GOLD: $1285.95 DOWN $11.10 (COMEX TO COMEX CLOSING)

Silver: $14.55 DOWN 26 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1286.70

silver: $14.58

OPTIONS EXPIRY FOR THE STOCK MARKET AND GLD/SLV IS TOMORROW

COMEX EXPIRY FOR GOLD/SILVER: TUES MAY 28/2019

LBMA/OTC EXPIRY: MAY 31.2019

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING

EXCHANGE: COMEX

CONTRACT: MAY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,296.300000000 USD

INTENT DATE: 05/15/2019 DELIVERY DATE: 05/17/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 4

661 C JP MORGAN 39 33

685 C RJ OBRIEN 1

737 C ADVANTAGE 11 17

905 C ADM 5

____________________________________________________________________________________________

TOTAL: 55 55

MONTH TO DATE: 288

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 55 NOTICE(S) FOR 5500 OZ (0.1710 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 288 NOTICES FOR 28800 OZ (.8958 TONNES)

SILVER

FOR MAY

4 NOTICE(S) FILED TODAY FOR 20,000 OZ/

total number of notices filed so far this month: 3377 for 16,885,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$7946 DOWN $285

Bitcoin: FINAL EVENING TRADE: $7820 DOWN $338

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A TINY SIZED 530 CONTRACTS FROM 203,788 UP TO 204,318 WITH YESTERDAY’S 2 CENT GAIN IN SILVER PRICING AT THE COMEX. ,LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER BUT IT NOW IN FULL FORCE FOR GOLD. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 263 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 263 CONTRACTS. WITH THE TRANSFER OF 435 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 263 EFP CONTRACTS TRANSLATES INTO 1.315 MILLION OZ ACCOMPANYING:

1.THE 2 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 18.355 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

13,566 CONTRACTS (FOR 12 TRADING DAYS TOTAL 13,566 CONTRACTS) OR 67,83 MILLION OZ: (AVERAGE PER DAY: 1131 CONTRACTS OR 5.653 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 67.83 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.69% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 808.93 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 530 WITH THE TINY 2 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 263 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE GAINED A SMALL SIZED: 793 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 263 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 530 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 2 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.81 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.022 BILLION OZ TO BE EXACT or 145% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 4 NOTICE(S) FOR 20,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 18.355 MILLION OZ ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG SIZED 6360 CONTRACTS, TO 526,224 DESPITE THE TINY RISE IN THE COMEX GOLD PRICE/(AN INCREASE IN PRICE OF $1.50//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5454 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 5454 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 524,355. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,814 CONTRACTS: 6330 OI CONTRACTS INCREASED AT THE COMEX AND 5454 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 11,814 CONTRACTS OR 1,181,400 OZ OR 36.75 TONNES. YESTERDAY WE HAD A TINY GAIN IN THE PRICE OF GOLD TO THE TUNE OF $1.50….AND WITH THAT TINY GAIN, WE HAD A HUGE GAIN OF 36.75 TONNES!!!!!!.??????

WITH RESPECT TO SPREADING: NOT TO NOTICEABLE WITH TODAY’S FALL IN PRICE

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS HAVE NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 70,859 CONTRACTS OR 7,085,900 OR 220.40 TONNES (12 TRADING DAYS AND THUS AVERAGING: 5904 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAYS IN TONNES: 220.40 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 220.40/3550 x 100% TONNES =6.20% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2035.95 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 6360 DESPITE THE TINY RISE IN PRICING ($1.50) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5454 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5454 EFP CONTRACTS ISSUED, WE HAD A STRONG SIZED GAIN OF 11,814 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5454 CONTRACTS MOVE TO LONDON AND 6360 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 36.75 TONNES). ..AND THIS HUMONGOUS DEMAND OCCURRED WITH A TINY RISE IN PRICE OF $1.50 IN YESTERDAY’S TRADING AT THE COMEX. WE NO DOUBT HAD A STRONG PRESENCE OF SPREADING TODAY.

we had: 55 notice(s) filed upon for 5500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $11.10 TODAY

WE HAVE A HUGE WITHDRAWAL OF 3.23 TONNES OF GOLD FROM THE GLD.

STRANGE THIS IS THE EXACT DEPOSIT AMOUNT PUT INTO THE GLD ON MAY 14//.

INVENTORY RESTS AT 733.23 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORy

SLV/

WITH SILVER DOWN 26 CENTS TODAY:

A BIG CHANGE IN SILVER INVENTORY AT THE SLV//

A WITHDRAWAL OF 1.031 MILLION OZ FROM THE SLV.

/INVENTORY RESTS AT 315.551 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A TINY SIZED 530 CONTRACTS from 203,788 UPTO 204,318 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER BUT HAVE NOW MORPHED INTO GOLD..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 263 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 263 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 637 CONTRACTS TO THE 263 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL GAIN OF 793 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 4.5 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 18.355 MILLION OZ FOR MAY

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 2 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A SMALL SIZED 263 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 17,03 POINTS OR 0.58% //Hang Sang CLOSED UP 6.36 POINTS OR 0.02% /The Nikkei closed DOWN 125.58 POINTS OR 0.59%//Australia’s all ordinaires CLOSED UP .74%

/Chinese yuan (ONSHORE) closed DOWN at 6.8884 /Oil UP to 61.64 dollars per barrel for WTI and 71.08 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8884 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9072 TRADE TALKS STILL ON//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

i)NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/Huawei

Huawei responds to the tech ban and in a concession to Trump the company states that it is willing “to engage to ensure the product safety.” It seems that Trump was right that Huawei was using its products for spying purposes.

( zerohedge)

ii)CHINA/CANADA

NOT GOOD!! Two Canadians held by Beijing in December are now facing the death penalty as they are being charged on espionage. No doubt that these are related to the Meng (CFO Huawei) arrest.

( zerohedge)

iii)Serious stuff going on in Washington with their nuclear option against Huawei. Huawei has offered to open up its devices in order for the USA to feel secure form spying. The USA counters by putting Huawei on the “Entity list” which would ban USA corporations from dealing with the company. Also, the timing for China seems odd that on the day that the USA puts Huawei on the “entity list” two Canadians were arrested for espionage and could face the death sentence. I guess travel to China is now out of the question.

(zerohedge)

4/EUROPEAN AFFAIRS

i)FRANCE

An excellent commentary on the state of affairs in France which has the highest social spending per GDP in the world at 31%. The social spending in totally non productive. France incomes are falling below even America’s poorest states. I guess this is the reason for the Yellow Vest Movement as they feel the pain inside France

( Ryan McMaken/ Mises)

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

a)SAUDI ARABIA/IRAN/YEMEN

The Saudis now claim the Iran has carried out the Aramco Pipeline attack in Saudi Arabia using drones. We now have footage and it is extensive.

The USA are not happy campers on this issue. Remember that the USA carrier Lincoln will be entering the Gulf shortly.

(courtesy zerohedge)

6. GLOBAL ISSUES

THE GLOBE

Maersk, the largest shipping company in the world sees a significant slowdown in business activity as the third largest transshipment port in the Mediterranean, located on the island of Malta.

Maersk is now going to shift operations from Malta to other African ports due to the slowdown

( zerohedge)

7. OIL ISSUES

A mystery tanker violates USA sanctions by unloading oil to China

(courtesy zerohedge)

8 EMERGING MARKET ISSUES

VENEZUELA

Officially the uSA suspends all passenger and cargo flights to Venezuela

(courtesy zerohedge)

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

ii)Market data

ii)USA ECONOMIC/GENERAL STORIES

(courtesy Brandon Smith/AltMarket.com)

b)The tariffs are killing USA farmers.

(courtesy Mac Slavo)

c)Too much rain has killed off much the corn planting

SWAMP STORIES

What a riot: there is now a dispute as to whether it was Comey or Brennan who pushed the Steele dossier: i.e. to be included into the intelligence community assessment

( zerohedge)

Let us head over to the comex:

Gold withdrawals;

i) We had 1 withdrawal:

from the Bank of Nova Scotia: 514.400 oz

16 kilobars

.

3 Charts Warning Investors To Rebalance Portfolios

by Frank Holmes via SeekingAlpha.com

Before we get to looking at those three charts, let’s talk about the trade war.

On Friday the Trump administration made good on its threat to raise tariffs on as much as $200 billion worth of Chinese imports to 25 percent from the previous 10 percent. The president also said that a decision could be made soon on whether to impose the same 25 percent rate on an additional $325 billion of Chinese goods, which, all told, would cover approximately the total amount of goods the U.S. imported from China in 2018.

So what does this mean?

Besides being a strain on international relations—a tariff is essentially a tax that must be paid to the U.S. government before a shipment can clear customs. But here’s the kicker: Tariffs are typically paid not by the exporting company but by the importer. In other words, it’s U.S.-based companies that are picking up the tab—then passing the extra expense on to American consumers.

With the exception of the U.S. Treasury, which collects the tariff payments, few stand to benefit here. A February study by Washington, D.C.-based Trade Partnership Worldwide (TPW) estimated that 25 percent tariffs on Chinese goods cost families of four close to $2,300 extra on average per year. They also have the potential to impact upwards of 2.2 million American jobs as well as risk diverting trade to other markets.

“By any measure, the imposition of tariffs by the United States and U.S. imports of steel, aluminum, motor vehicles and parts… is a net loss for the U.S. economy and U.S. workers,” the report reads. Workers “experience greater losses than gains,” and in many cases, according to TPW, “the tariff actions erase all of the anticipated gains from tax reform.”

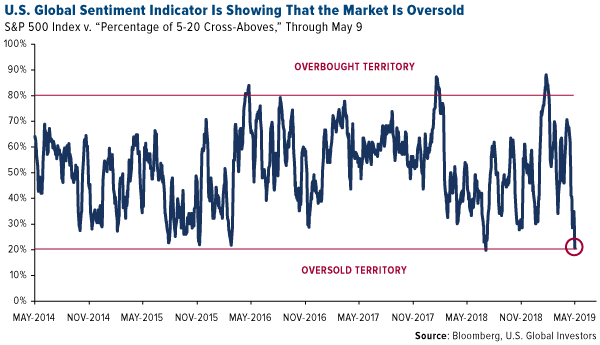

Market Sentiment at Its Lowest in 10 Months

Stocks sold off last week on the tariff news and plunged even further Monday after China announced that it would retaliate.

Equities are now officially in oversold territory. Our own U.S. Global Sentiment Indicator,which tracks as many as 126 commodities, indices, sectors, currencies and international markets, calculates the percentage of positions whose five-day moving averages are above or below their 20-day moving averages. Then we compare the data to the S&P 500 Index. Last week the sentiment indicator fell to 20 percent, showing that the market is at its most oversold since July 2018. Statistically, we should expect to see a bounce.

Stocks may still have further to slide before a resolution to the trade dispute is reached. But for now this could be a good opportunity for investors to pick up some distressed stocks as we await mean reversion. I recommend that investors who seek to get access to the robust U.S. economy but limit their exposure to international trade would do well to look at high-quality small and mid-cap equities. Smaller firms, those with market caps between $1 billion and $10 billion, have the potential to outperform right now because they rely much less on trade than their larger multinational peers. They’re also supported by a stronger U.S. dollar.

I would also recommend considering government and investment-grade municipal bonds, which historically have helped investors improve their risk-adjusted returns in times of economic uncertainty. And of course there’s always exposure to gold and other metals that are expected to be in greater demand in the coming years, copper chief among them.

This leads us to the main event. Below are three charts that I think will convince investors that time is running out to prepare for the next major downturn. All charts and data were brought to my attention by Michael Kantrowitz, head of portfolio strategy at market research firm Cornerstone Macro, who visited our office last week.

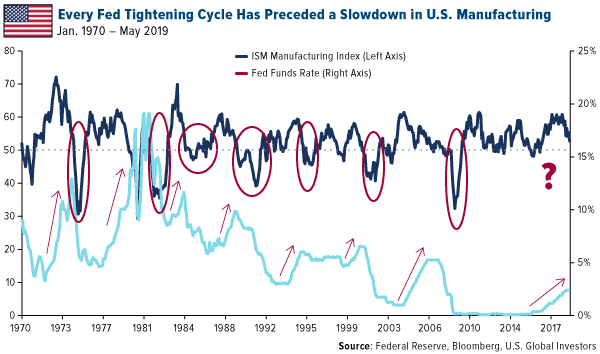

1. Is U.S. Manufacturing Growth Projected to Stall?

The ISM Manufacturing Index for the U.S. fell sharply in April to 52.8, down from 55.3 in March. This means that although the manufacturing sector is still expanding, it’s doing so at a much slower pace. What’s more, the manufacturing index could soon fall below 50.0, indicating a slowdown. For this we’d largely have the Federal Reserve to thank.

That’s according to Michael, who pointed out to us that every Fed tightening cycle going back to the 1950s has preceded a pullback in the ISM Manufacturing Index. And each of these pullbacks coincided with an economic recession and/or market selloff. (One notable exception was 1995, when the market continued to rally despite manufacturing weakness.)

So will this time be different?

I’ll let my friend Bob Moriarty—whose excellent book Basic Investing in Resource StocksI reviewed earlier this month—tackle this one: “The most dangerous words in investing are ‘This time it’s different.’ It’s never different.”

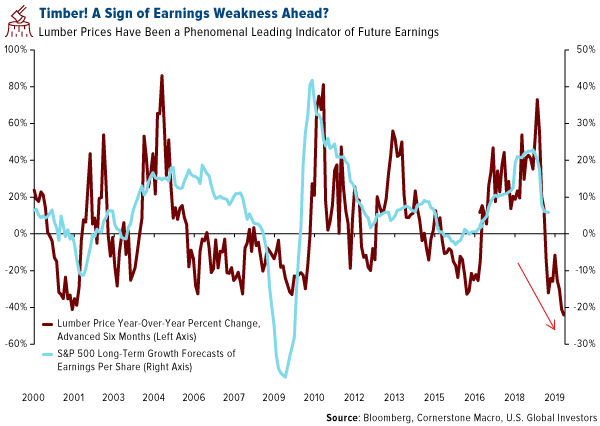

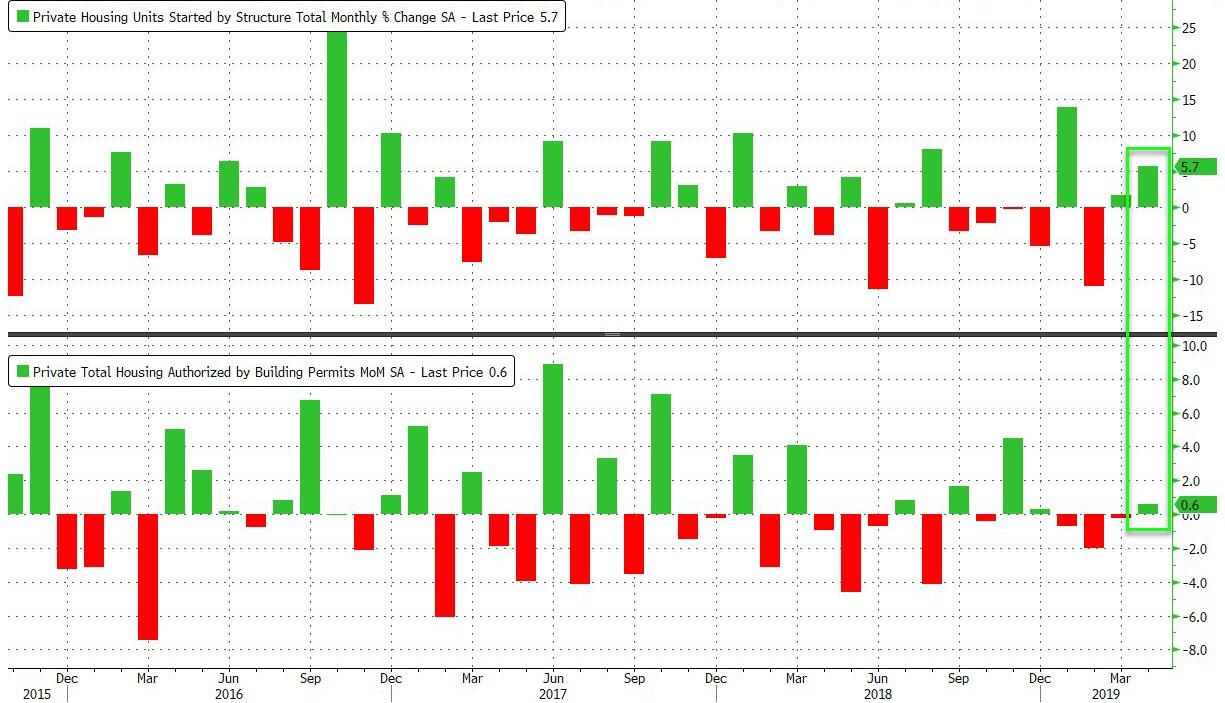

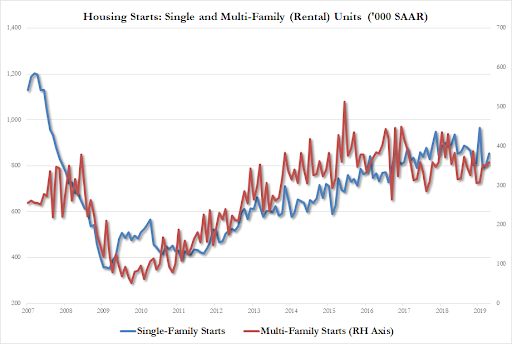

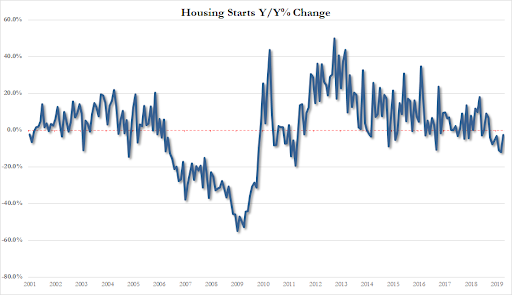

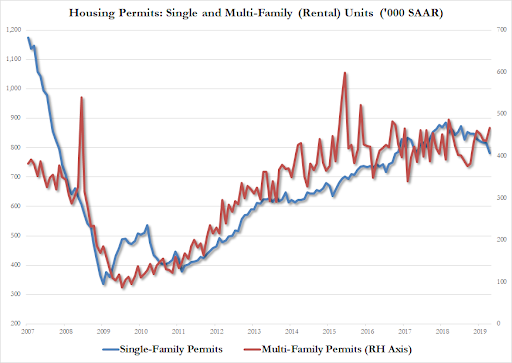

2. Trying to Predict Future Earnings Per Share Growth? Monitor Lumber Prices

One of the most eye-opening charts Michael shared illustrates the close relationship between lumber prices and future earnings per share (EPS) growth. “Believe it or not,” he told us, “lumber prices are among the most reliable leading indicators available.”

I believe it. Housing is a massive part of the U.S. economy, contributing between 15 percent and 18 percent to gross domestic product (GDP), according to the National Association of Home Builders (NAHB). Housing also has an extremely high multiplier effect. Every 100 homes in the U.S. can support up to 70 jobs on average and generate as much as $4.1 million in local income on an ongoing annual basis.

So it stands to reason that lumber prices can give us an incredibly accurate forecast of where the market is headed. In the chart below, lumber prices have been advanced forward six months to illustrate the lag time between changes in price and EPS estimates. When lumber tanked over the 12-month period, EPS followed around six months later. And when lumber soared, EPS estimates shot up.

You may have already detected the warning signal that lumber’s flashing right now. From its high in May of last year, the lumber price has plunged almost 50 percent. That’s the commodity’s sharpest 12-month decline on record. Going forward, then, keep your eyes on earnings, which are a central driver of stock prices.

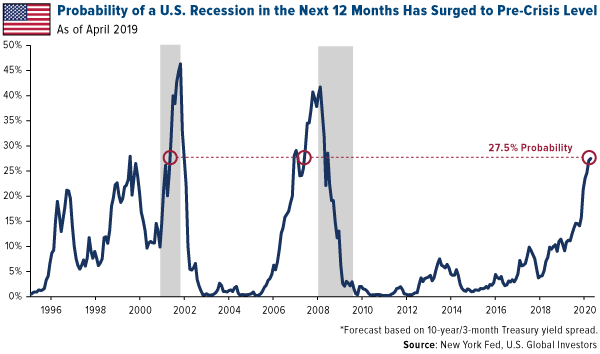

3. New York Fed on Recession Watch

Every month, the New York Fed updates its probability of an economic recession in the next 12 months. Probabilities are calculated using the spread between the 10-year and three-month Treasury yield—which inverted again last week for the first time since March.

According to the Fed’s most recent report, the probability that a recession will make landfall between now and April 2020 rose to 27.49 percent, its highest reading since January 2007 (as it was ascending, not falling), and before that, September 1999.

Past performance does not guarantee future results, of course, but the point I’m trying to make by sharing these charts is that it might be time to consider making some adjustments to your portfolio. That doesn’t mean rotating entirely into safe havens, especially since the market is so oversold right now.

News

Gold Settles With a Modest Gain, Remains Pinned Below

Gold Steadies as Stocks Retreat; Trade Uncertainty Persists

Weak U.s. Retail Sales, Industrial Output Highlight Slowing Economy

U.S., European Shares Strengthen After Trump Auto-Tariff Delay

Us Orders ‘non-emergency Government Employees’ to Leave Iraq

Commentary

3 Charts Warning Investors To Rebalance Portfolios

Global Trade Collapsing To Depression Levels

Calls For 120,000 Troops To Counter Iran

Iran’s Military “On The Cusp Of War” As US Allies Pull Troops From Iraq

Central Banks Are Buying Gold At The Fastest Pace In Six Years

Must Read Guide: Avoid ETF and ‘Platform Gold’ – 7 Real Risks to Your Gold Ownership

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

PART II of Chris Powell’s important interview on gold price suppression

(courtesy Chris Powell/GATA)

If they wise up, gold investors can beat price suppression, GATA secretary says

Submitted by cpowell on Wed, 2019-05-15 20:57. Section: Daily Dispatches

5:03p ET Wednesday, May 15, 2019

Dear Friend of GATA and Gold:

In the second part of his recent interview with GoldCore’s Mark O’Byrne, your secretary/treasurer discusses:

— The counterintuitive movements in the gold price that are caused by surreptitious government interventions.

— The silly explanations for these counterintuitive movements that are contrived by market analysts.

— The ability of gold investors themselves to defeat price suppression by wising up and avoiding “paper gold” and keeping their metal outside the banking system, where derivatives turn it into imaginary supply that is used to smash gold prices down.

— The failure of the governments of developing countries to oppose the market manipulations by which the developed countries exploit them.

— GATA’s primary objectives, which are limited, transparent, and accountable government and fair dealing among nations.

The interview is 32 minutes long and can be viewed at GoldCore here:

https://news.goldcore.com/us/gold-blog/video-we-have-the-power-to-end-go…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

LAWRIE WILLIAMS: Are GLD withdrawals a threat to the gold price?

So far this year a total of 62 tonnes of gold – worth nearly $US2.6 billion at current prices – has been taken out of the world’s largest gold ETF, SPDR gold shares (GLD), despie a couple of months when gold was added into the ETF. Yesterday there was a withdrawal of 3.2 tonnes, but this may have been ultra short term profit taking as there was a deposit of a similar amount a couple of working days prior and the gold price jumped in between!

Gold followers will recall that a continuing outflow of metal from GLD coincided with the big gold price fall in 2012 and 2013, which could worry gold investors should gold continue to bleed out of GLD. However so far the volumes of outflows are not at that kind of level and seem to be more than being balanced by announced increases in central bank gold holdings. With demand apparently picking up in India and perhaps falling off a little in China, although still at substantial levels, the supply/demand balance seems to be holding up. Increased tensions in the Middle East – in particular with the U.S. seemingly taking an increasingly belligerent stance with Iran – and the prospects of an escalating trade war between the U.S. and China, gold could yet be set fair for a substantial boost in the second half of the year should any of these come to a head. And there are other potential flashpoints out there – particularly if President Trump continues with a policy of utilisation of American military strength, and the imposition of sanctions, against regimes to which he is opposed.

This latter policy could even be imposed on supposed staunch allies. For example the U.S. is strongly opposed to the building of a new natural gas pipeline from Russia to Germany – the disputed NordStream 2 project. German Chancellor, Angela Merkel, seems to be heavily in favour and although there is dissension within the EC over the pipeline’s construction, Merkel says the EC can’t and won’t delay the project. But this could lay European companies involved in the pipeline construction open to possible U.S. sanctions, which President Trump seems keen to use as a persuasive tactic on friend and foe alike. Trying to impose U.S. policy on an ally like Germany as to who it can buy its natural gas from is likely to stir up considerable resentment. Multiply this across other jurisdictions over which the U.S. wishes to exert economic pressure and we will see a build-up of resentment against the U.S. Arguably this is already being demonstrated in countries trying to reduce their reliance on the dollar and their turning to gold as a replacement asset in their forex reserves.

The aggressive U.S. policy on Iran is another case in point. The unilateral cessation of the Iran nuclear deal by the U.S. has not found favour amongst the U.S.’s European allies and the slapping of sanctions on any nation continuing to trade with Iran is yet another economic flashpoint. The U.S. dollar has been the world’s principal reserve currency, backed up by virtually all trade in oil being conducted in U.S. dollars. However this is beginning to be eroded and will likely accelerate as time goes on. The law of unintended consequences! All this could be beneficial to gold as a direct, or indirect substitute for the dollar’s role.

So to come back to the question posed in the title, we don’t think so. We suspect withdrawals from GLD, and from other gold ETFs, will diminish and probably reverse as the year progresses. The general consensus is that the gold price is due for a sustained rise in the second half of the year – there seem to be a plethora of geopolitical factors out there which should favour gold and past performance suggests that a rising gold price tends to be accompanied by gold ETF inputs rather than withdrawals. We still think things are aligning positively for gold through the second half of the year – but then gold often confounds. We hope that this time we are correct.

16 May 2019

India’s Gold imports spike 54% to $3.97 billion in April

MUMBAI (Scrap Register): India’s gold imports spiked by 54% to $3.97 billion in April from $2.58 billion in the same month last year, according to latest data release from the Ministry of Commerce.

The rise in imports by the world’s second-biggest consumer of the precious metal was driven by strong demand during wedding season along with fall in prices which prompted purchases.

After recording negative growth for three consecutive months – October, November and December 2018 – gold imports grew 38.16% to $2.31 billion in January 2019. It again contracted by 10.8% to $2.58 billion in February.

In March 2019, gold imports grew by 31.22 % to $3.27 billion.

India is one of the largest gold importers in the world, and the imports mainly take care of demand from the jewellery industry.

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

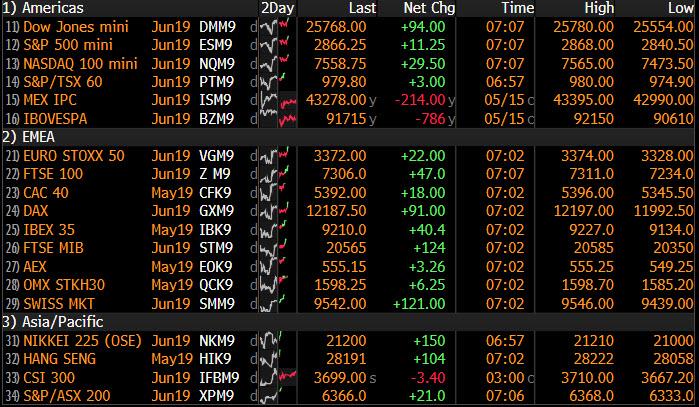

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.8880/

//OFFSHORE YUAN: 6.9072 /shanghai bourse CLOSED UP 17,03 POINTS OR 0.58%

HANG SANG CLOSED UP 6.36 POINTS OR 0.02%

2. Nikkei closed DOWN 125.58 POINTS OR 0.59%

3. Europe stocks OPENED GREEN /

USA dollar index FALLS TO 97.54/Euro RISES TO 1.1208

3b Japan 10 year bond yield: FALLS TO. –.06/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.63/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 62.52 and Brent: 72.27

3f Gold DOWN/JAPANESE Yen DWON CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.10%/Italian 10 yr bond yield DOWN to 2.71% /SPAIN 10 YR BOND YIELD DOWN TO 0.91%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.81: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.48

3k Gold at $1294.00 silver at: 14.79 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 18/100 in roubles/dollar) 64.47

3m oil into the 62 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.63 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0089 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1307 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.10%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.38% early this morning. Thirty year rate at 2.82%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.0056..they are toast

Futures Rebound Despite Trump’s Huawei Ban, Yuan Slides For Record 12th Day

It has been a session of two halves. Early on European and Asian stocks fell, government bond yields slipped and the Japanese yen firmed after the U.S. government hit Chinese telecoms giant Huawei with severe sanctions, further straining Sino-U.S. trade ties, with Beijing warning that the Huawei restrictions won’t be seen as a goodwill gesture and that China will take “all necessary measures” to defend its companies. Amid fresh trade war concerns, the European Stoxx 600 index fell as much as 0.5% in early European trading with the German DAX down 0.4%, while U.S. equity futures were initially down 0.4%.

The broad early weakness in European markets was offset by small gains in Chinese and Hong Kong stock indexes leading to only marginal losses on a global stock index as investors expected – what else – state authorities to step in to support the market and stabilize sentiment.

“Chinese stocks are up as markets expect authorities to intervene to support sentiment but this kind of activity is not sustainable and unless we see a clear resolution in the China-U.S. trade conflict, overall sentiment will remain weak,” said Neil Mellor, an FX strategist at BNY Mellon.

The initial weakness, however, reversed shortly after the European open, when with no fundamental reason, a wave of buying lifted the Emini, and US Treasuries erased a gain while European stocks also reversed a drop as a rally in chemicals and mining companies helped drive up the rebound.

S&P futures, trading at session lows of 2,840 at the European open, have jumped 25 points in a few short hours, with US equity futures now trading at session highs, even as China is expect to announce a response to yesterday’s executive order by Trump which effectively banned Chinese telecom companies from operating in the US.

Officially closing Q1 earnings season, Walmart shares rose in early trading after the company reported its best first quarter in nine years while warning that higher import tariffs can boost consumer prices.

Yet even as equities rebounded, German government bond yields continued to flirt with their lowest level in nearly three years while Dutch bond yields were about to dip into negative territory, a phenomenon not seen since October 2016.

The big overnight event, for anyone who missed it, was announced late on Wednesday when the U.S. Commerce Department said it was adding Huawei Technologies and 70 affiliates to its “Entity List”, effectively banning the company from acquiring components and technology from U.S. firms without government approval. The move took global markets by surprise as sentiment had steadied somewhat in the previous session on news that U.S. President Donald Trump was planning to delay tariffs on auto imports after a swathe of weak U.S. and Chinese economic data.

“Depending on how long this standoff with China lasts, that impacts growth for longer and might force the Fed’s hand,” Natixis strategist Esty Dwek told Bloomberg TV in Singapore. “I wouldn’t expect any big change in the short term, but the possibility of a cut much later in the year has risen.”

In rates, yields on 10-year U.S. Treasury bonds eased as low as 2.35%, near a 15-month low of 2.340% touched on March 28, however, just like stocks, they have since rebounded sharply, and were last seen rising as high as 2.39%. According to Bloomberg, treasuries were under pressure in early New York trading after a $630k/DV01 block trade in 10-year futures; they were mostly underpinned in Asia session and London morning as Europe outperformed, notably France following solid auctions. As a result, yields were cheaper by 0.5bp to 2.5bp across the curve with short end leading the sell-off after 2-year and 5-year yields closed at year-to-date lows on Wednesday; 10-year yields higher by ~1bp at 2.385%, 2s10s and 5s30s flatter by around 1.5bp. Looking at the short-end of the curve, Fed funds rate futures continue to fully price in a rate cut by the end of this year and more than a 50% chance of a move by September.

“The markets are inching step by step in pricing in a rate cut. That is a sea change from a year ago when the consensus was three to four rate hikes a year,” said Akira Takei, bond fund manager at Asset Management One.

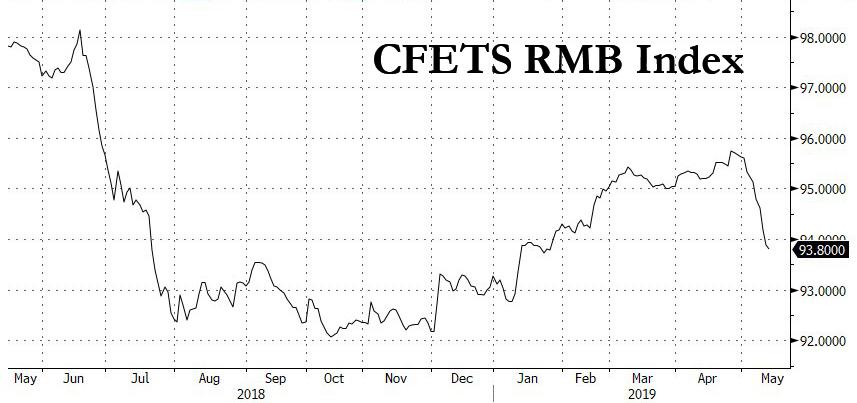

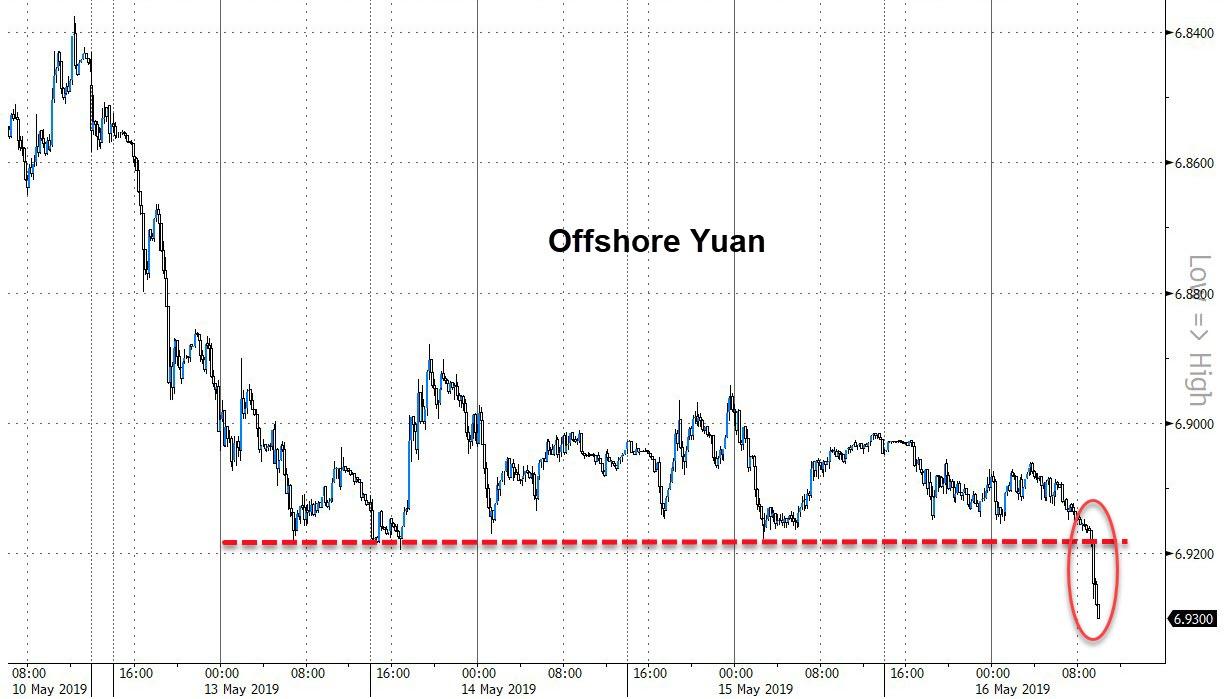

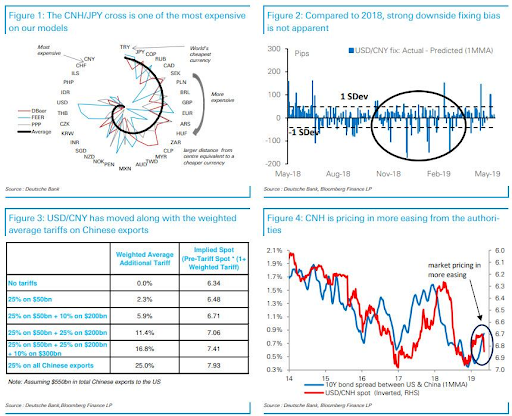

In FX, the notable mover was the Chinese currency because even as mainland stocks rose on expectations of more easing, the yuan extended its slump against its peers to a twelfth session, the longest in data going back to the start of 2015. While China’s currency was steady versus the dollar, the tumble in the Bloomberg CFETS RMB Index Tracker came after the yuan erased its gain for the year amid the China-U.S trade stand-off.

The offshore yuan has retreated about 2.5% this month as one of the world’s worst performers. Despite the yuan’s drop against the basket of 24 trading partners’ currencies, Khoon Goh, head of research at Australia & New Zealand Banking Group Ltd. in Singapore, said the index is still “within the range that is tolerable for the authorities.” He added that there is only a small chance the onshore yuan will weaken past 6.9 per dollar because the government will take steps to support the currency.

Across the Pacific, falling U.S. yields initially eroded support for the greenback with the dollar down 0.1 percent against a basket of its rivals in early trading, however as futures and yields jumped, so did the greenback, and the Bloomberg dollar index was trading near session highs.

Elsewhere, the pound dropped for a ninth day versus the euro – the longest losing streak since 2000 – after news that UK PM May is to be warned that she faces the prospect of confidence vote on June 12th if she does not agree to step down before summer, according to reports in the Telegraph. In related news, UK PM May will tell the executive of the 1922 Committee she needs several more weeks to pass key Brexit legislation in meeting tomorrow, according to FT’s political correspondent Laura Hughes. ITV Political Editor Peston tweeted Labour MP Emily Thornberry said her party will vote against WAB and signalled cross-party talks may collapse as soon as tomorrow, while Conservative MPs Vaizey and Bridgen agree PM May will be out next month.

In commodities, oil prices gained on the prospect of mounting tensions in the Middle East hitting global supplies despite an unexpected build in U.S. crude inventories. Brent crude rose 0.3% to $71.99 a barrel, while U.S. West Texas Intermediate (WTI) crude fetched $62.26, also half a percent higher.

Market Snapshot

- S&P 500 futures up 0.3% to 2,864.50

- STOXX Europe 600 down 0.2% to 377.45

- MXAP down 0.3% to 154.86

- MXAPJ down 0.2% to 508.98

- Nikkei down 0.6% to 21,062.98

- Topix down 0.4% to 1,537.55

- Hang Seng Index up 0.02% to 28,275.07

- Shanghai Composite up 0.6% to 2,955.71

- Sensex up 0.3% to 37,221.67

- Australia S&P/ASX 200 up 0.7% to 6,327.84

- Kospi down 1.2% to 2,067.69

- German 10Y yield fell 1.7 bps to -0.115%

- Euro up 0.1% to $1.1215

- Brent Futures up 0.8% to $72.33/bbl

- Italian 10Y yield rose 1.8 bps to 2.373%

- Spanish 10Y yield fell 4.5 bps to 0.91%

- Brent Futures up 0.8% to $72.33/bbl

- Gold spot up 0.03% to $1,296.91

- U.S. Dollar Index down 0.07% to 97.50

Top Overnight News from Bloomberg

- Theresa May flies back to London on Thursday morning to once again face colleagues seeking to oust her, as she struggles to find a way to pass her Brexit deal. The executive of the 1922 Committee, representing Tory members of Parliament, will use a meeting at the premier’s office at 11:30 a.m. Thursday to urge her to quit as soon as possible, according to two of its members, speaking on condition of anonymity

- Donald Trump signed an order Wednesday that’s expected to restrict Huawei and fellow Chinese telecommunications company ZTE Corp. from selling their equipment in the U.S. The Department of Commerce said it had put Huawei on a blacklist that could forbid it from doing business with American companies. This campaign could disrupt 5G rollouts globally

- China cut its U.S. Treasuries holdings to the lowest level since 2017 in March amid the trade dispute between the world’s two biggest economies

- The U.S. ordered its non-emergency government staff to leave Iraq amid increasing Middle East tensions that American officials are blaming on Iran, as fears rise that the region may be heading toward another conflict

- Trump will also give the EU and Japan 180 days to agree to a deal that would “limit or restrict” imports into the U.S. of automobiles and their parts in return for delaying new auto tariffs, according to a draft executive order seen by Bloomberg

- Global funds are taking cover in defensive trades amid a widening U.S.-China rift, with yuan sovereign bonds emerging as the top pick in developing Asia

Asian equity markets were mixed as blue-chip earnings and the US blacklisting of Huawei as well as 70 of its affiliates overshadowed the positive lead from Wall St, where sentiment was underpinned by reports that President Trump plans to delay the decision on tariffs for auto imports by up to 6-months. ASX 200 (+0.7%) and Nikkei 225 (-0.6%) were mixed in which the commodity-related sectors led the intraday recovery in Australia and as a higher Unemployment Rate stoked calls for an RBA rate cut, while Tokyo trade was pressured by disappointing earnings including Japan’s megabanks Mitsubishi UFJ Financial Group and Sumitomo Mitsui Financial Group. Hang Seng (U/C) and Shanghai Comp. (+0.6%) were initially subdued with underperformance seen in tech and telecoms following US President Trump’s national emergency declaration on foreign companies posing threats to US telecommunications, although strength in property names after firmer Chinese House Price data helped reverse the losses. 10yr JGBs were initially supported as they tracked recent upside in T-notes and amid weakness in Tokyo stocks, although gains were capped after the 5-year JGB auction results were relatively inline with the previous albeit with a weaker b/c.

Top Asian News

- Philippines Cuts Large Banks’ Reserve Ratio by 2Ppt to 16%

- Moody’s Changes Outlook on Japan Banking System to Negative

- China Says It Will Take Necessary Measures to Defend Its Firms

- MUFG Shifts Asia Rates Trading to London From Hong Kong

European equities have been volatile [Eurostoxx 50 +0.3%] following on from a mostly positive lead in Asia. Sectors are mixed with outperformance in material names (amidst rising base metal prices) whilst consumer discretionary lags as EU auto names pare back some of yesterday’s tariff-spurred gains. In terms of individual movers, Thyssenkrupp (+6.5%) shares rose to the top of the DAX after reports that Finland’s Kone (+3.8%) are exploring the viability of a bid for Thyssenkrupp’s EUR 14bln elevator division. Meanwhile, Thomas Cook (-18.4%) shares opened lower by over 20% after posting a Q1 pre-tax loss of EUR 1.465bln which came alongside a warning that “challenging” trading over the peak summer season would impact FY earnings, although the Co. did note that they have received multiple bids for all and parts of the group airline. Finally, Ubisoft (-12.4%) rests at the foot of the Stoxx 600 despite posting record sales figures, after a delay to its open-world game “Skull & Bones” into the next FY.

Top European News

- Car Stocks Retreat as Trump Seen Seeking Industry Import Curbs

- Burberry Falls as China Weakness Hangs Over Tisci’s New Looks

- ECB’s Weidmann Says Rate Tiering Could Be Net Negative For Banks

- Italian Banks Expectations Remain Demanding, Goldman Sachs Says

In FX, the Dollar is holding above Wednesday’s post-US data lows, but stands narrowly mixed vs G10 counterparts as the US-China trade dispute continues via recriminations over the cause of the derailment in talks that has sparked another round of reciprocal tariffs. However, the DXY is stuck in a narrow band either side of the 97.500 mark that has been pivotal for a while, and very close to the 30 DMA (94.428) between 97.565-438.

- NZD/EUR/CAD/JPY/AUD/CHF – All marginally firmer vs the Greenback, with the Kiwi outperforming or clawing back more losses than other so be precise from sub-0.6550 levels to circa 0.6580. Meanwhile, the single currency is holding above 1.1200 after reclaiming big figure+ status yesterday on the EU auto tax reprieve, but unable to breach the 30 DMA (1.1222) convincingly amidst increasingly dovish ECB market expectations and another potential clash between Italy and the EU on budget policy intentions. The Loonie has also rebounded from recent lows and a post-Canadian CPI dip to test resistance ahead of 1.3400 with some positive momentum coming from reports that the Canada, Mexico and the US are close to clinching a deal on steel tariffs (Peso paring losses as well as Usd/Mxn eyes 19.0000). Usd/Jpy continues to straddle 109.50 as the Yen retains a safe-haven bid, but also contends with more decent option expiry interest (1.55 bn from 109.15 to 109.25 and 2.2 bn between 109.40-55). Elsewhere, the Aussie has recovered from its latest slump in wake of more weak data on balance (labour report) and a dip through 0.6900 stops with the aid of underlying bids/short covering, and Aud/Usd has now absorbed supply said to be sitting around 0.6910 and above to trade back up around 0.6933. Lastly, funding for a proposed acquisition has been touted as a factor behind recent Franc strength, but Usd/Chf has bounced towards 1.0100 from a few pips above 1.0050 and Eur/Chf has crossed over 1.1300 again.

- GBP – Brexit and related UK political uncertainty is still haunting Sterling along with other global and geopolitical risk, with Cable retreating a tad further towards 1.2800 and Eur/Gbp inching close to 0.8750 as PM May meets the 1922 group in just under an hour.

- EM – The Rand is showing a degree of resilience in the face of somewhat negative reviews from Moody’s on SA’s credit outlook with Usd/Zar hovering at the lower end of 14.2650-1525 trading parameters and perhaps being drawn or attracted to an unusually large expiry at the 14.0000 strike (1.365 bn).

In commodities, a positive session thus far for WTI (+0.7%) and Brent (+0.5%) futures as tensions in the Middle East drift back into focus. The former remains above USD 62.00/bbl and in close proximity to USD 62.50/bbl whilst its Brent counterpart floats comfortably above the USD 72.00/bbl mark. On the Iranian front, ship tracking data showed that a tanker carrying Iranian oil (in violation with US sanctions) has unloaded its cargo of almost 130k tonnes of oil near Zhousan, in China. Iran will remain a focus as the JMMC convene this weekend in Jeddah, with ministers expected to discuss whether the supply gap from Iranian sanctions will need to be filled, and hence whether the output curb deal will need to be extended until the end of the year. In terms of technicals, analysts at PVM highlight resistance at 63.09 (21 DMA) in WTI and 72.60 in Brent (short-term DMA) which they believe will be tested today given the optimism emanating from Trump’s decision to delay EU auto tariffs, progress regarding the Canadian and Mexican aluminium and steel tariffs and concerns of supply disruptions from Middle Eastern tensions. Looking at metals, gold remains choppy below the 1300/oz level and flirts with its 100 DMA at 1296.82 ahead of its 50 DMA (1291.69). Elsewhere, copper prices are poised to notch a third day of gains amid a weakening buck and optimism surrounding Trump’s auto tariff delays with the red metal now back above 2.75/lb ahead of its 200 DMA at 2.7604.

US Event Calendar

- 8:30am: Housing Starts, est. 1.21m, prior 1.14m; Housing Starts MoM, est. 6.15%, prior -0.3%

- 8:30am: Building Permits, est. 1.29m, prior 1.27m; Building Permits MoM, est. 0.08%, prior -1.7%

- 8:30am: Philadelphia Fed Business Outlook, est. 9, prior 8.5

- 8:30am: Initial Jobless Claims, est. 220,000, prior 228,000; Continuing Claims, est. 1.67m, prior 1.68m

- 9:45am: Bloomberg Consumer Comfort, prior 59.8

DB’s Jim Reid concludes the overnight wrap

By the time you read this I’ll be flying back from the US West Coast and hopefully blissfully asleep. At the conference I was attending there was a panel on US politics with a couple of Washington insiders and a couple of things struck me from the conversation. Firstly, virtually every market person I’ve spoken to over the last few months wants a deal, pretty much any deal. However, in listening to the panel it’s quite clear that China has few friends on the trade front in Washington across the political spectrum. Also, the view was that behind closed doors virtually all US corporates were supportive of being more aggressive with China on Trade. They may not say so publicly but the impression given was that in private they believed the current trading relationship made life tougher for them. So, working in markets it’s easy to focus on the price action negatives and assume a rational compromise at some point. However, there is a bigger story than this. What makes this challenging though is that Mr Trump did everything to suggest he wanted a deal early this year and it looked like he was clearing the way for one regardless of the above support for more action. So second guessing the President’s next move is the hard part but don’t underestimate the support for a more aggressive stance politically and at a corporate level.

As discussed above though, markets have a very different view and given how fragile sentiment has become over the last 10 days, the last thing they needed was a string of soft data across China and the US. That was certainly the case until headlines hit in the mid-afternoon indicating that President Trump plans to delay the auto tariffs decision by up to six months.Even if that decision was broadly expected, there was always the chance that the President went ahead with them this week. More on the data later but the news about Trump’s auto tariffs delay ended up more than offsetting the weak China and US data with the NASDAQ (+1.13%) leading gains.The S&P 500 closed up a more modest +0.58% however was up +1.28% from the early lows while the DOW finished +0.45%. The STOXX 600 (+0.46%) also finished onside having spent the majority of the session in the red along with the DAX (+0.90%). Vol also abated with the VIX down -1.6pts to -16.4 and the V2X slipping -0.8pts to 16.7. It’s worth flagging that the European Autos sector rose +1.97% yesterday and +4.14% from the lows, while the S&P 500 Autos sector gained +1.00% and +2.70% off the lows.

Bond markets also witnessed a part reversal, however yields were still broadly lower across the board which goes to show that fixed income markets are still biased towards risk-off more generally.Indeed there was a multi-year low for Bunds which touched -0.134% intraday and closed at -0.100% (-2.8bps) for the lowest closing level since September 2016. That’s just 9bps off their all-time low from their summer 2016 post-Brexit levels. OATs rallied -2.3bps and Gilts -3.7bps while Treasuries were down another 3.7bps to 2.374% and the lowest since March despite yields rising after the auto tariff news.This morning they are hovering around similar levels. At the short end, 2y yields fell to 2.161% and to the lowest since February 2018. The 3m10y curve flattened back into negative territory at -2.9bps while there are now 31bps of cuts priced into the January 2020 Fed Funds futures contract. The one bond market that failed to join the party was BTPs which rose +1.8bps with the spread to Bunds hitting 292bps intra-day, which would have been the highest level of the year, before retracing slightly.The move for Bunds appeared to reflect a combination of the wider risk-off move and further reaction to Salvini’s early week comments about letting Italy’s deficit rise above EU limits, which he reiterated yesterday.

In other markets, US HY credit widened 6bps yesterday – and therefore bucking the equity move – while in currencies EM FX was +0.07% stronger. Unexpected comments from Mnuchin about US, Mexico, and Canada being closer to a deal to remove metal tariffs helped the Mexican Peso and Canadian Dollar rally +0.54% and +0.18% respectively. USTR Lighthizer met with the Democratic House leadership team to discuss passing the NAFTA-replacement deal, the USMCA, and Speaker Pelosi’s aide said the meeting was “productive” and that the Democrats want to “get to ‘yes.’” Meanwhile, WTI oil prices rose +2.12% from their lows (+0.39% on the day) after US data showed a +5.43mn barrel crude inventory build, which was not as big as feared.

After US markets closed, President Trump signed an executive order to declare a national emergency regarding “threats against information and communication” systems. While it did not mention China, Huawei or ZTE (which is down 5% overnight) by name, the move is likely a step on the path toward fully banning the Chinese tech firm from doing business in the US. Our economists in China wrote this morning that they believe this could be highly damaging, as it could trigger more voices in China’s policy circle against US business interests in China. See their note here .

Markets in Asia are a bit more mixed on the back of that news with declines for the Nikkei (-0.60%) and Kospi (-0.87%), and small gains for the Hang Seng (+0.24%) and Shanghai Comp (+0.20%) – the latter reversing earlier losses. The CNH is -0.10% weaker, trading at 6.911 – a level it has broadly hovered near for the last three days but failed to breach higher. Meanwhile US equity futures are down around -0.35%. A data point worth flagging this morning also is China’s holdings of Treasuries which hit the lowest level since 2017 in March following data released last night. It was also the first drop since November. The more significant data will be this month’s however which we will still have to wait a while for.

Back to that data in the US where first up was the April retail sales report where both the core (-0.2% mom vs. +0.3% expected) and control group (0.0% mom vs. +0.3% expected) prints both fell short.There were some modest upward revisions to the previous month but not enough to shrug off the overall disappointment. Adding to the pain was the April industrial production print released shortly after which unexpectedly fell -0.5% mom (vs. 0.0% expected), albeit somewhat offset by a three-tenths upward revision to March. It’s worth noting that manufacturing production also fell -0.5% mom (vs. 0.0% expected) and capacity utilization slipped from 78.5% to 77.9% – the lowest since February last year. The Atlanta Fed GDP tracker nudged down -0.5pp to 1.1% following the above data.

The better news came in the latest manufacturing sector survey data where the May empire manufacturing print rose +7.7pts to 17.8,far exceeding expectations for a drop to 8.0. In fact, it was the highest reading since November 2018. However, with the bulk of the responses coming prior to the rise in trade tensions it’s next month’s reading which will garner more attention.

Prior to this we had the preliminary Q1 GDP reading in Germany which matched expectations at +0.4% qoq. However, our economists in Germany now expect Q2 to be flat due to a negative payback for Q1 while the rise in trade tensions will also result in subdued growth for Q3. So the outlook appears less positive. For completeness, there was no change in the second revision for Q1 GDP for the Euro Area at +0.4% qoq while France’s April CPI was revised up one-tenth to +0.4% mom.

To the day ahead now, which this morning includes Q1 employment data in France, final April CPI revisions in Italy and the March trade balance for the Euro Area. In the US we’ll see April housing starts and building permits, the May Philly Fed PMI and the latest weekly initial jobless claims reading. Away from that the ECB’s Praet, Guindos and Coeure are all speaking at various stages today along with the Bundesbank’s Weidmann. The BoE’s Haskel also speaks this evening. Over at the Fed we’ll hear from Kashkari at 5.05pm BST when he is due to discuss monetary policy and the economy and then Brainard at 5.15pm BST who will be talking about a similar topic.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 17,03 POINTS OR 0.58% //Hang Sang CLOSED UP 6.36 POINTS OR 0.02% /The Nikkei closed DOWN 125.58 POINTS OR 0.59%//Australia’s all ordinaires CLOSED UP .74%

/Chinese yuan (ONSHORE) closed DOWN at 6.8884 /Oil UP to 61.64 dollars per barrel for WTI and 71.08 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8884 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9072 TRADE TALKS STILL ON//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

i)China/HUAWEI

Huawei responds to the tech ban and in a concession to Trump the company states that it is willing “to engage to ensure the product safety.” It seems that Trump was right that Huawei was using its products for spying purposes.

(courtesy zerohedge)

Huawei Responds To Tech Ban: In Concession To Trump Says “Willing To Engage To Ensure Product Safety”

It appears that Trump’s aggressive trade war escalation is proving the doubters wrong and already bearing fruit.

Earlier on Wednesday, President Trump signed an executive order declaring a “national emergency” in permitting the US federal government to legally block American companies from purchasing foreign-made telecom equipment deemed a national security risk. The move is expected to restrict Huawei and fellow Chinese telecommunications company ZTE from selling their equipment in the U.S. Shortly afterward, the Department of Commerce said it had put Huawei on a blacklist that could forbid it from doing business with American companies.

In the executive order, while Trump did not name any company specifically, it was the latest action in the ongoing security saga with Huawei. The order reads that “openness must be balanced by the need to protect our country against critical national security threats.”

Separately, the Commerce Department’s move to put Huawei on its “Entity List” means U.S. companies will need a special license to sell products to the Chinese company. A similar move against ZTE last year nearly forced the company to shut down before Trump intervened and a deal was reached.

As a result of allegations it works covertly with the Chinese government to facilitate industrial and other espionage, Huawei has been banned from building the 5G networks in the US, in Australia, and numerous other countries – if not in Europe, where the local liberal elite would rather be spied on by Beijing than appear to fold to the demands of the White House – after concerns were raised that the company’s products may be used by the Chinese government for surveillance.

And just a few hours after Trump signed the executive order, the Chinese telco released a statement in response to the US ban, in which while it warned that the country will lag behind in 5G networks made by “inferior” or “more expensive alternatives.”

Yet while Huawei leaders have long insisted their company operates independently of the Chinese government and that its products aren’t used for spying, it appeared to confirm just that when the company said that it is “ready and willing to engage with the U.S. government and come up with effective measures to ensure product security.”

Why Huawei needs to ensure product safety if, as it claims, its products are safe is certainly worth a scratch on the head, and if anything it validates Trump’s suspicions about Huawei’s less then noble motives, which resulted in the US leveling 23 charges against Huawei and its CFO, and daughter of the CEO, Meng Wanzhou including charges of violating trade sanctions with Iran and attempted theft of trade secrets. Huawei has, of course, maintained that it is all a “political” game with no credence.

Huawei’s full statement is below.

“Huawei is the unparalleled leader in 5G. We are ready and willing to engage with the US government and come up with effective measures to ensure product security. Restricting Huawei from doing business in the US will not make the US more secure or stronger; instead, this will only serve to limit the US to inferior yet more expensive alternatives, leaving the US lagging behind in 5G deployment, and eventually harming the interests of US companies and consumers. In addition, unreasonable restrictions will infringe upon Huawei’s rights and raise other serious legal issues.”

Trump’s order is clearly meant to ratchet up pressure on Beijing to concede in the trade war; and just to make sure Xi Jinping has a few days to contemplate the latest US retaliation, the Commerce Department’s blacklisting of Huawei isn’t effective until it’s listed in the Federal Register. The department didn’t say when that would occur. The administration official said Wednesday that the Commerce Department was expected to take as long as six months to fashion an approach to the order, so there might not be an immediate effect. The government may eventually prohibit products from specific companies or countries as Commerce carries out Trump’s order.

Last week, the U.S. Federal Communications Commission barred China Mobile Ltd. from the U.S. market over national security concerns and said it was opening a review of other Chinese companies.

Finally, in addition to getting Tom Friedman and Steve Bannon to agree on something, Trump’s hard line stance against China appears to be earning him some very unexpected friends: democrats. “This is a needed step, and reflects the reality that Huawei and ZTE represent a threat to the security of U.S. and allied communications networks,” said Democratic Senator Mark Warner of Virginia, the vice chairman of the Senate Intelligence Committee.

END

CHINA/CANADA

NOT GOOD!! Two Canadians held by Beijing in December are now facing the death penalty as they are being charged on espionage. No doubt that these are related to the Meng (CFO Huawei) arrest.

(courtesy zerohedge)

2 Detained Canadians Face Death Penalty As China Brings Espionage Charges

Just hours after President Trump signed an executive order blacklisting Huawei and 70 affiliates from doing business in the US, Chinese authorities announced that a Canadian businessman and a former Canadian diplomat have been formally charged with spying – a crime that could carry a death sentence in China.

Michael Spavor, a businessman who organized trips to North Korea for foreigners, and Michael Kovrig, a consultant and former diplomat, were detained in December and held as Chinese police carried out an investigation into charges relating to “state secrets”. Five months later, the two men have finally been formally charged, according to CBC.

Michael Spavor, Michael Kovrig

Many suspect that the arrests of the two men was retaliation against Ottawa For the arrest of Huawei CFO Meng Wanzhou, who was arrested in Vancouver late last year at the behest of federal prosecutors in New York, who are seeking to extradite her over allegations that she misled banks about Huawei’s relationship with a sanctions-violating subsidiary. Canadian diplomats have said there’s ‘no doubt’ the detentions of the two men were retaliation for Meng, who was released on $10 million bail in December and must wear an ankle monitoring bracelet.

The decision – which comes amid an unprecedented US crackdown on Huawei and the most tense period of negotiations since the trade-war truce was declared in December – will almost certainly escalate tensions between the US, Ottawa and Canada.

Chinese officials said they hoped Canada would refrain from criticizing their legal system.

“According to Chinese prosecutors’ approval, Michael Kovrig, due to being suspected of crimes of gathering state secrets and intelligence for foreign (forces), and Michael Spavor, for being suspected of crimes of stealing and illegally providing state secrets for foreign (forces), have in recent days been approved for arrest according to law,” foreign ministry spokesperson Lu Kang told a daily news briefing.

“We always act in accordance with the law, and we hope that Canada will not make irresponsible remarks on China’s legal construction and judicial handling,” Geng said at a regularly scheduled news conference.

The two men have been held in undisclosed detention facilities for months and have been denied access to lawyers, though they have been allowed visits from Canadian consular officials.

END