GOLD: $1307.75 UP $6.00 (COMEX TO COMEX CLOSING)

Silver: $15.48 UP 15 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1309.10

silver: $15.46

Comex options expire next week: Wednesday March 27

London/LBMA expires Monday March 31/2019.

The crooks continue with their whacking right in front of the authorities/regulators despite the criminal probe of precious metals manipulations.

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 2 NOTICE(S) FOR 200 OZ (0.00622 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 384 NOTICES FOR 38400 OZ (1.944 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

56 NOTICE(S) FILED TODAY FOR 280,000 OZ/

total number of notices filed so far this month: 5379 for 26,895,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4042:UP $1

Bitcoin: FINAL EVENING TRADE: $3976 DOWN 63

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today0/2

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,300.500000000 USD

INTENT DATE: 03/20/2019 DELIVERY DATE: 03/22/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

737 C ADVANTAGE 1

905 C ADM 2

____________________________________________________________________________________________

TOTAL: 2 2

MONTH TO DATE: 384

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST CONTINUES TO RISE FOR THE THIRD CONSECUTIVE TIME: THIS TIME BY A CONSIDERABLE SIZED 1211 CONTRACTS FROM 189,124 UP TO 190,335 DESPITE YESTERDAY’S 4 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 675 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 675 CONTRACTS. WITH THE TRANSFER OF 675 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 675 EFP CONTRACTS TRANSLATES INTO 3.375 MILLION OZ ACCOMPANYING:

1.THE 4 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 27.120 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

29,282 CONTRACTS (FOR 15 TRADING DAYS TOTAL 29,282 CONTRACTS) OR 146.410 MILLION OZ: (AVERAGE PER DAY: 1952 CONTRACTS OR 9.761 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 146.410 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 20.91% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 511.80 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1211 DESPITE THE 4 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 675 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 1886 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 675 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1211 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.33 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.936 BILLION OZ TO BE EXACT or 134% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 56 NOTICE(S) FOR 280,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 27.120 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST REVERSED COURSE BY RISING 1953 CONTRACTS, TO 516,116 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A DROP IN PRICE OF $5.15//YESTERDAY’S TRADING). THE GOLD COMEX HAS BEEN WITNESSING SOME VERY STRANGE BEHAVIOUR. WITH GOLD RISING IN THE PREVIOUS SESSIONS, THE OPEN INTEREST COLLAPSED AS IT SEEMS THAT WE STARTED THE SPREADING LIQUIDATION EARLY. THEN LAST NIGHT, INSTEAD OF FALLING ESPECIALLY WITH A LOWER PRICE, IT ROSE AND STRANGELY BY THE EXACT AMOUNT IT FELL ON TUESDAY. IT IS ANYBODY’S GUESS AS TO WHAT IS TRULY GOING ON BEHIND THE SCENES OTHER THAN THE CROOKS ARE SCARED OUT OF THEIR MINDS….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GIGANTIC SIZED 12,450 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 12,315 CONTRACTS,JUNE: 85 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 516,116. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GIGANTIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 14,403 CONTRACTS: 1,953OI CONTRACTS INCREASED AT THE COMEX AND 12,450 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 14,403 CONTRACTS OR 1,440,300 OR 44.79 TONNES.

YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $5.15....AND WITH THAT, WE HAD A HUGE GAIN IN TONNAGE OF 44.79 TONNES?????!!!!!!.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 103,587 CONTRACTS OR 10,358,700 OZ OR 322.199 TONNES (15 TRADING DAYS AND THUS AVERAGING: 6905 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAYS IN TONNES: 322.195 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 322.195/2550 x 100% TONNES = 12.63% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1191.18 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED SIZED INCREASE IN OI AT THE COMEX OF 1953 DESPITE THE LOSS IN PRICING ($5.15) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,450 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,450 EFP CONTRACTS ISSUED, WE HAD A GIGANTIC GAIN OF 14,403 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

12,450 CONTRACTS MOVE TO LONDON AND 1953 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 44.79 TONNES). ..AND ALL OF THIS HUGE DEMAND OCCURRED WITH A FALL OF $5.15 IN YESTERDAY’S TRADING AT THE COMEX???????!!!!!

we had: 2 notice(s) filed upon for 200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $7.00 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD/

INVENTORY RESTS AT 778.09 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 15 CENTS IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 310.848 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 1211 CONTRACTS from 189,124 UPTO 190,335 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 675 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 675 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1211 CONTRACTS TO THE 675 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 1886 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.43 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 27.120 MILLION OZ FOR MARCH.

RESULT: A CONSIDERABLE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 4 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A FAIR SIZED 675 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 10.82 POINTS OR 0.01% //Hang Sang CLOSED DOWN 249.41 POINTS OR 0.85% /The Nikkei closed HOLIDAY/ Australia’s all ordinaires CLOSED UP .03%

/Chinese yuan (ONSHORE) closed UP at 6.6917 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 58.40 dollars per barrel for WTI and 67/28 for Brent. Stocks inEurope OPENED RED

ONSHORE YUAN CLOSED UP // LAST AT 6.6917 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6946 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

i

3A//SOUTH KOREA

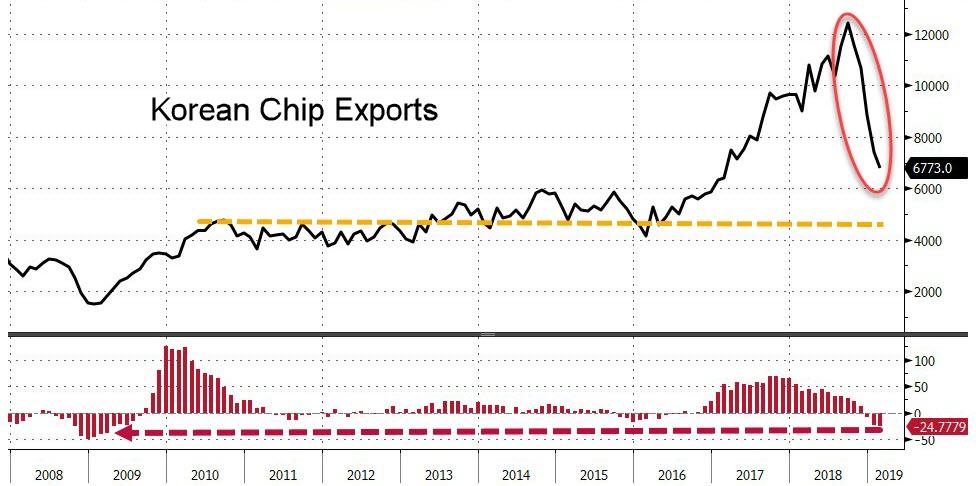

A good indicator telling us that the global economy is drying up: South Korean chip exports collapse by 25%

( zerohedge)

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

i)We may get our “no deal” Brexit if the EU will not allow an extension. England is in a mess right now

( zerohedge)

ii)An extremely important commentary from Mises as they state that a Hard Brexit would be good for the country and I agree with the author..so does Tom Luongo

iv)Switzerland

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

IRAN/USA/Lebanon/Iraq

Tom Luongo explains the inner workings of middle east developments with respect to Iran and its relationship with Iraq, Lebanon and other eastern nations. Iran seems to be withstanding the huge attack on it from the USA

( Tom Luongo)

6. GLOBAL ISSUES

i)Mexico/Mt Popocatepetl

This is dangerous: Mt. Popocatepet has just erupted and could devastate vegetation for miles and on top of that kill millions of people

( Michael Snyder/)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Venezuela

Guido’s chief of staff detained by Venezuelan intelligence in a pre dawn raid

(courtesy zerohedge)

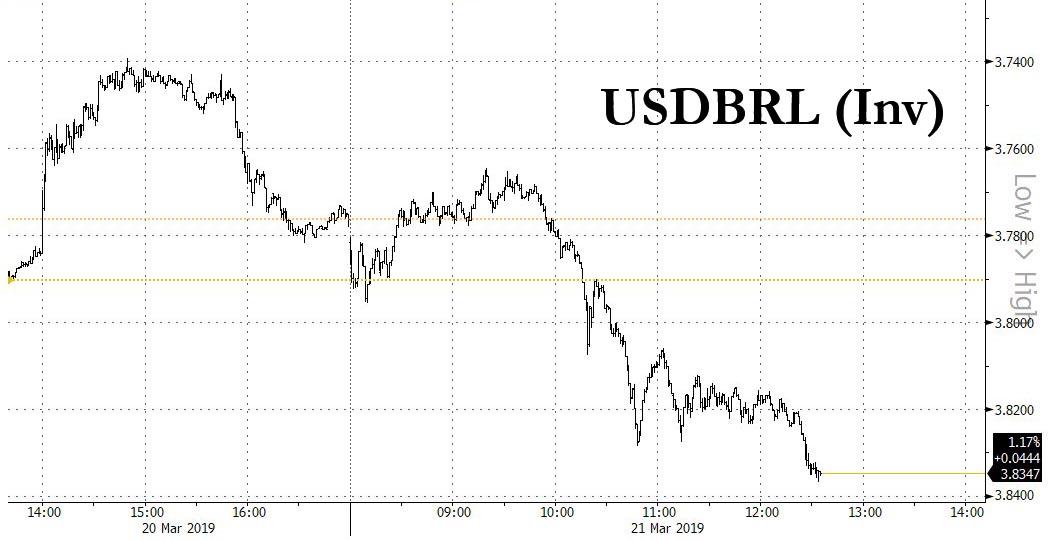

The Real tumbled this morning after former President Temer has been arrested as the part of the “car wash” scandal

(courtesy zerohedge)

9. PHYSICAL MARKETS

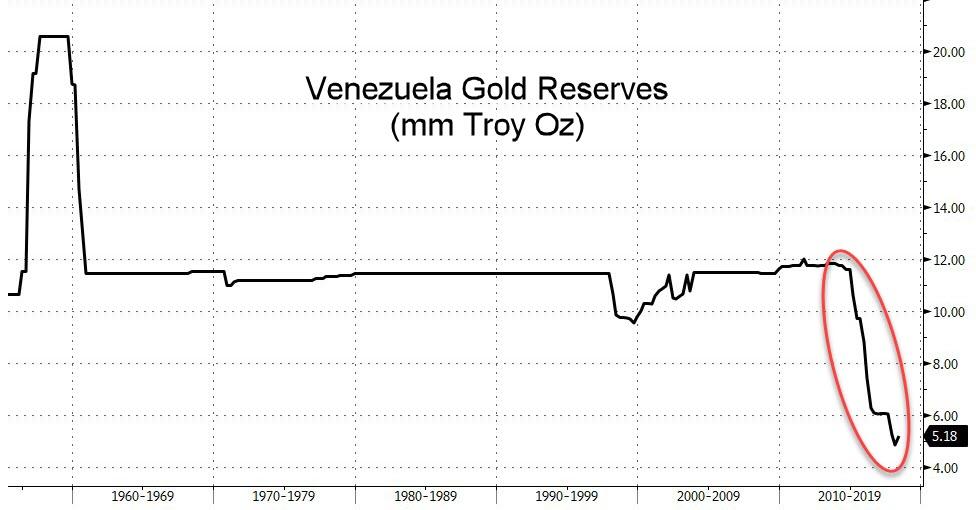

citigroup to sell 1.3 billion dollars worth of gold to repay 1.1 billion dollar loan. The excess will be placed into an account in NY..totally away from Maduro

(see article below)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

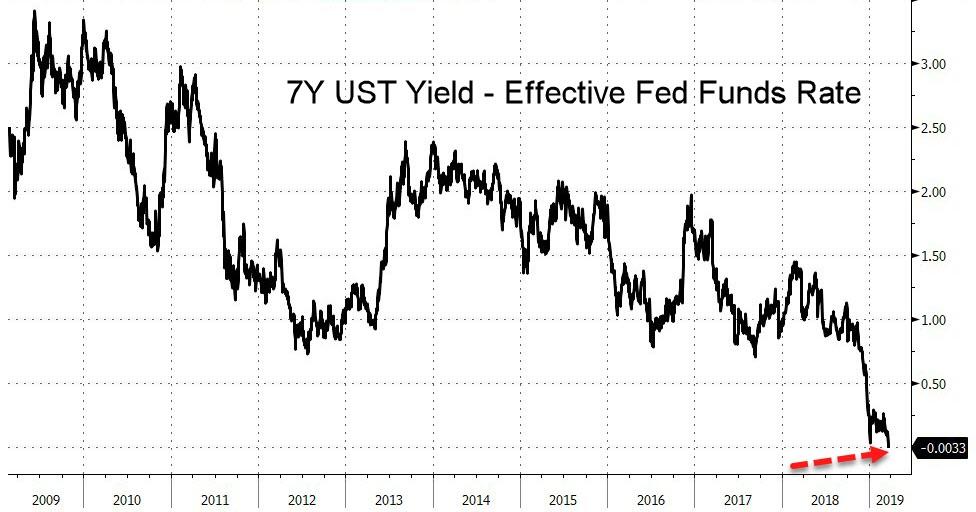

i)The 10 yr bond yield just collapsed to 2.495% ; the 7 yr bond yield inverts to the Federal fund rate as well. This shows how bad the USA economy is performing

( zerohedge)

late morning:

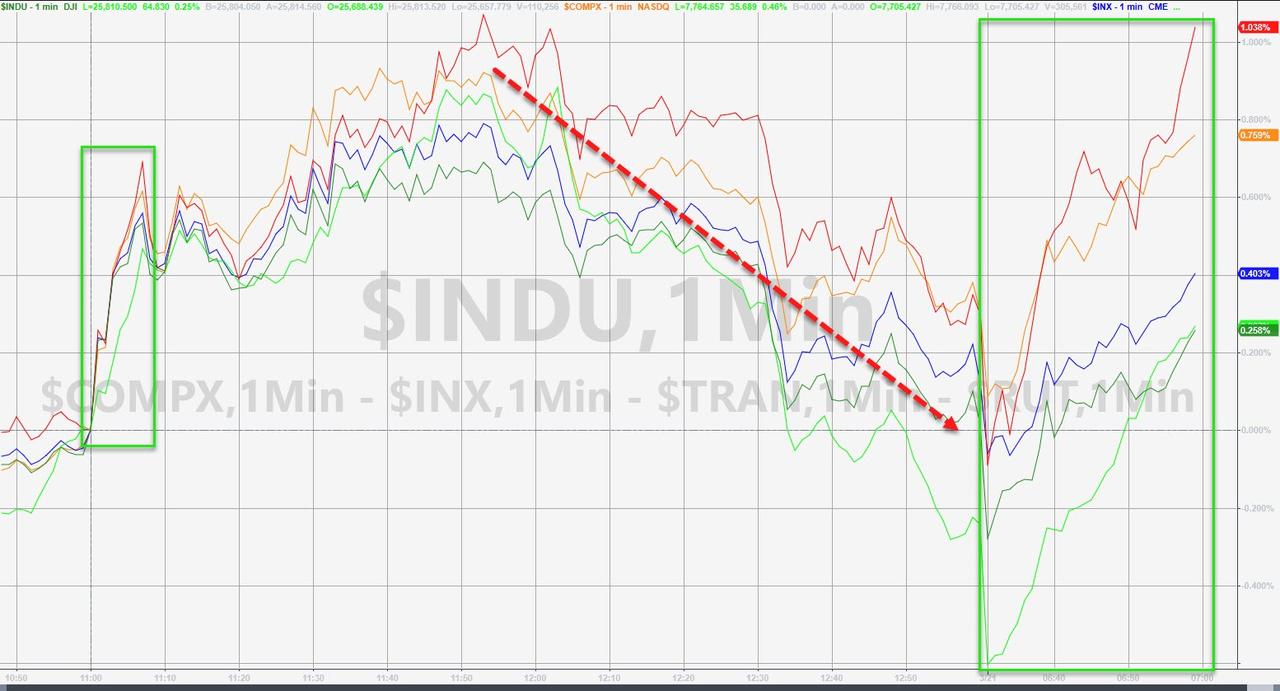

ii)stocks rise this morning in a buying panic but bonds are not buying it

( zerohedge)

ii)Market data

ii)USA ECONOMIC/GENERAL STORIES

a)_An outline of yesterday’s Fed decision to return the punchbowl to investors.

Please read carefully

(courtesy zerohedge)

b)To all our good friends in New Jersey: you are about to see your property tax rise due to a rain tax.

iv)SWAMP STORIES

The real collusion. Ukraine launches a criminal investigation into the Pro Hillary election meddling scandal

( zerohedge)

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL FELL TO 798 CONTRACTS FOR A LOSS OF 20 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ROSE BY 640 CONTRACTS UP TO 136,712 CONTRACTS. TODAY THE BANKERS RESUMED WITH THEIR QUEUE JUMPING..AS THE SILVER COMEX SEEMS TO BE IN SEVERE STRESS…

Exclusive Offer Of 6 Months Free Storage In Zurich and Valuable Complimentary Gifts

Exclusively For Retail, Pension and HNW Clients

Brexit and other arguably more significant financial risks such as Basle III loom. Given the many risks of today, we believe precious metal buyers should own gold and silver coins and bars in at least two jurisdictions. We have decided to provide exclusively to our clients a valuable storage offer in what we believe are the safest vaults in the safest jurisdiction in the world – Zurich, Switzerland.

Six Months Free Storage In Zurich

When you invest the minimum amount of $€£ 10,000 (no maximum) in physical gold and or silver for storage in our Loomis vaults in Zurich, Switzerland, you will pay zero storage fees for the first six months from the date of your purchases. This applies to all investments for storage in Zurich in the next 30 days.

All gold and silver is stored in professionally managed, specialist, high security precious metals vaults. In addition to this gold and silver stored in GoldCore Secure Storage is stored on a fully allocated and fully segregated basis – the safest way to store precious metals.

Complimentary Silver Bullion Coin

In addition to the 6 months’ worth of free Secure Storage we also appreciate that our clients enjoy seeing and holding their precious metals and that’s why we will also be delivering to you fully insured, a freshly minted, 2019, one ounce, legal tender, silver bullion coin. You can choose between two of the world’s most popular silver coins: the 2019 American Silver Eagle or the beautifully minted 2019 British Silver Britannia.

More information about the offer can be accessed here and if you wish to avail of the offer simply wire funds and transact online or on the phone. If you have any questions please email support@goldcore.com .

5 Ways to Prosper In the Coming Crisis – Goldnomics Podcast

The systemic challenges facing our planet and the five key ways to prosper in the coming global crisis are considered in our latest podcast.– Political, financial, economic and monetary systems are failing and will collapse

– Our human built economic systems are dependent on the environment and ecology of the planet is threatened and in crisis

– Medical, religious, belief paradigms are being questioned and in crisis

– Old systems are collapsing in the age of information as we enter a new era of consciousness

– Read, learn, develop skills and yourself

– Health is wealth – Don’t worry, be happy

What are the 5 ways to prosper in the coming crisis?

3. Avoid Excessive Debt or Leverage

5. Invest In Your Education, Learn, Grow and Contribute

News and Commentary

Gold climbs as Fed signals no 2019 rate hikes (MarketWatch.com)

Gold, the Federal Reserve, and the dollar – what’s driving up precious metal prices? (CityAM.com)

Citigroup to sell Venezuelan gold in setback to President Maduro (Reuters.com)

Trump says tariffs on Chinese goods may stay for ‘substantial period’ (Reuters.com)

Dovish Fed shift lifts Asian shares, dollar nurses losses sending gold higher (EuroNews.com)

Source: Bloomberg

Buy Gold, Sell Stocks Is the ‘Trade of Century’ Says One Hedge Fund (Bloomberg.com)

Why the EU holds all the cards on Brexit (TheTimes.co.uk)

‘I’m single, I’ve not become attractive overnight, just my WALLET!’: Bachelor factory worker, 58, scoops £71m on EuroMillions – but warns off gold-diggers as he vows windfall ‘bloody well WILL change him’ (MSN.com)

Warren Buffet Data Mines Again When Making Anti-Gold Argument (TheStreet.com)

Inside the Fed’s balance sheet in four charts (reuters.com)

Gold Prices (LBMA PM)

20 Mar: USD 1,303.00, GBP 985.07 & EUR 1,147.81 per ounce

19 Mar: USD 1,308.35, GBP 985.06 & EUR 1,152.53 per ounce

18 Mar: USD 1,305.35, GBP 986.19 & EUR 1,150.01 per ounce

15 Mar: USD 1,302.35, GBP 981.55 & EUR 1,150.55 per ounce

14 Mar: USD 1,299.20, GBP 982.84 & EUR 1,148.88 per ounce

13 Mar: USD 1,308.40, GBP 994.25 & EUR 1,158.20 per ounce

Silver Prices (LBMA)

20 Mar: USD 15.32, GBP 11.58 & EUR 13.49 per ounce

19 Mar: USD 15.41, GBP 11.61 & EUR 13.57 per ounce

18 Mar: USD 15.38, GBP 11.60 & EUR 13.54 per ounce

15 Mar: USD 15.35, GBP 11.58 & EUR 13.56 per ounce

14 Mar: USD 15.23, GBP 11.52 & EUR 13.48 per ounce

13 Mar: USD 15.52, GBP 11.80 & EUR 13.73 per ounce

Recent Market Updates

– 5 Ways to Prosper In the Coming Crisis – Goldnomics Podcast

– Deutsche Bank and Commerzbank May Become EU’s “Too Big To Fail” Bank

– Happy Saint Patrick’s Day from GoldCore

– 188 Internet Shutdowns In 2018 Show Why Physical Gold Is Ultimate Protection

– Buy Gold as Basel III Means “Central Banks and Banks Are Going To Be Buying Gold”

– Invest In Gold Or Bitcoin – Which Is The True Store Of Value?

– Silver Bullion Is The Portfolio Insurance To Buy Now

– EU Isn’t Ready for the Next Recession

– JPMorgan Is Bullish on Gold as a Hedge Against Rising Inflation

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

citigroup to sell 1.3 billion dollars worth of gold to repay 1.1 billion dollar loan. The excess will be placed into an account in NY..totally away from Maduro

(see article below)

Citigroup to sell Venezuelan gold in setback to President Maduro, sources tell Reuters

Submitted by cpowell on Thu, 2019-03-21 00:35. Section: Daily Dispatches

Looks like the Western central banks need the metal pretty badly. Otherwise wouldn’t Citigroup keep the metal for itself, now that the price is rising?

* * *

By Mayela Armas and Corina Pons

Reuters

Wednesday, March 20, 2019

CARACAS, Venezuela — Citigroup Inc. plans to sell several tons of gold placed as collateral by Venezuela’s central bank on a $1.6 billion loan after the deadline for repurchasing them expired this month, sources said, a setback for President Nicolas Maduro’s efforts to hold onto the country’s fast-shrinking reserves.

Maduro’s government has since 2014 used financial operations known as gold swaps to use its international reserves to gain access to cash after a slump in oil revenues left it struggling to obtain hard currency.

In the past two years, however, it has struggled to recover its collateral.

Under the terms of the 2015 deal with Citigroup’s Citibank, Venezuela was due to repay $1.1 billion of the loan on March 11, according to four sources familiar with the situation. The remainder of the loan comes due next year.

Citibank plans to sell the gold held as a guarantee — which has a market value of roughly $1.358 billion — to recover the first tranche of the loan and will deposit the excess of roughly $258 million in a bank account in New York, two of the sources said. …

… For the remainder of the report:

https://www.reuters.com/article/us-venezuela-politics-gold/citigroup-to-…

* * *

Join GATA here:

Mining Investment Asia

InterContinental Singapore Bugis Hotel

Singapore

Tuesday-Thursday, March 26-28

https://www.mininginvestmentasia.com/

Mines and Money Asia

Hong Kong Conference and Exhibition Center

Wan Chai, Hong Kong

Tuesday-Thursday, April 2-4

https://asia.minesandmoney.com/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Good Morning Bill/Harvey

Citi To Sell Confiscated Venezuelan Gold From Maduro Deal

While Venezuelan President Nicolas Maduro has resiliently stood his ground amid Washington’s surprisingly transparent coup attempt, today has been a tough one for the embattled leader of the socialist utopia.

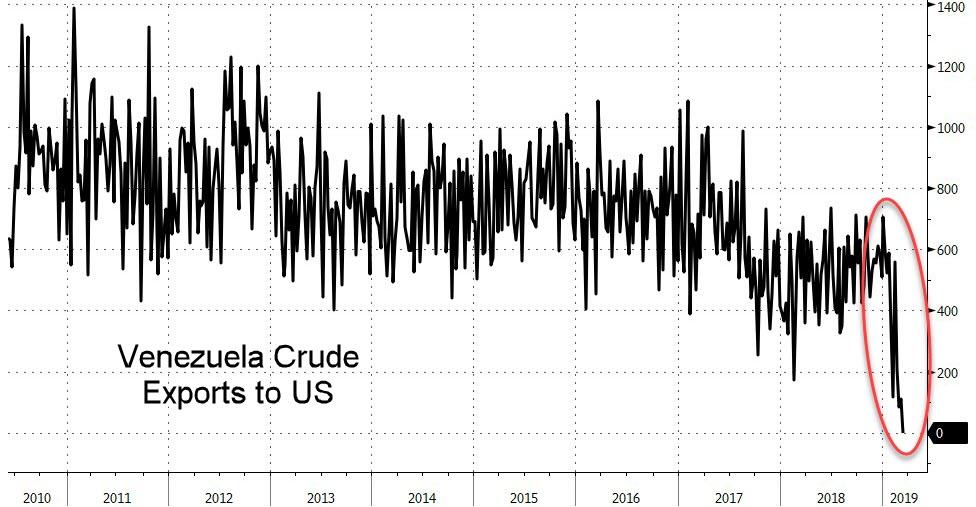

It began with confirmation that the US has now – for the first time ever – reduced all Venezuelan crude oil imports to zero.

Squeezing off yet another source of revenue for the sanction-riddled economy.

But Maduro then suffered another blow, as Reuters reports that Citigroup plans to sell several tons of gold placed as collateral by Venezuela’s central bank on a $1.6 billion loan after the deadline for repurchasing them expired this month.

As we detailed in February, back in April 2015, when Venezuela still had a somewhat functioning economy and hyperinflation was not yet rampant, the cash-strapped country quietly conducted a little-noticed gold-for-cash swap with Citigroup as part of which president Nicolas Maduro converted part of his nation’s gold reserves into at least $1 billion in cash through a swap with Citibank.

As Reuters reported then, the deal would make more foreign currency available to President Nicolas Maduro’s socialist government as the OPEC nation struggled with soaring consumer prices, chronic shortages and a shrinking economy worsened by low oil prices.

As Reuters further added:

“former central bank director Jose Guerra and economist Asdrubal Oliveros of Caracas-based consultancy Ecoanalitica said in separate interviews that the operation had been carried out. A source at the central bank told Reuters last month it would provide 1.4 million troy ounces of gold in exchange for cash. Venezuela would have to pay interest on the funds, but the bank would most likely be able to maintain the gold as part of its foreign currency reserves.”

Under the terms of the 2015 deal with Citigroup’s Citibank, Venezuela was due to repay $1.1 billion of the loan on March 11 2019, according to four sources familiar with the situation. The remainder of the loan comes due next year.

Needless to say, the socialist country’s economic situation is orders of magnitude worse now, and in addition to a full-blown blockade of the country’s only key export – see above – Washington’s not-so-stealthy coup, and financial system sanctions, making it impossible for Maduro to repay the loan and claim back his nation’s gold collateral.

A Venezuelan government source familiar with the matter confirmed that the country’s Central Bank did not transfer the money to Citibank this month.

And so, as Reuters reports, Citibank plans to sell the gold held as a guarantee – which has a market value of roughly $1.358 billion – to recover the first tranche of the loan.

Additionally, under the likely guidance of Washington’s coup-leaders, Citi will deposit the excess of roughly $258 million in a bank account in New York, two of the sources said; which is out of the reach of Maduro but very much available to Trump’s chosen one – Juan Guaido.

Meanwhile, far from pushing to reclaim its gold, Maduro has only been selling more of it, as Abu Dhabi investment firm Noor Capital confirmed when it said earlier this month that it bought 3 tons of gold from Venezuela’s central bank, but would halt further transactions until the country’s situation stabilizes.

Guaido has also asked British authorities to prevent Maduro from gaining access to gold reserves held in the Bank of England, which holds around $1.2 billion in bullion for Maduro’s government. So far the British central bank has refused to comply with Maduro’s demands to remit the gold back to Venezuela, although when asked for comment, the BOE said it does not comment on client operations.

Meanwhile, Hugo Chavez, who spent the last years of his life repatriating Venezuela’s gold is spinning in his grave.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.6917/

//OFFSHORE YUAN: 6.6946 /shanghai bourse CLOSED UP 10.82 POINTS OR 0.35% /

HANG SANG CLOSED DOWN 249.41 POINTS OR 0.85%

2. Nikkei closed //HOLIDAY

3. Europe stocks OPENED RED EXCEPT LONDON

/USA dollar index RISES TO 96.23/Euro FALLS TO 1.1386

3b Japan 10 year bond yield: FALLS TO. –.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.53/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 59.74 and Brent: 68.11

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.04%/Italian 10 yr bond yield UP to 2.46% /SPAIN 10 YR BOND YIELD UP TO 1.11%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.42: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.76

3k Gold at $1315.40 silver at:15.54 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 10/100 in roubles/dollar) 64.76

3m oil into the 59 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.53 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9941 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1318 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.04%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

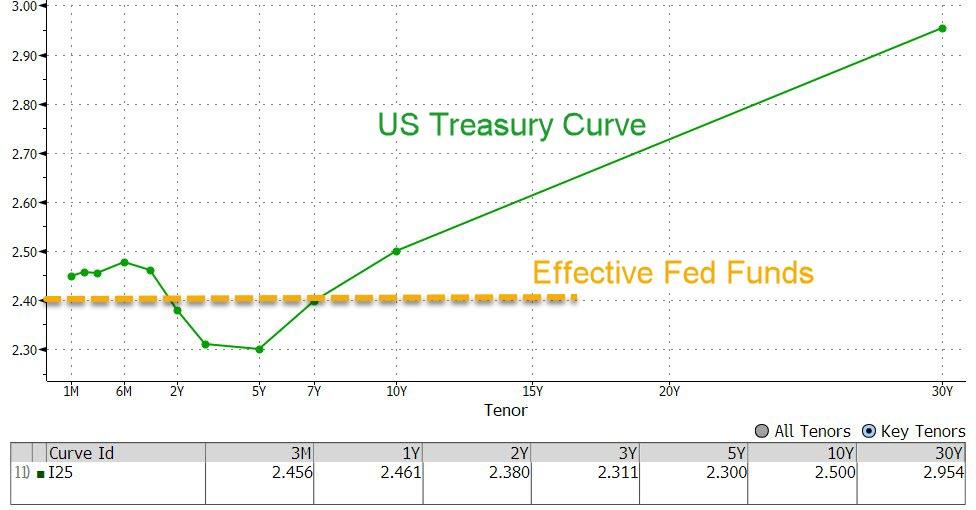

4. USA 10 year treasury bond at 2.51% early this morning. Thirty year rate at 2.96%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4566

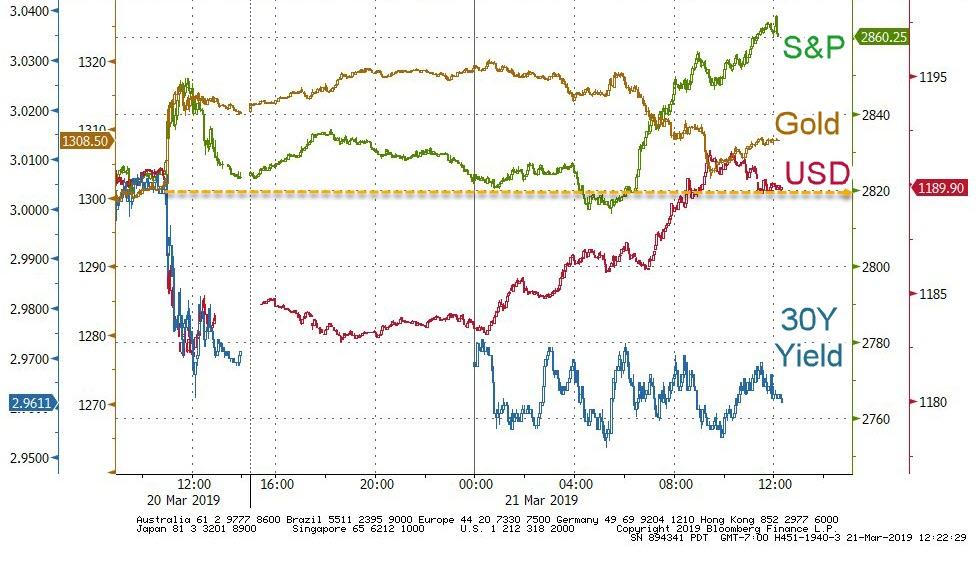

Stocks Slide, Bonds Soars, Dollar Rebounds As Traders Have A Question For Powell

Something is off.

Over the past decade, any time the Fed, BOJ or ECB surprised the market dovishly, risk assets surged. And yet, when the ECB did just that on March 9, when Draghi unveiled TLTRO prematurely, the Stoxx slumped. And, more concerningly, after a brief rally yesterday at 2pm in kneejerk response to a Fed that has now fully capitulated on normalizing monetary policy and announced it will end its balance sheet runoff by September, US markets not only faded all gains, but closed sharply lower.

When commenting on the Fed’s decision, and the market’s surprising reaction, we said that it was too early to draw conclusions from the S&P’s reaction, where a blast of selling took place at precisely 3:30pm setting the dour mood into the last 30 minutes of trading. However, the overnight session which saw both European stocks struggle and U.S. equity futures slide despite some bullish sentiment in Asia, it appears that investors still have a some questions for Powell, among which the most important one: “What does the Fed know that nobody else does for it to capitulate so abruptly”, and what might be lurking in the shadows.

So far that answer is missing, and it explains why US equity futures have continued to sink despite a Fed which is now all in on reflating if not the economy, which by now it is clear it has little control over, then at least capital markets. Meanwhile, as risk assets are shunned, investors are plowing into safe havens as the yield on 10-year Treasuries extended Wednesday’s drop, rates slumped across Europe and gold jumped.

As European shares wilted and futures faltered, banks suffered the brunt of selling from the dovish doubling down, expressing traders’ usual worries about low borrowing rates, and dragging the European STOXX 600 down 0.2%, though London’s FTSE edged up as its miners were lifted by higher copper and metals prices.

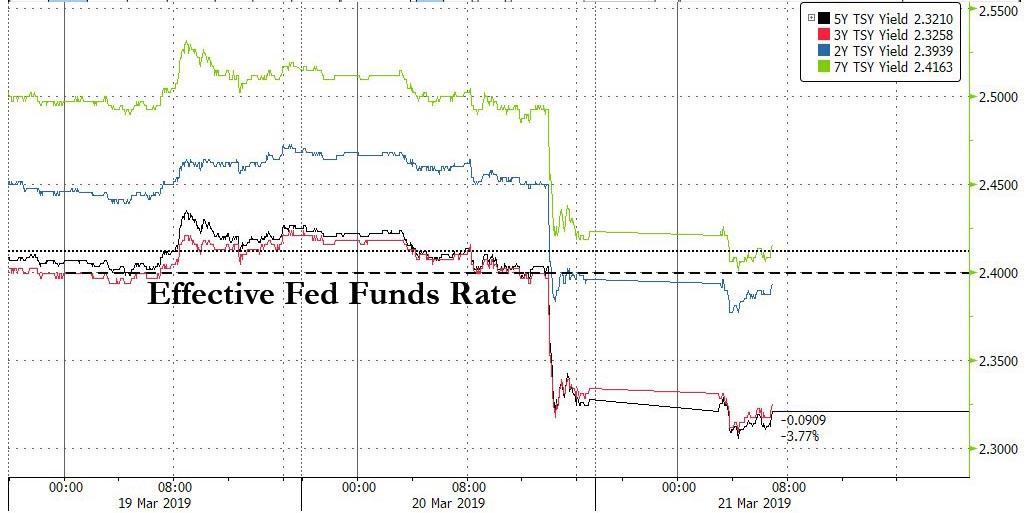

But the real action was in the bond markets, where the stampede into safety continued, with the 7Y inches away from inverting below the effective Fed Funds rate.

With investors rushing to price in the prospect of US rate cuts later this year, which traditionally have been followed by a recession 3 months later, Treasury yields dived to their lowest since early 2018 and those on German Bunds – Europe’s benchmark – to the lowest since October 2016. Ten-year Bund were offering buyers virtually nothing again at just 0.048%. Alongside widespread ‘curve’ flattening – where shorter and longer-term borrowing costs converge – there were alarm bells ringing.

Rabobank strategist Philip Marey said the worry is that, having cut rates to the bone and already tried full-scale money printing, many central banks are now low on traditionally ammunition to fight recessions.

“The Fed has the most leeway because it has raised rates nine times so it could cuts rates nine times,” Marey said. “But it will be much more difficult for other central banks which haven’t even started to hike yet.”

Earlier in Asia, MSCI’s broadest index of Asia-Pacific shares outside Japan was up 0.5%. Chinese blue-chips, which spent the morning swinging between small losses and gains, were up 0.4% in afternoon trade, while Seoul’s Kospi also added 0.4% as regulators announced plans to cut the stock transaction tax this year. Australian shares ended flat after see-sawing throughout the day. A drop in the jobless rate tempered market expectations of a rate cut. Markets in Japan were closed for a public holiday.

Meanwhile, in FX, after The Fed’s swerve sent the dollar sliding as far as 110.47 yen, with its 0.6 percent loss overnight the biggest drop since the flash crash of early January, the Bloomberg Dollar Spot Index rebounded sharply for the first time in five days as the greenback recovered some of the previous days losses as investors realized that if things are “this bad” in the US, they can only be far worse everywhere else, with the rest of the world only now starting to cut rates.

Despite the dollar’s rebound, it remains poised precariously on its 200-day moving average, and a sustained break would be taken as technically ‘bearish’, resulting in a slide that virtually every bank is expecting. “The downward pressure on U.S. yields continues to support our outlook for a weaker U.S. dollar this year,” said MUFG analysts in a note.

The pound saw the biggest decline as pressure built on Theresa May to gather a majority for her Brexit deal. The U.K. prime minister asked the European Union for a three-month extension to the March 29 deadline in a move that increases the risks of a no-deal departure. The Norwegian krone surged higher as Thursday’s top-performing G-10 currency after the Norges Bank followed the Federal Reserve in catching the market by surprise, but with a decision that was more hawkish than expected. The Norwegian krone rallied by the most since December versus the euro to touch a four-month high, after the Norges Bank hiked rates from 0.75% to 1.00%

The euro flew to a seven-week peak before things started to reverse in Europe. It was last trading at $1.1410, a world away from its recent low of $1.1177 while Brexit woes kept the pound down at $1.3175.

In other central bank news, also overnight, the Swiss National Bank kept rates on hold, cut its inflation forecast and said it will remain active in the currency market to curb any appreciation in the Swiss franc

Meanwhile, with the Fed now in the rearview mirror, trade concerns have returned, after President Trump on Wednesday warned that Washington may leave tariffs on Chinese goods for a “substantial period” to ensure Beijing’s compliance with any trade deal. China-U.S. trade talks are set to resume next week. Global growth worries extended to commodity markets, where oil prices, which had jumped Wednesday on supply concerns, retreated.

Brent (-0.3%) and WTI (-0.3%) are softer, and trade within a $1/bbl range. WTI did surpass the USD 60.0/bbl level overnight on the back of a dovish FOMC, however the complex has since drifted somewhat with WTI now trading just below the key level as fears about the global economy are dominating. Gold (+0.4%) is firmer, although off of session highs of around USD 1320/oz, on the back of dollar weakness after yesterdays dovish Fed, base metals more broadly have garnered support from the weaker dollar with copper rising 0.9 percent to $6,517 a tonne, having touched a near three-week high earlier in the session.

Elsewhere, Barclays note that the risks surrounding iron ore have not dissipated following the reopening of Vale’s Brucutu mine as two others have been temporarily closed recently and there is a risk of further mine closures.

Market Snapshot

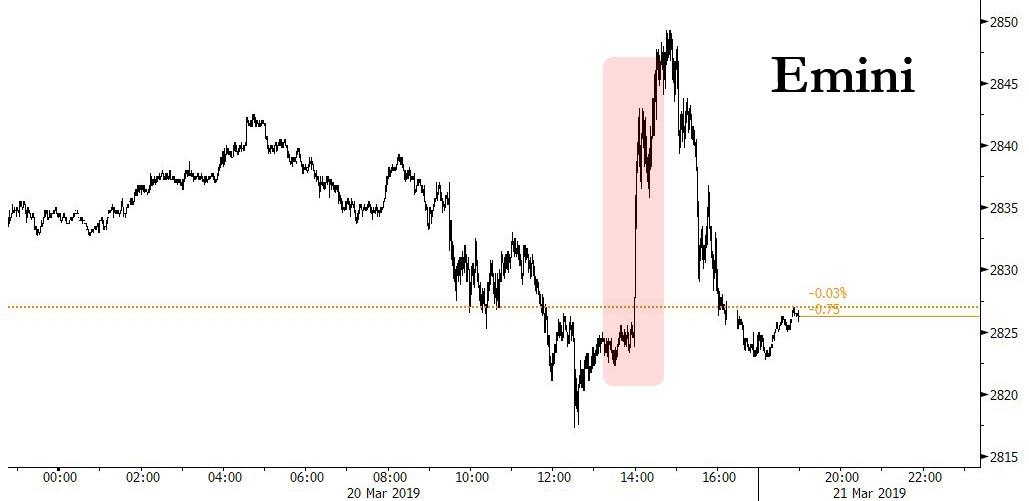

- S&P 500 futures little changed at 2,826.75

- STOXX Europe 600 down 0.2% to 380.25

- MXAP up 0.5% to 161.13

- MXAPJ up 0.3% to 530.58

- Nikkei up 0.2% to 21,608.92

- Topix up 0.3% to 1,614.39

- Hang Seng Index down 0.9% to 29,071.56

- Shanghai Composite up 0.4% to 3,101.46

- Sensex up 0.06% to 38,386.75

- Australia S&P/ASX 200 up 0.03% to 6,167.17

- Kospi up 0.4% to 2,184.88

- German 10Y yield fell 4.2 bps to 0.042%

- Euro down 0.2% to $1.1395

- Italian 10Y yield rose 3.2 bps to 2.172%

- Spanish 10Y yield fell 4.9 bps to 1.115%

- Brent futures up 0.1% to $68.59/bbl

- Gold spot up 0.4% to $1,318.32

- U.S. Dollar Index up 0.3% to 96.06

Top Overnight News

- Federal Reserve Chairman Jerome Powell said interest rates could be on hold for “some time” as global risks weigh on the economic outlook and inflation remains muted. Officials also decided to slow the drawdown of the U.S. central bank’s bond holdings starting in May, then end them in September

- In a dramatic address to the nation from her 10 Downing Street office on Wednesday, Theresa May hinted that she could even resign rather than agree to a lengthy postponement that would keep the U.K. in the bloc beyond the middle of the year. An emergency summit has already been penciled in for next week when the EU could propose a long extension to the negotiations, but with conditions attached, potentially including ripping up May’s proposal, calling a British election and even a second referendum

- Bank of England policy makers face more paralysis amid turmoil over the date of Britain’s departure from the European Union. Officials are likely to vote unanimously to hold the benchmark interest rate at 0.75 percent when they announce their decision at noon in London Thursday

- President Donald Trump said he’ll keep tariffs on China until he’s sure Beijing is complying with any trade deal, refuting expectations that the two nations will agree to roll back duties as part of a lasting truce to their trade war

- Australian unemployment dropped to a decade-low in February, defying the worst housing slump in a generation that’s forced a sharp slowdown in economic growth

- Dutch Prime Minister Mark Rutte’s coalition government is set to lose its majority in the Senate, with anti-EU party Forum for Democracy making a strong debut, highlighting the challenge leaders face in tackling populism two months before key European Parliament elections

- New Zealand has banned military style semi-automatics and assault rifles and will establish a nationwide buyback of the weapons in the wake of a terrorist attack on two mosques that left 50 people dead

- Norway’s central bank raised its main interest rate for a second time since September and signaled there’s more tightening to come, as western Europe’s biggest oil exporter lets a rebound in crude prices steer monetary policy. The krone appreciated as much as 1.1 percent against the euro after the decision

- The Swiss National Bank kept rates on hold, cut its inflation forecast and said it will remain active in the currency market to curb any appreciation in the Swiss franc

Asian equity markets eventually traded mostly higher in the aftermath of a dovish FOMC, which immediately supported risk sentiment, although the gains in the major US indices were later pared due to underlying growth and trade concerns. ASX 200 (Unch) was subdued as financials tracked the underperformance of their US counterparts post-FOMC and with a broad subdued tone across most sectors aside from commodity-related names. Elsewhere, Hang Seng (-0.8%) and Shanghai Comp. (+0.4%) remained afloat with CITIC Securities suggesting increased possibility of a PBoC rate cut following the dovish Fed stance, although gains were capped amid lingering trade uncertainty as US President Trump recently suggested tariffs on China will be kept in place for a “substantial” amount of time after a trade agreement is struck to ensure Beijing holds up its end of the bargain. As a reminder, Japanese and Indian markets were shut for Vernal Equinox and Holi respectively.

Top Asian News

- China Closes in on Plane Order From Africa Amid Overseas Push

- Fed’s Longer Pause Opens Door for Asian Central Banks to Cut

- Philippines Holds Benchmark Rate as Inflation Eases Into Target

- China Mobile Slides to Biggest Loss Since October After Earnings

Major European indices are mixed, but are generally little changed [Euro Stoxx 50 U/C], following the dovish FOMC; which has led to underperformance in financial names with the sector significantly lagging its peers and the likes of Lloyds (-2.8%) and RBS (-5.3%) underperforming (RBS are trading ex-dividends). The FTSE 100 (+0.3%) has been supported from the open by a rebound in material names such as Fresnillo (+5.3%), Antofagasta (+2.6%) and Glencore (+2.2%); with the broader sector outperforming its peers in a turn around from the significant underperformance seen yesterday in the material sector which was attributed to Vale surpassing a key milestone in resuming production. Other notable movers include, Inmarsat (+2.1%) in the green after speculation surrounding a counterbid for the Co. after reports yesterday that investors made a bid valued at GBP 2.5bln. At the bottom of the Stoxx 600 are IG Group (-7.6%) after poor earnings figures and the Co. stating they expect FY revenue to be lower than the priors. Separately, Skanska (-2.6%) are lower as the Co. states that they are not likely to hit their 2019-20 construction margin target.

Top European News

- Feud Erupts at EssilorLuxottica After Del Vecchio Cries Foul

- Deutsche Bank Vows More Wealth Management Hires to Reverse Flows

- Ted Baker Falls After Meeting Lowered Full-Year Estimates

- Sweden Moves Closer to Divesting $7.5 Billion Telia Stake

In FX, In stark contrast to the dovish FOMC and steady SNB, the Norges Bank delivered the 25 bp hike flagged at the start of the year and signalled another ¼ point tightening for the 2nd half of 2019 before 2 more next year. The accompanying statement was also more upbeat/hawkish than most expected, with upgrades to growth forecasts and 2019 core CPI, while the Board added that the domestic economy may even expand faster than previously envisaged. Moreover, Governor Olsen went one step further by assigning better than even odds of a 25 bp hike in June, and Eur/Nok has slumped in response from around 9.6900 to just over 9.5900 at one stage.

- DXY – The broad Dollar and index have pared some post-Fed losses, albeit mainly due to several rival G10 currencies failing to build on gains at the expense of the Greenback. Indeed, Usd/majors are somewhat mixed as the DXY reclaims 96.000 status, just. To recap, the FOMC was more dovish than expected given no further policy normalisation this year vs 2 hikes previously and confirmation that QT will end sooner than planned, with a slower monthly run-off from May and end by September.

- NZD/AUD/JPY – The other big beneficiaries of Usd weakness, with the Kiwi reclaiming the 0.6900 handle and gleaning independent support to a mostly solid NZ Q4 GDP update, while the Aussie is firmly back above 0.7100 as sub-forecast jobs growth in February was countered by a near 8 year low unemployment rate. Elsewhere, Usd/Jpy has reversed sharply through 111.00 and to the lower end of a 110.75-30 range as US Treasury yields recoil in wake of the aforementioned Fed policy shift.

- CAD/CHF/EUR/GBP – All underperforming to varying degrees, as the Loonie failed to sustain momentum through 1.3300 and the Franc resists advances towards 0.9900 in wake of the SNB quarterly policy review that maintained a high value assessment of the Chf amidst still fragile FX market conditions and the ongoing need for NIRP alongside close monitoring and intervention if needed. Meanwhile, the single currency has faded ahead of 1.1450 having cleared a Fib level at 1.1420 temporarily, and now looks prone to hefty option expiries at 1.1400 in 2.8 bn, with further upside attempts potentially capped by similar size between 1.1415-30 (2.9 bn). Turning to the Pound, Brexit remains the overriding issue and currently a mainly negative factor given even more uncertainty surrounding the conclusion and whether the EU is willing to grant an A 50 extension. Indeed, Cable only got a knee-jerk lift from better than forecast UK retail sales data before extending losses from 1.3200+ to circa 1.3135.

In commodities, Brent (-0.3%) and WTI (-0.3%) are marginally softer, and remain affixed within a USD 1/bbl range. WTI did surpass the USD 60.0/bbl level overnight on the back of a dovish FOMC, however the complex has since drifted somewhat with WTI now trading just below the key level. Regarding the 9.6mln draw in EIA Crude Inventories reported yesterday, UBS note that this is bullish in respect to both the API’s 2.1mln draw and compared to the 5yr average for this period; of around +5.4mln. Gold (+0.4%) is firmer, although off of session highs of around USD 1320/oz, on the back of dollar weakness after yesterdays dovish Fed, base metals more broadly have garnered support from the weaker dollar with copper rising to around a 3-week high overnight. Elsewhere, Barclays note that the risks surrounding iron ore have not dissipated following the reopening of Vale’s Brucutu mine as two others have been temporarily closed recently and there is a risk of further mine closures.

US Event Calendar

- 8:30am: Philadelphia Fed Business Outlook, est. 4.8, prior -4.1

- 8:30am: Initial Jobless Claims, est. 225,000, prior 229,000

- 8:30am: Continuing Claims, est. 1.77m, prior 1.78m

- 9:45am: Bloomberg Consumer Comfort, prior 60.8

- 9:45am: Bloomberg Economic Expectations, prior 54.5

- 10am: Leading Index, est. 0.1%, prior -0.1%

DB’s Jim Reid concludes the overnight wrap

This week’s serenity in markets was broken yesterday by a dovish FOMC outcome and the latest Brexit developments. It’s hard to call anything surprising in Brexit terms unless we discovered that Aliens had landed on top of the Houses of Parliament and had taken over proceedings. Anything other than this might raise an eyebrow or two but not have much shock value given all the surprises seen in recent months.

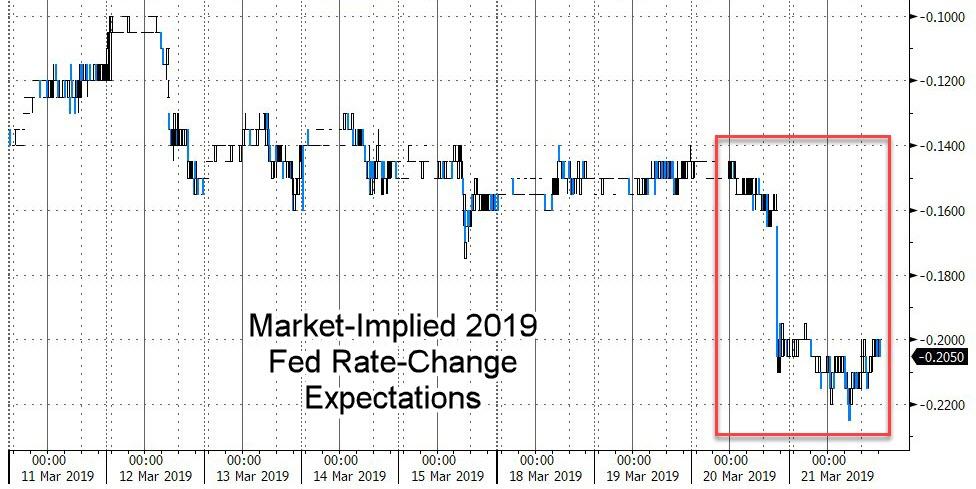

Anyway, first the Fed. They lowered their interest rate projections for this year and next, with the median forecast now calling for zero hikes in 2019 and one in 2020. That was below the consensus expectation, and two- and ten-year treasury yields fell -7.3bps and -9.0bps respectively. That pushed 10-year yields to their lowest level since January 2018, with yesterday’s fall the sharpest since last May. Also helping this move was growth and inflation being revised down and UST bullish news on the balance sheet (more below). The sharp rally didn’t stop the MOVE treasury volatility index reaching a new all-time low last night. The dollar weakened steeply, falling -0.42% and to its lowest level since February 4. Equities had been trading much weaker, mirroring the moves in Europe (more below), but rebounded sharply and into positive territory after the dovish outcome but then faded again into the close. The S&P 500 and DOW were -0.29% and -0.55% weaker, respectively, while the NASDAQ eked out a +0.07% gain. That leaves Mr Powell 8-1 down in terms of US equities on FOMC days under his leadership. 7-0 in 2018 and 1-1 in 2019. Elsewhere Emerging markets outperformed after the Fed though, with equities up +0.16% and currencies gaining +0.69%.

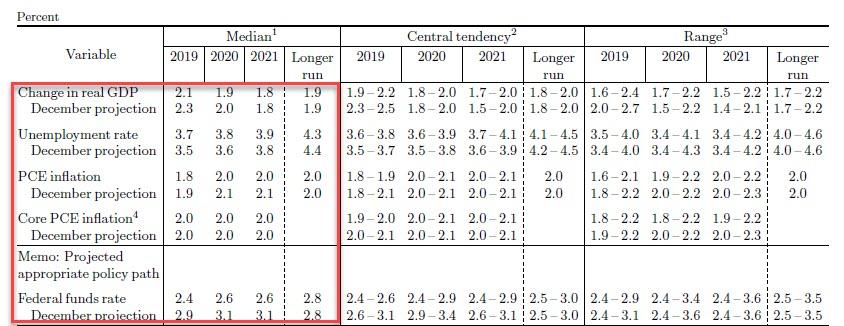

Apart from the headline change in the Fed’s interest rate projections, they also lowered their growth and headline inflation forecasts. The median expectation is now for growth of 2.1% and 1.9% for 2019 and 2020, down from 2.3% and 2.0%. Headline inflation projections are at 1.8% and 1.9%, from 1.9% and 2.1%. So overall a slightly less optimistic baseline to underlie the lower interest rate path. At the press conference, Chair Powell maintained his recent rhetoric, noting that “growth is slowing somewhat more than expected” and “financial conditions remain less supportive.” He also cited the persistent inflation undershoot and downside risks from Brexit and trade as reasons for the pause in rate hikes. In light of these dovish changes, our US economics team has updated their Fed call, and now think that the Fed will remain on hold through end-2020. However, their economic forecasts are still a bit more robust than the Fed’s, so they think the risks to their new view are still skewed toward the next move being another hike rather than a cut. Their full meeting review is available here .

Finally, the Fed also announced updates to their balance sheet policy, with a gradual taper in the runoff now planned. The caps on Treasury runoff will fall from $30bn to $15bn in May, which will entail more reinvestments each month. The MBS portfolio will be rolled into Treasuries as they mature, which will provide a further boost to the Fed’s Treasury purchases. New purchases will match the existing maturity structure of the Treasury’s outstanding debt stock, so it should be neutral for the curve. The balance sheet will thefore stabilize starting in October, though the Fed will re-examine the policy again over the course of this year. At some point, they will resume asset purchases as well, to accommodate increased demand for currency while maintaining the same level of excess reserves.

Overnight, sentiment has improved in Asia with markets making modest advances after the dovish tilt from the Fed. The Hang Seng (+0.18%), Shanghai Comp (+0.61%) and Kospi (+0.28%) are all up. China’s onshore yuan is up +0.18% at 6.6825, marking the strongest level since July 2018. Elsewhere, futures on the S&P 500 are also up +0.08%. Japanese markets are closed for a holiday.

After the FOMC and press conference was over, all of us in the U.K. crowded round our TVs and stopped what we were doing as she made a planned televised address to the nation. To be fair there wasn’t much she hadn’t said before and she continues to double, triple and quadruple down on her strategy. She has asked the EU to extend the Brexit deadline until June 30, but was pretty insistent that she would not be willing to go beyond that date. It’s therefore hard to see her continuing in office beyond that date, if her deal can’t pass before then. Election risks must have risen in recent days.

Before this, PM May sent the EU a letter formally asking for an extension of the Brexit deadline to June 30th. European Council President Tusk said in a press conference that a short extension would be possible, conditional on the UK Parliament passing a deal. If the UK does not pass a deal, it appears that Parliament will face a choice of either a long extension, or a no-deal exit. Reuters also reported that a Commission document stated that the EU only wanted to offer one extension (as opposed to an extension of the extension situation). We’ll find out more after the EU council meeting today and tomorrow. EU officials confirmed that May’s request came too late to make a full decision on it at today’s EU council meeting which makes it likely that it won’t be approved by the EU today. It’s likely that the option is left open until at an emergency Council meeting next week with the duration of any extension contingent on whether or not May passes the MV next week. A reminder that the U.K. is currently still on course to leave a week tomorrow 1001 days after the original vote.

Sterling weakened as much as -0.91% as the various developments took place yesterday, but ultimately ended the session -0.59% weaker at $1.3190 partly as the FOMC weakened the dollar. Oliver Harvey published his latest update yesterday (available here ), where he turned neutral on the pound. He thinks the odds of a no-deal Brexit have risen to 20%, and now views a long extension of Article 50 as a net negative for the currency. Such an extension would alleviate the near-term risks around Brexit, but would raise the odds of a new election and would therefore inject new political and policy uncertainty into the UK.

Elsewhere yesterday, Brent crude oil prices rose +1.85% to a new four-month high at $59.83 per barrel after US inventories fell by 9.59million barrels. That takes the cumulative decline in US stockpiles this year to -1.9mn barrels, which is the biggest drop since 2003. Usually, inventories rise in the winter, with the 25-year average for this point in the calendar at +16mn. The move helped US energy stocks advance +0.89%.

Markets in Europe yesterday were broadly lower on the back of a number of stock specific stories. The CEO of UBS (-2.41%) called Q1 “one of the worst” in recent history, BMW (-4.94%) warned that earnings will decline “well below” last year’s level, and Bayer (-9.61%) lost a ruling over a weed killer case. A big slump for FedEx (-3.51%) following a profit warning Tuesday evening also contributed to the early weakness yesterday morning. The STOXX 600 eventually ended -0.90% while the DAX ended -1.57%, both with their biggest one-day declines since February 7th. In rates, Bunds nudged down another -1.3bps also.

Before we wrap up, the only data that was out yesterday of any note came in the UK where core CPI in February printed slightly below expectations at +1.8% yoy (vs. +1.9% expected), and down one-tenth from January. Headline CPI has a touch higher than expected but at 1.9% YOY its still below 2%. The March CBI total orders data was also slightly on the softer side having fallen 5pts to +1 (vs. +5 expected).

Looking at the day ahead, this morning in the UK we’ve got February retail sales and public-sector net borrowing due out. That comes before the BoE meeting where no policy change is expected and given all the Brexit developments it’s hard to imagine being much of a game changer. This afternoon we’ve also got the March consumer confidence reading for the Euro Area while in the US we’ve get the March Philly Fed business outlook print, latest weekly initial jobless claims reading and February leading index. In all likelihood, the biggest event for markets today will be the EU Council meeting.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 10.82 POINTS OR 0.01% //Hang Sang CLOSED DOWN 249.41 POINTS OR 0.85% /The Nikkei closed HOLIDAY/ Australia’s all ordinaires CLOSED UP .03%

/Chinese yuan (ONSHORE) closed UP at 6.6917 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 58.40 dollars per barrel for WTI and 67/28 for Brent. Stocks in Europe OPENED RED

ONSHORE YUAN CLOSED UP // LAST AT 6.6917 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6946 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a SOUTH KOREA/

A good indicator telling us that the global economy is drying up: South Korean chip exports collapse by 25%

(courtesy zerohedge)

South Korean Chip Exports Collapse 25% – Worst Since 2009

South Korea’s exports are headed for another monthly drop amid slowing economic growth in China and weak demand for semiconductors, preliminary trade data for March shows.

The preliminary data – for the first 20 days of the month – saw exports fell 4.9% from a year earlier, putting them on course for a fourth consecutive monthly decline.

Imports in the first 20 days of March fell 3.4%, from a year earlier.

Shipments to China slid 12.6% while overall sales of semiconductors, a key driver of Korea’s economy, decreased by 25& – the biggest YoY decline since March 2009…

South Korea is one of the world’s key component suppliers in the tech sector and the continued slowdown in the expansion of semiconductor exports deepens concerns about the outlook for the global technology industry.

Not helped by the plunge in DRAM prices…

As a reminder, South Korea releases its trade data earlier than most other major economies and is a key link in the global supply chain, making it a bellwether for trade.

“Beijing is Seoul’s largest trading partner, with exports to China amounting to about 10 percent of Korea’s GDP,” said Bloomberg Economics’ Justin Jimenez.

“Our base case is that a continued cool down in Sino-U.S. tensions will provide some relief to China’s economy — and in turn, South Korea’s. A breakdown in talks though, remains the key risk.”

Bloomberg’s Justin Jimenez notes that “a double-digit drop in South Korea’s exports in February highlights risks for the trade-oriented economy…” but offers a glimpse at a potential green shoot – based on actual data – “…though a potential recovery in semiconductor demand and signs of stabilization in China’s economy may help to support South Korea’s exports in 2H.”

South Korea’s economic growth rate has been slowing and is likely to continue to do so unless there is a pickup in exports. A delegation from the International Monetary Fund said last week that Korea’s economy faces headwinds and should consider a “substantial” supplementary budget to meet its growth target of 2.6 percent to 2.7 percent for this year.

end

3 b JAPAN AFFAIRS

3 C CHINA

4.EUROPEAN AFFAIRS

We may get our “no deal” Brexit if the EU will not allow an extension. England is in a mess right now

(courtesy zerohedge)

Cable Slides As Civil War Looms – 17.4 Million Voted For Brexit & Are Being Denied It

Theresa May is meeting with EU leaders in Brussels, “working extremely hard,” according to her spokesperson, as a standoff between the UK PM and the EU over a Brexit delay has put the prospect of a cliff-edge departure back in play for British companies.

“If you’re a business now thinking no-deal was off the table,” Wednesday’s events “will be a bit of a shocker,” said Mats Persson, head of Brexit strategy at EY in London.

“If the EU doesn’t grant Parliament an extension, no-deal happens.”

This has put pressure on cable this morning…

May asked the EU for a three-month delay of the Brexit deadline to June 30. While she makes her case to EU leaders at a summit today, European Council President Donald Tusk has already said such a short extension would only be possible if the U.K. Parliament agrees to enact the existing divorce deal – which it’s twice rejected – by the current exit day of March 29.

But, as George Galloway fears below, the ongoing chaos could be a recipe for civil war…

I’ve known Speaker Bercow since he was a young man, wore a ‘Hang Nelson Mandela’ t-shirt, and was a secretary of the Monday Club – a conservative group so conservative that they’re probably wearing ‘Hang Bercow’ t-shirts today.

By all objective standards Bercow has been a poor speaker of the Commons. What you perhaps don’t know is that is testimony to the chilling effect of laid back liberalism.

Bercow has had an easy ride because he’s biased against a government so incompetent that if it were a “Carry-On” film you wouldn’t want it to end. But it isn’t and most people want it to end as swiftly as possible.

Thus, his devastating “pronunciamento” against the prime minister this week has proved wildly popular on the simple basis that anything which devastates this government must be right. But it is wrong.

Britain famously lives in the past, but basing parliamentary maneuvers on a 1604 precedent last used in 1920 is comedy gold but not 21st century governance. Even Jacob Rees-Mogg wasn’t around in 1604 (though he may have voted ‘against’ in the 1920 debate).

It’s simply not true that no matter can be brought back in the same form, in the same parliamentary session. If it were, Mrs. May would not have suffered her second defeat on her Brexit plan.

Not having a constitution, as Britain doesn’t, has at least the compensation of flexibility, of adapting to new situations. Of not being hidebound. Speaker Bercow just bound Mrs. May’s hide like it was 1599.

Because there was a new situation. Very new, since her second defeat parliament had taken ‘no deal’ off the table and sought an extension to Article 50, thus postponing Brexit. That’s pretty big news.

Moreover, and consequently, May’s Brexit deal now has a 50/50 chance of going through. That’s a new situation alright!

Having stared down the barrel of no Brexit at all, both the DUP allies and the ERG enemy within her party were beginning to decamp back under her tent. It cannot be right that one single man can pervert the course of governance on an entirely bogus basis when that man cannot be removed and doesn’t seek election.

The English fought a Civil War over that kind of thing not that long after 1604 and long before 1920. It ended with the parting of the king’s head from his shoulders.

17.4 million people voted for Brexit and are being denied it. That sounds like a recipe for civil war to me and the British rulers should remember what happened as a result of the last one.

Now, I am wholly against Theresa May’s Brexit deal on the simple basis that it isn’t Brexit at all. It is Brexit in name only. I may have been the first to give it a name, BRINO. I may have been the first to state also that I would rather be IN the EU and carry on the fight than OUT of the EU on Mrs May’s terms.

I am wholly against the British government on everything else too. I seek a general election and the sweeping of this gang that couldn’t shoot straight off the stage altogether. But I can’t associate with Bonapartism. And little Johnny Bercow is a “Poundland” Napoleon who isn’t even as nice as he looks. Watch out, sparks are about to fly!

Forget ‘Project Fear’, This Is What A “Hard Brexit” Could Mean For The UK

Authored by Patrick Barron via The Mises Institute,

When Britons voted on June 23, 2016 on whether or not to leave the EU there was no discussion of a “hard or soft Brexit”. These terms were invented after Brexit passed by a surprisingly large margin and the mostly anti-Brexit Tory Party government, especially its leadership, decided that it needed to negotiate the terms of leaving. Brexit supporters regard such terms as betraying the 2016 Brexit referendum itself. These 17.4 million Britons undoubtedly believed that Brexit would mean exactly that: Britain would no longer be governed by any EU laws, regulations, etc. Nevertheless, all that the world has heard since that day in June 2016 is a debate over the terms of leaving, with any so-called terms being labeled as a “soft Brexit” and leaving without any agreement as a “hard Brexit”.

In a “hard Brexit,” Britain just leaves and all EU regulations, etc. are null and void. It’s pretty clear cut. A “soft Brexit” can mean almost anything that is not a “hard Brexit”; i.e., Britain would agree to continue some or all of the manufacturing regulations, tariffs, and intergovernmental agreements — such as ceding jurisdiction to the European Court of Justice — that apply to EU countries. The list is almost endless and the time frame very nebulous, a perfect playground for those who wish to have a Brexit In Name Only. If there is to be Brexit of any sort, however, Parliament must act. Experts in British constitutional law claim that only Parliament can actually take Britain out of the EU and only Parliament can decide under what terms, if any, it will do so. Of course, one of the terms of separation could be that there are no terms of separation — thus, a “hard Brexit.”

The Effect on Imports

The current government has been exploring the possibility of dropping all import tariffs to zero except on “sensitive industries”. This would be very good for consumers, because the EU imposes tariffs on almost all imports from nations not in the EU itself. Most notably in its attempt to insulate inefficient European farms from worldwide competition, the EU imposes onerous tariffs on non-EU agricultural products via the Common Agricultural Policy (CAP). Eliminating these and many other tariffs would significantly lower the cost of living for the British people.The success of Brexit may depend entirely on whether Britain does in fact eliminate tariffs on most goods. It is a golden opportunity. The EU itself is very export oriented, so it is unlikely that it would impose any restrictions on member countries selling goods to Britain. So far so good!

The Effect on British Exports

Exports are another matter entirely. No longer in the tariff free customs union, it is assumed that the EU would impose tariffs on British products as it does on any other non-EU country, raising their cost to EU buyers, which one must assume would result in fewer British sales. The real harm would not fall on British exporters but on Britain’s EU customers, who now are forcibly prohibited from buying British goods at the previously advantageous price. On the other hand since it no longer must meet onerous EU manufacturing regulations, British industry might enjoy lower manufacturing costs which would enable it to sell more to non-EU countries. Although it might take time for Britain to develop new markets for its goods, some countries, led by the U.S. itself, have stated that they are ready to sign free trade agreements with Britain as soon as it leaves the EU.

The Effect on the City of London

The City of London is a massive global hub. Its banking and insurance companies are dominant in the EU and likely to remain so for reasons of depth of market knowledge and a high reputation for honesty and fair dealing. Although some companies have moved some operations to Frankfurt, it is unclear if these moves are significant in number and may be simply part of normal market flux. The same fears about the fate of the City were raised when Britain secured an opt-out from the 1992 Maastricht Treaty which formally created the euro. Unless the EU imposes some special tax or regulation prohibiting EU members from utilizing London firms, it is unlikely that the City will be much affected by a “hard Brexit”.

The Effect on Controlling borders