GOLD: $1290.65 DOWN $20.60 (COMEX TO COMEX CLOSING)

Silver: $15.00 DOWN 31 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1290.70

silver: $15.01

London/LBMA expires Friday March 29/2019.

The crooks continue with their whacking right in front of the authorities/regulators despite the criminal probe of precious metals manipulations.

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 0 NOTICE(S) FOR 100 OZ (0.0000 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 396 NOTICES FOR 39600 OZ (1.23176 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR NIL OZ/

total number of notices filed so far this month: 5424 for 27,120,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4009:DOWN $26

Bitcoin: FINAL EVENING TRADE: $4022 DOWN 14

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 0/0

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST WENT UP AGAIN : THIS TIME BY A STRONG SIZED 1406 CONTRACTS FROM 192,676 UP TO 194,082 DESPITE YESTERDAY’S 12 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 1684 FOR MARCH 2020 200 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1884 CONTRACTS. WITH THE TRANSFER OF 1884 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1884 EFP CONTRACTS TRANSLATES INTO 9.42 MILLION OZ ACCOMPANYING:

1.THE 12 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 27.120 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

35,928 CONTRACTS (FOR 20 TRADING DAYS TOTAL 35,928 CONTRACTS) OR 179.640 MILLION OZ: (AVERAGE PER DAY: 1796 CONTRACTS OR 8.982 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 179.640 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 25.57% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 544.94 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1406 DESPITE THE 12 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1884 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY STRONG SIZED: 3290 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1884 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1406 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 12 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.31 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.970 BILLION OZ TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR 0 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 27.120 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 4831 CONTRACTS, TO 504,744 WITH THE FALL IN THE COMEX GOLD PRICE/(A DROP IN PRICE OF $4.05//YESTERDAY’S TRADING).

I THINK WE JUST HAD OUR SECOND DAY OF OPEN INTEREST FALL DUE TO THE ANTICS OF THE SPREADERS. IT LOOKS LIKE THE SPREADERS LIQUIDATE THEIR CONTRACTS NOT SIMULTANEOUSLY BUT AT DIFFERENT TIMES DURING THE DAY TO CAUSE THE CASCADE OF PRICING IN OUR PRECIOUS METALS AND THAT IS HOW THEY ALWAYS WIN ON OPTION EXPIRY..THEY ARE SO CROOKED.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9166 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 5831 CONTRACTS,JUNE: 3335 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 504,744. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4335 CONTRACTS: 4831 OI CONTRACTS DECREASED AT THE COMEX AND 9166 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4335 CONTRACTS OR 433500 OR 13.48 TONNES.

YESTERDAY WE HAD A FALL IN THE PRICE OF GOLD TO THE TUNE OF $4.05....AND YET WITH THAT, WE HAD A CONSIDERABLE GAIN IN TONNAGE OF 14.38 TONNES!!!!!!. (HOWEVER ALL OF THE COMEX LOSS IS NO DOUBT DUE TO THE LIQUIDATION OF THE SPREADERS)

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 143,664 CONTRACTS OR 14,366,400 OR 446.85 TONNES (20 TRADING DAYS AND THUS AVERAGING: 7183 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAYS IN TONNES: 446.85 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 446.85/2550 x 100% TONNES = 17.52% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1315.81 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 4831 WITH THE LOSS IN PRICING ($4.05) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9166 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9166 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 5318 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9682 CONTRACTS MOVE TO LONDON AND 4831 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 13.48 TONNES). ..AND ALL OF THIS STRONG DEMAND OCCURRED WITH A FALL IN PRICE OF $4.05 IN YESTERDAY’S TRADING AT THE COMEX!!!!! HOWEVER THERE IS NO DOUBT THAT AGAIN WE HAVE LIQUIDATION OF SPREADERS AS WE HEAD INTO AN ACTIVE DELIVERY MONTH AND IT IS THEIR ACTION THAT LEADS TO A FALL IN PRICE SO UNDERWRITTEN CONTRACTS WOULD NOT BE EXERCISED. THIS IS HOW THE CROOKS WIN ALWAYS ON OPTIONS EXPIRY.

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $20.60 TODAY

VERY STRANGE!! NO CHANGES IN GOLD INVENTORY

INVENTORY RESTS AT 784.26 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 31 CENTS IN PRICE TODAY:

STRANGE!!!

A BIG CHANGE IN SILVER INVENTORY AT THE SLV TODAY

A DEPOSIT OF 469,000 OZ (WITH SILVER DOWN?)

/INVENTORY RESTS AT 309.957 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 1406 CONTRACTS from 192,676 UPTO 194,082 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 1684 FOR MAY AND MARCH 2020: 200 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1844 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1406 CONTRACTS TO THE 1884 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 3290 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 16.45 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 27.120 MILLION OZ FOR MARCH.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 12 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1884 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 27.78 POINTS OR 0.92% //Hang Sang CLOSED UP 46.96 POINTS OR 0.16% /The Nikkei closed UO 344.97 POINTS OR 1.61%/ Australia’s all ordinaires CLOSED UP 0.63%

/Chinese yuan (ONSHORE) closed DOWN at 6.7344 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 58.52 dollars per barrel for WTI and 67.05 for Brent. Stocks in Europe OPENED MIXED

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7344 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7450 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 C/ CHINA

I will believe this when I see Xi make these statements. Strangely the markets did not respond on these “major” concessions:

i) movement on forced technology transfers

ii) movement on China ready to engage the west’s cloud computing

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)GERMANY

The kingpin of derivatives, Deutsche bank is discussing raising up to $10 billion dollars to secure the Commerzbank deal. Who in the right frame of mind would lend to this hopeless basket case.

( zerohedge)

ii)UK/MORNING

ii b)UK /AFTERNOONAnother vote this afternoon and no doubt another failure. It looks like we will have a no deal BREXIT

(courtesy zerohedge)

iii)EUROPE

This is interesting: how the Europe is going to destroy us on internet usage

( Tom Luongo)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Turkey

The big news of the day: The Turkish lira collapses after news that the country burned through 1/3 of their USA (foreign reserves) in one month. Overnight swaps collapsed to just 40% from 1,338%. Remember also that Turkey has a huge amount of gold in their reserves and Erdogan will never part with the yellow stuff. This is becoming a full blown currency crisis as Turkey is massively short dollars and cannot find any on the markets

( zerohedge)

6. GLOBAL ISSUES

CANADA

Canadians are proud to the have the highest debt per GDP in the world and it is for this reason that many are shorting the Canadian banks due to their huge exposure to real estate

(courtesy zerohedge)

SWEDEN

Talk about timing: Swedbank fires its CEO one hour prior to the start of its annual meeting. It’s shares have been halted. They are being accused of huge moneylaundering

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

INDIA

Congratulations to India: they shot down a satellite and thus join an elite club of “Space Powers”

(courtesy zerohedge)

9. PHYSICAL MARKETS

( Bloomberg/GATA)

ii)Kevin W. reports to us on how Gold being a Tier one asset will play havoc to our banks

iii)Why you invest in gold

( Simon Black)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

ii)Market data

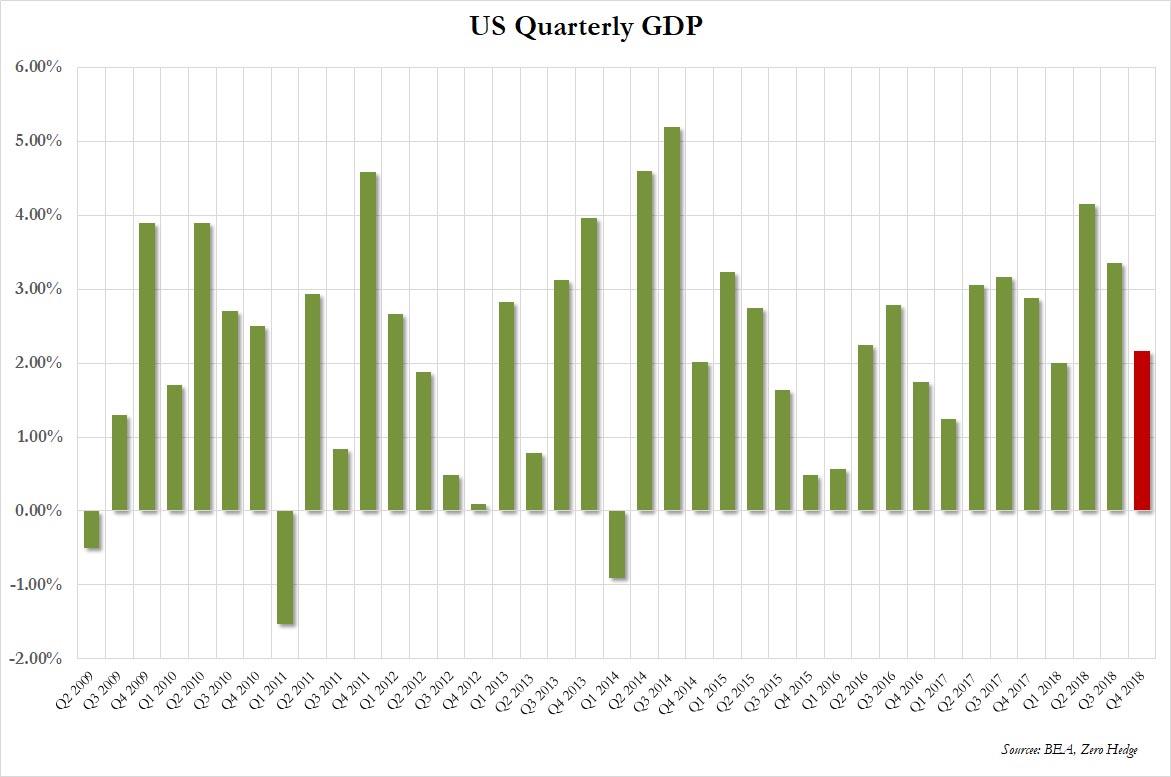

a)The USA 4th quarter has now been lowered to 2.2% from 2.6%. However the full year 2018 rises to 3.0% and thus Trump can boast that he engineered a 3% growth something that Obama never achieved in his 8 years

( zerohedge)

b)Housing is such a huge component of GDP..pending sales tumble 4.9% year over year..the 14th straight month of declines

ii)USA ECONOMIC/GENERAL STORIES

Trump correctly warns OPEC and the world that the markets are fragile and cannot stand 60 dollar oil

( zerohedge)

iv)SWAMP STORIES

a)State attorney General Foxx claims files “inadvertently” sealed. What an absolute joke. The FBI and the DOJ are reviewing the case and no doubt these guys will file charges.

(courtesy zero hedge)

b)TRUMP: the FBI and DOJ will investigate the case after a leaked email reveals a scramble to cover tracks

(courtesy zerohedge)

c)All nine Republicans demand the resignation of Schiff

(courtesy zerohedge)

end

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL LOWERS TO 666 CONTRACTS FOR A LOSS OF 101 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI GAINED 653 CONTRACTS UP TO 134,637 CONTRACTS.

i) Into the dealer: Delaware: 1799.99 oz

Brexit and Learning To “Live With Boom and Bust Economic Cycles”

by John Downing via Independent.ie

Generations of people have learned to live with boom and bust economic cycles.

Years of relative plenty were followed, as night follows day, by grief including high unemployment and forced emigration on a large scale.

![]()

In fact, if you go back much beyond the late 1960s, it would not be too cynical to say the cycles were often more about going from bust to really busted, as for decades the country was hit by crippling rates of largely enforced emigration.

The 1980s into the 1990s saw politicians across the western world, including Ireland, adopt the mantra: “We need to end that cycle of boom and bust.”

Ireland’s inexorable moves to joining the EU single currency began with voters endorsing the 1992 Maastricht Treaty. They were sealed with promises of “Brussels billions” at a fateful EU leaders’ summit in Edinburgh in December 1992.

Looking back now, the decision was sold by our political leaders as getting huge EU grant aid. But the move was also in part about pursuing a period of more prolonged, if not permanent, economic stability.

The so-called Maastricht criteria, effectively the single currency membership rules, fixed limits on national deficits and long-term debt as a proportion of national wealth. Well before Ireland’s final decision to join the euro, as launched on international money markets on January 1, 1999, we were told the single currency membership rules were a good thing in themselves.

The rules could help “end the cycle of boom and bust”. Since those days of relative innocence, Ireland’s economy has soared to the heights in the mid-2000s, plumbed the depths from 2008 onwards, and then surprised many by bouncing back again to fretful prosperity today.

The experience makes “ending the cycle of boom and bust” far more than a slogan.

When you consider that one in seven Irish people was out of work as recently as February 2012, also a time of high emigration, then you know that we have a yearning never to return to the days of bust.

But the reality is that things were motoring very well until Brexit hit us like a bucket of iced water in the early morning of June 24, 2016. Up to then, we had lived with the assumption that Brexit would be defeated and we would continue in a hopefully moderated and realistic “boomward direction”.

Over three years, we have watched the UK’s politics deteriorate at a distressing rate.

We have looked in vain for signs that a reasonable outcome would cushion Ireland’s economic Brexit fallout, which quickly became clear to most Irish citizens. Now we sit on the edge of another Brexit cliff, 16 days from a potential no-deal exit.

Yesterday, the ESRI spelt out the grim fallout from such an eventuality. The Taoiseach responded by saying it was not good news but we were not headed for bust. Then we learned the no-Brexit plan smacks of saying “sure, it’ll never happen at all”.

Editors note: Gold will again be an important way for people to protect their investments and savings in the inevitable boom and bust cycle.

News and Commentary

Gold futures retreat from March highs as U.S. stocks and yields (MorningStar.com)

Gold retreats as dollar rebounds, risk appetite grows (BRecorder.com)

World stocks rebound, U.S. yields above 15-month lows (BRecorder.com)

Russia adds more than 1,000,000 ounces of gold to country’s vast stockpile (RT.com)

China, Europe slowdown’s scale to determine impact on Fed policy: Evans (Reuters.com)

Source: Jim Willie via GoldSeek.com

GLD Fund: Divergence Signals Shortage (GoldSeek.com)

Gold Set To Shine – Grandich (PeterGrandich.com)

SWOT Analysis: Hedge Funds Boosting Their Long Position on Platinum (GoldSeek.com)

U.S. should do a ‘soft’ default on its debt by devaluing dollar (FoxBusiness.com)

Europe is glued to energy-rich Russia (DavidMCWilliams.ie)

Gold Prices (LBMA PM)

26 Mar: USD 1,315.25, GBP 993.15 & EUR 1,162.02 per ounce

25 Mar: USD 1,319.35, GBP 1001.39 & EUR 1,165.82 per ounce

22 Mar: USD 1,311.10, GBP 998.80 & EUR 1,159.41 per ounce

21 Mar: USD 1,317.30, GBP 1002.99 & EUR 1,155.80 per ounce

20 Mar: USD 1,303.00, GBP 985.07 & EUR 1,147.81 per ounce

19 Mar: USD 1,308.35, GBP 985.06 & EUR 1,152.53 per ounce

Silver Prices (LBMA)

26 Mar: USD 15.44, GBP 11.66 & EUR 13.65 per ounce

25 Mar: USD 15.52, GBP 11.77 & EUR 13.72 per ounce

22 Mar: USD 15.46, GBP 11.75 & EUR 13.68 per ounce

21 Mar: USD 15.54, GBP 11.85 & EUR 13.64 per ounce

20 Mar: USD 15.32, GBP 11.58 & EUR 13.49 per ounce

19 Mar: USD 15.41, GBP 11.61 & EUR 13.57 per ounce

Recent Market Updates

– ‘No Deal’ Brexit Risk Impacting UK and Irish Economies – Gold Gains On Recession Concerns

– America’s “Debt Crisis Is Coming Soon”

– Russia Buys 1 Million Ounces Of Gold In February – Become Your Own Central Bank

– 5 Ways to Prosper In the Coming Crisis – Goldnomics Podcast

– Deutsche Bank and Commerzbank May Become EU’s “Too Big To Fail” Bank

– Happy Saint Patrick’s Day from GoldCore

– 188 Internet Shutdowns In 2018 Show Why Physical Gold Is Ultimate Protection

– Buy Gold as Basel III Means “Central Banks and Banks Are Going To Be Buying Gold”

– Invest In Gold Or Bitcoin – Which Is The True Store Of Value?

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Truly amazing how the South African government is indifferent to gold..the main driver of their economy

(courtesy Bloomberg)

Indifferent to price suppression, South Africa remains a rich country insisting on being poor

Submitted by cpowell on Wed, 2019-03-27 13:39. Section: Daily Dispatches

Bell Tolls for Gold Mine That Once Powered South African Economy

By Felix Njini

Bloomberg News

Wednesday, March 27, 2019

The final demise of South Africa’s gold industry came a step nearer on Wednesday with the announcement that Sibanye Gold Ltd. won’t extend the life of Driefontein, once the biggest mine on the continent.

Last year the mine, more than 2 miles (3,200 meters) deep, produced about 300,000 ounces of gold, just a fifth of its peak output two decades ago. Now Sibanye will wind down Driefontein’s operations within 10 years, with plans to cut thousands of jobs as it shuts unprofitable shafts.

…

South Africa’s gold industry employs just over 100,000 people, less than a fifth of the number that used to drive the apartheid economy. With most of the nation’s gold operations unprofitable, more job cuts are inevitable. Moreover, the geological challenges faced by the world’s deepest mines saw fatalities at Sibanye’s gold operations soar last year. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-03-27/sibanye-s-driefontein…

* * *

end

Brexit, Gold Tier 1, QFC Stay Rules and MIFID II

To all of Harvey’s quite amazing group of followers, please apologize for e-mailing any of you. The “but” is because so many of you are tuned in more than me, I thought maybe someone could take the thought to a higher level. It has to do with Brexit, Gold Tier 1, QFC Stay Rules and MIFID II.

Although lengthy but maybe very significant. Tier 1 collateral of physical allocated, segregated, 99.99% assayed Gold just may be the bull’s eye after all.

The first link below came into effect just after January 1, 2019. The 2nd and 3rd links below came out just prior to Brexit in June 2016. They all deal with “Covered” QFC’s that are “centrally cleared” through an exchange. For Brexit 2016, the UK had just recently passed this ruling relating to QFC’s that are “covered & centrally” cleared. It brings back memories to me of the post-Brexit trading after the June 2016 vote on how the markets all recovered miraculously. This time around with so many institutions that have moved funds out of the UK, it makes me wonder if this time around the markets will be so lucky if a long Brexit delay is not agreed to before March 29. The European Union, a single political and economic bloc, has faced multiple challenges since 2016 that brought its viability into question not to mention China and Russia gaining so many inroads into Eurasian trade with European trade with US in decline led by Germany also appearing to lead the way south in economic activity in Europe. If after March 29, Brexit puts the fear that the U.K. actually leaves the bloc, it remains to be seen whether the EU still has the ability to withstand more shocks. Not even Q-Anon and MAGA sheeples will be able to keep from focusing on these shocks. And whereas most analyst appear to believe that Brexit will never happen, if along Brexit delay does not occur markets will react sharply.

https://www.federalreserve.gov/newsevents/press/bcreg/tarullo-opening-statement-qfr-20160503.htm

http://www.bloomberg.com/news/articles/2016-05-03/fed-expected-to-drag-hedge-funds-into-plan-to-halt-next-lehman (Unfortunately the Bloomberg link now requires subscriber access.)

As March 29 is significant again in Brexit as well as in reclassifying physical gold as Tier 1, maybe there is something significant in the protocol that will affect non-centrally cleared derivatives which in the US and UK have grown significantly since 2016. Now as of January 1, 2019 in the U.S. and June 106 in the UK, any and all “centrally” cleared QFC’s with ‘covered” counterparties in in effect. “Covered” institution are global systemically important banking organizations. “Centrally” cleared QFC’s of course are cleared through the ISDA system for all to see. These rulings prevents a “take your money from your counterparty and run” causing bankruptcy and market chaos whereas all centrally cleared QFC’s appear to have a 24-48 hour hold on allowing the “covered” winning entity from collecting from its “covered” losing counterparty if they can secretly enter a resolution proceeding and permit the transfer of the relevant obligations under the QFC to the solvent party

out of the public’s view in order to prevent a crash yet simultaneously redistribute assets. By hell or high water behind the curtain they will force, steal, threaten, or otherwise convince that losing counter party to enter into stay and transfer provisions even though the losing party hasn’t formally declared bankruptcy. The end result is making deals behind the table out of the public’s view preventing market chaos like we had in Lehman.

But to my knowledge because MFID ii in the Europe its own mammoth set of OTC Derivatives and CCP regulations are only 58% implemented in EU. MIFID ii applies to centrally cleared derivatives that unlike other financial instruments, have never really had a product identifier. MIFID ii assigns an identifier “ISIN” that makes “all” centrally cleared OTC derivatives easy to regulate by authorities, and market participants to identify collateral and thereby accurately re-price risk for “all” OTC centrally cleared derivatives. CCPs will be required to have a substantial minimum amount of “skin in the game.” Also relating to MIFID ii, in January 2018, the LBMA flatly rejected that OTC Gold would be included in that MFID II legislation. It makes me wonder if those same parties in the centrally cleared QFC’s have their eye on physical gold at the LBMA or elsewhere knowing behind the door resolutions will be made that permit the transfer of the relevant obligations under the QFC to the solvent party all the while gold is simultaneously getting Tier 1 status.

https://www.itiviti.com/insights/mifid-ii-turning-challenges-opportunities

It also makes we wonder if March 29 Brexit date could actually see a plethora of CCP’s in Europe, US. And UK whose QFC’s are notcentrally cleared take some swift action in the market after hard Brexit is confirmed without further delays. “In the first quarter of 2015, banks began reporting their volumes of cleared and non-cleared derivative transactions, as well as risk weights for counterparties in each of these categories. In the fourth quarter of 2018, 39.8 percent of banks’ derivative holdings were centrally cleared (see table 12). https://www.occ.gov/topics/capital-markets/financial-markets/derivatives/pub-derivatives-quarterly-qtr4-2018.pdf That means 60.1% of US financial institutions’ $176T in derivatives are not centrally cleared and do not have to abide by Fed QFC’s rules or MIFID ii guidelines. Considering in the US that the amount in non-centrally cleared derivatives of about $100T and centrally cleared of about $76T are about the same as in June 2016 and the current state of the EU banking system, some real havoc may ensue for those failing institutions with a Brexit trigger.

Tier 1 collateral of physical allocated, segregated, 99.99% assayed Gold just may be the bull’s eye after all.

Kevin Wallien

end

Why you invest in gold

(courtesy Simon Black)

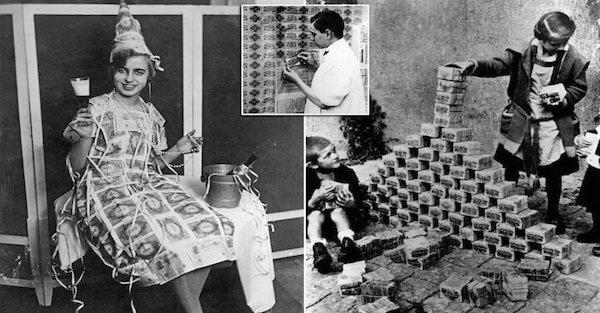

If Donald Trump Is The King Of Debt, These Guys Were The Kings Of Inflation

Authored by Simon Black via SovereignMan.com,

Maximilian Bern had saved up 100,000 German marks for what should have been a modest, but comfortable retirement.

But in 1923, he withdrew every last cent, and spent it all on one purchase: a subway ticket.

He rode around his city one last time before returning home, and locking himself in his home, where he died.

He didn’t kill himself. Hestarved to death… simply because he could no longer afford food. A single egg at the market would cost millions of marks, more than Maximilian Bern had saved over his entire life.

This was one of the most famous episodes of hyperinflation, certainly in modern history.

In the wake of World War One, Germany (known as the Weimar Republic) was completely broke.

The War to end all Wars had bankrupted them; and on top of losing the war, Germany was forced to make ‘reparation payments’ to the victors, including France, the UK, etc.

That took Germany’s overall war debt to impossible levels. So in a feeble attempt to keep the economy afloat and meet its war debt obligations, the German government printed massive amounts of paper money.

Prior to World War I, one US dollar was worth 4.2 German marks.

By 1923, a single US dollar was worth 4.2 TRILLION marks.

We’ve seen this in our own lifetime in places like Zimbabwe, and now Venezuela.

I remember the first time I went to Venezuela the official exchange rate was four bolivars to the US dollar—and the black market rate was eight to one.

The next time I went it was hundreds, then thousands and then tens of thousands of bolivars to just one US dollar.

Around two years ago when I was in Caracas, I changed a few hundred dollars and received an entire suitcase full of money in return. (I didn’t get to keep the suitcase).

The rate of inflation now in Venezuela was as high as 1.6 million percent last year. It’s difficult to even imagine what that means.

But we’ve all heard these horror stories of hyperinflation. Everyone seems to understand the horrible effects it has on the economy and individuals.

But somehow we’re supposed to believe that a little bit of inflation is somehow good for the economy. I find that absurd.

The Federal Reserve tries to keep the inflation rate between 2% and 3% per year. That might seem like chump change, but it adds up.

Even John Maynard Keynes, whose works underpin the foundation of modern central banking, once wrote:

“By continuing the process of inflation governments can confiscate secretly and unobserved an important part of the wealth of their citizens.”

It’s so subtle because it only steals a little at a time from you, over the course of many years.

But again, over time, it adds up.

As we’ve seen over the last couple decades, wages have not kept pace with inflation. So year after year, the average workers loses a little bit of prosperity.

1-2% per year doesn’t really matter. A decade or two of this, however, really has an impact.

We keep hearing these Bolshevik politicians calling for a Wealth Tax. They obviously fail to realize that a wealth tax already exists. It’s called inflation.

Ironically, Keynes continued to write about inflation, saving, “And while the process [of inflation] impoverishes many, it actually enriches some.”

And that’s true. Back in Germany’s hyperinflation days, there were a handful of sophisticated people who saw the writing on the wall. They knew that the government could never pay its debts, and that they would print money and debase the currency.

These guys set up their investments in a way to actually profit from hyperinflation.

Donald Trump famously referred to himself during the 2016 Presidential campaign as the “King of Debt” because he has been able to profit by borrowing money.

These investors in the Weimar Republic were known as the Kings of Inflation. And Hugo Stinnes was the King of Kings.

Stinnes had positioned himself perfectly for when hyperinflation hit.

He borrowed vast amounts of German marks and poured them into his coal, steel, and shipping companies.

He also kept gold in Switzerland, and made investments in foreign markets.

When hyperinflation hit, Stinnes was able to pay back his debts with the massively devalued German mark.

But Stinnes’ hard assets weren’t affected by the hyperinflation. They held their value. His businesses and investments flourished, making him one of the wealthiest men in the world.

This is just a reminder that, no matter what happens in financial markets or the global economy, there are always winners and losers.

And to continue learning how to ensure you thrive no matter what happens next in the world, I encourage you to download our free Perfect Plan B Guide.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

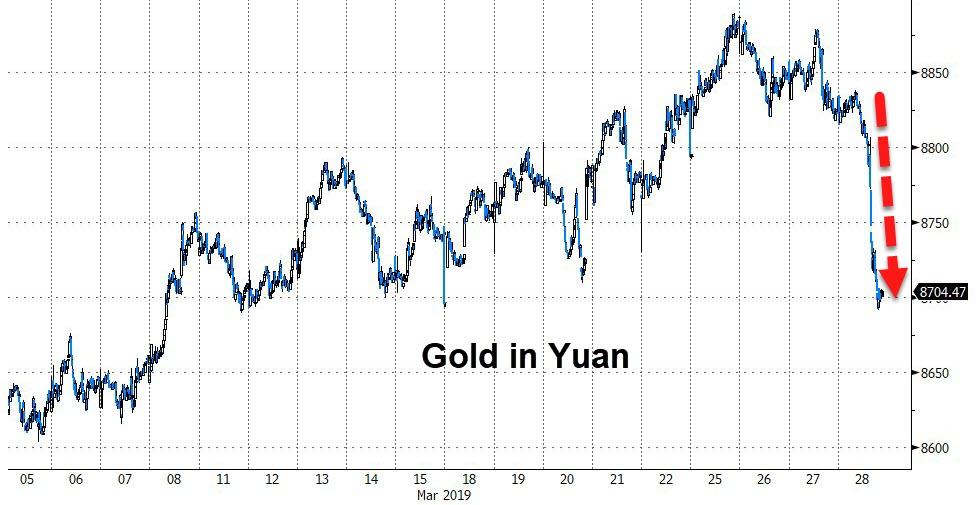

Gold was smacked $22 from top to bottom overnight and this morning. It was a classic paper derivative raid on the gold price, which was implemented after the large physical gold buyers in the eastern hemisphere had closed shop for the day. This is what it looks like visually:

As you can see, as each key physical gold trading/delivery market closes, the price of gold is taken lower. The coup de grace occurs when the Comex gold pit opens. The Comex is a pure paper market, as very little physical gold is ever removed from the vaults and the paper derivative open interest far exceeds the amount gold that is reported to be held in the Comex vaults (note: the warehouse reports compiled by the banks that control the Comex are never independently audited).

Today technically is first notice day for April gold contracts despite March 29th as the official designation. Any account with a long position that does not intend to take delivery naturally sells its long position in April contracts. Any account not funded to accommodate a delivery is liquidated by 5 p.m. the day before first notice. This dynamic contributes to the ease with which a paper raid on the gold price can be successfully implemented.

In all probability the price of gold (June gold basis) will likely not stay below $1300 for long. China’s demand has been picking up and India’s importation of gold is running quite heavy for this time of the year. Soon India will be entering a seasonal festival period and gold imports will increase even more. Today’s price hit will likely stimulate more buying from India on Friday.

end

* * *

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7344/

//OFFSHORE YUAN: 6.7450 /shanghai bourse CLOSED DOWN 27.78 POINTS OR 0.92% /

HANG SANG CLOSED UP 46.96 POINTS OR 0.16%

2. Nikkei closed //UP 344.97 POINTS OR 1.61%

3. Europe stocks OPENED MIZED

/USA dollar index RISES TO 97.14/Euro FALLS TO 1.1228

3b Japan 10 year bond yield: FALLS TO. –.09/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.31/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 58.52 and Brent: 67.05

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO –.09%/Italian 10 yr bond yield UP to 2.50% /SPAIN 10 YR BOND YIELD DOWN TO 1.08%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.59: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.80

3k Gold at $1304.25 silver at:15.20 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 31/100 in roubles/dollar) 65.16

3m oil into the 58 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.31 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9958 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1181 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.09%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.36% early this morning. Thirty year rate at 2.81%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.5897

Stocks Slide As Rate Drop Continues, Dollar Spikes

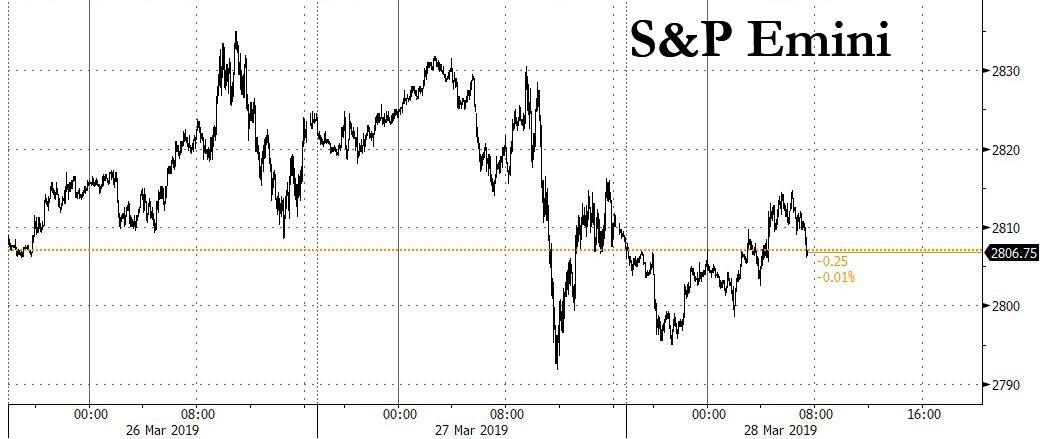

While global markets showed tentative signs of a rebound in sentiment in early Thursday trading, as the global bond rally showed signs of easing, with Treasuries turning lower alongside most sovereign debt in Europe, this quickly reversed around the time US traders start showing up at their desks, and European stocks faded almost all of their earlier gains, while U.S. equity futures drifted, once again within striking distance of the 2,800 key level.

After the 10-year US Treasury yield crept back above 2.37% during Asia trading, a renewed flight to safety saw the yield on the benchmark paper slide in the red again, as global bond yields continued to spiral lower on Thursday as recession fears fed expectations of more policy easing by major central banks, with the 10Y trading below 2.36% at last check.

After shares slumped in Japan and fell in China and South Korea at the start of trading, contracts on the S&P 500 pointed to a modestly red open fading an earlier rebound, while the Stoxx Europe 600 paring earlier gains of as much as 0.4 percent, with banking stocks the regional benchmark’s weakest sector. The Stoxx 600 was steady as of 11:36am in London, with the index tracking banking stocks dropping 1.3% following fresh turmoil in Sweden over money-laundering, while healthcare gauge climbs 0.8%. Rating agency S&P became the latest to cut its euro zone growth forecasts while a Reuters report that the United States and China had made progress in all areas in trade talks seemed to bolster sentiment a little, though sticking points still remained and there was no definite timetable for a deal.

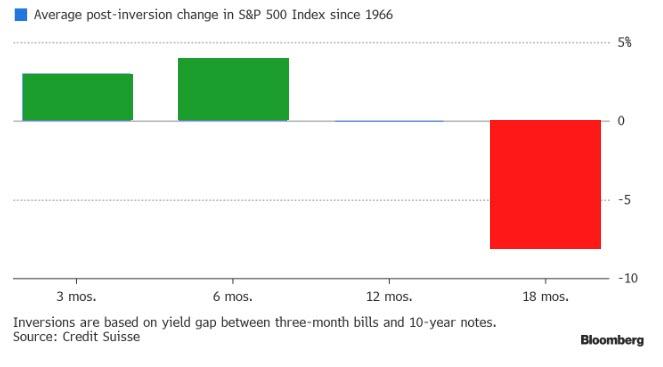

Worries that the inversion of the U.S. Treasury curve signaled a future recession only deepened as 10-year yields fell to a fresh 15-month low at 2.34% on Wednesday. “We think that the ongoing flattening, or outright inversion, of the curve is a bad sign for equities, as it usually has been in the past,” said Oliver Jones, markets economist at Capital Economics. “Arguments that the yield curve is no longer a reliable indicator seem to resurface every time it inverts, only to be subsequently proved wrong.”

Meanwhile, Chinese Premier Li said world economy faces slower growth and increasing uncertainties, while he added that some fluctuation in quarterly economic growth this year cannot be ruled out. Chinese Premier Li further commented that China must achieve goal of tax and fee cuts this year, while it will also publish a revised negative list for foreign investors and will treat domestic and foreign companies equally. Separately, adding that changes in their economy in March have exceeded expectations, adds that China’s economic operations were steady in Q1.

US administration official said US and China made progress in all areas of trade talks but enforcement and intellectual property remain sticking points, while China was also said to have made proposals on trade including tech transfers that are more specific and with wider scope than ever before. However, the official added that there is no specific timeframe for a trade deal with talks to conclude anytime from April-June and whether to lift current US tariffs on China is a sticking point and will be worked out as part of a deal. Subsequently, Chinese Premier Li said China must protect IP to support China’s transformation, adding that he does not think there is a trust deficit between US and China.

As the flight to safety accelerated, so did the rise in the dollar, which headed for a fifth gain in six sessions, while Britain’s pound weakened after the U.K. Parliament rejected eight possible options for a new Brexit strategy.

But it was the Turkish lira, one of the currencies at the heart of last year’s emerging market meltdown, which was once again the overnight highlight as plunged as much as 5% against after the central bank unveiled that it had burned through a third of its reserves in 1 month and the attempt to crush shorts had ended, inviting a fresh wave of bears. As Reuters notes, authorities were showing the first sign of easing a draconian squeeze put on international lira traders ahead of local elections this weekend but a day after the country’s stock market also slumped there was little good will. Ugras Ulku at the International Institute of Finance in Washington said the question was, when the dust settles, whether portfolio managers want to continue to invest in Turkey or not “we will have to wait and see,” he said

Elsewhere, hints of rate cuts from New Zealand’s central bank had the desired effect on its currency, which was pinned at $0.6816 after diving 1.6 percent overnight. The Aussie was on the defensive at $0.7090. Draghi’s comments likewise kept the euro back at $1.1250, and left the U.S. dollar a fraction firmer against a basket of its competitors at 96.874. Only the yen held its own thanks to its safe-haven status and firmed to 110.00 per dollar.

The Swiss franc’s surge to a 20-month high hasn’t spooked strategists at Credit Agricole CIB out of their bearish view. The Swiss National Bank is unlikely to tolerate further franc strength, which would threaten policy makers’ battle against deflation, and may rein in the exchange rate via currency interventions, according to the bank

In commodity markets, palladium was the focus of attention after sliding 7 percent on Wednesday as its meteoric rally finally ran into profit-taking. It was down 0.4 percent on Thursday. Gold was relatively sedate at $1,310.85 per ounce. Oil prices nursed modest losses after data showed U.S. crude inventories grew more than expected last week as a Texas chemical spill hampered exports.

Economic data include initial jobless claims and the final print of quarterly GDP. Accenture is due to report earnings.

Market Snapshot

- S&P 500 futures little changed at to 2,811.50

- STOXX Europe 600 up 0.06% to 377.51

- MXAP down 0.4% to 158.73

- MXAPJ up 0.1% to 523.64

- Nikkei down 1.6% to 21,033.76

- Topix down 1.7% to 1,582.85

- Hang Seng Index up 0.2% to 28,775.21

- Shanghai Composite down 0.9% to 2,994.94

- Sensex up 0.9% to 38,457.70

- Australia S&P/ASX 200 up 0.7% to 6,176.08

- Kospi down 0.8% to 2,128.10

- German 10Y yield rose 0.4 bps to -0.077%

- Euro down 0.03% to $1.1241

- Brent Futures down 0.7% to $67.37/bbl

- Italian 10Y yield fell 1.4 bps to 2.1%

- Spanish 10Y yield rose 1.4 bps to 1.07%

- Brent Futures down 0.7% to $67.37/bbl

- Gold spot down 0.1% to $1,308.46

- U.S. Dollar Index up 0.3% to 97.02

Top Overnight News

- Britain’s political standoff over Brexit escalated further, with even Theresa May’s announcement that she’ll quit as prime minister doing nothing to move closer to a resolution

- Federal Reserve Bank of Kansas City President Esther George says it was appropriate to put policy on hold after the central bank’s interest-rate increases last year. Asked if the Fed’s quarter- point hikes in September and December had been mistakes, George replied: “No, I do not think we made a mistake in September. I was one who advocated for a long time concern about low-for-long interest rates”

- Investors dumped Turkish bonds and stocks on Wednesday after the nation orchestrated a currency crunch to prevent the lira from sliding days before an election that will test support for President Recep Tayyip Erdogan’s rule. The cost of borrowing liras overnight on the offshore swap market soared past 1,000 percent at one point on Wednesday

- China’s economy is showing further signs of recovery after months of slowdown, though downward pressures still persist. That’s according to a Bloomberg Economics gauge aggregating the earliest available indicators on market sentiment and business conditions

- U.S. and China have made progress in focus areas under the trade talks, Reuters reports, citing four senior U.S. administration officials. One official said China had come up with proposals on forced tech transfers that went further than in the past in terms of scope and specifics

- The European Central Bank’s chief economist says there needs to be a solid monetary-policy case before officials act to mitigate the side effects of negative interest rates on banks. ECB staff are examining the issue of tiering — where some of banks’ excess reserves are exempt from the lowest rate — but action isn’t a done deal, Peter Praet says

- Thailand’s pro-military party won the most votes in Sunday’s election, authorities confirmed on Thursday, bolstering its claim to legitimacy as it competes with an anti-junta alliance to form a government

Asian equity markets traded mostly negative as the downbeat sentiment rolled over from US where all major indices finished lower amid lingering growth concerns and as the yield curve inversion deepened. As such, ASX 200 (+0.7%) opened subdued but with losses eventually pared by resilience across nearly all sectors, while Nikkei 225 (-1.6%) underperformed and briefly slipped below the 21000 level with selling exacerbated by a firmer currency and rotation into bonds. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (-0.9%) were also cautious with weakness in financials due to earnings in which China’s 2nd largest lender China Construction Bank missed on FY net forecasts and posted its first quarterly Y/Y profit decline since 2015 which doesn’t bode well for the other Big 4 banks to report this week, while China Life Insurance also posted a near-65% drop in FY net. Nonetheless, sentiment in China slightly improved as US and China senior trade negotiators began the latest round of trade talks in Beijing and a Trump administration official suggested progress was made in all areas of trade talks but some sticking points remained. Finally, 10yr JGBs were supported by the negative risk tone in Japan and amid the recent bond market rally as global yields declined in which the US 10yr yield fell to a fresh 15-month low and the Aussie 3yr yield printed its lowest on record, while the results of today’s 2yr auction were also bullish as all metric improved from the prior month, albeit marginally.

Top Asian News

- Sony’s Turnaround Architect Retires as Tech Giant’s Growth Slows

- Guinigundo Sees Flexibility to Consider Philippine Policy Easing

- China’s Economy Shows More Signs of Recovery, Earliest Data Show

- Thai Pro-Military Party Won Most Votes in General Election

Major European indices have gained some traction following a subdued start to the session [Eurostoxx 50 +0.2%] as the region diverges from the downbeat sentiment experienced in Asia. UK’s FTSE 100 (+0.6%) outperforms its peers as the weaker domestic currency bolsters the export-heavy index. Sector-wise, material stocks lead the gains as base metals benefit from recent turnaround in the risk sentiment whilst utility names lag as investors move away from defensive sectors. In terms of notable movers, Swedbank (-3.7%) shares took another hit amid the slew of open investigations in relation to money laundering. As the bank’s AGM gets underway, it announced that CFO Anders Karlsson has replaced Birgitte Bonnesen as acting President and CEO. Company shares are halted until further notice. Elsewhere, chip names remain pressured in a continuation of yesterday’s sell-off after DAX-listed Infineon (-1.1%) announced a profit warning due to rising global tensions.

Top European News

- Iliad Chairman Lombardini Faces French Market-Abuse Case

- Iceland’s Wow Air Says It Has Ceased Operations

- Hochtief Shares Drop After Atlantia Sells a Quarter of its Stake

- Euro Hits 10-Week Low Versus Yen as German Inflation in Focus

In FX, JPY/NZD were the best G10 performers, albeit off best levels as the Usd retains a firm underlying bid in its own right as a safe-haven amidst a tentative and intermittent revival in broad risk appetite. Usd/Jpy is holding above 110.00 within a 110.03-53 range having tested bids/support just ahead of the big figure where decent option expiry interest resides (1 bn) and is back above daily chart resistance between 110.07-12, while Eur/Jpy has also rebounded from sub-124.00 lows and heavy Japanese selling that pushed the cross down through a key Fib (123.81) at one stage. Meanwhile, the Kiwi has regained some composure after its post-RBNZ rout to reclaim 0.6800 status, but Nzd/Usd remains vulnerable following a marked deterioration in NZ business sentiment and expectations according to ANZ’s March survey, which provides more justification for the change in rate guidance towards an ease vs a neutral stance previously. Note, RBNZ Governor Orr is due to orate later on the new framework for monetary policy.

- AUD/EUR – Also weathering a bout of downside pressure relatively well, as the Aussie keeps tabs on the 0.7100 handle vs its US counterpart and remains above 1.0400 against the Nzd, however Aud/Usd could be hampered by a 1 bn expiry ahead of the NY cut along with dovish positioning for next week’s RBA on the notion that the balance of risks could shift towards cutting benchmark rates from a balanced prognosis at present, ala the RBNZ. Meanwhile, the single currency succumbed to spill-over Jpy cross sales vs the Usd that forced the headline pair through recent lows and chart support (at 1.1241), but not much further as it consolidates back above the 76.4% Fib retracement of the 1.1177-1.1448 move.

- GBP/SEK/NOK/CAD/CHF – All lagging their major peers, and especially the Pound, Swedish and Norwegian Crowns. Cable has fallen below a fairly resilient 1.3150 mark following the latest UK Parliamentary votes on Brexit ended with no majority support for any of the 8 options tabled, and in fact resounding rejection in 6 instances, leaving the situation even more uncertain than it was before the HoC took the baton from PM May. Meanwhile, Eur/Nok and Eur/Sek have both bounced further in wake of yesterday’s worse than expected Norwegian jobs data and as Swedbank suffers more investor angst over money laundering allegations, with the former up to 9.7465 and latter at 10.4935 before easing back. The Loonie is also weaker post-data, between 1.3400-30 vs its US rival, with the Franc still somewhat mixed as it pivots 0.9950 vs the Greenback and 1.1200 against the Euro in advance of a speech from SNB’s Maechler that could fan speculation about intervention to curb excess Chf strength/demand.

- DXY – The index has climbed into a higher range after recent declines amidst falling US Treasury yields and deeper curve inversion to probe above 97.000, and from a technical perspective the Buck may be able to overcome residual month end flows that are said to be mildly bearish.

- Brazil’s Economy Minister Guedes said that if the pension reform bill of BRL 1tln passes, interest rates would naturally decline by 2 percentage points. (Newswires)

- New Zealand ANZ Business Confidence (Mar) -38.0 (Prev. -30.9). (Newswires) New Zealand ANZ Activity Outlook (Mar) 6.3 (Prev. 10.5)

In commodities, WTI (-0.6%) and Brent (-0.6%) futures languish following yesterday’s pullback, although the benchmarks remain off worst levels amid an improvement in market sentiment. Despite this week’s builds in API and DoE crude inventories (API +1.9mln, DoE +2.8mln), UBS analysts note that both weekly data and for the year thus far are more bullish than usual. Meanwhile, WSJ reported that Saudi Aramco plans to issue a USD 10bln bond, to be used as part of a payment for their 70% purchase of Sabic which is valued at USD 69.1bln, according to sources. On the OPEC+ front, Russian Energy Minister Novak told RIA newspaper that the OPEC+ Charter could be signed in either May or June. Elsewhere, precious metals are pressured by firmer buck with gold (-0.2%) hovering close to its 50 DMA at 1307/oz. Meanwhile, base metals are faring better, with risk-gauge copper bouncing off lows as the risk appetite supports the red metal.

US Event Calendar

- 8:30am: GDP Annualized QoQ, est. 2.3%, prior 2.6%

- Personal Consumption, est. 2.6%, prior 2.8%

- GDP Price Index, est. 1.8%, prior 1.8%

- Core PCE QoQ, est. 1.7%, prior 1.7%

- 8:30am: Initial Jobless Claims, est. 220,000, prior 221,000; Continuing Claims, est. 1.78m, prior 1.75m

- 10am: Pending Home Sales MoM, est. -0.5%, prior 4.6%; Pending Home Sales NSA YoY, est. -3.0%, prior -3.2%

- 11am: Kansas City Fed Manf. Activity, est. 0, prior 1

DB’s Jim Reid concludes the overnight wrap

Last night saw the most exciting European vote in the U.K. since Bucks Fizz won the Eurovision Song Contest in 1981. MPs spent the evening making their minds up on 8 options in relation to Brexit although as expected no majority was found for any path. The vote occurred soon after Mrs May announced to backbench Conservative MPs that she would step down as PM after her Brexit deal was delivered and would not lead the next stage of negotiations. This was aimed at increasing the chances that her WA (MV3) can rise like Lazarus and pass, although as we’ll see later the speaker and the DUP have made it more difficult for the government to try again. Anyway, back to the votes, it is perhaps easiest to list the options available and show the scores on the doors in order of most votes in support of a particular pathway. There were no nul points.

- Putting any deal agreed to a second referendum. Defeated 295-268.

- Permanent customs union. Defeated 272-264.

- Labour’s plan (which includes a permanent customs union, but also involves alignment in a number of other areas). Defeated 307-237.

- Common Market 2.0. (stay in the single market, negotiate a customs union “at least until alternative arrangements” to avoid a hard border in Ireland have been found. Defeated 283-188.

- Revoking Article 50 if a deal has not been ratified and the House does not approve leaving without a deal. Defeated 293-184.

- Leaving with no-deal on 12 April. Defeated 400-160.

- Version of the Malthouse plan (UK offers EU payments for two years in return for market access). Defeated 422-139.

- Seek to remain a member of the EEA and reapply to join EFTA (so single market but not customs union). Defeated 377-65.

In terms of votes in favour, the amendment for a second referendum led the pack, while the customs union proposal was the closest vote, losing by a margin of only 8 votes. Indeed, both amendments achieved more positive votes than May’s deal did the second time round, when it achieved only 242 yes-votes. The pound depreciated -0.58% versus the dollar after the votes were taken, as the odds of continued stalemate and an eventual general election seem to be rising. The plan now is for a possible MV3 on May’s deal before the end of the week, followed by, assuming MV3 fails again, an additional set of indicative votes on Monday. Speaker Bercow said he would eliminate the less popular options and leave only the top few, to see if a majority can be achieved from a shorter list.

In terms of whether there’ll be a third meaningful vote soon, it’s obviously in the PM’s plan this week. However, this will have to circumnavigate Speaker Bercow’s further intervention that said any further vote would still have to comply with his ruling from March 18 that the House couldn’t vote on the same motion again and would require some form of change. Interestingly, he said that the government couldn’t seek to get round this using a ‘paving motion’, which blocks off a route the government could have possibly used to get round his ruling. Also the DUP said (late last night) at this stage they still can’t support the deal. Whether that changes or whether that just means an abstention is not clear although DUP Dodds said that with regards to the Union they don’t abstain. Before this there were signs that Prime Minister May is making some progress in winning over MPs to the deal, with a number of Conservative MPs who opposed the deal on the last meaningful vote saying they would now be willing to support the deal (generally out of a fear from pro-Brexit MPs that any alternative would only be a softer Brexit than the PM’s deal, or possibly no Brexit at all). However, without the DUP they will likely need a fair amount of Labour MPs on their side. Also, one wonders that with Mrs May now going, will loyal remain Tory MPs be fearful of a harder Brexit replacement PM and decide to vote against it to stop a Brexit that might then get handed over to the hard Brexiteers.

Outside of Brexit, the biggest story was the interaction of Draghi’s comments, European bank stocks, deposit tiering, and a big rates rally. On page 6-7 of our recent “How to fix European banks… and why it matters” (see here ) we explained how strange it was that of all the central banks operating with negative rates, the ECB were the only one not offering deposit tiering. Implementing this was a small part of our policy recommendation list. Recent news hasn’t suggested they were close to this, but things moved quite quickly yesterday. First, we had an early morning Reuters story which said that the ECB were looking at the idea of a tiered deposit rate and then at lunchtime Draghi said that “if necessary, we need to reflect on possible measures that can preserve the favourable implications of negative rates for the economy, while mitigating the side effects, if any.” The ECB have been worried that moving to such a system would lead to concerns that this signals rates staying low or negative for much longer. To be fair, this was what happened yesterday as Bunds rallied -6.6 bps to -0.081% with the front end of the curve flattening even more. Euribor futures for December 2019 and 2020 rallied by -4 and -7bps to their lowest levels ever, leaving the curve as flat as a pancake through the next six quarters. A 10bps hike is not fully priced in until March 2021.

This morning ECB’s Chief Economist Peter Praet has said that the tiered rate would need a monetary-policy case while adding that the lending conditions are not impaired and there is no need to rush for tiering. On TLTRO, he said that the ECB could decide on pricing at its June meeting while adding that the conditions could change during the program.

European banks made strong advances on the news though, albeit on a risk-off day with the STOXX Banks index up +1.85% with Italian banks +1.59%. Another side effect was a rally in 10yr BTPs, -1.4bps lower on the day and -10.2bps from the morning highs. Delving deeper into the bond move we also saw 10-year bund yields falling below 10-year Japanese government bond yields for the first time since October 2016. However, this morning in Asia the yield on 10yr JGBs (-1.2bps to -0.091%) is again below that of 10yr bund as the race to the bottom continues. In the US, yields continued to rally yesterday as well, with 2- and 10-year yields dropping -6.6bps and -5.7bps, respectively. That meant the 2s10s curve steepend again to 16.3bps, back to slightly above its year-to-date average. The 2yr and 10yr treasury yields are both down a further c. -1.2bps this morning with 10yr treasury yields now hovering at 2.355%, the lowest since December 2017.

Overnight, Asian markets are following Wall Street’s lead with the Nikkei (-1.45%), Hang Seng (-0.08%), Shanghai Comp (-0.26%) and Kospi (-0.78%) all down. Elsewhere, futures on the S&P 500 are down -0.24% while the Japanese yen is up +0.32%, alongside most G10 currencies.

Back to Mr Draghi, he also talked about inflation and said “we therefore remain confident that the sustained convergence of inflation to our aim has been delayed rather than derailed”. He nevertheless maintained his stance that “uncertainty remains high” and “the risks remain tilted to the downside.” The euro weakened after the speech, falling -0.17% versus the dollar. Staying with FX, we also saw the Swiss Franc climb to its strongest level against the euro since July 2017 yesterday to 1.1195. DB’s strategists don’t think intervention to prevent appreciation is likely until we approach 1.10, so there’s a bit more room to run before that becomes a risk.

It was a bad day for Turkish assets, with the BIST 100 index closing down -5.67% yesterday, its biggest fall since July 2016, while Turkish bond yields also rose dramatically, with local 10-year yields up +114bps to 17.93% and USD up +19.3bps to 7.74%. The overnight implied yield continued to blow out, rising to as high as 1,350% before ending the day at 750%. The market turmoil comes before local elections on Sunday, with the government likely hoping to maintain FX stability ahead of the votes. This morning the Turkish Lira is -1.94% as sentiment continues to be weak

The S&P 500, DOW, and NASDAQ retreated -0.46%, -0.13%, and -0.63% respectively. All sub-sectors fell except for industrials, which were boosted by a positive day for airlines (+1.92%). Southwest, a major operator of the grounded Boeing 737 Max, announced that the impact on first quarter revenue would be smaller than feared at only $150million. The dollar strengthened +0.19%, weighing on multinationals and exporters, after US trade data showed a smaller-than-expected deficit for January. The bilateral deficit with China narrowed by $2.4bn to -$34.4bn, providing a somewhat more positive backdrop as USTR Lighthizer and Treasury Secretary Mnuchin travel to Beijing today for trade negotiations.

In spite of the strong performance from financials, European equity markets fell back before the close, in line with a falling US market, with the STOXX 600 paring their gains to close flat. The DAX, CAC, and FTSE 100 also all closed flat on the session, although southern European equities put in a stronger performance, with the FTSE MIB (+0.26%) and the IBEX 35 (+0.51%) outperforming. This came despite unconfirmed reports in Italian newspaper Il Sole that the Italian government plans to lower its 2019 growth forecast to 0.1% and raise its deficit to 2.4% of GDP.

Looking at the European data, French consumer confidence was in line with expectations at 96, a seven-month high, but the readings from Italy were more negative, with the consumer confidence indicator falling to 111.2 (vs. 112.5 expected) to reach its lowest since August 2017, while the manufacturing confidence indicator fell to 100.8 (vs. 101.4 expected), its lowest since February 2015. The UK also saw some negative data, with the CBI’s reported retail sales index falling to -18 (vs 4 expected) in March, its lowest since October 2017.

In terms of the day ahead, we have a number of data readings, including German March CPI data, Eurozone M3 money supply data for February, and the final Eurozone consumer confidence reading for March. From the US, we’ll get the third reading of Q4 GDP, personal consumption and core PCE, along with pending home sales for February, the Kansas City Fed’s manufacturing activity index for March and weekly initial jobless claims. From central banks, both Federal Reserve Vice Chair Quarles and Vice Chair Clarida will be speaking, along with Bowman, Bostic and Bullard. From the ECB, we have Vice President de Guindos, while Villeroy de Galhau, Knot and Nowotny will also be making remarks.

Last but not least, we have the aforementioned Lighthizer and Treasury Secretary Mnuchin trip to Beijing today for trade negotiations.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 27.78 POINTS OR 0.92% //Hang Sang CLOSED UP 46.96 POINTS OR 0.16% /The Nikkei closed UO 344.97 POINTS OR 1.61%/ Australia’s all ordinaires CLOSED UP 0.63%

/Chinese yuan (ONSHORE) closed DOWN at 6.7344 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 58.52 dollars per barrel for WTI and 67.05 for Brent. Stocks in Europe OPENED MIXED

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7344 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7450 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA

I will believe this when I see Xi make these statements. Strangely the markets did not respond on these “major” concessions:

i) movement on forced technology transfers

ii) movement on China ready to engage the west’s cloud computing

(courtesy zerohedge)

Beijing Reportedly Open To “Major Concessions” On Technology Transfers, Cloud Computing

President Trump can still hammer crude prices lower with a tweet, but unfortunately for Larry Kudlow and Steven Mnuchin, optimistic trade headlines just don’t pack the same market “oomph” that they once did. Proof of this arrived Thursday morning, when a pair of ostensibly bullish stories from Reuters and WSJ failed to revive the market’s appetite for risk, even as anonymous US officials teased what they heralded as a “major concession” from Beijing on forced technology transfers, and a top Chinese official told a group of American tech CEOs about a proposal to lift restrictions on foreign cloud-computing companies.