GOLD: $1315.30 DOWN $7.30 (COMEX TO COMEX CLOSING)

Silver: $15.43 DOWN 13 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1315.70

silver: $15.43

Comex options expire next week: Wednesday March 27

London/LBMA expires Monday March 31/2019.

The crooks continue with their whacking right in front of the authorities/regulators despite the criminal probe of precious metals manipulations.

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 11 NOTICE(S) FOR 1100 OZ (0.00342 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 395 NOTICES FOR 39500 OZ (1.2286 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

4 NOTICE(S) FILED TODAY FOR 20,000 OZ/

total number of notices filed so far this month: 5384 for 26,920,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3928:DOWN $9

Bitcoin: FINAL EVENING TRADE: $3934 DOWN 2

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 2/11

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,321.900000000 USD

INTENT DATE: 03/25/2019 DELIVERY DATE: 03/27/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 2

661 C JP MORGAN 2

737 C ADVANTAGE 8 7

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 11 11

MONTH TO DATE: 395

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST CONTINUES TO RISE FOR THE SIXTH CONSECUTIVE TIME: THIS TIME BY A FAIR SIZED 866 CONTRACTS FROM 192,250 UP TO 193,116 WITH YESTERDAY’S 15 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 1210 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1210 CONTRACTS. WITH THE TRANSFER OF 1210 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1210 EFP CONTRACTS TRANSLATES INTO 6.050 MILLION OZ ACCOMPANYING:

1.THE 15 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 27.120 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

33,027 CONTRACTS (FOR 18 TRADING DAYS TOTAL 33,027 CONTRACTS) OR 165.135 MILLION OZ: (AVERAGE PER DAY: 1834 CONTRACTS OR 9.174 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 165.135 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 23.57% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 530.52 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 866 WITH THE 15 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1210 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY STRONG SIZED: 2076 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1210 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 866 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 15 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $15.56 WITH RESPECT TO FRIDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.936 BILLION OZ TO BE EXACT or 134% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 4 NOTICE(S) FOR 20,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 27.120 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE 6123 CONTRACTS, TO 524,865 WITH THE STRONG RISE IN THE COMEX GOLD PRICE/(AN INCREASE IN PRICE OF $9.85//YESTERDAY’S TRADING). AND NO EVIDENCE OF ANY SPREADING LIQUIDATION IN GOLD AS WE ARE NOW APPROACHING FIRST DAY NOTICE IN AN ACTIVE DELIVERY MONTH.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6007 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 4991 CONTRACTS,JUNE: 1016 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 524,865. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,130 CONTRACTS: 6123 OI CONTRACTS INCREASED AT THE COMEX AND 6007 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 12,130 CONTRACTS OR 1,213,000 OR 37.73 TONNES.

YESTERDAY WE HAD A GAIN IN THE PRICE OF GOLD TO THE TUNE OF $9.85....AND WITH THAT, WE HAD A HUGE GAIN IN TONNAGE OF 31.73 TONNES!!!!!!.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 124,816 CONTRACTS OR 12,481,600 OR 388.23 TONNES (18 TRADING DAYS AND THUS AVERAGING: 6934 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAYS IN TONNES: 388.12 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 388.23/2550 x 100% TONNES = 15.22% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1257.19 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 6123 WITH THE GAIN IN PRICING ($9.85) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6007 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6007 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG GAIN OF 12,130 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6007 CONTRACTS MOVE TO LONDON AND 6123 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 37.73 TONNES). ..AND ALL OF THIS STRONG DEMAND OCCURRED WITH A RISE IN PRICE OF $9.85 IN YESTERDAY’S TRADING AT THE COMEX!!!!!

we had: 11 notice(s) filed upon for 1100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $7.30 TODAY

NO CHANGES IN GOLD INVENTORY

INVENTORY RESTS AT 781.03 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 13 CENTS IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV TODAY

/INVENTORY RESTS AT 309.488 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A FAIR SIZED 866 CONTRACTS from 192,325 UPTO 193,116 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 1210 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1210 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 866 CONTRACTS TO THE 1210 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 2076 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 10.38 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 27.120 MILLION OZ FOR MARCH.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 15 CENT RISE IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A STRONG SIZED 1210 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 45.94 POINTS OR 1.51% //Hang Sang CLOSED UP 43.58 POINTS OR 0.15% /The Nikkei closed UP 451.28 POINTS OR 2.15%/ Australia’s all ordinaires CLOSED UP 0.07%

/Chinese yuan (ONSHORE) closed UP at 6.7129 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 59.53 dollars per barrel for WTI and 67.72 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7129 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7173 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

i)UK/ LAST NIGHT

Mutiny on the Bounty

(zerohedge)

iii)An excellent commentary from our resident expert on BREXIT and how the EU will do everything in their power to milk as much tax dollars out of Britain.The whole EU project will fail.

( Tom Luongo)

iv)In this latest rebuke of Washington, the EU and all of their capitals refuses to recommend a bloc wide Huawei ban

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Turkey

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Venezuela/Russia/USA

As soon as Russian troops arrive, Venezuela is plunged into darkness for the 3rd time this month

(courtesy zerohedge)

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

ii)Market data

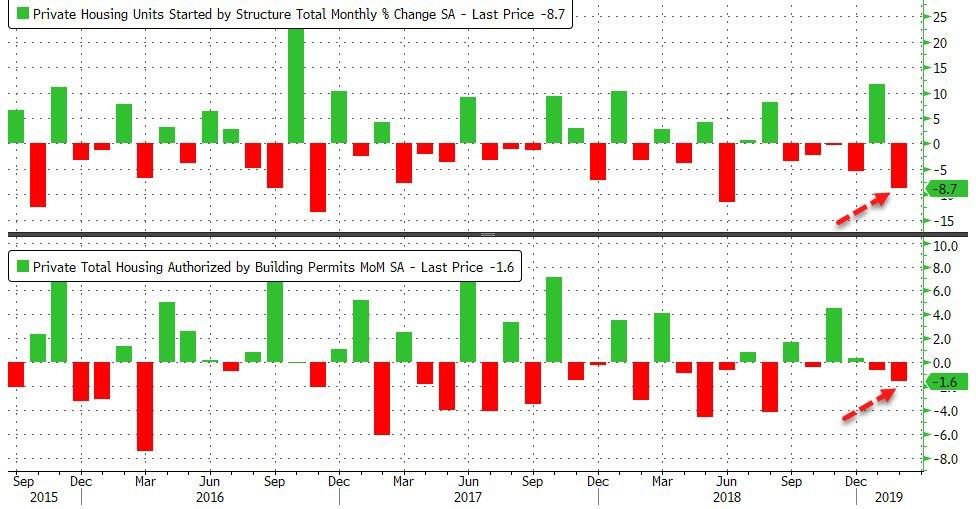

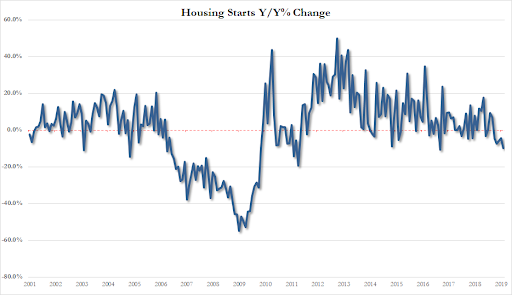

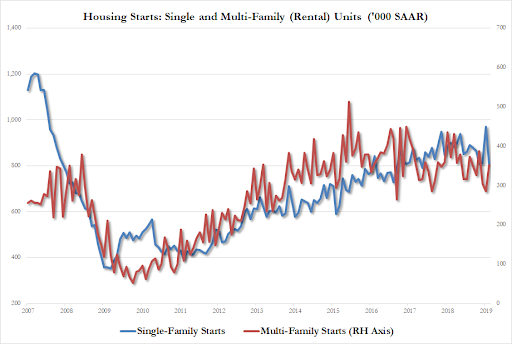

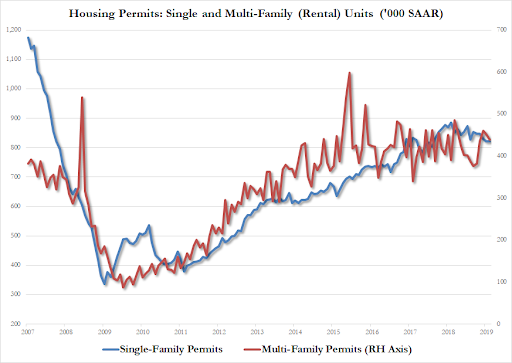

a)Housing is hammered again with starts and permits plunging

( zero hedge)

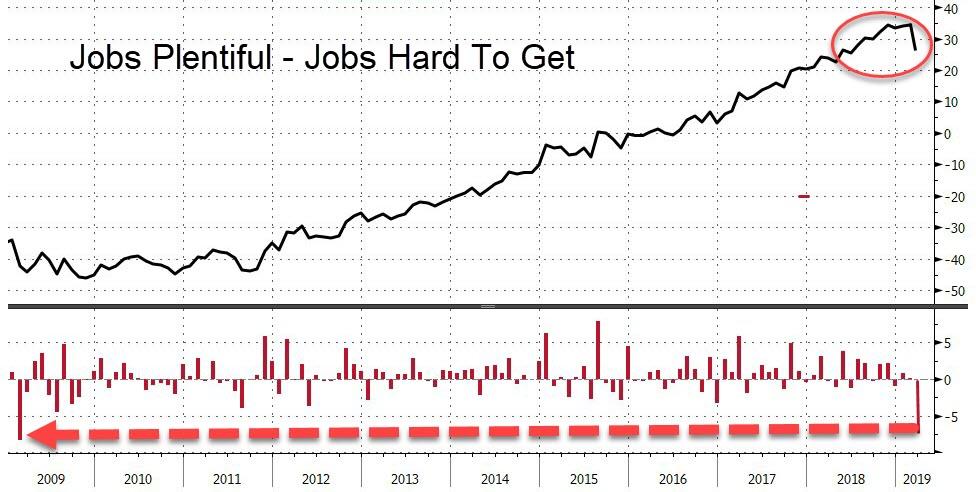

b)Soft data, consumer confidence crashes

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

An open letter to Jerome Powell from Mish Shedlock

( Mish Shedlock

iv)SWAMP STORIES

a)MSNBC anchors going nuts after their darling Avenatti was arrested

(courtesy zerohedge)

b)Just one word with respect to Brennan: Hogwash!!

( zerohedge)

end

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL LOWERS TO 774 CONTRACTS FOR A LOSS OF 3 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI FELL BY 399 CONTRACTS UP TO 136,260 CONTRACTS.

i)out of Scotia: 2057.60 oz

64 kilobars

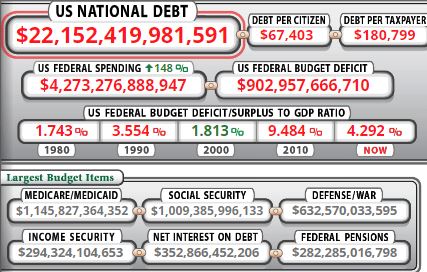

America’s “Debt Crisis Is Coming Soon”

– America’s “debt crisis is coming soon” warns economist Martin Feldstein

– To avoid economic distress, the government has to reduce future entitlement spending

– The most dangerous domestic problem facing America’s federal government is the rapid growth of its budget deficit and national debt

According to the Congressional Budget Office, the deficit this year will be $900 billion, more than 4% of gross domestic product. It will surpass $1 trillion in 2022.

The federal debt is now 78% of GDP. By 2028, it is projected to be nearly 100% of GDP and still rising.

All this will have very serious economic consequences, and the CBO understates the problem. It has to base its projections on current law—in this case, the levels of spending and the future tax rules and rates that appear in law today.

Source: USDebtClock.org

Those levels don’t match realistic predictions.

Current law projects that defense spending will decline as a share of GDP, from a very low 3.1% now to about 2.5% over the next 10 years. None of the military and civilian defense experts with whom I’ve spoken believe that will happen, given America’s global responsibilities and the need to modernize U.S. military equipment. It is likelier that defense spending will stay around 3% of GDP or even increase in the coming decade. And if the outlook for defense spending is increased, the Democratic House majority will insist that the non-defense discretionary spending should rise to match its trajectory.

If defense and other discretionary spending stays steady as a share of GDP, the annual deficit will increase by nearly 1% of GDP—from 4.2% of GDP now to about 5% of GDP 10 years from now. At the same time, the tax increases in current law that the CBO assumes will occur during the next decade as some of the recent cuts are phased out probably won’t happen. Congress will face strong political pressure to avoid a functional tax increase.

What does that mean for the long-run ratio of the federal debt to GDP? Federal debt will probably surpass 100% much sooner than 2028. If discretionary spending increases, debt growth will jump to 100% even quicker. When America’s creditors at home and abroad realize this, they will push up the interest rate the U.S. government pays on its debt. That will mean still more growth in debt. A 1% increase in the interest rate the government pays on its debt would boost the annual deficit by more than 1%. The higher long-run debt-to-GDP ratio would crowd out business investment and substantially reduce the economy’s growth rate. That in turn would mean lower real incomes and less tax revenue, leading to—you guessed it—an even higher debt-to-GDP ratio.

To avoid economic distress, the government either has to impose higher taxes or reduce future spending. Since raising taxes weakens incentives and further slows economic growth—worsening the debt-to-GDP ratio—the better approach is to slow government spending growth. Defense spending and nondefense discretionary outlays can’t be reduced below the unprecedented and dangerously low shares of GDP that the CBO projects.

Thus the only option is to throw the brakes on entitlements. In particular, the government needs to hold back the growth of Medicare, Medicaid and Social Security. Federal spending on the two major health programs is projected to rise from its current 5.5% of GDP to more than 7.2% by 2029. And it will only keep increasing after that.

The simplest approach is to raise the age of eligibility for Social Security, as Congress did in 1983. Bipartisan legislation then voted to postpone “full” benefits from age 65 to 67, allowing earlier benefits at an actuarially reduced level. Because Congress slowly phased the change in over several decades, it avoided any significant political opposition. In the intervening 35 years, the average life expectancy of Americans in their late 60s has risen about three years. It would be appropriate to increase the age of eligibility for full benefits from 67 to 70 and index it to life expectancy. Exceptions could be made for retirees with low lifetime incomes.

Lawmakers don’t like to cut spending, but they have to do something. Otherwise the exploding national debt will be an increasing burden on our children, economic growth and our future standard of living.

By Martin Feldstein in the Wall Street Journal

News and Commentary

Gold gains as U.S. recession fears lift safe-haven appeal (Reuters.com)

Russia sends more than 100 troops to Venezuela (SantiagoTimes.cl)

Stocks tumble, bonds rally as U.S. recession risk flashes ‘amber’ (Reuters.com)

One by One, Global Bond Markets Are Flashing the Same Warning (Bloomberg.com)

Trump nominates to Fed board a harsh critic of its chairman (Reuters.com)

The Debt Crisis Is Coming – Marty Feldstein (WSJ.com)

Bond Market Flashes Recession Warning Before Round of Auctions (Bloomberg.com)

Three Months of Gains Haven’t Conquered Fears: Taking Stock (Bloomberg.com)

What The Fed Got Wrong (But The Bond Market Knew All Along) (ZeroHedge.com)

Gold will be ‘last man standing in this nutty fiat currency world’ (KingWorldNews.com)

Gold Prices (LBMA PM)

22 Mar: USD 1,311.10, GBP 998.80 & EUR 1,159.41 per ounce

21 Mar: USD 1,317.30, GBP 1002.99 & EUR 1,155.80 per ounce

20 Mar: USD 1,303.00, GBP 985.07 & EUR 1,147.81 per ounce

19 Mar: USD 1,308.35, GBP 985.06 & EUR 1,152.53 per ounce

18 Mar: USD 1,305.35, GBP 986.19 & EUR 1,150.01 per ounce

15 Mar: USD 1,302.35, GBP 981.55 & EUR 1,150.55 per ounce

Silver Prices (LBMA)

22 Mar: USD 15.46, GBP 11.75 & EUR 13.68 per ounce

21 Mar: USD 15.54, GBP 11.85 & EUR 13.64 per ounce

20 Mar: USD 15.32, GBP 11.58 & EUR 13.49 per ounce

19 Mar: USD 15.41, GBP 11.61 & EUR 13.57 per ounce

18 Mar: USD 15.38, GBP 11.60 & EUR 13.54 per ounce

15 Mar: USD 15.35, GBP 11.58 & EUR 13.56 per ounce

Recent Market Updates

– Russia Buys 1 Million Ounces Of Gold In February – Become Your Own Central Bank

– 5 Ways to Prosper In the Coming Crisis – Goldnomics Podcast

– Deutsche Bank and Commerzbank May Become EU’s “Too Big To Fail” Bank

– Happy Saint Patrick’s Day from GoldCore

– 188 Internet Shutdowns In 2018 Show Why Physical Gold Is Ultimate Protection

– Buy Gold as Basel III Means “Central Banks and Banks Are Going To Be Buying Gold”

– Invest In Gold Or Bitcoin – Which Is The True Store Of Value?

– Silver Bullion Is The Portfolio Insurance To Buy Now

– EU Isn’t Ready for the Next Recession

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7129/

//OFFSHORE YUAN: 6.7173 /shanghai bourse CLOSED DOWN 45.94 POINTS OR 1.51% /

HANG SANG CLOSED UP 43.58 POINTS OR 0.15%

2. Nikkei closed //UP 451.28 POINTS OR 2.15%

3. Europe stocks OPENED GREEN

/USA dollar index FALLS TO 96.50/Euro RISES TO 1.1325

3b Japan 10 year bond yield: RISES TO. –.07/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.37/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 59.53 and Brent: 67.72

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO –.01%/Italian 10 yr bond yield UP to 2.48% /SPAIN 10 YR BOND YIELD UP TO 1.11%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.49: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.79

3k Gold at $1314.55 silver at:15.46 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 19/100 in roubles/dollar) 64.18

3m oil into the 59 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.37 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9927 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1239 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.01%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

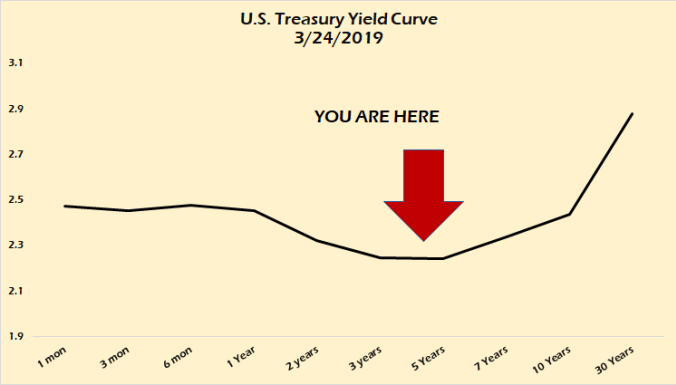

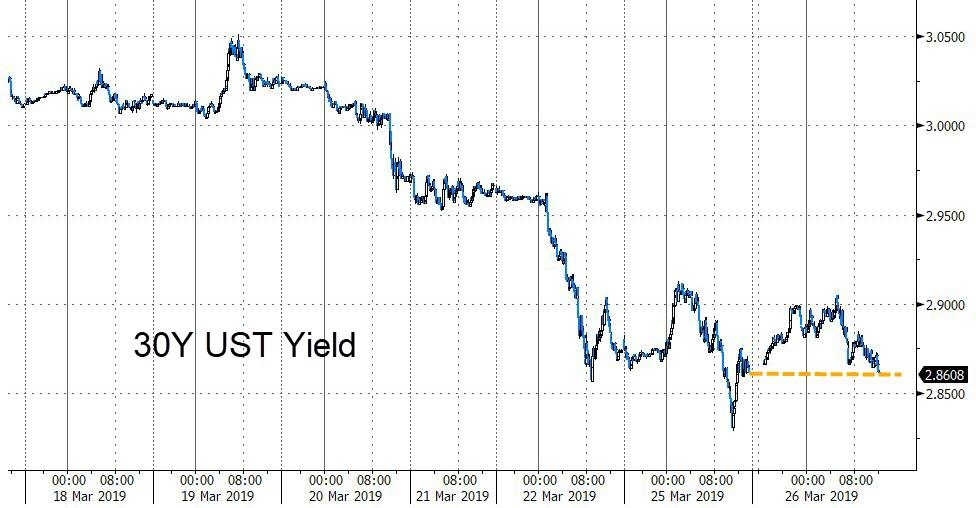

4. USA 10 year treasury bond at 2.45% early this morning. Thirty year rate at 2.90%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.5129

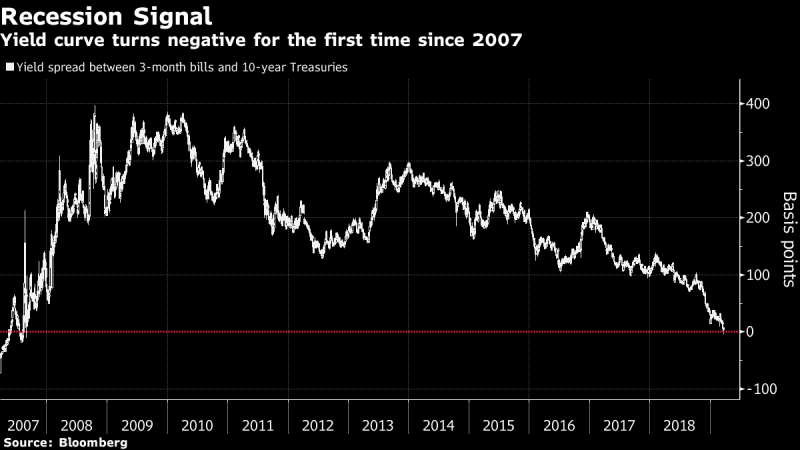

Global Stocks, US Futures Rebound As Recession Fears Fade, Yields Rise

And just like that, the panicked freakout over tumbling interest rates around the globe is over with calm returning to global markets as a steadier day for Europe and Asia’s markets and a rebound in bond yields helped ease nerves after a jarring few days dominated by recession worries.

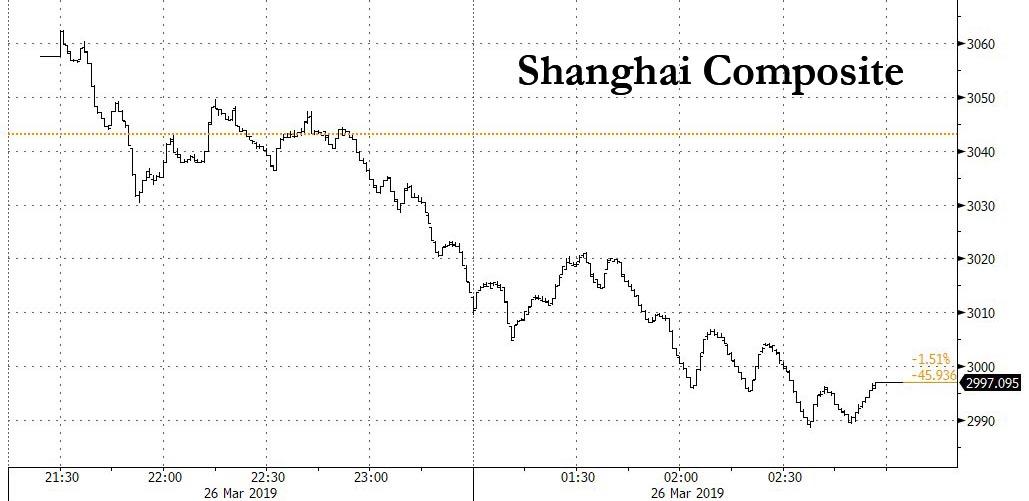

Even as over $10 trillion in global debt now carries a negative yield, a sense of optimism swept across global markets with S&P futures climbing sharply on Tuesday, following a rise in European and Asian shares even as Chinese stocks posted another steep, 1.5% drop, pushing the Shanghai Composite below 3,000 for the first time in two weeks.

Yields on US Treasuries rose across the curve after the 10Y yield closing below the effective fed funds rate of 2.4% on Monday, although the spread between three-month and 10-year rates remained in negative territory. The 10Y shed 5 basis points on Monday and a whopping 17.5 basis points since the Federal Reserve last week ditched projections for raising rates this year.

Meanwhile, fed funds rate futures are now fully factoring in a rate cut later this year, with about an 80 percent chance of a move priced in by September.

“The U.S. yield curve continues to invert,” said Michael Every, Hong Kong-based senior Asia-Pacific strategist at Rabobank. “This is not a healthy sign, as bond-market watchers should know and equity-market obsessives should rapidly learn.”

Equities took the modest rebound in stride, as futures on the Dow Jones, Nasdaq and S&P 500 indexes all advanced, and gains in healthcare companies helped the Stoxx Europe 600 into the green. The bond markets remained the main focus though: 10-year German government bond yields remained below zero as European bonds tracked Treasuries lower and the euro edged up against the greenback.

Earlier in Asia, the MSCI index of Asia-Pacific shares rebounded 1% after losing 1.4% in the previous session, though there were some eye-catching moves. Japan’s Nikkei jumped 2.1% after recording its biggest drop since late December on Monday; the Topix Index jumped more than 2.5 percent, a day after it had its biggest slide this year, helping MSCI Asia Pacific index rise one percent; even the Kospi eked out a 0.3% gain despite a profit warning from Samsung. Meanwhile, the selling in China continued, with the Shanghai Composite dropping below 3000 for the first time in 2 weeks.

India jumped over 1 percent whereas China’s blue-chip CSI300 index dropped more than 1 percent as trade war worries remained. The Aussie 10-year yield nudges three basis points higher after printing record low 1.75% in early trading, meanwhile JGB futures extend losses after uninspiring 40-year bond auction. Emerging-market currencies were steady as shares edged up.

“The world is looking to fade the risk aversion caused by the inversion of the (U.S.) yield curve,” said SocGen’s Kit Juckes, adding that it was anyway difficult to position for a hypothetical recessions.

Sure enough, as Reuters notes, investors have been spooked by sharp falls in U.S. bond yields and an inversion of the U.S. Treasury yield curve, widely seen as an indicator of an economic recession.

Going back to bonds, the US Treasury Department will sell $113 billion in coupon notes this week, including $40 billion in two-year notes on Tuesday, $41 billion in five-year notes on Wednesday and $32 billion in seven-year notes on Thursday. Investors will also be watching Fed policymakers scheduled to speak on Tuesday.

With bonds now signalling a recession, the outcome of trade talks between America and China and any developments in Britain’s tortuous exit of the European Union could help determine sentiment from here. “It’s premature to talk about the yield curve meaning that we have to go into recession,” Philip Wyatt, a Hong Kong-based economist for UBS Group AG, said on Bloomberg Television. “It’s possible for the long end to run too far, too fast,” he said of U.S. Treasuries.

In overnight central bank news, Fed’s Rosengren (voter, hawk) said returning Fed assets to pre-crisis levels is not desirable nor feasible and that the balance sheet is likely to grow, while he added that it may be important to increase share of Treasury bills as well as lower duration of balance sheet more quickly. Furthermore, Rosengren noted that Fed pause is the responsible action to do now and that the dot plot is not a promise of policy direction which depends on changes to the economy. Separately, Fed’s Harker said he was not supportive of the December move and reiterates that he is in wait and see mode, favoring at most one hike this year and one in 2020.

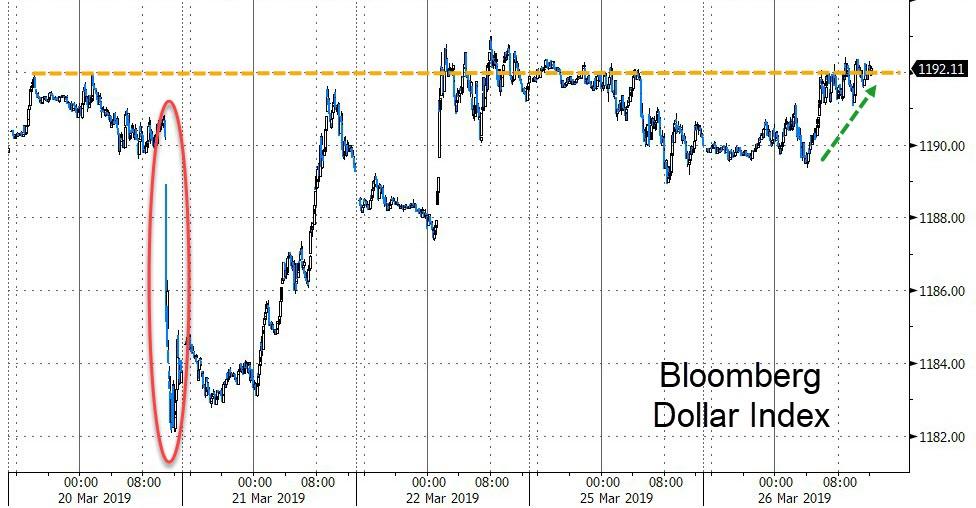

In the currency market, the Bloomberg dollar index marginally stronger while the euro stood firm at $1.1305, having gained a tad on Monday after Germany’s IFO Institute said its business climate index rose to 99.6, beating a consensus forecast of 98.5 and ending six consecutive months of decline. The dollar was 0.6 percent higher versus the yen at 110.42 yen, having hit a 1-1/2-month low of 109.70 on Monday, while British pound was barely budged at $1.3180 after lawmakers voted late on Monday to wrest further control of the Brexit process from Prime Minister Theresa May.

“We expect EUR/USD to stabilize around the current level of 1.13 and see a limited downside for the rest of week,” said currency strategists at ING.

Among commodities, oil prices hovered below their recent four-month peaks, as the prospect of tighter U.S. crude supply was offset by concerns about a slowdown in global economic growth. U.S. crude futures traded at $59.55 per barrel, up three-quarters of a percent on the day but below Thursday’s $60.39, which was its highest level since mid-November. Brent futures were up 0.7% as rising tension in Venezuela threatened to further curb supplies from the holder of the world’s largest crude reserves.

Gold retreated for the first time in three days, down a third of a percent at $1,317.60 having hit a one-month high of $1,324.60 on Monday.

Housing starts and Conference Board Consumer Confidence readings are due. Scheduled earnings include Carnival and IHS Markit

Market Snapshot

- S&P 500 futures up 0.2% to 2,813.25

- STOXX Europe 600 up 0.1% to 374.87

- MXAP up 1% to 159.86

- MXAPJ up 0.3% to 523.41

- Nikkei up 2.2% to 21,428.39

- Topix up 2.6% to 1,617.94

- Hang Seng Index up 0.2% to 28,566.91

- Shanghai Composite down 1.5% to 2,997.10

- Sensex up 0.5% to 37,982.27

- Australia S&P/ASX 200 up 0.07% to 6,130.59

- Kospi up 0.2% to 2,148.80

- German 10Y yield rose 0.3 bps to -0.025%

- Euro down 0.05% to $1.1306

- Brent Futures up 0.5% to $67.56/bbl

- Italian 10Y yield rose 5.3 bps to 2.148%

- Spanish 10Y yield rose 0.7 bps to 1.108%

- Brent Futures up 0.5% to $67.56/bbl

- Gold spot down 0.4% to $1,316.81

- U.S. Dollar Index up 0.04% to 96.60

Top Overnight News

- U.K. Parliament seized control of the Brexit process from Prime Minister Theresa May and will now seek to decide how Britain exits the European Union. In a vote late Monday, the House of Commons split 329 to 302 to schedule votes on a series of alternative strategies, potentially including a second referendum

- A global rush to buy sovereign debt kept on going in Treasuries Monday, with bond traders increasing wagers that the Federal Reserve will have to cut interest rates later this year. Overnight index swaps showed 25bps worth of easing are expected by the central bank’s October meeting

- The next step in Attorney General William Barr’s work on the Mueller report is deciding just how much of it to release, and one person is likely to get a big say in the answer: President Donald Trump

- Oil rebounded along with global markets as pessimism over the global growth outlook eased a little, and rising tension in Venezuela threatened to further curb supplies

- The global iron ore market will get a glimpse of how dire the supply situation looks when Vale addresses analysts this week for the first time since the fatal dam disaster in January in Brazil

- U.S. President Donald Trump and a key ally, Senate Judiciary Chairman Lindsey Graham, said Monday that after Robert Mueller closed his Russia probe, they want an investigation of the investigators

- Federal Reserve Bank of Boston President Eric Rosengren still thinks the central bank’s next move for interest rates is more likely to be a hike than a cut. He just won’t be surprised if that turns out wrong

- Euro-area banks will know by June how generous the terms of the European Central Bank’s new loans are going to be, according to Governing Council member Olli Rehn

- Turkish authorities have made it virtually impossible for foreign investors to short the lira. The overnight swap rate for the currency blew out by a whopping 73 percentage points to 96.34 percent on Monday, as offshore funds clamoring to close out long-lira positions failed to find counterparties, according to two people with direct knowledge of the matter

Asian equity markets were mostly higher as the region took the consolidation on Wall St as a cue to pick itself up from the prior day’s sell-off. ASX 200 (+0.1%) was choppy as weakness in energy, tech and financials off-set the strength in miners, while Nikkei 225 (+2.1%) outperformed on bargain hunting after the prior day’s 3% drop and its worst performance YTD with Tokyo sentiment also boosted by currency weakness and reinvestment buying heading into ex-dividend day tomorrow. Hang Seng (-0.2%) and Shanghai Comp. (-1.5%) both began higher, although sentiment in the mainland eventually deteriorated after another PBoC liquidity drain and amid tentativeness ahead of upcoming blue-chip earnings including the Big-4 banks later this week with the industry anticipated to post slower profit growth for a 5th consecutive year. Finally, 10yr JGBs were lower with demand subdued amid the heightened risk appetite in Tokyo and following the mixed results in the 40yr auction.

Top Asian News

- Once-in-Century Rain Hits Australia as Ports Return After Storm

- Citigroup Faces Fine for Allegedly Manipulating JGB Futures

- Election Cash Splash Spurs Southeast Asia’s Biggest Economy

- Ocado Says Coles Deal to Be Earnings Negative in Current Year

Major European indices are slightly firmer [Euro Stoxx 50 +0.3%] roughly in-line with how they started the session, in-spite of indices drifting somewhat into mixed/negative territory not long after the open. In a similar pattern, after opening the session all in the green, major sectors are now mixed, with some mild outperformance seen in Energy names. The FTSE 100 (+0.3%) is firmer, boosted by the likes of Ocado (+4.3%) after signing a deal with Australian supermarket chain Coles at the top of the index alongside housing names such as Persimmon (+2.3%) and Fresnillo (+1.2%) after positive broker moves. However, the FTSE 100’s gains are hampered by the significant underperformance seen in Ferguson (-9.0%) shares after the Co. warned that FY profit will be towards the lower end of expectations. Other notable movers include, Airbus (+2.4%) after reports just before 16:00GMT yesterday that they had secured an order from China at which Co. shares moved higher and Boeing shares saw some negativity. Subsequently, further details have emerged that the deal is for 300 jets with an estimated value of around USD 35bln; which is almost double the level that had been indicated by French President Macron in 2018. Elsewhere, Rolls Royce (-1.8%) who are in negative territory after being reiterated underweight at Morgan Stanley. Of note for tech names Samsung Electronics (005930 KS) guides Q1 earnigns to be lower than market expectations. For reference Co. shares closed around 0.6% lower.

Top European News

- Bang & Olufsen Shares Slump as Turnaround Efforts Stall

- Credit Suisse Raises Miners to Overweight on China Economy Play

- Intesa Considers Strategic Options for Unlikely-to-Pay Loans

- Pound Volatility Curve Stays Inverted on Various Brexit Options

In FX, the USD remains rangebound and mixed vs G10 counterparts, as the DXY pivots the 96.500 level with technical resistance capping the upside along with month end rebalancing signals pointing to moderate to modest selling vs several major currencies. However, the Buck is also underpinned ahead of 96.000 amidst relative weakness elsewhere, such as the Yen on improving or more stable risk sentiment, Pound on Brexit and Kiwi pre-RBNZ.

- JPY – As noted above, an upturn of recovery in risk appetite has prompted an unwind in safe-haven premiums to the detriment of the Yen in particular, and after recent strengthening through 110.00 vs the Usd the headline pair has now rebounded quite markedly through the big figure and a Fib at 110.23 to trip some stops on the way to 110.42. Note, a hefty 1.8 bn option expiry between 110.10-15 for today’s NY cut appears safe at the current juncture.

- NZD/GBP – Also back under pressure vs the Usd having forged gains on the back of better than forecast NZ trade data in the case of the Kiwi and for Sterling the latest vote in UK Parliament that effectively takes the onus away from PM May in terms of the next Brexit steps. Nzd/Usd is hovering around 0.6900 vs circa 0.6925 at best overnight, while Cable retreated from around 1.3225 to a 1.3160 base again (virtually matching Monday’s low) before rebounding firmly over 1.3200 handle to 1.3250. Note, next up for the Kiwi is March’s RBNZ policy meeting (full preview flagged on the headline feed and within the Research Suite), while the Pound remains hostage to Brexit and will be eyeing Wednesday’s indicative votes.

- AUD/CAD/EUR – All nudging new or nestling near highs vs the Usd, as the Aussie extends above 0.7100 with some favourable tailwinds via the Aud/Nzd cross that has rebounded firmly over 1.0300 amidst the aforementioned pre-RBNZ Kiwi caution. However, Aud/Usd still has some way to go from 0.7135 to arouse any expiry related interest from 1 bn rolling off from 0.7145 to 0.7150. Meanwhile, the Loonie is trying to extend gains above 1.3400 against the backdrop of firm oil prices and news that China has lifted some bans on Candian canola imports, and the single currency is sitting above 1.1300, albeit tight.

- EM – A more stable session so far for the TRY and some outperformance vs regional peers as the Lira continues to pare recent heavy losses, albeit due to intervention or various forms of capital repatriation and amidst further spikes in money market rates. Usd/Try currently near the middle of a 5.4660-5.5925 band. Elsewhere, Eur/Huf is also midway between trading parameters (316.80-00) ahead of a widely anticipated NBH rate hike

- New Zealand Trade Balance (Feb) M/M 12M vs. Exp. -200M (Prev. -914M, Rev. -948M). (Newswires) New Zealand Exports (Feb) 4.82B vs. Exp. 4.70B (Prev. 4.40B, Rev. 4.33B) New Zealand Imports (Feb) 4.80B vs. Exp. 4.90B (Prev. 5.32B, Rev. 5.28B)

In commodities, a firm rebound in the energy complex with WTI and Brent futures advancing further above USD 59.00/bbl and USD 67.50/bbl respectively as global growth pessimism takes a back seat (for now) and risk appetite takes the wheel. OPEC+ members are said to be planning the next JMMC meeting on May 19th after cancelling their April assembly before OPEC+ convenes on June 25-26. ING argues that the cancellation of the April meeting could suggest that the members “are not in agreement to extend the current deal”, set to last until the end of H1 2019. Analysts at ING also speculate that if this is the case, then it is likely that Russia believes an extension is not needed. Nonetheless, traders will be eyeing the usual API crude inventory release later today (2030 GMT/1530 ET) as a fresh catalyst. Elsewhere, metals are relatively mixed with gold (-0.6%) shedding recent gains amid the broad risk appetite whilst copper prices are supported for the same reason. Back to precious metals, UBS raised its 6 and 12-month silver forecasts, both to USD 16.30/oz from USD 15.50/oz and USD 16.00/oz respectively. BHP expects to resume loading iron ore ships at Port Hedland on Tuesday and ramp up output over the approaching days, while it found no major damage from the recent cyclone.

Looking at the day ahead, there are quite a few releases, with a possible highlight being the Conference Board’s consumer confidence reading for March, along with the Richmond Fed’s manufacturing index. In addition, we’ll get February’s data for housing starts and building permits, along with the FHFA’s House Price Index for January. In terms of central bank speakers, we’ve got the Fed’s Harker, Evans and Daly all speaking today, along with the BoE’s Broadbent.

US Event Calendar

- 8:30am: Housing Starts, est. 1.21m, prior 1.23m

- Building Permits, est. 1.31m, prior 1.35m

- 9am: FHFA House Price Index MoM, est. 0.4%, prior 0.3%

- 9am: S&P CoreLogic CS 20-City MoM SA, est. 0.3%, prior 0.19%

- S&P CoreLogic CS 20-City YoY NSA, est. 3.8%, prior 4.18%

- 10am: Richmond Fed Manufact. Index, est. 10, prior 16

- 10am: Conf. Board Consumer Confidence, est. 132.5, prior 131.4

DB’s Jim Reid concludes the overnight wrap

We’re back to Brexit being at the top of the agenda again after a brief interlude as the UK government lost another vote in the House of Commons last night (329-302), with three ministers breaking ranks and resigning to support the amendment. MPs supported the measure put forward by the Conservative backbencher, Sir Oliver Letwin, which allows MPs to take control of the parliamentary timetable away from the government tomorrow, thus allowing Parliament to hold a series of ‘indicative votes, where MPs could vote on a range of Brexit options. After the vote, the government released a statement criticizing the “dangerous, unpredictable precedent” set by the vote, but nevertheless pledged to work with parliament to achieve a reasonable outcome. The statement called for “realism” moving forward and, in her comments to parliament, May referenced a second referendum or an election as potential options. Uncertainty looks set to continue. Sterling is trading weak (-0.08%) this morning.

Oliver Harvey published a helpful explainer overnight titled Brexit: indicative votes. What are they and can they be implemented? (click here ). The seven principal options that have been proposed would be: 1) May’s deal, 2) revocation of Article 50, 3) a second referendum, 4) May’s deal plus a customs union, 5) May’s deal, a customs union and membership in the single market, 6) a free trade agreement, or 7) no-deal Brexit. There is uncertainty as to how the votes could be structured and whether the government would even implement them. So Oli’s base case remains for a general election, but there are many possible permutations discussed in his note.

Mrs May earlier said that the government won’t implement parliamentary votes that contradict manifesto commitments which is pertinent as both the Conservative and Labour manifestos in 2017 committed to leaving the Customs Union and Single Market. So if she is true to her word this could again create fresh gridlock and increase the risk of fresh elections where new manifestos could be created. Nevertheless, May left open the possibility of a third meaningful vote in the coming days, saying that “I continue to have discussions with colleagues across the House to build support, so that we can bring the vote forward this week, and guarantee Brexit.”

Sterling weakened yesterday (-0.10% versus the dollar) but did rally a bit as Parliament took control. Meanwhile ten-year gilt yields (-2.8bps) closed below 1% for the first time in 18 months. When it comes to the curve, attention has focused on the US, but it’s worth noting that the UK’s 2s10s curve has flattened to its lowest level since September 2008, reaching 34.5bps yesterday.

US markets ended the session close to flat, with the S&P 500 and NASDAQ shedding -0.08% and -0.07%, respectively, and the DOW gaining +0.06%. That’s only the eighth day this year when the S&P and DOW moved in opposite directions. The yield curve gave a similarly unclear signal, as the 3m10y and the 3m (18 month forward) vs 3m flattened further into inverted territory, by -2.3bps and -9.4bps to -3.6bps and -35.3bps respectively, while the 2s10s actually steepened by 3.6bps to 15.5bps. That puts the main measure of the yield curve right back in the center of its year-to-date range of between 19.9bps and 11.8bps, with a year-to-date average of 16.0bps. The curve has steepened another basis point this morning with US 10yr and 2yrs up 4bps and 3bps respectively.

Yesterday’s steepening was driven by a big rally in two-year treasuries, where yields fell -6.3bps to their lowest level in almost a year at 2.2499%. The market is pricing in an ever more aggressive timeline of Fed rate cuts, with a full 25bps cut now priced by the end of this year, and a second cut priced by next August. Before last week’s Fed meeting, a cut was not fully priced until the end of 2020.

European equity markets lost further ground yesterday, with the Stoxx 600 (-0.45%) down for a fourth consecutive session. The declines were spread across the continent, with the FTSE 100 (-0.29%), CAC 40 (-0.10%) and the DAX (-0.11%) all closing lower. In sovereign bond markets, 10yr bund yields briefly got altitude sickness and climbed back above zero after a stronger IFO survey but fell again to close down by -1.2bps on the day to reach -0.028%. Peripheral yields went in the opposite direction though with ten-year yields in Italy (+5.3bps) Spain (+3.2bps) and Portugal (+3.4bps) all higher yesterday. The flight to safety also supported gold (+0.67%), which rose for a second consecutive session.

Asian markets are trading mixed this morning with the Nikkei (+2.09%) leading the advancers. The Hang Seng (+0.11%) and Kospi (+0.29%) are also up while the Shanghai Comp (-0.99%) is down. Elsewhere, futures on the S&P 500 are +0.34%. Oil prices are higher this morning (WTI +0.73% and Brent +0.19%) on rising tensions in Venezuela which threaten further curbs to supplies as the US warned Russia not to intervene in the Latin American nation. Separately, Samsung Electronics issued a warning today suggesting it would report disappointing financial results in 2019 due to slumping prices for chips and LCD screens, in another sign of slowing demand for smartphones and other gadgets. The stock is down -0.55% this morning after falling -2.26% yesterday.

In other news, the US House Democrats have now formally requested that Attorney General William Barr should hand over the Special Counsel Robert Mueller’s report to Congress by April 2. The Democratic chairs of six House committees said in a letter to Barr yesterday that the attorney general’s four-page summary of the Mueller report “is not sufficient for Congress, as a coequal branch of government,” to examine President Donald Trump’s conduct.

In data, the German Ifo business climate survey for March came in above expectations at 99.6 (vs. 98.5 consensus). The uptick from February’s revised 98.7 reading puts an end to six successive monthly declines, offering some indication that the German economy could be stabilising. Moreover, the expectations reading (95.6) and the current assessment reading (103.8), both rose from the previous month. However, some caution is warranted as the Ifo readings contradict the message from last Friday’s PMI readings, where the German manufacturing, services and composite readings all fell in March compared to February. The data certainly is conflicting at the moment. The euro appreciated slightly against the dollar after yesterday’s release but ended close to flat at +0.10%.

Other data of note yesterday included the Chicago Fed National Activity Index, which fell to -0.29 in February from an upwardly revised -0.25 in January. However, this was above expectations for a -0.38 reading. Meanwhile, the Dallas Fed Manufacturing Activity index fell back, coming in at 8.3 (vs an expected 8.9 and below last month’s 13.1), and the new orders index fell to 2.4, the lowest level in over two years.

We also had a number of central bank speakers yesterday. From the ECB, Executive Board member Coeure said that “I don’t think that we’ve been to the limit of what we can do” at a discussion in Lisbon. Elsewhere, Patrick Harker, the Philadelphia Fed President, said in a speech in London, that his “current view is that, at most, one rate hike this year, and one in 2020, is appropriate, and my stance will be guided by data as they come in and events as they unfold.” Regarding the US economic outlook, he said that “on balance, the potential risks tilt very slightly to the downside, but I emphasize the word ‘slight.’ I still see the outlook as positive, and the economy continues to grow in what is on pace to be the longest economic expansion in our history.” That’s broadly consistent with his prior comments and our economists have him penciled in as one of the four FOMC members who still expect a hike this year.

Turning to the day ahead, this morning we’ll get the GfK consumer confidence reading for Germany, while from France there’ll be the final GDP reading for Q4, along with March’s manufacturing and business confidence. In the US, there are quite a few releases, with a possible highlight being the Conference Board’s consumer confidence reading for March, along with the Richmond Fed’s manufacturing index. In addition, we’ll get February’s data for housing starts and building permits, along with the FHFA’s House Price Index for January. In terms of central bank speakers, we’ve got the Fed’s Harker, Evans and Daly all speaking today, along with the BoE’s Broadbent.

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 45.94 POINTS OR 1.51% //Hang Sang CLOSED UP 43.58 POINTS OR 0.15% /The Nikkei closed UP 451.28 POINTS OR 2.15%/ Australia’s all ordinaires CLOSED UP 0.07%

/Chinese yuan (ONSHORE) closed UP at 6.7129 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 59.53 dollars per barrel for WTI and 67.72 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7129 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7173 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA

4.EUROPEAN AFFAIRS

UK/LAST NIGHT

Mutiny on the Bounty

(zerohedge)

Pound Climbs As MPs Seize Control Of Brexit Debate

It appears a cross-party group of lawmakers who have been conspiring for weeks to wrest power away from Theresa May’s government has emerged victorious after a contentious Monday evening vote.

During the vote on the “Letwin Amendment” , hordes of Tory backbenchers joined with opposition MPs, and even some government ministers (one of whom, Minister for Business and Industry Richard Harrington, resigned from the cabinet to support the amendment) to defy the government whips and vote to assume control over the Commons agenda. The amendment, which had been put forth by Tory MP Sir Oliver Letwin, passed by a slim margin of 329 vs. 302.

Here’s the text.

LETWIN Amendment A: Seeks to change the rules of parliament on March 27 in order to provide time for lawmakers to debate and hold indicative votes. It has been signed by more than 120 lawmakers. The result of any such indicative votes would not be binding on the government but if it showed a majority for an alternative Brexit path. A similar amendment voted on earlier this month lost by two votes, this is therefore expected to have a good chance of passing.

The amendment calls for time to be set aside on Wednesday for a series of ‘indicative votes’ on alternatives to the withdrawal agreement that May negotiated with the EU. The options will range from a ‘soft’ Brexit that could cross certain of May’s ‘red lines’ (like remaining in the customs union and/or single market), to a second referendum, to “no Brexit at all”.

Harrington wrote a scathing resignation letter, blaming May for “playing roulette with lives and livelihoods of the vast majority of people in this country.”

Richard Harrington

✔@Richard4Watford

This evening I wrote to the PM to offer her my resignation

UK Minister Steve Brine, Undersecretary of State for Primary Care and Public Health, has also resigned. MPs also narrowly passed ‘Amendment F’ – the Beckett Amendment – which calls for Parliament to hold a vote on whether to leave with ‘no deal’ if the UK comes within 7 days of the deadline without a deal.

Ultimately, some 30 conservatives broke ranks to support the Letwin Amendment.

Steven Swinford

✔@Steven_Swinford

It’s worth noting that TWICE as many Tory MPs backed the Letwin amendment tonight compared to the Benn amendment last week

The 15 new rebels are:

Brine

Burt

Collins

Costa

Green

Harrington

Jo Johnson

Lefroy

Masterton

Mitchell

Morgan

Neill

Newton

Pawsey

Spelman

The pound strengthened on the vote, which upped the odds of a ‘softer’ Brexit, or – like we said above – no Brexit.

Pound Rallies As Brexiteer Leader Tentatively Backs May’s Deal

Now that the House of Commons has gone full Lord of the Flies and seized control of Brexit from No. 10, Brexiteers like ERG leader Jacon Rees-Mogg and former Conservative Party leader Iain Duncan Smith have apparently realized that Theresa May wasn’t kidding when she said it’s either “this deal, no deal or ‘no Brexit'”.

After more than 30 Tories rebelled against the government last night to help pass the Letwin Amendment, guaranteeing that a series of ‘indicative votes’ on alternatives to May’s deal (including a lengthy Brexit delay and the possibility of holding another referendum) will be held on Wednesday, rumblings that the ERG and DUP might finally relent and back May’s deal have apparently been confirmed by Rees-Mogg himself.

During Tuesday’s episode of his podcast “The Moggcast”, JRM said he’d be willing to back May’s deal, because leaving under the conditions imposed by the withdrawal agreement would be preferable to “never leaving at all” – though “no deal” would still be preferable to May’s deal.

Jacob Rees-Mogg

✔@Jacob_Rees_Mogg

The choice seems to be Mrs May’s deal or no Brexit.https://www.conservativehome.com/highlights/2019/03/the-moggcast-deal-or-no-brexit-becomes-the-choice-eventually-mays-deal-is-better-than-not-leaving-at-all.html …

The Moggcast. Deal-or-No-Brexit “becomes the choice eventually…May’s deal is better than not…

Rees-Mogg details how the deal is “definitely not” worse than Remain. And: precisely why the Letwin plan is constitutionally “absurd”.

conservativehome.com

The pound rallied as traders once again hoped that a ‘no deal’ Brexit might finally be averted.

If more Brexiteers join with JRM and Dunan-Smith, the pound could see even more upside. But the real test will be winning over the intransigent DUP – the 10 unionist MPs from Northern Ireland who have proved to be the biggest thorn in May’s side during the nearly three years since the Brexit referendum. Then again, given the number of Tory rebels who have already crossed May, even finally winning over the Brexiteers might not be enough for May to pass the withdrawal agreement.

END

An excellent commentary from our resident expert on BREXIT and how the EU will do everything in their power to milk as much tax dollars out of Britain.

The whole EU project will fail.

(courtesy Tom Luongo)

Luongo: Liberalism’s Last Stand – Brexit

When the Soviet Union fell in 1991 Marxism was dealt a near fatal blow. The crown jewel of communism was no more and descended into the worst kind of lawlessness.

Francis Fukiyama famously declared the End of History and the U.S. went on a ‘to the victors go the spoils’ looting of 1990’s Russia that boggles the imagination.

Marxists were left floundering. They were convinced the end of capitalism would occur and communism would win. Their identity was shattered on the shores of collectivism’s inherent inconsistencies.

It’s lack of basic understanding of why man acts and what he hopes to achieve when he acts that dooms all forms of collectivism to eventual failure.

The cries went up among the committed Marxists to then blame the U.S.S.R. that it wasn’t real communism. And their argument shifted to European Democratic Socialism as the superior implementation.

For the past twenty-eight years we’ve been inundated with this by leftists who refuse to give up on the dream. It’s still just warmed-over Marxism but whatever.

The End Of OPM

Now with the European Union facing a populist uprising across the continent they have reached the turning point with Brexit. And the conundrum is enormous.

Brexit is the single most important political event of this century. It’s one of the few things that is bigger than Trump. So, paying close attention to it is important.

That’s why it has so divided people. It represents an existential threat to the inevitability of modern liberalism. The European Union is the symbol of that inevitability.

Because once that inevitability is breached the European Union will begin to unravel before our eyes.

Donald Trump, for his part, understands this. He is pressing the EU on the issue of tariffs and NATO spending.

He wants to break down the artificial financial support the EU receives to fund its ‘superior democratic socialism’ that U.S. liberals of the Bernie Sanders persuasion believe in.

Famously, former British Prime Minister Margaret Thatcher said, “The problem with socialism is that eventually you run out of other people’s money.”

That’s why Brexit has to be destroyed. Because if it happens and Britain thrives as a result, it will deal a fatal blow to Marxism.

This is why they fear Brexit so much. The EU will fail.

We got a microcosm of that on Thursday when Theresa May left a No-Deal option on the table. The EU Council turned a one-hour rubber stamp session into a five hour grudge match. which resulted in the EU caving at the last moment, offering an unconditional two-week extension to Article 50.

And the EU caved. Finally.

Tax Cows Unite

That’s why the Brits have to be made into voiceless tax-cows milked until they are depleted. That’s what socialism is, a giant tax vacuum which destroys capital and innovation.

And that is where the EU is today. They have run out of the British people’s willingness to fund their dreams of creating a better version of the U.S.S.R.

So is Italy. So is Poland, the Giles Jaunes in France, Hungary, Austria, Spain, the Czech Republic, and even Germany itself.

In the U.S., Trump refuses to pay for Europe’s externalities like defense, education and medical care. He’s attacking the fundamental argument made for socialism today.

It’s a cornerstone of his re-election strategy.

The Marxism of places like Norway, Denmark and the post WWII Great Britain were heavily subsidized not just by the U.S. via NATO and the Marshall Plan but also the massive oil and gas deposits they had relative to the size of the populations they were supporting.

But with the North Sea and Groningen fields drying up so is the revenue. And it’s placing immense strains on the promises of these democratic socialist governments.

Trump understands this. It’s why he’s activated the U.S.’s energy production the way he has. And he’s saying quite clearly to Europe, “No more will we fund your wealth transfers by paying import tariffs to protect inefficient industries and subsidize Germany’s car industry.”

I’ve given Trump a lot of grief in the past two years over tariffs because the economics are clear. Tariffs hurt domestic consumers at the expense of politically-connected domestic producers.

But I have always understood his reasoning for attacking the EU the way he has. I agree with the sentiment just not the implementation.

The End of Empires

Back to Brexit. If the EU wins its fight with the U.K. over this treaty it will be a short-term reprieve for Marxism. They will win a six to nine month grace period.

So, as I said recently on Strategic Culture:

Merkel and Juncker are trying to hold onto their manufactured leverage over the Brits to, in turn, hold onto a Union that is in the process of failing. May and her cabinet are trying to hold onto a relationship with the EU while the UK itself is now in danger of failing.

The Scots are pushing for independence to stay in the EU. Wales is beginning to consider it. Northern Ireland doesn’t like being anyone’s Trojan Horse.

They have thoroughly underestimated the will of the people and it will cost them what little cache they have left with voters. Remember, confidence lost in the institutions of government begets a loss of confidence in the money and their ability to manage it.

Because the global economy is rolling over. The data is everywhere.

The biggest proof is the central banks capitulating. Normalcy will not return to sovereign debt pricing.

The U.S. Yield Curve is a nightmare of convexity that is screaming, “Recession! Dead Ahead!”

Everyone fiddles while their empires burn, including the central banks.

The U.S. yield curve is inverted between 3 months and 10 years. The markets are braced for a severe dollar liquidity crunch. To me it means they know Brexit is irrelevant at this point.

Brexit isn’t the problem. It is the symptom of the far larger one that you can’t steal your way to infinite prosperity.

And that’s why it is inevitable.

end

Ransquawk outlines what comes next after Parliament has seized control of the Brexit procedures:

(courtesy Ransquawk)

Now That Parliament Has Seized Control Of Brexit, Here’s What Happens Next

Submitted via Ransquawk

LAST NIGHT’S VOTE: The government was defeated by a majority of 27 (329 vs. 302) on the Letwin amendment which seeks to change the rules of parliament on March 27 in order to provide time for lawmakers to debate and hold indicative votes. It is worth noting that three junior ministers resigned in order to vote in favour of the Letwin amendment. Furthermore, MPs voted (311 vs. 314) against the Beckett amendment (F) which called on the government to seek parliament approval on a no-deal if an agreement is not reached 1 week before the Brexit date, while the Labour amendment (D) to provide parliamentary time for lawmakers to find a majority for a different approach on Brexit was not moved. Following last night’s developments, Goldman Sachs analysts maintained their Brexit probabilities (PM May deal ratification 50%, no-deal Brexit 15% and no Brexit 35%) whilst stating that they are skeptical that this week’s votes will prove conclusive.

TODAY’S SCHEDULE (GMT):

Morning – Emergency Cabinet meeting

- 18:00 – ERG meeting

WHAT’S NEXT: In light of the Letwin amendment passing, on Wednesday 27th March, MPs will vote on a series of options to establish what could command a majority in parliament. The result of any such indicative votes would not be binding on the government as it goes against the Tory manifesto. There is no official list of options, although one has been generated by the Commons select committee for exiting the EU.

1. PM MAY’S DEAL: The deal has been rejected twice already by parliament but remains the only deal the EU can quickly ratify and therefore remains an option. If voted on, it will attract support from May loyalists, but DUP and ERG remain opposed.

2. NO DEAL BREXIT: This would lead to the UK leaving the EU on the new revised date of April 12th on WTO terms. HoC have twice voted against this option, albeit by only four votes last time.

3. ELIMINATING A BACKSTOP: This, in theory would mean re-writing the Withdrawal Agreement, something the EU repeatedly dismissed. A variant would be to promote “alternative arrangements” i.e., technology to monitor the flow of good that could replace the backstop. The EU have previously agreed to examine this, although implementation could take years.

4. CANADA-STYLE DEAL: A popular idea with hardcore Brexiteers, this would focus on the future trade deal with the EU rather than the Withdrawal Agreement. In theory, the UK would accept no continuing regulatory alignment with the EU, although is unclear how far the EU is willing to negotiate this. However, this would not solve the impasse regarding the Northern Irish border, nor has there been signs of many Labour are willing to support this.

5. NORWAY-PLUS DEAL: This soft-Brexit alternative would keep the UK in the single market by remaining in the European Economic Area (EEA) and European Free Trade Association (EFTA). Unlike EFTA, the deal would also keep the UK in the customs union (hence the plus). The deal has been promoted by a group of Tory backbenchers, Labour leader Corbyn has also shown some interest and some believe it would be the most popular option given a free vote. The Sun reported last night that over 100 are ready to back this deal after PM May’s deal is killed off.

6. LABOUR DEAL: This would mean the UK remains in a customs union with the EU and remain close to the single market. European Council President Tusk has previously deemed this as “promising”, although the plan was rejected by parliament. The Labour deal is unlikely to attract support of the Conservatives.

7. SECOND REFERENDUM: A replay of the 2016 referendum would be a separate option although nobody in parliament is seriously calling for that. However, a referendum could be attached to one of the options above. When a second referendum was put on PM May’s deal before the HoC this month, only 85 MPs voted for it after labour ordered its MPs to abstain.

In Latest Blow To Washington, EU Refuses To Recommend Bloc-Wide Huawei Ban

The Trump Administration probably didn’t need any more convincing that the longstanding post-war economic and military alliance between the US and Europe now exists solely on paper. But it got it all the same.

Just days after Beijing officially annexed Italy to the BRI, and with Brussels still deliberating what can be done to put Europe back on an even economic footing with China, the bloc has decidedly rejected Washington’s efforts to muscle Huawei out of the global 5G market. First, individual EU capitals unanimously rejected Washington’s warnings that Huawei posed an intractable national security, and refused to disallow the company’s telecoms equipment from being used in domestic 5G networks.

And on Tuesday, the European Commission tacitly embraced Huawei by refusing to recommend that member states exclude the company, a recommendation made in a set of security guidelines, Reuters reports.

EU member states will be required to share information about cybersecurity risks related to 5G, and even develop a plan to tackle them before the end of the year. But for all of Washington’s lobbying, the Commission has refused to specifically target Huawei.

According to ABC News, EU countries will have until the end of June to study 5G cybersecurity risks. Their findings will be incorporated into a bloc-wide assessment before Oct. 1. Using this assessment, the EU would need to agree on a plan to mitigate these risks by the end of the year. Experts said some measures could include certification requirements and tests of products or suppliers deemed security risks.

EU Digital Commissioner Andrus Ansip said this plan would help ensure that Europe’s 5G infrastructure would be “resilient” to attack.