GOLD: $1322.60 UP $9.85 (COMEX TO COMEX CLOSING)

Silver: $15.56 UP 15 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1322.40

silver: $15.54

Comex options expire next week: Wednesday March 27

London/LBMA expires Monday March 31/2019.

The crooks continue with their whacking right in front of the authorities/regulators despite the criminal probe of precious metals manipulations.

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 0 NOTICE(S) FOR nil OZ (0.00 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 384 NOTICES FOR 38400 OZ (1.944 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR NIL OZ/

total number of notices filed so far this month: 5380 for 26,900,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3987:DOWN $2

Bitcoin: FINAL EVENING TRADE: $3938 DOWN 66

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 0/0

MONTH TO DATE: 384

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST CONTINUES TO RISE FOR THE FIFTH CONSECUTIVE TIME: THIS TIME BY A STRONG SIZED 1335 CONTRACTS FROM 190,915 UP TO 192,250 DESPITE FRIDAY’S 7 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 378 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 378 CONTRACTS. WITH THE TRANSFER OF 378 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 378 EFP CONTRACTS TRANSLATES INTO 1.890 MILLION OZ ACCOMPANYING:

1.THE 7 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 27.120 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

31,817 CONTRACTS (FOR 17 TRADING DAYS TOTAL 31,817 CONTRACTS) OR 159.085 MILLION OZ: (AVERAGE PER DAY: 1871 CONTRACTS OR 9.357 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 159.085 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 22.72% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 524.47 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1335 DESPITE THE 7 CENT FALL IN SILVER PRICING AT THE COMEX /FRIDAY..THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 378 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1788 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 378 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1410 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 7 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.41 WITH RESPECT TO FRIDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.936 BILLION OZ TO BE EXACT or 134% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 27.120 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE 2562 CONTRACTS, TO 518,742 WITH THE STRONG RISE IN THE COMEX GOLD PRICE/(AN INCREASE IN PRICE OF $5.00//FRIDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7182 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 7148 CONTRACTS,JUNE: 34 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 520,184. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9744 CONTRACTS: 2562 OI CONTRACTS INCREASED AT THE COMEX AND 7182 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 9744 CONTRACTS OR 974400 OR 30.30 TONNES.

FRIDAY WE HAD A GAIN IN THE PRICE OF GOLD TO THE TUNE OF $5.00....AND WITH THAT, WE HAD A HUGE GAIN IN TONNAGE OF 30.30 TONNES!!!!!!.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 118,809 CONTRACTS OR 11,880,900OR 369.54 TONNES (17 TRADING DAYS AND THUS AVERAGING: 6988 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAYS IN TONNES: 369.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 369.54/2550 x 100% TONNES = 14.49% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1238.51 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 2562 WITH THE GAIN IN PRICING ($5.00) THAT GOLD UNDERTOOK FRIDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7182 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7182 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG GAIN OF 9744 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7182 CONTRACTS MOVE TO LONDON AND 2562 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 30.30 TONNES). ..AND ALL OF THIS STRONG DEMAND OCCURRED WITH A RISE IN PRICE OF $5.00 IN FRIDAY’S TRADING AT THE COMEX!!!!!

we had: 0 notice(s) filed upon for nil oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $9.85 TODAY

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/

A DEPOSIT OF 2.94 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 781.03 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 15 CENTS IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV TODAY

/INVENTORY RESTS AT 309.488 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 1335 CONTRACTS from 190,915 UPTO 192,325 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 378 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 378 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1335 CONTRACTS TO THE 378 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 1700 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 8.50 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 27.120 MILLION OZ FOR MARCH.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 7 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY.BUT WE ALSO HAD A SMALL SIZED 378 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 61.12 POINTS OR 1.97% //Hang Sang CLOSED DOWN 590.01 POINTS OR 2.03% /The Nikkei closed DOWN 650.23 POINTS OR 3.01%/ Australia’s all ordinaires CLOSED DOWN 1.15%

/Chinese yuan (ONSHORE) closed DOWN at 6.7136 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 58.94 dollars per barrel for WTI and 66.90 for Brent. Stocks in Europe OPENED RED

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7136 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7187 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 C/ CHINA

i)The USA demands that China uses the USA’s cloud computing services something that China refuses to budge on

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK/Sunday

Chaos supreme as there seems to be a coup underway trying to remove Theresa May from her position of PM.

Should be an interesting next 48 hours.

(courtesy zerohedge)

b)UK MONDAY

Fat chance that this will happen: May offers Brexiteers a deal: back the withdrawal agreement and she will resign

( zerohedge)

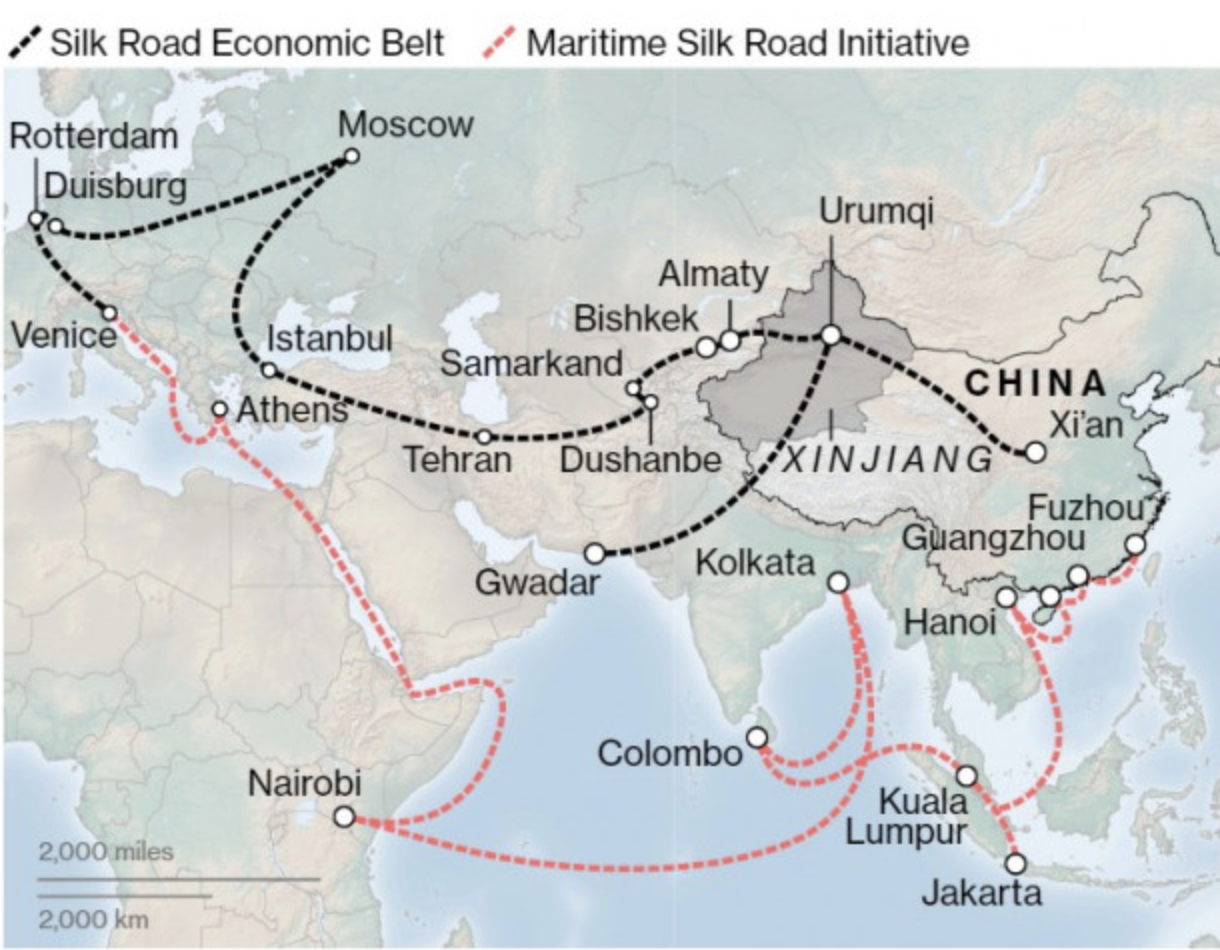

ii)ITALY/CHINA

Italy is going nowhere fast with Brussels and the EU. This is why Italy’s decision to join the ‘one belt,one road’ initiative makes sense much to the angry of the uSA and EU officials.

iv)Germany/Germany foils a plot stopping a planned attack to kil as many infidels as possible.

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Turkey

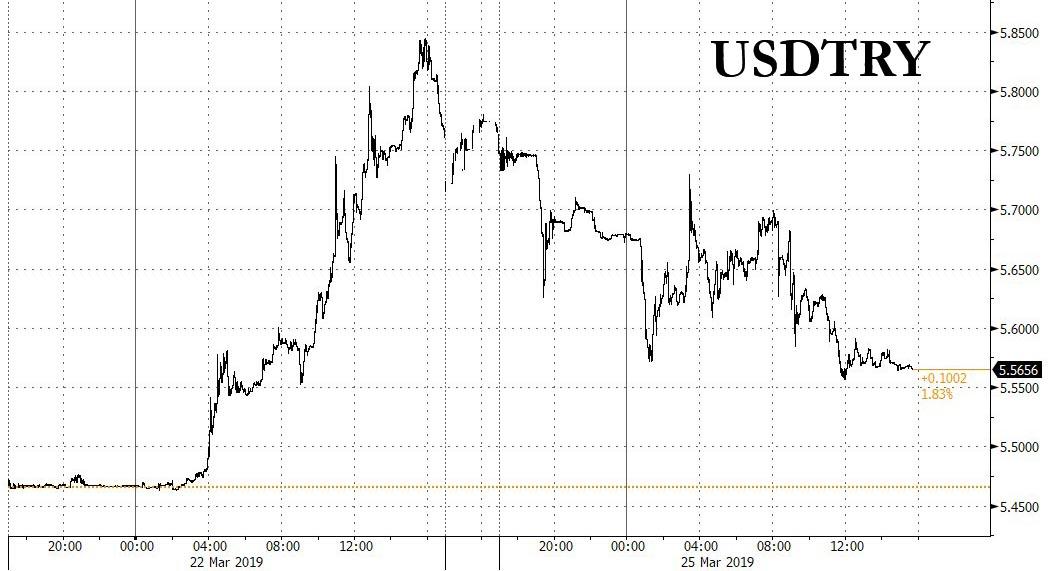

Interesting, on Friday regulators reported that Erdogan is burning through USA reserves like crazy. JPMorgan upon learning on the huge withdrawal of foreign reserves, gave a press release recommending a 5.90 target for the uSA/Turkish lira. Now Erdogan is launching a probe on the ‘manipulator’ JPM.

(zerohedge)

b)Expect an major Israeli assault on Gaza as Hamas fired a long range rocket that destroyed a house in the agricultural town of Mishameret, in the Sharon Valley(zerohedge)

c)ISRAEL strikes back as they rock Gaza and target the Hamas command centre.

6. GLOBAL ISSUES

GLOBAL EVENTS FROM FRIDAY

a)A good review of the major events that occurred on Friday and the weekend:

( Every Rabobank)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Venezuela/Russia/USA

a)Venezuela may become a powder keg. Venezuela is generally in the USA sphere of influence being in South America. However Russia and China have given huge loans to Venezuela. The USA is hoping for defaults which will cripple China and Russia.

Let us see how this plays out…

FINIAN CUNNINGHAM | 22.03.2019 | WORLD / | FEATURED STORY

(courtesy Strategic Culture/F. Cunningham)

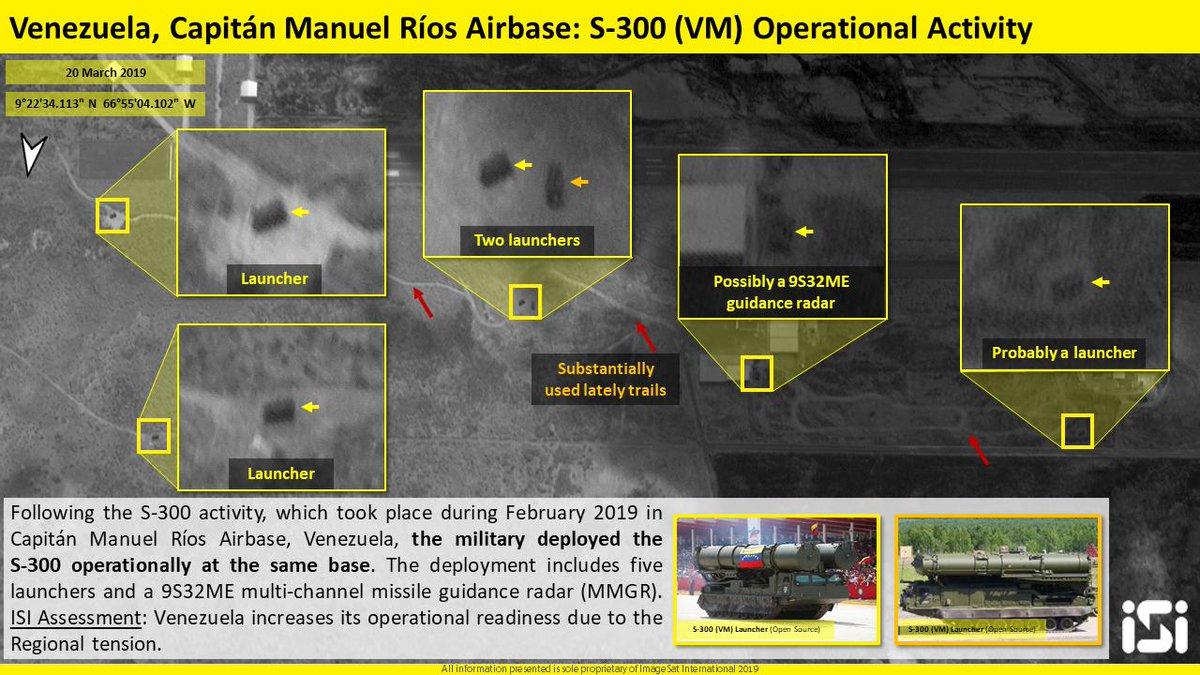

b)This does not look good: Russian troops arrive in Venezuela as they deploy S300 missile defense systems

( zerohedge)

9. PHYSICAL MARKETS

( Bloomberg/GATA)

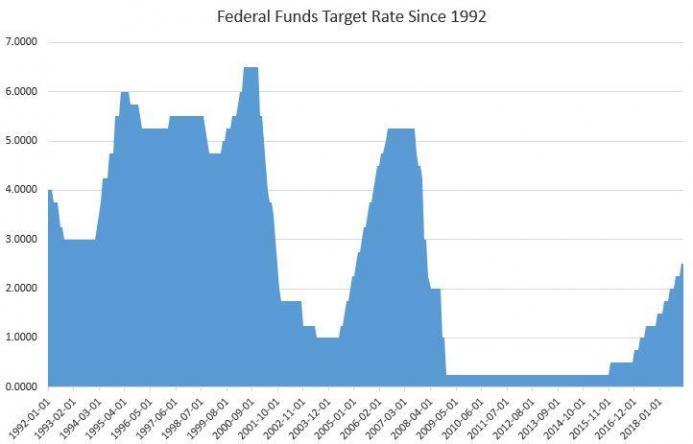

ii)I pointed this out to you on Friday but it is so important and I will repeat it: Trump is nominating to the Fed board a harsh critic of the Fed, Stephen Moore. Trump is going on the offensive.

( Reuters/GATA)

iii)He is correct: gold will be the last man standing in the crazy fiat currency world

Kingworldnews/Boockvar/GATA)

iv)this is interesting; according to the Wall Street Journal bitcoin trading is faked by unregulated exchanges:

(courtesy Vigna/Wall Street Journal//GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

ii)Market data

ii)USA ECONOMIC/GENERAL STORIES

i)Low interest rate and QE has caused inequality among investors as the wealthy can gain access to yield, something that the ordinary investor cannot.

A good commentary by Mises as they pound the table that the Fed has given up and we should be ready for increasing more QE

( McMaken/Mises)

(courtesy zerohedge)

iv)SWAMP STORIES

a)Mueller report: no collusion/no obstruction of justice!!

(courtesy zerohedge)

b)It starts: now that Trump et al have been cleared of the perpetuated hoax of Russian collusion, the House Intelligence committees are now ready for criminal referrals to the Attorney General Barr.

buckle your safety belt..this is going to be quite a bumpy ride..

(courtesy zerohedge)

b ii)The Republicans are now going full blast as Graham vows to investigate the FBI’s unprofessional conduct along with the troubling behaviour by Attorney General Loretta Lynch and of Comey and mcCabe.

(courtesy zerohedge)

c)Kim Strassel of the Wall Street Journal now urges the probe of the real scandal..the democrats trying to overthrough the duly elected President of the USA

(zerohedge/kim Strassel./WSJ

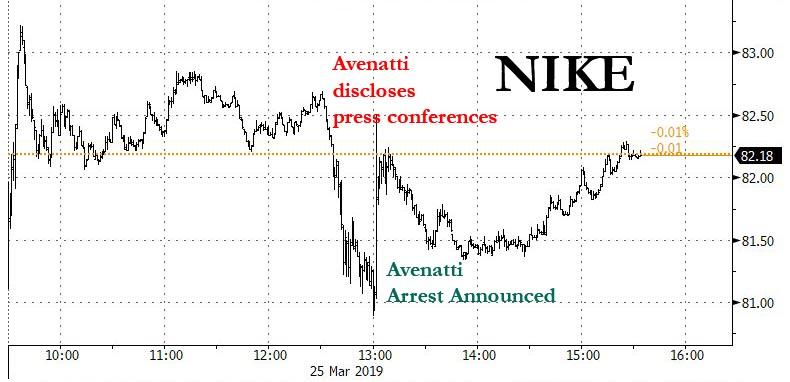

d)How this is cute: Michael Avenatti is now arrested in an extortion plan against Nike as well as embezzling client funds. What took them so long

( zerohedge)

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL LOWERS TO 777 CONTRACTS FOR A LOSS OF 20 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ROSE BY 733 CONTRACTS UP TO 136,659 CONTRACTS.

i)out of JPMorgan: 4932.05 oz

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

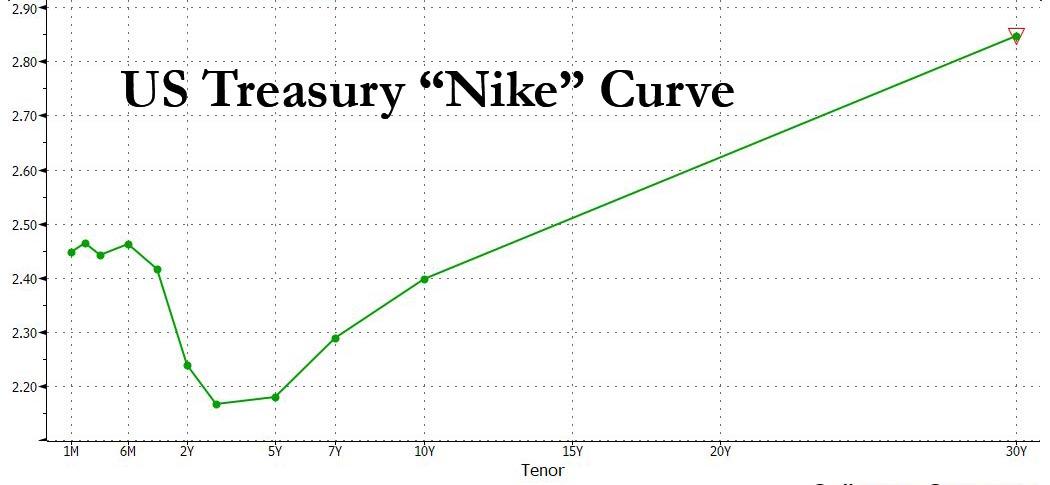

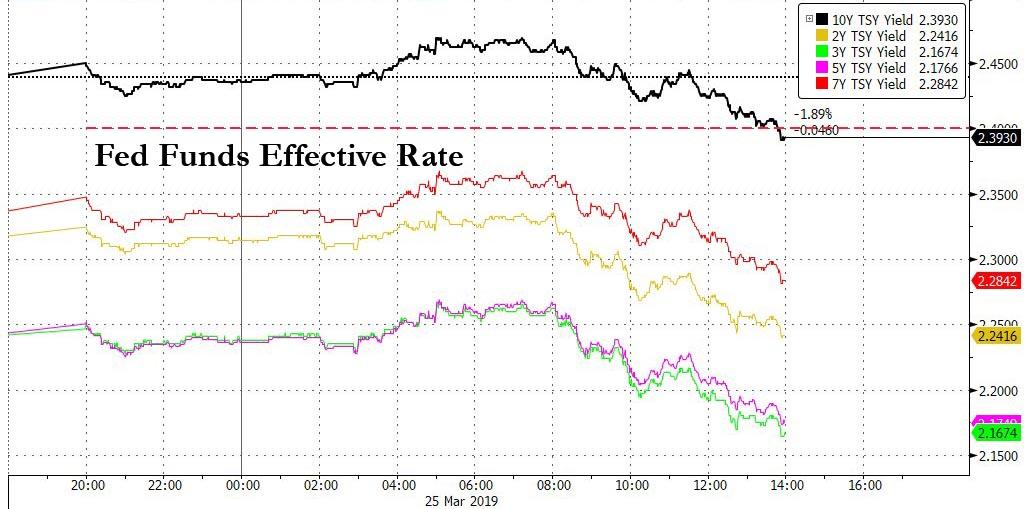

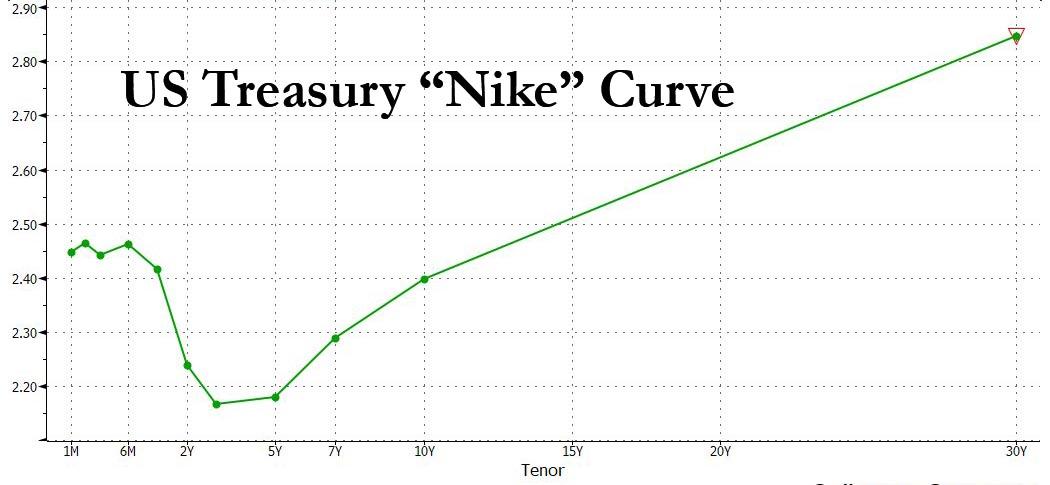

As noted on Friday we had treasury curve inversion especially on the 10 yr bond yield and the 3 month. This generally means recession:

(courtesy Bloomberg/GATA)

Treasuries buying wave triggers first yield curve inversion since 2007

Submitted by cpowell on Sat, 2019-03-23 05:16. Section: Daily Dispatches

By Emily Barrett and Katherine Greifeld

Bloomberg News

Friday, March 23, 2019

The Treasury yield curve inverted Friday for the first time since the last crisis, triggering the first reliable market signal of an impending recession and rate-cutting cycle.

The gap between the three-month and 10-year yields vanished as a surge of buying pushed the latter to a 14-month low of 2.416 percent. Inversion is considered a reliable harbinger of recession in the U.S. within roughly the next 18 months.

…

Demand for government bonds gained momentum Wednesday when U.S. central bank policy makers lowered both their growth projections and their interest-rate outlook. Most officials now envisage no hikes this year, down from a median call of two at the December Fed meeting. Traders took that dovish shift as their cue to dig into positions for a Fed easing cycle, pricing in a cut by the end of 2020 and a one-in-two chance of a reduction as soon as this year. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-03-22/u-s-treasury-yield-cu…

END

I pointed this out to you on Friday but it is so important and I will repeat it: Trump is nominating to the Fed board a harsh critic of the Fed, Stephen Moore. Trump is going on the offensive.

(courtesy Reuters/GATA)

Trump nominates to Fed board a harsh critic of its chairman

Submitted by cpowell on Sat, 2019-03-23 05:23. Section: Daily Dispatches

By Roberta Hampton

Reuters

Friday, March 22, 2019

PALM BEACH, Florida — President Donald Trump on Friday tapped Stephen Moore, a conservative economic commentator and fellow critic of Federal Reserve policy under Chairman Jerome Powell, to join the U.S. central bank’s board of governors, a move that would put a Trump loyalist inside the world’s most important financial institution.

…

Moore, who last year suggested in a radio interview that Trump had cause to fire Powell for “wrecking our economy,” would add a critical and unconventional voice to a collegial committee that unanimously backed Powell in keeping rate hikes on hold this month.

The group often reach policy decisions by consensus after debating the issues. …

… For the remainder of the report:

https://www.reuters.com/article/us-usa-fed-moore/trump-taps-a-strident-p…

* * *

END

He is correct: gold will be the last man standing in the crazy fiat currency world

Kingworldnews/Boockvar/GATA)

Gold will be ‘last man standing in this nutty fiat currency world,’ Boockvar tells KWN

Submitted by cpowell on Sat, 2019-03-23 06:00. Section: Daily Dispatches

1p ICT Saturday, March 23, 2019

Dear Friend of GATA and Gold:

The chief investment officer for Bleakley Financial Group, Peter Boockvar, tells King World News that he’s not sure if there is any case left against gold.

“The evaporation of the U.S. yield curve, on top of a further deepening of negative yielding bonds overseas, should be the fuel for the next move higher in gold and silver,” Boockvar says. “What’s also interesting is that, at least as of now, gold and the U.S. dollar are rallying at the same time and if that continues, I’m not sure what is left of the bear case on gold. Gold will be the last man standing in this nutty fiat currency world. Got any?”

Boockvar’s comments are posted at KWN here:

https://kingworldnews.com/peter-boockvar-says-this-will-be-the-fuel-for-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

this is interesting; according to the Wall Street Journal bitcoin trading is faked by unregulated exchanges:

(courtesy Vigna/Wall Street JournalGATA)

Most bitcoin trading faked by unregulated exchanges, study finds

Submitted by cpowell on Sun, 2019-03-24 01:18. Section: Daily Dispatches

How is this so different from the stock, bond, and commodity markets, where most trading now is done by machines following algorithms, much of it instigated by government agencies?

* * *

By Paul Vigna

The Wall Street Journal

Friday, March 22, 2019

Nearly 95 percent of all reported trading in bitcoin is artificially created by unregulated exchanges, a new study concludes, raising fresh doubts about the nascent market following a steep decline in prices over the past year.

Fraudulent trading volume has dogged cryptocurrency trading for years, but the extent of the market manipulation has been difficult to determine. Bitwise Asset Management said its analysis of trading activity at 81 exchanges over four days in March indicates that the actual market for bitcoin is far smaller than previously thought.

…

.The San Francisco-based company submitted its research to the U.S. Securities and Exchange Commission with an application to launch a bitcoin-based exchange-traded fund. The study, made public Thursday, is an attempt to alleviate the agency’s longstanding concerns that a bitcoin ETF would leave investors exposed to fraud and market manipulation.

Bitwise’s fund, if approved, would be based upon the 5 percent of trading it considers legitimate, said Matthew Hougan, Bitwise’s head of global research. That volume comes from 10 regulated exchanges that can verify that their trading data and customers are real. This slice of the market, he said, is well-regulated, transparent, and efficient. …

… For the remainder of the report:

https://www.wsj.com/articles/most-bitcoin-trading-faked-by-unregulated-e…

Brexit, Gold Tier 1, QFC Stay Rules and MIFID II

| Inbox | x |

|

Sun, Mar 24, 6:17 PM (13 hours ago) | |||

To all of Harvey’s quite amazing group of followers, please apologize for e-mailing any of you. The “but” is because so many of you are tuned in more than me, I thought maybe someone could take the thought to a higher level. It has to do with Brexit, Gold Tier 1, QFC Stay Rules and MIFID II.

Although lengthy but maybe very significant. Tier 1 collateral of physical allocated, segregated, 99.99% assayed Gold just may be the bull’s eye after all.

The first link below came into effect just after January 1, 2019. The 2nd and 3rd links below came out just prior to Brexit in June 2016. They all deal with “Covered” QFC’s that are “centrally cleared” through an exchange. For Brexit 2016, the UK had just recently passed this ruling relating to QFC’s that are “covered & centrally” cleared. It brings back memories to me of the post-Brexit trading after the June 2016 vote on how the markets all recovered miraculously. This time around with so many institutions that have moved funds out of the UK, it makes me wonder if this time around the markets will be so lucky if a long Brexit delay is not agreed to before March 29. The European Union, a single political and economic bloc, has faced multiple challenges since 2016 that brought its viability into question not to mention China and Russia gaining so many inroads into Eurasian trade with European trade with US in decline led by Germany also appearing to lead the way south in economic activity in Europe. If after March 29, Brexit puts the fear that the U.K. actually leaves the bloc, it remains to be seen whether the EU still has the ability to withstand more shocks. Not even Q-Anon and MAGA sheeples will be able to keep from focusing on these shocks. And whereas most analyst appear to believe that Brexit will never happen, if along Brexit delay does not occur markets will react sharply.

https://www.federalreserve.gov/newsevents/press/bcreg/tarullo-opening-statement-qfr-20160503.htm

http://www.bloomberg.com/news/articles/2016-05-03/fed-expected-to-drag-hedge-funds-into-plan-to-halt-next-lehman (Unfortunately the Bloomberg link now requires subscriber access.)

As March 29 is significant again in Brexit as well as in reclassifying physical gold as Tier 1, maybe there is something significant in the protocol that will affect non-centrally cleared derivatives which in the US and UK have grown significantly since 2016. Now as of January 1, 2019 in the U.S. and June 106 in the UK, any and all “centrally” cleared QFC’s with ‘covered” counterparties in in effect. “Covered” institution are global systemically important banking organizations. “Centrally” cleared QFC’s of course are cleared through the ISDA system for all to see. These rulings prevents a “take your money from your counterparty and run” causing bankruptcy and market chaos whereas all centrally cleared QFC’s appear to have a 24-48 hour hold on allowing the “covered” winning entity from collecting from its “covered” losing counterparty if they can secretly enter a resolution proceeding and permit the transfer of the relevant obligations under the QFC to the solvent party

out of the public’s view in order to prevent a crash yet simultaneously redistribute assets. By hell or high water behind the curtain they will force, steal, threaten, or otherwise convince that losing counter party to enter into stay and transfer provisions even though the losing party hasn’t formally declared bankruptcy. The end result is making deals behind the table out of the public’s view preventing market chaos like we had in Lehman.

But to my knowledge because MFID ii in the Europe its own mammoth set of OTC Derivatives and CCP regulations are only 58% implemented in EU. MIFID ii applies to centrally cleared derivatives that unlike other financial instruments, have never really had a product identifier. MIFID ii assigns an identifier “ISIN” that makes “all” centrally cleared OTC derivatives easy to regulate by authorities, and market participants to identify collateral and thereby accurately re-price risk for “all” OTC centrally cleared derivatives. CCPs will be required to have a substantial minimum amount of “skin in the game.” Also relating to MIFID ii, in January 2018, the LBMA flatly rejected that OTC Gold would be included in that MFID II legislation. It makes me wonder if those same parties in the centrally cleared QFC’s have their eye on physical gold at the LBMA or elsewhere knowing behind the door resolutions will be made that permit the transfer of the relevant obligations under the QFC to the solvent party all the while gold is simultaneously getting Tier 1 status.

https://www.itiviti.com/insights/mifid-ii-turning-challenges-opportunities

It also makes we wonder if March 29 Brexit date could actually see a plethora of CCP’s in Europe, US. And UK whose QFC’s are not centrally cleared take some swift action in the market after hard Brexit is confirmed without further delays. “In the first quarter of 2015, banks began reporting their volumes of cleared and non-cleared derivative transactions, as well as risk weights for counterparties in each of these categories. In the fourth quarter of 2018, 39.8 percent of banks’ derivative holdings were centrally cleared (see table 12). https://www.occ.gov/topics/capital-markets/financial-markets/derivatives/pub-derivatives-quarterly-qtr4-2018.pdf That means 60.1% of US financial institutions’ $176T in derivatives are not centrally cleared and do not have to abide by Fed QFC’s rules or MIFID ii guidelines. Considering in the US that the amount in non-centrally cleared derivatives of about $100T and centrally cleared of about $76T are about the same as in June 2016 and the current state of the EU banking system, some real havoc may ensue for those failing institutions with a Brexit trigger.

Tier 1 collateral of physical allocated, segregated, 99.99% assayed Gold just may be the bull’s eye after all.

Kevin Wallien

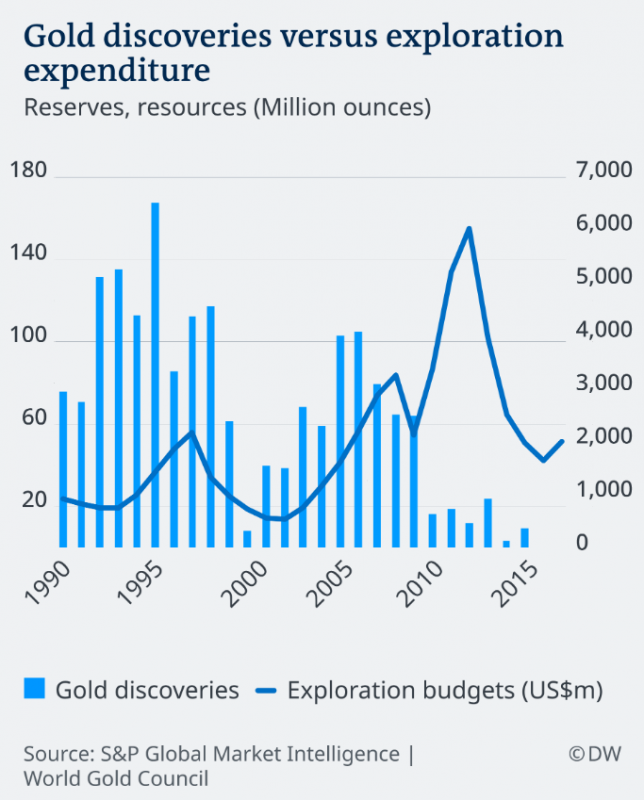

Are We Running Out Of Gold?

Authored by Tom Lewis via GoldTelegraph.com,

Gold has been used for jewelry and currency for thousands of years. It has always served as a source of status and wealth. The reason for its popularity is its rarity. Gold is a finite commodity. There is only so much of the golden metal available, and it can’t be manufactured.

Some experts, including Goldcorp’s chairman, Ian Telfer, are predicting that the amount of future gold to be mined is already on the decline. The fact that gold mining is on the decline is nothing new. That has happened before. What is worrying some investors is that the world may be running out of physical gold.

Should investors be worried?

The discovery of new gold deposits has been declining while mining companies are spending more money on exploration for new sites. Most of the newly-found deposits have been small and expensive to extract. No high-grade deposits with at least 5 million ounces of gold, or “world-class” deposits, have been found in a long time. These world-class deposits have yielded more than 50 percent of today’s available gold.

What little is being extracted is becoming costly to obtain. Many deposits are producing 1.4 grams of gold per ton, as compared to 10 grams in the 1970s.

Mining companies are struggling. Many have merged to offset decreasing profits and declining gold supply. The gold industry has been witnessing a wave of mergers over the past few months as producers battle poor returns and diminishing reserves.

In March of this year, Barrick Gold, the world’s second-largest gold producer, and Newmont Mining agreed on a joint venture in Nevada instead of Barrick Gold buying Newmont Mining outright. Newmont Mining acquired Goldcorp earlier this year in an effort at developing greater and more economical resources.

Barrick Gold believes that Nevada still has plenty of gold, perhaps 76 million ounces.

According to mining analyst John Ing, it may be cheaper to buy another gold mining company than explore for new gold. This opinion is seconded by analyst Ryan Hanley of Laurentian Bank Securities, who claims that the time and cost of gold exploration makes mergers a more profitable proposition for these majors.

The real problem is not the lack of gold but the current price of gold. The price of gold has been holding at around $1,300 an ounce, down from its high of $1,800 an ounce in 2012. However, with peak gold in sight, we anticipate the price of gold to elevate so more exploration dollars can be allocated.

The amount of money mining companies have allocated for new explorations has declined from a high of $21 billion in 2012 to $10.1 billion in 2018.

While global economies are currently presenting a strong picture, it is anticipated that economic growth will slow down globally. This could very well see the price of gold climbing to $1,300 an ounce, its highest level since 2013. A rise in gold prices is very likely with geopolitical and recession risks to coincide with peak gold.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7136/

//OFFSHORE YUAN: 6.7187 /shanghai bourse CLOSED DOWN 61.12 POINTS OR 1.99% /

HANG SANG CLOSED DOWN 599.01 POINTS OR 2.03%

2. Nikkei closed //DOWN 650.29 POINTS OR 3.01%

3. Europe stocks OPENED RED

/USA dollar index FALLS TO 96.62/Euro RISES TO 1.1308

3b Japan 10 year bond yield: FALLS TO. –.08/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.12/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 58.94 and Brent: 66.90

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO –.01%/Italian 10 yr bond yield UP to 2.48% /SPAIN 10 YR BOND YIELD DOWN TO 1.09%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.49: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.77

3k Gold at $1317.55 silver at:15.53 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 28/100 in roubles/dollar) 64.28

3m oil into the 58 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.12 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9937 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1236 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to –0.01%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.46% early this morning. Thirty year rate at 2.90%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6907

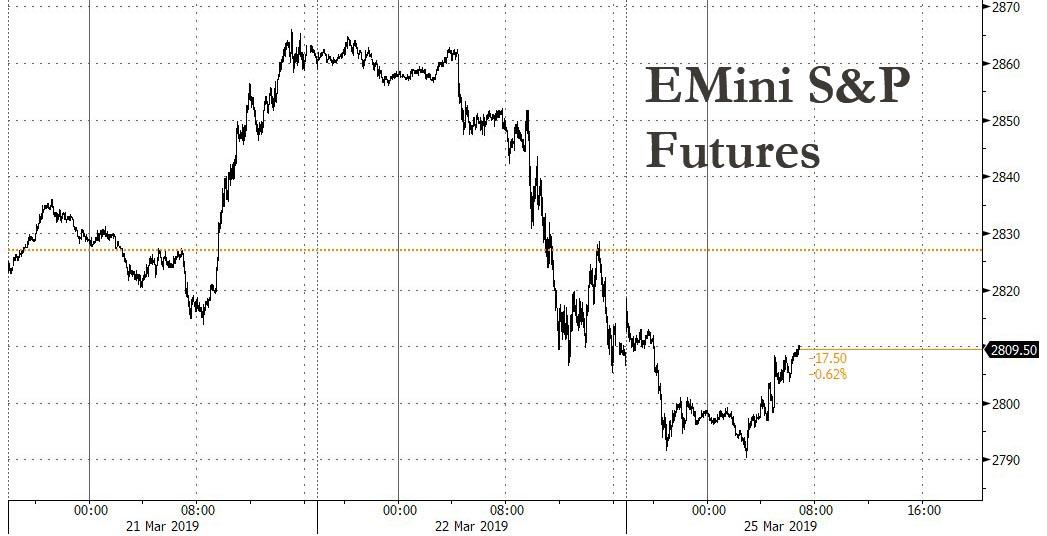

Asia Crumbles, Futures Hug 2,800 As Traders Await New Recession Signals

Following Friday’s global beatdown when the 3M-10Y yield curve inverted for the first time since 2007, launching the countdown to the next recession, optimism was scarce to start the week as European shares slumped, S&P futures pointed to another day of fighting the gravitational attraction of 2,800 and Asian stocks tumbled, even as a glimmer of hope emerged in Germany where the IFO index beat expectations, helping push Treasury yields higher and the bund briefly rose above 0.00%.

The session started on the back foot, with the MSCI Asia Pacific index tumbling 2%, its biggest drop of the year, as regional stocks tracked Friday’s heavy Wall Street losses, and Japan’s Nikkei hit a five-week low after diving 3.1 percent for its largest one-day percentage fall since late December. South Korea’s Kospi index declined 1.7 percent, while China shares was also in the red with the blue-chip CSI 300 index down 1.4 percent.

MSCI’s gauge of stocks across the globe slipped 0.5 percent. The gloomy mood was expected to spread to U.S. markets with S&P 500 futures skidding 0.2 percent. However, they were down as much as 0.5 percent earlier in the day.

World stocks hit a 12-day trough on Monday as fears for economic growth sent investors dashing for safe-haven assets, but the selloff lost some momentum after better-than-expected data from Germany.

A faint glimmer of hope that Europe’s recession may be fading came from the Ifo Institute’s March business climate index which unexpectedly rose, printing at 99.6, above the 98.5 expected (98.7 in February)…

… soothing nerves after Friday’s dismal German manufacturing data, which helped spark a global selloff that hammered stock markets and pushed key benchmark bond yields below zero.

Whereas the much discussed inversion in the 3M-10Y yield curve – the Fed’s favorite leading recession indicator – on Friday stoked fears that the world’s largest economy was headed for recession, the Ifo report lent some cheer. It helped European shares – where tech shares led declines – rise off early lows. Paris traded flat, London’s FTSE was down 0.2 percent, and Frankfurt inched up 0.14 percent after the numbers. Europe’s banking as well as industrial goods & services sectors which were down 1 percent at one point, recouped losses to trade flat. But the jitters are far from over.

Futures on the S&P 500 Index decreased as much as 0.5 percent to the lowest in almost two weeks, before rebounding and hugging the 2,800 “sextuple top.”

Meanwhile, the flight to safety continued around the globe, with Australia’s 10-year bond yield sliding to an all-time low and Japan’s hit the lowest since September 2016.

“Global equities were kind of complacent” as rates markets reflected growth concerns, said Marcella Chow, global market strategist at JPMorgan Asset Management in Hong Kong. “It was the release of global PMI data last Friday that shook off the complacency,” she added.

The glimmers of German economic optimism helped push spreads between U.S. three-month and 10-year Treasury yields positive. U.S. 10-year treasury yields stood at 2.47% after yields inverted for the first time since 2007 on Friday: historically a failsafe harbinger of upcoming recession.

“The bond market price action is an enormous blaring siren to anyone trying to be optimistic on stocks,” JPMorgan analysts said in a note to clients. “Growth, and bonds/yield curves, will be the only thing stocks should be focused on going forward, and it’s very hard to envision any type of rally until economic confidence stabilizes and bonds reverse.”

“We had a dire end to 2018 which was then recouped so you have a very good reason to lighten up on portfolios,” said Marie Owens Thomsen, chief economist at CA Indosuez in Geneva, adding that confusion over the state of play in Britain’s impending departure from the European Union clouded the picture more. “Many people may have realized a major part of their expected returns for the year, so in light of recent gains it makes sense for investors to should lighten up on risk.”

And while investors also digesting news that Special Counsel Robert Mueller found no evidence anyone close to President Donald Trump colluded with Russia in the 2016 presidential campaign, judging by the lack of notable reaction the news did not come as much of a surprise to traders. While Mueller failed to exonerate Trump on obstruction of justice, Attorney General William Barr said he did not find enough evidence to pursue that charge.

In overnight central bank news, Fed’s Evans (voter, dove) said the US economy is in a strong position and that it is a good time to pause and be cautious, while he added that US monetary policy is currently neither accommodative or restrictive. Evans also commented they will take action if inflation undershoots, while he wants to see more inflation and does not expect a rate hike till H2 next year. Adding they may have to ease if economic activity weakens more than expected and that the recent US data has been softer than expected. Fed’s Harker (non-voter, dove) said economic risks tilt very slightly to the downside, and that outlook is pretty good. He reiterated the Fed’s wait-and-see stance whilst stating he favors one rate hike at most this year. He noted inflation is around the Fed’s target, is edging slightly downward. Finally, he expects GDP slightly above 2% in 2019, returning to around 2% trend level in 2020.

ECB’s Rehn said Brexit is the biggest threat to Euro zone in the short-term and that markets are underestimating the risks, while he added Euro zone growth has slowed significantly and that we must be concerned. ECB’s Hansson says that the Euro-area slowdown may continue in the medium term; tiered deposit rate has not really been discussed. QE could be restarted in event of major shock.

Political turmoil in Britain over the country’s exit from the European Union also remains a drag on risk assets. Prime Minister Theresa May held crisis talks with senior colleagues and hardline Brexiteers on Sunday trying to breathe life into her twice-defeated European divorce deal after reports her cabinet was plotting to topple her.

Rupert Murdoch’s Sun newspaper said in a front page editorial May must announce on Monday she will stand down as soon as her Brexit deal is approved. The British pound was 0.2% lower after three straight days of wild gyrations. The currency had slipped 0.7 percent last week.

Elsewhere in FX, the Turkish lira, which crashed on Friday, recouped some of its losses which followed the start of an investigation by Turkey’s banking regulator into JPMorgan Chase and another probe of unspecified banks for stoking the currency’s plunge. The Bloomberg dollar spot index was steady while the euro rose to a session high, European stocks bounced from a session low and the 10-year Bund yield climbed back above zero percent after stronger-than-forecast German Ifo business confidence, alleviating some fears of a sharp economic slowdown. Sweden’s krona led gains among Group-of-10 peers as it recovered some of the sharp losses on Friday while the yen led declines, after earlier touching a six-week high, as an earlier haven bid faded while Japan’s bonds rallied and 10-year yields fell to the lowest since 2016.

In commodities, WTI (+0.1%) and Brent (-0.1%) futures rebounded off lows amid an improvement in risk-appetite with the former flirting with the USD 59.00/bbl to the upside whilst the latter resides just below the USD 67.00/bbl level. The latest CFTC data also showed that speculators increased next longs in NYMEX WTI by over 54k lots with a bulk of this increase driven by fresh positions. Elsewhere, Chinese crude imports increased by 2% in February to average around 10.3mln BPD, with a Y/Y increase of just under 22%. Furthermore, the country increased its share of Iranian and Venezuelan imports over February.

Economic data include index readings on manufacturing and national activity. Red Hat is due to report earnings.

Market Snapshot

- S&P 500 futures down 0.2% to 2,807

- STOXX Europe 600 down 0.8% to 373.20

- MXAP down 2.1% to 158.05

- MXAPJ down 1.6% to 521.06

- Nikkei down 3% to 20,977.11

- Topix down 2.5% to 1,577.41

- Hang Seng Index down 2% to 28,523.35

- Shanghai Composite down 2% to 3,043.03

- Sensex down 1.2% to 37,725.77

- Australia S&P/ASX 200 down 1.1% to 6,126.21

- Kospi down 1.9% to 2,144.86

- German 10Y yield rose 0.4 bps to -0.011%

- Euro down 0.02% to $1.1300

- Brent Futures down 0.5% to $66.69/bbl

- Italian 10Y yield fell 0.8 bps to 2.095%

- Spanish 10Y yield rose 1.5 bps to 1.087%

- Brent Futures down 0.5% to $66.69/bbl

- Gold spot up 0.3% to $1,317.02

- U.S. Dollar Index down 0.02% to 96.64

Top Overnight News

- U.K. Prime Minister Theresa May is under pressure from colleagues inside her Cabinet to name a date when she will step down, according to people familiar with the matter

- Special Counsel Robert Mueller found no evidence that anyone close to Donald Trump colluded with Russia after a 22-month investigation, and Attorney General William Barr said there wasn’t enough evidence that the president obstructed justice either

- Australia’s10-year bond yield fell below 1.8% for the first time amid a rally in developed debt markets, with the inversion of the U.S. curve adding to concern global growth is slowing

- Turkey’s lira rebounded after President Recep Tayyip Erdogan warned that bankers deemed responsible for speculating against the currency would be punished

- The openness of China’s financial markets to the rest of the world isn’t high, so there’s a lot of room for increased access, according to People’s Bank of China Governor Yi Gang

- China will increase market’s decisive role in yuan exchange rate formation system and keep yuan rate flexible, China Business News reports, citing PBOC Deputy Governor Pan Gongsheng

- Oil extended losses on signs global growth may weaken further, overshadowing a drop in the amount of American rigs exploring for crude to the lowest level in almost a year

- The Bloomberg dollar spot index was steady while the pound edged lower at the start of another dramatic week for Theresa May’s premiership, with all Brexit options still in play; Theresa May is under pressure from colleagues inside her Cabinet to name a date when she will step down, according to people familiar with the matter

- The euro rose to a session high, European stocks bounced from a session low and the 10-year Bund yield climbed back above zero percent after stronger-than-forecast German Ifo business confidence, alleviating some fears of a sharp economic slowdown

- Sweden’s krona led gains among Group-of-10 peers as it recovered some of the sharp losses on Friday while the yen led declines, after earlier touching a six-week high, as an earlier haven bid faded while Japan’s bonds rallied and 10-year yields fell to the lowest since 2016

Asian equity markets began the week with hefty losses as the region followed suit to the stock sell-off last Friday on Wall St where disappointing PMI data from both sides of the Atlantic added to slowdown concerns, while curve inversion in which yields on US 3-month T-bills rose above 10yr yields for the first time since the GFC also stoked recession fears. ASX 200 (-1.1%) and Nikkei 225 (-3.1%) declined from the open in which Tech and Energy led the broad losses across the sectors in Australia, while selling in Tokyo was exacerbated by flows into JPY which dragged the local benchmark below the 21,000 level. Elsewhere, Hang Seng (-2.0%) and Shanghai Comp. (-1.9%) conformed to the negative tone as participants digested a slew of earnings and after PBoC inaction resulted to a CNY 60bln liquidity drain, with oil names among the worst hit following a recent slip in crude prices. Finally, 10yr JGBs were underpinned by safe-haven demand and as yields tracked the declines in global counterparts to push the 10yr JGB yield to its lowest since September 2016 and 30yr JGB yields to its lowest since November 2016.

Top Asian News

- Thaksin Allies Claim Victory in Thai Election, Challenging Army

- Thai Poll Agency Says it Was Hacked, Will Release Results 4pm

- China Stocks Slide, Bonds Rally as Global Growth Worries Weigh

- Citigroup Moves Sales Traders to Cover for Ousted Hong Kong Team

European equities kicked off Monday trade mostly lower [Stoxx 600 -0.2%] following a dismal lead from Asia wherein the Nikkei 225 shed 3.0% and closed below 21,000 for the first time in over a month. Back in Europe, stocks have somewhat nursed opening losses as sentiment improved following a better-than-forecast German Ifo Survey which aided the DAX (+0.1%) climb into positive territory. Elsewhere, Italy’s FTSE MIB (+0.4%) is marginally outperforming its peers as Fiat Chrysler (+3.3%) supports the index amid reports its chairman is pushing for a tie up with a rival, Peugeot (-0.7%) has been touted as a potential suitor. Sector-wise, IT names are underperforming, in-fitting with the sector’s performance overnight, whilst the consumer discretionary sector is buoyed by the overall positivity in auto stocks. Finally, this morning saw a LVMH (-0.5%) open lower by just under 9% and immediately pared losses with traders citing a potential “fat-finger” incident.

Top European News

- May Faces Endgame as U.K. Leader Is Losing Control of Brexit

- Majestic Wine Slides on ‘Drastic and Unexpected’ Strategy Shift

- Banks Cut at Barclays, Making Room for Real Estate and Utilities

In FX, the Euro was not the biggest G10 mover or best performer, but the single currency has staged a firmer recovery rebound from sub-1.1300 lows vs the Dollar in wake of an encouraging Ifo survey, with beats on all 3 key metrics compounded by upward revisions to the previous month across the board. Hot on the heels of last Friday’s dire Eurozone preliminary PMIs, and an especially worrying German manufacturing print, the institute contends that the bloc’s number one economy is displaying relative resistance, and this has helped to dispel some concerns about a deeper slowdown, or even recession. However, Eur/Usd has not clearly breached upside technical resistance in the form of the 30 DMA that comes in around 1.1321.

- SEK/NOK – The Scandi Crowns are back on the front foot and leading the major league, with the Sek especially buoyant on a mixture of improving risk sentiment, bullish technicals and the Riksbank maintaining repo rate guidance for further tightening. Eur/Sek is back down below 10.4500 and Eur/Nok is eying bids/support at 9.6500 against the backdrop of oil prices trying to recover some poise after their end of week rout.

- AUD/NZD/CAD – All firmer vs their US counterpart after sharp underperformance last Friday when aversion was rife and safe-haven positioning escalated. Aud/Usd is back within striking distance of 0.7100 and Nzd/Usd is not too much further from 0.6900 even though Aud/Nzd has crossed 1.0300 from its latest decline through the big figure, while Usd/Cad is hovering near the bottom end of a 1.3445-05 range, as the Loonie also derives some underlying support from the aforementioned bounce in crude.

- JPY/GBP/CHF – Usd/Jpy has bounced from overnight safe-haven lows in line with the gradual improvement in risk appetite and through heavy 110.00 option expiry interest at the round number (2 bn), while Cable also looks unlikely to test expiry interest or hedges at the 1.3200 strike (1.6 bn) given ongoing/heightened Brexit jitters that have pulled the Pound down towards 1.3160 and close to 0.8600 vs the Euro (Ifo also impacting this pair). Similarly, the Franc has unwound some safe-haven premium towards 0.9950 against the Greenback from circa 0.9933 at one stage and 1.1250 vs around 1.1223 against the single currency.

- EM – Yet more thrills and spills for the Lira after official intervention against a big US bank that put out a bearish trade recommendation on the Try, and the CBRT’s decision to double swap limits on outstanding FX maturities after shelving 1 week repos. Usd/Try currently at 5.6400 within a 5.7700-5.5700 band.

- Turkish President Erdogan said those in the finance sector that purchase foreign currencies on expectations a decline in TRY, will pay a very heavy price. (Newswires)

In commodities, WTI (+0.1%) and Brent (-0.1%) futures have rebounded off lows amid an improvement in risk-appetite with the former flirting with the USD 59.00/bbl to the upside whilst the latter resides just below the USD 67.00/bbl level. The latest CFTC data also shows that speculators increased next longs in NYMEX WTI by over 54k lots with a bulk of this increase driven by fresh positions. Elsewhere, Chinese crude imports increased by 2% in February to average around 10.3mln BPD, with a Y/Y increase of just under 22%. Furthermore, the country increased its share of Iranian and Venezuelan imports over February. Metals are largely on the front foot with gold (+0.4%) gaining further ground above USD 1300/oz with the recent fears surrounding and inverted yield curve between the US front-end and 10yr (Note: this has reversed) prompting additional demand in the yellow metal. Elsewhere, the twin cyclones which hit Australia over the weekend impacted mining and energy operations in the region, with reports stating some activities have been halted at BHP and Rio Tinto’s Pilbara mine. The mine is located in Western Australia and accounts for almost 40% of global iron ore production. The storms have now weakened to a category two, however there is no clarity on how long production will be halted and of any potential costs to the Australian economy.

US Event Calendar

- 6am: Fed’s Harker Speaks in London on Economic Outlook

- 8:30am: Chicago Fed Nat Activity Index, est. -0.4, prior -0.4

- 10:30am: Dallas Fed Manf. Activity, est. 9, prior 13.1

- 8:30pm: Fed’s Rosengren Speaks at Finance Conference in Hong Kong

DB’s Jim Reid concludes the overnight wrap

I hope you all had a good weekend. Only 4 weeks until we move into our new house and on Saturday my wife went out to dinner and casually mentioned our complete gutting and redesigning of our new place. She was asked whether we’d found room for a ‘wrapping room’? She tells me she looked very puzzled but apparently these are now a thing in some circles. Basically, it’s a room dedicated to wrapping presents and its filled with built in rolls of gift paper hanging off the walls and a workstation in the middle with posh sellotape and ribbons of different varieties having their own special structured place. When my wife first told me I had images of a room where a hologram of Kanye West might emerge from the shadows. Anyway, I can’t imagine how many rooms I’d need to have to feel that such a room was the next cab off the ranks. Probably around 3000 rooms! However, I’d love to hear from any readers with a wrapping room or who knows of anyone with one!

To stay with a rap, the mantra of last week was that “the Fed was dovish but the markets were sluggish!”. With volatility returning close to multi-year or all time lows in many assets classes in the first half of last week, the second half certainly jolted markets back to life. Firstly, the dovish Fed on Wednesday made people wonder what they saw in the future to make them so cautious. Yields collapsed and then Friday’s awful flash manufacturing PMIs in the core of Europe accelerated this and the US yield curve responded and inverted at more points on the curve, including some of those closely watched by the Fed. Indeed, the US 3m10y curve inverted for the first time since 2007 on Friday, and the spread between the 3m yield 18 months forward and the current 3m bill (an apparent favourite at the Fed) dropped to -25.9bps, its lowest level since 2008. The data and inversion led to the S&P 500 (-1.89%) experiencing its worst day since January 3, 2019.

It’s worth reminding readers of our “Yield Curve 101” note from last December (click here ). Throughout my career the US YC has been by a long distance my favourite lead indicator of the US economy. This note shows that the most reliable indicator of a looming recession has actually been a 2s10s inversion. Last week this flattened -3.0bps (-0.9bps Friday) to 11.8bps (below 10bps at the intra-day lows), its flattest level since December. We still haven’t inverted yet and the lag between inversion and recession is usually 12-18 months. The problem is we are a bad session or two from doing so. As a reminder, we don’t care why the curve inverts but instead think that in a capitalist economy like the US, animal spirits – and with it economic growth – are very linked to the steepness of the curve. Before last week, our view was that the curve may invert in the second half of 2019 and elevate the risks of a recession in H2 2020. However, the move over the last few days increases the risks of both arising earlier even if we haven’t yet changed our view. There will be those who say that this time is different and indeed the Fed’s Evans said today in a speech in Hong Kong that there has been a secular decline in long-term interest rates and in such an environment it’s more natural for yield curves to be somewhat flatter than historically was the case. He added that the US labor market is extremely strong at present and he’s not worried about inflationary pressures increasing.

To be fair, what happens next with US/China trade talks will probably have a big influence on the curve (and global growth) in the near term, so all eyes on US Trade Representative Lighthizer and Treasury Secretary Mnuchin trip to China for further talks on Thursday and Friday.

For now though Asia markets are following Wall Street’s lead from Friday with the Nikkei (-3.10%), Hang Seng (-1.77%), Shanghai Comp (-1.38%) and Kospi (-1.76%) all trading in a sea of red alongside most markets. Elsewhere, futures on the S&P 500 are down -0.44% extending Friday’s declines, while, yields on 10y JGBs are down -1.2bps to -0.092% the lowest since September 2016, when the BoJ overhauled its monetary policy to focus less on asset purchases. 10yr USTs are broadly flat.

Just before Asia opened, US Attorney General Barr said that Special Counsel Robert Mueller found no evidence of Trump colluding with Russia after his 22-month report on the matter was delivered late on Friday. The report did fail to exonerate President Trump on obstruction of justice even if the Attorney General said he didn’t find enough evidence to pursue an obstruction charge. This is clearly good news for the President but the battle will now be on how much gets released from the report. The Democrats will clearly be pushing hard to see the full report with the US House of Representatives Speaker Nancy Pelosi and Senate Democratic leader Chuck Schumer already saying in a joint statement that “Congress requires the full report and the underlying documents so that the committees can proceed with their independent work, including oversight and legislating to address any issues the Mueller report may raise.” Further, Jerrold Nadler, chairman of the House Judiciary Committee, has said in a tweet that, “in light of the very concerning discrepancies and final decision making at the Justice Department following the Special Counsel report, where Mueller did not exonerate the President, we will be calling Attorney General Barr in to testify.” So one to continue to watch.

As for Brexit, the situation is very very fluid and MV3 probably won’t come this week if there is no chance of it passing. Instead, we may move onto to indicative votes either voluntarily or forced upon the government. MPs will debate Brexit today and a series of amendments are likely coming, which will surely include a vote on indicative votes. The UK weekend press was rife with speculation that Mrs May was close to being toppled with a caretaker PM expected to oversee Brexit negotiations. However, as Sunday progressed the names discussed as potential caretakers distanced themselves from the process and we’re no further along on knowing whether Mrs May will survive the week. Mrs May convened a gathering of many prominent Brexiteers and some cabinet members at her country retreat Chequers yesterday and we’ll likely know much more today if anything came of that. In the meantime, in a front page editorial today, the Sun newspaper has called on May to resign to help seal her deal and deliver Brexit. The Telegraph had also reported over the weekend that PM May is only prepared to set out a timetable for her resignation once she is sure that she had the votes to support her Brexit deal. Overnight, the Telegraph’s political reporter said that PM May is considering offering indicative votes on Brexit options including her deal, no deal, a 2nd referendum, revoking A50 and a FTA customs union and single market. Sterling is trading down (-0.11%) this morning after falling -0.66% last week. At the lows on Thursday, as no-deal risks increased, it was down -2.15% for the week.

Back to Friday, now with the big news coming from the sharp downside surprise in the flash manufacturing European PMI data, which sparked a significant rally in global core rates and a selloff in equities. The Euro-area manufacturing PMI fell -1.7pts to 47.6, its lowest level since April 2012, being dragged down by the very weak print in Germany, where the manufacturing PMI fell -2.9pts to 44.7, the second lowest since 2009. The new orders sub-index did fall to a new post-crisis low at 40.1. Remarkably bad numbers. The composite euro area print fell -0.6pts to 51.3, which is consistent with quarterly growth around 0.15% qoq. That’s dangerously close to stalling speed, though it’s consistent with DB’s House View for Q1 growth of 0.1% qoq. France’s composite print fell -1.7pts to 48.7, dipping into contractionary territory with manufacturing -1.7pts to 49.8 and services -1.5pts to 48.7. Services in Germany and the Euro-Area held up well at 54.9 and 52.7 respectively so this is predominantly a manufacturing story for now. Can the recent mini China stimulus and upcoming trade talks save the day?

Anyway the data made it a difficult week as the STOXX 600 fell -1.33% (-1.22% on Friday) and the DAX shed -2.75% (-1.61% Friday). Bund yields fell -9.8bps (-5.6bps Friday) to -0.02%, sliding below zero for their first time since October 2016. The drop in yields weighed on financials, with an index of bank stocks declining -4.52% (-3.05% Friday). The S&P 500 and NASDAQ marginally outperformed, shedding -0.77% and -0.60% (-1.89% and -2.50% Friday), respectively. Other core government bond markets benefited from the flight to safety, with 10-year yields in the US and UK falling -15.5bps and -19.7bps (-10.5bps and -5.0bps on Friday) on the week.

One area of notable stress was in emerging markets, where an index of equities fell -2.93% on Friday for their worst session since October (-1.51% on the week). An index of EM currencies weakened -1.12% on the week, including -1.71% on Friday with losses led by the Turkish lira. The lira had its worst session since last August, depreciating -6.03% on Friday as the combination of slower European growth and evidence of capital outflows weakened the outlook. There are also suspicions that the central bank has been intervening to maintain the currency’s strength in recent weeks, and the CBT’s move to tighten liquidity by suspending its one-week repo auctions did not inspire confidence among investors. The one-week facility is nominally the main policy instrument, but officials steer financing into the more expensive overnight facility (at 25.5%) or the late liquidity window (27%) when they want to tighten conditions. The lira has recouped some of the Friday’s decline’s and is up +2.2% this morning with Turkey’s government announcing an investigation into JPMorgan and another probe of unspecified banks that the CBT reproached for stoking the lira’s Friday’s plunge.

Back to the Fed and on Friday, President Trump announced his intention to nominate Stephen Moore as a Fed Governor. It will be interesting to see how he is received by the Senate and by other Fed leadership, considering he recently called for the entire Fed Board to “be thrown out for economic malpractice.” Whether or not this added to market nerves on Friday its hard to tell but it is certainly controversial.

Believe it or not, the quarter draws to a close on Friday with a few interesting events on the agenda before it does. Outside of Brexit and the end of week trade talks mentioned earlier, we also have a number of central bank speakers, including ECB President Draghi (Wednesday), Federal Reserve Vice Chair Clarida and Vice Chair Quarles (both Thursday). Finally, a number of key data releases are expected, with the highlights including the German IFO surveys (today), Eurozone CPI data (Friday) and updated readings for Q4 GDP in the US (Thursday), UK (Friday) and France (Tuesday).

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 61.12 POINTS OR 1.97% //Hang Sang CLOSED DOWN 590.01 POINTS OR 2.03% /The Nikkei closed DOWN 650.23 POINTS OR 3.01%/ Australia’s all ordinaires CLOSED DOWN 1.15%

/Chinese yuan (ONSHORE) closed DOWN at 6.7136 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 58.94 dollars per barrel for WTI and 66.90 for Brent. Stocks in Europe OPENED RED

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7136 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7187 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA

The USA demands that China uses the USA’s cloud computing services something that China refuses to budge on

(courtesy zerohedge)

Another Trade-Deal Obstacle Emerges: China Refuses To Budge On Cloud Computing

With trade-related news in a rare lull, fears about an imminent global recession appeared to be at the forefront of investors’ minds last week, as the Fed took a surprisingly dovish turn, which was accompanied by another apprehensive cut to its GDP forecasts, and a spate of weak industrial production data out of Europe (Where the Continent’s largest economy has likely already slid into recession) stoked fears that what has been one of the longest expansions in modern history might reach its disastrous conclusion before the end of the year.

Amid the vertiginous twists in US equities – amid a spate of single-stock narratives (Boeing’s continued troubles, the decline in Nike’s North American sales, bank stocks being hammered by the yield curve inversion) – President Trump’s comments about a possible tariffs compromise on Friday didn’t raise too many eyebrows.

But what he said, though the White House once again declined to elaborate, is still important. Because it once again inadvertently illustrated just how far apart Washington and Beijing are. Despite the optimistic rhetoric, it appears that a final deal remains bewilderingly remote.

And as Robert Lighthizer and Steve Mnuchin prepare to return to Beijing this week to continue talks with Liu He, another obstacle in the increasingly fraught negotiations appears to have emerged.

By all accounts, Beijing hasn’t dropped its demands that the US lift most – if not all – of its trade-war tariffs on Chinese imports – immediately as part of the final deal. And while issues ranging from enforcement to currency manipulation to Chinese structural reforms have yet to be resolved, when it comes to the latter of these, the Financial Times on Sunday offered a little more clarity about a particularly important issue: digital trade.

As Amazon searches for still more growth markets, and Apple pivots to being a “services”-focused company, America’s tech giants are insisting that China lower its barriers to competition for American cloud computing providers. Per the FT’s sources, the issue is expected to be one of the main topics of discussion during this week’s meetings.

According to three people briefed on the talks, China has yet to offer meaningful concessions on US requests that it end discrimination against foreign cloud computing providers, curb requirements for companies to store data locally, and loosen limits on the transfer of data overseas.

The impasse over digital trade is among the issues expected to be on the table when Robert Lighthizer, the US trade representative, and Steven Mnuchin, the Treasury secretary, travel to Beijing on March 28 for meetings with Liu He, China’s vice-premier and leading economic official. Mr Liu is expected to return to Washington the following week, and the two sessions combined could be pivotal for the fate of the talks.

With North Korea already acting up, it’s worth considering that Beijing might be pulling strings to exert more pressure on the US, now that the trade-deal impasse has persisted for months now. On a similar note, analysts and traders have long pondered how Washington’s war against Huawei might impact trade talks.