GOLD: $1248.00 UP $10.60 (COMEX TO COMEX CLOSINGS)

Silver: $14.69 UP 13 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1246.00

silver: $14.64

For comex gold and silver:

DEC

Again, we have Goldman Sachs dealer and JPMorgan customer account stopping (receiving the gold) 9/12 contracts.

EXCHANGE: COMEX

CONTRACT: DECEMBER 2018 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,237.000000000 USD

INTENT DATE: 12/14/2018 DELIVERY DATE: 12/18/2018

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 7

661 C JP MORGAN 2

737 C ADVANTAGE 12 3

____________________________________________________________________________________________

TOTAL: 12 12

MONTH TO DATE: 7,273

NUMBER OF NOTICES FILED TODAY FOR DEC CONTRACT: 12 NOTICE(S) FOR 1200 OZ (0.037 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7273 NOTICES FOR 727300 OZ (22.622 TONNES)

SILVER

FOR DECEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

Total number of notices filed so far this month: 3899 for 19,495,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3367: up 152

Bitcoin: FINAL EVENING TRADE: $3521 up 299.00

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY SIZED 872 CONTRACTS FROM 175,076 DOWN TO 173,574 DESPITE FRIDAY’S CONSIDERABLE 21 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 20 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1919 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1919 CONTRACTS. WITH THE TRANSFER OF 1919 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1919 EFP CONTRACTS TRANSLATES INTO 9.595 MILLION OZ ACCOMPANYING:

1.THE 21 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

NOW 20.730 INITIALLY STAND FOR DECEMBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DEC: 19,723 CONTRACTS (FOR 11 TRADING DAYS TOTAL 19,723 CONTRACTS) OR 98.62 MILLION OZ: (AVERAGE PER DAY: 1793 CONTRACTS OR 8.966 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 98.62 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 14.08% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,775.68 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

ACCUMULATION FOR NOVEMBER /2018: 247.18 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 872 DESPITE THE CONSIDERABLE 21 CENT LOSS IN SILVER PRICING AT THE COMEX //FRIDAY.. AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1919 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A FAIR SIZED: 1047 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1919 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 872 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 21 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.56 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .875 BILLION OZ TO BE EXACT or 125% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DEC MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./AND NOW DEC. AT 20.900 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 3049 CONTRACTS DOWN TO 397,688 WITH THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $5.60//.FRIDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 10,219 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 10,219 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 397,688. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7170 CONTRACTS: 3049 OI CONTRACTS DECREASED AT THE COMEX AND 10,219 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 7170 CONTRACTS OR 717,000 OZ = 22.30 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $5.60???

FRIDAY, WE HAD 9668 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC : 95.966 CONTRACTS OR 9,596,600 OZ OR 298.49 TONNES (11 TRADING DAYS AND THUS AVERAGING: 8724 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAYS IN TONNES: 298.49 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 298.49/2550 x 100% TONNES = 11.70% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 7069.46 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018: 552.88 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 3049 WITH THE LOSS IN PRICING ($5.60) THAT GOLD UNDERTOOK FRIDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 10,219 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 10,219 EFP CONTRACTS ISSUED, WE HAD AN STRONG GAIN OF 7170 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

10,219 CONTRACTS MOVE TO LONDON AND 3049 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 22.30 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $5.60 IN YESTERDAY’S TRADING AT THE COMEX??

we had: 12 notice(s) filed upon for 1200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $10.60 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 763.56 TONNES

Inventory rests tonight: 763.56 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 13 CENTS TODAY:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV

i) a withdrawal of 939,000 oz with silver rising?

/INVENTORY RESTS AT 317.796 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 872 CONTRACTS from 174,446 DOWN TO 173,574 AND MOVING FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1919 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1919 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 872 CONTRACTS TO THE 1919 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD GAIN OF 1047 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 5.235 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. AND NOW 20.900 MILLION OZ STANDING IN DECEMBER.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 21 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// FRIDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 1919 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 4.23 POINTS OR 0.06% //Hang Sang CLOSED DOWN 6.81 POINTS OR 0.03% //The Nikkei closed UP 132.85 OR 0.62%/ Australia’s all ordinaires CLOSED UP 0.95% /Chinese yuan (ONSHORE) closed UP at 6.8971 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.76 dollars per barrel for WTI and 61.08 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED UP AT 6.8966AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8971: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

i

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)We reported to you last week, the ugly numbers that China reported on retail sales and industrial production..probably their most important figures. Jeffrey Snider reports on those figures and what it means….Is the lack of USA dollars in China going to create a crisis…he believes so

a must read..

(courtesy Jeffrey Snider)

ii)Don’t you feel sorry for us Canadians: Canada helped its neighbour in arresting Meng and now they are in a heap of trouble with China. Canada and China have had strong relations since 1949 (Norman Bethune, a Canadian helped China win their independence) Now China is preparing for an escalation of conflict with Canada.

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)FRANCE

France in turmoil over the weekend as pepper spray was used on protesting yellow vests. Also bare breasted Mariannes began to face off with the French police

(courtesy zerohedge)

b)Macron admits that he made mistakes: mainly not listening to his people…the movement now spreads to Israel,Belgium, Canada and the Netherlands

ii)UK

i)May’s cabinet secretly are talking about a ‘second referendum” which would not be good. However the UK just does not know what to do next

( zerohedge)

ii)The vote is now set for Jan 14.2019 and it will be either yes or no. Then the fun begins

( zerohedge)

iv)Daniel Lacalle states that the ECB’s problem has never been a lack of stimulus..but an excess of stimuli.He outlines why!

( Daniel Lacalle)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

MALAYSIA/GOLDMAN SACHS

This could be far reaching: Malaysia files a criminal fraud charge against USA Goldman Sachs and this may be followed by the uSA

(courtesy zerohedge)_

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)Venezuela

9. PHYSICAL MARKETS

ii)As expected, here comes the class action lawsuits against JPMorgan for rigging gold and silver. I believe it is a touch to early. What JPMorgan’s chief trader admitted to was only 1% of the fraud

( Giel/CNBC/GATA)

iv)A good history lesson of an early attempt at standardizing money using international gold coins failed.( JP Konig/Bullionstar/GATA)

v)Your most important commentary of the day. For over 18 years I have been pounding the table on the dangers of derivatives and it seems that this danger is coming to fruition. Last month a small sector had trouble clearing a trade of just over 100 million dollars. The leveraged bond market has basically busted as there were no takers for a trade and the banks were obliged to put this junk on their books. The big problem is what he highlighted to you on Friday, the huge BBB- bonds trading (3/4 of a trillion dollars) and if they are downgraded one step to junk, the game is over….

a must must read..

( Ambrose Evans Pritchard)

vi)They are perfectly correct: there is a lack of liquidity, stock markets collapse.

another must read..

( Jain/Times of India/GATA)

vii)Von Greyerz at Kingworld news highlights correctly the collapse of the European bank stock index and he warns that there will be an imminent crash of the European banking system and then a stock market crash.

(Kingworld news/ Von Greyerz/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

the “king” has spoken. Bond King Jeffrey Gundlach spooks the markets

(courtesy zerohedge)

ii)Market data/

a)Even soft data is now coming in at horrifying levels. Today the all important Empire mfg index (New York mfg) plunges to almost 2 year lows

( zerohedge)

a)Friday night, a judge in Texas ruled that Obamacare is unconstitutional after Trump eliminates the individual mandate. No doubt that this will be appealed right to the Supreme Court. Trump is elated.

( zerohedge)

b)More and more important people are calling for the Fed to stop tightening in a bad economic environment. Today it is Stanley Druckenmiller and most important former Fed governor Kevin Warsh

b ii) Trump again slams the Fed on the eve of a rate decision. He correctly states that the Fed hiking is causing the “world to blow up”!!

c)Despite earning over 8% on many of the state pension funds and an eight billion dollar contribution, the shortfall overall worsened to $134 billion dollars. The Illinois pension system is totally bust:(Dabroski/Klingner/Wirepoints.com)

d)Graham Summers gives a short but powerful message to us all; the everything bubble has burst. Banks are pulling deals because nobody out there can buy the junk. The leveraged loan market has officially gone bust and over the weekend we learned that a major part of the bond market was frozen out..it could not be price!!

e)And now the high yield bond market has frozen; no bids.

( zerohedge)

f)We have highlighted each of the following credit problems to you in the past two months…Mish has put it together nicely.

( zerohedge)

iv)SWAMP STORIES

a)Judge Emmett Sullivan will not be happy with this. The FBI disobeys the Judge and hands over a 302 summary of the Flynn interview 6 months after the original 302 was written up

stay tuned on this one…

(courtesy zerohedge)

c)It looks like there is going to be a government shutdown as Trump is digging in; he wants his wall!

d)This is interesting (and never told to the public at large), the FBI and the CIA told the Washington Post’s Miller that they doubted key allegations in the Steele dossier( zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of DECEMBER and here in this front month of December we now have 281 contracts standing for a LOSS of 22 contracts. We had 26 contracts stand for delivery yesterday so we gained 4 contracts or an additional 20,000 oz will not stand for delivery as these guys morphed into London based forwards as well as accepting a fiat bonus.

After December we have the non active January contract month and here we saw a LOSS of 50 contracts up to 1831 contracts. February saw its another 5 contract gain to stand at 112. March, the next big delivery month after December saw a LOSS of 1872 contracts down to 142,531

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

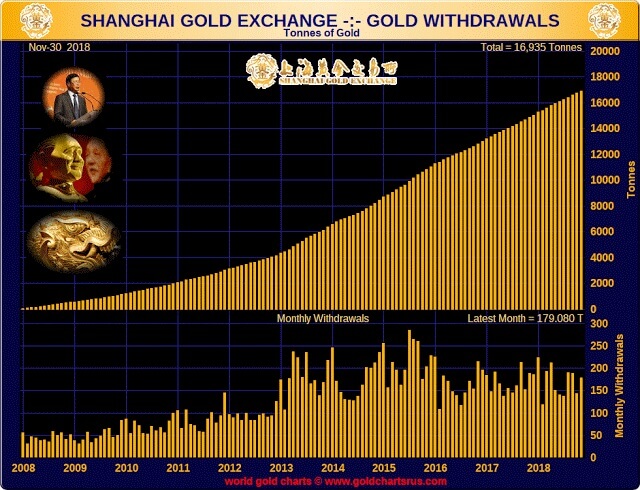

Gold Flowing From West To East and Now To Goldman Sachs

Gold is not only flowing from West to East.

It is also flowing into the house account at Goldman Sachs. Or at least the paper claims for it in New York.

Below is the monthly report showing the large amounts of physical gold which have been steadily flowing through the Shanghai markets into strong hands in China.

Few commentators are talking about this.

What is less familiar, and what I have not read about much, is the very large amount of gold that Goldman Sachs has been taking delivery on the Comex this month.

Attached are a few of the clearing reports below.

Notice that the big takers are the house account at Goldman, and some presumably large customer at JPM.

What’s up with that?

Secure Storage Ireland – Click here for information

Secure Storage Ireland – Click here for information

News and Commentary

Gold prices edge down as firm dollar weighs (Reuters.com)

Stocks Struggle as Dollar Slips to Start Fed Week: Markets Wrap (Bloomberg.com)

Malaysia Files 1MDB-Linked Criminal Charges Against Goldman Sachs (Bloomberg.com)

China Sees Bankruptcies Surge; Bondholders May Get Less Back (Bloomberg.com)

Here come the class-action lawsuits against JPM for rigging gold and silver futures (CNBC.com)

Europe’s Retail Apocalypse Spreads to Online From Shopping Malls (Bloomberg.com)

Source: Bloomberg

Now May Be a Good Time for Silver as Undervauled Versus Gold (Bloomberg.com)

Commodities have strong fundamentals and demand growth in 2019 (Bloomberg.com)

Here’s what 2019 may have in store for commodities such as gold and natural gas (MarketWatch.com)

This Gold Chart Analysis Shows We’re Closer To A SIGNIFICANT Monetary Event (HubertmoolMan)

Ten years on, Fed’s long, strange, trip to zero redefined central banking (Reuters.com)

BIS fears financial seizure at the heart of the world’s clearing system (Telegraph.co.uk)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

14 Dec: USD 1,239.15, GBP 983.39 & EUR 1,096.90 per ounce

13 Dec: USD 1,244.45, GBP 982.87 & EUR 1,093.62 per ounce

12 Dec: USD 1,244.75, GBP 993.31 & EUR 1,098.24 per ounce

11 Dec: USD 1,248.25, GBP 988.99 & EUR 1,096.59 per ounce

10 Dec: USD 1,246.80, GBP 980.61 & EUR 1,092.57 per ounce

07 Dec: USD 1,241.20, GBP 972.98 & EUR 1,091.51 per ounce

Silver Prices (LBMA)

14 Dec: USD 14.58, GBP 11.61 & EUR 12.92 per ounce

13 Dec: USD 14.68, GBP 11.60 & EUR 12.90 per ounce

12 Dec: USD 14.66, GBP 11.68 & EUR 12.93 per ounce

11 Dec: USD 14.64, GBP 11.62 & EUR 12.85 per ounce

10 Dec: USD 14.53, GBP 11.48 & EUR 12.73 per ounce

07 Dec: USD 14.49, GBP 11.34 & EUR 12.73 per ounce

Recent Market Updates

– Brexit Risk Sees Gold Rise To Test EUR 1,100 Per Ounce

– Yellen Warns Another Financial Crisis Is Brewing

– Gold Krugerrand Coin Worth $1,200 Donated To Charity Again

– EU Recession Imminent – Euro Disunion as Brexit, Italy and End of QE Loom

– Gold and Silver Gained 2% and 3% Last Week While Stocks Dropped Nearly 5%

– Irish Central Bank Refuses To Discuss Gold Reserves In Bank of England Vaults

– “Fake Markets” To Lead to Global Financial Crisis? – Goldnomics Podcast

– Gold Is “Coiled” and Looks Set To Surge Like Natural Gas — Bloomberg Intelligence

– “Collapse Of Civilisation Is On The Horizon” – Attenborough Warns World Leaders

BMG Group’s Brandon White: Governments less able to hide intervention against gold

Submitted by cpowell on Sat, 2018-12-15 01:12. Section: Daily Dispatches

8:15p ET Friday, December 14, 2018

Dear Friend of GATA and Gold:

With his Friday night “This Week in Three Minutes” commentary, Brandon White of gold dealer BMG Group in Ontario says the new year will be a defensive one for investors and that surreptitious intervention by governments against gold is being increasingly exposed as agencies refuse to answer questions about it.

White’s commentary is headlined “Sentiment Off” and it can be viewed here:

https://wr211.infusionsoft.com/app/linkClick/67230/efd7456dd2c489a6/1844…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

As expected, here comes the class action lawsuits against JPMorgan for rigging gold and silver. I believe it is a touch to early. What JPMorgan’s chief trader admitted to was only 1% of the fraud

(courtesy Giel/CNBC/GATA)

Here come the class-action lawsuits against JPM for rigging gold and silver futures

Submitted by cpowell on Sat, 2018-12-15 12:43. Section: Daily Dispatches

JPMorgan Faces Potential Class-Action Lawsuit After Guilty Plea by a Former Metals Trader

By Dawn Giel

CNBC, New York

Thursday, December 13, 2018

Traders from across the U.S. are banding together to accuse JPMorganChase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation’s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut unveiled a plea agreement with a former JPMorganChase metals trader

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm’s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to JPMorgan’s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class-action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case. …

… Dispatch continues below …

https://www.cnbc.com/2018/12/13/jp-morgan-faces-lawsuits-after-guilty-pl…

end

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

- At least six lawsuits, all making similar allegations against the nation’s biggest bank, have been filed in the last month in New York federal court.

- The cases could potentially include thousands of people who trade in the precious metals market.

- A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015.

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation’s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut unveiled a plea agreement with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm’s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan’s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co-conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds’ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department’s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak’s suit, sought to re-interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

end

A good history lesson of an early attempt at standardizing money using international gold coins failed.

(courtesy JP Konig/Bullionstar/GATA)

J.P. Koning: An early attempt at standardizing money using international gold coins

Submitted by cpowell on Sun, 2018-12-16 16:39. Section: Daily Dispatches

11:43a ET Sunday, December 16, 2018

Dear Friend of GATA and Gold:

Writing at Bullion Star today, economist J.P. Koning recounts attempts from the mid-1800s to standardize the gold coins of the major Western nations to facilitate international trade. The mechanics weren’t too difficult but the politics proved to be.

Of course computers and the internet today make gold’s divisibility and exchange in international commerce easier than ever, but the politics is a greater problem, since no government really wants to diminish its power by increasing gold’s use in the world monetary system and thereby liberating people from fiat money.

Koning’s essay is headlined “An Early Attempt at Standardizing Money Using International Gold Coins” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/jp-koning/an-early-attempt-at-standard…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Your most important commentary of the day. For over 18 years I have been pounding the table on the dangers of derivatives and it seems that this danger is coming to fruition. Last month a small sector had trouble clearing a trade of just over 100 million dollars. The leveraged bond market has basically busted as there were no takers for a trade and the banks were obliged to put this junk on their books. The big problem is what he highlighted to you on Friday, the huge BBB- bonds trading (3/4 of a trillion dollars) and if they are downgraded one step to junk, the game is over….

a must must read..

(courtesy Ambrose Evans Pritchard)

Ambrose Evans-Pritchard: BIS warns of seizure at heart of financial clearing system

Submitted by cpowell on Mon, 2018-12-17 00:30. Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Sunday, December 16, 2018

https://www.telegraph.co.uk/business/2018/12/16/bis-fears-financial-seiz…

The pillars of the global financial system are fundamentally unstable and could lead to a frightening chain-reaction in the next crisis, the world’s top watchdog has warned.

Giant “central counterparties” (CCPs) that clear much of the $540 trillion (L428 trillion) nexus of derivatives are themselves vulnerable to failure in times of extreme stress.

This is a worry looming ever larger as rising US interest rates expose the weak links in global debt markets.

The Bank for International Settlements said in its quarterly report that the CCPs could cause “a destabilising feedback loop, amplifying stress.”

The implicit message is that well-meaning regulators may have made the financial architecture more dangerous by mistake.

The near meltdown of the Scandinavian counterparty Nasdaq Clearing AB in September came as a rude shock to the global authorities, and a foretaste of what might happen on a much bigger scale should anything serious go wrong.

In that case a E114 million default by Norwegian trader Einar Aas — caught on the wrong side of a “convergence play” on electricity prices — burned through his collateral and then through two thirds of a reserve fund from non-defaulting members. The crisis was contained but it exposed the fragility of the system.

The notional value of the derivatives cleared worldwide is 4.4 times world GDP, up from 2.8 times in 2008. JP Morgan alone has a $30 trillion book.

The BIS warned that regulators have inadvertently created a “CCP-bank nexus” — somewhat akin to the sovereign/bank doom loop in the eurozone — in which the two feed on such other.

The rotten apple contaminates the healthy banks. A fire sale of assets spreads contagion. Banks may be forced to hoard liquidity to protect themselves. The BIS said “balance sheet interlinkages” and what it calls the “CCP default waterfall” could unravel with “potentially system-wide effects.”

It is just one of many late-cycle pathologies highlighted by the Swiss-based watchdog, the bank of the central banking fraternity and the high priest of orthodoxy.

Another brutal week on Wall Street has brought these risks into sharper focus. The three key equity indexes in the United States are all in a full correction after falling over 10 percent from their peak.

Germany’s DAX index has dropped 19 percent since January, and the Shanghai Composite is down 27 percent. “The market tensions we saw during this quarter were not an isolated event,” said Claudio Borio, BIS chief economist.

Central banks are walking a tightrope as they try to extract themselves from a decade of emergency stimulus. Quantitative easing and ultra-low rates have lifted debt ratios to levels that are 40 basis points higher than the pre-Lehman peak, this time led by emerging markets. Nobody knows where the pain threshold lies for monetary tightening in such circumstances.

The BIS says the nature of the world’s business cycle has entirely changed over the last three decades. For most of the 20th century booms turned to bust when rising inflation forced authorities to jam on the brakes.

This is no longer the case. Globalization and the inclusion of China and emerging Asia in the trading system have suppressed inflation. What now brings the party to an end is excess credit and rising debt service ratios. As conditions tighten, the financial system eventually buckles under its own weight.

The thrust of BIS research is that we may be close to this inflexion point. Standard & Poor’s says the number of junk bonds rated B minus or below has jumped from 17 to 25 percent over the last year. This is now the highest since global financial crisis.

The average yield on U.S. junk bonds has risen 165 basis points to 7.2 percent over the last year. A cascade of downgrades has begun. The spike has been even more dramatic in the eurozone where stress is nearing danger levels, leaving credit analysts baffled by the European Central Bank’s decision to halt quantitative easing this month.

The BIS fears a waterfall effect. “The bulge of BBB corporate debt, just above junk status, hovers like a dark cloud over investors. Should this debt be downgraded, if and when the economy weakened, it is bound to put substantial pressure on a market that is already quite illiquid,” said Mr. Borio.

The volumes are sobering. The ratio of U.S. corporate debt to gross domestic product is 73.5 percent of GDP, higher than in 2008, although this is a children’s playground compared to China. The share of leveraged loans in the U.S. with risky “covenant-lite” contracts has reached 80 percent this year.

The $1.3 trillion market for leveraged loans has become an increasing worry. Prices of this debt on the secondary market are breaking down. To clear the transaction in early December, JPMorgan slashed the price for an XOJET takeover loan to 93 cents on the dollar.

The Achilles’ heel for the global economy is the surging U.S. dollar. The BIS says offshore lending in dollars by European, Japanese, and increasingly Chinese and emerging market banks has risen to $12.8 trillion. The figure is probably far higher if opaque “off-balance-sheet” liabilities are included.

This web of dollar liabilities is coming under intense strain as the U.S. Federal Reserve drains liquidity, pushing up global lending rates. A worldwide dollar shortage is emerging. This is acting as tourniquet, tightening an international system built on dollar funding.

An estimated $9 trillion of global contracts are priced off 3-month LIBOR rates, which have doubled to 2.77 percent over the last year. The “LIBOR-OIS spread” has also jumped to 40 basis points and is flashing early-warning signs of stress in the overnight funding markets for dollars in Europe and Asia. The 30 percent crash in European banks stocks this year is hinting at a incipient credit crunch.

The BIS warned that some of these offshore dollar lenders may face a “funding squeeze” of their own, forcing them to withdraw credit in a chain-reaction. “Cross-border funding, regardless of the source, may be fickle in a crisis,” it said.

The possibility that a major central counterparty might “fall over” in the next crisis is sobering. The G20 mandated a shift in global finance towards CCPs after the 2008 crisis, deeming them the “unlikely heroes” of the Lehman shock. The counterparties managed to auction, liquidate, or transfer almost all of Lehman’s derivative portfolios in an orderly fashion, including $9 trillion of interest rate swaps made up of 66,390 trades.

But the G20 may have over-interpreted the Lehman lesson. There have been plenty of CCP failures in the past. France’s Caisse de Liquidation des Affaires came awry in 1974 when the sugar market blew up. The Hong Kong Futures Guarantee Corp. failed in 1987. The Chicago Mercantile Exchange had a close shave the same year after the October crash.

There was a whiff of trouble immediately after the Brexit referendum when margin calls hit $27 billion. It is a foretaste of what could happen to Europe’s financial system if the European Union persists in its refusal to reciprocate the UK pledge to recognize the legal continuity of E45 trillion of derivative contracts after March 2019.

Nobody knows what would happen if Britain’s LCH or Germany’s Eurex Clearing came under stress. They have thin layers of capital compared to banks.

Before the 2008 crisis most derivatives were cleared by trading parties in direct dealings. The G20 shift has lifted the share of CCPs for interest rate derivatives from 20 to 60 percent. The effect is to concentrate risk. The BIS warns that the system may encourage a rush for the exit in events of extreme stress.

The International Monetary Fund has also flagged the dangers. It warned this year that CCPs “increase the risk of a failure of the infrastructure itself” and could lead to a “catastrophe” if the all layers of defense were overrun by a big default. It would be like the failure of the Maginot Line.

The G20 may have made the world financial system more hazardous.

…

END

They are perfectly correct: there is a lack of liquidity, stock markets collapse.

another must read..

(courtesy Jain/Times of India/GATA)

Ritesh Jain: It’s the liquidity, Stupid! That’s what is causing all the turmoil

Submitted by cpowell on Mon, 2018-12-17 00:42. Section: Daily Dispatches

By Ritesh Jain

The Times of India, Mumbai

Sunday, December 16, 2018

https://economictimes.indiatimes.com/markets/stocks/news/its-the-liquidi…

Nedbank strategists Mehul and Neels write some exciting stuff and, like me, they don’t confuse fundamentals with liquidity. They write in a strategy note:

There is a strong relationship between the change in global dollar liquidity (M1) and the performance of the global stock market — a correlation of 76 percent.

Global dollar liquidity leads global stock markets by an average of eight months.

— If there is no boost to global dollar liquidity, we expect this relationship to hold. As a result, the risk of further downside potential for stock markets across the world would remain intact.

— We believe this is the “canary in a coal mine” for risk assets.

— U.S. dollar-denominated debt of emerging market corporates has grown from $650 billion in 2009 to the current $3.2 trillion and there are significant mismatches — U.S. dollar-denominated debt as a percentage of gross domestic product is 70 percent and that of percentage of reserves is 75 percent.

— Amid a slowdown in global growth, coupled with a tighter global dollar-Liquidity environment, if emerging-market corporate spreads continue to widen, it would negate our view below on emerging-market equities — that is, that a short-term bounce is possible.

… My two cents

So, it comes down to liquidity — and the global money supply is not expanding. In fact it is contracting. The Fed is already in quantitative tightening mode. (Forget rate increases, which are only the cost of providing liquidity.) In a widely expected decision, the European Central Bank has also decided to stop its quantitative easing.

So how will existing debt be serviced and how will the new debt be created if the private sector and consumer are already leveraged?

* * *

END

Von Greyerz at Kingworld news highlights correctly the collapse of the European bank stock index and he warns that there will be an imminent crash of the European banking system and then a stock market crash.

(Kingworld news/ Von Greyerz/GATA)

Von Greyerz, at KWN, notes collapse of European bank stocks

Submitted by cpowell on Mon, 2018-12-17 01:29. Section: Daily Dispatches

8:31p ET Sunday, December 16, 2018

Dear Friend of GATA and Gold:

Swiss gold fund manager Egon von Greyerz, in commentary posted at King World News, calls attention to both the long-term and short-term collapse of the European bank stock index, which he construes as an indicator of the imminent crash of the European banking system and then a stock market crash.

Von Greyerz’s commentary is headlined “We Have Just Seen a Huge Warning that a Global Collapse Is about to Unfold” and it’s posted at KWN here:

https://kingworldnews.com/greyerz-we-have-just-seen-a-huge-warning-that-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

|

4:15 AM (3 hours ago) |

|

||

|

||||

_

|

10:07 AM (25 minutes ago) |

|

||

|

||||

________________

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8971/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8966 /shanghai bourse CLOSED UP 4.23 POINTS OR 0.16%

HANG SANG CLOSED DOWN 6.81 POINTS OR 0.03%

2. Nikkei closed UP 132.85 POINTS OR 0.62%

3. Europe stocks OPENED ALL RED

/USA dollar index FALLS TO 97.24/Euro RISES TO 1.1343

3b Japan 10 year bond yield: FALLS TO. +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.62/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.76 and Brent: 61.08

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.25%/Italian 10 yr bond yield UP to 2.95% /SPAIN 10 YR BOND YIELD UP TO 1.40%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.70: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.32

3k Gold at $1239.75 silver at:14.62 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 31/100 in roubles/dollar) 66.33

3m oil into the 51 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.28 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9935 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1270 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.25%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.88% early this morning. Thirty year rate at 3.14%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3765

Global Stock Rally Fizzles As Europe Slammed By “Retail Apocalypse”

Another attempt to rally S&P futures overnight has fizzled, this time as a result of weakness in Europe and a mixed session in Asia, following a sharp decline in European retailers due to a record plunge in UK online retailer Asos Plc which collapsed after warning that Christmas shopping got off to a disastrous start, dragging its shares to a 2 year low and hitting the sector.

In an otherwise quiet session as traders prepare for this week’s critical Fed meeting, shares in European retailer Asos plunged by over 40% after the company cut expectations for the current financial year. The last time its shares traded this low was back in 2015/16. The company said it was experiencing a “significant deterioration” in the trading month of November and that conditions remain challenging. Guidance is slashed to 15% from earlier expectation of 20-25%. As Inezfrans notes, “the move lower is absolutely astonishing.”

Asos cut its full-year sales-growth guidance on a “significant deterioration” in November, blaming a high level of discounting amid economic uncertainty and low consumer confidence, which has been undermined in the U.K. by the continuing Brexit saga.

The rest of the Europe’s big retailers including Marks & Spencer, JD Sports, Next and Boohoo all fell in London, while German giant Zalando has also joining the implosion of the retailers, falling by 15% on Xetra.

Commenting on Europe’s “retail apocalypse“, Bloomberg notes that the gloomy update from the online retailer – which competes with Amazon.com and has furnished fashions to the likes of Meghan Markle – shows that retail weakness is widespread in the runup to the holidays. Last week, Sports Direct International Plc Chief Executive Officer Mike Ashley said sales were “unbelievably bad” in November, sending the shares off a cliff.

“This goes against the script,” said Stephen Lienert, a credit analyst at Jefferies. “It was supposed to be bricks and mortar that’s dying and online is the future, but that headline gets ripped up today.”

The Asos news shows that retailers can’t rely on online operations to make up for a decline in stores this year. If December doesn’t improve, the New Year may bring more profit warnings, or worse, to the sector. Meanwhile, other retailers such as Debenhams Plc and Marks & Spencer, which are in the midst of turnaround plans, may be particularly vulnerable. The U.K.’s shopping districts have already been decimated by a series of collapses, including the insolvency of department-store chain House of Fraser, which Ashley rescued earlier this year.

Investors in retail debt are also feeling the pain. Debenhams’ 200 million pounds of bonds due July 2021 have plummeted 35 pence on the pound since the start of the year to 64 pence, the lowest since the notes were sold in 2014, according to data compiled by Bloomberg.

Europe’s Stoxx 600 Index dropped to session lows, down 0.5% following the Asos plunge and retail sector weakness. In contrast, mining shares are up 1% after China managed to close modestly higher after the PBOC injected a net CNY150BN in reverse repo liquidity after 36 days of silence. Among Europe’s other biggest decliners are Novartis -1%, Adidas -3.4% and H&M -7.2%.

Earlier in the session, Asian markets began the week cautiously following the downbeat lead from Wall Street in which the three major indexes closed lower by around 2% each with the Dow plunging almost 500 points to its lowest level since early May, led

lower by shares in Apple and Johnson & Johnson, while the S&P and Nasdaq were dragged down by tech names as the sector

lagged. Australia’s ASX 200 (+1.0%) was buoyed by material and mining names after MOFCOM confirmed the suspension of retaliatory tariffs on US vehicles and auto parts, while Nikkei 225 (+0.7%) initially outperformed on currency effect as the export-heavy index benefitted from the weaker JPY. Elsewhere, Hang Seng (Unch) and Shanghai Comp. (+0.1%) traded choppy and swung between gains and losses in which the indices initially dipped in the red as industrial names were again pressured in a continuation from the weak IP data last week, housing names then provided the bourses with some support amid an improvement in house prices data.

Futures on the Dow, S&P and Nasdaq fluctuated before dipping in the red, dragged lower by Europe’s weakness.

Treasuries posted modest gains to start the week, with the 10Y yield dipping 1 basis point to 2.8786% and have seen some bull steepening with 2s/10s and 10-year futures uneventful ahead of an action-packed central bank week, that kicks off with the Chinese Central Economic Work Conference from Tuesday ahead of the FOMC on Wednesday, with BoJ, BoE and more thereafter, alongside US housing data tomorrow.

In foreign exchange markets, most currencies were little changed. The dollar fell after a strong week that took it to the highest in a month, following bizarre strength in the euro which hit fresh session high even as data show annual euro-area inflation slipped to 1.9% in November, the lowest since May, from 2.2% the previous month; the yen was steady after a bout of risk aversion hammered global equities in recent sessions. Emerging-market shares and currencies edged higher thanks to the drop in the dollar: Mexico’s peso rallied after President Andres Manuel Lopez Obrador promised a surplus in next year’s budget.

“The market appears to be underpricing the Fed, and any indication of additional gradual increases is likely to bring potential dollar upside versus rate-sensitive currencies,” Barclays strategists wrote in a note.

Core EU bonds have recovered some ground after touching session lows (163.04 and 123.37) with Bunds deriving some support from another retreat in BTPs (trading near lows at 125.20), that has pushed German benchmark futures back above par to print new highs at 163.29. Italian bond yields edged higher even as Prime Minister Giuseppe Conte forged a deal with populist leaders to submit a revised budget proposal to the European Commission in a bid to avert fines: The new plan confirms the 2019 deficit target will be lowered to 2.04 percent of GDP from 2.4 percent as Conte flagged to Brussels last week. Meanwhile Gilts have been further depressed by the accounting changes at the ONS which “effectively wipes out the Brexit buffer” after the Brexit-driven downturn, that has pushed the benchmark to trade in close proximity to lows of the day.

Elsewhere, Malaysia turned up the heat on Goldman Sachs Group Inc., filing criminal charges against the U.S. bank.

Markets are expected to be relatively quiet until this week’s FOMC announcement, when the Fed is expected to raise interest rates for a fourth time this year, but it will be Chairman Powell’s remarks that will be closely studied for hints on their future path and whether the dot plot is trimmed to forecast 2 rate hikes in 2019 instead of 3; a failure to turn more dovish would lead to another rout in risk assets as global growth forecasts for next year are being trimmed at an accelerating pace.

“A final key rate hike for 2018 is almost a done deal, but what is more important is how the Fed’s dot plots shift in 2019 and beyond. If U.S. monetary policymakers are seeing a serious risk of economic slowdown, those dots should be pulled downwards,”said FXTM strategist Hussein Sayed.

In this week’s other key events, investors will be looking to a speech by China’s President Xi Jinping on Tuesday marking the 40th anniversary of China’s reforms and opening up. China – where the economy has been rapidly losing momentum – is also expected to hold its annual Central Economic Work Conference later this week, where key growth targets and policy goals for 2019 will be discussed. The top decision-making body of the Communist Party, the Politburo, said last week China will keep its economic growth within a reasonable range next year, striving to support jobs, trade and investment while pushing reforms and curbing risks.

“It’s generally assumed that you will need to expand fiscal and monetary support to achieve those goals,” said Tokai Tokyo Research strategist Wang Shenshen.

The optimism before Xi’s speech helped base metals rise, although weak economic indicators capped gains.

Meanwhile political uncertainty still grips investors. There are yet more personnel changes within the Trump administration and confusion remains over Britain’s future relationship with the European Union.

“There’s been a reevaluation of growth and inflation prospects over 2019 with the trade war now looking extremely negative,” Steve Goldman, fund manager at Kapstream Capital, told Bloomberg TV in Sydney. “We’re going to see a lot of volatility.”

As reported over the weekend, Trump’s Interior Secretary Ryan Zinke will leave at the end of the year amid a swirl of federal investigations.

Elsewhere, in the neverending Brexit drama, investors will monitor Theresa May’s comments after her team pushed back against reports they are warming to a second referendum on Brexit. The U.K. prime minister will face Parliament on Monday.

In commodities, Brent (+1.0%) and WTI (+1.0%) have shown a modest upside in prices which is more a by-product of currency effects as the dollar drifts lower. This morning there have been reports that Russia’s oil output has been at a record high of 11.42mln BPD in December, with prices unreactive to this news. Additionally, the UAE Energy Minister has said that he expects everyone to cut oil supply following the OPEC agreement, and separately reports state that China’s Shenghong has begun building a 330k BPD refinery in Jiangsu. Gold has traded within a tight USD 4/oz range, but has recently begun to firm slightly as the DXY has remained largely unchanged ahead of this week’s FOMC meeting. Elsewhere, steel and iron ore prices have begun to rise due to winter production cuts, as Chinese authorities are trying to reduce air pollution levels.

Expected data include Empire State Manufacturing Survey. Heico, Oracle, and Red Hat are reporting earnings.

Market Snapshot

- S&P 500 futures up 0.2% to 2,610.50

- STOXX Europe 600 down 0.4% to 345.76

- MXAP up 0.3% to 149.57

- MXAPJ up 0.3% to 482.53

- Nikkei up 0.6% to 21,506.88

- Topix up 0.1% to 1,594.20

- Hang Seng Index down 0.03% to 26,087.98

- Shanghai Composite up 0.2% to 2,597.97

- Sensex up 0.9% to 36,290.73

- Australia S&P/ASX 200 up 1% to 5,658.27

- Kospi up 0.08% to 2,071.09

- German 10Y yield rose 0.3 bps to 0.255%

- Euro up 0.2% to $1.1327

- Italian 10Y yield fell 1.7 bps to 2.577%

- Spanish 10Y yield rose 0.7 bps to 1.419%

- Brent futures up 0.7% to $60.70/bbl

- Gold spot little changed at $1,239.59

- U.S. Dollar Index down 0.2% to 97.23

Top Overnight News from Bloomberg

- The dollar’s gains over the past three months have spurred hedge funds to cut bullish bets to the lowest since June. Leveraged funds trimmed positions wagering on gains in the greenback by the most since September, according to the latest data from the U.S. CFTC based on eight currency pairs

- Donald Trump won’t be sitting down with Special Counsel Robert Mueller to answer more questions in his investigation into election interference, Rudy Giuliani, the president’s attorney, vowed on Sunday

- U.K. Prime Minister Theresa May will attack supporters of a second Brexit referendum on Monday as she explains to Parliament why European Union leaders rebuffed her attempt to make her divorce deal more attractive to lawmakers

- Australia is on track to return to the black for the first time since the global financial crisis, almost doubling the size of its projected surplus in fiscal 2020, according to projections from the Treasury

- The Italian government will trim its deficit target for next year in its latest proposal that seeks to avoid EU sanctions for violating the bloc’s budget rules, the Ansa news agency reported

- The toll Brexit is taking on the U.K. housing market was laid bare in surveys published Monday

Asian equity markets began the week somewhat cautiously following the downbeat lead from Wall St. in which the three major bourses closed lower by around 2% each. The Dow plunged almost 500 points to its lowest level since early May, led lower by shares in Apple and Johnson & Johnson, while the S&P and Nasdaq were dragged down by tech names as the sector lagged. ASX 200 (+1.0%) was buoyed by material and mining names after MOFCOM confirmed the suspension of retaliatory tariffs on US vehicles and auto parts, while Nikkei 225 (+0.7%) initially outperformed on currency effect as the export-heavy index benefitted from the weaker JPY. Elsewhere, Hang Seng (Unch) and Shanghai Comp. (+0.1%) traded choppy and swung between gains and losses in which the indices initially dipped in the red as industrial names were again pressured in a continuation from the weak IP data last week, housing names then provided the bourses with some support amid an improvement in house prices data. Finally, 10yr JGB yields touched over 5-month lows as fears of slower global growth boosted demand for the debt.

Top Asian News

- China Built a Global Economy in 40 Years, Now It Has a New Plan

- JDI Posts Record 2-Day Rally as Company Hints Demand May Improve

- Takeda Downgraded by Moody’s on Lofty Debt After Shire Deal

- 1MDB USD Bonds See Biggest Drop In 2 Weeks After Malaysia Charge

- China Bond Issuers Shorten Process to Clinch Year-End Deals

Major European indices are in the red [Euro Stoxx 50 -0.3%], with losses generally broad-based although there is some underperformance in the SMI (-0.6%) with heavyweight UBS (-0.4%) in the red having lost ground against rivals after USD 3.1bln was removed from their ETF business in November; alongside Swatch (-3.0%) and Richemont (-0.9%) who were both downgraded at Morgan Stanley. Similarly, sectors are in the red with some underperformance seen in Consumer Discretionary alongside the European Retail Sector, the latter dropping to its lowest level since July 2016. This follows Asos (-40.0%) plummeting after cutting their full year outlook, which has pulled other retail names down in sympathy. In addition, ABB (+0.8%) are up after the Co has reached a deal with Hitachi regarding their power grids division valued at USD 11bln. SSE (-2.0%) are lower as they have been unable to come to an agreement with Innogy (-1.0%) on revised commercial terms.

Top European News

- SSE Pulls the Plug on U.K. Energy Retail Merger With Innogy

- Euro- Area Inflation Revised Down After ECB Pledged to Halt QE

- Italy Govt Has Resources to Cover 2.04% Deficit in 2019: Ansa

- DWS Head Asoka Woehrmann Reshuffles Regional Leadership Roles

- Toxic Politics and Fading Stimulus: East Europe’s 2019 Risks

In FX, the DXY has traded in a 97.199-463 range for the index almost says it all in terms of the lacklustre start in currency markets to the final full week of the year. However, the Dollar is treading cautiously into the FOMC amidst an approximate 75% probability for a 4th 25 bp hike, with the focus firmly on updated policy guidance and fresh dot plots to see whether the consensus has shifted towards a pause in tightening or a shallower rate profile from 2019 out.

- NZD/AUD – The Kiwi is just about keeping its head above 0.6800 vs its US counterpart and in front of the G10 pack, but largely by default and relative weakness in the Aud after the Australian Treasury downgraded its 2018/9 growth forecast to 2.75% from 3% overnight. Indeed, Aud/Usd remains capped ahead of 0.7200 where a decent 1.1 bn option expiry resides, while the Aud/Nzd cross is back under 1.0550.

- EUR – The single currency has reclaimed 1.1300+ status vs the Greenback, but may also be hampered by expiry interest between 1.1320-35 as 1.1 bn runs off at the NY cut, or technical resistance at the 30 DMA circa 1.1353 if the headline pair manages to clear option-related offers/hedges convincingly. No discernible reaction to final Eurozone inflation data even though the EU-harmonised measure was unexpectedly trimmed to 1.9% y/y from 2%

- JPY/CAD – Both relatively flat vs the US Dollar and rangebound (113.25-50 and 1.3375-90 respectively), with the former awaiting the last BoJ meeting of the year ahead of the Fed and the latter only deriving modest momentum from firmer crude prices.

- EM – The Mxn is benefiting from the broad Usd downturn and some bullish Peso sentiment following the Mexican budget projections to retest resistance ahead of 20.0000, but the Try is bucking the general trend in wake of considerably weaker than expected Turkish ip data, as the Lira struggles to hold above 5.4000.

In commodities, Brent (+1.0%) and WTI (+1.0%) have shown a modest upside in prices with this more a by-product of currency effects as the dollar drifts lower. This morning there have been reports that Russia’s oil output has been at a record high of 11.42mln BPD in December, with prices unreactive to this news. Additionally, the UAE Energy Minister has said that he expects everyone to cut oil supply following the OPEC agreement, and separately reports state that China’s Shenghong has begun building a 330k BPD refinery in Jiangsu. Gold has traded within a tight USD 4/oz range, but has recently begun to firm slightly as the DXY has remained largely unchanged ahead of this week’s FOMC meeting. Elsewhere, steel and iron ore prices have begun to rise due to winter production cuts, as Chinese authorities are trying to reduce air pollution levels. Separately, Vedanta may restart its 400ktpa Indian copper smelter following it’s forced closure by the government due to pollution. UAE Energy Minister says he expects “everyone” to cut oil supply as per the OPEC agreement. Kuwait Oil Ministers resignation is said to have been accepted, according to sources.

US Event Calendar

- 8:30am: Empire Manufacturing, est. 20, prior 23.3

- 10am: NAHB Housing Market Index, est. 60.5, prior 60

- 4pm: Total Net TIC Flows, prior $29.1b deficit

- 4pm: Net Long-term TIC Flows, prior $30.8b

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 4.23 POINTS OR 0.06% //Hang Sang CLOSED DOWN 6.81 POINTS OR 0.03% //The Nikkei closed UP 132.85 OR 0.62%/ Australia’s all ordinaires CLOSED UP 0.95% /Chinese yuan (ONSHORE) closed UP at 6.8971 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.76 dollars per barrel for WTI and 61.08 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED UP AT 6.8966AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8971: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

We reported to you last week, the ugly numbers that China reported on retail sales and industrial production..probably their most important figures. Jeffrey Snider reports on those figures and what it means….Is the lack of USA dollars in China going to create a crisis…he believes so

a must read..

(courtesy Jeffrey Snider)

“What We Are Left With Is Pure Ugly” – Will The Communists Panic Next Week?

Authored by Jeffrey Snider via Alhambra Investment Partners,

The Relevant Word Is ‘Decline’

The English language headline for China’s National Bureau of Statistics’ press release on November 2018’s Big 3 was, National Economy Maintained Stable and Sound Momentum of Development in November. For those who, as noted yesterday, are wishing China’s economy bad news so as to lead to the supposed good news of a coordinated “stimulus” response this was itself a bad news/good news situation.

If the Communist State Council is to be flustered into action, the title of the release might suggest maybe not. Then again, there isn’t a month that goes by where the NBS writers don’t write pretty much the same thing. In a Communist country, any wording less than “sound momentum” is surely frowned upon especially when there is no momentum.

Underneath, the figures were all bad. Were they bad enough? I don’t believe anything short of full-fledged collapse will be, but this is attempting to game and analyze a political factor whose proportions are never going to be fully known.

What we are left with is pure ugly. The last time Industrial Production grew at a 5.4% annual rate, as it did last month, it was February 2016 and the worst of times for modern, industrial China. It was also the same month the last “stimulus” was uncorked.

It doesn’t get any lower than the 2015-16 downturn so for Chinese industry to already be at that depth with “this one” just getting started, it all tells us that perhaps there is a lot of downside left to come and that officials are keenly aware of the possibility.

If this was somehow unexpected and unapproved, so to speak, they wouldn’t have waited for 5.4% to reappear. That goes double for consumer spending, or retail sales in this case. Chinese retail activity grew by just 8.1% in November. You have to go back fifteen years to find something less.

What should really stand out especially for the stimulus whisperers is whenChina’s latest economic inflection transpired. It wasn’t Trump and trade, it was in the middle of last year for both IP as well as RS.

Why mid-2017? That was when authorities began to realize the full extent of their predicament. They had done the “stimulus” stuff in a rush to begin 2016 and it didn’t get anywhere. There are often heavy costs to doing these kinds of things, so to pay out a lot and receive very little in return from it is a big counterpoint to thinking about doing it again.

China simply has, as we’ve been writing and speaking about for half a decade (and more, less specifically about China), no monetary room with which to get any kind of internal growth started. That point was driven home last year. The global economy despite all officials protestations everywhere has never once picked up toward recovery.

Therefore, the Chinese government is left between the rock (external malaise) and the hard place (no internal monetary space). Only a few months after June 2017, Communist officials convened at the 19th Party Congress and “elected” to move authoritarian. This, I don’t believe, is mere coincidence.

The only mild positive so far in 2018 is how Fixed Asset Investment (FAI) has stabilized albeit at extremely low levels. Private FAI, in particular, is growing at around a 9% rate (8.8% in November) which is better than late last year.

The flipside of that is how Private FAI seems to have hit a ceiling around 9%, nowhere near the 25% rate that for a few years kept China out of trouble. Even with officials at lower levels (almost certainly on orders from the central government) in the provinces no longer clamping down on the waste of State-owned FAI, it hasn’t stabilized China’s economy because it can’t.

On an accumulated basis, Public FAI rose 2.3% in November (meaning YTD) while on a monthly basis it was less than 7% (annual rate) for the second straight month. Like Private FAI, better than before but not really meaningfully so. It seems more like messaging than meaning.

To me, this adds up to the same thing – an attempt at managing the decline rather than intentions to turn it around as expectations for globally synchronized growth would have required. I wrote more than three years ago, a little over a week after the big shock of CNY in August 2015:

I think they made a conscious effort to try to avoid Japan’s disaster by actively engaging to manage a bubble decline regardless of how much growth had to be “sacrificed” to do so.