GOLD: $1297.05 UP $1.50 (COMEX TO COMEX CLOSING)

Silver: $14.81 UP 2 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1296.70

silver: $14.81

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 1/1

EXCHANGE: COMEX

CONTRACT: MAY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,294.700000000 USD

INTENT DATE: 05/14/2019 DELIVERY DATE: 05/16/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 1

737 C ADVANTAGE 1

____________________________________________________________________________________________

TOTAL: 1 1

MONTH TO DATE: 233

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 1 NOTICE(S) FOR 100 OZ (0.003215 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 233 NOTICES FOR 23300 OZ (.7247 TONNES)

SILVER

FOR MAY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR NIL OZ/

total number of notices filed so far this month: 3373 for 16,865,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$7946 DOWN $9

Bitcoin: FINAL EVENING TRADE: $7946 UP $160.00

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A TINY SIZED 102 CONTRACTS FROM 203,890 DOWN TO 203,788 WITH YESTERDAY’S 2 CENT GAIN IN SILVER PRICING AT THE COMEX. ,LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER BUT IT NOW IN FULL FORCE FOR GOLD. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 435 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 435 CONTRACTS. WITH THE TRANSFER OF 435 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 435 EFP CONTRACTS TRANSLATES INTO 1.665 MILLION OZ ACCOMPANYING:

1.THE 2 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 18.335 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

13,303 CONTRACTS (FOR 11 TRADING DAYS TOTAL 13,303 CONTRACTS) OR 66,51 MILLION OZ: (AVERAGE PER DAY: 1209 CONTRACTS OR 6.045 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 66.51 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.19% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 807.62 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 102 WITH THE TINY 2 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 435 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE GAINED A SMALL SIZED: 333 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 435 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 102 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 2 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.79 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.020 BILLION OZ TO BE EXACT or 145% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 18.335 MILLION OZ ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 2490 CONTRACTS, TO 517,995 WITH THE FALL IN THE COMEX GOLD PRICE/(AN INCREASE IN PRICE OF $5,45//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5436 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 5436 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 517,995. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2946 CONTRACTS: 2490 OI CONTRACTS DECREASED AT THE COMEX AND 5436 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 2946 CONTRACTS OR 494,600 OZ OR 9.163 TONNES. YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $5,45.…AND WITH THAT STRONG LOSS, WE HAD AN GOOD GAIN OF 9.163 TONNES!!!!!!.??????

WITH RESPECT TO SPREADING: NOT TO NOTICEABLE WITH TODAY’S FALL IN PRICE

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS HAVE NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 65,405 CONTRACTS OR 6,540,500 OR 203.43 TONNES (11 TRADING DAYS AND THUS AVERAGING: 5945 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAYS IN TONNES: 203,43 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 203,43/3550 x 100% TONNES =5,73% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2018.99 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX OF 2490 WITH THE FALL IN PRICING ($5.45) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5436 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5436 EFP CONTRACTS ISSUED, WE HAD A FAIR SIZED GAIN OF 4566 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5436 CONTRACTS MOVE TO LONDON AND 2490 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 9.163 TONNES). ..AND THIS GOOD DEMAND OCCURRED WITH A FALL IN PRICE OF $5.45 IN YESTERDAY’S TRADING AT THE COMEX. WE NO DOUBT HAD A SMALL PRESENCE OF SPREADING TODAY.

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $1.50 TODAY

INVENTORY RESTS AT 736.46 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORy

SLV/

WITH SILVER UP 2 CENTS TODAY:

A BIG CHANGE IN SILVER INVENTORY AT THE SLV//

A WITHDRAWAL OF 1.031 MILLION OZ FROM THE SLV.

/INVENTORY RESTS AT 315.551 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 102 CONTRACTS from 201,956 UPTO 203,788 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER BUT HAVE NOW MORPHED INTO GOLD..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 435 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 435 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 102 CONTRACTS TO THE 435 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL GAIN OF 333 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 1.665 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 18.335 MILLION OZ FOR MAY

RESULT: A CONSIDERABLE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 2 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 435 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 55.07 POINTS OR 1.91% //Hang Sang CLOSED UP 146.69 POINTS OR 0.52% /The Nikkei closed UP 121.33 POINTS OR 0.58%//Australia’s all ordinaires CLOSED UP .69%

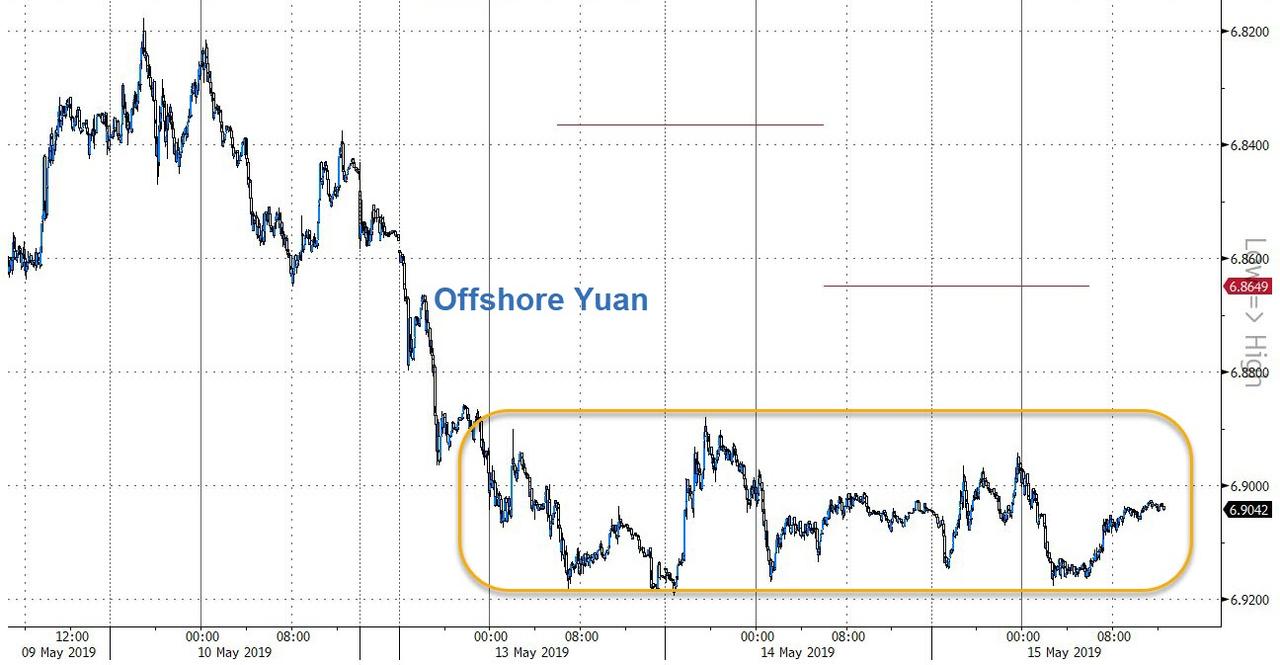

/Chinese yuan (ONSHORE) closed DOWN at 6.8830 /Oil UP to 61.64 dollars per barrel for WTI and 71.08 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8830 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9148 TRADE TALKS STILL ON//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP THREATENS TO RAISE RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

i)NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

China reports today, like the USA that all green shoots are dead. China’s retail sales and Industrial production falter.

(courtesy zerohedge)

ii)Huawei offers to sign a “no spy” pact with governments as the UK is set on embark on 5 G

( zerohedge)

4/EUROPEAN AFFAIRS

i)ITALY

ii)UK

In the words of Ron Burgundy: Boy! did that escalate fast: The new Brexit party surges to 34% while the Tories drop to 5th place. Labour has not benefited at all on the fall of the Tories. This is what happens to a party when you go against the wishes of the people.

( Mish Shedlock/Mishtalk)

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

a)Turkey

Turkey again in the new today. In order to create some USA revenue it is imposing a .1% tax on foreign exchange transactions. Of course this will hurt investors who are already reeling from interest rates at 25.5%. Turkey is adamant on purchasing Russians S400 defense shield. Down goes the Lira this morning

( zerohedge)

(courtesy zerohedge)

6. GLOBAL ISSUES

THE GLOBE

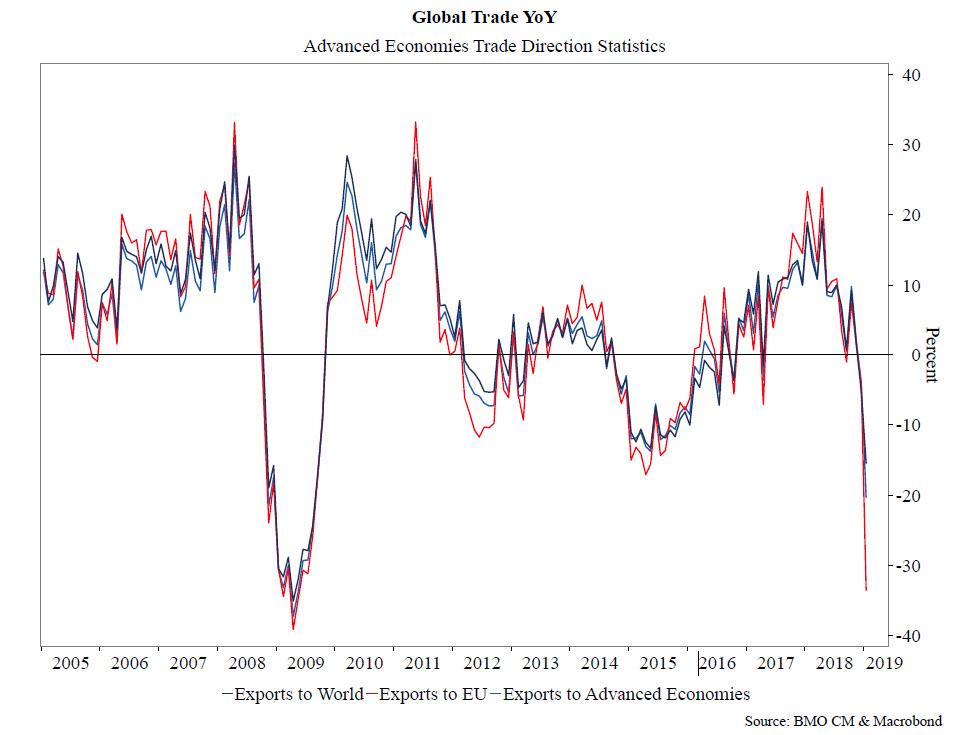

We have been pointing out to you since October who global trade has been collapsing. The trade war is not helping

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA

9. PHYSICAL MARKETS

( Kranzler/IRD/GATA)

ii)Ed Steer discusses the late Bart Chilton’s revelation that JPMorgan was allowed to manipulate the silver price. He also discusses the use of derivatives by central banks to control the price of the precious metals.

( Ed Steer/Silver Doctors/GATA)

iii)Craig Hemke believes that 2019 is the shakeout year for both gold and silver

(Craig Hemke/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

ii)Market data

First retail spending contracted big time with auto sales leading the way

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

Esther George is one of the hawks at the Fed. She warns against cutting interest rates as she states that will lead to bubbles. She is correct on that point..however she states that cutting rates will lead to a recession..wrong. If the Fed raises rates a recession will surely be upon the USA

( zerohedge)

SWAMP STORIES

i)This is a big story. The Bidens are big crooks and took huge bribe money form both Ukraine and China while Joe Biden was Vice President. Schweizer wrote a book on this and demands that Hunter Biden must testify over these revelations

(Courtesy zerohedge)

ii)This is big!! USA Attorney Joe DiGenova tells Laura Ingram that John Durham has already been on the case for a couple of months now. He states that John Brennan, the orchestra leader and Comey are in big trouble. Also the issuance of those FISA applications will probably cause headaches for many in the Democratic field.

(/Ingram Angle)

iii)What a joke: He now know that Andrew Weissmann hand picked all of those “angry Democrats” to lead the witch hunt against Trump et al

( zerohedge)

iv)White HOuse tells Nadler that there is no “do over” with respect to the Russian collusion hoax. It is over…

( zerohedge)

Let us head over to the comex:

Gold withdrawals;

i) We had 1 withdrawal:

from the Bank of Nova Scotia: 289.35 oz

9 kilobars

.

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Kranzler believes that the Fed is losing control on the interest rate front..and they may lose control of the goldprice as well…

(courtesy Kranzler/IRD/GATA)

Dave Kranzler: Fed is losing control of rates, then may lose control of gold too

Submitted by cpowell on Tue, 2019-05-14 13:05. Section: Daily Dispatches

9:05a ET Tuesday, May 14, 2019

Dear Friend of GATA and Gold:

Dave Kranzler of Investment Research Dynamics in Denver explains today why a big move up in the monetary metals may be at hand at last.

Kranzler writes: “The inverted yield curve, combined with an effective Fed funds rate that is above the interest rate used to calculate the quantity of free money given by the Fed to the banks on excess reserves, is strong evidence that the Fed is losing its ability to control the financial markets. At some point the Fed and its Western central bank collaborators, led by the Bank for International Settlements, will also lose control of the gold price.”

Kranzler’s analysis is headlined “Gold and Silver May Be Setting Up for a Big Move” and it’s posted at IRD here:

http://investmentresearchdynamics.com/gold-and-silver-may-be-setting-up-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Ed Steer discusses the late Bart Chilton’s revelation that JPMorgan was allowed to manipulate the silver price. He also discusses the use of derivatives by central banks to control the price of the precious metals.

(courtesy Ed Steer/Silver Doctors/GATA)

GATA’s Ed Steer discusses Chilton’s admission, commodity price control

Submitted by cpowell on Tue, 2019-05-14 13:46. Section: Daily Dispatches

9:45a ET Tuesday, May 14, 2019

Dear Friend of GATA and Gold:

GATA Board of Directors member Ed Steer, editor of Ed Steer’s Gold & Silver Digest letter, was interviewed the other day by James Anderson for Silver Doctors. They discussed former U.S. Commodity Futures Trading Commission member Bart Chilton’s confirmation that the commission allowed JPMorganChase to manipulate the silver market. They also discussed the use of derivatives by central banks and their agents to control commodity prices.

The interview is 20 minutes long and can be heard at Silver Doctors here:

https://www.silverdoctors.com/headlines/world-news/ed-steer-gold-silver-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Craig Hemke believes that 2019 is the shakeout year for both gold and silver

(Craig Hemke/GATA)

Craig Hemke at Sprott Money: Recalling 2010

Submitted by cpowell on Tue, 2019-05-14 20:01. Section: Daily Dispatches

4p ET Tuesday, May 14, 2019

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing at Sprott Money today, explains why he is more persuaded that 2019 will follow 2010’s pattern of a shakeout in the monetary metals followed by a sharp rally. His analysis is headlined “Recalling 2010” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/recalling-2010-craig-hemke-14-052019.ht…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Central Banks Are Buying Gold At The Fastest Pace In Six Years

Authored by Simon Black via SoveriegnMan.com,

Earlier this month the World Gold Council published its quarterly report– and it shows that central banks and foreign governments from around the world are buying up gold at their fastest pace in six years.

This is pretty big news, and it says a LOT about the future of the dollar.

Remember, central banks and foreign governments hold literally TRILLIONS of dollars of reserves… and traditionally they do this by buying US government debt.

It sounds strange, but to big institutions, banks, etc., US government debt is equivalent to cash. They use it as a form of money.

More importantly, they hold US dollars because that’s the global standard: the US dollar has been the world’s primary international reserve currency for seventy five years.

So US debt is extremely liquid. In fact, the $22 trillion US debt market is the biggest and most liquid market in the world.

But foreign governments have started breaking with the tradition of buying treasuries.

As the World Gold Council’s report showed us, foreign governments and central banks have been buying a LOT more gold than in previous years.

Net gold purchases in Q1/2019 among foreign governments and central banks was nearly 70% greater than Q1/2018… and the highest rate of first quarter purchases in six years.

The Chinese in particular, have been stockpiling gold faster than ever, while at the same time, Chinese ownership of US treasuries as a percentage of total holdings has been gradually declining over the past years.

And it’s not just China.

Russia, Turkey, Qatar, and even Colombia – a long-time ally of the US – have been diversifying and buying a lot more gold.

There are a few obvious reasons behind that.

The debt of the US federal government recently reached $22 trillion. And it isn’t getting any better– they add at least $1 trillion to the debt each year.

And the Congressional Budget Office forecasts that the Uncle Sam will NEVER again see an annual budget deficit of less than $1 trillion starting in 2021.

That has serious impact on the ability of the US government to repay its obligations to foreign creditors.

And if the Bolsheviks come to power next year and offer free goodies (paid for with more debt) to anyone with a pulse, the debt burden will explode.

Anyone who thinks owning 10-year US treasuries – or even worse, 30-year government bonds – is risk-free, is completely insane.

The dollar’s problems aren’t limited to the US government’s pitiful finances either.

Even the Federal Reserve– the central bank of the United States– is close to insolvency, according to its own financial statements.

And the Fed’s coffers are routinely plundered by Congress in order to fund pet projects in Washington.

It’s so ridiculous that, in late 2015, Congress passed a law to steal $53.3 billion from the Federal reserve, putting the central bank on the brink of insolvency.

Then of course there’s the looming prospect of escalating US trade wars… and it’s easy to see why so many foreign governments and central banks are diversifying out of the dollar and into gold.

History shows that reserve currencies come and go.

There was a time when the British pound was the dominant currency in the world. And before that, Dutch guilders, Spanish pieces of eight…

Reserve currencies go all the way back before the gold solidus coin of the Byzantine Empire.

Today, the US dollar is the dominant currency in the world.

This is unlikely to change in the near future. But it would be equally foolish to assume that the dollar’s dominance will last forever.

Gold, on the other hand, has been a constant of wealth preservation for nearly all of human history.

It was first used as money more than 3,000 years ago. And an ounce of gold continues to buy roughly the same amount of goods over time.

There are a number of reasons for that. Gold is scarce, portable, and it can stand the test of time without corroding.

Today, I own gold as an insurance policy. It’s a form of wealth with no counter party risk, and one that has global demand.

Virtually anywhere you can possibly go in the world, gold has value, and it’s definitely worth your consideration.

One interesting benefit– we’re living in a time where nearly every other asset is at an all-time high. Stocks, bonds, real estate, etc.

A single troy ounce of gold sells for nearly 50% below its record price from 2011.

Given what’s happening with central banks, foreign governments, and US debt, it’s clear that demand is rising.

But simultaneously, the supply of gold is under a lot of pressure. We’ve discussed before that large mines have been closing, and large producers haven’t invested in new discoveries.

So there could be significant potential for rising gold prices in the future.

And to continue learning how to ensure you thrive no matter what happens next in the world, I encourage you to download our free Perfect Plan B Guide.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

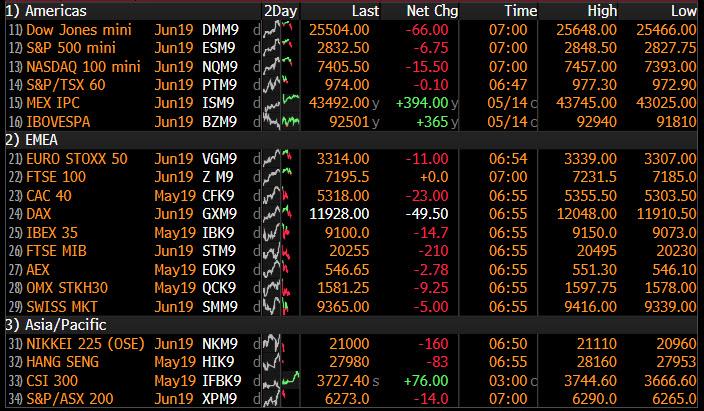

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.8830/

//OFFSHORE YUAN: 6.9148 /shanghai bourse CLOSED UP 55.07 POINTS OR 1.91%

HANG SANG CLOSED UP 146.69 POINTS OR 0.52%

2. Nikkei closed UP 121.33 POINTS OR 0.58%

3. Europe stocks OPENED RED /

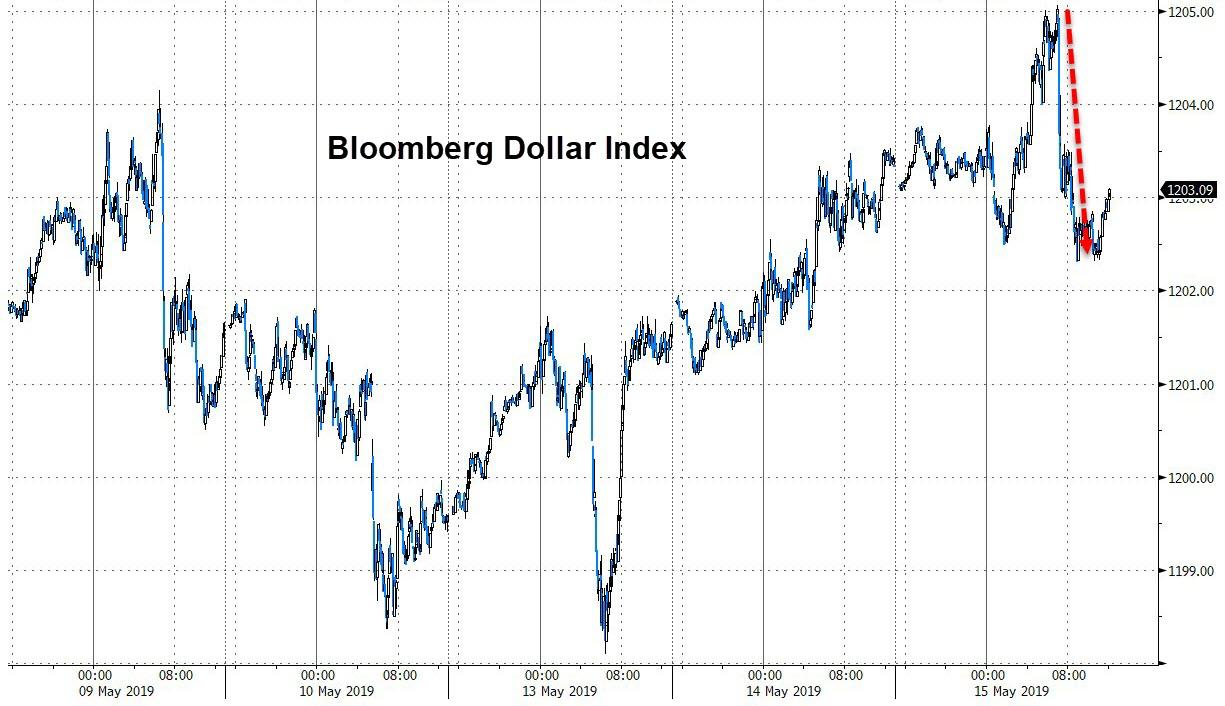

USA dollar index RISES TO 97.64/Euro FALLS TO 1.1184

3b Japan 10 year bond yield: FALLS TO. –.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.35/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.07 and Brent: 70.22

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

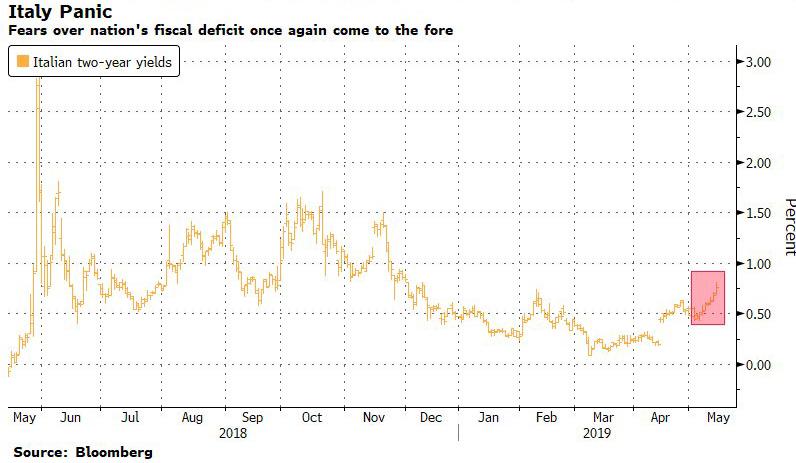

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.12%/Italian 10 yr bond yield UP to 2.77% /SPAIN 10 YR BOND YIELD DOWN TO 0.96%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.89: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.57

3k Gold at $1300.00 silver at: 14.82 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 7/100 in roubles/dollar) 64.84

3m oil into the 61 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.35 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0082 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.175 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.12%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.38% early this morning. Thirty year rate at 2.82%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.0639..they are toast

Markets Slide Despite Stimulus Hopes After Dire Chinese Data; Yields Plunge

It’s about time we had some bad news which, as everyone knows, is great news for central-bank supported, centrally-planned markets.

The global equity bounce following what many misinterpreted as softer rhetoric by President Donald Trump on the trade dispute with China, fizzled on Wednesday despite dismal Chinese data, while fresh Italian debt woes kept BTFDers on the sidelines.

Ironically, China’s data miss was not the catalyst for the drop. As we reported last night, in April every Chinese economic metric posted a sharp decline and missed expectations:

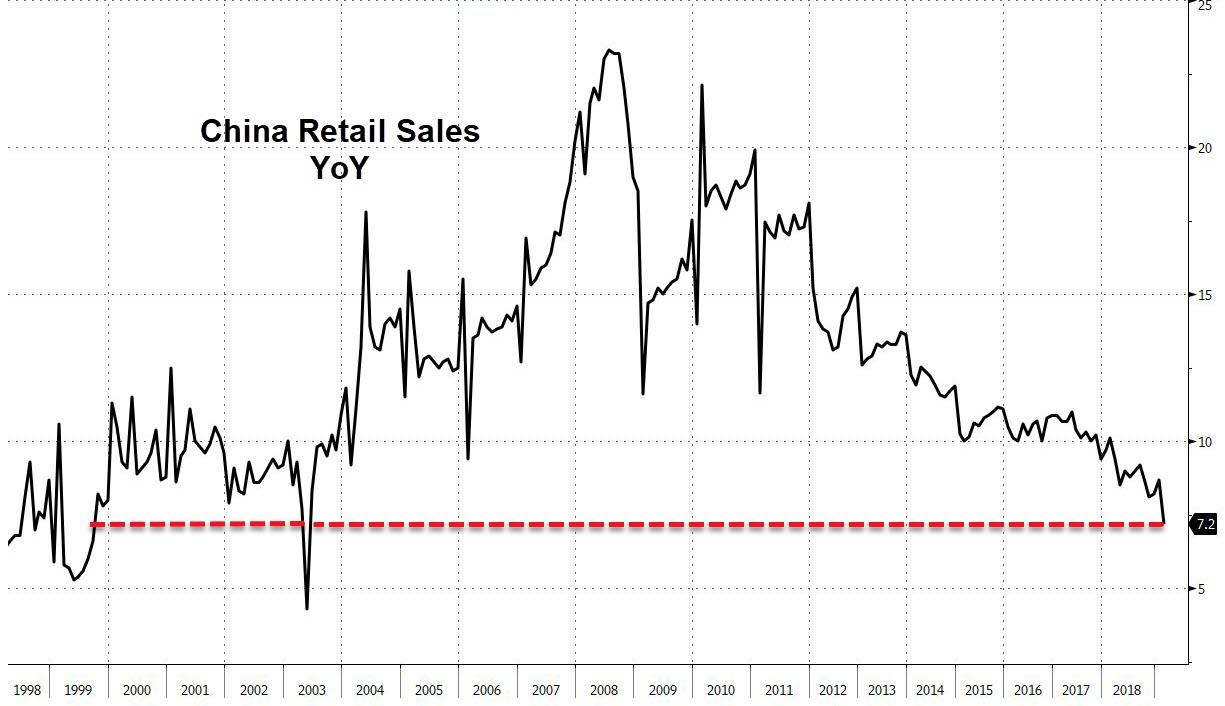

- Retail sales rose just 7.2% (against +8.7% in March) – lowest since May 2003 (the 7.2% year-on-year rise in retail sales is actually weaker than all the estimates. The lowest was 7.5%, and the median was 8.6%)

- Industrial Production growth slumped from a hope-filled +6.5% YTD YoY in March to 6.2%.

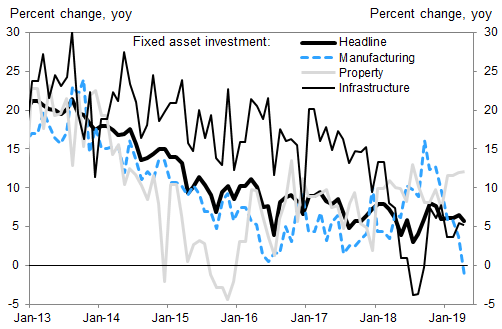

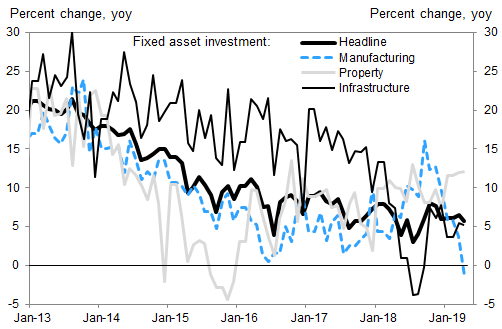

- Fixed Asset Investment slowed to just 6.1% YoY.

“Investors had been waiting for data to confirm signs of stabilization in the Chinese economy which, in turn, would bolster expectations that the global economy could start making a sustainable recovery,” said Neil McKinnon at VTB Capital. “The recent escalation in tariffs makes that more difficult and can only add to investor risk aversion and increase the risk of a more prolonged economic downturn.”

However, considering the surge in Chinese stocks, which closed 1.9% higher as traders speculated Beijing will consider more measures to support the economy after data showed weaker-than-expected growth in April, the only thing about the dismal Chinese data is that it wasn’t even worse to prompt even greater global hopes for a Chinese stimulus.

As a result, the MSCI Asia Pacific Index gained for the first time in three days, with China rebounding and Indonesia declining. MSCI Asia Pac rose +0.5%, with top contributors including: CAR Inc +13%, Renesas +11%, Meitu +11%, Luzhou Laojiao +10%, Mitsubishi Estate +9.2%; in Japan, the Topix Index rose 0.6%, the same as the Nikkei 225, while Hong Kong’s Hang Seng Index +0.5%, an the CSI 300 was 2.2% higher.

China’s horrendous economic data was not enough to spark a buying frenzy on stimulus hopes in Europe, where Italian bonds and stocks traded lower with automakers falling the most, though off session lows, as risk sentiment remains nervous in the wake of trade and domestic political concerns. European bank stocks underperformed the SXXP on Wednesday, with the sector index falling 0.9% as three lenders post earnings misses and the latest bout of merger speculation fades.

- Austria’s Raiffeisen Bank International was the biggest decliner on the Stoxx 600 Banks Index after its 1Q profit missed estimates; stock drops as much as 5.4%

- Credit Agricole slid as much as 3.9%, also related to a profit miss as higher costs eat into earnings

- ABN Amro down 2.6%, falling to the lowest since Oct. 2016 after reporting a 20% decline in 1Q profit due to negative interest rates and Brexit preparations

- Commerzbank erased an early 2.9% gain and is down 2.2% at 10:20 a.m. in Frankfurt; The stock jumped 4.3% on Tuesday on a report that ING and UniCredit are lining up advisers to explore a potential takeover of the German lender

As reported yesterday, investor concerns continue to rise over Italy’s fiscal situation after Rome said it was ready to break EU fiscal rules to spur employment. Italian stocks declined 0.7% to lead European stocks lower while France’s benchmark slipped 0.4%. Data confirming that Germany’s economy had returned to growth in the first quarter cushioned the DAX which eased 0.2%. London’s FTSE rose 0.2%. AS a result, the Euro Stoxx 50 trades down 0.2%, having traded as much as -0.7% earlier, with move lower led by autos and basic resources.

The souring mood also looked to spill over to Wall Street with U.S. futures pointing to a softer open following healthy gains in the previous session. MSCI’s broadest index of world stocks traded flat.

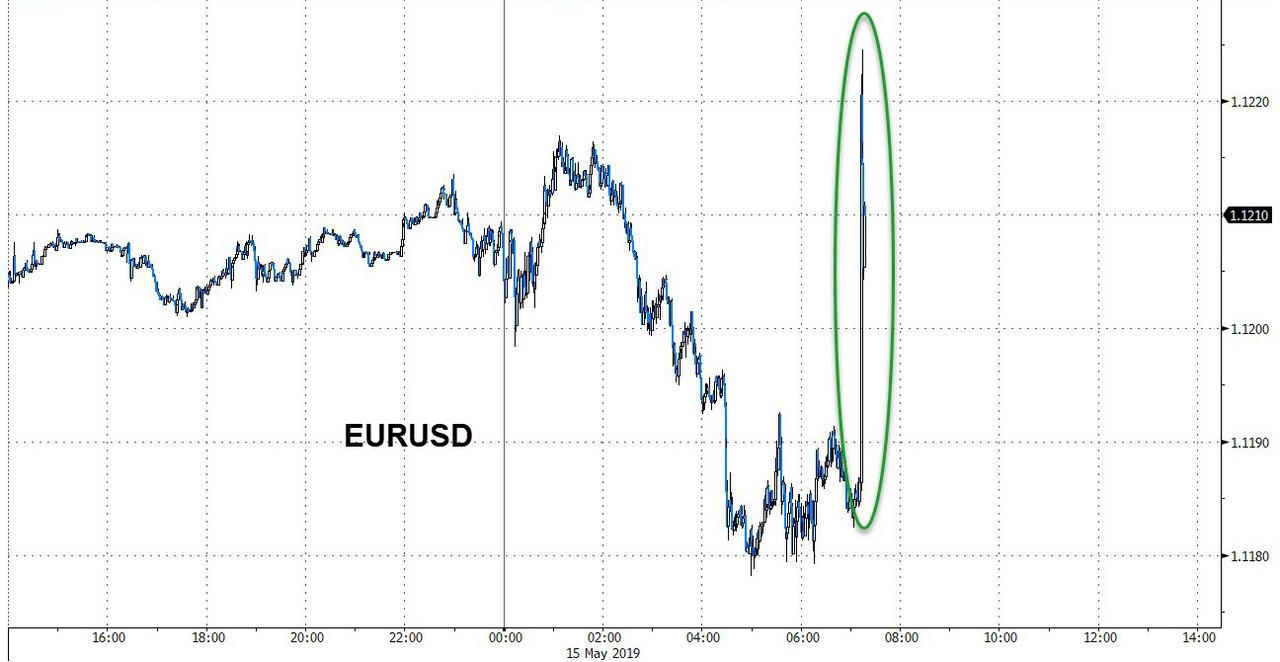

In currency markets, the Australian dollar – a proxy of China-related trades – fell to its lowest level in three months amid the China data fallout. The Bloomberg USD neared session highs, not long after it traded down to unchanged, with most G-10 pairs trading in tight ranges. The euro remained anchored at $1.1214 while the dollar index against a basket of six major currencies was nearly flat at 97.524 after gaining 0.2% the previous day. The pound remained near a two-week low after Prime Minister Theresa May’s spokesman said late on Tuesday she planned to put forward her thrice-rejected Brexit deal in early June to try to secure an agreement on how to extract Britain from the European Union before the summer holiday.

The Chinese yuan was a shade firmer at 6.9056 per dollar in offshore trade, having edged away from a five-month trough of 6.9200 set on Tuesday.

In rates, Italian yields rise across the 2y-10y tenors, with curve bear flattening, with 2-yr yields +8bps and 10-yr yields +3bps.

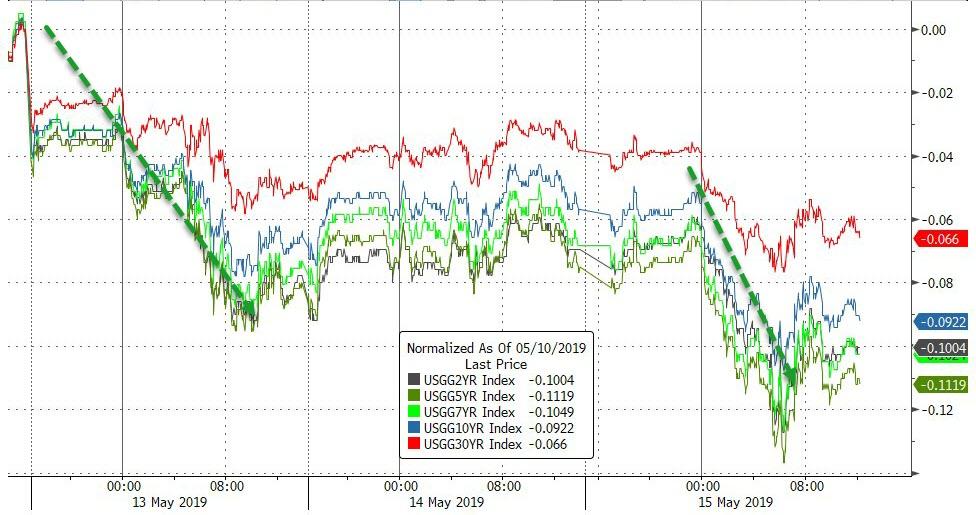

Haven bonds outperform, with 10-yr bund yield -3bps to -0.10%, lowest level since 2016, and 10-yr UST yield -2bps to 2.39%. In the US, Treasury yields sank to the lowest level since March, while yields on 10-year German bunds slipped to the lowest since 2016, but they jumped for Italy’s debt, as the nation’s deputy premier Matteo Salvini racheted up tensions over the country’s deficit.

In commodities, both WTI ($61.38) and Brent ($71.03) traded lower after API reported a bigger-than-expected build in crude inventory and IEA cut its forecast for 2019 oil demand. U.S. crude inventories rose by 8.6 million barrels in the week to May 10 to 477.8 million, compared with analysts’ expectations for a decrease of 800,000 barrels. Brent and WTI surged the previous day after Saudi Arabia said explosive-laden drones launched by a Yemeni-armed movement aligned to Iran had attacked facilities belonging to state oil company Aramco.

Expected data include mortgage applications, retail sales, and industrial production. Alibaba, Macy’s, and Cisco are among companies reporting earnings

Market Snapshot

- S&P 500 futures little changed at 2,839.25

- MXAP up 0.5% to 155.33

- MXAPJ up 0.4% to 510.12

- Nikkei up 0.6% to 21,188.56

- Topix up 0.6% to 1,544.15

- Hang Seng Index up 0.5% to 28,268.71

- Shanghai Composite up 1.9% to 2,938.68

- Sensex up 0.5% to 37,485.81

- Australia S&P/ASX 200 up 0.7% to 6,284.20

- Kospi up 0.5% to 2,092.78

- STOXX Europe 600 down 0.1% to 375.80

- German 10Y yield fell 2.4 bps to -0.094%

- Euro up 0.08% to $1.1213

- Italian 10Y yield rose 2.9 bps to 2.355%

- Spanish 10Y yield fell 0.5 bps to 0.966%

- Brent futures down 0.3% to $71.06/bbl

- Gold spot up 0.1% to $1,298.37

- U.S. Dollar Index down 0.1% to 97.47

Top Overnight News

- Theresa May set a date for her final Brexit showdown, promising to bring her deal back to Parliament at the start of June

- China’s economy lost steam in April, underscoring the fragility of the world’s second-largest economy as it girds for an intensified face-off with the U.S. over trade. Industrial output, retail sales and investment all slowed more than economists forecast

- Trump rejected a report that his administration is planning for war with Iran, but then warned he’d send “a hell of a lot more” than 120,000 troops to the Middle East in the event of hostilities

- President Donald Trump called on the Federal Reserve to “match” what he said China would do to offset economic hardship being caused by tariffs as he sought to draft the U.S. central bank into his simmering trade war

- New York Fed President John Williams and his Kansas City colleague Esther George, who vote on policy this year, acknowledged that new tariffs on Chinese imports could affect the outlook for U.S. inflation and growth. But both saw no need for the central bank to react

- Japanese Prime Minister Shinzo Abe said propping up domestic demand would be a priority for his government as economic data show signs of weakness ahead of a planned increase in the sales tax in October

- Germany’s economy emerged from stagnation at the beginning of 2019, returning to growth despite a slump in manufacturing that continues to plague the nation.

- U.K.’s Theresa May will bring her Brexit deal back to Parliament at the start of June in the hope that she can persuade MPs to support it

Asian equity markets eventually traded mostly higher following the positive lead from the US where sentiment was underpinned by President Trump’s optimism regarding a US-China trade deal, but with gains in the Asia-Pac region capped as participants digested earnings, as well as disappointing Chinese Industrial Production and Retail Sales data. ASX 200 (+0.7%) was led higher by strength in tech as the sector tracked the outperformance of its counterpart stateside, while Nikkei (+0.6%) mirrored a somewhat indecisive currency with heavy losses seen in Takeda and Nissan shares post-earnings. Hang Seng (+0.5%) and Shanghai Comp. (+1.9%) were positive after President Trump’s encouraging rhetoric and with the first phase of the PBoC’s targeted RRR adjustment taking effect today which would release around CNY 100bln of long-term funds and resulted to a decline in Chinese money market rates, although the gains across the region were somewhat capped by disappointing Chinese Industrial Production and Retail Sales data. Finally, 10yr JGBs were flat with price action hampered by the ambiguous risk tone in Japan and with today’s BoJ Rinban operation at a relatively paltry JPY 505bln concentrated in the belly.

Top Asian News

- China’s Xi Calls Efforts to Reshape Other Nations ’Foolish’

- Turkey Imposes 0.1% Tax for Some Foreign Exchange Transactions

- Rich Asia Investors Face Rising Risk in Leveraged Bond Funds

- Wanda to Plow Billions Into China After Dumping Assets Abroad

Choppy trade in European equities [Eurostoxx 50 -0.6%] following on from a positive Asia-Pac as sentiment deteriorated in early trade. Major indices are now mostly lower after opening with marginal gains, although initial downside coincided with defensive comments from China’s Foreign Minister, which seemed to have dampened the prospects of a US-China trade deal in the near term. Sectors are mostly lower with defensive stocks buoyed for the time being and broad-based losses seen across the rest. In terms of individual movers, Renault (-4.0%) fell to the foot of the CAC as shares of its alliance partner Nissan tumbled in the wake of dismal earnings. Meanwhile, Italian banks [Intesa Sanpaolo -1.7%, Unicredit -1.5%, Banco BPM -1.5%] fell in tandem with the decline in BTPs (albeit off lows), given the banks’ large holdings of the sovereign debt. Elsewhere, given the looming US auto import tariffs deadline (May 18th), analyst at Morgan Stanley believe that the German economy will be hit the hardest due to direct impact and through supply chains, adding that Germany’s exports of vehicles and auto parts to the US make up around 2% of the total goods exports, thus, “a US car tariff increase to 25% could lower growth in Germany by ~0.25pp, with any knock-on impact on sentiment on top.”

Top European News

- German Economy Rebounds From Stagnation With 0.4% Expansion

- Credit Agricole Revenue Misses Estimates on Key Italian Market

- Italy Rocks European Bond Markets Over Its Deficit Once Again

- Pound Turns Currency Laggard as Brexit Bad News Is Seen Looming

In FX, we start with CHF/JPY/EUR/GBP – The Franc is back in favour and outperforming after a temporary loss of safe-haven appeal on Tuesday as a combination of sub-forecast Chinese data (IP and retail sales) and Italian fiscal jitters offset less acute angst on the US-China trade front, although the latest barbs from Beijing have been quite inflammatory. Usd/Chf has retreated towards 1.0050 again and Eur/Chf is back down below 1.1300 even though the single currency remains relatively resilient vs a broadly firm Dollar having survived another test of 1.1200 with the aid of some firm Eurozone GDP prints. Meanwhile, Usd/Jpy has also pulled back from yesterday’s rebound highs to probe bids under 109.50 and expose Fib support at 109.23 that was breached on Monday when the headline pair got to within a whisker of 109.00. Note, however, decent option expiry interest may keep the headline pair afloat given 1.2 bn rolling off between 109.00-20 and almost 1.8 bn at 109.40-50. Elsewhere, the Pound has also defended poignant big figure levels at 1.2900 in Cable and 0.8700 vs the Euro as UK PM May prepares for Thursday’s 1922 showdown and another stab at getting the WA through the HoC in early June.

- AUD/NZD/CAD – All under pressure and down vs their US counterpart, with the Aussie hit by soft wages on top of the aforementioned disappointing Chinese macro releases ahead of tomorrow’s jobs report that has been flagged by the RBA as key in terms of near term policy and whether a rate cut is required. Aud/Usd is just off fresh multi-month lows around 0.6920 and Aud/Nzd is pivoting 1.0550 as the Kiwi hovers just above 0.6550 against the Greenback. Meanwhile, the Loonie is meandering between 1.3476-56 and in a tighter range than on Tuesday awaiting some independent impetus/direction from Canadian CPI that is due alongside US retail sales and with the DXY equally contained within 97.432-578 parameters and just above the 30 DMA (97.417).

- EM – The Lira remains in the spotlight and volatile after yesterday’s seemingly impressive recovery, as Usd/Try bounced back over 6.0000 despite more efforts by the CBRT to stop the rot via a return of tax

In commodities, WTI (-1.3%) and Brent (-0.9%) futures are on the backfoot with the initial decline sparked by a substantial surprise build in API crude inventories (+8.6mln vs. Exp. -1.3mln). Crude prices then recovered off lows amid positive sentiment in Asia-Pac trade before an intensifying risk-averse mood pressured the complex. Upside in the energy market is also capped by the IEA Monthly Oil Report which cut 2019 oil demand growth estimate by 90k bpd to 1.3mln bpd, in contrast to yesterday’s OPEC monthly report where the total world oil demand growth for 2019 was left unchanged at 1.21mln BPD. On a technical front, WTI Jun’19 futures reside just below its 50 DMA (61.45) ahead of its 200 DMA (60.40) whilst its Brent counterpart seems to have been recently finding support its 50 DMA (currently at 69.78). Looking ahead, traders will be keeping an eye out for the more widely followed EIA crude stocks release later today wherein ING agrees that numbers similar to the API would likely be seen as bearish in the immediate term. Elsewhere, the receding buck and soured risk tone has modestly supported gold (+0.3%) in recent trade, as the yellow metal fluctuates above its 100 DMA (1296.64) and in close proximity to the 1300/oz level. Meanwhile, Chinese steel production increased by 12.7% Y/Y to the highest level on record as stronger margins allowed steel mills to increase utilisation rates. However, ING believes that margins can come under pressure moving forwards as “the more recent strength in Chinese steel prices [are] reflecting stock building following the Chinese New Year.”

US Event Calendar

- 7am: MBA Mortgage Applications, prior 2.7%

- 8:30am: Empire Manufacturing, est. 8, prior 10.1

- 8:30am: Retail Sales Advance MoM, est. 0.2%, prior 1.6%; Retail Sales Ex Auto MoM, est. 0.7%, prior 1.2%; Retail Sales Control Group, est. 0.3%, prior 1.0%

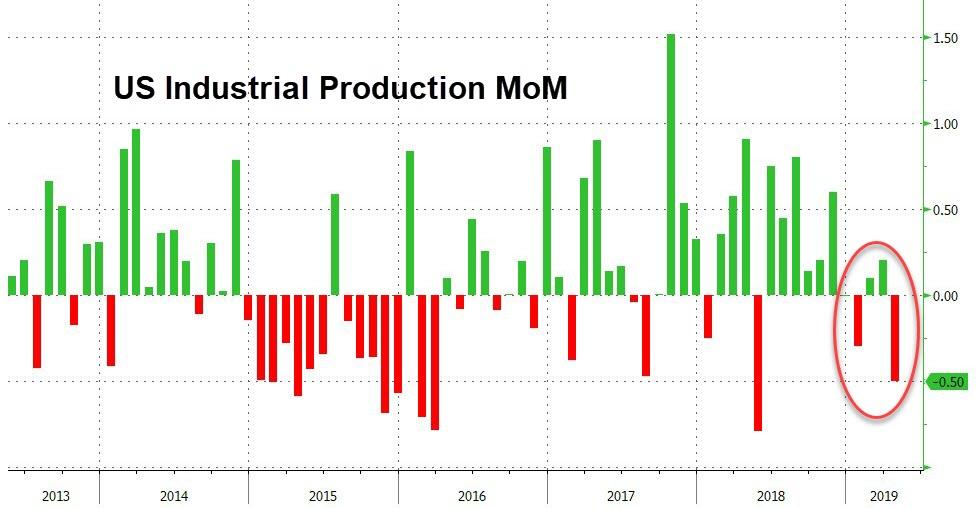

- 9:15am: Industrial Production MoM, est. 0.0%, prior -0.1%; Manufacturing (SIC) Production, est. 0.0%, prior 0.0%

- 10am: NAHB Housing Market Index, est. 64, prior 63

- 10am: Business Inventories, est. 0.0%, prior 0.3%

- 4pm: Net Long-term TIC Flows, prior $51.9b; Total Net TIC Flows, prior $21.6b deficit

DB’s Jim Reid concludes the overnight wrap

Given the thousands of cold, dark, early starts that have been associated with writing the EMR over the last 12-13 years, I hope readers will forgive me one indulgence in setting the scene in front of me in contributing to today’s edition. I’m on the US West Coast and the moon is alighting the coastline and I can hear the gentle caressing of waves upon the shore below. I have a small glass of red and I’m about to fall into a blissful sleep as jet lag catches up with me. After a tough 10 days, even markets are starting to look better. However, this scene won’t last forever and maybe the recovery might not either.

Indeed, although markets might have staged a mini recovery yesterday it wasn’t like there was a material piece of new news to help drive a change in view on the US-China trade spat.The fact that both sides appear willing to continue conversing is perhaps fuelling some hope that there will still be a positive outcome to this down the line but it’s hard to see it disappearing from our screens anytime soon. The next point of call will be the data with a number of sentiment indicators due out from the end of this month which should capture this recent escalation. Indeed, yesterday NY Fed President Williams said he is focused on the latest survey data to gauge the impact of the trade stress. Until then, its likely markets remain in a state of relative flux.

The recovery for risk yesterday included a +0.80% gain for the S&P 500 – only the second positive day in the last six sessions. At a sector level some of the biggest gains were reserved for the recently beaten up tech and financials sectors. Indeed the NASDAQ closed up +1.14% although is still down -2.30% this week while the DOW rose +0.82%. The semi-conductor index also closed up +2.40%, halving its loss on the week. In Europe the STOXX 600 finished +1.01% and DAX +0.97%. The VIX (-2.2pts) also dipped back below 20 while in credit US HY spreads ended -2bps tighter. The recent rally for Treasuries also abated with 2y and 10y yields both rising +0.9bps, although Bunds did hold back down at the lowly levels of -0.072%. BTPs (+2.9bps) did however underperform on the back of headlines quoting Northern League head Salvini as saying that Italy is ready to break EU fiscal rules. His coalition partner Luigi di Maio of the Five Star Movement directly contradicted him to reporters, calling Salvini’s comments “irresponsible” and cited the widening spread to bunds as a concern. In normal times that might be encouraging to hear from an Italian politician, but since it currently also implies stress within the coalition and potentially elevated odds of an early election, such internal dissent is not optimal. Elsewhere EM FX (+0.14%) had a rare up day, helped by the offshore yuan’s +0.12% rally, its first in six sessions. That also helped the MSCI EM equity index gain +1.40%, while safe haven currencies like the Yen (-0.28%) and Swiss Franc (-0.23%) slipped.

This morning Asia has followed the lead from Wall Street with gains led by China with the Shanghai Comp and CSI 300 gaining +1.10% and +1.35% respectively. That actually comes despite disappointing data following the release of the April activity indicators in China. Industrial production (+5.4% yoy vs. +6.5% expected), retail sales (+7.2% yoy vs. +8.6% expected) and fixed asset investment (+6.1% ytd yoy vs. +6.4% expected) all missed and slipped from March, although a bright spot was property investment which rose one-tenth to +11.9% yoy. Overall though the data does throw a little bit of doubt into the recovery thesis especially given the timing just before the latest ratcheting up in the trade war which makes next month’s data of significance. We should note that the data has been countered by a comment from a spokesman for the National Bureau of Statistics who said China still has ample room to step up policy support – suggesting further scope for policy stimuli – which appears to be helping to support markets this morning. The Hang Seng (+0.73%), Nikkei (+0.18%) and Kospi (+0.55%) are posting more modest gains.

Back to yesterday where the main trade headlines of note included China’s Global Times running an editorial carried by the Xinhau News Agency that included a reference to the “people’s war” against Washington’s “greed and arrogance” and the Chinese “fighting back to protect its legitimate interest”. A separate story from the Global Times claimed that “what is important is how much pain the US economy will be forced to endure”.

As for Trump, the President tweeted that “when the time is right we will make a deal with China” and that “my respect and friendship with President Xi is unlimited but, as I have told him many times before, this must be a great deal for the United States or it just doesn’t make any sense”.Trump also tweeted that “China will be pumping money into their system and probably reducing interest rates, as always, in order to make up for the business they are, and will be, losing….if the Federal Reserve ever did a ‘match’, it would be game over”. Away from that Axios reported a senior administration official as saying that a “trade deal with China isn’t close and the US could be in for a long trade war”.So all in all nothing that really suggests there is a feeling of de-escalation around the corner. Markets seemed to like the fact that Trump is still focused on a deal and that he continues to speak in good terms about President Xi.

One last mention of trade for this morning, yesterday Craig published a short note looking at potential returns and spreads for USD HY under scenarios of further trade escalation filtering through to the trade proxy PMI, as well as relative sector betas and r-squareds to trade. See his note here .

In other news, Sterling underperformed again yesterday, sliding -0.41% versus the dollar and -0.25% versus the euro (to its lowest level since February), as the situation around Brexit continued to deteriorate.The government confirmed last night that it plans to bring a Brexit bill back to Parliament in early June. There are two problems with this: 1) Labour is not on board, with one official saying “today hasn’t helped” after the hard-Brexit wing of the conservative party dug in their heels against a customs union, and 2) the European Parliament elections are likely to show a big setback for the Conservative party, which would weaken Prime Minister May’s position. A poll yesterday (Kantar Public) showed Labour 9pts ahead of the Tories. Something has to give soon and perhaps this will be Mrs May last roll of the leadership dice.

We also got some Fedspeak yesterday, with NY Fed President Williams speaking in Zurich and repeating the mantra that “policy is in the right place.” He went on to say that he doesn’t “see any reason to have a bias up or downward,” confirming that policy is on hold for now. This view was subsequently reiterated by The Kansas City Fed’s Esther George, considered the most hawkish member of the committee, who said “the wait-and-see approach is appropriate.” She did hedge a little, saying that a 50bps undershoot of the 2% inflation target was acceptable to her, which is more in-line with her prior views but shouldn’t signal any change to the centre of the committee’s thinking.

As for economic data, the highlight was the latest UK jobs report which showed the unemployment rate down 0.1pp to 3.8%, a fresh 44-year low, while wage inflation was softer than expected at 3.2% from 3.5%. In Germany, April headline CPI was confirmed at 2.0% yoy, while the ZEW survey was mixed. The current situation assessment rose to 8.2 from 5.5, but the expectations component slid to -2.1 from 3.1. The euro area ZEW expectations index similarly fell to -1.6 from 4.5. In the US, import prices were softer than expected at 0.2% mom versus expectations for 0.7%. That miss can largely be explained by the dollar’s recent rally, so the effect should fade over the next few months. Separately, the NFIB small business optimism survey rose to 103.5 from 101.8, better than expected and the third consecutive rise.

Looking at the day ahead, this morning we’re due to get a first look at Q1 GDP for Germany where the consensus is for a +0.4% qoq reading. Later on this morning we’ll also get a second reading of Q1 GDP for the Euro Area. A reminder that the flash showed a +0.4% qoq print. Also due this morning is the final April CPI revisions in France and Q1 employment data for the Euro Area. In the US this afternoon we’ve got the April retail sales report due up where the consensus expects a +0.3% mom core and control group reading. We’ll also get the May empire manufacturing reading, April industrial production reading, May NAHB housing market index reading and March business inventories print. Away from the data we’ve got the Fed’s Quarles and Barkin due to speak, along with the ECB’s Coeure and Praet.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 55.07 POINTS OR 1.91% //Hang Sang CLOSED UP 146.69 POINTS OR 0.52% /The Nikkei closed UP 121.33 POINTS OR 0.58%//Australia’s all ordinaires CLOSED UP .69%

/Chinese yuan (ONSHORE) closed DOWN at 6.8830 /Oil UP to 61.64 dollars per barrel for WTI and 71.08 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8830 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9148 TRADE TALKS STILL ON//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP THREATENS TO RAISE RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

i)China/

China reports today, like the USA that all green shoots are dead. China’s retail sales and Industrial production falter.

(courtesy zerohedge)

China ‘Green Shoots’ Are Dead – Retail Sales, Industrial Production, & FAI Slump

And there goes another ‘narrative’…

On the back of one better than expected soft survey PMI print, the world became convinced that as green shoots emerged, China was about to be reborn into magnificent credit-fuelled expansion and would save the world.

Tonight, that narrative died – everything missed expectations:

- Retail sales rose just 7.2% (against +8.7% in March) – lowest since May 2003 (the 7.2% year-on-year rise in retail sales is actually weaker than all the estimates. The lowest was 7.5%, and the median was 8.6%)

- Industrial Production growth slumped from a hope-filled +6.5% YTD YoY in March to 6.2%.

- Fixed Asset Investment slowed to just 6.1% YoY.

Not green shoot-y!

Bloomberg’s Wes Goodman sums things up:

“The China data miss suggests the U.S. tariffs already in place are biting, putting the stocks gain Wednesday at risk. For now China shares are up strongly, even if gains have been pared, while the Aussie dollar is holding above earlier lows.”

Don’t worry though – there’s more stimulus to come everyone:

China’s NBS says it will implement counter-cyclical adjustments to maintain steady, healthy economic development.

Raymond Yeung of ANZ Bank makes the point that China needs to maintain growth above 6.3% or above.

“Today’s numbers are not supportive. We believe the State Council will launch more measures to shore up the market sentiment. More tax cuts and consumer subsidies are in the pipeline.”

Because all the stimulus so far has been working so well until now!

Blooomberg’s Enda Curran notes that numbers these bad will heighten scrutiny of the yuan’s moves. Will Beijing allow it to soften materially from here or will they keep a floor under it? It’s a double-edged sword for them.

The weaker the yuan, the greater the risk of financial market instability and the need for intervention. At the same time though, with exporters facing rising tariffs and slowing growth, the currency will remain center stage.

Does this move the trade deal pendulum back in Trump’s favor, forcing China to make a deal? We suspect that will be the bullish spin by the morning and why you should by any dip…

Finally there is this Orwellian nonsense – China’s economy is increasingly resilient to risks, the stats bureau spokeswoman says despite the weaker-than-expected data.

end

Huawei offers to sign a “no spy” pact with governments as the UK is set on embark on 5 G

(courtesy zerohedge)

Huawei Offers To Sign ‘No-Spy’ Pacts With Governments As UK Embarks On 5G

Chinese smartphone and telecommunications equipment giant Huawei is willing to sign ‘no-spy’ agreements with governments which adopt their technology, including Britain, according to chairman Liang Hua.

The Trump administration has warned allies not to use Huawei’s technology to implement 5G networks over concerns that they would allow Chinese intelligence services to spy on whoever uses it.

Moreover, Huawei and its CFO, Meng Wanzhou, are facing criminal charges in the United States over the alleged theft of trade secrets and sanctions violations in Iran.

As Reuters reports, Britain is still deciding on how much they will rely on Huawei – the world’s largest supplier of telecom equipment – for their 5G networks.

“The security and resilience of the UK’s telecoms networks is of paramount importance, and we have strict controls for how Huawei equipment is currently deployed in the UK,” said a spokesman for the British government on Tuesday, adding that the results of a supply chain review would be announced soon.

Prime Minister Theresa May sacked her defense minister, Gavin Williamson, this month over leaked claims that Huawei would have a role in the 5G network, putting Britain at odds with its biggest intelligence ally, the United States.

Williamson has denied he leaked from the confidential talks.

Liang, speaking on the sidelines of a meeting with Huawei’s British technology partners, said the company never intended to be in the eye of a political storm. –Reuters

“The cyber security issue is not exclusive to just one single supplier or one single company, it is a common challenge facing the entire industry and the entire world,” said Liang, adding that Huawei had long cooperated with the UK’s National Cyber Security Centre’s technology oversight efforts, while improving its software engineering capabilities.

Liang also said that Huawei does not take direction or act on behalf of the Chinese government in any international market.

“Despite the fact Huawei has its headquarters in China, we are actually a globally operating company,” he said, adding “Where we are operating globally we are committed to be compliant with the locally applicable laws and regulations in that country.”

“There are no Chinese laws requiring companies to collect intelligence from a foreign government or implant back doors for the government.”

Last month, Ars Technica reported the discovery of a backdoor-like vulnerability in Huawei’s Matebook laptop series which could have allowed remote hackers to gain access to the system. Microsoft confirmed the security flaws were discovered by Windows Defender Advanced Threat Protection (ATP) kernel sensors, which traced the vulnerability back to a Huawei driver.

Huawei responded to Tom’s Hardware’s inquiry about the Matebook security flaw. They reiterated that the security flaw was not a backdoor attempt to spy on customers. Huawei also suggested it may take legal action against media over “misleading reports” about this issue.

UK minister Jeremy Wright will announce the findings of the government’s telco supply-chain review soon, and has said that the benefits of cheap Chinese equipment would not take precedence over security concerns.

Liang pushed back, suggesting that economic factors should be a top consideration, saying “I believe the decision should be based on risk assessment and supply-chain assessment, and should also reflect the requirements the UK has in terms of economic development when they choose suppliers,” and adding “Cyber security is indeed a very important factor to consider (…) but at the same time it should be a balanced decision between cyber security and economic prosperity.”

Huawei has inked over 40 5G contracts; 25 in Europe, 10 in the Middle East and six in Asia.

As Reuters notes, Germany says they’ve seen no indication that the company was offering a “no-spy” agreement.

In Latest Move Against Huawei, Trump To Order New Restrictions On Foreign Telecom Companies

In what appears to be the US government’s latest salvo in its war against Huawei, President Trump is reportedly preparing to sign an executive order that would prohibit American firms from using equipment made by foreign telecom companies that pose a ‘security threat’, according to Bloomberg, which sourced its report to administration insiders.

The official who spoke with Bloomberg insisted the order wasn’t intended to single out any country or company, but anybody who has been following the ongoing spat with Huawei should instantly recognize that this simply isn’t true (though, with the trade negotiations at a very delicate impasse, we understand why the administration needs to maintain this pretense). Though Huawei and its fellow Chinese telecoms giant ZTE already face serious restrictions on selling their products in the US, Huawei still maintains a US subsidiary in Texas.

The order, which could be signed as soon as Wednesday, wouldn’t outright ban sales to US entities, but it would grant the Commerce Department more authority to review products and purchases made by firms with connections to adversarial countries (we doubt that’s directed at Ericsson and Sweden).

China’s foreign ministry has already lashed out at the US over reports of the executive order.

“This is neither graceful nor fair,” ministry spokesman Geng Shuang said at a news briefing in Beijing. “We urge the U.S. to stop citing security concerns as an excuse to unreasonably suppress Chinese companies and provide a fair and equitable and non-discriminatory environment for Chinese companies to operate in the U.S.”

Washington has been campaigning for months to stop its allies around the globe from allowing Huawei products to be used in their 5G networks, but to little avail. Yesterday, Huawei promised to sign a “no spy” pledge to governments like the UK that are still deciding how much reliance on Huawei they are willing to stomach.

As Huawei pushes to assume a global leadership position in 5G, the US’s efforts to try and discredit the company have included successfully pushing for the arrest of its CFO, Meng Wanzhou, in Canada, on charges she helped the company violate US sanctions on Iran.

American lawmakers suspect Huawei’s equipment could be used for spying – and not without reason.

Just last month, Ars Technica found a backdoor like vulnerability in Huawei’s Matebook laptop series which could have allowed remote hackers to gain access to the system. Chinese law also could technically compel companies like Huawei to cooperate with authorities.

But even if the order is signed on Wednesday, it might not take effect for six months, as it would take time for the Commerce Department to “fashion an approach” to the order.

In the meantime, Verizon and other US telecoms firms are still way behind in the war to dominate the global market for 5G networking equipment.

Latest Trade War Developments

Between Trump tweets and Chinese whispers via state-controlled media, it can be difficult to pinpoint precisely where things stand in the ongoing battle between the world’s two economic superpowers. Saxo’s Christopher Dembik says the CNYUSD rate is the best proxy we have. Here’s why.

Submitted by Christopher Dembik of SaxoBank

As Saxo Head of FX Strategy John Hardy and I both mentioned, we need to look closely at the Chinese yuan this week. In my view, the yuan fixing is the right proxy to understand how the US-China trade negotiations are going. And it isn’t pretty! Since the end of last week, the yuan/dollar fixing has been cut by 45pips to 6.8365. As negotiations are probably going nowhere in the coming days, we could see the fixing moving closer to 6.90. However, I don’t think that the psychological threshold of 7.00 could be reached as it would have deep negative consequences on local firms that use their CNY profits to repay their USD debt. A large devaluation is still a risk but is not the central scenario for the Chinese authorities.

Softer tone in the US vs tougher tone in China

Yesterday evening, senior Trump administration officials tried to appease tensions. US secretary of the Treasury Mnuchin confirmed, without giving much detail, that the US-China trade talks are still ongoing. The tone is clearly different in China where the official media, such as CCTV and People’s Daily, adopted a tougher stance. It is interesting to note that in the previous rounds of trade disputes that occurred since Autumn 2018, People’s Daily articles mostly used the term “trade friction” instead of “trade war” until now… As of yesterday, all the articles and TV reports mention “trade war”. This terminology change means a lot and confirms that the negotiations have entered a more dangerous phase. In addition, China has tightened its “national security” review for foreign investments, which can be considered as another step in the retaliation process.

This is not 2018 again in the FX market

Looking at the initial reaction of the market yesterday, it is likely that the USD will not benefit from the trade war, contrary to what happened in 2018, as investors expect its main US impact would be to damage the economy and increase the likelihood of Fed rate cut this year. Investors are betting that there is a 60%-70% probability that the December 12 Federal Open Market Committee will see a rate cut. Policymakers are starting to pay attention and it may influence forward guidance in the upcoming June meeting by increasing the focus on the market reaction to the trade war and macroeconomic effect of higher tariffs (leading both to higher inflation and less growth which wwould pose a serious policy dilemma to the Fed).

Trump’s approval rate is still high

On the US domestic front, President Trump is now seeking $15 billion to bail out farmers in order to mitigate the negative impact of the trade war. Interestingly, more and more Republican Congressmen that were interviewed yesterday on US TV were very vocal against the latest measures decided by the Trump administration. It is, however, unlikely to have any influence on the ongoing process or to push the administration to comprise with Beijing. Trump is looking at polls and the message they send is bright and clear: as of yesterday, 42% of US voters supported Trump’s policy (FiveThirtyEight). His electoral base has remained stable, faithful and very broad since he was elected.

What’s next?

- By May 18 – Potential US tariffs on global auto sector.