GOLD: $1305.80 UP $17.10 (COMEX TO COMEX CLOSING)

Silver: $14.59 UP 6 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1305.25

silver: $14.59

QUITE A WEEK!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 16/58

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,287.100000000 USD

INTENT DATE: 05/30/2019 DELIVERY DATE: 06/03/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 26

363 C WELLS FARGO SEC 6

657 C MORGAN STANLEY 8

661 C JP MORGAN 13

661 H JP MORGAN 3

686 C INTL FCSTONE 4 1

690 C ABN AMRO 4

709 C BARCLAYS 2

737 C ADVANTAGE 32 1

800 C MAREX SPEC 2

905 C ADM 14

____________________________________________________________________________________________

TOTAL: 58 58

MONTH TO DATE: 58

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 58 NOTICE(S) FOR 5800 OZ (0.1804 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 58 NOTICES FOR 5800 OZ (.1804 TONNES)

SILVER

FOR MAY

216 NOTICE(S) FILED TODAY FOR 1,080,000 OZ/

total number of notices filed so far this month: 216 for 1080,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ N/A

Bitcoin: FINAL EVENING TRADE: $ N/A

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A SMALL SIZED 961 CONTRACTS FROM 213,540 DOWN TO 212,579 DESPITE THE 19 CENT GAIN IN SILVER PRICING AT THE COMEX. LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER BUT IT NOW IN FULL FORCE FOR GOLD. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 595 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 595 CONTRACTS. WITH THE TRANSFER OF 595 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 595 EFP CONTRACTS TRANSLATES INTO 2.95 MILLION OZ ACCOMPANYING:

1.THE 19 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.260 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

27,309 CONTRACTS (FOR 22 TRADING DAYS TOTAL 27,309 CONTRACTS) OR 136.55 MILLION OZ: (AVERAGE PER DAY: 1241 CONTRACTS OR 6.207 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 136.55 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.50% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 892.11 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 961 DESPITE THE 19 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A VERY SMALL SIZED EFP ISSUANCE OF 595 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE LOST A SMALL SIZED: 366 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 595 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 961 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 19 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.64 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.064 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 216 NOTICE(S) FOR 1,080,000, OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.260 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY ANOTHER UNBELIEVABLE SIZED 10,944 CONTRACTS, TO 443,231 DESPITE THE $6.40 PRICE GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY/THE SPREADING LIQUIDATION STILL CONTINUED TODAY.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8499 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 8499 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 443,231. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A CONSIDERABLE SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2445 CONTRACTS: 10,944 OI CONTRACTS DECREASED AT THE COMEX AND 8499 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 2445 CONTRACTS OR 244,500 OZ OR 7.6 TONNES. YESTERDAY WE HAD A GOOD GAIN OF $6.40 IN GOLD TRADING….AND WITH THAT GAIN IN PRICE, WE HAD A CONSIDERABLE LOSS OF GOLD TONNAGE OF 7.6 TONNES!!!!!!

WITH RESPECT TO SPREADING: WE HAD STILL CONSIDERABLE LIQUIDATION OF THE SPREADERS TODAY

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS HAVE NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 144,386 CONTRACTS OR 14,438,600 OR 449.10 TONNES (22 TRADING DAYS AND THUS AVERAGING: 6563 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22 TRADING DAYS IN TONNES: 449.10 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 449.10/3550 x 100% TONNES =11.89% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2277,92 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: ANOTHER UNBELIEVABLE SIZED DECREASE IN OI AT THE COMEX OF 10,944 DESPITE THE PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY(6.40)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8499 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8499 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED LOSS OF 2455 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8499 CONTRACTS MOVE TO LONDON AND 10,944 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 7.6 TONNES). ..AND THIS LOSS OF DEMAND OCCURRED WITH THE RISE IN PRICE OF $6.40 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD A STRONG PRESENCE OF SPREADING LIQUIDATION TODAY/

we had: 58 notice(s) filed upon for 5800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $17.10 TODAY//SEEMS THE BOYS FOUND RELIGION

A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A HUGE “PAPER” GOLD DEPOSIT OF 3.52 TONNES

INVENTORY RESTS AT 740.86 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 6 CENTS TODAY:

A BIG CHANGE IN SILVER INVENTORY AT THE SLV:

A DEPOSIT OF 422,000 OZ INTO THE SLV

/INVENTORY RESTS AT 312.038 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY AN SMALL SIZED 961 CONTRACTS from 213,540 DOWN TO 212,579 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER BUT HAVE NOW MORPHED INTO GOLD..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 595 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 595 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 961 CONTRACTS TO THE 595 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 366 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 1.83MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 1.260 MILLION OZ FOR JUNE.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 19 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 595 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

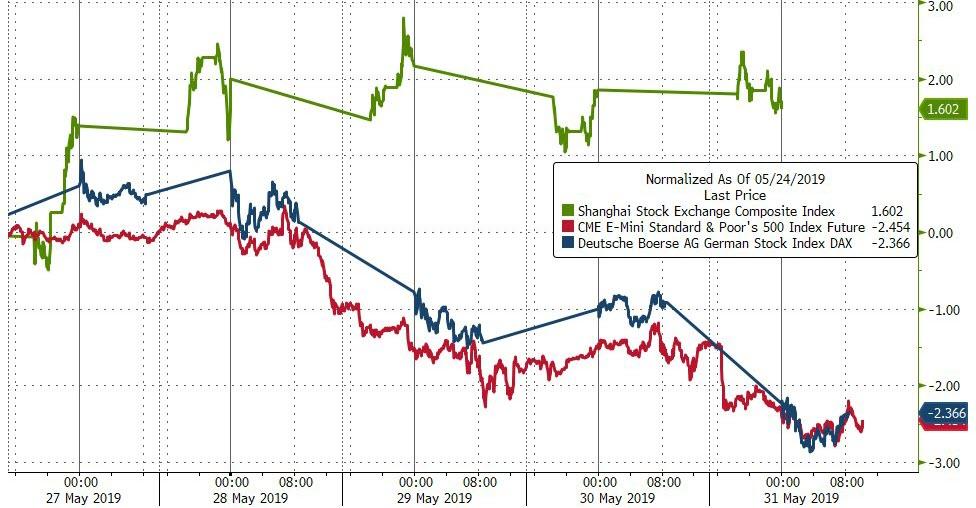

SHANGHAI CLOSED DOWN 7.11 POINTS OR 0.24% //Hang Sang CLOSED DOWN 213.79 POINTS OR 0.79% /The Nikkei closed DOWN 341.34 POINTS OR 1.63%//Australia’s all ordinaires CLOSED UP 0.04%

/Chinese yuan (ONSHORE) closed DOWN at 6.9097 /Oil DOWN TO 57,28 dollars per barrel for WTI and 68.41 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9097 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9437 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)The bond markets are correct: the trade war is taking a huge bit out of China manufacturing as its PMI tumbles back into

contraction mode

( zerohedge)

4/EUROPEAN AFFAIRS

i)EUROPE/

Countries are continuing to shun the USA , which is not good for USA hegemony

a very important commentary from Tom Luongo

( Tom Luongo)

ii)FRANCE

iv)Late this morning: right on cue..Italy says what the EU wants to hear..but do they mean it?

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iraq

An explosion rips through the oil city of Kirkuk in the Kurdistan region of Iraq

( zerohedge)

ii)IRAN/USA

( zerohedge)

iii)RUSSIA/TURKEY

( AlmasdairNews)

6. GLOBAL ISSUES

i)This is the reason for stock markets around the world collapsing: Trump unleashes tariffs on Mexico for allowing illegal immigration through its borders. He has initiated firstly a 5% rate and that will increase until they get their act together.

( zerohedge)

ii)seems Mnuchin and Lighthizer reportedly opposed trump’s Mexico tariffs because they felt it would hinder their New NAFTA no2 dea

(courtesy zerohedge)

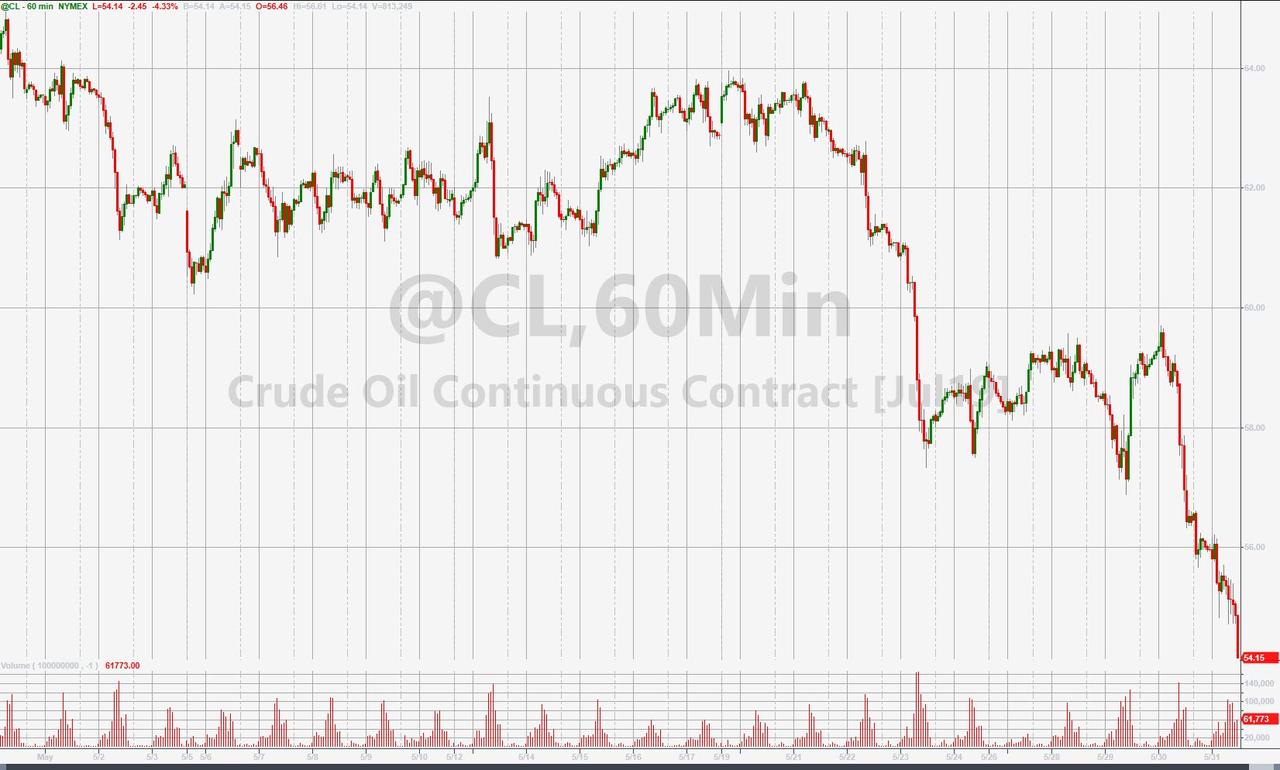

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA/

Another good look at Venezuela where the cost of bullets are too expensive even for the criminals. Nothing pays in Venezuela, even crime

( Mac Slavo)

9. PHYSICAL MARKETS

Two commentaries

(Reuters/GATA)

ii)Judy Shelton is without a doubt the right pick for Trump. Let us hope that she gets the job of Fed governor. She is a strong advocate for gold backed currency and less dependency on the Fed.

( London’s Financial Times/Judy Shelton/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Last night, after the bell:

Pence warns that the uSA can double tariffs..bond yields tumble.

b)10 yr yield at 1 am est:

ii)Market data

a)As we pointed out to you yesterday, Trump is not winning in the trade battle. Last night imports fell by 2.7% and imports a drop of 4.0%

This caused the trade deficit to rise despite the tariffs. Remember the words of Alasdair Macleod..unless the USA saves, the trade deficit will continue to rise

He is right…

( Mish Shedlock/Mishtalk)

b)As we pointed out to you yesterday, Trump is not winning in the trade battle. Last night imports fell by 2.7% and imports a drop of 4.0%

This caused the trade deficit to rise despite the tariffs. Remember the words of Alasdair Macleod..unless the USA saves, the trade deficit will continue to rise

He is right…

( Mish Shedlock/Mishtalk)

iii)USA ECONOMIC/GENERAL STORIES

Trump approval rating hits a two year high:

( zerohedge)

SWAMP STORIES

Barr strikes back on Mueller and stated that he should have reached a decision on obstruction if he wanted to. He also stated that 3 times Mueller told Barr that his decision is not based on the

Office of Council’s opinion that you cannot indict a sitting president.

( zerohedge)

Let us head over to the comex:

Gold withdrawals;

i) We had 0 withdrawals:

.

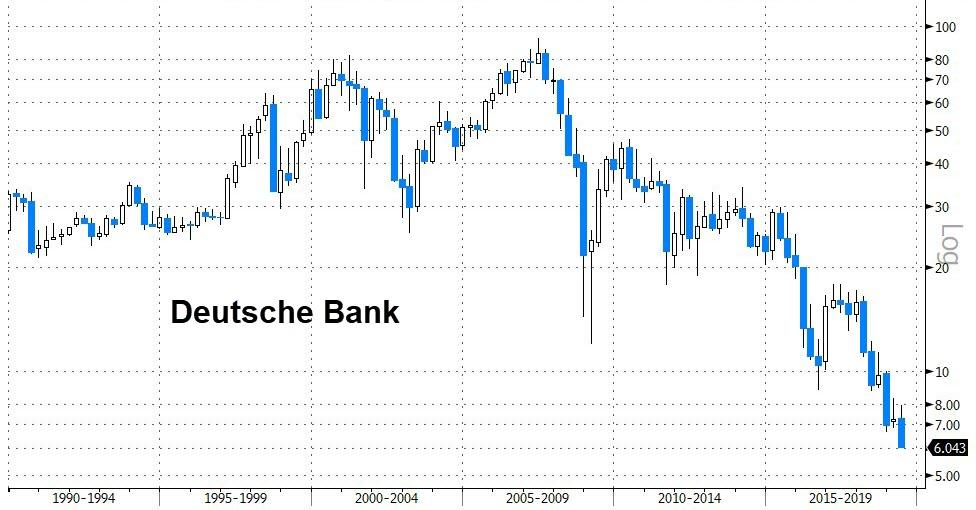

Gold Sees Safe Haven Gains As Stocks Fall Sharply and Deutsche Plummets

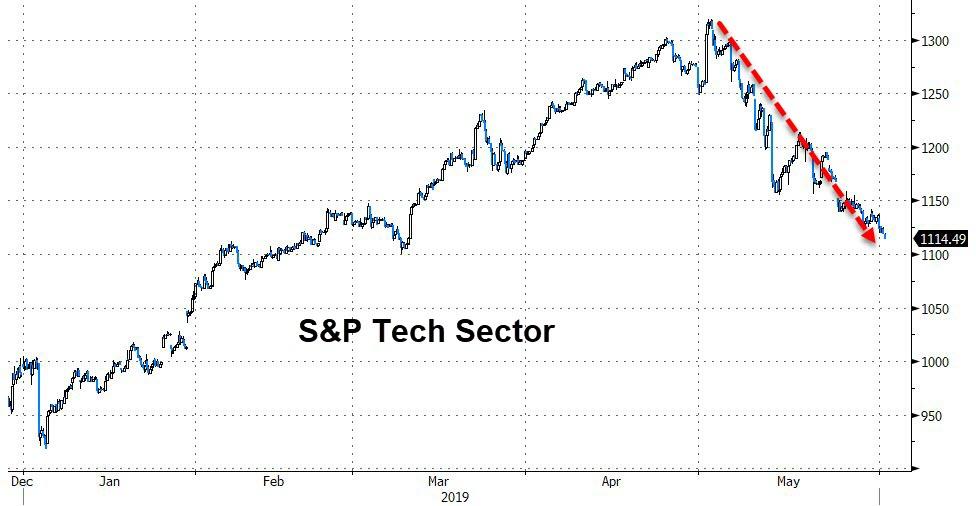

Gold rose to a two week high and was higher in most currencies today after Washington’s threat of tariffs on Mexico exacerbated fears of a global trade war and recession, which saw a ‘flight to quality’ and gains for safe haven gold.

Spot gold jumped 0.9% to $1,298.80 an ounce this morning, its highest since May 15. Gold bullion has risen over 1.2% this month and appears headed for its first monthly gain in four months. This is important from a technical perspective and the fundamentals of growing risk aversion and robust demand should lead to further gains in June.

European trading has seen a clear flight to quality after President Trump unexpectedly politicised tariffs by slapping 5% on all goods coming from Mexico.

The increasingly hopeless case of a U.S. and China trade deal looked even further away after China drew up an “Unreliable entities” list of foreign parties (presumably mostly U.S.) that harm Chinese firms.

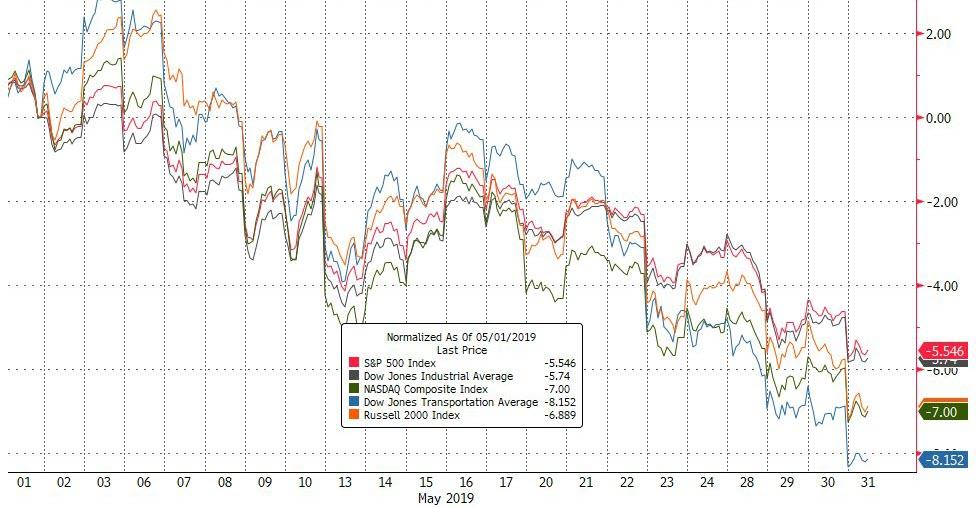

Stocks are red across the board globally with the S&P 500 breaking down sharply below its 200 day moving average (DMA). 2776 is a key level and Wall Street and Wasshington will not want a close below this level. Market intervention is quite possible, if not likely.

A weekly close below the 200 day moving average (DMA) could lead to follow through selling on Monday which could get ugly given the economic backdrop.

Financial stocks are particularly under pressure including UBS and embattled Deutsche Bank with the latter posting new “all time” lows of around €6. A whiff of contagion is in the air.

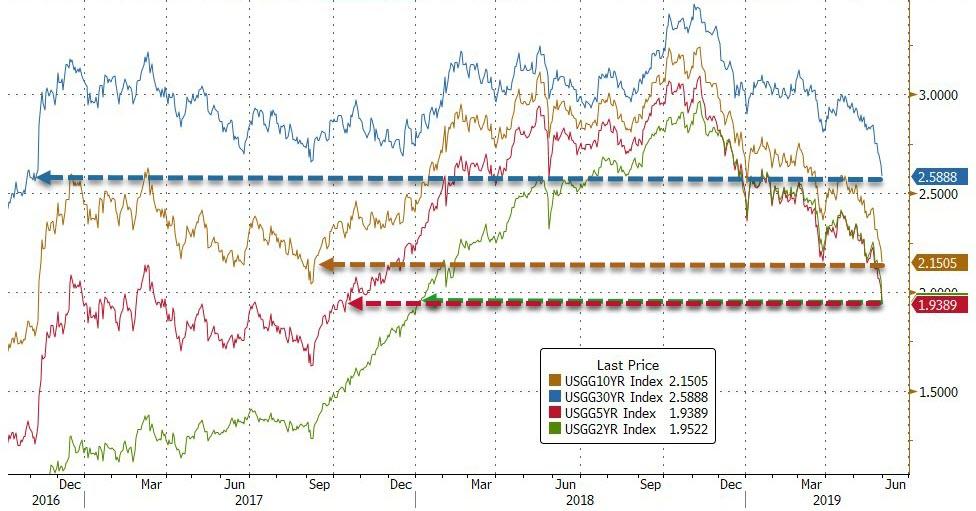

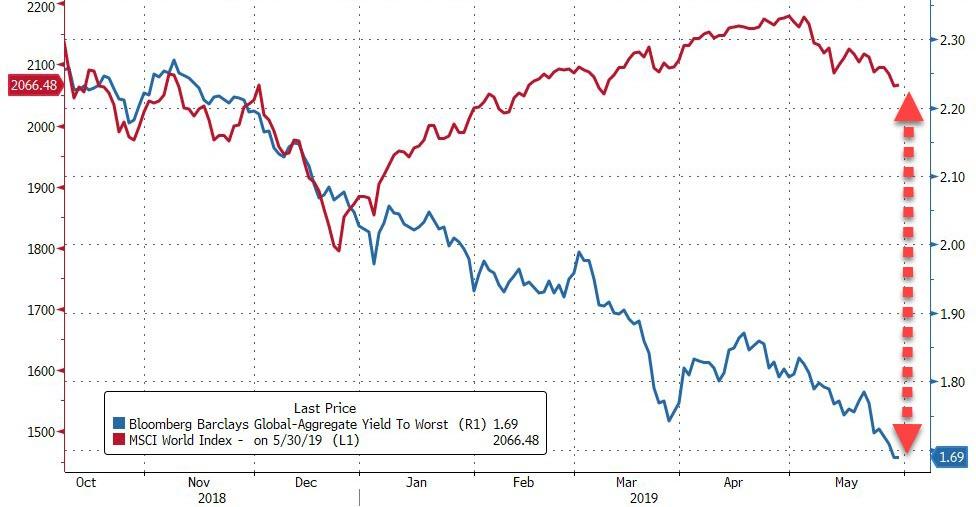

US and German bond yields hitting recent lows indicate the Fed might be backed into a rate cut sooner than they have been guiding with an inverting yield curve being a good barometer of trouble ahead

The greenback has also benefited somewhat from the risk off trade, in the face of this, silver and particularly gold are holding up well despite the recent sell off.

$1,300/oz and $14.60/oz are the respective hurdles approaching for both. Weekly closes over these levels should see follow though buying and further gains.

How far down we go, nobody knows, but it makes sense to stay cautious and prepared.

Fasten your seat belts it could be a lively Friday afternoon and weekend…

LBMA Gold Prices (USD, GBP & EUR – AM/ PM Fix)

30-May-19 1276.45 1280.95, 1010.44 1015.92 & 1146.25 1151.70

29-May-19 1283.50 1281.65, 1016.02 1013.27 & 1151.04 1150.67

28-May-19 1283.90 1278.30, 1012.87 1008.20 & 1146.91 1142.29

27-May-19 UK Bank Holiday

24-May-19 1281.50 1282.50, 1011.36 1011.89 & 1145.92 1145.40

23-May-19 1275.95 1283.65, 1009.79 1015.37 & 1146.19 1152.46

22-May-19 1274.00 1273.80, 1005.44 1008.09 & 1141.12 1141.20

21-May-19 1276.00 1271.15, 1004.85 998.62 & 1144.19 1139.84

20-May-19 1275.25 1276.85, 1000.05 1003.22 & 1142.63 1143.42

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Malaysia’s Prime Minister raps currency rigging and proposes currency pegged to gold to settle East Asian trade

Two commentaries

(Reuters/GATA)

Malaysia’s prime minister raps currency rigging, urges using gold to settle East Asian trade

Submitted by cpowell on Thu, 2019-05-30 22:55. Section: Daily Dispatches

Malaysia’s Mahathir Proposes Common East Asia Currency Pegged to Gold

By Rozanna Latiff and A. Ananthalakshmi

Reuters

Thursday, May 30, 2019

KUALA LUMPUR, Malaysia — Malaysian Prime Minister Mahathir Mohamad today mooted the idea of a common trading currency for East Asia that would be pegged to gold, describing the existing currency trading in the region as manipulative.

Mahathir said the proposed common currency could be used to settle imports and exports, but would not be used for domestic transactions.

…

In the Far East, if you want to come together, we should start with a common trading currency, not to be used locally but for the purpose of settling of trade,” he said at the Nikkei Future of Asia conference in Tokyo.

“The currency that we propose should be based on gold because gold is much more stable.”

He said under the current foreign-exchange system, local currencies were affected by external factors and were manipulated. He did not elaborate on how they were manipulated. …

… For the remainder of the report:

https://www.reuters.com/article/us-malaysia-currency/malaysias-mahathir-…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Malaysian PM elaborates on currency market rigging, resents dictation by U.S.

Submitted by cpowell on Thu, 2019-05-30 23:26. Section: Daily Dispatches

Dr. M. Moots Currency Backed by Gold

From the Malaysian National News Agency

via Free Malaysia Today, Petaling Jaya, Malaysia

Thursday, May 30, 2019

https://www.freemalaysiatoday.com/category/nation/2019/05/30/dr-m-moots-…

TOKYO — Prime Minister Dr. Mahathir Mohamad says Malaysia is proposing a new currency based on gold, as this would be more stable than the current currency trading, which is manipulative.

He said the precious metal could be used to evaluate import and export activities among the East Asian countries.

…

We can make settlements” using the new currency using gold, the prime minister said. “That currency must relate to the local currency as to the exchange rate, and that is something that can be related to the performance of that country.

“That way we know how much we owe and how much we have to pay in the special currency of East Asia,” he said during a dialogue session at the 25th International Conference on The Future of Asia (Nikkei Conference) here today.

Mahathir arrived in Tokyo last night for a three-day working visit.

He said the new currency could also be extended to countries outside the East Asian region.

Currently, he said, the global market is tied to the U.S. dollar, which gives room for the currency to be manipulated.

“Just because that one country is affected, there is infection to the other countries. Malaysia was very stable way back in 1997 … but because of the problems that occurred in Thailand” during the Asian financial crisis, “they said we must peg the Malaysian currency also.

“What happened? The currency traders sold the Malaysian currency down and the value of Malaysian currency depreciated.

“It is not even the money that they have. They never had any Malaysian currency but nevertheless they were able to sell huge quantities of Malaysian currency, and when it is depressed, of course they can buy and sell it at a higher price when it comes up,” he added.

“Currency trading is not something that is healthy because it is not about the (economic) performance of countries but about manipulation.

“Anything that you have in oversupply, we will lose value. Anything that is short of supply will increase in value, so they sell huge quantities of money they don’t have, and because the amount is so big, there is depression of the value.”

Mahathir said that if countries are downgraded or upgraded, it should be done by an uncommitted international forum, not a country.

Here, he hit out at the United States for “labeling” other countries.

“The United States is fond of labeling that country as no good, this country as no good, and telling countries about ways to conduct their business.

“You are not democratic. That is not for any single power to decide. If you want to live in a united world, a stable world, we must resort to sustainability through agreement between all nations that have a stake in that problem.”

Asked if the Japanese yen or Chinese yuan could be used as the common currency in Asia, Mahathir replied: “If we try to promote our own currency, there will be conflict. But if we have a common currency for East Asia, a common trading currency that is not used in each country but for the purpose of settlement trade only, then there will be stability.

“But trying to promote the yen or the yuan, that is not the way to go.”

END

Judy Shelton is without a doubt the right pick for Trump. Let us hope that she gets the job of Fed governor. She is a strong advocate for gold backed currency and less dependency on the Fed.

(courtesy London’s Financial Times/Judy Shelton/GATA)

Fed candidate Shelton slams central bank’s ‘Soviet’ power over markets

Submitted by cpowell on Fri, 2019-05-31 14:14. Section: Daily Dispatches

By James Politi

Financial Times, London

Friday, May 31, 2019

https://www.ft.com/content/46c4b186-8308-11e9-b592-5fe435b57a3b

Judy Shelton, a senior US official who is being vetted for a job on the board of the Federal Reserve, has attacked the central bank for wielding undemocratic, Soviet-style powers over markets and suggested it should not even be in the business of setting interest rates.

In an interview with the Financial Times at the Trump International Hotel in Washington this week, Ms. Shelton called on the Fed to “think about whether they are doing more harm than good.” If appointed to the board, she would be “asking tough questions” about its most basic mission, she said.

…

In an interview with the Financial Times at the Trump International Hotel in Washington this week, Ms. Shelton called on the Fed to “think about whether they are doing more harm than good.” If appointed to the board, she would be “asking tough questions” about its most basic mission, she said.

“How can a dozen, slightly less than a dozen, people meeting eight times a year, decide what the cost of capital should be versus some kind of organically, market-supply-determined rate? The Fed is not omniscient. They don’t know what the right rate should be. How could anyone?” Ms. Shelton said.

“If the success of capitalism depends on someone being smart enough to know what the rate should be on everything … we’re doomed. We might as well resurrect Gosplan,” she said, referring to the state committee that ran the Soviet Union’s planned economy. Ms. Shelton did post-doctoral research on the Soviet economy at Stanford University’s Hoover Institution and was designated to be the Russia expert on the board of the National Endowment for Democracy.

The U.S. representative on the board of the European Bank for Reconstruction and Development, Ms. Shelton is being considered by Donald Trump to be a Fed governor after his previous proposed candidates — Stephen Moore and Herman Cain — were dropped from contention. Both Mr. Moore and Mr. Cain withdrew this year after Republicans in the upper chamber balked at their limited qualifications for the job, personal factors that emerged during their vetting, and fears that they would not be independent enough from Mr. Trump.

Ms. Shelton, who obtained an MBA in business administration from the University of Utah, has already passed muster with Congress for the EBRD job, which could make it harder for the Senate to turn her down. But her possible nomination suggests that Mr. Trump is in no mood for a less controversial pick for the US central bank, and wants a disruptive candidate to argue for unorthodox policies within the Fed.

As well as questioning whether the Fed should even be steering monetary policy, Ms. Shelton has called for the central bank to stop paying banks interest on excess reserves, a policy introduced during the financial crisis, saying it was turning financial institutions into “utilities,” rewarding them for allowing money to “sit doing zilch” rather than being loaned out.

She also said that the Fed should continue to reduce its balance sheet below the $3.5 trillion target set by Jay Powell, the chairman. “I would rather the Fed be less of an entity. When a central bank buys up government debt, that’s the beginning of compromised finances.”

She also said the Fed had become so influential that it unnaturally drove investment decisions and affected financial markets. “It’s the distorting aspect of the Fed that is the worst aspect — it’s a wag-the-dog situation. People are fixated on the Fed and are making money by arbitraging, trillions of a second after the latest FOMC announcement,” she added.

Ms. Shelton has long been sympathetic to the gold standard, which the U.S. fully abandoned in the early 1970s in favour of a flexible exchange rate for the dollar. “People call me a goldbug, and I think, well, what does that make them? A Fed bug,” she says.

Her big dream is a new Bretton Woods-style conference — “if it takes place at Mar-a-Lago, that would be great” — to reset the international monetary system, replacing the current regime, mostly based on floating currencies. Ms. Shelton said countries should agree to tie their currencies to a “neutral reference point, a benchmark” — which she envisages to be a “convertible gold-backed bond.”

“Now is the pivotal moment to question whether central banking is really delivering what the central bankers themselves aspire to. They are going through self-examination so I think it’s reasonable to say there are alternatives,” she said.

Ms. Shelton, who has close ties to Larry Kudlow, the director of the National Economic Council, as well as David Malpass, the president of the World Bank, worked for Mr. Trump as an economic adviser during the 2016 presidential campaign. She endorsed his “pro-growth economic agenda,” from tax cuts to deregulation.

She also supports the U.S. president’s trade war with China, including the decision to ratchet up tariffs after turning away from a deal at the eleventh hour. “I think it took a lot of guts to say that [the deal offered by China in early May] will mean everything we were fighting for was just a joke,” Ms. Shelton said.

“Thank goodness he is sticking it out. I’ve always thought we had to fight fire with fire with China, Europe’s talked about it for ages and never really did anything with teeth in it, and neither did the U.S. until now.”

* * *

end

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9097/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9437 /shanghai bourse CLOSED DOWN 7.11 POINTS OR 0.24%

HANG SANG CLOSED DOWN 213.79 POINTS OR 0.79%

2. Nikkei closed DOWN 341.34 POINTS OR 1.63%

3. Europe stocks OPENED RED /

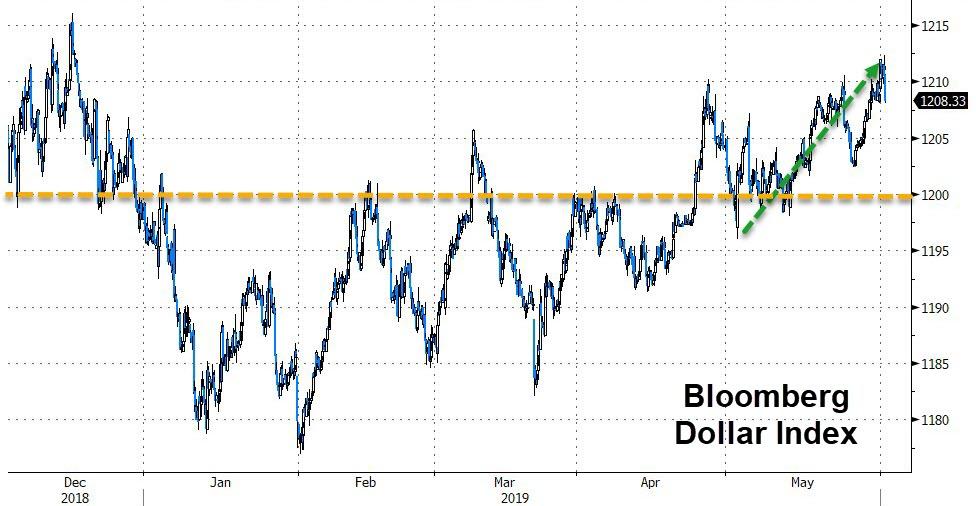

USA dollar index RISES TO 98.00/Euro RISES TO 1.1149

3b Japan 10 year bond yield: FALLS TO. –.09/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.72/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 55.45 and Brent: 63.73

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

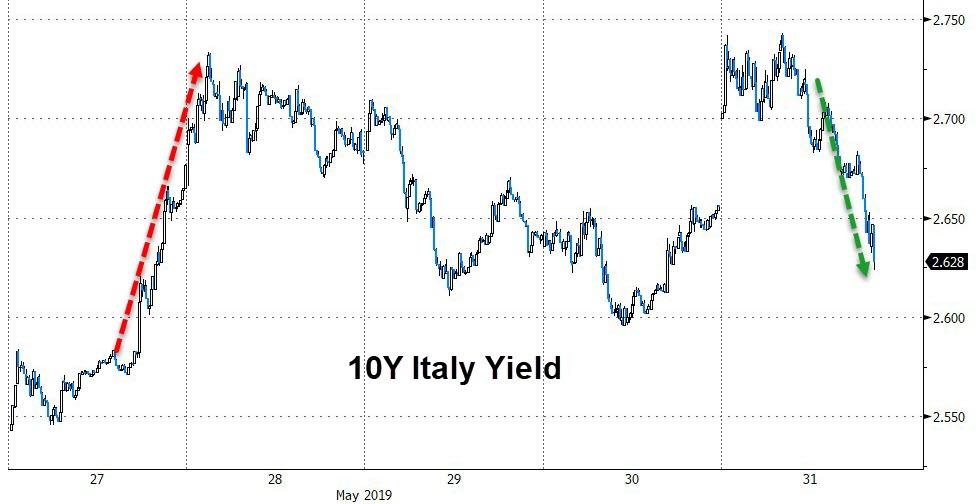

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.21%/Italian 10 yr bond yield UP to 2.71% /SPAIN 10 YR BOND YIELD DOWN TO 0.73%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.92: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.99

3k Gold at $1297.20 silver at: 14.51 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 42/100 in roubles/dollar) 65.55

3m oil into the 55 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.72 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0058 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1201 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.21%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.15% early this morning. Thirty year rate at 2.60%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8641..they are toast

Global Markets Routed After Trump Tariff Bombshell, Bund Yields Crater To Record Low

To those who sold in May, congratulations. To everyone else, we hope you are enjoying the bloodbath.

US stock futures, global markets and sovereign bond yields tumbled on Friday as investors feared President Donald Trump’s shock threat of tariffs on Mexico – a 5% tariff from June 10, which would then rise steadily to 25% until illegal immigration across the southern border was stopped – risked tipping the United States, and maybe the whole world, into recession.

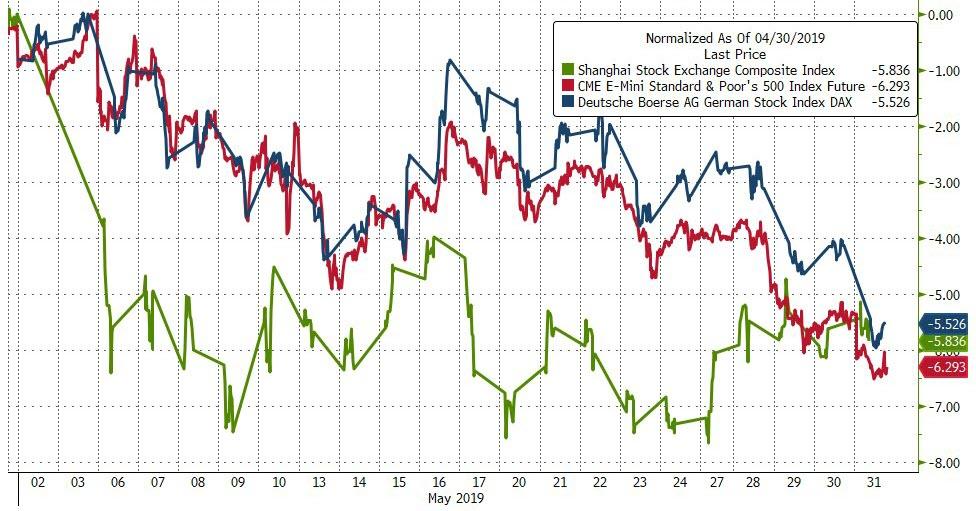

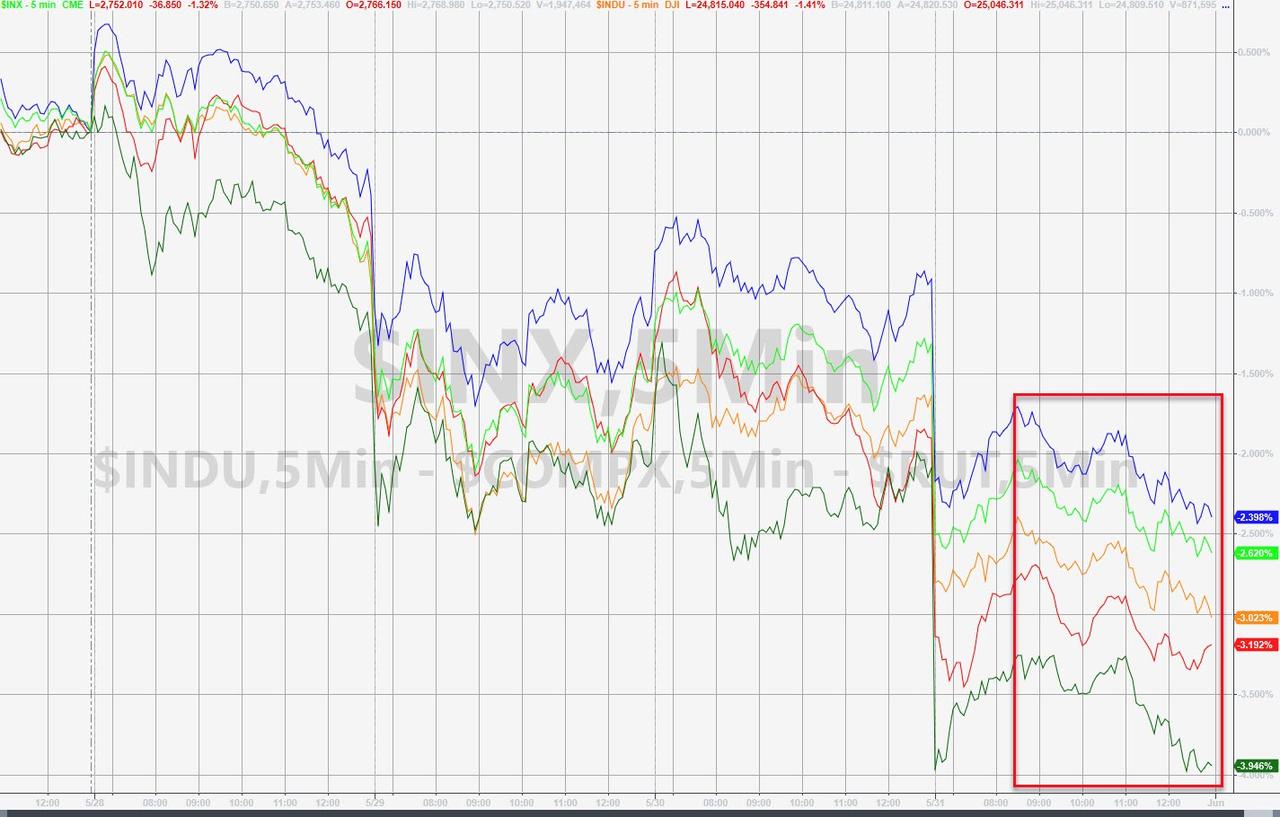

The rout, which sent the Dow below 25,000 and the S&P below its 200 DMA, will break the S&P’s unbroken monthly streak in 2019, with May set for the first monthly loss since the December rout. In fact, May will be the third worst month since the US downgrade in August 2011.

Trump announced the decision on Twitter late Thursday, catching markets completely by surprise.

“The mercurial President Trump has signalled via Twitter this morning that his mindset is shifting ever farther from reaching trade deals,” warned Saxo’s Eleanor Creagh. “It seems now that market participants are finally realising that the narrative of an H2/19 recovery is fast dissipating,” she added. “As escalating trade tensions across the globe cause growth expectations to be recalibrated, risk off sentiment will remain and volatility will increase.”

“We are seeing a Trump who is going all-out,” said Kay Van-Petersen, global macro strategist at Saxo Capital Markets Pte. “This raises the bar not just for Mexico and Canada, but also for China.”

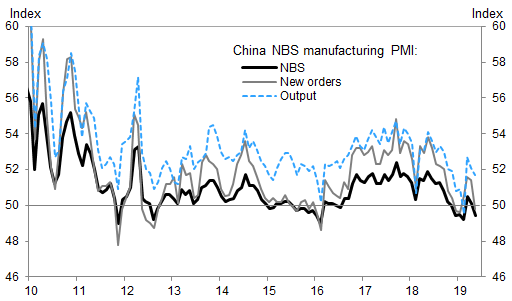

After Trump’s announcement, investor mood hit pitch black when China’s May manufacturing PMI printed not only below expectations, but below the lowest expectation, raising questions about the effectiveness of Beijing’s stimulus steps. The official NBS manufacturing PMI fell to 49.4 in May, from 50.1 in April. Sub-indexes suggested lower price inflation and weaker trade growth in May. Trade indicators worsened further – the imports sub-index declined to 47.1, from 49.7, and the new export order index went down to 46.5, vs. 49.2 in April. Inventory indicators rose – the raw material inventories index was 0.2pp higher at 47.4, and the finished goods inventory index rose to 48.1 in May.

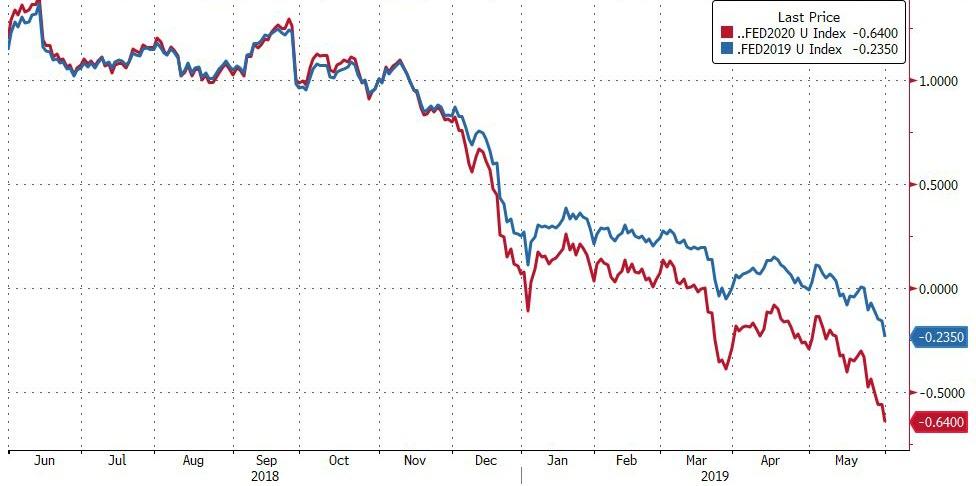

With traders throwing in the towel, global markets moved aggressively to price in deeper rate cuts by the Federal Reserve this year, while bond yields touched fresh lows and curves inverted further in a warning of recession.

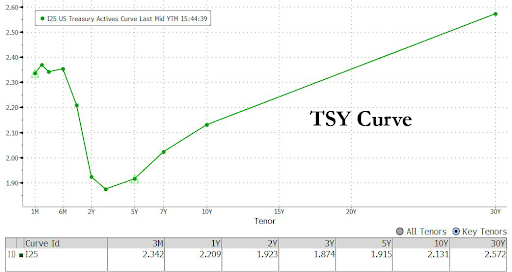

With markets tumbling, traders flooded into the safety of bond market and the dollar, with yields on the 10-year Treasury note quickly fell to a fresh 20-month low of 2.17%, while the dollar jumped 1.7% on the Mexican peso. In the US, all Treasury tenors from 2Y to 5Y were now trading below 2.0%, while the 3M-10Y was inverted as much as 21bps. Bonds extended their bull run with 10-year Treasury yields now down a steep 33 basis points for the month and decisively below the overnight funds rate. Such an inversion of the yield curve has presaged enough recessions in the past that investors are wagering the Fed will be forced to ease policy just as “insurance”.

Yet Treasuries were hardly alone in rallying, with bond yields across Europe either at or near record lows. Yields in Australia and New Zealand have also hit an all-time trough on expectations of rate cuts there. Bund yield falls 4bps to -0.213%, below the previous all-time low touched in July 2016, as core bonds outperformed semi-core, and German provincial CPI numbers are weaker than economists estimated.

As if that wasn’t enough, stocks extended declines on reports that China will establish a list of “unreliable” entities to target firms it says damage the interests of domestic companies.

The Stoxx Europe 600 Index fell, with all industry sub indexes down, led by autos and basic resources.European shares extend losses, alongside U.S. futures, as China announces it is preparing for retaliation by implementing a list of “unreliable” entities in order to target firms it says damage the interests of domestic companies. Stoxx 600 Index falls 1.4%. European shares set for largest monthly drop since January 2016; Stoxx Europe 600 Index down 6.2% in May, with the biggest pain felt again by Deutsche Bank shareholders, as DBK tumbled to new all time lows.

Asian shares fell at first, only to draw month-end bargain hunting having endured a torrid few weeks. MSCI’s broadest index of Asia-Pacific shares outside Japan edged up 0.3%, though it was still down a whopping 7.3% for the month.

China’s blue chip index held steady, partly on talk Beijing would now have to ramp up its stimulus, but again was nursing loses of 6.8% for May. Japan’s Nikkei fell 1.3%, dragged down by big falls in car makers, which left it off 7.1% for the month.

There was one silver lining: Apple suppliers rose in Taipei Friday, boosting the Taiex index, after China said it would protect foreign businesses’ legitimate rights. The comments from China’s commerce ministry official Thursday was interpreted as an indication that Beijing doesn’t intend to retaliate against Apple and other American firms doing business on the mainland, according to Concord Securities assistant vice president Allan Lin, although that may be over as soon as today.

Another silver lining: investors clearly felt encouraged that opening a new front in the trade wars would pressure central banks everywhere to consider new stimulus. On Thursday, Fed Vice Chair Richard Clarida said the central bank would act if inflation stays too low or global and financial risks endanger the economic outlook.

“What the Clarida’s comments have done is clarify in many people’s minds the answer to the questions of whether low inflation proving more than transitory would itself be enough to get the Fed to ease – the answer appears to be ‘yes’,” said Ray Attrill, head of FX strategy at National Australia Bank. “That served to reinforce prevailing market expectations that the Fed will be easing in the second half of this year.”

Not surprisingly, in FX the DXY dollar index ramped to new two-year highs against a basket of currencies at 98.115. The euro was huddled at $1.1129, having shed 0.7% for the month. The safe-haven yen fared better as the dollar lost 0.6% on the day to a three-month low of 108.94. Sterling was poised for the biggest monthly drop in a year as the imminent departure of Theresa May as prime minister deepened fears about a chaotic divorce from the European Union. The pound was last at $1.2611 and nursing a 3.2% loss for the month so far.

In commodity markets, spot gold firmed 0.4% to $1,293.33 per ounce. Oil prices fell to their lowest in almost three months on fears a global economic slowdown would crimp demand. U.S. crude was last down 55 cents at $56.04 a barrel, while Brent crude futures lost 91 cents to $65.96.

Expected data include personal income and University of Michigan Sentiment Index. Big Lots is reporting earnings.

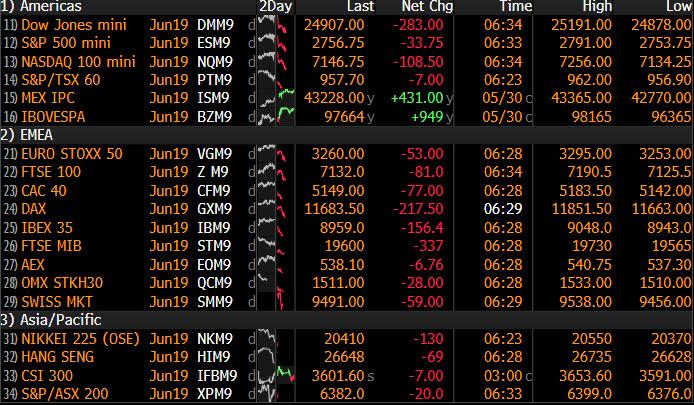

Market Snapshot

- S&P 500 futures down 1.1% to 2,759.25

- STOXX Europe 600 down 1% to 368.54

- MXAP down 0.04% to 152.22

- MXAPJ up 0.2% to 498.43

- Nikkei down 1.6% to 20,601.19

- Topix down 1.3% to 1,512.28

- Hang Seng Index down 0.8% to 26,901.09

- Shanghai Composite down 0.2% to 2,898.70

- Sensex down 0.3% to 39,707.10

- Australia S&P/ASX 200 up 0.07% to 6,396.85

- Kospi up 0.1% to 2,041.74

- German 10Y yield fell 2.7 bps to -0.202%

- Euro up 0.2% to $1.1148

- Italian 10Y yield rose 1.4 bps to 2.283%

- Spanish 10Y yield fell 1.8 bps to 0.746%

- Brent futures down 3.3% to $64.70/bbl

- Gold spot up 0.7% to $1,297.30

- U.S. Dollar Index down 0.1% to 98.00

Top Overnight News from Bloomberg

- Trump vowed to impose tariffs on Mexican goods until that country stops immigrants from entering the U.S. illegally, jeopardizing a new North American trade agreement. The tariff would take effect on June 10 and has major implications for American automakers and other companies with production south of the border

- U.S. Senate Finance Committee Chairman Chuck Grassley (R-Iowa) calls President Trump’s Mexico tariff Plan a “misuse” of authority. “Following through on this threat would seriously jeopardize passage of USMCA.” Mexican President Andres Manuel Lopez Obrador says in letter to Trump posted to Twitter “from start, I express that I don’t want confrontation.”

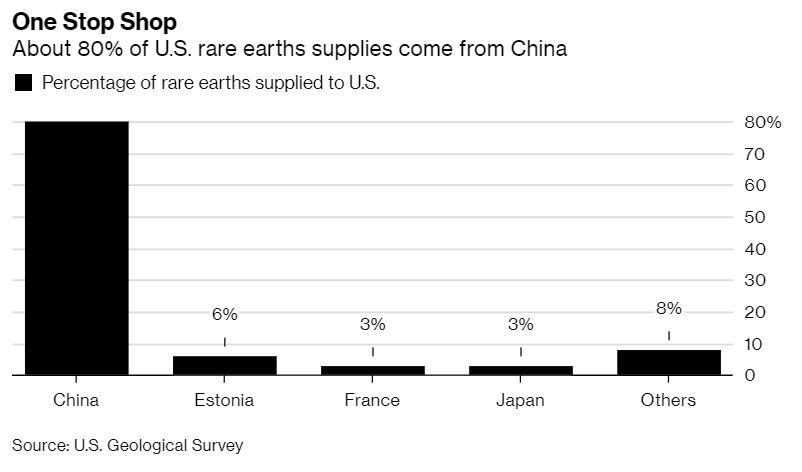

- China has prepared the steps it will take to use its stranglehold on the critical minerals in a targeted way to hurt the U.S. economy, people familiar said. The measures would likely focus on heavy rare earths, a sub-group of the materials where the U.S. is particularly reliant on China

- China will establish a list of so-called “unreliable” entities in order to target firms it says damage the interests of domestic companies, according to an announcement carried by state media on Friday

- Mitsubishi UFJ Financial Group Inc., Japan’s largest bank, is preparing major job cuts in London, offering voluntary redundancy packages to about 500 directors and managing directors in London, according to an emailed statement. That’s roughly a quarter of its workforce in the city

- India’s Prime Minister Narendra Modi picked leaders with experience for key portfolios as he began a second five-year term facing an economic slowdown and global headwinds

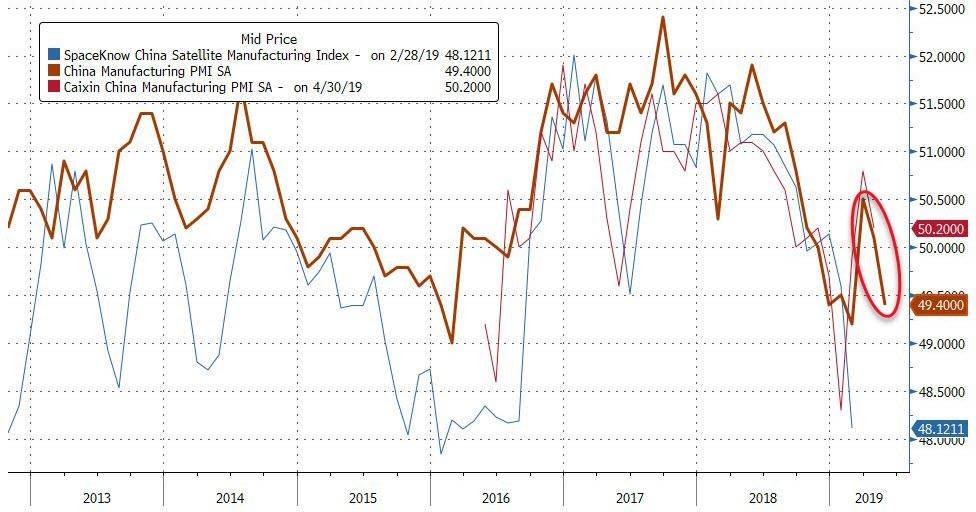

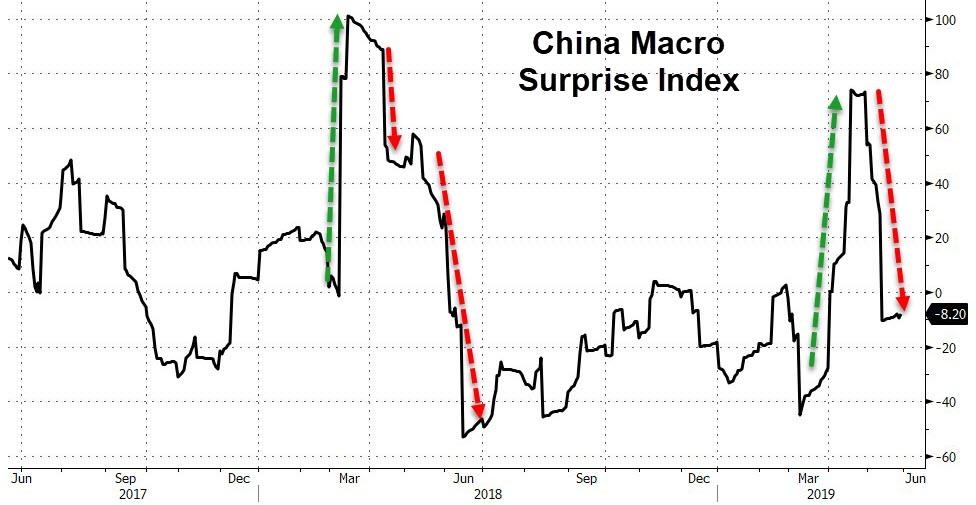

- The outlook for China’s manufacturing sector deteriorated more than expected in May, as weakness in the domestic economy combined with escalation in the trade standoff with the U.S.

- Federal Reserve Vice Chair Richard Clarida says “if the incoming data were to show a persistent shortfall in inflation below our 2% objective or were it to indicate that global economic and financial developments present a material downside risk to our baseline outlook, then these are developments that the committee would take into account in assessing the appropriate stance for monetary policy

- Mitsubishi UFJ Financial Group Inc., Japan’s largest bank, is preparing major job cuts in London, offering voluntary redundancy packages to about 500 directors and managing directors in London, according to an emailed statement. That’s roughly a quarter of its workforce in the city

- India’s Prime Minister Narendra Modi picked leaders with experience for key portfolios as he began a second five-year term facing an economic slowdown and global headwinds

Asian equity markets traded mixed heading into month-end with early pressure seen after US President Trump announced to place 5% tariffs on all goods from Mexico from June 10th, which will increase to as much as 25% by October 1st and remain there until Mexico addresses the illegal immigration inflows to the US through its territory. The announcement pressured US equity futures to give back the prior session’s gains in which the Emini S&P breached its 200DMA to the downside and the DJIA briefly slipped below the 25K level, with Wall St on track for its worst monthly performance YTD. ASX 200 (Unch.) was lower for most the session with tech and energy the underperformers although strength in gold and other mining names stemmed the downside in the index, while Nikkei 225 (-1.6%) suffered from currency flows and with automakers spooked by fears of a trigger-happy ‘Tariff Man’. Hang Seng (-0.8%) and Shanghai Comp. (-0.2%) were mixed as participants digested varied Chinese PMI data in which Manufacturing PMI fell short of estimates and slipped into contractionary territory but Non-Manufacturing PMI printed inline, and although the PBoC refrained from open market operations, its efforts this week resulted to a total net injection of CNY 430bln. Finally, 10yr JGBs followed suit to the upside in T-notes as Trump’s announcement spurred safe-haven demand, while the BoJ were also present in the market for JPY 680bln of JGBs in the belly to super long-end.

Top Asian News

- Anta Jumps After Fighting Back on ‘Misleading’ Short Sell Attack

- BOJ Paves Way to Buy Fewer Bonds as Growth Worries Sink Yields

- Apple Suppliers Rise as China Shows No Intention to Retaliate

- Philippine Central Bank Governor ‘Promises’ More Rate Cuts

European Indices trade firmly in negative territory this morning [Euro Stoxx 50 -1.7%] as sentiment took a hit as US President Trump revisited his ‘Tariff Man’ persona by announcing the placement of 5% tariffs on all goods stemming from Mexico as of June 10th; which may increase by up to an additional 20% by October 1st. Currently eight automakers including Volkswagen (-3.6%) and Fiat Chrysler (-4.6%) operate plants in Mexico, as such the Stoxx 600 Auto Sector (-2.8%) is significantly lagging its peers with the Dax (-1.6%) the underperforming bourse due to automakers/parts having around a 14% weighting in the Dax. Auto names aside, other companies with exposure to Mexico have been significantly affected by President Trump’s announcement with the likes of Tenaris (-4.7%) afflicted due to the Co. operating one of the world’s largest manufacturing centres for steel tubes in Mexico. Elsewhere, Italian banks are at their lowest level since November 2016 due to the ongoing internal political tensions as well as the potential for Italy to face EU disciplinary procedures in the form of a EUR 3.5bln fine. Other notable movers this morning include Wirecard (-11.3%) who are lagging the Stoxx 600 after reports that several public prosecutors are said to see the Co. as the central payment processor for the fraudulent trading site Option888. Bucking the risk-off sentiment and at the other end of the Stoxx 600 are Whitbread (+1.9%) after the Co’s board decided that the second phase in their three phase capital programme is a GBP 2bln tender offer.

Top European News

- Brexit Delay Boosts U.K. Mortgage Lending, Consumer Borrowing

- German Yields Set New Sub-Zero Record as Haven Seekers Rush In

- Visco Says Italy’s Debt Load Is ‘Severe Constraint’ on Economy

- Europe Car Stocks Sink to Five-Month Low on Trump’s Mexico Plan

In FX, the broad Dollar and Index are on the backfoot this morning with DXY now back below 98.000, albeit marginally. The Buck awaits key US data in the form of April PCE prices as traders look for any clues if the “dip in inflation was transitory” as the Fed stated at its most recent meeting. On a technical front, to the downside DXY sees its 50 DMA just under the 97.50 level at 97.47 ahead of clean air down to 97.00.

- MXN, CAD – The clear underperformers today, more-so the Peso after President Trump dampened USMCA hopes by taking aim at Mexico. The Peso immediately saw downside and continued that trajectory throughout the session, with USD/MXN spiking higher from around 19.1500, through its 50 WMA (19.2766) and 200 DMA (19.3360) to a high of 19.7360. Meanwhile, from Canada’s side, the potential ramifications on the USMCA deal, coupled with lower energy prices sent USD/CAD higher to around 1.3550 from a low of around 1.3494 ahead of a barrage of Canadian data including Q1 GDP.

- JPY, CHF – The Yen stands as the clear G10 outperformer this morning amid the overall risk aversion in the market with downside vs. the USD exacerbated as Trump spills his trade war into Mexico. USD/JPY cleanly broke below the 109.00 figure and continues to lose ground below the level, having traded within a wide 109.62-108.76 band, with buyers reported at 108.75 ahead of the Jan 28 low just above 108.50. Following the latest developments, Morgan Stanley believes that a breach below 109.00 support opens downside potential to 107.70. Meanwhile, the Swiss Franc also posts gains, albeit to a lesser extent, with traders speculating potential SNB intervention to keep the CHF strengthening further. USD/CHF currently rests just above the 1.0050 mark ahead of its 100 DMA at 1.0037.

- EM – The EM space is weaker across the board amidst the Trump-sparked collapse in the Mexican Peso, albeit the TRY has shown some resilience as it consolidates following yesterday’s stellar performance. However, geopolitical risks for the Lira remain as the Turkish Foreign Ministry spokesperson has dismissed reports that the Russian S-400 delivery will be delayed, which comes after US pressured the country to dump the USD 2.5bln deal with Russia, which contradicted prior reports that the Russian system will be delivered ahead of scheduled. Either way, markets are looking at any potential US sanctions on Turkey if the delivery does go through, which Turkey noted was “a done deal”

- AUD, NZD, EUR, GBP – All marginally firmer against the Greenback (ex-GBP), albeit more due to a pullback in the USD than individual factors. The Antipodeans were little fazed by the overnight miss in the Chinese NBS manufacturing PMI as currencies await the Caixin release next week alongside the RBA’s “live” rate decision and Aussie GDP. Elsewhere, the expectations for a post-Easter collapse sees the EUR largely shrugging off the downticks in German state inflation numbers, as markets gear up for the national release at 1300BST. EUR/USD resides closer to the top of today’s 1.1126-54 band with resistance reported at 1.1155 ahead of 1.1170. Meanwhile, the Pound has lost some ground in recent trade, particularly vs the EUR with some citing RHS demand and EUR/GBP bids at 0.8850 as factors.

Commodities are mixed with the energy markets plumbing the depths as risk sentiment further deteriorates amid trade war escalations coupled with rising US crude production. WTI (-2.1%) straddles around the USD 55/bbl level, having already dipped below the figure whilst its Brent (-2.5%) counterpart follows the same trajectory as it hovers around USD 64.50/bbl. Furthermore, some geopolitical risk premium may have also unwound in the oils amid reports that US has delayed tougher sanctions Iran’s petrochemical sectors in an attempt to dial back tensions. Elsewhere, gold (+0.6%) benefits from the risk aversion and the receding USD as it creeps closer to the USD 1300/oz level, whilst copper extends its decline below the USD 2.600/lb level amid the soured risk tone coupled with disappointing Chinese PMI data.

US Event Calendar

- 8:30am: Personal Income, est. 0.3%, prior 0.1%; Personal Spending, est. 0.2%, prior 0.9%

- 8:30am: PCE Deflator MoM, est. 0.3%, prior 0.2%; PCE Deflator YoY, est. 1.6%, prior 1.5%

- 9:45am: MNI Chicago PMI, est. 54, prior 52.6

- 10am: U. of Mich. Sentiment, est. 101.5, prior 102.4; Current Conditions, prior 112.4; Expectations, prior 96d

DB’s Jim Reid concludes the overnight wrap

The final day of May probably couldn’t come soon enough for most given the change in tide driven by a 102-word tweet from President Trump 26 days ago. Well, somewhat fittingly, the month was bookended by another surprise tweet from the US President last night, this time announcing a set of tariffs on imports from Mexico. According to Trump, the US will institute a 5% tariff on imports from Mexico effective June 10, with the rate set to rise by 5% every month until it reaches 25% in October. However, the new duties will be removed on Mexico if “illegal migrants coming through Mexico, and into our country, STOP” as per his tweet. For reference, the US imports around $30bn of goods from Mexico each month, and around 30% of those are autos. Tariffs at 25% on that flow of goods, in addition to the duties on China, would start having a significant and potentially crippling impact on US industry, so it’s possible that this move is aimed at pushing the US Congress to act on either the USMCA deal or on an immigration package. So far Mexico has stated that they will not retaliate until talking with the US, however the damage is likely to be already done to US-Mexico relations which since President AMLO was elected, had been improving. As for markets, the Mexican Peso has weakened -2.14% as we go to print, S&P 500 futures are down -0.65%, 10y Treasuries are down -3.1bps at 2.182% and WTI oil is down -1.15%. So, June starts right where May finished with tweet/tariff-induced selloffs.

As we’ve been arguing, these tweets have the potential to change the dynamics of global markets and it now seems like we could get a serious trade escalation that wasn’t likely at the start of last month, especially as it had appeared Trump had looked like he wanted to get a deal done in 2019. The landscape has changed dramatically and it could be an interesting summer ahead. The reality also is that with it being the first day of June tomorrow, tariffs will officially kick in between the US and China with the US applying 25% tariffs on $200bn of China exports to the US, while China will apply 5-25% tariffs on $60bn of US exports to China.

Needless to say, this also means economic data will be closely scrutinized as to the impact that the trade escalation has had, with next week’s final PMIs and ISM report top of that list. In the meantime this morning we’ve already had the final official May PMIs in China, which slid more than expected. The manufacturing print came in at 49.4, and the new orders and new export orders sub indexes were notably soft at 49.8 and 46.5. The non-manufacturing print came in at 54.3 as expected, bringing the composite PMI to 53.3 and slightly lower versus April. Equity markets in China initially opened in the red, however have since recovered with the Shanghai Comp (+0.01%) and CSI 300 (+0.06%) now pretty much unchanged. The Nikkei (-0.70%) and Hang Seng (-0.19%) are in the red, however markets do appear to be holding their own for the most part given both this data and the tariff news and it’s the same with Asia FX which has been broadly stable. That said it’s worth noting that the auto sector has borne the brunt of the pain, with Japanese automakers currently down -2.60%. To add to the headline risk the moves this morning also come despite China announcing that it is prepared to restrict exports of rare earths to the US if needed as per Bloomberg.

The overnight newsflow is clearly the main story and in any case it follows a mostly dull session on Wall Street yesterday prior to the latest tariff announcement. The good news is that risk assets did stage a rebound – albeit a modest one – with the S&P 500 rising +0.21%, however it still did close below the 2,800 level. Overnight, Binky Chadha published a timely note (available here ) estimating that the trade war has cost around $5 trillion in forgone equity gains, equal to 12-years’ worth of the bilateral trade deficit with China. Meanwhile the NASDAQ ended +0.27% while in Europe the STOXX 600 rose +0.42%. Volumes were however well below average across most markets, though markets did experience some late-session volatility after Vice President Pence said that the US can “more than double” tariffs on China if needed. As we highlighted yesterday, speculation also continued to swirl about a planned Pence speech next week which could be used to announce new sanctions on specific companies (per CNBC).Equities slipped into the red but ultimately closed higher, while bonds yields fell more persistently. Indeed 10y Treasuries rallied -4.9bps, though Bunds had already closed flat near their all-time lows at -0.177% before the rally. The US 2s10s was steady at 14.9bps while the 3m10y curve slid another -6.7bps to -15.9bps, its lowest level since May 2007. The VIX (-0.6pts) closed at 17.3, though high yield credit spreads in the US finished +3bps wider. HY spreads were flat in Europe.

Away from trade it’s worth noting that Italy could be a talking point again today with the government expected to respond to the EU’s request for an explanation of the violation of the debt rule for 2018. However, our economists have pointed out that there are more arguments for not opening a procedure right now. In particular they flag Italy’s deteriorating growth outlook, for which corrective measures could prove to be pro-cyclical. They also highlight different estimations of the output gap between Rome and Brussels, conciliatory steps adopted by Italy and the potential impact of the European election. Yesterday, Italian press reports – including from Il Messaggero and Il Corriere della Sera – claimed that Italy will argue that a corrective measure will be counterproductive and result in further growth deterioration. In any case, one to potentially watch. We should note that Italian assets underperformed yesterday with the FTSE MIB down -0.24% and 10y BTPs up +1.6bps in yield (compared to -4.3bps at the lows) following headlines suggesting that Deputy PM Salvini is ready to end the coalition government should he not get backing for his flat tax plan and other priority measures.

Elsewhere, though it didn’t end up moving markets, Fed Vice Chair Clarida’s comments yesterday did get some attention, since he was one of the key officials who initiated the pivot away from hikes earlier this year. He said that the economy is in a “very good place” and that the “current stance of policy remains appropriate.”He thinks policy should remain patient, which “means that we should allow the data on the US economy to flow in and inform our future decisions.” When asked about the yield curve’s recent flattening, Clarida seemed relatively sanguine, citing global and financial factors as the main drivers. He said that the curve is roughly flat right now, but that he would only be worried if it inverted more deeply and more persistently.

As for the data yesterday, where the second reading for Q1 PCE was revised down three-tenths to +1.0% qoq. So a fairly dovish print, however we should flag that the details did show that the revisions were mostly in financial services and insurance – a category that was already known to be weak in Q1 and is still expected to bounce back. Looking ahead, it’s worth noting that today we’ll get the April PCE reading which is expected to print at +0.2% mom for the core. Our US economists are forecasting a +0.3% reading which in their view would provide evidence that at least some of the recent weakness in the Fed’s preferred measure was likely transitory.

Meanwhile the second reading for Q1 GDP in the US was revised down to +3.1% qoq saar, marginally better than expected.However it didn’t go unnoticed that corporate profits were down -2.8% qoq, the second quarterly decline and biggest fall since Q4 2015. Elsewhere, claims printed at 215k, a small uptick on the week prior but more or less in line with expectations, while the April advance goods trade balance showed a deficit of $72.1bn compared to $71.9bn in March. Retail and wholesale inventories rose +0.5% mom and +0.7% mom respectively while April pending home sales fell -1.5% mom (vs. +0.5% expected).

To the day ahead now, which this morning kicks off in Germany where we’ll get April retail sales data, followed by the final Q1 GDP revisions in Italy, April money and credit aggregates data in the UK, and preliminary May CPI readings for Italy and Germany. In the US the big focus will be on that April PCE data, while personal spending and income data for April, the May Chicago PMI and final May revisions for the University of Michigan survey. Away from the data the Fed’s Visco is due to speak this morning while this afternoon the Fed’s Bostic is due to moderate a discussion on the global economy, while the Fed’s Williams speaks this evening on the topic of monetary policy theory and practice. Expect the fallout from the latest tariff announcement to be the big talking point however.

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 7.11 POINTS OR 0.24% //Hang Sang CLOSED DOWN 213.79 POINTS OR 0.79% /The Nikkei closed DOWN 341.34 POINTS OR 1.63%//Australia’s all ordinaires CLOSED UP 0.04%

/Chinese yuan (ONSHORE) closed DOWN at 6.9097 /Oil DOWN TO 57,28 dollars per barrel for WTI and 68.41 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9097 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9437 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

The bond markets are correct: the trade war is taking a huge bit out of China manufacturing as its PMI tumbles back into

contraction mode

(courtesy zerohedge)

Trade War Bites As China Manufacturing PMI Tumbles Back Into Contraction

China’s Official May Composite PMI printed modestly lower than April’s at 53.3, with Services at 54.3 (in line with last month and goal-seeked expectations), while Manufacturing (expected to decline into contraction at 49.9) was considerably worse than expected, printing 49.4.

This was below the lowest analyst estimate of 49.5, and close to the lowest level in about a decade.

Under the hood of the manufacturing data, Output growth slowed, New Orders tumbled into contraction (with export orders plunging), inventories rose, employment slipped, and input & output prices contracted. The most affected were Small Enterprises.

The Services data also showed weaker new orders and employment with selling prices slumping into contraction

The drop clearly reflects pressure on the production side of the economy from the escalating trade war (following some pre-tariff stocking-up).

None of this should be a big surprise as much of Asia’s flash PMIs were weak and after spiking on record credit injections in the early part of the year, China’s macro data has collapsed against renewed optimistic expectations…

Looks like we are “gonna need a bigger boat” of cash to keep this red ponzi afloat, which is a problem as the signal from China’s April credit data was also negative. The unexpectedly large fallback in credit raised fresh doubts about whether the economy has found a bottom.

Beijing Has Reportedly Developed Plan For Rare-Earth Export Ban

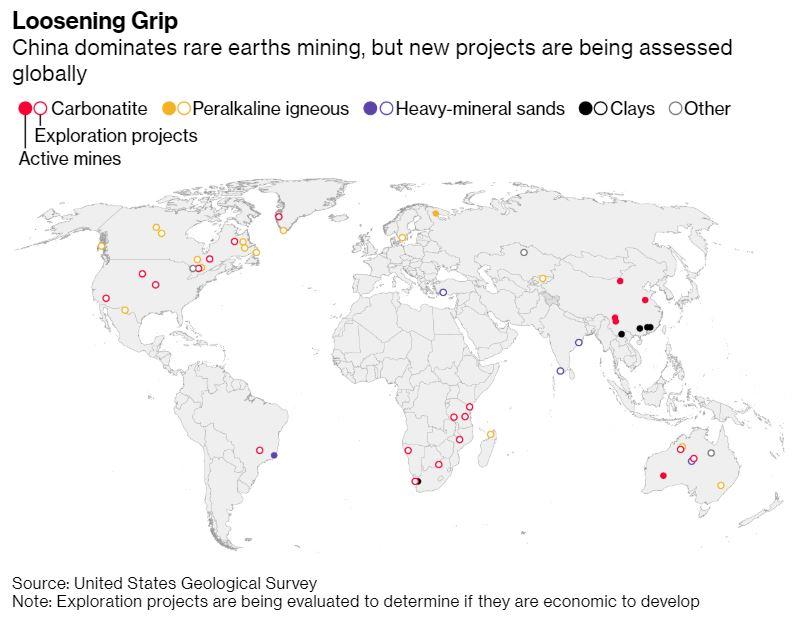

Despite last night’s disappointing PMI print, the latest sign that the trade-war backlash is hurting the mainland economy (especially since the credit injections from earlier this year are fading into the distance), Beijing is apparently undeterred, and on Friday, it continued to ratchet up threats about invoking the “nuclear option” of curbing exports of rare earth metals to the US, a move that would cause significant disruptions to supply chains for everything from microchips to to fighter jets.

Beijing has reportedly prepared a plan to cut off exports of rare earths to the US, Bloomberg reports, though it didn’t offer any details about what this plan might entail.

Beijing has readied a plan to restrict exports of rare earths to the U.S. if needed, as both sides in the trade war dig in for a protracted dispute, according to people familiar with the matter.

The government has prepared the steps it will take to use its stranglehold on the critical minerals in a targeted way to hurt the U.S. economy, the people said. The measures would likely focus on heavy rare earths, a sub-group of the materials where the U.S. is particularly reliant on China. The plan can be implemented as soon as the government decides to go ahead, they said, without giving further details.

China produces 80% of the world’s rare earth metals – which, contrary to what their name might suggest, are actually more plentiful than precious metals like gold.

However, most rare earths imported by the US travel through intermediaries before arriving at US ports. Washington exempted the critical metals, which are used in a broad range of high-tech products, from tariffs.

One analyst cautioned that nothing is yet set in stone.

“Currently, it’s still just a possibility that China may ban or do some kind of restrictions,” Racket Hu, a researcher at Shanghai Metals Market, said in a Bloomberg TV interview. “But if it does happen, then we believe prices of rare earths will surge,” he said, citing what happened in 2010 when China curbed shipments to Japan.

Indeed, it appears traders are already starting to price in the export curbs, as the VanEck Vectors Rare Earth ETF has risen off its 2019 lows since Trump’s Huawei blacklisting elicited threats of retaliation from Beijing.

Though miners, including Australia’s Lynas, are scrambling to open new mines…

…the new capacity likely won’t be ready in time to prevent significant supply disruptions should Beijing make good on its threats.

end

4/EUROPEAN AFFAIRS

i) EUROPE

Countries are continuing to shun the USA , which is not good for USA hegemony

a very important commentary from Tom Luongo

(courtesy Tom Luongo)