GOLD: $1293.90 UP $5.40 (COMEX TO COMEX CLOSINGS)

Silver: $15.60 UP 0 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1293.45

silver: $15.59

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 3 NOTICE(S) FOR 300 OZ (0.0093 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 538 NOTICES FOR 53800 OZ (1.6734 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

7 NOTICE(S) FILED TODAY FOR 35,000 OZ/

total number of notices filed so far this month: 644 for 3,220,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3614: UP 61

Bitcoin: FINAL EVENING TRADE: $3575 UP $24

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 2/3

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,286.200000000 USD

INTENT DATE: 01/15/2019 DELIVERY DATE: 01/17/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 2

737 C ADVANTAGE 3 1

____________________________________________________________________________________________

TOTAL: 3 3

MONTH TO DATE: 541

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN SMALL SIZED 553 CONTRACTS FROM 191,369 UP TO 191,922 DESPITE YESTERDAY’S 4 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED SLIGHTLY CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1421 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1421 CONTRACTS. WITH THE TRANSFER OF 1421 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1421 EFP CONTRACTS TRANSLATES INTO 7.105 MILLION OZ ACCOMPANYING:

1.THE 4 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.605 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 27,578 CONTRACTS (FOR 11 TRADING DAYS TOTAL 27,158 CONTRACTS) OR 137.890 MILLION OZ: (AVERAGE PER DAY: 2507 CONTRACTS OR 12.535 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 137.89 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.69% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 137.89 MILLION OZ.

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 553 DESPITE THE 4 CENT FALL IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1421 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A CONSIDERABLE SIZED: 1974 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1421 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 553 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.60 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .896 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 7 NOTICE(S) FOR 35,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.605 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A strong SIZED 6,777 CONTRACTS UP TO 501,605 DESPITE THE LOSS IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $1.45//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 11,496 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 11496 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 501,605. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUGELY ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 18,273 CONTRACTS: 11.496 OI CONTRACTS INCREASED AT THE COMEX AND 6777 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 18,273 CONTRACTS OR 1,827,300 OZ = 56.80 TONNES. AND ALL OF THIS HUMONGOUS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF A TINY $1.45??????????

YESTERDAY, WE HAD 6045 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 90,925 CONTRACTS OR 9,092,500 OZ OR 282.81 TONNES (11 TRADING DAYS AND THUS AVERAGING: 8265 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAYS IN TONNES: 282.81 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 282.81/2550 x 100% TONNES = 11.09% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 282.81 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 6777 DESPITE THE FALL IN PRICING ($1.45) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A VERY HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,496 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11496 EFP CONTRACTS ISSUED, WE HAD AN UNBELIEVABLE GAIN OF 18,273 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11496 CONTRACTS MOVE TO LONDON AND 8268 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 56.80 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE TINY FALL OF $1.45 IN YESTERDAY’S TRADING AT THE COMEX??????????. THIS IS THE 3RD STRAIGHT DAY THAT WE RECORDED ATMOSPHERIC RISES IN OI ON BOTH EXCHANGES!

we had: 3 notice(s) filed upon for 300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $5.40 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 797.71 TONNES

Inventory rests tonight: 797.71 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER FLAT IN PRICE TODAY:

A HUGE CHANGE IN SILVER INVENTORY/

A WITHDRAWAL OF 2.158 MILLION OZ/

/INVENTORY RESTS AT 311.005 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 553 CONTRACTS from 191.309 UP TO 1919227 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1421 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1421 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 553 CONTRACTS TO THE 1421 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A CONSIDERABLE GAIN OF 1974 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.445 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.605 MILLION OZ STANDING IN JANUARY..

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 4 CENT PRICING FALL THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A TINY SIZED 1421 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

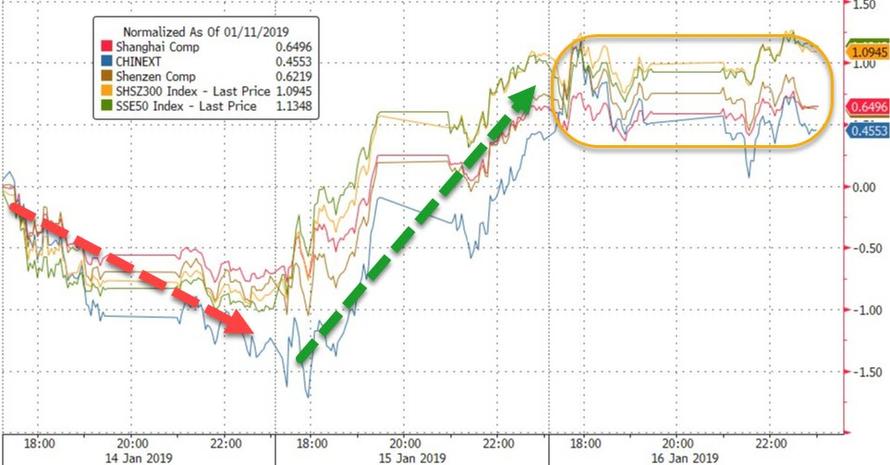

SHANGHAI CLOSED UP 0.08 PTS OR 0.00% //Hang Sang CLOSED UP 71.81 POINTS OR 0.27% /The Nikkei closed DOWN 112.54 PTS OR .96%/ Australia’s all ordinaires CLOSED UP 0.37%

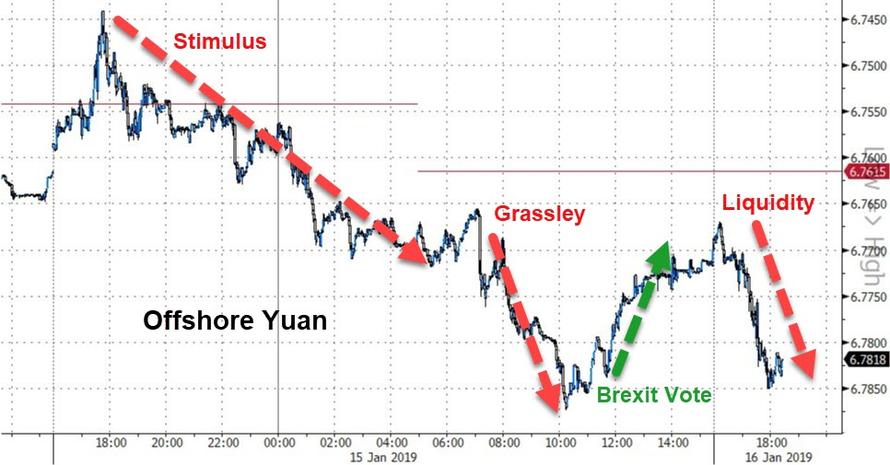

/Chinese yuan (ONSHORE) closed DOWN at 6.7620 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 51.68 dollars per barrel for WTI and 60.31 for Brent. Stocks in Europe OPENED /MIXED

//. ONSHORE YUAN CLOSED DOWN AT 6.7620 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7684: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/CHINA

b) REPORT ON JAPAN

3 C/ CHINA

i)CHINA

China tries to rescue the globe with a massive liquidity injection

(courtesy zerohedge)

ii)CHINA had talks with the USA over the weekend where China is now becoming more belligerent. They do not want USA ships to pass through the Taiwan strait. It will no doubt, come shortly that Beijing demands the unification of Taiwan to the Mainland.

( zerohedge)

4/EUROPEAN AFFAIRS

i)EUROPE/

Meijer describes the European catastrophe perfectly

a must read…

( Raul Meijer)

ii)GREECE

Chinese gangs operating out of the port of Piraeus were engaged in tax fraud as they avoided import duties etc. Greece has been fined over 200 million euros for not catching this sooner. China owns the port of Piraeus

(courtesy zerohedge)

iv)GERMANY/DEUTSCHE BANK/BAFIN

Quite a story…BAFIN is the German regulator and they have been after a merger between Deutsche bank, the no 1 derivative player in the world and Commerzbank bank. Now the regulator states that both are too weak, and they are pushing for Deutsche bank to merger with one of their competitors in another sovereign country..to spread the pain of trillions of derivatives.

(courtesy zerohedge)

v) ECB/Fed/Bank of Japan

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

ISIS/SYRIA/USA

ISIS is not dead yet: An ISIS attack in the northern section of Syria (Manbij) killed two Americans while on patrol in Syria

(courtesy zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

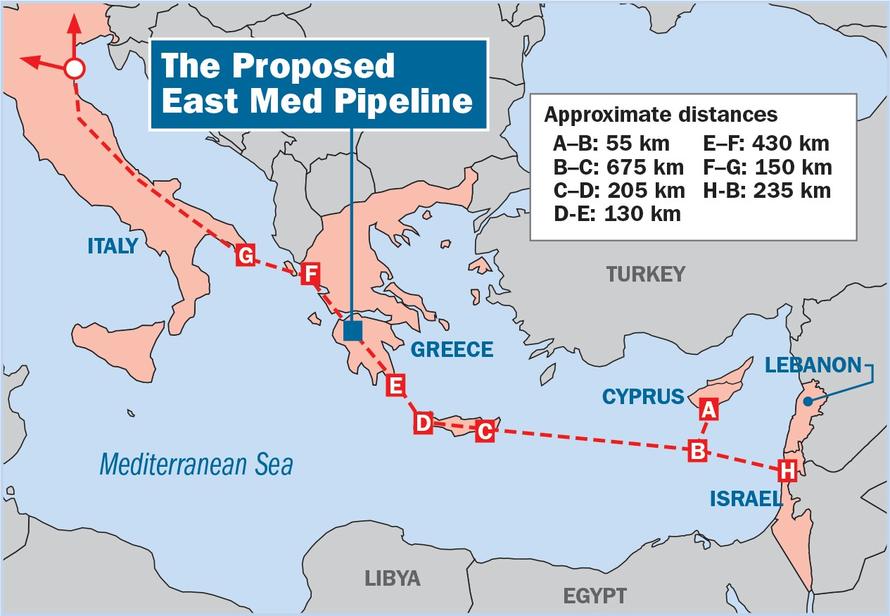

This is a huge story. Israel arrived for the first time into Cairo since 2011. Egypt and Israel have a an agreement where Israel is to export gas to Egypt and to create an “energy export hub”. In this meeting were representatives for Italy, Greece, Cyprus, Jordan and the Palestinian authority. The Palestinian authority could benefit greatly from this alliance as gas has been found on their territory. This hub will augment the huge East Med pipeline built from Israel via Cyprus and onto Greece/Italy and the rest of Europe

a big story.

( zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

Craig Hemke forecasts what he thinks gold/silver will do in 2019

( Craig Hemke)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

All data points seems to suggest that the world’s economy fell flat on its face. Today USA import prices fell with the prime culprit being petroleum

( zerohedge)

a)This is interesting: the student debt crisis widens as the Florida Board of Health suspends licenses over student debt defaults.

( Mac Slavo./SHFTPlan.com)

b)Beige book confirms that the uSA economy is slowing

(courtesy zerohedge)

c)As I pointed out to you yesterday, the hawkest of all hawks states that the fed should pause. It looks like the economy is really faltering

iv)SWAMP STORIES

a)My goodness: the FBI’s top lawyer is now under criminal investigation for being a central leaker to the press. He is James Baker.

( zerohedge)

b)This is a major victory for Judicial watch: a federal judge orders Ben Rhodes, Susan Rice and other obama officials to respond to the Clinton/Benghazi email scandal.

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI ROSE BY 3 CONTRACTS UP TO 460. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI ROSE BY 277 CONTRACTS UP TO 143,550 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

i) Out of Scotia: 3324.24 oz

Turbulence and Brexit Make Safer Options Like Gold and Cash Essential

Turbulence and Brexit Make Safer Options Like Gold and Cash Essential

– Turbulent markets and Brexit mean it is essential to consider safer options like gold

– You need to take some risk in a portfolio – cash, gold and planning are essential

– To build a financial fortune & long-term wealth one must diversify assets & own gold

– “Physical gold (bars & coins) can be bought from an online bullion dealer –the likes of Goldcore” writes Jeff Prestridge for This Is Money UK

– Gold is considered by many to be a “safe haven in stormy times”

by Jeff Prestridge for This is Money:

Accumulating sufficient wealth to take us into – and through – retirement usually requires a near lifetime of patient saving and investing.

It involves putting money in the building society, buying a home (maybe a buy-to-let too), paying into the works pension, managing a share portfolio and taking out a tax-friendly Isa.

Often the journey is smooth but, on occasions, hiccups de-rail it – unexpected events such as redundancy and unnerving episodes such as sliding stock markets. Certainly, recent sharp falls in equity prices have unsettled many investors.

Excerpt of article and full article can be accessed on This Is Money here

Watch Our Latest Video Updates On YouTube Here

News and Commentary

May Faces Worst Government Defeat in 95 Years in Brexit Vote (Bloomberg.com)

Gold steady as dollar gains on fears of economic slowdown (Reuters.com)

Gold prices finish higher, but $1,300 remains just out of reach (MarketWatch.com)

Newmont takes top gold producer spot with $10 billion Goldcorp buy (Reuters.com)

Wall Street falls as China prompts global slowdown worries (Reuters.com)

![]()

U.K. Economy Won’t Ride Out Brexit Uncertainty This Time (Bloomberg.com)

Explosion in U.S. debt foretells dollar’s devaluation against gold (Tocqueville.com)

2019 Will Be “Turbulent”: Gold and Silver To Outperform Most Assets (GoldSeek.com)

Gold and Commodities Set to Soar in 2019 (Forbes.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Recent Market Updates

– Where Will The “Pending” Financial Crisis Originate?

– Gold and Silver Prices To Rise To $1,650 and $30 By 2020? Video Update

– Gold Outlook 2019: Uncertainty Makes Gold A “Valuable Strategic Asset” – WGC

– Blackrock Say Gold Will Be A “Valuable Portfolio Hedge” In 2019

– Financial Advice In 2019: Own Gold To Hedge $250 Trillion Global Debt Bubble – GoldCore In Irish Times

– China Adds 320,000 Ounces To Gold Reserves – First Central Bank Purchase Since October 2016

– Gold At 6 Month High At $1,300 and All Time Record Highs In Australian Dollars Over $1,870

– Gold Hedges Stock Market Falls In 2018 – Gains 2.7% In Euros and 3.8% In Pounds

– Hope For Best In 2019 But Prepare For Worst by Increased Allocations to Gold and Silver – Outlook 2019 Podcast

– Prepare For Global Debt Bubble Collapse – Outlook 2019

– Happy Christmas From All The Team in GoldCore

* * *

Gold Holds Steady Near $1,300/oz As Geopolitical Risks Including Brexit Loom Large

Gold Holds Steady Over £1,000 – Increased Likelihood Of A Disorderly Brexit

– Gold supported near $1,300/oz ahead of important British Brexit no-confidence vote

– Gold is consolidating in range between $1,280 and $1,300/oz (over £1,000/oz and €1,100/oz) – A break of resistance at $1,300 will likely see gold rise rapidly in all currencies

– Physical demand for gold coins and bars has picked up in the UK and Ireland, aided by Brexit uncertainty

Gold is holding steady today supported by a very tentative recovery in equities. Bullion should be supported as caution deepens ahead of a no-confidence vote on British Prime Minister Theresa May’s government and other geopolitical risks including the US government shutdown loom large in investors minds.

Physical demand for gold coins and bars has picked up in the UK and Ireland, due to Brexit and UK political uncertainty.

British opposition Labour Party leader Jeremy Corbyn called a vote of no confidence in the UK government, to be held at 1900 GMT today, after May’s Brexit deal was defeated by lawmakers on yesterday.

A Jeremy Corbyn government would not be good for the pound and would benefit gold in sterling terms.

The date set for Britain’s departure from the European Union is March 29, but as the deadline approaches quickly, markets are hoping that there will be an extension.

The increased likelihood of a disorderly Brexit and the extension of a U.S. government shutdown have helped keep gold which is well supported near a more than six-month high of $1,300 per ounce.

Most stock markets globally have stabilised after strong volatility and sharp falls at the end of last year. Rightly or wrongly they are taking much comfort from the resumption of China-U.S. trade talks.

The likelihood that the Fed will slow or indeed stop its interest rate hikes is also making gold increasingly attractive to investors.

end

Craig Hemke forecasts what he thinks gold/silver will do in 2019

(courtesy Craig Hemke)

Craig Hemke at Sprott Money: 2019 price forecast for gold and silver

Submitted by cpowell on Tue, 2019-01-15 19:02. Section: Daily Dispatches

2p ET Tuesday, January 15, 2019

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing at Sprott Money, today details why 2019 should be a strong year for the monetary metals, even as the bullion banks will retard all rallies to keep gold and silver under control. Hemke’s analysis is headlined “Gold and Silver 2019 Price Forecast” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/gold-and-silver-2019-price-forecast-cra…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

–

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.7620/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.7684 /shanghai bourse CLOSED UP 0.08 PTS OR 0.00%

HANG SANG CLOSED UP 71.81 POINTS OR 0.27%

2. Nikkei closed DOWN 112.54 POINTS OR .55%

3. Europe stocks OPENED ALL MIXED

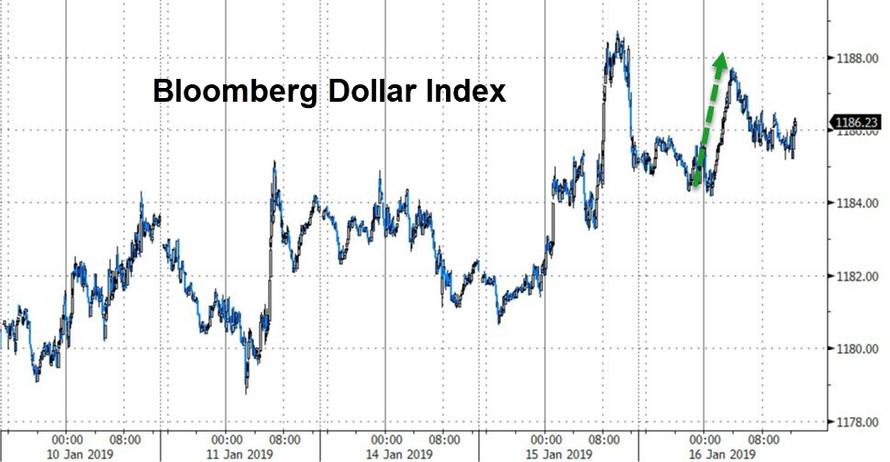

/USA dollar index RISES TO 95.91/Euro FALLS TO 1.1422

3b Japan 10 year bond yield: FALLS TO. +.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.80/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.68 and Brent: 60.31

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.23%/Italian 10 yr bond yield UP to 2.80% /SPAIN 10 YR BOND YIELD DOWN TO 1.38%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.57: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.25

3k Gold at $1289.00 silver at:15.51 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 33/100 in roubles/dollar) 66.73

3m oil into the 51 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.80 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9897 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1269 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.23%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.73% early this morning. Thirty year rate at 3.10%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3917

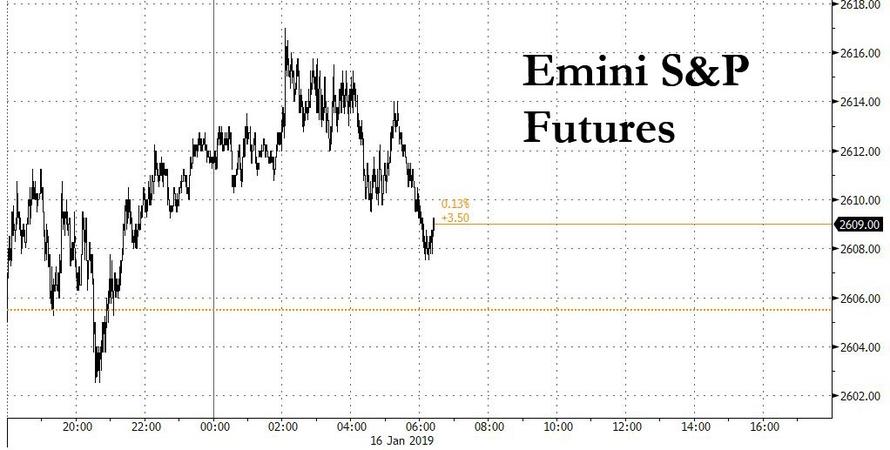

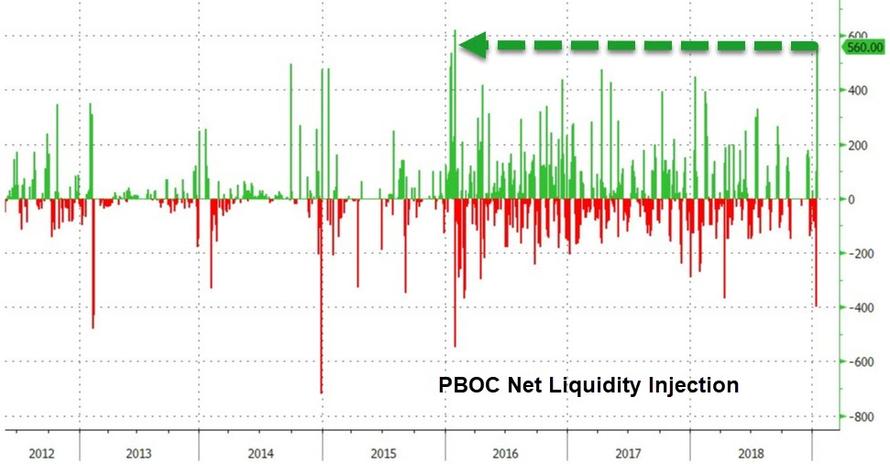

Global Stocks Rise, Pound Mixed Ahead Of May Confidence Vote After Record Liquidity Injection By China

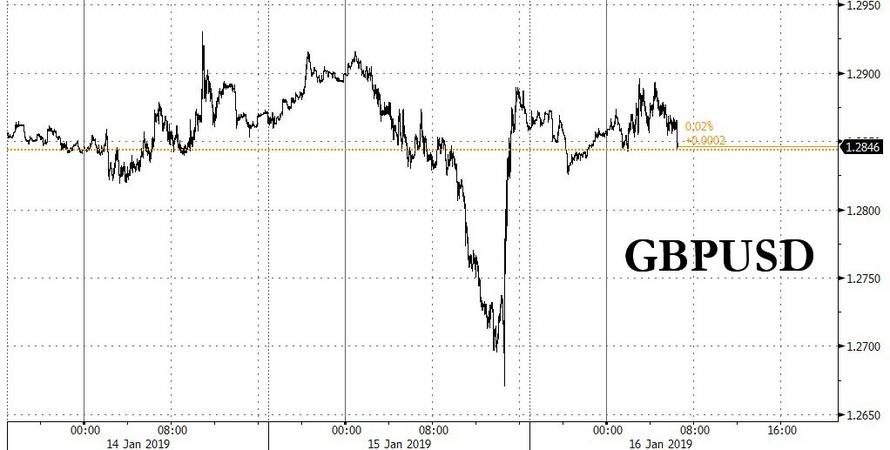

Stocks in Europe gained along with U.S. futures while Asian stocks were muted as investors saw potential for legislative deadlock to force London to delay its departure from the EU following the heavy parliamentary defeat for British Prime Minister Theresa May’s Brexit deal. The pound fluctuated and gilts fell before a no-confidence vote in Prime Minister Theresa May’s government…

… while S&P futures rose initially then faded some of their gains.

The MSCI world equity index, which tracks shares in 47 countries, was flat, while MSCI’s main European Index gained 0.3 percent. Europe’s Stoxx 600 Index was modestly in the green, led by banks and insurers following China’s plans to boost fiscal stimulus, cut taxes and shore up growth and President Mario Draghi’s comments that stimulus is still needed in the euro area. The U.K.’s FTSE 100 declined as investors contemplated May’s Brexit defeat and the pound squeeze higher continued.

Earlier in the day MSCI’s broadest index of Asia-Pacific shares outside Japan ticked up 0.2 percent, with South Korea’s Kospi and Hong Long’s Hang Seng both scaling six-week highs. Asian shares responded well to China’s central bank injecting a record amount of money into the country’s financial system. That underscored Chinese officials’ commitment to signal more measures to stabilize a slowing economy.

Global markets have drawn succor from the resumption of Sino-U.S. trade talks, though scepticism over the absence of detailed progress was underlined overnight as the U.S. trade representative that he did not see any progress made on structural issues during U.S. talks with China last week.

May’s government faces a no confidence vote on Wednesday after the shattering rejection left Britain’s exit from the European Union in disarray. May is expected to survive the vote but investors see little sign of breakthrough on the Brexit impasse. As a result, they are increasing betting on Britain being forced to postpone its planned March 29 exit, though few have any clarity on what that would mean for the country in the longer run.

Markets had largely priced in the overnight defeat, and in early trade major European bourses mirrored overall resilience in Asian markets. There, stocks were also lifted by signs that China will take more steps to bolster its slowing economy and the U.S. Federal Reserve may pause its run of interest rate rises.

“The evidence yesterday is that there is a quorum of (British) MPs who will do what’s required to avoid a no-deal Brexit,” said Chris Scicluna, head of economic research at Daiwa Capital Markets in London. “So there’s a strong probability of an extension of Article 50 and that means there’s an increased probability of a softer Brexit or no Brexit at all.”

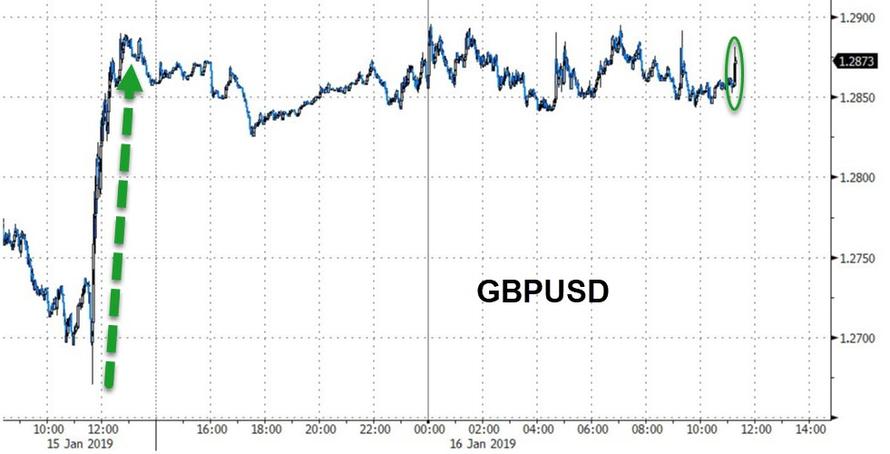

With some expecting a delay to raise chances of a softer Brexit, for example based on the opposition Labour party’s idea of membership of a permanent customs union, sterling was flat against the dollar at $1.2860. “We do think it is unlikely that sterling will fall to fresh lows unless the current government falls, and that unlikely although the risk is not zero,” said Alvin Tan, an FX strategist at Societe Generale in London. “Volatility is expected to remain high, but we do think that there is upside for sterling. Sterling is very cheap on the long-term basis, partly because of the probability of the no-deal Brexit.”

Ahead of today’s May confidence vote, Sky Deputy Political Editor said up to 100 Labour MPs will pivot towards a second referendum this morning. Meanwhile, the UK Government minister told business leaders that there is a backbench motion being prepared to delay Article 50, also says no confidence motion will fail. Elsewhere, BBC’s Political Correspondent tweets “Boris Johnson tells me May should ditch backstop, withhold at least half money till free trade deal done, accelerate no deal preparations. Says a new agreement can be reached before March 29.” At the same time, Talk Radio’s Kempsell tweets, Shadow Chancellor John McDonnell tells me he is not ruling out repeated motions of no confidence contrary to suggestions earlier.

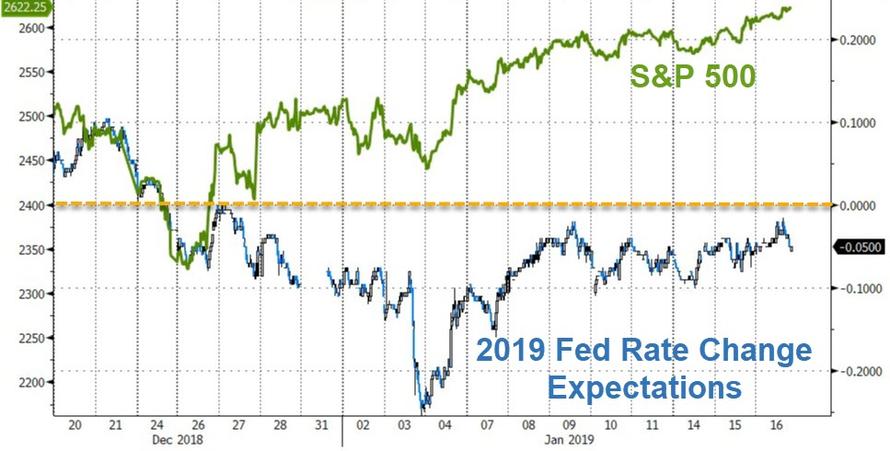

Investors are also betting that the U.S. Federal Reserve will slow its interest rate hikes. On Tuesday U.S. policymakers agreed the Federal Reserve should pause further rate hikes until it is clear how much the U.S. economy will be held back by larger risks like slowing growth in China. Investors “are mainly focused on the outcome of the U.S.-China trade negotiations, but it may take more than a month before it will become clear,” said Ayako Sera, market strategist at Sumitomo Mitsui Trust Bank in Tokyo.

Treasury yields slipped amid large-size selling of call spreads on 5-, 10-year notes and the 10Y yield rose to 2.738% up from 2.71%, while the dollar recovered as the London session progressed, trading in tight ranges. British government bonds underperformed versus their German peers in early trade, with March gilt futures opening 30 ticks lower at 122.90, underperforming German Bund futures by around 10 ticks.

The mood in markets remains fairly buoyant after China pledged to step up efforts to support growth and Draghi said the euro area will avoid a recession even though recent data signaled softening momentum. Still, there are plenty of worries to give investors pause before taking this month’s rally in equities further. The political impasse in Washington continues to leave swathes of the federal U.S. government shuttered, and the U.K.’s Brexit drama threatens to impair business confidence in the second-largest European economy.

Oil prices firmed after climbing about 3 percent in the previous session as expectations that OPEC-led supply cuts will tighten markets despite signs of a global economic slowdown. Brent crude oil futures were at $61.17 per barrel at 0904 GMT, 0.1 percent above their last close.

Expected data include mortgage applications. Bank of America, BlackRock, Schwab, and Goldman Sachs are among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.2% to 2,610.25

- STOXX Europe 600 up 0.07% to 348.96

- MXAP down 0.05% to 152.37

- MXAPJ up 0.2% to 494.28

- Nikkei down 0.6% to 20,442.75

- Topix down 0.3% to 1,537.77

- Hang Seng Index up 0.3% to 26,902.10

- Shanghai Composite unchanged at 2,570.42

- Sensex up 0.08% to 36,348.11

- Australia S&P/ASX 200 up 0.4% to 5,835.16

- Kospi up 0.4% to 2,106.10

- German 10Y yield rose 2.2 bps to 0.228%

- Euro up 0.06% to $1.1420

- Italian 10Y yield rose 3.0 bps to 2.513%

- Spanish 10Y yield fell 0.9 bps to 1.381%

- Brent futures little changed at $60.64/bbl

- Gold spot little changed at $1,289.58

- U.S. Dollar Index little changed at 95.96

Top Overnight News

- The Trump administration has ordered thousands of furloughed federal employees back to work without pay to inspect planes, issue tax refunds, monitor food safety and facilitate the sale of offshore oil drilling rights

- The EU is refusing to remove the Irish-border element that U.K. lawmakers most oppose

- The European Union said it was horrified by the massive scale of the U.K. Parliament defeat of the Brexit deal agreed with PM May but said there was no option to renegotiate. Brexit pushes Britain to brink as government fights for survival

- On an hour- long conference call following Parliament’s overwhelming rejection of the government’s deal to leave the EU, Chancellor of the Exchequer Philip Hammond floated the possibility of delaying the departure beyond the March 29 deadline, according to four people with knowledge of the call

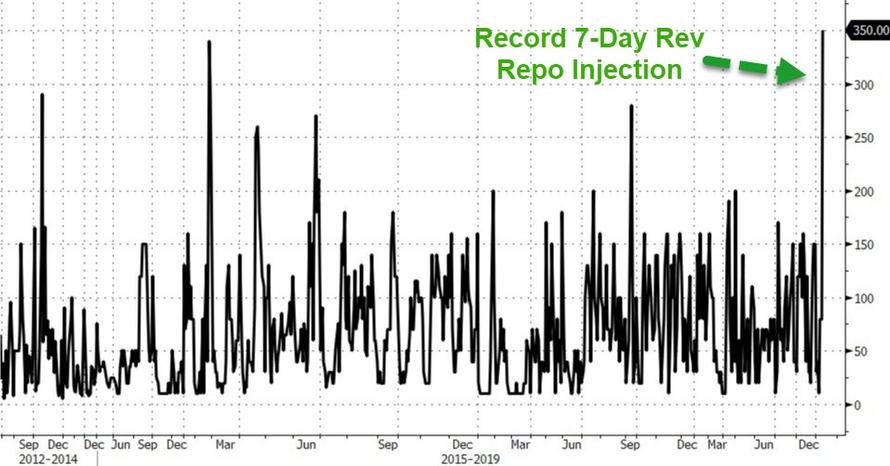

- China’s central bank injected a net 560b yuan ($83b) into the financial system through open-market operations, the biggest one-day addition on record

- BOE Governor Mark Carney told lawmakers in London that the rebound in the pound after Prime minister May’s Brexit vote defeat would appear to reflect some expectation that the process of resolution would be extended and that the prospect of no deal may have been diminished; said the BOE is in discussions with the U.K. Treasury about the powers it needs to smooth any financial ructions if the country leaves the EU without a deal

- The German government is planning to extend the contract of Bundesbank President Jens Weidmann by another eight years when it expires at the end of April, according to people familiar with the matter

- The euro-area economy isn’t headed for a recession, even though softening momentum underscores the need for ECB stimulus, according to President Mario Draghi

- China’s central bank boosted injections via open-market operations to the most on record to meet seasonal demand for cash due to tax payments and major holidays

- Federal Reserve Bank of Kansas City President Esther George, who has been one of the most hawkish members of the central bank’s policy group, urged her peers to be patient and pause before considering additional rate increases.

- Sweden’s Social Democratic leader Stefan Lofven is poised for another four years in power after convincing the Left Party to support his new centrist government, shutting out the nationalists from influence

Asian equity markets traded mixed as the region struggled for firm direction after the tech-led gains on Wall St. and PM May’s Brexit deal defeat in parliament. ASX 200 (+0.4%) finished positive as gains in tech and financials eventually outweighed the weakness across the commodity-related sectors, while Nikkei 225 (-0.6%) suffered the fallout from a firmer currency. Hang Seng (+0.3%) and Shanghai Comp. (Unch.) conformed to the indecisive tone but with the mainland kept afloat for most the session after stronger than expected Loans and Aggregate Financing data, while the PBoC also conducted its largest ever daily net liquidity injection heading into next month’s Chinese New Year celebrations in which it cited rapidly falling liquidity due to tax payments. Finally, 10yr JGBs eked only minimal gains despite the underperformance of riskier assets in Japan and firmer results in the latest 5yr JGB auction.

Top Asian News

- BOJ Is Said to Cut Inflation Forecast on Cheaper Oil

- Another Xiaomi Stock Sale Adds Grease to $32 Billion Rout

- World’s Most Valuable Startup Takes a Hit From China’s Slowdown

- China Injects Record Funds to Counter Tax, Holiday Cash Demand

- Top China Fund Sees Bonds Trouncing Stocks Again This Year

Major European equities are mixed after trimming opening gains [Euro Stoxx 50 -0.1%] with outperformance seen in the FTSE MIB (+0.5%) where banking names are up, in particular UniCredit (+2.6%) at the top of the index following the Co. stating they consider their NPE coverage to be fully adequate. Sectors are largely in the green, with financial names outperforming; in particular the Stoxx 600 Banking sector is up by over 1% as some are interpreting the governments Brexit defeat as reducing the likelihood of Britain crashing out of the EU. Other notable movers include Hammerson (+1.7%) after being upgraded at Deutsche Bank and Ryanair (+2.1%) who are up in sympathy following United Continental Holdings posting a beat on their top and bottom line overnight; were subsequently up 6% after-market. Elsewhere, Deutsche Bank (+1.7%) and Commerzbank (+1.5%) are up following reports that German officials have spoken to watchdogs regarding a potential deal between the two.

Top European News

- Reckitt CEO Kapoor to Leave After 8 Years Capped by Setbacks

- BASF Is Said to Weigh Pigments Unit Sale as Rival Also Exits

- Denmark’s DSV Bids $4 Billion for Swiss Freight Rival Panalpina

- Banks Are Said to Seek Exemptions in Looming Romania ‘Greed Tax’

- Cineworld Slips; CFO Notes Cost of ‘80s’ U.S. Cinemas Refurbs

In FX, the DXY was little changed following last night’s advances in which the index attempted, but failed to breach 96.000 to the upside, while it creeps closer to the top of a 95.850-96.080 range. Impetus for the buck was initially provided following yesterday’s comments from US Senator Grassley who cited USTR Lighthizer as US-China talks showed little progress in key issues. The dollar then came off highs as Fed hawk (and voter) George noted that it might be a good time to pause on rate hikes. Subsequently DXY fell to around 95.850 amid the Fed member’s shift in stance before recouping losses. In terms of technical DXY eyes its 100 DMA at 96.03 to the upside, though looking ahead, US retail sales have been postponed amid the ongoing US government shutdown.

- GBP – The calm after the storm as PM May’s deal was defeated by a historical 230 votes shortly before Labour leader Corbyn tabled a motion of no confidence (as expected), scheduled for 1900GMT today. The move higher came amid hopes that Article 50 will be extended past March 29th as PM May will attempt to conjure up a revised deal with the EU or face a hard-Brexit which is unfavoured by most UK MPs. However, the EU made it clear that renegotiations will not be open, while Commons leader Leadsom mentioned that the UK Government is not looking to postpone the Brexit date ahead of tonight’s vote of no confidence. The Pound was largely unreactive to Corbyn’s no confidence motion as the Conservative party and the DUP (alongside some Labour MPs) are likely to support the Government rather than amplify the chaos in Parliament. Moving on, on the data front, Sterling side-line the release of inflation figures which largely printed in-line with expectations. Cable currently resides just below 1.2900, just above its 100 HMA at 1.2857 after having tested the big figure to the upside on multiple occasions.

- EUR, JPY- Meanwhile, the EUR is relatively flat against the buck as a lack of fresh catalysts (and all eyes on Brexit) largely shelved the single currency as it moves in tandem to the greenback. EUR/USD further extends losses below 1.1450 and fluctuates on either side of the 1.1400 level ahead of its 50 DMA at 1.1380. Of note, 950mln in options expiries are seen at strike 1.1380-1.1400. Similarly, with the Yen overnight safe-haven driven gains were largely neutralised by the strengthening dollar as USD/JPY rises to the top of a 108.38-73 range with almost 1.7bln in option expiries scattered between 108.75-109.00.

- TRY – The Turkish Central Bank left rates unchanged at with their main rate at 24.00% while largely reiterating its tight stance, stating that the CB are to further monetary policy tightening will be delivered if needed. As such USD/TRY fell from 5.4134 to an intraday low of 5.3800 before pairing back a third of the move.

In commodities, Brent (-0.1%) and WTI (-0.5%) are drifting further into negative territory, with WTI losing the USD 52.00/bbl handle. As the positive market sentiment following yesterday’s 0.560mln draw in API crude inventories begins to fade; despite a 3% rally in the previous session on the back of this. Elsewhere, ARA region crude inventories rose 2.4mln/bbl to 51.3mln/bbl for the week ending January 11th. Markets will be looking ahead to today’s weekly EIA release, where crude stocks are expected to post a draw of 1.5mln. Gold (-0.1%) is relatively flat, but towards the bottom of it’s slim USD 4/oz range; as the dollar remains relatively uneventful and FX market reaction to the Brexit vote defeat is largely positive as the prospect of a no-deal has lessened. Separately, the US Senate has voted to advance a resolution which criticises sanctions on companies tied to Oleg Deripaska, which includes Rusal.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 23.5%

- 8:30am: Retail sales data postponed by govt shutdown

- 8:30am: Import Price Index MoM, est. -1.3%, prior -1.6%; 8:30am: Import Price Index YoY, est. -0.8%, prior 0.7%

- 10am: Business inventories data postponed by govt shutdown

- 10am: NAHB Housing Market Index, est. 56, prior 56

- 2pm: U.S. Federal Reserve Releases Beige Book

- 4pm: TIC Flows data postponed by govt shutdown

DB’s Jim Reid concludes the overnight wrap

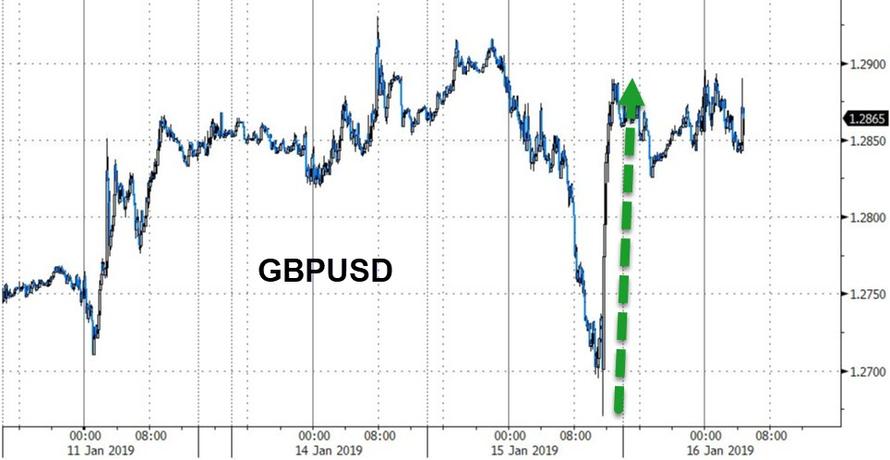

I got back late last night from Brussels and I suspect that many more U.K. politicians and Brexit negotiators will be making the opposite journey in the days and weeks ahead. To cut to the chase the DB house view is that in spite of the biggest defeat for a U.K. government (432-202) on record in the big Brexit vote, last night’s news flow was very positive for the pound and very supportive of a soft Brexit.

We’ll come to why it was so positive but first the detail. Some 118 Tory MPs broke ranks to vote against the deal as did all 10 DUP members. PM May slightly outflanked the opposition and offered them the chance to hold a no-confidence vote today, which stole Mr Corbyn thunder a bit, but he promptly demanded one. This will likely be a non-event and actually gives the Government a chance to get a confidence-restoring win with the DUP and the hard Brexit ERG Conservative group almost immediately saying they’ll back the Government. Amusingly, the 6 hour debate and 7pm vote was scheduled to follow a short lunchtime bill today that asks for low letter boxes to be banned to save postmen’s backs and to stop them being attacked by cats and dogs. Hopefully this bill survives as it will be good to see that Parliament can still get other business done in the midst of such political turmoil.

The reason DB feels this was a positive night for Sterling was that PM May surprised by immediately agreeing to cross-party talks to determine a way forward on Brexit. The exact quote from May was “… if the House confirms its confidence in this government I will then hold meetings with my colleagues, our confidence and supply partner the DUP and senior parliamentarians from across the House to identify what would be required to secure the backing of the House. The government will approach these meetings in a constructive spirit, but given the urgent need to make progress, we must focus on ideas that are genuinely negotiable and have sufficient support in this House… if these meetings yield such ideas, the government will then explore them with the European Union”.

On the positive side, since there is a large parliamentary majority in favour of a soft Brexit outcome, possibly in the form of membership of the customs union, the odds of a market-friendly outcome have risen sharply. If you were looking for doubts though then you might say a) Mrs May comments were slightly vague in who she would have cross party talks with. Is senior Parliamentarians wide enough? Will it include Jeremy Corbyn?, b) is there a consensus for anything in Parliament that the EU would accept?, c) previously the Labour Party’s executive have said that if they can’t get a general election (they likely won’t after their first attempt tomorrow) they will move policy towards a second referendum. If such an outcome materialises it might confuse the issue. It would also result in a more binary outcome and increase the risk of leaving with no deal. It could be very positive or negative, and d) how will the Conservative Brexiters react to a softer Brexit? Do they have any power? So these and many more questions remain unresolved but on balance last night opened the way to much more benign Brexit.

On c) above, Sky News reported overnight that up to 100 Labour members will shift to calling for a second referendum today, in an apparent effort to pressure Corbyn into supporting one after the confidence vote likely fails. This might complicate cross-party talks as PM May made it quite clear when extending an olive branch that the U.K. is definitely leaving the EU, so we could reach an impasse very quickly if Labour adopts this strategy. Plus, May’s spokesman said that she remains committed to an independent trade policy, which would preclude a compromise deal that includes membership in the customs union. So it remains to be seen what sort of compromise could emerge from any cross-party negotiations.

DB’s Oliver Harvey has published a special report titled “It’s time to buy the pound,” available here . He outlines the current state of play and the main risks to the view, which are: a) May losing the confidence vote today, b) May reneging on her pledge to seek a cross-party compromise, or c) parliament’s deliberations resulting in a consensus for a second referendum. The last is probably the biggest risk, but Oli is still confident that the most likely scenario is a pivot toward a softer Brexit.

In market terms the pound had depreciated -1.31% ahead of the vote, as defeat for May looked likely, but it completely pared its losses versus the dollar after PM May’s speech and her apparent pivot toward cross-party compromise. This was helped by support announced in May’s favour in the confidence vote. Futures on the FTSE 100 traded -0.47% lower after the European close, reflecting the impact of the stronger pound. Sterling is trading largely flat (-0.06%) this morning.

In reaction from the EU to the Brexit vote, officials in Brussels ruled out the prospect of an extraordinary summit of the 27 EU leaders any time soon saying there’s little to discuss if lawmakers in the UK can’t decide what they want while most diplomats said they were stunned by the extent of the loss. Elsewhere, the EC President Jean-Claude Juncker told the UK, “Time is almost up” while, French President Emmanuel Macron said that the EU won’t offer any more concessions to the UK to solve “an internal UK politics problem” and added that ‘I will be very vigilant on that, we went as far as we could.”

Prior to last night’s main event it had for the most part already been a constructive session for risk assets, helped mostly by the China fiscal headlines from earlier in the morning. That said, there was some reasonable divergence across the main US equity markets with the NASDAQ (+1.71%) leading the way in part due to a price hike by Netflix which analysts deemed will be successful (+6.52%) while the NYSE FANG index (+2.72%) turned in its third >2% move of 2019 already. The S&P 500 finished +1.07% as banks lagged a bit (+0.78%) following JP Morgan’s results – more on that shortly – while the DOW closed up a more modest +0.65%. Earlier in the day we’d seen the STOXX 600 end +0.35% and the FTSE 100 +0.58% with the latter benefit from a weakening Pound during the European session.

Elsewhere credit markets were pretty quiet with US and European HY spreads ending -4bps and -2bps tighter respectively. Yesterday we published a short note detailing our updated spread forecasts in light of the moves in credit spreads since we published our 2019 outlook in mid-November. Our qualitative expectations of moderate spread widening by year end with a bear market rally in the first few months of the year still holds. Click here for the link to the report.

Treasuries ended up pretty much unchanged and appear to have finally found a floor for now in the 2.60% to 2.70% range. Bunds (-2.4bps) were a touch stronger although the reality is that they are still in the middle of the 12bps YTD range with ECB President Draghi doing little to shake things up – confirming that “recent economic developments have been weaker than expected and uncertainties remain prominent”. Elsewhere, BTPs (+3.1bps) actually underperformed despite reports of over €35bn of bids for Italy’s first syndicated deal this year (about 10% higher than a sale last year) and Italian bank stocks dropped -2.19% after Il Sole 24 Ore reported that the ECB is implementing new rules on non-performing loans. The banks will have seven years to fully provision for current and future potential losses. Gilts were down -3.9bps and tracked the Sterling move while the eye catching move in the commodity complex came once again from oil where WTI darted back up +2.93% following two days of declines.

Turning to Fedspeak, the most notable comments came from Kansas City Fed President George, who is a voter this year and has recently been the most hawkish member of the committee. She said that another hike “is not urgent” and that called for “patience in considering our policy actions.” So a definite shift away from the hawkish end of the spectrum and toward the center of the committee, which is consistent with no rate hikes until June. Separately, Politico reported that Liu He has formally accepted the invitation to meet with US officials in Washington on January 30-31, as expected. So the twin supports of a more dovish Fed and positive progress on the trade front continued to support markets yesterday.

This morning in Asia markets are trading mixed with the Nikkei (-0.58%) leading the decline on a strengthening yen (+0.18%) while the Hang Seng (-0.09%) and Shanghai Comp (-0.06%) are off their lows and trading flattish with the Kospi (+0.37%) up. Meanwhile, the PBoC injected CNY 560bn into the financial system on Wednesday, the biggest one-day addition on record, to meet seasonal demand for cash due to tax payments and major holidays. China’s onshore yuan is down -0.11% on the liquidity injection. In other overnight news, Bloomberg reported (citing sources) that the BoJ is almost certain to cut its inflation forecast for the fiscal year starting in April citing the sharp fall in oil prices, the government’s decision to make pre-school education free and looming cuts to mobile phone charges as the reasons. The BoJ’s next board meeting and policy decision is scheduled on January 23. Elsewhere, futures on S&P 500 are up +0.24%.

Coming back to yesterday and those JP Morgan earnings that we highlighted above, the bank’s share price opened -2.32% lower but rallied to close +0.73% after earnings missed. Similar to Citigroup the day prior, fixed income sales and trading revenues came in much weaker than expected and in fact down 18% yoy and the weakest Q4 revenue in a decade. This was partially offset by strong investment banking revenues, though loan provisions were larger than expected too. Wells Fargo shares fell -1.55% as revenues and expenses both disappointed and management said they expect to operate under the Federal Reserve-mandated asset cap through end-2019, rather than through June as previously expected. A reminder that today we get results from Bank of America and Goldman Sachs.

In other news, yesterday’s economic data in the US was softer than expected but didn’t appear to really phase markets. The January empire manufacturing reading printed at just +3.9 which compared to expectations for +10.0 and an upwardly revised +11.5 in December. That was actually the lowest reading since May 2017 while the expectations component (+17.8) also hit the lowest since February 2016. That also leaves the ISM-adjusted empire index at 51.9 and the lowest since January 2017. So a marked deterioration to start the year, but not a shift into contractionary or recessionary territory. It’ll be worth seeing if the Philly Fed district report conveys a similar message to this tomorrow.

In addition to that, the December PPI reading also aired on the disappointing side at both the headline (-0.2% mom vs. -0.1% expected) and core (-0.1% mom vs. +0.1% expected) levels. That said health care PPI was solid at +0.15% which therefore points to upside for the health care component of PCE inflation and therefore the broader core PCE, which our economists expect to print around 1.89% later this month (or later, depending on the US government shutdown).

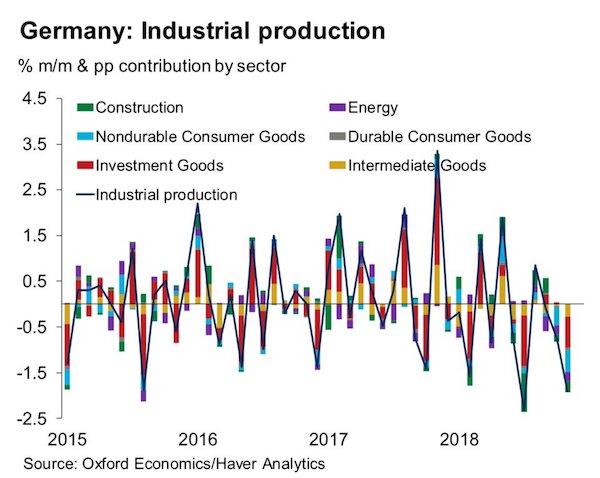

Here in Europe the main data focus was Germany’s 2018 GDP reading which hit expectations at 1.5%. Importantly, that implies only modest growth for Q4 (but at least likely positive after recent fears of a negative print) and while our economists had expected some positive payback after the WLTP shock to push growth temporarily above trend in Q1 2019, they have seen very limited evidence of this so far and as such estimate Q1 GDP at around +0.25% qoq. The result of this is a downward revision to their 2019 growth forecast in Germany to 1% from 1.3% previously. Given the recent weakness in the Euro area macroeconomic data, the ECB President Draghi said in his address to the European parliament yesterday that the Euro-area economy is not heading towards recession but to a slowdown and “it could be longer than expected.”

Other than digesting the fallout from last night’s Parliament vote in the UK today and preparing for the confidence vote, we’ll also have the December inflation data docket here in the UK to keep an eye on this morning, while there’s also the final December CPI prints due in Germany and Italy. Given the government shutdown in the US the retail sales report is to be postponed along with business inventories, leaving the December import price index and January NAHB hosing market index data as the only releases due. The Fed’s Beige Book is also due out this evening. Meanwhile the Fed’s Kashkari is due to speak late this evening while the BoE’s Carney and ECB’s Nowotny speak this morning. Earnings wise it’s the turn of Bank of America and Goldman Sachs today.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 0.08 PTS OR 0.00% //Hang Sang CLOSED UP 71.81 POINTS OR 0.27% /The Nikkei closed DOWN 112.54 PTS OR .96%/ Australia’s all ordinaires CLOSED UP 0.37%

/Chinese yuan (ONSHORE) closed DOWN at 6.7620 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 51.68 dollars per barrel for WTI and 60.31 for Brent. Stocks in Europe OPENED /MIXED

//. ONSHORE YUAN CLOSED DOWN AT 6.7620 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7684: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i)CHINA

China tries to rescue the globe with a massive liquidity injection

(courtesy zerohedge)

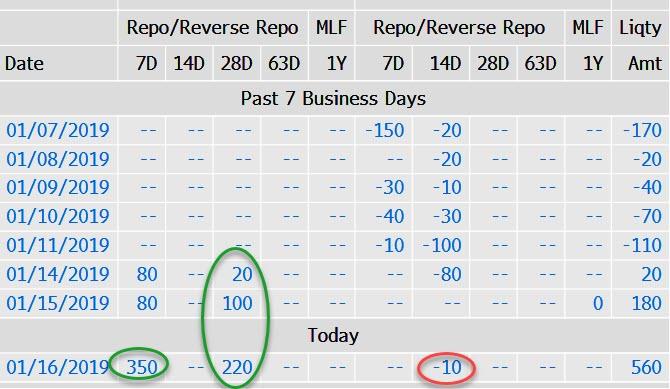

Yuan Extends Slide After Massive PBOC Liquidity Injection

Having risen almost non-stop since the start of the year – despite dismal economic data, a still-tightening Fed, and an increasingly ‘easing’ PBOC – the last two days have seen offshore yuan start to fade.

Following stimulus headlines overnight (“but not a flood of liquidity” according to the PBOC), US Sen. Grassley admitted today that Sino-US trade talks had made “little progress” – both of which sent yuan notably lower.

This drop was interrupted by cable’s surprise surge (squeeze) after the Brexit vote (stronger pound, weaker dollar, stronger yuan), but yuan has reverted back down again to the lows after the PBOC injected a near-record amount of liquidity into the financial system.

China’s central bank injected a near-record amount of liquidity via open-market operations amid tax payments and the looming ‘annual’ year-end liquidity crisis.

The PBOC injects net 350b yuan into the banking system using 7-day reverse repo contracts – the largest one-day addition of 7-day money on record, according to data compiled by Bloomberg.

And the aggregate net 560 billion yuan liquidity injection is nearly the largest ever…

The move is aimed at “keeping reasonable and sufficient liquidity in banking system as liquidity falls relatively fast during peak season for tax payments,” according to a statement from the PBOC.

With the Lunar New Year falling on Feb 5th this year (two weeks earlier than last year), we suspect liquidity provisions will be a daily occurrence from here (the last 3 days have seen 340 billion yuan for a 28-day term injected – to cross the new year liquidity threshold).

Do not mistake this for ‘stimulus’ as it will be withdrawn or rolled and merely plugs a hole – that we suspect will grow larger as trade data suggested capital outflows are re-accelerating.

END

CHINA had talks with the USA over the weekend where China is now becoming more belligerent. They do not want USA ships to pass through the Taiwan strait. It will no doubt, come shortly that Beijing demands the unification of Taiwan to the Mainland.

(courtesy zerohedge)

China To US Navy Chief: Army Will Defend Taiwan Claims “At Any Cost”

A rare and under-reported tense exchange occurred between US and Chinese military commanders in Beijing on Tuesday. A high level Chinese military official, General Li Zuocheng, told the head of the United States Navy, Admiral John Richardson, in a face to face meeting that Beijing would defend its claim to Taiwan “at any cost”.

“The Taiwan issue is an internal matter of China, concerns China’s fundamental interests and the national feelings of the Chinese people, and no outside interference will be tolerated,” Li Zuocheng said in a statement released by the Ministry of Defense, cited by the AFP.

After a series of recent instances involving US Navy warships making provocative passages through the Taiwan Strait — which the US says is its right according to freedom to navigate international waters, it appears China is going “gloves off” in direct statements challenging US military commanders.

Gen. Zuocheng, who is a powerful member of the Central Military Commission further told the US Navy chief:

If anyone wants to separate Taiwan from China, the Chinese army will defend the unity of the motherland at any cost.

Alarmingly this comes after President Xi Jinping provoked an angry rebuke from Taiwan’s pro-independence president when he demanded during a landmark speech on Jan. 2 that Taiwan submit to “reunification” with Beijing.

And in a follow-up speech days after this before military officials, Xi took his belligerent rhetoric one step further by issuing his first military command of 2019: that “all military units must correctly understand major national security and development trends, and strengthen their sense of unexpected hardship, crisis and battle.” Xi had essentially ordered the Chinese military to prepare for war as his first act of 2019.

Thus it appears top military officials have been emboldened, enough to deliver the uncompromising face-to-face message of an “at any cost” defense of China’s longtime claims over Taiwan in this week’s meeting with America’s highest naval officer.

China’s foreign ministry has consistently condemned US ships passing through the Taiwan Strait as an issue of “China’s sovereignty and territory” — to which the Pentagon has responded in multiple statements expressing commitment to “a free and open Indo-Pacific.” The Pentagon has pledged in repeat statements: “The U.S. Navy will continue to fly, sail and operate anywhere international law allows,” he added.

Just the day prior to the Chinese military’s severe warning of non-interference, Admiral Johnson hailed the talks as a “constructive and candid” discussion with his Chinese counterpart. Richardson is meeting with senior leaders of the PLA, with the goal of “continuing a results-oriented, risk reduction-focused dialogue” between the two militaries, according to a US navy statement.

Or in other words, the two sides are working to prevent prospects of any “unintentional” series of “accidents” and provocations that could lead to a major US-China war that a number of analysts have predicted could resultfrom the current soaring Washington-Beijing tensions on many fronts.

4.EUROPEAN AFFAIRS

/EUROPE/

Meijer describes the European catastrophe perfectly

a must read…

(courtesy Raul Meijer)

Europe Is Burning

Authored by Raul Ilargi Meijer via The Automatic Earth blog,

There will be elections for the European Parliament on May 23-26 2019. They will likely change the face of Europe more than anything has done since the EU was founded. That is not some wild prediction. Many European countries have held elections since the last European elections in 2014, and just about all had outcomes that shook up domestic political ratios.

In most cases, countries went from traditional parties to newly founded ones. France erased the Socialists and center-right in 2017, and the final round of the presidential elections was between Marine Le Pen’s Front National and Emmanuel Macron’s brand-new En Marche. Macron won sort of by default, because France as a country would never have voted for Le Pen.

In Italy, M5S and Lega have taken over. In Germany, Merkel’s CDU/CSU coalition lost bigly though it remained the biggest party, but Angela lost her ‘socialist’ SPD partner which gave up so much it didn’t want to be in government anymore. In Spain, Mariano Rajoy’s center right lost enough to cede power to the Socialists who came up tops because they played a smart game, not because the Spanish wanted it to rule.

We don’t have to go through all 27/28 different countries to establish that there are almost tectonic shifts happening all over, away from traditional parties and towards whoever showed up without insanely extreme views. And if you think this move is now completed, you may want to think again.

It’s amusing to realize that the country with the biggest political shift, the UK, is the only one that still hangs on to its traditional parties, and seeks its protest voice in a different way, namely through Brexit. That is, Britain shows it can get no satisfaction from the EU, whereas in the other major EU nations the dissatisfaction is projected onto domestic parties.

The underlying thought is the same: people are fed up with incumbent politicians and their affiliation with the European project. And nobody in Brussels really appears to be willing to realize this: the only thing they talk about is more Europe. But all these changes will now be reflected in the power politics of the European parliament.

And they do know that. They just hope they can limit the damage through the model in which power is divided in Europe. And to get any of that power, national parties need to find partners from other countries to form European parties (blocks) with. You need parties from at least 7 other nations to run for the European Parliament.

There are really only two parties in that parliament that really matter: the center right European People’s Party (EPP) which has 217 MEPs (members of European Parliament), and the center-left Progressive Alliance of Socialists & Democrats (S&D) which has 190 MEPs. Then there are the European Conservatives and Reformists – 74 MEPs, the Alliance of Liberals and Democrats for Europe (ALDE) – 70 MEPs, the European United Left/Nordic Green Left (GUE) – 52 MEPs, and the European Greens/European Free Alliance – 50 MEPs.

These numbers, like the national ones, are set to change, a lot. How exactly is hard to predict, because it’s not clear which block which -relatively- new party will be part of. But it’s not a wild guess to think that at the end of May the division of powers will not be left vs right (both of which are pretty much fake anyway), but pro-EU and anti-EU. Or rather, More Europe vs Less Europe.

Germany’s up-and-coming real right-wing AfD at their conference this weekend voted in a resolution that calls for getting rid of the European Parliament itself, calling it undemocratic, and claiming the “competence to make laws is exclusively for nation states.” Similar sentiments play out in Italy, Poland, Hungary and many other member states.

Given the changes in vote ratios mentioned before, it’s hard to see the More Europe model survive the elections. But that of course doesn’t keep the main parties (blocks) from running outspoken pro-Europe candidates to replace Jean-Claude Juncker as head chief after the elections. The EPP has German Europe stalwart Manfred Weber as ‘Spitzenkandidat’, the so-called Socialists/Democrats have Dutch Frans Timmermans, Juncker’s right-hand man.

They think they will be able to continue business as usual, and accumulate more power and sovereignty in the process, while support for the EU crumbles more by the day. But that’s all in the far far future, that is a whole 4 months away. And who knows what Europe will look like by then? Brussels sure doesn’t seem to know, or want to.

In Germany, the entire political system will have to reinvent itself after Merkel. And as said before, with an entire new look as far as vote numbers go. Far right and the Greens are on their way to becoming new power blocks, the Christian center right CDU/CSU and the formerly left SPD are on their way to much less support.

This is a pattern that plays out all over Europe, but what happens in Germany is, because of the way the EU is set up, crucial for all EU member states. Nothing happens in Europe without approval from Berlin. And what will the other 26 remaining members do when that level of power moves towards the AfD?

Of even more immediate concern may be Germany’s economic performance. Because the latest signs are not encouraging. Germany and Holland have done very well, but that is because they have all the others as their ‘domestic’ market. And now not even that turns out to be enough. Germany’s numbers are going down fast:

Then again, for now, worries about Germany will be trumped by those about France and Britain. The numbers of Yellow Vests in the streets of France was much larger again the past weekend than the last few ones. Macron keeps on making ever bigger mistakes. This Saturday, his riot police was filmed carrying semi-automatic weapons with live ammo. As he claimed that many of his people want to get things without making any effort.

Macron all along has tried to drive a wedge between the protesters and the people. But a large majority of the people support the protests, even if they don’t don a yellow vest. Still, Paris claims that the protesters are not the Republic, and they’re trying to overthrow democracy. When the Yellow vests approached government buildings last weekend, government spokesman Benjamin Griveaux fled, saying: “It wasn’t me who was attacked, it was the Republic.” Ergo: Not the people are the Republic, the government is. That should sell well.

For a very large number of French this sounds like they are not actually considered French by their own government. And now Macron insists on holding a national debate, in which everyone can have their say, but at the same time he insists he will not change his policies, which are what the Yellow Vests are protesting in the first place.

What they see is that Little Napoleon hasn’t hardly appeared in public for a very long time (big no-no!), but he does try to dictate to them what democracy is, and then in the same breath that they only have the choices he gives them. Protests are only allowed if the government gives permission, Paris proclaims.

Macron has cancelled his spot in the upcoming Davos spectacle for the wealthy and powerful, and I bet you the thought has crossed his mind that if he went he wouldn’t be allowed back in to his country. Not decisive, but that thought surely counts. He’s seen the whole Let Them Eat Cake scenario play out in his mind’s eye. Before putting his hand over his heart while looking in the mirror.

Macron does everything wrong than he can. And in that France has a lot in common with our for now last topic, subject, victim, take your pick, the UK.

Theresa May has lost another vote, and more chaos is guaranteed. Both the Leave and the Remain camps, opposites as they are, are divided into countless other camps, and there is no way there will ever be an agreement. You’d have a hard time finding even just two people who think Brexit means the same, let alone millions.

I wrote earlier today I wondered how come Britain is so quiet in the face of that, with the Yellow Vests example just a few miles away. And I really don’t know. Maybe we’ll find out tomorrow. The EU has hinted Brexit may not happen until the summer, not on March 29. But that’s the EU, and that’s what the Brexit vote was meant to move away from, not let them dictate even more.

Theresa May basically sat on her hands for two years, and wanted to do the work in 6 months, but that was always going to be a pipedream. The UK, in 40-odd years of EU membership, signed up to thousands of pieces of legislation, which contain hundreds of thousands of pages of legalese. All that must be checked, if need be changed, negotiated about, voted on, etc.

Not something anyone can do in half a year, and that has nothing to do with liking the EU or not. May has held her country hostage for the entire time she’s been PM, and she does that even more now, as she’s saying it’s either her deal or no Brexit at all. She’s decided No Deal is not an option. Which may be wise in view of all those documents, but who is she to decide eth entire nation future for decades to come? She wasn’t even elected as PM.

We’ll know more tomorrow after that Parliament vote, which May lost. Or will we? If Brussels accepts a major delay in Brexit, chances are May will stay in office, and we’ll have 4-5-6 more months of the same road to nowhere. Second referendum, general election? Poisoned chalices all of them.

Nothing will change either. All possible outcomes are guaranteed to have a large group of people standing against them. All options will create the appearance of a small group of people dictating life-changing events for everyone else.

Where are the British Yellow Vests? The mayor of Poland’s second-biggest city, Gdansk, was stabbed to death in public on a stage where he held a speech, Is that where we’re going?

And lest we forget, what happens in Europe is not very different from what happens in the US; things merely play out slightly differently in different locations. In the US, as in the UK, there are no whole new parties taking over, no AfD and Macron and Yellow Vests and Salvini, but there is Trump and Brexit.

The common denominator is people’s anger with the economic models that leave them scrambling to make do, all the while seeing their lives being taken away from them bit by bit while whoever’s in power keeps bankers and other rich folk contented.

It’s not much use seeing all this as separate incidents or developments. It’s a big wave that will reshape the world as we know it. Let Them Eat Cake has gone global, and there’s not nearly enough cake to go round.

GREECE

Chinese gangs operating out of the port of Piraeus were engaged in tax fraud as they avoided import duties etc. Greece has been fined over 200 million euros for not catching this sooner. China owns the port of Piraeus

(courtesy zerohedge)