GOLD: $1312.75 UP $5.00 (COMEX TO COMEX CLOSING)

Silver: $15.41 DOWN 7 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1313.15

silver: $15.43

Comex options expire next week: Wednesday March 27

London/LBMA expires Monday March 31/2019.

The crooks continue with their whacking right in front of the authorities/regulators despite the criminal probe of precious metals manipulations.

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 0 NOTICE(S) FOR nil OZ (0.00 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 384 NOTICES FOR 38400 OZ (1.944 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1 NOTICE(S) FILED TODAY FOR 5,000 OZ/

total number of notices filed so far this month: 5380 for 26,900,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3987:UP $5

Bitcoin: FINAL EVENING TRADE: $3996 UP 16

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 0/0

MONTH TO DATE: 384

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST CONTINUES TO RISE FOR THE FOURTH CONSECUTIVE TIME: THIS TIME BY A SMALLER SIZED 580 CONTRACTS FROM 190,335 UP TO 190,915 DESPITE YESTERDAY’S STRONG 15 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 2175 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2175 CONTRACTS. WITH THE TRANSFER OF 2175 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2175 EFP CONTRACTS TRANSLATES INTO 10.787 MILLION OZ ACCOMPANYING:

1.THE 15 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 27.120 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

31,439 CONTRACTS (FOR 16 TRADING DAYS TOTAL 31439 CONTRACTS) OR 157.195 MILLION OZ: (AVERAGE PER DAY: 1964 CONTRACTS OR 9.824 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 157.195 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 22.45% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 522.58 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 580 WITH THE 15 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2157 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 2737 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2157 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 580 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 15 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $15.48 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.936 BILLION OZ TO BE EXACT or 134% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 27.120 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY ONLY 64 CONTRACTS, TO 516,180 DESPITE THE STRONG RISE IN THE COMEX GOLD PRICE/(AN INCREASE IN PRICE OF $6.00//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8040 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 8040 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 516,180. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8,104 CONTRACTS: 264 OI CONTRACTS INCREASED AT THE COMEX AND 8040 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 8104 CONTRACTS OR 810,400 OR 25.20 TONNES.

YESTERDAY WE HAD A GAIN IN THE PRICE OF GOLD TO THE TUNE OF $6.00....AND WITH THAT, WE HAD A HUGE GAIN IN TONNAGE OF 25.20 TONNES!!!!!!.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 111,627 CONTRACTS OR 11,162,700OR 347.185 TONNES (16 TRADING DAYS AND THUS AVERAGING: 6977 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAYS IN TONNES: 347.185 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 347.185/2550 x 100% TONNES = 13.61% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1216.18 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A TINY SIZED THAN EXPECTED INCREASE IN OI AT THE COMEX OF 64 DESPITE THE STRONG GAIN IN PRICING ($6.00) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8040 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8040 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 8104 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8040 CONTRACTS MOVE TO LONDON AND 64 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 25.20 TONNES). ..AND ALL OF THIS STRONG DEMAND OCCURRED WITH A RISE IN PRICE OF $6.00 IN YESTERDAY’S TRADING AT THE COMEX!!!!!

we had: 0 notice(s) filed upon for nil oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $5.00 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD/

INVENTORY RESTS AT 778.09 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 7 CENTS IN PRICE TODAY:

A BIG CHANGES IN SILVER INVENTORY AT THE SLV//

THE CROOKS ROB THE COOKIE JAR OF 1.356 MILLION OZ/ (WITHDRAWAL)

/INVENTORY RESTS AT 309.488 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A FAIR SIZED 580 CONTRACTS from 190,335 UPTO 190,915 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 2157 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2157 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 720 CONTRACTS TO THE 2157 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 2737 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 10.787 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 27.120 MILLION OZ FOR MARCH.

RESULT: A FAIR SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 15 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A FAIR SIZED 2157 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 2.69 POINTS OR 0.09% //Hang Sang CLOSED UP 41.69 POINTS OR 0.14% /The Nikkei closed UP 13.42 POINTS OR .09%/ Australia’s all ordinaires CLOSED UP .44%

/Chinese yuan (ONSHORE) closed DOWN at 6.7133 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 59.51 dollars per barrel for WTI and 67.25 for Brent. Stocks in Europe OPENED RED

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7133 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7201 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

a)This is not going to happen: North Korea is demanding the USA remove weapons from Guam and Hawaii. What planet is Kim on anyway? This is escalating!!

(zerohedge)

(courtesy zerohedge)

b) REPORT ON JAPAN

3 C/ CHINA

i)Not good: another horrifying blast at a Chinese chemical plant kills 47 and injures a whopping 650 poor souls

( zerohedge)

the uSA preparing for a military conflict with China in the South China seas?

( zerohedge)

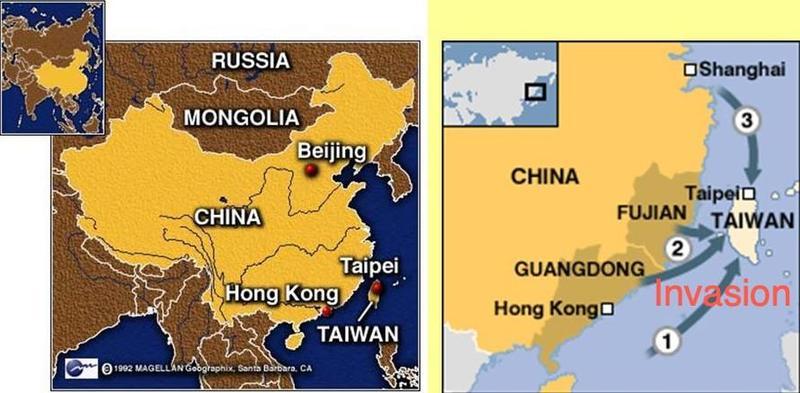

iii) Taiwan seeks to buy 100 main battle tanks as it believes that China will invade:

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)UK

The pound rallies as the EU only gives them a 2 week “unconditional'” Brexit delay. What difference will two weeks do?

( zerohedge)

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Russia is accusing the USA of stoking tensions by deploying 6 nuke capable bombers to Europe

( zerohedge)

6. GLOBAL ISSUES

CANADA

Looks like Canada will become the next Sweden as we witnessed the largest influx of immigrants since 1913 following Trudeau’s open door policy.

(courtesy zerohedge)

7. OIL ISSUES

Berman warns the USA oil patch to stop overproducing:

(courtesy Art Berman/OilPrice.com)

8 EMERGING MARKET ISSUES

Brazil

Very scary!! Brazilian nuclear fuel convoy attacked by gansters

(courtesy zerohedge)

9. PHYSICAL MARKETS

( Gata/Reuters)

ii)Ted Butler on the JPMorgan’s massive accumulation of silver on top of its massive short position. This is not a conspiracy as the CFTC confirmed the huge accumulation of silver by JPM

( Ted Butler/Cook/GATA)

iii)A super commentary from Alasdair Macleod on why we must accumulate physical gold. We must prepare for the next move in gold

(Alasdair Macleod/GATA)

iv)Paulson, the doorknob opposes Newmont’s bid for Goldcorp. The bozo owns huge amounts of GLD shares which has no gold inside the fund

( reuters/GATA)_

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

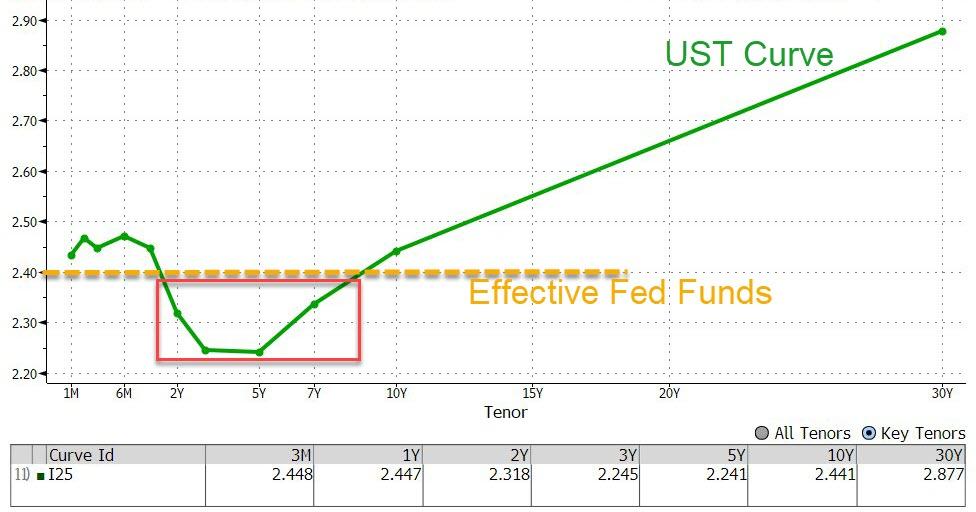

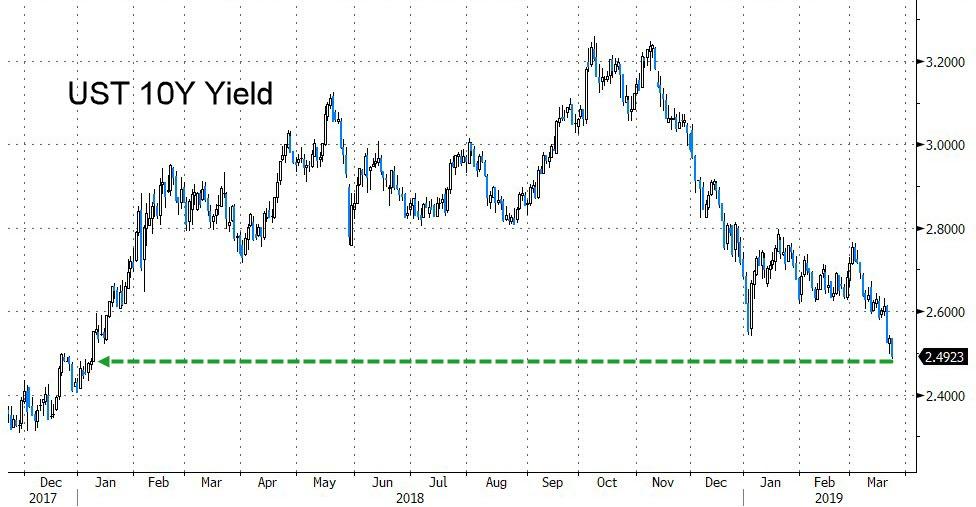

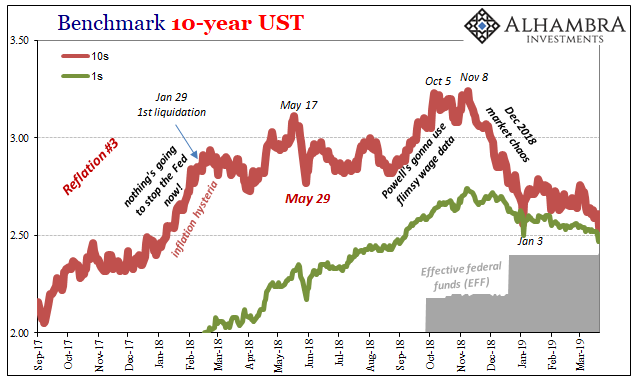

the 10 yr bond yield collapses to below 250 and that signals imminent recession..this is very dangerous

( zerohedge)

ii)Market data

a)There is no doubt that the Boeing fiasco will be a major hit on first quarter and then second quarter GDP

( zerohedge)

c)the only positive data today to report” existing home sales rise as mortgage rates tumble

( zerohedge)

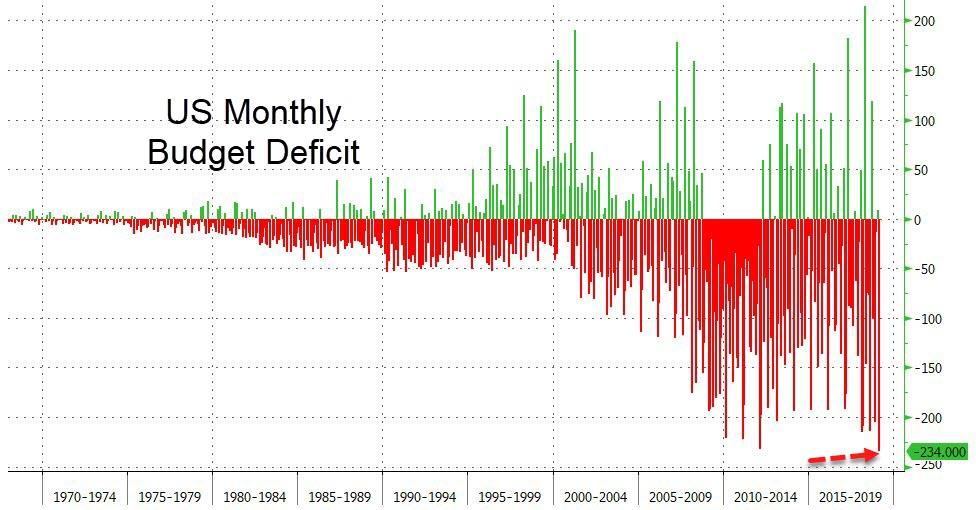

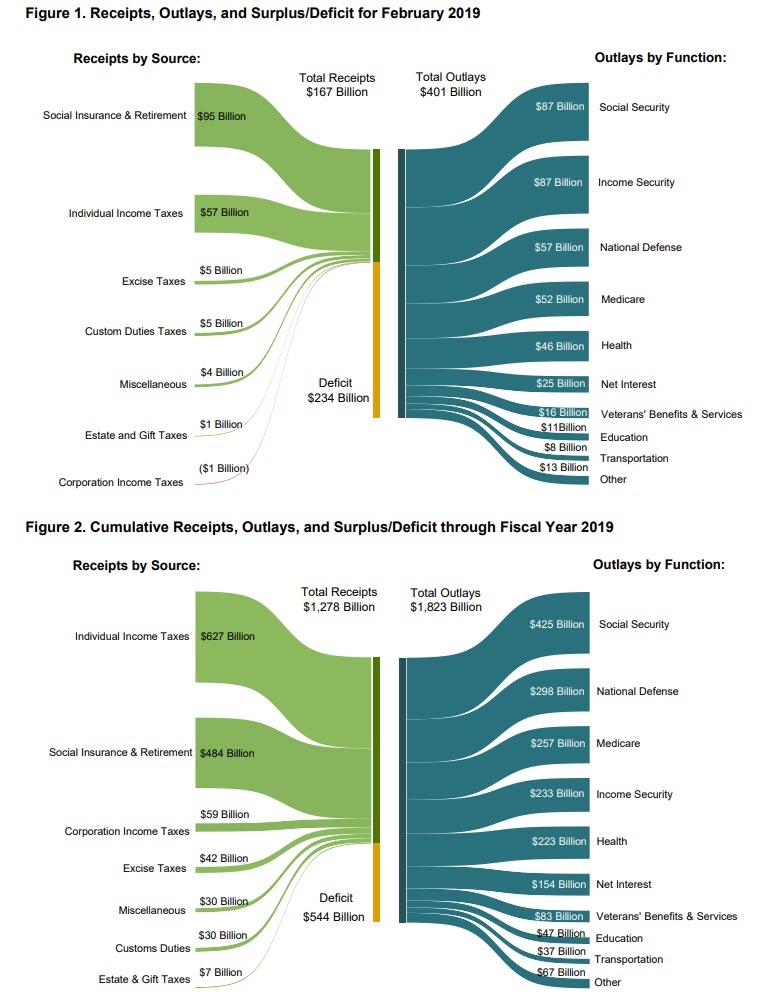

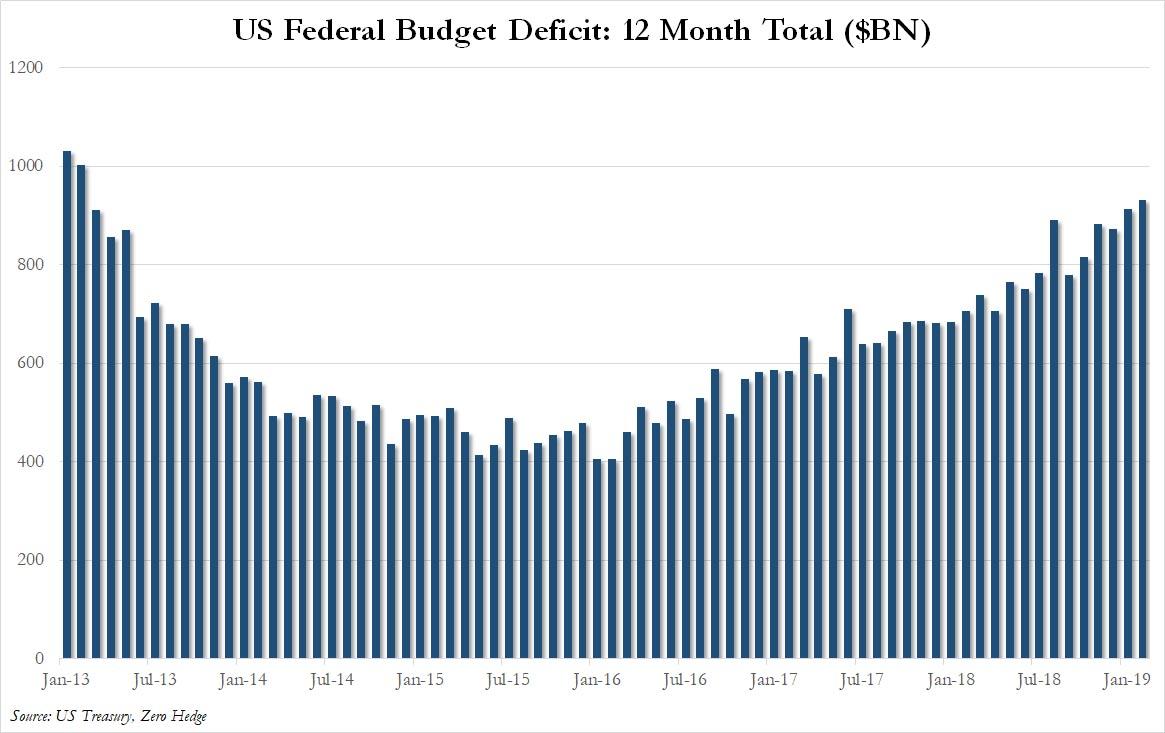

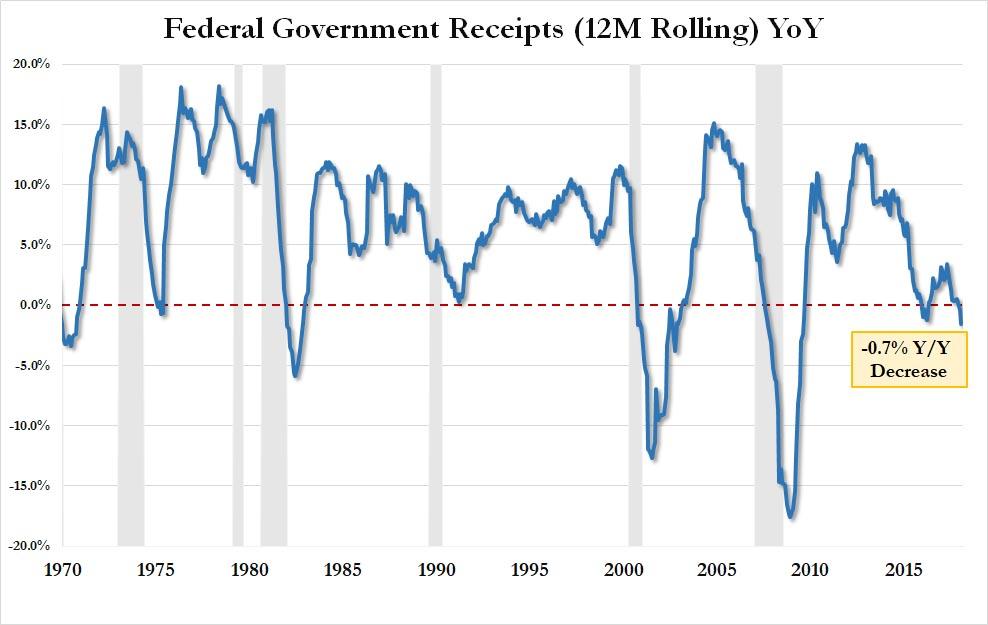

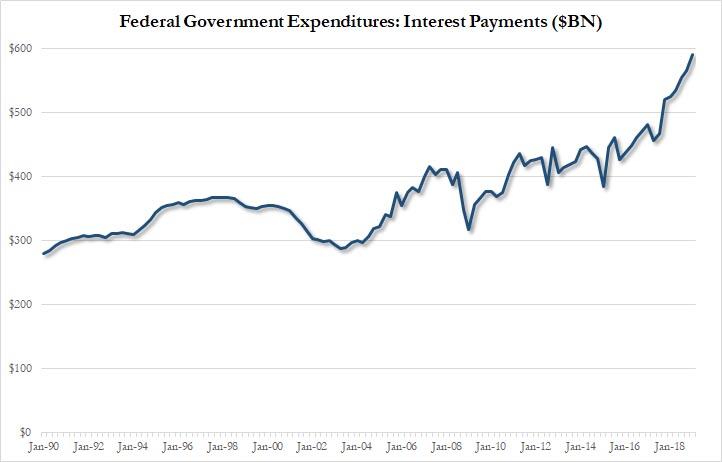

d)As promised to you, the USA budgetary deficit was going to rise this year. For the month of Feb which is a pretty bad month for treasury due to tax refunds being paid out: the deficit climbed to a record $234 billion dollars.

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

a)He is right: Gundlach states that the economy feels like 2007: he blasts the Fed’s unprecedented reversal

( zerohedge/Gundlach)

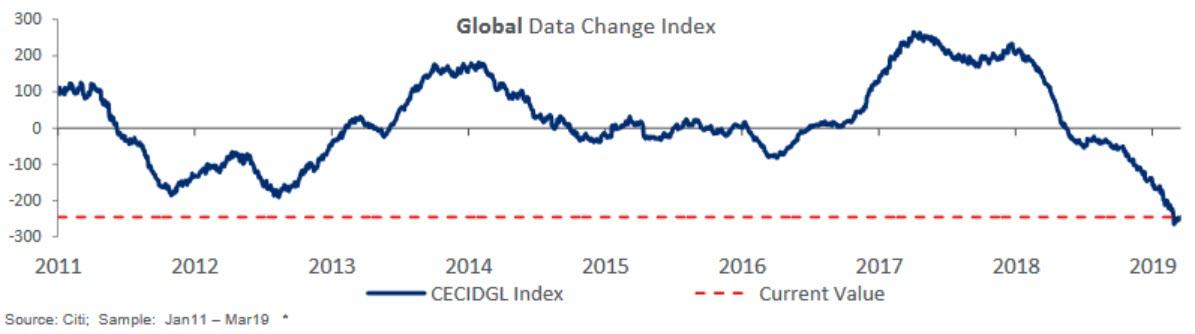

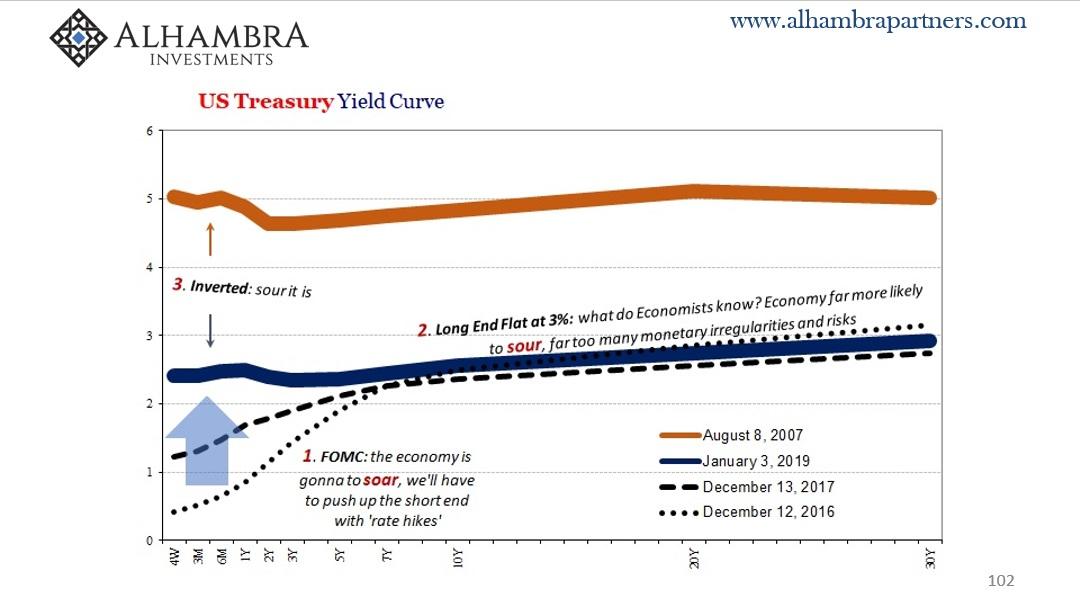

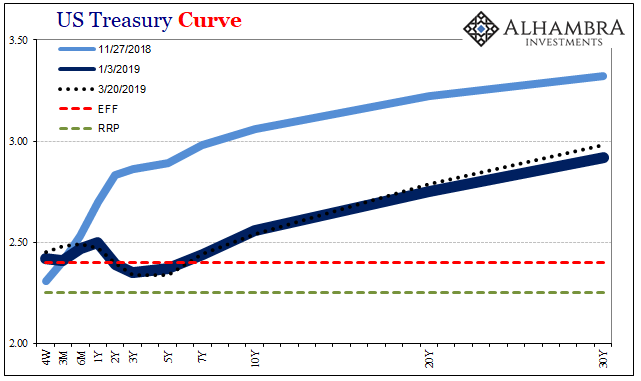

b) i BOND MARKET ARMAGEDDON

( jEFFREY SNIDER)

b ii:

c)The flooding that is occurring now in the Midwest is just the beginning. There is still a huge pile of snow waiting to melt which will saturate the rivers. This will threaten the USA food production

d)This is just the beginning…Indonesia Airlines just cancels hits $6 billion 737 Max order

iv)SWAMP STORIES

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL REMAINS AT 797 CONTRACTS FOR A LOSS OF 1 CONTRACT. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI FELL BY 786 CONTRACTS DOWN TO 135,925 CONTRACTS.

Russia Buys 1 Million Ounces Of Gold In February – Become Your Own Central Bank

The systemic challenges facing our planet and the five key ways to prosper in the coming global crisis are considered in our latest podcast.

– Political, financial, economic and monetary systems are failing and may collapse

– Our human built economic systems are dependent on the environment and ecology of the planet is threatened and in crisis

– Long held belief paradigms are being questioned and in crisis

– Old systems are collapsing in the age of information as we enter a new era of consciousness

– Read, learn, develop skills and yourself

News and Commentary

Gold settles at a one-week high on dovish Fed (MarketWatch.com)

Wall Street powers world stocks; dollar up on Brexit woes (Reuters.com)

U.S. effective fed funds rate rises above interest on reserves (the first time ever) (Reuters.com)

No-deal Brexit fears send pound to a one-week low (RTE.ie)

Russian Gold Stockpile Grows as Analysts Warn of Global Recession (CNN.com)

EU Stops No-Deal Crash Now, Kicking Can to April: Brexit Update (Bloomberg.com)

Overnight stock futures have been manipulated upward for years (MRamseyKing.com)

US Housing Hits A Brick Wall: “The House Price Deceleration Is Staggering” (ZeroHedge.com)

Gold Prices (LBMA PM)

21 Mar: USD 1,317.30, GBP 1002.99 & EUR 1,155.80 per ounce

20 Mar: USD 1,303.00, GBP 985.07 & EUR 1,147.81 per ounce

19 Mar: USD 1,308.35, GBP 985.06 & EUR 1,152.53 per ounce

18 Mar: USD 1,305.35, GBP 986.19 & EUR 1,150.01 per ounce

15 Mar: USD 1,302.35, GBP 981.55 & EUR 1,150.55 per ounce

14 Mar: USD 1,299.20, GBP 982.84 & EUR 1,148.88 per ounce

Silver Prices (LBMA)

21 Mar: USD 15.54, GBP 11.85 & EUR 13.64 per ounce

20 Mar: USD 15.32, GBP 11.58 & EUR 13.49 per ounce

19 Mar: USD 15.41, GBP 11.61 & EUR 13.57 per ounce

18 Mar: USD 15.38, GBP 11.60 & EUR 13.54 per ounce

15 Mar: USD 15.35, GBP 11.58 & EUR 13.56 per ounce

14 Mar: USD 15.23, GBP 11.52 & EUR 13.48 per ounce

Recent Market Updates

– Exclusive Offer Of 6 Months Free Storage In Zurich and Valuable Complimentary Gifts

– 5 Ways to Prosper In the Coming Crisis – Goldnomics Podcast

– Deutsche Bank and Commerzbank May Become EU’s “Too Big To Fail” Bank

– Happy Saint Patrick’s Day from GoldCore

– 188 Internet Shutdowns In 2018 Show Why Physical Gold Is Ultimate Protection

– Buy Gold as Basel III Means “Central Banks and Banks Are Going To Be Buying Gold”

– Invest In Gold Or Bitcoin – Which Is The True Store Of Value?

– Silver Bullion Is The Portfolio Insurance To Buy Now

– EU Isn’t Ready for the Next Recession

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Interesting: Citigroup is going to sell back the Venezuelan gold to Maduro. First of all where on earth will Maduro get the money as his exports of oil has been dwindling to zero. Gold is very tight and thus western central banks will probably seek to borrow his gold

(courtesy Gata/Reuters)

Citigroup to sell Venezuelan gold in setback to President Maduro, sources tell Reuters

Submitted by cpowell on Thu, 2019-03-21 00:35. Section: Daily Dispatches

Looks like the Western central banks need the metal pretty badly. Otherwise wouldn’t Citigroup keep the metal for itself, now that the price is rising?

* * *

By Mayela Armas and Corina Pons

Reuters

Wednesday, March 20, 2019

CARACAS, Venezuela — Citigroup Inc. plans to sell several tons of gold placed as collateral by Venezuela’s central bank on a $1.6 billion loan after the deadline for repurchasing them expired this month, sources said, a setback for President Nicolas Maduro’s efforts to hold onto the country’s fast-shrinking reserves.

Maduro’s government has since 2014 used financial operations known as gold swaps to use its international reserves to gain access to cash after a slump in oil revenues left it struggling to obtain hard currency.

…

In the past two years, however, it has struggled to recover its collateral.Under the terms of the 2015 deal with Citigroup’s Citibank, Venezuela was due to repay $1.1 billion of the loan on March 11, according to four sources familiar with the situation. The remainder of the loan comes due next year.

Citibank plans to sell the gold held as a guarantee — which has a market value of roughly $1.358 billion — to recover the first tranche of the loan and will deposit the excess of roughly $258 million in a bank account in New York, two of the sources said. …

… For the remainder of the report:

https://www.reuters.com/article/us-venezuela-politics-gold/citigroup-to-…

* * *

Join GATA here:

Mining Investment Asia

InterContinental Singapore Bugis Hotel

Singapore

Tuesday-Thursday, March 26-28

https://www.mininginvestmentasia.com/

Mines and Money Asia

Hong Kong Conference and Exhibition Center

Wan Chai, Hong Kong

Tuesday-Thursday, April 2-4

https://asia.minesandmoney.com/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Ted Butler on the JPMorgan’s massive accumulation of silver on top of its massive short position. This is not a conspiracy as the CFTC confirmed the huge accumulation of silver by JPM

(courtesy Ted Butler/Cook/GATA)

Ted Butler details JPMorganChase’s manipulation of the silver futures market

Submitted by cpowell on Fri, 2019-03-22 03:23. Section: Daily Dispatches

10:25a ICT Friday, March 22, 2019

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler, interviewed by Jim Cook of Investment Rarities, details his conclusion that JPMorganChase is behind the rigging of the silver futures market and has managed to amass a huge physical stockpile of the metal. While the U.S. Commodity Futures Trading Commission conducted a years-long investigation of the silver market and found no impropriety, Butler notes, the U.S. Justice Department has gotten a confession from a former trader for JPMorganChase that he manipulated both the gold and silver markets during the CFTC’s investigation and did so with the knowledge of his superiors.

The interview is headlined “On the Hot Seat” and is posted at GoldSeek’s companion site, SilverSeek, here:

http://silverseek.com/commentary/hot-seat-17609

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

On The Hot Seat

|

March 21, 2019 – 9:10pm

Jim Cook Interviews Ted Butler

Q: A minor analyst recently remarked that he didn’t believe any of the claims you make about market manipulation and called it conspiratorial stuff. What do you say about that?

A: That’s the main reason my arguments have never caught on in a big way. Nobody wants to be associated with a conspiracy. However, I draw my conclusion from government data like the Commitment of Traders report and the Bank Participation report. There’s nothing conspiratorial about the data and my conclusions are factual.

Q: You have cast JPMorgan as the main villain in a market manipulation of silver. Hundreds, maybe thousands of people have queried the main regulator, the CFTC, about this manipulation and they have never responded to anyone. Are they writing us all off as conspiracy nuts?

A: They would probably like to. The Justice Department just indicted a JPMorgan trader for spoofing and indicated their investigation of this highly manipulative tactic was ongoing. Normally this comes under the jurisdiction of the CFTC. Why did they miss or ignore this practice when I told them about it a hundred times? We need an explanation.

Q: JPMorgan would certainly claim they are doing nothing wrong.

A: For ten years they have held the largest short position on the COMEX and in collusion with other banks, they have acted to suppress the price. Meanwhile they have accumulated a vast hoard of physical silver in their own COMEX warehouse and elsewhere. I call this an illegal market manipulation on steroids. Somebody please tell me where I’m wrong.

Q: I believe JPMorgan would say that they are short along with hundreds of other traders. Nothing wrong with being short and nothing wrong with buying physical silver.

A: First of all, you have great concentration among 8 big banks on the short side. That’s collusion and a key ingredient in a price manipulation. These 8 banks are currently short more than 500 million ounces or two-thirds of all the silver produced in a year. No other commodity comes close to this.

Q: Why go short at such a low price?

A: It’s hugely profitable if you dominate the market. In ten years JPMorgan has never lost money on a short sale. I can document that, if anybody in the government cares. They’ve made billions doing this while never a losing trade, which anyone who knows anything about futures trading will tell you is absolutely impossible. You do that by cheating.

Q: I’m not going to ask you about the big counterparties who are the losers in these trades because we are running out of space. JPMorgan is showing nearly 150 million ounces of silver in their name in their COMEX warehouse. That’s more than the Hunt brothers owned in 1980. However, you claim they have 800 million ounces in total. You don’t have the same kind of solid documentation on this figure as you do on the 150 million in their warehouse. Don’t you think this hurts your credibility?

A: I’ve been focusing on the futures market and silver for more than 30 years. I’ve been scrutinizing JPMorgan’s activities closely for ten years. They acted to squash and suppress the price of silver while accumulating as much physical silver as they could. This is the ultimate market crime. Of course they have tried to hide this fact, but if you read my newsletter, you will see the kind of detective work I have used to track their acquisition of the greatest hoard of silver in the history of mankind.

Q: You are saying they grossly manipulated the market to set up a mind-boggling profit, right?

A: For every ten dollars that silver rises they make 8 billion dollars. They forced down the market and bought silver bars on the cheap to set themselves up for an astonishing profit.

Q: Any other evidence?

A: Take JPMorgan out of the short side and the price of silver would be much higher. That’s proof of manipulation in itself. Look at the government data. It’s conclusive. It’s illegal to conspire to suppress the price of a commodity in order to buy it at a lower price and reap a big profit after you close out your short sale.

Q: Might this never end?

A: Manipulations always end and I’m hopeful the Justice Department will be all over this. How can they not be? That would end the manipulation and set the price of silver free. That in itself will be something to behold.

Q: What do you say to people who are getting impatient waiting for this to happen?

A: Waiting does not diminish the incredible opportunity for gain that I believe exists in silver. People who own silver will be glad they waited. The coming price rise in silver will be talked about for decades.

Jim Cook is the President of Investment Rarities.

END

A super commentary from Alasdair Macleod on why we must accumulate physical gold. We must prepare for the next move in gold

(Alasdair Macleod/GATA)

Alasdair Macleod: Preparing for the next move in gold

Submitted by cpowell on Fri, 2019-03-22 04:47. Section: Daily Dispatches

By Alasdair Macleod

GoldMoney.com, Jersey, Channel Islands

Thursday, March 21, 2019

The global economic outlook is deteriorating. Government borrowing in the deficit countries will therefore escalate. U.S. Treasury data confirms foreigners have already begun to liquidate dollar assets, adding to the U.S. government’s future funding difficulties.

The next wave of monetary inflation, required to fund budget deficits and keep banks solvent, will not prevent financial assets suffering a severe bear market, because the scale of monetary dilution will be so large that the purchasing power of the dollar and other currencies will be undermined.

Failing fiat currencies suggest the dollar-based financial order is coming to an end. But with few exceptions, investors own nothing but fiat-currency dependent investments. The only portfolio protection from these potential dangers is to embrace sound money — gold. …

… For the remainder of the commentary:

https://www.goldmoney.com/research/goldmoney-insights/gold-preparing-for…

Gold – preparing for the next move

Note: this article is not and must not be construed as investment advice. It is analysis based purely on economic theory and empirical evidence.

The global economic outlook is deteriorating. Government borrowing in the deficit countries will therefore escalate. US Treasury TIC data confirms foreigners have already begun to liquidate dollar assets, adding to the US Government’s future funding difficulties. The next wave of monetary inflation, required to fund budget deficits and keep banks solvent, will not prevent financial assets suffering a severe bear market, because the scale of monetary dilution will be so large that the purchasing power of the dollar and other currencies will be undermined. Failing fiat currencies suggest the dollar-based financial order is coming to an end. But with few exceptions, investors own nothing but fiat-currency dependent investments. The only portfolio protection from these potential dangers is to embrace sound money – gold.

The global economy is at a cross-road, with international trade stalling and undermining domestic economies. Some central banks, notably the European Central Bank, the Bank of Japan and the Bank of England were still reflating their economies by suppressing interest rates, and the ECB had only stopped quantitative easing in December. The Fed and the Peoples’ Bank of China had been tightening in 2018. The PBOC quickly went into stimulation mode in November, and the Fed has put monetary tightening and interest rates on hold, pending further developments.

It is very likely this new downturn will be substantial. The coincidence of the top of the credit cycle with trade protectionism last occurred in 1929, and the subsequent depression was devastating. The reason we should be worried today is stalling trade disrupts the capital flows that fund budget deficits, particularly in America where savers do not have the free capital to invest in government bonds. Worse still, foreigners are now not only no longer investing in dollars and dollar-denominated debt, but they are suddenly withdrawing funds. According to the most recent US Treasury TIC data, in December and January these outflows totalled $257.2bn.[i] At this rate, not only will the US Treasury need to fund a deficit likely to exceed a trillion dollars in fiscal 2019, but the US markets will need to absorb substantial sales from foreigners as well.

In short, America is going to face a funding crisis.To have this funding problem coinciding with the ending of credit expansion at the top of the credit cycle is a lethal combination, as yet unrecognised as the most important factor behind both American and global economic prospects. The problem is bound to emerge in coming months.

While today’s trade protectionism is less vicious than the Smoot-Hawley Tariff Act, America’s drawn-out trade threats today are similarly destabilising. The top of the credit cycle in 1929 was orthodox; its principal effect had been to fuel a speculative stock market frenzy in 1927-29.

This time, the credit bubble is proportionately far larger, and its implosion threatens to be even more violent. Governments everywhere are up to their necks in debt, as are consumers. Personal savings in America, the UK and in some EU nations are practically non-existent. The potential for a credit, economic and systemic crisis is therefore considerably greater today than it was ninety years ago.

Bearing in mind the Dow fell just under 90% from its 1929 peak, the comparison with these empirical facts suggests we might experience no less than a virtual collapse in financial asset values. However, there is an important difference between then and now: during the Wall Street crash, the dollar was on a gold standard. In other words, the price-effect of the depression was reflected in the rising purchasing power of gold. This time, no fiat currency is gold-backed, so a major credit, economic and systemic crisis will be reflected in a falling purchasing power of fiat currencies.

The finances of any government whose unbacked currency is the national pricing medium are central to determining future general price levels. Just taking the US dollar for example, the government’s debt to GDP ratio is over 100% (in 1929 it was less than 40%). At the peak of the cycle, the government should have a revenue surplus reflecting underlying full employment and the peak of tax revenues. In 1929, the surplus was 0.7% of estimated GDP; today it is a deficit of 5.5% of GDP. In 1929, the government had minimal legislated welfare commitments, the net present value of which was therefore trivial. The deficits that arose in the 1930s were due to falling tax revenues and voluntary government schemes enacted by Presidents Hoover and Roosevelt. Today, the present value of future welfare commitments is staggering, and estimates for the US alone range up to $220 trillion, before adjusting for future currency debasement.[ii]

Other countries are in a potentially worse position, particularly in Europe. A global economic slump on any scale, let alone that approaching the 1930s depression, will have a drastic impact on all national finances. Tax revenues will collapse while welfare obligations escalate. Some governments are more exposed than others, but the US, UK, Japan and EU governments will see their finances spin out of control. Furthermore, their ability to cut spending is limited to that not mandated by law. Even assuming responsible stewardship by politicians, the expansion of budget deficits can only be financed through monetary inflation.

That is the debt trap, and it has already sprung shut on minimal interest rates. For a temporary solution, governments can only turn to central banks to fund runaway government deficits by inflationary means. The inflation of money and credit is the central banker’s cure-all for everything. Inflation is not only used to finance governments but to provide the commercial banks with the wherewithal to stimulate an economy. An acceleration of monetary inflation is therefore guaranteed by a global economic slowdown, so the purchasing power of fiat currencies will take another lurch downwards as the dilution is absorbed. That is the message we must take on board when debating physical gold, which is the only form of money free of all liabilities.

Gold can only give an approximation of the loss of purchasing power in a fiat currency during a slump, because gold’s own purchasing power will be rising at the same time. Between 1930 and 1933 the wholesale price index in America fell 31.6% and consumer prices by 17.8%.[iii] These price changes reflected the increasing purchasing power of gold, because of its fixed convertibility with the dollar at that time.

Therefore, the change in purchasing power of a fiat currency is only part of the story. However, the comparison between purchasing powers for gold and fiat currency is the most practical expression of the change in purchasing power of a fiat currency, because the choice for economic actors for whom gold has a monetary role is to prefer one over the other.

It is an ongoing process, about to accelerate. Chart 1 shows how four major currencies have declined measured in gold over the last fifty years. The yen has lost 92.4%, the dollar 97.42%, sterling 98.5%, and the euro 98.2% (prior to 2001 the euro price is calculated on the basis of its constituents).

The ultimate bankruptcy of currency-issuing governments, likely to be exposed by the forthcoming slump, will be reflected in another lurch downwards in currency purchasing powers.

Technical and market analysis of gold’s position

It should become apparent as time progresses that the price of gold in fiat currencies will continue to rise. The reasons are not yet clear to the consensus of portfolio investors and speculators, but it is likely that the more prescient among them will begin to realise that in the event of a significant recession, slump or depression, the dollar price of gold will rise substantially.

For the moment, they are likely to concentrate on timing, using technical analysis, rather than thinking through economic concepts. Chart 2 illustrates the current technical position.

Following its peak in September 2011, gold found a bottom at $1047 in December 2015. That was followed by a 31% rally to $1375 in July 2016, since when gold has established a triangular consolidation pattern. Last August, the price sold off to $1160, becoming oversold to record levels. That established the second point of a rising trend, marked by the lower solid line.

In February the gold price mounted a challenge to the upper parameter of the consolidation range before retreating to test established support at $1280-$1305, shown by the pecked lines.

There is a good chance that another attempt to break through the $1350 level will take place soon, and that it will succeed. The following bullet points sum up this positive case:

- The current rally commenced from a record oversold condition on Comex. The selloff was consistent with extreme selling exhaustion, indicating a major turning point.

- The net managed-money position on Comex indicates the gold contract is still moderately oversold. However, the April contract is running off the board, which means that some 200,000 expiring contracts are still to be sold, stand for delivery or rolled forward by the end of this month (March). This suggests a little more consolidation may be needed before gold advances to attempt a challenge on the $1350 level.

- The 55-day and 200-day moving averages recently completed a bullish golden cross, with the price above both signalling a bullish trend. A retest of the 55-day MA occurred at the beginning of this month and is normal.

- If, as the chart suggests, a triangle pattern is emerging, it is an ascending triangle, which is bullish. An ascending triangle has a flat top and a rising base. Admittedly, the top line declines slightly but not enough to put it in the class of symmetrical triangles, where the eventual break-out direction is less certain.

- It is possible for the gold price to trade another down leg within the confines of the triangle before making its final breakout to the upside. In which case, the gold price might decline towards the low $1200s before making its upwards break.

The possibility that the ascending triangle might need longer to play out leads to the common technical recommendation to wait until gold breaks through the $1350-$1365 level before buying for the next leg of the bull market.

Chart 3 gives a longer-term perspective of gold’s valuation. It is of the gold price adjusted by mine supply and for changes in the fiat money quantity. Simply put, FMQ is the sum of cash, bank deposits and savings accounts, and also bank reserves held at the Fed. It is the total amount of fiat money both in circulation and available for circulation.

In 1934-dollars, deflated by the increase in the fiat money quantity, gold has returned to the extreme lows seen on only two previous occasions. The first was when the London gold pool failed in the 1960s followed by the collapse of the Bretton Woods Agreement in 1971. At that time the decline in the FMQ-adjusted price of gold since 1934 was fuelled by monetary expansion until a point was reached which could go no further. This led to an explosive recovery taking the price of gold in adjusted terms back to 1934 levels.

The realisation that the dollar faced the prospect of uncontrolled price inflation forced the Fed to raise interest rates so that the banks’ prime rate exceeded 21% in December 1980. This was sufficient to prevent the gold price from further rises, and physical gold then became the collateral of choice for a developing carry trade. Central bank sales were designed to signal the demonetisation of gold and deter buyers. They leased significant quantities of bullion for the carry trade, which increased supply synthetically and drove the gold price back to the same extreme valuation lows seen in the 1960s. This was 2000-2002.

After rallying from these extreme lows to a nominal high in September 2011, an increase in derivative supply coupled with the banking and investment establishment retaining an increasingly rosy view of fiat currencies have been instrumental in returning gold to the valuation lows of the 1960s and 2000 – 2002.

It is in this context that the outcome predicted in Chart 2 should be considered. If, as argued earlier in this article, America and the rest of the world faces a global slump, a premium for physical gold is likely to arise relative to the systemic risks of holding gold substitutes, such as derivatives and even physically-backed ETFs. In that event, a return to the 1934 price level for gold in FMQ-adjusted terms before any further monetary dilution implies a nominal gold price of about $24,000.

This conclusion does no more than indicate an upper target for the price of gold adjusted for historic monetary inflation. If, as seems likely, a developing credit crisis occurs as a consequence of today’s events, the quantity of fiat money in issue will rise significantly from current levels as government debt is monetised. Therefore, given the extreme undervaluation of gold suggested by Chart 3, it is hard to see how the price of gold, measured in dollars, can go much lower.

Defining the gold market and vanishing liquidity

The gold market has three basic elements to it. There is an underlying stock of approximately 170,000 tonnes, increasing at about 3,000 tonnes a year. It is impossible to define how much of the total above-ground stock is monetary gold, not least because jewellery in Asia is bought as a store of monetary wealth and is used as collateral against loans. However, if we are to classify Asian jewellery as non-monetary gold, then monetary gold in the form of bars and coin is thought by many experts to represent between thirty and forty per cent of the total.Assuming a median estimate of 35%, this is 60,000 tonnes, of which 33,760 tonnes is stated to be in national reserves. This leaves an estimated 26,240 tonnes of investment gold in public hands, worth $1.1 trillion. Much of this can be regarded as being in long-term storage. For market purposes, the physical market on its own is relatively illiquid.

Secondly, there are regulated futures and options markets, the most important of which is America’s Comex. Currently, there are about 520,000 Comex contracts of 100 oz each outstanding, which are worth a total of $68bn. Options on futures total a further 220,000 contracts, which are impossible to notionally value, being puts and calls at varying strike prices.

Third, there are unregulated OTC derivatives, mostly forward contracts in London. The last Bank of International Settlements statistics estimated total gold forwards and swaps were valued at $419bn, over six times the size of Comex. In addition, there were $149bn of OTC options.

The liquidity is broadly confined to Comex, London forwards and other OTC media. These are all derivatives, with minimal physical settlement taking place. Consequently, the price of physical gold is not determined by the marginal supply and demand for bullion, but almost entirely reflects financial factors in the banking system. If financial market conditions return to an approximation of the 1929-32 period for the reasons described earlier in this article, there is likely to be a banking crisis, or at the very least a serious dislocation of financial markets. Therefore, it is possible that at the same time investment funds and private individuals seek to gain portfolio exposure to the gold price, they will be doing so while the means of doing so are contracting, or even disappearing altogether.

An outcome of this sort hinges on the depth and pace of economic deterioration. Time will tell as to whether the current rapid deterioration in the economic outlook goes on to replicate the 1929-32 precedent, but it is getting increasingly difficult to argue against it happening. In which case, the gold price could rise rapidly due to its current undervaluation, a shortage of monetary gold outside central bank reserves, systemic disruption of paper markets and a renewed pace of monetary inflation before the fiat-money investment community realises what is happening.

Portfolio switching from fiat to gold

If the combination of both a developing credit and trade crises leads to a modern version of the 1929-32 global economic slump, financial asset values will fall heavily. But this time, there is the additional factor of a renewed acceleration of monetary inflation, which at some point might offer some support to stock prices, at least in nominal currency terms. In every hyperinflation, an index of stock prices can perform well on this basis, but adjusted for the currency’s loss of purchasing power, stock prices actually suffer substantial losses.

That assumes, of course, the rest of the world’s economy is broadly stable, which is almost certainly not going to be the case in our scenario.

Additionally, the inflationary conditions of a fiat currency’s twilight moments involve the market imposing increasing levels of time-preference on everything, including bond prices. Therefore, the discount between market prices and final redemption values widens dramatically. Governments and other borrowers face a near-impossible funding task, unless they are prepared to pay increasingly higher interest coupons. Unlike the experience of the great depression when interest rates reflected those of gold, this time bond yields paid in fiat currencies will rise and continue rising.

This leads towards a different progression of notable developments compared with 1929-32. An approximate sequence of how these might evolve is described as follows:

1. Evidence of a looming recession becomes increasingly apparent. Central banks respond in their time-honoured way, by easing monetary policy and replacing stalling credit creation with extra base money. Government bond prices rise as they are seen to be the least risky investment in an uncertain economic outlook, and equities rally after an initial sell-off. At the same time, lending bankers observe increasing risk in commercial lending and respond by quietly withdrawing loan facilities from all but the largest manufacturers of goods and producers of services. This appears to approximate to the current situation.

2. With unsold inventory increasing, industrial production is reduced, and rising numbers of workers are laid off. Analysts revise their forecasts for corporate profits downwards, and the number of corporate failures increases. Bond dealers adjust their expectations of government borrowing, and quantitative easing is reintroduced by central banks to ensure government bonds can be issued at suppressed interest rates. At this stage, investors face a worrying combination of falling equity prices reflecting a deteriorating economic outlook, combined with unexpected monetary inflation in the form of QE.

3. Foreigners liquidate US investments in order to sell dollars (the reserve currency – this appears to have started early) and repatriate funds to support their base operations. Bond dealers facing a glut of government bond issues expect bond yields to continue to rise. Stock markets slide, and with it is a growing realisation that the recession is turning into a wealth-destroying slump.

4. As the markets’ demands for increased time-preference undermine all debtors’ finances, investors increasingly avoid bonds and equities, abandoning hope of any recovery in financial asset prices. Hedging into gold mines and gold ETFs gathers pace, and the purchasing power of gold continues to rise measured against both fiat currencies and against the commodity and energy complex.

5. Having fallen behind the time-preference demanded by markets, central banks are reluctantly forced to raise overnight interest rates to protect the currency and bring price inflation under control. They have no choice, but this is seen as capitulation by investors. Residential mortgage costs increase sharply, driving consumers into negative equity as property prices suffer from forced selling. In countries where the home has become the middle class’s principal asset, the effect on consumer spending is devastating. Governments end up bailing-out or bailing-in lenders while trying to moderate mortgage interest costs.

6. By now, the gold price measured in unbacked currency is beginning to discount a continuing acceleration in monetary inflation. The gold price will be at multiples of current levels in all currencies, including the dollar.

7. The sense of crisis escalates and mounting bad debts at the banks raise the prospect of a systemic banking crisis. Despite depositor protection schemes, depositors begin to take steps to reduce their bank balances. With the facility to encash bank deposits being strictly limited, alternatives to deposits in insolvent banks will be in high demand. These will be gold, silver and other perceived stores of value. Cryptocurrencies could come into their own as an escape route from holding deposits in the banking system.

8. Those who attempt to escape systemic risk by exchanging bank balances for alternatives are simply passing bank deposits to the vendors. This is fine, so long as vendors are happy to accept the systemic risk. If not, then prices of alternative stores of value must rise to compensate. A classic flight out of money into anything else develops and is made more urgent by the lack of a cash alternative.

9. The currency rapidly loses purchasing power, and it will be moving into its end-of-life. Government bonds will have lost nearly all their value, measured in gold, and governments will still be accelerating inflationary financing, because bond financing without the central bank buying them will not be possible.

During this process, with few exceptions financial assets will face annihilation. A further problem is failing banks are the custodians of stock entitlements, with few being directly registered in the beneficial owners’ names. At best, this leads to a temporary loss of ownership. At worst, it provides the means for confiscation.

An intense bear market destroys wealth. At some stage, investors will begin to realise their portfolios are almost totally exposed to fiat currency risk. The belief that inflation hedges, such as overweight equities and underweight bonds, offer protection against extreme monetary inflation will be disproved. Investors will need a radical new approach, using sound money as their performance criteria. This is cannot be an inflation index, which is likely to become increasingly manipulated by statistical method. It has to be gold, instead of rapidly depreciating fiat currency.

The problem investors will then face is mathematical. There are probably less than 30,000 tonnes of monetary gold, excluding Asian jewellery, in private hands, today worth about $1.1 trillion. According to The Boston Consulting Group[iv], in 2015 there were $71.4 trillion of portfolio assets, of which $36.1 trillion were in US dollars. With the monetary gold held outside government reserves being about 1.5% of portfolio assets, how do you replace non-performing fiat-currency dependent assets with a portfolio designed with sound money in mind?

This is why the return to sound money will destroy the West’s financial system, driving the purchasing power of gold higher, measured against commodities, goods and services, while that of paper fiat moves towards worthlessness. The destruction of financial wealth could easily compare with 1929-32, and if it wipes out fiat currencies will be even worse.

The removal of cash as an effective escape route for investors fleeing systemic risk turns systemic risk directly into a collapsing preference for money relative to goods, gold, cryptocurrencies and the rest. One it starts, it could happen quite quickly.

END

Paulson, the doorknob opposes Newmont’s bid for Goldcorp. The bozo owns huge amounts of GLD shares which has no gold inside the fund

(courtesy reuters/GATA)_

Paulson opposes Newmont’s bid for Goldcorp

Submitted by cpowell on Fri, 2019-03-22 07:59. Section: Daily Dispatches

By Nichola Saminather

Reuters

Thursday, March 21, 2019

TORONTO, Ontario, Canada — Paulson & Co. Inc. will not support Newmont Mining Corp.’s planned $10 billion takeover of rival Goldcorp Inc. as the premium offered is unjustified, the investor said in a letter today.

The transaction is dilutive to Newmont shareholders and only Goldcorp shareholders would benefit from the deal’s synergies, founder John Paulson and partner Marcelo Kim said in the letter to Newmont Chief Executive Officer Gary Goldberg. …

… For the remainder of the report:

https://www.reuters.com/article/us-newmont-mining-m-a-goldcorp/paulson-s..

END

|

3:16 AM (4 hours ago) | |||

|

||||

Good Morning Bill/Harvey (from a Johannesburg experiencing near blackout conditions)

There were some very agitated expressions of disappointment in the opening lines of yesterdays’ MIDAS concerning the failure of the paper price of gold to react in a meaningful way to complete FED capitulation. If you are ‘agitated’, you are probably living on your nerves because you are ‘on margin’, and any ‘investor’ (punter) playing in the futures market almost certainly will not win by adopting a ‘long only’ position.

How should the price of paper gold react to the latest FOMC capitulation? If 50,000 long contracts had been thrown at the COMEX and the cartel had allowed the paper price of gold to rise by (say) $50,then these new longs would have been vulnerable to the inevitable ‘profit taking’ on Sunday evening as a ‘whatever it takes’ volume of short contracts would be dumped at the most illiquid moment possible. Maybe the Cartel would have waited a few more days and enlisted the support of a substantial margin hike. The Cartel simply cannot be overwhelmed in the paper gold markets with their limitless resources. MIDAS/Harvey have warned against the chicanery prevailing on the COMEX for many years now and Harvey’s warning against GLD has also been headlined in red for a long time now. Perhaps the message is now well understood. Indeed the LBMA has long ago abandoned its proposal to disseminate even high level consolidated data relating to OTC trading volumes/prices and the daily London fix data has now been virtually hidden from any true visibility. The only worthwhile information available about the true state of the physical gold market emanates from knowledgeable insiders like Andrew Maguire. Perhaps the GATA camp should be well pleased that the response of the last 48 hours has not been an insane and calamitous headlong lemming like rush into the corrupted paper markets.

Otherwise this physical gold market is opaque to the extreme. All we truly know is that China and Russia (and many others) continue to accumulate physical gold in accordance with their Master Plan along the lines expounded by Jim Willie. The role out of the Chinese blue print for the development of the historic Silk Road trading route gathers pace (even a beleaguered Italy is now reported to be extremely interested). It may be a few years (or just a few months) before China starts to re-introduce a role for gold into that rapidly expanding theatre of trading operations in which it is dominant. Then the USD and the failed concept of fiat currencies die. So before anyone laments the apparent anemic response of the paper price of gold to this week’s events, remember that the only response that matters is the impact on the demand for physical gold, and very few of us have any insight into that market. The paper gold market is just an amusing sideshow encapsulating the death throes of an atrophying empire as it goes the way of all empires before it.

Regards

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7133/

//OFFSHORE YUAN: 6.7201 /shanghai bourse CLOSED UP 2.69 POINTS OR 0.09% /

HANG SANG CLOSED UP 41.69 POINTS OR 0.14%

2. Nikkei closed //UP 13.42 POINTS OR .09%

3. Europe stocks OPENED RED

/USA dollar index RISES TO 96.69/Euro FALLS TO 1.1304

3b Japan 10 year bond yield: FALLS TO. –.07/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.40/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 59.51 and Brent: 67.25

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO –.01%/Italian 10 yr bond yield UP to 2.47% /SPAIN 10 YR BOND YIELD DOWN TO 1.08%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.48: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.77

3k Gold at $1312.50 silver at:15.46 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 46/100 in roubles/dollar) 64.36

3m oil into the 59 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.40 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9944 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1242 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to –0.01%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.49% early this morning. Thirty year rate at 2.93%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.5833

Global Markets Slide, Yields Collapse As European Recession Deepens

After yesterday’s furious rebound in the S&P, which almost appeared staged to confirm the Fed hasn’t lost control after its shocking doubling down on dovishness which resulted in a bizarre drop in stocks in the last 30 minutes of trading on Wednesday, the rally once again fizzled overnight, dragged lower by European stocks with U.S. equity futures following, while the euro tumbled and 10-year German bunds slumped into negative for the first time since 2016 after miserable data from the German manufacturing sector renewed worries about global growth on Friday.

The Stoxx Europe 600 reversed earlier gains, with German shares tumbling 0.6% to hit their lowest in two weeks as markets in Paris and London FTSE tumbled 0.8% after Markit reported that sentiment in Germany’s manufacturing sector cratered, plunging to 44.7, the lowest since 2012.

Europe’s auto sector led the fall, dropping one percent, while industrial goods and banks dropped sharply as well. Notable movers this morning included Aggreko (+3.8%) at the top of the Stoxx 600 after being upgraded to buy at Stifel Nicolaus. Smith’s Group (+1.1%) are in the green following the company stating they plan to separate their medical business and thereafter separately list it in the UK.

“Numbers like the ones we have seen this morning from the European manufacturing sector in Europe would suggest there is more weak data to come,” said Tim Graf, EMEA Head of Macro Strategy at State Street Global Advisors. “Everybody is looking for that inflection point, I guess, for when it is finally going to get better – and it’s not quite arrived yet.”

“Manufacturing output has been declining, which means that growth continues to be based on service sector developments,” Bert Colijn, Senior Economist at ING Bank NV in Amsterdam, said in email to clients. “To fire on both cylinders again, the euro zone seems to require the global growth outlook to improve.”

The MSCI World index slipped 0.2%, pulling away from the 5-1/2 months high hit earlier in the week. U.S. stock futures indicated the souring mood would spill over to Wall Street, with e-mini futures for the Down Jones, S&P and Nasdaq all down 0.5%.

Meanwhile, on Friday Bloomberg reported that U.S. officials downplayed the prospect of an imminent trade deal with Beijing, just as a U.S. trade delegation headed by Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin is set to visit China on March 28-29.

The euro erased a modest gain, tumbling almost 100 pips and briefly dipping below 1.13…

… as and sovereign bonds reversed earlier losses and the 10Y Bund drifted briefly back under 0.00% for the first time since 2016.

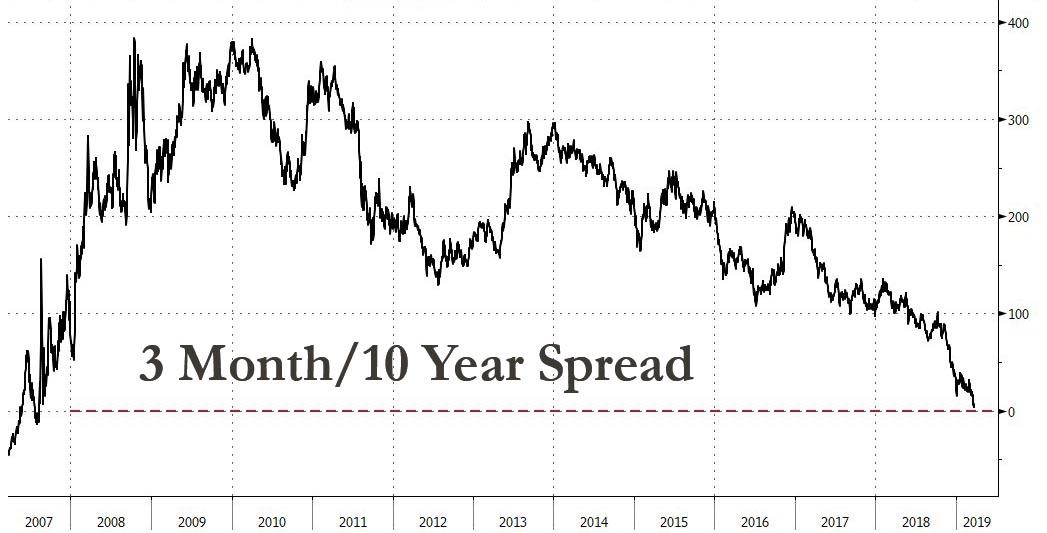

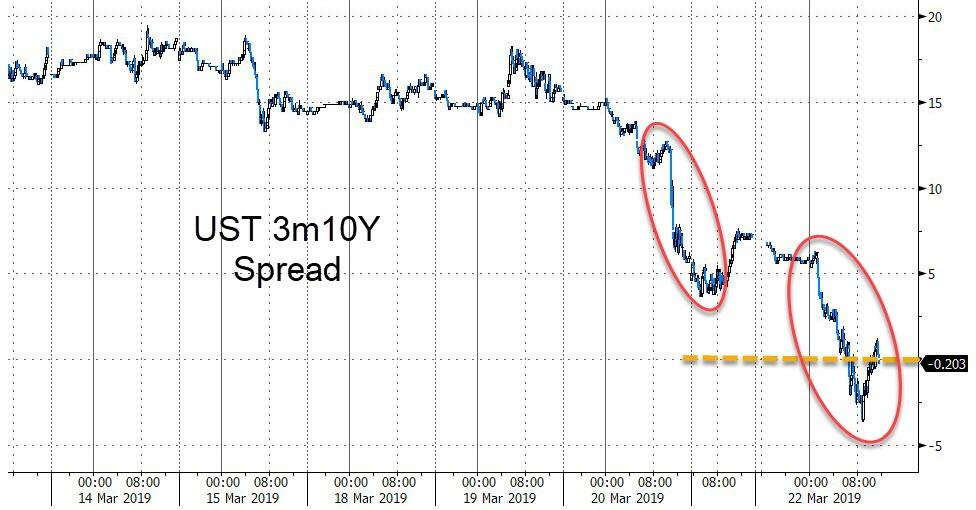

The decline in German bund yields comes after the U.S. yield curve flattened further overnight, indicating increased market expectations of a recession. The spread between the three-month Treasury bill yield and the 10-year note yield shrank to its narrowest level since August 2007, collapsing to just 2 basis points.

“The main market reaction to the Fed’s announcement was that it has become a consensus that the Fed’s next move is a rate cut,” said Naoya Oshikubo, senior manager at Sumitomo Mitsui Trust Asset. “As economic data from China and elsewhere has not bottomed out yet, investors will be looking at economic fundamentals for now. If there are improvements, then markets could roll back expectations of a Fed rate cut.”

The plunge in the euro helped push the dollar up 0.3 percent against a basket of six rival currencies in a second straight day of gains.

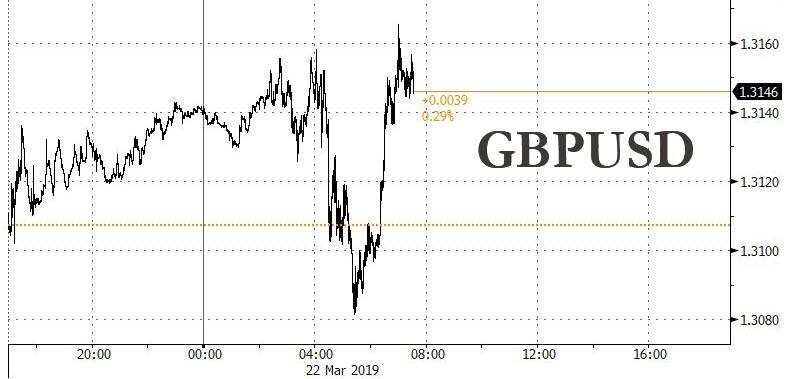

One day after the EU granted Theresa May an unconditional 2 week Brexit delay until April 12, the algos were in charge of setting the price, with the British pound swinging wildly without news, and after sliding sharply from 1.3160 to 1.3082 before squeezing the new weak hand shorts sharply higher.

On Thursday, sterling plunged towards $1.30 on Thursday in its biggest one-day fall of 2019 as fears mounted that Britain would crash out of the EU on March 29. The EU has said Britain can have a short delay to Brexit, as requested by May, but she must first win parliamentary approval for her withdrawal deal that sets out the future relationship between London and its biggest trading partner.

Elsewhere, in commodity markets, oil prices pulled away from 2019 peaks as economic growth concerns hurt sentiment, pausing a three-month rally that was driven by OPEC-led supply cuts and U.S. sanctions against Iran and Venezuela.

Brent crude oil futures and U.S. crude futures slipped both around 0.7 percent to $67.36 and $59.56 per barrel respectively.

Gold headed for its best week since early February. Earlier in Asia, a late-day turnaround put benchmark stock indexes in Japan, Korea and Australia back into the green.

Market Snapshot

- S&P 500 futures down 0.4% to 2,851.25

- STOXX Europe 600 down 0.01% to 380.65

- MXAP up 0.2% to 161.05

- MXAPJ up 0.1% to 530.71

- Nikkei up 0.09% to 21,627.34

- Topix up 0.2% to 1,617.11

- Hang Seng Index up 0.1% to 29,113.36

- Shanghai Composite up 0.09% to 3,104.15

- Sensex down 0.4% to 38,249.63

- Australia S&P/ASX 200 up 0.5% to 6,195.23

- Kospi up 0.09% to 2,186.95

- German 10Y yield fell 2.1 bps to 0.02%

- Euro down 0.5% to $1.1322

- Italian 10Y yield fell 6.9 bps to 2.103%

- Spanish 10Y yield fell 1.5 bps to 1.086%

- Brent futures down 0.5% to $67.52/bbl

- Gold spot up 0.1% to $1,311.17

- U.S. Dollar Index up 0.1% to 96.63

Top Overnight News

- European Union leaders staved off the threat of the U.K. crashing out of the bloc without a deal next Friday by giving Theresa May an extra two weeks to work out what to do

- Japan’s 10- year bond yield dropped to its lowest since November 2016, joining a rally in sovereign debt around the world after the Federal Reserve this week cut its forecast for projected interest-rate increases to zero

- U.S. officials are downplaying the prospect of an imminent trade deal with China as President Donald Trump’s top negotiators prepare to head to Beijing for a fresh round of talks next week, according to people familiar with the matter

- Italy’s populist government is struggling to reach agreement on a tax-reduction plan that could extend the country’s indebtedness and lead to another clash with the European Union.

- Stephen Moore, a visiting fellow at the Heritage Foundation and a long-time supporter of Donald Trump, is being considered by the president for a seat on the Federal Reserve Board, according to two people familiar with the matter. Also under consideration for the board is Herman Cain, the former pizza company executive who ran for the 2012 Republican presidential nomination, according to the people, who asked not to be identified discussing Trump’s private deliberations

- Bond yields around the world are tumbling to multi-year lows as the global shift by central banks to a more accommodative stance has put the kibosh on the oft-predicted but still-unrealized end of the long bull run in government debt.

- European Union leaders staved off the threat of the U.K. crashing out of the bloc without a deal next Friday by giving Theresa May an extra two weeks to work out what to do. But in private, EU leaders weren’t so optimistic that May will be able to pull it off next week.

- U.S. officials are downplaying the prospect of an imminent trade deal with China as President Donald Trump’s top negotiators prepare to head to Beijing for a fresh round of talks next week, according to people familiar with the matter.

- Turkey’s lira tumbled along with bonds and stocks amid mounting signs local investors are losing faith in the currency ahead of elections later this month. The lira weakened more than 2 percent to 5.5791 per dollar, breaking out of a tight range that’s held since November.