GOLD: $1276.25 DOWN $9.70 (COMEX TO COMEX CLOSING)

Silver: $14.41 DOWN 13 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1277.70

silver: $14.42

OPTIONS EXPIRY FOR THE STOCK MARKET AND GLD/SLV WAS TODAY

COMEX EXPIRY FOR GOLD/SILVER: TUES MAY 28/2019

LBMA/OTC EXPIRY: MAY 31.2019

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 2/2

EXCHANGE: COMEX

CONTRACT: MAY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,285.000000000 USD

INTENT DATE: 05/16/2019 DELIVERY DATE: 05/20/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 2

737 C ADVANTAGE 2

____________________________________________________________________________________________

TOTAL: 2 2

MONTH TO DATE: 290

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 2 NOTICE(S) FOR 200 OZ (0.0062 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 290 NOTICES FOR 28000 OZ (.9020 TONNES)

SILVER

FOR MAY

15 NOTICE(S) FILED TODAY FOR 75,000 OZ/

total number of notices filed so far this month: 3392 for 16,960,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$7255 DOWN $632

Bitcoin: FINAL EVENING TRADE: $7104 DOWN $766

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A MONSTROUS SIZED 5190 CONTRACTS FROM 204,318 UP TO 209,508 DESPITE YESTERDAY’S 26 CENT LOSS IN SILVER PRICING AT THE COMEX. LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER BUT IT NOW IN FULL FORCE FOR GOLD. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 1368 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1368 CONTRACTS. WITH THE TRANSFER OF 1368 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1368 EFP CONTRACTS TRANSLATES INTO 6.84 MILLION OZ ACCOMPANYING:

1.THE 26 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 18.650 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

14,934 CONTRACTS (FOR 13 TRADING DAYS TOTAL 14,934 CONTRACTS) OR 74,67 MILLION OZ: (AVERAGE PER DAY: 1148 CONTRACTS OR 5.743 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 74.67 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 10.66% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 815,77 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5190 DESPITE THE LARGE 26 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1368 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE GAINED A GIGANTIC SIZED: 6558 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1368 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 5190 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 26 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $14.55 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.022 BILLION OZ TO BE EXACT or 145% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 15 NOTICE(S) FOR 75,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 18.650 MILLION OZ ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 3112 CONTRACTS, TO 521,243 DESPITE THE CONSIDERABLE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $11.10//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 14,239 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 14,239 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 521,243. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,127 CONTRACTS: 3112 OI CONTRACTS DECREASED AT THE COMEX AND 14,239 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 11,127 CONTRACTS OR 1,112,700 OZ OR 34.60 TONNES. YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $11.10.…AND WITH LARGE LOSS, WE HAD A HUGE GAIN OF 34.60 TONNES!!!!!!.??????

WITH RESPECT TO SPREADING: WE MAY HAVE HAD SOME ACTIVITY WITH TODAY’S FALL IN PRICE

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS HAVE NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 85,098 CONTRACTS OR 8,509,800 OR 264.69 TONNES (13 TRADING DAYS AND THUS AVERAGING: 6546 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAYS IN TONNES: 264.69 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 264.69/3550 x 100% TONNES =7.43% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2080.23 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 3112 DESPITE THE LARGE FALL IN PRICING ($11.10) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A MONSTROUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 14,239 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 14,239 EFP CONTRACTS ISSUED, WE HAD A STRONG SIZED GAIN OF 11,127 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

14,239 CONTRACTS MOVE TO LONDON AND 3112 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 34.60 TONNES). ..AND THIS HUMONGOUS DEMAND OCCURRED DESPITE THE FALL IN PRICE OF $11.10 IN YESTERDAY’S TRADING AT THE COMEX.WE MAY HAVE HAD A STRONG PRESENCE OF SPREADING TODAY IN THE RAID ORCHESTRATED BY THE CROOKS.

we had: 2 notice(s) filed upon for 200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $9.70 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD/

INVENTORY RESTS AT 733.23 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORy

SLV/

WITH SILVER DOWN 13 CENTS TODAY:

A HUGE 3.186 MILLION OZ WITHDRAWAL OF PAPER SILVER FORM THE SLV.

THIS PAPER SILVER WAS USED IN THE ATTACK TODAY.

/INVENTORY RESTS AT 312.366 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUMONGOUS SIZED 5284 CONTRACTS from 204,318 UPTO 209,602 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER BUT HAVE NOW MORPHED INTO GOLD..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 1368 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1368 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 5190 CONTRACTS TO THE 1368 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 6558 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 32.79 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 18.650 MILLION OZ FOR MAY

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 26 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1368 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 73.42 POINTS OR 2.48% //Hang Sang CLOSED DOWN 328.61 POINTS OR 1.16% /The Nikkei closed UP 187.11 POINTS OR 0.89%//Australia’s all ordinaires CLOSED UP .69%

/Chinese yuan (ONSHORE) closed DOWN at 6.9145 /Oil UP to 61.64 dollars per barrel for WTI and 71.08 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9145 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9468 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

i)NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

Trade optimism fizzles as China states it has no more plans for talks. Obviously they are quite concerned with the Huawei situation

(courtesy zerohedge)

ii)Huawei bonds tumble the most on record after the new prohibition of sales of components from uSA sources to it

iii)Very problematic as Beijing faces China and Russia who have their back as they both firmly oppose unilateral USA sanctions

iv)An excellent commentary from James Rickards as he discusses the problems China faces with the trade war

( James Rickards)

4/EUROPEAN AFFAIRS

i)UK

Corbyn is a fool: the opposition leader wants to nationalize the UK national energy grid. They just handed the election to Farage as both the conservatives and labour disintegrate

( Mish Shedlock/Mishtalk)

ii)UK

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

a)TURKEY

Early last night, the Turkish lira tumbles to 6.0840 after Trump terminates its preferential trade agreement with Turkey stating that Turkey is no longer in need of help as a developing nation and thus all goods will have the normal tariffs assigned to those goods. However as a kind gesture, he has initiated a 25% tariff on Turkish steel instead of the 50% that everybody else pays.

( zerohedge)

b)IRAN

There is fear that Iranian operatives have moved missiles in Iraq and are planning to attack USA interests there. We do not know how many missiles have been mobilized

( zerohedge)

6. GLOBAL ISSUES

Canada/Mexico/USA

Canada and Mexico reach a deal with the USA as they both lift tariffs against each other

(courtesy zerohedge

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA

9. PHYSICAL MARKETS

i)My goodness, I guess that there is inflation

(Bloomberg/GATA)

ii)For the first time Kitco is allowed to mention gold manipulation. The interview is with Max Keiser and the interviewer is Daniela Cambone

( Kitco/GATA)

iii)Another Cdn miner going into the dust bin: Iamgold explores its sale amid gold sector consolidation

(Bloomberg/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

Late trading today.

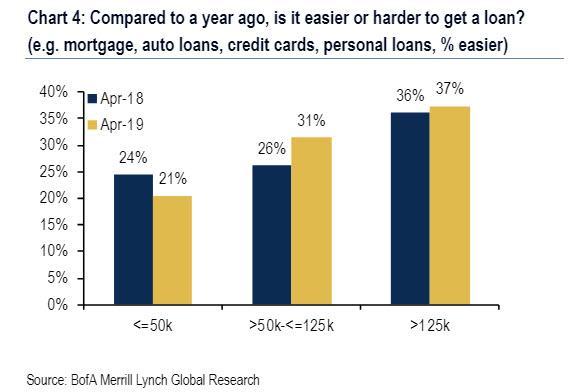

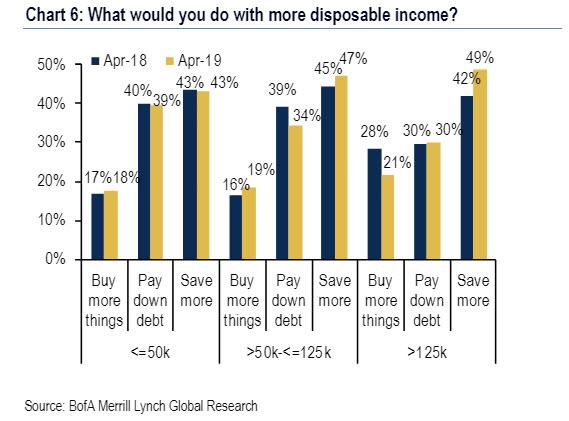

ii)Market data

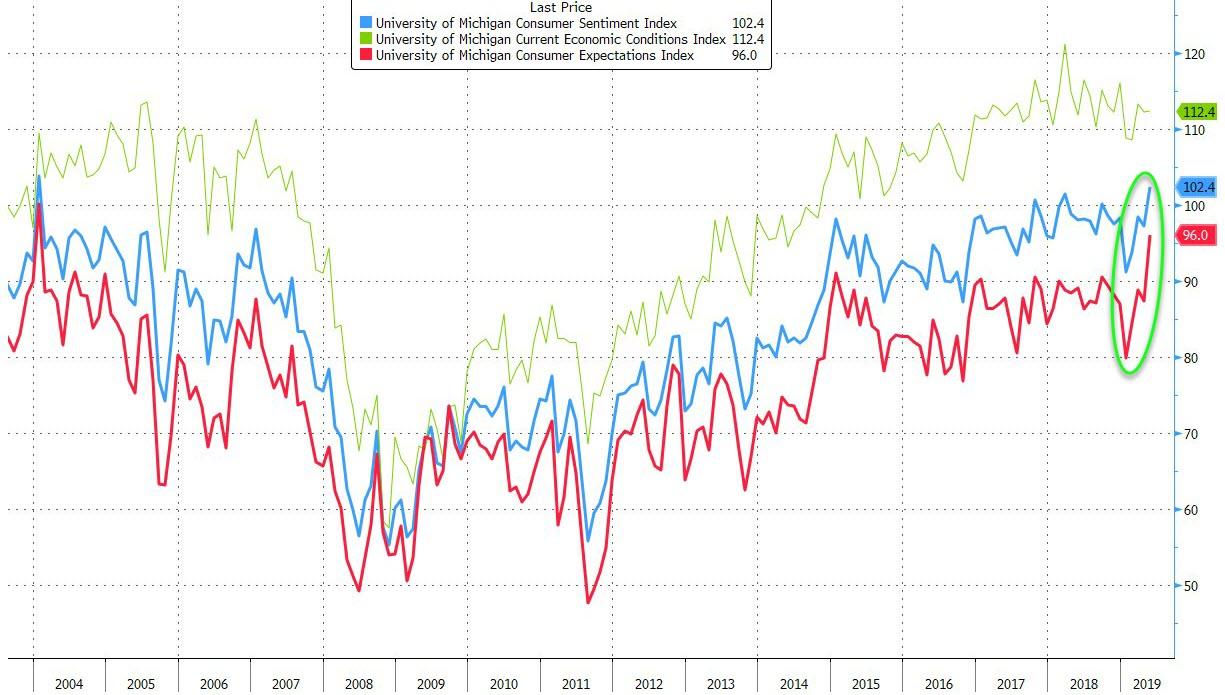

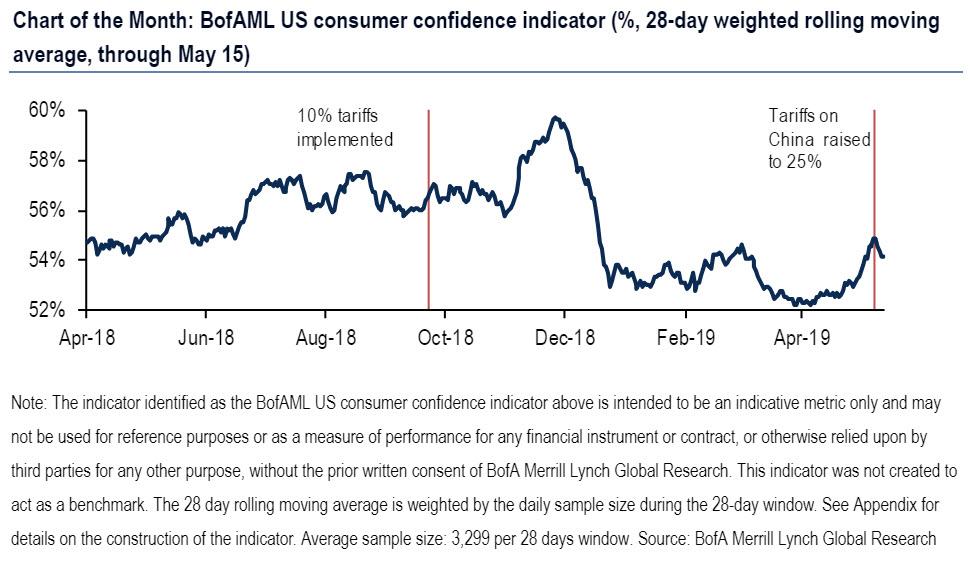

The generally more accurate gauge of consumer confidence is the Bank of America survey as compared to the U. of Michigan report. Yesterday the U. of Michigan was bullish on confidence. Today’s B of America report was bearish.

(courtesy zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

b)auto loan delinquencies are now spiking levels not seen since 3rd quarter of 2009

(courtesy WolfRichter)

SWAMP STORIES

a)Barr’s first interview with Bill Hammer: Government power was used to spy on American citizens states Barr.

(courtesy Fox news/Bill Hammer/Bill Barr)

b)This is good: Nellie Ohr deleted emails on Bruce Ohr’s computer while she was doing her research digging up dirt on Trump. So we have a non government employee destroy evidence on a government employee’s computer.. Sounds like obstruction of justice to me

( zerohedge)

c)Maxine Waters is one nutjob: here she calls Trump’s very immigration plan racist because it is not important for new immigrants to learn English and have a job

Let us head over to the comex:

Gold withdrawals;

i) We had 0 withdrawal:

.

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

My goodness, I guess that there is inflation

(Bloomberg/GATA)

Koons’ silver Rabbit sets living artist record

Submitted by cpowell on Thu, 2019-05-16 13:39. Section: Daily Dispatches

Thank God there’s no inflation.

* * *

By Katya Kazakina and Allison McCartney

Bloomberg News

Thursday, May 16, 2019

It was another heady auction night in New York.

Minutes after Robert Rauschenberg’s painting Buffalo II fetched $88.8 million at Christie’s — almost five times the late artist’s previous auction record — Jeff Koons’s sculpture of an inflatable silver bunny topped that at $91.1 million, the most ever paid for a work by a living artist at auction.

The Koons led Christie’s postwar and contemporary art sale today, which totalled $539 million, up 36 percent from a year ago. The evening saw seven new artist records, with a $32.1 million spider sculpture by Louise Bourgeois joining Koons and Rauschenberg.

…

The 1986 Rabbit was bought by art dealer Bob Mnuchin, U.S. Treasury Secretary Steven Mnuchin’s father, who was in the midtown Manhattan salesroom and said he made the purchase on behalf of a client. Estimated at $50 million to $70 million, it was part of a group of works consigned by the family of late media mogul Si Newhouse. …

… For the remainder of the report:

END

For the first time Kitco is allowed to mention gold manipulation. The interview is with Max Keiser and the interviewer is Daniela Cambone

(courtesy Kitco/GATA)

Kitco lets Max Keiser mention gold market manipulation

Submitted by cpowell on Thu, 2019-05-16 15:18. Section: Daily Dispatches

11:19a ET Thursday, May 16, 2019

Dear Friend of GATA and Gold:

Gold market manipulation makes a surprising appearance at Kitco today as Daniela Cambone interviews financial market commentator Max Keiser about the monetary metal’s underperformance. The interview is 11 minutes long and can be viewed at Kitco News here:

https://www.kitco.com/news/2019-05-16/Fair-Value-For-Gold-Price-2-900-Bi…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Another Cdn miner going into the dust bin: Iamgold explores its sale amid gold sector consolidation

(Bloomberg/GATA)

Iamgold explores sale amid gold-sector consolidation

Submitted by cpowell on Fri, 2019-05-17 02:10. Section: Daily Dispatches

By Scott Deveau and Dinesh Nair

Bloomberg News

Thursday, May 16, 2019

Canadian miner Iamgold Corp. is exploring a possible sale of all or part of the company amid a wave of consolidation in the gold sector, according to people familiar with the matter.

The Toronto-based miner is working with advisers and has spoken to several potential buyers, said the people, who asked not to be identified because the matter is private.

Iamgold’s plans could still change and there’s no guarantee it would succeed in selling itself, the people said.

A representative for Iamgold declined to comment. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-05-16/iamgold-is-said-to-ex…

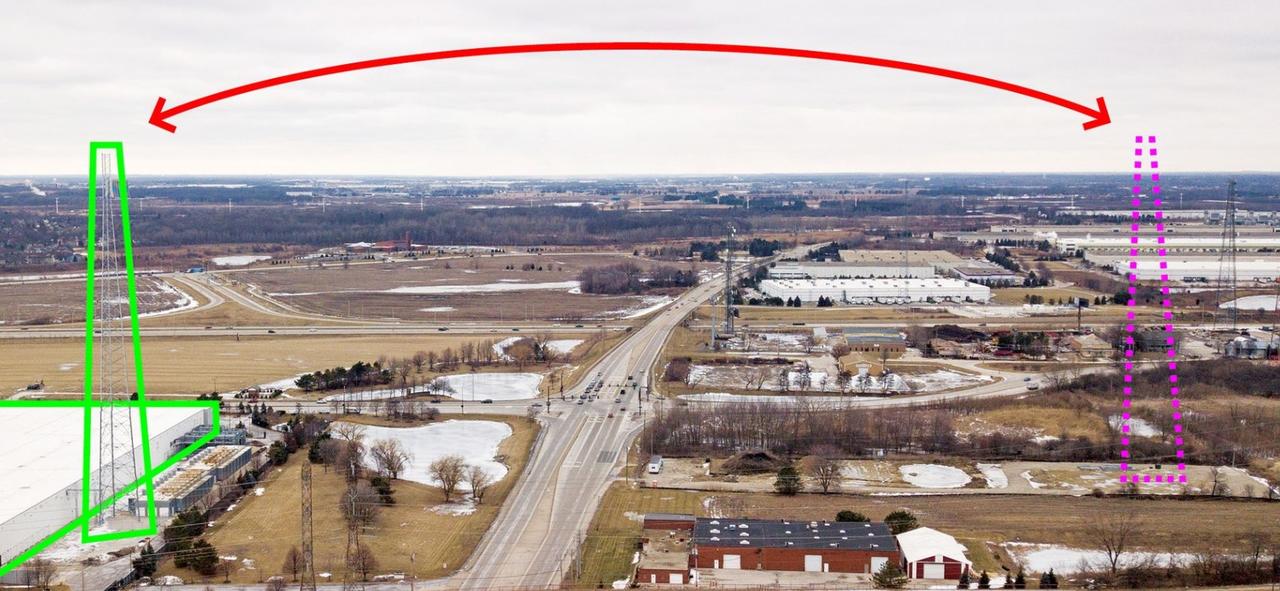

Futures Exchange To Introduce Gold, Silver “Speed Bump” To End HFT Manipulation

No sooner had we covered the battle of high frequency traders physically moving infrastructure and microwave towers to gain nanosecond advantages, that we learned that Intercontinental Exchange (ICE) has planned on launching the first ever “speed bump” for the US futures market that would negate some of these advantages. Despite two of the CFTC’s five commissioners disagreeing with the decision, the exchange still looks set to impose a split second delay on some trades, according to the Wall Street Journal.

Those not in favor of the decision claim that the “speed bump” would unfairly punish firms that rely on their speed advantage. Those in favor, say that it’s about time someone did something to stop the HFTs from frontrunning everyone in the futures market. Which is also why some of the largest high frequency trading firms are vocally opposed to the plan.

As part of the proposed speed bump, the ICE is looking to introduce a 3 millisecond pause before executing some trades in its gold and silver futures contracts. Trading in those contracts is relatively tiny, as most gold and silver futures trades take place at the CME Group. However, traders have been watching this decision because of the precedent it could set.

The CFTC had a chance to block the proposal within 90 days, but that period ended on Tuesday. Now, ICE is free to do as it pleases. The CFTC’s Division of Market Oversight said it’s going to watch carefully to analyze the impact of the new “speed bump” saying it “does not view the certification of the ICE Rule as establishing a precedent with respect to the legal and policy merits of speed bump functionalities generally.”

Other attempts to create similar “speed bumps” at other exchanges will be assessed on individual merits, according to the Division. Both a Democratic and Republican commissioner issued objections to the decision. The Republican cited Kurt Vonnegut’s short story “Harrison Bergeron”, where the government forces handicaps on talented people to create a level playing field, in his dissent.

Republican Brian Quintenz said: “Those that invent, and invest in, faster information transmission technologies to capitalize on market dislocations reap the profits of their advantage. That process enhances market efficiency.”

ICE hasn’t given a timeline for when they are going to implement the “speed bump”. The exchange commented: “We are very pleased with the CFTC’s decision to allow our rule amendment for passive order protection—or what is commonly referred to as a speed bump—in futures markets to become effective.”

HFT giants like Citadel Securities LLC and DRW Holdings LLC, which make the bulk of their revenue from frontrunning slower retail and “dumb money whale” orders, were opposed to the idea, along with trade group Managed Funds Association, which represents hedge funds. Stephen Berger, global head of government and regulatory policy for Citadel Securities said: “We appreciate the commission’s confirmation that today’s rule change is limited in scope to two specific contracts and that any future expansion will require a new rule filing and legal analysis.”

The best hot take on the speed bump belonged to Tom McClellan, who said that “high-frequency algo traders spent all that money, locating their offices closer to ICE server farms and buying high-speed fiber connections to get an edge on trading, and now ICE is introducing a 3-millisecond delay trying to level the playing field.”

Tom McClellan@McClellanOscHigh-frequency algo traders spent all that money, locating their offices closer to ICE server farms and buying high-speed fiber connections to get an edge on trading, and now ICE is introducing a 3-millisecond delay trying to level the playing field. https://www.wsj.com/articles/first-speed-bump-coming-to-u-s-futures-markets-11557924822 …

First ‘Speed Bump’ Coming to U.S. Futures Markets

The ICE futures exchange is set to blunt the advantages of ultrafast traders by imposing a split-second delay on some trades.

wsj.com

Which also explains why they are all so furious.

Several smaller firms welcomed the idea, however, claiming it would allow greater competition. HFT firms now have to spend significant amounts of capital to shave millionths of a second off their trades. Large firms have built out microwave infrastructure and have jostled to get close to exchanges to find minuscule advantages, as we have profiled in the past.

The “bump” is set to apply to incoming orders seeking to hit unexecuted buy or sell orders already posted on ICE, while traders posting new orders to be displayed on the exchange won’t be affected. Eric Swanson, head of the Americas unit of XTX Markets said: “By negating costly HFT speed advantages at millisecond time frames, ICE’s speed bump will reduce the indirect operational tax on end users.”

Still, some critics claim that the delay could actually cause more volatility in periods of market turmoil.

DRW founder and Chief Executive Donald Wilson Jr. said: “During episodes of volatility, there would be essentially fake liquidity on the screen. I think that’s a very dangerous thing.”

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.9145/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9468 /shanghai bourse CLOSED DOWN 73.42 POINTS OR 2/48%

HANG SANG CLOSED DOWN 328.61 POINTS OR 1.16%

2. Nikkei closed UP 187.11 POINTS OR 0.89%

3. Europe stocks OPENED RED /

USA dollar index RISES TO 97.89/Euro FALLS TO 1.1168

3b Japan 10 year bond yield: RISES TO. –.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.64/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 63.52 and Brent: 73.05

3f Gold FLAT/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.11%/Italian 10 yr bond yield DOWN to 2.62% /SPAIN 10 YR BOND YIELD DOWN TO 0.87%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.73: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.42

3k Gold at $1286.00 silver at: 14.49 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 1/100 in roubles/dollar) 64.43

3m oil into the 63 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.64 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0104 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1285 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.11%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.38% early this morning. Thirty year rate at 2.82%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.0615..they are toast

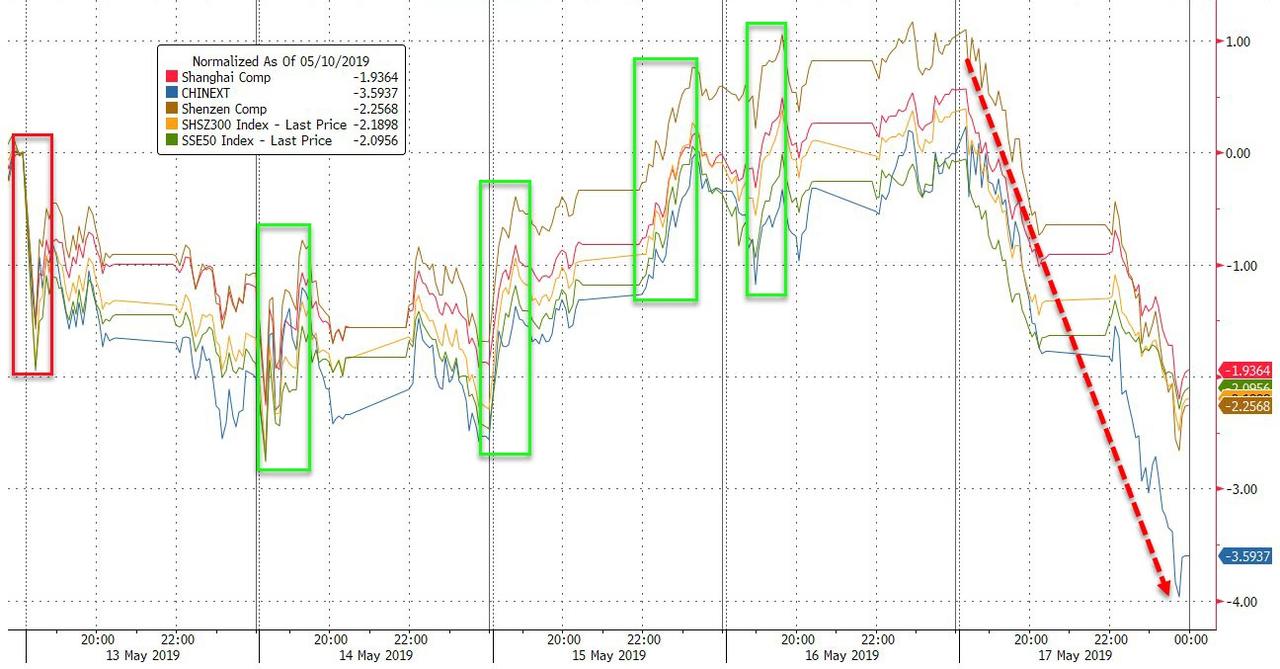

Global Markets, Yuan Tumble As China Crushes Trade Hopes

After yesterday’s bizarre, gamma-chasing rally, the week was set to close in a sea of red as world markets suffered a fresh bout of risk aversion on Friday after China doused hopes for a quick deal when its state media signaled a lack of interest in resuming trade talks with the U.S. under the current threat to escalate tariffs, while the government said stimulus will be stepped up to buttress the domestic economy. Meanwhile bets on a new pro-Brexit leader in Britain whipped the pound towards its worst week since October.

After an initial advance, Asian stocks erased most gains for the day with the MSCI index of Asia-Pacific shares outside Japan sliding to 15-week lows and down 2.6% for the week at the end of trading. An advance in Japanese stocks failed to offset falling Chinese shares. The Topix Index rose 1.1%, led by electric appliances, while China’s Shanghai Composite Index fell 2.5% after a front page commentary in the Communist Party’s People’s Daily evoked the patriotic spirit of past wars, saying the trade war would never bring China down.

“The China state media commentaries fueled concerns that the U.S.-China trade disputes will prolong, deterring risk-taking,” said Koji Fukaya, CEO of Japan’s FPG Securities. “This issue will probably be one of the major market drivers for a while as U.S.-China trade war influences global economic conditions.”

In terms of how the trade conflict plays out, “the next fortnight will be very, very important,” UniCredit strategist Kiran Kowshik said. “Chinese counter-tariffs are due on June 1 and if those get effective, I think markets will price in the risk of the U.S. imposing its additional $300 billion of tariffs ahead of the G20 meeting (near the end of June).”

Elsewhere, stocks retreated in South Korea and Hong Kong, while India’s S&P BSE Sensex Index extended a rebound into the second day and the main Australian index climbed to an 11-year peak as higher commodity prices boosted miners.

As Bloomberg notes, “traders are reassessing prospects for a trade deal after commentary on the blog Taoran Notes, which was carried by state-run Xinhua News Agency and the People’s Daily, the Communist Party’s mouthpiece, accused the U.S. of playing “tricks to disrupt the atmosphere.” Indications that the talks are paused will focus attention on the next opportunity for Presidents Xi Jinping and Donald Trump to meet — at the Group of Twenty meeting in Japan next month.”

As a result of the collapse in trade “optimism”, US equity futures including the S&P 500, Dow Jones and Nasdaq signaled a lower U.S. open after yesterday’s gains, while the Stoxx Europe 600 Index fell for the first time in four days, led by autos, with most sectors in red. Germany’s exporter-heavy DAX fell the most, auto stocks lost as much as 1.6%. Easyjet was a standout of the gauge after releasing earnings, while takeaway food delivery firms including Just Eat and Delivery Hero tumbled after Amazon confirmed an investment in rival Deliveroo.

Sentiment on Thursday was briefly, if erroneously soothed by better U.S. economic news, with housing starts surprisingly strong and a welcome pickup in the Philadelphia Federal Reserve’s manufacturing survey. Upbeat results from Walmart burnished the outlook for retail spending, though the chain also warned that tariffs would raise prices for U.S. consumers.

As the US earnings season winds down, of the 457 S&P 500 companies reporting about 75% have beaten profit expectations, according to Reuters data.

In rates, the sudden trade wind chilling helped Treasuries, with the 10-year yield down at 2.37% after a second strong week running for bond markets. German bonds pushed toward fresh highs with yields having dropped 14bps over the past two weeks as the U.S.-China trade conflict and uncertainty over Italy has spurred a strong risk-off bid. Yields on Spanish 10-year debt fell to a record as bonds across the euro region firmed.

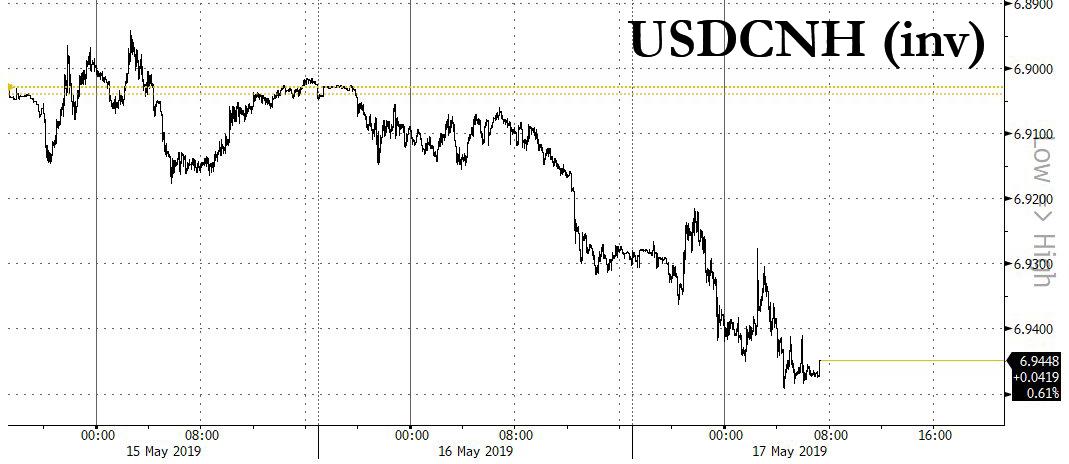

In FX, the standout mover was the yuan, which was already trading at five-month lows, and smashed support after stops were triggered once the offshore Yuan tumbled below 6.92 yesterday, prompting Deutsche Bank to suggest “Stairway to Seven” is in the cards. The USDCNH hit a multi month high of 6.9491 even though Reuters reported again that the PBOC would not allow the currency to drop below 7.00.

Elsewhere in FX, the dollar lost a little of its shine against the safe-haven yen to stand at 109.64 from a top of 110.03. Against a basket of currencies, the dollar increased for a second day to head for its best week since February. The once again was depressed by fears about a Savlini government in Italy, holding at $1.1173, down 0.5% for the week so far. Sterling, down for the 6th day in a row, was one of the worst performers as Britain’s Prime Minister Theresa May battled to keep her Brexit deal, and her premiership, intact amid growing fears of a disorderly departure from the European Union. The pound touched a three-month low of $1.2783 and was down 1.6% for the week so far. Also under pressure was the Australian dollar, losing 1.5% for the week to $0.6880 as investors piled into bets that interest rates would be cut in June.

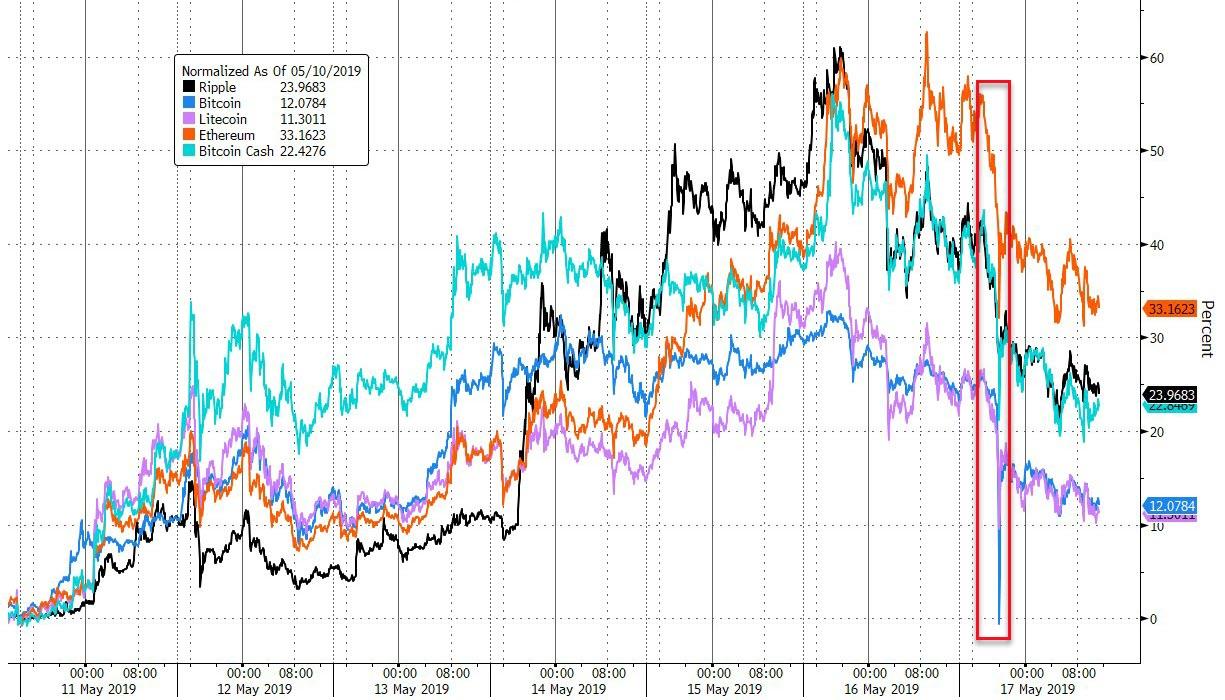

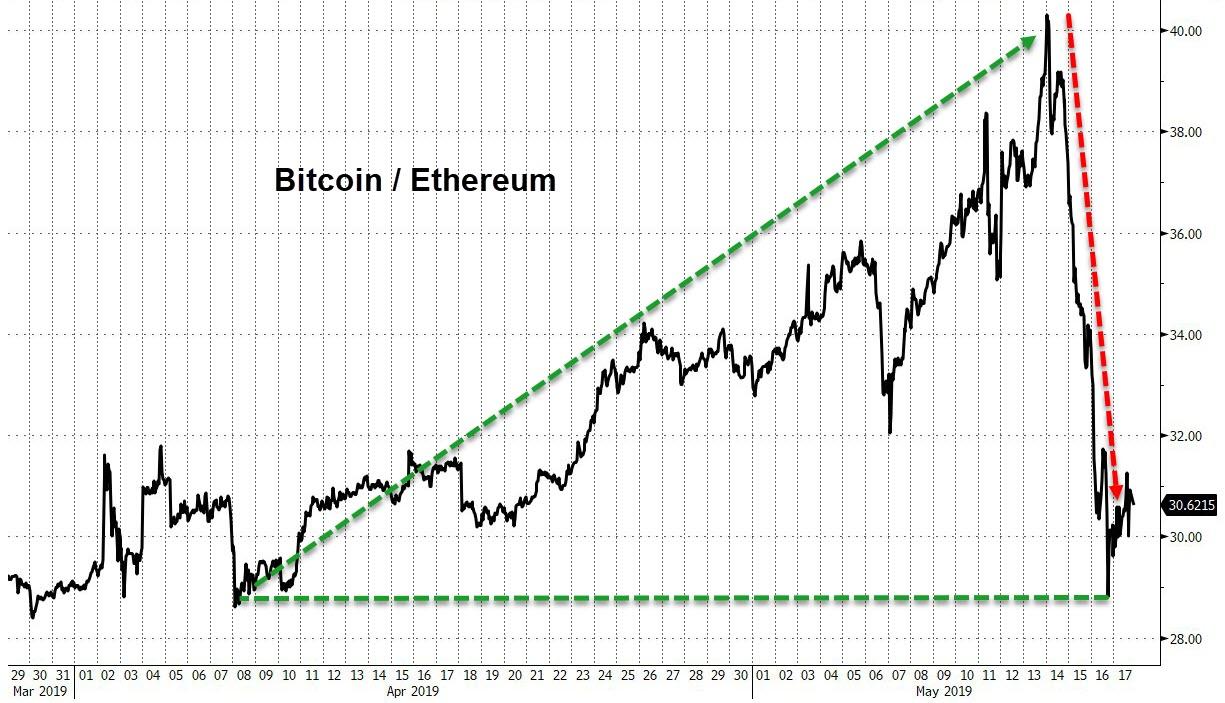

Of note, after soaring 100% in two weeks, Bitcoin tumbled over 20% at one stage after what appeared to be a flash crash. It was last down 7%, albeit back on course for its third week of gains and having doubled in value this year.

In commodity markets, spot gold steadied at $1,287 per ounce as risk sentiment soured. Crude oil gained, as rising tensions in the Middle East stoked fears of potential supply disruptions, while iron ore rose to its highest level in almost five years on supply woes. WTI was last up 33 cents at $63.20 a barrel, while Brent crude futures rose 19 cents to $72.81. OPEC and non-OPEC producers will meet in Saudi Arabia this weekend over whether to continue with supply cuts that have boosted prices more than 30% so far this year.

Expected data include Leading Index and University of Michigan Consumer Sentiment Index. CAE and Deere report earnings.

Market Snapshot

- S&P 500 futures down 0.5% to 2,864.25

- STOXX Europe 600 down 0.6% to 380.63

- MXAP down 0.02% to 154.55

- MXAPJ down 0.8% to 504.53

- Nikkei up 0.9% to 21,250.09

- Topix up 1.1% to 1,554.25

- Hang Seng Index down 1.2% to 27,946.46

- Shanghai Composite down 2.5% to 2,882.30

- Sensex up 1% to 37,777.24

- Australia S&P/ASX 200 up 0.6% to 6,365.30

- Kospi down 0.6% to 2,055.80

- German 10Y yield fell 1.1 bps to -0.106%

- Euro unchanged at $1.1174

- Italian 10Y yield fell 6.2 bps to 2.311%

- Spanish 10Y yield fell 4.7 bps to 0.858%

- Brent futures up 0.2% to $72.74/bbl

- Gold spot little changed at $1,286.67

- U.S. Dollar Index little changed at 97.90

Top Overnight News from Bloomberg

- China’s state media signaled a lack of interest in resuming trade talks with the U.S. under the current threat to escalate tariffs and without new moves that show the U.S. is sincere. The Chinese government said stimulus will be stepped up to buttress the domestic economy.

- Without new moves that show the U.S. is sincere, it is meaningless for its officials to come to China and have trade talks, according to a commentary by the blog Taoran Notes, which was carried by state-run Xinhua News Agency and the People’s Daily, the Communist Party’s mouthpiece

- Theresa May is confronting the end of her premiership after her own party forced her to agree to set a timeline to quit as U.K. prime minister. Before announcing the schedule for her departure, May will try one last time to finish the job she started and get her Brexit deal approved in a vote in Parliament at the beginning of June

- The pound headed for the longest losing streak against the euro since the turn of the century as rising U.K. political risks fanned concern about the nation’s ability to achieve an orderly Brexit.

- President Donald Trump is wary of drawing the U.S. into a war with Iran, in part out of concern that an armed conflict with the Islamic Republic would imperil his chances at winning a second term, according to people familiar with the matter. U.S.’s evidence of Iran threat readied for release by Pentagon

- The U.S. announced a rollback of steel tariffs against Turkey that it originally levied in August as trade and diplomatic relations deteriorated because of Turkey’s economic crisis and a row over the Turkish government’s detention of an American pastor.

- Italy’s Matteo Salvini has a new medicine to fix his country, and he calls it “the Trump cure.” After being the steady hand in Rome’s populist coalition government for most of the past year, the deputy prime minister and anti-immigrant League party leader projected himself as the country’s Donald Trump on Thursday

- Amazon.com Inc. is leading a $575 million investment in Deliveroo, buying a slice of the fast-growing startup to propel its drive into the European food and groceries business. U.K.-based Deliveroo has raised $1.53 billion to date.

- Deputy prime minister and anti-immigrant League party leader Matteo Salvini projected himself as the country’s Donald Trump during intense campaigning for the European Parliamentary elections on May 26.

- European Central Bank officials dragging their feet over a potential revamp of their negative interest rates might be shutting off one way to convince investors they are serious on stoking inflation.

Asian equity markets were mostly higher as the region took impetus from the positive performance on Wall St, where all major indices notched a 3rd consecutive win streak with risk sentiment underpinned by encouraging earnings from Walmart and Cisco. ASX 200 (+0.6%) and Nikkei 225 (+0.9%) traded positive with Australia led by continued strength in tech and amid the growing list of calls for a rate cut next month including notorious RBA watcher McCrann, while Japanese exporters were buoyed by recent favourable currency moves and as Sony shares surged over 10% after the announcement of a JPY 200bln share buyback. Hang Seng (-1.2%) and Shanghai Comp. (-2.5%) were pressured after a lack of PBoC reverse repo operations throughout the week resulted to net weekly drain of CNY 50bln. In addition, China cancelled orders of 3247 tons of pork from US which was the largest cancellation in more than a year and was seen to be another fallout of the ongoing US-China trade dispute, while commentary in Chinese state media suggested China may have no interest in resuming trade discussions with the US for now. Finally, 10yr JGBs were lower amid the upbeat risk tone in Japan and on spill-over selling from the bear flattening stateside, while the BoJ’s Rinban announcement was for a reserved JPY 200bln of long to super-long JGBs.

Top European News

- Europe Could Reap Silver Lining From U.S.-China Trade Dispute

- Euro-Area Core Inflation Revised Up to 1.3%, Highest Since 2017

- LetterOne Wins Enough Shareholder Backing to Take Over DIA

- EasyJet Gains After Insulating Against Drop in Summer Fares

- Spanish Yield Drops to a Record as Nation’s Debt Allure Grows

A relatively downbeat session thus far for major European stocks [Eurostoxx 50 -0.5%], following on from a mixed lead in Asia where the Shanghai Composite shed 2.5% as hopes for a trade deal dwindled amid reports that China may not want to continue trade talks with the US for now. Major indices are broadly lower by around 0.5-0.7%, although, the FTSE 100 outperforms as UK exports benefit from the weaker Sterling. Sectors are showing broad-based losses with the exceptions of utilities (defensive sector) and energy names due to price action in the complex. Elsewhere, Thomas Cook (-24.8%) shares slumped for a second consecutive day, with traders citing the downside to a downgrade at Citi with a price target of zero. Finally, GVC Holdings (+2.5%) remain near the top of the Stoxx 600 after the Co. cut its potential impact from the FOBT GBP 2 limit from GBP 120mln to GBP 105mln. Notable pre-market US earnings this morning from Deere & Co (DE), who missed on EPS but beat on revenue and lowered their net income guidance.

Top Asian News

- China Traders Snap Up Most Hong Kong Stocks Since Early 2018

- Nissan Adds Renault’s Bollore to Board as Part of Overhaul

- Taiwan Parliament Approves Gay Marriage Law in First for Asia

- Offshore Yuan Smashing Support Level Brings Record Low in Sight

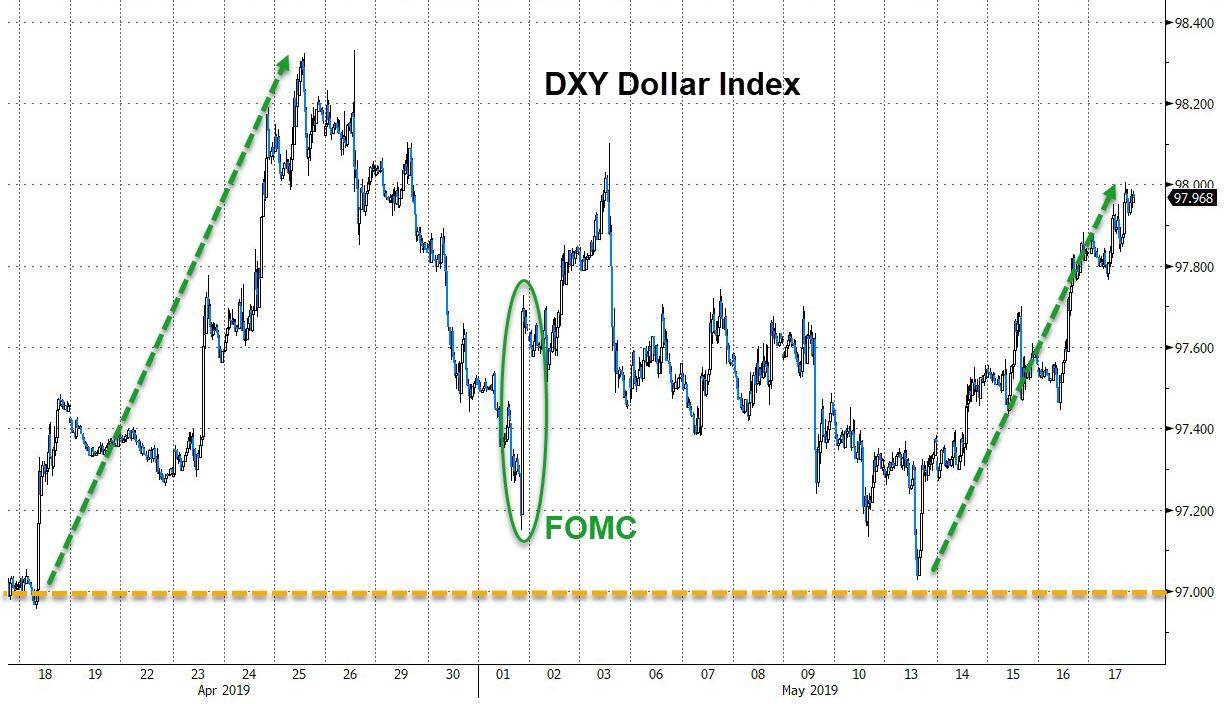

In FX, the Greenback has held onto the bulk of its post-US data/survey gains by virtue of advances against riskier/high beta counterparts as safer-havens within the G10 community are outperforming in wake of pretty defiant comments from China revealing a reluctance to pursue talks further given recent actions taken by the US. The index is hovering just below the 98.000 level after an apparent clean break of Fib resistance at 97.842 within a 97.953-759 range. To recap, 98.102 is the mtd DXY high and then the 2019 peak at 98.346 comes into focus.

- JPY/CHF – As noted, the Yen and Franc are back in favour on US-China trade stains, but also as Brexit, Italian budget and geopolitical issues weigh on broad risk sentiment, with Usd/Jpy retreating from circa 110.00 highs back towards 109.50 and away from decent option expiries at the big figure (1.2 bn). Usd/Chf is holding around 1.0100, but Eur/Chf is back below 1.1300 and near recent lows not far from key chart supports and levels that may prompt some form of SNB action.

- CAD/AUD/GBP – All on the back foot due to the aforementioned bearish/negative factors, as the Loonie revisits recent lows around 1.3500 and Aussie extends losses through 0.6900 to 0.6873 following latest jobs data that heightens the prospect of a June RBA rate cut after this month’s dovish hold. Similarly, the Pound continues to slide, and Cable has now hit fresh lows since the Valentine’s Day base of 1.2773 at 1.2755 on confirmation that cross party talks have come to a conclusion with no collusion in terms of an alternative WA. Note also, Gbp/Jpy has tripped stops on a break of the psychological 140.00 level.

- EUR/NZD – Also victims of the ongoing Usd revival and overall downturn in risk appetite, with the single currency declining to fresh weekly lows and testing bids said to be sitting at 1.1160 and protecting 1.1150 ahead of the current 1.1135 May base, while the Kiwi is slipping further away from 0.6550 and closer to 0.6525 given only scant support from Aud/Nzd cross flows within 1.0550-25 parameters.

- EM – Mixed blessings for the Turkish Lira as the US halved its tariff on steel, but removed preferential status on metals overall, while the AKP is still reportedly on a mission to tap CBRT reserves. Usd/Try extending above 6.0000 and testing resistance at 6.1000 before paring back, while the Yuan is not taking much heed of reports that 7.0000 is the PBoC’s line in the sand as the US-China tariff spat shows no sign of improving.

In commodities, choppy trade in the energy complex, although WTI (+1.1%) and Brent (+0.7%) futures are ultimately higher ahead of this week’s JMMC meeting in Saudi Arabia, which sets the stage for the OPEC/OPEC+ meeting in June. Focus will be on Iran’s situation amidst US sanctions and the expiry of waivers and whether there is scope to extend the current output cut deal between OPEC and its allies. Ship tracking data showed that Iranian oil shipments in May thus far has fallen to zero, however, ING highlights that a large number of Iranian tankers turn off their transponders. This follows reports of a tanker carrying Iranian oil reportedly unloading its cargo of almost 130k tonnes of oil near Zhousan, in China, Iran’s largest customer. Furthermore, comments from Iran’s revolutionary guard emphasis rising tensions between the country and the US, with the latest stating that “even short-range missiles can reach US warships in the Gulf”. Market participants will be on the lookout for how US President Trump reacts to these threats from Iran. In terms of weekly price action so far, WTI futures are poised for a positive week after having breached its 50 WMA (61.81) to the upside whilst similarly, Brent futures are set for a week of gains, after having dipped below USD 70/bbl (and its 50 WMA at the figure) earlier in the week. Elsewhere, precious metals are little changed with spot gold (-0.2%) meandering further below the 1300/oz level after having lost more ground to yesterday’s rising Buck.

US Event Calendar

- 10am: Leading Index, est. 0.2%, prior 0.4%

- 10am: U. of Mich. Sentiment, est. 97.2, prior 97.2; Current Conditions, est. 112.2, prior 112.3

DB’s Jim Reid concludes the overnight wrap

It’s a bit of a teary eyed trip down memory lane coming up this weekend as I’m playing my first proper gig in over a decade. The cricket club that I’m President of is having a fund raiser and although there are discussions that they’d raise more money if I didn’t sing and play live, I have offered up my services nevertheless. We haven’t rehearsed so we’re doing almost the identical covers set to our last gig and even then it was out of date. Given that the average age of the cricket club is probably early 20s I wonder how many of our set will have been released before these guys were born. So I’m a bit worried they won’t know any of them. Tragically this also means I’ll miss Britain coming near the bottom of the pile at Eurovision tomorrow night. Nul points!!!

Unlike voters unfairly shunning Britain’s annual song contest entry, markets have been surprisingly well behaved over the last few sessions and have seemingly become becalmed about the current trade spat regardless of the fact that a resolution anytime soon is very unlikely. That was even despite the latest Huawei developments late on Wednesday night. A +0.89% gain for the S&P 500 yesterday means that the index is up for three days in a row and has retraced to being down only -2.65% from the recent highs now. That being said more trade-sensitive sectors and stocks are still struggling. The semi-conductor index for example – which fell -1.68% yesterday – is down -10.00% from the highs of last month, while Apple is still down -10.23% over the past two weeks. Nevertheless, the VIX index continues to slide lower, falling -1.1pts yesterday to back below 16 for the first time in eight sessions.

Yesterday we saw China’s Global Times Editor Hu Xijin – a must follow now on Twitter – tweet that “Since the US has made unfair requests with China, we are willing to accompany the US suffering more and more negative impact though China may take greater pain. We have no choice.” Although grammatically the tweet doesn’t quite make sense it leaves you with the impressions that pride is as important as the economic impact to the Chinese at the moment. On the other side White House Commerce Secretary Wilbur Ross said that President Trump has a “wide range of actions” he could take on auto tariffs. On that, Bloomberg ran a story suggesting that Trump would give the EU and Japan 6 months to curb auto sales into the US in return for delaying new tariffs. So that is a tentative November timetable which means that the uncertainty window has the potential to run for some time now. Imagine if we had Auto tariffs and a hard Brexit occurring within days of each other!! European Autos declined -0.48% yesterday and underperformed the broader STOXX 600 index (+1.27%).

As for other markets, there were decent gains for the likes of the NASDAQ (+0.97%), DOW (+0.84%) and DAX (+1.74x%). High yield credit spreads were -7bps tighter in the US while in bond markets we saw Bunds hold steady at -0.097% while Treasuries weakened +2.5bps to touch 2.40% again. However Europe wasn’t all one-way traffic with BTPs (-6.2bps) standing out and reversing some of the recent underperformance. That appeared to partly reflect comments from the 5SM’s Di Maio who suggested that Italy’s debt-to-GDP ratio won’t breach 140%. On the flip side the League’s Salvini said that the government will “tear apart every single rule butchering Italy” should the League do well in the EU elections. There’s a real good-cop-bad-cop dynamic going on in Italy right now with much of it political posturing ahead of the EU elections. As for currencies, EM FX finished -0.32%, with high yielders like the Brazilian real (-0.98%) and Turkish lira (-0.69%) underperforming. Weak currencies pressured EM equities, with MSCI EM down -0.44%. In other FX space, the euro (-0.24%) was a shade weaker and the dollar rallied +0.28% for its third consecutive advance. Sterling was a bigger mover though, falling -0.37% and below $1.280 following the latest Brexit developments – more on that below.

Overnight, the Trump administration has said that new restrictions on Huawei announced earlier in the week would take effect today, with the parent company and 67 affiliates in 26 countries placed on a blacklist that will limit Huawei’s access to US suppliers, according to the Federal Register notice. The US Commerce Secretary Wilbur Ross also said that Trump has given his department 150 days to establish a process to screen US companies’ purchases of equipment from Huawei, and other equipment providers with which officials have concerns. In the meantime, China’s Toran Notes, a WeChat blog run by state-owned Economic Daily, reported today that if the US doesn’t make any new moves that truly show sincerity, then it is meaningless for its officials to come to China and have trade talks. The blog added that “We can’t see the U.S. has any substantial sincerity in pushing forward the talks. Rather, it is expanding extreme pressure,” citing Trump’s steps this week to curb Chinese telecom giant Huawei while reiterating that China has three main concerns including tariff removal, achievable purchase plans and a balanced agreement text. The blog went on to say, “In addition, if anyone thinks the Chinese side is just bluffing, that will be the most significant misjudgement since Korean War”. The same article was also carried by state-run Xinhua News Agency and the People’s Daily (Communist Party’s mouthpiece). So, rhetoric and actions continues to indicate that neither side is in any rush to temper the recent escalation. Elsewhere, China’s National Development and Reform Commission spokeswoman Meng Wei said that China will “study the possible impact of US tariffs on the Chinese economy, and roll out responsive measures when necessary,” possibly hinting that more stimulus is likely to come.

The above rhetoric from China on not being interested in talking to the US if attitudes don’t change is weighing on Chinese and Hong Kong markets this morning with the CSI (-1.67%), Shanghai Comp (-1.46%) and Shenzhen Comp (-1.66%) all down over 1% while the Hang Seng is down a relatively modest -0.77%. The Nikkei (+1.02%) and Kospi (+0.14%) are both up but they are off their highs since China’s state media reports started filtering in. It’s noteworthy that CNH didn’t rally alongside equities yesterday as it weakened another -0.35% (a further -0.15% this morning), highlighting the continued fears over trade despite the improvement in risk appetite. Elsewhere, futures on the S&P 500 are down -0.28% this morning erasing earlier gains.

Back to yesterday, where our FX strategists published their latest Blueprint report entitled “Stairway to Seven”. With Brexit, trade tensions and geopolitical issues still in play, their bias is for higher volatility and weaker risk appetite. In terms of their trade recommendations, with Europe – and especially Germany – particularly exposed to global risks the team are abandoning their positive view on the euro and see EUR/USD potentially breaking 1.10 through the summer. They are also becoming even more concerned on Asia and see USD/CNY breaking through 7. They do not see a quick resolution to the trade war and argue that Chinese authorities will become more amenable to currency weakness. The JPY should be a continued beneficiary of global volatility and they forecast a move down to 105 in USD/JPY. See their full report here .

Over to Brexit, where Prime Minister May is under ever increasing pressure from within her own party. She met yesterday with the 1922 Committee, which governs the Conservative party’s internal rules and could greenlight a leadership challenge against her via a change in rules. Though she survived without an immediate threat, May also agreed to meet with the Committee again after her WA gets put to another vote. That vote, likely to be held the week of June 3, will be key. As it currently stands, it looks likely to fail. Now that May looks likely to depart if it fails, that lowers the incentive for Labour to cooperate. The odds of a Tory leadership struggle resulting in a hard-Brexit Prime Minister and a subsequent general election have risen. Indeed, that’s why our FX team remains bearish the pound in yesterday’s FX blueprint.

In the US, Fed Governor Brainard, viewed as a good representative of the centre of the FOMC’s thinking, was the latest Fed official to toe the party line on inflation dynamics, calling the latest misses “transitory” and citing the trimmed mean as a truer measure of underlying pressures. However, she did also discuss the potential benefits of letting inflation rise above 2%, in order to “demonstrate to the public our commitment to our inflation goal on a symmetric basis.” That sounds like she would likely support a shift to average inflation targeting or a similar regime next year. Separately, Minneapolis Fed President Kashkari, one of the more dovish FOMC members, echoed her comments, saying the Fed should “actually allow inflation to climb modestly above 2 percent in order to demonstrate that we are serious about symmetry.”

As for the data, given that the releases at the moment are still covering the pre-trade escalation period they are somewhat being taken with a pinch of salt for now. For completeness though, the May Philly Fed PMI rose +8.1pts and far more than expected to 16.6 (vs. 9.0 expected). The details were a bit more mixed though with employment stronger but new orders weaker. As for the April housing data, starts (+5.7% mom vs. +6.2% expected) and permits (+0.6% mom vs. +0.1% expected) missed and beat respectively however both benefited from upward revisions to the prior month. Finally claims declined 16k to 212k and a little bit more than expected following a holiday related spike. No particularly big takeaways overall therefore.

Looking at the day ahead, this morning we’ve got final April CPI revisions due for the Euro Area (no change from the preliminary core reading of +1.2% yoy expected) and March construction output data. In the US the April leading index and preliminary May University of Michigan consumer sentiment survey is due. Away from that the Fed’s Williams is due to meet community leaders at 4.15pm BST and 7pm BST while Clarida is due to speak at a ‘Fed Listens’ event at 6.40pm BST. The BoE’s Brazier is also due to speak at 1pm BST. Elsewhere, EU finance ministers are due to meet in Brussels to discuss a plan for the Euro Area budget.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 73.42 POINTS OR 2.48% //Hang Sang CLOSED DOWN 328.61 POINTS OR 1.16% /The Nikkei closed UP 187.11 POINTS OR 0.89%//Australia’s all ordinaires CLOSED UP .69%

/Chinese yuan (ONSHORE) closed DOWN at 6.9145 /Oil UP to 61.64 dollars per barrel for WTI and 71.08 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9145 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9468 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

i)China/

Trade optimism fizzles as China states it has no more plans for talks. Obviously they are quite concerned with the Huawei situation

(courtesy zerohedge)

Trade Optimism Fizzles As China Says No Plans For More Talks

Well, it looks like President Trump finally did it. He finally pushed Beijing so hard on Huawei that they had no choice but to respond.

The Chinese weren’t kidding when they warned that Washington’s latest aggression toward Huawei – adding the Chinese telecoms giant to a blacklist that will make it extremely difficult, if not impossible, for Huawei to buy components from American companies – might crash trade talks.

Because after the Commerce Department formally added Huawei to the blacklist, the Chinese media and Chinese officials turned up the rhetoric, warning that there are no plans for another round of talks. Markets didn’t take this well: Chinese stocks plunged 2.5% overnight on Friday – a big drop, though still not as bad as the 3% decline from last Monday,the market’s worst day in three years. European shares didn’t fare much better because, as one analyst explained to Bloomberg…

“The China state media commentaries fueled concerns that the U.S.-China trade disputes will prolong, deterring risk-taking,” said Koji Fukaya, chief executive officer at FPG Securities Co. in Tokyo. “This issue will probably be one of the major market drivers for a while as U.S.-China trade war influences global economic conditions.”

US futures were in the red, leaving stocks on track for a lower open. Yields on Treasuries and bunds declined. Asia’s emerging currencies and the yuan weakened. The yen and Swiss franc advanced.

A comment on Taoran, seen as a venue for the government’s views, accused the US of playing “little tricks to disrupt the atmosphere,” and insinuated that the Huawei blacklisting had seriously jeopardized talks.

“We can’t see the U.S. has any substantial sincerity in pushing forward the talks. Rather, it is expanding extreme pressure,” the blog wrote. “If the U.S. ignores the will of the Chinese people, then it probably won’t get an effective response from the Chinese side,” it added.

One former government official said there’s no point in holding another round of talks if the US won’t listen to Beijing.

“If the U.S. doesn’t make concessions in key issues, there is little point for China to resume talks,” said Zhou Xiaoming, a former commerce ministry official and diplomat. “China’s stance has become more hard-line and it’s in no rush for a deal” because the U.S. approach is extremely repellent and China has no illusions about U.S. sincerity,” he said.

This comes after Treasury Secretary Steven Mnuchin said this week that he and the other negotiators “will mostly likely go to Beijing at some point” in the near future.

As BBG noted, another striking detail about the coverage is that China’s strident trade rhetoric has suddenly been plastered across state-controlled media. The People’s Daily ran three aggressive articles, including two editorials, with titles like “No Power Can Stop The Chinese People From Achieving Their Dream” – “the trade war will not cripple China, it will only strengthen us as we endure it.”

Looking ahead, President Xi and President Trump might have an opportunity to revive talks at the G-20 summit in Osaka next month. Until then, both sides will likely dig in.

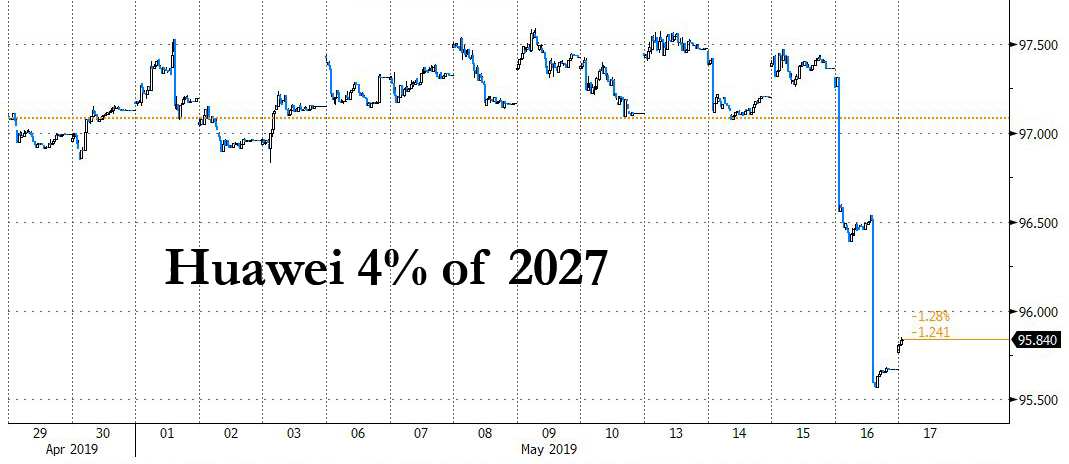

Huawei Bonds Tumble Most On Record

Washington invoked what BBG called “the nuclear option” Thursday night, meaning that a new prohibition on sales of components to the Chinese telecom giant will take place on Friday.

And as investors question how Huawei will adapt, or whether this new status might have serious repercussions for its business, they sold first and asked questions later, with Huawei’s dollar-denominated bonds (4% of 2027) suffered their largest drop on record in the past two days.

The company’s 4% due-2027 notes plunged by a record 2.1 cents to 94 cents on the dollar as of 3:49 am in Hong Kong, their lowest level in two months. Huawei’s 4.125% 2026s also fell 2 cents to 95.4 cents on the dollar as creditors fled the Chinese telecom giant.

The drop outpaced the declines in Asian equity and currency markets, which have been reeling from Beijing’s aggressive trade rhetoric.

The plunge came even as China’s Economic Daily reported overnight that Huawei has “drafted a contingency plan years ago to cope with restrictions on supply of U.S. chips and technologies one day,” citing a letter to employees from He Tingbo, president of Huawei’s chip division Hisilicon. The report also claimed that Huawei will be able to continue its service to clients in such scenario, and will push for innovation and achieve technological independence.

Beijing, meanwhile, tried to shift the focus to “Huawei-related stocks” which climbed even as the Shanghai Composite closed down 2.5%, and cited this as evidence that the narrative of Huawei’s ‘back-up plan’ is helping to reassure markets.

Hu Xijin 胡锡进@HuXijin_GTShanghai stock exchange index dropped 2.48% Friday due to worry of an overall escalation of trade war, but Huawei related stocks soared. This is vote of confidence of the market on Huawei’s long prepared back-up plan. Huawei’s US supplies will become real victims.

But bond holders aren’t convinced. For now, the most likely scenario the company’s suddenly panicking bondholders are seeing, is insolvency.

Beijing Backs Iran, “Firmly Opposes” Unilateral US Sanctions

In the latest sign of Beijing’s frustration with the US, the Chinese leadership have reiterated their opposition to American sanctions against Iran. After a meeting with Iranian Foreign Minister Javad Zarif, Chinese Foreign Minister Wang Yi reiterated Beijing’s ‘firm opposition’ to unilateral US sanctions against Iran.

- CHINA’S FOREIGN MINISTER WANG YI MEETS IRAN’S ZARIF

- CHINA FIRMLY OPPOSES U.S.’S UNILATERAL SANCTIONS AGAINST IRAN

With the US moving more firepower into the Persian Gulf, an attempt to send Tehran an unmistakable message, Zarif asked Beijing to try and save the 2015 nuclear deal, WSJ reports.

Iranian Foreign Minister Javad Zarif and Chinese Foreign Minister Wang Yi.

Zarif’s meeting with his Chinese counterpart is the first step on a tour of Asia, as Iran canvasses its key economic partners now that US sanctions have been reimposed.

Mr. Zarif’s visit to China, where he will meet his Chinese counterpart, is part of a longer trip that includes other key economic partners Russia, Japan and India. It comes amid growing tensions between Washington and Tehran, which spiked over the past week when the U.S., citing unspecified intelligence, deployed an aircraft carrier, a bomber task force and other personnel to the Middle East.

The Iranian embassy in China said on Twitter that Mr. Zarif had “arrived in Beijing to maintain consultations between all-weather friends in the wake of new efforts to manufacture unnecessary tensions.”

China’s Foreign Ministry confirmed Mr. Zarif’s visit but declined to release further information.

The Iranian situation is difficult for Beijing, said Yin Gang, a Middle East politics expert with the government-backed Chinese Academy of Social Sciences. He said the conflict isn’t simply between the U.S. and Iran but between Arab states and Iran. China, Mr. Yin said, “wants a balanced diplomacy in the Middle East, and hopes to make friends and do business with everyone.”

China imports crude from Iran and has expressed reservations about US sanctions in the past. However, given the state of the relationship between Washington and Beijing, the Chinese appear to be signaling that a proxy war over Iran could be just around the corner if Washington doesn’t seriously reevaluate its approach.

end

An excellent commentary from James Rickards as he discusses the problems China faces with the trade war

a must read

(courtesy James Rickards)

Is China’s “Mandate Of Heaven” In Jeopardy?

Authored by James Rickards via The Daily Reckoning,

U.S. policy through the Bush and Obama administrations was to soft-pedal questionable Chinese trade practices, pirating technology and theft of intellectual property in return for cheap manufactured goods and China’s willingness to finance trillions of dollars of U.S. government debt.

Now Trump has changed the rules of the game. He’s said lost jobs in the U.S. are not worth the cheap goods and cheap financing. He bet that China had no alternative but to keep producing those goods and keep buying our debt, even if the U.S. imposes tariffs to help create manufacturing jobs here.

President Trump and President Xi had been on a collision course involving issues of trade, tariffs, and currency manipulation, which are coming to a head.

It’s important to understand that China’s economy is not just about providing jobs, goods and services. It is about regime survival for a Chinese Communist Party that faces an existential crisis if it fails to deliver. It is an illegitimate regime that will remain in power only so long as it provides jobs and a rising living standard for the Chinese people. The overriding imperative of the Chinese leadership is to avoid societal unrest.

Once the Chinese job machine stalls out, popular unrest could emerge on a scale much greater than the 1989 Tiananmen Square protests. This is an existential threat to Communist power.

If China encounters a financial crisis, Xi could quickly lose what the Chinese call, “The Mandate of Heaven.” That’s a term that describes the intangible goodwill and popular support needed by emperors to rule China for the past 3,000 years.

If The Mandate of Heaven is lost, a ruler can fall quickly.

China has serious structural economic problems and its internal contradictions are catching up with it. Economies can grow through consumption, investment, government spending and net exports. The “Chinese miracle” has been mostly a matter of investment and net exports, with minimal spending by consumers.

The investment component was thinly disguised government spending — many of the companies conducting investment in large infrastructure projects were backed directly or indirectly by the government through the banks.

This investment was debt-financed. China is so heavily indebted that it is now at the point where more debt does not produce growth. Adding additional debt today slows the economy and calls into question China’s ability to service its existing debt.