GOLD: $1301.75 DOWN $5.15 (COMEX TO COMEX CLOSING)

Silver: $15.33 DOWN 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1313.70

silver: $15.48

Comex options expire next week: Wednesday March 27

London/LBMA expires Monday March 31/2019.

The crooks continue with their whacking right in front of the authorities/regulators despite the criminal probe of precious metals manipulations.

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 20 NOTICE(S) FOR 2000 OZ (0.0622 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 382 NOTICES FOR 38200 OZ (1.881 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

20 NOTICE(S) FILED TODAY FOR 100,000 OZ/

total number of notices filed so far this month: 5323 for 26,615,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4012:DOWN $5

Bitcoin: FINAL EVENING TRADE: $4029 UP 13

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 2/20

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,305.000000000 USD

INTENT DATE: 03/19/2019 DELIVERY DATE: 03/21/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 2 6

661 C JP MORGAN 15 2

685 C RJ OBRIEN 2

737 C ADVANTAGE 3 7

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 20 20

MONTH TO DATE: 382

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FINALLY STOPS ITS DESCENT AND ROSE FOR THE SECOND TIME THIS WEEK: , THIS TIME BY A CONSIDERABLE SIZED 980 CONTRACTS FROM 187,144 UP TO 189,124 WITH YESTERDAY’S 6 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 968 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 968 CONTRACTS. WITH THE TRANSFER OF 968 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 968 EFP CONTRACTS TRANSLATES INTO 4.84 MILLION OZ ACCOMPANYING:

1.THE 6 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 26.935 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

28,607 CONTRACTS (FOR 14 TRADING DAYS TOTAL 28,607 CONTRACTS) OR 143.035 MILLION OZ: (AVERAGE PER DAY: 2043 CONTRACTS OR 10.216 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 143.035 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 20.42% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 508.42 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 980 WITH THE 6 CENT RISE IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 968 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 2948 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 968 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1980 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 6 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $15.37 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.936 BILLION OZ TO BE EXACT or 134% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 20 NOTICE(S) FOR 100,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 26.935 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST SURPRISINGLY AGAIN FELL BY 3,179 CONTRACTS DOWN TO 514,163 DESPITE THE GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $4.60//YESTERDAY’S TRADING). ON MONDAY I STATED THIS: “EITHER WE HAD A MASSIVE SHORT COVERING OR THE SPREADERS STARTED TO LIQUIDATE A LITTLE EARLIER THAN USUAL” I AM NOW CONVINCED THAT THE SPREADERS HAVE STARTED THEIR LIQUIDATION EARLIER THAN USUAL. YOU WILL RECALL THAT THEY USUALLY LIQUIDATE A CONSIDERABLE AMOUNT OF THEIR OPEN INTEREST ONE WEEK PRIOR TO THE FIRST DAY NOTICE OF AN ACTIVE MONTH. SOMEHOW THEY HAVE DECIDED TO START TWO WEEKS BEFORE FIRST DAY NOTICE. SOMETHING SINISTER IS GOING ON BEHIND THE SCENES!!~

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2173 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 2173 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 514,163. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE. FOR THE THIRD DAY IN A ROW, A FAIR SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1006 CONTRACTS: 3,179 OI CONTRACTS DECREASED AT THE COMEX AND 2173 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 1006 CONTRACTS OR 100,600 OR 3.129 TONNES.

YESTERDAY WE HAD A GAIN IN THE PRICE OF GOLD TO THE TUNE OF $4.60....AND WITH THAT, WE HAD A LOSS IN TONNAGE OF 3.129 TONNES?????!!!!!!.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 91137 CONTRACTS OR 9,113,700 OZ OR 283.47 TONNES (14 TRADING DAYS AND THUS AVERAGING: 6509 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAYS IN TONNES: 283.47 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 283.47/2550 x 100% TONNES = 11.11% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1152.46 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED SIZED DECREASE IN OI AT THE COMEX OF 3179 DESPITE THE STRONG GAIN IN PRICING ($4.60) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 2173 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 2173 EFP CONTRACTS ISSUED, WE HAD A FAIR LOSS OF 652 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

2173 CONTRACTS MOVE TO LONDON AND 3179 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 3.129 TONNES). ..AND ALL OF THIS DROP IN DEMAND OCCURRED WITH A RISE OF $4.60 IN YESTERDAY’S TRADING AT THE COMEX???????!!!!!

we had: 20 notice(s) filed upon for 2000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $5.15 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD/

INVENTORY RESTS AT 778.09 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 4 CENTS IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 310.848 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 1980 CONTRACTS from 187,144 UPTO 189,124 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 968 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 968 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2166 CONTRACTS TO THE 968 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 2948 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 14.74 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 26.935 MILLION OZ FOR MARCH.

RESULT: A CONSIDERABLE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 6 CENT RISE IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 968 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 0.34 POINTS OR 0.01% //Hang Sang CLOSED DOWN 145.31 POINTS OR 0.49% /The Nikkei closed UP 42.07 POINTS OR 0.20%/ Australia’s all ordinaires CLOSED DOWN .40%

/Chinese yuan (ONSHORE) closed UP at 6.6944 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 58.40 dollars per barrel for WTI and 67/28 for Brent. Stocks in Europe OPENED RED

ONSHORE YUAN CLOSED UP // LAST AT 6.6944 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6972 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

i

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/

b) REPORT ON JAPAN

3 C/ CHINA

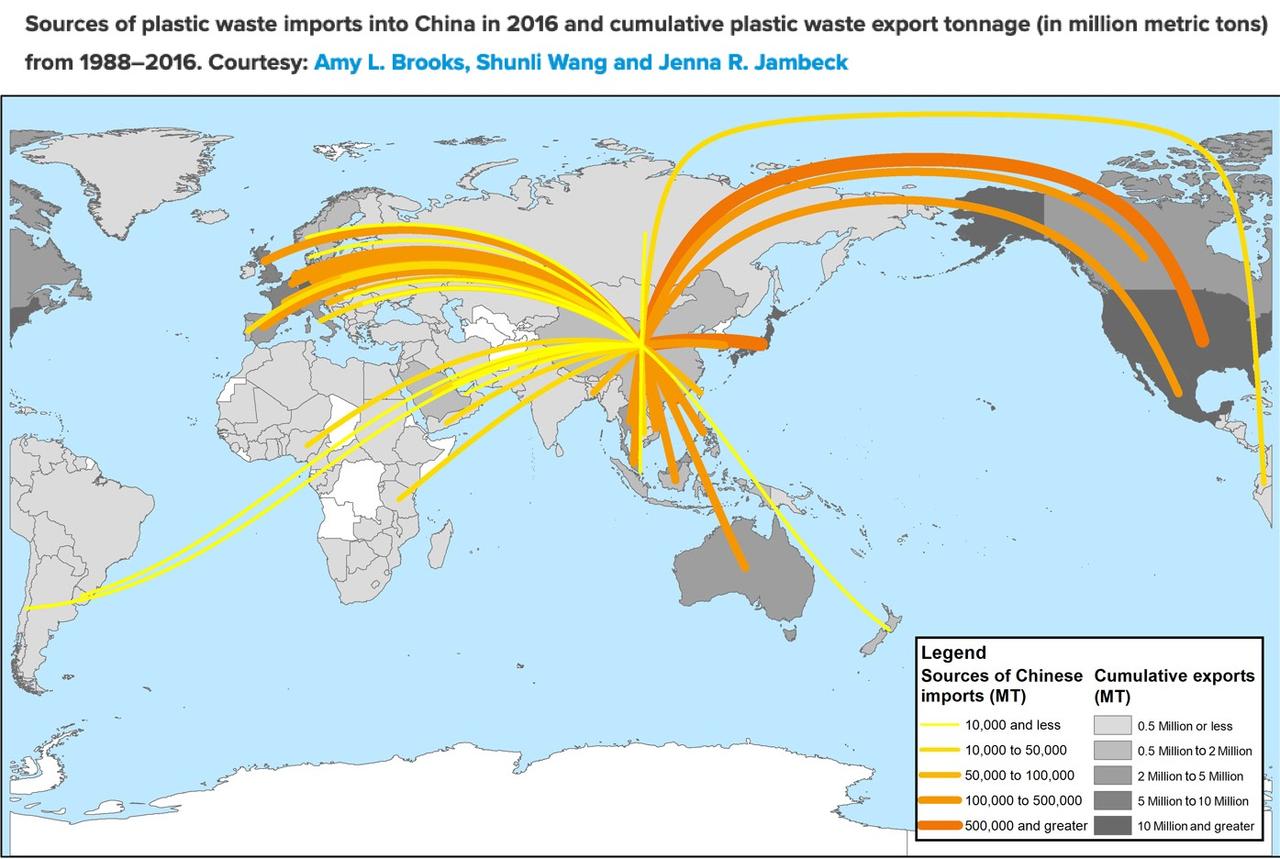

i)China halts the plastic waste of the USA as we warned you that this was going to happen . Now the uSA has no place to send all of its plastic waste

( zerohedge)

4/EUROPEAN AFFAIRS

i) Switzerland/UBS:

Oh OH! this is something that we must pay attention to: UBS warns that its first quarter is one of the worst in recent history. Its banking revenue implodes

( zerohedge)

ii)UK

Embattled May states that she will not seek a long delay in the Brexit proceedings: the pound slides ealry this morning

(courtesy zerohedge)

iii)The pound drops further as MP’s are furious. May requests a Brexit extension. The EU will only give a long extension something that the UK does not want. It is a mess..

(courtesy zerohedge)

iv)GERMANY:

Bayer AG, a former stalwart on the German /uSA stock exchanges suffered a major blow from its second trial on weed killer Roundup

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

i)BOEING

The following should give the authorities enough clues as to what happened on both of the crashes of those Boeing 737 Max 8

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Venezuela

the USA has now allowed the Venezuelan opposition to seize diplomatic properties in the USA. However there is still not enough support inside Venezuela for a takeover of power.

(courtesy zerohedge)

9. PHYSICAL MARKETS

( zerohedge)

ii)The USA imposed sanctions on Venezuela’s state owned gold mining operation Minerven and its president, Perdomo

(courtesy Reuters/GATA)

iii)Hugo comments that the road for the dollar will not be pretty: a steady devaluation

( Hugo Salinas Price)

iv)Craig Hemeke describes the dilemma facing the Fed as it tries to pare its balance sheet and raise rates

( Craig Hemke)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

END

ii)Market data

ii)USA ECONOMIC/GENERAL STORIES

a)the USA cancelled 362,000 passports last year over supposed back taxes. The government does not have to prove that you owe the taxes.

Simon Black states that it is now a good idea to have a second passport

(Simon Black/Sovereign Man)

b)Unusual sun behaviour and a shift in the magnetic pole seems to have caused crazy weather patterns throughout the USA. Nebraska flooding has broken 17 records and many states has seen huge amounts of snow

d).Boeing tumbles after the FBI joins into the 737 Max approva(courtesy zerohedge)

iv)SWAMP STORIES

b)More documents will be released which shows that there have been USA ambassadors who conspired with the DOJ to bring down Trump. This document will be released shortly

(courtesy zerohedge)

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL ROSE TO 818 CONTRACTS FOR A GAIN OF 12 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ROSE BY 1093 CONTRACTS UP TO 1360729 CONTRACTS. TODAY THE BANKERS TOOK A LITTLE BREATHER WITH RESPECT TO QUEUE JUMPING..MAYBE THEY JUST COULD NOT FIND ANY PHYSICAL METAL AT THE SILVER COMEX…

5 Ways to Prosper In the Coming Crisis – Goldnomics Podcast

Topics considered are

– Political, financial, economic and monetary systems are failing and will likely collapse

– Our human built economic systems are dependent on the environment of the planet which is threatened

– Medical, religious and other beliefs and paradigms are being questioned and in crisis

– In the age of information, old systems are collapsing as we enter a new era of consciousness

– Read, learn, develop skills and grow yourself in order to be a contribution to your family, company and community

– Mental, emotional and physical health is wealth

GoldCore Exclusive Offer

For the next 30 days when you buy a minimum of 10,000 ($,€,£) in physical gold and silver for storage in Zurich, you will benefit from Free Secure Storage on this investment for 6 months along with other valuable bonus gifts. Access key information here

News and Commentary

Gold prices slip as dollar firms ahead of Fed decision (Reuters.com)

Canada Lifts Bond Borrowing Ahead of Election (Bloomberg.com)

U.S. Sees China Trade Pushback as Trump Touts Progress (Bloomberg.com)

China banks face huge capital hole as stimulus spurs lending (Twitter.com)

Is The World Running Out Of Gold? (DW.com)

Gold and Silver Will Head to New Highs (Youtube.com)

A Recession Is Coming, And Maybe a Bear Market, Too (Bloomberg.com)

Market Cycles Signal Imminent “Collision Between Reality & Widespread Fantasy” (ZeroHedge.com)

The Pentagon’s Missing Trillions: What You Need to Know (Youtube.com)

Ireland’s Dunnes-loving, cheese-eating unsqueezed middle (DavidMCWilliams.ie)

How Asset Inflation Will End — This Time (Mises.org)

Gold Prices (LBMA PM)

19 Mar: USD 1,308.35, GBP 985.06 & EUR 1,152.53 per ounce

18 Mar: USD 1,305.35, GBP 986.19 & EUR 1,150.01 per ounce

15 Mar: USD 1,302.35, GBP 981.55 & EUR 1,150.55 per ounce

14 Mar: USD 1,299.20, GBP 982.84 & EUR 1,148.88 per ounce

13 Mar: USD 1,308.40, GBP 994.25 & EUR 1,158.20 per ounce

12 Mar: USD 1,296.95, GBP 986.85 & EUR 1,150.78 per ounce

Silver Prices (LBMA)

19 Mar: USD 15.41, GBP 11.61 & EUR 13.57 per ounce

18 Mar: USD 15.38, GBP 11.60 & EUR 13.54 per ounce

15 Mar: USD 15.35, GBP 11.58 & EUR 13.56 per ounce

14 Mar: USD 15.23, GBP 11.52 & EUR 13.48 per ounce

13 Mar: USD 15.52, GBP 11.80 & EUR 13.73 per ounce

12 Mar: USD 15.44, GBP 11.83 & EUR 13.72 per ounce

Recent Market Updates

– Deutsche Bank and Commerzbank May Become EU’s “Too Big To Fail” Bank

– Happy Saint Patrick’s Day from GoldCore

– 188 Internet Shutdowns In 2018 Show Why Physical Gold Is Ultimate Protection

– Buy Gold as Basel III Means “Central Banks and Banks Are Going To Be Buying Gold”

– Invest In Gold Or Bitcoin – Which Is The True Store Of Value?

– Silver Bullion Is The Portfolio Insurance To Buy Now

– EU Isn’t Ready for the Next Recession

– JPMorgan Is Bullish on Gold as a Hedge Against Rising Inflation

– Gold – It Might Be Different This Time

(COURTESY ZEROHEDGE)

Gold Tumbles Back Below $1300 As Someone Suddenly Dumps $1 Billion Of ‘Precious Paper’

As Europe closed, it seems someone decided now was a great opportunity to puke over $1 billion notional of paper gold into the futures market to send the precious metal back below the key $1300 level…

Huge volume spike…

Spot gold broke back below its 50DMA…

Well it is Fed Day after all.

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

This is something that we have been telling you. We have already reached peak gold production as most of the major mines have already been found

(courtesy zerohedge)

A shortage of gold? Only at such a low price

Submitted by cpowell on Tue, 2019-03-19 15:14. Section: Daily Dispatches

Is the World Running Out of Gold?

From Deutsche Welle

Bonn, Germany

Tuesday, March 19, 2019

The murmurs that the world is running out of gold deposits have grown louder in the past two years.

Several experts and industry magnates, including Canadian miner Goldcorp’s chairman, Ian Telfer, have forecast a perpetual decline in gold production from its current peak.

Gold production reaching its peak levels is nothing new. The production of the yellow metal has reached its highest levels on at least four occasions in the past before witnessing sharp declines.

…

But many say there is something that makes the current gold peak stand out: There is simply no new major gold deposit left to be discovered.

“The largest and most prolific reserves have already been found,” Matthew Miller, an analyst at CFRA Research, told Deutsche Welle. “Gold miners are struggling to grow reserves in line with their production.” …

“The gold miners realize that the prices of companies are at such attractive levels that it’s cheaper to buy gold in the stock market than it is to explore for it,” John Ing, a mining analyst at Maison Placements Canada, told DW. …

“Finding gold is a function of the gold price,” Ing said. “There is no shortage of gold in the world but just at this price there is a shortage. It’s quite possible that gold will be $2,000 per ounce. Then you will see a rush of exploration and more deposits being found.” …

… For the remainder of the report:

https://www.dw.com/en/is-the-world-running-out-of-gold/a-47974833

END

The USA imposed sanctions on Venezuela’s state owned gold mining operation Minerven and its president, Perdomo

(courtesy Reuters/GATA)

U.S. Treasury seems to consider gold to be money after all

Submitted by cpowell on Wed, 2019-03-20 02:22. Section: Daily Dispatches

U.S. Sanctions Venezuela’s Government-Owned Gold-Mining Company for Backing Maduro

By Lesley Wroughton, Susan Heavey, and Doina Chiacu

Reuters

Tuesday, March 19, 2019

WASHINGTON — The United States imposed sanctions on Tuesday against Venezuela’s state-run gold mining company Minerven and its president, Adrian Perdomo, accusing them of illicit operations and propping up the government of President Nicolas Maduro.

The announcement comes days after Uganda said it was investigating its biggest gold refinery for importing Venezuelan gold. Washington has imposed half a dozen rounds of sanctions against Maduro and senior Venezuelan officials as it tries to choke off funding to the government. It has warned gold traders not to deal in Venezuelan gold or oil.

…

Treasury is targeting gold processor Minerven and its president for propping up the inner circle of the corrupt Maduro regime,” U.S. Treasury Secretary Steven Mnuchin said in a statement. …

… For the remainder of the report:

https://www.reuters.com/article/us-venezuela-politics-usa-sanctions/u-s-…

* * *

Join GATA here:

Mining Investment Asia

Marina Bay Sands Conference and Exhibition Center

Singapore

Tuesday-Thursday, March 26-28

https://www.mininginvestmentasia.com/

Mines and Money Asia

Hong Kong Conference and Exhibition Center

Wan Chai, Hong Kong

Tuesday-Thursday, April 2-4

https://asia.minesandmoney.com/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Hugo comments that the road for the dollar will not be pretty: a steady devaluation

(courtesy Hugo Salinas Price)

Hugo Salinas Price: The road ahead for the dollar will be like the road behind

Submitted by cpowell on Wed, 2019-03-20 02:33. Section: Daily Dispatches

9:34a ICT Wednesday, March 20, 2019

Dear Friend of GATA and Gold:

Hugo Salinas Price of the Mexican Civic Association for Silver forecasts this week the future of the U.S. dollar by reviewing its history of steady devaluation.

Salinas Price writes: “The Federal Reserve is in box. It has boxed itself into an insoluble problem. It cannot stop creating more credit, expanding its balance sheet, no matter what Jerome Powell, chairman of the Fed, may say he is doing or going to do. To stop creating more Federal Reserve dollars means only one thing — total collapse of the whole humongous Federal Reserve dollar scheme.”

Salinas Price’s commentary is headlined “The Road Ahead for the Dollar” and it’s posted at the association’s internet site, Plata.com, here:

http://plata.com.mx/enUS/More/374?idioma=2

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Bill King:

overnight stock futures have been manipulated upward for years. No surprise here!

(courtesy King/Ramsey/GATA)

King Report: Overnight stock futures have been manipulated upward for years

Submitted by cpowell on Wed, 2019-03-20 02:56. Section: Daily Dispatches

By Bill King

The King Report

M. Ramsey King Securities, Burr Ridge, Illinois

Wednesday, March 20, 2019

https://mramseyking.com/king-report

Once again someone juiced E-Mini S&P Index futures (ESMs) during early European trading Tuesday. The manipulation of ESMs during the wee hours in the U.S. creates the psychology that induces other traders, particularly the momentum investors, to get long for the coming session.

There is a long pattern going back to the 1990s of overnight manipulation of S&P 500 futures to arrest negative sentiment and create a cycle of equity buying that spreads from Europe to the U.S.

…

The overnight manipulation became so blatant that saner angels would check to see which firms were “fooling” around with the S&P futures on Globex during off-session trading. Manipulators then pressured the powers that be not to disclose the identity of the firms that were trading the futures. The secrecy continues to this day.

The ESM manipulation commenced during the second hour of European trading. ESMs rallied 11 handles within two hours. But that was the top. From 6:53 a.m. ET until the European close, ESMs gyrated wildly with a downward bias until someone juiced ESMs for the European close. …

It is crystal clear that someone, probably from Team Mnuchin, keeps leaking positive U.S.-China trade stories to The Wall Street Journal. It is evident that the leaks are intended to boost stock prices. Qui bono? …

end

LAWRIE WILLIAMS: Palladium and Rhodium prices soar on strong fundamentals

Palladium plus a very small amount of rhodium are the principal catalytic metals nowadays for use in petrol (gasoline) fuelled internal combustion engine exhaust anti-pollution systems and both are suffering from supply shortages which have been boosting prices. Indeed palladium keeps hitting new highs and is heading up towards double the price of platinum which used to be far more expensive than the former and was, some years ago, itself the primary catalyst in petrol engine exhaust cleaning systems. Palladium used also to be far less costly than gold, but currently command a premium of over 205 above the yellow metal.

When platinum was far more expensive than palladium this led to the research which saw platinum replaced by palladium as the dominant catalyst in exhaust emission controls for petrol engines. Thus we have to ask is it now possible that the reverse will occur and the auto industry generate a switch back to platinum as the principal catalyst in emission controls for both diesel engines (where it is still dominant) and for petrol engines too?

If the auto industry and catalytic exhaust system manufacturers see the current price differential as persisting we think there is a good chance that this could happen given the platinum market remains in substantial surplus and palladium and rhodium in deficit. But if this does happen it will take time for the catalyst manufacturers to prove up a replacement system and switch over. Probably a couple of years at least, over which time the catalyst manufacturers would have to make a judgement call that the pricing parameters for the two metals won’t reverse yet again. Historically platinum has commanded a good price premium over palladium and there’s obviously no guarantee that this will not re-occur at some stage in the future.

The principal difference now is that it is already known that platinum-base catalysts work as being effective in cleaning pollutants from petrol engine exhausts whereas prior to its substitution with palladium the latter’s catalytic properties in the process were, to a major extent, unknown, so much basic research had to be undertaken before the switch was made. Arguably, since then, continuing use and research has meant that the palladium/rhodium catalyst combination is more efficient at cleaning petrol engine exhausts than the old platinum catalysts. But if a similar amount of research is put into regeneration of platinum as a petrol engine exhaust catalyst, perhaps in combination with rhodium or some other metal, there has to be a reasonable possibility that platinum could again become the dominant catalytic metal for all types of internal combustion engine.

Should the above occur then the big platinum surpluses could soon disappear and the palladium deficit be reduced or eliminated altogether, but then the price differences between the two metals could fall away, or be reversed, which represents a balancing act equation for the catalyst and auto manufacturers to take into account. The longer palladium maintains the current kind of substantial price premium over platinum, the more this reverse substitution process is likely to come about.

The writer’s view is that probably the research to see if platinum-based exhaust control catalysts are capable of meeting today’s more rigorous anti-pollution standards will already be under way. But, because of the potential for the pricing differential between platinum and palladium to be eliminated, or reversed the likelihood is that there may well be a place for both metals in future catalytic systems for petrol driven internal combustion engines which could bring prices back nearer equality – positive for platinum and negative for palladium.

Precious metals consultancy, Metals Focus, certainly sees the strength in the palladium price continuing this year and sees it overtaking $1,700. Indeed it is already getting close reaching over $1,600 at one time yesterday. It sees potential supply disruption ahead for all the pgms in the world’s largest producer, South Africa, which dominates platinum production and is probably the second largest producer of palladium after Russia The consultancy thus notes, in its latest weekly newsletter: “With regard to the 2019 price outlook, we therefore expect palladium to generate further upside, surpassing $1,700 before year-end. On the supply side, risks of industrial action in South Africa (as wage negotiations get underway in the PGM market) are likely to have a far greater impact in the palladium market, compared with platinum. With respect to palladium demand, relatively weak Chinese light vehicle sales will be offset by tighter emissions legislation, resulting in a new high for global palladium automotive demand.”

Russia has added to the supply worries as it is reported as saying that it will stop the export of precious metals scrap and tailings from May to September this year. Given that palladium and rhodium supplies appear to be in deficit, this decision will affect the prices of these two metals the most.

Overhanging all this, though, will be the growth in the uptake of electric, hybrid electric/petrol and fuel cell vehicles which is perhaps advancing faster than analysts have been anticipating. This growth is likely to accelerate with more and more countries and cities planning to ban sales of, or access by, internal combustion engine cars at some point in the future and as ever-continuing research expands electric vehicle (EV) battery life, speeds up charging and leads to more and more charging points becoming available thus eliminating, or substantially reducing, range anxiety. Virtually all major car manufacturers are developing electric vehicles and it may not be long before these dominate the new vehicle markets as greener credentials become the norm rather than the exception. At this point the price differential between platinum and palladium will become an irrelevance unless new uses can be found for the metals and the prices for both metals could be decimated. This may not occur for some years yet, but we wouldn’t like to bet on the ultra long term survival of the internal combustion engine as the principal power unit for land- based transportation systems.

20 Mar 2019

-END-

Central Banks Going Long Gold – Andrew Maguire

By Greg Hunter On March 20, 2019

World renowned precious metals expert Andrew Maguire says pay attention to the new rule that goes into effect at the end of March that will allow gold to become fully valued and monetized as a tier 1 asset for banks around the world. Maguire explains, “Basel III is coming into effect in less than two weeks from now, and it will effectively remonetize physical gold. Of course, that is a big deal. While the synthetic players shuffle chips in this siloed CME casino, the insider bullion banks are positioning for higher gold prices. That is it right there. Bottom line is what are the big boys doing?”

So, is it safe to say central banks and big banks are going long gold? Maguire says, “They’re all going long gold. Why is that? It is because they are already allocating gold for their own house accounts. . . . The minute the global physical markets see unallocated positions are being mark to market at a certain price, the physical market will explode. There will be a gap higher, and the offer to sell physical will rise to a point where someone is actually willing to sell it. . . . I think you are going to see in a few days that it will suit the bullion banks to have a higher price than a lower price. . . . At some point, they are going to want a higher price, and we all know why. There are trillions of dollars of derivatives and unbacked zero value intrinsic assets out there in the market place, and someone has to settle this stuff. It is not going to be settled without a much higher gold price.”

Maguire goes on to say, “Look at platinum, it’s a vertical rise. What is that? That is a physically driven short squeeze. People look at it and say it must be speculation. It’s not speculation. It was a massive short position just like in silver and just like in gold, but more so in silver. What we are seeing is a relentless drive to cover. We are going to see a similar situation (in gold and silver). What is that price? You are already seeing that with the LBMA projecting $1,530 per ounce in gold for this year. . . . It amazes me that people are not seeing this massive tectonic event. It’s going to be a shock, but I think it is part of a central plan move to revalue gold. It has to.”

Maguire says watch silver for an extreme spike to the upside. Maguire says, “Silver is going to break out. I think $50 per ounce is a joke. I think it’s going to be substantially higher than that. It’s not going to be a question of how you can run into resistance with silver. It’s going to be how much physical is available. It’s going to be a heck of a lot higher when you start to have a run on the price.”

Join Greg Hunter as he goes One-on-One with precious metals expert Andrew Maguire.

-END-

Good Morning Bill/Harvey (from a Johannesburg that is facing devastation-more on that later)

I had an affinity with the podcast of Lawrence Lepard in yesterday’s Midas. He confessed that one of his errors was to underestimate the immense combined power and resources of all the satanic globalized forces that conspire to suppress the price of gold. This has been the Achilles ’ heel of GATA’s arguments for so long and the flaw in the seminal research of Frank Veneroso. In respect of any excitement concerning the imminent advent of29th March 2019 as being a significant date in respect of the emancipation of physical gold, this assumption is not well founded at all. The advisory framework of BASEL III did indeed elevate gold to a tier one asset status on 1st January 2019 but simultaneously de-emphasized the attractiveness of gold in both the LCR (Liquidity Coverage Ratio) and NSFR (Net Stable Funding Ratio) bases of computations. The only significance of 29th March 2019 would be that it is the last working day of the 1st quarter of 2019, and many regulatory returns are based on quarter end data. Any bank seeking to report physical gold on its balance sheet at the end of the first quarter would have presumably engaged in this acquisition process throughout the first quarter (or maybe for a longer period) so we would have already witnessed most of the impact on the physical gold market. It, may, however, take many years for individual sovereign regulators to incorporate various selective aspects of the BASEL III advisory framework into their own regulatory templates, so the 29th March 2019 is one big nothing burger in this regard.

Johannesburg (indeed the whole of South Africa) is probably out looking in the near future a situation of 4 hours of Eskom power and then four hours of load shedding on a serial basis for several years-probably eternity. Only a few years after the end of the Nelson Mandela era, South Africa unfortunately had to endure the destruction wreaked by one of Africa’s most evil sons, Jacob Zuma. The situation engineered at the power utility, Eskom, is so bad that despite a plethora of some of the continent’s most highly paid executives, Eskom will not be able to even report on the full and true extent of its catastrophic decline for several weeks. The sad truth is that the fortunes of Eskom are now not capable of being fixed, since even if funding is thrown at the problem, such funding can only be channeled via BBBEE entities (Broad Based Black Economic Empowerment) and the overriding purpose of such constructs is the enrichment of the shareholders, and ability to achieve business objectives within a budgeted and contractual framework does not feature in this’ Nigerian ‘style of doing business. At least further moves to a cashless South Africa must presumably be put on hold as digital currency alternatives are predicated on the availability of a national grid at least 99% of the time.

Presumably we will soon witness euphoria in global equity markets if Deutsche Bank is merged with Commerz Bank. Why not link the supervision of Chernobyl to the ELE (extinction level event) of Fukushima Daiichi and thereby miraculously save the planet? Engineers in South Africa have long known that linkage of one toxic overflowing sewer with another such sewer equals a problem solved and the award of mega bonuses all round to the architects of the ‘solution’.

Regards

Nicholas

end

Nicholas in a second email to us, describes the huge run up in the price of Palladium and what it might portend for gold/silver.

Bill/Harvey,

A second email within a couple of hours might be pressing my luck in respect of publication, but here goes anyway.GATA members well understand that gold price suppression cannot be defeated via seeking to overwhelm the shorts in the paper markets.Such an attempted outmaneuver would seek to conquer ‘infinity’,which is impossible (and yet there seems to be no shortage of demented players)..The paper market in Palladium could well be of interest to those of us who are looking for a sign that the Comex crooks can be defeated.A minute ago, the paper price of palladium was quoted at $1,575. Now here is an extract of an article by John Dizard from the Financial Times of London (no less), published on 28th September 2018,when the price of palladium had just risen to $1,076. Hindsight is a wonderful vantage point, but the tenor of the full article is an urgent plea to short palladium at its current bubble price of $1,076.

“Bubbles need half-smart participants to get under way. The forthrightly stupid will stand there like stubborn beasts as the proposition is put forward. The truly clever will ask lots of questions and undertake too much research. The best investment bubble propositions incorporate the familiar and the incomprehensible. Take, for example, the past month’s bubble in palladium, the price of which has risen by more than a quarter since the middle of August. The largest single application for the dull silvery metal is in the exhaust filters of petrol engines. A few grammes of palladium in the devices help convert toxic gases such as nitrogen oxide and carbon monoxide into water vapour, carbon dioxide and nitrogen, without being consumed in the process. Therefore, we have something familiar to investors (cars) and something incomprehensible (the physical chemistry of catalytic converters) — perfect conditions for a bubble. The filters for diesel engines use proportionately more platinum — palladium’s shinier and more glamorous relative — to perform the same function. Historically, platinum has been the more expensive. That has changed in the past couple of years and in recent days the trading-screen price of palladium has been $1,076 a troy ounce, while platinum is $816.”

Great advice indeed.

Regards

Nicholas B

end

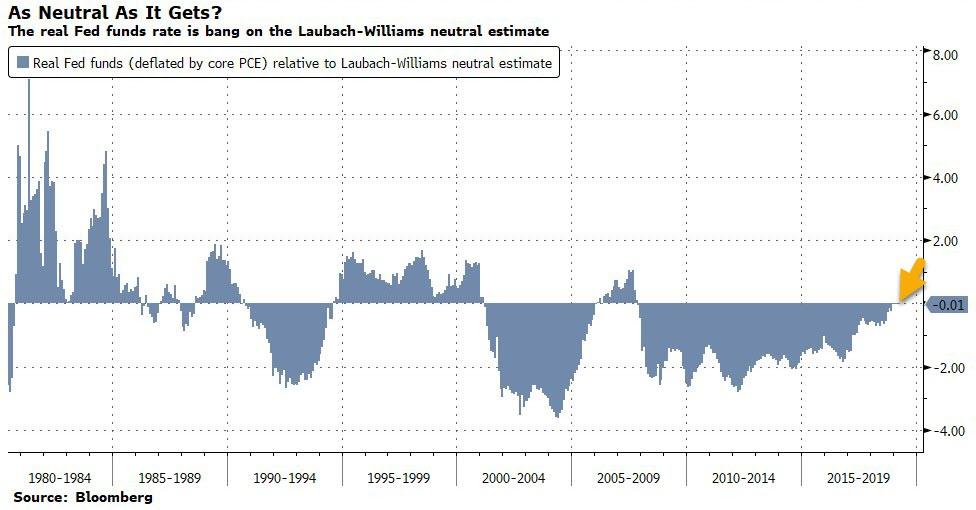

Craig Hemeke describes the dilemma facing the Fed as it tries to pare its balance sheet and raise rates

(courtesy Craig Hemke)

Ahead Of The Fed – Craig Hemke

“As 2019 unfolds, you’ll need to monitor the obvious breakout levels for both metals. For COMEX gold, price has…”

by Craig Hemke of Sprott Money News

This week brings another FOMC meeting, with discussions of interest rates, balance sheets, and the economy. How will this impact the precious metals?

While most of the media attention this week will be on Chairman Powell and what he states during his press conference on Wednesday, it will be vital to remember the long game as you watch gold and silver prices fluctuate with every Powell utterance.

As we wrote back in January, the year 2019 will unfold in a manner similar to 2010. If you missed that post, here’s the link for your review:

• https://www.sprottmoney.com/Blog/gold-and-silver-2…

The year 2010 began with talk of economic strength and “green shoots” rising from the economic rubble of the Financial Crisis. In 2009, the Fed had taken the unprecedented step of directly monetizing some U.S. debt through a program called “Quantitative Easing”, but this initiative had ended by early 2010 and this interest rate manipulation scheme was widely considered to be a one-off drastic measure that would never need to be used again.

And then something unexpected happened. After peaking at 3.2% GDP growth in Q2 of 2010, the U.S. economy began to decline, and quarterly GDP turned negative by early 2011. In response, The Fed announced a second round of Quantitative Easing in November of 2010.

This next program, dubbed “QE2”, revealed to all that The Fed had no plan and was simply responding to economic conditions with “every tool in the toolbox”. Confidence in the U.S. dollar fell and gold set off on an amazing run, as investors and traders globally sought precious metal in any form.

Well, here we are in 2019 and a nearly identical situation is playing out.

By late 2018, the global central banks were all on a stated course to raise interest rates and tighten their balance sheets. This was the plan, until the global equity markets crashed in Q4 and economies began to contract. The European Central Bank was the first to capitulate earlier this month, and the U.S. Fed won’t be far behind.

How do we know this? Check the data. In recent weeks, nearly every U.S. economic data point has been underwhelming, with falling retail sales, declining durable goods orders, and meager job creation the most obvious signals. The Atlanta Fed GDPNow forecast, which many utilize as an excellent prognostication tool, is currently projecting just 0.4% “growth” for the U.S. economy in Q1 2019. Again, doesn’t this remind you of 2010?

Thus, be advised to pay little attention to Chairman Powell this week as he focuses upon the present. Instead, look over the horizon to where this is all headed in 2019 and then ponder how the prices of precious metal will respond. The chart below from Incrementum AG shows a very high correlation between Fed tightening and U.S. recessions. Thus, now is the time to plan for a U.S. recession that is almost certainly coming later this year.

Once this recession is recognized, you can expect:

• U.S. interest rate cuts that lead to another program of Quantitative Easing.

• A drop in the U.S. dollar as confidence in The Fed wanes.

• Falling real interest rates as asset prices fall and disinflation takes hold.

• Soaring debt levels as government tax receipts collapse.

You just lived through this within the past decade, and now here it comes again. However, this time, there are no mulligans. The Fed will be revealed as having no plan, and the world will realize that we are all still living in the giant economic experiment kicked off by Bernanke and his ilk in 2009.

What can you expect from gold and silver? Well, you no doubt remember what transpired in 2010-2011. Gold prices soared from $1050 to $1920 while silver rallied from $16 to $49. Could this happen again? Of course! Will it? I guess we’ll wait and see.

As 2019 unfolds, you’ll need to monitor the obvious breakout levels for both metals. For COMEX gold, price has not posted a weekly close above $1360 in nearly five years! Thus, any breakout and move toward $1400 will be noticed globally, and the result will be a sharp increase in upside momentum.

In COMEX silver, The Banks have diligently painted a downtrend that runs along the 200-week moving average. This trend has been in place since late 2016, and it won’t be easy to break. However, once it is broken, a move toward $18 and $20+ will follow, with even higher highs pending for later this year and 2020.

So be prepared for price volatility later this week, but be sure to keep your eyes on the prize. The global central banks are irreversibly moving toward rate cuts and monetary easing. As was the case in 2010, this will lead to higher precious metal prices in 2019.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.6944/

//OFFSHORE YUAN: 6.6972 /shanghai bourse CLOSED DOWN 0.34 POINTS OR 0.01% /

HANG SANG CLOSED DOWN 145.31 POINTS OR 0.49%

2. Nikkei closed UP 42.07 POINTS OR 0.20%

3. Europe stocks OPENED RED

/USA dollar index RISES TO 96.45/Euro FALLS TO 1.1352

3b Japan 10 year bond yield: FALLS TO. –.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.49/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 58.40 and Brent: 67.28

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.10%/Italian 10 yr bond yield UP to 2.54% /SPAIN 10 YR BOND YIELD UP TO 1.18%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.44: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.75

3k Gold at $1304.30 silver at:15.31 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 3/100 in roubles/dollar) 64.34

3m oil into the 58 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.49 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9999 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1342 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.10%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.60% early this morning. Thirty year rate at 3.01%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4781

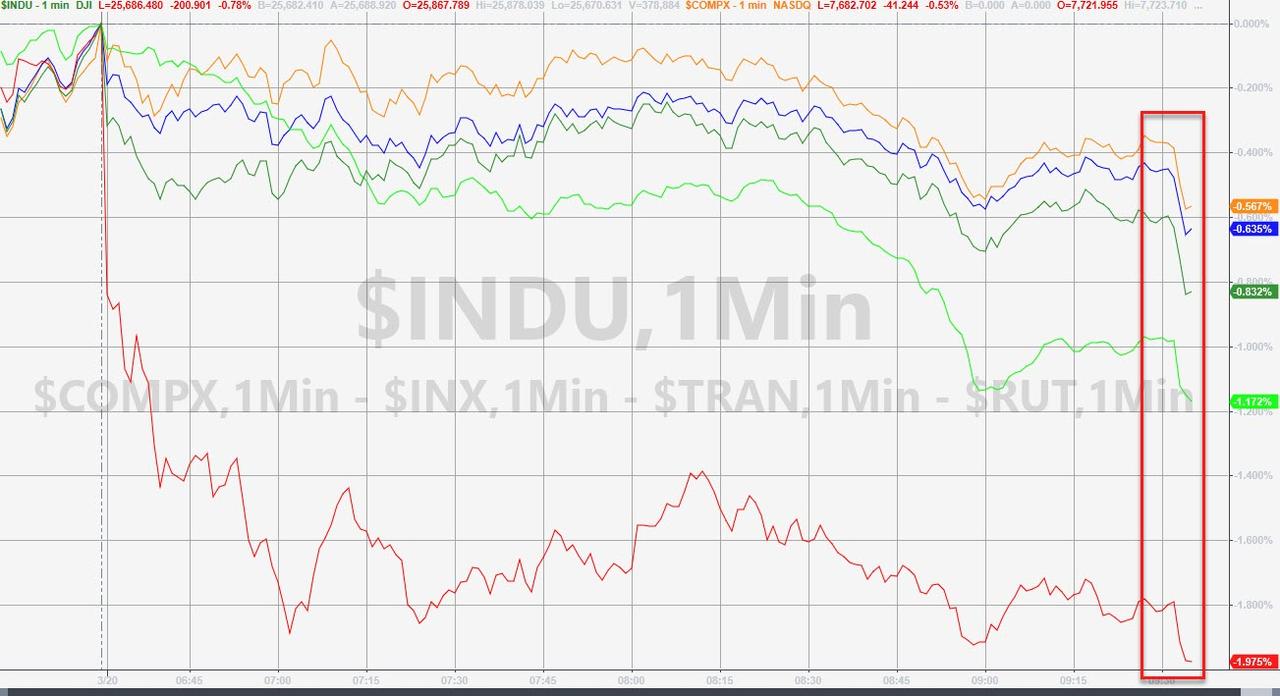

FOMC Drift Dead As Global Stocks Slide Ahead Of Fed

After yesterday’s last day selloff, the FOMC Drift is again missing again this morning, with S&P futures in the red following a drop in Asian shares and a bigger slump in Europe, where the Brexit chaos returned after May said she would not seek a long delay from the EU while a sharp drop in Bayer and BMW shares dragged Germany’s DAX 1% lower. The dollar rose and ten-year Treasury yields slipped.

US equity futures erased an earlier gain, as nervous investors sold ahead of today’s FOMC meeting, with the mood souring on Tuesday after reports of renewed tensions in U.S.-China trade talks also fraying nerves.

As a result, the longest winning streak in global shares since 2017 was set to end with a whimper as investors took profits on Wednesday before the U.S. Federal Reserve’s policy decision, ending 7 consecutive days of increases in the MSCI World.

Europe’s STOXX 600 fell 0.3%, with indexes in Britain and France also slightly down as investors closed positions before the Fed’s decision, due at 2pm this afternoon.

Germany’s DAX led the retreat as BMW warned earnings would fall and chemical maker Bayer headed for the biggest drop in 16 years after the company lost the first phase of a U.S. jury trial over claims its Roundup weed killer causes cancer. The steep decline has a negative impact of almost 100 points on the DAX. Additionally, German automaker BMW stumbled 4.2%, after warning earnings will fall “well below” last year’s level. The news dragged down peers with Daimler down 2%, Continental -1.7%, and Volkswagen -2.1%.

Elsewhere, the largest Swiss bank UBS warned the first quarter “was one of the worst in history.”

Earlier, Asian equity markets lacked firm direction following a lacklustre US session as global risk appetite was hampered by the looming FOMC meeting and ongoing US-China trade uncertainty. ASX 200 (-0.3%) and Nikkei 225 (+0.2%) traded mixed in which the former was pressured by weakness in financials and mining names, while Sony and Nintendo shares were among the biggest decliners in Japan following Google’s announcement of a cloud-based gaming service, although losses in the broader Tokyo market were later pared by a drop in the yen. Hang Seng (-0.2%) and Shanghai Comp. (U/C) conformed to the indecisive tone due to trade uncertainty following conflicting news flow in which US-China trade talks were said to be at the final stages with senior trade negotiators to meet from next week, although other reports noted expectations that China may walk back on some trade offers and that issues remained regarding data services and pharma.

Looking at today’s main event, the U.S. central bank is expected to hold rates steady and cut the number of hikes projected for the rest of the year, signaling since early this year a “patient” approach to increasing borrowing costs, while also unveiling its plan to end the balance sheet rolloff.

“Some traders expect the Fed to be a little on the neutral side. The Fed will be optimistic – but not overly optimistic – to send a neutral but upbeat message to the market,” said David Madden, an analyst at CMC Markets in London.

Also in play were concerns on rising tension in the U.S. trade negotiations, which pushed MSCI’s broadest index of Asia-Pacific shares outside Japan down 0.2 percent. Bulls retreated on Tuesday afternoon, after a Bloomberg report of U.S. concerns that China is pushing back against American demands in trade talks. Talks are set to resume next week – the first since President Donald Trump delayed a March 1 deadline to raise tariffs on Chinese imports – in an acceleration aimed at ending an eight-month trade war between the world’s two largest economies. U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin plan to travel to China next week for another round of talks with Chinese Vice Premier Liu He.

On the whole, though, many investors are holding on to hopes of a deal between Washington and Beijing, even as officials from the two sides remained locked in negotiations: “China is eager to come to an agreement so I’m not too worried,” said Wang Shenshen, strategist at Tokai Tokyo Research Center. “As long as they are holding meetings, many things will work out.”

Two-year Treasury yields remained below the top of the Fed’s policy target range amid expectations of a dovish tone from the central bank, while the dollar ticked higher after three days of losses. The pound fell as U.K. Prime Minister Theresa May was said to ask for only a short extension to the Brexit process, scuttling expectations that Brexit is all but over. The euro held steady after German producer inflation data missed estimates. European sovereign bonds were mixed.

Kazakhstan’s tenge fell half a percent against the dollar as Kassym-Jomart Tokayev, a career diplomat fluent in Russian, English and Chinese, was sworn in as president. Tokayev pledged to continue the policies of veteran leader Nursultan Nazarbayev, who unexpectedly resigned on Tuesday after three decades in power, and will serve out the presidential term ending in April 2020.

It was unclear whether Tokayev, the former prime minister, will run for a full term as president of the vast oil- and gas-rich country of 18 million people, adding to uncertainty for investors already facing a shift from long-term structural reforms towards populist policies.

In commodities, oil prices were firm, supported by supply cuts led by producer club OPEC as well as U.S. sanctions against Iran and Venezuela, though gains were limited by concerns over global economic growth. International Brent crude oil futures were at $67.65 a barrel by 0925 GMT, up 0.1 percent from their last close.

Looking at the day ahead, the FOMC rate decision is due, while scheduled earnings include Micron, General Mills.

Market Snapshot

- S&P 500 futures up 0.1% to 2,839.75

- STOXX Europe 600 down 0.5% to 383.01

- MXAP down 0.1% to 160.28

- MXAPJ down 0.2% to 529.52

- Nikkei up 0.2% to 21,608.92

- Topix up 0.3% to 1,614.39

- Hang Seng Index down 0.5% to 29,320.97

- Shanghai Composite down 0.01% to 3,090.64

- Sensex up 0.2% to 38,427.54

- Australia S&P/ASX 200 down 0.4% to 6,165.35

- Kospi down 0.02% to 2,177.10

- German 10Y yield fell 0.4 bps to 0.093%

- Euro down 0.07% to $1.1344

- Brent Futures up 0.4% to $67.85/bbl

- Italian 10Y yield rose 3.9 bps to 2.14%

- Spanish 10Y yield unchanged at 1.171%

- Brent Futures up 0.4% to $67.85/bbl

- Gold spot down 0.3% to $1,302.97

- U.S. Dollar Index up 0.1% to 96.50

Top Overnight News

- Brexit-backers in U.K. PM May’s cabinet have threatened to resign if an extension is so long the U.K. has to take part in European Parliament elections. The EU had indicated that a long delay is needed if May can’t get her deal through Parliament, and chief negotiator Michel Barnier hinted the bloc would like to see a second referendum

- “Huge Tory revolt” is underway to stop U.K. Prime Minister Theresa May asking EU for Brexit delay of nine months or more, ITV Political Editor Robert Peston says on his Twitter feed. Theresa May has been “requested to address the 1922 committee of Conservative MPs at 5pm

- U.S. negotiators are concerned China is pushing back against American demands in trade talks, according to people familiar with the negotiations, even as President Donald Trump sounded optimistic about reaching a deal

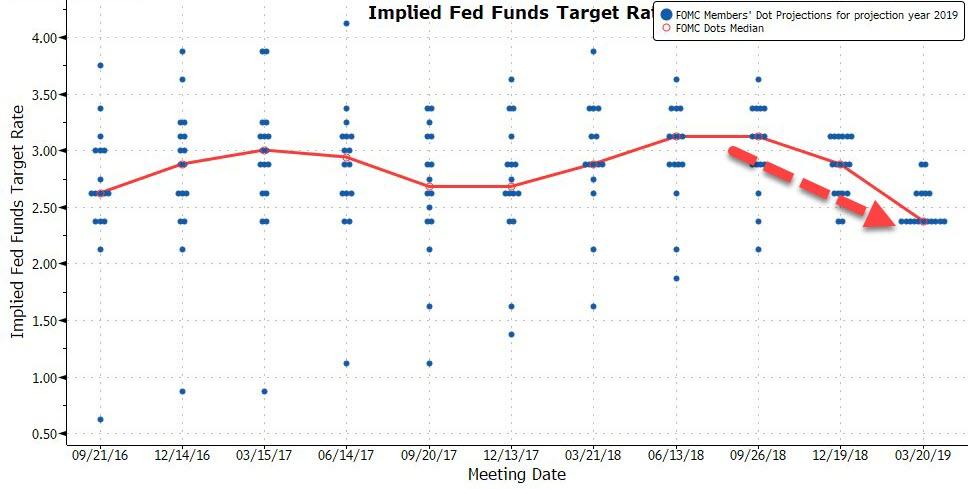

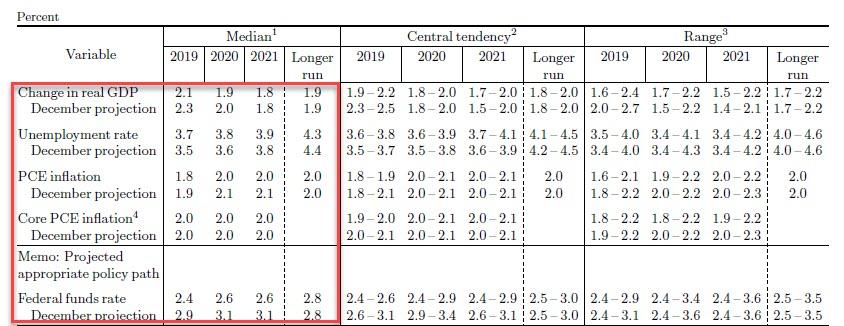

- Most market watchers expect the more-aggressive projections in the Fed’s dot plot to come down this week, shifting the middle ground to just one hike this year and possibly another in 2020

- Sydney’s apartment market is “quite soft” due to a sharp rise in supply that’s increased risks to financial stability, RBA’s Bullock said, urging banks to loosen up lending rules if they can

- One of nine Bank of Japan board members said it was necessary for the central bank to avoid expectations of no policy change becoming excessively fixed in financial markets, according the meeting minutes

- Oil’s rally stalled after some U.S. officials were said to fear a Chinese pushback in trade negotiations between the world’s two largest energy consumers

- Former U.S. Vice President Joe Biden has begun telling some supporters that he’s making plans to jump into the 2020 Democratic race

- Around 10,000 jobs in Frankfurt could be at risk from the potential merger between Deutsche Bank and Commerzbank; UBS Group’s Chief Executive Officer Sergio Ermotti gave a gloomy outlook to investors, saying conditions in the first three months have been among the toughest in years

- Hedge funds focused on the $5.1 trillion-a-day foreign exchange market are trying to circumvent the dearth of volatility by going farther afield to find an edge

Asian equity markets lacked firm direction with the region cautious following a lacklustre lead from Wall St and as global risk appetite was hampered by the looming FOMC meeting and ongoing US-China trade uncertainty. ASX 200 (-0.3%) and Nikkei 225 (+0.2%) traded mixed in which the former was pressured by weakness in financials and mining names, while Sony and Nintendo shares were among the biggest decliners in Japan following Google’s announcement of a cloud-based gaming service, although losses in the broader Tokyo market were later pared by favourable currency moves. Hang Seng (-0.2%) and Shanghai Comp. (U/C) conformed to the indecisive tone due to trade uncertainty following conflicting news flow in which US-China trade talks were said to be at the final stages with senior trade negotiators to meet from next week, although other reports noted expectations that China may walk back on some trade offers and that issues remained regarding data services and pharma. Finally, 10yr JGBs were restrained as they reflected the flat picture in T-notes and uneventful BoJ Minutes release, although prices were then pressured as Tokyo trade began to improve and following a tepid BoJ Rinban operation of JPY 500bln concentrated in the belly.

Top Asian News

- China Developers Jump as Property Tax Law Omitted From 2019 Plan

- Bank of Thailand Holds Interest Rate as Election Risks Mount

- Singapore Gets First Guilty Plea in S$8b Penny Stock Rout

Major European indices are in the red [Euro Stoxx 50 -0.5%], with clear underperformance seen in the Dax (-1.0%). Underperformance in the Dax was seen at the open following Bayer (-12.5%) opening significantly lower following a US Jury ruling that the Co’s Roundup was a ‘substantial factor’ in causing a man’s cancer, for reference the Co. has around a 8.3% DAX weighting. Losses in the Dax were subsequently exacerbated by BMW (-4.8%) reporting that they see 2019 group profit before tax significantly lower than the prior years levels; other German names have been dragged down in sympathy. In terms of sectors the material sector continues to underperform, after opening lower than peers at the open, which has been attributed by some to a potential easing of supply constraints after Vale surpassed a milestone in their path to resume production at their Brucutu, Brazil mine. Other notable movers include UBS (-2.3%) are in the red, after the CEO stated that Q1 investment bank revenues are down by around a thirds Y/Y, adding that the CO’s global wealth management income remains under pressure. Elsewhere, Inmarsat (+16.6%) after reports that the Co. have received their 3rd takeover bid this year; which valued the Co. at GBP 2.5bln. Of note, Norsk Hydro (+1.0%) stated that it is too early to determine the exact operational and financial impact of the cyber attack they were subject to yesterday.

Top European News

- Hermes Says China Demand Is Still Rising. Neckties, Not So Much.

- Rolls-Royce Sees Record Year in China Even as Car Market Slumps

- Moncler Underperforms After Eurazeo Sells Remaining Stake

- Kingfisher CEO Laury to Step Down as DIY Retailer Struggles

In FX, the USD appears to have stabilised as the clocks tick down to the Fed, partly on technical grounds and short covering, but also due to the plight of others like the Pound that is underperforming on latest Brexit developments. The DXY is back within touching distance of the 96.500 level having stopped the rot just ahead of Fib support at 96.264, but it remains to be seen whether the index closes above another chart retracement level at 96.434, which did not hold yesterday, and this in turn depends on how dovish the FOMC proves to be via a combination of the revised growth and inflation forecasts, updated dot plots and especially QT guidance – for a full preview of the looming and pivotal event check out the Ransquawk Research Suite.

- GBP – In contrast to the Buck’s resolve, Sterling seems resigned to heightened Brexit risk, and in particular the increased uncertainty that extending the A 50 deadline might bring, assuming the EU accepts the request of course. Latest reports suggest that PM May will ask for a short delay of up to June 30 after discussing the alternative of a longer postponement from March 29 with her Cabinet, but meeting staunch opposition to the latter from Tory Leave rebels. However, Brussels remains adamant that any request will only be considered, let alone granted, if accompanied by a rationale reason or firm plan of action, while stressing no going back to the table and renegotiating the WA. Moreover, a 3 month extension crosses the EU election deadline and event itself, as the deadline falls on April 12 for May 23. Cable has accordingly recoiled from another approach towards 1.3300, stopping just short of 1.3200, and Eur/Gbp is hovering near the top of a 0.8590-50 range.

- G10 – Elsewhere, Usd/majors remain relatively rangebound and narrowly mixed, with the AUD, CHF and EUR marginally outperforming vs the JPY, CAD and NZD that are on a moderately softer footing vs the Dollar. Aud/Usd is holding close to 0.7100, and gleaning some support from the Kiwi on cross-positioning as Aud/Nzd climbs back above 1.0350 and Nzd/Usd is capped ahead of 0.6850 in advance of NZ Q4 GDP data that is likely to carry downside risks vs consensus. Usd/Jpy is pivoting 111.50 after more dovish leaning Japanese rhetoric from BoJ Governor Kuroda and the Government, while the Loonie has lost Tuesday’s bullish momentum and retreated further from 1.3250 to almost 1.3350 alongside crude prices. Turning to the single currency and Franc, trading parameters are still extremely tight around parity and 1.1350 respectively, with the Chf not just wary of the FOMC, but also the SNB on Thursday, while Eur/Usd does not seem likely to trigger decent option expiries at 1.1320-35 (1 bn) or 1.1390-1.1400 (2 bn) at this stage.

In commodities, Brent (-1.0%) and WTI (-0.5%) prices have slipped, and eliminated the support to prices garnered from yesterdays surprise API draw of -2.1mln vs. Exp. +0.3mln. Separately, UBS highlights that the slowing US’s slowing supply, which they note was highlighted in the EIA’s monthly report, suggests that oil markets are continuing to tighten. Looking ahead we have the EIA Weekly Crude report, where expectations are for a crude stocks draw of 0.775mln; at 14:30GMT. Gold (-0.3%) is trading towards the bottom of the days range, weighed on by a stronger dollar and ahead of FOMC rate decision later in the session. Elsewhere, copper has traded uneventfully this morning and Glencore are reportedly in talks with Aeris to offload their CSA copper mine for USD 575mln.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 2.3%

- 2pm: FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap

The countdown has now ticked down to under a month until we move into our new house after two years of anticipation and stress. Last night was the time for the final decision on paint for the kitchen with my wife giving me chapter and verse on the merits of a gloss or matt finish. Apparently one is more hard wearing which is preferable in the kitchen and I think I also heard that one can be a bit harsh in a kitchen for dark colours. To be honest it was all quite complicated and “glossed” over me. So I’m not 100% sure what we agreed on. Suffice to say that if I was in charge the kitchen would actually now be a golf simulator so it’s probably good that I’m not.

Elsewhere although the countdown to Brexit is technically now down to 9 days – without an extension – yesterday’s break in big Brexit news meant we’ve had a chance to revisit the real world in the last 24 hours and it’s looking a bit rosier than the inner walls of the House of Commons at the moment. However some concerns about the progress of US/China trade talks took the shine off the second half of the US session and this has spread into Asia a little too. Before this European equities closed at the highest point since the end of September and the S&P traded above 2850 intra-day for the first time since early October. US markets did fall -0.7% from the peaks though to eventually close just about flat (-0.01%) but still around its 5-month high, while the NASDAQ gained +0.12% to reach a fresh high since October 9. As mentioned the relatively sharp reversal around lunchtime in New York came as Bloomberg reported that US trade officials are becoming concerned over the apparent strong degree of pushback from China on issues related to intellectual property. According to the reports, Chinese officials believe that they have already made concessions by opening up some industries and moderating their joint venture requirements, and they want reciprocal commitments from the US in the form of eliminated tariffs. Other sources subsequently downplayed the stories, including President Trump who said that “talks with China are going very well.” USTR Lighthizer and Treasury Secretary Mnuchin are set to travel to China next week to continue talks.