GOLD: $1310.40 DOWN $4.85 (COMEX TO COMEX CLOSING)

Silver: $15.72 DOWN 13 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1306.50

silver: $15.67

For the entire week, China has been off for their lunar New Year. China is such a huge purchaser of physical gold, the crooks now have an easy time shorting gold/silver because they do not have to cover until Monday.

So do not pay any attention to the whacking of gold/silver today. It will last until Monday morning.

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 54 NOTICE(S) FOR 5400 OZ (0.1679 tonnes

TOTAL NUMBER OF NOTICES FILED SO FAR: 8862 NOTICES FOR 886,200 OZ (27.564 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

9 NOTICE(S) FILED TODAY FOR 45,000 OZ/

total number of notices filed so far this month: 500 for 2,545,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3408: DOWN 63

Bitcoin: FINAL EVENING TRADE: $3401 DOWN $71

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 30/54

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,314.200000000 USD

INTENT DATE: 02/05/2019 DELIVERY DATE: 02/07/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 12

661 H JP MORGAN 18

686 C INTL FCSTONE 3

690 C ABN AMRO 20 1

737 C ADVANTAGE 23 6

800 C MAREX SPEC 7 1

880 H CITIGROUP 16

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 54 54

MONTH TO DATE: 8,862

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A STRONG SIZED 2358 CONTRACTS FROM 209,459 DOWN TO 207,101 ACCOMPANYING YESTERDAY’S 3 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

235 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 235 CONTRACTS. WITH THE TRANSFER OF 235 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 235 EFP CONTRACTS TRANSLATES INTO 1.175 MILLION OZ ACCOMPANYING:

1.THE 3 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.595 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 4210 CONTRACTS (FOR 5 TRADING DAYS TOTAL 4210 CONTRACTS) OR 21.050 MILLION OZ: (AVERAGE PER DAY: 842 CONTRACTS OR 4.210 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 21.050 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.00% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 238.51 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2358 WITH THE 3 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD SMALL SIZED EFP ISSUANCE OF 235 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A STRONG SIZED: 2123 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 235 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 2358 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 3 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.85 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.047 BILLION OZ TO BE EXACT or 150% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 9 NOTICE(S) FOR 45,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.595 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A GOOD SIZED 5223 CONTRACTS UP TO 479,736 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $0.30//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5510 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 5510 CONTRACTS, DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 479,736. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,733 CONTRACTS: 5223 OI CONTRACTS INCREASED AT THE COMEX AND 5510 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 10,733 CONTRACTS OR 1,073,300, OZ = 33.18 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A GAIN IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $0.30.

YESTERDAY, WE HAD 10,064 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 28,633 CONTRACTS OR 2,863,300 OZ OR 89.06 TONNES (5 TRADING DAYS AND THUS AVERAGING: 5726 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAYS IN TONNES: 89.06 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 89.06/2550 x 100% TONNES = 3.49% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4,720.39 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 5223 WITH THE GAIN IN PRICING ($0.30) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5510 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5510 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 10,733 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5510 CONTRACTS MOVE TO LONDON AND 5223 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 33.18 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $0.30 IN YESTERDAY’S TRADING AT THE COMEX

we had: 54 notice(s) filed upon for 5400 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.85 TODAY

THE FRAUD CONTINUES:

A STRONG PAPER WITHDRAWAL OF 1.37 TONNES

/GLD INVENTORY 811.82 TONNES

Inventory rests tonight: 811.82 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 13 CENTS IN PRICE TODAY:

A BIG CHANGE IN INVENTORY AT THE SLV.

A WITHDRAWAL OF 938,000 OZ OF SILVER FROM THE SLV/

/INVENTORY RESTS AT 309.656 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A STRONG SIZED 2358 CONTRACTS from 209,459 DOWN TO 207,101 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

235 CONTRACTS FOR MARCH. 0 CONTRACTS FOR MAY., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 235 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2358 CONTRACTS TO THE 235 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG LOSS OF 1551 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 10.62 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.595 MILLION OZ STANDING IN FEBRUARY.

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 3 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 235 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED CHINESE NEW YEAR //Hang Sang CLOSED NEW YEAR /The Nikkei closed UP 29.61 PTS OR 0.14%/ Australia’s all ordinaires CLOSED UP 0.39%

/Chinese yuan (ONSHORE) closed DOWN at 6.7422 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 53.59 dollars per barrel for WTI and 61.92 for Brent. Stocks in Europe OPENED RED //.

ONSHORE YUAN CLOSED DOWN AT 6.7422AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7700: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA

4/EUROPEAN AFFAIRS

Germany

German industrial orders plunge 1.6%, the most since 2012 as it seems that the German economy has hit a brick wall

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/USA

Venezuela says that it has intercepted covert USA weapons from Miami

( zerohedge)

9. PHYSICAL MARKETS

c)Palladium is the first metal to break out of the price suppressing derivative cage set up for precious metals by the futures market.

a good read…

( Craig Hemke/Sprott/GATA)

e)France has been for centuries a gold loving country even from the time of Napoleon Bonaparte. Now we see a French magazine challenge the Bank of France’s gold lending scheme as nothing but a scam( Chris Powell/Edouard Freval/Politique magazine_)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

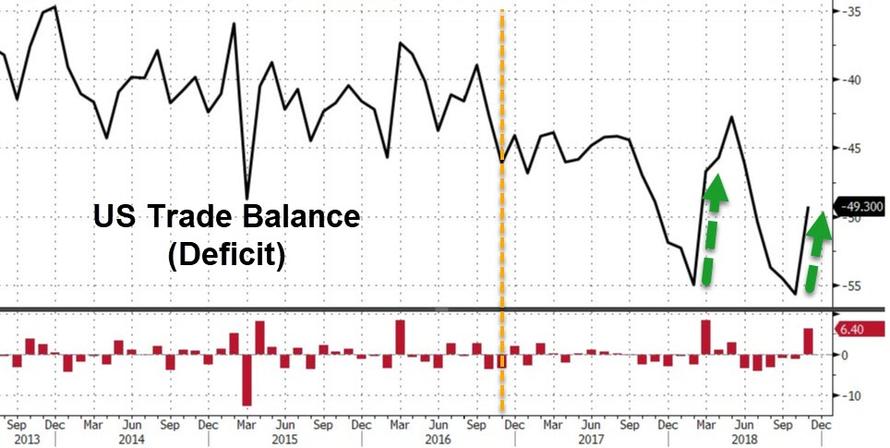

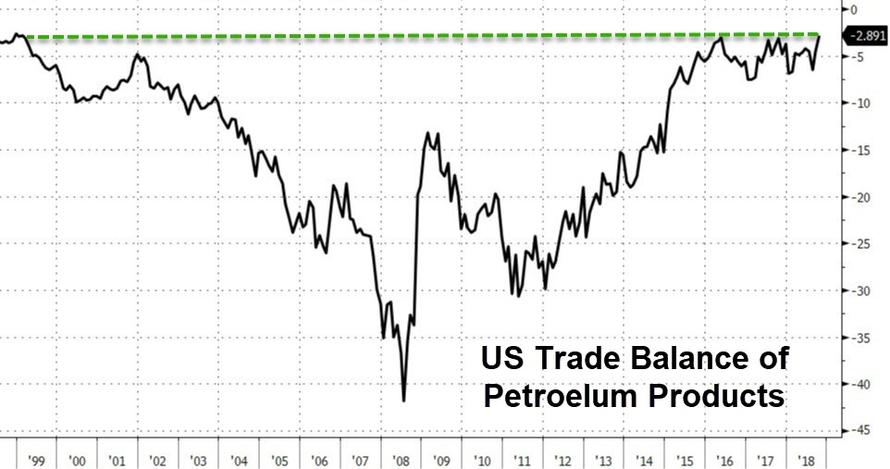

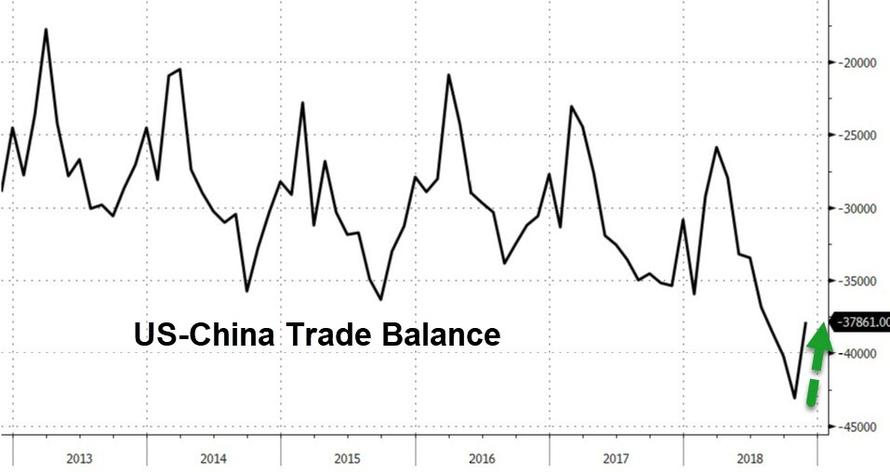

The trade deficit shrunk by 11.5% from 51.6 billion down to 49.3 billion dollars. However it was caused by the slowing of imports and a slowing of exports. The slowing of exports exceeds the slowing of imports and thus the improvement

( zerohedge)

a)January was a poor sales month for cars. Today car dealers are overflowing with unsold cars as the ticket price is just too high for the public.

( zerohedge)

iv)SWAMP STORIES

Looks like Eliz. Warren (Fauxcahontas) will never live this one down: in 1986 she identifies herself as an American Indian on her 1986 bar registration. She claimed she never used her “Indian” status to gain entry to anywhere…she was wrong.

( zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 3514 CONTRACTS DOWN TO 134,486 CONTRACTS. AFTER MARCH, APRIL ROSE FROM 17 OPEN INTEREST CONTRACTS TO STAND AT 18 FOR A GAIN OF 1. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 905 CONTRACTS UP TO 40,098 CONTRACTS.

FOR COMPARISON SILVER COMEX CONTRACT MONTH FEB 2018 VS FEB 2019

ON FIRST DAY NOTICE FEB 1/2018 CONTRACT MONTH WE HAD 670,000 OZ. AT THE MONTH’S CONCLUSION WE HAD 2.035 MILLION OZ STAND AS WE WITNESSED QUEUE JUMPING ON A REGULAR BASIS AT THE SILVER COMEX.

TODAY THE INITIAL AMOUNT OF SILVER STANDING IS 2.050 MILLION OZ./

ITALEXIT: Italy’s Debt Crisis Will Lead To Banking Crisis, Euro Exit and Will “Rock EU To Its Foundations”

– ITALEXIT: Italy to crash out of Euro and ‘rock EU to its foundations’

– Italy’s debt crisis will lead to default, exit from the euro, or both claims respected economist Bootle

– Italy has fallen back into recession with its economy shrinking by 0.2% in the last quarter

– “When Italy finally blows up, it will cause both a banking crisis that will shake the European economy and a political crisis that will rock the EU to its foundations”

by Roger Bootle of Capital Economics in the Daily Telegraph

Last week’s data showing a drop in Italian GDP in Q4 of last year confirmed what many observers had already suspected: Italy is in recession.

Or rather, in another recession, for this follows similar phases in 2008, 2011 and 2012.

Where is this going to end?

Although we have got used to weak economic performance from Italy, for much of the post-war period Italy grew rapidly. In 1987 its GDP even briefly overtook the UK’s. It subsequently dropped down the international league tables so that by the time the euro was formed in 1999 it was already a weak performer. But the euro has made matters worse. Since its formation, Italy has grown by only 9pc.

By contrast, the poor old UK, self-excluded from the benefits of the single currency, has grown by 44pc. Funny that.

It is perhaps surprising that it has taken so long for Italy to reach the current impasse.

Why Italy’s Debts Are Europe’s Big Problem. Click to enlarge. Source: Bloomberg

Why Italy’s Debts Are Europe’s Big Problem. Click to enlarge. Source: Bloomberg

There are several factors that have kept an incipient crisis at bay. First of all, until recently there was hope. Italy couldn’t just carry on as before and being in the euro offered a real alternative. It may well have been an uncomfortable route, but austerity and “internal devaluation” were supposed to make Italy competitive while also improving the public finances.

After all, Spain has achieved an impressive turnaround. In some ways it helped Italy that Greece was obviously in such a dire position, both running up to the eurozone crisis of 2012 and after it. At least Italy wasn’t Greece.

Continuing the previous trend, throughout Italy’s 20 years in the euro, the political system has been in a mess. Brussels called the shots and the Italian establishment felt in no position to challenge it. Bear in mind that not only was Italy a founding member of both the EU and the euro, but for a long time the Italian public was particularly enthusiastic about the EU and its plans for integration. Resentment of the EU (and Germany in particular) is a relatively new phenomenon.

Over recent years, the recovery of the world economy, encompassing the eurozone, gave hope that the rising tide would float even Italy’s beached boats. And indeed from 2015 to 2017 there was a mild recovery and unemployment fell back.

But now the situation looks completely different. It looks as though the world economy is weakening decisively. The message to be drawn from the US Fed’s abrupt change of tone at its meeting last week is that it suspects the US economy is about to enter a slowdown. (Friday’s strong payrolls data apparently suggested otherwise.)

Italy is closely dependent upon the health of the world economy, with over 30pc of its GDP accounted for by exports, compared to only 12pc for the US. With the Italian economy now contracting again, unemployment is rising from its already appallingly high level of 10pc. Moreover, the surveys suggest continued weakness for the rest of 2019. Despite austerity, the ratio of government debt to GDP is now at 132pc. And there has been no improvement whatsoever in competitiveness against other euro members. Admittedly, Spain continues to do remarkably well but it has become painfully obvious that while Italy isn’t Greece, it isn’t Spain either.

What’s more, the political situation is now radically different. You shouldn’t be misled by last year’s agreement between the EU Commission and the Italian government on Italy’s budget deficit. This was a typical EU fudge. The Italian government believes that stronger growth will be made possible by its laxer fiscal policies, with the result that the budget deficit will come in much lower than the Commission believes. But after recent economic news from both Italy and the wider world, this view goes beyond optimism and into fantasy.

The Italian government has tried to blame the economic slowdown on weakness in the world economy and particularly the slowdown in China. This sounds plausible. One part of the Italian economy that has been particularly weak recently is car production. (Would the UK’s Society of Motor Manufacturers and Traders, which is wont to blame weakness in the UK’s car production on Brexit, please take note.)

But in Q4 of last year net exports boosted Italian GDP. The key feature of recent Italian GDP numbers has been the weakness of consumers’ expenditure. Expectations of future unemployment have risen and consumers have increased the proportion of their incomes devoted to saving. In essence, the Italian public seems to be sensing trouble ahead.

They are right to. The bond markets continue to worry about the sustainability of Italy’s debt position and its continued membership of the euro. Italian 10-year bond yields are about 2.6pc above their German equivalents, compared to 1.2pc before the current government was formed. Unless Italy manages to conjure up a sustained growth spurt, then the eventual result will be a default, an exit from the euro, or both.

Meanwhile, partly reflecting these prospects, the imbalance in monetary movements within the eurozone continues to widen. Germany continues to build up huge claims on other countries within the euro system, with claims against Italy being the largest. Italy’s (Target 2) liabilities within the euro system have now risen to some €500bn (£438bn).

And who can say how the domestic political situation will pan out? The government could lose popularity as the Italian recession deepens. In May’s elections to the European parliament, Eurosceptic candidates are likely to do well across the continent.

Here in the UK the economic establishment has its gaze fixed on Brexit.

Yet, while Remainers try to find ways of keeping the UK in the EU, the ties that bind the union to one of its founder members and erstwhile keenest supporters are fraying.

As and when Italy finally blows up this will cause both a banking crisis that will shake the European economy and a political crisis that will rock the EU to its foundations.

Click here to read the Telegraph piece in full

News and Commentary

Gold steady as Trump speech stokes fears of govt shutdown (CNBC.com)

Gold finishes lower for third session in a row (MarketWatch.com)

Goldman said to plan cuts to commodity trading desk (MarketWatch.com)

Gold deal rush sweeps by broader mining sector – “options running out” (Reuters.com)

Euro-Area Weakness to Unite East Europe With Rates Seen on Hold (Bloomberg.com)

The Relevance of Gold as a Strategic Asset (Gold.org)

Crypto CEO Dies Holding Only Passwords That Can Unlock Millions in Customer Coins (Bloomberg.com)

Brexit and Who Is Going to Cut Down the Irish Fairy Tree? (BonnerAndPartners.com)

Listen on iTunes,Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

05 Feb: USD 1,314.00, GBP 1009.15 & EUR 1,150.67 per ounce

04 Feb: USD 1,311.00, GBP 1004.36 & EUR 1,145.55 per ounce

01 Feb: USD 1,320.75, GBP 1008.54 & EUR 1,150.83 per ounce

31 Jan: USD 1,322.50, GBP 1006.95 & EUR 1,152.16 per ounce

30 Jan: USD 1,312.95, GBP 1002.04 & EUR 1,148.44 per ounce

29 Jan: USD 1,308.35, GBP 994.48 & EUR 1,143.24 per ounce

28 Jan: USD 1,301.00, GBP 987.98 & EUR 1,139.81 per ounce

Silver Prices (LBMA)

05 Feb: USD 15.86, GBP 12.19 & EUR 13.89 per ounce

04 Feb: USD 15.74, GBP 12.05 & EUR 13.75 per ounce

01 Feb: USD 16.01, GBP 12.26 & EUR 13.96 per ounce

31 Jan: USD 16.07, GBP 12.24 & EUR 13.99 per ounce

30 Jan: USD 15.91, GBP 12.15 & EUR 13.92 per ounce

29 Jan: USD 15.85, GBP 12.05 & EUR 13.87 per ounce

28 Jan: USD 15.68, GBP 11.93 & EUR 13.75 per ounce

Recent Market Updates

– “Right” Trump and “Left” Ocasio-Cortez Will Join Forces And Debase The Dollar

– 7 Financial Truths In An Uncertain 2019

– Central Banks Buy More Gold In 2018 Than Any Year Since 1967

– Gold Breaks Out of Range After Dovish Fed – Further 1% Gain to $1,321/oz

– U.S.-China War May Be “Just A Shot Away”

– Buy Bitcoin or Gold? Bitcoin Buyers Investing In Gold In 2019

– Gold Consolidates Above $1,300 After 1.2% Gain Last Week

– Gold Bullion Will Protect From Politicians, Brexit and Increasing Market Volatility In 2019

– Brexit – The Pin That Bursts London Property Bubble

– Davos: David Attenborough Warns We Are Damaging The World ‘Beyond Repair’

– Gold May Return 25% In 2019 Given Brexit, Trump and Other Risks – IG TV Interview GoldCore

– Brexit, EU, Germany, China and Yellow Vests In 2019 – Something Wicked This Way Comes

– Three Reasons Gold May Embark On An Extended Rally

Answer GATA’s questions on gold market rigging, congressman tells CFTC

Submitted by cpowell on Tue, 2019-02-05 21:13. Section: Daily Dispatches

Congressman Demands CFTC Explain Its Failure to Find Silver Market Manipulation Where Justice Department Did

From Money Metals News Service, Eagle, Idaho

Tuesday, February 5, 2019

https://www.moneymetals.com/news/2019/02/05/cftc-silver-market-manipulat…

WASHINGTON — A member of the U.S. House Financial Services Committee today pressed the Commodities Futures Trading Commission on its conspicuous failure to uncover the very silver market manipulation now being prosecuted by the U.S. Department of Justice.

In a probing letter dated today to CFTC Chairman J. Christopher Giancarlo, Rep. Alex X. Mooney, R-West Virginia, writes:

“The U.S. Justice Department obtained a guilty plea from a former commodities trader for JPMorganChase & Co. to charges of manipulating the gold and silver markets between 2009 and 2015, and its investigation into the actions of related parties is ongoing.

“The period at issue substantially overlaps the time during which your commission was investigating complaints of manipulation of the silver market — 2008 to 2013. However, in 2013 the commission announced that it had closed its investigation without finding any wrongdoing.

“Why did the commission fail to find the wrongdoing the Justice Department has confirmed and continues to investigate? Also, will the commission now be re-opening its investigation into silver market manipulation and opening an investigation into gold market manipulation? If not, why not?”

Meanwhile, Rep. Mooney asks about the CFTC’s recent refusal to answer questions posed by a non-profit watchdog group called the Gold Anti-Trust Action Committee (GATA) that investigates government interventions in gold and silver markets:

Rep. Mooney’s letter seeks answers from the CFTC about its apparent reporting discrepancies, the unusual correlation between the Chinese yuan and the gold price, and whether the CFTC believes it has jurisdiction over gold market trading by the U.S. government or foreign governments.

“Congressman Mooney understands that a lack of transparency in the gold and silver markets not only undermines confidence, but also enables governments and powerful financial interests to manipulate currencies and asset prices to Americans’ great detriment,” said Jp Cortez, policy director for the Sound Money Defense League.

“Gold and silver are true money, and the CFTC has a responsibility to expose and punish those who seek to secretly manipulate its value.”

Rep. Mooney’s letter to CFTC Chairman J. Christopher Giancarlo can be accessed here:

http://gata.org/files/MooneyLetterToCFTC-02-05-2019.pdf

The Sound Money Defense League is a public policy group working nationally to bring back gold and silver as America’s constitutional money. The group also maintains America’s Sound Money Index.

* * *

end

The New York Sun bestows the virtues on a hopeful Fed nominee, Dr Judy Shelton..a strong money advocate (and a gold bug)

(courtesy New York Sun/GATA)

New York Sun: Trump’s ideal nominee for the Fed

Submitted by cpowell on Mon, 2019-02-04 18:39. Section: Daily Dispatches

From The New York Sun

Monday, February 4, 2019

It looks like this could be the moment at which President Trump makes his move in respect of the Federal Reserve. We say that because the chatter we hear is that he’s considering nominating to its board of governors the economist Judy Shelton. The Sun endorses her heartily. It would mark a brilliant start to redeeming his campaign promises in respect of monetary policy and our central bank.

Ms. Shelton is no stranger to readers of Sun editorials — or the editorial page of The Wall Street Journal. She has long since emerged as one of the most articulate, but measured, advocates of the idea that our economic troubles spring in large part, if not exclusively, from the fiat nature of our currency. And that we need to bring back into our political economy the idea of sound money. …

… For the remainder of the commentary:

https://www.nysun.com/editorials/trumps-ideal-nominee-for-the-fed/90559/

end

Palladium is the first metal to break out of the price suppressing derivative cage set up for precious metals by the futures market.

a good read…

(courtesy Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: Mr. Palladium punches back

Submitted by cpowell on Wed, 2019-02-06 04:08. Section: Daily Dispatches

11p ET Tuesday, February 5, 2019

Dear Friend of GATA and Gold:

Palladium may be the first metal to bust out of the price-suppressing derivatives cage built for it by the futures markets and the banks and central banks that control them, the TF Metals Report’s Craig Hemke writes today at Sprott Money. The gap between physical supply and futures delivery commitments is enormous, Hemke writes.

Hemke’s analysis is headlined “Mr. Palladium Punches Back” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/mr-palladium-punches-back-craig-hemke-0…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

France has been for centuries a gold loving country even from the time of Napoleon Bonaparte. Now we see a French magazine challenge the Bank of France’s gold lending scheme as nothing but a scam

(courtesy Chris Powell/Edouard Freval/Politique magazine_)

(GATA) French magazine challenges Banque de France’s gold lending plans

Submitted by cpowell on 05:47PM ET Wednesday, February 6, 2019. Section: Daily Dispatches

12:45p ET Wednesday, February 6, 2019

Dear Friend of GATA and Gold:

Politique magazine in Paris this week published a report by Edouard Freval about the Banque de France’s new interest in lending and swapping gold through JPMorganChase & Co. even as credit and currency risks are rising and other central banks are acquiring the monetary metal to guard against those risks.

The report quotes former French central bankers criticizing the scheme. It also quotes your secretary/treasurer at some length.

Even when read in English through Google Translator the report does very well casting suspicion on the Banque de France’s scheme and reminding readers that gold is the ultimate money, not to be trifled with.

The article is headlined “La France Est-Elle en Train d’Hypothequer Son Stock d’Or?” — “Is France Mortgaging Its Gold Stock?” — and it’s posted at the Politique internet site here:

https://www.politiquemagazine.fr/economie/la-france- est-elle-en-train-dhypothe

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

De-Dollarization Accelerates: Iran Unveils Gold-Backed Cryptocurrency

Authored by Adrian Zmudzinski via CoinTelegraph.com,

Four banks in the Islamic Republic of Iran have developed a gold-backed cryptocurrency called PayMon,financial news website Financial Tribune reported on Jan. 30.

image courtesy of CoinTelegraph

According to the article, the crypto asset has been developed in cooperation with the Parsian Bank, the Bank Pasargad, Bank Melli Iran and Bank Mellat. Iran Fara Bourse, an over-the-counter (OTC) cryptocurrency exchange, will reportedly list the new cryptocurrency.

The director of Kuknos, the blockchain company taking care of the technical aspects, said that the new crypto asset is a way to tokenize assets and excess properties of the banks.

A billion PayMon tokens will be initially released, according to the article.

As Cointelegraph recently reported, Iran is allegedly negotiating with Switzerland, South Africa, France, the United Kingdom, Russia, Austria, Germany and Bosnia to carry out financial transactions in cryptocurrency.

Recently, rumors spread that Iran could unveil its state-backed cryptocurrency at the Electronic Banking and Payment Systems conference that took place last week in Tehran, but the announcement has not been made as of press time. In July 2018, it was reported that the country confirmed that it will create its own state-issued cryptocurrency to circumvent United Statessanctions.

At the end of this January, Iranian lawmakers noted that they would seek to introduce legislation to block the use of crypto for payments inside the country and keep citizens from having significant holdings.

In December last year, Cointelegraph reported that Alireza Daliri, deputy for management development and resources at the vice presidency for science and technology, said that blockchaincan help improve the country’s national economy.

image courtesy of CoinTelegraph

In a similar move, Venezuela launched its oil-backed cryptocurrency, Petro, in October of last year. However, it is unclear which exchanges the coin is currently trading on, and critics have pointed outthat the oil-fields that purportedly back Petro show little signs of activity.

Finally, CoinDesk notes that last month saw US lawmakers introduce bills against Iran’s efforts to create a sovereign cryptocurrency.

Portions of the Blocking Iran Illicit Finance Act, introduced by Rep. Mike Gallagher (R-Wisc.), called for an investigation into Iran’s crypto efforts. A corresponding bill was submitted in the Senate by Sen. Ted Cruz (R-Texas). The proposals call for sanctions against those who knowingly provide Iran with funding, services or “technological support, used in connection with the development of Iranian digital currency.”

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7422/

//OFFSHORE YUAN: 6.7700 /shanghai bourse CLOSED /CHINESE NEW YEAR FOR THE WEEK

HANG SANG CLOSED

2. Nikkei closed UP 29.61 POINTS OR 0.14%

3. Europe stocks OPENED RED

/USA dollar index RISES TO 96.16/Euro FALLS TO 1.1394

3b Japan 10 year bond yield: FALLS TO. –.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.75/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.58 and Brent: 61.92

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.17%/Italian 10 yr bond yield UP to 2.81% /SPAIN 10 YR BOND YIELD UP TO 1.25%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.64: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.90

3k Gold at $1313.90 silver at:15.75 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 12/100 in roubles/dollar) 65.73

3m oil into the 53 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.75 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9999 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1392 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.20%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.69% early this morning. Thirty year rate at 3.03%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2144

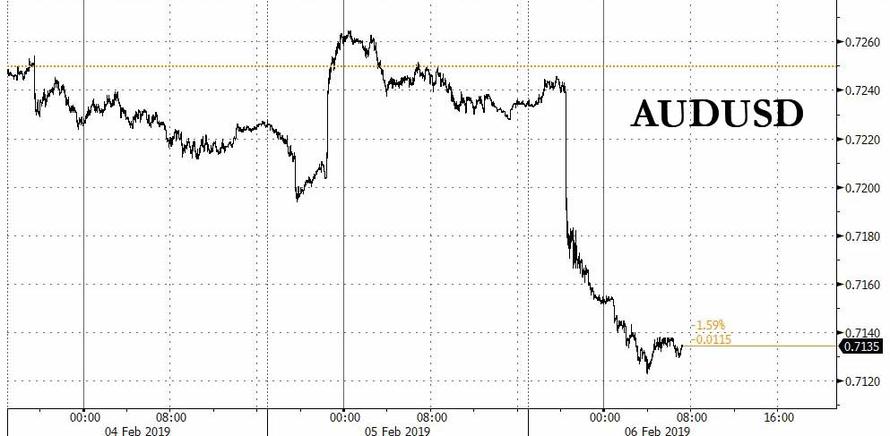

Global Rally Fizzles After Horrible German Data; Aussie Dollar Plunges, Iron Ore Surges

Repeating a pattern that has become a distinct feature to the start of 2019, global markets and US equity futures have been lower ahead of the US cash session (at which point they levitate sharply in the last 2 hours of trading), and today is no exception with the rally that brought global stocks to a 2 month high reversing overnight with China still on Lunar New Year holiday, and the MSCI world equity index last down 0.07% on Wednesday morning.

In the key event overnight, President Trump delivered the State of the Union Address in which he said the state of the union is strong and unemployment has reached its lowest level in half a century. President Trump also noted that he sent a proposal to Congress that includes plans for a physical barrier or wall on the southern border and said that he will get the border wall built, while he also commented that a new trade agreement with China must include end to unfair trade practices, reduce chronic trade deficit and protect American jobs.

Futures on the S&P 500, Dow Jones and Nasdaq all drifted lower. European stocks markets opened slightly in negative territory and then traded mixed as a fresh new batch of earnings failed to lift spirits after Trump’s address touched on trade and budget issues but provided investors with few insights. Banks were the biggest drag on the STOXX 600, with shares BNP Paribas down 1.6 percent after France’s largest-listed lender lowered its profit and revenue growth targets for 2020 after a tough fourth quarter.

Germany’s DAX dropped 0.5% with Daimler weighing after their earnings report, the German carmaker’s cautious tone reigniting concern about global trade. Tech sector is the best performing, banks also trade well. BNP Paribas bucks the trend but trades off worst levels as France’s CAC 40 traded 0.4% lower and Spain’s IBEX fell 0.1%. The eurozone Stoxx 600 blue chip index fell 0.3%.

Further weak data from Europe prompted demand for core euro zone bond yields as investors pushed back expectations that the ECB will hike rate any time soon. Of note, German industrial orders fell unexpectedly on weak foreign demand in December, tumbling 7% in December, the biggest drop since 2012, and a further sign that companies in Europe’s largest economy are struggling with a slowing world economy and trade disputes.

Earlier, Asia saw another muted session as the Lunar New Year holiday continued. Australia’s dollar tumbled after the central bank chief signaled a shift to a neutral stance on policy, and opened the door to a possible rate cut in a remarkable shift from its long-standing tightening bias, a further indication of global economic slowdown.

The policy shift caught some investors off-guard as only just the previous day the RBA had steered clear of an easing signal when holding its official cash rate at a record low 1.50 percent for the 30th straight month. The Australian dollar plunged 1.5 percent overnight and was set for its biggest daily drop since May 2017 after Australia’s central bank became the latest to signal policy easing in the face of global economic headwinds.

Elias Haddad, rates and FX strategist, at Commonwealth Bank of Australia said that while there was a risk the Aussie dollar could test $0.70, a more pronounced downward move was unlikely. “As a bank we have pushed out our call for a 25 basis point rate hike by one year to November 2020 from November 2019,” he said.

With the Lunar New Year holidays tempering volumes across a large part of Asia, and President Donald Trump’s State of Union speech providing limited impetus to markets, the dollar’s rebound was the main driver for assets. Developing-nation currencies extended their decline to the longest streak since September, while stocks showed marginal gains and credit spreads widened.

Donald Trump’s combative SOTU address added to the gloom on markets as the U.S. president unveiled no new infrastructure initiatives and instead raised the prospect of another shutdown should financing not be forthcoming for the wall on the U.S.-Mexico border he wants to build. As such the dollar settled near a two-week high.

In the annual speech outlining his priorities for the coming year, Trump said illegal immigration was a national crisis and reiterated his vow to build the border wall. While Trump’s address offered little direction on trade talks with China, he said a deal would have to reduce the U.S. trade deficit and protect American workers and businesses.

“While the threat of another government shutdown remains, the lack of negative rhetoric on trade should not be seen as a negative for risk environment,” Petr Krpata, a strategist at ING in London said in a note to clients. Investors were watching rate decision in Brazil and Poland, where policy makers were expected to follow Thailand in keeping borrowing costs unchanged.

Sterling meanwhile was a shade lower at $1.2930 after losing nearly 0.7 percent on Tuesday on weak Purchasing Managers Index data for Britain and uncertainty about Brexit talks. U.K. Prime Minister Theresa May will travel to Brussels on Thursday to tell EU leaders they must accept legally binding changes to the Irish border arrangements of Britain’s divorce deal or face a disorderly no-deal Brexit.

German 10-year government bond yields, the benchmark for the region opened one basis point lower on Wednesday at 0.16 percent, well off the 0.21 percent highs hit on Tuesday. Italian debt was in focus with the Treasury planning to sell a 30-year bond via a syndicate of banks. Italian 30-year government bond yields jumped to three-week highs at 3.678 percent as investors sold bonds to make way for the new issue. 10Y Treasurys were largely unchanged trading just shy of 2.70%.

Despite jittery sentiment, global markets are close to levels not seen since November, thanks entirely to the Fed’s dovish capitulation. Further clues on what 2019 holds may come Wednesday from Chairman Jerome Powell’s first public comments following the January meeting and interest-rate decision. There’s also the looming meetings in Beijing next week between U.S. Trade Representative Robert Lighthizer, Treasury Secretary Steven Mnuchin and their Chinese counterparts. And in his State of the Union speech, Trump said he will meet with North Korea leader Kim Jong Un in Vietnam at the end of the month.

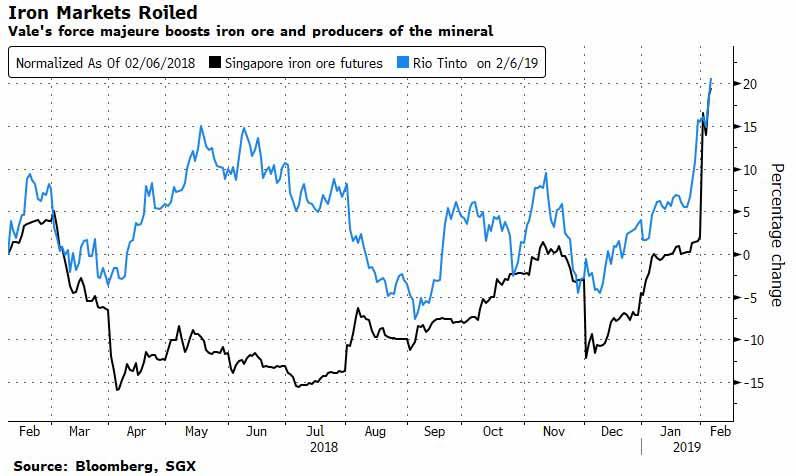

Elsewhere, in commodities, iron ore continued its recent surge, rallying toward $90 a metric ton after Brazil’s Vale SA declared force majeure on some contracts, raising the prospect of a deficit of the commodity this year.

West Texas oil fell toward $53 a barrel after the latest API report indicated to a rise in U.S. crude inventories. Copper climbed to its highest level this year, helping to boost Bloomberg’s industrial-metals index to near a four-month high.

Market Snapshot

- S&P 500 futures down 0.2% to 2,725.50

- STOXX Europe 600 down 0.07% to 364.75

- MXAP down 0.01% to 157.03

- MXAPJ down 0.1% to 513.74

- Nikkei up 0.1% to 20,874.06

- Topix down 0.05% to 1,582.13

- Hang Seng Index up 0.2% to 27,990.21

- Shanghai Composite up 1.3% to 2,618.23

- Sensex up 1% to 36,997.89

- Australia S&P/ASX 200 up 0.3% to 6,026.15

- Kospi down 0.06% to 2,203.46

- German 10Y yield fell 0.5 bps to 0.165%

- Euro down 0.1% to $1.1391

- Italian 10Y yield rose 5.9 bps to 2.435%

- Spanish 10Y yield fell 0.5 bps to 1.251%

- Brent futures down 1.2% to $61.25/bbl

- Gold spot down 0.1% to $1,313.46

- U.S. Dollar Index up 0.1% to 96.16

Top Overnight News from Bloomberg

- President Donald Trump says he is “making it clear to China that after years of targeting our industries, and stealing our intellectual property, the theft of American jobs and wealth has come to an end”

- Trump announces in his State of the Union address that he will meet with North Korea’s Kim Jong Un in Vietnam on Feb. 27-28

- British Prime Minister Theresa May risked enraging members of her Conservative Party by insisting she wants to keep the most contentious part of her Brexit plan for avoiding a hard border with Ireland

- U.K. growth be sluggish for the next few years even if a Brexit deal is secured, lowering its estimate for growth this year to 1.5 percent from 1.9 percent, according to the National Institute of Economic and Social Research

- Investor appetite for Italian debt is at a record, and the nation is making the most of it. The Treasury surprised the markets Tuesday when it unveiled the sale of 30-year notes, just two weeks after investors put in orders totaling three times the amount it offered by way of 15-year bonds

- European Central Bank officials see no urgent need to offer new long-term loans to banks and aren’t certain to do so at their next policy meeting in March, according to people familiar with the matter

- The search for a way to get Britain out of the European Union with a deal will intensify Wednesday, as Theresa May begins the second day of her visit to Northern Ireland and her Irish counterpart, Leo Varadkar, travels to Brussels to hold his own Brexit talks

- RBA’s Lowe shifted to a neutral policy outlook as he acknowledged increased economic risks at home and abroad, sending the nation’s currency down by more than half a U.S. cent

- Italy pulled in more than 26 billion euros ($30 billion) of offers for its second syndicated sovereign bond of the year, as investor appetite shows little let-up from a record-breaking deal just three weeks ago

- Here are the finance firms cutting jobs after turmoil in markets. Asset managers and banks are under pressure as volatility roils global markets and investors pile into passive, low-fee funds

Asian equity markets traded quietly with most bourses in the region closed for holidays, although the few that opened were kept afloat after the gains of their counterparts in US where earnings remained in focus and the S&P 500 notched a 5th consecutive win streak. ASX 200 (+0.3%) was led higher by tech as it mirrored the sector’s outperformance stateside, although the index was initially pressured and briefly retreated below the 6000 level amid weakness in financials due to profit taking and after its top component CBA posted a decline in H1 net. Nikkei 225 (+0.2%) also benefitted from the tailwinds and with focus centred on earnings releases, which has seen the list of best and worst performing stocks in Japan dominated by recent corporate updates. Finally, price action in 10yr JGBs was contained as the lack of demand due to the positive risk tone in Japan, was counterbalanced by the BoJ’s presence in the market. US President Trump is to meet with Chinese President Xi later this month. In related news, US Trade Representative Lighthizer and Treasury Secretary Mnuchin will visit Beijing early next week for trade discussions, while reports also noted that China is said to have agreed to negotiate on items which were previously off-limits according to a senior administration official.

Top Asian News

- SoftBank’s Son Seeks to Close Valuation Gap With Share Buyback

- Indonesia’s Economy Shows Resilience as GDP Beats Forecasts

Major European equities are in the red [Euro Stoxx 50 -0.2%], with the exception of the AEX (+0.4%) following earnings from ING Groep (+5.3%). Sectors are broadly in the red, with the exception of IT names who are outperforming slightly following on from their strong performance in the US and overnight. Other notable movers include, CYBG (+15.2%) who are at the top of the Stoxx 600 after the Co. guides their net interest margin to the upper end of their prior range. Also firmly in the green after a 13% increase in their Q4 non-IFRS revenue are Dassault Systemes (+8.6%). This mornings significant earnings came from BNP Paribas (-2.0%) and Daimler (-3.2%) who are both in the red after lowering guidance and missing on Q4 EBIT respectively. At the bottom of the Stoxx 600 are Ocado (-7.9%) as yesterday’s fulfilment enter incident will lead to a sales growth reduction until capacity can be increased elsewhere. Separately, GlaxoSmithKline (-1.5%) are expected to report their earnings today at 12:00 GMT. In recent news flow the proposed merger between Alstom (+2.1%) and Siemens (-0.5%) has been rejected by the EU.

TRop European News

- Nordea Bonuses Slump 31% as CEO Sees No Reason to Lead on Pay

- ING’s Hamers Moves Past 2018 Missteps With Gains on Profit, Cost

- Ocado Plunges as Fire Shuts Automated Warehouse, Curbing Growth

- France Hits Out at EU’s Expected Veto of Siemens-Alstom Deal

- Santander CoCo Bonds Jump as Dollar AT1 Bond Sale Said to Begin

In currencies, having rallied in relief after the RBA policy meeting yesterday, the Aussie has recoiled sharply following comments from Governor Lowe signalling a shift in rate guidance via the omission of tightening as the next move and a cut now on the agenda if the jobs market and economy overall weakens. Aud/Usd is now at risk of filling bids ahead of 0.7100 and then 0.7075, while Aud/Nzd is hovering just above 1.0400 vs 1.0500+ in the immediate aftermath of Tuesday’s RBA decision and statement, even though the Kiwi has been dragged down with its Antipodean peer – Nzd/Usd now hovering around 0.6850 from circa 0.6900 overnight. Note, the delayed GDT auction could help the Nzd pare some losses if prices rise again per indications via futures, but a decline after 4 increases in a row cannot be ruled out.

- CAD – Another G10 underperformer and victim of a broad downturn in risk sentiment that has spread to oil, with the Loonie retreating further from sub-1.3100 highs vs its US counterpart and now testing support near 1.3200. Ahead, Canadian building permits may provide some independent impetus along with comments from BoC’s Lane not long after the data.

- JPY – Bucking the overall trend of losses against the Greenback, as the DXY consolidates above 96.000, after another failure to sustain gains above 110.00, has seen the headline pair pull-back towards 109.50 again, and with hefty option expiries between 109.50-65 (2.2 bn) also a potential draw.

- GBP/CHF/EUR – All narrowly mixed vs the Dollar, but with the Pound paring losses on the back some technical buying as Cable based around 1.2925 for a 2nd time and leverage accounts reportedly took profit on short positions instigated from 1.3050 to 1.3000 yesterday. Recovery high 1.2973, just shy of the 21 DMA at 1.2975. Meanwhile, the Franc remains anchored around parity and the single currency probed a bit further below 1.1400 to test bids at 1.1380 before regaining some composure ahead of 1.1375 Fib support. However, Eur/Usd still looks fundamentally bearish amidst yet more disappointing German data/surveys (factory orders and construction PMI).

In commodities, a relatively downbeat session in the energy complex thus far, with WTI (-0.7%) and Brent (-0.6%) pressured by the overall risk-averse sentiment, alongside a firmer dollar and latest release of the API crude stocks. US crude stocks increase by 2.514mln barrels last week, a wider build than the expected 2.200mln barrels while distillate fuel oil inventories printed a surprise build. News flow has been light for the complex, though prices failed to gain any lasting support from reports that all Libyan oil exporting ports are shut due to adverse weather conditions. Looking ahead, participant will be eyeing the DoE crude inventory at 15:30GMT today alongside US production numbers which remained at a record for three consecutive weeks. Elsewhere, metals are mixed with spot gold (-0.2%) largely dictated by Dollar moves rather than the risk-sentiment. Meanwhile, iron ore May’19 futures rose in excess of 3% after Brazilian mining giant Vale declared a force majeure on some contracts, including one affecting 30mln tonnes of iron ore production a year, amid health and safety concerns. Finally, copper prices found some support amid hopes of easing trade tensions after US President Trump said he is to meet with Chinese President Xi later this month.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -3.0%

- 8:30am: Trade Balance, est. $54.0b deficit, prior $55.5b deficit

- 8:30am: Productivity Release with Limited Data Due to Shutdown

- 6:05pm: Fed’s Quarles Speaks on Bank Stress Testing

- 7pm: Fed Chairman Powell to Host Town Hall Meeting with Educators

Looking at the day ahead, we get the US November trade balance, the Fed’s Quarles is due to speak late this evening on bank stress testing while Fed Chair Powell is due to host a town hall meeting with educators. Given the venues of both, it would be a surprise if either was particularly market moving. Meanwhile the earnings highlights today include MetLife and General Motors.

DB’s Jim Reid concludes the overnight wrap

Over the past month social media has been awash with the ten year photo challenge where you post a picture of you now and one of you 10 years ago. I shunned this but have only just realised that the photo you all see at the top of all our research is one that was shot in 2009. Maybe this brings into question the credibility of research when I can masquerade as a fresh faced, innocent, naive 34/35 year old. Is there anyone out there with an older corporate mug shot? Taking this a step further if you want to see what I’ll look like in 10yrs have a look at the front cover of our Konzept in June here . One common theme transcends the past, present and future…….. Baldness!!!

What we would all give to know exactly where markets will be in one month let alone ten years. For the moment though markets continue to be in risk-on mode after another day of broad-based gains. Indeed the S&P 500 closed up +0.46% last night which means it has now closed up for the last five sessions. In fact the index is up on 18 out of 24 trading days so far in 2019 with YTD gains of +9.20%. Only 5 other years in history have matched or beat this in terms of least number of negative days to this point in the year. 1954, 1961, 1965 and 1971 saw the same number, while only 1967 saw less negative days (5) through February 5th. The S&P is now up +16.43% since its Christmas Eve trough, advancing on 21 of 28 days since then. That’s the best such streak since November 2017. Remarkable momentum no matter how you slice it.

Overnight, President Trump’s State of the Union address mostly met expectations, with a wide-ranging discussion of policy issues. On the topics most relevant for markets, Trump did not declare a national emergency or give a firm signal on whether he plans to push for another government shutdown when funding lapses next week. He spoke positively about trade talks with China, but he also endorsed the success of his tariff policy. Trump also announced a new summit with Kim Jung Un for February 27-28. S&P 500 futures, the dollar, and treasuries traded mostly flat while he spoke and futures on the S&P 500 (+0.05%) are continuing to trade flat a couple of hours later. Elsewhere, Dow Jones reported that the US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin are going to lead the trade talks in Beijing starting early next week with it likely to pave the way for a meeting between Mr Trump and China’s President Xi Jinping subsequently. The report also added that China has agreed to widen areas of discussion for trade talks to include hacking.

This morning in Asia markets are largely heading higher following Wall Street’s lead with the Nikkei (+0.29%) and Australia’s ASX (+0.41%) both up. The outperformance by the ASX has been largely on account of a surprise shift in communication from the RBA Governor Philip Lowe. He indicated that monetary policy will now shift to a neutral stance from a long period of flagging prospective tightening ahead. This also led the Australian dollar to weaken by -1.11% and sent the yield on Australia’s 10y sovereign paper down by -6.2bps. Markets in Hong Kong, China and South Korea continue to remain closed for holidays.

Back to yesterday and as discussed it was a fairly broad based rally although the NASDAQ (+0.74%) did marginally outperform which puts the five-day return for the index at an impressive +5.32% (+11.56% YTD). Banks were one of the sole laggards on the day, with the S&P 500 banks index sliding -0.33% as yields fell and the curve flattened. In Europe, the STOXX 600 closed +1.41% and is quietly up for six days in a row for the first time since September last year with the FTSE 100 (+2.04%) also clocking up a sixth successive rally (with the index up +6.38% in that time) boosted yesterday by BP’s results. Chinese markets remained closed for the lunar new year.

Meanwhile in credit markets cash HY spreads tightened -6bps in both Europe and the US. Despite the one-way traffic for risk Treasuries were actually stronger across much of the curve yesterday with 2y yields -1.4bps lower and 10y yields -2.7bps lower (making the 2s10s curve -1.3bps flatter at 17.3bps). The 10y traded as high as 2.738% intraday (before closing at 2.697%) before a slightly softer January ISM non-manufacturing report saw yields track lower. The headline reading of 56.7 was slightly lower than expected (57.1 consensus) and down 1.3pts from 58.0. Notably the employment component did improve slightly to 57.8 and the associated text in the statement also made plenty of reference to the impact of the shutdown which argues for a rebound perhaps in future months. It’s worth adding that the 54.2 services PMI was unrevised from the flash.

In contrast, bond markets were more mixed in Europe. Bunds briefly went above 0.200% intraday after the final January PMI revisions leaned a bit more positively compared to the flash data (more below) but then tracked the Treasury move in the afternoon to finish -0.7bps lower at 0.170%. BTPs did underperform however with 10y yields +6.0bps higher after the unexpected announcement of a new 30y debt sale, following strong demand at the 15y offering last month. Prior to this, rates in Europe appeared fairly non-fussed by Reuters headlines suggesting that ECB policymakers are reluctant to change forward guidance as it might tie the hands of the next ECB President. The same story also suggested that policymakers saw TLTRO as a priority – which wasn’t a great surprise. To avoid deleveraging, they’ll probably need to announce new credit easing by April, while they can leave their rate guidance on autopilot through the summer if they want.

Coming back to the PMIs, in Europe the composite reading for the Euro Area was confirmed at 51.0 which was a 0.3pt increase from the flash but a very marginal 0.1pt decline from December. That is however the lowest reading in five and a half years. The services reading drove the upward revision, jumping 0.4pts to 51.2 from the flash. Regionally, the services reading in Germany was revised down 0.1pts to 53.0 while France was revised up 0.3pts to 47.8 – albeit a still significantly contractionary reading. Italy (49.7 vs. 50.0 expected; 50.5 previously) disappointed however Spain (54.7 vs. 53.0 expected; 54.0 previously) was the big positive surprise. In fact Spain is now at a 7-month high which contrasts to the 62-month and 50-month lows in Italy and France, respectively. It’s worth noting that the composite PMI for the Euro Area is consistent with around 0.5% annualised growth.

Here in the UK the data didn’t make for particularly great reading. The services PMI dropped 1.1pts and more than expected to 50.1 (vs. 51.0 expected), which when combined with the manufacturing number puts the composite at 50.3. The last time the composite was lower was July 2016 when it temporarily spiked lower after the Brexit vote. The latest data however follows weak construction and manufacturing data in the UK which raises the prospect of the BoE not only revising down GDP forecasts this Thursday, but also sounding a lot more dovish with the biggest risk being a removal of the tightening bias. Nevertheless, market pricing for BoE policy rates did not move much on the weaker data. They continue to discount around 50% odds of a rate hike by year-end.

That data weighed on Sterling, with it falling below $1.300 in the morning and then dropping further in the afternoon to touch a low of $1.2925. In terms of the Brexit latest, yesterday we learned from one of May’s spokesman that the PM is to update the EC’s Juncker at their meeting tomorrow. May isn’t expected to meet Barnier however. The tensions within the governing coalition resurfaced again yesterday, after May told an audience in Northern Ireland that she is only seeking “legal changes” to the Irish backstop and not the scrapping of it. This is certainly the calm before the storm week for Brexit though. Events heat up next week ahead of the February 14 Parliamentary votes.

On the Fedspeak front, ahead of comments from Quarles and Powell tonight, Dallas Fed President Kaplan said that “it would be prudent for the Fed to exercise patience.” This basically reiterates the consensus view of the committee. He went on to say that “I expect we will get some further clarity during the first half of 2019,” which is a bit more explicit in terms of calendar-based guidance for the pause in interest rate hikes than Powell’s comments. Kaplan is one of the more dovish committee members, so these comments were consistent with our economists’ views.

In terms of the day ahead, early this morning in Germany we’re due to get December factory orders while later this afternoon in the US the November trade balance is due to be released. The Fed’s Quarles is due to speak late this evening on bank stress testing while at midnight Fed Chair Powell is due to host a town hall meeting with educators. Given the venues of both, it would be a surprise if either was particularly market moving. Meanwhile the earnings highlights today include MetLife and General Motors.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED CHINESE NEW YEAR //Hang Sang CLOSED NEW YEAR /The Nikkei closed UP 29.61 PTS OR 0.14%/ Australia’s all ordinaires CLOSED UP 0.39%

/Chinese yuan (ONSHORE) closed DOWN at 6.7422 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 53.59 dollars per barrel for WTI and 61.92 for Brent. Stocks in Europe OPENED RED //.

ONSHORE YUAN CLOSED DOWN AT 6.7422AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7700: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

The following is a live case on going right now. Huawei tried to steal an individual’s technology of a very strong glass. The problem for our illustrious company Huawei is that this individual was working with the FBI almost from the beginning

(courtesy zero hedge)

Huawei Tried To Steal His Technology, But He Was Working For The FBI All Along

Adam Khan believed he had invented nearly indestructible glass that was going to revolutionize the technology industry. His “diamond glass” looked like ordinary glass, but was 6 times stronger than the industry standard. His plan, according to a new Bloomberg article? License the technology to phone manufacturers and turn a pretty penny for his company, Akhan Semiconductor, Inc.

As part of his research, he sent a specimen of his glass to a San Diego lab that was owned by Huawei Technologies to have it evaluated for potential licensing – but the sample he received back after testing was badly damaged, leading him to believe it may have been tampered with.

Khan said he was optimistic at first: “We were very optimistic. Having one of the top three smartphone manufacturers back you, at least on paper, is very attractive.”

But he then found himself paranoid about knockoffs – and became even more paranoid when Huawei began to “behave suspiciously” after getting his sample. They missed a deadline to return his sample and when they did return it, it was broken in several pieces and three shards of glass were missing altogether.

He said: “My heart sank. I thought, ‘Great, this multibillion-dollar company is coming after our technology. What are we going to do now?’”

Khan was likely further surprised when he was approached by the FBI to help with an ongoing investigation into Huawei. The FBI wanted Khan and Akhan’s chief operations officer, Carl Shurboff, to conduct an undercover meeting with Huawei in Las Vegas at the Consumer Electronics Show. Shurboff was outfitted with surveillance devices and recorded the conversation, while a reporter from Bloomberg watched from a safe distance.

During the conversation, Khan and his COO “succeeded in getting Huawei representatives to admit, on tape, to breaking the contract with Akhan and, evidently, to violating U.S. export-control laws.”

Subsequent to that, when an FBI gemology expert was able to examine the glass Khan had received back, they determined the Huawei had blasted it with a 100 kW laser, which is “powerful enough to be used as a weapon”.

The investigation Khan is involved in is separate from recent indictments against the company. It is hardly the last as it seems that every day, more Huawei stones continue to turn over.

“Today should serve as a warning that we will not tolerate businesses that violate our laws, obstruct justice, or jeopardize national and economic well-being,” FBI Director Christopher Wray said in a January 28 press release about indictments regarding technology allegedly stolen by Huawei from T-Mobile. On that same day, the FBI raided the San Diego lab where Khan had sent his glass.

Display glass is considered to be a significant competitive advantage in the world of smart phones. Khan had been working on diamond glass going back to his college days when he began learning about nanodiamonds at the age of 19. According to Bloomberg:

After graduation, he ran experiments at the Stanford Nanofabrication Facility and teamed up with researchers at the U.S. Department of Energy’s Argonne National Laboratory, eventually developing and patenting a way to deposit a thin coating of tiny diamonds on materials such as glass. He also licensed diamond-related patents for Akhan from the Argonne lab in 2014. By the following year, Khan was confident enough to start promoting his new technology.

If the FBI’s new investigation into Huawei continues to provide substantial evidence, it will bolster the Trump administration’s case to block the Chinese company from selling equipment for 5G use in the US. Some countries, like Australia, have already banned Huawei equipment for fear of not being able to protect IP that’s in the interest of national security.

Khan’s final take? All companies of all sizes should be watching out for Huawei as closely as possible: “I think they’re identifying technologies that are key to their road map and going after them no matter what the size or scale or status of the business. I wouldn’t say they’re discriminating.”

To read Bloomberg’s full long-form writeup with more details on the story, click here.

4.EUROPEAN AFFAIRS

Germany

German industrial orders plunge 1.6%, the most since 2012 as it seems that the German economy has hit a brick wall

(courtesy zerohedge)

German Factory Orders Plunge Most Since 2012 As Economy Hits A Wall

Adding more fuel to the rapidly worsening outlook on the German economy, which economists at Deutsche Bank warned on Tuesday appeared to be drifting toward recession, German factory orders posted their biggest yoy slump since 2012 in December, extending a slump that began seven months ago.

December’s 1.6% monthly drop was the steepest in six months, contributing to a staggering 7% drop yoy. This fed speculation that the German economy, seen as the growth engine of Europe, contracted in the final quarter of 2018. The latest downbeat print from Q4 suggests that growth may have turned negative in the closing months of last year. If the data bear this out, it would officially signal that Germany has entered recessionary territory.

The biggest factor behind the slump was a drop-off in demand for investment goods from outside the eurozone. In one of the report’s few bright spots, orders rose 0.3% in the fourth quarter, helped by demand for investment goods. Demand for German cars, which have adapted to new emissions standards, climbed 10.2%.

But overall, data released since the beginning of the year suggests the situation in Europe’s largest economy has gone from bad to worse. A flash PMI reading published earlier this week showed German manufacturing activity contracted in January for the first time in four years. In a sign of just how quickly the outlook for the German economy is deteriorating, Bundesbank President Jens Weidmann said last week that he expects significantly slower growth in 2019 than he did only a few weeks ago as companies battle struggle with uncertainties related to the US-China trade war and Brexit.

As if Europe needed any more bad news, reports on Wednesday showed the European Commission slashed its growth forecasts for the Italian economy to just 0.2%. To sum up, if Mario Draghi needed an excuse to follow in Powell’s footsteps, this is it.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7 OIL ISSUES

8. EMERGING MARKETS

Venezuela

Venezuela says that it has intercepted covert USA weapons from Miami

(courtesy zerohedge)

Venezuela Says It Intercepted Covert US Weapons Shipment From Miami

Venezuelan officials have announced the seizure of a large shipment of American weapons which they say were bound for anti-Maduro “terrorist groups”. This comes following US national security advisor John Bolton’s pledge to deliver “humanitarian aid” into the country, covertly if need be, despite embattled President Nicolas Maduro’s vow to prevent such unauthorized shipments from entering.