GOLD: $1243.00 DOWN $2.00 (COMEX TO COMEX CLOSINGS)

Silver: $14.77 UP 2 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1242.90

silver: $14.76

For comex gold and silver:

DEC

Again, we have Goldman Sachs dealer and JPMorgan customer account stopping (receiving the gold) 49/71 contracts.

EXCHANGE: COMEX

CONTRACT: DECEMBER 2018 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,244.400000000 USD

INTENT DATE: 12/12/2018 DELIVERY DATE: 12/14/2018

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 36

323 C HSBC 4

657 C MORGAN STANLEY 1

661 C JP MORGAN 13

690 C ABN AMRO 24

737 C ADVANTAGE 45 12

800 C RCG 2 2

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 71 71

MONTH TO DATE: 7,208

NUMBER OF NOTICES FILED TODAY FOR DEC CONTRACT: 71 NOTICE(S) FOR 7100 OZ (0.2208 tonnes)

SILVER

FOR DECEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

279 NOTICE(S) FILED TODAY FOR 1395,000 OZ/

Total number of notices filed so far this month: 3873 for 19,365,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3404: DOWN 22

Bitcoin: FINAL EVENING TRADE: $3304 down 143

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A GOOD SIZED 1005 CONTRACTS FROM 174,071 UP TO 175,076 WITH YESTERDAY’S 22 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 20 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2446 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2446 CONTRACTS. WITH THE TRANSFER OF 2446 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2446 EFP CONTRACTS TRANSLATES INTO 12.23 MILLION OZ ACCOMPANYING:

1.THE 22 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

NOW 20.730 INITIALLY STAND FOR DECEMBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DEC: 16,394 CONTRACTS (FOR 9 TRADING DAYS TOTAL 16.394 CONTRACTS) OR 81.97 MILLION OZ: (AVERAGE PER DAY: 1821 CONTRACTS OR 9.107 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 81,97 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 11.71% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,759.03 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

ACCUMULATION FOR NOVEMBER /2018: 247.18 MILLION OZ

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1005 DWITH THE 22 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY.. AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2446 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 3451 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2246 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1005 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 22 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.75 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .875 BILLION OZ TO BE EXACT or 125% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DEC MONTH/ THEY FILED AT THE COMEX: 279 NOTICE(S) FOR 1,395,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./AND NOW DEC. AT 20.730 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 2485 CONTRACTS UP TO 404,735 WITH THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $3.05//.YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 11080 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 11080 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 404,735. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 13,565 CONTRACTS: 2485 OI CONTRACTS INCREASED AT THE COMEX AND 11080 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 13.565 CONTRACTS OR 1,356,500 OZ = 42,19 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A GAIN IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $3.05

YESTERDAY, WE HAD 9745 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC : 76079 CONTRACTS OR 7,607,900 OZ OR 236.63 TONNES (9 TRADING DAYS AND THUS AVERAGING: 8453 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAYS IN TONNES: 236.63 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 236.63/2550 x 100% TONNES = 9.27% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 7001.01 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018: 552.88 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 2485 WITH THE GAIN IN PRICING ($3.05) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11080 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11080 EFP CONTRACTS ISSUED, WE HAD AN HUMONGOUS GAIN OF 14,788 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11080 CONTRACTS MOVE TO LONDON AND 2485 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 42,19 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE RISE OF $3.05 IN YESTERDAY’S TRADING AT THE COMEX

we had: 71 notice(s) filed upon for 7100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $2.00 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 763.56 TONNES

Inventory rests tonight: 763.56 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 2 CENTs TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 318.735 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GOOD SIZED 1005 CONTRACTS from 174,071 DOWN TO 175,076 AND MOVING FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2446 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2446 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1106 CONTRACTS TO THE 2446 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 3451 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 17.26 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. AND NOW 20.730 MILLION OZ STANDING IN DECEMBER.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 22 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 2446 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 31.90 POINTS OR 1.23% //Hang Sang CLOSED UP 337.64 POINTS OR 1.29% //The Nikkei closed UP 213.44 OR 0.99%/ Australia’s all ordinaires CLOSED UP 0.14% /Chinese yuan (ONSHORE) closed UP at 6.8811 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 50.58 dollars per barrel for WTI and 59.62 for Brent. Stocks in Europe OPENED MIXED//. ONSHORE YUAN CLOSED UP AT 6.8764AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8811: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

i

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)Another indicator highlighting the growth problems inside China. Today is the total collapse of Chinese auto sales. It is their first decline in 30 years.

( zero hedge)

ii)We now have a second Canadian citizen who has been suddenly “disappeared” in China

4/EUROPEAN AFFAIRS

i)UK

the mess that Gr Britain finds itself today. May returns to Brussels but she will come back empty handed. She will lose a vote of no confidence but there is no Conservative willing to take on the job in this quagmire.

( zerohedge)

ii)ITALY

Not sure of the story but it seems that Italy has revised its budgetary deficit to 2.0% and that sent Italian bonds and their stock market higher. We are also not sure if the EU will accept this. I am surprised that Italy lowered its budgetary deficit in light of what France wants to do: increase its budgetary deficit to 3.5%

( zerohedge)

( zerohedge)

v)GERMANY/MERKEL

seems that the new leader of the CDU is a mirror image of Merkel

( Tom Luongo)

vi)ECB

The ECB today confirms that it will end asset purchases. However it will reinvest maturities in full and that will help Italy for a short time. They will probably do a sell short term bonds and buy long term to also help keep Italian bonds yields low.

( zerohedge)

vii)Tom Luongo explains what is going on in Europe right now with France and England in the centre of things

( Tom Luongo)

viii)Investors were not happy with the key words used by Draghi: there are now “downside risks” and GDP and inflation forecasts have been cut….down goes the Euro

(courtesy zerohedge_

ix)A multi billion hedge fund just reports a record loss (GAM holdings). It is one of Eurpe’s largest alternative money managers. It has frozen withdrawals at some of their bond funds after a huge surge in redemptions.

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)RUSSIA/USA

Butina now admits in court to being a Kremlin agent and it sought to influence politics through the NRA. She has no influence and did not meet Trump or any of their election staff.

( zerohedge)

6. GLOBAL ISSUES

CANADA

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)Venezuela

Socialism at its finest:

The big Goodyear plant has decided to shutter its sole remaining plant and then as a Christmas bonus it is giving tires out as severance

(courtesy zerohedge)

9. PHYSICAL MARKETS

iii)A good one tonight from bill Holter as he warns be crash alert as we are no doubt facing the huge global margin call

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

The following is a very important data point: USA import and export prices plunge with fuel prices one of the culprits. However there is no question that China is sending deflation our way

( zerohedge)

3 Trump tweet storm:

a)Trump distances himself from Cohen

b) threatens GM again

c) hopes the Fed will not hike interest rates any more:

(zerohedge)

iv)SWAMP STORIES

a)Trump claims that he never directed Michael Cohen to break the law. He correctly states that Cohen is a lawyer and he ought to know the law. Trump also sstates that Cohen pled guilty to finance issues which were not criminal but used by Mueller to embarrass Trump

( zerohedge)

b)This is getting quite out of hand: now the New York Attorney General (staunch Democrats) have started a criminal probe into trump inauguration spending’

(courtesy zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of DECEMBER and here in this front month of December we now have 552 contracts standing for a LOSS of 78 contracts. We had 173 contracts stand for delivery yesterday so we gained 95 contract or an additional 475,000 oz will not stand for delivery as these guys morphed into London based forwards as well as accepting a fiat bonus.

After December we have the non active January contract month and here we saw a gain of 9 contracts up to 1909 contracts. February saw its another 16 contract gain to stand at 98. March, the next big delivery month after December saw a gain of 1341 contracts down to 144,759

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

we still have not had any adjustments out of the dealer to the customer account to signify a settlement

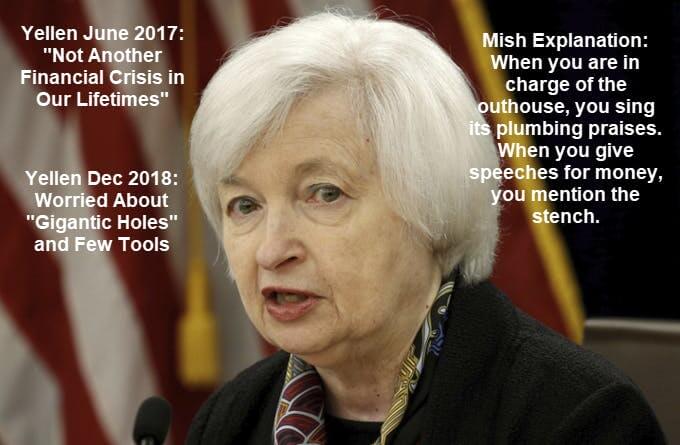

Yellen Warns Another Financial Crisis Is Brewing

– ‘Gigantic holes in the system’ warns former Fed Head

– Interest rates will remain lower than they have been in past

– Leveraged loans pose risks and there is unfinished regulation

– “I think things have improved, but then I think there are gigantic holes in the system”

– No new financial crisis in ‘our lifetimes’, Yellen said only last year

– Editors note: Yellen should know as she and her predecessors are responsible for some of the “gigantic holes”

Image Source: Mike Shedlock

Former Federal Reserve Chairperson Janet Yellen told an audience in New York that she fears there could be another financial crisis brewing.

She warned of leveraged loans and the inability for the Fed to bail out banks. She said that banking regulators have seen reductions in their authority to address banking and financial panics and warned of the current push to deregulate.

“I think things have improved, but then I think there are gigantic holes in the system,” Yellen warned Monday evening.

“The tools that are available to deal with emerging problems are not great in the United States,” she said in a discussion moderated by New York Times columnist Paul Krugman at CUNY.

Yellen warned that leverage loans are an area of concern, something also mentioned by the current Fed leadership.

Secure Storage Ireland – Click here for information

Secure Storage Ireland – Click here for information

News and Commentary

May Returns to Brexit Front Line After Surviving Tory Ambush (Bloomberg.com)

Gold edges lower, palladium hits record high (Reuters.com)

Asia stocks rally into a second day with Hong Kong markets in the lead (MarketWatch.com)

Gold settles higher as inflation in line and the dollar takes a dip (MarketWatch.com)

Stocks cheered by Trump trade talk; sterling claws off lows (Reuters.com)

Source: Marketwatch

Bitcoin Was a Bubble. And It Popped (IndiaTimes.com)

Bitcoin’s collapse looks familiar to bubble watchers (MarketWatch.com)

S&P 500 lows? We ain’t seen nothing yet, says Gundlach (MarketWatch.com)

Why Gundlach Is “Scared Sick” Of The Global Economy (ZeroHedge.com)

Germany Accelerates Plans For Deutsche Bank-Commerzbank Megamerger (ZeroHedge.com)

Gold Technical Analysis: Gold has formed a bull flag (FXStreet.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

12 Dec: USD 1,244.75, GBP 993.31 & EUR 1,098.24 per ounce

11 Dec: USD 1,248.25, GBP 988.99 & EUR 1,096.59 per ounce

10 Dec: USD 1,246.80, GBP 980.61 & EUR 1,092.57 per ounce

07 Dec: USD 1,241.20, GBP 972.98 & EUR 1,091.51 per ounce

06 Dec: USD 1,236.45, GBP 971.48 & EUR 1,091.66 per ounce

05 Dec: USD 1,236.15, GBP 970.13 & EUR 1,090.16 per ounce

Silver Prices (LBMA)

12 Dec: USD 14.66, GBP 11.68 & EUR 12.93 per ounce

11 Dec: USD 14.64, GBP 11.62 & EUR 12.85 per ounce

10 Dec: USD 14.53, GBP 11.48 & EUR 12.73 per ounce

07 Dec: USD 14.49, GBP 11.34 & EUR 12.73 per ounce

06 Dec: USD 14.38, GBP 11.28 & EUR 12.68 per ounce

05 Dec: USD 14.48, GBP 11.34 & EUR 12.75 per ounce

Recent Market Updates

– Gold Krugerrand Coin Worth $1,200 Donated To Charity Again

– EU Recession Imminent – Euro Disunion as Brexit, Italy and End of QE Loom

– Gold and Silver Gained 2% and 3% Last Week While Stocks Dropped Nearly 5%

– Irish Central Bank Refuses To Discuss Gold Reserves In Bank of England Vaults

– “Fake Markets” To Lead to Global Financial Crisis? – Goldnomics Podcast

– Gold Is “Coiled” and Looks Set To Surge Like Natural Gas — Bloomberg Intelligence

– “Collapse Of Civilisation Is On The Horizon” – Attenborough Warns World Leaders

– Deutsche Bank May Cause The Next Global Crisis

– Ireland’s Mr Gold Reveals Nuggets Of Wisdom For When The Next Crash Comes

– BREXIT May Lead to UK Property Crash and Depression

Barrick moves closer to resolving Acacia dispute with Tanzania

By Danielle Bochove, Thomas Biesheuvel, and Kenneth Karuri

Bloomberg News

Wednesday, December 12, 2018

Barrick Gold Corp. has reached an agreement with the Tanzanian government on a $300 million payment, a milestone toward resolving a dispute that has crippled the miner’s subsidiary in the African country, according to people familiar with the situation.

Executives from the Toronto-based producer and Randgold Resources Ltd., which is being bought by Barrick, met with Tanzanian negotiators on Dec. 7, said the people, who declined to be identified as the talks are private.

During that meeting the two sides made significant progress on a deal that includes Acacia Mining paying $300 million in installments. The terms are now being handed off to a tax working group in Tanzania for review, the people said. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-12-12/barrick-gold-is-said-…

END

No surprise here: the CFTC refuses to address questions posed by Chris Powell and myself on the gold and silver rigging

(courtesy GATA/ChrisPowell)

CFTC refuses to address GATA’s questions about gold and silver market rigging

12:21p ET Thursday, December 13, 2018

Dear Friend of GATA and Gold:

The U.S. Commodity Futures Trading Commission has refused to reply to or even to acknowledge GATA’s questions about manipulation of the gold and silver futures markets that are purportedly regulated by the commission.

By letters in July and September, GATA asked the commission to explain the explosion in the use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodity Exchange; to determine whether gold futures prices had been linked by the Chinese government’s manipulative trading to the value of the yuan; and whether the commission has jurisdiction over manipulative futures trading by the U.S. government itself.

GATA’s letters are posted here:

Having gone months without any acknowledgment from the commission, GATA asked your secretary/treasurer’s U.S. representative, John B. Larson, Democrat of Connecticut’s 1st District, to press the commission to reply, which his office did several times.

Today Larson’s office forwarded a copy of a letter put into the mail to GATA yesterday by the commission’s director of legislative affairs, N. Charles Thornton III. But Thorton’s reply is little more than a form letter, outlining the commission’s general objectives and purposes. Thornton makes no reference to GATA’s questions:

http://gata.org/files/CFTCReply-12-12-2018.pdf

Ordinarily a response so vapid could be considered insulting, but it fairly may be considered confirmation that the U.S. government and other governments are surreptitiously rigging commodity markets, as has been strongly suggested by the official filings of CME Group, operator of the New York Commodities Exchange and other commodities exchanges in the United States. These filings confirm that governments and central banks are among the exchange operator’s clients and receive discounts from the exchanges for their secret trading of all commodity futures contracts:

http://www.gata.org/node/14385

http://www.gata.org/node/14411

GATA’s correspondence with the CFTC shows how easy it is to demonstrate government instigation of or complicity with market manipulation. Since demonstrating this is so easy, the bigger challenge is to persuade mainstream financial news organizations to pursue the issue and to persuade commodity-producing companies and their investors to agitate against it.

You can help by bringing GATA’s work to their attention and urging them to act.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

People continually ask “when” will it happen? For the last 6 months we have responded “it is happening right before your very eyes”! In fact, as of this morning 52% of global markets are now down over 20% from their highs and qualifying as bear markets. Please understand the financial backdrop these weakening markets are falling into. Bluntly, the world is facing a giant margin call that cannot be met.

Liquidity had become extremely tight even as markets made their high water marks. It is this lack of liquidity which threatens to become a self reinforcing flash crash to hell via margin calls. “Don’t worry” they say, central banks will come to the rescue. There is one fundamental problem with this line of thought, the value of the issued currencies themselves. There is zero mathematical way to service and pay off current debt with current currency values … currencies must be massively printed and thus devalued if they are to pay off the mountains of debt! Central banks created the problem, they will not be the solution. Rather, their demise will be part of the solution.

Looking at the backdrop that a revolving door of “buy the dip(pers)” on CNBC assure us is the right thing to do, the list is many and for the most part the issues are carved in stone. Obviously number one on the list are the levels of consumer, corporate, state and sovereign debt. By any measure, we have never been at current levels. Then we have the current unfunded pension problem. This is not just a US problem, it is a $400 trillion mathematical sinkhole seen worldwide.

We can of course add in “valuations”. Current valuations of everything from stocks, bonds, real estate or nearly everything considered an “asset” are at levels not supported by anything including common sense. A move back to the mean would be considered a crash … but pendulums (markets)rarely work that way. Markets almost always overshoot fair value in both directions up and down. The problem which few talk about is markets have “become” the economy. A huge bet was made in belief higher asset values would produce a “wealth effect” and the real economy would levitate. This only bought time but now time is up, declining markets are now eliciting a reverse effect. We are witnessing the end of a global Ponzi scheme where no new money is entering and players are beginning to leave. Remember, fear is a far greater emotion than greed!

One very important area to address is the latest trade issues with China. They have spent years setting up trade deals/routes, clearing facilities as an alternative to SWIFT, financing facilities and of course buttressing their reserves with physical gold. China’s imports of US goods dropped 25% from last November so tariffs are obviously beginning to bite.

Now for the reason I am issuing this warning, last week we found out Huawei’s CFO was arrested in a Canadian airport over violating US sanctions on Iran . I cannot stress how important/dangerous this event is! First, is a Chinese citizen running a Chinese company bound by US law? Not to mention the “timing” of her arrest which occurred while Presidents Trump and Xi were meeting in Argentina. Mr. Trump says he was not aware of the arrest at the time. I don’t know which would be more troubling, whether he knew of the arrest and lied or had no clue the arrest was taking place?

Please consider the ramifications here. This is the equivalent of the CFO of Microsoft being arrested in Thailand, thrown in jail without bail awaiting extradition to Beijing! China will retaliate in violent fashion if she is not released and profuse apologies not given publicly. The bottom line is this, we have weaponized the SWIFT system at the very same moment global players are already questioning the use of dollars for trade… Did they really need anything else as a dollar disincentive?

Also understand the connection between trade, GDP and thus cash flow …versus the ability to service the outsized debt. At the very moment more cash flow is needed, this action on trade will act to turn off the spigot! What we now face is a credit freeze up like 2008-09 with no white knight waiting in the wings with a fire hose of needed liquidity. …And the Fed will again raise rates this month and continue to shrink their balance sheet? This would all be hilarious if it didn’t mean our way of life as we “knew” it will be destroyed.

To finish, do we get a bounce and some relief? Markets are very oversold and short term they are certainly due a bounce, but do we get it? It does not matter because the debt (mathematically unpayable in current currency values) is already in place …and debt does not ever go away until it is either paid, restructured or defaulted. The financial snake has already taken its tail into its mouth and has been swallowing for six months or more already. The only question is how long it will take for marginal players to make the decision the snake will in fact eat itself, and liquidate their positions … or alternatively receive margin calls and be forced into liquidation?

This is NOT the time to be a deer in the headlights! We will look back and see this final chapter as one where a massive flight from “liability” took place. The problem of course is that most all assets either are liabilities themselves or have values bid up via liabilities (loaned capital). All past financial panics were best survived by hiding in “cash”. Today, this sector is comprised by a dichotomy where one side is purely liability of a central bank or has no liability at all. The non liability side (gold and silver) also has a rocket booster attached in the form naked sales. Trolls for years have laughed at this fact as it did not matter …until it does. The amount of REAL gold and silver available for delivery is now miniscule at the very moment in time a position of non financial liability is mandatory! COMEX represents a registered gold inventory of a whopping 4 tons. A cash call by China will expose the fractional reserve nature of our ENTIRE SYSTEM!

The coming crash is a mathematical certainty and one that historians will ask in the future “what were they thinking”. While CNBC parades clown after clown to tell you this is a buying opportunity, I would simply advise DON’T BE STUPID and use your own common sense! We lived through the biggest super cycle of credit the world has ever seen …how do you think this ends?

Standing a fearful watch,

Bill Holter

Holter-Sinclair collaboration

end

_________________

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8811/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8764 /shanghai bourse CLOSED UP 31.90 POINTS OR 1.23%

HANG SANG CLOSED UP 377.64 POINTS OR 1.29%

2. Nikkei closed UP 213.44 POINTS OR 0.99%

3. Europe stocks OPENED ALL MIXED

/USA dollar index FALLS TO 96.99/Euro RISES TO 1.1377

3b Japan 10 year bond yield: RISES TO. +.06/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.44/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 50.53 and Brent: 59.62

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.28%/Italian 10 yr bond yield DOWN to 2.90% /SPAIN 10 YR BOND YIELD UP TO 1.40%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.62: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.22

3k Gold at $1242.45 silver at:14.71 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 4/100 in roubles/dollar) 66.41

3m oil into the 50 dollar handle for WTI and 59 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.44DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9916 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1282 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.28%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.90% early this morning. Thirty year rate at 3.14%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3626

Rally Fizzles: Europe, US Turn Red After Warnings From ECB, PBOC

With algos trying to force a rally for the third day in a row, the “STFR” crowd arrived early as stocks in Europe and S&P futures surrendered early gains as investors initially bought on the latest optimistic developments in America-China trade relations, which however turned into selling after a BBG report that the ECB – as everyone had already expected – will lower its inflation forecast for 2019 when it publishes an updated outlook on Thursday.

Europe’s Stoxx 600 declines were led by energy shares as oil slide back under $51, offsetting gains in raw materials as the index erased an early advance to turn lower. Hong Kong and Chinese stocks outperformed as equities across Asia continued their rebound ignoring news that a second Canadian citizen had “disappeared” in China.

In the U.K., gilts climbed and the FTSE 100 edged lower after May won a vote of confidence in her leadership of the Conservative Party, though it’s likely to be only a temporary reprieve as the embattled premier faces hardened opposition to her Brexit deal.

Earlier, the Nikkei and other Asian stocks had pushed roughly 1 percent higher ahead of several central bank meetings including a landmark one for the ECB which was set to end its quantitative easing program. Gains were concentrated in Chinese shares, with Chinese blue-chips up 1.5 percent and Hong Kong’s Hang Seng index gaining 1.1 percent. Japan’s Nikkei stock index ended 1 percent higher, while Australian shares gained 0.1 percent.

“All eyes will be on the ECB,” said Morgan Stanley FX strategist Hans Redeker. “It may revise its growth projections lower but continue to prepare the markets for allowing QE to end.”

Futures on the S&P 500 initially rose after news broke that Chinese importers have bought U.S. soybeans, though they since hit an air pocket and dropped after US traders got to their desks and after PBOC Governor Yi Gang warned that China’s economy faces rising downward pressure. And since the market is entirely controlled by algos, spoos hit yesterday’s lows before rebounding.

Investor optimism was boosted on Wednesday after China resumed purchases of American soybeans and reiterated its officials were in close contact with U.S. counterparts on negotiating details of a broader deal, while considering revising the controversial “Made in China 2025” strategy. Still, worries for global relations remain after China detained a second citizen of Canada for questioning, further heightening tensions between those two countries. Also on Wednesday, Trump administration officials signaled that Beijing will have to do more to end the tariff war.

Yoshinori Shigemi, a global market strategist at JPMorgan Asset Management, cautioned against reading too much into trade headlines: “U.S.-China trade negotiations are subject to very high uncertainty. So lots of headlines come and go, and markets come and go also,” he said. “We have to see the evolution of this negotiation.”

US Treasuries popped higher as NBC suggested that Trump is increasingly concerned about impeachment, while in Europe Italy’s BTPs resume their upward trend, breaking through 126.00 after PM Conte confirmed that Italy’s proposed budget deficit has been cut to just the laughably precise 2.04% in Italy’s latest concession to the European Commission.

Two-year Italian bond yields tumbled to 0.51 percent which took them back to where they were before a late May eruption of tensions triggered the worst day for short-term Italian debt in 25 years. Italy’s five-year and 10-year government bond yields dropped to their lowest level in 2 1/2 months and the closely watched Italy/Germany 10-year bond yield spread improved to its tightest since the start of October.

“I think the momentum can carry on in the near term as we have a number of supportive factors for Italian debt beyond just the hopes the budget deal can be reached,” said Commerzbank rates strategist Christoph Rieger.

The euro was steady as the ECB was said to be lowering its inflation forecast for 2019 in an outlook due Thursday, while the dollar was little changed. The pound added to its advance after May survived an attempted ouster, although little has changed on the ongoing Brexit impasse. The Norwegian krone was the biggest gainer versus the dollar as the central bank maintained its key rate but said it sees a hike “most likely” in March 2019. The yen weakened against all of its major peers as demand for haven assets waned amid signs of a further thaw in U.S.-China trade ties.

On Brexit UK Prime Minister May was heading to an EU summit in Brussels following her confidence vote win to try and get some additional concessions on the controversial Irish border aspect of the agreement to placate rebels within her own party and Ulster unionist allies. Markets reckon May’s continued premiership for now makes a ‘no deal’ Brexit less likely at the margins and her survival takes at least some of the immediate headline risk out of the market – even if the Brexit impasse is really no clearer.

Elsewhere, WTI oil slipped below $51 a barrel as a smaller-than-expected decline in U.S. crude stockpiles renewed fears a global glut. In terms of recent newsflow, the latest IEA’s monthly report saw the agency cut non-OPEC oil supply growth forecasts by 415,000 BPD to 1.5mln BPD vs. 2.4mln BPD in 2018. The IEA also left global oil demand growth unchanged at 1.3mln BPD and 1.4mln BPD for 2018 and 2019 respectively. This follows yesterday’s monthly OPEC report where demand estimates were left unchanged. Gold is trading flat within a slim USD 2/oz range, as the dollar steadies with the DXY unchanged on the day. Base metals continue to see support after yesterday’s news that China are preparing to increase access for overseas companies with sentiment also bolstered this morning after the Chinese Commerce Ministry stated that they would welcome a US trade delegation visit.

Market Snapshot

- S&P 500 futures down 0.1% to 2,653.5.50

- STOXX Europe 600 down 0.2% to 349.21

- MXAP up 0.6% to 151.37

- MXAPJ up 0.8% to 488.58

- Nikkei up 1% to 21,816.19

- Topix up 0.6% to 1,616.65

- Hang Seng Index up 1.3% to 26,524.35

- Shanghai Composite up 1.2% to 2,634.05

- Sensex up 0.3% to 35,901.53

- Australia S&P/ASX 200 up 0.1% to 5,661.61

- Kospi up 0.6% to 2,095.55

- German 10Y yield unchanged at 0.28%

- Euro up 0.09% to $1.1379

- Italian 10Y yield fell 11.9 bps to 2.637%

- Spanish 10Y yield fell 0.8 bps to 1.421%

- Brent futures down 0.6% to $59.79/bbl

- Gold spot little changed at $1,245.01

- U.S. Dollar Index down 0.1% to 96.96

Top Overnight News from BBG:

- The European Central Bank is set to lower its inflation forecast for 2019 when it publishes an updated outlook on Thursday, according to people familiar with the matter

- Theresa May heads for Brussels Thursday to plead for a lifeline after her Brexit plans provoked a revolt from her Conservative Party. “I will be seeking legal and political assurances that will assuage the concern that Members of Parliament have” on the backstop, May said

- EU27 leaders will affirm after dinner at their meeting in Brussels that the EU stands by the withdrawal agreement “and intends to proceed with its ratification,” Politico reported, citing draft summit conclusions

- Mario Draghi is about to end an era by halting the European Central Bank’s flagship stimulus program even with an economic outlook that is murky at best

- China is considering plans to delay some targets in its strategy to dominate high-end technologies as it tries to ease trade tensions with America. Beijing may postpone some aspects of its ambitious industrial program by a decade to 2035, according to people familiar with the matter

- Chinese importers have purchased 1.5m to 2m metric tons of American soy over the past 24 hours, the U.S. Soybean Export Council said, citing industry sources

- President Recep Tayyip Erdogan put Turkey on course for another clash with the U.S. by threatening to start a military operation within a few days targeting America’s Kurdish allies in northeastern Syria

- Italian Prime Minister Giuseppe Conte proposed to cut the deficit target to 2.04% of output for next year in a significant concession to the European Commission

- Global funds snapped up a record amount of Japanese bonds last week in a trend that threatens to complicate the central bank’s yield-curve-control policy

Asian equity markets traded positively as the region followed suit to the gains on Wall St amid trade-related hopes after news of further potential concessions by China. As such, ASX 200 (+0.1%) and Nikkei 225 (+1.0%) were higher but with gains in Australia capped by losses in the telecoms sector after the competition regulator expressed preliminary concerns regarding proposed TPG Telecom – Vodafone Hutchison Australia merger which resulted to a near-17% drop in TPG shares, while property-related weakness also restricted upside. Hang Seng (+1.3%) and Shanghai Comp. (+1.4%) were lifted amid the encouraging trade-related developments with China preparing to increase access for overseas companies and is working to replace its Made in China 2025 plan with one that tones down its bid to dominate manufacturing, while Chinese importers have also resumed purchases of US soybeans and are said to purchase as much as 2mln tons of US soybeans vs. earlier reports of 500k tons. Finally, 10yr JGBs traded lacklustre amid gains in stocks and similar subdued price action in T-notes, with a mixed 5yr auction result adding to the drab mood.

Top Asian News

- Philippines Puts Rate Hikes on Pause as Inflation Eases

- Nissan Said to Be Repatriating Cash as Renault Tensions Brew

- Air China Is Said to Have Held Talks to Buy HNA’s Airlines

- Qinghai Provincial Says in Talks With SOEs on Restructuring

Major European Indices are mixed with the FTSE MIB (+1.0%) outperforming due to the indices banks outperforming on Italian PM Conte stating the nations deficit goal is now 2.04%; while the EC comments that good progress has been made on this. FTSE 100 (U/C) is trading flat, with Associated British Foods (-0.6%) and 3I group (-2.1%) trading ex-dividends towards the bottom of the index. At the top of the index are TUI (+5.0%) expecting 10% underlying earnings growth at constant currencies for 2019. In terms of other notable movers G4S (+9.0%) are reviewing separation options for their cash solution business and Sainsbury’s (+1.3%) are up as they are challenging a refusal for additional time by the regulator regarding their merger with Asda. Sectors are broadly in the red with some underperformance seen in Energy while Utilities are the outperforming sector.

Top European News

- ECB Is Said to Lower 2019 Inflation Forecast as Bond-Buying Ends

- Italy Offers 2.04% Budget Deficit Target in EU Peace Gesture

- France’s Yellow Vests Are Starting to Enjoy the Radical Life

- Ukraine’s Renewed Privatization Drive Falls at First Hurdle

- SNB Sees Downside Risks as It Keeps Crisis Policy Settings

In currencies, GBP, EUR – Sterling the major G10 outperformer in the aftermath of PM May’s confidence vote victory last night, with some support also provided by the a draft document including the possibility that the EU are to look into giving more backstop assurances. As such cable remains firmly above 1.2600, albeit off highs of 1.2685 with large options around 1.2650-60 (1.2bln) perhaps hampering further attempts towards 1.2700. Meanwhile, the EUR also feels some benefit from the softer dollar, but is lagging vs. the Pound as EUR/GBP slips below 0.9000 ahead of the ECB policy decision. Note: please refer to the research suite for a full preview.

- NOK, CHF – Staying with the Central Bank theme, two out of the four end of year meetings have already passed and the Norwegian Crown strengthened in light of the Norges Bank’s current assessment reaffirming that rates will “most likely” be raised in March 2019. This, alongside upgrades to core CPI pulled EUR/NOK to lows of 9.7071 (vs. high of 9.7531). Conversely, the CHF was largely docile in wake of the SNB keeping its key rate and corridor unchanged, as expected. The Swiss Central Bank also maintained that the Franc is “highly valued” alongside reiterating its preparedness to intervene if required and utilise the balance sheet to react in the event of shocks. Note, SNB Head Jordan stressed the risk of major and sudden exchange rate movements which would significantly alter monetary conditions. As such EUR/CHF remains within a the bottom of a 1.1301-1.1281 range.

- AUD, NZD – The high-beta currencies continue to prosper in the more positive US-China trade environment, with the with AUD/USD building on gains above 0.7200 to just shy of 0.7250 at one stage, but also wary of big option interest at 0.7200 (1.3bln). Meanwhile NZD/USD remains sub-0.6900, albeit near the top of a 0.6880-42 range despite the downward revisions in the New Zealand HY economic and fiscal updates.

- JPY – Rangebound trade for the Yen ahead of tonight’s Tankan Survey release with USD/JPY hovering sub-113.50 (with resistance around the figure). In terms of technical, a key fib level sits at 113.61, with 750mln between 113.60-65. In terms of noteworthy option expiries to the downside, 113.00-10 (1.1bln) and 113.30-40 (1bln)

- TRY – Back to Central Banks, CBRT left its key one-week repo on hold as widely expected and maintained a tightened bias until the inflation outlook displays a significant improvement, though the Bank did acknowledge the recent sub-forecast CPI release, along with import prices and domestic demand condition. As such USD/TRY fell to lows just shy of 5.3000 vs. highs of 5.3837

In commodities, Brent (-0.3%) and WTI (-0.4%) are down on the session in a continuation of yesterday’s price action. In terms of recent newsflow, the latest IEA’s monthly report saw the agency cut non-OPEC oil supply growth forecasts by 415,000 BPD to 1.5mln BPD vs. 2.4mln BPD in 2018. The IEA also left global oil demand growth unchanged at 1.3mln BPD and 1.4mln BPD for 2018 and 2019 respectively. This follows yesterday’s monthly OPEC report where demand estimates were left unchanged. Whereas, non-OPEC oil supply in 2018 is forecast to grow by 2.5mln BPD, which was an upward revision of 190k BPD; with this in mind, some suggest that OPEC will need to make further cuts over the second half of 2019. Gold is trading flat within a slim USD 2/oz range, as the dollar steadies with the DXY unchanged on the day. Base metals continue to see support after yesterday’s news that China are preparing to increase access for overseas companies with sentiment also bolstered this morning after the Chinese Commerce Ministry stated that they would welcome a US trade delegation visit. Copper prices have hit a 1-week high on these trade developments. Separately, steel prices have risen on a potential boost to demand arising from expectations that China are to launch more infrastructure products next year.

US Event Calendar

- 8:30am: Import Price Index MoM, est. -1.0%, prior 0.5%; YoY, est. 1.3%, prior 3.5%

- 8:30am: Export Price Index MoM, est. -0.3%, prior 0.4%; YoY, prior 3.1%

- 8:30am: Initial Jobless Claims, est. 226,495, prior 231,000; Continuing Claims, est. 1.65m, prior 1.63m

- 9:45am: Bloomberg Consumer Comfort, prior 60.3

- 2pm: Monthly Budget Statement, est. $199.0b deficit, prior $100.5b deficit

DB’s Jim Reid concludes the overnight wrap

There were high emotions last night as UK PM May now has to write 117 fewer Xmas cards after winning her leadership battle by a vote of 200-117. That result is enough to insulate May from another leadership challenge within the next 12 months from within her party. However, more than a third of her party and likely more than half of her backbenchers voted against her and the result was less supportive than most thought beforehand.

The pound had already gained as much as +1.47% to above $1.265 in advance of the vote, as it became clearer that May would have sufficient support to win the confidence vote. However, with the actual margin less than expected the currency surrendered around a third of its gains at one stage before closing up +1.14% on the day after the vote. Overnight, it held that advance and is trading around $1.262 as we go to print.

So after all the noise, we’re left where we started. As before, the eventual outcome and the implications for UK assets will depend on May’s approach. Will she allow for modifications to her deal, or press ahead as-is? In her brief speech after the result she acknowledged the opposition in the leadership results and to the deal but didn’t immediately appear inclined to change tact. Her tactic at the moment still seems to get concessions out of Europe. Problem is, it seems quite clear that her European partners will not offer any of note. Basically, it all boils down to the backstop on the Irish situation. On this it’s worth noting that EU leaders are due to meet later today to discuss their position. Let’s see if a rabbit is pulled out of a hat. Seems unlikely. Where this ends is still highly uncertain. If a solution to the backstop can’t be found, we will probably have to pivot to a totally different tactic. Either a much softer Brexit (EEA type arrangement) or maybe a second referendum.

Aside from the Sterling move, this morning in Asia markets are off to a solid start with the Nikkei (+1.08%), Hang Seng (+1.22%), Shanghai Comp (+1.47%) and Kospi (+0.76%) all up. More signs of diffusing trade tensions seem to be the driver. The US Soybean export council said late yesterday night that Chinese importers have purchased 1.5mn to 2mn tons of US soybeans over the last 24 hours thus providing further evidence that the talks are moving in the right direction. Meanwhile, yesterday’s story in the WSJ about China working on a replacement for its ‘Made in China 2025’ plan with one that plays down its bid to dominate manufacturing has also aided sentiment. The article is noteworthy as it is the first sign that we’ve seen on a compromise on issues between the US and China that go beyond the bilateral deficit and focus on specifics. Futures on S&P 500 are also up +0.35% overnight while the CNY is +0.20% stronger.

Those moves overnight come after an impressive first half to the session on Wall Street yesterday but one that saw intra-day gains fade yet again. US markets still rallied +0.5 to +1% but gains of over +1.8% to +3% were seen earlier depending on the indices. Before this we saw another strong day for risk in Europe. Indeed, it felt like you could take your pick from a number of riskfriendly catalysts yesterday. Hopes that Brexit can have a softer bias with a May win, further signs of softening on the budget in Italy, a steady as she goes US CPI print, the WSJ story about China above, and talk of President Trump intervening on the Huawei case to push through a trade deal with China, all played a part. In the end, the S&P 500 (+0.54%), DOW (+0.64%) and NASDAQ (+0.95%) stayed higher after the blip while in Europe the STOXX 600 closed +1.69% to clock up its best two-day run since July 2016. European banks also bounced +2.99%. Treasuries were well offered with 10y yields climbing +3.1bps, while the 2s10s curve finished +2.2bps steeper. Elsewhere, the FTSE 100 (+1.08%) lagged a bit, which was understandable with the Sterling move, however, the more domestic focused FTSE 250 did rise +1.90%, while the FTSE MIB climbed +1.91% and CAC +2.15% – the latter seemingly still reacting to the budget measures announced by Macron. HY cash spreads in the US and Europe were also -8bps and -11bps tighter respectively.

The more notable moves in Italy yesterday were for Italian Banks, which rallied +3.0% while 2y and 10y BTP yields fell -7.7bps and -11.9bps, respectively. The latter closed back under 3% (at 2.996% to be exact) for the first time since September with the catalyst being the reports about Italian Premier Conte potentially proposing a 2% deficit target for next year. After Europe closed it was confirmed by Conte that the revised budget would be 2.04% of GDP. The euro also gained +0.46% on the day on the news while other bond markets in Europe were more mixed, however 10y Bunds did climb back up +4.6bps to 0.276%. Elsewhere, as noted above, yesterday’s US CPI print didn’t do much to move the dial with the unrounded core reading of 0.2093% for November more or less bang on expectations. That did, however, confirm a move higher in the year-on-year rate to +2.21%, which puts it at the highest since July. Both the three-month and six-month annualised rates also ticked higher to +2.1% and +2.0%, respectively.

That should alleviate concerns over the slight recent slowdown in core inflation, which had seen the 3m annualized rate dip to 1.6% last month. As markets continue to debate the fallout from last night’s confidence vote, there is at least the distraction of an ECB meeting to look forward to today. As a reminder, our economists expect the ECB to confirm that net asset purchases will cease at year-end. However, they also expect the ECB and Draghi to argue that the policy stance is not tightening. Indeed, they expect a classic ‘dovish tightening’ bias to the event. The team expects Draghi to say that “the market understands the guidance”, meaning the delayed pricing of the first hike is broadly appropriate. They also expect Draghi to hint that the TLTRO2 liquidity will be replaced in 2019. Overall, the risks today are balanced to a more dovish outcome. It is not just that the ECB staff forecasts are likely to be downgraded, the balance of risks could also shift to the downside. At the softer end of options, the ECB could make a dovish revision to the forward guidance on the timing of reinvestment tapering and among the stronger responses are a twist of the asset portfolio. This could come within the details of the reinvestment programme, which are due. We’ll know for certain later with the decision due at 12.45pm BST and Draghi’s press conference shortly after.

Back to yesterday, where, not to be outdone, emerging markets were also back in vogue following the headlines that hit in the morning quoting Turkey President Erdogan as saying that Turkey will “start an operation in Syria within days”. The Turkish Lira immediately sold off as much as -0.54% on the news, but the move appeared to be more kneejerk in reaction than anything else as it ultimately closed slightly stronger, up +0.37% on the day. EM FX more broadly was +0.58% while the MSCI EM equity index ended +1.46%. This came despite another slip in oil prices, with WTI down -0.97% as data showed that US oil inventories fell only -1.2 million barrels last week compared to the expected -3.5 million barrels. That’s the 12th time the inventories data has shown a smaller drawdown than expected over the last three months, the longest such stretch since April 2015.

As for the other economic data that was out yesterday, in the US, mortgage applications data showed a +1.6% week-on-week increase. That’s the third consecutive monthly increase, the best streak since March, and maybe a sign that recent housing sector weakness may be bottoming out. In Europe, October’s industrial production ended up being a bit of a wash with the stronger than expected October reading (+0.2% mom vs. +0.1% expected) offset by a downward revision to September to a sharper -0.6% mom decline (versus -0.3% previously). In Italy, the unemployment rate dipped to 10.2%, a new cycle low and the best print since Q1 2012.

In terms of the day ahead, a combination of the follow through from last night’s confidence vote on UK PM May and the aforementioned ECB meeting later today will no doubt be front and centre. Aside from that we’ve also got the final November CPI revisions due in Germany and France this morning while this afternoon in the US we get the November import price index print and latest weekly initial jobless claims reading. The latter is well worth keeping an eye on in light of the recent uptick in claims. Indeed, the four-week moving average has risen from a multi-decade low of 206k in the middle of September to 228k as of December 1st. Away from all that, EU leaders are also due to meet today in Brussels to discuss the EU budget and Brexit amongst other topics.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 31.90 POINTS OR 1.23% //Hang Sang CLOSED UP 337.64 POINTS OR 1.29% //The Nikkei closed UP 213.44 OR 0.99%/ Australia’s all ordinaires CLOSED UP 0.14% /Chinese yuan (ONSHORE) closed UP at 6.8811 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 50.58 dollars per barrel for WTI and 59.62 for Brent. Stocks in Europe OPENED MIXED//. ONSHORE YUAN CLOSED UP AT 6.8764AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8811: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

Another indicator highlighting the growth problems inside China. Today is the total collapse of Chinese auto sales. It is their first decline in 30 years.

(courtesy zero hedge)

Chinese Auto Sales Accelerate Historic Collapse, Set For First Annual Decline In 30 Years

Progress in the United States/China trade war seems to be happening at just the right time.

The automobile industry in China has been crippled, partly as a result of this trade war, partly due to the ongoing domestic economic slowdown in the mainland, and absent major subsidies – which don’t appear to be coming – the outlook for the rest of 2018 and 2019 is not promising. The collapse has been historic and according to new data, continued through November.

November data confirmed a continuation of the ugly trends that we discussed last month. For instance, passenger vehicle wholesales were down 16.1% on the year, according to the China Association of Automobile Manufacturers. This data includes sedans, SUVs and crossover utility vehicles.

November vehicle wholesales were also down well into the double digits, dropping 13.9% to 2.55 million units year-over-year. Total retail passenger vehicles fell 18% on the year and SUV sales fell 20.6% year-over-year to 854,289 units, according to the Passenger Car Association.

As a result, CICC now expects China’s full year production and sales to drop more than 5% year-over-year for 2018. This would be the first annual decline in Chinese car sales in nearly three decades.

They also predicted that inventory levels at dealerships across the country will likely continue to rise as automakers “stuff channels” in hopes of fooling investors that sales are stronger than they are. The sales data for November suggested “much weaker demand in lower end segments and fears [of] competition in the SUV market” according to the CICC note.

They association concluded that a turnaround for the sector is only likely after Spring Festival, which occurs in the beginning of February. CICC found that domestic brands are becoming more competitive in new energy vehicles and SUV’s, while Japanese carmakers still have the advantage in sedans.

To be sure, this should not come as a surprise to regular readers as we have been reporting on the anemic numbers coming out of China in both October and November, although the severity of the slowdown has caught even the optimists by surprise.

Last month we also noted that China was mentioned very cautiously by automakers, many of whom offered pessimistic forecasts for the remainder of this year. Renault recently blamed its poor numbers on a global slowdown in sales in places like China and Europe, as well new emissions standards. Volkswagen also recently cut its sales forecast for China, citing a slowdown in the country as well as the looming trade war with the United States.

China’s slowdown has also hit names like General Motors which last month reported a 15% drop in China deliveries for the three months ended Sept. 30, the first quarterly report since the trade tensions with the U.S. began escalating in July.

That said, on Tuesday morning it was reported that China is considering cutting its tariffs on US autos, which could potentially serve as a short-term boost to demand.

Bloomberg said China is planning to cut tariffs on US-made cars to 15% from the current 40% has been submitted to China’s Cabinet to be reviewed in the coming days. China boosted tariffs on US-made cars to 40% as part of a raft of retaliatory measures against the US imposed over the summer. To be sure, nothing is set in stone just yet. The decision is being reviewed, and could still change.

Second Canadian Citizen Disappears In China

For a trade war that was supposed to be between the US and China, Canada has found itself increasingly in the middle of the crossfire. And so after the arrest of a former Canadian diplomat in Beijing in retaliation for the detention of the Huawei CFO in Vancouver, Canada said a second person has been questioned by Chinese authorities, further heightening tensions between the two countries.

The second person reached out to the Canadian government after being questioned by Chinese officials, Foreign Minister Chrystia Freeland said, at which point Canada lost contact with him. His whereabouts are currently unknown and Global Affairs Canada said they are in contact with his family.

“We haven’t been able to make contact with him since he let us know about this,” Freeland told reporters Wednesday in Ottawa. “We are working very hard to ascertain his whereabouts and we have also raised this case with Chinese authorities.”

According to the he Globe and Mail, the man was identified as Michael Spavor, a Canadian whose company Peaktu Cultural Exchange brings tourists and hockey players into North Korea. He gained fame for helping arrange a visit to Pyongyang by former NBA player Dennis Rodman, and he met North Korean leader Kim Jong Un on that trip, the newspaper reported. Attempts to reach Spavor on his contact number either in China, or North Korean went straight to voicemail.

Spavor’s personal Facebook page contains several images of him with North Korean leader Kim Jong-un including one of him with both Jong-un and former Dennis Rodman at an undisclosed location.

Michael P. Spavor, right, pictured here with North Korean leader Kim Jong-un, second from right, and Dennis Rodman.Another image shows the two sharing a drink on a boat.

Michael P. Spavor, right, pictured here with North Korean leader Kim Jong-un, second from right, and Dennis Rodman.Another image shows the two sharing a drink on a boat.

The unexplained disappearance takes place after China’s spy agency detained former Canadian diplomat Michael Kovrig in Beijing on Monday, who was on leave from the foreign service. The arrest came nine days after Canada arrested Huawei Chief Financial Officer Meng Wanzhou at the request of U.S. DOJ. While Canada has asked to see the former envoy after it was informed by fax of his arrest, Canada is unaware of Kovrig current whereabouts or the charges he faces.

“Michael did not engage in illegal activities nor did he do anything that endangered Chinese national security,” Rob Malley, chief executive officer of the ICG, said in a written statement. “He was doing what all Crisis Group analysts do: undertaking objective and impartial research.”

One possibility is that Kovrig may have been caught up in recent rule changes in China that affect non-governmental organizations, according to Bloomberg. The ICG wasn’t authorized to do work in China, Foreign Ministry Spokesperson Lu Kang said during a regular press briefing in Beijing Wednesday.

“We welcome foreign travelers. But if they engage in activities that clearly violate Chinese laws and regulations, then it is totally another story,” he said, adding he had no information on Kovrig specifically.

As Bloomberg further notes, foreign non-governmental organizations are now required to register with the Chinese authorities under a 2017 law that subjects them to stringent reporting requirements. Under the law, organizations without a representative office in China must have a government sponsor and a local cooperative partner before conducting activities. ICG said this is the first time they’ve heard such an accusation from the Chinese authorities in a decade of working with the country. The company closed its Beijing operations in December 2016 because of the new Chinese law, according to a statement. Kovrig was working out of the Hong Kong office.

Meanwhile, realizing that it is increasingly bearing the brunt of China’s retaliatory anger, Trudeau’s government distanced itself from Meng’s case, saying it can’t interfere with the courts, but is closely involved in advocating on Kovrig’s behalf.

So far Canada has declined to speculate on whether there was a connection between the Kovrig and Meng cases, with neither Freeland nor Canadian Trade Minister Jim Carr saying Wednesday that there is any indication the cases are related. Then again, it is rather obvious they are. Indeed, Guy Saint-Jacques, who served as ambassador to China from 2012 to 2016 and worked with Kovrig, says the link is clear. “There’s no coincidence with China.”

“In this case, they couldn’t grab a Canadian diplomat because this would have created a major diplomatic incident,” he said. “Going after him I think was their way to send a message to the Canadian government and to put pressure.”

Even though Meng was granted bail late Tuesday, that did not placate China, whose foreign ministry spokesman said that “The Canadian side should correct its mistakes and release Ms. Meng Wanzhou immediately.”

The tension, according to Bloomberg, may force Canadian companies to reconsider travel to China, and executives traveling to the Asian country will need to exercise extra caution, said Andy Chan, managing partner at Miller Thomson LLP in Vaughan, Ontario.

“Canadian business needs to look at and balance the reasons for the travel’’ between the business case and the “current political environment,’’ Chan said by email. Chinese officials subject business travelers to extra screening and in some case reject them from entering, he said.

Earlier in the day, SCMP reported that Chinese high-tech researchers were told “not to travel to the US unless it’s essential.”

And so, with Meng unlikely to be released from Canada any time soon, expect even more “Chinese (non) coincidences”, until eventually China does detain someone that the US does care about.

Navarro Affirms Arrests Of Canadian Citizens In China Was “Retaliation” For Huawei CFO

With US stocks set to open higher on Thursday, traders’ blood pressure probably spiked when they saw headlines from an interview with White House trade advisor Peter Navarro hitting the tape (who can forget his infamous comments two week ago when he chided traders and Wall Street banks for pushing for a trade detente, warning that talks with China hadn’t yielded any progress).

Fortunately for equity bulls, stock futures remained in the green as Navarro offered a mix of bullish and bearish commentary during a brief chat with Fox Business’s Maria Bartiromo, where the notorious China hawk discussed the Trump administration’s goals in its negotiations with its trade war rival, and advised traders to “focus on March 1” instead of trying to read too deeply into every report “on the front page of the Wall Street Journal” (comments that, on the surface, would seem to undercut the impetus for yesterday’s rally).