GOLD: $1284.60 UP $4.00 (COMEX TO COMEX CLOSING)

Silver: $14.77 DOWN 9 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1283.90

silver: $14.76

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 3/5

EXCHANGE: COMEX

CONTRACT: MAY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,279.400000000 USD

INTENT DATE: 05/08/2019 DELIVERY DATE: 05/10/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 3

737 C ADVANTAGE 5 2

____________________________________________________________________________________________

TOTAL: 5 5

MONTH TO DATE: 176

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 5 NOTICE(S) FOR 500 OZ (0.0155 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 176 NOTICES FOR 17600 OZ (.5474 TONNES)

SILVER

FOR MAY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

49 NOTICE(S) FILED TODAY FOR 265,000 OZ/

total number of notices filed so far this month: 3328 for 16,640,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$6106 UP $107.00

Bitcoin: FINAL EVENING TRADE: $6136 UP $115

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A TINY SIZED 685 CONTRACTS FROM 199,497 DOWN TO 198,782 ACCOMPANYING YESTERDAY’S 3 CENT FALL IN SILVER PRICING AT THE COMEX. ,LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER BUT IT NOW COMMENCES FOR GOLD. TODAY WE705RRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 730 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 730 CONTRACTS. WITH THE TRANSFER OF 730 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 730 EFP CONTRACTS TRANSLATES INTO 3.650 MILLION OZ ACCOMPANYING:

1.THE 3 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 18.225 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MOAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

9538 CONTRACTS (FOR 7 TRADING DAYS TOTAL 9538 CONTRACTS) OR 47.69 MILLION OZ: (AVERAGE PER DAY: 1362 CONTRACTS OR 6.81 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 47.69 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.81% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 788.52 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 685 WITH THE 3 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 730 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE GAINED A TINY SIZED: 45 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 730 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 685 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 3 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.89 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.999 BILLION OZ TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 49 NOTICE(S) FOR 245,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 18.225 MILLION OZ ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A HUMONGOUS SIZED 12,786 CONTRACTS, TO 462,825 DESPITE THE FALL IN THE COMEX GOLD PRICE/(AN DECREASE IN PRICE OF $3.70//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 3268 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 8232 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 462,825. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 20,152 CONTRACTS: 12,786 OI CONTRACTS INCREASED AT THE COMEX AND 7366 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 20,152 CONTRACTS OR 2,015,200 OZ OR 62.68 TONNES. YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF ONLY $3.70….AND WITH THAT FALL, WE HAD A HUMONGOUS GAIN IN TONNAGE OF 62.58 TONNES!!!!!!.??????????????????????????????????????????

AS YOU WILL SEE, THE CROOKS HAVE NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER A NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 41,650 CONTRACTS OR 4,165,000 OR 129.54 TONNES (7 TRADING DAYS AND THUS AVERAGING: 5950 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAYS IN TONNES: 129.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 129.54/3550 x 100% TONNES =3.64% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1945.11 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUGE SIZED INCREASE IN OI AT THE COMEX OF 12,786 DESPITE THE FALL IN PRICING ($3.70) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7366 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7366 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC SIZED GAIN OF 20,152 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7366 CONTRACTS MOVE TO LONDON AND 12,786 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 62.68 TONNES). ..AND THIS HUGE DEMAND OCCURRED WITH A FALL IN PRICE OF $3.70 IN YESTERDAY’S TRADING AT THE COMEX. NO DOUBT THAT A STRONG PERCENTAGE OF OI GAIN WAS DUE TO THE CONTINUING OF THE SPREADING OPERATION AS I HAVE OUTLINED ABOVE.

we had: 5 notice(s) filed upon for 500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $4.00 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 739.64 TONNES

IT LOOKS LIKE WE HAVE REACHED THE BOTTOM OF THE BARREL FOR PHYSICAL GOLD BEING SUPPLIED TO THE CROOKS.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 9 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 316.582 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 685 CONTRACTS from 199,467 DOWN TO 198,782 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER BUT HAVE NOW MORPHED INTO GOLD..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 730 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 730 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 685 CONTRACTS TO THE 730 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL GAIN OF 45 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 0.225 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 18.225 MILLION OZ FOR MAY

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 3 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 730 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

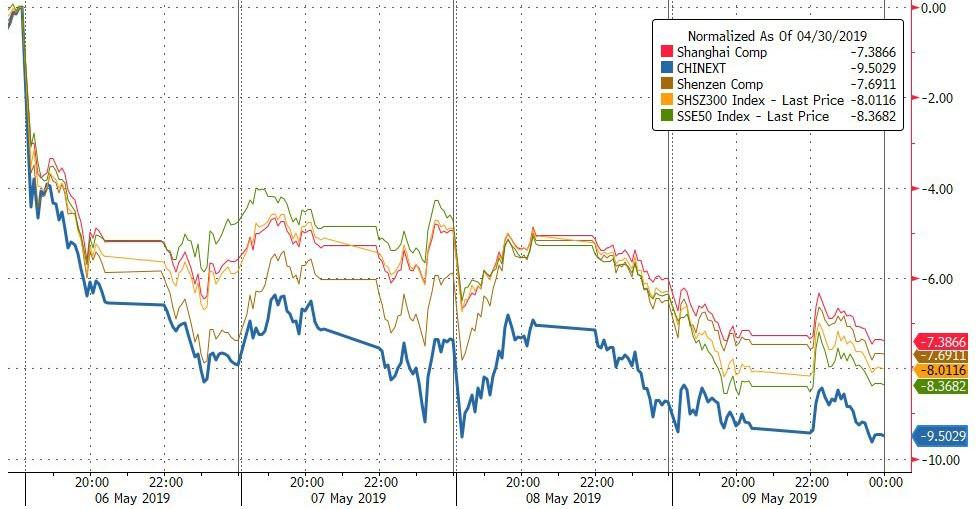

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 42.80 POINTS OR 1.48% //Hang Sang CLOSED DOWN 692.13 POINTS OR 2.39% /The Nikkei closed DOWN 200.46 POINTS OR 0.93%//Australia’s all ordinaires CLOSED UP .40%

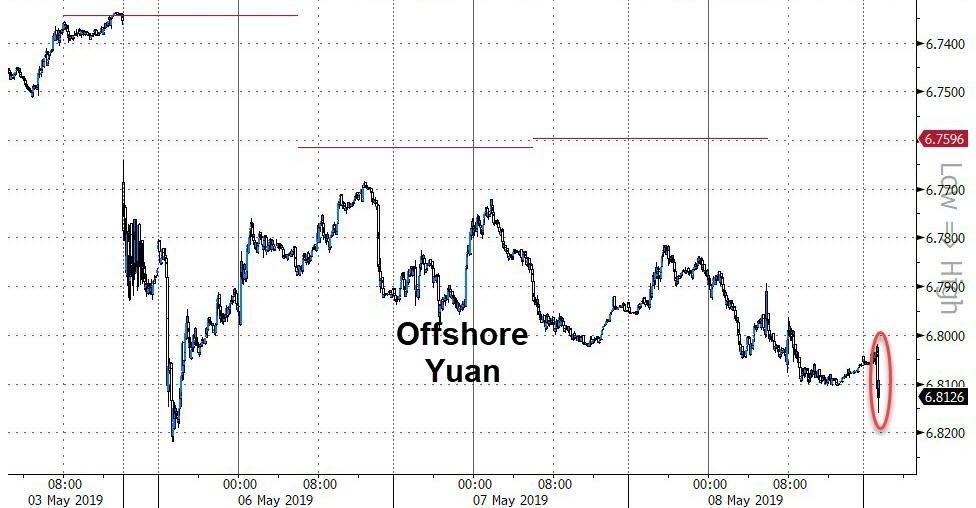

/Chinese yuan (ONSHORE) closed DOWN at 6.8243 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 61.92 dollars per barrel for WTI and 70.47 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8243 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8483 TRADE TALKS STILL ON//TRUMP THREATENS A NEW 25% TARIFFS ON FRIDAY/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP THREATENS TO RAISE RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA/FED

Interesting: China is playing hardball because they read us: namely that the USA economy is not doing too good. Also the fact that Trump is asking the Fed’s Powell to lower interest rates is a powerful indicator that the uSA economy is waning.

( zerohedge)

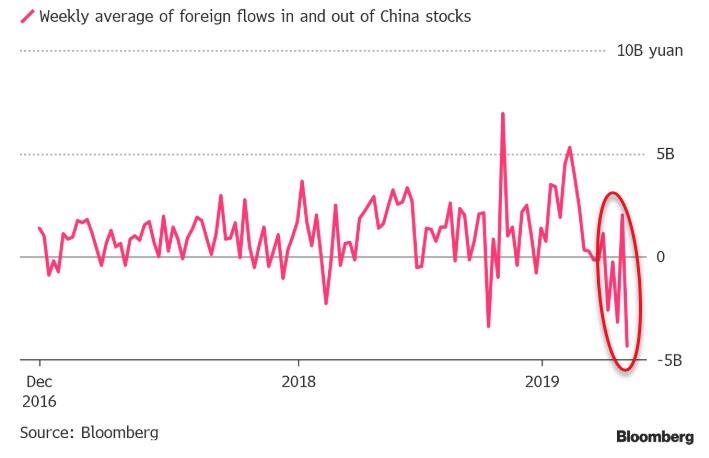

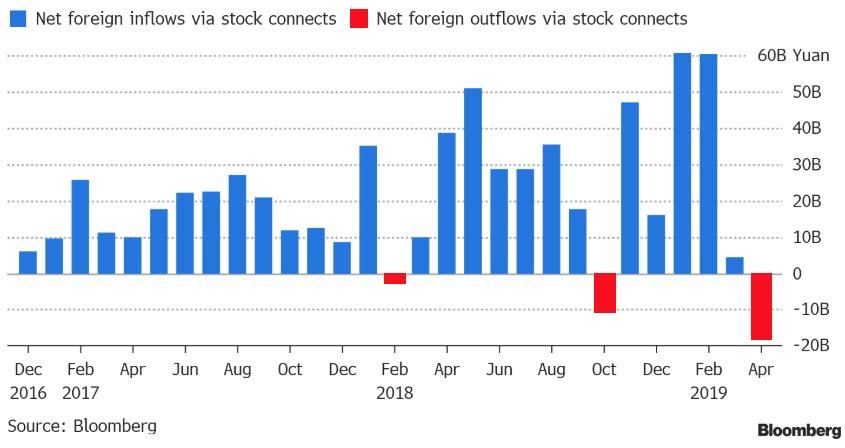

ii)CHINA/FOREIGNERS

Foreigners are dumping Chinese stocks with reckless abandon as they are frightened ahead of the expected tariff increase.

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

This is serious stuff: The USA threatens the UK over their potential of Huawei in the 5G wireless space

( Mish Shedlock/Mishtalk)

ii)Europe/Iran/USA

Trump’s plan to issue sanctions on Iran’s base metals industry is a stroke of genius. The aim is to cripple their domestic industry as over 600,000 Iranians are employed in this sector. Europe is standing strong as they reject Iranian ultimatums on the nuclear deal. Iran had given Europe a 60 day notice that they need sanctions relief or else…

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)ISRAEL GAZA/WEST BANK/PALESTINIANS

Israeli Newspaper leaks terms of Trump’s new Middle East Peace Plan between Israel, Gaza and the Palestinians in the West Bank. It is interesting but I doubt if Hamas in Gaza will entertain such a project

( Middle East Monitor)

iii)TURKEY

The lira plummeted to 6.24 which causes citizens to bail on its currency as they desperate try to convert to dollars that which is in low supply.

Remember: Turkey has about 11 billion in ture asset reserves of which gold, at 511 tonnes is around 24 billion dollars. Turkey will never sell an ounce of gold contrary to the doorknob Maduro in Venezuela. Turkey must face China and Russia and then default on its western assets. This will break most of the European banks.

(courtesy zerohedge)

6. GLOBAL ISSUES

i)A good global Bellwether on the shape of economies and growth for the world.

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA/USA

Trump now turns on Bolton for accusing him of trying to start a war in Venezuela according to the Washington Post

( zerohedge)

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading: last night

“Trump last night: China broke the deal and they will be paying..”

(zerohedge)

ii)Market data

a)The Fed are just not getting the inflation traction that they need: core PPI records its slowest growth in 11 months

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

SWAMP STORIES

So true: where the USA is headed as we enter the 2020 election cycle.. Will the electorate see through the chaos created by the Democrats.

( Theodore Schatt)

Let us head over to the comex:

THE COMEX DATA FOR SOME REASON HAS NOT BEEN SUPPLIED BY THE CME BY THE TIME I USUALLY PUBLISH

THE DATA IS IMPORTANT AND I WILL UPDATE AS SOON AS IT ARRIVES FROM THE CROOKS.

IT LOOKS LIKE THE RATS ARE FLEEING A SINKING SHIP!

Gold withdrawals;

i) We had 0 withdrawals:

.

GOLD SUPPRESSION IS “THE BIGGEST ISSUE IN THE WORLD TODAY” – CHRIS POWELL OF GATA

– GOLD PRICE SUPPRESSION is “the BIGGEST ISSUE in the WORLD … it involves the valuation of all capital, labor, goods and services in the world and these valuations are being set in a really imperialistic and totalitarian way and not in an open and transparent way & we think this is evil

– Brief introduction to Chris Powell, Treasurer and Secretary of GATA and Bill Murphy of GATA and LeMetropoleCafe.com, two of the most important financial whistle blowers of recent years

– GATA’s tireless and courageous campaign for freely traded gold, silver and foreign exchange markets with little support from ‘Main Street, Wall Street, most of the gold industry and most of the media

RECEIVE LATEST GOLD & SILVER VIDEO NEWS UPDATES FROM GOLDCORE – SIGN UP HERE

– Why do central banks and “officialdom” manipulate gold and silver prices lower?

– “I could not be more disappointed with and contemptuous of 99% of the mainstream financial news organizations will not touch the issue of governments rigging markets”

– Voluminous evidence that GATA.org have amassed over the years have been published and sent to key financial press and media

– Central bankers and government insiders are on record re manipulation including Alan Greenspan- “Central banks stand ready to lease gold in increasing quantities should the price rise.” Greenspan testified to Congress in July 1998

– “Joint intervention in gold sales to prevent a steep rise in the price of gold, however, was not undertaken. That was a mistake.” Paul Volcker, reflecting on an international currency revaluation in 1973 (wrote in memoirs published by the Nikkei Weekly in Japan in November 2004)

– History of gold throughout history, through to Roosevelt and Nixon going off the Gold Standard and the Gold Exchange Standard- History of suppression including the London Gold Pool, creation of gold futures market, Exchange Stabilization Fund (ESF), Working Group on Financial Markets aka the Plunge Protection Team (PPT)

– Grossly unfair for any one nation to have “exorbitant privilege” of the ability to issue the sole reserve currency exclusively as you could EXPROPRIATE THE WORLD THAT WAY” as was done by the Nazis in World War II. Primary mechanism of Nazi expropriation of Europe was monopolising the banking systems and currency rigging thus weakening the conquered nations currencies versus the Deutsche Mark

– The original must read book of Ferdinand Lips on the history of “Gold Wars” – the forerunner to Jim Rickards and his books including Currency Wars

– U.S. diplomatic cables were leaked by Wikileaks and one from an official in the British Embassy to the State Department stated that they had surveyed the bullion banks and they were of the view that if gold futures were started, “they would be able to inject so much volatility into the gold price that they could scare ordinary investors away from the precious metal”

– Gold trades completely counter intuitively and frequently falls with massive concentrated bouts of selling of gold futures (billions in seconds) frequently despite very positive gold news

– “Flash crashes” done “to get the price down” and therefore likely governments and central banks

– Recent developments including ‘Irish Cuban American’ Senator Mooney’s recent support for the GATA cause and questions to the CFTC, the FED and Treasury regarding government manipulation of the gold prices

– The CME Group, which operates the major futures exchanges in the U.S., has recently renewed what it calls its ‘central bank incentive program’, which gives enormous volume trading discounts to governments and central banks for surreptitiously trading all the futures markets. The CME group has created mechanisms for secret trading by governments to get discounts while trading gold and silver futures in the U.S.

– Follow GATA for the hugely important information imparted by them, subscribe, donate on GATA.org

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

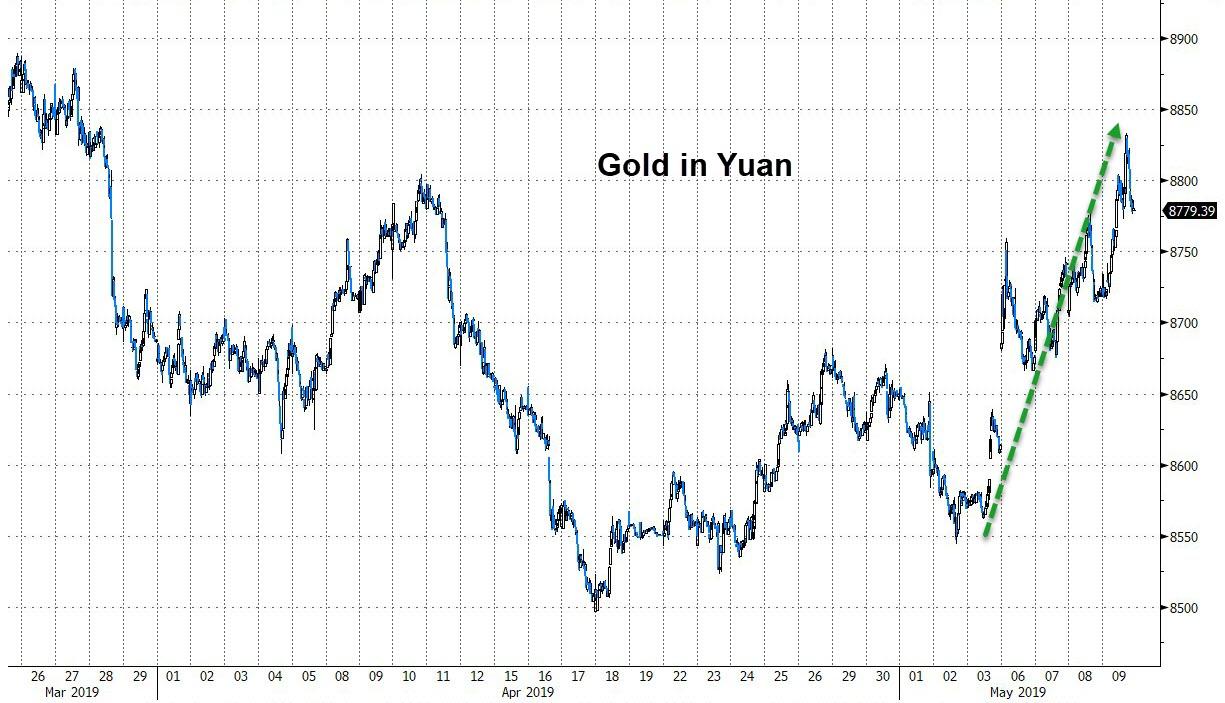

We brought this story to you yesterday but it is worth repeating. China announces its 5th straight increase in reserves by 14.93 tonnes. However they are not including all of the gold that they produce which is around 33 tonnes per month. Eventually China will announce their true hoard.

(courtesy London’s Financial Times/Sanderson)

China announces fifth straight month of growth in gold reserves

Submitted by cpowell on Wed, 2019-05-08 13:57. Section: Daily Dispatches

China’s Central Bank Stocks up on Gold as It Seeks to Diversify

By Henry Sanderson

Financial Times, London

Wednesday, May 8, 2019

China’s central bank added gold to its reserves for the fifth month in a row in April, the latest emerging market central bank to stock up on the yellow metal.

The People’s Bank of China said its gold reserves rose to 61.1 million ounces last month, an increase of 480,000 ounces from March, and bringing its total gold holdings to about $78.3 billion. …

… For the remainder of the report:

https://www.ft.com/content/860a418c-7172-11e9-bf5c-6eeb837566c5

end

This should be good!! Congressman Mooney Rep West Virginia (R) proposes in new legislation a complete and full audit of the gold owned by the USA and that covers leases and swaps with other entities.

(courtesy Money Metals News/ Eagle Idaho/Stefan Gleason/GATA)

Congressman proposes U.S. gold audit that covers leases, swaps

Submitted by cpowell on Wed, 2019-05-08 16:15. Section: Daily Dispatches

From Money Metals News Service, Eagle, Idaho

Wednesday, May 8, 2019

WASHINGTON — U.S. Rep., R-West Virginia, this week introduced legislation to provide for the first audit of United States gold reserves since the Eisenhower administration.

The Gold Reserve Transparency Act (H.R. 2559) — backed by the Sound Money Defense League and government accountability advocates — directs the comptroller of the United States to conduct a “full assay, inventory, and audit of all gold reserves, including any gold in ‘deep storage,’ of the United States at the place or places where such reserves are kept.”

…

HR 2559 requires more than just a physical assay, inventory, and audit, however. Even if all United States gold can be physically accounted for, it may nevertheless be encumbered with third-party obligations — or otherwise be impaired by bank financialization.

Therefore, Mooney’s gold audit bill also requires “a full accounting of any and all sales, purchases, disbursements, or receipts … a full accounting of any and all encumbrances, including those due to lease, swap, or similar transactions presently in existence or entered into” in the past 15 years, and “an analysis of the sufficiency of the measures taken to ensure the physical security of such reserves.”

Over the years the U.S. Treasury has faced allegations that it has sold, swapped, leased, or otherwise placed encumbrances upon some of America’s gold reserves. …

… For the remainder of the report:

https://www.moneymetals.com/news/2019/05/08/legislation-requires-audit-u…

* * *

end

-END-

Gold trading/

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

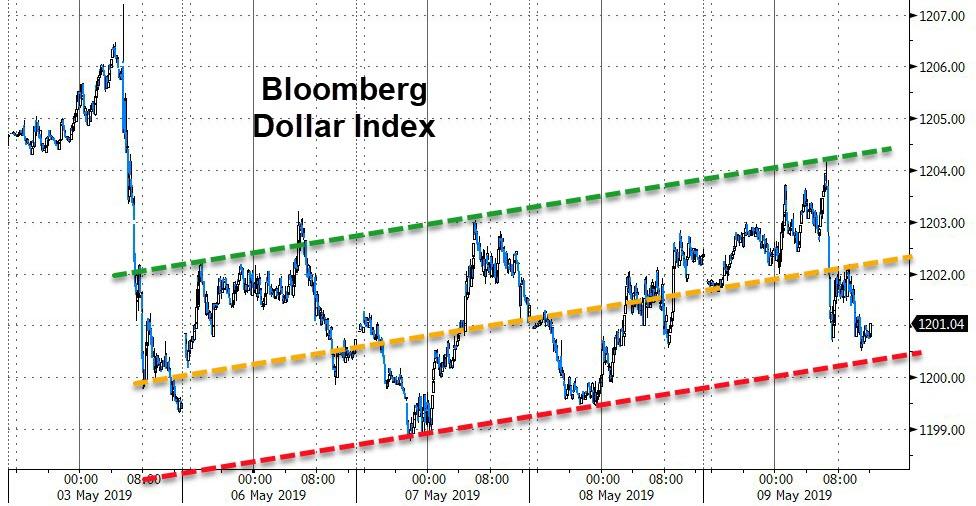

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.8243/

//OFFSHORE YUAN: 6.8483 /shanghai bourse CLOSED DOWN 32.63 POINTS OR 1.12%

HANG SANG CLOSED DOWN 692.13 POINTS OR 2.39%

2. Nikkei closed DOWN 200.46 POINTS OR 0.93%

3. Europe stocks OPENED RED /

USA dollar index FALLS TO 97.60/Euro FALLS TO 1.1189

3b Japan 10 year bond yield: FALLS TO. –.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.97/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.92 and Brent: 70.47

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO –06%/Italian 10 yr bond yield UP to 2.67% /SPAIN 10 YR BOND YIELD DOWN TO 0.96%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.73: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.52

3k Gold at $1283.35 silver at: 14.83 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 21/100 in roubles/dollar) 65.28

3m oil into the 61 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.78 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0185 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1396 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.06%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.45% early this morning. Thirty year rate at 2.87%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.2307..they are toast

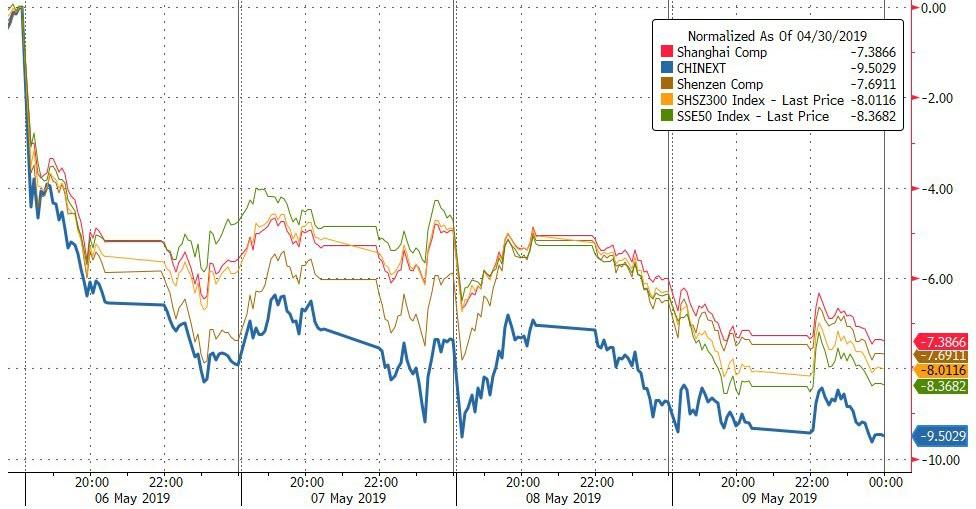

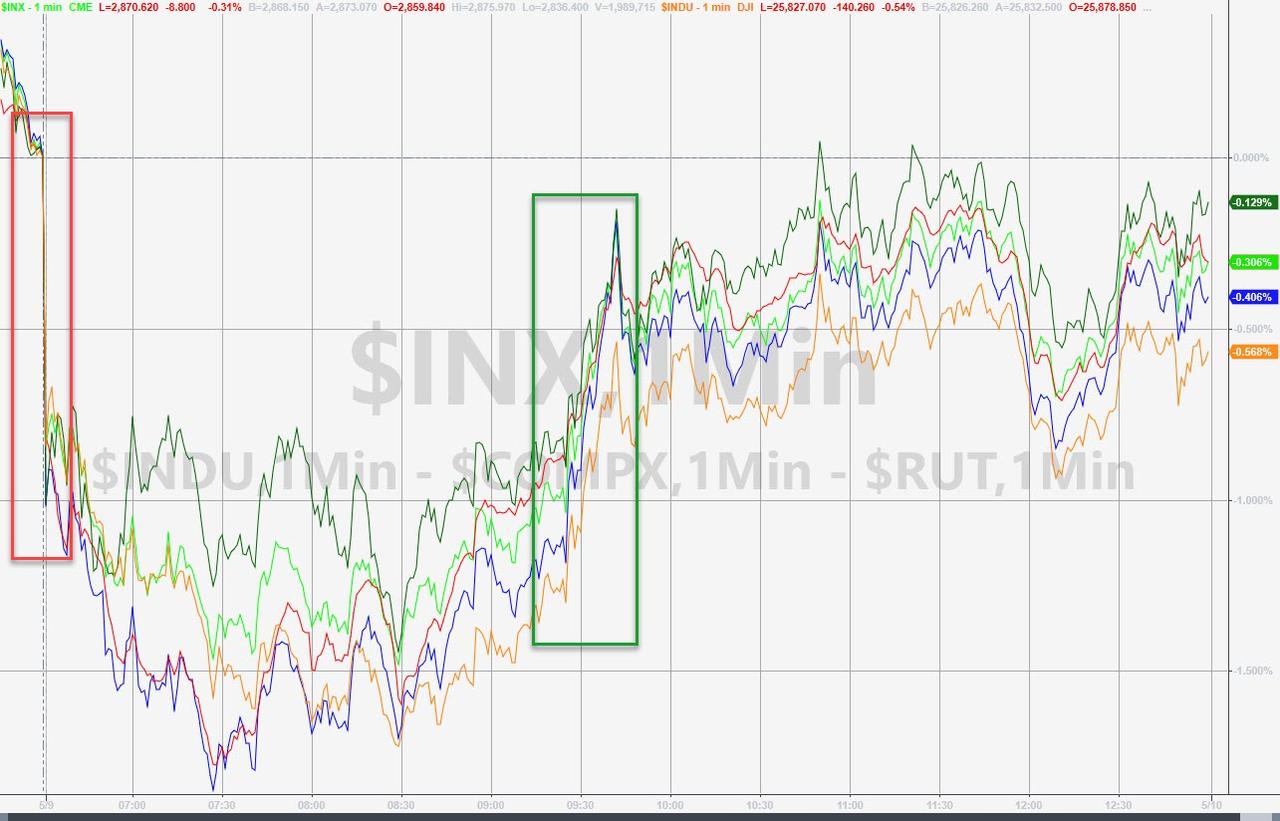

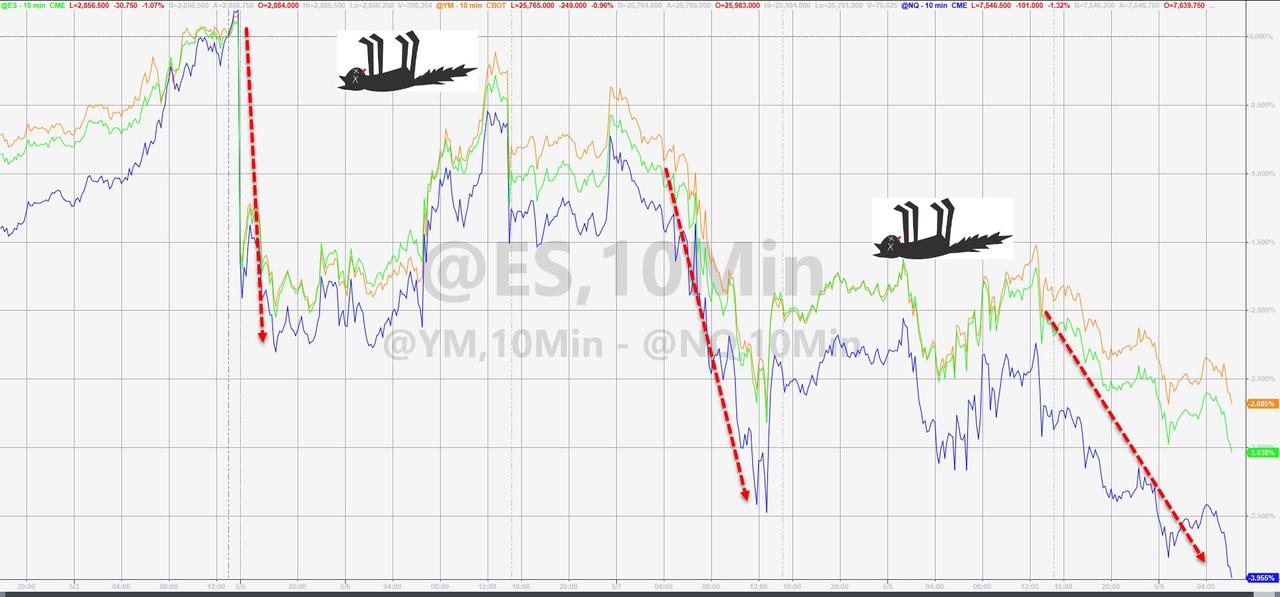

S&P Futures Tumble, Chinese Stocks Plunge As Tariffs Loom

Four words from Donald Trump during his Panama City Beach rally on Wednesday night is all it took for the rug to be pulled from under markets: “China broke the deal” Trump said with Chinese Vice Premier Liu He on route to Washington for two days of talks, and then said another three to cement the sell-off: “They’ll be paying.”

And though Trump added that “it will all work out”, Beijing warned it will retaliate should the U.S. hike tariffs as advertised at 12:01am on Thursday against Friday. With traders already extra jumpy in a week in which the trade war tide reversed unexpectedly and furiously, that’s all it took to accelerate this week’s slide in risk, and world shares tumbled for a fourth day running on Thursday, the result a sea of red amid global markets…

… with S&P500 futures dropping again on Thursday, sliding as much as 0.8% as the deadline approached for America and China to raise reciprocal tariffs.

If talks indeed fail to reach a deal, Washington is set to raise tariffs on $200 billion of Chinese goods to 25% from 10% at 12:01 a.m. ET on Friday. Kazuhiko Fuji, senior fellow at RIETI, a Japanese government-affiliated think-tank, said the trade talks looked fragile.

“I would suspect the U.S. will just hand China an ultimatum. No wonder the U.S. yield curve is almost inverting again,” he said.

“Markets remain on edge ahead of the Chinese vice premier’s visit to Washington today,” Rabobank analyst Bas van Geffen said. “Doubt that this tariff increase can be avoided is growing,” he added as Goldman Sachs also put the chance of a hike at 60 percent.

“In the event of a complete breakdown in talks and higher tariffs, we would expect this to see U.S. stocks trade 10–15 percent below their highs and a fall of around 15–20 percent in the Chinese market,” Mark Haefele, global chief investment officer at Global Wealth Management at UBS, said.

With tariffs imminent barring a last minute miracle, the FT reported that US trade official said the additional tariffs on Chinese goods would apply to goods exported from Friday and will not include goods already in transit, which reports noted provides negotiators a window between 2-4 weeks before the full impact of higher tariffs.

As the flight from risk continued, Treasuries and the yen climbed with gold as investors sought havens, while the yuan fell to its weakest since January. European stock markets sank almost immediately after a torrid day for Asia. Europe’s Stoxx 600 hit session low shortly after the open, falling for the third time in four days, led lower by shares in cyclical sectors including automakers and miners, European tech stocks dropped as much as 1% dragged by a drop in semiconductor shares after Intel’s disappointing forecasts while banking stocks tumbled, with Banco BPM down 6.3% after disappointing quarterly results. The Stoxx 600 was down as much as 1.1%, its lowest level since March 29; the index has fallen 3.6% since hitting its peak in late April, on track to post its biggest weekly drop since December. There was broad based carnage in tech as well: wafer-maker Siltronic -3%, Infineon -2.6%, STMicro -2.6%, and AMS -1.6% all tumbled after Intel gave long-term forecasts for low, single-digit sales growth. Smaller European chip peer and Apple supplier Dialog Semiconductor gives up early gains to trade 0.3% lower after saying 2019 underlying revenue likely to decline this year.

Earlier in the session, Asian stocks fell for a fourth day, headed for their largest decline in six weeks led by technology and material firms; the rout was led by China, whose Shanghai Composite – which is often seen as the bellwether for how this trade war hits home – tumbled 1.5% while South Korea plunged 3%.

Most Asian markets were down, with Japan, South Korea and Hong Kong leading declines. The Topix gauge fell 1.4%, led by Toyota Motor Corp. and Honda Motor Co. The Shanghai Composite Index closed 1.5% lower, with Kweichow Moutai Co. and Ping An Insurance Group Co. among the biggest drags. The S&P BSE Sensex Index declined as much as 1%, as Reliance Industries Ltd. and HDFC Bank Ltd. contributed the most to losses.

Further hurting sentiment was the latest credit data out of China, where April money and credit growth decelerated from the rebound in March, with new CNY loans and total social financing below expectations. Overnight, the PBOC reported that new CNY loans were RMB 1020bn in April, below the RMB 1200bn expected, while Total social financing increased only RMB 1360bn in April, well below the RMB 1650bn consensus. According to the PBOC, TSF stock growth was 10.4% yoy in April, vs. 10.7% yoy in March. The implied month-on-month growth of adjusted TSF was 9.2% SA ann, lower than 11.5% in March.

In addition to trade headlines, traders will also be closely watching the pricing on ride-hailing firm Uber’s initial public offering, which is set to be the biggest of the year so far.

In the currency market, the Japanese yen surged to a three-month high of 109.64 yen as one-week yen volatility surged to its strongest level in four months, while China’s yuan fell half a percent to hit a four-month low of 6.838 and was headed for its worst four-day decline in a year as Australia’s currency falls on weak China credit growth data. A hawkish Norges Bank saw the krone climb against the euro even as faltering risk sentiment and depressed oil prices limited gains, after the central bank signaled a June rate hike. The pound was on track to wipe out last week’s advance against the euro as a Brexit deal resolution still proves elusive. Losses in sterling were limited as Prime Minister Theresa May earned a stay of execution from her Conservative Party.

In geopolitical news, following initial reports that North Korea had fired an unidentified projectile, further reports indicate this this was likely 2 short-range missiles. Prior to the further reports South Korea stated that it is unclear whether North Korea fired single or multiple projectiles.

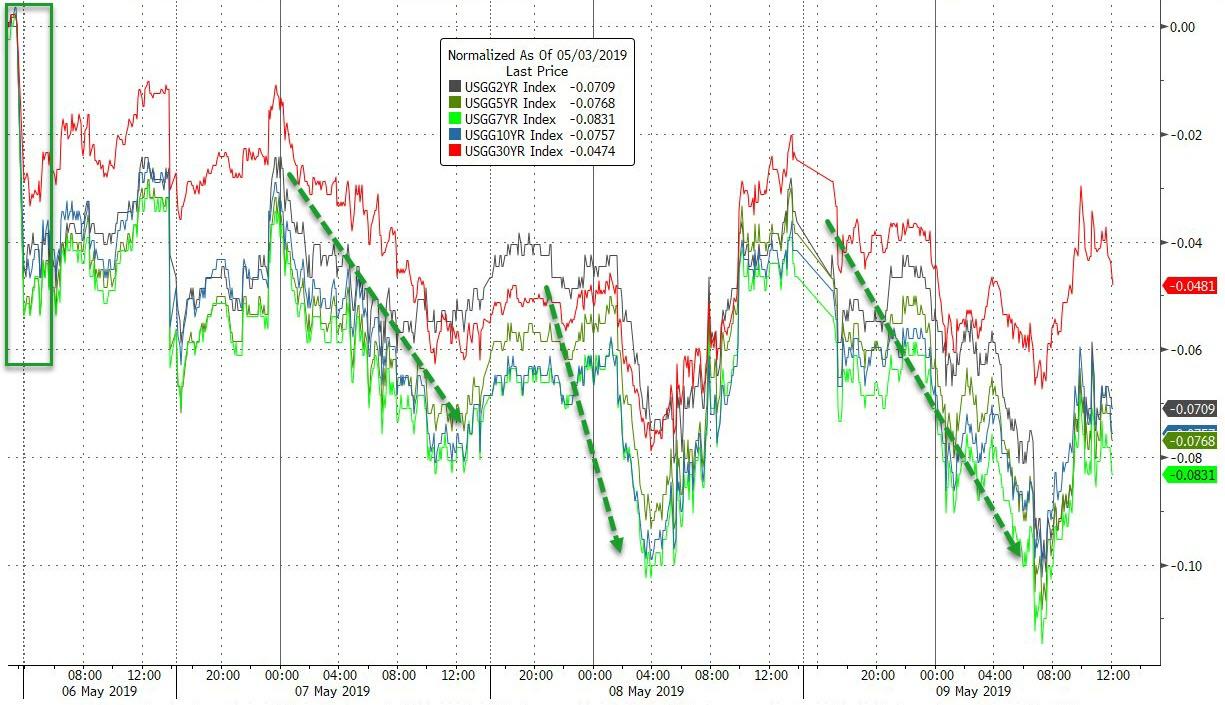

In rates, Treasury 10-year notes jumped due to the escalation in risk-aversion, just hours after Wednesday’s auction saw the weakest demand for the benchmark bond in a decade. The yield spread between three-month U.S. government bonds and the 10-year notes shrank to 3 basis points, compared with about 15 basis points a few weeks ago. The spread first turned negative in late March, spooking investors, who read the development as portending a recession. The benchmark 10-year Treasury yield stood at 2.4529%, having touched its lowest level in five weeks of 2.426 percent on Wednesday before an especially poor 10Y auction sent the yield surging.

Commodity markets also felt the U.S.-China trade strains according to Reuters. Brent crude futures dropped 0.6 percent to $69.92 a barrel, while U.S. West Texas Intermediate crude also retreated 0.6 percent to $61.75 despite a surprise fall in U.S. crude stockpiles. London copper hit its lowest in nearly three months, going as low as $6,111 a tonne.

Expected data include PPIs, trade balance, jobless claims, and inventories. Canadian Natural Resources, Hydro One, Dropbox, and Yelp are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.8% to 2,864.25

- STOXX Europe 600 down 0.8% to 379.05

- MXAP down 1.4% to 156.55

- MXAPJ down 1.8% to 515.76

- Nikkei down 0.9% to 21,402.13

- Topix down 1.4% to 1,550.71

- Hang Seng Index down 2.4% to 28,311.07

- Shanghai Composite down 1.5% to 2,850.95

- Sensex down 0.8% to 37,474.17

- Australia S&P/ASX 200 up 0.4% to 6,295.33

- Kospi down 3% to 2,102.01

- German 10Y yield fell 1.5 bps to -0.059%

- Euro down 0.07% to $1.1184

- Italian 10Y yield fell 0.4 bps to 2.243%

- Spanish 10Y yield fell 0.4 bps to 0.956%

- Brent futures down 0.3% to $70.15/bbl

- Gold spot up 0.3% to $1,285.02

- U.S. Dollar Index little changed at 97.58

Top Overnight News

- U.S. President Donald Trump declared China’s leaders “broke the deal” he was negotiating with them on trade, before adding that “it will work out.” Chinese state media warned that “fighting while talking” may become the new normal in trade relations with the U.S

- China’s credit growth slowed more than expected in April after record expansion in the first quarter

- North Korea fired at least one unidentified projectile Thursday, South Korean military officials said, in the country’s second test launch of weapons in less than a week

- The Bank of Japan will quickly consider additional easing steps if risks such as protectionist moves by the world’s two largest economies wipe out upward price momentum in Japan, its Governor Haruhiko Kuroda said

- U.K. Prime Minister won a reprieve from her Tory party after a key panel of lawmakers kept the rules on leadership challenges unchanged. May agreed to meet with the executive of the so-called 1922 Committee of Tory Members of Parliament next week to discuss her future

- Theresa May earned a stay of execution from her Conservative Party after a key panel of lawmakers kept the rules on leadership challenges unchanged, as talks with the opposition Labour Party to find a compromise on Brexit gained new life

- The U.S. Treasury on Wednesday saw the weakest demand for its benchmark 10-year note in a decade, illustrating the diminishing appetite among some investors to accept current yields

- Trump issued an executive order on Wednesday prohibiting the purchase of Iranian iron, steel, aluminum and copper, ratcheting up tensions with the Islamic Republic less than a day after it declared it may begin enriching uranium again in two months

- House price growth in the U.K. remained weak in April as the slump in southeast England and London depressed the market, the latest survey from the Royal Institution of Chartered Surveyors showed

Asian equity markets were mostly negative as US-China trade uncertainty kept global risk sentiment cautious ahead of trade talks in Washington and as the region also digested a heavy slate of corporate earnings, as well as mixed Chinese data. Nonetheless, ASX 200 (+0.4%) was the exception due to corporate updates. Nikkei 225 (-0.9%) was weighed by currency effects and with individual stocks driven by a plethora of earnings releases, while Hang Seng (-2.4%) and Shanghai Comp. (-1.5%) were the worst hit on trade concerns after the US issued a notice confirming that tariffs will be increased on Friday and with China’s Mofcom mulling counter measures. There was also some sabre rattling from US President Trump who alleged that China broke the deal in trade talks and warned to not backdown until China stops cheating US workers, otherwise the US will not do business with them. Furthermore, overnight data releases were mixed in which Chinese CPI printed inline and PPI topped forecasts, although lending data disappointed with both New Yuan Loans and Aggregate Financing below expectations. Finally, 10yr JGBs initially saw mild upside on the risk averse tone and with the BoJ present in the market focused in the belly. However, the gains were later pared amid mixed comments from BoJ Governor Kuroda who reiterated to continue with powerful monetary easing under YCC given that inflation is still below target, but noted that JGB purchases are slowing and suggested that even if BoJ bond purchases slow to JPY 30tln annually, it would not cause huge trouble.

Top Asian News

- Bahrain Is Set to Receive $2.3 Billion From Allies in 2019

- Singapore’s First 2019 Mainboard IPO Falls in Trading Debut

European bourses have succumbed to the risk aversion [Eurostoxx 50 -1.0%] seen in Asia and Wall Street, with the downbeat tone exacerbated by reports of further missiles tests in North Korea. Sectors are largely lower with the exception of defensive sectors such as Utilities (Unch) and Consumer Staples (+0.2%). A few themes are in play today; 1) a guidance cut by Intel yesterday has prompted a sell-off in European chip names with Infineon (-2.8%) and STMicroelectronics (-2.8%) shares plumbing the depths, albeit Dialog Semiconductor (+0.2%) is bucking the trend on the back of optimistic earnings. 2) Mining names bear the brunt of sentiment-subdued base metal prices coupled with ArcelorMittal’s (-3.9%) 33% drop in profits, thus Rio Tinto (-0.9%), Antofagasta (-1.3%) and Glencore (-1.8%) all weigh on the sector. 3) Against the backdrop of weaker auto earnings, Continental (-3.2%) also reported dismal numbers which dragged its peers Michelin (-0.9%) and Pirelli (-1.2%) lower in sympathy. Finally, Renault (-2.0%) shares declined amid press reports that Nissan could lower its 2022 guidance. Back to earnings, some analysis from JPM notes that thus far, 55% of the Stoxx 600 companies topped EPS estimates (vs. 76% in the S&P 500) whilst 58% of firms are beating on topline with sales growth at 1% Y/Y (vs. +5% Y/Y in the S&P 500), “This is consistent with our view that sales growth in Europe would underwhelm relative to the US, given the weaker macro momentum in the region” JPM says.

Top European News

- Continental AG Sees China Auto Rebound Boosting Second Half

- Norges Bank Says It Will ‘Most Likely’ Raise Rates in June

- Airbus 320 Makes Emergency Landing in Sweden After Cabin Smoke

- SocGen Introduces Crypto to $2 Trillion Market for Covered Bonds

In FX, demand for the Yen remains fervent and the Franc is also back in favour as tensions rise ahead of the US/China face-off in Washington, while geopolitical factors are also weighing on sentiment given the US-EU-Iran sanctions dispute and NK firing an unidentified projectile. Hence, Usd/Jpy has retreated a bit further from 110.00+ to fill/trip a few stops between 109.75-70 and test the top end of decent option expiry interest spanning 109.60-50, while Usd/Chf and Eur/Chf have pulled back from 1.0200+ and 1.1400 respectively.

- USD – Notwithstanding the greater appeal for safer-havens noted above, the Dollar retains a firm underlying bid vs the other G10s and especially EMs that are suffering in their own right. Indeed, the DXY continues to find support below 97.500 and its 30 DMA (97.398) with the index currently hovering in a 97.702-517 range.

- AUD – The major underperformer and most prone to the threat of a complete breakdown in US-China trade dialogue that would trigger an exchange of more aggressive tit-for-tat tariffs. Aud/Usd has recoiled from recent recovery highs towards this week’s multi-month low around 0.6963 and Aud/NZD has unwound more post-RBNZ spike gains to sub-1.0600 as Nzd/Usd holds more comfortably above 0.6550 and depths plunged in wake of Wednesday’s NZ rate cut. On that note, Governor Orr has reiterated that the policy outlook is now more neutral and it is too soon to assess if more easing is required ahead of testimony on the latest meeting and action to a parliamentary select committee.

- NOK – Staying with the Central Bank theme, but in stark contrast to the RBNZ, Norway’s Norges Bank flagged a hike at next month’s meeting and the Nok shot up across the board in response. However, gains were rapidly eroded and reversed at one stage amidst the aforementioned risk-averse tone before the Norwegian Crown regained bullish momentum on the fact that rates are set to rise against the general global grain of steady to easier policy. Eur/Nok is back under 9.8000, albeit just within 9.7784-8393 trading parameters and eyeing hefty expiry interest (1.1 bn) at the strike.

- EUR/GBP/CAD – All narrowly mixed vs the Greenback, but with a bearish bias below 1.1200, 1.3000 and only just over 1.3500 respectively. Eur/Usd has multi-bn expiries stretching from 1.1150 to 1.1200 and beyond to keep price movement contained along with the 30 DMA (1.1223) and interim chart support at 1.1155, while Cable has gleaned some traction around a Fib (1.2980) and ahead of the 200 DMA (1.2960), but needs to recapture the 100 DMA (1.3013) to revisit best levels of 1.3025. Back to the Loonie, Canadian trade data looms alongside house prices.

- EM – More widespread losses vs the Usd, but once again the Try is underperforming and has been down to through 6.2450 with the Lira lamenting another decline in Turkish foreign reserves.

In commodities, Brent (-0.5%) and WTI (-0.4%) prices are choppy, with prices initially subdued amid the general risk sentiment as markets await US-China updates and the most recent geopolitical developments being reports that North Korea has fired an unidentified projectile at 16:30 local time, although it is still unknown whether it was a single or multiple projectiles. Despite the recent price action being sentiment-driven, the macro picture still stands, with Iranian/Venezuelan sanctions, Libyan tensions and OPEC-led cuts still on the table. Thus, Barclays revised their Q3 2019 Brent and WTI forecasts higher by USD 4/bbl amid expectations of tightening market conditions. In terms of US supply, ING highlights that refinery run rate remain at a season-low at 88.9% last week amid a heavier maintenance season alongside several unplanned outages. Meanwhile, gold (+0.3%) has been accumulating some risk premium in light of the aforementioned developments in the Korean peninsula whilst conversely, copper is pressured by the humdrum risk tone emanating from the seemingly escalating US-Sino tensions and geopolitical concerns. Finally, China State Planner stated that strict pollution related controls will be imposed on steel-making capacity in key pollution area whilst also raising domestic iron ore production. It’s worth noting that earlier in March, a level 1 smog alert was issued which requires steel mills to curb production by 40-70%. Although, it is worth assuming that iron ore production will be hiked to offset volatility in the base metal. China’s State Planner state they will impose strict controls on steel-making capacity in key pollution areas.

Looking at the day ahead, we will get the April PPI report where the market consensus is pegged at +0.2% mom for the core. Expect there to be focus on the health care and portfolio management services components of the report as a read-through for the core PCE deflator. Away from that we’ll also get the latest claims reading and March trade balance print, followed later by the final March wholesale inventories revisions. Away from that we’re due to hear from the ECB’s Hakkarainen while over at the Fed, Powell is scheduled to speak in the early afternoon, albeit only opening remarks with no Q&A to follow. The Fed’s Bostic and Evans also speak today.

US Event Calendar

- 8:30am: PPI Final Demand MoM, est. 0.3%, prior 0.6%; YoY, est. 2.3%, prior 2.2%

- PPI Ex Food and Energy MoM, est. 0.2%, prior 0.3%, YoY, est. 2.5%, prior 2.4%

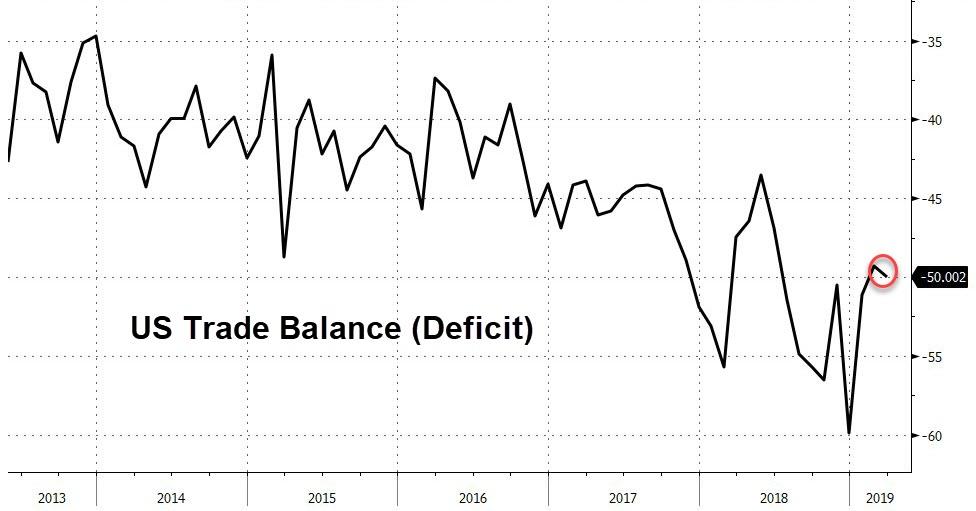

- 8:30am: Trade Balance, est. $50.1b deficit, prior $49.4b deficit

- 8:30am: Initial Jobless Claims, est. 220,000, prior 230,000; Continuing Claims, est. 1.67m, prior 1.67m

- 9:45am: Bloomberg May United States Economic Survey; Bloomberg Consumer Comfort, prior 60.4

- 10am: Wholesale Trade Sales MoM, est. 0.55%, prior 0.3%; Wholesale Inventories MoM, est. 0.0%, prior 0.0%

DB’s Jim Reid concludes the overnight wrap

As US/China trade and Brexit talks looked increasingly more vulnerable yesterday at least here in the UK we had the first glance of a new royal baby to distract us. I was disappointed he was named Archie rather than Divock after Liverpool’s Tuesday night heroics which have still yet to fully sink in. As it stands I have a one-way flight to Madrid booked and no final tickets. I also haven’t run the idea of a weekend away watching football by my wife yet. I thought I’d work on this in stages. Flight out first (only tick so far), ticket second, flight back third, accommodation next (but I could camp) and then ask permission. No point asking permission and firing a bullet if you can’t logistically do it. If Liverpool’s performance was astonishing one would have to say Spurs also coming back from 3-0 down in the tie at HT against Ajax last night and winning on away goals deep in injury time was also remarkable. My long-time work colleague Nick Burns is a Spurs season ticket holder and entitled to final tickets and as I reserved him an flight to the final yesterday just in case I will assume he’s reserved me a ticket this morning. This morning could be the defining moment in his 2019 appraisal.

Outside of the knowledge of the craziness of sport, the last 24-48 hours has taught us that markets have no greater insight as to whether this week’s trade developments are just hardball from Trump or the start of a very real threat to the global growth narrative. If it’s the latter then you can’t help but feel that markets look extremely complacent at this point. However if it’s just hardball negotiation en route to a deal then we’ll likely resume the rally. A big bid offer admittedly, but in the very short term the risks probably look greater than the rewards as it feels unlikely that either side can back down in the near term. Maybe over weeks but not over the next few days.

At the time of writing, China’s top trade negotiator Liu He is flying over to Washington DC for talks with Lighthizer and Mnuchin. Time is not on China’s side though with tariffs due to kick in in a little under 24 hours after the Office of the US Trade Representative yesterday signed off that tariffs on $200bn of China goods are to be raised on Friday morning at 12:01am ET.

In line with the back-and-forth newsflow, markets slipped between gains and losses before ending the US session slightly lower. Just four minutes before the Office of Trade statement in late morning US time, President Trump tweeted that China were “coming to the US to make a deal” which appeared to at least hold some hope of optimism in markets. A bigger boost came after White House spokeswoman Sarah Sanders said that the White House had received an “indication” that China is ready to make a deal. Within half an hour, however, a commerce department statement from China said that “The US intends to raise the tariff of 200 billion US dollars of Chinese exports to the United States from 10% to 25% on May 10. The escalation of trade friction is not in the interests of the people of the two countries and the people of the world. The Chinese side deeply regrets that if the US tariff measures are implemented, China will have to take necessary countermeasures.”

Overnight, while addressing a rally in Panama City Beach, Florida, President Trump has said that China’s leaders “broke the deal” he was negotiating with them on trade and added there’s “nothing wrong with taking in $100 billion a year” in tariffs on Chinese imports, in the absence of a trade deal. However, he also said, “they come in tomorrow and whatever happens, don’t worry about it. It will work out. It always does.” Elsewhere, the WSJ has reported that China’s Vice Premier Liu He is not carrying the title of President Xi’s “Special Envoy” while visiting the US for trade negotiations and this means that he cannot make any big concessions. China’s Global Times is also reporting this morning that China wont flinch in the face of a tough-talking US and is likening the trade talks to a “Banquet at Hongmen”, a Chinese reference to a historical event that took place in 206 BC at Hong Gate and implies a treacherous situation. So emotions and rhetoric are being raised in both sides. It should be worth watching China’s regular ministry of commerce briefing at 03:00 pm Beijing time (08:00 am London) to get further insight into the situation.

All nice and straightforward then. The end result to the conflicting headlines yesterday was a bit of volatility for the S&P 500 just before Europe went home, opening -0.37% lower before rallying to +0.47%, but ultimately closing -0.15% after a sharp late drop. That leaves May’s returns at a still pretty mild -2.24% though considering all that has gone on. The VIX touched an intraday high of 21.74 yesterday though – a level it hasn’t closed at since January 3 – before ending at 19.92, trading in a range of 3.5pts. That’s the third consecutive day with a range of over 3pts, the first such stretch since January 4. The NASDAQ fell -0.26% and the DOW traded flat (+0.01%), while in Europe the STOXX 600 finished +0.15% after spending the bulk of the session in the red.

Meanwhile, bond markets couldn’t quite make their minds up yesterday with 10y Treasury yields rising +2.7bps, +5.9bps off the morning low but 2bps lower again in Asia. The 3m10y curve steepened +1.9bps yesterday, taking it back to +5.8bps after flirting with another inversion over the last few sessions. The 2y10y is still hovering around 18.3bps and the reality is that this has been in a broad 10-20bp range ever since December. Bunds have been more of a beneficiary of the risk-off moves, hitting an intraday low of -0.065% yesterday before closing at -0.044% as risk rallied back into the European close. For reference, the recent low mark for Bunds was -0.095% on an intraday basis back at the end of March. BTPs have been caught up in the broader risk off move – with the recent budget headlines also not helping – though they retraced their +7.7bps intraday move yesterday to end the session flat. Elsewhere EM FX traded flat overall, with the Turkish lira again underperforming (-0.56%) as the government announced plans to re-hold the Istanbul elections. Balancing this was a +0.26% rally by the South African rand, as the country held national elections yesterday, with the results due this morning.

This morning in China we saw the release of April aggregate financing data which came in at CNY 1,360bn (vs. 1,650bn expected and 2,859.3bn last month) with new loans standing at CNY 1,020bn (vs. 1,200bn expected and 1,690bn last month). Weakness in China’s credit data along with the possibility of further escalations in the trade war is continuing to weigh on Asian markets with the Nikkei (-1.01%), Hang Seng (-1.95%), CSI (-1.90%), Shanghai Comp (-1.35%), Shenzhen Comp (-1.03%) and Kospi (-1.67%) all down over -1% alongside most Asian markets. China’s onshore yuan is down -0.39% to 6.8090, the weakest since January. Other EM Fx is also trading weak this morning with the exception of Turkish Lira which is up +0.37% while the Korean won is leading losses (-0.56%). G10 Fx is also weak with the exception of the Japanese yen which is up +0.14%. Elsewhere, futures on the S&P 500 are down -0.53% and crude oil prices (WTI and Brent both down -0.74%) are also weak. In terms of other data releases China’s April CPI came in line with consensus at +2.5% yoy while PPI stood at +0.9% yoy (vs. +0.6% yoy expected).

In other news, cross-party talks between the Conservatives and Labour continued yesterday but finding common ground remains elusive. In the meantime, the BBC has reported this morning that Labour Party’s Jeremy Corbyn is set to launch his European elections campaign later and will say that the party backs “the option of a public vote” if a “sensible” Brexit deal cannot be agreed and there is not a general election. Elsewhere Prime Minister May looks set to survive for at least another week as the 1922 committee failed to agree on any changes to Conservative party rules at this week’s meeting. The 1922 head Graham Brady said he expects May to hold a vote on the Withdrawal Agreement Bill next week, which could possibly still leave time to exit the European Union before the European Parliament elections but that is looking very very unlikely.

Back to the US and Fed Governor Brainard made some headlines yesterday by expressing interest in a form of yield curve control as a future policy option. She said “we might turn to targeting slightly longer-term interest rates — initially one-year interest rates, for example, and if more stimulus is needed, perhaps moving out the curve to two-year rates.” This would potentially allow the Fed to better signal how long it plans to keep rates low. Such tools could be needed in a future recession if short-term interest rates again approach zero.

Oil prices rose +1.101% before this morning’s fall as tensions between the US and Iran continued to intensify and the outlook for Iranian oil exports continues to darken. First, Iran announced that it is also withdrawing from the nuclear deal, following the US’s move exactly one year ago. While the Iranian government did not declare an intention to renege on all the deal’s elements, they did announce their plans to resume stockpiling low enriched uranium and heavy water, and signalled that they would resume construction of a closed reactor if Europe fails to compensate for the US’s unilateral sanctions. That comes after news that Europe’s mechanism to avoid US sanctions, which reportedly would have allowed Iran to export more oil, will actually only apply to food and humanitarian aid. Finally, the US administration followed up by adding new sanctions to Iran’s iron, steel, aluminium, and copper industries.

Before we wrap up, the data yesterday included a better than expected March industrial production print in Germany (+0.5% mom vs. -0.5% expected) albeit somewhat offset by downward revisions to February. In the UK the Halifax house price index rose +1.1% mom in April and more than expected. US mortgage applications rose +2.7% last week, the first rise since March.

Finally to the day ahead, where there are no data releases due in Europe this morning however in the US this afternoon we will get the April PPI report where the market consensus is pegged at +0.2% mom for the core. Expect there to be focus on the health care and portfolio management services components of the report as a read-through for the core PCE deflator. Away from that we’ll also get the latest claims reading and March trade balance print, followed later by the final March wholesale inventories revisions. Away from that we’re due to hear from the ECB’s Hakkarainen while over at the Fed, Powell is scheduled to speak in the early afternoon, albeit only opening remarks with no Q&A to follow. The Fed’s Bostic and Evans also speak today.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 42.80 POINTS OR 1.48% //Hang Sang CLOSED DOWN 692.13 POINTS OR 2.39% /The Nikkei closed DOWN 200.46 POINTS OR 0.93%//Australia’s all ordinaires CLOSED UP .40%

/Chinese yuan (ONSHORE) closed DOWN at 6.8243 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 61.92 dollars per barrel for WTI and 70.47 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8243 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8483 TRADE TALKS STILL ON//TRUMP THREATENS A NEW 25% TARIFFS ON FRIDAY/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP THREATENS TO RAISE RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

i)China/USA/FED

Interesting: China is playing hardball because they read us: namely that the USA economy is not doing too good. Also the fact that Trump is asking the Fed’s Powell to lower interest rates is a powerful indicator that the uSA economy is waning.

(courtesy zerohedge)

How Trump’s Attacks On Powell Led To Collapse Of China Trade Talks

In what will almost certainly be remembered as one of the most chaotic weeks for global markets in recent memory due to the unceasing flow of trade news, global stocks were back in risk-off mode Thursday after a seemingly offhanded remark by President Trump during a MAGA rally last night doused the sense of optimism that had prevailed earlier in the day.

But with the Chinese delegation having arrived in Washington, more reports published late Wednesday and early Thursday have offered new insights into why Beijing decided to play hardball, and how Washington is planning to show that it means business while stopping short of torpedoing any accumulated goodwill with new tariffs.

Though paperwork filed by the Trade Representative’s office on Wednesday suggests that tariffs will almost certainly rise on Friday, the administration has apparently come up with an important caveat that could allow negotiators more time: The new tariff rates won’t apply to goods already in transit, which would give negotiators up to a month to work out a deal before the new rates take effect, according to the FT.

The clarification offers US and Chinese negotiators a window of two to four weeks to reach a deal before the bulk of the pain from the higher tariffs hits US consumers and businesses, based on shipping times between the countries.

On Wednesday morning, Mr Trump noted on Twitter that Mr Liu was still coming to the US capital to “make a deal.”

The president’s latest tweets were posted just before the US equity markets were set to open after two days of losses driven by the flare-up in trade tensions with China. US stocks were volatile but trading slightly higher on Wednesday compared to earlier in the week.

Meanwhile, in a lengthy piece purporting to explain why Beijing decided to start playing ‘hardball’ so late into the talks (though, to be sure, other reports suggest that Beijing had taken a hard line almost from the start), WSJ claimed that President Xi and the senior leadership interpreted Trump’s attacks on Fed Chairman Jay Powell as a sign that Trump would be ready to compromise.

The reason? It was interpreted as evidence that Trump secretly believed the US economy was more fragile than the official data reflected. Meanwhile, the Chinese economy has stabilized, in part thanks to a massive stimulus program.

Beijing was further emboldened by Trump’s professions of ‘friendship’ with Xi, and his praise for Liu. Then, an April 30 Trump tweet praising Chinese economic policy cemented this view, according to WSJ’s sources.

An analyst quoted in the WSJ piece offers an apt summary: “Why would you be constantly asking the Fed to lower rates if your economy is not turning week?”

That’s a great question. We’re still waiting for an explanation on that one.

A spokesman for MOFCOM on Thursday rejected US accusations that Beijing had reneged on its promises, which is what allegedly prompted Trump’s tariff threats. Beijing has vowed to retaliate to any new tariffs out of Washington, but the takeaway from Thursday’s reports is that even if a deal doesn’t happen Friday (which it almost certainly won’t), the trade negotiations will remain an intense market focus for at least the next two weeks, until the new rates take effect.

At any rate, we imagine the WSJ report was at least a small consolation to Powell, who has now been partially vindicated for his slightly hawkish tilt during the post-FOMC press conference earlier this month.

END

CHINA/FOREIGNERS

Foreigners are dumping Chinese stocks with reckless abandon as they are frightened ahead of the expected tariff increase.

(courtesy zerohedge)

Foreigners Are Dumping Chinese Stocks At A Record Pace Ahead Of Tariffs

Having surged to over a 30% gain this year, far ahead of Europe and US markets, Chinese stocks have dramatically weakened back to EU,US stocks in the last few weeks.

China’s initial weakness was likely triggered by local officials comments on exuberance and actions to rein in some of the margin surge that always seems to occur when the Chinese investing population discover a trend.

However, as the trend broke, another set of investors has decided to exit the burning building – foreigners!

“Offshore investors chose to lock in profits given the great uncertainty in Sino-U.S. relations,” said Li Bin, a Shanghai-based fund manager at Capital Corise Asset Management Co.

“The bigger declines on the SSE 50 index might be a result of consistent foreign outflows.” The SSE 50 has fallen 8.4% this week, while the Shanghai Composite Index is down 7.4%.

Foreign investors net sold an average 4.4 billion yuan ($646 million) of mainland shares a day through trading links with Hong Kong this week, according to data compiled by Bloomberg.

They are on track for the heaviest week of selling since the Shenzhen connect opened in late 2016…

The exodus extends a trend from April, which saw net sales of 18 billion yuan, a monthly record…

Of course, this could all change by this time tomorrow as Liu arrives in DC and US tariffs hit (and possible China retaliatory tariffs).

4/EUROPEAN AFFAIRS

UK

This is serious stuff: The USA threatens the UK over their potential of Huawei in the 5G wireless space

(courtesy Mish Shedlock/Mishtalk)

US Threatens UK Over Huawei And 5G Wireless

Authored by Mike Shedlock via MishTalk,

US Sec. of State Mike Pompeo warns the UK about 5G wireless. Pompeo threatens to end defense cooperation with the UK.

Via the Guardian Live Blog, Pompeo warns the UK that Huawei 5G role could put defense cooperation with US at risk.

Here are the main points from the press conference given by Mike Pompeo, the US secretary of state, and Jeremy Hunt, the UK foreign secretary.

Pompeo implied that the UK could put defense cooperation with the US at risk if it allowed Huawei a role in operating its 5G infrastructure. In his opening remarks Pompeo said:

We discussed at some length the importance of secure 5G networks. I will have a little more to say on that this afternoon, but I’m confident that each of our two nations will choose a path which will ensure security of our networks.

Then, when asked if a decision by the UK to allow Huawei a role in constructing its 5G infrastructure, would affect the special relationship, he replied:

I have great confidence that the United Kingdom will never take an action that will break the special relationship.

With respect to 5G, we will continue to have technical discussions. We are making our views very well known from America’s perspective.

Each country has a sovereign right to make its own decision about how to deal with the challenge.

The United States has an obligation to ensure that, [in] places where we operate, places where American information is, places where we have our national security risks, that they operate inside trusted networks. And that’s what we will do.

Pompeo Hammers Jeremy Corbyn

Labour Leader Jeremy Corbyn is a socialist who admires former Venezuela leader Hugo Chavez. Pompeo had this to say.

It is disgusting to see leaders, not only in the United Kingdom but in the United States as well, who continue to support the murderous dictator Maduro.

It is not in either of our country’s best interests for those leaders to continue to advocate on their behalf. The Venezuelan people have spoken through their constitutional mechanism. They have put Juan Guaido as their interim president, and he is the duly elected leader there. And Maduro is on borrowed time.

Hunt Agrees

This is a country where three million people have fled the country, GDP has gone down by 40% in the last four years, people can’t access basic medicine, people are rifling through rubbish bags to get food in the streets. [Shadow chancellor] John McDonnell describes this as socialism in action and I think people need to draw their own conclusions about what his own plans might be for the UK.

Yes, this is the same Labour Party leader that Theresa May is in bed with to deliver Brexit.

5G Issues

In regards to 5G the US is woefully behind. Security threats may be overblown.

Because much of Europe is on previous versions of Huawei, there is a clear backward compatible way forward, but only if those nations using Huawei select its option as the way forward. Otherwise, it may take years to upgrade, and possibly to inferior technology.

For further discussion of 5G issues, please see:

- EU Pokes Trump Again, This Time Over Huawei’ s 5G Technology

- Trump Tweets Promote US 5G “Even 6G” ASAP

Ultimately, the EU nations and the UK will make their own decisions. Some of them will undoubtedly select Huawei.

Expect Trump to fume.

end

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

ISRAEL/GAZA/WEST BANK/PALESTINIANS

Israeli Newspaper leaks terms of Trump’s new Middle East Peace Plan between Israel, Gaza and the Palestinians in the West Bank. It is interesting but I doubt if Hamas in Gaza will entertain such a project