APRIL 29/OPTIONS EXPIRY TOMORROW ON LBMA/OTC CONTRACTS: GOLD DOWN $7.00 TO $1279.70//SILVER DOWN 13 CENTS//AGAIN NO GOLD ENTERS THE GOLD ARENA BUT A HUGE 69,365 OZ LEAVE//GOLD OZ STANDING WITH ONE DAY TO GO: 22.23 TONNES AGAINST 8 TONNES OF REGISTERED GOLD//USA LEAVES THE CHINESE TRADE TALKS //CHINA HAS A MASSIVE 8.1% OF NON PERFORMING LOANS//GOLDMAN SACHS NOW BASHES TURKEY AND STATES THAT THE LIRA WILL FALL TO 6.25 TO ONE//BART CHILTON FORMER COMMISSIONER OF THE CFTC AND A GOOD FRIEND DIES SUDDENLY//HUGE SWAMP STORIES FOR YOU TONIGHT//

GOLD: $1279.70 DOWN $7.00 (COMEX TO COMEX CLOSING)

Silver:$14.92 DOWN 13 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1279.50

silver: $14.90

TOMORROW, WE HAVE EXPIRY ON THE BIG ONES OTC/LONDON LBMA CONTRACTS FOR GOLD/SILVER. WE MIGHT HAVE A LITTLE WEAKNESS IN THE MORNING AND THEN CLEAR SAILING.

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 118/201

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,284.900000000 USD

INTENT DATE: 04/26/2019 DELIVERY DATE: 04/30/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 199

657 C MORGAN STANLEY 2 661 C JP MORGAN 118

686 C INTL FCSTONE 2

991 H CME 81

____________________________________________________________________________________________

TOTAL: 201 201

MONTH TO DATE: 7,149

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 201 NOTICE(S) FOR 20100 OZ (0.6251 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7149 NOTICES FOR 714900 OZ (22.23 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 775 for 3,875,000 oz

IN SILVER THE COMEX OI FELL BY A HUMONGOUS SIZED 11,845CONTRACTS FROM 212,944 DOWN TO 201,099DESPITE FRIDAY’S 12 CENT RISE IN SILVER PRICING AT THE COMEX. , WE DID HAVE CONSIDERABLE LIQUIDATION OF SPREADERS WITH TODAY’S READING AND IT HAD A HUGE EFFECT ON PRICE. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGEAMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERYSTRONGSIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR APRIL, 2155 FOR MAY, 0 FOR JUNE, 894 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 3049 CONTRACTS. WITH THE TRANSFER OF 3049CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3049 EFP CONTRACTS TRANSLATES INTO 15.24 MILLION OZ ACCOMPANYING:

1.THE 12 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

36,399 CONTRACTS (FOR 20TRADING DAYS TOTAL 36,399 CONTRACTS) OR 181.99MILLION OZ: (AVERAGE PER DAY: 1819 CONTRACTS OR 9.098 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 181.99 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 25.99% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 749.79 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 11,845 DESPITE THE 12 CENT RISE IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGESIZED EFP ISSUANCE OF 3049CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE LOST A HUGE SIZED:8796 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3049 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 11,845OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 12 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $15.05 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.008 BILLION OZ TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0NOTICE(S) FOR nil OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.875 MILLION OZ/

HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 5498 CONTRACTS, TO 429,551 DESPITE THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $9.20//FRIDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6931 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 6931 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 429,551. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1433 CONTRACTS: 5498 OI CONTRACTS DECREASED AT THE COMEX AND 6931EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1433 CONTRACTS OR 143,300 OZ OR 4.457 TONNES. FRIDAYWE HAD A GAIN IN THE PRICE OF GOLD TO THE TUNE OF $9.20.…AND WITH THAT RISE, WE HAD A GOOD GAIN IN TONNAGE OF 8.696 TONNES!!!!!!.??????????????????????????????????????????

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 138,405 CONTRACTS OR 13,840,500 OR 430.49 TONNES (20 TRADING DAYS AND THUS AVERAGING: 6920 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAYS IN TONNES: 430.49 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 430.49/3550 x 100% TONNES =12.12% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1803.88 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 5,498 DESPITE THE GAIN IN PRICING ($9.20) THAT GOLD UNDERTOOK FRIDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6931 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6931 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 2796CONTRACTSIN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6931 CONTRACTS MOVE TO LONDONAND5498CONTRACTS DECREASEDAT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 4.457 TONNES). ..AND THIS STRONG DEMAND OCCURRED WITH A RISE IN PRICE OF $9.20 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 201 notice(s) filed upon for 20100 oz of gold at the comex.

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $7.00 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 746.69 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 13 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 311.979 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A HUMONGOUS SIZED 11,845 CONTRACTS from 212,944 DOWNTO 201,099 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..TODAY,IT LOOKS LIKE OUR SPREADERS SAW CONSIDERABLE ACTION WITH RESPECT TO THEIR USUAL AND CUSTOMARY LIQUIDATION, BUT TODAY NO EFFECT ON THE PRICE OF SILVER

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER AN ACTIVE DELIVERY MONTH. THUS SILVER HAS THE ACTIVE MONTH OF MAY COMING UP AND THUS SPREADERS DO THE FOLLOWING:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 2155 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 894 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3049 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 11,845 CONTRACTS TO THE 3049OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG LOSS OF 8380 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 43.98MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.875 MILLION OZ FOR APRIL.

RESULT: A HUMONGOUS SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 12 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A SMALL SIZED 3049 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ FRIDAY NIGHT:

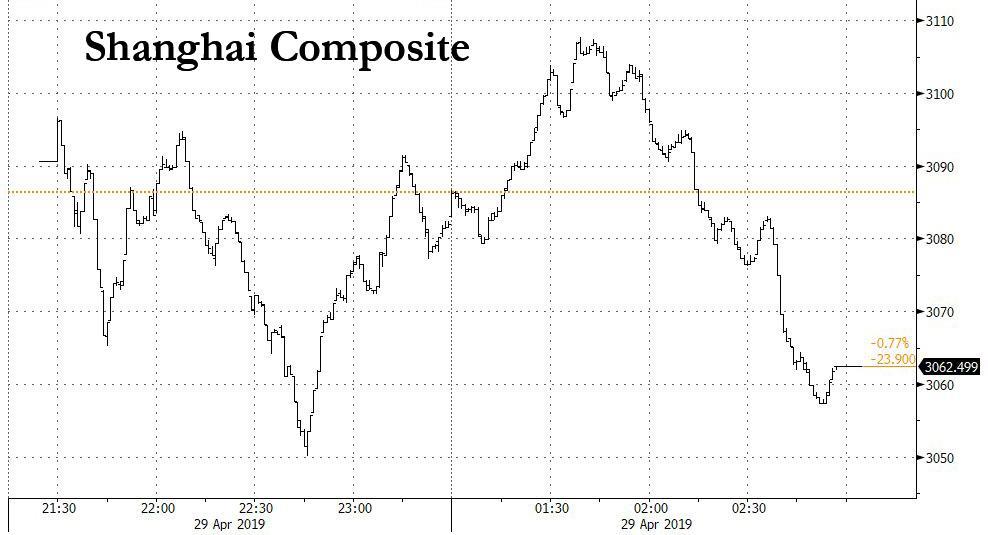

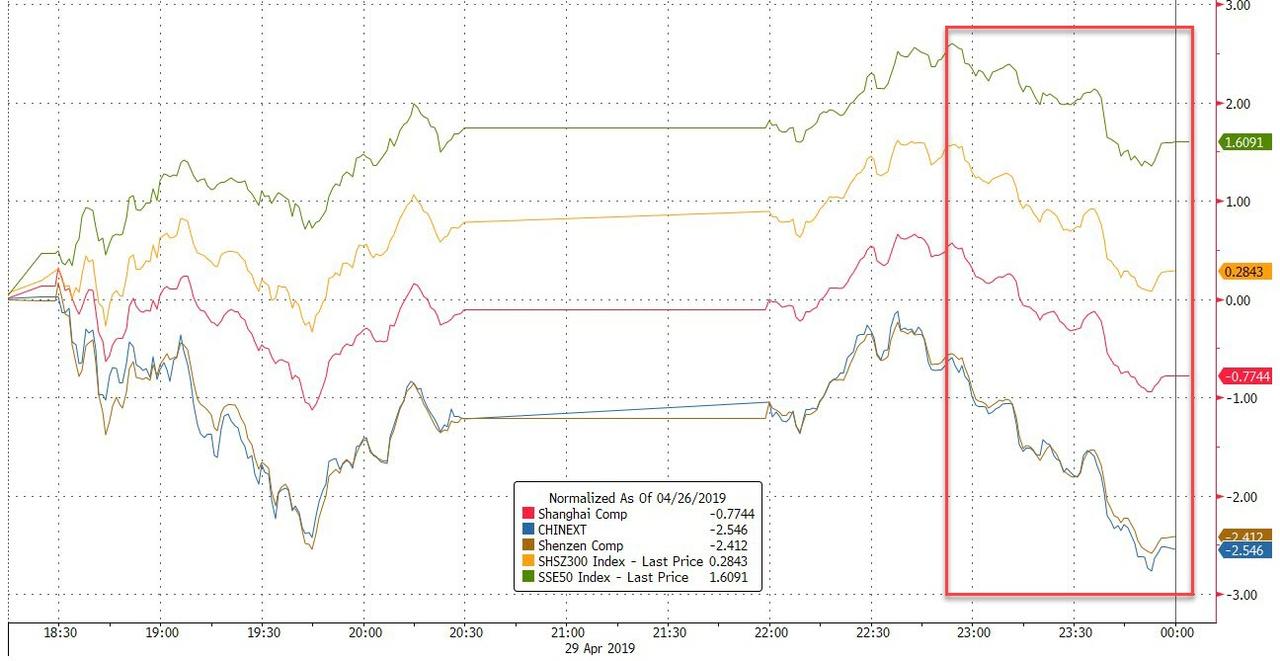

SHANGHAI CLOSED DOWN 23.90 POINTS OR 0.77% //Hang Sang CLOSED UP 187.80 POINTS OR 0.97% /The Nikkei closed/ Australia’s all ordinaires CLOSED DOWN .36%

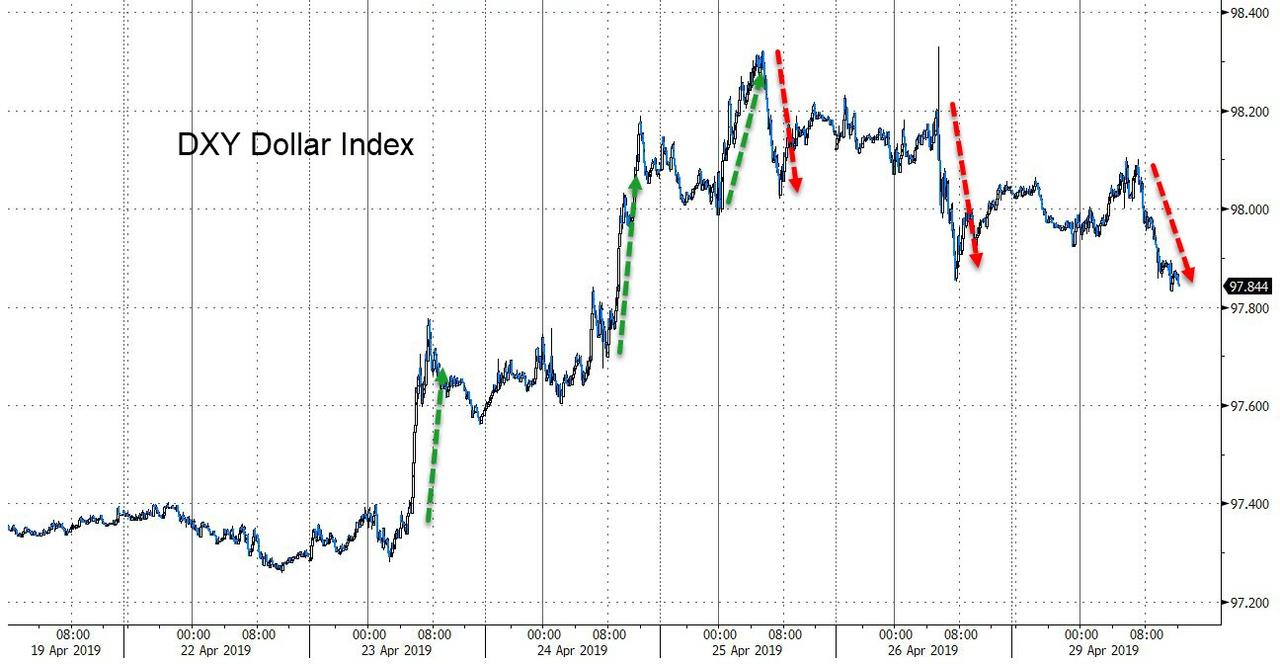

/Chinese yuan (ONSHORE) closed UP at 6.7283 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 64.03 dollars per barrel for WTI and 72.83 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.7283 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7380/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA/ SOUTH KOREA

NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA

As promised, the trade deal with China is shattered. Again the White HOuse is threatening to walk away from the table. The USA does not understand that it is better off with what they have already..they are exporting worthless dollars to pay for goods.

( zero hedge)

ii)This will surely infuriate the Chinese as two USA warships sail through the Taiwan Strait

( zerohedge)

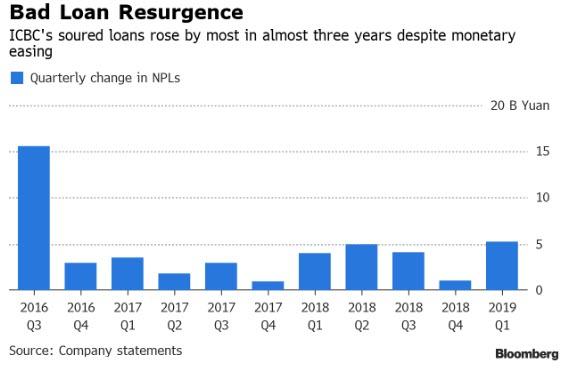

iii)The following is China’s Neutron Bomb: non performing loans. The total of all loans in China is around $35, billion dollars (and another 9 billion dollars in the peer to peer shadow banking sector. It looks like we have about an 8.1 % bad debt ratio or 081 x 35 = 1 trillion dollars of bad debts that the banks have to write off.

( zero hedge)

4/EUROPEAN AFFAIRS

i)EU/HUAWEI/USA/

War of words between Juncker and the USA as Europe will not ban Huawei just because it is Chinese

( zerohedge)

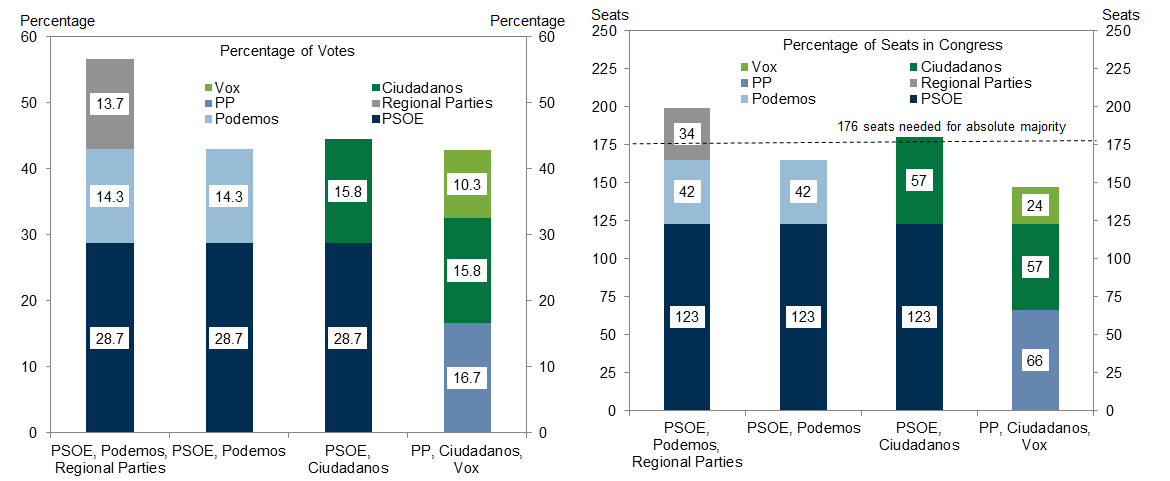

ii) Spain

Spain election: A hung parliament but they would probably gain some support form the Catalan separatists. The populist party VOX gains entry into Parliament with 24 seats.

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY

The Turkish lira plummets to 6;95 as Goldman Sachs has entered the bashing of Turkey arena. They are recommending that the Lira will fall to 6.25 to the dollars. The reserves of Turkey in dollars is negative if you remove their gold value (511 tonnes..$21billion//total reserves including gold: 12 billion dollars)

(courtesy Goldman Sachs/zerohedge)

ii)Turkey indicts its third USA consulate worker in Istanbul on terrorism charges related to Gulen. He and his family our Turkish citizens.

(courtesy Middle East Monitor)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Argentina

9. PHYSICAL MARKETS

i)A central bank is seeking gold through the Comex via the EFP’s.

( Andrew Maguire/Kingworldnews?GATA)

ii)Chris Powell highlights is gold’s deliverance is at hand with the revelation that a sovereign is after gold at the comex.

(Chris Powell/GATA)

iii)Maguire explains how the Comex is designed for market rigging and that it is about to end as a sovereign wishes to attack the comex for its precious metal//gold.

(Maguire/GATA)

iv)The Russian Central banker Elvira is one smart cookie. She no doubt distrusts the dollar and that is why she is buying gold with reckless abandon

( CNBC/GATA)

v)One of great commissioners of the CFTC and a good friend, passes away at the age of 58 due to a “sudden illness”

( GATA)

vi)Two important points: The UK seems to be shipping gold directly to China. Generally China takes kilobars but maybe they are refining their own bars. The second importan points is tiny Azerbaijan who liquidated all of its 32 tonnes of gold in 2016, had decided that they had better buy some of the gold back. They added 8 tones.

(courtesy Lawrie Williams)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/TRADING

ii)Market data

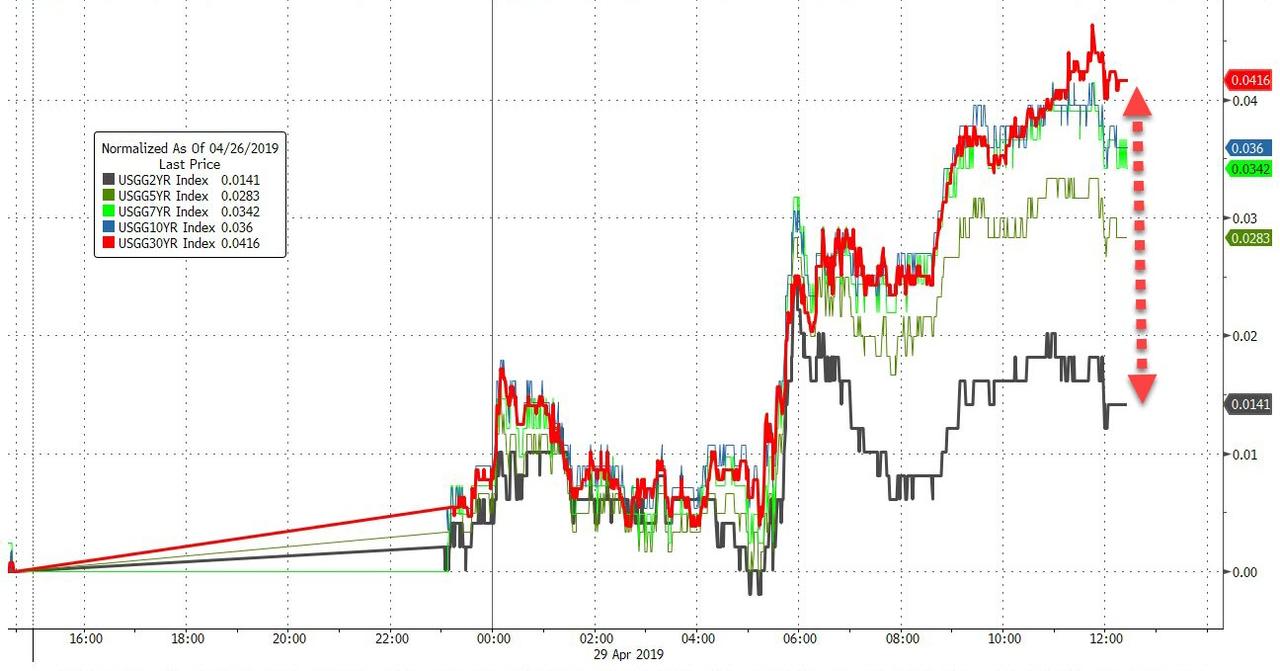

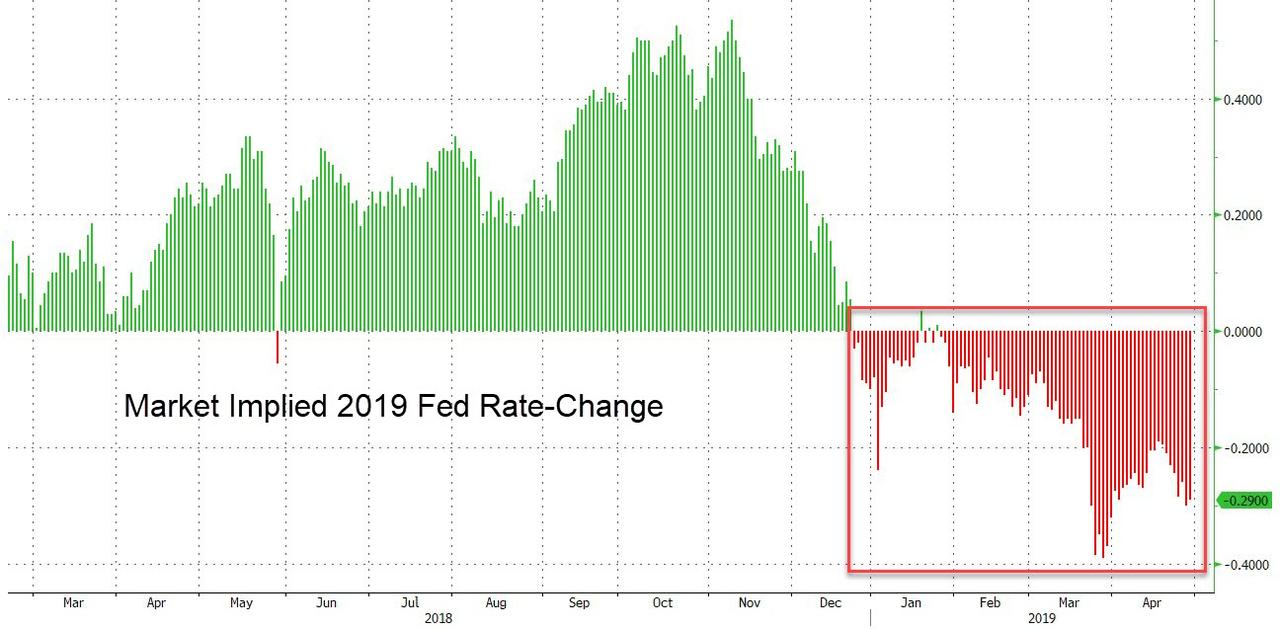

Without getting too technical but believe me that it is true that there is a shortage of dollars in the USA banking system despite the massive 1.5 trillion dollars of excess reserves. The dollar shortage of funding is causing havoc in banking circles and now Charlie McElligott of Nomura has now come out and states that he now expects a 50 basis cut out of gate and this will be soon. The problem is that the effective fund rate has surpassed the IOER or the rate at which the Fed gives a high interest rate for excess reserves.

Don’t pay attention to the details although it is true..just get the gist of the story and what will happen

(courtesy zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

a)An extremely important commentary from Alasdair Macleod as he points out that there is no escape from the USA debt trap. He along with everybody else is highlighting the fact that the USA budgetary deficit must rise because of Trump’s spending initiatives. He gives a detailed explanation as to why (without increase US A savings) the uSA trade deficit must also rise and cannot fall despite Trump’s efforts at increasing tariffs..it is a foo’s game

( Macleod/GoldMoney.com)

b)A few things to note here:

Personal spending rose by a huge .9% month/month and thus USA savings rate plummets again

Person income: constant

thus from Alasdair Macleod’s thesis: as the USA budgetary deficit is skyrocketing so much its trade deficit

(zerohedge)

c)Michael Snyder correctly points out that 102 million Americans do not have a job right now and it is worse than at any point during the last recession.

( Michael Snyder)

d) It seems that everyone is perplexed as the strong GDP report on Friday. It is a fake

( zerohedge)

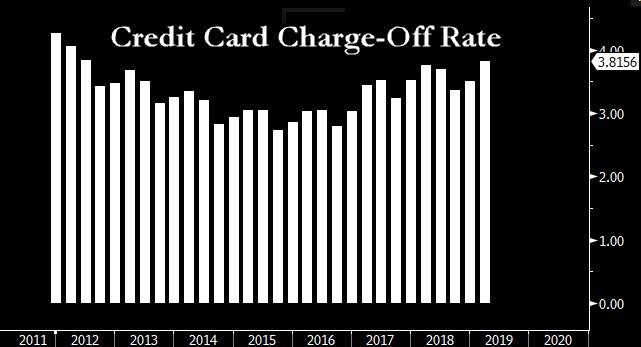

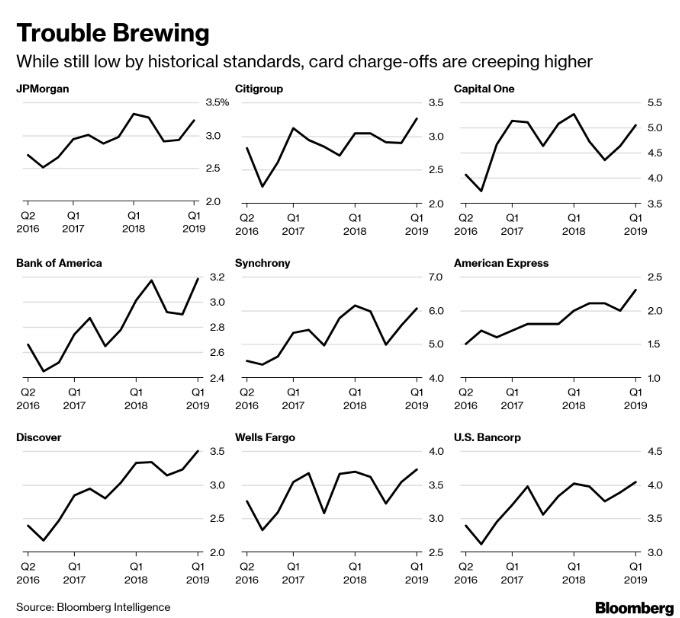

e)This is alarming: credit card write off soar to 7 yr highs.( zerohedge)

f)More Boeing troubles as the FAA turn to the new Dreamliner hydraulic leakage

( zerohedge)

SWAMP STORIES

a) the Ukraine connection and how the Ukrainian government did everything in their power to illegally help Clinton win against Trump and how the Manafort investigation started.

( zerohedge)

b)A good one!! Meijer explains why Biden’s nomination for President will be harmful to the DNC as he has considerable bad baggage

( Raul Meijer)

c)Another great commentary from Kim Strassel. Why didn’t Mueller determine whether the Steele dossier was Russian disinformation. Maybe I G Horowitz or Bill Barr will give us the answer to that

( Kim Strassel)

d)Lots of fun and games with this one>Kim Foxx is being subpoenaed over her office’s decision to drop the Smollet case

( zerohedge)

e)Joe DiGenova is one of the best constitutional lawyers in the uSA. He explains in detail why the Don Jr. meeting at Trump Tower is a phony..ie. the collecting of dirt from a foreign national violates USA election laed

(a must read…Joe Digenova)

E)SWAMP STORIES/MAJOR STORIES//THE KING REPORT

Let us head over to the comex:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A CONSIDERABLE 5498 CONTRACTS.TO A LEVEL OF 430,914 DESPITE THE STRONG GAIN IN THE PRICE OF GOLD ($9.20) IN FRIDAY’S // COMEXTRADING)

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS., THAT IS 6931 EFP CONTRACTS WERE ISSUED:

FOR APRIL 0 FOR JUNE ’19: 6931 CONTRACTS , DEC; 0 CONTRACTS: 0 AND ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6931 CONTRACTS.

THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. ALSO REMEMBER THAT THERE IS NO DOUBT A HUGE DELAY IN THE ISSUANCE OF EFP’S AND IT PROBABLY TAKES AT LEAST 48 HRS AFTER LONGS GIVE UP THEIR COMEX CONTRACTS FOR THEM TO RECEIVE THEIR EFP’S AS THEY ARE NEGOTIATING THIS CONTRACT WITH THE BANKS FOR A FIAT BONUS PLUS THEIR TRANSFER TO A LONDON BASED FORWARD.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES:1433 TOTALCONTRACTS IN THAT 6931 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST A HUGE SIZED 5498 COMEX CONTRACTS.

NET GAIN ON THE TWO EXCHANGES : 1433contracts OR 143300 OZ OR 4.457 TONNES.

We are now in the active contract month of APRIL and here the open interest stands at 201 contracts, having LOST 46contracts.

We had 46 notices filed upon yesterday, so we LOST 0 contracts or an additional NIL oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. THE GOLD COMEX ,AND FOR THAT MATTER THE GLOBE, IS VOID OF GOLD AS THE CROOKS DESPERATELY SEARCH FOR BADLY NEEDED GOLD. TO PUT OUT FIRES OCCURRING ELSEWHERE!! THIS ENDS THE STREAK AT 9 CONSECUTIVE DAYS WHERE WE HAD AN INCREASE IN THE AMOUNT OF GOLD STANDING AND THE ODDS ARE THAT DURING THAT STREAK THE BANKERS WERE SEARCHING FOR METAL. HOWEVER DUE TO THE FACT THAT LONDON IS BASICALLY OUT OF METAL, IT IS POSSIBLE THAT SOVEREIGNS OR BIG INVESTORS MAY TURN TO THE COMEX FOR PHYSICAL GOLD.

The next non active delivery month after APRIL is the NON active delivery month is MAY and here the OI FELL by 353 contracts FALLING TO 571 contracts. The next contract month after May is June and it is an active month. Here the open interest FELL by 5584 contracts DOWN to 300,726 contracts.

TODAY’S NOTICES FILED:

WE HAD 201 NOTICES FILED TODAY AT THE COMEX FOR ,20,100 OZ. (0.1430 TONNES)

Total COMEX silver OI FELL BY A HUGE SIZED 11,845 CONTRACTS FROM 214,818 DOWN TO 201,099(AND FURTHER FROM THE NEW RECORD OI FOR SILVER SET ON AUGUST 22.2018. THE PREVIOUS RECORD WAS SET APRIL 9.2018/ 243,411 CONTRACTS)AND TODAY’S STRONG OI COMEX LOSS OCCURRED DESPITE A 12 CENT GAIN IN PRICING.//YESTERDAY.

WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL AND THE OPEN INTEREST IN THIS FRONT MONTH RESTS AT 0 CONTRACTS FOR A LOSS OF 1 CONTRACT ON THE DAY.

WE HAD 1 NOTICE SERVED UP ON FRIDAY, SO WE GAINED 0 CONTRACT OR AN ADDITIONAL NIL OZ OF SILVER WILL STAND AT THE COMEX AS INVESTORS REFUSED TO MORPH INTO LONDON BASED FORWARDS AS WELL AS NEGATING A FIAT BONUS. THE COMEX IS RUNNING OUT OF METAL TO FEED THE CROOKS.

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 19,459 CONTRACTS DOWN TO 13,767. CONTRACTS.. THE NEXT MONTH OF JUNE GAINED 132 CONTRACTS TO 535. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 6959 CONTRACTS UP TO 142,361 CONTRACTS.

ON A NET BASIS WE LOST A HUMONGOUS SIZED 8796 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 11845 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 3049 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS ON THE TWO EXCHANGES: 8796CONTRACTS...AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A 12 CENT GAIN IN PRICING// FRIDAY????

TODAY’S NUMBER OF NOTICES FILED:

We, today, had 0 notice(s) filed for NILOZ for the MARCH, 2019 COMEX contract for silver

Trading Volumes on the COMEX TODAY: 198,286 CONTRACTS

CONFIRMED COMEX VOL. FOR YESTERDAY: 290,281 contracts

Total monthly oz gold served (contracts) so far this month

7149 notices

714900 OZ

22.236 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

HOW COULD THIS BE POSSIBLE? WE NOW HAVE ONE TRADING DAYS LEFT, ( TUESDAY)

WE HAVE 22.23 TONNES OF GOLD STANDING AGAINST 8.8 TONNES??

we had 0 dealer entries:

total dealer deposits: nil oz

total dealer withdrawals: nil oz

We had 0 kilobar entries

we had 0 deposit into the customer account

i) Into JPMorgan: nil oz

ii) Into everybody else: zero oz

total gold deposits: nil oz

very little gold arrives from outside/ again zero amount arrived today

we had 0 gold withdrawals from the customer account:

(maybe investors are taking our advice by not storing their gold at the comex.)

this will hurt our bankers as they need to replace leased gold as all gold stored at the gold comex is unallocated.

Gold withdrawals;

i) we had ONE HUGE withdrawal

i) out of JPMorgan; 69,365.576 oz was withdrawn out of the customer account of JPMorgan.

total gold withdrawals; 69,365,576 oz

IS SOMETHING SCARING JPMORGAN ??

we had 0 adjustments…

FOR THE APRIL 2019 CONTRACT MONTH)

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 201 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 118 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL /2019. contract month, we take the total number of notices filed so far for the month (7149) x 100 oz , to which we add the difference between the open interest for the front month of APRIL. (247 contract) minus the number of notices served upon today (201 x 100 oz per contract) equals 714,900 OZ OR 22.236 TONNES) the number of ounces standing in this active month of APRIL

Thus the INITIAL standings for gold for the APRIL/2019 contract month:

No of notices served (7149 x 100 oz) + (247)OI for the front month minus the number of notices served upon today (201 x 100 oz )which equals 714,900 ozstanding OR 22.236 TONNES in this active delivery month of APRIL.

WE LOST TODAY 0 CONTRACTS OR 0 ADDITIONAL OZ WILL STAND AT THE COMEX AND THESE GUYS REFUSED TO MORPH INTO LONDON BASED FORWARDS.(AS WELL AS ACCEPTING A FIAT BONUS FOR THEIR EFFORTS). THIS ENDS THE NINE CONSECUTIVE GAINS AT THE GOLD COMEX. TO HAVE 9 CONSECUTIVE GAINS IN AMOUNT STANDING IS UNPRECEDENTED AT THE COMEX. AS I DESCRIBED TO YOU LAST MONTH THE GOLD COMEX IS IN SERIOUS STRESS ALONG WITH THE SILVER COMEX. YOU CAN ALSO BET THE FARM THAT BASEL III IS PLAYING A BIG PART IN THIS AS THE BANKS SCRAMBLE TO REMOVE PAPER GOLD COLLATERAL ON THEIR BOOKS FOR THE REAL STUFF.

SURPRISINGLY LITTLE GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 8.856TONNES OFREGISTERED ( GOLD OFFERED FOR SALE) VS 22.236 TONNES OF GOLD STANDING// (with a probable 4.2 tonnes already settled.)

THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total registered or dealer gold: 284,725.713 oz or 8.856 tonnes

total registered and eligible (customer) gold; 7,782,015.791 oz 242.05 tonnes

FOR COMPARISON FIRST DAY NOTICE FOR APRIL 2018 AND FINAL STANDING APRIL 30 2018

AT FIRST DAY NOTICE APRIL 1.2018: 19.897 TONNES STOOD FOR DELIVERY

AT CONCLUSION APRIL 30/2018: ONLY 4.6407 TONNES STOOD AS THE REST MIGRATED TO LONDON THROUGH EFP’S. AT THE BEGINNING OF APRIL IT LOOKED LIKE WE WERE GOING TO HAVE A REPEAT OF LAST YEAR WHERE MANY MORPH TO LONDON BECAUSE THERE IS NO METAL AT THE COMEX. WE ARE PROVEN WRONG: WE ARE DOING MUCH BETTER IN 2019 AS WE NOW HAVE TO 22.373 TONNES OF GOLD STANDING.

AT FIRST DAY NOTICE MAY 1 2018: WE HAD 1.284 TONNES OF GOLD STAND. BY MONTH’S END: 2.27 TONNES AS WE HAD ONE QUEUE JUMPING IN THE MIDDLE OF THE MONTH.

AND IF YOU ARE KEEPING SCORE AT THE SAME TIME LAST YEAR:

IN GOLD ON APRIL 27/2018 WE HAD 571 OPEN INTEREST CONTRACTS STILL REMAINING TO BE SERVED//1 TRADING DAY VS 574 CONTRACTS APRIL 29.2019 WITH 1 TRADING SESSION LEFT.

IN THE LAST 31 MONTHS 113 NET TONNES HAS LEFT THE COMEX.

THE GOLD COMEX IS NOW IN STRESS AS

1. GOLD IS LEAVING THE COMEX

2. GOLD IS LEAVING THE REGISTERED CATEGORY OF THE COMEX.

end

And now for silver

AND NOW THE DELIVERY MONTH OF APRIL

INITIAL standings/SILVER

APRIL 29 2019

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

31,753.042oz

cnt

DELAWARE

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

21,913.462 oz

Int Delaware

No of oz served today (contracts)

0

CONTRACT(S)

(NIL OZ)

No of oz to be served (notices)

0 contracts

NIL oz)

Total monthly oz silver served (contracts)

775 contracts

3,875,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

**

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

total dealer withdrawals: nil oz

we had 1 deposits into the customer account

into JPMorgan: nil

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 149.469 million oz of total silver inventory or 48.80% of all official comex silver. (149 million/305 million)

into Int Delaware:: 21,913.462 oz

total customer deposits today: 21,913.462 oz

we had 2 withdrawals out of the customer account:

i) Out of CNT: 24,868.052 oz

ii) Out of Delaware: 6884.990 oz

total withdrawals: 31,753.042 oz

we had 0 adjustments..

total dealer silver: 91.518 million

total dealer + customer silver: 307.050 million oz

The total number of notices filed today for the APRIL 2019. contract month is represented by 0 contract(s) FOR nil oz

To calculate the number of silver ounces that will stand for delivery in APRIL, we take the total number of notices filed for the month so far at 775 x 5,000 oz = 3,875,000 oz to which we add the difference between the open interest for the front month of APRIL. (0) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL/2019 contract month:775(notices served so far)x 5000 oz + OI for front month of APRIL( 0) -number of notices served upon today (0)x 5000 oz equals 3,875,000 oz of silver standing for the APRIL contract month. This is a strong number of oz standing for an off delivery month.

We gained 0 contracts or an nil will stand at the comex as these guys refused to morph into London based forwards as well as negating a fiat bonus.

FOR COMPARISON VS LAST YEAR:

ON FIRST DAY NOTICE MARCH 29/2018: WE HAD 1,805,000 OZ STAND FOR DELIVERY FOR THE APRIL 2018 DELIVERY MONTH

AT CONCLUSION OF APRIL 2018: 2,485,000 OZ STOOD FOR DELIVERY AS QUEUE JUMPING WAS ALREADY WELL DEVELOPED IN SILVER. (APRIL IS A NON ACTIVE SILVER DELIVERY MONTH)

ON FIRST DAY NOTICE APRIL 30/2018 (FOR THE MAY 2018 CONTRACT MONTH) WE HAD 24.11 MILLION OZ STAND FOR DELIVERY. BY MONTH END WE HAD HUGE QUEUE JUMPING AND THUS 36.285 MILLION OZ EVENTUALLY STOOD FOR DELIVERY.

ON APRIL 27.2018 WE HAD A LARGE 14,230 OPEN INTEREST CONTRACTS STILL LEFT TO BE SERVED WITH 1 TRADING SESSION TO GO/ VS TODAY, APRIL 29.2019: 13,767 CONTRACTS//1 TRADING SESSIONS.

TODAY’S ESTIMATED SILVER VOLUME: 81,699 CONTRACTS (it will go higher on confirmation)

CONFIRMED VOLUME FOR YESTERDAY: 133,684 CONTRACTS..( we had huge liquidation of our spreaders//)

..

YESTERDAY’S CONFIRMED VOLUME OF 133,684 CONTRACTS EQUATES to 668 million OZ 95.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

1. Sprott silver fund (PSLV): NAV RISES TO -3.77% (APRIL 29/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.76% to NAV (APRIL 29/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -3.77%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 12.83TRADING 12.28/DISCOUNT 4.31

END

And now the Gold inventory at the GLD/

APRIL 29/WITH GOLD DOWN $7.00: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 746.69 TONNES

APRIL 26/WITH GOLD UP $9.2//ANOTHER BIG CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD.//INVENTORY LOWERS TO 746.69 TONNES TONNES

APRIL 25//WITH GOLD UP $.05 TODAY (BASICALLY FLAT) NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 747.87 TONNES

APRIL 24 WITH GOLD UP $6.00 TODAY// TWO TRANSACTIONS: 1)A HUGE WITHDRAWAL OF 2.05 TONNES FROM THE GLD AND THEN II) ANOTHER WITHDRAWAL OF 1.76 TONNES//INVENTORY RESTS AT 747.87 TONNES

APRIL 23./WITH GOLD DOWN $4.45 TODAY: NO CHANGES AT THE GLD/INVENTORY RESTS AT 751.68 TONNES//

APRIL 22/WITH GOLD UP $1.75//A SMALL WITHDRAWAL OF .59 TONNES OF GOLD FROM THE GLD INVENTORY//INVENTORY RESTS AT 751.68 TONNES

APRIL 18/WITH GOLD DOWN $.45 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT752.27 TONNES

APRIL 17/WITH GOLD DOWN $0.10 TODAY: ANOTHER HUGE WITHDRAWAL OF 1.76 TONNES AT THE GLD WHICH WAS USED IN YESTERDAY’S RAID/INVENTORY RESTS AT 752.27 TONNES

APRIL 16/WITH GOLD DOWN $13.60 TODAY: A HUGE WITHDRAWAL OF 3.82 TONNES AT THE GLD/INVENTORY RESTS AT 754.03

APRIL 15/WITH GOLD DOWN $3.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.85 TONNES

APRIL 12/WITH GOLD UP $2.10 TODAY:NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757..85 TONNES

APRIL 11/WITH GOLD DOWN $19.85 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.85 TONNES

APRIL 10/WITH GOLD UP $5.45 AGAIN TODAY, THE CROOKS AGAIN RAIDED THE COOKE JAR BY 2.64 TONNES/INVENTORY RESTS AT 757.85 TONNES

APRIL 9/WITH GOLD UP AGAIN BY $6.40/THE CROOKS RAIDED THE COOKIE JAR AGAIN BY 1.18 TONNES/INVENTORY RESTS AT 760.49 TONNES

APRIL 8/WITH GOLD UP AGAIN BY $6.40: THE CROOKS RAIDED THE COOKIE JAR AGAIN BY .88 TONNES//INVENTORY RESTS TONIGHT AT 761.67 TONNES.

APRIL 5/WITH GOLD UP$1.35: ANOTHER WITHDRAWAL OF 1.74 TONNES OF PHYSICAL GOLD FROM THE GLD INVENTORY: INVENTORY RESTS AT 762.55 TONNES

APRIL 4/WITH GOLD DOWN 90 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.29 TONNES

APRIL 3:WITH GOLD DOWN 20 CENTS: ANOTHER WHOPPER OF A WITHDRAWAL: 3.81 TONNES FROM THE GLD//INVENTORY RESTS AT 764.29 TONNES

APRIL 2//WOW! WE LOST A WHOPPING 16.16 TONNES OF GOLD WITH A RISE IN PRICE OF $1.80//INVENTORY RESTS AT 768.10

APRIL 1/WITH GOLD DOWN $3.80: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 784.26 TONNES

MARCH 29/WITH GOLD UP $2.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 784.26 TONNES

MARCH 28/WITH GOLD DOWN $20.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 784.26 TONNES

MARCH 27/SURPRISING! WITH GOLD DOWN AGAIN BY $4.05, THE CROOKS NEEDED TO PUT GOLD BACK INTO THE GLD: THEY ADDED 3.23 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 784.26 TONNES

MARCH 26/WITH GOLD DOWN $7.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 781.03 TONNES

MARCH 25/WITH GOLD UP $9.85: A STRONG 2.94 TONNES DEPOSIT INTO THE GLD/INVENTORY RESTS AT 781.03 TONNES

MARCH 22/WITH GOLD UP $5.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 778.09 TONNES

MARCH 21/WITH GOLD UP $7.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 778.09 TONNES

March 20/WITH GOLD DOWN $5.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 778.09 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 29/2019/ Inventory rests tonight at 746.69 tonnes

*IN LAST 588 TRADING DAYS: 18.28 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 488 TRADING DAYS: A NET 21.44 TONNES HAVE NOW BEEN LOST INTO THE GLD INVENTORY.

WE MUST BE GETTING CLOSER TO THE BOTTOM OF THE BARREL FOR PHYSICAL GOLD AT THE GLD.

end

Now the SLV Inventory/

APRIL 29/ WITH SILVER DOWN 13 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.979 MILLION OZ.

APRIL 26//WITH SILVER UP 12 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.979 MILLION OZ//

APRIL 25/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.979 MILLION OZ///

APRIL 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.979 MILLION OZ//

APRIL 23./WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.979 MILLION OZ///

APRIL 22/WITH SILVER UP 4 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.979 MILLION OZ///

APRIL 18/WITH SILVER FLAT TODAY: A SHOCKING 2.8122 MILLION PAPER OZ WERE ADDED INTO SLV INVENTORY: INVENTORY RESTS AT 311.979 MILLION OZ/

APRIL 17/WITH SILVER UP ONE CENT TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 309.167 MILLION OZ///

APRIL 16/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 309.167 MILLION OZ//

APRIL 15: WITH SILVER DOWN ONE CENT TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 750,000 OZ//INVENTORY RESTS AT 309.167 MILLION OZ.

APRIL 12 WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 309.917 MILLION OZ.

APRIL 11/WITH SILVER DOWN 37 CENTS TODAY: A DEPOSIT OF 750,000 OZ INTO THE SLV/INVENTORY RESTS AT 309.917 MILLION OZ//

April 10/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 309.167 MILLION OZ.

APRIL 9/WITH SILVER DOWN ONE CENT: NO CHANGES IN SILVER INVENTORY AT THE SLV.INVENTORY RESTS AT 309.167 MILLION OZ///

APRIL 8/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.INVENTORY RESTS AT 309.167 MILLION OZ///

APRIL 5/WITH SILVER DOWN 2 CENTS: NO CHANGES IN SILVER INVENTORY: THE CROOKS CANNOT RAID ANY SILVER BECAUSE THERE IS NONE: INVENTORY RETS AT 309.167 MILLION OZ//

APRIL 4/WITH SILVER FLAT TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 309.167 MILLION OZ/

APRIL 3/WITH SILVER UP TWO CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 309.167 MILLION OZ/

APRIL 2/ WITH SILVER DOWN ONE CENT TODAY: A SMALL WITHDRAWAL OF 134,000 OZ FROM THE SLV TO PAY FOR FEES/INVENTORY RESTS AT 309.167

APRIL 1/WITH SILVER DOWN ONE CENT TODAY: A SMALL WITHDRAWAL OF 656,000 OZ FROM THE SLV/INVENTORY RESTS AT 309.301 MILLION OZ//

MARCH 29/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 309.957 MILLION OZ/

MARCH 28/WITH SILVER DOWN 31 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 469,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 309.957 MILLION OZ/

MARCH 27/WITH SILVER DOWN 12 CENTS; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 309.488 MILLION OZ//

MARCH 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 309.488 MILLION OZ//

MARCH 25/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 309.488 MILLION OZ////

MARCH 22/WITH SILVER DOWN 7 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.356 MILLION OZ///INVENTORY RESTS AT 309.488 MILLION OZ///

MARCH 21/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 310.848 MILLION OZ/

March 20/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY RESTS AT 310.848 MILLION OZ//

APRIL 29/2019:

Inventory 311.979 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

THE RISE IN LIBOR IS CREATING A SCARCITY OF DOLLARS BECAUSE FOREIGN EXCHANGE SWAPS (COSTS) ARE SIMPLY PROHIBITIVE

YOUR DATA…..

6 Month MM GOFO 2.13/ and libor 6 month duration 2.62

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: + .51/

XXXXXXXX

12 Month MM GOFO

+ 2.46%

LIBOR FOR 12 MONTH DURATION: 2.72

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.26

end

PHYSICAL GOLD/SILVER STORIES

end

i) GOLDCORE BLOG/Mark O’Byrne

Death of Infl

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

A central bank is seeking gold through the Comex via the EFP’s.

(courtesy Andrew Maguire/Kingworldnews?GATA)

A central bank is seeking gold through Comex ‘exchange for physicals,’ Maguire tells KWN

Submitted by cpowell on Sat, 2019-04-27 00:50. Section: Daily Dispatches

8:45p ET Friday, April 26, 2019

Dear Friend of GATA and Gold:

In an interview today with King World News, London metals trader Andrew Maguire says a central bank is seeking to acquire gold with the mysterious “exchange for physicals” mechanism by which gold futures contracts on the New York Commodities Exchange appear to be transferred to London for delivery without any actual delivery ever being made there.

Maguire insists that the physical gold market is beginning to discipline the paper market, where price smashdowns have been frequent lately but of less lasting effect than in the past.

CHRIS POWELL, Secretaty/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

The Russian Central banker Elvira is one smart cookie. She no doubt distrusts the dollar and that is why she is buying gold with reckless abandon

(courtesy CNBC/GATA)

Russia gains gold to diversify reserves, not to distrust dollar, central banker says

Submitted by cpowell on Sat, 2019-04-27 00:59. Section: Daily Dispatches

By Matt Clinch

CNBC, New York

Friday, April 26, 2019

Russia’s gold-buying surge over the past year is simply down to a wish to diversify its portfolio of reserves, the central bank governor told CNBC today.

The country overtook China last year to become the world’s fifth largest official sector holder of gold. The central bank bought 8.8 million troy ounces of bullion last year, beating a record 7.2 million ounces set in 2017, and fresh data continues to show that the buying hasn’t stopped.

…

Experts have speculated that Western sanctions could have caused the move, with the safe-haven asset being exempt from any possibility of blacklisting. Others suggest Russia wants to reduce its reliance on the U.S. dollar, or is shying away from the euro or the pound, which have seen their values fall due to policy easing and Brexit, respectively.

But Elvira Nabiullina, the governor of Russia’s central bank, told CNBC’s Geoff Cutmore in Moscow that “diversification” was the key reason behind the purchases, not a lack of trust for any specific currency. …

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

One of great commissioners of the CFTC and a good friend, passes away at the age of 58 due to a “sudden illness”

(courtesy GATA)

Former CFTC Commissioner Bart Chilton, lately TV news show host, dies at 58 after ‘sudden illness’

Submitted by cpowell on Sun, 2019-04-28 04:10. Section: Daily Dispatches

Chilton arranged for GATA to testify at the U.S. Commodity Futures Trading Commission’s hearing on the monetary metals markets in 2010 and wanted the commission to investigate manipulation of those markets.

* * *

‘Boom Bust’ Host, Former CFTC Commissioner Bart Chilton, dies at Age 58

From Russia Today, Moscow

Saturday, April 27, 2019

With great sorrow, we announce that our beloved colleague Bart Chilton has passed away at age 58 after a sudden illness.

Our friend Bart brought a unique combination of passion for business and extensive experience in the sphere of finance to his role as host of signature financial show, “Boom Bust,” elevating the content and profile to a new level, making it one of the most popular programs on RT America.

…

His trademark show opening, “Let’s go!” was a perfect expression of his enthusiasm and drive to constantly do more and learn more.

Since the first day he walked into our newsroom — tall, with a distinctive white mane, trademark cowboy boots, and his enchanting smile — Bart started making friends. We soon felt that he belonged with us. He became a member of our team and a part of us.

Bart always seemed to project a strong, quiet sense of dignity, and treated every person he met with respect, nomatter what their position, status, or age. He was one of those people who won hearts without saying a word.

His friends and colleague knew him as an overachiever. Prior to his TV career, Bart Chilton was commissioner at the U.S. Commodity Futures Trading Commission from 2007 to 2014. At the commission he headed the Energy and Environmental Advisory Committee and the Global Markets Advisory Committee.

He served on multiple local, federal, and presidential campaigns, the Obama presidential transition team, and in the U.S. House, Senate, and executive branch offices. His subject matter expertise spanned from politics and policy — specifically U.S. and global financial markets, agricultural, energy and the environment, and transportation — to music, movies, and pop culture.

Commissioner Chilton was known for his individualistic approach to financial regulation, his myriad media appearances, speeches, and frequent opinion editorials. From 1995 to 2001 Commissioner Chilton was a political appointee of President Bill Clinton, rising to deputy chief of staff to U.S. Agriculture Secretary Dan Glickman.

* * *

* * *

Maguire explains how the Comex is designed for market rigging and that it is about to end as a sovereign wishes to attack the comex for its precious metal//gold.

Maguire explains how Comex is designed for metals market rigging, expects silver to pop back up soon

Submitted by cpowell on Sat, 2019-04-27 15:48. Section: Daily Dispatches

11:45a ET Saturday, April 27, 2019

Dear Friend of GATA and Gold:

In his new interview with King World News, London metals trader Andrew Maguire details how the rules of the New York Commodities Exchange were designed to prevent ordinary futures traders from taking advantage of the market-rigging facilities of the bullion banks. He also explains why he thinks silver prices will shoot back up soon. The interview is 22 minutes long and can be heard at KWN here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

Chris Powell highlights is gold’s deliverance is at hand with the revelation that a sovereign is after gold at thecomex.

(Chris Powell/GATA)

Could gold’s day of deliverance be at hand?

Submitted by cpowell on Sun, 2019-04-28 03:37. Section: Daily Dispatches

Get back to work. If it comes, you’ll notice.

* * *

11:48p ET Saturday, April 27, 2019

Dear Friend of GATA and Gold:

Does this weekend’s assertion on King World News by London metals trader Andrew Maguire that a central bank intends to acquire whatever gold remains at the New York Commodities Exchange —

— mean the end of the international gold price suppression policy?

Any central bank with substantial financial resources indeed could make trouble for the policy, since not much gold ever seems to be immediately available through the Comex. But don’t bet your life that Maguire’s story begins the countdown to the day of deliverance — if only because, like many involved with GATA, you may already have bet too much that the day of deliverance will come in your lifetime.

Here are a few cautionary thoughts.

Maguire is as sharp and experienced as they come in the monetary metals business, is supremely well-informed, and has done heroic service in fighting price suppression policy and exposing its tactics in the futures and over-the-counter markets. But are his sources telling him the truth? Or are they telling him what they would like the world to think, or using him to send a threat that may not be fulfilled?

For a few years now central banks have turned from net gold sellers to net gold buyers, announcing their purchases with some frequency, without exploding suppression policy and without reversing the trend of the gold price, which has been downward since 2011.

Prior to April 2013 many financial analysts were writing that China’s steady acquisitions had placed a put under the gold price. But the smashdown in gold in that month, obviously a coordinated intervention by central banks, vaporized the idea of a Chinese put. China’s foreign exchange reserves, the world’s largest, enable China to control any market, and the April 2013 smashdown could not have succeeded without China’s assent.

The U.S. economists Paul Brodsky and Lee Quaintance hypothesized in 2012 that most central banks, including those acquiring gold, were participating in suppression policy because its objective is to let central banks reacquire gold cheaply in a redistribution of world gold reserves in favor of central banks whose foreign exchange reserves are held disproportionately in U.S. dollars, which central banks figure must be devalued. Upon completion of that redistribution and the dollar’s devaluation, Brodsky and Quaintance predicted, central banks would reliquefy themselves by revaluing gold dramatically upward:

The Brodsky-Quaintance hypothesis fits the facts and was reiterated if without attribution seven weeks ago by a surprisingly candid report in the Italian newspaper It Sole / 24 Ore:

Also more or less confirming that all major central banks have been participating in gold price suppression was a speech given in 2005 by the head of the monetary and economic department of the Bank for International Settlements, William R. White. He told a conference at BIS headquarters in Basel, Switzerland, that among the five most important objectives of central bank cooperation is “the provision of international credits and joint efforts to influence asset prices (especially gold and foreign exchange) in circumstances where this might be thought useful.”

That is, rigging the gold and currency markets is simply what modern central banking does:

So a central bank’s move on the Comex gold futures market, a primary mechanism of price suppression, would suggest that central bank cooperation was weakening if not coming apart.

But even if such a move is underway, it well might be resisted for a long time with countermeasures by other central banks and governments.

Vaulting the gold of many other countries, the United States and United Kingdom have access to plenty of metal that might be thrown at the Comex to repel an attack, at least for a while. The Bank of England already has essentially confiscated Venezuelan gold reserves at the request of the United States:

If such countermeasures seemed likely to fail, they might be backed up by more of the economic warfare the United States is already waging against much of the world, weaponizing the dollar, the world reserve currency, more than ever before.

GATA has been documenting international gold price suppression policy for almost 20 years —

— and while it has been an amazing education — the secret knowledge of the financial universe, actually — it is also the study of a cosmic injustice, the daily triumph of totalitarian imperialism. So no one could wish for the policy to explode more than GATA does. We would like to turn our lives to something else — if only flying saucers, Bigfoot, or the search for D.B. Cooper.

For many years we have thought that gold price suppression policy’s implementation through market intervention could not get more obvious, and yet it has gotten more obvious almost every week, still with not a peep of complaint or even curiosity from the monetary metals mining industry or mainstream financial news organizations.

In that respect GATA has been a humiliating failure.

So while we hope for victory and expect that the ascent of man will continue through the centuries ahead, we don’t predict or promise victory, just persistence, figuring that, as Lee Strasberg’s Hyman Roth tells Al Pacino Michael Corleone in the second “Godfather” movie, “This is the business we’ve chosen”:

Whenever gold price suppression policy blows up or is changed — whether it happens Sunday night, or next year, or 10 years on, or longer — if you’re still alive, you’ll notice.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

* * *

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

No one in authority helped the monetary metals cause as much as Bart Chilton did

Submitted by cpowell on Mon, 2019-04-29 01:35. Section: Daily Dispatches

9:36p ET Sunday, April 28, 2019

Dear Friend of GATA and Gold:

While the former member of the U.S. Commodity Futures Trading Commission, Bart Chilton, disappointed some monetary metals investors, he was a hero to GATA for several reasons.

First, he forced the commission to take public testimony from GATA Chairman Bill Murphy and GATA Director Adrian Douglas at the commission’s much-publicized hearing on the monetary metals markets in March 2010. This brought national attention to our issue.

…

Second, he repeatedly gave credence in public to complaints of manipulation of the gold and silver markets.Third, he conscientiously answered mail from ordinary investors and others.

Fourth, he saw his responsibility to represent the producing classes against the financial class, which has taken over the country and the world.

And fifth, he did what he could to legitimize the market manipulation issue without violating what he understood as the confidentiality requirements of a regulatory agency.

No one in any official position has done more than that during GATA’s campaign against surreptitious market rigging by governments and their agents.

Bloomberg News has produced a news obituary for Chilton here:

Three weeks before Chilton died your secretary/treasurer e-mailed him to try to pin him down about something he had been hinting at, a question the CFTC has refused to answer for GATA and U.S. Rep. Alex Mooney, R-West Virginia.

Could Chilton, your secretary/treasurer asked, say whether manipulative futures trading undertaken directly or indirectly by the U.S. government is subject to the CFTC’s jurisdiction, or is it legal?

Uncharacteristically Chilton did not acknowledge the inquiry — which may have been as dispositive an answer as the CFTC’s refusal to answer.

By virtue of his work on the CFTC Chilton surely knew the answer, which would explain why the commission looks away from even the most blatant manipulations of the monetary metals markets. We can only hope that his knowing the answer and his willingness to hint at it had nothing to do with the “sudden illness” to which his death is being attributed. But the world is full of evil governments and evil financial institutions.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

Bart Chilton, arguably the most famous CFTC commissioner who on various occasions vowed to crack down (unsuccessfully) on precious metals and VIX manipulation, who called for cryptocurrency regulation, and who sported shoulder-length silver hair and wore cowboy boots during his frequent TV appearances, has died “after a sudden illness”, RT reports. He was only 58.

Chilton, who most recently was an op-ed writer for Forbes and had his own daily business and finance television show “Boom Bust with Commissioner Bart Chilton on RT America” spent a career in government during the Clinton, Bush and Obama Administrations, on Capitol Hill as a senior staffer in the House and Senate, concluding as a CFTC financial regulator between 2007 and 2014 where he repeatedly railed against precious metal manipulation and called for appropriate regulation of crypto currencies. In his own words, “I’ve always looked out for average folks and spoken my mind.”

At the CFTC, he headed the Energy and Environmental Advisory Committee and the Global Markets Advisory Committee. He has served on multiple local, federal and presidential campaigns, the Obama presidential transition team, and in the US House, Senate, and Executive branch. His subject matter spanned from politics and policy – specifically US and global financial markets, agricultural, energy and the environment, and transportation – to music, movies, and pop culture. Commissioner Chilton was known for his individualistic approach to financial regulation, his myriad media appearances, speeches, and frequent opinion editorials. From 1995 to 2001, Commissioner Chilton was a political appointee of President Bill Clinton, rising to Deputy Chief of Staff to US Secretary of Agriculture Dan Glickman.

“We remember his intelligence, his compassion, his joyful laughter. With his passing, nothing could fill the void in our newsroom, nor the space Bart held in our hearts,” said Mikhail Solodovnikov, RT America’s News Director. “We will seek solace, and honor his memory, by delivering the best news content to our viewers, with the dedication and diligence that is the hallmark and legacy of our friend Bart Chilton.”

Our News Team expresses deepest condolences to Bart’s wife, Sherry.

Over the years, Zero Hedge had repeatedly covered Chilton’s seemingly sole attempts to crackdown on precious metals regulation, often critically, as in the end he was unable to put an end to an activity that has subsequently cost banks billions in legal settlement fees. That said, Chilton was at least one of the few regulators to admit that Wall Street is rigged, most notably in his Christmas 2013 CFTC parting letter which we posted at the time, and which we excerpt from one last time.

* * *

While one may criticize now-ex CFTC commissioner Bart Chilton for years and years of sound and fury signifying nothing, countless promises of regulatory enforcement (all of which fell short of the target) and finally putting an end to precious metals manipulation only for the world to discover that while every other asset class is manipulated (involving such individuals as JPM’s chief currency dealer), gold and silver are exempt, one must admit the former regulator does have a way wtih words (and of course haircuts). Sure enough, Chilton’s most memorable parting gift will not be something he did, but rather what he said.

William Cohan memorializes his parting message: “As we long suspected, Wall Street continues to use every trick in its playbook to do whatever it can to eviscerate numerous post-financial-crisis rules. The arsenal includes high-powered lobbyists who outnumber lawmakers 10-to-1; $1,000-an-hour letter-writing lawyers who gain strength from negotiating over arcana; and the occasional hoodwinking of a president whose knowledge of the ways of finance are close to nil.”

Chilton’s take home message: “The lesson for me is: The financial sector is so powerful that they will roll things back over time,” Chilton says. “The Wall Street firms have tremendous influence, and they can impact policy to a greater degree than any one regulator or a small group of regulators can.”

What are Chilton’s other laments? Why being underfunded of course. Because if the CFTC only had more money, all would have been fixed.

In fiscal 2013, for example, the CFTC requested funding of $308 million and got only $195 million ($10 million less than the previous year) despite many new responsibilities. “There are crooks who are getting away with crimes because we don’t have the resources to go after them,” Chilton says. The SEC has a similar discrepancy between its appropriation and what it needs to fulfill legal mandates.

With its regulators overwhelmed and underfunded, Wall Street firms then move to the relentless negotiation stage. “As you try to deal with the regulatory agency,” he says of Wall Street, “the first thing you do is you say, ‘Well, would you exempt us?’ And when that doesn’t work, you try to ameliorate your regulation.” If that strategy fails, the industry defaults to litigation.

Chilton said he has noticed one additional tactic that Wall Street has been employing lately: stalling or thwarting nominees to regulatory agencies. The nomination of Timothy Massad, the U.S. Treasury Department official who managed the Troubled Asset Relief Program, to replace Gary Gensler as CFTC chairman came late in the year and a confirmation vote has now been delayed, probably to February 2014. That means further Dodd-Frank rule-writing and enforcement could be delayed, too, because only two of five commissioners will be seated and they would both have to agree to get anything done. “It’s a gift to Wall Street,” he said. “This is what they’ve been trying to do. They’ve been trying to stop Dodd-Frank.”

Chilton knows why Wall Street always seems to win. Financial-industry executives contribute more money “in every election, than any other sector, and they have made more profits in every single quarter since the fall of 2008 when many of them helped crash the economy,” he explains. “So while the rest of the nation is suffering still, and trying to get a leg up to get out of the ditch, the financial sector didn’t miss a beat.”

In case you didn’t catch Chilton’s meaning, here is the shorter version: Unless and until Wall Street’s disproportionate ability to bully Washington is curtailed, the rest of us will be held hostage to its agenda. For those interested in the fuller version, Chilton has been writing a book. Its working title: “Theft.”

One sure can’t say that those 30 years he spent in Washington of which nearly 7 years at the CFTC were lost on the Alexander Godunov lookalike: at least he figured out who runs the show.

END

Bill Murphy on the death of Bart Chilton…

Sunday…

*The stunning news today is that former CFTC Commissioner Bart Chilton died at the age of 58 from a “sudden illness.” It is really sad. Having met Bart personally in December of 2009 in Washington, D.C., I know he was one of the good guys. Bart assembled a government group to hear what GATA had to say about the manipulation of the gold and silver markets. Then in March of 2010 Bart arranged for me to speak on GATA’s behalf in front of a CFTC hearing on the monetary metals, which was televised on the internet.

There are no two ways around it. Bart’s death is something out of a conspiracy movie made for TV, or perhaps a Russian/North Korean spy movie. He was one of the very few out there in the government world that would give GATA’s price suppression viewpoints the light of day. And now he is dead.

Does anyone else, outside of Harvey Organ, even know another commissioner’s name? In our world it was Bart Chilton and nobody else.

Andrew Maguire had been in touch with Bart last week and said he was “fighting fit.” Andrew interviewed Bart in December and Bart pointed to JP Morgan as far as having a role in the manipulation issue. And now he is dead.

A coincidence? Nobody will probably ever know, but this is not the first mysterious death of someone going up against JPM. Was it a coincidence that my presentation at the CFTC hearing was the only one not televised, “due to technical difficulties?” Whatever suddenly happened to Bart, his demise will be food for the fodder mill for years to come. Very much a bummer anyway you look at it.

end

From my good friend: “J. Johnson” on Bart Chilton

Standing Against The Machine, and now RIP, Mr. Bart Chilton

I had posted a concern that Mr. Chilton should be placed under protective custody for his own safety after I heard his interview. Now he’s dead but his employment history he just walked us thru needs to be congressionally reviewed. Who was it that Mr. Chilton worked for that helped in this collusion that Bart may have viewed live? Good Ol’ Gary Gensler was there leading the regulatory body into questionable actions like the conversation GG had with a Senator over a weekend, that soon became the head of a collapsed commodity investment firm out there named MFGlobal. Not only was Gensler watching over the regulatory body, he was best friends with John Corzine who just so happened to be one of Obama’s greatest money finders during his run for presidency. We remember the accusation brought out during the Congressional Hearing and we also remember nothing being done after many of the MFG regulators claimed Corzine knew what he was doing using other people’s money to trade. We also remember Gary Gensler being very helpful when it came to voting in the Frank-Dodd act, now it’s time to review it all, criminally.

Sure we’ll leave room for Bart dying a natural death, but that interview was a major blow out against the regulatory body that has been used to protect the machine against the people the body was created to protect in the first place. This regulatory group needs to be fully and publicly exposed, including those that came in and left, to go back to the banks they worked for before they entered into the regulatory body. Not all are bad, but the few who are, need to be dragged out so the public can see the who/what/when/why/where it all leads to.

God Bless you Bart Chilton, to me you are an American Patriot! The rest of us, need to continue to pick apart the system that is coming down as we watch. It is happening ever so slowly, then all at once, like in the merging currencies! So keep your precious metals close, have a positive attitude no matter what, take more precious metals out of the system if you can, and as always …

Stay Strong!

J. Johnson

end

Due to the criminal conviction of trader Edmonds, the USA prosecution is seeking to halt the civil lawsuit. I was misinformed: all discoveries in a civil suit are public and because of that, the prosecution gives the defendants the right to plead the 5th if their testimony incriminates them

(courtesy zerohedge/Chris Powell)

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

A sign of JP Morgan Chase Bank is seen in front of their headquarters tower in New York.

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

A federal judge tells traders that they can combine cases (with the other 6 banks) as they accused JPMorgan of rigging the precious metals market

(courtesy CNBC)

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Spencer Platt | Getty Images

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.