GOLD: $1236.95 DOWN $4,25 (COMEX TO COMEX CLOSINGS)

Silver: $14.49 DOWN 6 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1237.00

silver: $14.49

For comex gold and silver:

DEC

NUMBER OF NOTICES FILED TODAY FOR DEC CONTRACT: 73 NOTICE(S) FOR 7300 OZ (0.227 tonnes)

Total number of notices filed so far for DEC: 4125 for 4012500 OZ (12.830 TONNES)

FOR DECEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

245 NOTICE(S) FILED TODAY FOR 1,225,000 OZ/

Total number of notices filed so far this month: 3027 for 15,135,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4043: DOWN 59

Bitcoin: FINAL EVENING TRADE: $3812 DOWN 138

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A FAIR SIZED 828 CONTRACTS FROM 180,737 DOWN TO 179,909 DESPITE YESTERDAY’S 10 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

746 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 721 CONTRACTS. WITH THE TRANSFER OF 746 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 746 EFP CONTRACTS TRANSLATES INTO 3.730 MILLION OZ ACCOMPANYING:

1.THE 10 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

NOW 18.685 INITIALLY STAND FOR DECEMBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DEC: 4475 CONTRACTS (FOR 3 TRADING DAYS TOTAL 1994 CONTRACTS) OR 22.38 MILLION OZ: (AVERAGE PER DAY: 1491 CONTRACTS OR 7.46 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 22.38 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.19% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,699.40 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

ACCUMULATION FOR NOVEMBER /2018: 247.18 MILLION OZ

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 828 DESPITE THE 10 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A VERY GOOD SIZED EFP ISSUANCE OF 746 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A TINY SIZED: 82 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 746 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 828 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 10 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.55 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .9050 BILLION OZ TO BE EXACT or 129% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DEC MONTH/ THEY FILED AT THE COMEX: 245 NOTICE(S) FOR 1,225,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./AND NOW DEC. AT 18.685 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY CONSIDERABLE SIZED 4121 CONTRACTS UP TO 399,919 WITH THE GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $7.25//.YESTERDAY’S TRADING) AS THESE GUYS JOINED SILVER IN THE ROUTINE MIGRATION OVER TO ETF’S AS WE APPROACH AN ACTIVE DELIVERY MONTH.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5233 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 5233 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 401,110. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9,354 CONTRACTS: 4121 OI CONTRACTS INCREASED AT THE COMEX AND 5233 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 9,354 CONTRACTS OR 935,400 OZ = 29,09 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $7.25

YESTERDAY, WE HAD 11677 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC : 25,948 CONTRACTS OR 2,594,800 OZ OR 80.71 TONNES (3 TRADING DAYS AND THUS AVERAGING: 6487 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAYS IN TONNES: 80.71 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 80.71/2550 x 100% TONNES = 3.16% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,845.09 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018: 552.88 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 4121 WITH THE GAIN IN PRICING ($7.25) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5233 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5233 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 9,354 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5233 CONTRACTS MOVE TO LONDON AND 4121 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 29,09 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $7.25 IN YESTERDAY’S TRADING AT THE COMEX

we had: 73 notice(s) filed upon for 7300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.25 TODAY

NO CHANGE IN GOLD INVENTORY

/GLD INVENTORY 758.21 TONNES

Inventory rests tonight: 758.21 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 6 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 321.552 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A FAIR SIZED 828 CONTRACTS from 180,737 DOWN TO 179,909 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

746 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 746 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 828 CONTRACTS TO THE 746 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A TINY LOSS OF 82 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 0.4100 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. AND NOW 18.685 MILLION OZ STANDING IN DECEMBER.

RESULT: A FAIR SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 10 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 746 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 16.15 POINTS OR 0.61% //Hang Sang CLOSED DOWN 440.76 POINTS OR 1.62% //The Nikkei closed DOWN 116.72 OR 0.52%/ Australia’s all ordinaires CLOSED DOWN 0.84% /Chinese yuan (ONSHORE) closed DOWN at 6.8570 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 52.99 dollars per barrel for WTI and 61.95 for Brent. Stocks inEurope OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.8570AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8581: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

Last night China dismisses the confusion by saying the meeting with Trump was very successful. However the difficult part of the deal will be how China and the uSA handle intellectual property theft.

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)ECB

This is going to hurt USA hegemony: the ECB just launched a better than blockchain instant payment system. Now will the big banks play along?

( Don Quijones/WolfStreet)_

ii)ITALY/EU

Tria is probably the “sole” adult in the room of Italian ministers. His departure will be a death blow to the Italian economy

( zerohedge)

iii) UK

iv)After yesterday’s historic contempt vote, JPMorgan now raises the odds of a “no Brexit” had 40%. I believe it is higher than that.( zerohedge)

v)FRANCE

vi)This ought to ruffle the feathers of the wealthier citizens of France: In order to calm our yellow vests ahead of the Saturday riots, Macron stated that he might institute a “wealth tax” to pay for climate change. I think the last time he proposed that many wealthy left the country.( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)SAUDI ARABIA/USA

Many senators have seen the evidence and conclude that the Crown Prince MbS orchestrated the murder. Let us see how this will play out in the future.

( zerohedge)

iii)Turkey

I have been highlighting the problems for Turkey for quite some time now. The chief problem was the country’s reliance on cheap USA money during the 2006-2012 period. Households borrowed huge amounts of money and now we are witnessing huge non performing loans similar to what we see in Italy. This is a house of cards and no doubt we will see a huge debt crisis emerging here.

( zerohedge)

6. GLOBAL ISSUES

Canada

this is not good!! The Bank of Canada folds on its economic enthusiasm highlighting a poor housing sector and low crude prices. They have decided to keep interest rates unchanged and will not raise rates in 2019

( zerohedge)

7. OIL ISSUES

i)Day one and no firm commitment to lower production. Oil dumps after initially gaining on the day

( zerohedge)

ii)On no!! this is going to be a disaster for Canada. Already reeling from giving huge discounts because of bottlenecks..now Canada is legislated that sulfur content in the oil must be reduced to .5 % from 3.5%. That is going to add 7 to 8 dollars of cost onto the already all price that they are receiving (as low as 16 dollars cdn/barrel). This will knock Canada out of the oil business.

( Irina Slav/OilPrice.com

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

ii)There is now a shortage of Palladium. Normally cars would switch back to Platinum but changes to the automobile to accept palladium has made it almost impossible to switch back to Platinum unless the auto makers undergo huge costs to accept the cheaper Pt. The shortage of Palladium will be a forerunner to the shortage of gold and silver( Craig Hemke/GATA)

iii)Spanish speaking Univision quotes Bullion star Ronan Manly on the expropriation of Venezuelan gold.

( GATA/Univision/Ronan Manly)

iv)My goodness: Sudan is Africa’s second leading gold producer and this is all due to artisanal miners. They mine primitively using mercury and it is extremely poisonous to those miners engaging in that activity.

( GATA/France 24)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

Mish explains the meaning of the inversion of the yield curve. It generally signals a recession. However you can still enter a recession without the inversion

(courtesy Mish Shedlock)

a)Seems that our good friends over at Goldman lost 800 million dollars during a trade with an indicted 1 MDB linked bank, Singapore’s Falcon bank

( zerohedge)

b)This is going to be a lots of fun: The USA charges 4 men responsible for the Panama Papers operations

They will sing and this will lead to many arrests

(courtesy Adam Klasfeld and special thanks to Robert H for sending this to us)

iv)SWAMP STORIES

Many were expecting some detail from Mueller in his sentencing memorandum issued last night. There is nothing on the issue of whether Trump or his election people where involved with Russians in fixing the USA election

(courtesy zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of DECEMBER and here in this front month of December we now have 976 contracts standing for a loss of 248 contracts. We had 269 contracts stand for delivery yesterday so we gained 21 contracts or an additional 105,000 oz will stand for delivery as these guys refused to morph into London based forwards as well as negating to accept a fiat bonus. We continue where we left off last month as queue jumping in silver is the norm for at least 20 months.

After December we have the non active January contract month and here we saw a loss of 32 contracts down to 1938 contracts. February saw its another 9 contract gain to stand at 35. March, the next big delivery month after December saw a loss of 601 contracts down to 146,933

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

we still have not had any adjustments out of the dealer to the customer account to signify a settlement

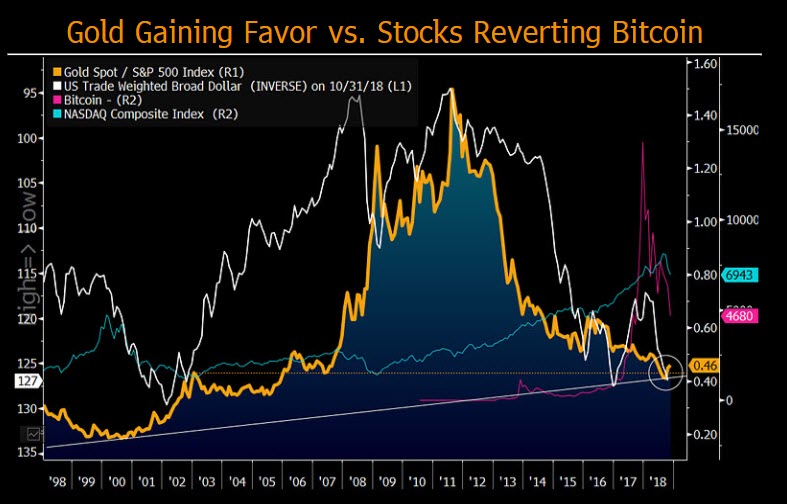

Gold Is “Coiled” and Looks Set To Surge Like Natural Gas — Bloomberg Intelligence

– Gold’s “setup” is “similar to natural gas before its big rally”

– Gold is gaining favour over stocks, bitcoin and cryptos

– Metals may be primary beneficiaries of imminent greenback peak

– Silver “appears ready for a potential longer-term recovery”

– GoldCore editors note: Natural gas is 56% higher year to date

by Bloomberg Intelligence (appeared first on the Bloomberg Terminal)

Metals should be primary beneficiaries of an imminent greenback peak, with normalization in U.S. stock-market out performance, Federal Reserve tightening near a finish and the trade-weighted broad dollar approaching multiyear highs.

Though the dollar tops the list of this year’s best performing major assets, gold and copper show divergent strength. Industrial metals appear to be at a discount in a bull market with favorable demand vs. supply conditions.

Indications from precious metals, notably gold, offer a setup that’s similar to natural gas before its big rally.

Bound to historically compressed trading ranges with many typical pressure factors nearing multiyear extremes, precious metals appear close to a maximum loss of faith vs. the strong stock market and greenback.

Gold is low vs. stocks if dollar has peaked

Gold should shine vs. stocks, particularly if the dollar stops advancing. Our graphic illustrates that the gold-to-stocks ratio is potentially bottoming from a good support level despite a resilient greenback. A declining U.S. equity market is a primary force to pressure the dollar, supporting metals. Mean-reversion risks in the trade-weighted broad dollar near the 2002 and 2016 highs may outweigh further appreciation potential.

Reversion in stock prices and Bitcoin toward their means is more than a coincidence, in our view. They’ve rallied together in the past few years with a common support factor — global quantitative easing.

Cryptocurrencies, considered alternatives to fiat currencies such as the dollar, gained plenty of advocates as global central banks rapidly increased money supply to offset deflationary forces.

Gold ETFs to prevail vs. record short futures

Gold ETF inflows appear unstoppable absent a severe bear market, which is unlikely with inflation picking up, an extended stock market and the dollar near multiyear highs. Resolute gold ETFs are focusing on portfolio hedging and have greater upside vs. downside potential, in our view. Representing about 70% of all commodity ETFs, total known gold holdings have increased about 10x the rate of change in the spot price since the start of 2015. In this rate-hike cycle, ETF holdings are up about 50% vs. 15% for spot gold. ETFs’ gold positions continue to increase despite this year’s lower spot price.

Buy-and-hold-focused ETFs are facing off with more-speculative futures. Managed-money net gold positions haven’t recovered much from the record-short levels reached in October, which is providing a bid below the market.

Gold ready to follow the lead of natural gas

Much like natural gas earlier this year, gold has the drivers in place to rally from its compressed range. Increasing inflation and debt levels are positive companions, as is gold’s divergent strength to the dollar, which is vulnerable as it nears a good resistance level.

GoldCore editors note: Natural gas is 56% higher YTD

Since the start of the current Federal Reserve tightening cycle, and despite rallies in the metal’s traditional adversaries — the greenback (up 5% on a trade-weighted basis) and the stock market (S&P 500 up 36%), the dollar price of gold is up 14%.

With rate hikes nearing a potential end-game, gold is ripe to rally. The narrowest 24-month Bollinger bands for the longest period in 16 years indicate the metal’s upside. For gold to decline, it would likely need the dollar to remain above multiyear highs, plus a decline in equity-market volatility.

Silver backed to key support, dollar resistance

The trade-weighted broad dollar is near a peak and silver a bottom, in our view, and the potential for mean reversion should outweigh continuing-the-trend risks. Silver, among the most negatively correlated to the dollar and positively to industrial metals, appears ready for a potential longer-term recovery. For it to stay down — about 15% this year — we’d need to see sustained dollar strength and weakness in industrial metals and gold. That’s unlikely. Near multiyear highs, dollar risks are tilting toward reversion, notably if U.S. equities keep sagging.

Rate-hike expectations have begun to ease, stalling the greenback rally. Significant for silver — often called leveraged gold — would be a peak in the dollar. If silver catches up some to industrial metals, it would be closer to $20 an ounce, vs. about $14.50 today.

Silver backed to key support, dollar resistance

The trade-weighted broad dollar is near a peak and silver a bottom, in our view, and the potential for mean reversion should outweigh continuing-the-trend risks. Silver, among the most negatively correlated to the dollar and positively to industrial metals, appears ready for a potential longer-term recovery. For it to stay down — about 15% this year — we’d need to see sustained dollar strength and weakness in industrial metals and gold. That’s unlikely. Near multiyear highs, dollar risks are tilting toward reversion, notably if U.S. equities keep sagging.

Rate-hike expectations have begun to ease, stalling the greenback rally. Significant for silver — often called leveraged gold — would be a peak in the dollar. If silver catches up some to industrial metals, it would be closer to $20 an ounce, vs. about $14.50 today.

Access the full Bloomberg article here & the full Bloomberg Commodity Outlook (December 2018 Edition) here

Secure Storage Ireland info here

Secure Storage Ireland info here

News and Commentary

Gold futures tally highest finish since July (MarketWatch.com)

Gold prices steady as dollar edges higher (Reuters.com)

What President Bush’s day of mourning means for stock, bond & commodity traders (MarketWatch.com)

Palladium at record high, with prices at their closest to gold in 16 years (MarketWatch.com)

Dow plunges nearly 800 points on rising fears of an economic slowdown (CNBC.com)

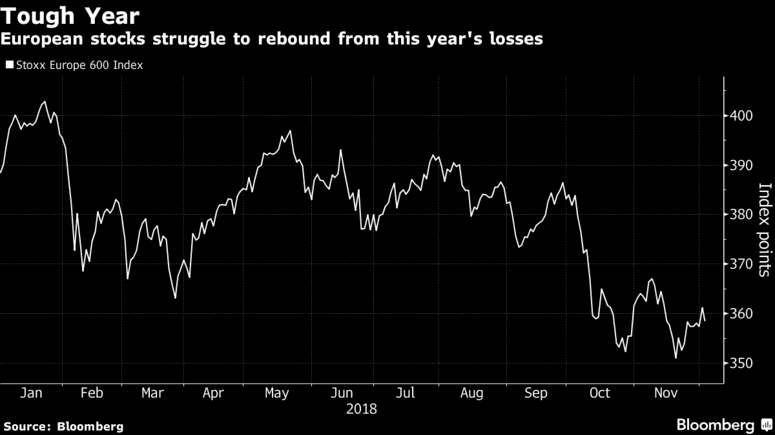

European Stocks Slump on Trade Woes as Banks to Miners Slide (Bloomberg.com)

Source: Bloomberg

This signal is the closest you’ll get to a sure thing in economics (MoneyWeek.com)

During stock-market volatility, how would you invest $100,000? (MarketWatch.com)

GATA has proved gold market manipulation, and here’s more proof -Taylor (Gata.org)

Europe Plays With Fire on Italy Contagion (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

04 Dec: USD 1,239.25, GBP 966.74 & EUR 1,086.45 per ounce

03 Dec: USD 1,231.05, GBP 966.00 & EUR 1,084.92 per ounce

30 Nov: USD 1,220.45, GBP 956.95 & EUR 1,073.75 per ounce

29 Nov: USD 1,226.25, GBP 960.03 & EUR 1,077.87 per ounce

28 Nov: USD 1,213.20, GBP 949.69 & EUR 1,074.77 per ounce

27 Nov: USD 1,225.05, GBP 959.70 & EUR 1,082.21 per ounce

Silver Prices (LBMA)

04 Dec: USD 14.55, GBP 11.35 & EUR 12.77 per ounce

03 Dec: USD 14.39, GBP 11.31 & EUR 12.69 per ounce

30 Nov: USD 14.24, GBP 11.16 & EUR 12.52 per ounce

29 Nov: USD 14.26, GBP 11.17 & EUR 12.55 per ounce

28 Nov: USD 14.15, GBP 11.06 & EUR 12.54 per ounce

27 Nov: USD 14.28, GBP 11.20 & EUR 12.61 per ounce

Recent Market Updates

– “Collapse Of Civilisation Is On The Horizon” – Attenborough Warns World Leaders

– Deutsche Bank May Cause The Next Global Crisis

– Ireland’s Mr Gold Reveals Nuggets Of Wisdom For When The Next Crash Comes

– BREXIT May Lead to UK Property Crash and Depression

– General Motors And General Electric Highlight The Ponzi Scheme That Is The US Economy

– A Worldwide Debt Default Is A Real Possibility

– Risk of Lower Lows in Gold Remains Prior to Spectacular Rally to Follow

– Gold and Silver Hold Firm as Stocks and Oil Lower in to US Holiday Weekend

– Is Brexit a Massive Threat to Globalisation?

– Stock Markets Remains Extremely Overvalued – Hussman

Jay Taylor: GATA has proved gold market manipulation, and here’s more proof

Submitted by cpowell on Tue, 2018-12-04 16:01. Section: Daily Dispatches

11a ET Tuesday, December 4, 2018

Dear Friend of GATA and Gold:

In his November 16 edition, our old friend Jay Taylor, publisher of Jay Taylor’s Gold, Energy, and Tech Stocks newsletter —

— wrote extensively about gold market manipulation and credited GATA for proving it.

Taylor went on to present a chart of morning and afternoon gold price fixes from the London Bullion Market Association showing that the gold price has nearly always been knocked down during London trading, so much so that buying on the afternoon fix and selling on the morning fix long has been spectacularly profitable, while doing the opposite long has been spectacularly unprofitable.

…

Taylor asks: “How can it be that skimming profits every day by buying the PM fix and selling the AM fix the next day is possible if the LBMA paper market isn’t rigged?”

With Taylor’s kind permission, his November 16 letter’s section on manipulation is posted in PDF format at GATA’s internet site here:

http://www.gata.org/files/JayTaylorLetter-11-16-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

There is now a shortage of Palladium. Normally cars would switch back to Platinum but changes to the automobile to accept palladium has made it almost impossible to switch back to Platinum unless the auto makers undergo huge costs to accept the cheaper Pt. The shortage of Palladium will be a forerunner to the shortage of gold and silver. Today Palladium rose to $1239.00 per oz and thus for the first time ever, it is higher than gold.

(courtesy Craig Hemke/GATA)

Craig Hemke at Sprott Money: What is Mr. Palladium

telling us?

Submitted by cpowell on Tue, 2018-12-04 21:59. Section: Daily Dispatches

5p ET Tuesday, December 4, 2018

Dear Friend of GATA and Gold:

A shortage of palladium and a squeeze in the London market for the metal may hint at similar squeezes soon in the monetary metals, the TF Metals Report’s Craig Hemke writes today at Sprott Money.

Hemke writes that back in the 1960s “physical gold shortages created an inability to manage price, and this led to the inevitable demise of the London Gold Pool in 1968. A true global palladium shortage that forces the hand of the banks and exposes their schemes to the light of day could be the first step to ending the ongoing LBMA/Comex gold pool 50 years later.”

Hemke’s analysis is headlined “What Is Mr. Palladium Telling Us?” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/what-is-mr-palladium-telling-us-craig-h…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Spanish speaking Univision quotes Bullion star Ronan Manly on the expropriation of Venezuelan gold.

(courtesy GATA/Univision/Ronan Manly)

Univision quotes Bullion Star’s Manly on expropriation

of Venezuelan gold

Submitted by cpowell on Wed, 2018-12-05 02:08. Section: Daily Dispatches

9:10p ET Tuesday, December 4, 2018

Dear Friend of GATA and Gold:

Univision, the big Spanish-language television network in North America, yesterday quoted Bullion Star gold market analyst Ronan Manly in a report about the Bank of England’s refusal to repatriate Venezuela’s gold.

In an English version of Univision’s reporting, Manly says “the more logical and likely explanation” for the expropriation of Venezuela’s gold “is that the United States, through the White House, U.S. Treasury, and State Department has been liaising with the British Foreign Office and Her Majesty’s Treasury to put pressure on the Bank of England to delay and push back on Venezuela’s gold withdrawal request.”

The Univision report is posted here:

https://www.univision.com/univision-news/latin-america/dont-let-venezuel…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

My goodness: Sudan is Africa’s second leading gold producer and this is all due to artisanal miners. They mine primitively using mercury and it is extremely poisonous to those miners engaging in that activity.

(courtesy GATA/France 24)

Sudan becomes second leading gold producer in

Africa on backs of artisanal miners

Submitted by cpowell on Wed, 2018-12-05 03:00. Section: Daily Dispatches

10p ET Tuesday, December 4, 2018

Dear Friend of GATA and Gold:

If you think Western investors in the monetary metals have had a tough few years, take a look at Helene Renaux’s report for France 24 about artisanal gold miners in Sudan, who help make the country the second-largest producer of gold in Africa and the ninth in the world at the expense of practically bathing themselves in liquid mercury every day without much awareness of its poisonous effects on their health.

…

.

Sudan’s government seems interested in transitioning the country’s gold-mining industry to modern methods but also seems to be unaware of the international gold price suppression scheme, which makes all developing countries less attractive for foreign investment.

So if you have any connections with the Sudanese government, please let them know that GATA would be glad to send a representative to Khartoum to explain how the country is getting screwed but doesn’t have to remain another rich country insisting on being poor.

The France 24 report is headlined “Sudan’s Gold Rush Driven by High-Risk, Unregulated Mining,” is five minutes long, and can be viewed here:

https://www.france24.com/en/20181204-focus-sudan-unregulated-gold-rush-h…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

end

________________________________________

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8570/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8581 /shanghai bourse CLOSED DOWN 16.15 POINTS OR 0.61%

. HANG SANG CLOSED DOWN 440.76 POINTS OR 1.62%

2. Nikkei closed DOWN 116.72 POINTS OR 0.53%

3. Europe stocks OPENED ALL RED

/USA dollar index FALLS TO 96.89/Euro RISES TO 1.1296

3b Japan 10 year bond yield: FALLS TO. +.07/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.96/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.99 and Brent: 61.95

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.26%/Italian 10 yr bond yield DOWN to 3.06% /SPAIN 10 YR BOND YIELD UP TO 1.45%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.79: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.17

3k Gold at $1237.45 silver at:14.49 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 14/100 in roubles/dollar) 66.74

3m oil into the 52 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.96DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9978 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1327 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.26%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.91% early this morning. Thirty year rate at 3.17%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3408

US Futures, Global Stocks Pare Losses After China,

“Tariff Man” See Deal

While U.S. cash markets will be closed to mark the death of President George H. W. Bush, S&P futures were open and rebounded modestly from yesterday’s furious selloff, rising 0.5% after yesterday’s 3.2% drop, as “Tariff Man” Trump said he sees a China trade deal coming “either now or into the future”…

… while European and Asian stocks trimmed losses after China pledged to start delivering on trade agreements reached with America, provide a modest risk backstop.

China’s announcement, another twist in the trade war saga, was a much-needed dose of positive news, as it ended days of silence from the Asian nation following a weekend meeting between Presidents Donald Trump and Xi Jinping. Upbeat statements from Trump had not been immediately matched by Beijing, helping fuel the equity tumult which sent US stocks plunging over 3% on Tuesday.

On Wednesday morning, a happy Trump tweeted an excerpt from a Bloomberg article according to which “China officially echoed President Donald Trump’s optimism over bilateral trade talks” and noting that “Chinese officials have begun preparing to restart imports of U.S. Soybeans & Liquified Natural Gas, the first sign confirming the claims of President Donald Trump and the White House that China had agreed to start “immediately” buying U.S. products.”

Donald J. Trump

✔@realDonaldTrump

“China officially echoed President Donald Trump’s optimism over bilateral trade talks. Chinese officials have begun preparing to restart imports of U.S. Soybeans & Liquified Natural Gas, the first sign confirming the claims of President Donald Trump and the White House that……

Global markets were left reeling after Tuesday’s steep sell-off in New York, but nerves steadied after China’s Commerce Ministry said on Wednesday morning that Beijing will start to “quickly implement” specific items where there’s consensus with the U.S. and will push forward on trade negotiations within the 90-day “timetable and road map.”

Asian stocks slid across the board on Wednesday, dragged down by Wall Street’s tumble as sharp declines in long-term U.S. Treasury yields and resurgent trade concerns stoked investor worries about global economic growth. MSCI’s broadest index of Asia-Pacific shares outside Japan fell 1.3 percent. The Shanghai Composite Index slipped 0.6% and Japan’s Nikkei dropped 0.5 percent, but rebounded from session lows. Australian stocks lost 0.8%, pressured by global losses. The mood further soured after data showed Australia’s third-quarter growth fell short of expectations. The Australian dollar D4 was down 0.7 percent at $0.7288.

Worries about U.S. bond markets signaling an impending recession, and a still rumbling trade war between the world’s top two economies, sent European shares to a 2 week low, yet while the Stoxx Europe 600 Index slumped as much as 1.2%, hitting the lowest since Nov. 23, and traded down 0.7% last, that was far less than the 3.2% plunge recorded by the S&P 500 a day earlier. Financials were the biggest drag on European shares as investors dumped sectors highly sensitive to economic growth. Europe’s bank index fell 1.7%, while oil and mining sectors fell 1.5 percent each.

“Cyclicals are really dependent upon accelerations in growth, they’re very real economy sensitive for higher revenues,” said John Ricciardi, CEO and lead portfolio manager at Kestrel Investment Partners. The inversion of parts of the U.S. yield curve means investors are beginning to panic about future growth and inflation, Ricciardi added.

Chipmakers AMS, STMicroelectronics and Infineon fell 1.2 percent to 4.5 percent following a sharp drop in Apple and chip stocks on Wall Street, while German carmakers outperformed the DAX as investors digested what seemed a relatively positive outcome from auto executives’ meeting at the White House. President Trump pressed carmakers to increase investments in the United States, something the executives said they planned to do but wouldn’t be able to if the administration went ahead with threatened tariffs.

Concerns about slowing U.S. growth have accelerated the flattening of the yield curve, which has preceded the last seven US recessions. “The market decline in the U.S. overnight and the flattening of the yield curve reflect that economic growth momentum is taking over as the primary concern for investors, even as the latest ISM manufacturing data is holding up well,” wrote Tai Hui, market strategist at J.P. Morgan Asset Management. On Wednesday, the Treasury cash/futures will remain closed.

The German curve steepened slightly, yields lower by ~1bp across the curve and touching the lowest since mid-2017 amid the risk-off mood, while Italian bonds jumped. UK Gilt yields rose by ~4bps as the curve bear flattens, widening 4.5bps to Germany after yesterday’s Brexit votes. BTPs push higher, supported by decent demand at the Spanish bond auctions and a turnaround in FTSE MIB off the lows.

The dollar initially advanced versus all major peers before reversing and turning slightly lower on the day. The Aussie dollar led losses among majors after 3Q GDP data missed forecasts, adding to fears of a global slowdown. The pound climbed as investors digested legal advice over Prime Minister Theresa May’s Brexit deal, which confirmed that the so-called customs backstop could remain “indefinitely.”

In the latest Brexit news, legal advice has been published states “backstop could mean the UK is subject to protracted and repeating rounds of negotiations”; according to BuzzFeed. Adding that “these talks could still be taking place years later, and the UK would be breaking the law if it left the backstop without the EU’s agreement”. Sky News reported that the UK does not need to pass legislation to revoke Article 50. Telegraph’s Rothwell Tweets “EU sources adamant that there can be no Withdrawal Agreement without a fully legally operational backstop…even if MPs reject the deal and/or May resigns”. UK Trade Secretary Fox states that in the wake of last night’s vote in Parliament, there is a chance that there might not be a Brexit.

In commodities, WTI (-0.2%) and Brent (-0.3%) bounced off lows as the latest OPEC+ meeting goes underway, with the Omani Oil Minister hinting at a 3-6 month production cut ahead of tomorrow’s key OPEC meeting. Furthermore, The WSJ reports that OPEC delegates are concerned that Saudi and Russia are making output agreements without input from OPEC; it was also stated that the Russia-Saudi relationship was a key factor in Qatar’s withdrawal. Markets will be looking ahead to the postponed EIA weekly data coming out tomorrow following the unexpected API build, alongside the OPEC meeting with emphasis on any decision to cut oil production that may arise. Reports today by RIA stating that OPEC wants Russia to reduce oil output by a minimum of 300k BPD. However, TASS has reported that Russia is only seeking a symbolic production cut which follows previous reports that they would only agree to a 140k BPD cut. Elsewhere, Libya’s NOC stated that all port terminals are shut due to bad weather, with storage capacity at Zawiya (usual production of 120k BPD) affected and the 300k BPD Sharara oil field production to be cut by 50% tomorrow morning.

Gold has weakened from the 5-week high reached in the previous session, as the dollar is marginally firmer. The majority of base metals have fallen due to being weighed on by US-China trade tensions following US President Trump commenting that there will have a real deal or no deal at all with China.

Treasury markets are closed for a day of mourning in the U.S. in honor of ex-President George H.W. Bush. Below is a schedule of US market closure on Dec. 5

- CME Globex trading hours for Interest rate products will close at their regular time on Tuesday Dec 4th and will not reopen until their regularly scheduled time on Wednesday Dec 5th 2300GMT/1700CST.

- Both the open outcry and CME Globex trading session for FX products will have normal trading hours on Wednesday Dec 5th

- CME Globex trading hours for CME Group U.S.-based equity products on Wednesday Dec 5th will include an abbreviated

- session, closing after overnight trading at 1430GMT/0830CST and reopening at their regularly scheduled time on Wednesday Dec 5th at 2300GMT/1700CST

- New York Stock Exchange, NYSE American, NYSE National, NYSE Arca and NASDAQ have announced that they will be closed for trade on Wednesday Dec 5th

- ICE Futures U.S is open for trading, Wednesday Dec 5th will be a regular ICE Clear US business day

Market Snapshot

- S&P 500 futures up 0.4% to 2,713.75

- STOXX Europe 600 down 0.7% to 355.78

- MXAP down 1% to 153.65

- MXAPJ down 1.3% to 495.24

- Nikkei down 0.5% to 21,919.33

- Topix down 0.5% to 1,640.49

- Hang Seng Index down 1.6% to 26,819.68

- Shanghai Composite down 0.6% to 2,649.81

- Sensex down 0.8% to 35,836.22

- Australia S&P/ASX 200 down 0.8% to 5,668.35

- Kospi down 0.6% to 2,101.31

- German 10Y yield fell 0.8 bps to 0.255%

- Euro down 0.02% to $1.1341

- Italian 10Y yield rose 1.0 bps to 2.789%

- Spanish 10Y yield fell 1.0 bps to 1.475%

- Brent Futures down 1% to $61.45/bbl

- Gold spot down 0.2% to $1,236.00

- U.S. Dollar Index up 0.03% to 97.00

Top Overnight News

- China said Wednesday the trade meeting with the U.S. was “very successful” and is “confident” of implementing the results agreed upon at the talks, but didn’t provide any further details on the outcome

- Federal Reserve Bank of New York President John Williams gave an optimistic review of the U.S. economy, reiterated his support for further gradual interest-rate increases and expressed no concern that market participants have dialed back expectations for policy tightening in 2019

- Australia’s economy slowed last quarter as commercial construction fell and household spending slowed, casting doubt on the central bank’s outlook and all but ruling out an interest-rate increase next year

- Bank of Japan Deputy Governor Masazumi Wakatabe gave a more cautious view on the outlook for prices as economists increasingly see inflation weakening over the next year

- With less than 48 hours to go before a critical OPEC gathering, Saudi Arabia and Russia are set to meet in Vienna for a make-or-break preparatory meeting on Wednesday that’s going to set the direction for the oil market

- Italy’s Di Maio says ’climate is changing’ in budget talks with EU

- U.K. Trade Sec Fox says possibility of no Brexit if parliament rejects deal

- Trump believes will make China deal ’either now or into the future’

- China calls U.S. trade meeting ’very successful’; will quickly implement

- OPEC+ nations didn’t yet discuss proposals to cut production: Kuwait Min

Asian stock markets were pressured following the sell off on Wall Street where doubts regarding a US-China trade deal saw all US majors drop over 3% in which the S&P 500 fell below its 200DMA and DJIA lost near 800 points on the day. This weighed heavily on the China-sensitive sectors in the US such as Industrials, Materials and Tech, while Financials took the biggest hit amid a slump in yields and ongoing yield-inversion. ASX 200 (-0.8%) was led lower by tech and financials with disappointing Q3 GDP adding to the downbeat tone, while Nikkei 225 (-0.5%) also finished negative albeit off worse levels as USD/JPY attempted to nurse losses. Elsewhere, Hang Seng (-1.6%) and Shanghai Comp. (-0.6%) conformed to the downbeat tone but with the declines in the region less drastic than the bloodbath observed stateside following stronger than expected Chinese Caixin Services PMI which jumped to a 5-month. Furthermore, there was a seemingly concerted effort by some officials to dispel the trade-related doubts in which White House Trade Adviser and ‘China hawk’ Navarro suggested to give talks a chance and that it is premature to lose faith in US-China discussions, while Mofcom also declared the US-China trade meeting was successful although Trump remained unrelenting and reiterated his threat of tariffs if they fail to reach a deal. Finally, 10yr JGBs initially rose to levels last seen over 2 years ago amid safe-haven demand and as they tracked the upside in T-notes. However, prices then pulled back to return flat after the BoJ’s bond buying operation in which it upped purchases in the 10yr-25yr maturities by JPY 20bln, as the bank is on course to reduce monthly purchases of superlong JGBs by JPY 150bln if it continues at the current pace given the previously announced reduction of operations for December.

Top Asian News

- India’s Sensex Extends Decline as RBI Holds Rates, Policy Stance

- IPhone Lens-Maker Largan Warns of December Sales Slide

- India Holds Interest Rates After Inflation Undershoots Forecast

- Japan Eases Changes for Tariffs on Delayed Solar Projects

European bourses (Eurostoxx -0.9%) have followed suit from their US and Asia-Pac counterparts to trade lower across the board as the trade-inspired optimism seen at the start of the week continues to dissipate. China’s Mofcom declared the USChina trade meeting as successful, although were said to be puzzled and irritated by the Trump administration’s triumphant rhetoric. This came after Trump yesterday branded himself as a ‘Tariff Man’ and also tweeted that the US will either have a real deal with China or no deal at all and that the US will levy major tariffs against imports of Chinese products if a deal is not made with China. In terms of sector specifics, all ten majors trade in the red with IT, materials and industrials lagging their peers. Downside in financial names has also been hampered by the current yield environment as markets continue to speculate over the Fed’s 2019 rate hike plans in lieu of recent comments from Fed Chair Powell and with the German 10yr yield briefly slipping below 0.25%. UK homebuilders have seen some reprieve this morning (Berkeley Group +8.1%, Taylor Wimpey +6.3%, Barratt Developments +6.5%) after Barclays highlighted the sector as a potential major beneficiary of a Brexit deal being passed in Parliament. Individual movers include Shire (+2.6%) who stand near the top of the Stoxx 600 after amid shareholder approval for their merger with Takeda Pharmaceutical. Elsewhere, broker downgrades have placed weight on names such as Hargreaves Lansdown (-3.3%), Saint Gobain (-3.2%) and Osram Licht (-1.7%).

Top European News

- Weak Euro-Area Growth Is Here to Stay as Italy Recession Looms

- U.K. Services Unexpectedly Weaken to Worst Since July 2016

- Yandex Starts Selling $270 Smartphone to Rival Google in Russia

- Telia Sells Uzbek Unit That Cost It Almost $1 Billion in Fines

In FX, AUD,NZD – AUD the major G10 underperformer in light weaker-than-expected Q3 Aussie GDP (slowest pace of growth in two years, and well below consensus) which dragged AUD/USD to sub-0.7300 levels vs. highs of 0.7356 and not far from 0.7400 in recent sessions. Meanwhile, AUD/NZD slumped through 1.0600 to circa 1.0525, to the benefit of the Kiwi that managed to maintain 0.6900+ vs. the buck.

- GBP – Choppy trade for the Pound amid ongoing Brexit pandemonium after UK PM May suffered a hat-trick of defeats, giving more power to Parliament if her deal is voted down in next week’s meaningful vote. Cable currently trying to recover having slumped to a new YTD low yesterday at 1.2659 (ahead of the psychological 1.2650), with a rebound through 1.2700 and 1.2750, albeit amidst a generally softer USD and despite a worryingly weak services PMI (headline just above 50). Similarly, Sterling has regained composure against the EUR, with the cross back down below 0.8900 even though the single currency has pared losses elsewhere amid ECB sourced talk about discussions over further policy normalisation next year. Indeed, EUR/USD is back above 1.1350 from close to 1.1300 at one stage.

- CAD – USD/CAD is within striking distance of 1.3300 (vs. yesterday’s lows of 1.3160) as retreating oil prices weigh on the Canadian currency with traders also eyeing the BoC interest rate decision later today. No change in the policy is expected though focus will be on the tone of the statement given the recently battered energy complex. For a more detailed preview, refer to our research suite or headline feed.

- EM – Lira trades around the middle of a 5.4518-.3345 range vs. the Greenback after the CBRT set their inflation target at 5% (vs. November CPI at 21.62%) and pledged to do more to bring consumer prices back down, cushioning the TRY from wider bearish and risk averse sentiment.

- DXY – Given all the above, the broad Dollar and index have handed back some of Tuesday’s pronounced gains made amidst the Wall St. selloff, and ahead of today mark of respect day for passed President George H.W Bush. DXY pivoting 97.000 within a range 97.206-96.827.

In commodities, WTI (-0.2%) and Brent (-0.3%) bounced off lows as the JMMC meeting goes underway, with the Omani Oil Minister hinting at a 3-6 month production cut ahead of tomorrow’s key OPEC meeting. Furthermore, The WSJ reports that OPEC delegates are concerned that Saudi and Russia are making output agreements without input from OPEC; it was also stated that the Russia-Saudi relationship was a key factor in Qatar’s withdrawal. Markets will be looking ahead to the postponed EIA weekly data coming out tomorrow following the unexpected API build, alongside the OPEC meeting with emphasis on any decision to cut oil production that may arise. Reports today by RIA stating that OPEC wants Russia to reduce oil output by a minimum of 300k BPD. However, TASS has reported that Russia is only seeking a symbolic production cut which follows previous reports that they would only agree to a 140k BPD cut. Elsewhere, Libya’s NOC stated that all port terminals are shut due to bad weather, with storage capacity at Zawiya (usual production of 120k BPD) affected and the 300k BPD Sharara oil field production to be cut by 50% tomorrow morning. Gold has weakened from the 5-week high reached in the previous session, as the dollar is marginally firmer. The majority of base metals have fallen due to being weighed on by US-China trade tensions following US President Trump commenting that there will have a real deal or no deal at all with China. Separately, China’s construction steel rebar is up

US Event Calendar

- 7am: MBA Mortgage Applications, prior 5.5%

- 2pm: U.S. Federal Reserve Releases Beige Book

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 16.15 POINTS OR 0.61% //Hang Sang CLOSED DOWN 440.76 POINTS OR 1.62% //The Nikkei closed DOWN 116.72 OR 0.52%/ Australia’s all ordinaires CLOSED DOWN 0.84% /Chinese yuan (ONSHORE) closed DOWN at 6.8570 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 52.99 dollars per barrel for WTI and 61.95 for Brent. Stocks inEurope OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.8570AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8581: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

Last night China dismisses the confusion by saying the meeting with Trump was very successful. However the difficult part of the deal will be how China and the uSA handle intellectual property theft.

(courtesy zerohedge)

China Dismisses Confusion Claims, Says “Very Successful” Meeting With Trump

Following a story from The Washington Post quoting a former U.S. government official who was said to have been in contact with Chinese officials, claiming Beijing are “puzzled and irritated” by the Trump administration’s behavior, and widespread confusion across media claiming the ‘truce’ as a nothingburger; China’s Ministry of Finance has denied any confusion or negativity exists.

The WaPo report went to claim the unknown former US official said:

“You don’t do this with the Chinese. You don’t triumphantly proclaim all their concessions in public. It’s just madness,” the former official, who asked for anonymity to describe confidential discussions, told the Post.

While President Trump’s dinner with Chinese leader Xi yielded a cease-fire in the trade war between the world’s two biggest economies,judging by the market’s moves today, the details are proving less than satisfying to those hungering for a lasting truce.

But, tonight, China says trade meeting with U.S. is “very successful” and is “confident” to implement the results agreed upon at the talks, according to a statement on Ministry of Commerce website.

A reporter asked: We know that the Chinese economic and trade team has returned to Beijing. What is your comment on this meeting?

A: The meeting was very successful and we have confidence in the implementation.

Q: How is China prepared to promote the next economic and trade consultation?

A: The economic and trade teams of the two sides will actively promote the consultation work within 90 days in accordance with a clear timetable and road map.

Q: What are the priorities for China?

A: China will start from implementing specific issues that have reached consensus, and the sooner the better.

Of course, as Torsten Slok, chief international economist at Deutsche Bank AG said:

“The market wants to see more details before it can make up its mind,

It remains unclear for the market whether the trade war will escalate or deescalate from here.”

And, as Axios reports, Mike Pillsbury is worried Trump’s negotiations with China are unraveling. The hawkish former Pentagon official — who Trump has called “probably the leading authority on China” and who reportedly huddled with Trump in the Oval the day before Trump left for his G20 meeting with President Xi — said “there’s a risk the deal will come undone.”

Pillsbury said he’s “getting warnings from knowledgeable Chinese about the American claims of concessions” that the Chinese have said they never made. These contradictions include U.S. claims that the Chinese agreed to “immediately” address their most egregious industrial behavior, to “immediately” restart purchases of U.S. agriculture, and to slash tariffs on American cars.

“I have advised the president’s team that for the past 40 years the American side avoids disclosing Chinese concessions before the final agreed written statement is released,” Pillsbury told me in a phone interview today.

Sounds an awful lot like WaPo’s anonymous source? And is the opposite of the official word from China.

Pillsbury’s comments were rapidly followed by White House trade adviser Peter Navarro who told Fox News that it would be premature for people to “lose faith” in the trade discussions the U.S. is holding with China.

“The Chinese haven’t even gotten back to China yet,” Navarro tells Fox in an interview;

“Let’s give it some time”

Navarro says he is bullish on the economy and “I’m bullish on this deal”

Navarro also noted he is optimistic about progress being made over market access and structural changes with China during the 90 day-period in which the talks will be held.

However, Navarro did admit that communication by the administration over the outcome of the talks perhaps could have been better,pointing out, echoing Mnuchin’s earlier comments, that the market may be “trying to parse whether the Fed’s going to raise interest rates again,” which Navarro says would be a mistake.

Nevertheless, President Trump would have the last word once again,

insisting, as he did earlier that “We are either going to have a REAL DEAL with China, or no deal at all…”

Donald J. Trump

✔@realDonaldTrump

We are either going to have a REAL DEAL with China, or no deal at all – at which point we will be charging major Tariffs against Chinese product being shipped into the United States. Ultimately, I believe, we will be making a deal – either now or into the future….

Donald J. Trump

✔@realDonaldTrump

…..China does not want Tariffs!

Which some may interpret as Trump giving himself an ‘out’ if things don’t work out – although “Tariff Man” has been consistently hawkish.

end

4.EUROPEAN AFFAIRS

ECB

This is going to hurt USA hegemony: the ECB just launched a better than blockchain instant payment system. Now will the big banks play along?

(courtesy Don Quijones/WolfStreet)_

ECB Just Launched “Better Than Blockchain”

Instant Payments System

But will the big banks play along?

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

On Friday the ECB launched, with minimal fanfare, a brand new system aimed at enabling banks to settle payments instantaneously across Europe, helping them to compete with PayPal and other global tech giants. Developed in little over a year, the ECB’s not-for-profit TARGET Instant Payment Settlement (TIPS) system will let people and businesses in Europe transfer euros to each other almost instantly, at extremely low cost, and irrespective of the opening hours of their local bank.

The first ever payment via TIPS took place on Friday between a customer of Spain’s CaixaBank and one of French bank Natixis. The payment went through in a matter of seconds.

“In launching TIPS, the Eurosystem is acknowledging the changing reality that digitization is erasing the borders between wholesale and retail,” said ECB Executive Board Member Yves Mersch at the TIPS launch event, in Rome. Mersch was one of the senior European central bankers who oversaw the new payment system’s roll out, work on which began in June 2017.

Earlier this year he bragged to Bloomberg that the new system would leave blockchain in the dust. “TIPS is 10 seconds, 0.2 cents. DLT transactions are at best 30 euros and take at least one hour,” Mersch said. “We have a mandate for efficient payment systems, and we go for efficiency. We are not bound to a technology, we are bound to results.”

TIPS was developed as an extension of TARGET2, the ECB’s real-time gross settlement platform for euro payment transactions, and settles payments in central bank money. The newly launched system currently only settles payment transfers in euros, the ECB says on its website, but “in case of demand, other currencies could be supported as well.”

According to Mersch, the TIPS system has put in place “three strong building blocks” for unleashing the potential for retail payments innovation in Europe:

- The standardization and harmonization of business rules: One year after its launch, more than 2,000 payment service providers from 16 different countries — roughly half of all of Europe’s payment service providers — have joined the TIPS scheme, “proving their commitment by following the Euro Retail Payments Board guidance on instant payments.”

- A state-of-the-art market infrastructure: TIPS is a “truly domestic market infrastructure for pan-European instant payments” with settlement in central bank money. Using TARGET2 as a basis, TIPS “can provide wide reach and scale, tapping into an established network of over 1,700 participants and more than 51,000 addressable Business Identifier Codes (BICs).”

- A sound legal basis: “The revised Payment Services Directive (PSD2) provides the legal framework for retail payments innovation by setting rules for third-party payment service providers. PSD2 enhances consumer protection and increases security for payment services.” But it is still not fully implemented.

One major obstacle holding TIPS back is the low number of banks that have agreed to participate in the scheme. So far, just eight mostly medium- or small-sized banks from Spain, Germany and France have signed up, with Spain’s BBVA the only A-league banking giant to have joined so far. The other participants are Spain’s CaixaBank, Abanca Corporación Bancaria, Banco de Crédito Social Cooperativo and Caja Laboral Popular Cooperativa de Crédito, French bank Natixis and Germany’s Berlin Hyp and Teambank.

“We need to address the reasons for the scarcity of major European players in the payments market,” ECB director Yves Mersch said. “If there is a lack of investment capacity…we should not shy away from pooling resources and volumes and creating bigger players.”

The lack of participation in the initiative is not due to a lack of interest in instant payment (IP) solutions. During a poll conducted by the ECB itself at a banking event in February, 61% of the banks in attendance said they are actively preparing for the roll out of IP; 15% of the audience believe IP will be the new norm within one year; 63% expect a take-up in the coming five years; and 21% believe that regulation is necessary to drive IP adoption.

As we reported a year ago, big banks on both sides of the Atlantic are all over blockchain technology and have been pouring money into developing their own “digital currencies.” They include European too-big-to-fail giants like Santander, Deutsche and UBS, which, alongside New-York based BNY Mellon, have been working together to create a digital currency known as Utility Settlement Coin (USC), which will facilitate payment and settlement for institutional financial markets.

It’s easy to see the lure blockchain holds for alpha lenders such as these: Combining shared databases and cryptography, the technology offers multiple parties simultaneous access to a constantly updated digital ledger that cannot be altered. With it, banks could offer a safer, faster, cheaper, more transparent service to their customers, while doing away with the need for a central operator.

Settlements could be executed almost instantaneously on a bank-by-bank basis rather than having to be netted at the end of each working day by the respective central bank. The subsequent cost savings could be huge.

But now the ECB may have stolen their thunder, by launching a cross-continental instant payments system. By doing so, it has become the first major global central bank to try to offer an alternative to the payment systems offered by tech giants such as Apple, Google, PayPal and Amazon that currently dominate Europe’s digital payment industry.

Unlike cryptocurrencies, TIPS is highly centralized. It is also largely untested, at least at the sort of levels the ECB aspires to achieve, offers zero anonymity and is extremely low-cost, with a transaction fee of just 0.2 cents and no entry or account maintenance fees, which is great news for bank customers but not such great news for banks themselves.

This may help explain why only eight out of thousands of European lenders have so far signed up to the system. But rest assured that in the coming months the ECB will do everything it can within its not insignificant power to change that dynamic.

end

ITALY/EU

Tria is probably the “sole” adult in the room of Italian ministers. His departure will be a death blow to the Italian economy

(courtesy zerohedge)

Italian Economy Minister Said Close To Resigning Over

Rift With PM

As Italy’s ruling populists hint that they would be open to lowering their budget deficit target (on the condition that they have enough left over to fulfill their campaign promises for generous tax cuts and social welfare programs), investors in Italian bonds are happier than they have been in months. Yields on Italian bonds declined to their lowest level in five months, having erased the entirety of their budget conflict-inspired rise, on reports that the EU might be willing to shelve its “Excessive Debt Proceedings” if the Italians agree to a meaningful reduction.

But amid the sudden shift in the relationship between the EU and the leaders of the bloc’s third largest economy, one Italian newspaper appeared determined to spoil the fun. La Corriere della Sera published a story on Wednesday claiming that Economy Minister Giovanni Tria – who is still viewed by investors as the adult in the room, despite having set aside his concerns about fiscal prudence by comparing a budget-deficit reduction to “suicide” – might be looking to leave the government before the new year, according to Bloomberg.

According to the report, Tria is “more tempted” to leave than before, and is privately said to be contemplating departing his post during the period between Christmas and New Year’s, after the budget has (hopefully) been approved by the EU. Tria is said to be “tired” of attacks on his credibility and has become increasingly dissatisfied with Prime Minister Giuseppe Conte, who recently told the Italian press that he would be “in charge” of talks with Brussels. According to media reports, Conte is preparing to deliver another budget draft to the EU that would shrink the projected deficit to 2%. Conte told the newspaper La Repubblica that he believes the government can shave 2 billion euros off the cost of its “citizens income”. But since Conte has taken on the role of lead negotiator, Tria has felt “paralyzed” and is struggling to find a new place in the government. The economy minister skipped a Q&A with lawmakers that followed the government’s trip to negotiate with Brussels because Conte handled it.

Yesterday, Tria told reporters following a meeting with EU finance ministers that the government’s pension reform plans would be preserved, adding that talks were “collegial”, though he declined to say what specifically had been discussed, according to Reuters.

When asked by reporters, Deputy Prime Minister Matteo Salvini denied the rumors and claimed that Tria and Conte “get along well.”While Italy appears to be making progress, Tria’s departure could easily spoil the recovery in Italian assets by adding to concerns about the Italian economy, which contracted during the three months through September. And “soft” data – specifically the November PMI – released since then suggest that the slowdown will only continue. Manufacturing shrunk at its fastest pace in four years last month, according to the data.

If Tria leaves, expect investors to worry that the populists’ recent flirtations with a more disciplined budget deficit could fizzle after the departure of the one “adult in the room.”

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

SAUDI ARABIA/USA

Many senators have seen the evidence and conclude that the Crown Prince MbS orchestrated the murder. Let us see how this will play out in the future.

(courtesy zerohedge)

Senators Convinced By CIA’s “Smoking Saw” Evidence

Crown Prince Orchestrated Khashoggi Murder

Trump’s attempt to keep the Saudi Crown Prince away from the spotlight – and keep pumping as much oil as possible to keep the price of oil low – just suffered a major blow when US senators said a classified CIA memo convinced them that Saudi Crown Prince Mohammed bin Salman played a role in dissident columnist Jamal Khashoggi’s dismemberment, with one describing the evidence as “a smoking saw.”

Foreign Relations Chairman Bob Corker of Tennessee rejected Jared Kushner’s Donald Trump’s efforts to downplay the prince’s role, and according to Bloomberg said that if a jury were to consider a case against Prince Mohammed, he’d be convicted of murder in 30 minutes.

“There is zero question in my mind that the crown prince directed the murder and was kept apprised of the situation all the way through,” Corker said Tuesday after the closed-door briefing with CIA Director Gina Haspel and a handful of senators. “Zero question in my mind.”