GOLD: $1323.30 UP $17.50 (COMEX TO COMEX CLOSING)

Silver: $14.78 UP 19 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1325.50

silver: $14.79

QUITE A WEEK!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 8/32

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,305.800000000 USD

INTENT DATE: 05/31/2019 DELIVERY DATE: 06/04/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 18

363 C WELLS FARGO SEC 6

661 C JP MORGAN 15 6

661 H JP MORGAN 2

686 C INTL FCSTONE 2 4

690 C ABN AMRO 4

709 C BARCLAYS 2

737 C ADVANTAGE 1 2

800 C MAREX SPEC 2

____________________________________________________________________________________________

TOTAL: 32 32

MONTH TO DATE: 90

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 32 NOTICE(S) FOR 3200 OZ (0.0995 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 90 NOTICES FOR 9000 OZ (.2799 TONNES)

SILVER

FOR MAY

45 NOTICE(S) FILED TODAY FOR 225,000 OZ/

total number of notices filed so far this month: 261 for 1305,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ N/A

Bitcoin: FINAL EVENING TRADE: $ N/A

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A CONSIDERABLE SIZED 2615 CONTRACTS FROM 212,579 DOWN TO 20,964 DESPITE THE 6 CENT GAIN IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER AND IT STOPPED FOR GOLD AS WELL. WE WILL WITNESS A RISE IN THE SPREADERS IN SILVER ONCE WE START TRADING IN JUNE… READY FOR THE FIRST DAY NOTICE JULY CONTRACT.) TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 2185 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2185 CONTRACTS. WITH THE TRANSFER OF 2185 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2185 EFP CONTRACTS TRANSLATES INTO 10.925 MILLION OZ ACCOMPANYING:

1.THE 6 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.330 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

2185 CONTRACTS (FOR 1 TRADING DAYS TOTAL 2185 CONTRACTS) OR 10.925 MILLION OZ: (AVERAGE PER DAY: 2185 CONTRACTS OR 10.925 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 10.924 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.428% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 903.03 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2615 DESPITE THE 6 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A VERY LARGE SIZED EFP ISSUANCE OF 2185 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE LOST A SMALL SIZED: 500 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2173 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 2615 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 6 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.59 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.053 BILLION OZ TO BE EXACT or 150% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 45 NOTICE(S) FOR 225,000, OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.330 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY AN UNBELIEVABLE SIZED 21,846 CONTRACTS, TO 465,977 WITH THE $17.10 PRICE GAIN WITH RESPECT TO COMEX GOLD PRICING FRIDAY// YESTERDAY/THE SPREADING LIQUIDATION HAS STOPPED AND THESE GUYS WILL MORPH INTO SILVER ONCE JUNE GETS UNDERWAY. THE GAIN IN OI GOLD CONTRACTS IS REAL AND NOT PUMPED UP BY SPREADING.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 15,085 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 15,085 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 465,077. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 36,931 CONTRACTS: 21,846 OI CONTRACTS INCREASED AT THE COMEX AND 15,085 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 36,931 CONTRACTS OR 3,693,100 OZ OR 114.87 TONNES. FRIDAY WE HAD A GOOD GAIN OF $17.10 IN GOLD TRADING….AND WITH THAT GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 114.87 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

WITH RESPECT TO SPREADING: WE HAD ZERO ACTIVITY OF THE SPREADERS//

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 15,085 CONTRACTS OR 1,508,500 OR 46.92 TONNES (1 TRADING DAYS AND THUS AVERAGING: 15,085 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAYS IN TONNES: 46.92 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 46.92/3550 x 100% TONNES =1.32% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2324.84 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: AN UNBELIEVABLE SIZED INCREASE IN OI AT THE COMEX OF 21846 WITH THE PRICING GAIN THAT GOLD UNDERTOOK ON FRIDAYDAY($17.10)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 15,085 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 15085 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC SIZED GAIN OF 36,931 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

15,085 CONTRACTS MOVE TO LONDON AND 21,846 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 114.87 TONNES). ..AND THIS GAIN OF DEMAND OCCURRED WITH THE RISE IN PRICE OF $17.10 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING LIQUIDATION //FRIDAY /TODAY/

we had: 32 notice(s) filed upon for 3200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $17.50 TODAY//SEEMS THE BOYS FOUND RELIGION

A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A HUGE “PAPER” GOLD DEPOSIT OF 2.35 TONNES

INVENTORY RESTS AT 743.21 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 19 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 312.038 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY AN CONSIDERABLE SIZED 2615 CONTRACTS from 212,579 DOWN TO 210,267 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER AND GOLD FOR NOW BUT WILL NOW MORPH INTO SILVER AS THE COMEX SILVER MONTH OF JUNE COMMENCES IN EARNEST..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 2185 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2185CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2615 CONTRACTS TO THE 2185 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 500 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 2.500MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 1.260 MILLION OZ FOR JUNE.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 6 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2185 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 8.62 POINTS OR 0.30% //Hang Sang CLOSED DOWN 7.23 POINTS OR 0.03% /The Nikkei closed DOWN 190.31 POINTS OR 0.92%//Australia’s all ordinaires CLOSED DOWN 1.25%

/Chinese yuan (ONSHORE) closed UP at 6.9072 /Oil DOWN TO 54.12 dollars per barrel for WTI and 62.58 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED UP // LAST AT 6.9072 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9250 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/Fed=ex

We highlighted to you China’s anger of the “misplacing of two pkgs destined for China’s Huawei. Now China is investigation what happened as well as giving warning to foreign companies.

( zerohedge)

ii)And the next domino to fall: Bank of Jinzhou with total assets of 105 billion USA

4/EUROPEAN AFFAIRS

i)EUROPE/ITALY

Luongo outlines the roadmap that Salvini faces with respect to coalition partner 5 star and the ERU

( Tom Luongo)

ii)Michel Barnier talks of lies when he talks about Great Britain and their Brexit strategy.

iii)GERMANY

iv)UKTrump now endorses Boris Johnson and also says that Farage should lead the Brexit talks

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Israel

The USA has confirmed that it has now updated its maps showing the disputed Golan Heights, the property of Israel.

( zerohedge)

i b)Israel

ii)IRAN/SAUDI ARABIA/ISRAEL

iii)Russia/Malaysia/Holland

iv)ISRAEL/SYRIA

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

This is a major blow to Maduro as a major Russian defense contractor exits Venezuela and it appears that this contractor has withdrawn most of its advisers. This is a broad signal of a major Russia exit form a defense supporting the Maduro government.

(zerohedge)

ii)INDIA/USA

Now it is India’s turn to face the wrath of Trump. Trump now signals that he wants to end India’s designation as a developing nation as he continues with his protectionist policies..

(courtesy zerohedge)

iib)First India and now Trump is considering Australia. Soon Trump will hit the entire globe with tariffs

(courtesy Mish Shedlock/Mishtalk)

9. PHYSICAL MARKETS

a)A GOOD COMMENTARY BY TED BUTLER. He explains how JPMorgan while being the largest short in silver acquired a massive 850 million oz of silver.

(courtesy Ted Butler/GATA)

b)A good commentary from the South China Morning Post in Hong Kong. Here the paper wonders if China has enough USA dollars on its balance sheet to survive a trade war

( SCMP/GATA)

c)The Malaysian prime Minister wants a gold backed currency: will the uSA try and overthrow him?

( RT/GATA)

d)In Britain, you can invest in gold and pay no capital gains tax if you sell

(London Telegraph/Williams)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

Market trading/last night/Shanghai initial trading 8 pm est

Key data points : 8 pm

usa dollar vs cny: 6.9080

usa dollar vs cnh: 6.9380

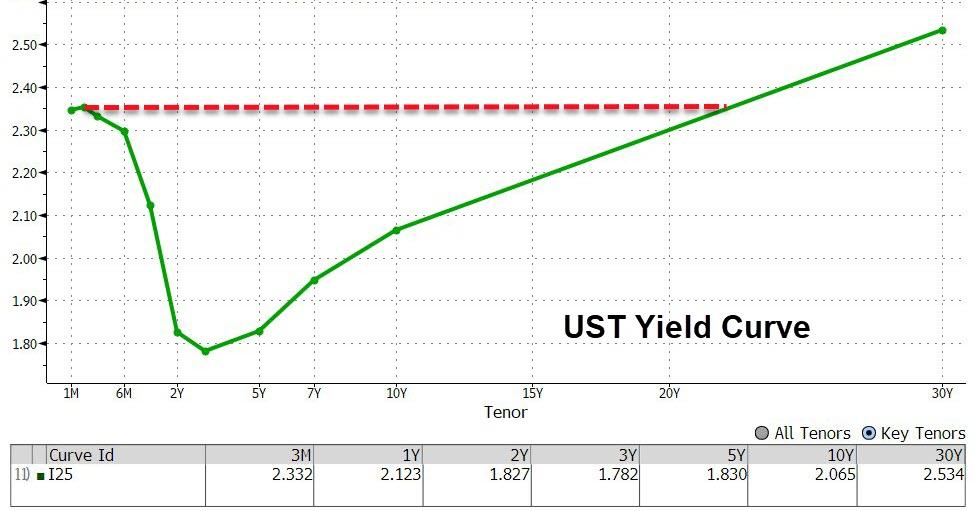

usa 10 yr bond yield: 2.12… deadly//

Trump continues with protectionist policies.

ii)Market data

iii)USA ECONOMIC/GENERAL STORIES

a)Trump declares war on the Silicon Valley: the dept of Justice is launching an atin monopoly probe on Google due to its huge number of purchases of over 200 start ups.

It looks like the remedy will be a blockage of purchases for Google as opposed to the EU which fined the company in the billions

( zerohedge)

b)Monday morning/Google to open down 3%

b ii)And now the Federal trade Commission opens up a competition probe against Facebook

b iii)AND NOW APPLE ON REPORTS OF A DEPT OF JUSTICE ANTI TRUST PROBE(COURTESY ZEROHEDGE)

c)As if Boeing does not have enough problems: Now the FAA is ordering Boeing to replace wing components on hundred of Boeing 737’s(zerohedge)

e)Why is Trump angry with Huawei? It is not that Huawei is spying on the USA but Huawei will not let the USA spy on the rest of the world with Huawei technology. Also the reason for the Mexican tariffs is to stop Chinese goods coming into Mexico and then re importing to the USA(courtesy Tom Luongo)

f)Trumps calls for a A T and T boycott to force big changes at CNN

SWAMP STORIES

( Steve Cohen/N.Y.University)

ii)Two important points here:

quite a story…

the report:

iii)The GOP now are targeting both Brennan and Comey as the investigation heats up

( zerohedge)

Let us head over to the comex:

Gold withdrawals;

i) We had 1 withdrawal:

out of Delaware: 999.99 oz

.

Gol

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

A GOOD COMMENTARY BY TED BUTLER. He explains how JPMorgan while being the largest short in silver acquired a massive 850 million oz of silver.

(courtesy Ted Butler/GATA)

Ted Butler: The CFTC’s summer camp letter

Submitted by cpowell on Fri, 2019-05-31 15:33. Section: Daily Dispatches

11:30a Friday, May 31, 2019

Dear Friend of GATA and Gold:

Silver market analyst and market rigging critic Ted Butler today makes good fun of the U.S. Commodity Futures Commission’s refusal to answer questions about seemingly improper activity in the monetary metals futures markets. Butler’s commentary is headlined “The CFTC’s Summer Camp Letter” and it’s posted at GoldSeek’s companion site, SilverSeek, here:

http://silverseek.com/commentary/cftc%E2%80%99s-summer-camp-letter-17657

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

end

The CFTC’s Summer Camp Letter

|

May 31, 2019 – 8:25am

About 30 years ago, my wife arranged for our then ten-year old son to attend a sleep-away YMCA summer camp in Tallulah Falls, in the Georgia Mountains. While Ross wound up going back to the same camp for several years, eventually serving as a counselor, I knew the first year would involve more than a little concern for his mother (and me) for how he was doing. Since the only communication would be by postal mail (no cellphones or texting back then) and I knew my son was not likely to write without some prodding, I sent him off with a number of pre-printed letters, in which all he had to do was fill in the blanks.

I can’t say my mail assistance appeared constructive upon receiving Ross’ first letter, as he indicated that he made no new friends, the weather was rotten, as was the food and his camp counselor wasn’t nice – all in addition to him having no fun. Fortunately, subsequent letters were progressively better and, as I indicated, the camp turned out to be a great experience for years to come. I also recollect how he told us later about a kid who cried every night going to sleep because he missed his parents. Asked on the last night why he was crying since he was going home the next day, the kid responded because he was going to miss the camp.

Given the CFTC’s abject failure to respond to simple questions about how commodity prices are being set through speculative futures positioning, I thought it might be instructive to attempt to make it as simple as possible for it to answer – in a fill in the blank and multiple choice format. The attempt is not to put words in the agency’s mouth, but just help it address the important issues at stake. Feel free to send along any you might wish to add.

- The main purpose of futures trading is to allow (real producers and users to hedge price risk or large paper speculators to make bets). An alternative default answer to all questions is we don’t know or haven’t looked or JPMorgan told us not to look.

If the answer to #1 is to allow real producers and users and to hedge price risk, then why are there no real producers and users present in COMEX silver futures and managed money speculators are the largest single category?

If the answer to #1 is we don’t know or haven’t thought about that, then go back to sleep and forget the rest of the quiz. If the answer to #2 is because JPMorgan told us not to look, then proceed.

- 2. Data published by your agency indicates that JPMorgan has been the biggest short seller in COMEX silver futures since acquiring Bear Stearns in 2008 and, further, that it has never taken a loss, only profits in COMEX silver futures. Is this true?

If the answer to #2 is we don’t know/haven’t looked, then take an Ambien and try to get back to sleep. If the answer is because JPMorgan told us not to look, then proceed.

- Since 2011, JPMorgan has amassed, all while remaining the biggest short seller in COMEX silver futures, the largest hoard of physical silver in history, some 850 million oz. Does the CFTC find it all odd or even potentially illegal for the same entity to be both the largest paper short seller and physical acquirer of the same commodity?

If the answer to #3 is we don’t know/haven’t looked, then take two more Ambien and count backward from 10,000 until unconsciousness sets in. If the answer is because JPMorgan told us it wasn’t necessary to ask or look, then schedule another junket to Boca Raton and update your employment application to JPM.

- Final question – what does the agency do all day? (Try to look relevant, give speeches, make sure we’re not deviating from what JPMorgan wishes, try to get some sleep).

I hope no one takes me to mean that any of this is humorous, because nothing could be more serious than if prices of important commodities are being set artificially. And it’s not just silver, but many other important commodities, like crude oil, corn, soybeans and cotton, to name just a few. All these commodities and more share a manipulative common denominator, namely, the participation and market share of the managed money technical funds have grown so large that only those not looking (or willfully blind) can fail to see it. A few examples.

About a month ago, the most important US crop, corn, was trading close to multi-year lows ($3.50 per bushel). At that time, the managed money technical funds held their largest net and gross short position in history (the CFTC began publishing managed money positions in late 2009). The gross short position of the 105 traders on the short side of Chicago Board of Trade (owned by the CME Group) on April 23 was 530,000 contracts or 2.65 billion bushels of corn, an average of more than 5000 contracts per trader (25 million bushels).

As of last Tuesday, May 21, corn had rallied to nearly $4 per bushel (more since then) as the managed money traders bought back 190,000 contracts of gross shorts (and even more on a net basis). Yes, I’m aware of corn prices declining as a supposed consequence of the trade war and rising because of very late historical planting progress (due to the flooding in farm country). But can anyone seriously doubt the price influence of record managed money shorting at the price lows and the 250,000 net contracts of buying by managed money traders on the rally? I mean, anyone apart from the CFTC and CME Group? And yes, corn prices penetrated the key moving averages on the way down and way up.

In soybeans (another CBT/CME market), prices fell to 10-year lows, penetrating $8 per bushel earlier this month. As of May 7, the managed money traders held a record net and gross short position in soybeans, with a gross short position of more than 223,000 contracts (1.1 billion bushels) held by 100 traders. Prices have rallied sharply since then but, unlike corn, it’s too soon to see how much managed money short covering has and will take place. Yes, I know that soybeans have been at the center of the trade war dispute with China, but can anyone fail to see the connection between record price lows and record high managed money short positions? (Excepting the CFTC and CME).

Finally, cotton is also a very important US crop and has also traded close to multi-year price lows, falling close to 15 cents per pound to 65 cents in early May in a matter of weeks. The managed money technical funds were, of course, the big sellers and short sellers on that price smash and as of last Tuesday, May 13, held their largest net and gross short position in history. Can anyone fail to see the connection between record large managed money short positions and record to near-record low prices? It’s not just silver investors and miners taking it on the chin, thanks to the still sleeping, good for nothing regulators at the CFTC, the American farmer is getting hammered as well.

And just so no one thinks I’m just barking at the moon about something that can’t possibly be fixed, let me assure you that the solution to the managed money traders building up such massive short and long positions that it distorts prices is quite simple. The solution is legitimate speculative position limits. Let’s face it, everyone (including the CFTC) agrees that the managed money traders are speculators, pure and simple. Therefore, the solution is legitimate speculative positions on the managed money technical funds.

Since the technical funds operate as one, buying and selling when prices penetrate moving averages, those traders abiding by this particular strategy, must be consolidated and assigned position limits that reflect the aggregate position of the technical funds. The problem is not that many individual managed money technical funds build up long and short positions that are far in excess of what would be considered excessive on an individual basis. The problem is that collectively they build up such large collective positions that do distort prices – as outlined above.

Assigning individual position limits doesn’t do much good if there are many traders following the exact same strategy – as is evident from the record collective positions. The solution is to assign speculative position limits that apply to the technical funds collectively. Sure, the CME Group will scream because this might cut into its trading revenue, but what’s more important – profits for the CME or the financial well-being of real producers, like the American farmer? It’s mindboggling to me that I believe I am the only one pointing this out. And not for a minute am I forgetting that the massive and excessive managed money positions are put on and taken off with a large measure of influence from their commercial counterparties. That’s little solace to a real producer whose cost of production exceeds a corn or cotton price driven down by record managed money shorting.

Of course, as egregious and manipulative as the collective managed money positions have become in just about every commodity, none compare to COMEX silver futures. As of last Tuesday, May 21, the gross short position of the managed money traders in COMEX silver futures was 81,988 contracts, just shy of 410 million oz, and held by 47 traders or more than 8.7 million oz per trader. I would not at all be surprised if this short position is even larger when the new COT report is published on Friday, but I doubt it will exceed the record managed money gross short position of 104,482 contracts of last Sept 4, held by 62 traders. It is interesting that last week’s managed money short position was larger per trader than back on Sept 4.

410 million oz is roughly half of total world annual silver mine production. No other commodity, not crude oil, corn, soybeans or cotton come close to rivalling the amount of managed money buying or selling in real world terms as exists in silver. For instance, the recent record gross short position in corn is less than 10% of world corn production and extreme managed money long or short positions in crude oil rarely exceed a percent or two of annual world oil production. Purely speculative traders shouldn’t be allowed to hold such large positions which clearly affect prices, but COMEX silver futures positioning is in a league of its own.

What makes the situation even more egregious is that of the 47 managed money traders holding 410 million oz of silver short, half the world’s annual mine production, not a single ounce represents a legitimate hedge of any kind, just a rank speculation. For the umpteenth time, I am not opposed to speculation (I’m a speculator myself); I’m opposed to speculators dictating prices to the world’s real producers and consumers. I’m not trying to trick anyone when I ask this simple question – would the price of silver be higher or lower if there didn’t exist 47 speculators holding 410 million oz short? I’m not asking you to pick a specific price, just whether the price would be higher or lower. Only a wise guy (or a drug-induced sleeping regulator) would fail to conclude higher prices. That, my friends, is conclusive proof of manipulation.

To complete the story, the prime counterparties to the managed money traders in COMEX silver (and gold) have been commercial banks, led by JPMorgan. But based upon Bank Participation report data, these commercial banks, particularly U.S. banks, are not especially prominent players in crude oil, corn, soybeans, cotton and most other commodities – just precious metals. Therefore, while I publicly assail JPMorgan as being the big silver and gold manipulator and crook, I see scant evidence of JPM’s involvement in other commodities. No doubt that the managed money traders are being led by the price nose into and out from the extreme positions they hold by traders called commercials – just that the commercials in this case are not primarily banks and JPMorgan. Fair is fair.

On the other hand, I doubt JPMorgan could have affected its brilliant stroke of (criminal) genius in other commodities that it has pulled off in silver and gold. Of course, I’m referring to JPM’s almost unbelievable physical accumulation of 850 million oz of silver and more than 20 million oz of gold. It would be impossible to amass anywhere near equivalent physical quantities of any other commodities. For starters, there would be no place to store such quantities – not a problem for silver or gold. And make no mistake, JPM’s physical silver and gold holdings will make all the difference in the world at some point, particularly considering that JPMorgan has now completely eliminated its COMEX silver short position.

Ted Butler

May 31, 2019

END

The Malaysian prime Minister wants a gold backed currency: will the uSA try and overthrow him?

(courtesy RT/GATA)

Will the U.S. now try to overthrow Malaysia’s prime minister too?

Submitted by cpowell on Fri, 2019-05-31 23:30. Section: Daily Dispatches

‘Gold Is More Stable’: Malaysia Needles U.S. with Proposal for Pan-Asian Bullion-Backed Currency

From Russia Today, Moscow

Friday, May 31, 2019

Malaysian Prime Minister Mahathir Mohamad has floated the idea of creating a gold-backed common trading currency for all of East Asia, slamming regional currency exchange as “manipulative” and criticizing the United States’ heavy-handed foreign policy. …

Libyan leader Muammar Gaddafi proposed a pan-African gold dinar that would be used to sell the country’s oil on the world market in 2009, less than two years before his government fell to a NATO-backed regime change operation that has left the once-prosperous nation a conflict-ridden war zone.

…

One of the “moderate” rebels’ first actions upon brutally murdering Gaddafi was to create a central bank to replace the state-owned monetary authority that had previously managed Libya’s wealth.

The United States has historically not taken kindly to countries that attempted to trade oil in non-dollar currencies, as Iraq’s Saddam Hussein can attest — or could, if he hadn’t been regime-changed as well.

Syria too dropped its peg to the dollar in 2007, not long before the West went from awarding Bashar al-Assad the French medal of honor to declaring him a bloodthirsty monster.

… For the remainder of the report:

https://www.rt.com/business/460698-malaysia-proposes-gold-forex-currency…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

For your interest…

Dawson City tourism group plans to scatter gold to trigger second gold rush

Submitted by cpowell on Sun, 2019-06-02 02:48. Section: Daily Dispatches

By Sidney Cohen

Canada Broadcasting Corp., Toronto

Saturday, June 1, 2019

A Dawson City tourism group wants to reboot the most storied period in Yukon’s history.

The Klondike Visitors Association is pitching Gold Rush 2: a tourism campaign that would offer a gold-rush-esque experience to visitors of the town famous for wealth and debauchery at the turn of the century.

…

The association hopes to crowd-fund $100,000, which it will use to buy “real Klondike gold.” That gold will then be scattered along the banks of Bonanza Creek to simulate a modern-day bonanza.

You read that correctly.

The tourism group wants people to pay for gold that will be tossed into the river.

Its goal is to lure visitors up to Dawson to pan for gold themselves. …

… For the remainder of the report:

https://www.cbc.ca/news/canada/north/dawson-gold-rush-revival-1.5157613

END

A good commentary from the South China Morning Post in Hong Kong. Here the paper wonders if China has enough USA dollars on its balance sheet to survive a trade war

(courtesy SCMP/GATA)

Does China have enough U.S. dollars to survive the trade war?

Submitted by cpowell on Sun, 2019-06-02 02:58. Section: Daily Dispatches

By Karen Yeung

South China Morning Post, Hong Kong

Friday, May 30, 2019

The Chinese government is officially sitting on the world’s largest stockpile of foreign exchange reserves, but it has been scrambling recently to block backchannels for capital outflows as trade tensions with the United States increase.

Beijing’s increasing scrutiny of the use of the U.S. dollar by Chinese companies and individuals, in the absence of any immediate signs of a financial crisis, along with accelerating efforts to lure in foreign capital, have raised suspicions among analysts that the world’s second-largest economy is worried about the risk of running short of the U.S.

…

On the surface, China should be the last country to worry about a shortage — about two-thirds of its U.S.$3.1 trillion worth of foreign exchange reserves, the world’s largest, are believed to be held in U.S. dollar-denominated assets.

But the huge foreign reserves and a relatively stable currency do not reflect the true stresses underlying the economy, analysts said, because the concerns are that those reserves may not be enough to provide the safety buffer needed to pay for China’s imports and pay off its debt in adverse circumstances if the yuan faced a devaluation or a sharp drop in value. …

… For the remainder of the report:

https://www.scmp.com/economy/china-economy/article/3012460/does-china-ha…

END

In Britain, you can invest in gold and pay no capital gains tax if you sell

(London Telegraph/Williams)

How to invest in gold and pay no capital gains tax in the UK

Submitted by cpowell on Mon, 2019-06-03 01:14. Section: Daily Dispatches

By Adam Williams

The Telegraph, London

Sunday, June 2, 2019

In turbulent times, investors traditionally turn to gold. Its appeal is a lack of correlation between its price and those of other assets. But gold is often held for decades, often leading to a hefty tax bill when the owner comes to sell.

Yet a loophole exists that allows gold investors to dodge capital gains tax altogether. The tax is not applied to any British legal currency, which means that gold sovereigns, gold Britannia coins and silver Britannia coins are exempt, regardless of how much they increase in value.

…

Those who invest in gold bars, by contrast, are liable to pay tax on their profit, potentially costing them thousands of pounds. While the initial purchase price of sovereigns is slightly higher, the tax break means long-term savings can be considerable.

Rob Halliday-Stein of BullionByPost, a gold dealer, said: “For wealthy individuals looking to realise large profits from their investment, sovereigns represent the best value.”

The price of gold bars and sovereigns is broadly the same, at between L1,050 and L1,070 an ounce, although it fluctuates over time. Older gold coins are typically sold at a premium as they have historical value in addition to the cost of the precious metal itself.

This premium can grow significantly over time if a coin becomes scarce.

Mr. Halliday-Stein added: “Gold bullion coins have commanded large premiums in the past, depending on market factors at the time. In the 1960s there was a premium of up to 40 percent on gold sovereigns.”

The Royal Mint is currently selling a rare 200-year-old George III gold sovereign for L100,000. It was minted in 1819 and there are thought to be just 10 left in the world. …

… For the remainder of the report:

https://www.telegraph.co.uk/money/consumer-affairs/invest-gold-pay-no-ca…

* * *

end

Good Morning Bill/Harvey,

Today is the first working day of June so (big drum roll) the ‘transparent’ LBMA has now released the particulars of total loco London vault gold holdings as at 28th February 2019.A minute ago the Deutsche Bank share price was quoted at Euro 5.89 (a new recent low).A banking analyst would examine the most recently promulgated data re assets/liabilities/contingent liabilities/value of derivative contracts etc. in order to make an informed determination as to whether this 5.89 is a fair price or whether NIL would be more appropriate value for a Deutsche Bank share.

When it comes to the LBMA, we are expected to be appreciative of this new ‘transparency’, but it is more in the realms of complete disinformation because there is absolutely no disclosure concerning all the claims on this loco London vault gold. What is the use of any information on Deutsche Bank’s assets, if it has to be reviewed in a total vacuum of information relating to liabilities? I recently read that, at a price of $18,000 , more detailed monthly information can be obtained in respect of LBMA monthly trading volumes. What an absolute farce! All disclosed LBMA particulars of physical vault gold are metronomically stable, so the gross value of LBMA trading nets out to a zero sum game of mere farcical churning of paper contracts. Maybe a dribbling of physical gold supply does enter/leave the LBMA in a particular month, but is this single piece of data worth $18,000? If one assumes that all LBMA trading is merely the churning of paper contracts in a zero sum game, how incorrect can such a base case assumption be given that month end vault gold holdings never fluctuate more than microscopic amounts.

Nicholas

-END-

Our resident expert on silver exports/production Steve St Angelo provides a great commentary on the huge importation of silver by India

(courtesy Steve St Angelo)

U.S. Silver Exports To India Explode Past Six Months

While silver investment demand in the West continues to remain weak, Indians are purchasing the white shiny metal hand over fist. In just the past six months, U.S. silver exports to India have exploded to record highs. Yes, there is no better way of putting it if we compare how little silver India imported from the United States during the previous six month period.

Furthermore, according to the Metals Focus Consultancy, they forecast even stronger Indian silver demand in 2019 due to rural Indians spending their “Cash Handouts” from the government to assist local economies ahead of the President’s election. How interesting. When Americans receive a government check in the mail, they use it to buy more throw-away crap they don’t need. However, many Indians use it to purchase silver as an investment.

Regardless, the chart below shows just how much silver the U.S. has exported to India over the past six months;

From March to August 2018, U.S. silver shipments totaled a paltry two metric tons. Now, compare that to the 517 metric tons from September to February 2019. Even if we include U.S. silver exports to India for Jan-Feb 2018, it only amounted to 1.2 metric tons. So, as we can see from the data above, there is extremely high demand for silver in India.

Now, if we look at the total annual U.S. silver exports for the past several years, the change in Indian demand is even more striking:

Total U.S. silver exports were 289 metric tons (mt) in 2016 and fell to 157 mt in 2017. Then due to the enormous increase in Indian silver demand, total U.S. silver exports surged to 604 mt in 2018. However, if we remove the “Indian component” in 2018, total U.S. silver exports would have only been 205 mt in 2018.

Moreover, the 517 mt of U.S. silver exports to India for the past six months was nearly double the total exports in 2016 and more than triple that of 2017. While it’s true that this huge increase in Indian silver demand hasn’t impacted the price yet, wait until the economy and financial system start to really come apart over the next few years.

Today, as the markets continue to sell off due to more Trade Wars with Mexico, gold and silver are in the green. Even though gold is outperforming silver today, they are doing exactly as I predicted during significant market downturns. And, I believe this is only the beginning of an even greater dislocation between the overall markets and precious metals in the years ahead.

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

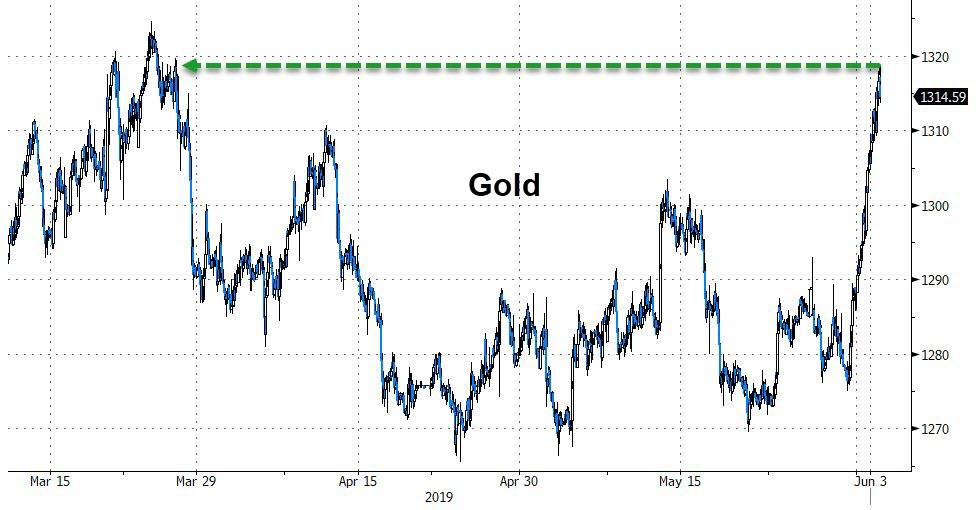

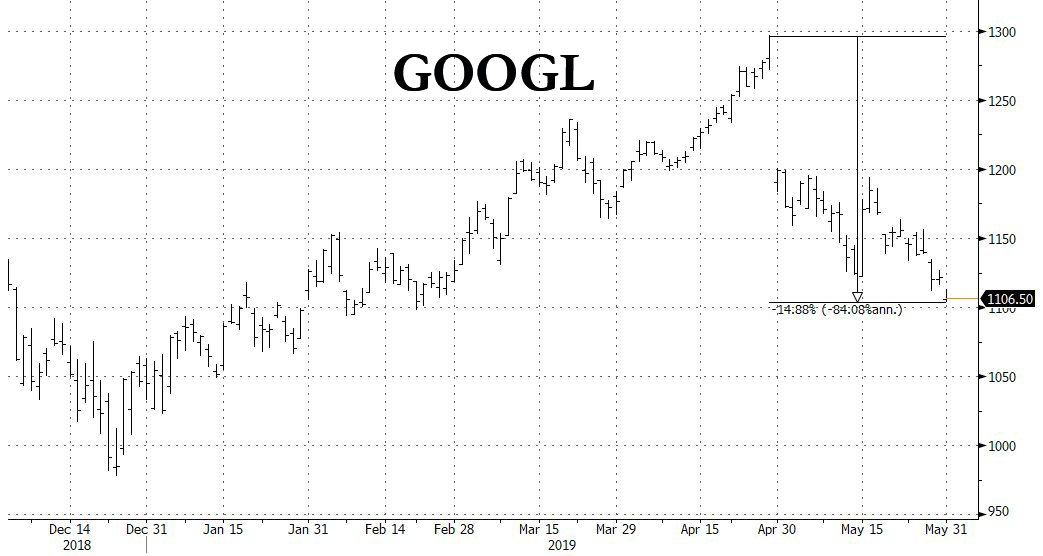

Gold Surges Above “Key Pivot”, Hits 3-Year High Against Yuan

Gold futures prices are up $45 in the last two trading days, bursting through the $1300 Maginot Line, and surging to the highest since March (in USDollars).

Silver is also on a good run…

But Gold’s outperformance continues, with Gold/Silver ratio near 90.0x – the highest since 1993…

Goldman earlier highlighted $1307 as a key pivot in gold. Their bias was for that level of resistance to hold but instead it broke and gold is up significantly the second consecutive day of large gains.

“Getting through 1,307 would allow for a minimum next level target at 1,330. The broader implications of that break would however support the view that Gold might finally be continuing a trend that stalled in January,” they wrote.

However, in Yuan, gold is near 3-year highs, as the quasi-peg has officially broken…

END

* * *

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9072/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9250 /shanghai bourse CLOSED DOWN 8.62 POINTS OR 0.30%

HANG SANG CLOSED DOWN 7.23 POINTS OR 0.03%

2. Nikkei closed DOWN 190.31 POINTS OR 0.92%

3. Europe stocks OPENED RED /

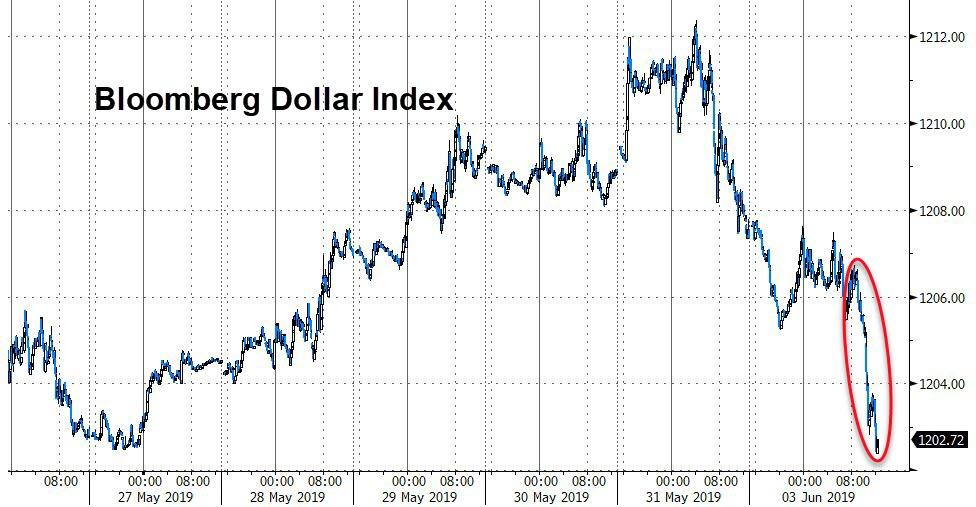

USA dollar index FALLS TO 97.65/Euro RISES TO 1.1187

3b Japan 10 year bond yield: FALLS TO. –.09/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.32/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.12 and Brent: 62,58

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.21%/Italian 10 yr bond yield DOWN to 2.62% /SPAIN 10 YR BOND YIELD DOWN TO 0.71%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.83: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.88

3k Gold at $1317.00 silver at: 14.70 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 20/100 in roubles/dollar) 65.37

3m oil into the 54 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.72 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9986 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1167 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.21%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.10% early this morning. Thirty year rate at 2.56%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8774..they are toast

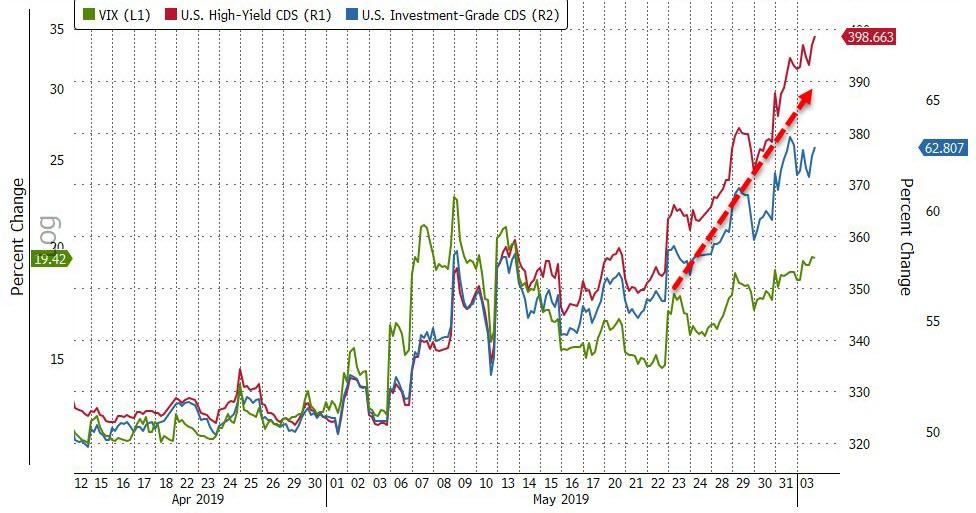

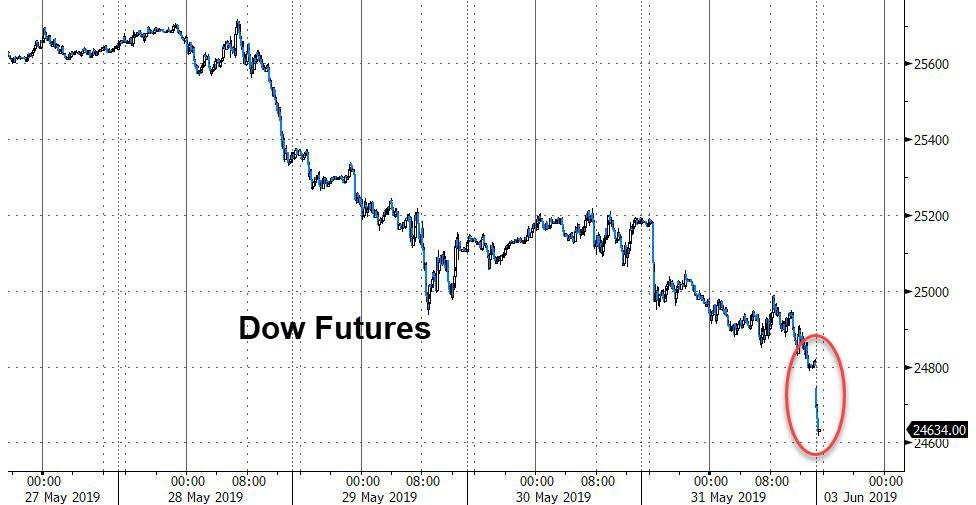

“Sea Of Red” For Global Markets As Traders Brace For Recession Amid Global Trade War

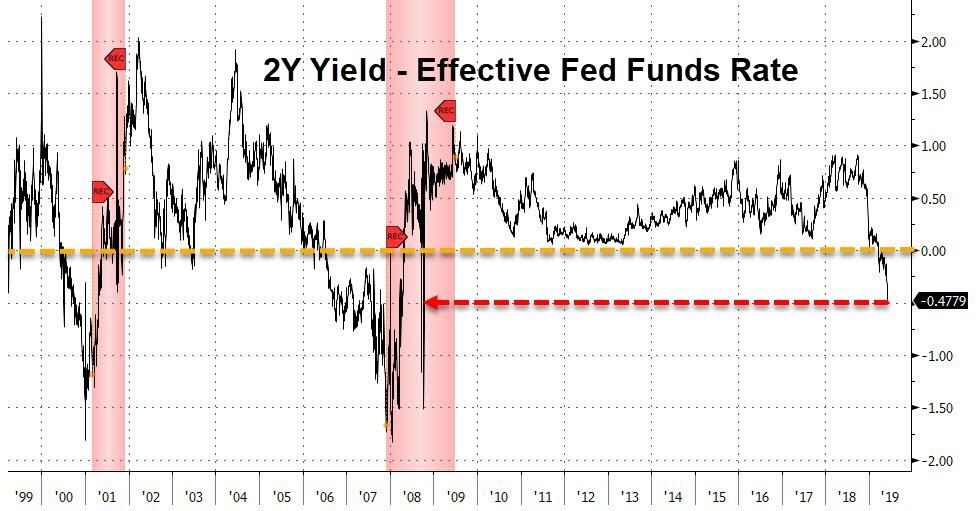

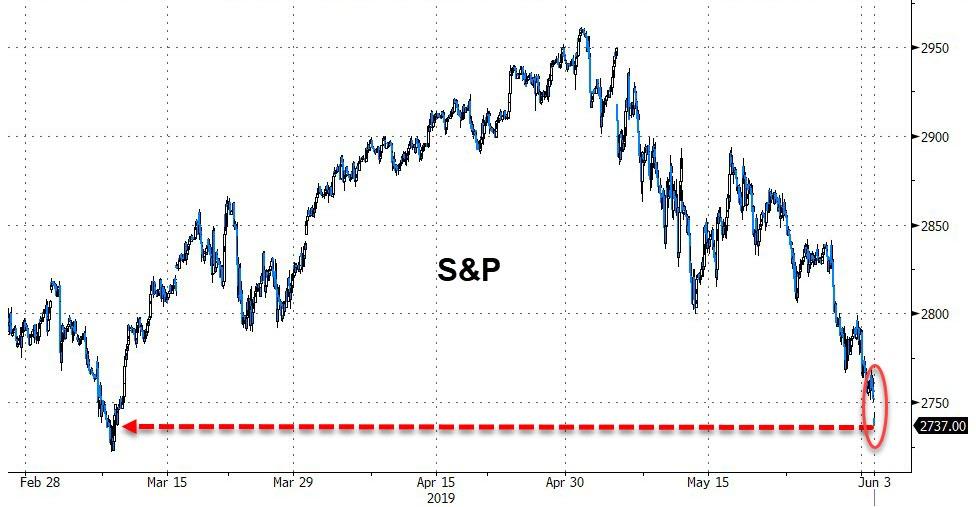

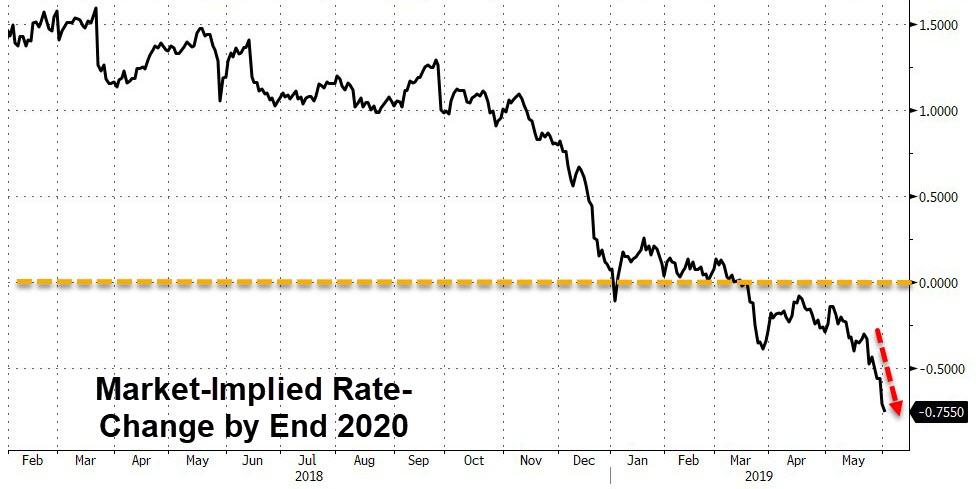

Global stocks continued to slide and investors sought the safety of government bonds, the yen, the Swiss franc and gold on the first trading day of June as rising trade tensions sparked fears of an upcoming recession (which according to Morgan Stanley will hit in 3 quarters or less, while JPMorgan said the probability of a U.S. recession in the second half of 2019 had risen to 40% from 25% a month ago) denting stocks again…

… sending the 10Y TSY yield as low as 2.07%, the lowest level in almost 21 months, after JPMorgan said it now expects the 10Y yield to drop to 1.75% by year end…

… pushing the inversion between the 3M and 10Y yield to a whopping 28 bps…

… and sending oil sliding close to bear market territory.

With no improvement in tone or sentiment between the US and China, and in fact with China striking a combative tone on Sunday, blaming the U.S. for the collapse in trade talks and saying it won’t be pressured into concessions after the White House rattled markets Friday by announcing tariffs on Mexican goods, the worsening trade and broader economic backdrop made for a jarring start to June after a torrid May that wiped $3 trillion off global equities.

Also over the weekend, China’s Defence Minister Wei Fenghe warned the United States not to meddle in security disputes over Taiwan and the South China Sea, after acting U.S. Defence Secretary Patrick Shanahan said Washington would no longer “tiptoe” around Chinese behaviour in Asia.

“We’re in a phase of brinkmanship — it’ll be a difficult month,” Rob Mumford, an emerging market portfolio manager at GAM Investments, said at a roundtable in Hong Kong. “We’re at the maximum pressure.”

US equity index futures all pointed to a drop at the open, though losses were pared modestly from earlier in the session. In Europe, the Stoxx 600 Index also came off its lows, with gains in food and healthcare shares offsetting declines in banks. European shares fell further and the Swiss franc jumped to a two-year high as Beijing sent another shot across Washington’s bows on trade and then euro zone data came in weak though the main groundswell was in bonds.

“No one now thinks a deal would be possible at the G20. It is going to be a prolonged battle. Investors are rushing to the safe assets,” Mitsubishi’s Fujito said.

German government bond yields dropped to a new record all-time lows of -0.219%, while those on two-year U.S. Treasuries were seeing their biggest two-day fall since early October 2008, when the global financial crisis was kicking off.

“Bonds are more or less on fire and I think we are going to spend the week with trade dominating everything else,” said SocGen fx strategist Kit Juckes. With German and UK political concerns and worries about Italy’s finances resurfacing too, “it is hard to think the yen is not going to be at least one of the winners this week.”

There was not flight to safety for Deutsche Bank, whose stock dropped to a new all time low, sliding below €6.00 for the first time ever after JPMorgan said DB’s issue is not about capital or liquidity but about poor operating profitability and it needs to stop “tinkering with its restructuring efforts.” The German bank “needs to make objective decisions about what business and/or asset can be closed or reduced”, JPM’s Kian Abouhossein and Amit Ranjan wrote, adding that CEO Sewing is “up to the challenge” to take action against status quo as he is over-delivering on cost targets. One look at the chart below suggests the market disagrees.

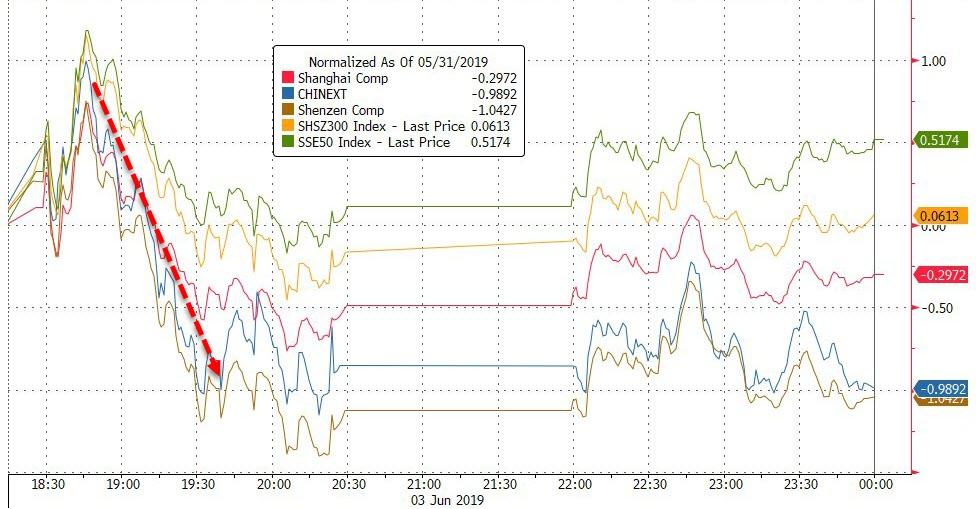

Asian stocks reversed an earlier decline as utilities and IT stocks boosted the regional index. Markets in the region were mixed. South Korea’s Kospi index and India’s S&P BSE Sensex Index rose, while Japan’s Topix index and Australia’s S&P/ASX 200 fell. The MSCI Asia Pacific Index climbed 0.2% in Hong Kong. The Kospi closed 1.3% higher, with Chasys Co. and Heung-A Shipping Co Ltd leading gains. India’s S&P BSE Sensex Index advanced 1.2%, led by basic materials and technology shares. Chinese shares ended little changed though the yuan faced pressure.

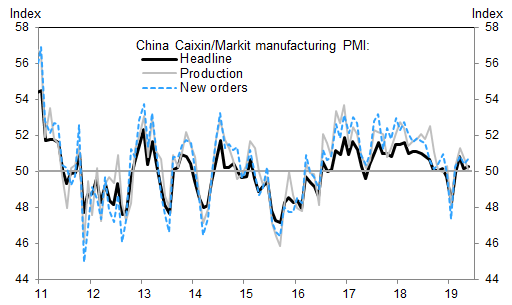

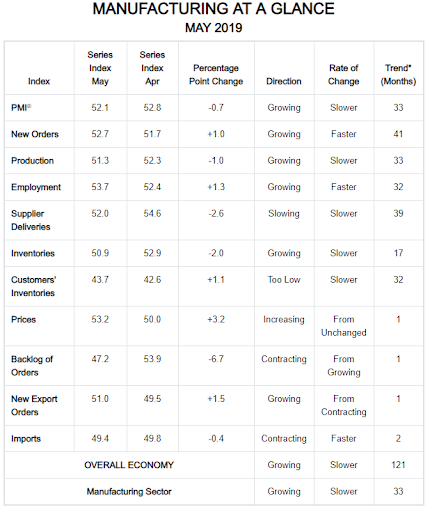

A private survey of China’s manufacturing sector published on Monday suggested a modest expansion in activity as export orders bounced from a contraction. In contrast to the fall in NBS manufacturing PMI, the Caixin manufacturing PMI was unchanged in May at 50.2, and above the 50.0 expected, although sub-indexes suggested weaker production, higher inventories and stronger new orders. Business confidence appeared to have deteriorated in light of lingering trade tension with the US.

Additionally, economists noted increases in new export orders pointed to possible front-loading of U.S.-bound shipments to avoid potential tariff hikes that U.S. President Donald Trump – who kicked off a potentially confrontational state visit to Britain on Monday – had threatened to slap on another $300 billion of Chinese goods. “Chinese companies probably see the current export conditions as severe as during the China shock in 2015,” said Wang Shenshen, economist at Tokai Tokyo Research Center.

And speaking of economic headwinds, with the bitter trade weighing, factory activity contracted in most Asian countries and the euro zone last month, the latest PMI surveys showed. The eurozone’s slowdown was for the fourth month running, and at an accelerating pace, as slumping automotive demand, Brexit and wider political uncertainty took their toll. “The sector remains in its toughest spell since 2013,” said Chris Williamson, chief business economist at IHS Markit.” The UK mfg PMI also dipped below 50, indicating contraction.

Elsewhere, Emerging market stocks and currencies were heading for their biggest 3-day gain in two months as bets a sell-off last month had gone too far outweighed falling oil prices and renewed trade tensions. The MSCI Emerging Markets Index of stocks climbed to a two week high, while its currency counterpart traded above its 200-day moving average.

“Why should emerging markets sell off just because the U.S. is shooting itself in the head?” said Jan Dehn, Ashmore Group’s head of research based in London. “I can understand why Mexico sold off, but this is a policy mistake, which will hurt America. So it is only right that America is sold, not emerging markets.”

Asian currencies led by South Korea’s won were the best performers, while Chinese telecom stocks rallied after a report Beijing will issue commercial licenses for fifth-generation telecommunication services. The Yen rose, as did Europe’s go-to safety play, the Swiss franc, which rallied to its highest in nearly two years against the euro. The euro hovered at $1.1171 having been stuck in one of its tightest ranges ever against the dollar.

Brent crude fell for a fourth day, tumbling as much as 1.8% to $60.86 per barrel. Oil has dropped almost 20% since April, approaching a bear market. WTI futures dropped 1.3% too to below $53 a barrel for the first time since mid-February. Copper futures in Shanghai fell 0.5% to two-year lows while safe-haven gold jumped as much as 0.5% to a 10-week high of $1,312.4 per ounce.

Expected data include PMIs and construction spending. Box and Coupa Software are reporting earnings.

Market Snapshot

- S&P 500 futures down 0.4% to 2,742.00

- STOXX Europe 600 down 0.7% to 366.56

- MXAP up 0.2% to 152.60

- MXAPJ up 0.5% to 500.95

- Nikkei down 0.9% to 20,410.88

- Topix down 0.9% to 1,498.96

- Hang Seng Index down 0.03% to 26,893.86

- Shanghai Composite down 0.3% to 2,890.08

- Sensex up 1% to 40,124.89

- Australia S&P/ASX 200 down 1.2% to 6,320.55

- Kospi up 1.3% to 2,067.85

- German 10Y yield fell 1.1 bps to -0.213%

- Euro up 0.03% to $1.1172

- Italian 10Y yield rose 1.4 bps to 2.297%

- Spanish 10Y yield fell 2.7 bps to 0.688%

- Brent futures down 3.8% to $62.05/bbl

- Gold spot up 0.7% to $1,315.17

- U.S. Dollar Index little changed at 97.71

Top Overnight News from Bloomberg

- Trump landed in the U.K. for a three-day state visit at a sensitive time for the country’s ruling Conservative Party. Rival candidates are jostling to replace outgoing Prime Minister Theresa May, and the president has already weighed in with his own opinions on the contenders

- Trump opened another potential front in his trade war, terminating India’s designation as a developing nation and thereby eliminating an exception that allowed the country to export nearly 2,000 products to the U.S. duty-free. Meanwhile China was planning retaliatory trade measures against the U.S.

- China’s government says it’s willing to work with the U.S. to end an escalating trade war but blames President Donald Trump’s administration for the collapse in talks and won’t be pressured into concessions

- “We don’t have plans to change our inflation target, but are looking at our framework more broadly,” San Francisco Fed President Mary Daly says in reply to question after speech in Singapore

- President Trump on Saturday defended his decisions to impose or raise levies against imports from Mexico and China, respectively, saying “companies are moving to the U.S.” to avoid paying the levies

- Trump downplayed the chance he would impose tariffs on Australia, a top U.S. ally, after the New York Times reported his administration considered doing so last week

- With U.K. Prime Minister Theresa May about to hand over the reins of power, candidates to succeed her now feel free to speak out on issues such as Huawei Technologies Co. Ltd.’s role in the country’s 5G telecoms infrastructure

- The Social Democrats, the junior coalition partner in Germany’s government, will begin searching for an interim chief after Andrea Nahles said she lost the support of her party

- Factory output in the euro area fell close to a six-year low in May, with slumping orders and declining workforces signaling a bleak outlook for demand. The data underscores a picture of an economy that is struggling to emerge from a slowdown that has lasted more than a year

- Britain’s manufacturing sector unexpectedly shrank in May for the first time since the direct aftermath of the 2016 Brexit referendum. IHS Markit’s manufacturing PMI dropped to 49.4 from 53.1 in April as factories unwound Brexit preparations when the departure date was pushed back. The reading was weaker than the 52 forecast

- Deutsche Bank AG and UniCredit SpA moved some of their swaps trades from London to Frankfurt in May as banks used a lull in the ongoing Brexit drama to prepare for the worst

Asian equity markets traded negatively with risk appetite subdued as the US faces a 2-front trade war against China and Mexico, although stronger than expected Caixin PMI data helped limit losses in China. Nonetheless, a risk averse tone was seen from the reopen after China released a white paper that blamed the US for the setback of trade talks which pressured US equity futures to extend on the losses from Wall St’s worst May performance since 2010. ASX 200 (-1.2%) and Nikkei 225 (-0.9%) declined with the energy sector the underperformer in Australia after the recent oil slump, while safe-haven currency flows weighed on Tokyo stocks and with weakness in SoftBank exacerbated on reports of funding difficulties for its next USD 100bln tech fund. Hang Seng (U/C) and Shanghai Comp. (-0.3%) were initially higher after the PBoC maintained net liquidity through CNY 80bln of reverse repos and after Chinese Caixin Manufacturing topped estimates, although the gains were short-lived as trade concerns remained heavily in focus with China playing the blame game, while it is also set to draft its own blacklist of ‘unreliable’ entities and probe FedEx over possible infringement of Huawei’s legal rights regarding rerouted packages. Finally, 10yr JGBs were steady with only marginal gains seen despite the widespread risk aversion and the BoJ presence in the market for JPY 800bln in up to 5yr JGBs.

Top Asian News

- Bank of Jinzhou Auditors Resign Citing Loan Inconsistencies

- China’s Top Courier Gains as FedEx Targeted in U.S. Trade War

- SpiceJet Has ‘Offers’ for Stake in Indian Budget Airline

- Turkish Inflation Slows Again as Food Prices Bring Relief

Major European indices began the week lower in continuation from the Asia-Pac session which was weighed on by China releasing a white-paper blaming the US for the set back in trade talks and are to draft a ‘black-list’ of unreliable entities. Throughout the mornings trade bourses have been grinding higher but are still in negative territory [Euro Stoxx 50 -0.1%]; sectors are mixed on the day with some moderate outperformance seen in Utilities, which Nomura Quants note is not sufficient to trigger an excessive volatility shock as the sell-off in cyclicals in minimal compared with prior selloffs. Notable movers this morning include Infineon (-6.4%) who are near the bottom of the Stoxx 600 after it was reported that they are to acquire Cypress Semiconductors for an enterprise value of EUR 8bln; Co’s boards have already consented to this acquisition. Elsewhere, airline names are somewhat subdued after reports that the global airline industry is to record its lowest profit in five-years, particularly easyJet (-2.1%) which is also weighed on following reports that the Co. are this week to drop out of the FTSE 100 (-0.4%). At the other end of the Stoxx, and topping the DAX are Wirecard (+2.3%) following the CEO stating they expect an outstanding H1.

Top European News

- Euro-Area Manufacturing Remained Stuck in Its Slump in May

- U.K. Manufacturing Slips Into Contraction After Brexit Delay

- Danske Moves Toward Total Baltic Exit Amid Laundering Saga

- One Man’s $75 Million Perk Triggers Indignation in Denmark

- Glencore’s Executive Departures Hasten as Oil Chief Leaves

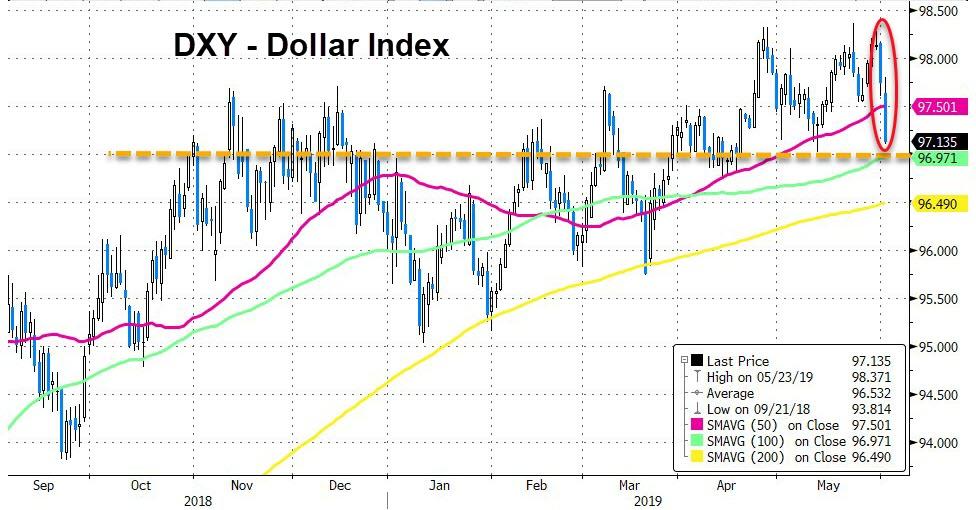

In FX, the dollar was little changed on the day thus far, following on from a relatively subdued session overnight as the index remains sub-98.00 ahead of this week’s key risk events which includes US ISM manufacturing PMI, ECB’s monetary policy meeting and US jobs data. The index remains near the middle of the intraday 97.57-80 range with gains capped by bleeding US yields.

- EUR/GBP – Hardly fazed on manufacturing PMI day in which the EZ number was unrevised (as expected) whilst UK’s manufacturing sector slipped into contraction, with new orders and employment both declining whilst stockpiling paused following the Brexit delay. Sterling remains dedicated to Brexit related development as new members line up for the Tory leadership, with the latest from Environmental Sectary Gove, a front runner, reportedly considering a further extension beyond October 31st, whilst leading candidate Johnson said that if he is elected, the UK will leave the bloc with or without a deal on Brexit day. EUR/USD remains within a relatively tight 1.1157-90 range with clean air to the upside until the 1.1200 handle. Beyond that, the pair’s 50 DMA resides around 1.1208 with resistance seen at 1.1264 (May high). Meanwhile, Cable hovers around the 1.2650 mark with little seen to the upside by way of near-term tech levels.

- CHF/JPY – Both firmer on the day, albeit the Yen to a lesser extent, in a continuation of the Trump triggered risk-off mood around the market. USD/JPY fell to whisker away from the 108.00 level (low 108.08) whilst its Franc counterpart slipped further below parity vs. the Greenback. Deutsche Bank recommends “good news rallies should be sold as trade tensions may get relief rallies” as the JPY-crosses “should remain under pressure”. It’s worth keeping in mind USD/JPY sees almost 1bln in option expiries at 108.00-15 ahead of supports at 107.77 and 107.27 (Jan 10 low and 61.8% Fib respectively) whilst USD/CHF sees its 200 DMA at 0.9959 (having already tested the level) ahead of its 200 WMA at 0.9847.

- AUD/NZD – Marginally firmer in the aftermath of optimistic China Caixin manufacturing data which provided the antipodeans with some relief following last week’s losses. AUD/USD hovers around the 0.6950 mark (high 0.6960, low 0.6928) despite a looming RBA rate cut, with participants on the look-out for guidance into the aggressiveness of the much-anticipated easing cycle. Meanwhile, its antipodean counterpart seems to be benefiting more as the AUD/NZD cross breached its 200 DMA (1.0624) as it tests the 1.0600 level ahead of its 50 DMA (1.0571)

In commodities, WTI and Brent futures are recovering off Asia-Pac lows with the former back above the 53.00/bbl handle and climbing towards the next round figure, whilst the latter is attempting to turn positive on the day having already dipped below the 61.00/bbl figure overnight. The weekend saw the release of Russian May crude production which stood at an 11-month low at 11.11mln BPD, down from last month’s 11.24mln BPD, although this was mainly due closures from the Druzbha pipeline due to oil contamination. Elsewhere, Saudi reported a M/M decline in oil output to 9.65mln BPD from the prior 10.05mln BPD, whilst the Kingdom’s energy minister stated that Saudi is committed to do whatever is required to stabilise the oil market. GS takes into account the supply/demand side concerns and net-net expects prices to remain volatile in the coming months, albeit around current levels. Turning to OPEC, the bank sees higher production from Saudi, Russia, UAE and Kuwait to offset Iranian and Venezuelan shortfalls. Thus, GS expects backwardation to persist in the coming months, whilst also revising lower its Q2 Brent forecast to 65.50/bbl from 72.50/bbl, also citing spare capacity created by a new Permian pipeline. Elsewhere, gold (+0.7%) benefits from its safe haven characteristics and extends gains above its 1300/oz level whilst copper prices are seeing some reprieve following last week’s slump as the red metal was underpinned by optimistic Caixin manufacturing data from China.

Goldman Sachs suggest that oil prices may recover from here due to a tight EU crude market, sudden moves lower, OPEC’s reluctance to increase supply and above consensus growth forecasts, However, increasingly uncertain macro outlook, rising production an OPEC spare capacity suggests prices at likely to remain around current levels with high volatility

US Event Calendar

- 9:45am: Markit US Manufacturing PMI, est. 50.6, prior 50.6

- 10am: ISM Manufacturing, est. 53, prior 52.8

- 10am: Construction Spending MoM, est. 0.4%, prior -0.9%

- Wards Total Vehicle Sales, est. 16.9m, prior 16.4m

DB’s Jim Reid concludes the overnight wrap

Obviously being a Liverpool supporter it was a glorious weekend for me. Not even the kids could spoil it although on Saturday we went out strawberry picking as a family and aimed to leave at 930am but eventually left hot, bothered and bad tempered at 1pm. There were tantrums, numerous toilet related accidents, several changes of clothes, more tantrums, buckets of suncreams to apply, sunglasses to find, pack lunches to prepare etc etc. Originally we finally got ready to leave 2 hours late and then as we reversed the car we found that our electric gates wouldn’t open. After 30mins of failed brute force we called someone out. They came in an hour, fixed it and off we went 3.5 hours late. As for the final it was an awful game. In fact given it was Europe’s premier sporting occasion and given that it featured two English sides I’d imagine those in Brussels this morning will be lobbying extensively for the hardest possible Brexit so they don’t have to watch such a poor spectacle again. Anyway a great result… for me at least.