GOLD: $1288.10 UP $6.40 (COMEX TO COMEX CLOSING)

Silver: $14.53 UP 19 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1288.70

silver: $14.53

LBMA OPTIONS EXPIRY TOMORROW:

LBMA/OTC EXPIRY: MAY 31.2019

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 24/49

EXCHANGE: COMEX

CONTRACT: MAY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,280.600000000 USD

INTENT DATE: 05/29/2019 DELIVERY DATE: 05/31/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 3

661 C JP MORGAN 24

661 H JP MORGAN 49

685 C RJ OBRIEN 1

737 C ADVANTAGE 20

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 49 49

MONTH TO DATE: 363

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 49 NOTICE(S) FOR 4900 OZ (0.1524 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 306 NOTICES FOR 3060000 OZ (.9517 TONNES)

SILVER

FOR MAY

119 NOTICE(S) FILED TODAY FOR 595,000 OZ/

total number of notices filed so far this month: 3770 for 18,850,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ N/A

Bitcoin: FINAL EVENING TRADE: $ N/A

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A CONSIDERABLE SIZED 4065 CONTRACTS FROM 217,605 DOWN TO 213,540 DESPITE THE 11 CENT GAIN IN SILVER PRICING AT THE COMEX. LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER BUT IT NOW IN FULL FORCE FOR GOLD. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 1773 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1773 CONTRACTS. WITH THE TRANSFER OF 1773 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1773 EFP CONTRACTS TRANSLATES INTO 8.865 MILLION OZ ACCOMPANYING:

1.THE 11 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 18.845 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

26,714 CONTRACTS (FOR 21 TRADING DAYS TOTAL 26,714 CONTRACTS) OR 133.57 MILLION OZ: (AVERAGE PER DAY: 1272 CONTRACTS OR 6.360 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 133.57 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.08% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 874.67 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD AN CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4065 DESPITE THE 11 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A VERY STRONG SIZED EFP ISSUANCE OF 1773 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE LOST A STRONG SIZED: 2292 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1773 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 4065 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 11 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.45 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.068 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 119 NOTICE(S) FOR 595,000, OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 18.845 MILLION OZ ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY AN UNBELIEVABLE AND MOST LIKELY CRIMINAL SIZED 50,951 CONTRACTS, TO 454,175 DESPITE THE $3.90 PRICE GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY/THE SPREADING LIQUIDATION ENDED YESTERDAY.

WE ARE NOW 1 TRADING DAY PRIOR TO FIRST DAY NOTICE.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6678 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 6678 CONTRACTS, AUGUST 2019: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 454,175. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 44,273 CONTRACTS: 50,951 OI CONTRACTS DECREASED AT THE COMEX AND 6678 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 44,273 CONTRACTS OR 4,427,300 OZ OR 137.7 TONNES. YESTERDAY WE HAD A GOOD GAIN OF $3.90 IN GOLD TRADING ….AND WITH THAT GAIN IN PRICE, WE HAD AN UNBELIEVABLE LOSS OF GOLD TONNAGE OF 137.7 TONNES!!!!!!

WITH RESPECT TO SPREADING: WE HAD A GIGANTIC LIQUIDATION OF THE SPREADERS TODAY

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS HAVE NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 135,887 CONTRACTS OR 1,3588,700 OR 422.66TONNES (21 TRADING DAYS AND THUS AVERAGING: 6470 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAYS IN TONNES: 422,66 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 422.66/3550 x 100% TONNES =11.89% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2238.18 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: AN UNBELIEVABLE AND CRIMINAL SIZED DECREASE IN OI AT THE COMEX OF 150,951 DESPITE THE PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY(3.90)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6678 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6678 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC SIZED LOSS OF 44,273CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6678 CONTRACTS MOVE TO LONDON AND 50,951 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 137.70 TONNES). ..AND THIS LOSS OF DEMAND OCCURRED WITH THE RISE IN PRICE OF $3.900 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD A HUGE PRESENCE OF SPREADING LIQUIDATION YESTERDAY/

we had: 49 notice(s) filed upon for 4900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $6.40 TODAY//SEEMS THE BOYS FOUND RELIGION

A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A HUGE “PAPER” GOLD DEPOSIT OF 3.52 TONNES

INVENTORY RESTS AT 740.86 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 19 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 311.616 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY AN GIGANTIC SIZED 4065 CONTRACTS from 217,605 DOWN TO 213,540 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER BUT HAVE NOW MORPHED INTO GOLD..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 1773 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1773 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 4065 CONTRACTSTO THE 1773 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG LOSS OF 2292 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 11.46MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 18.765 MILLION OZ FOR MAY

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 11 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1173 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 8.89 POINTS OR 0.31% //Hang Sang CLOSED DOWN 120.83 POINTS OR 0.44% /The Nikkei closed DOWN 60.84 POINTS OR 0.29%//Australia’s all ordinaires CLOSED DOWN 0.73%

/Chinese yuan (ONSHORE) closed UP at 6.9070 /Oil UP TO 59.03 dollars per barrel for WTI and 68.78 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.9070 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9264 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

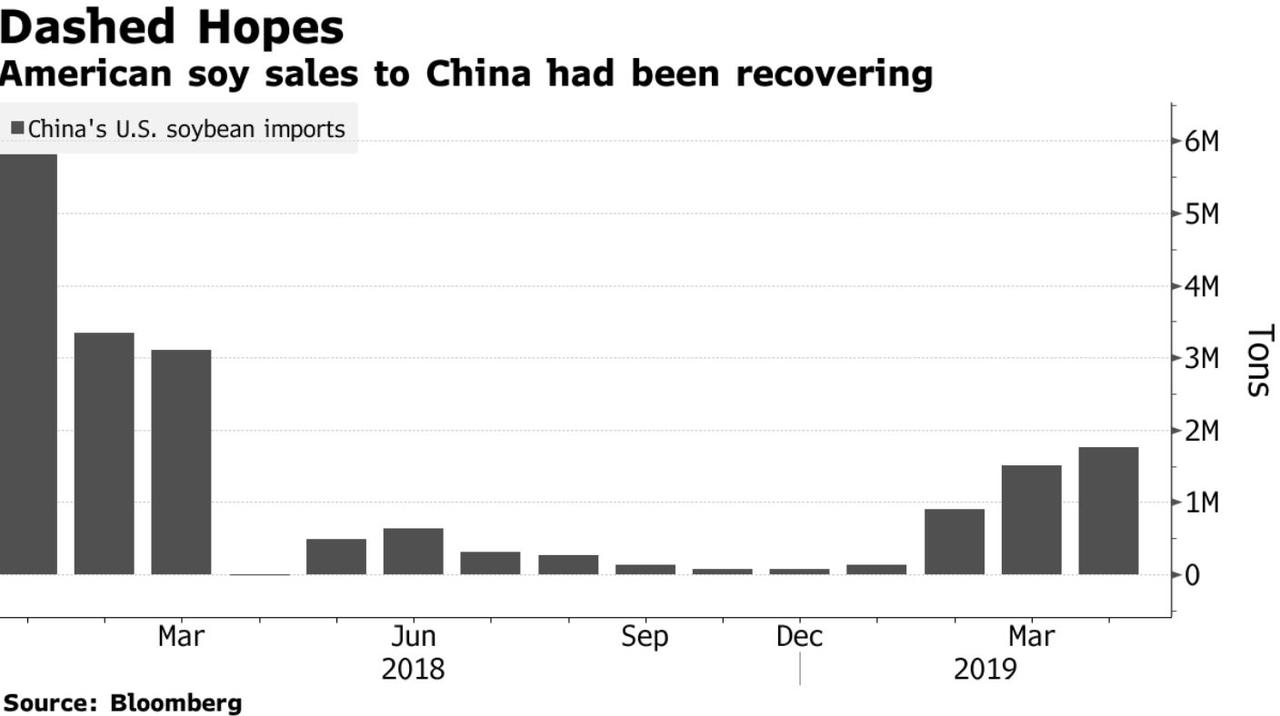

i)China halts its “goodwill” gesture soybean purchases from the uSA

( zerohedge)

4/EUROPEAN AFFAIRS

i)GERMANY/FRANCE/REST OF EUROPE VS USA

Trump gave a 6 month reprieve to Europe so that a deal could be arranged between Europe and the USA. You will recall that the EU is notorious for its high tariffs especially in autos

Trump has demanded the EU to lower tariffs equal to the uSA, something that the stubborn EU will not do. Thus expect a new front in the trade war once the 6 months is up

( zerohedge)

ii)Italy

Italy is a powder keg ready to explode. Italy’s debt to GDP has been relatively stable at 132% of GDP. However lately its economy has been moribund. Salvini wants to go into further debt to stimulate its economy from a deficit of 2.0% to 2.5% something that Brussels will not listen. Now Italian yields have jumped as Salvini is threatening to crash the government. If Italy leaves the EU then the entire European financial system implodes and it will probably take the world’s banks with them

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iran

USA troops are now to be based in Saudi Arabia and Qatar

( zerohedge)

ii)IRAN/USA

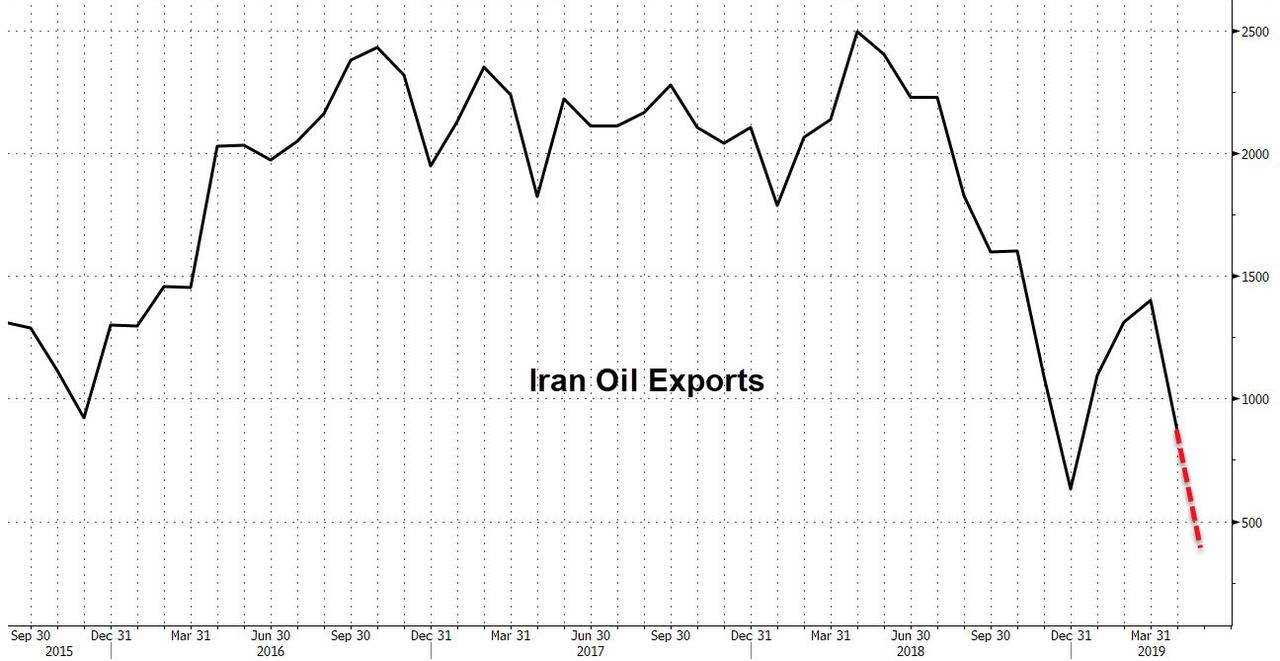

Trump is the big winner: Iran’s oil exports plunge to only 400,000 barrels per day in May

(Paraskova/OilPrice.com)

iii)TURKEY

iv)SERBIA/KOSOVO

For twenty plus years we have had peace between the tiny Republic of Kosovo and the Serbia. However Serbian troops are now on combat alert after Kosovo police raided a Serbian enclave in an anti smuggling mission. Serbia never recognized Kosovo

( zerohedge)

6. GLOBAL ISSUES

Brandon Smith is one smart cookie: here he continues with his theme on how the markets will crumble as the globalists pit themselves against the populists. He states that we are just one major event away from destruction. He outlines 3 powder kegs

a must read…

( Brandon Smith)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA/

9. PHYSICAL MARKETS

( Incrementum/GATA)

ii)Bloomberg wonders what if everybody is expelled from the USA financial system for aiding Iran etc

(Bloomberg gATA)

iii)Now it is the central bank of the Philippines that joins other central banks in hoarding gold

(Bloomberg/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

MARKET TRADING/Europe

ii)Market data

a)Trump is not to happy as his Q2 GDP has been lowered a notch in its first revision down to 3.1%

( zerohedge)

b)Housing is such an important part of the GDP calculations for the USA. Pending home sales suffer their worst decline in over 10 years

( zerohedge)

d)Today’s inflation report is something that Jerome Powell, of the Fed will look upon with much surprise and anger. The Fed uses archaic tools in its forecasting for inflation as they leave out the volatile food and energy hoping that it keeps inflation at around their supposed level of 2.0%. The problem is the fact that the economy is faltering terribly and now their revered figure of inflation is now down to 1% in the last quarter from 1.3% in the previous quarter. It will be difficult for Powell to raise rates again

( zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

SWAMP STORIES

It sure looks like Mueller lied to Barr. On 3 occasions Barr questioned Mueller on his report on the subject of obstruction. Mueller told Barr that his lack of charges on obstruction had nothing to the do with the opinion of the office of legal council whose long time policy is that you cannot indict a sitting president. It looks to me like he has lied

( zerohedge

Let us head over to the comex:

Gold withdrawals;

i) We had 0 withdrawals:

.

Heightened Political and Geopolitical Uncertainty Is Also Supporting Gold” – GoldCore

Gold and Silver Settle Higher, Buoyed by Global Stock-market Weakness

Gold Draws Support From U.S.-China Trade, Global Downturn Fears

Dollar Rises Amid U.S.-China Trade Worries

World Stocks Drop, Bonds Rally as Trade Tensions Fan Growth Fears

Bank of Canada Holds Rate at 1.75%, Says Economic Slowdown Likely Temporary

“Heightened Political and Geopolitical Uncertainty Is Also Supporting Gold” – Goldcore

Falling Interest Rates Are Sending a Warning Signal to the Stock Market

Shares of Rare Earth Miners Skyrocket After Beijing Threatens to Cut Off the Minerals

SWOT Analysis: Another Two Countries Want to Up Their Gold Intake

A Random Encounter In A Diner On Memorial Day Shows Exactly Where America Is Heading…

LBMA Gold Prices (USD, GBP & EUR – AM/ PM Fix)

29-May-19 1283.50 1281.65, 1016.02 1013.27 & 1151.04 1150.67

28-May-19 1283.90 1278.30, 1012.87 1008.20 & 1146.91 1142.29

27-May-19 Closed for UK Holiday

24-May-19 1281.50 1282.50, 1011.36 1011.89 & 1145.92 1145.40

23-May-19 1275.95 1283.65, 1009.79 1015.37 & 1146.19 1152.46

22-May-19 1274.00 1273.80, 1005.44 1008.09 & 1141.12 1141.20

21-May-19 1276.00 1271.15, 1004.85 998.62 & 1144.19 1139.84

20-May-19 1275.25 1276.85, 1000.05 1003.22 & 1142.63 1143.42

17-May-19 1285.80 1280.80, 1007.55 1005.17 & 1152.08 1146.70

16-May-19 1295.55 1291.70, 1009.62 1009.46 & 1155.76 1154.78

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

A great commentary on gold by Incrementum but they forget to include the manipulation

(courtesy Incrementum/GATA)

More great research by Incrementum — and all beside the point

Submitted by cpowell on Thu, 2019-05-30 01:37. Section: Daily Dispatches

9:39p ET Wednesday, May 29, 2019

Dear Friend of GATA and Gold:

Liechtenstein-based investment fund Incrementum’s annual “In Gold We Trust” report, compiled by Ronald-Peter Stoeferle and Mark J. Valek, was published this week and again described the reasons for gold’s glorious prospects. Among them:

— Loss of trust in international relations and everyday society amid ever-more-polarized politics.

— Gold’s generally good performance in most currencies apart from the U.S. dollar.

…

The extreme lows at which commodity prices generally now reside, implying a reversal.

— Increasing purchases by central banks.

But while the report mentions past currency market interventions by governments and central banks that have affected asset prices, there doesn’t seem to be anything in the report explaining why, despite the longstanding supportive fundamentals, gold has yet to realize its glorious prospects — why gold’s future never comes.

For example, there doesn’t seem to be anything in the report about the constant and surreptitious gold trading by the Bank for International Settlements on behalf of its member central banks, the discounts given to governments and central banks by CME Group for surreptitiously trading all major futures contracts in the United States, or the refusal of the U.S. Federal Reserve and Treasury Department to answer a congressman’s questions about which markets they are surreptitiously trading in and why.

All these developments have been extensively reported by GATA over the past year. It would seem hard for any gold market analyst to overlook them.

So while the Incrementum report is full of great research, analysis, and charts, it offers little insight about the thing that matters most: gold’s price and its primary determinant, intervention in the gold market by central banks, as lately summarized by GATA here:

http://www.gata.org/node/18979

When even gold’s scholars and mining companies are indifferent to the primary determinant of the monetary metal’s price, gold’s great future can seem only more distant.

Abbreviated and complete versions of Incrementum’s “In Gold We Trust” report can be found here:

https://ingoldwetrust.report/igwt/?lang=en

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Bloomberg wonders what if everybody is expelled from the USA financial system for aiding Iran etc

(Bloomberg gATA)

What if everybody got expelled from the U.S. financial system?

Submitted by cpowell on Thu, 2019-05-30 13:47. Section: Daily Dispatches

U.S. Warns Europe That Its Iran Workaround Could Face Sanctions

By Jonathan Stearns and Helene Fouquet

Bloomberg News

Wednesday, May 29, 2019

The Trump administration escalated its battle with European allies over the fate of the Iran nuclear accord, threatening penalties against the financial body created by Germany, the U.K., and France to shield trade with the Islamic Republic from U.S. sanctions.

Sigal Mandelker, the Treasury Department’s undersecretary for terrorism and financial intelligence, signaled in a May 7 letter obtained by Bloomberg that Instex, the European vehicle to sustain trade with Tehran, and anyone associated with it could be barred from the U.S. financial system if it goes into effect.

…

“I urge you to carefully consider the potential sanctions exposure of Instex,” Mandelker wrote in the letter to Instex President Per Fischer. “Engaging in activities that run afoul of U.S. sanctions can result in severe consequences, including a loss of access to the U.S. financial system.”

Germany, France, and the U.K. created Instex in January to allow companies to trade with Iran without the use of U.S. dollars or American banks — thus allowing them to get around wide-ranging U.S. sanctions that were imposed after the Trump administration abandoned the 2015 Iran nuclear deal last year. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-05-29/u-s-warns-europe-that…

END

Now it is the central bank of the Philippines that joins other central banks in hoarding gold

(Bloomberg/GATA)

Philippines joins gold rush by central banks

Submitted by cpowell on Thu, 2019-05-30 16:51. Section: Daily Dispatches

By Siegfrid Alegado and Ranjeetha Pakiam

Bloomberg News

Wednesday, May 29, 2019

The Philippines is joining a slew of central banks that are increasing gold holdings in foreign reserves.

Sales to Bangko Sentral ng Pilipinas could reach almost 1 million fine troy ounces a year from the current 20,000 to 30,000 ounces as a new law that exempts taxes on the monetary authority’s bullion purchases from small-scale miners takes effect, according to Deputy Governor Diwa Guinigundo.

…

The law seeks to remedy the 99-percent drop in the BSP’s domestic purchases from 2010, the central bank said after the legislation was released last week. While a previous law imposing taxes on gold sales to the central bank was enacted in 2008, it was enforced only in 2011 under an administration keen to plug revenue leaks to shore up funds for state coffers. …

“The percentage of gold in the central bank reserves of a few emerging markets is quite small, so some building up is natural,” said Georgette Boele, senior foreign-exchange and precious metals strategist at ABN Amro Bank NV. “Some countries buy up their own production to support the sector, while others have a more reserve diversification motive. In the case of the Philippines, its goal is to support local miners.” …

Small-scale producers are allowed to sell their gold only to the central bank, but they instead settled for lower prices on the black market to circumvent the taxes, Guinigundo said last week in a reply to questions from Bloomberg News.

The tax exemption was beneficial to both the miners and the BSP, which can continue buying gold with pesos, Guinigundo said. “If we use dollars to buy gold from the world market, it would simply involve a rebalance of the foreign-exchange reserve composition from dollars to gold.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-05-29/gold-rush-by-central-…

* * *

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

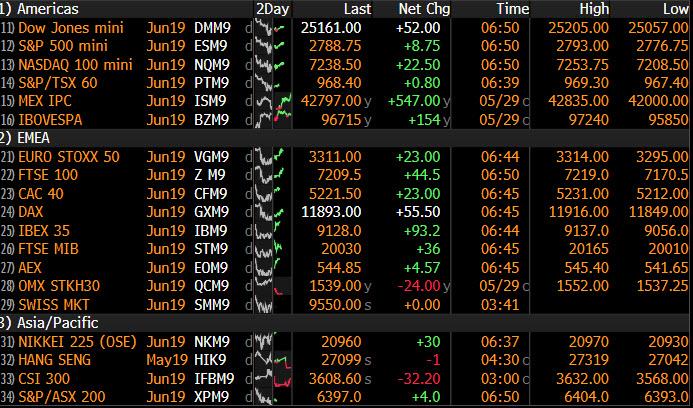

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9070/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9264 /shanghai bourse CLOSED DOWN 8.89 POINTS OR 0.31%

HANG SANG CLOSED DOWN 120,83 POINTS OR 0.44%

2. Nikkei closed DOWN 60.84 POINTS OR 0.29%

3. Europe stocks OPENED GREEN /

USA dollar index RISES TO 98.12/Euro RISES TO 1.1138

3b Japan 10 year bond yield: RISES TO. –.08/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.69/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 59.03 and Brent: 68.78

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.17%/Italian 10 yr bond yield DOWN to 2.61% /SPAIN 10 YR BOND YIELD DOWN TO 0.76%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.78: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.06

3k Gold at $1277.20 silver at: 14.41 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 1/100 in roubles/dollar) 64.96

3m oil into the 57 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.69 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0083 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1216 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.17%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.26% early this morning. Thirty year rate at 2.68%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8748..they are toast

Stocks Rebound Even As Traders Brace For “Long-Term Trade War”

US equity futures and global stocks rebounded on Thursday as traders took a break from selling stocks and pumping money into safe-haven bonds and the dollar, awaiting the latest headlines in the ongoing trade war.

With just two days left in what has so far been the most turbulent month of the year, investors are busy squaring up positions, shaken by a violent escalation in trade war which has left many traders dazed and confused and the S&P back under 2,800 but above its 200 day moving average for now.

US equity futures drifted higher in the overnight session, while Europe’s Stoxx 600 advanced, with tech among the biggest gainers, a day after posting its biggest drop in nearly three weeks. European stocks nudged 0.2%-0.5% higher having lost a third of the 15% gain they had been carrying into May, the major currencies paused, while German Bund yields climbed for the first time in four days having hit record lows.

Asian stocks were little changed, with MSCI’s index of Asia-Pacific shares ex-Japan slipping to a fresh four-month low before finding a bit of traction to edge up 0.1% into the close. Japan, Hong Kong and Shanghai falling while South Korean, Indian and Indonesian equities advanced as gains in the technology sector were offset by declines in health care and consumer staples. The Topix gauge fell 0.3% to its lowest level since January, led by Japan Communications Inc. and Avant Corp while the Nikkei slumped 0.5%. The Shanghai Composite Index dropped 0.3% after the PBOC’s latest liquidity injection was a sharp dip from Wednesday’s 250bn yuan, with China Life Insurance Co. contributing the most to the index decline.

Elsewhere in Asia, Australian stocks shed 0.85% as local miners suffered the worst month for copper prices since 2016 having slumped over 9%. Indian equities advanced for a fourth day in five amid continued optimism that Prime Minster Narendra Modi will adopt more policies to support economy.

As usual traders were focused on the war of trade, tech and words between Washington and Beijing. “We oppose a trade war but are not afraid of a trade war,” Chinese Vice Foreign Minister Zhang Hanhui said on Thursday in Beijing, when asked about the tensions with the United States. “This kind of deliberately provoking trade disputes is naked economic terrorism, economic chauvinism, economic bullying.”

“The equity markets are in the midst of pricing in a long-term trade war, with participants shaping their portfolios in anticipation of a protracted conflict,” said Soichiro Monji, senior strategist at Sumitomo Mitsui DS Asset Management.

“The upcoming G20 summit could provide the markets with relief, as the United States and China could use the event to begin negotiating again over trade,” he added, referring to the June 28-29 gathering of leaders in Japan.

In rates, the 10-year Treasury yield was at 2.27% after falling to a nearly two-year low of 2.21% Wednesday, with the 3M-10Y yield curve staying deep in inverted territory, most recently at -10bps.

“What’s going on in Treasury markets is ultimately a repricing of growth expectations,” JPMorgan’s John Bilton said on Bloomberg TV. “We don’t see a recession coming in the next 12 months even allowing for the yield-curve inversion we’ve seen, typically that’s a signal that has a long lead time.”

In FX, the dollar traded at a five-month high ahead of first-quarter revised GDP due later that could give clues on the direction of U.S. interest rates. The dollar was little changed at 109.68 yen after bouncing back from a two-week low of 109.150 and the euro steadied at $1.1132 following three successive days of losses. “The strength in the dollar is surprising given that markets are now expecting multiple rate cuts by 2020,” Commerzbank FX strategist Ulrich Leuchtmann said.

In commodities, oil prices rose modestly following volatile trading on Wednesday, when oil prices fell to near three-month lows at one point as trade war fears gripped the commodity markets. WTI futures were up 0.66% at $59.20 per barrel after brushing $56.88 the previous day, their lowest since March 12. Brent crude added 0.37% to $69.71 per barrel. Trade worries have weighed on oil but supply constraints linked to the Organization of the Petroleum Exporting Countries’ output cuts and political tensions in the Middle East have offered some support.

Market Snapshot

- S&P 500 futures up 0.4% to 2,790.50

- STOXX Europe 600 up 0.4% to 371.84

- MXAP down 0.09% to 152.43

- MXAPJ up 0.2% to 498.00

- Nikkei down 0.3% to 20,942.53

- Topix down 0.3% to 1,531.98

- Hang Seng Index down 0.4% to 27,114.88

- Shanghai Composite down 0.3% to 2,905.81

- Sensex up 0.9% to 39,853.99

- Australia S&P/ASX 200 down 0.7% to 6,392.13

- Kospi up 0.8% to 2,038.80

- German 10Y yield rose 1.9 bps to -0.16%

- Euro up 0.05% to $1.1137

- Italian 10Y yield fell 4.1 bps to 2.269%

- Spanish 10Y yield rose 0.9 bps to 0.742%

- Brent futures down 0.2% to $69.34/bbl

- Gold spot down 0.3% to $1,276.30

- U.S. Dollar Index little changed at 98.16

Top Overnight News from Bloomberg

- A succession of domestic dilemmas on both sides of the Atlantic threaten to frustrate efforts at a U.S.-EU trade pact before they’ve even begun. It’s been 10 months since talks have gone anywhere meaningful with European officials frustrated with a Trump administration that’s distracted by the breakdown in talks with China and also issues with Japan

- China’s grip on the global market for rare-earth metals gives it the ability to target American weaponry in its trade war with the U.S. Rare earths have been thrust into the spotlight by a series of media reports in China signaling Beijing is gearing up to use the minerals as a counter in its trade battle with Washington

- Ray Dalio, the billionaire founder of investment management firm Bridgewater Associates, said Wednesday that he viewed the U.S.-China conflict as more than a “trade war” and that increasing export controls would be a major escalation

- A second referendum is preferable to a general election to resolve Brexit, according to U.K.’s Chancellor of the Exchequer Philip Hammond. Candidates to succeed Theresa May are honing their pitches amid deep divisions over whether to leave the European Union without a deal in October

- Italy will tell the European Commission that any budget tightening this year would jeopardize a sluggish economic recovery, pushing back in its reply to a demand from Brussels to explain the nation’s increasing debt load, newspapers reported Thursday

- The U.K. will need interest-rate increases if Brexit goes ahead smoothly, according to Bank of England Deputy Governor Dave Ramsden. His comments echo those of BOE Governor Mark Carney, who spent much of his last press conference making the case for faster rate hikes than money markets imply

- Australia’s GDP growth will slow to a decade low despite cushioning provided by de-synchronized movements in house prices and commodity prices, Fitch Ratings says in a new report. Australia 1Q business investment falls the most since Sept. 2016

- The slump in global yields as investors seek out trade-war havens is increasing speculation in Tokyo that the Bank of Japan may cut bond purchases again in June. The central bank could lower the target purchase range for 10-25 year maturities in its monthly plan on Friday, according to Naomi Muguruma, senior market economist at Mitsubishi UFJ Morgan Stanley Securities

- Oil rebounded to climb back above $59 after the release of an industry report showing a much bigger than expected drop in U.S. crude stockpiles

- Israeli Prime Minister Benjamin Netanyahu failed to form a government by Wednesday’s deadline, opting instead for new elections that thrust both his future and the Trump administration’s peace plan into question

Asian equity markets mostly tracked the declines of their counterparts on Wall St where all majors extended on losses amid little in the way of catalysts to inspire a rebound and as participants looked ahead to upcoming US GDP and PCE inflation. Furthermore, trade uncertainty lingered, and technical selling was at play in which the DJIA briefly slipped below the 25K level and the S&P 500 tested its 200DMA to the downside. As such, ASX 200 (-0.7%) and Nikkei 225 (-0.3%) were subdued following the weak lead from their global peers with only the telecoms sector bucking the trend in Australia, while sentiment in Tokyo continued to be hampered as USD/JPY remained at a sub-110.00 level. Hang Seng (-0.4%) and Shanghai Comp. (-0.3%) were negative amid no signs of trade tensions abating as China’s Global Times Editor suggested US is shifting from protecting its interest to destroying China in its crackdown on Huawei. Finally, 10yr JGBs were lower as they tracked the pullback in T-notes but with downside stemmed by support around the 153.00 level and after improved results at the 2yr auction.

Top Asian News

- Sakurai’s Caution on Stimulus Signals Diverging Opinions at BOJ

- Short Seller Aandahl Targets China Apparel-Maker Anta Sports

- Anta Slumps Most in 15 Months as Blue Orca Recommends Short

- Singapore Minister Bats Away Criticism Over GIC, Temasek Pay

Major European Indices [Euro Stoxx 50 +0.5%] opened, and have remained, positive; diverting from the poor performance seen overnight in Asia-Pac indices which were largely subdued in sympathy with Wall St. As such, sectors are predominantly in the green with some outperformance in Energy names, although the sector has been weighed on by the recent sell off in oil prices, with Brent currently in negative territory. While the defensive utilities and healthcare sectors are underperforming given the broad risk-on sentiment this morning. In spite of the positivity across bourses, notable individual movers are sparse. Axel Springer (+21.3%) have moved substantially higher following reports that KKR are to make a bid to take the Co. private, with the Co. having been valued at EUR 4.9bln. Separately, Daily Mail & General Trust (+9.6%) have printed higher this morning post results, where they stated FY outlook is currently in-line with guidance. Also, post-earnings, but at the bottom of the Stoxx 600 are Johnson Matthey (-4.1%). Finally, Wirecard (1.3%) are at the top of the DAX (+0.6%) after announcing a strategic partnership with XBN relating to international e-commerce.

Top European News

- Italy Set to Warn Against Budget Tightening in Reply to EU

- U.K. Will Need Hikes If Brexit Goes Smoothly, BOE’s Ramsden Says

- ECB Seen Offering Generous Loans to Banks to Boost Feeble Growth

- Watches of Switzerland Gains After London Share Offering

In FX, the broad Dollar and the index trades relatively flat thus far, albeit still north of the 98.000 level, as participants await a barrage of tier 1 US data in the form of Q1 GDP (2nd estimate), Core PCE, advances goods trade balance and initial jobless claims. DXY fluctuated between a reasonable 98.08-24 band for now, ahead of some mild resistance around the 98.37-40 mark. US-China news-flow has consisted of MOFCOM reiterations wherein the Chinese noted that tariffs will not solve trade imbalance and will not accept a deal which hurts sovereignty and pride. Nonetheless, focus of today will remain on the aforementioned US data with expectations for the GDP figure to be revised marginally lower (3.1% vs. Prev. 3.2%) whilst the Core PCE Q1 prelim figure is expected to be unchanged at 1.3% (FOMC noted that the recent dip in PCE is transitory) and initial jobless claims are expected to tick slightly higher to 215k from 211k. Elsewhere, Citi’s month-end FX hedge rebalancing model indicates moderate buying of the USD at month end, with the signal (ex-USD/JPY) measuring just over +0.5 historical standard deviations across all crosses.

- AUD,NZD,CAD – A firmer risk appetite or perhaps some consolidation from yesterday’s decline sees the risk currencies on a firmer footing this morning. AUD/USD has shrugged off the dismal Building Approval figures overnight ahead of the much anticipated RBA meeting next week. UBS believes the AUD is “too short for its own good” heading into the weekend, adding that “only a complete equity meltdown could drive the Aussie lower at this stage”. In terms of technicals, AUD/USD trades within a relatively tight 0.6917-36 range ahead of resistance at 0.6940. Meanwhile, the Kiwi is largely moving in tandem with its Aussie counterpart after showing little reaction to the NZ budget, in which it sees the 2018/19 cash balance at -2.785bln vs. the Prev. forecast of -4.993bln. NZD/USD also remains within a tight range with the antipodeans eyeing Chinese NBS Manufacturing PMI following the aforementioned US data. Elsewhere, the Loonie nurses some of yesterday’s post-BOC loses, with the aid of rising oil prices amid a much wider than expected build in crude stocks reported by APIs last night. In terms of technical, USD/CAD hovers around the 1.3500 mark having moved in a 1.3493-3520 range, with support flagged at 1.3490. Looking ahead for the CAD, current account data is due at 1330BST whilst BoC’s Wilkins is due to give a speech around 1930BST.

- EUR,GBP – Little changed and trading mostly at the whim of the Greenback amid tentative newsflow. EUR/USD remains within a tight 20 pip range (1.1125-45) with support flagged at 1.1125 and 1.1105. In terms of upside, resistance levels are noted at 1.1155 ahead of 1.1170 (with 1bln in option expiries at strike 1.1175-85). Similarly, the Pound has done little on the day thus far and GBP/USD remains within a 1.2612-39 band with little new to report on the Brexit front. Meanwhile, EUR/GBP is currently flat on the day around within a 0.8810-25 with resistance around 0.8845-50.

- CHF,JPY – Both safe haven currencies are marginally weaker vs. the Buck amid the rebound in risk sentiment in early EU trade. USD/JPY remains above 109.50, having tested the level overnight, with resistance flatted at 109.80-85, whilst USD/CHF eyes 1.01 to the upside as it flirts around the top of today 1.0072-94 range.

- EM – Lira remains the outperformer amongst its EM counterpart as the US-Turkey does not seem to be detreating as (fast as) expected, following a phone call between the two President yesterday in which they agreed to meet on the side-lines of the G20 summit in June. USD/TRY is not back below the 6.00 figure and closer to 5.95, ahead of President Erdogan’s presentation of his judicial reform strategy programme at the presidential palace at 1200BST following by a meeting of the National Security Council at 1300BST.

In commodities, WTI (+0.3%) and Brent (-0.8%) futures are mixed with the former relatively flat whilst the latter has failed to hold onto its post-API gains in which US crude stocks showed a wider-than-forecast drawdown (-5.27mln vs. Exp. -0.9mln). This mornings downside in Brent was exacerbated as 69.0/bbl was taken out to the downside, with Brent currently trading around 68.80/bbl. News-flow for the complex has been light, although amidst the little clarity in regard to the OPEC/OPEC+ meeting schedule, the Azeri Energy Minister noted that the meeting will likely take place in early July (touted dates include July 3rd/4th). As a reminder, the DoEs will be release later today at 1600BST amid US’ market absence on Monday. Elsewhere, gold prices (-0.2%) are marginally pressured amid the improvement in the risk tone. Meanwhile, copper prices remain near 4-month lows due to a weak performance in China. Further for the red metal, supply side disruptions are to keep an eye on after Chile’s CODELCO mine workers voted in favour of a strike in the Chuquicamata mine which is the largest open-pit copper mine in the world.

US Event Calendar

- 8:30am: GDP Annualized QoQ, est. 3.0%, prior 3.2%; Personal Consumption, est. 1.2%, prior 1.2%; Core PCE QoQ, est. 1.3%, prior 1.3%

- 8:30am: Initial Jobless Claims, est. 214,000, prior 211,000; Continuing Claims, est. 1.66m, prior 1.68m

- 8:30am: Advance Goods Trade Balance, est. $72.7b deficit, prior $71.4b deficit

- 8:30am: Retail Inventories MoM, est. 0.2%, prior -0.3%; Wholesale Inventories MoM, est. 0.1%, prior -0.1%

- 9:45am: Bloomberg Consumer Comfort, prior 60.3

- 10am: Pending Home Sales MoM, est. 0.5%, prior 3.8%; NSA YoY, est. 0.1%, prior -3.2%

DB’s Jim Reid concludes the overnight wrap

Today sees the start of the cricket World Cup here in England. A massive event for a large part of the global population and a complete nonevent for an even bigger part of the global population. I’ve mentioned this before so apologies if you remember the story but the last time it was hosted in England 20 years ago I was on the brink of pop stardom as I sang on the Barmy Army’s (England’s supporters club) “Come on England” pop song. We were lined up to appear on all the major UK TV current affairs and pop shows the week of the release. I was extremely excited. However, the problem was we delayed the release of the single to the start of the knockout stages to ensure maximum publicity. The flaw in the plan that no-one considered at the time was that England might get knocked out in the group stages. Sadly they did, one day before the song was released and the knockout stages begun. So the wave of publicity shrivelled up and died just as record shops got their deliveries. In all fairness, it did shoot into the national charts that week at a very respectable no.45, which at least allows me to say I’ve sung on a top 50 single. For those who want to see the awful video, please feel free to see the link on my Bloomberg page header or email me and I’ll send it to you. I appear for a few frames throughout with the first glance at 22 seconds. It was a low budget affair with the theme being based on “goodies” versus “baddies” from history as that’s what the prop team had in their cupboard. The star turn was Faye from pop band Steps who was captain of the goodies from history for some reason. Joining her were the likes of Winston Churchill. On the baddies side Saddam Hussein was captain. It has a few celebrities in it but in reality it’s truly awful. Anyway good luck to England over the next 6 weeks!!

Unlike England in 1999, there’s no doubt that the global risk sell-off has gathered momentum this week but as we’ll see later risk assets did bounce off their lows after Europe went home last night. The next big event will be the latest Chinese PMI early tomorrow morning, which is expected to dip from 50.1 to 49.9 and below the psychologically important 50 level, which normally indicates contraction. In reality, the relationship isn’t quite that simple but there’s no doubt that recession fears are rising across markets. As for other imminent events to look out for, I was speaking to DB’s man in Washington (Frank Kelly) last night and he pointed out that US VP Pence will give a very important speech on US-China relations on Tuesday (June 4th), which is the 30th anniversary of the Tiananmen Square incident. Frank was of the opinion that it could be pretty hawkish given the signs out of Washington and his previous speeches on the matter. So watch this space.

Back to the recession fears and two of the Fed’s preferred yield curve measures – the 3m10y and 18m3m 3m – hit new lows yesterday at -9.5bps (-1.1bps on the day) and -50.1bps (-7.6bps), respectively. Both have now eclipsed their March lows and in fact you have to go back to the depths of the financial crisis to find the last time they were lower. A quick look at our screens now shows that all measures of 3m, 6m and 1y curves from 1y to 10y are inverted. The 2y curve is inverted at 3y and 5y but marginally positive at 2y7y (at 5.1bps) while the closely followed 2y10y is at 15.2bps and in fact was marginally steeper on the day yesterday (+1.4bps). This still remains our favourite recession indicator as we discussed in our “Yield Curve 101” note here . Indeed ahead of the last 9 recessions, this measure of the curve has always inverted beforehand with the earliest inversion to recession timing being 8 months and the average being nearer 12-18 months. As mentioned in our spread forecasts update, I think we still have a minimum of 12 months left in this US cycle (outside of a complete and sudden meltdown in global trade) but my confidence of an extended cycle beyond that is low given we’re close to an inversion and with other indicators we have previously discussed suggesting we are quite late cycle. So my views of a sell-off this summer are trade oriented at the moment rather than end of cycle oriented. However, the economic worries are building.

The broad curve flattening (with the exception of 2y10y) came despite fairly small eventual moves in cash treasuries, where the 10-year yield fell -0.5bps and the 2-year yield fell -1.8bps. That still took the 10-year to a new 20-month low, but it was well off the intraday trough of being -5.8bps on the day. Bunds also hit -0.1797% intraday yesterday – before closing at -0.1788% – and as a reminder the low mark back in July 2016 was -0.189%. So we’re only a sneeze away from those levels now. The rest of the European sovereign market rallied as well,including -4.2bps rally for BTPs despite the risk-off, and a -6.8bps rally in Portugal. The S&P 500 (-0.69%), DOW (-0.87%) and NASDAQ (-0.79%) all ended in the red, though they all rallied off their lows. Counterintuitively, cyclical sectors, including materials, financials, and industrials, actually outperformed, with losses instead concentrated in defensives and real estate. In Europe, the STOXX 600 (-1.43%) had its worst day in nearly 3 weeks – albeit partly as a result of playing catch up to the moves in the US late Tuesday. The move in rates also saw European Banks fall -1.56%, which puts them down now -15.77% from the April highs. For comparison, US Banks are down -7.60% from the recent highs. Meanwhile, the VIX rose +0.4pts to 17.87 yesterday, while EM FX and equities ended up +0.21% and +0.65%, respectively.

WTI oil prices initially fell as much as -3.82% before rallying back as investors first digested the news that Russia is pushing back against holding an OPEC+ meeting on June 25-26, pushing instead for July 3-4. This seemingly routine discussion has been interpreted by some as a tacit signal that Russia does not want to renew the December 2018 supply agreement. However, prices bounced back to end the day only -0.6% lower and are up +0.7% in Asia after a bigger fall than expected in US inventories.

This morning in Asia markets are trading on the softer side with the Nikkei (-0.85%), Hang Seng (-0.28%) and Shanghai Comp (-0.83%) all lower while the Kospi (+0.33%) is up. Elsewhere, futures on the S&P 500 are up +0.18% continuing a little of the late rally back from last night. In other news, negative rhetoric around the US-China trade war continues with China’s Vice Minister of Foreign Affairs Zhang Hanhui saying at a briefing today that deliberately provoking trade disputes is economic terrorism, economic hegemony and economic chauvinism. Note that it’s Ascension Day across parts of Europe today so there will be some countries out on holiday.

Back to yesterday and in truth there wasn’t a great deal of new news. The price action more appeared to reflect some of the fallout from recent reports of China potentially cutting exports of rare earth materials, adding to the long line of evidence that de-escalation is no nearer. The move below 2,800 on the S&P 500 was also seen as an important technical break at the same time as curves flattened. Meanwhile, Bloomberg reported that the US had warned Europe that its Iran ‘workaround’ could face sanctions. Elsewhere, it’s worth noting that yesterday’s BoC meeting – while not hugely interesting – was the first G7 central bank meeting since the recent trade escalation period. However, the comments on trade were fairly balanced, with the BoC noting that “the recent escalation of trade conflicts is heightening uncertainty about economic prospects. In addition, trade restrictions introduced by China are having direct effects on Canadian exports. In contrast, the removal of steel and aluminum tariffs and increasing prospects for the ratification of CUSMA will have positive implications for Canadian exports and investment.”

Turning to US politics, where attention was dominated by Special Counsel Robert Mueller’s first public comments in almost two years. He said that “under long-standing department policy, a president cannot be charged with a federal crime while he is in office,” though “if we had had confidence that the president clearly did not commit a crime, we would have said so.” President Trump greeted the remarks by tweeting “Nothing changes from the Mueller Report (…) The case is closed!” On the other hand, leading Democratic Presidential candidate Joe Biden said via a spokesman that impeachment “may be unavoidable.” It is likely that this drama will continue to linger over the coming months.

In European politics, the EU Commission formally sent Italy a letter confirming that the country risks disciplinary action unless it takes remedial actions. This was a legal requirement under the EU’s governing treaties, and Italy now has two days to respond. The more interesting item to watch will be Italy’s 2020 budget, due by end of September, which could include fiscally costly items like the flat tax and no VAT, which is more likely to spark a substantive confrontation with the Commission.

In other news, it was a quiet day for data yesterday with the only release in the US being the Richmond Fed manufacturing index, which rose +2pts to 5 in May, albeit below expectations for a 7 reading. That’s unlikely to move the dial much for expectations for next week’s ISM print. Prior to this in Europe we saw the May CPI reading in France rise only +0.2% mom (vs. +0.3% expected) while unemployment in Germany in May unexpectedly rose one-tenth to 5.0%. That’s the first time unemployment has ticked higher since November 2013; however, it appeared to be mostly down to a technical reclassification. Swedish GDP printed at 0.6% qoq, compared with expectations for 0.2%, but the details of the report showed a deterioration in consumption and investment, with the outperformance driven almost entirely by net exports.

Looking ahead to the rest of today, we’ll have to wait until this afternoon for the main data highlights with the second reading of Q1 GDP due in the US. Following a stronger than expected +3.2% qoq saar preliminary reading, the consensus expects a small downward revision to +3.0%; however, our economists note that in light of last week’s downward revisions to core durable goods orders and the latest quarterly services survey, it is possible that Q1 growth slips below 3%. Also due out this afternoon will be the latest claims reading, April advance goods trade balance, April retail and wholesale inventories and April pending home sales. Away from that, we’re due to hear from Fed Vice Chair Clarida at 5pm BST when he speaks to the economic club of New York, while US Secretary of State Pompeo is due to travel to meet German Chancellor Merkel in Berlin.

3. ASIAN AFFAIRS

)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 43.77 POINTS OR 0.67% //Hang Sang CLOSED DOWN 155.10 POINTS OR 0.57% /The Nikkei closed DOWN 256.77 POINTS OR 1.21%//Australia’s all ordinaires CLOSED DOWN 0.67%

/Chinese yuan (ONSHORE) closed DOWN at 6.9091 /Oil DOWN TO 57,28 dollars per barrel for WTI and 68.41 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9091 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9273 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China halts its “goodwill” gesture soybean purchases from the uSA

(courtesy zerohedge)

In Latest Trade-War Salvo, China Halts ‘Goodwill’ Soybean Purchases

The money from President Trump’s second farm bailout can’t be disbursed quickly enough.

Trump’s farm-state supporters have already been struggling with a dip in agriculture exports to China, which has exacerbated the low commodity prices that have pushed thousands of American farmers to the brink of bankruptcy. America’s farmers are extremely vulnerable right now, which is probably why Beijing has opted for this latest precision strike in the trade conflict: Bloomberg reports that China’s largest state-run grain buyers have been instructed to halt the ‘goodwill’ purchases of American soybeans as Beijing ratchets up the pressure on the White House, which could soon approve new tariffs on $300 billion of Chinese imports.

Thanks to February’s pledge to buy another 10 million tons of American soybeans, sales to Chinese grain buyers by American soybean farmers started to recover during the opening months of 2019. Since President Trump and Xi called the trade-war truce back in December, China has bought some 13 million tons of soybeans from American farmers. Data from the Department of Agriculture show that China’s grain buyers have yet to take delivery on about 7 million tons of US soybeans that it has committed to buying.

The timing of Beijing’s latest blow is notable: Friday marked the conclusion of a two-week tariff ‘grace period’ (since the higher rates didn’t apply to goods already in transit, analysts speculated that the two sides would have roughly two weeks to find a resolution before the new levies were actually imposed), which suggests that more retaliation from Beijing could be in the offing.

Last night, Washington imposed preliminary anti-dumping tariffs on Chinese mattresses and beer kegs (the keg tariffs will also impact Mexico and Germany), though a final decision isn’t expected until October.

As it ratchets up the pressure on the administration with one hand, Beijing is trying appeal to potentially sympathetic voices with the other by reportedly asking state media organizations to soften their criticism of the US in the hopes of keeping open the possibility that tensions with Washington could ease.

“We have been told not to use ‘the US side’ generally in our copy because there are many different voices within the US,” one unidentified official reportedly told the SCMP.

At the same time, Beijing is keeping up its threats about a possible rare earth export ban, much to the chagrin of the American defense and tech industries. Ministry of Commerce Spokesman Gao Feng said Thursday during a regular press briefing that China can’t accept its rare earth metals being used against itself, though it remains willing to meet other countries’ demands for the metals. Gao added that China will fight “until the end” if the US continues to escalate the trade fight, adding that China won’t tolerate US bullying.

4/EUROPEAN AFFAIRS

i)GERMANY/FRANCE/REST OF EUROPE VS USA

Trump gave a 6 month reprieve to Europe so that a deal could be arranged between Europe and the USA. You will recall that the EU is notorious for its high tariffs especially in autos

Trump has demanded the EU to lower tariffs equal to the uSA, something that the stubborn EU will not do. Thus expect a new front in the trade war once the 6 months is up

(courtesy zerohedge)

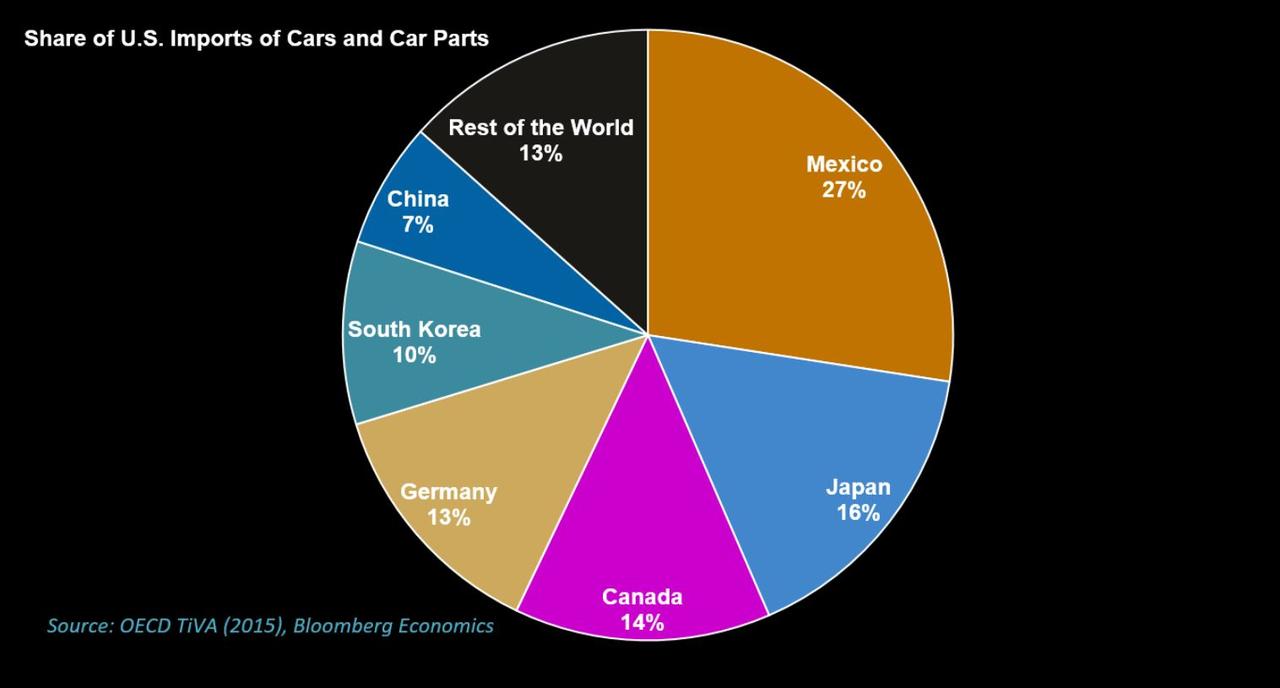

Trump Risks New Front In Trade War As Talks With Europe Falter

Two months ago, analysts at Bank of America proclaimed that “spring is coming” for the European economy after it slipped into a mild recession late last year. Unfortunately, a massive stimulus injection from Beijing has failed to spark a global reflationary wave, and on Wednesday, Germany – the largest and most important constituent of the European economy – revealed that its labor market had hit a major pothole, the latest sign that the economic pain on the Continent may have only just begun.

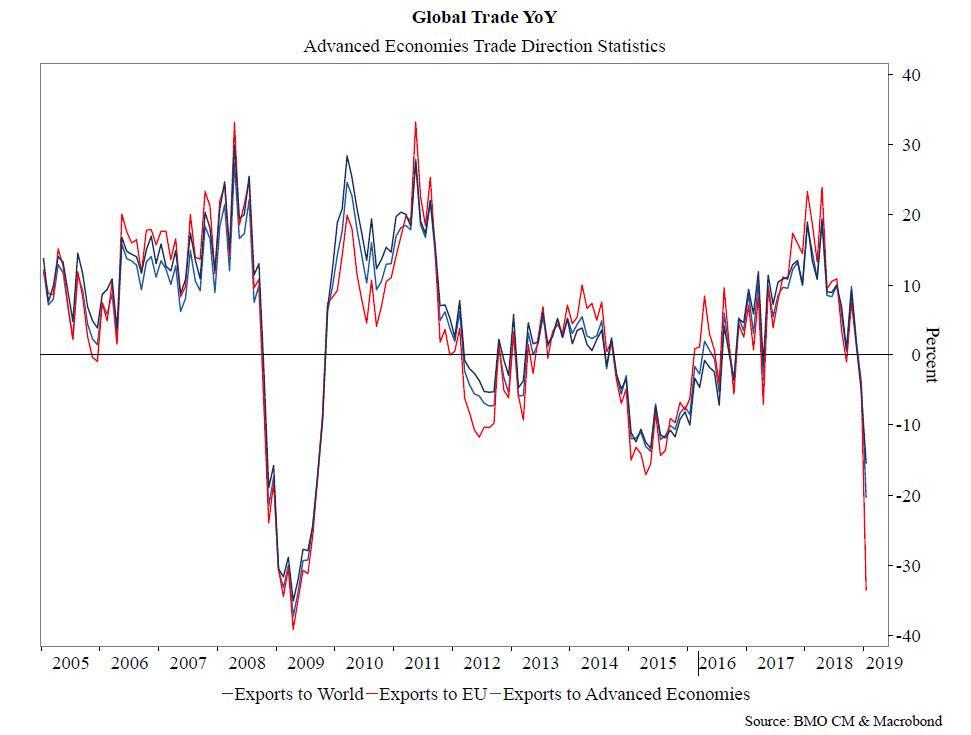

With global trade in free fall…

…And with slumping sales already weighing on the global auto industry, a critical engine (no pun intended) of Europe’s industrial economy, EU bureaucrats now find themselves in the uncomfortable position: They’re at the mercy of Washington and President Trump, who has been threatening to open up another front in his trade war by slapping ‘Section 232″ national security tariffs on imports of cars and car parts (with exceptions for USMCA partners Canada and Mexico).

But ironically, President Trump’s decision to delay his decision by six months to allow more time for negotiations with Europe and Japan might not make much of a difference: Because, with a leadership change coming in October, Brexit still unresolved and a strong showing by populist parties in the EU Parliamentary vote, Europe simply isn’t in a good position to negotiate

“You’re seeing an EU that is fighting fires on so many fronts that I just don’t think they are going to be confident and able to negotiate that deal” with the U.S., said Heather Conley, head of the Europe program at the Center for Strategic and International Studies.

As Bloomberg explains, Trump’s auto-tariff deadline will hit just as the new European Commission takes over from the body led by Jean Claude Juncker, who successfully negotiated a trade truce with Trump last year during a meeting at the White House. With the current Commission now entering a lame duck phase, its mandate to negotiate will be severely weakened.

Adding another layer of complication, France and Germany have competing priorities that could make it more difficult to reach a final deal.

France’s Emmanuel Macron led some EU member states in resisting U.S. efforts to include agriculture in any transatlantic discussions, something the EU insists Trump gave away last July as part of the Rose Garden truce. Though many in Washington, including Senate Finance Committee Chairman Chuck Grassley, have said any deal that didn’t include agriculture wouldn’t get through Congress.

Germany, which exported 27.2 billion euros of cars and car parts in 2018, is more concerned about Trump’s threat of automobile tariffs than protecting European agricultural interests. The home of Mercedes-Benz, BMW and Porsche generated a surplus of 22 billion euros in automotive trade with U.S. last year.

In a discouraging sign of things to come, trade talks in Washington and Paris this month made little progress, which leaves more muddling or a sharp escalation as the most likely paths.

Brussels’ best hope for averting more tariffs would be Trump’s decision to risk angering auto workers in South Carolina and other key states by moving ahead with the auto tariffs, which American car makers like GM and Ford vehemently oppose.

But as the market fallout from the China trade spat has showed, Trump has increased tolerance for painful decisions. So that’s hardly something Europe can bank on.

ii)Italy

Italy is a powder keg ready to explode. Italy’s debt to GDP has been relatively stable at 132% of GDP. However lately its economy has been moribund. Salvini wants to go into further debt to stimulate its economy from a deficit of 2.0% to 2.5% something that Brussels will not listen. Now Italian yields have jumped as Salvini is threatening to crash the government. If Italy leaves the EU then the entire European financial system implodes and it will probably take the world’s banks with them

(courtesy zerohedge)

Italian Yields Jump As Salvini Threatens To Crash Government

Clearly emboldened by the EU Parliamentary results, where the League won a plurality of the vote in Italy, Matteo Salvini on Thursday sent BTP yields higher by threatening to crash the Italian government if the Five Star Movement doesn’t back his tax-cut plan.

BTP yields have been moving higher over the past two weeks as Salvini has brushed off Europe’s threats to fine Italy up to €4 billion over its refusal to rein in its debt and deficit-spending plans. This would be the first time the European Commission has fined a member state over violations of its fiscal rules.

But Salvini, who is now indisputably the most powerful political figure in Italy, isn’t backing down. He has remained defiant, even as Italy braces for the EU to initiate another excessive debt proceeding on Wednesday, when reviews of member states’ fiscal compliance are expected.

As the Telegraph’s Ambrose Evans-Pritchard pointed out in a column yesterday, Salvini has revived threats to initiate an Italian parallel currency – the so-called “mini-BOT” Italian Treasury bills that a Forbes columnist once warned was the “biggest threat to the future of the eurozone.”

And with Salvini adding to the political chaos by taking the first tentative steps toward ousting Five Star from the ruling coalition, Italian bond holders will have only themselves to blame if they don’t anticipate more market-rattling political chaos, and position accordingly.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

Iran

USA troops are now to be based in Saudi Arabia and Qatar

(courtesy zerohedge)

US Troops To Be Based In Saudi Arabia, Qatar Against “Iran Threat”

Just hours after US National Security Advisor John Bolton formally accused Tehran of conducing the May 12 tanker “sabotage” attacks near the Strait of Hormuz, Iran’s foreign ministry has responded that “we are ready for war” amid fears that Washington could still be on a war footing in the Persian Gulf.

“We hope that we can start a dialogue, but we are ready for war,” Deputy Foreign Minister Abbas Araqchi told RIA Novosti.

Bolton had told a press conference earlier in the day in Dubai, “The point is to make it very clear to Iran and its surrogates that these kinds of actions risk a very strong response from the United States.”