GOLD: $1280.60 DOWN $3.70 (COMEX TO COMEX CLOSING)

Silver: $14.86 DOWN 3 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1284.60

silver: $14.91

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 5/7

EXCHANGE: COMEX

CONTRACT: MAY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,283.500000000 USD

INTENT DATE: 05/07/2019 DELIVERY DATE: 05/09/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 5

737 C ADVANTAGE 2 2

905 C ADM 5

____________________________________________________________________________________________

TOTAL: 7 7

MONTH TO DATE: 171

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 7 NOTICE(S) FOR 700 OZ (0.0217 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 171 NOTICES FOR 17100 OZ (.5318 TONNES)

SILVER

FOR MAY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

152 NOTICE(S) FILED TODAY FOR 760,000 OZ/

total number of notices filed so far this month: 3279 for 16,395,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5930 UP 79.00

Bitcoin: FINAL EVENING TRADE: $5953 UP 101

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A TINY SIZED 705 CONTRACTS FROM 199,591 DOWN TO 199,467 ACCOMPANYING YESTERDAY’S 3 CENT FALL IN SILVER PRICING AT THE COMEX. ,LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER BUT IT NOW COMMENCES FOR GOLD. TODAY WE705RRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 529 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 529 CONTRACTS. WITH THE TRANSFER OF 529 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 529 EFP CONTRACTS TRANSLATES INTO 2.645 MILLION OZ ACCOMPANYING:

1.THE 3 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 18.1 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MOAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

8808 CONTRACTS (FOR 6 TRADING DAYS TOTAL 8808 CONTRACTS) OR 44.01 MILLION OZ: (AVERAGE PER DAY: 1468 CONTRACTS OR 7.34 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 44.01 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.28% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 784.87 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD A TINY SIZED 176 INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 705 WITH THE 3 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 529 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE LOST A TINY SIZED: 176 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 529 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 705 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 3 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.89 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.008 BILLION OZ TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 152 NOTICE(S) FOR 760,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 18.1 MILLION OZ ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A HUGE SIZED 7551 CONTRACTS, TO 450,039 WITH THE TINY RISE IN THE COMEX GOLD PRICE/(AN INCREASE IN PRICE OF $1.85//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 3268 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 3268 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 450,039. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,819 CONTRACTS: 7551 OI CONTRACTS INCREASED AT THE COMEX AND 3268 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 10,819 CONTRACTS OR 1,081,900 OZ OR 33.65 TONNES. YESTERDAY WE HAD A GAIN IN THE PRICE OF GOLD TO THE TUNE OF ONLY $1.85….AND WITH THAT TINY RISE, WE HAD A HUGE GAIN IN TONNAGE OF 33.65 TONNES!!!!!!.??????????????????????????????????????????

AS YOU WILL SEE, THE CROOKS HAVE NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER A NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 33,418 CONTRACTS OR 3,341,800 OR 103.44 TONNES (6 TRADING DAYS AND THUS AVERAGING: 6030 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAYS IN TONNES: 103.45 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 103.45/3550 x 100% TONNES =2.91% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1919.51 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUGE SIZED INCREASE IN OI AT THE COMEX OF 7551 WITH THE RISE IN PRICING ($1.85) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A SMALL SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 3268 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 3268 EFP CONTRACTS ISSUED, WE HAD AN VERY STRONG GAIN OF 10,819 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

3268 CONTRACTS MOVE TO LONDON AND 7551 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 33.65 TONNES). ..AND THIS HUGE DEMAND OCCURRED WITH A TINY RISE IN PRICE OF $1.85 IN YESTERDAY’S TRADING AT THE COMEX. NO DOUBT THAT A STRONG PERCENTAGE OF OI GAIN WAS DUE TO THE CONTINUING OF THE SPREADING OPERATION AS I HAVE OUTLINED ABOVE.

we had: 7 notice(s) filed upon for 700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $3.70 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 739.64 TONNES

IT LOOKS LIKE WE HAVE REACHED THE BOTTOM OF THE BARREL FOR PHYSICAL GOLD BEING SUPPLIED TO THE CROOKS.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 3 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 316.582 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 705 CONTRACTS from 200,172 DOWN TO 199,467 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER BUT HAVE NOW MORPHED INTO GOLD..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 581 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 581 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 705 CONTRACTS TO THE 529 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 176 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 0.300 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 18.1 MILLION OZ FOR MAY

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 3 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 529 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 32.63 POINTS OR 1.12% //Hang Sang CLOSED DOWN 359.82 POINTS OR 1.23% /The Nikkei closed DOWN 321.13 POINTS OR 1.46%//Australia’s all ordinaires CLOSED DOWN .50%

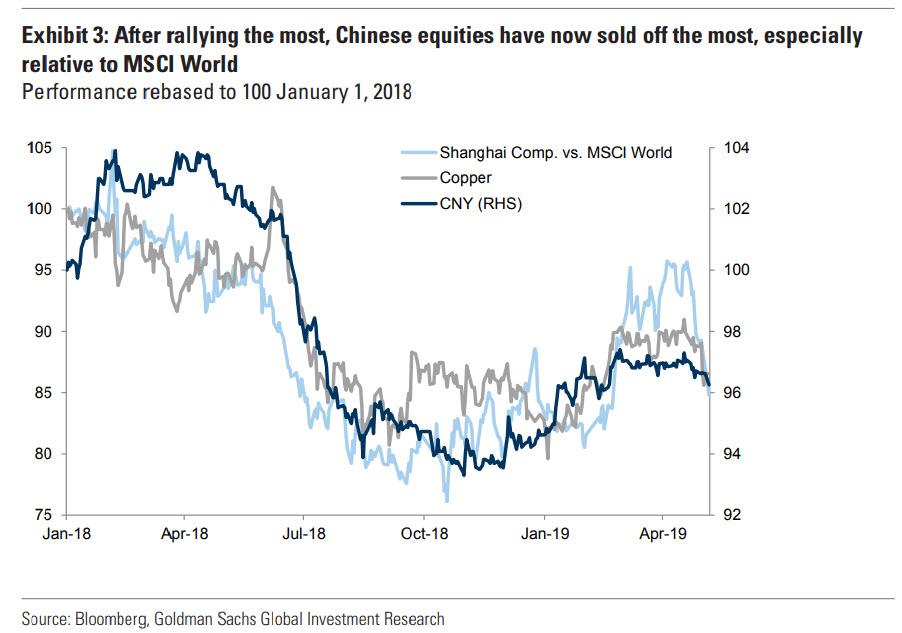

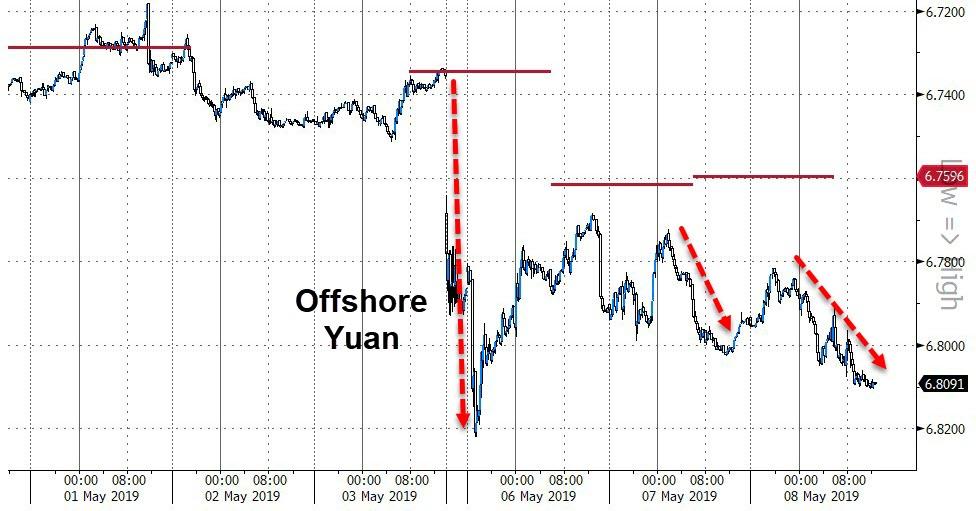

/Chinese yuan (ONSHORE) closed DOWN at 6.7824 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 61.22 dollars per barrel for WTI and 69.56 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7824 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8005 TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP THREATENS TO RAISE RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA

China responds to Trump as they are fully prepared for an escalated trade war:

(courtesy zerohedge)

ii)Then: bang!!

China boycotts the 10 yr auction as indirects (which is usually China) plunges. The bankers took up double to make up for the loss

(courtesy zerohedge)

iii)Goldman capitulates and now sees a greater chance that we will see a tariff increase on Friday

4/EUROPEAN AFFAIRS

i)ITALY

Major problems with the Italian coalition partners as well as Italian budget chaos brings the Italian 10 yr yield much higher to 2.69% and the spread between the German bund and Italian funds rise to 2.75%

( zerohedge)

ii)UK

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAQ/USA/IRAN

Pompeo makes a surprise Iraqi visit as they site Iranian escalation.

( zerohedge)

ii)Iran

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

( zerohedge)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading: last night

ii)Market data

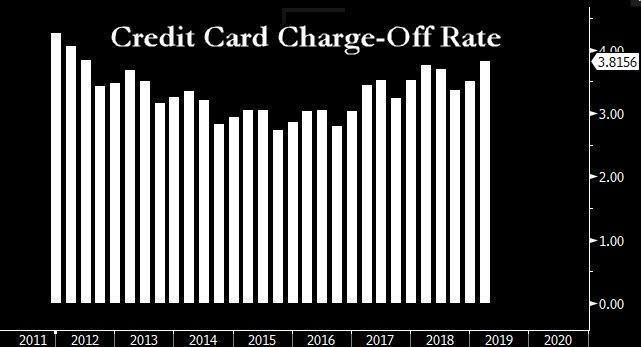

Credit card defaults climb as banks are hoarding the riskiest accounts.

(courtesy zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

a)California’s mandatory minimum wage at $15.00 is already starting to backfire.

( zerohedge)

b)We have been highlighting to you on several occasions that Trump’s new tariffs hurt the USA as much as China because it is the USA citizen that must pay for thee higher cost of goods.

( Tom Luongo)

SWAMP STORIES

i)The following is a huge story: Steel made a damning pre fisa confession that the dossier is political and must be out before Nov 8. Also the FBI retroactively classified this document.

my goodness.

( zerohedge)

i b)former FBI official states that James Comey is in a heap of trouble

ii) a Trump asserts executive privilege over the Mueller report and its underlying documents even though Barr released the report already to the public at large save the redacted stuff.

( zerohedge)

iib)Ridiculous!! The House Judiciary committee votes to hold Barr in contempt over the Mueller report which Barr refuses to hand over. This will end up in court and the Dems will lose

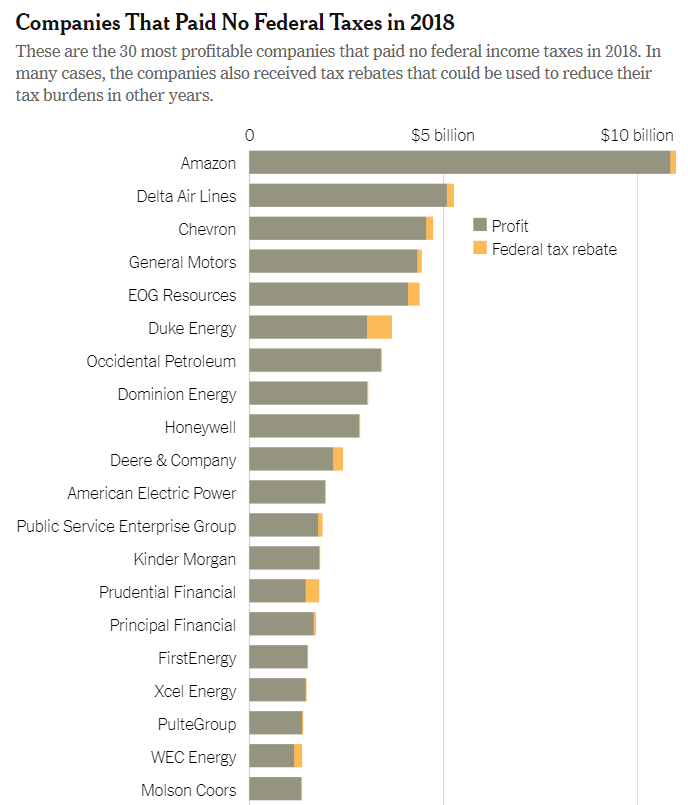

iii)The Democrats are now taking aim at corporations that pay zero Federal taxes (even though they probably have loses.

( zerohedge)

iv)trump had severe losses in his New York Times report. The losses stem from his casinos and airline endeavours.

He has done nothing wrong.

(courtesy New York Times/zerohedge)

Let us head over to the comex:

IT LOOKS LIKE THE RATS ARE FLEEING A SINKING SHIP!

Gold withdrawals;

i) We had 2 withdrawals:

Out of JPMorgan: 40,629.560 oz

ii) Out of Scotia: 6,001.06 oz

.

Deutsche Bank’s Crisis Will Likely Lead To U.S. and Global Banking Crisis

by Christopher Whalen, via TheAmericanConservative.com

Americans generally think of Europe first as a wonderful place to visit. They rarely ponder the economic and financial ties between the United States and European Union, but in fact these ties are extensive and significant to the stability of both economies.

One area of particular connection involves the large banks and companies that provide services on both sides of the Atlantic. It is this area of commercial finance that risks are actually growing to the United States—in large part due to political gridlock in Europe stemming from the 2008 financial crisis.

Credit market professionals have been aware of problems among the European banks for many years. Their lack of profitability, combined with high credit losses and a lack of transparency have created a minefield for global investors going back decades. Whereas the United States has a bankruptcy court system to protect investors, in Europe the process of resolving insolvency is an opaque muddle that leans heavily in favor of corporate debtors and their political sponsors.

When we talk about true mediocrity among European banks, one of the leading example are, surprisingly, German institutions. Germany, after all, has a reputation for being the economic leader of Europe and a global industrial power, thus the continued failures in the financial sector are truly remarkable.

The biggest example, Deutsche Bank, Germany’s largest bank, has had problems with capital and profitability going back decades.

But Deutsche Banks’s problems are not unique.

What is troubling and indeed significant for American policy makers, however, is the nearly complete failure of our friends in Europe to address their banking sector, either in terms of cleaning up bad assets or raising capital to enable the cleanup.

One of the political understandings that came out of the Basel III process (a regulatory regime first introduced in 2013 to promote stability in the international financial system) was that the United States would take a harder view on mortgage related exposures and particularly intangible assets like mortgage servicing rights. The Europeans, it is said by participants, agreed to take a tougher line on bad assets loitering inside banks and to particularly require banks to take a reserve against bad credits immediately.

Prior to 2018, when the president of the European Central Bank, Mario Draghi, directed EU banks to start recognizing bad credits, international accounting rules essentially allowed EU banks to ignore bad credits. Indeed, EU banks could pretend that loan payments were still being received. Loans that defaulted prior to 2018 were not included in the directive. Thus Europe has a decade of detritus sitting in the loan portfolios of many banks that is neither disclosed nor properly valued. Whereas in the United States banks must charge-off bad assets down to some expected recovery value, in Europe we extend and pretend.

Many observers were surprised several years ago when Chinese airline conglomerate HNA arrived on the scene as the new shareholder of Deutsche Bank, a significant global investment bank that provides a range of services in the United States. The German lender had been marketing an offering of new equity shares for years without luck, thus the arrival of the high-flying and highly-leveraged HNA was greeted with quiet gratitude in European capitals. No European politician wants to be caught dead talking about large banks in anything but the most responsible tones, thus nobody asked any questions about HNA or its owners.

Sadly the HNA equity investment in Deutsche Bank was financed with a lot of debt.When the Chinese firm started to literally implode two years ago due to massive debt payments on its $40 billion in obligations, it began to sell its shares in Deutsche Bank, creating the latest crisis for the chronically underperforming bank. Today HNA is being liquidated under the supervision of the Chinese government. And to this day, nobody among United States or European bank regulators really knows who owns the company that was briefly the largest shareholder of Deutsche Bank

The setback with HNA led to discussions of merging Deutsche Bank with Germany’s Commerbank, another poor performer among the country’s banking sector.

Again, German politicians led by Chancellor Angela Merkel refuse to even hint at public assistance for Deutsche Bank, but the mounting troubles with banks across Europe may force Merkel’s hand as it has in Italy.

Bank earnings in Europe are weak, notes veteran bank consultant Mayra Rodriguez Valladares. As she exlains in a recent Forbes column:

Unfortunately, many of European banks’ woes are of their own making. A host of regulatory and legal fines and ongoing money laundering investigations of several banks do not bode well for European earnings. According to a Moody’s Investors Services report: ‘European banks were fined over $16 billion from 2012 to 2018 related to money laundering and trade sanction breaches.’

Rodriguez Valladares notes that U.S. and EU banks are enormously intertwined, particularly in terms of funding and derivatives—two areas of keen interest to U.S. regulators. But the fact of the matter is that the EU banking system and the EU economy are still too weak to shoulder the burden of a general cleanup of bad credits in EU banks.

The economic reality and ugly politics are both too daunting for EU leaders to engage publicly on these issues. Indeed, German Finance Minister Olaf Scholtz, who is touted as a possible successor to Merkel, was attacked by opposition politicians because of the prospective job losses in a Deutsche-Commerzbank merger.

But sadly the union of two zombie banks was not to be. “Banking giant Deutsche Bank and its crosstown rival Commerzbank ended merger talks, leaving in tatters the German government’s hope to shore up both banks and create a banking powerhouse,” The Wall Street Journal reported on April 25.

So now the German government must try to identify another politically expedient way to hide the Deutsche Bank problem without resorting to an explicit state bailout. Not only is financial help for EU banks problematic politically, but the EU simply lacks the economic resources to clean up the broader asset quality problems affecting European banks.

The tendency of EU politicians to stick their heads in the sand when it comes to these issues represents a smoldering threat to global financial stability. Troubles affecting Deutsche Bank and other EU lenders could easily explode into financial contagion if markets decide to turn away from these banks à la Lehman Brothers. For American business leaders and political leaders, the festering problems in European banks are a source of potential risk that could cause significant economic problems for all of us. Stay tuned.

News & Commentary

Stocks Resume Slide on Tariff Worries; Dollar Dips

China vice premier going to U.S. for trade talks despite Trump threatsGold glitters in India during key festival as prices dip

Gold ends higher on U.S.-China trade-induced jittersWatch Video Here

Global Stock Sell-Off Exposes Stretched Valuations

A Synchronized Global Downturn Intensifies As JPM Global Manufacturing PMI Plunges

Silver Backwardation Signals Rally – Maguire

When The S&P Hit A Record High, The Only Buyer Was Buybacks; Everyone Else Was Selling

What’s Wrong With Mainstream Economics? Werner

American Scholars Say The Real Threat To The U.S. Is Russophobia

Recent Market Updates

– Global Gold Demand Gains In Q1, 2019: Central Banks Buy Gold Bullion and ETFs See Inflows

– Newstalk Interview: Investors Looking To Store Gold In Dublin Rather Than London

– Australia and Many Property Markets To Crash Like Ireland?

– Death of Inflation and the Death of Equities?

– SWOT Analysis: Venezuela Sells $400 Million Worth Of Gold Bullion

– World’s Central Banks Want More Gold – India May Buy 1.5M Ounces In 2019

– Russia’s 2019 Gold Rush Continues: Buys 600,000 Ounces of Gold In March

– When Should You Sell Your Gold and Silver? (GoldCore Video)

– Understanding Gold: A Step By Step Guide To Gold As An Asset Class

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

These two days will go down in infamy as they were the May Day massacre of silver in 2011 and the Bank of England’s gold sales in 1999

(courtesy zerohedge)

Craig Hemke: Two inglorious anniversaries for gold and silver

Submitted by cpowell on Tue, 2019-05-07 21:25. Section: Daily Dispatches

5:25p ET Tuesday, May 7, 2019

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing at Sprott Money, today recalls the anniversaries of the Bank of England’s infamous gold sales of 1999 and what he calls the May Day Massacre of silver by JPMorganChase in 2011.

His point, Hemke writes, is “to remind you that in 2019 the bullion banks and their enablers at the CME Group, the U.S. Commodity Futures Trading Commission, and in London continue to seek to dominate and control price. However, as with the London Gold Pool of the 1960s —

https://en.wikipedia.org/wiki/London_Gold_Pool

— this modern-day LBMA/Comex gold and silver pool will also reach a point of self-destruction.”

Hemke’s commentary is headlined “Two Inglorious Anniversaries” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/two-inglorious-anniversaries-craig-hemk…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

LAWRIE WILLIAMS: Equities dive, gold up, China buys more

Yesterday tended was an interesting one markets- wise. U.S. equities all fell sharply, followed overnight by their Asian counterparts, as President Trump’s belligerent statement on raising tariffs on some $200 billion of Chinese imports with a deadline on Friday re- ignited trade war fears. As Warren Buffett stated following the U.S. President’s announcement, a trade war between the world’s two biggest economies would be ‘bad for the whole world’.

Gold, on the other hand, after a fairly dismal start, began to trade upwards and was some $3 higher by the New York close, and then moved higher still after hours This morning it hit $1,290 in European trade and, interestingly with palladium falling sharply to below $1,300 the price differential between the two precious metals had come back to around $10. We predicted earlier this year that the gold price could exceed that of palladium again this year, and it wouldn’t now take much of a move in either metal’s price to bring this about. Sharp falls in auto sales globally, palladium’s biggest market, won’t be helping the catalytic metal’s demand picture.

Whether gold’s rise and the fall in equities was connected is uncertai, but probably the two were connected in some respects. However, there were a couple of other factors seen as gold price supportive. Indian demand and imports are reported by Bloomberg to have risen sharply in April, ahead of the Akshaya Tritya Festival. This is seen as an auspicious time to buy gold and silver in the sub- continent and, coupled with lower gold prices over the past few weeks, seems to have boosted demand. India used to be the world’s largest gold consumer, but has been comfortably overtaken in this position by China in recent years.

But there was also positive news for gold out of China as well. The nation’s central bank has been announcing monthly gold purchases again since December last year and in April it reported it added 14.93 tonnes of gold to its reserves– its highest monthly total since it commenced re-reporting monthly increases and the fifth successive month of reported increases. Of course we have always been of the opinion that the reporting of Chinese central bank gold increases is likely something of a fiction and that the nation’s true gold reserves are substantially higher than the estimated 1.911 tonnes if we take the IMF’s latest figures and add in the central bank’s reported monthly increases for March and April. This reported figure still puts China in 6th place among national holders of gold, almost 280 tonnes behind Russia in fifth pace, but we think China’s true gold reserve figure could be far higher, if one takes into account the nation’s track record of holding substantial amounts of gold in accounts it has, in the past, deemed not reportable to the IMF.

To set against these positives, global gold ETFs have seen some gold being liquidated out of their holdings – particularly from the largest of all, GLD in the USA. But at the moment central bank purchases do seem to be more than matching the gold ETF liquidations. It should be remembered though that big gold reductions in the gold ETF holdings back in 2011-2013 accompanied the gold price fall from its 2011 US dollar peak, although gold is riding high in some other currencies even now like the Australian dollar today.

According to the latest figures from the World Gold Council it is estimated that gold ETFs bled 16.3 tonnes in the first 4 months of 2019, led by GLD which shed 41 tonnes on its own. Since the beginning of May, GLD has seen liquidations of a further 6.75 tonnes, although yesterday saw a very small net deposit.

New gold supply is pretty flat at the moment given that there are few signifinant new gold miniing projects coming on stream and the price has not been high enough to stimulate amy additional scrap sales. If anything the global gold sector is going through a consolidation phase and our view is that global production is still increasing, albeit at a tiny rate – maybe 1% at most. Others consider peak gold is already with us, but however the global situation pans out, there is unlikely to be any significant boost in supply over the next few tears. Even if the gold price rises sharply the lead time taken to bring new projects into production is long. Indeed higher gold prices could conversely lead temporarily to a production downturn as miners open up lower grade sections to prolong mine lives. And lower grades at unchanged mill throughputs means lower output.

08 May 2019

-END-

-END-

Gold trading/

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7824/

//OFFSHORE YUAN: 6.8005 /shanghai bourse CLOSED DOWN 32.63 POINTS OR 1.12%

HANG SANG CLOSED DOWN 359.82 POINTS OR 1.23%

2. Nikkei closed DOWN 321.13 POINTS OR 1.46%

3. Europe stocks OPENED RED /EXCEPT GERMAN DAX

USA dollar index RISES TO 97.57/Euro RISES TO 1.1202

3b Japan 10 year bond yield: FALLS TO. –.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.97/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.22 and Brent: 69.56

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO –06%/Italian 10 yr bond yield UP to 2.69% /SPAIN 10 YR BOND YIELD DOWN TO 0.95%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.75: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.45

3k Gold at $1289.15 silver at: 14.93 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 20/100 in roubles/dollar) 65.29

3m oil into the 61 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.97 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0171 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1390 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.06%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

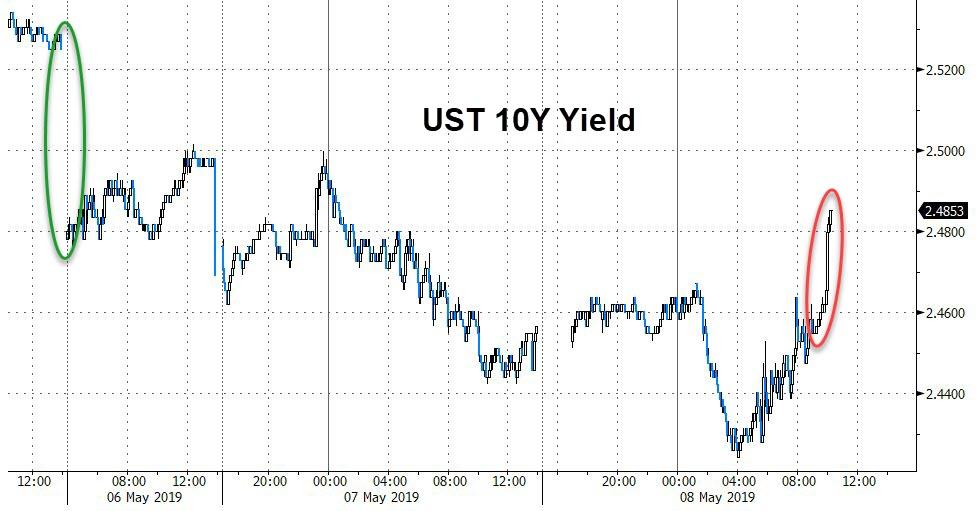

4. USA 10 year treasury bond at 2.43% early this morning. Thirty year rate at 2.84%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.1884..they are toast

Futures, Bond Yields Tumble As Traders Brace For Trade Talks Collapse

6 months of “trade talk optimism” is being unwound in hours before our eyes.

World shares dropped to five-week lows on Wednesday as S&P futures and European stocks continued their slide following steep declines in Asia, as markets started to accept that a deal with China now appears impossible, at least in the short term. Bond yields slumped, the dollar jumped, the safe haven yen surged to a six-week high against the dollar, the pound slipped as Brexit breakthrough hopes faded, the Kiwi tumbled after New Zealand unexpectedly cut interest rates overnight, while Chinese stocks dropped after China reported an unexpected contraction in exports.

As Bloomberg notes, Trump’s unexpected escalation on trade in the past few days caught global equity markets off-guard. Many had been testing record highs, seemingly priced to perfection on the assumption a deal between the U.S. and China would get done. Still, many refuse to give up hope, and JPMorgan boss Jamie Dimon still put the odds of that at 80%, and the S&P 500 has only fallen to levels seen a month ago – nonetheless investors will be on edge as China’s top trade negotiator visits Washington this week.

“The two largest economic powerhouses, the U.S. and China, either will be at a trade war or a trade peace and in reality there’s only a couple of people who know the answer to that and it isn’t those of us on Wall Street,” Larry Robbins, Glenview Capital Management’s CEO, told Bloomberg TV in New York. “It’s to be expected that there’s some volatility into this critical week.”

“I think it’s a major risk that Trump raises tariffs,” said Christophe Barraud, chief strategist at the Market Securities brokerage in Paris. “If that happens we can imagine that negotiations will break down, implying another few months of uncertainty… All-in all, bonds as well as other safe-havens such as yen, look set to benefit from this situation in the short-term.”

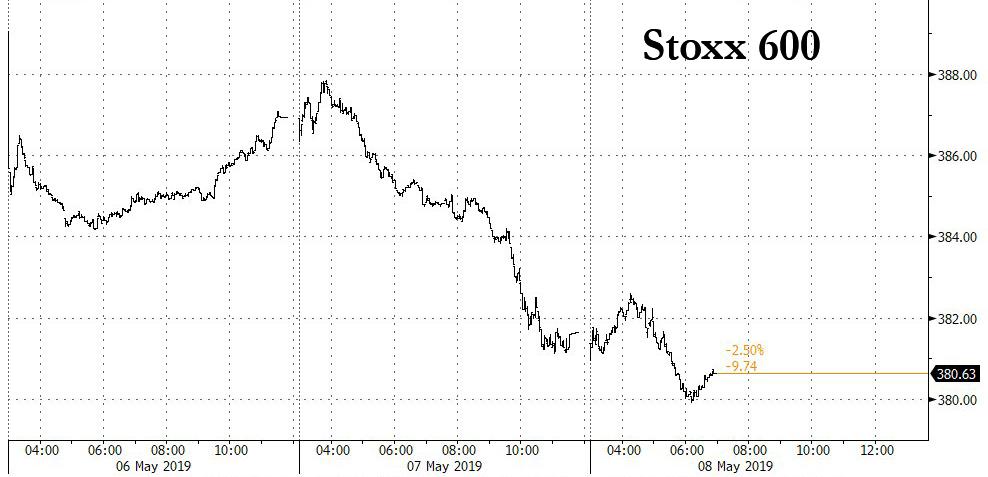

European stocks pared early gains, with the Stoxx 600 trading as low as -0.4% and down for 5 of the past 6 days, as China reiterated its position on trade negotiations ahead of potential U.S. imposition of additional tariffs on Friday. Risk sentiment deteriorated after Reuters cited sources saying China backtracked on nearly all aspects of U.S. trade deal last week even as it added that “U.S. officials have little hope that Liu will come bearing any offer that can get talks back on track, said two of the sources.”

While macro concerns and broader market moves eclipsed corporate results this week, earnings season continues apace. Commerzbank results were in line with estimates, while Siemens posted a beat. Toyota and Honda forecast profit and sales short of analysts’ estimates. Lyft exceeded sales expectations after the close on Tuesday but reported a staggering net loss and disappointed some in its tepid (lack of) profit outlook.

The European Bank for Reconstruction and Development (EBRD) trimmed its growth forecast for its region on Wednesday, citing a slowdown in global trade as well as the sharp economic deceleration in Turkey. Growth is forecast to recover in 2020 to 2.6%, the bank said, noting however that the outlook is still clouded by risks such as trade tensions between the United States and its major trading partners. “A widespread escalation of global protectionism remains a major concern,” the EBRD wrote in its report.

There are concerns also for Germany, the euro zone’s largest economy. While industrial output rose unexpectedly in March, the economy ministry warned that the outlook remained subdued. The data also follows weak industrial orders figures, and the downward revision of euro zone growth by the European Commission. All that reinforces a weak backdrop for the euro zone economy and a perception that the European Central Bank will keep rates at record low levels for longer than expected.

Earlier in the session, Asian stocks fell for a third day, with MSCI’s Asia-Pacific share index excluding Japan falling almost one percent to touch its lowest level since late-March, driven by healthcare and consumer staples firms. Almost all markets in the region were down, with Japan and China leading losses. The Nikkei dropped -1.5% and the Topix closed 1.7% lower, with Hoya Corp. and Takeda Pharmaceutical Co. among the biggest drags. The Shanghai Composite Index dropped 1.1%, as large banks and insurers drove declines. In India, the S&P BSE Sensex Index retreated 0.8%, led by Reliance Industries Ltd. and HDFC Bank Ltd. Elsewhere, Hong Kong’s Hang Seng Index dropped -1.2%; Hang Seng China Enterprises -1.5%; the CSI 300 dipped -1.4%, South Korea’s Kospi Index -0.4%; Kospi 200 -0.4%, Australia’s S&P/ASX 200 -0.4%; New Zealand’s S&P/NZX 50 +0.4%, India’s S&P BSE Sensex Index -0.8%; NSE Nifty 50 -0.7%.

Overnight, the yuan edged lower as data showed Chinese exports unexpectedly fell in April and imports rose. The latest Chinese trade data added to market jitters after it showed solid imports but an unexpected fall in April exports. Commenting on the latest Chinese trada data, Goldman writes that China’s export growth dropped to -2.7% yoy in April from +13.8% year-on-year in March, primarily on the fading of Chinese New Year distortions. The figure was below both consensus expectations and our below-consensus forecast. In contrast, imports rebounded +4.0% yoy in April, above consensus but roughly in line with our forecast. Distortions from the VAT cut effective on April 1 probably contributed to the rebound.

“Chinese exports were negative which suggests the world economy remains weak,” Barraud said noting that the latest manufacturing surveys had painted a subdued picture of new export orders worldwide. “As we saw with New Zealand today, central banks will remain tilted to the dovish side. They are trying to buy some kind of insurance against negative shocks.”

In rates, German yields steady, with 10-year BTP/Bund spread 3bps tighter at 263bps. In the US, yields dropped in 2-yr through 10-yr tenors, with the benchmark 10Y rate sliding to 2.42%, the lowest since the end of March. Germany’s 10-year bund yields hovered near five-week lows at -0.04 percent, not far from the 2-1/2 year low of -0.094 percent while Japan’s 10-year yield burrowed deeper into negative territory and last stood at minus 0.055 percent.

In currencies, demand for safe-havens boosted the Japanese yen which firmed 0.2 percent against the dollar at 110.07 yen, taking its gains to more than 1 percent this month and briefly rising above 110 vs the USD. The big move overnight was from the New Zealand kiwi which slumped more than 1% to a six-month low after New Zealand became the first country in the developed world to cut interest rates since the Fed turned tail on policy earlier this year, though other central banks, from Sweden to Canada have hinted at policy easing. The Reserve Bank of New Zealand lowered its official cash rate, before it pared most of the decline amid speculation that the central bank will refrain from easing policy further. The U.S. dollar was stronger versus most Group-of-10 peers as Treasuries edged lower, while sterling led losses as U.K. cross-party Brexit talks were inconclusive

New Zealand’s central bank governor Adrian Orr cited the U.S.-China trade dispute as a major risk for his country’s economy.

In emerging markets, the lira extended losses against the dollar amid the fallout from Turkey’s decision to re-run municipal elections in Istanbul. The South African rand strengthened as the country headed to the polls for a national election.

In commodities, Brent crude oil futures at $70.31 per barrel, 43 cents, or 0.6 percent above their last close.

On today’s calendar, Disney, Marathon Petroleum are among companies reporting earnings; the only economic data is the mortgage applications which rose 2.7% after dropping -4.3%

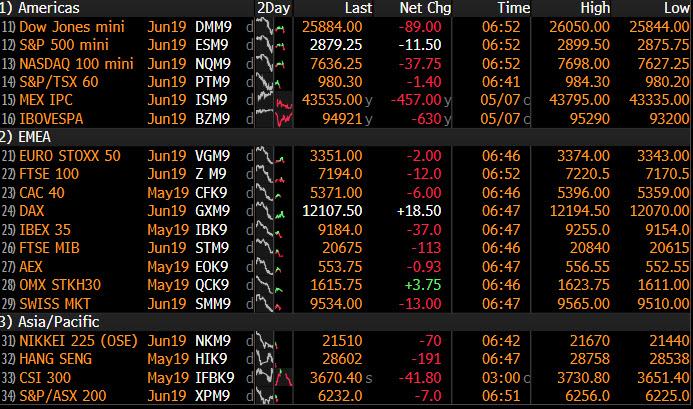

Market Snapshot

- S&P 500 futures 2,873, down -0.6%

- STOXX Europe 600 up 0.1% to 382.11

- MXAP down 1% to 159.02

- MXAPJ down 0.7% to 526.12

- Nikkei down 1.5% to 21,602.59

- Topix down 1.7% to 1,572.33

- Hang Seng Index down 1.2% to 29,003.20

- Shanghai Composite down 1.1% to 2,893.76

- Sensex down 0.7% to 38,009.06

- Australia S&P/ASX 200 down 0.4% to 6,269.15

- Kospi down 0.4% to 2,168.01

- German 10Y yield rose 0.7 bps to -0.031%

- Euro up 0.1% to $1.1206

- Italian 10Y yield rose 3.9 bps to 2.247%

- Spanish 10Y yield fell 1.4 bps to 0.95%

- Brent Futures up 0.1% to $69.95/bbl

- Gold spot up 0.2% to $1,287.12

- U.S. Dollar Index down 0.2% to 97.47

Top Overnight News from Bloomberg

- China, in a diplomatic cable on Friday, removed its commitments in the draft trade deal to alter laws to resolve key complaints made by the U.S., Reuters reported, citing three unidentified people in the U.S. government and private sector briefed on talks

- JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon put the odds of the U.S. and China reaching a trade deal at 80%, sounding a note of optimism even after the rising specter of tariffs roiled global markets

- Iran is scaling back its commitments under the 2015 nuclear deal in response to U.S. sanctions and will resume uranium enrichment beyond agreed limits in 60 days if European signatories don’t find a way to ensure it can sell oil and trade with the world

- President Donald Trump’s advisers are pushing him to defy congressional investigations in hopes of luring Democrats into escalating a fight that they say will turn voters against the party in the 2020 elections. The advisers are counting on news coverage of the battle with Congress distracting attention from candidates vying to replace Trump

- Spin, bluster and outright hostility marked the Italian government’s reaction to the latest European Union warning that the country’s fiscal situation is set to worsen this year and next. The backlash sets the stage for a replay of the budget conflict between Rome and Brussels that roiled markets last year

Asian equity markets were mostly negative as ongoing US-China trade uncertainty continued to take its toll on risk sentiment which resulted to heavy losses on Wall St and underperformance of the trade-sensitive sectors such as tech, industrials and materials, while the region also digested mixed Chinese trade data. ASX 200 (-0.4%) was led lower by weakness in tech, as well as disappointing corporate updates including CSR and Treasury Wine Estates. Nikkei 225 (-1.4%) was weighed by currency strength and with index heavyweight Fast Retailing subdued after a decline in April same store sales. Elsewhere, Hang Seng (-1.2%) and Shanghai Comp. (-1.1%) conformed to the downbeat tone due to the US-China trade tensions as some reports noted the possibility of an escalation is seriously increasing (potential retaliatory tariffs by China on US imports) and as Chinese media also suggested China is not afraid to fight and will do so if necessary. However, mainland markets have nearly fully recovered on some optimism from confirmation Premier Liu He will travel to Washington for trade talks this week and after the mixed trade data. Finally, 10yr JGBs were mildly higher due to the risk averse sentiment in the region but with gains later pared amid a softer 10yr auction result

Top Asian News

- Thailand Keeps Key Rate Unchanged as Economic Growth Risks Mount

- Bank of Thailand Holds Rate as It Forecasts Weaker Growth

- Apple Preps Push in India With Short List for First Retail Store

- Jokowi Set to Reboot Cabinet as Graft Probe Engulfs Ministers

Major European bourses have given up their early gains [Eurostoxx 50 -0.3%%] following on from a mostly downbeat Asia-Pac session, as sources released details regarding the break-down in US-China trade talks. Sentiment deteriorated as China reportedly backtracked on legal issues throughout text of proposed US trade agreement, affecting nearly every chapter. Furthermore, the sources stated that China looked for changes in the text of intellectual property protection and theft, technology transfer, financial service access and competition policy. Nonetheless, DAX (-0.3%) whilst in negative territory is modestly firmer than its peers, buoyed by optimistic German industrial output, whilst heavyweight Siemens (+4.7%) alongside Wirecard (+2.4%) also underpinned the index amid optimistic earnings, with the latter upgrading guidance. Sectors are relatively mixed with no stand-out out/underperformers. In terms of individual movers, Imperial Brands (-4.6%) shares fell despite optimistic earnings as its e-cigarette sales in the US were disappointing.

Top European News

- German Industrial Output Unexpectedly Gains in Euro-Zone Boost

- Steel Giant Flags Risks If Trade Deal ‘Doesn’t Get Sorted Out’

- May Faces Parliament With Labour Talks Stalling: Brexit Update

- Greece Lowers Surplus Targets in Test to Deal With Creditors

In FX, a relatively constrained 97.589-409 range in the DXY index is fairly reflective of the tentative tone in currencies ahead of the pivotal and potentially game-changing talks in Washington between top level US and Chinese trade negotiators as sourced headlines intimate that China retracted legal pledges in virtually all sections of the proposal document. Looking at a breakdown of the basket, the Dollar is mixed vs major counterparts with the safer-havens outperforming in contrast to high betas, predictably.

- NZD/AUD – The Kiwi has been the most volatile G10 unit for obvious reasons, with a swoon to circa 0.6530 lows vs its US peer and 1.0720 against the Aussie in the immediate aftermath of the 25 bp RBNZ rate cut that was rated as roughly 50-50 in terms of probability and was accompanied by a lower projected profile going forward. However, Nzd/Usd and Aud/Nzd have both reversed course rather sharply to around 0.6590 and 1.0640 respectively as RBNZ Governor Orr revealed in the post-meeting press conference and subsequent comments that the outlook appears more balanced than prior to the ease, with the Bank now inclined to monitor data as it unfolds. Meanwhile, Aud/Usd is sitting tight within a 0.7025-00 post-on hold RBA range and awaiting the SOMP on Friday in addition to the aforementioned US-China trade situation.

- GBP – Sterling remains vulnerable amidst the overall cautious risk environment and on Brexit uncertainty, as talks continue between the Conservative and Labour Parties, and while UK PM May battles to fend off latest leadership challenges. Indeed, Cable is now testing support ahead of 1.3000, such as the 30 DMA and a Fib (1.3036/1.3021), with Eur/Gbp nudging higher towards 0.8600 and the Pound not gleaning any support from firm Halifax house prices or decent BRC and Barclaycard retail surveys.

- CHF/JPY – As noted above, the Franc and Yen are both benefiting from risk-off flows, as Usd/Chf retreats from 1.0200+ to revisit recent lows near 1.0170 and Eur/Chf slips back below 1.1400. Meanwhile, Usd/Jpy is just hovering around 110.00 after breaching Fib and daily support at 110.44 and 110.31 respectively, and a dip to 109.90, with stops said to be sitting between 109.75-70.

- EUR – The single currency remains resilient either side of 1.1200 and 30 DMA resistance at 1.1224 vs Fib support at 1.1186 and lows seen earlier this week around 1.1160. A decent beat vs consensus in German ip has provided some traction against more Italian fiscal largesse.

- NOK – In contrast to the above, weak Norwegian manufacturing output has undermined the Nok and pushed the Eur cross back over 9.8000 vs Eur/Sek that remains sub-10.7500.

In commodities, choppy trade in the energy complex with Brent and WTI futures straddling just above USD 69.40/bbl and USD 61/bbl respectively amid the release of details regarding the deterioration of US-Sino trade discussions. The release of the a wider-than-forecast build in API stocks did little to sway prices in the immediate aftermath as the sector was overshadowed supply woes emanating from Libyan and Iranian tensions, Venezuelan sanctions and scope for OPEC to curb output till year-end. Yesterday also saw the release of the EIA Short-Term Energy Outlook which showed a raise in 2019 global oil demand expectations by 20K to 1.38mln, whilst 2020 demand forecasts were increased by 80K. Elsewhere, China’s trade balance showed that the country imported a record 10.7mln BPD of crude in April, +11%Y/Y and +15% M/M, albeit, ING notes that the strong oil numbers were likely due to heavy stockpiling ahead of Iranian waiver expiries. From a technical point, the benchmarks remain above their respective 50 and 200 DMAs (WTI: 60.95 and 60.75; Brent: 69.29 and 69.16 respectively, having formed a golden cross yesterday. Gold (+0.3%) largely benefits from the safe-haven flows amid the step-backs in US-China trade discussions and as US are set to hike tariffs on USD 200bln worth of Chinese goods at 12:01 ET tomorrow. Meanwhile, copper came off highs after sources reported that China’s backtracking in talks affected every chapter in the trade accord. The red metal did gain some impetus during Asia-Pac hours as imports from China topped estimates. Finally, iron ore prices rose to near five-year highs on supply woes after Vale, the worlds largest iron ore producer, lowered its production forecasts for the base metal.

US event calendar

- 7am: MBA Mortgage Applications, prior -4.3%

DB’s Jim Reid concludes the overnight wrap

As regular readers know, when I’m not travelling my wife and I try to bond for an hour a night in front of the telly with a good box set. Last night given that Liverpool were already 3-0 down to Barcelona from the first leg in the Champions League semi-final I said to my wife that I probably wouldn’t bother watching it and as such she’d lined up “Billions”. However at the last minute I said I’d watch the first 5 minutes while she ran a couple of errands. Luckily her errands took at least 7 minutes and an early goal left me postponing her. 90 minutes later she was still waiting to watch Billions as Liverpool mounted one of the greatest comebacks of all time winning 4-0 and reaching the Champions League final again in the most remarkable game I’ve seen given the context and remember I was at Istanbul in 2005. I still can’t believe what I watched. At least I know the soundproofing we put in so we couldn’t hear the kids banging on the non-insulated 100 year floorboards upstairs does work as I was screaming with joy at the telly in the 2nd half and no child stirred. Bronte the dog was a bit scared though and kept clawing me to make sure I was ok after each goal. So I’m a bit shattered and emotional this morning. Am looking forward to Billions tonight and will forgo the 2nd semi-final to get back in the family good books!!

Markets seem dull relative to the above but the reality is that there’s a lot going. The last 24 hours has seen a bit of a delayed reaction to Trump’s China tariff tweet from Sunday as markets decided to take the glass half empty view as opposed to Monday’s more half full take. Indeed the S&P 500 fell -1.65% for its biggest decline in over six weeks, though stocks again bounced into the close, rallying +0.75% in the final 20 minutes of trading to prevent yesterday from being the worst day since January 3. The moves still put the index below the lows of early Monday morning and -2.09% below Friday’s close. It wasn’t any better for the NASDAQ (-1.96%) or the DOW (-1.79%) with tech leading losses at a sector level – although the reality is that all sectors closed in the red. In fact, only 7% of S&P 500 companies advanced, the lowest rate of the year.

It was similarly bleak in Europe where the STOXX 600 fell -1.37% to cap a two-day decline of -2.24% which is the most since December 7. Bunds closed down at -0.038% after dropping 4.4bps yesterday while 10y Treasuries closed -1.6bps lower at 2.453% – although they were as much as -5.7bps off the morning highs. BTP yields rose +4.2bps (+8.4bps to Germany) on the general risk off and perhaps also as a result of the European Commission’s dreary new economic and budgetary forecasts. The details are below, but the most eye-catching headline concerned Italy’s government deficit, which the Commission now expects at 2.5% of GDP this year before rising to 3.5% of GDP next year, barring a policy change. Northern League head Salvini responded by insisting that the government will proceed with tax cuts, regardless of whether it causes the deficit to breach the treaty limit.

The VIX closed up over +3.88pts at 19.32, the sharpest move since December 24 and the suddenly back to the highest level since January 23. Similarly, the V2X in Europe is at the highest since January 10. High yield spreads also widened by +9bps and +7bps in Europe and the US, respectively. Meanwhile EM FX was down -0.34% with a basket of currencies now down at the lowest since December last year. WTI Oil also slumped -1.62%, not helped by news of increased supply out of Saudi Arabia.

Overnight markets in Asia are trading in a sea of red (a bit like Anfield last night) with the Nikkei (-1.63%), Hang Seng (-0.70%), Shanghai Comp (-0.11%) and Kospi (-0.38%) all down. The South China Morning Post this morning suggested that President Xi vetoed the further concessions demanded by the US negotiators last week and this is not helping sentiment. Elsewhere, futures on the S&P 500 (+0.03%) are trading flat suggesting a break in the declines for now. The New Zealand dollar is down -0.27% this morning as the central bank cut the key rate by 25bps to 1.50%.

Also in Asia we’ve had the conveniently timed April trade data released in China with the trade surplus standing at $13.84bn (vs. $34.56bn expected). This was driven by a drop in exports (-2.7% yoy vs. +3% expected) while imports rose (+4% yoy vs. -2.1% expected). Speaking in terms of trade with the US, exports declined -13.1% yoy in April; however, the decline in imports was larger at -25.7% yoy bringing the trade balance to $21bn (-5.1% yoy). The YtD 2019 surplus with the US stands at $83.5bn (+3.8% yoy) as exports to the US declined -10.1% yoy while imports dropped -30.2%. China’s onshore yuan is trading broadly unchanged (+0.07%).

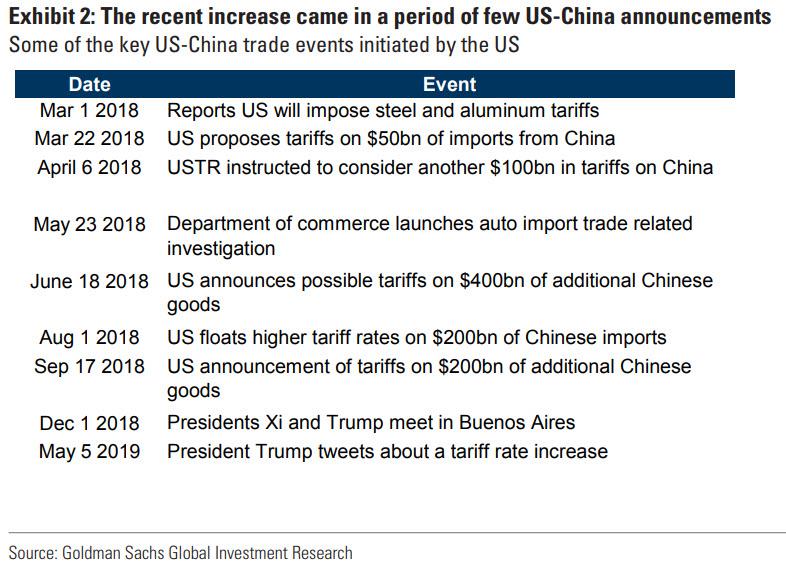

To be fair there wasn’t a lot of new news to report yesterday besides the ongoing trade-related rumbles. As of right now, China’s top trade negotiator Liu He is still due to travel to Washington tomorrow to meet with Lighthizer and Mnuchin. The suggestion is though that China is planning retaliatory tariffs immediately after the US increases theirs. This makes tomorrow and Friday’s meetings of critical importance and ultimately will dictate whether the threat is real or just hard ball negotiating tactics. Chinese state media has intensified its rhetoric, saying that “we will not take any step (that is) unfavourable to us (…) Do not even think about it.” MNI also reported yesterday that talks between China and the US could drag into 2020. Maybe the lessons learned from the long, drawn out and exhausting Brexit process will come in handy after all.

On a related note the auto tariffs deadline is suddenly just eleven days away so that is still lingering in the background, though there is certainly the possibility that a decision could slip beyond the deadline. There is some suggestion in the market that Trump is now less likely to move on auto tariffs if he’s renewing the trade battle with China, the view being there are only so many battles one can take on at once. On the other hand we have Mr Trump’s unpredictability to weigh up. We’ll see in the next couple of weeks.

Also fitting in with the negative sentiment yesterday were the latest European Commission forecasts that although just moved closer to market’s expectations seemed to weigh on the overall market mood. The highlights were a -0.1pp downgrade to the euro area growth forecast for this year (to 1.2%), driven by a -0.6pp cut to Germany’s forecast to 0.5% and a -0.1pp to Italy’s to 0.1%. The inflation forecast for this year stayed steady at 1.4%, but the 2020 figure was revised down -0.1pp to 1.4%.

Elsewhere planned comments from the Fed’s Clarida were on many people’s radar but they didn’t appear to diverge too much from the message from last week’s Fed meeting. He agreed with Powell’s assessment that soft inflation is “temporary” and spoke positively about global growth. He did note that there could be downside risks if trade discussion resolve negatively. Perhaps most interestingly, he emphasized that the Fed’s goal is to get inflation back to 2%, tacitly pushing back against the argument that the Fed should run the economy hot to make up for prior downside misses. As the Fed continues toward its highly-anticipated policy review, Clarida seems to be positioning himself as in favour of the status quo. He said that average inflation targeting or other make-up strategies “look great in the textbooks” but that there are “important implementation challenges that we would have to look at seriously before we would move away from our existing framework.”

Here in the UK it was a busy day for Sterling which closed down -0.17% after paring an early advance in the morning. The change in tone followed a steady release of Brexit headlines which included confirmation that a deal will not be agreed in time in order for the UK to avoid taking part in the European Parliament elections later this month. Headlines also confirmed what most expected and that is that cross party talks have still yet to yield any sort of consensus on moving forward. In addition, reports suggested (per Guardian) that the 1922 Committee is ever-closer to rewriting the rules to unseat PM May, with the latest unconfirmed reports saying that the committee is deadlocked at a vote of 8-8, so one more defection would be enough allow a challenge to May.

As for yesterday’s data, in the US the March JOLTS survey revealed that the number of job openings rose by 346k in March to 7.49 million, and more than expected. The quits rate did however hold steady at 2.3%. In Germany, factory orders in March were disappointing at just +0.6% mom (vs. +1.4% expected), albeit rising for the first time in three months.

Yesterday, Nick and Craig published a joint USD/EUR HY note revisiting Bs vs BBs in light of the spread ratio being at an extreme wide. The note argues that while the ratio alone optically favours Bs, further analysis suggests that both the yield environment and dispersion make this a more complicated topic. See the link here . A reminder that our global monthly credit chartbook was out last week in my absence (link here ) along with our monthly US credit strategy excel data release (link here ). Michal Jezek has also published a few IG/CDS note recently. 1) Rising Inequality among Corporate Bonds (Tue 7 May) – a deep dive into IG bond spread dispersions over time, demonstrating stronger preference for quality in the recent rally vs. comparable periods last year (“quality” includes CSPP eligibility). 2) Carving Carry-Neutral Macro Credit Shorts (Mon 6 May) – a macro credit piece with most recent views, recommending efficient shorts that do not consume carry. 3) Global Issuance and Fund Flows (Fri 3 May) – big picture of global supply and demand in credit across currencies. So plenty of stuff from the team for those interested in credit.

To the day ahead now, where this morning we’ll get March industrial production data out of Germany and April house price data in the UK. There is nothing of note in the US this afternoon however the Fed’s Brainard is due to speak just after lunch. Prior to that we’re due to hear from the ECB’s Draghi in Frankfurt at a student’s event, while the BoE’s Ramsden speaks this morning. South Africa’s national and provincial legislative elections are also due today, while US Secretary of State Pompeo is due to travel to London and meet with PM May.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 32.63 POINTS OR 1.12% //Hang Sang CLOSED DOWN 359.82 POINTS OR 1.23% /The Nikkei closed DOWN 321.13 POINTS OR 1.46%//Australia’s all ordinaires CLOSED DOWN .50%

/Chinese yuan (ONSHORE) closed DOWN at 6.7824 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 61.22 dollars per barrel for WTI and 69.56 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7824 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8005 TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP THREATENS TO RAISE RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

i)China/USA

China responds to Trump as they are fully prepared for an escalated trade war:

(courtesy zerohedge)

China Responds To Trump: “We Are Fully Prepared For An Escalated Trade War”

Though Steven Mnuchin insisted on Monday that the White House’s plan to impose more tariffs on Chinese goods was free from market-related considerations, after another punishing session for markets on Tuesday, it’s looking like the White House has reverted to its strategy of using optimistic trade rhetoric to jawbone the markets higher.

But this time around, Beijing has apparently lost its willingness to play along. To wit, an editor from the Global Times, seen as a mouthpiece for the Communist Party, responded to Trump’s claim that China wants a deal by insisting that the exact opposite is true.

China is “fully prepared for an escalated trade war” he said, and added that Beijing is betting on the fact that its political system will ultimately give China more leverage over Trump (the opposite of the market consensus).

Hu Xijin 胡锡进@HuXijin_GTChina has fully prepared for an escalated trade war. It is a new strategy of China to engage in trade talks while fighting a trade war. I think China bets on the fact its politics is more powerful than US politics. Trade war will be decided by domestic politics eventually.

Traders largely ignored the tweet, as the market continued to ramp ahead of the arrival of China’s trade delegation in Washington.

Markets also appeared to ignore reports in Chinese media published earlier in the session warning that Beijing is already preparing retaliatory tariffs should Trump follow through with his promise to raise tariffs on $200 billion in Chinese exports on Friday.

end

Then: bang!!

China boycotts the 10 yr auction as indirects (which is usually China) plunges. The bankers took up double to make up for the loss

(courtesy zerohedge)

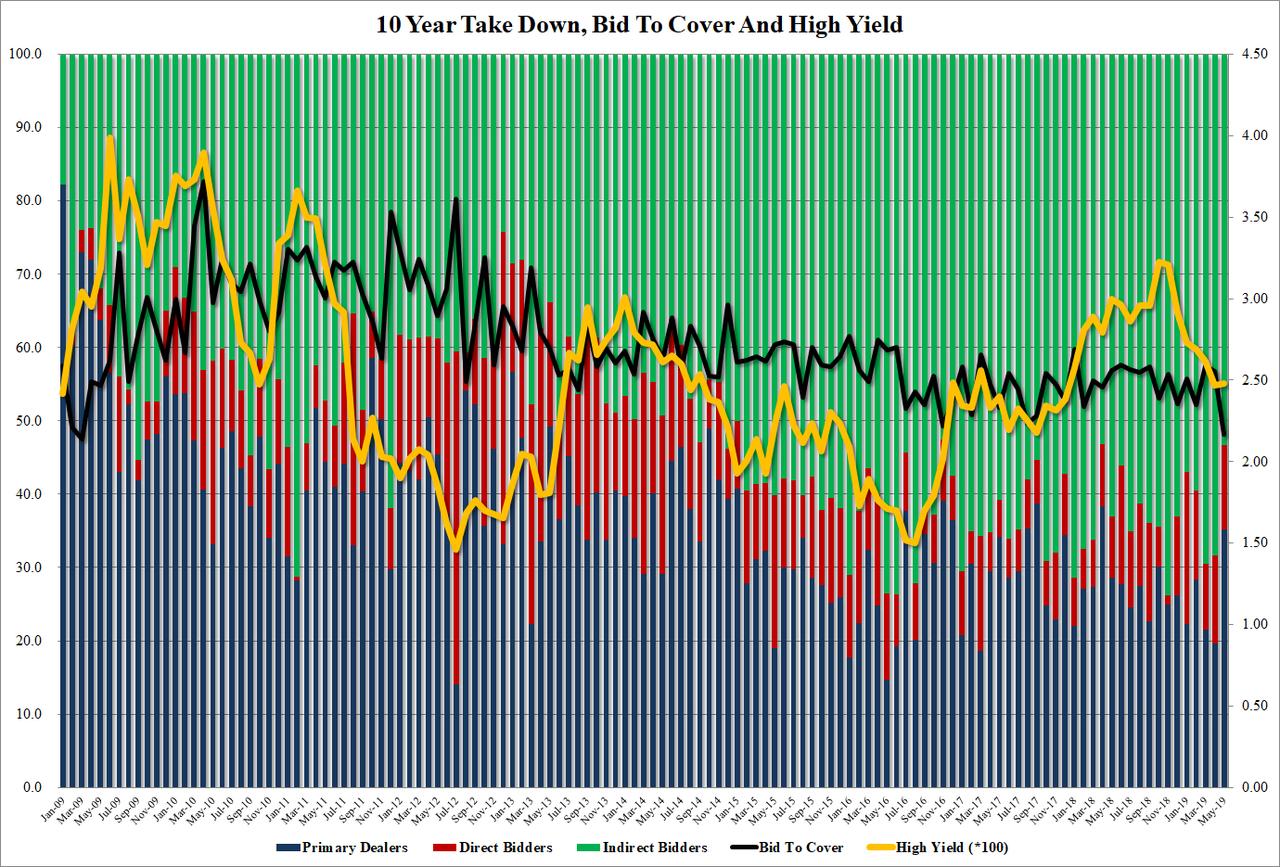

China Boycotts Shockingly Ugly, Tailing 10Y Auction: Indirects Plunge, Lowest Bid/Cover In 10 Years

There is just one word to describe today’s just concluded sale of $27 billion in 10Y notes: disastrous.

Sparking immediate speculation if China simply decided not to show up for today’s budget deficit funding operations, the 10Y auction was ugly from top to bottom. The high yield of 2.479% tailed the When Issued 2.465% by a whopping 1.4bps, the biggest tail since August 2016. The tail was so big that whereas the auction was initially expected to price at the lowest yield since December 2018, as the WI was below last month’s 2.476%, the disappointing reception meant that the yield actually rose compared to last month.

But if the tail was bad, the internals were far worse, starting with the Bid to Cover, which plunged from 2.55 to 2.17. There is no point in comparing this to the recent average, because this was the lowest BTC going all the way back to March 209, or a decade earlier.

As for the reason for speculation if China bailed, one look at the Indirects, or foreign official authorities were China traditionally dominates, showed it tumbling from 68.4% to 53.3%, the lowest since November 2016. And with Directs doing their best to offset the collapse in Indirects, and taking down 11.5%, or in line with last month, Dealers were forced to hold 35.2%, almost double April’s 19.6%, and the highest since April 2018.

Overall, a very ugly auction, and if China wanted to send a message to the US, it clearly succeeded judging by the violent repricing in the 10Y whose immediately yield promptly blew out by over 2 bps.

Goldman Capitulates, Now Sees Tariff Increase As The Base Case

Just call it Gartman Sachs.

The past 12 months have been a catastrophe for anyone who followed Goldman’s advice or trade recommendations. And for the bank which until last December predicted 4 rate hikes in 2019 (and now barely sees one more, some time in late 2020), and has been pitching a dollar short for as long as we can remember, resulting in substantial losses to anyone who listened as the greenback has continued to rise, it’s time to admit it has been wrong on arguably the most important issue facing the market.

As Goldman’s chief political economist, Alec Phillips writes, when President Trump “surprised” those gullible enough to believe a trade deal with China was imminent, and announced on Sunday (May 5) his intention to increase tariffs on $200bn of imports from China starting on Friday (May 10), Goldman “believed that there was a 40% probability that the increase would take place and that it was instead slightly more likely that the tariff increase would be narrowly avoided.”

Since then however, Phillips writes that two key developments suggest the outlook has worsened incrementally.