GOLD: $1237.40 DOWN $5.60 (COMEX TO COMEX CLOSINGS)

Silver: $14.56 DOWN 21 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1238.50

silver: $14.57

For comex gold and silver:

DEC

Again, we have Goldman Sachs dealer and JPMorgan customer account stopping (receiving the gold) 38/53 contracts.

EXCHANGE: COMEX

CONTRACT: DECEMBER 2018 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,242.700000000 USD

INTENT DATE: 12/13/2018 DELIVERY DATE: 12/17/2018

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 27

323 C HSBC 3

661 C JP MORGAN 11

737 C ADVANTAGE 48 12

800 C RCG 2

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 53 53

MONTH TO DATE: 7,261

NUMBER OF NOTICES FILED TODAY FOR DEC CONTRACT: 53 NOTICE(S) FOR 5300 OZ (0.1648 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7261 NOTICES FOR 726100 OZ (22.584 TONNES)

SILVER

FOR DECEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

26 NOTICE(S) FILED TODAY FOR 130,000 OZ/

Total number of notices filed so far this month: 3899 for 19,495,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3302: up 2

Bitcoin: FINAL EVENING TRADE: $3207 down 94

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY SIZED 630 CONTRACTS FROM 175,076 DOWN TO 174,446 WITH YESTERDAY’S 2 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 20 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1410 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1410 CONTRACTS. WITH THE TRANSFER OF 1410 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1410 EFP CONTRACTS TRANSLATES INTO 7.05 MILLION OZ ACCOMPANYING:

1.THE 2 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

NOW 20.730 INITIALLY STAND FOR DECEMBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DEC: 17,804 CONTRACTS (FOR 10 TRADING DAYS TOTAL 17,804 CONTRACTS) OR 89.02 MILLION OZ: (AVERAGE PER DAY: 1780 CONTRACTS OR 8.900 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 89,02 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 12.71% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,766.08 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

ACCUMULATION FOR NOVEMBER /2018: 247.18 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 630 DESPITE THE 2 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY.. AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1410 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A SMALL SIZED: 780 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1410 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 630 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 2 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.77 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .875 BILLION OZ TO BE EXACT or 125% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DEC MONTH/ THEY FILED AT THE COMEX: 26 NOTICE(S) FOR 130,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./AND NOW DEC. AT 20.880 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 3998 CONTRACTS DOWN TO 400,737 WITH THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $2.00//.YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9668 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 9668 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 400,737. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5670 CONTRACTS: 3988 OI CONTRACTS DECREASED AT THE COMEX AND 9668 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 5670 CONTRACTS OR 567,000 OZ = 17,63 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $2.00

YESTERDAY, WE HAD 11080 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC : 85747 CONTRACTS OR 8,574,700 OZ OR 266.70 TONNES (10 TRADING DAYS AND THUS AVERAGING: 8574 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAYS IN TONNES: 266.70 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 266.70/2550 x 100% TONNES = 9.27% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 7031.08 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018: 552.88 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 3988 WITH THE LOSS IN PRICING ($2.00) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9668 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9668 EFP CONTRACTS ISSUED, WE HAD AN GOOD GAIN OF 5670 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9668 CONTRACTS MOVE TO LONDON AND 3988 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 17.63 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $3.05 IN YESTERDAY’S TRADING AT THE COMEX

we had: 53 notice(s) filed upon for 5300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $5.60 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 763.56 TONNES

Inventory rests tonight: 763.56 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 22 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 318.735 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 630 CONTRACTS from 175,076 DOWN TO 174,446 AND MOVING FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1410 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1410 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 630 CONTRACTS TO THE 1410 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A FAIR GAIN OF 780 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 3.90 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. AND NOW 20.880 MILLION OZ STANDING IN DECEMBER.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 2 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 1440 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 40.31 POINTS OR 1.53% //Hang Sang CLOSED UP 429.46 POINTS OR 1.62% //The Nikkei closed DOWN 441.36 OR 2.02%/ Australia’s all ordinaires CLOSED DOWN 0.98% /Chinese yuan (ONSHORE) closed UP at 6.9008 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 52.16 dollars per barrel for WTI and 60.91 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED UP AT 6.9008AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9015: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

i

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)You now have proof that China’s economy is plummeting: today the big duo reports: retail sales and industrial production both plummet

( zerohedge)

ii)China is trying to appease Trump: they are rolling backing their new auto tariffs for 3 months.

4/EUROPEAN AFFAIRS

i)UK

Theresa May leaves Brussels empty handed after considerable contentious talks. As promised the EU will not give in. The UK should leave the EU without any deal and without paying a nickel.

( zerohedge)

ii) GERMANY

Jeffrey Snider asks a very good question: why the rush to combine the two big German banks?

(courtesy Jeffrey Snider/Alhambra Investments

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

CANADA

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)Venezuela

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)USA manufacturing output disappoints again for the 2nd straight month. Trump does not like this as tariffs are suppose to help manufacturing

(courtesy zerohedge)

c)This is a very big story. I have always highlighted to you events on this very important story. The last remaining investment grade of bonds that corps are allowed to hold are BBB rated bonds. Once you enter below this level at BB or less, then corporations are now longer allowed to carry these bonds on their books as they must be sold. There are approx 3/4 of a trillion dollars worth of BBB bonds trading. You will recall that we commented on the A graded bonds and how it was likely that a huge number would be downgraded to the BBB level and sure enough a massive 176 billion A rated bonds have been downgraded to BBB. Once considerable amount of BBB bonds are downgraded, then we are on the verge of a massive crisis as nobody is capable of holding these bonds.

( zerohedge)

a)This is interesting: banks are unable too offload loans and outflows multiply

( zerohedge)

iv)SWAMP STORIES

a)If Trump used his own personal money as hush money, I cannot see what is wrong and why the markets are reacting so badly to this

( zerohedge)

c)The GOP says there is no plan for the wall…Trump will hold out for the wall as there is only 3 weeks left before the Democrats take over.

( zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of DECEMBER and here in this front month of December we now have 303 contracts standing for a LOSS of 249 contracts. We had 279 contracts stand for delivery yesterday so we gained 30 contract or an additional 250,000 oz will not stand for delivery as these guys morphed into London based forwards as well as accepting a fiat bonus.

After December we have the non active January contract month and here we saw a LOSS of 28 contracts up to 1881 contracts. February saw its another 9 contract gain to stand at 107. March, the next big delivery month after December saw a LOSS of 863 contracts down to 143.803

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

we still have not had any adjustments out of the dealer to the customer account to signify a settlement

Brexit and Global Growth Risks Sees Gold Gains In Euros, Pounds and Other Currencies

‘Hard’ Brexit Risk Sees Gold Gain In Euros and Pounds – Nears £1,000/oz & €1,100/oz

Gold was lower today in dollars but saw slight gains in pounds and euros. It was supported by increasing concerns about the likelihood of a ‘hard’ Brexit, about global economic growth and uncertainty around the Fed’s interest rate policies in 2019.

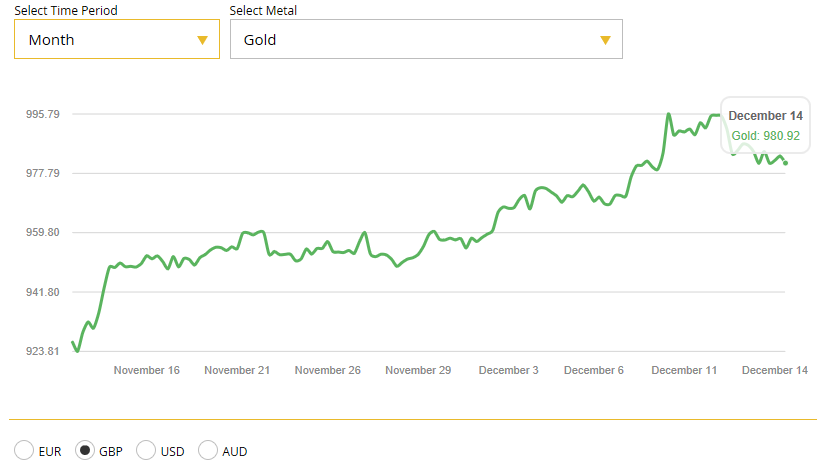

Gold in GBP – 1 Month (GoldCore)

Gold has consolidated on last week’s 2% gains in dollar terms and is essentially flat in dollars but has seen gains in euros and pounds today and this week.

Gold is down 0.3 percent for the week in dollars but has seen gains in not just pounds and euros, but also Australian dollars, New Zealand dollars and other fiat currencies.

Concerns about trade wars have abated in the short term but the risk has not gone away completely and will support gold.

Gold in EUR – 1 Month (GoldCore)

Other risks will also support gold. These include the fallout from a ‘hard’ or ‘no deal’ Brexit on UK and EU economic growth and indeed increasing concerns of another global financial crisis. This has been warned of by ex Fed Chair Yellen and indeed the IMF this week (see below).

Silver fell 0.6% today to $14.65 per ounce but is up about 0.4 percent for the week and is building on last week’s 3% gain.

The Fed is expected to hike interest rates next week which could lead to short term weakness for gold. However, with the Fed likely to pause interest rate hikes in 2019, gold will be supported and should indeed see gains in the medium term and in 2019.

The risk of a recession in the U.S. in the next two years has risen to 40 percent, according to a poll of economists by Reuters. There is also a significant shift in expectations toward fewer Fed interest rate rises next year due to concerns regarding U.S. and global economic growth.

Among other precious metals, spot palladium was down 0.5 percent at $1,254.50 per ounce, having hit an all-time high of $1,269.25 yesterday. Palladium is on track to mark it’s third week of gains with prices up another 2 percent this week.

Gold will be a valuable portfolio diversification in what looks set to be a volatile 2019.

As the business and economic cycle turns, risk assets such as bonds and stocks look increasingly vulnerable. Many property markets globally also appear vulnerable and gold will hedge investors exposures.

News, Commentary and Market Updates This Week

Yellen Warns Another Financial Crisis Is Brewing

Gold Krugerrand Coin Worth $1,200 Donated To Charity

EU Recession Imminent – Euro Disunion as Brexit, Italy and End of QE Loom

Irish Central Bank Refuses To Discuss Gold Reserves In Bank of England Vaults

Gold and Silver Gained 2% and 3% Last Week While Stocks Dropped Nearly 5%

Germany Accelerates Plans For Deutsche Bank-Commerzbank Megamerger

South African Gold Output Collapse Continues – Drops 13th Straight Month in October

Secure Storage Ireland – Click here for information

Secure Storage Ireland – Click here for information

News and Commentary

Gold prices steady on Fed policy outlook uncertainty (Reuters.com)

US budget deficit hits record $204.9 billion for November (APNews.com)

Wall Street edges lower as trade-fueled rally loses steam (Reuters.com)

Dow gives up 200-point gains as digests latest US-China trade developments (CNBC.com)

India and United Arab Emirates to stop using U.S. dollars in trade (GulfNews.com)

U.S. Leveraged Loan Funds Lose Cash at Fastest Pace Ever (Bloomberg.com)

Source: Bloomberg

Brexit isn’t the only geopolitical risk to stocks – Rebalance your portfolio (GoldSeek.com)

What does May’s victory mean for markets? (MoneyWeek.com)

How to prepare your portfolio for a “bare-bones” Brexit (MoneyWeek.com)

CFTC refuses to address GATA’s questions about gold and silver market rigging (Gata.org)

Australia’s House Of Cards Is Collapsing: Recession Coming Up (ZeroHedge.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

13 Dec: USD 1,244.45, GBP 982.87 & EUR 1,093.62 per ounce

12 Dec: USD 1,244.75, GBP 993.31 & EUR 1,098.24 per ounce

11 Dec: USD 1,248.25, GBP 988.99 & EUR 1,096.59 per ounce

10 Dec: USD 1,246.80, GBP 980.61 & EUR 1,092.57 per ounce

07 Dec: USD 1,241.20, GBP 972.98 & EUR 1,091.51 per ounce

06 Dec: USD 1,236.45, GBP 971.48 & EUR 1,091.66 per ounce

Silver Prices (LBMA)

13 Dec: USD 14.68, GBP 11.60 & EUR 12.90 per ounce

12 Dec: USD 14.66, GBP 11.68 & EUR 12.93 per ounce

11 Dec: USD 14.64, GBP 11.62 & EUR 12.85 per ounce

10 Dec: USD 14.53, GBP 11.48 & EUR 12.73 per ounce

07 Dec: USD 14.49, GBP 11.34 & EUR 12.73 per ounce

06 Dec: USD 14.38, GBP 11.28 & EUR 12.68 per ounce

Recent Market Updates

– Yellen Warns Another Financial Crisis Is Brewing

– Gold Krugerrand Coin Worth $1,200 Donated To Charity Again

– EU Recession Imminent – Euro Disunion as Brexit, Italy and End of QE Loom

– Gold and Silver Gained 2% and 3% Last Week While Stocks Dropped Nearly 5%

– Irish Central Bank Refuses To Discuss Gold Reserves In Bank of England Vaults

– “Fake Markets” To Lead to Global Financial Crisis? – Goldnomics Podcast

– Gold Is “Coiled” and Looks Set To Surge Like Natural Gas — Bloomberg Intelligence

– “Collapse Of Civilisation Is On The Horizon” – Attenborough Warns World Leaders

– Deutsche Bank May Cause The Next Global Crisis

– Ireland’s Mr Gold Reveals Nuggets Of Wisdom For When The Next Crash Comes

Paulson wins control of Detour board in key shareholder vote

Submitted by cpowell on Thu, 2018-12-13 20:26. Section: Daily Dispatches

By Scott Deveau and Danielle Bochove

Bloomberg News

Thursday, December 13, 2018

Paulson & Co. has convinced shareholders of Detour Gold Corp. to overthrow the bulk of the Canadian miner’s board of directors, including its interim CEO, ending a nasty six-month proxy battle.

Five of the Paulson-backed nominees were chosen, while Detour Chairman Alex Morrison and interim Chief Executive Officer Michael Kenyon were removed from the board during a special shareholders meeting today in Toronto, the miner said in a statement.

…

Kenyon has resigned as CEO and James Gowans, who was one of three new directors appointed in August, will become the chairman, Detour said. The board will be fixed at nine members.

Marcelo Kim, a partner at Paulson who was on the hedge fund’s slate of board nominees, was not elected.

“Seven out of eight directors have changed since we started this campaign,” Kim said at the 18-minute shareholders’ meeting that was closed to media. “But it’s not about who won or who lost. It’s about what’s best for the company.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-12-13/detour-gold-sharehold…

* * *

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Alasdair Macleod: Gold — a perfect storm for 2019

Submitted by cpowell on Thu, 2018-12-13 21:25. Section: Daily Dispatches

4:27p ET Thursday, December 13, 2018

Dear Friend of GATA and Gold:

In his new essay, “Gold — A Perfect Storm for 2019,” GoldMoney research director Alasdair Macleod itemizes the factors likely to favor gold and weaken the U.S. dollar and other currencies in the year ahead, especially as central banks engage in another frenzy of currency creation to stave off the next recession and sharp declines in stock and housing prices.

Of course the more that fundamentals favor gold against government currencies, the more governments may be inclined to use the futures markets to suppress the prices of gold, silver, and commodities generally. So GATA may have to keep working on that problem.

Macleod’s analysis is posted at GoldMoney here:

https://www.goldmoney.com/research/goldmoney-insights/gold-a-perfect-sto…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Gold – A Perfect Storm For 2019

Authored by Alasdair Macleod via GoldMoney.com,

This article is an overview of the principal factors likely to drive the gold price in 2019. It looks at the global factors that have developed in 2018 for both gold and the dollar, how geopolitics are likely to evolve, the economic outlook and how it is worsened for the dollar by President Trump’s tariff war against China, the availability and likely demand for bullion, and the technical position in paper markets. Taken together, the outlook is bullish for gold.

2018 reprise

For gold bulls, 2018 was disappointing. From 11 December 2017, when gold made a significant bottom against the dollar at $1243, it has ended virtually unchanged today, after being 4.2% up. Gold had to struggle against a rising dollar, whose trade-weighted index rose a net 3.7% over the same period, and as much as 9.4% from its mid-February low.

Dollar strength has been driven less by trade imbalances and more by interest rate differentials. A speculating bank for its own book or for a hedge fund client can borrow 3-month Euro Libor at minus0.354% and invest it in 3-month US Treasury bills at 2.36%, for a round trip of over 2.7%. Gear this up ten times or more, either on a bank’s capital, or through reverse repos for annualised returns of over 27%. To this can be added the currency gain, which at times has added enough to overall returns for an unhedged geared position to double the investment.

Not that these forex returns have been guaranteed, but you get the picture. The ECB and the Bank of Japan have been frozen into inactivity, reluctant to raise rates to correct this imbalance, and the punters have known it.

Financial commentators have routinely misunderstood the fundamental reason for the dollar’s strength, attributing it to foreigners’ desperate need for dollars. In fact, non-US holders of dollars hold it in record amounts, with over $4 trillion in deposits in correspondent bank accounts alone, and a further $930 billion in short-term debt. This $5 trillion of total liquidity was the last reported position, as at end-June 2017. Speculative dollar demand since then, driven by interest rate differentials, will have added significantly to these figures. The continuing US trade deficit, currently running at close to a trillion dollars annually, is both an associated and additional source of dollar accumulation in foreign hands.

Meanwhile, the same US Government data source reveals that US residents’ holdings of foreign securities was $6.75 trillion less than the foreign ownership of US securities, and the US Treasury reports that major US market participants (i.e. the US banks and financial entities operating in the spot, forwards and futures contracts) sold a net €2.447 trillion in the first nine months of 2018. Assuming these sales were not absorbed by official intervention on the foreign exchanges or by contracting bank credit, they can only have added to foreign-owned dollar liquidity.

To summarise the point; far from there being a dollar shortage, as market participants believe, the world is awash with dollars to an extraordinary degree.

The great dollar unwind is now overhanging markets, which will remove the principal depressant on the gold price. And when it begins, as a source of supply these hot-money dollars will be seen as the continuation of escalating supply, with the prospect of future US trade and budget deficits to be discounted. These dynamics are a duplication of those that led to the failure of the London gold pool in the late-sixties, which led to the abandonment of the Bretton Woods gold-dollar relationship in 1971. And as I argue later in this article, the supply of physical liquidity in bullion markets to satisfy demand arising from dollar liquidation is extremely tight.

Geopolitics and gold in 2018

It is likely that at a future date we will look back on 2018 as a pivotal year for both geopolitics and gold. Russia has moved to a position whereby it has substantially replaced its dollar reserves with physical gold. It is now able, if it should care to, to do away with the dollar entirely for its energy exports payments. It is even possible for it to link the rouble to gold.

China took the seemingly innocuous step of launching an oil contract denominated in yuan. It had prevaricated since at least 2014 before making this move, presumably conscious that it was an in-your-face threat to the monopoly of the dollar in pricing energy.

There was expectation that the oil-yuan futures contract would be a segway into a yuan-gold futures contract either in Hong Kong or Dubai, allowing countries such as Iran to avoid receiving dollars entirely. And indeed, a number of gold exchanges and interests in Asia have banded together to open a 1500-tonne vault in Qianhai to facilitate gold storage resulting from pan-Asian trade flows.

These include the China Gold and Silver Exchange Society, the Hong Kong Gold Exchange, and gold market interests in Singapore, Myanmar and Dubai. The objective is to give Hong Kong the opportunity to coordinate Asian gold markets and develop a “gold corridor” for the countries along China’s Belt and Road initiative. Therefore, both private and public sectors will be able to accumulate the oldest form of money as a backstop to local currencies, as an alternative to accumulating those of their trading partners.

Geopolitics evolved from fighting proxy wars in the Middle East and Ukraine, which were effectively won by Russia, to the less obvious war of trade tariffs. President Trump has styled himself as “A Tariff Man”. We have presumed that he is ignorant of economics, but that is no longer the point. Tariffs have evolved from a policy to make America great again to bankrupting China. China is seen as the greatest economic threat to America, and in this duel, tariffs are Trump’s weapon of choice.

The objective is to impede China’s technological development. It was tolerated when China, to steal a line from Masefield’s Cargoes, was the world’s supplier “…of firewood, iron-ware and cheap tin trays”. But China is moving on, creating a sophisticated economy with a technological capability that is arguably overtaking that of America. The battle for technological supremacy came out into the open with the detention on 1 December in Vancouver of Meng Wanzhou, the CFO of Huawei. Huawei is China’s leading developer of 5G mobile technology, installing sophisticated equipment around the world. 5G’s capability will make internet broadband redundant and will become widely available from next year.

Ms Meng’s arrest represents such an escalation of deteriorating relations between China and America that many assume it was ordered by rogue elements in America’s deep state. Maybe. But these things are difficult to reverse: does America tell the Canadian authorities to just let her go? It would uncharacteristic for America to admit a mistake, and it would probably need President Trump to personally intervene. This is difficult for him because application of the law is not in his hands.

If Ms Meng is not released, we will enter 2019 with the Chinese publicly insulted. They will realise, if they haven’t already, that ultimately there can be no accommodation with America. Fighting tariffs with more tariffs is a policy that will achieve nothing and damage China’s own economy.

It therefore becomes a matter of time when, and not if, China deploys financial weapons of its own. These will be targeted at the US’s obvious weaknesses, including her dependency on China for maintaining and increasing holdings in US Government debt. The increasingly compelling use of physical gold to both protect the yuan from attack in the foreign exchanges and limit the rise of yuan interest rates would serve to insulate China from the fall-out of a collapsing dollar.

The economic outlook, and the effect on the dollar

For market historians, the economic situation rhymes strongly with 1929, when the Smoot-Hawley Tariff Act was being debated. Eighty-nine years ago, the first round of votes in Congress was passed on 30 October, and Wall Street fell heavily that month in anticipation of the result. Following the G20 meeting two weeks ago, where it was vainly hoped there would be progress in the tariff negotiations between the US and China, markets fell heavily, reminding market historians of the 1929 precedent.

When President Hoover stated his intention to sign Smoot-Hawley into law on 16 June 1930, Wall Street crashed again. The lesson for today is that equity markets are likely to crash again if Trump continues with his tariff policies. Smoot-Hawley raised import tariffs on over 20,000 imported raw materials and goods, increasing the average tariff rate from 38% to over 60%. The difference today is that instead of tariffs being used only for protectionism, they are being targeted specifically against China.

There will be two likely consequences. The first is the the undermining of financial markets, which in the 1930s led to the virtual collapse of the US banking system and the global depression. And secondly, there is the escalation of a wider financial war raging between China and the US. These two factors are potentially very serious, with stock markets already on shaky ground.

This is not the uppermost reason for market weakness in investors’ minds, who worry about the economic outlook more generally. The conventional credit cycle features rising interest rates as a consequence of earlier monetary expansion, and the exposure of malinvestments. Markets discount the phases of the credit cycle when they become apparent to far-sighted investors, and only indirectly contribute to the collapse itself. But when valuations have become wildly optimistic, the fall in markets becomes a crisis on its own, contributing to the collapse in business that follows. This was the point taken up by Irving Fisher in the wake of the 1929-32 bear market.

In any event, the global economy appears to be at or close to the end of its expansionary phase, and is heading for recession, or worse. As well as the potential impact from an unanchored reserve currency, price inflation in the US will be boosted by Trump’s tariffs, which amount to additional consumer taxes. Price inflation pressures will then call for further rises in interest rates, while economic prospects will point to easing monetary conditions.

We have yet to see how this will be resolved. A further problem is that an economic downturn will increase government welfare commitments and therefore borrowing requirements. Bond yields will tend to rise and therefore borrowing costs, driving spendthrift governments into a debt-trap, just when price inflation is likely to demand higher interest rates. The most likely outcome will be further losses of fiat currencies’ purchasing power.

The 1930s depression saw a rising purchasing power for the dollar, with all commodity and consumer prices declining. The dollar was on a gold standard, and prices were effectively measured in gold, the dollar acting as a gold substitute. This is no longer true, and the purchasing power of the dollar, along with all other fiat currencies will at best remain stable measured against consumer products, or more likely will decline. In other words, a severe recession which looks increasingly likely on cyclical grounds, will lead to higher gold prices, irrespective of fiat currency interest rates.

The gold-fiat relationship and monetary inflation.

According to the World Gold Council, central bank gold reserves total 33,757 tonnes, worth $1.357 trillion at current prices. Global fiat money is estimated to total about $90 trillion, which suggests there’s 66 times as much in global cash and bank deposits as there is gold to back it.[iii] Admittedly, issuers have different gold-to-currency ratios, but overall this suggests the gold price would be far higher if a sustainable level of currency convertibility is to return.

The reason we must consider this relationship is that in the light of all the foregoing, the gulf between the two quantities is set to accelerate from the currency side.

In the early 1930s, dollar prices of raw materials and commodities fell heavily, bankrupting farmers and miners world-wide. The purchasing power of the dollar rose, because it acted as a gold substitute. Today there is no convertibility between the dollar and gold at all, so the effect of a global economic depression is bound to see the gulf between the dollar and gold widen, as central banks expand the quantity of money in an attempt to fight recession and keep their governments solvent. There can be no doubt the policy response from the Fed and all the other welfare-state central banks will be neo-Keynesian, exploiting all the freedoms of unsound money.

In fact, the increase in the money quantity is not new, dating from the Lehman crisis. This is shown in the chart below, of the fiat money quantity, compared with its long-term pre-Lehman growth path.

FMQ is basically the sum of true (Austrian) money supply and commercial bank reserves held at the Fed. Even though its growth has recently stalled, the gap between the pre-Lehman crisis growth path still stands at $5.55 trillion.

Now imagine what will happen when the global economy stalls. The Fed, along with other central banks, will be forced to make yet more currency available to support the banks, finance government spending and encourage consumption. The injection in the US last time was roughly $10 trillion, or 55% of GDP. Next time, with interest rates needing to be maintained in order to support the currency, it will almost certainly require more aggressive quantitative easing, with central banks substantially increasing their purchases of government bonds.

Gold is already close to all-time lows, relative to the money quantity. This is shown in the next chart.

It was from similar indexed levels that gold bottomed in the late sixties. A return to the level set by President Roosevelt in January 1934 implies a price of $53,250 today. This is not a forecast, and its only relevance is to illustrate the potential for an upward adjustment in the gold price, based on the degradation of the dollar since 1934.

Physical factors

Demand for physical gold consistently exceeds mine supply. Central banks are accumulating bullion, adding 425 tonnes in the year to September 2018. Chinese private sector demand continues at a steady pace, which measured by withdrawals from the Shanghai Gold Exchange, is running at a 1,900-tonne annualised rate. India’s total gold imports were 919 tonnes in the year to end-September (according to the World Gold Council), so adding identified central bank demand to private sector demand from India and China, these three sources account for 3,344 tonnes annually, which is the same as global mine supply.

The supply/demand balance is more complicated than these figures suggest. Some of the mine supply is not available to markets. For example, China, which is the largest mine supplier by far, severely restricts gold exports. Official reserves at central banks are only what are declared and includes gold out on lease or swapped, and therefore not in possession of the central bank. They are therefore short of actual possession, exposing them to potential counterparty and price risk.

Net demand from the rest of the world and from unrecorded categories is satisfied from the existing above-ground stock of bullion, which we estimate to be about 175,000 tonnes. Only an unknowable fraction of this is available for market liquidity. The most identifiable swing-factor is ETF demand, which saw outflows of 103 tonnes in the three months to September[iv]. Looking back over recent years, another substantial ETF outflow was in 2016 Q4, when the gold price bottomed, and in 2015 Q2 to Q4 saw net outflows every quarter. It appears that ETF demand is acting as a contrary indicator of future price trends.

This fits in with market theory, which based on investor psychology predicts investors are at best trend-chasers, investing most heavily at market tops and liquidating positions at price lows. The peak of net ETF liquidation in 2018 was in June and August. In June the gold price breeched the psychologically important $1300 level, and in August the market turned higher at $1160. ETF net selling tells us therefore the gold price may have recently indicated a turning point.

Supply from ETFs at market lows satisfies demand from those that have a continuing demand. We have seen the pattern of central banks increasing their buying on lower prices, but there is also some evidence commercial banks are accumulating bullion for their own books, possibly for risk purposes.

Under the new Basel III standard, physical gold held on an allocated basis is now classified as cash and has the advantage of zero risk weighting, compared with a 15% haircut under Basel II. Besides physical cash notes (which in practice banks try to minimise in their branches), the only other alternative to cash is balances held on the bank’s account at a central bank. The ECB and the Bank of Japan charge negative interest rates on these balances, which for commercial banks in the EU and Japan leaves only physical gold as an alternative.

For the thinking banker, it makes sense to hedge fiat currency exposure (which is the entirety of his business) with some physical bullion. The opportunity cost in the form of lost interest is not a factor, with overnight money-market rates in euros and yen negative. And the regulatory cost of holding gold is being removed.

A brief analysis of the availability of physical supply points to acute shortages on any expansion of demand. Seasonal factors can have a significant impact, with the Diwali festival in India a month ago, and the Chinese New Year in early February leading to an accumulation of bullion inventories.

The absorption of available liquidity from mine supply and scrap recycling tells us the physical market has become extremely tight. Instability in fiat currencies, particularly weakness developing in the dollar’s trade-weighted index, could therefore have a disproportionate effect on the gold price as a wide range of investing institutions and commercial banks try to correct their almost zero asset allocation to gold.

Paper markets for gold

As the chart below shows, gold bottomed in December 2015, since when it has been in a narrowing consolidation. Within this pattern, there is a seasonal effect, whereby gold sells off in early December and subsequently rallies. This is shown by the three black arrows on the chart.

There are reasons why this is so. The December contract is the last active contract to expire before the year end, when many hedge funds and bullion banks make up their accounts. Hedge fund managers want to present a balance sheet with less risk exposure than they normally run, and banks will wish to present shareholders and regulators with a sanitised version of their risk exposure as well.

This exposure cycle has had an extra twist this time, because market speculators in futures markets have shorted a wide range of futures in order to capture a strong dollar. In the case of the Comex gold future, this has led to an unprecedented technical position, shown in the next chart.

Over the last twelve years, hedge funds (which are represented in this category of speculator) have only been net short of Comex gold contracts twice. The first time was in late-2015, which marked the end of the 2011-15 bear market, and the second was recently, marking the sell-off to $1160. The only reason it has partially corrected is due to the expiry of the December contract.

Market sentiment is still markedly pro-dollar and anti-everything else, including gold. The underlying assumption appears to be that foreigners require dollars and the dollar has the highest interest rates of the major currencies. This being the case, the first supposition is an error. There is a growing expectation that the US economic growth will slow next year, and the Fed is under pressure not to raise rates any further.

When these changing factors are taken into account, the dollar is likely to be sold, and hedge fund speculators will take the other tack. The market-makers, traditionally the bullion banks, are bound to be aware of this possibility and will therefore try to maintain an even book.

Conclusion

All factors examined in this article point to higher gold prices in 2019. They can be summarised as follows:

- The world is awash with dollars at a time when markets act as if there is a shortage. When the truth emerges, the dollar has the potential to fall substantially against other currencies, leading to a rise in the price of gold.

- The move towards gold and against the dollar in Asia accelerated in 2018, with Russia having replaced the dollar with gold as its principal reserve currency. China has laid the foundation with an oil-yuan futures contract, which can be a bridge to yuan-gold contracts in both Hong Kong and Dubai. This is a direct challenge to the dollar as a reserve currency, and likely to be attractive to oil suppliers, such as Iran, seeking to circumvent use of the dollar and accumulate gold instead.

- America’s trade war against China appears to be less about unfair trade practices and more about stopping China from evolving into a serious technological competitor against the US. In 2019, there is a strong possibility the tariff war will escalate into a wider conflict, with China selling down its exposure to the dollar and US Treasury debt. That would create significant difficulties for the US Government and the dollar itself.

- With the credit cycle turning and the addition of American tariffs, markets are at a growing risk of replicating the 1929-32 crash and the economic depression that followed. This time, instead of commodities and consumer products effectively priced in gold through a gold standard, they will be priced in fiat currency. Monetary policies will ensure liquidity is freely available to support the commercial banks, government spending and economic activity. This is a recipe for higher gold prices.

- Demand for physical gold continues to outstrip mine supply. In 2019, risk-weighting rules in Basel III open up the opportunity for commercial banks to augment their liquidity with allocated bullion, attractive to euro- and yen-based banks who face negative interest rates on short-term cash alternatives.

- The technical position in the paper markets looks favourable, with close to record levels of bearishness, and an established pattern of December rallies in the gold price.

_________________

end

A must watch interview of Andrew Maguire as he talks to Bart Chilton about the gold/silver manipulation

start at 19.20

|

7:14 AM (15 minutes ago) | |||

|

||||

All,

This from My live RT America interview last night with Commissioner Bart Chilton who starts by validating my gold and silver manipulation evidence which was provided to the CFTC that JPM has been manipulating silver and Gold & goes as far as to also validate the JPM /Bear Sterns manipulation event which we better get downloaded before JPM demand to have it pulled.

https://www.youtube.com/watch?v=Bf8HMgSH050 it commences at the 19.20 min point .

Unfortunately , there was so little time and he kept throwing other questions at me but he has agreed to have me in the studio to talk nothing but silver & gold at some point. At least this counters all the naysayers like Christian etc. who still deny any form of manipulation.

Chris I am getting you a time slot with Bart, would you be able to actually travel to the NY or DC studio?

Warmest regards

Andrew

here is the big interview:

//mail.google.com/mail/u/0/#inbox/FMfcgxvzLhjckJqvWHthfWldjdXRHbzj?projector=1

END

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.9008/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.9015 /shanghai bourse CLOSED DOWN 40.31 POINTS OR 1.53%

HANG SANG CLOSED DOWN 429.46 POINTS OR 1.62%

2. Nikkei closed DOWN 441.36 POINTS OR 2.02%

3. Europe stocks OPENED ALL RED

/USA dollar index RISES TO 97.57/Euro FALLS TO 1.1287

3b Japan 10 year bond yield: FALLS TO. +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.62/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.16 and Brent: 60.91

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.26%/Italian 10 yr bond yield UP to 2.97% /SPAIN 10 YR BOND YIELD UP TO 1.40%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.71: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.25

3k Gold at $1237.95 silver at:14.60 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 31/100 in roubles/dollar) 66.52

3m oil into the 52 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.62DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9973 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1257 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.26%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.88% early this morning. Thirty year rate at 3.15%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3840

Global Stocks Tumble On Poor Econ Data From China To Europe

It’s a sea of red to end the week as world stocks and US futures tumbled on Friday after weak economic data from China to Europe raised global recession fears and left investors nervous over the impact of a still-unresolved Sino-U.S. trade dispute even as China announced it would roll back retaliatory auto tariffs by 3 months; Treasuries and the dollar jumped amid a renewed flight to safety.

Growth concerns came back into focus after European Central Bank President Mario Draghi said economic risks were moving to the downside, while in China retail sales and industrial production figures for November fell significantly short of estimates. The lackluster readings from Europe on car sales and manufacturing simply added to the gloom.

The MSCI All-Country World Index was down half a percent, with all major markets deep in the red. Europe’s Stoxx 600 Index headed for a weekly loss, dragged lower by automakers after regional sales slumped in November for the third month in a row.

Euro zone business ended the year on a weak note, expanding at the slowest pace in over four years as new order growth all but dried up, hurt by trade tensions and the Yellow Vests” movement. The France PMI survey showed French business activity plunged unexpectedly into contraction this month, retreating at the fastest pace in over four years with the slowdown largely blamed on the recent violent anti-government protests.

Elsewhere, Germany’s private sector expansion slowed to a four-year low, suggesting growth in Europe’s largest economy may be weak in the final quarter as Mfg PMI declined from 51.8 to 51.5 (exp. 52.0) while the Services PMI dropped from 53.3 to 52.2, also missing expectations for a rebound to 53.4.

Adding to the ECB’s gloomy outlook, the Bundesbank lowered German growth projections, warning of downside risks: the German central bank today revelaed its updated growth projections, which cut back the GDP forecast to just 1.5% this year from 2.0% expected previously, hardly a surprise after the -0.2% q/q contraction in Q3. The forecast for 2019 was cut to 1.6% from 1.9% and for 2020 and 2021 the Bundesbank expects rowth of 1.6% and 1.5% respectively.

Stock markets in Europe opened sharply lower, with Germany’s DAX index falling 1.5% while the pan-European STOXX 600 index was down 0.9%, paring some losses as European automakers saw their losses cut in half on the China tariff news.

The data out of Europe added to weak readings from China, where November retail sales grew at the weakest pace since 2003 and industrial output rose the least in nearly three years, underlining risks to the world’s second-largest economy as Beijing works to defuse a trade dispute with the United States.

A Chinese statistics bureau spokesman said the November data showed downward pressure on the economy is increasing.

The data “means that the worst is yet to come and policymakers will be very worried, particularly with consumption growth falling off a cliff,” said Sue Trinh, head of Asia FX strategy at RBC Capital Markets in Hong Kong. “So I expect further support measures including rate cuts will come in coming weeks, although these data would indicate measures to date aren’t really working.”

The Chinese yuan weakened 0.4% to 6.9063 per dollar in offshore trade following the data.

As a result, equities slumped across Asia, with shares in Hong Kong and Japan leading the retreat. MSCI’s index of Asia-Pacific shares ex Japan fell 1.5%. Japan’s Nikkei, also dragged down by the country’s weak tankan sentiment index, dropped 2.0%. China’s benchmark Shanghai Composite and the blue-chip CSI 300 closed down 1.5 percent and 1.7 percent, respectively, and Hong Kong’s Hang Seng was off 1.5 percent.

“The data this morning out of France really hasn’t helped the mood. You look at China data, you look at the flash PMIs out of France and Germany and they’ve really sort of reinforced concerns that the global economy is slowing down,” said CMC Markets chief markets analyst Michael Hewson. “Ultimately, I think it rather questions the wisdom of the ECB ending its asset purchase program at the end of this month. You’ve got Mario Draghi basically tightening into a downturn.”

Over in the US, S&P 500 futures also pointed to a drop at the open, though both declines were tempered somewhat on news that China will temporarily remove a retaliatory duty on U.S.-imported automobiles.

“Although hopes of progress in U.S.-China talks and cheap valuations are supporting the market for now, we have lots of potential pitfalls,” said Mizuho’s Nobuhiko Kuramochi. “If U.S. shares fall below their triple bottoms hit recently, that would be a very weak technical sign.”

In the currency market, the euro was down 0.7 percent after the weak PMIs, last changing hands at $1.1288. The Bloomberg Dollar Spot Index headed for its best week in four months, rising to 1,215 and just shy of 2018 highs. Antipodean currencies led losses in the Group-of-10 basket.

Sterling’s rally fizzled as signs that the British parliament was headed towards a deadlock over Brexit prompted traders to take profits from its gains made after Prime Minister Theresa May had survived a no-confidence vote.

The European Union has said the agreed Brexit deal is not open for renegotiation even though its leaders on Thursday gave May assurances that they would seek to agree a new pact with Britain by 2021 so that the contentious Irish “backstop” is never triggered.

In overnight Trump-related news, Federal prosecutors are investigating whether US President Trump’s inaugural committee misspent some of the record amount of funds it raised, while there were later comments from White House Press Secretary Sanders that President Trump had limited engagement with the inauguration committee. President Trump is also said to be considering Kushner for Chief of Staff, while there were separate reports that US President Trump is said to have met with Chris Christie to discuss Chief of Staff position. Axios reported that US President Trump sees Chris Christie as a top contender to replace John Kelly as Chief of Staff

Oil prices gave up some of their Thursday’s gains following inventory declines in the United States and expectations that the global oil market could have a deficit sooner than they had previously thought. U.S. crude futures edged down 0.5% to $52.32 per barrel and Brent crude slipped 0.6 percent to $61.09, after both gained more than 2.5 percent on Thursday. Gold (-0.3%) is set for is biggest weekly fall in five weeks due to a firmer USD as traders focus on next week’s tabled Fed rate hike. Looking at base metals, copper is on track for a third consecutive weekly drop with downside exacerbated by the downbeat Chinese industrial production translating into weaker demand as the red metal faces a 15% yearly decline.

Expected data include retail sales, industrial production, and PMIs. No major companies are reporting earnings

Market Snapshot

- S&P 500 futures down 0.9% to 2,626.25

- STOXX Europe 600 down 1.4% to 344.61

- MXAP down 1.4% to 149.12

- MXAPJ down 1.5% to 481.32

- Nikkei down 2% to 21,374.83

- Topix down 1.5% to 1,592.16

- Hang Seng Index down 1.6% to 26,094.79

- Shanghai Composite down 1.5% to 2,593.74

- Sensex up 0.03% to 35,940.82

- Australia S&P/ASX 200 down 1.1% to 5,602.00

- Kospi down 1.3% to 2,069.38

- German 10Y yield fell 3.4 bps to 0.251%

- Euro down 0.6% to $1.1292

- Italian 10Y yield fell 4.3 bps to 2.594%

- Spanish 10Y yield fell 0.8 bps to 1.416%

- Brent futures little changed at $61.42/bbl

- Gold spot down 0.2% to $1,239.08

- U.S. Dollar Index up 0.5% to 97.53

Top Overnight News

- European leaders rebuffed Theresa May’s pleas to help her sell the Brexit agreement to a skeptical U.K. Parliament, toughening their stance as they stepped up planning for a chaotic no-deal divorce

- The euro-area economy is closing out 2018 on a gloomy note, with a measure of activity unexpectedly dropping to its lowest in just over four years

- China’s economy slowed again in November as retail sales and industrial production weakened, creating a challenging backdrop for policy makers who gather next week to set the tone for the year at their annual Economic Work Conference in Beijing

- As Japanese government bond yields slide, some Bank of Japan officials see no problem with them dropping to zero or even below, according to people familiar with the matter

- In Washington and Beijing, the idea that China is willing to water down its plans for high-tech industrial dominance to appease President Donald Trump is already meeting with skepticism

Asian equity markets were negative across the board as sentiment in the region soured following the lacklustre lead from Wall St and as region digested disappointing data from China. ASX 200 (-1.1%) and Nikkei 225 (-2.0%) both declined from the open with Australia led lower by tech, telecoms and the largest weighted financials sector, while the Japanese benchmark was subdued amid a firmer JPY and mixed Tankan data despite the headline Large Manufacturers Index and Large All Industry Capex topping estimates. Elsewhere, Hang Seng (-1.6%) and Shanghai Comp. (-1.5%) were also pressured after Chinese Industrial Production and Retail Sales data both fell short of estimates, with underperformance seen in Hong Kong as this year’s run of lacklustre stock market debuts continued in the domestic exchange. Finally, 10yr JGBs were higher as they tracked gains in T-notes and with prices underpinned by safe-haven demand which saw 10yr JGBs print the highest since November 2016.

Top Asian News

- Some at BOJ Are Said to Be Fine With Yields Going to Zero

- Thailand’s Richest Man Said to Tap BofA, UBS for $1.5b AWC IPO

- SoftBank IPO Said to See 2-3 Times Demand From Big Investors

- Not Such a Happy Friday for Asia’s Beleaguered Stock Traders

- Japan Post Is in Talks to Buy Minority Stake in Aflac

European equities are poised to finish the week on the backfoot (Eurostoxx 50 -0.9%) following the weak lead from Asia as sentiment turned sour amid the release of disappointing Chinese industrial production and retail sales, highlighting weakness in the Chinese economy. As such, around 75% of the Stoxx 600 (-0.9%) are in the red, Switzerland’s SMI (-1.4%) marginally lags peers with all 20 stocks in negative territory. In terms of sectors, IT names underperform alongside auto names (seen as trade proxies due to heavy exports) as a result of the aforementioned Chinese retail sales signalling an impact from ongoing trade disputes. However, European auto names spiked higher following reports that China are to lift retaliatory tariffs on US autos for 3-months from January 1st next year (i.e. suspending the 40% tariff plan and sticking to 15%). In terms of individual movers GVC Holdings (+8.8%) shares rose to the top of the UK benchmark with Citi citing next week’s Parliament vote on FOBT stakes being “significantly positive” as shareholders will be paid out GBP 676mln if the legislation is not passed by 28th March 2019.

Top European News

- Sweden Moves Step Closer to New Election as Lofven Loses PM Vote

- How Ireland Outmaneuvered Britain on Brexit

- Italian Bonds Get No Favors From Draghi’s Reinvestment Plans

- European Car Sales Slump in November With No Sign of Rebound

In currencies, The Antipodean Dollars have derived some scant support from reports that China will freeze and backtrack on a proposed increase in US auto tariffs w/e January 1 next year, in line with recent speculation, but the Aussie and Kiwi remain on the backfoot and significantly weaker than their G10 counterparts following sub-forecast Chinese data overnight and RBNZ consultations about lifting high grade bank capital requirements by 100%. Aud/Usd is holding just off a fresh December low around 0.7155 after breaching 0.7200 and tech supports below the figure at 0.7186 (55 DMA) and 0.7163 (Fib), while Nzd/Usd has lost grip of 0.6800 as the Aud/Nzd cross pivots 1.0550.

- EUR/GBP: Also major underperformers, as the single currency extended post-ECB losses on the back of further declines in EZ PMIs (French readings especially dire as manufacturing, services and composite all tumbled into sub-50 contractionary territory) and through recent support just ahead of 1.1300 vs the Greenback to 1.1286 before finding some bids. Note, a decent 1 bn option expiry at the 1.1300 strike may provide some traction. Meanwhile, Brexit remains the big bane for Sterling and given the ongoing impasse between UK PM May and EU leaders on the back-stop, Cable has retreated sharply towards 1.2570 and chart-wise back below the 10 DMA circa 1.2660.

- JPY: As usual, demand for the safe-haven Yen is just keeping Usd/Jpy depressed within a tight 113.70-40 range, along with 1.4 bn expiries at 113.75.

- EM: An unexpected, though far from total surprise ¼ point CBR rate hike has underpinned the Rub against the grain of overall regional currency weakness on risk-off flows, with the Rouble comfortably above 66.5000 vs the Usd.

In commodities, WTI (-0.7%) and Brent (-0.9%) swings between gains and losses following an uneventful overnight session as prices consolidated after yesterday’s rally. The complex saw some upside in recent trade after Libya’s NOC chairman was pessimistic about reopening its 300k BPD El-Sharara after an armed group halted production at the oilfield. Traders will be eyeing this evening’s Baker Hughes rig count as fresh catalyst. Note, WTI Jan’19 options expire today at 19.30GMT. Elsewhere, gold (-0.3%) is set for is biggest weekly fall in five weeks due to a firmer USD as traders focus on next week’s tabled Fed rate hike. Looking at base metals, copper is on track for a third consecutive weekly drop with downside exacerbated by the downbeat Chinese industrial production translating into weaker demand as the red metal faces a 15% yearly decline. Finally, Shanghai steel extended gains for a third day in a row after two major steelmaking cities (Tangshan and Xuzhou) demanded mills to curtail production amid worries that they will not meet pollution reduction targets this year. For context, Tangshan accounts for 10% of China’s total steel output while Xuzhou is in the number two steelmaking province.

Looking at the day ahead, in the US there should be plenty of focus on the November retail sales report where expectations is for a +0.4% mom ex auto and gas print and +0.5% mom control group reading. A reminder that the latter is a direct input into the GDP accounts. Also due out across the pond is the November industrial production print (+0.3% mom expected) and October business inventories. Meanwhile we’re due to get comments from the ECB’s Guindos and Lautenschlaeger this morning before Angeloni speaks this afternoon.

US Event Calendar

- 8:30am: Retail Sales Advance MoM, est. 0.1%, prior 0.8%; Retail Sales Ex Auto MoM, est. 0.2%, prior 0.7%

- Retail Sales Ex Auto and Gas, est. 0.4%, prior 0.3%; Retail Sales Control Group, est. 0.4%, prior 0.3%

- 9:15am: Industrial Production MoM, est. 0.3%, prior 0.1%; Manufacturing (SIC) Production, est. 0.3%, prior 0.3%

- 9:45am: Bloomberg Dec. United States Economic Survey

- Markit US Composite PMI, prior 54.7

- Markit US Manufacturing PMI, est. 55, prior 55.3;

- Markit US Services PMI, est. 54.6, prior 54.7

- 10am: Business Inventories, est. 0.6%, prior 0.3%

DB’s Jim Reid concludes the overnight wrap

With just ten business days left in 2019 now, after the Brexit shenanigans earlier this week markets were always hoping that the ECB would be a less eventful affair. Indeed, luckily there was no sign of a scrooge surprise from Mario Draghi in what proved to be a fairly non-eventful policy meeting yesterday.

As expected we got confirmation that net asset purchases were to cease by the end of the year while the dovish tightening that we expected was affirmed with an endorsement of the short end rally and a hint that a replacement for TLTRO2 is in the pipeline. In line with the views of our economists (link here ), the reinvestment programme retains a lot of flexibility over the purchases. There was no twist of the portfolio, and the ECB’s preference was for a revision to the guidance on the period of full reinvestment, implying this could last longer. “Continuing confidence with increasing caution” was Draghi’s new mantra our colleagues highlight. That said there was one surprise and that was the suggestion that the ECB is starting to rethink the structural impact of negative deposit rates on the banking system. This increases the possibility of a technical deposit rate hike – a hike for non-cyclical/non-monetary policy purposes – in 2019. Draghi said the reductions to the staff GDP growth forecasts take the economy on a path “closer to potential”. This could be an admission that the window to raise rates to address structural bank profitability is getting narrower.

So where does that leave us? In their 2019 outlook our economists delayed the timing of lift-off of the policy rate tightening cycle from September 2019 to March 2020 given the deteriorating expectations for growth and inflation. However they also mentioned the risk of a technical, one-off deposit hike and the team believe that March 2019 is perhaps the best time for the technical hike now.This is arguably when the replacement for TLTRO2 will be due. It is also six months before the current time commitment to unchanged policy rates expires, meaning March is the appropriate time to consider an extension of the commitment if they are right about the outlook for the economy. Something to consider then.

The market also seemingly viewed the meeting as a bit of a non-event. The euro initially declined and hit as low as -0.33% versus the dollar intraday but ended up closing -0.07%. The STOXX 600 flipped between gains and losses with no real conviction and eventually closed a shade in the red with a -0.17% decline. Meanwhile, 10y Bund yields did nudge to an intraday low of 0.254% at one stage but also reversed into the close to finish at 0.281% and +0.5bps on the day. A remarkable statistic about Bund yields is that they are currently lower than they were when QE started in March 2015, when Draghi supersized QE and cut the depo rate in March 2016, and when Draghi outlined plans to end QE this December and set guidance for a rate hike at the June meeting earlier this year.

Also keep in mind that the ECB’s balance sheet has increased by €2.5tn since QE started. In that time it has cost the ECB about €119bn for each one-tenth of a percent to get the year-on-year headline CPI number to where it is now although Eurozone CPI hasn’t risen by that different an amount to US CPI over the same period. More startling is the fact that it has cost the ECB €625bn for each tenth of a percent increase in core CPI which has been in a fairly narrow range over the whole period. The gap between Eurozone and US core CPI has also stayed pretty constant. In addition, while Bund yields have in essence moved sideways, 10y BTP yields are 171bps higher and eurozone banks have lost €152bn in market cap. We will never know the counterfactual but there’s been a huge financial cost to the program but with inconclusive evidence about its success.