GOLD: $1311.25 DOWN $4.05 (COMEX TO COMEX CLOSING)

Silver: $15.31 DOWN 12 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1309.70

silver: $15.27

I am sorry that I made a little error these past few days. Comex expiry was yesterday and the LBMA and OTC options expire on March 29.2019. That sets up a nightmare for the banks as Basel III also begins on March 29.

I am assure you that there is going to plenty of gold oz standing for the upcoming April contract month.

London/LBMA expires Friday March 29/2019.

The crooks continue with their whacking right in front of the authorities/regulators despite the criminal probe of precious metals manipulations.

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 1 NOTICE(S) FOR 100 OZ (0.00311 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 396 NOTICES FOR 39600 OZ (1.23176 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

40 NOTICE(S) FILED TODAY FOR 200,000 OZ/

total number of notices filed so far this month: 5424 for 27,120,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4017:UP $68

Bitcoin: FINAL EVENING TRADE: $4019 UP 77

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 1/1

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,314.300000000 USD

INTENT DATE: 03/26/2019 DELIVERY DATE: 03/28/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 1

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 1 1

MONTH TO DATE: 396

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FOR THE FIRST TIME IN 7 TRADING SESSIONS LOWERS ITS OPEN INTEREST : THIS TIME BY A SMALL SIZED 440 CONTRACTS FROM 193,116 UP TO 192,676 WITH YESTERDAY’S 13 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 1017 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1017 CONTRACTS. WITH THE TRANSFER OF 1017 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1017 EFP CONTRACTS TRANSLATES INTO 5.065 MILLION OZ ACCOMPANYING:

1.THE 13 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 27.120 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

34,044 CONTRACTS (FOR 19 TRADING DAYS TOTAL 34,044 CONTRACTS) OR 170.220 MILLION OZ: (AVERAGE PER DAY: 1891 CONTRACTS OR 9.456 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 170.220 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 24.28% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 535.52 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 440 WITH THE 13 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1017 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY SMALL SIZED: 577 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1017 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 440 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 13 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.43 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.978 BILLION OZ TO BE EXACT or 138% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 40 NOTICE(S) FOR 200,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 27.120 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A HUMONGOUS 15,290 CONTRACTS, TO 509,575 WITH THE FALL IN THE COMEX GOLD PRICE/(A DROP IN PRICE OF $7.30//YESTERDAY’S TRADING). YESTERDAY I COMMENTED ON MONDAY’S OI READINGS: “NO EVIDENCE OF ANY SPREADING LIQUIDATION IN GOLD AS WE ARE NOW APPROACHING FIRST DAY NOTICE IN AN ACTIVE DELIVERY MONTH.” I THINK WE JUST HAD OUR INITIAL HUGE FALL IN OPEN INTEREST DUE TO THE LIQUIDATION OF THE SPREADERS.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9682 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 8760 CONTRACTS,JUNE: 922 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 509,575. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5608 CONTRACTS: 15,290 OI CONTRACTS DECREASED AT THE COMEX AND 9682 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 5608 CONTRACTS OR 560,800 OR 17.44 TONNES.

YESTERDAY WE HAD A FALL IN THE PRICE OF GOLD TO THE TUNE OF $7.30....AND WITH THAT, WE HAD A CONSIDERABLE LOSS IN TONNAGE OF 17.44 TONNES!!!!!!. (HOWEVER ALL OF THE COMEX LOSS IS PROBABLY DUE TO THE LIQUIDATION OF THE SPREADERS)

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 134,498 CONTRACTS OR 13,449,800 OR 418.34 TONNES (19 TRADING DAYS AND THUS AVERAGING: 7078 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAYS IN TONNES: 3418.34 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 418.34/2550 x 100% TONNES = 16.40% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1287.30 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX OF 10,924 WITH THE LOSS IN PRICING ($7.30) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9682 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9682 EFP CONTRACTS ISSUED, WE HAD A VERY SMALL LOSS OF 1242 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9682 CONTRACTS MOVE TO LONDON AND 15,290 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 17.44 TONNES). ..AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A FALL IN PRICE OF $7.30 IN YESTERDAY’S TRADING AT THE COMEX!!!!! HOWEVER THERE IS STRONG EVIDENCE THAT AGAIN WE HAVE LIQUIDATION OF SPREADERS AS WE HEAD INTO AN ACTIVE DELIVERY MONTH.

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.05 TODAY

VERY STRANGE!! A BIG CHANGE IN GOLD INVENTORY

A DEPOSIT OF 3.23 TONNES

INVENTORY RESTS AT 784.26 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 12 CENTS IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV TODAY

/INVENTORY RESTS AT 309.488 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 440 CONTRACTS from 193,116 UPTO 192,676 AND FURTHER FORM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 1017 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1017 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 440 CONTRACTS TO THE 1017 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 577 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 2.885 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 27.120 MILLION OZ FOR MARCH.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 13 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A STRONG SIZED 1017 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 25.62 POINTS OR 0.85% //Hang Sang CLOSED UP 161.34 POINTS OR 0.56% /The Nikkei closed DOWN 49.66 POINTS OR 0.23%/ Australia’s all ordinaires CLOSED UP 0.07%

/Chinese yuan (ONSHORE) closed DOWN at 6.7241 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 59.53 dollars per barrel for WTI and 67.72 for Brent. Stocks in Europe OPENED RED

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7241 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.73127 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

i)UK/ LAST NIGHT

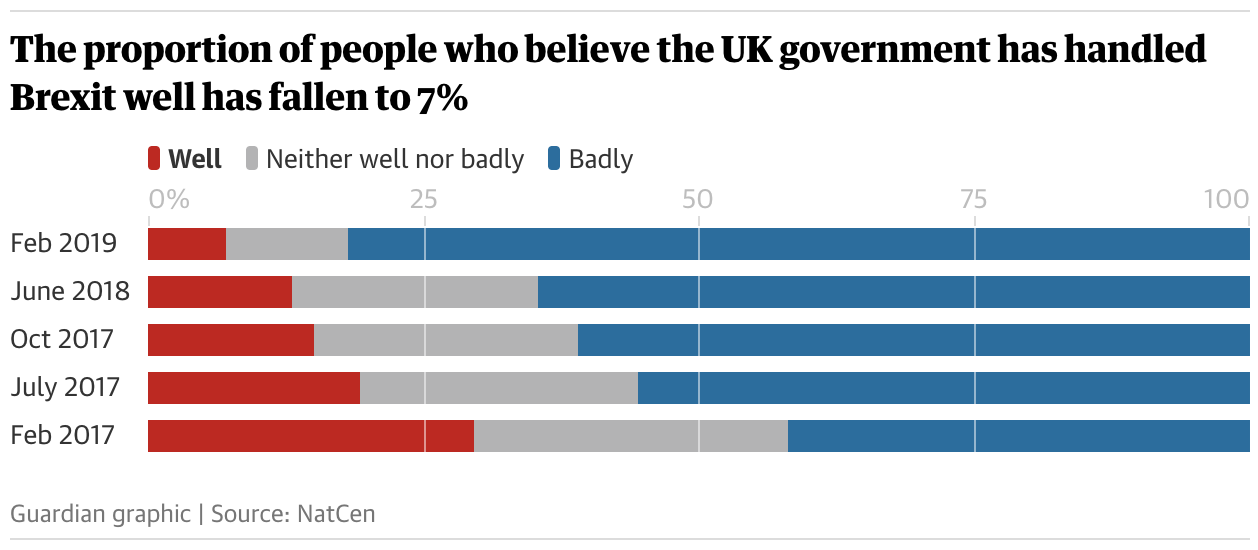

This is not good: only 7% of all Britons support Theresa May’s handling of Brexit.

(courtesy zerohedge)

ii)ECB

As you know Europe has negative rates. Now the ECB is contemplating stopping the payment by banks with respect to excess reserves. Japan is doing this but it has had little effect on helping the banks return to profitability

a real mess..

( zerohedge)

iii)Germany

IV)THIS MORNING/GERMANY

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Turkey

Erdogan realizes his countries economy is in a mess as he needs outside funding namely in dollars. However the central bank bought out just about all liquidity which caused overnight swaps to hit 700%..totally unheard of… Turkey, in order to survive must need dollars and by causing overnight swaps to rise, the opposite occurs..funding disappears. Credit default swaps skyrocketed to 478% last night.

LATE IN THE DAY: SWAPS HIT 1000%/IT SURE LOOKS LIKE TURKEY MAY FAIL

( zerohedge)

Israel strikes the GAZA strip again last night despite reports of a cease fire

(courtesy zerohedge)

6. GLOBAL ISSUES

Canada

Canada might stop Trump’s NAFTA deal if he does not stop steel and aluminum tariffs

( Mish Shedlock/Mishtalk)

Swedbank is one of the oldest banks in Sweden founded in 1820. These guys are now next in line in the money laundering business and this scandal is huge and may implicate Manafort. Their offices were raided early this morning.

( zerohedge)

7. OIL ISSUES

Venezuela is the the USA sphere of influence. However both China and Russia lent money to Venezuela and now Russian troops are on the ground in Venezuela as Putin wants his money back

(courtesy zerohedge)

8 EMERGING MARKET ISSUES

Venezuela/Russia/USA

Venezuela is the the USA sphere of influence. However both China and Russia lent money to Venezuela and now Russian troops are on the ground in Venezuela as Putin wants his money back

(courtesy zerohedge)

9. PHYSICAL MARKETS

i)Craig Hemke writes on the short squeeze on Palladium

( Craig Hemke/Sprott/GATA)

ii)Economist Todd Stein of Fox Business claims that a “soft” default i.e. a huge devaluation of the dollar will not be as catastrophic as a hard default i.e. not paying off its bills. I beg to differ

( Todd Stein/Fox News)

iii)Peter Grandich is back reporting on gold. He comments that gold will overcome the price suppression engineered by governments and central banks. He expects them to restore gold to its rightful place in the financial system

( Peter Grandich/GATA)

v )I liked Jim Willie’s latest piece as he zeros in on the fraud at GLD, exactly how I described to you what is happening in this crooked arena.(courtesy Jim Willie)

a must read

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

ii)Market data

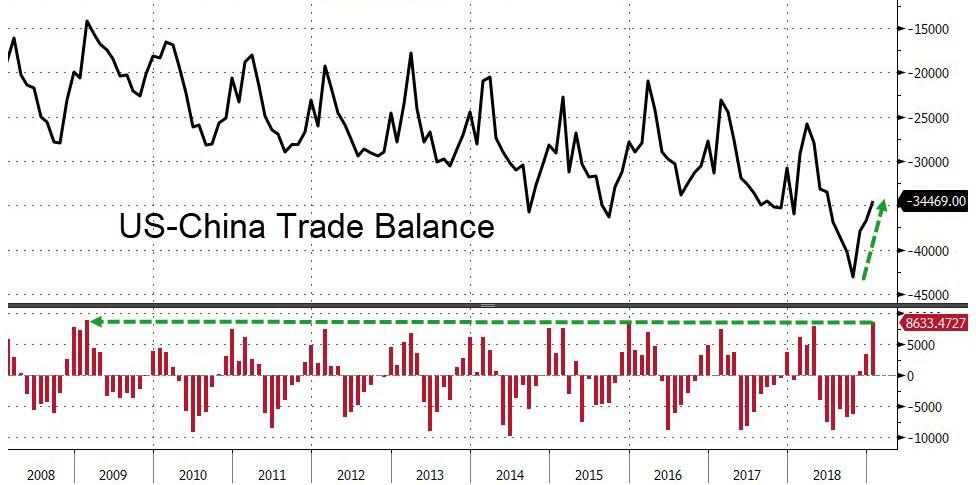

a)Trump will be pleased with this as the USA trade deficit shrank to 51.1 billion dollars form 60 billion dollars. However they still have a long way to go

( zerohedge)

b)I promised you that Stephen Moore was going to be a handful for the Fed officials. He is calling for a 50 basis point cut in the Federal funds rate. This is why bond yields have been plummeting across the globe today

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

a)Look what happens if you have a cell tower next to your home. I can vouch for cancer problems with this. We had a hydro electric plant next to our house and many children developed cancer. They tried to tell us that it was the hydro electric plant but we knew otherwise.

( zerohedge)

iv)SWAMP STORIES

a)The Mueller report will be released in weeks and not months. The White House may receive an advanced copy of the full report in case they wish to place executive privilege of some of the stuff

( zerohedge)

end

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL LOWERS TO 767 CONTRACTS FOR A LOSS OF 7 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI FELL BY 2276 CONTRACTS DOWN TO 133,984 CONTRACTS.

Gold Gains On Recession Concerns and ‘No Deal’ Brexit Risks

– Gold gains due to concerns about slowing growth, monetary and geopolitical risks

– Increasing possibility of ‘No Deal’ Brexit heightens recession risks in UK, Ireland

– Brexit uncertainty is impacting UK & Irish economies; Likely do long term damage

– UK sees sharp slowdown in mortgage approvals in February as housing market slows

– Gold surges to near all time record highs in Australian dollars at $1,860/oz

– Gold in sterling, euros and dollars to follow Aussie dollar in coming months

Gold in GBP (1 Year)

Gold rose to 4 week highs overnight prior to profit taking saw the yellow metal give up some of those gains. Gold marched higher yesterday, extending it’s recent rally due to growing, if belated, concerns over slowing economic growth and the Federal Reserve’s move to looser monetary policies again.

Gold rose 0.8% yesterday to $1,323.40 per ounce which was it’s highest level in a month. Investors have diversified into safe haven gold following news the Fed expects to suspend interest rate rises in 2019. This was something we wrote and spoke about (podcast and video interviews) as inevitable given the fragile nature of the economic recovery.

Even greater uncertainty around Brexit, just three days before Britain’s scheduled departure from the EU on March 29th may impact sterling and markets and should support gold, especially in sterling which has risen to the £1,000/oz level again.

The UK saw a sharp slowdown in mortgage approvals in February which suggests heightened Brexit uncertainties is taking its toll on the UK housing market. UK banks approved the fewest mortgages in six years as Brexit nears and unsecured consumer credit growth also slowed.

The FTSE 100 joined European stock market counterparts in heading lower yesterday as Brexit worries permeate through European markets.

There will be a very negative impact on Ireland’s economy in the long-term as a result of Brexit, a new report by the Irish ESRI and Department of Finance has concluded. The European Commission (EC) said yesterday that it has completed preparations for a no-deal Brexit, noting “it is increasingly likely that the United Kingdom will leave the European Union without a deal on 12 April”.

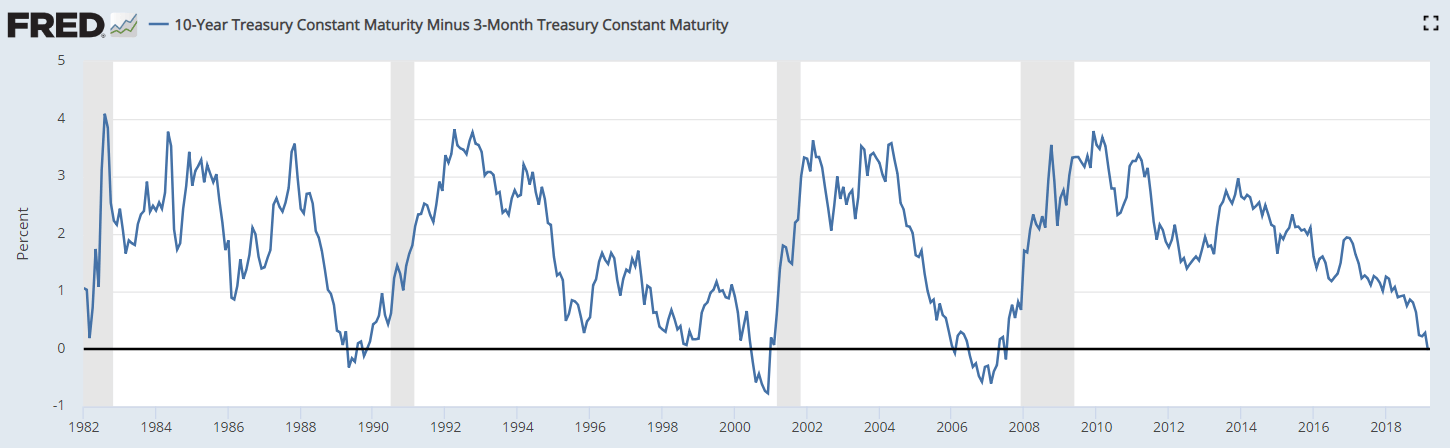

Along with gold, certain government bonds have gained, pushing yields to their lowest level in more than a year, while one yield curve measure has inverted for the first time since August 2007. The inversion of the yield curve for three-month and 10-year Treasuries has righted led to recession worries in the market and led to sell offs in stock markets in recent days.

Markets were already attempting to come to grips with weaker economic data of late including poor global manufacturing data and US consumer spending.

Spot gold was up about 1 per cent last week, notching a third consecutive week of gains. Gold has gained nearly 13 per cent since it’s most recent sell off in August.

News and Commentary

Gold has highest finish in a month as global market jitters persist (MarketWatch.com)

Gold hits 3-week high as global growth fears lift safe-haven appeal (Reuters.com)

Asian shares shaky as U.S. bond yields hit lowest since late 2017 (Reuters.com)

U.S. Treasury yields hit lowest since late 2017, global stocks fall (Reuters.com)

Fed should consider holding more short-term bonds: Rosengren (Reuters.com)

Source: St Louis Fed

A genuinely scary moment for markets (MoneyWeek.com)

The Staggering Amount Of Gold & Silver Investment Since The 2008 Financial Crisis (Twitter.com)

What an Inverted Yield Curve means to the market (Youtube.com)

Over $10 Trillion In Debt Now Has A Negative Yield (ZeroHedge.com)

The Gold Trade Note Has Been Introduced, The [CB] Is On The Chopping Block:Jim Willie (Youtube.com)

Marc Faber – Huge Asset Bubble Will Be Deflated (Youtube.com)

20 Days Left to Find Buying Opportunities in Gold (TheTechnicalTraders.com)

Gold Prices (LBMA PM)

25 Mar: USD 1,319.35, GBP 1001.39 & EUR 1,165.82 per ounce

22 Mar: USD 1,311.10, GBP 998.80 & EUR 1,159.41 per ounce

21 Mar: USD 1,317.30, GBP 1002.99 & EUR 1,155.80 per ounce

20 Mar: USD 1,303.00, GBP 985.07 & EUR 1,147.81 per ounce

19 Mar: USD 1,308.35, GBP 985.06 & EUR 1,152.53 per ounce

18 Mar: USD 1,305.35, GBP 986.19 & EUR 1,150.01 per ounce

Silver Prices (LBMA)

25 Mar: USD 15.52, GBP 11.77 & EUR 13.72 per ounce

22 Mar: USD 15.46, GBP 11.75 & EUR 13.68 per ounce

21 Mar: USD 15.54, GBP 11.85 & EUR 13.64 per ounce

20 Mar: USD 15.32, GBP 11.58 & EUR 13.49 per ounce

19 Mar: USD 15.41, GBP 11.61 & EUR 13.57 per ounce

18 Mar: USD 15.38, GBP 11.60 & EUR 13.54 per ounce

Recent Market Updates

– America’s “Debt Crisis Is Coming Soon”

– Russia Buys 1 Million Ounces Of Gold In February – Become Your Own Central Bank

– 5 Ways to Prosper In the Coming Crisis – Goldnomics Podcast

– Deutsche Bank and Commerzbank May Become EU’s “Too Big To Fail” Bank

– Happy Saint Patrick’s Day from GoldCore

– 188 Internet Shutdowns In 2018 Show Why Physical Gold Is Ultimate Protection

– Buy Gold as Basel III Means “Central Banks and Banks Are Going To Be Buying Gold”

– Invest In Gold Or Bitcoin – Which Is The True Store Of Value?

– Silver Bullion Is The Portfolio Insurance To Buy Now

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Craig Hemke writes on the short squeeze on Palladium

(courtesy Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: An inflection point for palladium?

Submitted by cpowell on Wed, 2019-03-27 03:46. Section: Daily Dispatches

11:48a SST Wednesday, March 27, 2019

Dear Friend of GATA and Gold:

The short squeeze in palladium is showing signs of moderating, the TF Metals Report’s Craig Hemke writes this week at Sprott Money, while adding that the metal’s upward price trajectory remains intact. It is still an open question, Hemke writes, whether the commodity market-rigging banks will regain control of the market or whether an explosion in palladium will impugn their rigging in the monetary metals markets. Hemke’s analysis is headlined “An Inflection Point for Palladium?” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/an-inflection-point-for-palladium-craig…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Economist Todd Stein of Fox Business claims that a “soft” default i.e. a huge devaluation of the dollar will not be as catastrophic as a hard default i.e. not paying off its bills. I beg to differ

(courtesy Todd Stein/Fox News)

Todd J. Stein: U.S. should do a ‘soft’ default on its debt by devaluing dollar

Submitted by cpowell on Wed, 2019-03-27 04:07. Section: Daily Dispatches

By Todd J. Stein

FOX Business, New York

Tuesday, March 19, 2019

Last month, the national debt Opens a New Window. surpassed $22 trillion — or nearly $180,000 per taxpayer. That figure will roughly double within three decades, since spending on Social Security, Medicare, and Medicaid will balloon as America’s population ages.

Such stratospheric debt levels will be completely untenable — it’d be like saddling every taxpayer with an additional mortgage on top of his or her existing housing, credit card, and student loans. Most tax revenue would go toward interest on the debt, leaving little for safety-net programs, the military, or core government functions. By 2050 the federal government will spend more on interest payments than Social Security, health care, or national defense. …

Our leaders have dug us into a hole. And the best way out is a “soft” default on the national debt.

A hard default, where the government simply refuses to pay its debts, would cause a global economic meltdown. Dollar-denominated Treasuries and federal reserve notes are the lifeblood of the global financial system.

But a soft default — a one-time devaluation of the dollar that enables the government to pay back its debts in full, albeit at a lower intrinsic value — needn’t be catastrophic.

Here’s how a soft default would work. …

… For the remainder of the commentary:

https://www.foxbusiness.com/economy/the-federal-government-should-defaul…

end

Peter Grandich is back reporting on gold. He comments that gold will overcome the price suppression engineered by governments and central banks. He expects them to restore gold to its rightful place in the financial system

(courtesy Peter Grandich/GATA)

Peter Grandich: Why gold is set to shine again

Submitted by cpowell on Wed, 2019-03-27 05:46. Section: Daily Dispatches

1:47p SST Wednesday, March 27, 2019

Dear Friend of GATA and Gold:

It’s good to hear GATA’s old friend, former market analyst and financial letter writer Peter Grandich, commenting again on gold’s prospects in a podcast on his internet site. Grandich sees a number of factors helping the monetary metal gradually to overcome the price suppression engineered by certain governments and central banks. He also expects other governments and central banks to restore gold formally to the world financial system. Grandich’s comments are headlined “Gold Set to Shine,” are 10 minutes long, and can be heard here:

http://petergrandich.com/2019/03/25/grandich-podcast-gold-set-to-shine/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Whistleblowers awarded $50 million by SEC in JPMorgan Case

Submitted by cpowell on Wed, 2019-03-27 05:56. Section: Daily Dispatches

By Matt Robinson and Neil Weinberg

Bloomberg News

Tuesday, March 26, 2019

The U.S. Securities and Exchange Commission agreed to pay a total of $50 million to a pair of whistleblowers who provided information that helped the agency win a $267 million settlement with JPMorgan Chase & Co. over claims that the bank failed to inform wealthy clients of conflicts of interest in managing their money.

One of the informants will get $37 million, the third-biggest payout in the history of the SEC’s whistleblower program, the agency said in a statement today. The SEC didn’t name the company involved or the people getting the awards, citing federal law that protects confidentiality.

Labaton Sucharow, a law firm that represents one of the whistleblowers, disclosed the link to the JPMorgan case after the SEC’s announcement.

“Blowing the whistle is rarely easy, and it certainly hasn’t been for my client, but this historic SEC whistleblower award and related enforcement action reaffirm that doing the right thing pays,” Jordan Thomas, the whistleblower lawyer, said in a statement. Thomas said his client is a JPMorgan executive. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-03-26/two-whistleblowers-aw…

And here is the Bloomberg story in full:

Two Whistleblowers Awarded $50 Million In “Massive Enforcement Action” Against JPMorgan

The SEC today announced awards totaling $50 million to “two whistleblowers whose high-quality information assisted the agency in bringing a successful enforcement action.” The whistleblowers provided information that helped the agency win a $267 million settlement with JPMorgan over claims that the bank failed to inform wealthy clients of conflicts of interest in managing their money.

One of the whistleblowers will receive $13 million for reporting a tip to the SEC that led to a massive enforcement action charging J.P. Morgan. The second informant will receive $37 million, the third-biggest payout in the history of the SEC’s whistleblower program, the agency said in a statement. The SEC didn’t name the company involved or the people getting the awards, citing federal law that protects confidentiality.

Jordan A. Thomas, chair of Labaton Sucharow’s Whistleblower Representation Practice, served as counsel to the whistleblower, a J.P. Morgan executive, who cooperated in the agency’s investigation. The case, in which JPM agreed to pay $267 million to settle the charges in December 2015, is one of the largest enforcement actions initiated by an SEC whistleblower since the SEC Whistleblower Program was enacted.

“Blowing the whistle is rarely easy, and it certainly hasn’t been for my client, but this historic SEC whistleblower award and related enforcement action reaffirms that doing the right thing pays,” said Mr. Thomas, himself pocketing several million of the SEC award. “Thanks to the SEC Whistleblower Program, today corporate whistleblowers know that the Commission has their back and blowing the whistle anonymously dramatically increases the probability of a happy ending”… certainly one for the law firm which will likely keep about a third of the gross proceeds for filing some paperwork and sending out a few Fedexes.

In December 2015, JPMorgan agreed to pay more than $300 million to the SEC and to the CFTC when it admitted disclosure failures from 2008 to 2013 related to two units that manage money – its securities subsidiary and its nationally chartered bank – as part of the SEC settlement.

“Whistleblowers like those being awarded today may be the source of ‘smoking gun’ evidence and indispensable assistance that strengthens the agency’s ability to protect investors and the capital markets,” Jane Norberg, chief of the SEC’s whistleblower office, said in the agency’s statement.

As Bloomberg reminds us, tipsters are eligible for payouts if they voluntarily provide the SEC with unique information that leads to a successful enforcement action. Compensation can range from 10 to 30% of the money collected in a case where sanctions exceed $1 million. While the SEC has paid out about $376 million since issuing its first award in 2012, today’s award was the agency’s first since September.

end

I liked Jim Willie’s latest piece as he zeros in on the fraud at GLD, exactly how I described to you what is happening in this crooked arena.

(courtesy Jim Willie)

a must read….

GLD Fund: Divergence Signals Shortage

By: Jim Willie CB, GoldenJackass.com

— Published: Wednesday, 27 March 2019

A Perfect Storm is hitting the Gold market, with an internal factor (QE), an external factor (SGE), and a systemic factor (Basel). All three forces are positive in releasing Gold from the corrupt clutches of the Anglo- American banker organization. The West has an all-out blitz to ditch the USDollar and to adopt the Gold Standard in its early form, namely trade payment. In the last ten years since the Lehman Brothers failure, all systems have undergone the same reckless treatment that the mortgage bonds endured. Slowly the realization is coming to the fore, stated by a few astute analysts. In the last decade, the US-UK banksters have created the USTreasury bond as the global subprime bond. This is the result of astounding persistent magnificent QE abuse, debt explosion, and hidden corruption. The so-called financial stimulus is actually hyper monetary inflation, which has destroyed the bond market. There are no legitimate USTreasury buyers outside the US foreign vassal states.

PERFECT FINANCIAL STORM

The perfect financial storm will be three to five times worse than the 2008 financial crisis that engulfed the subprime bond market. The corporate bond market is turning gradually into a $trillion BBB junk bond field and broken bone yard, after years of abused bond issuance devoted to share buybacks and executive options. It can be stated with accuracy that the entire global bond market is subprime, led by the USTBonds. In the last ten years, absolutely nothing has been fixed, no remedy even attempted, while all the errors, crimes, and reckless monetary policy that created the Lehman fiasco with the Global Financial Crisis, have been repeated on a global scale. Debt has exploded globally, and especially in the USGovt finances. The great unfolding crisis will engulf sovereign bonds, national banking systems, and major corporations. For the last ten years, the USD-based money supply has almost tripled. The process created a coiled spring. The Gold price is due to triple in compensation. Much lost time will be made up for. It just needs some internal, external, and systemic pushes. The Gold market will never let a crisis go to waste; it will respond.

The unfolding global crisis will expose the USTreasury Bond as toxic, the new subprime bond. It will struggle to maintain the safe haven status, but lose the battle. Gold will assume the safe haven status, along with other undetermined hard assets. Attempts by the Basel bunch of uber-bankers, who have no official authority over the Western central banks, will change the course of banking history. That Gold is made a risk-free Tier-1 asset will put forth a direct challenge to the USTBond in banking reserves. All systems will change.

GLD FUND FLASHING SIGNAL OF SHORTAGE

The GLD Exchange Traded Fund can serve as a very reliable early warning signal for a very tight gold supply, and corresponding Gold price upward moves. It signals shortage and tight supply now, with a divergence between London Gold price versus GLD Fund inventory in tonnage.

Consider a lesson on the GLD Exchange Traded Fund. Some preliminary remarks are necessary. It is a fund to deceive the public, whose prospectus is routinely violated by the London banksters. The GLD Fund is used as a magnet for naive ignorant lazy investors, lured to think they own gold. While they might enjoy the upside potential in the Gold price, their investment is a major vehicle used to keep the price down. Its inventory is raided by the US-UK banks, and sold into the market in regular frequent events. The big investors are often denied access to physical gold delivery, since not club members at the big banks, a violation. Nobody enforces the rule. The inventory contains real gold metal, but it is a massive vat for discharge into the market in pure price suppression by the criminal banker set. They manage the fund like a criminal slush fund. With each raid on the GLD vault, the LBMA official Gold price comes down. Notice the tight correlation in the graph below, except in recent months.

Evidence is clear. A divergence can now be seen, from the clear signal between the LBMA Gold price and the critically low GLD vault inventory. The Gold price is going up, while the GLD inventory is going down. Since three months ago, the divergence has begun to show itself. The chart shows data through February of this year.

Another key but subtle point of interest. The official inventory level of the GLD Fund includes gold in motion, a term to describe delivery from mining firms that is in transit. It is never truly in the vaults, since when a delivery is made, another delivery is in motion under new contract stipulation. By that is meant not just trucks loaded with bars, but trucks loaded with concentrated ore heading to refineries, plus bars under contract delivery within the quarter (three months). Furthermore, other gold shows up in the GLD inventory, but it is not available, such as private elite accounts, even pledged allocated gold.

Therefore the effective zero level is far above the posted zero level, which is often estimated by the expert analysts (like EuroRaj) to be around 400 to 600 tonnes gold, very much unknown.This is an important point, since the official GLD inventory is just above 750 tonnes currently. It has varied from 750 tonnes to 850 tonnes in the last 18 months, now near the effective zero mark. As the GLD vaults reach effective zero, the Boyz on Wall Street and London Centre lose the ability to reach into the vaults overnight in dumping exercises intended to pull the Gold price down. They essentially have a tool taken away.

Consider sage words from a Jackass colleague. The purpose of GLD is a private warehouse run by the Bank of England. When the public demand or central bank demand has to be met, they raid the inventory by redeeming share baskets and remove physical bars overnight. The redemption of shares is an act of selling of the paper that drives prices lower, when more exactly the process is actually driven by drainage of physical at this banker slush fund. There is physical gold but it belongs primarily to BOE and certain billionaires. The sheeple cannot get access to it unless they pony up enough cash for 10,000 ounces, and even then, they are often denied the metal. Since the USFed went dovish in December in a reversal of language away from further tightening, and toward more easing, the Gold price has been going up while the GLD Fund tonnage has been going down. The Big Boyz know the RESET is here. Refer to the divergence in progress for the last three months.

The clear signs of physical gold drainage lead to growing distrust in the entire USDollar & USTreasury framework like a creeping slow motion cancer. Gold drainage affects the delicate Supply & Demand equilibrium. The result is an assured imminent situation that reeks of financial instability. The true refuge will be Gold held in personal possession or with trusted access by agents. The irony could be that broken trust of the GLD Fund and broken trust of the LBMA/COMEX, complete with lawsuits, could bring down the paper game and lead the masses into true physical Gold holdings. For more background and other discussion, see Sprott Money (HERE) with a Craig Hemke interview.

DUAL UNIVERSE

The next stage for global finance will incorporate regional structures and platforms. The entire community of nations is making major adjustments as preliminary preparation to the Global RESET, in order to minimize the shock, disruption, and potential chaos. Expect regional themes to dominate, as the Dual Universe comes into form. The East will prefer to trade in Chinese RMB terms, and often in Euro terms. The West will prefer to conduct trade in USD terms, but also British Pounds in trace amounts within the old colonies. A dichotomy has formed with great geopolitical division amidst hostility and trade friction. The entire USFed QE initiative, coupled with unbridled $trillion USGovt debts, has fostered a rebellion amidst visible bond fraud. The rest of the globe is in active revolt, whose movement gains momentum each month. The transition period will involve the two dominant currencies at work: the USD and RMB. The USDollar will not go away quickly or easily. It is well rooted in trade payments systems, in credit systems, in banking systems, and more. The entire Langley seven silos of corrupt illegal enterprises (narcotics, weapons, human trafficking, human organs) are based in the USDollar, with gargantuan savings accounts and business investments. They will not go away anytime soon, which dictates an interim period. The Dual Universe has been born, without much fanfare. The Chinese RMB is to be the designated caretaker, used for ushering in the Gold Standard.

In the meantime, the United States will face an acute risk for the transition. It must assure import supply. The USTreasury Bill will no longer be trusted, or even accepted, following the RESET. Entirely new trade payments systems are coming, and the US will lose its privilege of paying for hard goods with phony money and IOU coupons. The USTBill has a fraudulent backing, an unlimited supply, fraudulent masters, and is coupled with massive debt which is widely seen as unpayable. The US must adapt to the Gold Trade Note in usage. It must contend with shortages and rising prices, following import supply interruptions. It must share global power, while losing the exceptional status. It must ward off isolation. It must reindustrialize. It must pay down the $22 trillion debt. It must source gold for the new currency. It must face the risk of a stark reality in the New Scheiss Dollar, a Third World conception, provided the USGovt resorts to its usual fraudulent finances.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7241/

//OFFSHORE YUAN: 6.7327 /shanghai bourse CLOSED UP 25.62 POINTS OR 0.85% /

HANG SANG CLOSED UP 161.34 POINTS OR 0.56%

2. Nikkei closed //DOWN 49.66 POINTS OR 0.23%

3. Europe stocks OPENED RED

/USA dollar index FALLS TO 96.74/Euro FALLS TO 1.1270

3b Japan 10 year bond yield: RISES TO. –.07/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.37/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 59.52 and Brent: 67.85

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO –.05%/Italian 10 yr bond yield UP to 2.54% /SPAIN 10 YR BOND YIELD DOWN TO 1.08%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.59: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.80

3k Gold at $1318.50 silver at:15.46 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 43/100 in roubles/dollar) 64.84

3m oil into the 59 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.28 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9932 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1196 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.05%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.38% early this morning. Thirty year rate at 2.84%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4349

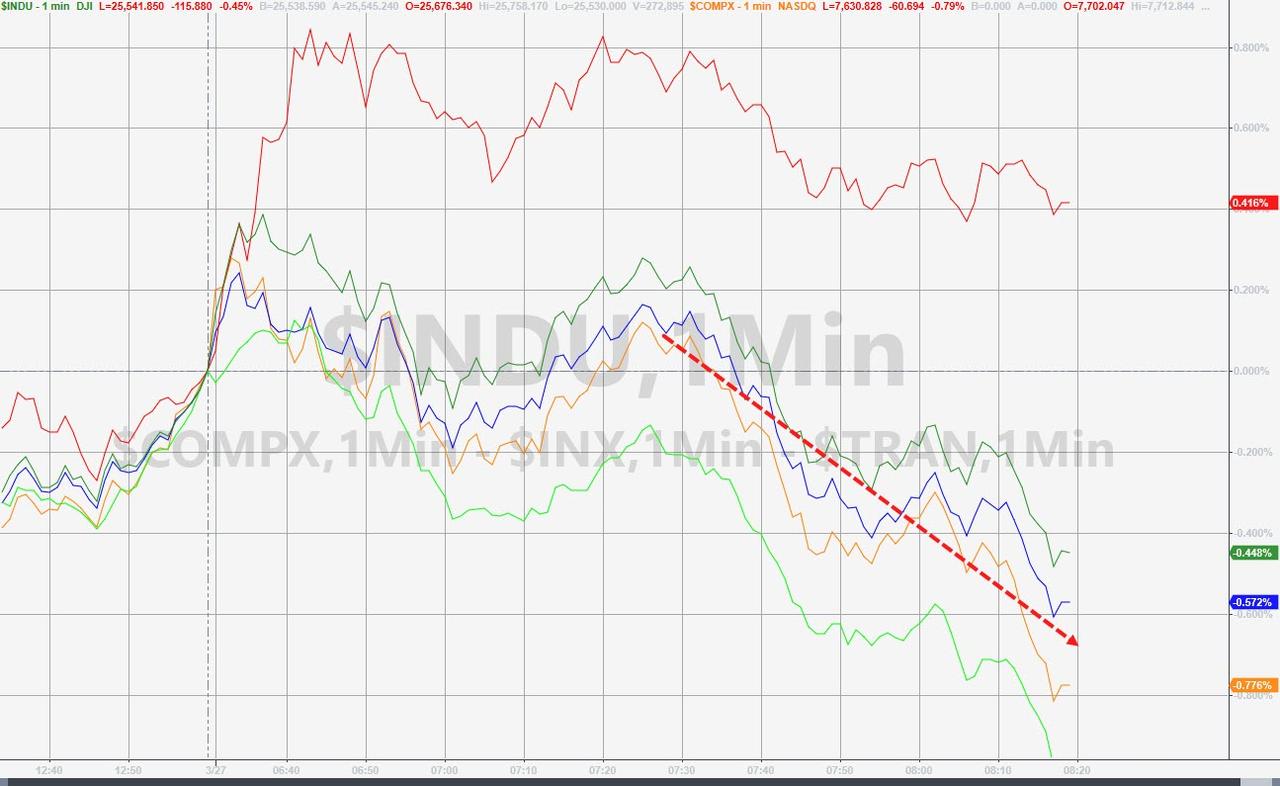

Global Stocks, US Futures Slide As Interest Rates Resume Plunge

Monday’s “recession off” optimism lasted just one day, and global markets and US equity futures are once again falling as yields resume their slide and the US yield curve inverts further.

After a brief respite on Monday when mortgage hedgers appeared to take the day off, treasuries resumed their rally with the 10Y yield tumbling as low as 2.35%, following the slide in Bunds as Germany auctioned off its first negative yielding debt with a negative yield at auction, as investors again turned their attention to a deteriorating economic outlook and a shift toward accommodation by major central banks. As a result, stocks in Europe reversed gains along with U.S. equity futures.

Europe’s Stoxx 600 fell, led by utilities and telecommunications shares, while S&P500 futures slipped, even though so far the selling is contained, with the Stoxx 600 down only ~0.4%, far cry from last Friday’s 1.2% rout.

The MSCI Emerging Markets Index’s 0.1% decline also looks tame compared with Monday’s 1.1% slide. Cyclical sectors such as autos and miners are in the green – car makers in particular are getting a boost from Nissan-Renault M&A chatter – and declines are largely confined to bond-proxy sectors. Dividend-paying sectors such as consumer staples, real estate and utilities are outperforming in the lower-for-longer era, according to Bloomberg.

Mario Draghi said in a speech in Frankfurt an accommodative policy stance is still needed in the euro region, although he hinted at possible rate tiering, noting that banks are being hurt by NIRP.

Earlier, Asian markets were mixed, though Chinese shares pushed higher as a burst of diplomacy suggests Beijing and Washington remain determined to de-escalate their trade war. Markets got a reminder of global growth risks after Chinese data showed industrial profits shrank the most since late-2011 in the first two months of the year. Chinese mainland shares bounced almost one percent as expectations deepened of more central bank stimulus.

“Our view is that reflation story remains on track. We do expect the (Chinese) government to come to the rescue and provide some respite,” said Justin Onuekwusi, portfolio manager at Legal and General Investment Management. “It feels to me that markets had priced in a lower-for-longer (interest rate) environment even before central banks. They had come a long way very quickly and now they are taking a bit of a breather. Global growth overall looks reasonably healthy, despite the slowdown,” he added.

All eyes remain on the US bond market, however, where the key recession indicator, the 3 Month – 10 Year yield hit fresh post crisis lows, sliding as low as -11bps before rebounding modestly.

The U.S. yield curve inversion, which has preceded every U.S. recession for the last 50 years, triggered a sharp stock selloff last week. The drop in yields picked up pace after the U.S. Federal Reserve signaled a halt to its rate increases.

Meanwhile, speculation that the Fed will need to cut rates spread overnight, with some such as Legg Mason’s Brandywine Global

unit even forecasting a cut this year. Stephen Moore, President Trump’s pick for an open Fed board seat, said in an interview with the New York Times that the central bank should immediately cut rates by half a percentage point.

“The money-market curve is telling us that the Federal Reserve needs to do more,” Francis Scotland, director for global macro research at Brandywine, told Bloomberg TV in Hong Kong.

With the global economy headed for recession, traders will be especially focused on the outcome of U.S.-China trade talks, which resume this week, as well as any developments in Britain’s ridiculously interminable Brexit.

In the latest Brexit news, PM May will be urged by her own MPs to name the date of her departure today as the price of getting her Brexit deal through Parliament. PM May will be meeting with the 1922 Committee at 1700GMT today, according to Sky News. UK PM May’s team are debating a potential timetable for her to stand down, which might not necessarily see her make the announcement before MV3, according to the FT.

Additionally, the UK Cabinet Minister is now not expecting free votes for tonight’s indicative votes as some demanded, risking further resignations; according to Sky News’ Faisal Islam. BBC’s Nick Eardley added, however, that no decision has been made as of yet. Opposition Leader Corbyn is preparing to whip his MPs to back a move today that would keep Britain in the single market and customs union.

In overnight FX moves, the pound wobbled as a key Brexit hardliner indicated he’s willing to back Theresa May’s departure deal. But it was the New Zealand dollar that was the standout, tumbling more than 1% after the central bank joined its peers in the United States and Europe by turning dovish – it flagged a possible interest rates cut, sending the kiwi dollar 1.6 percent lower to its lowest in 2-1/2 weeks. The move also weighed on the Australian dollar.

“The market was taken by surprise by the dovish tone,” Thu Lan Nguyen, an analyst at Commerzbank said of the Reserve Bank of New Zealand. “Most central banks have turned dovish. Even those that hiked interest rates did it with a very cautious outlook on rates.”

The dollar index versus a basket of six major currencies was up 0.1 percent at 96.745, building on modest gains overnight.

In emerging markets, there were renewed concerns over Turkey and Argentina where currencies have fallen sharply in recent days. The lira liquidity squeeze has sent overnight swap rates on lira to 700 percent.

In commodities, WTI gave back some of its gains in the previous session after Russia said it was on track with output cuts and disruptions to refiners along the Houston Ship Channel added to supply concerns.

Trade balance and current account figures are due. Companies reporting earnings include Vale, Lululemon and Lennar

Market Snapshot

- S&P 500 futures up 0.1% to 2,826.50

- STOXX Europe 600 down 0.3% to 376.33

- MXAP down 0.2% to 159.39

- MXAPJ down 0.06% to 523.53

- Nikkei down 0.2% to 21,378.73

- Topix down 0.5% to 1,609.49

- Hang Seng Index up 0.6% to 28,728.25

- Shanghai Composite up 0.9% to 3,022.72

- Sensex down 0.2% to 38,147.42

- Australia S&P/ASX 200 up 0.09% to 6,135.97

- Kospi down 0.2% to 2,145.62

- German 10Y yield fell 2.4 bps to -0.039%

- Euro down 0.04% to $1.1262

- Brent Futures up 0.3% to $68.20/bbl

- Italian 10Y yield fell 3.5 bps to 2.114%

- Spanish 10Y yield fell 3.0 bps to 1.062%

- Brent Futures up 0.3% to $68.20/bbl

- Gold spot down 0.1% to $1,314.90

- U.S. Dollar Index up 0.1% to 96.87

Top Overnight News

- Mario Draghi said the ECB is ready to soften the impact of negative interest rates if they are found to harm the transmission of monetary policy. The ECB has kept its deposit rate below zero since June 2014 with policy makers insisting negative rates remain part of the tool kit.

- U.K. PM Theresa May’s Brexit deal may finally be winning support from Conservative hardliners, though she may have to promise to step down to get it over the line. Meanwhile Parliament is preparing to vote on rival plans that could soften — or cancel — Britain’s departure from the European Union.

- Three months after news first emerged of a hedge fund blowup that threatens to saddle Citigroup Inc. with millions of dollars in losses, details of the fund’s implosion are becoming clearer. GTEC Pandion fund, whose prime broker was Citigroup, started unraveling in August on currency trades mainly involving the Turkish lira.

- U.S. and Chinese officials resume high-level trade talks this week as they close in on a deal that could just be the first step in the long road to economic peace.

Asian equity markets were mixed as the region somewhat failed to maintain the broad positive momentum from US where all majors finished in the green with the gains led by outperformance in energy and financials. ASX 200 (+0.1%) and Nikkei 225 (-0.2%) were both negative throughout the day although the Australian benchmark just about recovered at the close, while Tokyo stocks underperformed amid currency effects and mass ex-dividend day involving over 1000 stocks including blue-chips Mitsubishi UFJ, SoftBank and Sony. Elsewhere, Hang Seng (+0.6%) and Shanghai Comp. (+0.8%) were initially indecisive amid continued PBoC liquidity inaction and as participants mulled over another deluge of earnings, as well as discouraging data in which February YTD Industrial Profits slumped by the most in nearly a decade. However, sentiment in China then improved with energy names boosted by the recent advances in oil, while there was also reports confirming that China and Italy signed an MOU to make Italy the first western European country to join the Belt & Road initiative. Finally, 10yr JGBs were slightly higher as they tracked the marginal gains seen in T-notes and as the subdued risk appetite in Japan kept prices afloat.

Top Asian News

- Hong Kong Property Prices May Rise 7% on Liquidity: JPMorgan

- A $17 Billion Funding Challenge Facing China’s Evergrande

- Euro Extends Drop Before Draghi; Pound Slips as Volatility Rises

- Tata, GIC Buy $1.2 Billion Stake in Delhi Airport Operator

A relatively choppy session for European equities thus far [Eurostoxx 50 -0.4%] as sentiment soured after a mixed lead from Asia. Sectors are mostly lower although the consumer discretionary sector (+0.2%) is driving the gains amid the slew of positive news-flow for the auto sector. Renault (+3.4%) shares spiked higher at the open amidst fresh merger talks with Nissan ahead of a bid for Fiat Chrysler (+3.3%), whilst Daimler (+1.2%), BMW (+0.5%), and Volkswagen (+0.4%) shares also march in tandem. Reports stated Daimler was close to selling its 50% “Smart” stake to Geely, meanwhile Volkswagen struck a multi-year partnership with Amazon. Elsewhere utilities underperform despite its defensive properties with Centrica (-1.3%), National Grid (-1.4%), E.ON (-1.6%) all near the foot of their respective bourses. In terms of notable movers, Wirecard (-4.5%) shares shed some of yesterday’s gains after the company announced that some of its Singapore employees may face criminal liability regarding the ongoing accounting scandal. Finally, Swedbank (-7.8%) shares declined after the company confirmed that a search is currently underway at the head office, following on from reports that an internal investigation has been initiated by the Swedish Economic Crime Authority.

Top European News

- May’s Deal Gains Support Ahead of Votes on Plan B: Brexit Update

- Billionaire Ashley Weighs Bid Valuing Debenhams at $81 Million

- Bank of Russia Says Inflation Expectations Fell Again in March

- Wirecard CEO Braun: We Have No Plans to Release Full Report

In FX, all eyes were on the NZD/AUD as the Antipodean Dollars are back on the rack, with the Kiwi sharply underperforming in wake of OCR cut revelations from the RBNZ overnight after an unexpected switch from neutral to easing mode amidst a bleaker assessment of the economy and heightened risks of a more pronounced downturn. Nzd/Usd slumped over a big figure in response and is clinging to 0.6800, as the Aud/Nzd cross extended recovery gains well beyond 1.0300 to circa 1.0450 before consolidating, and with Aud/Usd retreating to sub-0.7100 at one stage on the back of worrying Chinese data in the form of industrial profits (-14% y/y and weakest in almost 10 years).

- NOK – Another G10 laggard following a rise in Norwegian unemployment vs the consensus for an unchanged jobless rate, with Eur/Nok back up above 9.6500 vs a more stable SEK around 10.4200 vs the single currency amidst mixed Swedish sentiment indicators, a wider trade surplus and 2019 GDP forecast upgrade via the NIER.

- JPY/CHF/EUR – Relative outperformers and all firmer vs the Greenback as the Jpy benefits from renewed safe-haven positioning within a 110.70-30 range and moves further away from decent option expiry interest sitting between 110.70-75 (1.4 bn). Similarly, the Franc is benefiting from another downturn in risk sentiment and revisits recent highs around 0.9900 and through 1.1200 against the Euro, which looked vulnerable independently when testing Tuesday’s lows vs the Buck around 1.1250 before some timely support from ECB President Draghi who contended that a more sustained downturn in external demand and other factors have merely hampered rather than scuppered Eurozone inflation convergence towards target. Eur/Usd has subsequently rebounded relatively firmly to challenge Fib resistance at 1.1280, but could be capped ahead of 1.1300 given hefty expiries spanning 1.1255-65 (1.5 bn).

- GBP/CAD – The Pound remains rangebound around 1.3200 vs the Usd awaiting the next chapter of Brexit and up to 16 amendments to be voted on in Parliament after the Letwin approval – see our headline feed for a situation update and detailed analysis of all the motions tabled that could be selected by the HoC Speaker later today. Note, Cable survived an early downside attempt, and like Eur/Usd held around yesterday’s base, but is likely to face some offers around 1.3250 by the same token. Elsewhere, the Loonie is losing some support from oil prices with Usd/Cad towards the top of a 1.3407-1.3376 band ahead of trade data from Canada and the US.

- DXY – The index has come up against some psychological and chart resistance just shy of 97.000, with a Fib at 96.956 only marginally and briefly breached. Moreover, the broad Dollar has conceded ground to the aforementioned comeback in rival currencies.

In commodities, the oil complex is extending losses as the risk-off sentiment took the wheel. WTI (-0.8%) futures gave up the recently claimed USD 60/bbl and flirts closer to USD 59.50/bbl whilst Brent futures (-0.3%) rests just below USD 68.00/bbl. Last night’s APIs showed a surprise build of 1.9mln barrels (vs. Exp. draw of 1.2mln) with trader eyeing the release of this week’s DoEs as a fresh catalyst. Further supply side news-flow may also be contributing to the downside as sources stated that Russian oil output in March (so far) stood at 11.30mln BPD, only marginally lower from February’s 11.34mln BPD. Finally, oil officials noted that crude loading operations have resumed in Iraq’s Southern Terminals following a stoppage. Elsewhere metals are largely benefiting from the marginal pullback in the buck with gold (-0.2%) gains also exacerbated by safe-haven demand. However, dollar-induced upside in copper is capped by the risk averse sentiment as the red metal trades sideways. Finally, the majority of miners and port operators in Australia have resumed after 4-6 days of disruption following cyclone activity.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 1.6%

- 8:30am: Trade Balance, est. $57.0b deficit, prior $59.8b deficit

- 10am: Current Account Balance, est. $130.0b deficit, prior $124.8b deficit

- 12pm: Revisions: Industrial Production and Capacity Utilization

DB’s Jim Reid concludes the overnight wrap

For those of you reading this today who manage people, imagine if your team kept on saying to you that you weren’t doing a very good job and were the worst boss ever (to my team please don’t get any ideas). Then imagine that they got together and first tried to get rid of you but then realised that they couldn’t. Instead, they organised a coup to relieve you of your powers for a day so they could prove they could do a better job.

Well that’s the position the U.K. government finds itself in today as we welcome in what will be another extraordinary day in U.K. politics. Backbenchers will take over proceedings for a day with indicative votes on the agenda with the aim being to try to break the impasse in the most important legislative process faced by the country in a couple of generations.

As things currently stand, Speaker Bercow will announce what options will be considered at 3pm today, the vote will take place at 7pm, and results will be announced around 8:30pm. The vote will reportedly be a single ballot containing every option with a yes/no decision to be made. So it’s quite possible that we end up getting a muddled outcome with no clear majority position. It’s also not yet clear if the government will whip votes or if MPs will be given free reign. The latter seems unlikely. Meanwhile, Sir Oliver Letwin, who had brought forward the motion for parliamentarians to take control of Brexit earlier in the week, has said that there is a little chance that the House of Commons will produce a majority for an alternative way forward today in just a single vote. He further added that, we will have to use this process today “and on Monday to try to work towards a consensus that can carry a majority”. So indicating that a further set of votes on narrowed down alternative options could happen early next week. Sterling is down (-0.18%) this morning.

Obviously, the outcome to today’s indicative votes will depend on what options are actually offered up to be voted on, but when the House of Commons held indicative votes on reforming the House of Lords in 2003, they voted against the status quo of an all-appointed upper house, but then went on to vote against all the alternatives that were presented! With parliament having already voted against May’s deal twice, voted in amendments against a no-deal Brexit and against a second referendum, it seems a big step to think a majority will be found unless horse trading around customs union / single market membership is done cross benches. Whatever happens, it’s worth noting that as things stand, with the Withdrawal Agreement still not approved by MPs and no further extension agreed right now, the legal default remains a no-deal Brexit on April 12.

In terms of yesterday’s developments, Jacob Rees-Mogg, who chairs the European Research Group of Conservative MPs favouring a hard Brexit, said on Twitter that “The choice seems to be Mrs May’s deal or no Brexit.” The implication being that if a no-deal outcome isn’t going to happen, he would reluctantly back the deal rather than risk losing Brexit altogether. Also Boris Johnson said that if “we” vote down May’s deal again there is “an appreciable risk” that Brexit won’t happen. He later said on the BBC that the next stage of negotiations need a new approach with some suggesting it was a hint that he’d consider backing the deal if Mrs May stepped aside.

These two potential key conversions might be too late in the day, especially as Sky News reported yesterday that the DUP would prefer a long extension over accepting Prime Minister May’s deal, and the party’s Brexit spokesman, Sammy Wilson, wrote in the Telegraph that this was a “toxic deal”. For reference, in the last meaningful vote on 12 March, the government lost by 149 votes, so they’d need 75 MPs to switch sides in order for the deal to win. However, the noise is that there may be one last try tomorrow or Friday. Importantly, Mrs May will speak at a private meeting of Conservative politicians early this evening where she will try to persuade them to vote for her deal while many of her party members are expecting her to use the meeting to announce a date when she will quit as prime minister in return for voting for her WA.

Back into a world that carries on outside of our domestic bubble, the S&P 500 rebounded yesterday, advancing +0.72%, with every sub-index rallying. The energy sector advanced +1.45% as Brent crude oil rose +1.31% to within 1% of its four-month high. Comments from Russia’s energy minister Alexander Novak heightened confidence that OPEC+ will maintain its output cap agreements to limit supply and support prices. The DOW and NYFANG indexes lagged a bit, gaining +0.55% and +0.37% respectively, largely due to underperformance by Apple (-1.03%). A US trade judge ruled against the tech giant and recommended bans on imports of certain iPhones (iPhone 7 and iPhone 7 Plus), saying that the products had violated a patent owned by chipmaker Qualcomm (+2.40%). After the US markets closed, the International Trade Commission came up with a second ruling where the full commission ruled against Qualcomm in a different case, which would have led to an import ban on a broad range of iPhones, including the iPhone 7, iPhone 7 Plus, iPhone 8, iPhone 8 Plus, and the discontinued iPhone X. Apple was up +0.62% in after-market trading while Qualcomm was down -0.78%.

European equities also recovered, with the STOXX 600 closing +0.77%, while the FTSE 100 (+0.58%), CAC 40 (+0.26%) and the DAX (+0.89%) all advanced. Government bond yields made a comeback too, with ten-year yields in the UK and Germany up +2.1bps and +1.1bps, respectively, although 10yr Bunds stayed below zero. Italy was an exception however, where yields on ten-year BTPs fell by -3.3bps, reflecting more positive risk appetite, while the flight from safe havens also saw gold lose ground, down -0.44%. US 2 and 10yr yields were both up 2.5bps, mirroring the slight global reversal of the sharp yield rally seen over the preceding few days. This morning, 2yr and 10yr US yields are down -2.7bps and -0.5bps, respectively, steepening the 2s10s curve to 17.9bps from 15.7bps yesterday. This is now near the top of the YTD range having got to the bottom of it last Friday. The move comes in the light of an interview from the Fed Governor nominee Stephen Moore to the New York Times overnight, where he walked back some of his prior critical rhetoric of the Fed but also said that he would want to immediately cut rates by 50bps. The market will take note of this and it could be construed as an attempt by Mr Trump to more politicise the Fed.

Overnight, markets in Asia are trading mixed with the Hang Seng (+0.64%) and Shanghai Comp (+0.55%) up while the Nikkei (-0.42%) and Kospi (-0.04%) are down. Elsewhere, futures on the S&P 500 are up +0.13% while the New Zealand dollar is down -1.56% this morning after the country’s central bank joined the growing global bandwagon of dovish central banks by saying that its next move is more likely to be a rate cut.

Mary Daly, President of the San Francisco Fed, gave a speech on inflation and reiterated the recent Fed position in favour of patience on the rates front. She noted that “data have been coming in a little bit slower than we thought” and that “we’ve seen financial conditions tighten up.” With inflation persistently below target and “inflation expectations edging lower,” Daly is in favor of maintaining an easy policy stance. She mentioned that she is “in the curiosity stage” when asked about changes to the Fed’s inflation targeting framework, a topic that will certainly remain in focus this year.