is the US business community as well as US farmers, particularly those growing soybeans in states he needs to win to get re-elected in 2020. As Bloomberg notes, Trump hailed the “incredible deal” on Air Force One while heading back to the U.S., telling reporters that China will buy “a tremendous amount” of agricultural goods.

“Trump doesn’t give up much by a short pause and gets a chance to ship the soybean harvest to China while the negotiations are ongoing,” said Brad Setser, a former Treasury official and now a senior fellow at the Council on Foreign Relations in Washington. “The hard part is finding the basis for a real deal that settles the broader issues rather than agreeing on a pause.”

It is there that little progress is expected absent a material deterioration in markets and economies.

Meanwhile, signs of discord continued, and the most notable was the failure to issue a joint statement laying out the framework for talks. Each side gave its own readout of the outcome, and they contained key differences: China, for instance, made no mention of the 90-day time frame, while the U.S. didn’t reference the One-China policy regarding Taiwan ties.

China’s omission on the deadline indicates it has reservations on how to handle U.S. demands, according to Wang Peng, an associate research fellow of the Chongyang Institute for Financial Studies, Renmin University of China.

Making the type of domestic reforms sought by the U.S. is “extremely difficult as such moves involve the country’s reputation, the party’s authority and the structure of the domestic economy,” he said.

But the biggest hurdle and the crux of Trump’s deeper concerns with China is found in the 53-page report issued by Trade Representative Robert Lighthizer’s office about 10 days before the Trump-Xi meeting. It accused China of continuing a state-backed campaign of intellectual property and technology theft, downplayed its moves to ease foreign investment restrictions and raised alarm about its “Made in China 2025” policy to lead the world in sectors such as artificial intelligence and robotics.

Meanwhile, Chinese officials have repeatedly countered by saying moves to ease rules on foreign ownership of financial firms and automakers show they are opening up to the world, when in reality Beijing is merely looking for international bagholders as China suffered a burst of record defaults which has made local investors shy away from risky local assets. At the same time, they also strictly rule out dropping government support for companies in strategic Made in China industries over fears that would undermine China’s future economic prospects and threaten the power of the ruling Communist Party.

The bottom line is that despite much fanfare, the divergence in worldviews makes any lasting solution difficult to achieve unless either Trump or Xi backs down and neither is willing or ready to do so. Still, given the emerging risks to the global economy, and the political costs that entails for each leader, it is likely that both will be motivated enough to concede just enough to keep dragging out the talks without handing the other side a victory.

“Growth is going to slow in both countries,” said TCW analyst David Loevinger,. “While it doesn’t remove the the sword of Damocles hanging over trade, having blinked tonight you’d have to guess that the U.S. will blink again in March.”

* * *

Finally, what does the truce mean for the markets? According to one “base case” which correctly predicted that a Truce – in which existing tariffs stay in place – is the most likely outcome (with a 70% chance), while also accurately predicting a 3 month ceasefire, the agreement will be enough to get the S&P to 2,800…

… so look for a burst of buying in the S&P over the next 24 hours which pushes the stock index higher, but not much higher as trader concerns will next revert back to the Fed which now that trade tensions have been temporarily removed, may promptly revert back to its hawkish bias and resume rising rates well into 2019 which in turn will be the next bearish event-risk to put a damper on any substantial Christmas rally.

end

Peter Tchir gives his take on the “deal” with China..basically it was a nothing burger.

(courtesy Tchir/Academy Securities)

It’s Either Tied in Bottom of 9th or in Extra Innings

I guess we should continue with Friday’s T-Report theme of treating the President Trump and President Xi meeting as though it was a baseball game.

We walk in a run. The game goes on, possibly to extra innings. The real-world equivalent is some promise by China to reduce the trade deficit, us putting on hold any new or increased tariffs and both sides agreeing that Intellectual Property rights are important and that both sides agree to focus on…

…This is my highest probability scenario.

As far as I can tell from the press coverage I’ve seen

- China agreed to buy more agricultural and commodity goods (as we’ve been suggesting all along is part of the ‘easy’ deal)

- We agreed not to go ahead with the scheduled tariff increases (which were hurting us as well)

- Both sides have agreed to talk more with what seems like a 90 day target for progress (though a timeline that could easily be extended again)

Is this ‘Deal’ Good Enough for Markets?

It seems like this should be good enough for markets to continue with the rally that took S&P 500 and Nasdaq up 4.9% and 5.6% respectively on the week.

I think the outcome is marginally better than what people were pricing in and took some of the disaster scenarios off the table.

I would expect VIX to collapse now that the biggest wildcard is either off the table or at least postponed. (Brexit and Italy while moving Europe around seem to have lost their ability to whip U.S. markets back and forth – for now). We have Mueller and the change in the House in January to deal with on the domestic front – but that seems to be a few weeks away, which in this choppy market, can seem like a lifetime.

The biggest driver could be the market’s view, which we share,that Powell is trying to walk back a little on the dogmatically hawkish side (though part of this apparent change makes perfect sense for a data dependent Fed that is seeing the data weaken).

Corporate bonds were noticeably weak and an outlier on Friday. Despite the S&P 500 and Nasdaq both gaining about 0.8%, the CDX IG index was a ½ bp wider on the day, high yield was down roughly a ¼% depending on whether you looked at CDX HY or the big HY ETFs. The leveraged loan market bounced a little (at least BKLN did) but floating rate IG corporate bonds continued to trade poorly.

The Bloomberg Corporate bond OAS moved out 2 on Friday to 137 (from 109 in the middle of October), and it probably understates the weakness as the bond indices tend to lag their traded Beta counterparts when tracking moves to the downside (for example, corp bond spreads widened according to the index on Wednesday while CDX IG gapped 5 bps tighter and even the often ignored LQDH rallied).

If VIX can come down and the new issue calendar can show signs of slowing into year-end, credit should be able to turn around – but since its weakness on Friday was noteworthy, across the board, we will be watching that closely.

Bottom Line

Assuming the reporting we have seen so far is accurate, this deal, coupled with some oversold technicals and generally favorable seasonality, I’d expect a moderate risk-on move to begin.

But, since I am already trying to think about what could derail this move, and when to start cutting back on risk again, I think the rally won’t be as big or long lasting as I’d like to see.

Goldman Pours Cold Water On Trade War Truce: “The

Odds Of A Comprehensive Deal In 3 Months Are 20%”

Heading into this weekend’s historic Trump-Xi dinner date, Goldman was skeptical, stating that it was “too soon for a deal” and while it said the odds of a truce were just under 40%, it gave better than even odds of further escalation stating that “it is slightly more likely that the talks end with an optimistic tone but that there is no immediate commitment to delay the step-up in the tariff rate to 25%.” Goldman did hedge, however, saying that “we view this as a reasonably close call.”

And with one look at futures this morning following a summit conclusion that kicked the can on new tariffs and rate hikes by 90 days, it’s a good thing it did (unlike JPM which correctly predicted truce odds were 70%, forecasting that the market’s most likely reaction would be to send the S&P to 2,800 which is precisely where the ES is stuck now).

So what does Goldman think happens next? Perhaps not surprisingly, while the central banker incubating hedge fund tacitly admits its gloomy forecast was misplaced and praises the near-term can-kicking, the bank retains its overall pessimism and in its post-mortem writes that “this outcome is closest to the “pause” scenario we outlined in recent comments although the length of the pause is fairly short” and notes that while “the result shows the willingness of the two sides to reach a deal” Goldman still thinks that “finding a mutually agreeable compromise that leads to a comprehensive rollback of tariffs will be challenging.”

As part of its hot take, Goldman lists the tentative agreements that were reached on a “few less controversial issues” including:

- Chinese purchases of US products. The US press release stated “China is to purchase a very substantial amount of agricultural, industrial and energy products” from the US. The White House appears to expect purchases of agricultural products to start immediately. No quantity or specific commodities were mentioned, but purchases are likely to involve more meat, especially pork, products, given there has been an ongoing swine flu outbreak in China which led to the slaughtering of large amount of pigs and higher demand for alternative protein sources. Soybean purchases also seem likely, as they have been among the most politically important aspects of China’s retaliatory tariffs on US exports. This could also signal a partial unwinding of China’s retaliatory tariffs, which targeted agricultural products in earlier rounds.

- China will make fentanyl a controlled substance. China’s drug control is concentrated in traditional substances and awareness of use of such substances as drugs among the general public and officials is low. Traders have been arbitraging this regulatory gap and exporting this substance to the US. This is not viewed as a big issue in China and given the US focus it is easy to understand that President Xi agreed make this move.

- The US press release quoted President Xi as saying that, should the Qualcomm NXP merger request be presented to him, he is open to approving it. Official Chinese media reports did not mention this issue.

- Reporting from Xinhua suggests that the US agreed to continue to welcome Chinese students in the US. This comes following recent reporting in the US media that the White House could soon announce new restrictions. The US statement does not mention this. Xinhua also states that the US has pledged to continue to respect the “One China” policy regarding Taiwan as part of this understanding, though the US statement does not mention this.