GOLD: $1310.75 UP $0.35 (COMEX TO COMEX CLOSING)

Silver: $15.71 DOWN 1 CENT (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1310.50

silver: $15.73

For the entire week, China has been off for their lunar New Year. China is such a huge purchaser of physical gold, the crooks now have an easy time shorting gold/silver because they do not have to cover until Monday.

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 28 NOTICE(S) FOR 2800 OZ (0.087 tonnes

TOTAL NUMBER OF NOTICES FILED SO FAR: 8890 NOTICES FOR 889,000 OZ (27.651 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

11 NOTICE(S) FILED TODAY FOR 55,000 OZ/

total number of notices filed so far this month: 500 for 2,600,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3409: UP 5

Bitcoin: FINAL EVENING TRADE: $3401 DOWN $71

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 15/32

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,309.500000000 USD

INTENT DATE: 02/06/2019 DELIVERY DATE: 02/08/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 3

661 H JP MORGAN 12

686 C INTL FCSTONE 1

690 C ABN AMRO 20

737 C ADVANTAGE 6 5

800 C MAREX SPEC 1

880 H CITIGROUP 8

____________________________________________________________________________________________

TOTAL: 28 28

MONTH TO DATE: 8,890

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A GOOD SIZED 1055 CONTRACTS FROM 207,101 UP TO 208,276 DESPITE YESTERDAY’S 13 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

788 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 788 CONTRACTS. WITH THE TRANSFER OF 788 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 788 EFP CONTRACTS TRANSLATES INTO 1.175 MILLION OZ ACCOMPANYING:

1.THE 13 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.595 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 4998 CONTRACTS (FOR 6 TRADING DAYS TOTAL 4998 CONTRACTS) OR 24.990 MILLION OZ: (AVERAGE PER DAY: 833 CONTRACTS OR 4.165 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 24.990 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.57% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 242.45 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1055 DESPITE THE 13 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD SMALL SIZED EFP ISSUANCE OF 788 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 1843 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 788 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1055 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 13 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.72 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.047 BILLION OZ TO BE EXACT or 150% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 11 NOTICE(S) FOR 55,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.595 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A FAIR SIZED 1857 CONTRACTS UP TO 481,593 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $4.85//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3148 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 3148 CONTRACTS, DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 481,593. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A VERY GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5293 CONTRACTS: 2145 OI CONTRACTS INCREASED AT THE COMEX AND 2145 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 5293 CONTRACTS OR 529,300, OZ = 16.46 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $4.85.

YESTERDAY, WE HAD 5510 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 31,781 CONTRACTS OR 3,178,100 OZ OR 96.77 TONNES (6 TRADING DAYS AND THUS AVERAGING: 5296 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAYS IN TONNES: 96.77 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 96.77/2550 x 100% TONNES = 3.79% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4,730.2 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED INCREASE IN OI AT THE COMEX OF 1857 DESPITE THE LOSS IN PRICING ($4.85) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 3148 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 3148 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 5,005 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

3148 CONTRACTS MOVE TO LONDON AND 1857 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 15.56 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $4.85 IN YESTERDAY’S TRADING AT THE COMEX

we had: 28 notice(s) filed upon for 2800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $0.35 TODAY

THE FRAUD CONTINUES:

ANOTHER STRONG PAPER WITHDRAWAL OF 2.06 TONNES

/GLD INVENTORY 809.76 TONNES

Inventory rests tonight: 809.86 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 1 CENT IN PRICE TODAY:

NO CHANGES IN INVENTORY AT THE SLV.

/INVENTORY RESTS AT 309.656 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GOOD SIZED 1055 CONTRACTS from 207,101 DOWN TO 208,156 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

788 CONTRACTS FOR MARCH. 0 CONTRACTS FOR MAY., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 788 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1055 CONTRACTS TO THE 788 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1843 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.815 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.595 MILLION OZ STANDING IN FEBRUARY.

RESULT: A FAIR SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 13 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 788 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED CHINESE NEW YEAR //Hang Sang CLOSED NEW YEAR /The Nikkei closed UP 29.61 PTS OR 0.14%/ Australia’s all ordinaires CLOSED UP 0.39%

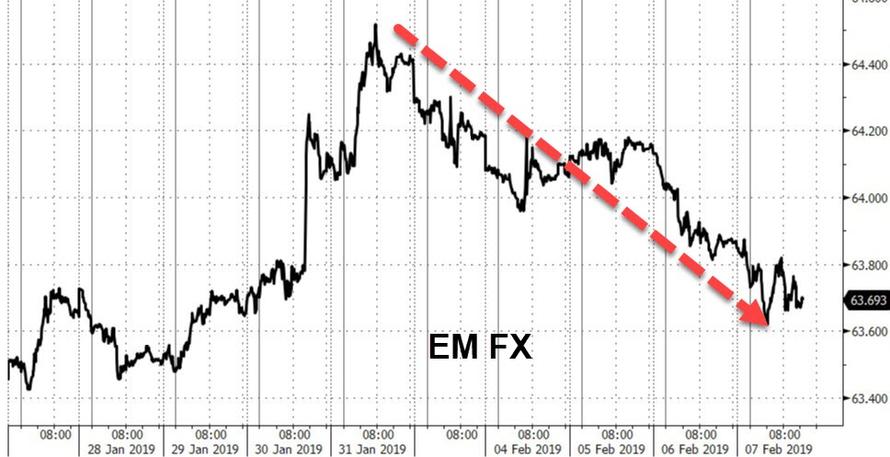

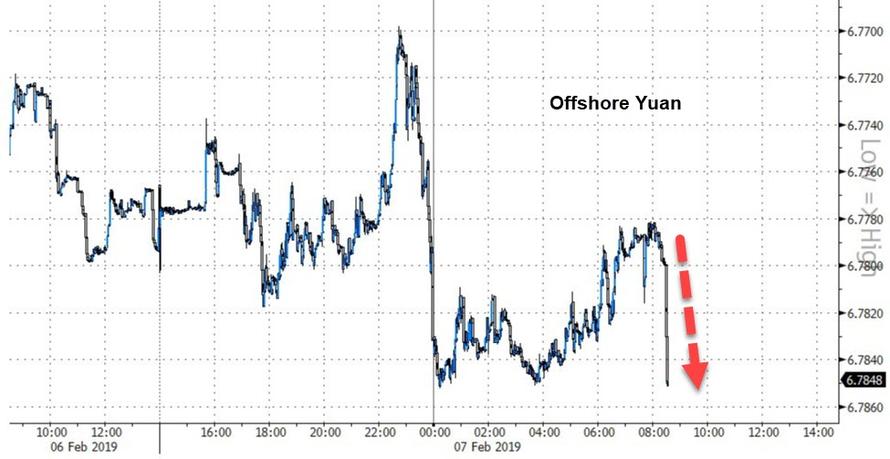

/Chinese yuan (ONSHORE) closed DOWN at 6.7422 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 53.60 dollars per barrel for WTI and 62.41 for Brent. Stocks in Europe OPENED RED //.

ONSHORE YUAN CLOSED DOWN AT 6.7422AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7837: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/USA

My goodness, the Clintons are involved with Huawei as the company has deep ties to the former Sec of state Hillary Clinton and President Bill Clinton

( Dick Morris/WesternJournal.com)

4/EUROPEAN AFFAIRS

i)UK

Not good for England this morning after the Bank of England slashes its GDP forecast for the year as well as warning of rising BREXIT damage

( zerohedge)

iii)Germany/Wirecard

Looks like we have another massive fraud on our hands with respect to German based Wirecard as a whistleblower exposes accounting fraud.

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/USA

Admiral states that the USA is now military ready to protect uSA personnel in Venezuela.

( zerohedge)

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

b)) Then: stocks further collapse on reports that Trump and Xi will not meet

ii)Market data/

a)Another good indicator to suggest the economy is faltering: Class 8 heavy truck orders just crashed by 68% in January

( zerohedge)

( zerohedge)

d)Marriage rates are down, while cohabiting rates are up. Young adults refuse to marry because mainly their student debt is just too high. Also family formations is in decline and again due to the high student and auto debt

( Mishtalk,Mish Shedlock)

e)Quite a stat: The total debt of Americans that still have student loans and are over 60 years of age is a whopping $86 billion dollars.

( zerohedge)

f)Moody’s warns the new Illinois Governor that his state is in dire shape. He warns that any new taxes will make more residents to flee and thus less citizens to pay the taxes and purchase goods to stimulate their economy

( Dabroski/Klingner/WirePoints.com

iv)SWAMP STORIES

TRUMP is furious as Schiff hires former National Security Council to trying and find stuff on him. These guys are deep staters and will stop on nothing. This is going to be a huge witch hunt

( zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 2574 CONTRACTS DOWN TO 131,912 CONTRACTS. AFTER MARCH, APRIL ROSE FROM 18 OPEN INTEREST CONTRACTS TO STAND AT 26 FOR A GAIN OF 8. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 3472 CONTRACTS UP TO 43,570 CONTRACTS.

FOR COMPARISON SILVER COMEX CONTRACT MONTH FEB 2018 VS FEB 2019

ON FIRST DAY NOTICE FEB 1/2018 CONTRACT MONTH WE HAD 670,000 OZ. AT THE MONTH’S CONCLUSION WE HAD 2.035 MILLION OZ STAND AS WE WITNESSED QUEUE JUMPING ON A REGULAR BASIS AT THE SILVER COMEX.

TODAY THE INITIAL AMOUNT OF SILVER STANDING IS 2.050 MILLION OZ./

comex gold volumes are getting extremely low as players just do not want to play in this casino.

ITALEX

Maduro sold 40% of Venezuela’s gold last year amid cash crunch

Submitted by cpowell on Thu, 2019-02-07 00:12. Section: Daily Dispatches

By Patricia Laya and Alex Vasquez

Bloomberg News

Wednesday, February 6, 2019

President Nicolas Maduro blew through more than 40 percent of Venezuela’s gold reserves last year in a desperate bid to fund government programs and pay millions to bondholders.

The government sold a total of 73 tons of gold to two firms in the United Arab Emirates and another in Turkey, opposition lawmaker Carlos Paparoni told reporters in Caracas on Wednesday. That drained reserves to about 110 tons at the end of last year from 184 tons, according to a person with knowledge of the situation, who corroborated Paparoni’s data.

…

Maduro raided the central bank’s vaults of the 2.34 million ounces of gold (worth about $3.1 billion at current spot prices) as debt piled ever higher and financing options dried up after the U.S. imposed sanctions against his regime.

Amid an international push to persuade the authoritarian ruler to cede power to a transitional government, the opposition is also seeking to thwart further gold sales to prevent a ransacking of the country during Maduro’s final days in power. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-02-06/maduro-sold-40-of-ven…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Mystery Surrounding ‘Lost’ $150M Crypto Fortune Deepens As Analysts Question Exchange Founder’s Death

We were half-joking when we speculated last week that QuadrigaCX CEO Gerald Cotten – founder of a Canadian crypto exchange that has become embroiled in a $150 million fiasco after Cotten died and purportedly took the keys to the exchange’s cold wallets to his grave, rendering his customers’ coins immovable – faked his own death in a foreign land to abscond with a fortune belonging to his customers. But a Bloomberg report published Wednesday evening has raised red flags suggesting that this ludicrous “conspiracy theory” might soon become a “conspiracy fact.”

Gerald Cotten

But since Quadriga filed for bankruptcy protection last month in the face of a rash of lawsuits being filed by angry customers demanding their coins be returned, a group of analysts and crypto-sleuths have been trying to suss out whether the claims made by Quadriga and Cotten’s widow – that the notoriously security-conscious (some might say paranoid) executive was the only employee who handled moving coins deposited with the exchange, and that he had recently shifted the bulk of the exchange’s holdings into “cold storage” platforms to which only he possessed the encrypted key, which they have been unable to locate – hold water.

And as it turns out, there has been some suspicious activity that, at first brush, would seem to call these claims into question. As one Cornell professor who spoke with BBG claimed, Quadriga’s story didn’t pass “the smell test.” If the coins were truly frozen, then why hadn’t the exchange at least furnished the public keys that would allow auditors to verify their holdings on the blockchain?

The argument that that’s what happened with Quadriga didn’t pass the smell test for many in the industry who are adept at scouring the anonymous ledgers that underpin the decentralized networks for evidence of where digital coins may be stored.

“The Quadriga story doesn’t make sense,” Emin Gün Sirer, a professor at Cornell University and co-director of the Initiative for CryptoCurrencies and Contracts, wrote in an email Wednesday. “The one amazing thing about blockchains is that anyone can audit, in essence, any company.”

[…]

“If the funds are frozen and the cold wallet is inaccessible, it should be possible for the exchange to provide the cold wallet addresses so their claims can be verified with the help of the blockchain,” Sirer said.

But the fact that the exchange hasn’t disclosed which wallets belong to it hasn’t stopped amateur investigators from analyzing transactions and taking an educated guess.

And what they found might come as disturbing – at least for QuadrigaCX’s 115,000 customers. The analysts said they couldn’t find any cold wallets holding the Ether that supposedly was one of the cryptocurrencies held on the exchange. Instead, they found that Quadriga had been moving Ether from its wallet to larger exchanges through mid-January.

But that would seem to contradict the exchange’s story that Cotten was the only one who had access. After all, he died in December.

Analysis firms such as Elementus say that by examining the blockchain patterns, they can guess which particular wallets holding coins belong to. The researcher says it couldn’t find any cold wallets holding Ether, one of the cryptocurrencies that’s missing. Instead, Quadriga was moving Ether to larger exchanges through mid-January, Elementus said.

At the same time, the patterns could mean that the exchange had set up automatic transfers to larger exchanges when its wallet balances reached a certain amount, or, alternatively, that “there’s some fishy business going on,” Elementus founder Max Galka said.

The head of one exchange where Quadriga had stashed some of its coins said that the vast majority of its holdings recently disappeared. He also noted that not being transparent about where coins are on the blockchain is troubling.

Jesse Powell, head of exchange Kraken, said it has some Quadriga balances. Of about 230,000 Ether coins that Quadriga is supposed to have had, only about 1,000 coins remain in its own wallets, Galka said.

“Not to be transparent” about where the money is exactly on a blockchain “is unusual,” said Christine Duhaime, a Canadian lawyer specializing in anti-money laundering.

According to the company, Cotten, aged 30, died of complications from Crohn’s disease in Jaipur, India in December while reportedly doing research for an orphanage he planned to build.

But if the coins have in fact been moved since his death, that could mean one of two things: Either the exchange is lying, and Cotten’s former colleagues are seeking to take advantage of his death by robbing his customers.

Or, Cotten is still alive, and has already taken the money and run?

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7422/CLOSED

//OFFSHORE YUAN: 6.7837 /shanghai bourse CLOSED /CHINESE NEW YEAR FOR THE WEEK

HANG SANG CLOSED

2. Nikkei closed DOWN 122.78 POINTS OR 0.59%

3. Europe stocks OPENED RED

/USA dollar index RISES TO 96.63/Euro FALLS TO 1.1335

3b Japan 10 year bond yield: FALLS TO. –.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.79/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.60 and Brent: 62.41

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE CLOSED DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

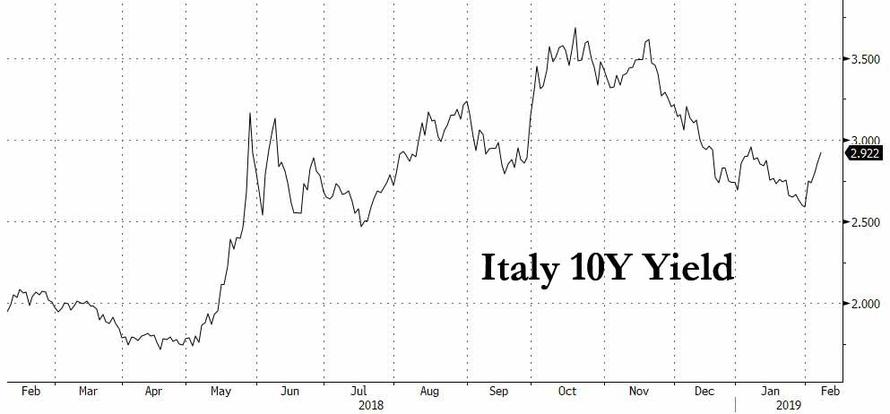

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.12%/Italian 10 yr bond yield UP to 2.92% /SPAIN 10 YR BOND YIELD UP TO 1.25%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.80: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.96

3k Gold at $1306.85 silver at:15.67 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 19/100 in roubles/dollar) 66.06

3m oil into the 53 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.79 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0087 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1398 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.12%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.67% early this morning. Thirty year rate at 3.01%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2645

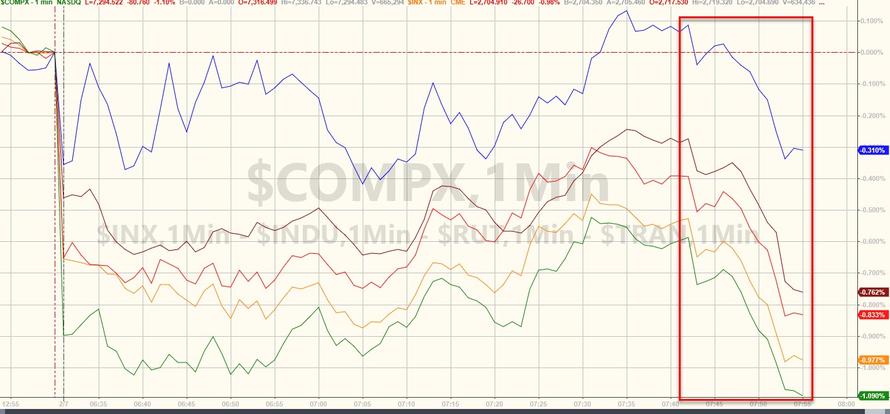

Global Stocks Slide As Dollar Spikes, Italian Bonds Tumble After EC Slashes GDP

The amazing post-Christmas/PPT/Trump rally appears to finally be over.

US traders walked in to a sight that brought in painful memories from December: a sea of red in global markets as stocks in Europe fell alongside S&P futures following a mixed session in Asia where India’s central bank joined the global easing bandwagon with a surprise rate cut. Italian bond prices tumbled after the European Commission confirmed yesterday’s media reports when it slashed growth forecasts for the euro region’s major economies, while dollar scored its longest winning streak since a hot run in early October that helped set off a wave of global bear markets.

Poor earnings and weak data out of Germany ensured Europe’s main bourses started lower and kept MSCI’s index of world stocks heading for only its second two-day run of falls of the year so far. Europe’s Stoxx 600 Index tumbled, dragged down by automakers and banks as sharply lower trading revenue from Societe Generale countered positive results from UniCredit and DNB.

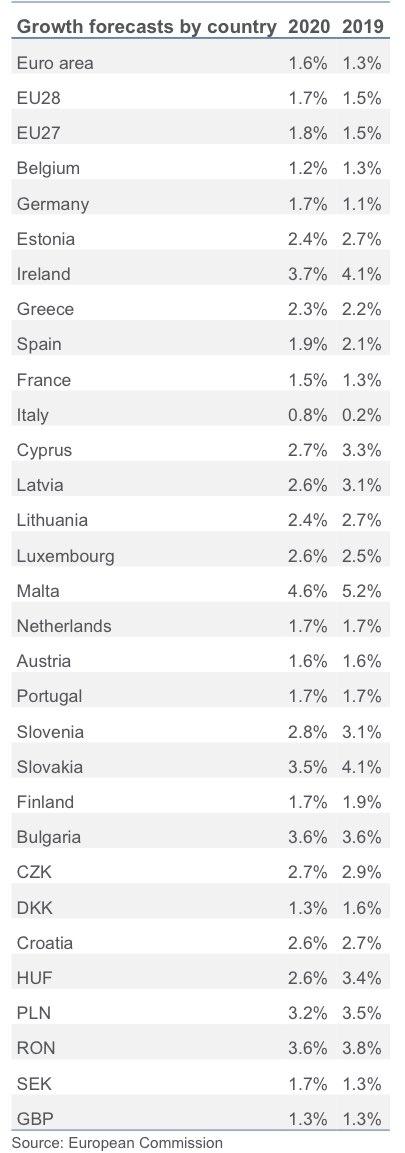

The euro weakened and bunds rose after the European Commission warned in their dour growth forecast that Brexit and the slowdown in China threaten to make the region’s outlook even worse, slashing Euro area growth to 1.3%, while Italy’s 2019 GDP forecast was cut from 1.2% to just 0.2%, barely above recession territory, and putting the country’s controversial deficit forecast in jeopardy.

.

As a reminder, Italy agreed a deficit target of 2.04 percent in December, averting a major fall-out with the EU, though this was based on a growth assumption of 1.0 percent. Slowing growth in Italy could make it harder for the country to remain within EU rules. As a result of the downgrade, Italian 10Y yields popped higher, rising near 2019 highs, which is notable because when the report first hit yesterday, markets were largely oblivious and instead were congratulating themselves on the 5x oversubscribed Italian 30Y bond that priced yesterday tighter than expected. Today is the hangover.

However, Benjamin Schroeder, rates strategist at ING, said he did not expect the EU to demand more fiscal tightening from Italy, should its forecasts be reduced. “The EU has another thing to deal with — Brexit — and the other thing is do you want to infuse the campaign ahead of the parliamentary elections with this topic.”

European banks reversed initial gains after the EC cut its growth forecasts for the region’s major economies. The Stoxx 600 Banks Index is down 0.9% as of 11:48am CET, having earlier risen as much as 0.5%. Biggest fallers are Raiffeisen and Commerzbank, both -3.3%. Italian banks trimmed earlier gains of as much as 2.7%, with the FTSE Italia All-Share Banks Index still up 0.2%. UniCredit raises 2% after 4Q earnings that exceeded plans for cost cutting and improving asset quality. London’s FTSE was the only major bourse clinging to positive territory.

Adding insult to European injury, the euro slumped to $1.1330 following the latest dismal report out of Berlin as Germany reported its fourth consecutive drop in industrial output, which declined -0.4% in December, far below the 0.7% increase expected, and down -3.9% YoY: “Another day, another piece of terrible German data. EUR/USD risks a move to $1.1300,” said ING’s chief EMEA FX and interest rate strategist, Petr Krpata.

Futures on the S&P 500, Dow and Nasdaq indexes all slipped. In Japan, shares fell amid a raft of corporate earnings, although SoftBank surged 18% on plans for its biggest-ever buyback. China and Hong Kong markets are shut.

Earlier, MSCI’s broadest index of Asia-Pacific shares outside Japan added 0.1% as it rose to its highest since early October, rising steadily since early January as the Fed capitulated to markets and changed its tune and emerging markets have surged more broadly after a torrid 2018. Australia’s benchmark stock index jumped 1.2 percent amid expectations of easy monetary policy after the country’s central bank chief shifted away from his previous tightening bias. Japan’s Nikkei slipped 0.6 percent though and the caution quickly spread to Europe.

Treasuries climbed with the dollar, which advanced for a sixth day as Federal Reserve Chairman Jerome Powell gave a brief but positive assessment of the economy and several of the world’s central banks put their tightening plans on hold.

Elsewhere the pound was struggling near $1.29 again ahead of a Bank of England meeting, while gloomy jobs data saw New Zealand’s dollar suffer a similar flop as its Australian counterpart had seen the previous day. The kiwi slid to $0.6744, losing nearly 2 percent in the past 24 hours, as investors wagered on the risk of a cut in interest rates there. The country’s central bank holds its first meeting of the year next week.

The next major trigger for markets will more likely be any breakthrough in the U.S.-Sino tariff talks when the two sides meet in Beijing next week. Probably more pressing though for the U.S. markets is the threat of another government shutdown, Nick Twidale, an analyst at Rakuten Securities Australia said. “With both sides of the house standing firm on the contentious border wall issue at present and the deadline approaching swiftly on Feb 15 we could be back where we were just a few weeks ago.”

The broad dollar gains put pressure on gold, which eased to $1,303.96 per ounce, slipping further from last week’s top of $1,326.30. Oil prices eased too after U.S. crude inventories rose and as production levels in the country held at record levels. Brent crude futures slipped 23 cents to $62.46. U.S. crude eased 19 cents to $53.82 a barrel.

Expected data include jobless claims. Fiat Chrysler, Kellogg, Philip Morris, T-Mobile, and Twitter are among companies reporting earnings.

Market Snapshots

- S&P 500 futures down 0.5% to 2,716.25

- STOXX Europe 600 down 0.2% to 364.70

- MXAP down 0.3% to 156.49

- MXAPJ up 0.07% to 514.12

- Nikkei down 0.6% to 20,751.28

- Topix down 0.8% to 1,569.03

- Hang Seng Index up 0.2% to 27,990.21

- Shanghai Composite up 1.3% to 2,618.23

- Sensex up 0.2% to 37,051.70

- Australia S&P/ASX 200 up 1.1% to 6,092.46

- Kospi unchanged at 2,203.42

- German 10Y yield fell 0.7 bps to 0.155%

- Euro down 0.2% to $1.1345

- Italian 10Y yield rose 6.4 bps to 2.499%

- Spanish 10Y yield fell 1.3 bps to 1.244%

- Brent futures down 0.2% to $62.58/bbl

- Gold spot little changed at $1,306.71

- U.S. Dollar Index up 0.2% to 96.59

Top Overnight News

- President Trump underscored his desire to reduce the trade gap with China in his State of the Union speech Tuesday, yet the deficit is on track to balloon again as a solid economy boosts American demand for imports

- The top Democrat working on a border- security deal to avoid another government shutdown said lawmakers should be able to reach a bipartisan agreement by the end of this week

- Former Fed Chair Janet Yellen said the central bank must rely on incoming economic data to determine if its next policy move will be up or down, while likening the current moment to 2016 when she kept rates on hold almost all year

- Oil resumed its drop as rising U.S. production and concern over the outlook for the global economy countered a decline in American fuel inventories

- The European Commission slashed its growth forecasts for all the euro region’s major economies from Germany to Italy and warned that Brexit and the slowdown in China threaten to make the outlook even worse

- German industrial output unexpectedly declined for a fourth month in December, feeding concerns that temporary setbacks in Europe’s largest economy may prove more protracted

- India’s central bank unexpectedly cut the benchmark interest rate and dumped its hawkish stance, as slowing inflation allowed policy makers room to support the government in spurring economic growth

Asian equity markets were somewhat mixed with the region cautious following the subdued performance on Wall St, where all majors posted mild losses and the S&P 500 snapped a 5-day win streak. Nikkei 225 (-0.6%) was negative with sentiment dampened by a firmer currency and as participants digested a slew of earnings, although the index was not short of success stories as Mazda was buoyed after an upward revision to guidance and SoftBank surged over 17% on higher profits and the announcement of a JPY 600bln buyback. Elsewhere, KOSPI (Unch) traded indecisively and struggled to maintain the early exuberant tone on return from the Lunar New Year holidays, while ASX 200 (+1.1%) outperformed its peers with broad-based gains as sentiment continued to get a lift from RBA Governor Lowe’s recent dovish shift to a more evenly balanced view on rates. Finally, 10yr JGBS failed to benefit from the risk averse tone in Japan with demand kept subdued amid a similar picture seen in T-notes, while firmer results at today’s 30yr JGB auction were also ineffective in spurring prices. Italy’s industry minister has denied reports that the government will ban China’s Huawei and ZTE from it’s 5G plans; adding that there is no evidence that Huawei presents a threat to national security

Top Asian News

- India’s New Central Bank Chief Delivers Surprise Rate Cut

- Australia Bank Probe Claims Biggest Victim as NAB Chief Quits

- A Rare Hostile Takeover Bid in Japan Signals Changing Times

- Philippines Keeps Key Rate Unchanged as Inflation Nears Target

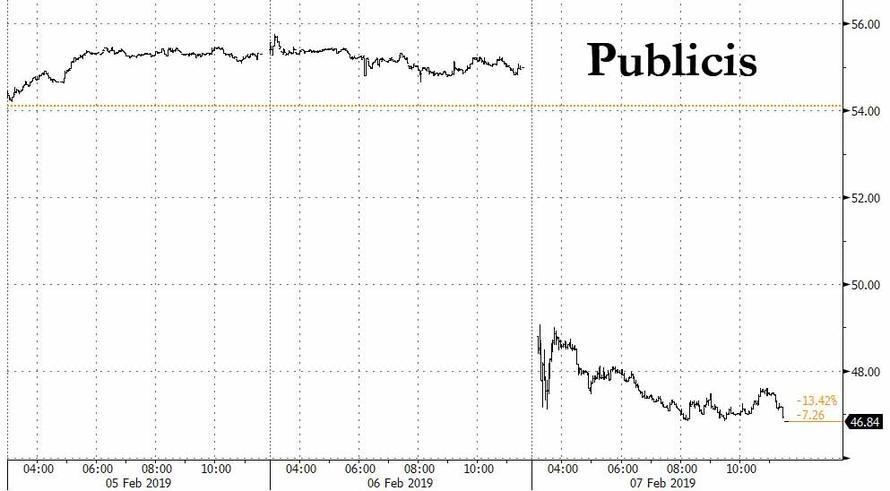

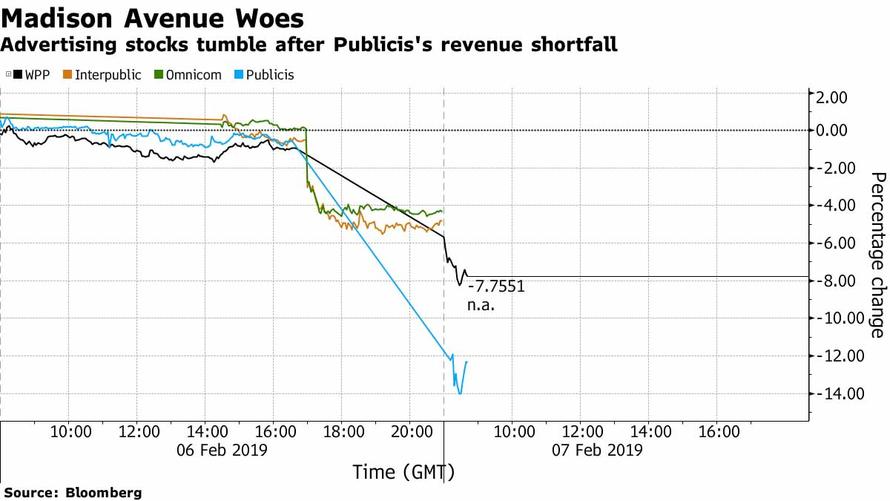

All major European equities kicked off the day in the red [Euro Stoxx 50 -0.8%], taking the lead from the softer performance seen on Wall Street; losses extended as the risk-averse sentiment intensified following the European Commission’s cut to Eurozone GDP and inflation forecasts. The FTSE 100 (-0.1%) is less impacted amid currency effects. Sectors are mixed with some underperformance seen in telecom names and some outperformance in healthcare. Towards the bottom of the Stoxx 600 are Tui (-16.7%) following the Co. cutting profit outlook due to sector headwinds. Separately, Publicis (-12.4%) are down following Q4 revenue growth coming in below expectations; pressuring WPP (-6.2%) and Prosiebensat (-3.1%) in sympathy.

Top European News

- Vestas Expects Margins to Tighten Even as Turbine Sales Grow

- Thomas Cook to Weigh Options for Airline Unit After Losses

- Total Profit Beats Estimates as Output Growth Accelerates

- Norway Wealth Fund Steps Up Voting Against CEO Pay Packages

- European Output Gauges Decline, Feeding Doubts Over Rebound

In FX, the Kiwi has dropped to the bottom of the G10 pile on the back of a relatively bleak NZ jobs report overnight, as employment growth almost dried up in Q4 and the unemployment rate rose more than expected. Nzd/Usd is now hovering around 0.6750 and in danger of testing support just ahead of 0.6700 having lost grip of the 0.6900 and 0.6800 handles in very short order, while the Aud/Nzd cross has snapped back above 1.0500 from close to 1.0400 only yesterday even though the Aussie continues to weaken independently on the RBA shift from a tightening to neutral bias, with Aud/Usd pivoting 0.7100 and edging closer to bids/tech support circa 0.7075.

- EUR/CAD/GBP – All extending losses vs the Greenback as well, and the single currency blighted by more weak Eurozone data, confirmation of downside economic risks via the latest ECB monthly bulletin and GDP/inflation downgrades from the EU Commission. Eur/Usd has now filled bids at 1.1350, with bears targeting the 1.1320 level next for more buying interest ahead of the 30 DMA around 1.1316 before 1.1300. Meanwhile, consolidation in crude prices and a stalling of recent recovery momentum has combined with a change in the technical landscape for the Loonie that has retreated further from recent highs to 1.3250+, and Sterling continues to suffer Brexit-related jitters on top of the overriding Dollar strength (DXY holding firm above 96.500), with Cable testing support just under 1.2900 (namely 1.2895 where 30 and 100 DMAs align).

- JPY/CHF – Relative outperformers and benefiting from their safe-haven appeal as risk sentiment wanes, with Usd/Jpy reversing from another 110.00+ foray and Eur/Chf has retreating further from 1.1400+ even though the Franc remains below par vs the Buck.

In commodities, Brent (-0.5%) and WTI (-0.4%) prices have been choppy but are ultimately in the red, although off of session lows as the impact from yesterday’s EIA data showing production remained unchanged at the record level of 11.9mln BPD dissipated overnight where trade in the complex was largely flat. In recent news flow Libya’s NOC is said to have not ordered the Sharara oil field to be reopened; Libya are reportedly producing 950k BPD of oil. Separately, the TransCanada Keystone oil pipeline was shut due to a potential leak in the Missouri area; however, it was unknown if the leak originated from Keystone. Finally, sources noted that Saudi oil output fell to 10.24mln BPD, below the target level under the OPEC production pact. Gold (Unch) prices are muted and trading within a thin USD 5/oz range, the yellow metal is still above the USD 1300/oz level and continues to move in tandem with the buck. Similarly, London Metal Exchange copper has retreated from the two months high reached in the previous session as the dollar firms and China’s absence due to their holiday continues to impact markets.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 221,000, prior 253,000

- 8:30am: Continuing Claims, est. 1.73m, prior 1.78m

- 9:45am: Bloomberg Consumer Comfort, prior 57.4

- 3pm: Consumer Credit, est. $17.0b, prior $22.1b

DB’s Jim Reid concludes the overnight wrap

We’re in full blown DB research promotion mode at the top here this morning as we have just published a major global growth downside risk analysis, have downgraded our European growth forecasts and have published our latest House View document. We also have a few spaces left at a high profile Brexit panel this afternoon in London to offer up to readers.

Overnight our global economic team published a comprehensive note reviewing the major downside growth risks: trade policy, Brexit, and China. They look at the “tail risk” scenarios for each, reasonably finding that the different shocks would have disparate effects on various regions, though a perfect storm of worst-case outcomes on each front would prompt a very severe downturn. They also downgrade their baseline forecast for euro area growth to +0.9% this year. The full note is available here .

Separately, my House View team published the latest edition of their flagship publication, titled: At the crossroads. They review the global macro outlook, the key themes and risks, and our strategists’ cross-asset forecasts. Overall, there are not major changes to the outlook from the December edition, but many of the major issues impacting growth and markets are set to escalate or be resolved in the next several weeks. The report is available here .

For those that want to know exactly what is going to happen with Brexit, DB is hosting an event later with three high calibre external speakers on UK politics and Brexit. James Forsyth, Political Editor of the Spectator, will help us solve the rubics cube of Conservative Party factions and upcoming Westminster votes. Stephen Bush, Political Editor of the New Statesmen, one of the most plugged in commentators on the Labour Party, will help navigate Jeremy Corbyn’s vision for Brexit and government. Allie Renison, Head of Europe and Trade Policy at the IOD, will help us understand how industry is preparing for no deal, and the EU’s side of talks. DB’s Brexit expert Oli Harvey will moderate. The event starts at 4.45pm in the Deutsche Bank Auditorium, with drinks afterwards with DB Macro Trading. Please register your interest in attending here .

More on Brexit later but in listening to the adverts above you haven’t missed much as this continues to be a quiet week as was expected given the lull in important events. US bourses ended slightly lower last night, with the closing moves for the S&P 500, DOW and NASDAQ being -0.22%, -0.08% and -0.36% respectively. The S&P 500 snapped its run of five straight daily advances, while the dollar notched its fifth straight advance, gaining +0.32%. That was after the STOXX 600 eked our gains of +0.15% in Europe to take its run of successive gains to seven and the most since September-October 2017. Cash HY spreads in Europe and the US were -6bps and -2bps tighter respectively while Treasuries and Bunds ended the day close to flat. So really not much to write home about. To be fair I suspect my wife would be very confused if I wrote home to tell her anything about anything. In fact it seems crazy to think that when I was a student I used to write long flowing letters to old friends, girlfriends and family and then find a letter box to post them. It would be interesting to know the age of the youngest reader who has actually sent regular love letters in the post rather than an email or a WhatsApp. Even phone calls when I was a student were a sign of needless extravagance.

Anyway I digress, in terms of what news we did get yesterday, US Treasury Secretary Mnuchin unsurprisingly reiterated the intention to reach a trade deal with China. He said that “we’re putting in an enormous amount of effort to try to hit this deadline and get a deal.” Elsewhere the US trade deficit data for November was released yesterday, showing a slightly better-than-expected balance at -$49.3 billion. That could mechanically raise fourth quarter growth expectations, but our economists expect it to be balanced out by large imports in December, probably in an effort to front-run tariffs that took effect on January 1. Meanwhile Germany’s soft factory orders data in the morning initially sparked a bit of risk-off with earnings not helping as the day progressed.

Indeed weaker than expected reports from Electronic Arts (-13.31%) and Take Two (-13.76%) seemed to more than overshadow positive snippets from General Motors (+1.58%) and Snap (+21.59%). Microchip Technology (+7.29%) also had a good day after the CEO predicted that we may have seen the bottom in the cycle for the industry. Those remarks helped the broader semiconductor index gain +2.59%, taking it back to near its level of early October.

Over in Europe our equity strategists highlighted overnight that with 30% of companies having reported, Q4 European EPS growth stands at 1% year-on-year, down from the Q3 growth rate of 8%. This is in line with consensus expectations for the companies that have reported. However, EPS growth expectations for the full Q4 earnings season have been marked down from 3% at the start of the season to almost 0% now. Energy, consumer staples and consumer discretionary sectors have seen the biggest upside surprises to earnings, while communication services and technology have seen major disappointments. Click here for the link.

Late last night we heard from Fed Chair Powell and the Fed’s vice chairman for banking supervision Quarles. Powell gave a brief but positive assessment of the economy by saying that “The U.S. economy is now in a good place; at the moment, unemployment is low, prices are near two percent inflation, so we’re in a good place now.” Quarles also gave a similar assessment of the economy by saying that “the outlook is still very solid and the labour market is an extremely solid labour market, and inflation pressures remain muted.” However, Quarles added that global risks represent the most significant risk to the outlook and like the Fed’s Kaplan who provided calendar-based guidance earlier in the week, Quarles went on to say that he will be looking to analyze these risks more over the next 6 months. So, another member to provide a bit more explicit guidance in terms of calendar-based guidance.

In Asia this morning markets are trading mixed with the Nikkei (-0.62%) leading the decline with almost every sector trading lower amidst a slew of earnings releases even as Softbank shares are up as much as +17.54% on the announcement that the company will buy back as much as JPY 600bn ($ 5.5bn) of stock. Meanwhile, the Kospi (-0.03%) is trading flattish post markets re-opening after three days of holiday and the Australia’s ASX (+1.10%) is continuing its move up after yesterday’s surprise shift in policy stance by the RBA. Markets in Hong Kong and China are closed for holidays. Elsewhere, futures on the S&P 500 are down -0.23%. In other news, the US President Trump has nominated senior Treasury official David Malpass to lead the World Bank. In the past, Malpass has been sharply critical of China and has called for a shakeup of the global economic order.

As for Brexit, as we today enter T-50 until March 29th, it was a case of sifting through all the noise again yesterday. The most headline-grabbing comments on Bloomberg was perhaps those from Tusk who didn’t mince his words by saying that there is “a special place in hell for those people who promoted Brexit without any plan for how to deliver it”. This won’t encourage the hard Brexiteers to compromise and will therefore not be seen as helpful. He also confirmed that the EU will make no new offer to PM May and “will not gamble with peace in Ireland or put a sell-by date on reconciliation”. The EC’s Juncker and May are due to meet this morning at 10am GMT however there is little sign of any concessions from either the EU or Ireland to May. What is interesting though is contrasting the Tusk comments to those from Germany. Yesterday Reuters reported that a German government spokesman had said that Germany is “prepared to show creativity on Brexit”. That backs up earlier softer comments from Merkel, albeit comments that seemed to be stretched somewhat in the press. The euro finished -0.39% yesterday.

Staying in Europe, BTPs underperformed (10y +6.6bps) yesterday after the new 30-year deal was confirmed as an €8bn deal which seemed to eclipse expectations for closer to €6-7bn. That said the order book did pass an eye-watering €41bn and therefore eclipsed last month’s demand for shorter bonds. Separately, Italian news agency Ansa reported that the European Commission may downgrade Italy’s 2019 growth forecast to as low as 0.2% in new updates due later today. Our economists are at 0.7%, in line with the consensus private sector forecast. Meanwhile, the IMF in its review of Italian economy said that the annual GDP growth is likely to stay below 1% through 2023 while also adding that the Italian government is falling short on needed reforms for sustainable growth. Finally, Bloomberg reported that the ECB sees no urgency for implementing new TLTROs, which would also be bearish for Italy if true.

In other markets yesterday WTI oil closed +0.50% higher after US data showed smaller-than-expected builds in crude and gasoline inventories. Iron ore rose +0.76% yesterday, as it continues to steal the limelight in commodities post the tragic Brazil dam disaster. The video clips are truly horrifying if you haven’t seen them. Iron ore is up +25.53% this year already and +36.26% from the early-December lows.

Moving on. The main event today should be the BoE meeting. While no change in policy is expected our economists expect the outcome to be a lot more dovish with a material risk (50% chance) that the MPC drop their tightening bias altogether and move to neutral. The rational is: a) significantly weaker domestic survey data pointing to below potential growth b) weaker external conditions c) sizeable downside miss to the BoE’s inflation forecasts. As a minimum the team expect Carney to endorse current market pricing which right now is around 15bps worth of hikes this year. More in their report here .

As for the data that was out yesterday, as highlighted at the top, Germany’s December factory orders data made for fairly bleak reading with orders down -1.6% mom during the month (vs. +0.3% expected). The annual rate weakened to -7.0% yoy as a result which is the weakest since 2012.

Finally to the day ahead, where this morning we’ve got more important data out of Germany with the December industrial production report (+0.8% mom expected). Shortly after we get the December trade balance in France and then January house prices data in the UK. This all comes before the BoE meeting at midday while in the US this afternoon we’ll get the latest weekly initial jobless claims reading – which is worth a watch in light of the big spike to 253k last week (shutdown related or not?) – and then December consumer credit data later this evening. Away from that, the Fed’s Kaplan (2.15pm GMT) and Clarida (2.30pm GMT) are scheduled to speak today while the ECB’s Mersch speaks shortly after midday. The European Commission’s latest forecasts are also out while the earnings highlights are Total, L’Oreal, Sanofi, Twitter and T-Mobile.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED CHINESE NEW YEAR //Hang Sang CLOSED NEW YEAR /The Nikkei closed UP 29.61 PTS OR 0.14%/ Australia’s all ordinaires CLOSED UP 0.39%

/Chinese yuan (ONSHORE) closed DOWN at 6.7422 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 53.60 dollars per barrel for WTI and 62.41 for Brent. Stocks in Europe OPENED RED //.

ONSHORE YUAN CLOSED DOWN AT 6.7422AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7837: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

My goodness, the Clintons are involved with Huawei as the company has deep ties to the former Sec of state Hillary Clinton and President Bill Clinton

(courtesy Dick Morris/WesternJournal.com)

How The Clintons Made Money From Huawei

Authored by Dick Morris, op-ed via WesternJournal.com,

When Meng Wanzhou, the chief financial officer of Huawei Technologies, was arrested in Canada on Dec. 1 through an extradition warrant from the United States, American media described in detail how the company had apparently conspired to evade U.S. sanctions on Iran. (provided by Harvey)

Huawei has long been involved in helping terrorist states and seemingly seeking to thwart U.S. sanctions. Meng is the daughter of Huawei’s founder, Ren Zhengfei.

As details of Huawei’s complicity with Iran emerge, it is time to look back on the Clinton family and its close relationship with Huawei. When their connection was first exposed more than a decade ago, it just seemed like another shady Clinton deal. But now, it becomes clear that Huawei has been central to the Iranian efforts to evade first U.N. and then U.S. sanctions.

The Clintons were apparently conspiring with the enemy.

Huawei has long been a bad actor in undermining U.S. foreign policy. The company has had a deep and long term relationship with the Clinton family.

Huawei and the Clintons’ ties began when Terry McAuliffe, the Clintons’ top fundraiser and future governor of Virginia, bought a Chinese car company – GreenTech Automotive – and moved it to the U.S. in the hopes that it would produce electric cars.

McAuliffe got Huawei to invest in GreenTech through a financing firm called Gulf Coast Funds Management, headed by Hillary’s brother, Tony Rodham. Gulf Coast, boasting the Rodham name, agreed to help Huawei get visas for its top executives under the EB-5 program, which awards visas to those who invest at least $500,000 in the U.S. to create jobs.

The feds had already turned Huawei down because of its links to the Chinese military.

Huawei’s misdeeds are plentiful.

It helped Saddam Hussein install fiber optic cables in violation of U.S. sanctions.

It also helped the Taliban by installing a phone system in Kabul, Afghanistan.

It stole proprietary material from U.S. high-tech company Cisco Systems. This material ended up in Chinese hands.

In 2013, Huawei tried to sell telecom equipment made by Hewlett-Packard to Iran in defiance of sanctions. And, until a few weeks ago, the parent company of Huawei’s Iranian business partner was partly owned by the Islamic Revolutionary Guard Corps, which is playing the key role in Iran’s nuclear program.

According to the South China Morning Post, the U.S. action against Huawei “will severely damage, even cripple, the Chinese company. Of Huawei’s 92 core suppliers, 33 are U.S. corporations, including chip makers Intel, Qualcomm, Broadcom, Marvell and Micron. If Washington now prohibits these companies from selling to Huawei, the Chinese telecoms giant will struggle to survive.”

And, if their full role in the liaison with Huawei comes out, so will Bill and Hillary.

4.EUROPEAN AFFAIRS

UK

Not good for England this morning after the Bank of England slashes its GDP forecast for the year as well as warning of rising BREXIT damage

(courtesy zerohedge)

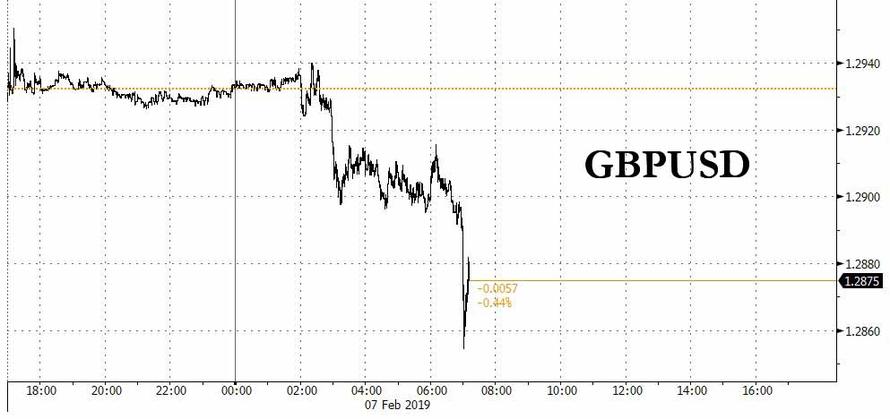

Pound Tumbles After BOE Slashes GDP Forecast, Warns Of Rising Brexit Damage

The Bank of England kept its rates on hold at 0.75%, as expected, in a unanimous decision despite rumors of a hawkish dissenter.

Bank of England

✔@bankofengland

We have kept interest rates at 0.75%. Find out why in our visual summary: https://b-o-e.uk/2HV7rYw #InflationReport

However, the reason why pound plunged following the report is that the central bank joined the Fed and other central banks, in retreating from plans for multiple interest rate rises as it downgraded its economic outlook amid mounting Brexit uncertainty and slowing global growth.

With the March 29 deadline to leave the EU and no Brexit deal yet concluded which has depressed spending and confidence, the BOE said that “uncertainty had intensified,” and now forecasts 1.2% growth this year, down from 1.7% predicted three months ago, the biggest downgrade since the 2016 referendum according to Bloomberg. The global backdrop has also weakened, as highlighted in the European Commission’s sweeping cuts to the euro-area economic outlook on Thursday.

The messaging was clearly negative, even as potential growth offsets the debate around slack in the economy, meaning less growth is required for inflation; so while the report was not unequivocally dovish, the GBP tumbled on the release, with the 10Y gilt now down at 1.1650.

The BOE’s decision follows recent dovish statements from the U.S. Federal Reserve and European Central Bank. U.K. officials noted the impact of China’s slowdown and said trade wasn’t contributing as much to growth as they expected.

The forecasts came alongside the latest policy decision by the Monetary Policy Committee, led by Governor Mark Carney. It voted 9-0 to hold the key interest rate at 0.75 percent, as predicted by all economists in a Bloomberg survey. The bank last lifted the rate in August.

Some details from the report:

- With the final Brexit terms still unresolved, the BOE said that its forecasts would need to be updated “once greater clarity emerged about the nature of EU withdrawal.” Acknowledging the huge impact of uncertainty, it ran an analysis showing that less uncertainty would lead to much stronger growth – 1.6% this year and 2.2% in 2020.

- Assuming a smooth Brexit, policy makers reiterated that limited and gradual rate increases will be necessary. Nevertheless, the forecasts suggested that just one more quarter-point hike would be needed in the next three years to return inflation to close to the 2 percent target, down from almost three hikes seen in November.

- The MPC also cut their prediction for business investment to a 2.75% drop this year, having previously forecast a +2% increase.

- Why Brexit outcomes are so important: On GBP, the MPC highlighted that their forecasts are especially sensitive to moves. A 5% depreciation in GBP would lift inflation to 2.4% percent by the end of 2021, versus 2.1% in the current projections – while a gain of that magnitude would drop the rate to 1.8%.

As a result, investors now see almost no chance of a quarter-point rate move by the end of the year. Furthermore, the BOE bank said that productivity is recovering more slowly than it had thought and that the supply capacity of the economy had shrunk. Officials said that potential supply growth is now a “little below” the 1.5 percent previously estimated.

The report wasn’t uniformly dovish, and in two years, the BOE sees demand outstripping supply, implying some inflationary pressure building in the economy. In the near-term, however, inflation will drop below the BOE’s 2 percent goal due to lower oil prices.

The committee also noted how sensitive its forecasts are to swings in the pound. A 5 percent depreciation in sterling would lift inflation to 2.4% by the end of 2021 versus 2.1% in the current projections, while a gain of that magnitude would drop the rate to 1.8 percent. Judging by today’s GBP drop, more inflation, or rather stagflation, may be in the cards.

France Recalls Ambassador From Italy After “Unprecedented” Verbal Attacks

The diplomatic row between France and Italy is escalating. More than half a year after Italy summoned the French ambassador over Europe’s migrant row, on Thursday France one-upped Italy when it announced it would recall its ambassador to Italy, citing “outrageous” verbal attacks, repeated “meddling” in its domestic affairs and “unacceptable” provocations.

The French foreign ministry said the decision was taken following a meeting between Italy’s deputy prime minister Luigi Di Maio and leaders of the French Yellow Vest protester movement, trumpeting his support for the grassroots protests in defiance of President Emmanuel Macron.

“This is unprecedented since the war,” the foreign ministry said in an emailed statement on Thursday. “Having disagreements is one thing, but using the relationship for electoral purposes is quite another.”

Luigi di Maio, Italy’s Deputy Prime Minister and leader of the anti-establishment 5-Star Movement hailed the “winds of change across the Alps” yesterday on Twitter after meeting with Yellow Vest activists Cristophe Chalencon and Ingrid Levavasseur.

Oggi con @ale_dibattista abbiamo fatto un salto in Francia e abbiamo incontrato il leader dei gilet gialli Cristophe Chalençon e i candidati alle elezioni europee della lista RIC di Ingrid Levavasseur.

Il vento del cambiamento ha valicato le Alpi. pic.twitter.com/G8E0ypLalX— Luigi Di Maio (@luigidimaio) February 5, 2019

“The latest interference is an additional and unacceptable provocation,” according to a statement issued by the Foreign Ministry on Thursday. It added that this “violates the respect that democratically and freely elected governments owe each other.”

“All these acts create a serious situation that questions the intentions of the Italian government” towards France.

A diplomatic feud has been growing between Paris and Rome over repeated expressions of support for the Yellow Vest protests coming from top Italian officials. Di Maio’s co-deputy PM Matteo Salvini said this week that French people “will be able to free themselves from a terrible president” in May after European parliamentary elections take place.

Chalencon and Levavasseur are themselves planning to run in those elections, according to French media reports.

end

Germany/Wirecard

Looks like we have another massive fraud on our hands with respect to German based Wirecard as a whistleblower exposes accounting fraud.

(courtesy zerohedge)

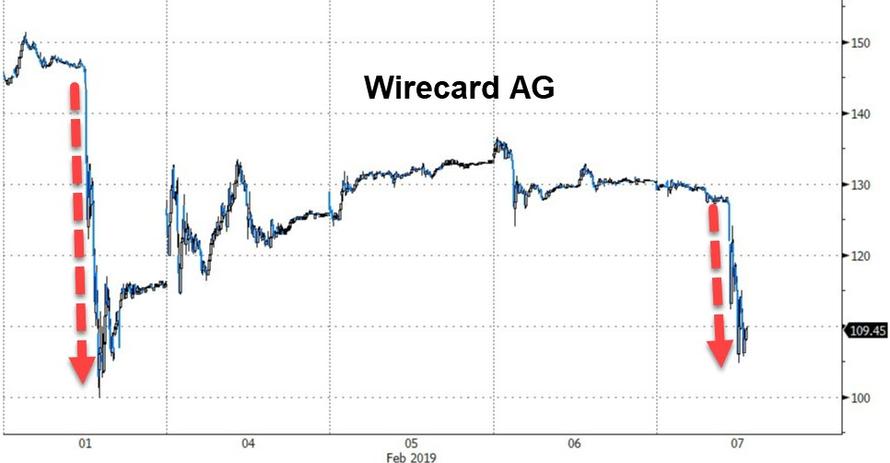

Wirecard Shares Sink As Theranos-Style Whistleblower Exposes Accounting Fraud

Last month, the Financial Times sent shares of German global payments company Wirecard – a market darling which had seen its shares nearly quintuple in a span of less than four years – reeling when it published a story purportedly sourced from company insiders revealing the existence of an internal investigation into widespread accounting fraud. Before the rout was over, Wirecard shares had fallen more than 20%. But analysts backed up the company’s insistence that no wrongdoing had actually taken place, with one calling the report “fake news”.

But refusing to back down, the FT returned on Thursday with another even more extensive story, sourced Theranos-style “whistleblower” company insider who claimed to have been complicit in the alleged fraud. The whistleblower managed to leak a copy of a report compiled by a law firm that examines the alleged malfeasance in great and sometimes stunning detail. And as a result, Wirecard’s shares are moving lower once again.

This time around, investors might find it difficult to ignore the FT’s findings, or find them anything short of compelling. because not only does it cite information from company insiders, but it also includes details from a preliminary report from one of Asia’s top law firms that appear to back up the allegations of wrongdoing. The company, according to the report, committed widespread book-padding as it sought to take over a regional payments business from Citigroup that ultimately granted Wirecard a stretch of territory spanning from New Zealand to India.

The gist is simple: As Wirecard embarked on its quest for globe-spanning domination in the payments space, heads of regional businesses were encouraged to inflate the company’s transaction volume numbers, mainly through the use of a technique referred to by the FT as “round tripping.”

One year ago, Edo Kurniawan, a jovial 33-year-old Indonesian who runs the Asia-Pacific accounting and finance operations for global payments group Wirecard AG, called half a dozen colleagues into a Singapore meeting room. He picked up a whiteboard pen and began to teach them how to cook the books.

His company would soon become one of Germany’s most valuable financial institutions, but as Mr Kurniawan spoke, the immediate task at hand was to create figures that would convince regulators at the Hong Kong Monetary Authority to issue a licence so Wirecard could dole out prepaid bank cards in the Chinese territory.

The group was seeking to take over payment operations from Citigroup, covering 20,000 retailers in 11 countries stretching from India to New Zealand. Regulatory approvals in every territory were crucial, even if it meant inventing numbers to be used in the Hong Kong licence application.

Mr Kurniawan then sketched out a practice known as “round tripping”: a lump of money would leave the bank Wirecard owns in Germany, show its face on the balance sheet of a dormant subsidiary in Hong Kong, depart to sit momentarily in the books of an external “customer”, then travel back to Wirecard in India, where it would look to local auditors like legitimate business revenue.

The practice, according to the report cited by the FT, was used to appease regulators throughout Asia, which suggests that the fraud wasn’t merely the work of one rogue employee.

In isolation, Mr Kurniawan’s scheme might have appeared to be the act of a rogue employee in the provincial outpost of a little known financial group. But the account of what happened, in a preliminary report on the investigation by one of Asia’s most eminent legal firms, indicated it was part of a pattern of book-padding across Wirecard’s Asian operations over several years. Documents seen by the Financial Times show two senior executives in the Munich head office had at least some awareness of the round-tripping scheme: Thorsten Holten and Stephan von Erffa, respectively the company’s head of treasury and head of accounting.

The revelations call into question the figures reported by one of Europe’s few technological success stories, a German fintech group that has grown into a €20bn global payments institution. Before the FT exposed the existence of the investigation last week, the group was more valuable than Deutsche Bank or Commerzbank, whose place it has taken in Germany’s main stock market index. Wirecard is a favourite of retail investors, who saw its rapid expansion into Asia as a sign that it can challenge the world’s biggest banks for primacy in the $1.4tn market for payments.

The “whistleblower” who spoke with the FT helped initiate the internal probe after finding the brazenness of one of the company’s regional managers, who had called a meeting to explain to employees how the fraud would be carried out, almost too shocking to be believed.

This time questions about its Asian operations began internally, prompted by a whistleblower left stunned by Mr Kurniawan’s January meeting last year. Notifying Wirecard’s senior legal counsel in the region on March 26, the whistleblower identified two senior finance executives, James Wardhana and Irene Chai, as accomplices in the book-cooking operation. A separate whistleblower also raised concerns in February, and on April 3 that person supplied the compliance team with a suspect contract they had received via Telegram, the encrypted messaging app. Daniel Steinhoff, Wirecard’s head of compliance in Munich, flew in to Singapore for a briefing. On April 13 he ordered the email archives of these individuals “mirrored”, with copies seized. Compliance staff, who evidently found the accounts of the whistleblowers credible, soon found enough in the documents to warrant a snap investigation, codenamed Project Tiger. They called in Singapore-based Rajah & Tann, which sent in a team of former prosecutors.

Eventually, much of the behavior that the whistleblower had complained about was borne out by the report, including “forgery and/or falsification” as well as “cheating, criminal breach of trust, corruption and/or money laundering.”

On May 4 R&T submitted a preliminary report, running to 30 pages of bombshell allegations:evidence in the documents of “forgery and/or of falsification of accounts”, as well as reasons to suspect “cheating, criminal breach of trust, corruption and/or money laundering” in multiple jurisdictions. The trio in Singapore, led by Mr Kurniawan, appears to have been fabricating invoices and agreements to create a paper trail which could be shown to auditors at EY, as if money was moving in and out of Wirecard for legitimate purposes.

And in what was undoubtedly a bad look for the company’s top brass, once the investigation got rolling, the company’s top brass installed a senior employee who had allegedly been involved in some of the fraudulent activities to help oversee the probe, inviting comparisons to the “fox guarding the hen house.”

A briefing document dated May 7 2018 was prepared for a meeting of Wirecard’s four most senior executives. Alexander von Knoop, chief financial officer, thanked the author in an email following the meeting “for the great job you are doing to clarify the circumstances and to prevent Wirecard Group from any financial and reputational damage”. The email also announced that Jan Marsalek, Wirecard’s chief operating officer, had been appointed to co-ordinate the inquiry, “to get the necessary pressure on the investigation”, Mr von Knoop said.

[…]

Wirecard’s lawyers in Singapore warned Mr Marsalek’s proposed role presented “a perceived and potential conflict of interest.” He was a material witness of fact who had worked closely with Mr Kurniawan on certain projects, they said.

To sum up, to call Thursday’s FT report “damning” would be an understatement. It suggests that managers throughout the company’s vast global network brazenly and blithely invented money flows and even in some cases fake customers to back them up. The company also reportedly violated AML reporting guidelines. Taken together, the fraud calls into questions not just Wirecard’s recent earnings results, but the very perception of WireCard as one of the Continent’s most successful fintech startups.

Which begs the question: When this is all said and done, will Wirecard be remembered as Germany’s “Theranos?” As the whistleblower put it: “If a payments company can do this, how can we trust the system?”

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

A global crash is coming: the entire world’s economies are entering contraction/crisis

(courtesy Graham Summers/Phoenix Research Capital)

This Is Your Final Warning Before Things Get UGLY

The next leg down is officially here.

The big picture story for the markets is that the US/China trade deal is no longer important. Even if the two nations did agree on a perfect deal that resolves the structural issues between their economies (highly improbable), the fact is that the global credit cycle has turned and we are entering a contraction/ crisis.

Europe is now officially weakening with most major economies (Germany, France, Italy and Spain) approaching, if not already in, recessions.

The market is fully aware of this. The German DAX has ended its bull market from the 2009 low. This latest rally is a pathetic dead cat bounce in the context of a larger bear market.

The situation is even worse in China. There we have the beginning of complete systemic collapse as the largest pile of garbage debt/ financial fraud finally blows up. China spends $25 in debt for every $1 in GDP growth. And its economy is growing, at best, by 2% per year.

The market similarly knows this which is why China has broken in 20+ year bull market trendline. The Chinese stock market has been in a series of successive bubbles followed by spectacular crashes for the last two decades. This time around, the Crash will be something truly astonishing to behold.

This leaves the US, where despite all the fanfare, the economy is almost certainly contracting if not already in a full-blown recession.

Maxing out your credit card is very different from getting a raise. What’s happened in the US in the last two years is the country maxing out its credit card on a personal, state, and national level.

Here again the market knows this, which is why we’ve broken the bull market trendline from the 2009 lows. The ultimate downside for this collapse is at best 2,000, and more likely than not we’ll go to the high 1,000s (think 1,750-1,800).

A Crash is coming…

end

Another indicator of a global slowdown: Advertising giant Publicis, suffers an historic rout as USA consumer brand spending tumbles

(courtesy zero hedge)

Ad Industry Suffers Historic Rout As US Consumer Brand Spending Tumbles