GOLD: $1324.15 UP $.85 (COMEX TO COMEX CLOSING)

Silver: $14.79 UP 1 CENT (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1325.80

silver: $14.83

TODAY’S DOW/NASDAQ RISE WAS CAUSED BY POWELL RELENTING AND STATING THAT HE MAY NEED NEW TOOLS TO FIGHT THE SOFTENING ECONOMY

HE WAS HINTING ON TWO THINGS:

- CUTTING RATES

- USING NIRP AND ZIRP AS WORLD GROWTH CRUMBLES TO NOTHING

GOLD AND SILVER SHOULD HAVE SKYROCKETED ON THIS NEWS BUT WAS HELD BACK BY THE BANKERS

THIS TIME, LOWER RATES WILL NOT HELP THE ECONOMIES OF THE WORLD.

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 61/358

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,322.700000000 USD

INTENT DATE: 06/03/2019 DELIVERY DATE: 06/05/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 217

357 C WEDBUSH 1

435 H SCOTIA CAPITAL 350

657 C MORGAN STANLEY 9

661 C JP MORGAN 61

686 C INTL FCSTONE 5 40

737 C ADVANTAGE 2 19

800 C MAREX SPEC 7

905 C ADM 1 4

____________________________________________________________________________________________

TOTAL: 358 358

MONTH TO DATE: 448

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 358 NOTICE(S) FOR 35800 OZ (1.1113 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 448 NOTICES FOR 44,800 OZ (1.393 TONNES)

SILVER

FOR JUNE

1 NOTICE(S) FILED TODAY FOR 5,000 OZ/

total number of notices filed so far this month: 262 for 1310,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

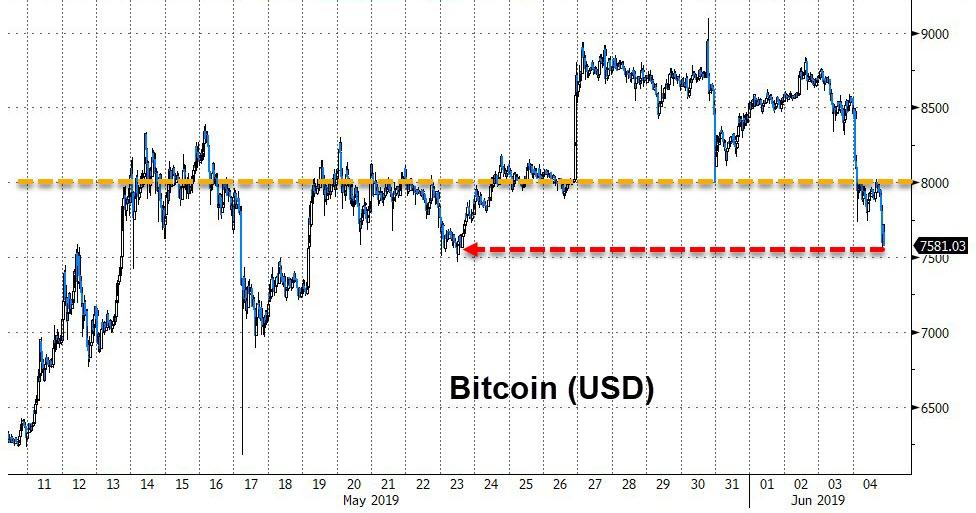

Bitcoin: OPENING MORNING TRADE : $ 7956 DOWN 230

Bitcoin: FINAL EVENING TRADE: $ 7650 DOWN 545

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A CONSIDERABLE SIZED 3517 CONTRACTS FROM 209,964 UP TO 213,481 DESPITE THE 19 CENT GAIN IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER AND IT STOPPED FOR GOLD AS WELL. WE WILL WITNESS A RISE IN THE SPREADERS IN SILVER ONCE WE START TRADING IN JUNE… READY FOR THE FIRST DAY NOTICE JULY CONTRACT.) TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 3658 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 3658 CONTRACTS. WITH THE TRANSFER OF 3658 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3658 EFP CONTRACTS TRANSLATES INTO 18.29 MILLION OZ ACCOMPANYING:

1.THE 19 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.330 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

6523 CONTRACTS (FOR 2 TRADING DAYS TOTAL 6523 CONTRACTS) OR 32.615 MILLION OZ: (AVERAGE PER DAY: 3,262 CONTRACTS OR 16.30 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 16.30 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 2.32% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 921.32 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3658 WITH THE 19 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A VERY HUGE SIZED EFP ISSUANCE OF 3658 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED AN ATMOSPHERIC SIZED: 7175 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3658 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 3517 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 19 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.78 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.067 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000, OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.330 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A HUMONGOUS SIZED 11,627 CONTRACTS, TO 476,704 WITH THE $17.50 PRICE GAIN WITH RESPECT TO COMEX GOLD PRICING FRIDAY// YESTERDAY/THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADING FELLOWS WILL MORPH INTO SILVER ONCE JUNE GETS UNDERWAY. THE GAIN IN OI GOLD CONTRACTS IS REAL AND NOT PUMPED UP BY SPREADING.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 12,400 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 12,400 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 476,704. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 24,027 CONTRACTS: 11,627 OI CONTRACTS INCREASED AT THE COMEX AND 12,400 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 24,027 CONTRACTS OR 2,402,700 OZ OR 74.73 TONNES. YESTERDAY WE HAD A GOOD GAIN OF $17.50 IN GOLD TRADING….AND WITH THAT GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 74.73 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

WITH RESPECT TO SPREADING: WE HAD ZERO ACTIVITY OF THE SPREADERS//

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 27,485 CONTRACTS OR 2,748,500 OR 85.48 TONNES (2 TRADING DAYS AND THUS AVERAGING: 13,742 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAYS IN TONNES: 85.48 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 85.48/3550 x 100% TONNES =1.32% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2363.4 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUGE SIZED INCREASE IN OI AT THE COMEX OF 11,627 WITH THE PRICING GAIN THAT GOLD UNDERTOOK ON YESTERDAY($17.50)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,400 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,400 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC SIZED GAIN OF 24,027 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

12,400 CONTRACTS MOVE TO LONDON AND 11,627 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 74.73 TONNES). ..AND THIS GAIN OF DEMAND OCCURRED WITH THE RISE IN PRICE OF $17.50 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING LIQUIDATION ///TODAY/

we had: 358 notice(s) filed upon for 35,800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $0.85 TODAY//SEEMS THE BOYS FOUND RELIGION

A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: A HUGE “PAPER” GOLD DEPOSIT OF 16.44 TONNES. THERE IS ABSOLUTELY NO WAY THAT THEY FOUND ANYTHING CLOSE TO THIS TONNAGE…THUS IT WAS ONLY A PAPER GAIN.

INVENTORY RESTS AT 759.65 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 1 CENT TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 312.038 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUMONGOUS SIZED 3517 CONTRACTS from 210,267 UP TO 213,481 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER AND GOLD FOR NOW BUT WILL NOW MORPH INTO SILVER AS THE COMEX SILVER MONTH OF JUNE COMMENCES IN EARNEST..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 3658 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3658 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 3517 CONTRACTS TO THE 3658 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC GAIN OF 7175 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 35.875MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 1.330 MILLION OZ FOR JUNE.

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 19 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A HUGE SIZED 3658 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 27.80 POINTS OR 0.96% //Hang Sang CLOSED DOWN 132.34 POINTS OR 0.49% /The Nikkei closed DOWN 2.34 POINTS OR 0.01%//Australia’s all ordinaires CLOSED UP .01%

/Chinese yuan (ONSHORE) closed DOWN at 6.9087 /Oil DOWN TO 52.49 dollars per barrel for WTI and 60.38 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED UP // LAST AT 6.9087 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9287 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China

In a new report, we find out how China is circumventing the tariffs by exporting to nations not subject to tariffs and then this is re imported back into the USA without the tariffs implemented.

( zerohedge)

ii)Yesterday, Beijing warned students about studying in the USA. Now they take it one step further by issuing an official travel advisory highlighting the risks of traveling in the uSA i.e.” robbery and theft”

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

This is a big story!! One of England’s biggest and respected Hedge Fund, Neil Woodford has blocked redemptions from his huge 3.7 billion pound equity income fund after a large investor exodus. He has an extremely high profile as a fund manager. This may scare other funds into an investor exodus.

(zerohedge)

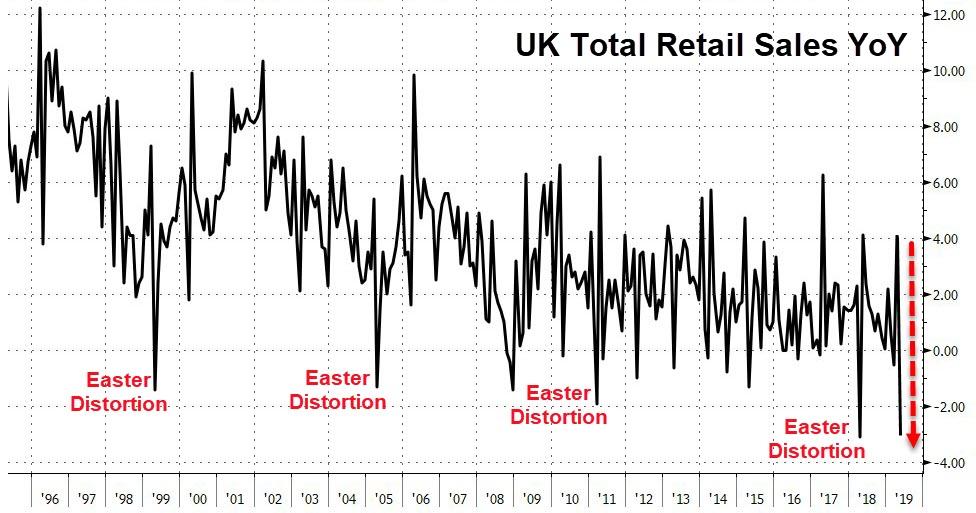

ii)The UK continues to falter as the key retail sales crash by the most on record

Tom Luongo discusses the fact that in Europe the center parties are just not holding power any more

( Tom Luongo)

iv)EU VS USA BANKING SYSTEMS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

i)AUSTRALIA

Another country shows its true colours after a raid on a News Corp journalist after she reports on government spying on ordinary citizens

(courtesy zerohedge)

ii)Mexico/uSA

Trump’s Mexican tariffs are hurting Constellation Brand’s stock which is mostly made up of Mexican beer. The best sellers are the Corona beer and Modelo and this will make beer move expensive to Americans.

( zero hedge)

iii)The Peso climbs as AMLO supposedly caves into Trump and will crack down on immigration. The problem is that he does not control the cartels

( zerohedge)

iii b)Then after the markets closed, Trump threatens with a New National Emergency to enact the Mexican tariffs

iv)We now have a reading on the entire globe’s PMI and it is at a 7 year low.

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

i)James Truk explains how gold and silver have broken out of the downtrends. But most importantly he describes that in the physical market, gold and silver are in strong demand

( James Turk/Kingworldnews)

ii)Our resident expert on Chinese gold demand describes the country is firing on all cylinders with physical gold demand.

iii)Bitcoin rally is nothing by renewed exuberance as speculators bid up the price: nobody is using the coin for spending purposes

iv)Tom Luongo now discusses gold and he is of the belief that gold will shoot up having been repressed by the our banker friends for so long

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading/early morning/

The algos will look for anything no matter how stupid it is to rank up stocks and whack gold/silver

( zerohedge)

b)LATE MORNING:

ii)Market data

iii)USA ECONOMIC/GENERAL STORIES

( zerohedge)

b)The House Judiciary Committee announces a bipartisan probe into whether large tech companies are suppressing competition

( zerohedge)

c)ILLINOIS’ new 45 billion dollar capital spending binge is exposed

(courtesy Mark Glennon/WirePoints.com)

SWAMP STORIES

c)This ought to be good: Christopher Steele has finally agreed to meet IG Horowitz. He decided to meet Horowitz after he was told the report would deeply undermine him. His scope is narrow and he will only answer to questions relating to his involvement with USA intelligence forces.(courtesy zerohedge)

Let us head over to the comex:

Gold withdrawals;

i) We had 1 withdrawal:

out of BRINKS: 4983.405 oz

.

Gold Hits 10 Week High At $1,328/oz as Trade Wars Spur Safe Haven Demand

Gold has consolidated on yesterday’s gains and is marginally higher as risk aversion creeps back into markets. Gold rose 1.5% yesterday to its highest level in more than three months.

Concerns that trade wars look set to escalate globally and fears that President Trump’s threat of tariffs on Mexico will hurt the global economy are spurring safe haven demand.

Gold had a fourth straight session gain yesterday, settling at their highest in more than three months, as investors fled to the safety of havens like precious metals and bonds amid persistent tariff tensions between the U.S. and its global trade partners.

“Gold is looking good here—responding to the rise in economic wars via tariffs to the global economic slowdown,” said Peter Spina, president and chief executive officer of GoldSeek.com.

“Bonds are surging and gold should too … There are good reasons to believe the breakout in gold is developing as we speak and by the end of this year we will see it explode towards $1,400-$1,500,” he told MarketWatch.

News and Commentary

Gold Extends Win Streak to Fourth Day, Ending at More Than 3-month High

Gold Hits 10 Week ‘Peak’ as Trade Fears Spur Safe-haven Interest

Dollar Dips on Increased Expectations of a 2019 Fed Rate Cut

U.S. Manufacturing Activity Grows at Slowest in Two-and-a-half Years: ISM

‘Flight to Quality’ and Gains for Safe Haven Gold – GoldCore

Internet Shutdowns Don’t Make Anyone Safer

Feds Target Four of the Biggest Tech Companies in U.S., and Their Stocks Are Getting Slammed

Goldman Sachs Is Predicting an Escalation of Global Trade Wars

Morgan Stanley Tells Investors to Play Defense as Cycle Indicator Flashes ‘downturn’

This Cycle’s Most Dangerous Bubble, In Three Charts

They Ditched America to Retire by a Lake in Chile on About $3,000 a Month — and Rarely Come Back

LBMA Gold Prices (USD, GBP & EUR – AM/ PM Fix)

03-Jun-19 1313.95 1317.10, 1039.47 1042.35 & 1175.99 1175.38

30-May-19 1276.45 1280.95, 1010.44 1015.920 & 1146.25 1151.70

29-May-19 1283.50 1281.65, 1016.02 1013.27 & 1151.04 1150.67

28-May-19 1283.90 1278.30, 1012.87 1008.20 & 1146.91 1142.29

27-May-19 Closed for UK Holiday

24-May-19 1281.50 1282.50, 1011.36 1011.89 & 1145.92 1145.40

23-May-19 1275.95 1283.65, 1009.79 1015.37 & 1146.19 1152.46

22-May-19 1274.00 1273.80, 1005.44 1008.09 & 1141.12 1141.20

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

end

James Truk explains how gold and silver have broken out of the downtrends. But most importantly he describes that in the physical market, gold and silver are in strong demand

(courtesy James Turk/Kingworldnews)

Gold and silver have broken out of downtrends, Turk tells KWN

Submitted by cpowell on Mon, 2019-06-03 18:06. Section: Daily Dispatches

2:07p ET Monday, June 3, 2019

Dear Friend of GATA and Gold:

GoldMoney founder James Turk tells King World News today that physical demand for gold in London is strong,

both gold and silver have broken sharply out of their downtrends, and silver has a lot of catching up to do. His comments are posted at KWN here:

Ronan Manly: China’s physical gold market still firing on all cylinders

Submitted by cpowell on Tue, 2019-06-04 00:12. Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Monday, June 3, 2019

While headlines may be on the Sino-U.S. trade war, China’s gold market continues to fire on all cylinders, with physical gold continuing to flow into, and through, the world’s largest gold hub.

Year-to-date, Chinese wholesale gold demand is on a par with recent years, Chinese central bank gold purchases have officially recommenced after a two-year halt, and gold import data into China is now more transparent than ever before. …

… For the remainder of the analysis:

https://www.bullionstar.com/blogs/ronan-manly/still-firing-on-all-cylind…

Bitcoin rally masks uncomfortable fact: Almost nobody uses it for spending

Submitted by cpowell on Tue, 2019-06-04 00:19. Section: Daily Dispatches

By Olga Kharif

Bloomberg News

Monday, June 3, 2019

Bitcoin has a lingering problem that few people are talking about amid the renewed exuberance of the recent price surge.

Hardly anyone is using the world’s largest cryptocurrency for anything beyond speculation.

Data from New York-based blockchain researcher Chainalysis Inc. show that only 1.3 percent of economic transactions came from merchants in the first four months of 2019, little changed over the boom-and-bust cycles of the prior two years.

…

Even though marque companies such as AT&T Inc. now let customers pay with cryptocurrencies, the problem is that few speculators want to use the digital coins to pay for wireless services when the digital asset’s price might surge another 50 percent in a matter of weeks. That has become the main dilemma with the cryptocurrency: Bitcoin needs the hype to attract mass appeal to be considered a viable electronic alternative to money, but it has developed a culture of “hodlers” who advocate accumulation rather than spending. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-05-31/bitcoin-s-rally-masks…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

end

-END-

MY RESPONSE TO NICHOLAS:

|

4:51 AM (0 minutes ago) |

|

||

|

||||

you are no doubt absolutely correct on this:

Venezuela Defaults on Gold Swap With Deutsche Bank

Venezuela has defaulted on a gold swap agreement valued at $750 million with Deutsche Bank AG, prompting the lender to take control of the precious metal which was used as collateral and close out the contract, according to two people with direct knowledge of the matter.

As part of a financing agreement signed in 2016, Venezuela received a cash loan from Deutsche Bank and put up 20 tons of gold as collateral. The agreement, which was set to expire in 2021, was settled early due to missed interest payments, said the people, who asked not to be named speaking about a private matter.

In the meantime, opposition leader Juan Guaido’s parallel government has asked the bank to deposit $120 million into an account outside President Nicolas Maduro’s reach, which represents the difference in price from when the gold was acquired to current levels. As part of efforts to unseat Maduro, the U.S. and more than 50 countries have recognized Guaido as the legitimate leader of Venezuela even though he still doesn’t control key institutions at home, including the central bank.

“We’re in touch with Deutsche Bank to negotiate the terms under which the difference owed to the central bank will be paid to the legitimate government of Venezuela,” said Jose Ignacio Hernandez, Guaido’s U.S.- based attorney general. “Deutsche Bank can’t risk negotiating with the central bank’s illegitimate authorities,” particularly after it was sanctioned by the U.S. government, Hernandez said.

-END-

Gold Makes Its Grievances Heard

Gold is getting its revenge. Try as he might Mr. Tariff Man can’t dominate all the headlines all the time. Everyone once in a while something more important than the Trump Man-Baby Show should take center stage.

Gold has moved more than $50 in just under three trading sessions, blowing past near term resistance and, more importantly, reminding everyone just how quickly the reserve asset of the world economy can call bullshit on the proclamations and machinations of the morons who think they run the world.

You always know when you’re reaching the end of a bear market.

Last week I tweeted out:

Tom Luongo@TFL1728I think we’re reaching Peak Gold Bearishness. If the dollar is an attractive safe-haven asset, which it isn’t, just a necessary evil after a decade of ZIRP, then of course this will weigh on gold. That doesn’t mean demand isn’t there.https://seekingalpha.com/news/3467311-gold-longer-attractive-complacent-market-says-wells-fargo-analyst#email_link …

Gold no longer attractive in complacent market, says Wells Fargo analyst

Gold prices no longer look attractive based on the way the metal has reacted to recent economic events, says Wells Fargo’s John LaForge, noting that gold’s complacent reaction to market volatility is

seekingalpha.com

When an analyst at Wells is looking at the day-to-day ticker of gold looking for silly and binary safe haven arguments to warn people off of gold, I know we’re nearly there.

This isn’t a complacent market. In fact, as I’ve pointed out in the past, it’s an incredibly volatile one.

You don’t have to be a whiz with numbers, or worse a quant working for a central bank, to see the differences here.

And the reason for this massive increase in volatility across all asset classes is Trump’s insistence on tariffs being the cure all for what ails America’s trade ‘imbalances.’

Not convinced by the Dow? How about the change in the U.S. Yield Curve over the past year.

Ain’t convexity a bitch?

For months gold has bided its time, building a stronger and stronger base that, frankly, bad analysts refuse to see. Gold is trapped between falling dollar liquidity and rising distrust of government institutions to contain the chaos.

All of the correlations between gold and interest rates, money supply figures and the rest only function within the parameters of a market convinced of future political stability. Once that future stability begins getting deep discounts by markets and those relationships falter, gold consolidates, bides its time and then pops spectacularly.

It’s pretty simple. U.S. bonds and U.S. stocks have preferentially seen safe haven inflows as traders look for yield in a world of exploding negative yielding debt.

So now, with more than $10 trillion in debt yielding less than gold’s zero percent is it any wonder we’re seeing a move into gold?

This is the gold’s big grievance it has with central bankers. They have tried to maintain confidence for so long by suppressing interest rates and injecting liquidity that doesn’t circulate that its creating the mother of all bases from which gold will break out of soon.

All it took was one economic retard with bad hair and a massive insecurity complex to finally wake the market up to the reality of our predicament.

The Post-Brexit high of $1375 is still in place but look at the defining pattern of this chart… a succession of higher lows with falling volatility. Each bearish impulse is met with more bulls pushing back at higher prices.

2019’s Spring breakdown was only good for around $90 and just over three months. This latest up move may take a while to resolve above that central banker Maginot Line, but it’s coming as surely as Trump will tariff someone else after his twelfth Diet Coke.

Don’t tell me you haven’t been warned.

* * *

Support for Gold Goats ‘n Guns can happen in a variety of ways if you are so inclined. From Patreon to Paypal or soon SubscribeStar or by your browsing habits through the Brave browser where you can tip your favorite websites (like this one) for the work they provide.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

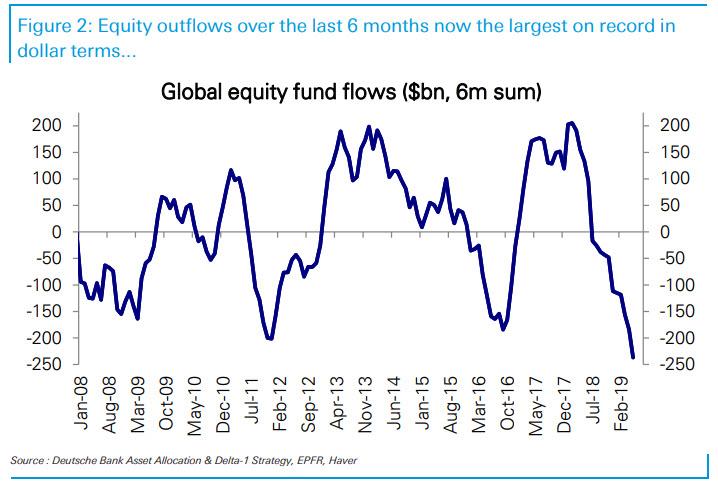

Gold Sees Biggest Inflow Since Brexit As Investor Exodus Contagion Spreads To Credit

Last week we highlighted a shocking Deutsche Bank report that showed global equity fund outflows over the last 6 months in dollar terms have now been larger than over any prior 6-month period.

As a percentage of AUM, the latest half-year outflows were only exceeded by those seen around the 2008-09 recession and the European financial crisis.

That investor exodus recently spread to the credit markets, with HY funds seeing huge outflows as prices plunged ominously.

With HY credit markets screaming about dead canaries in coalmines…

And now that investor exodus has spread to other segments of the credit markets…

As Bloomberg reports, the biggest leveraged loan ETF, BKLN, had its largest ever daily outflow in the most recent session for which Bloomberg has data…

Additionally, State Street’s High-Yield Muni ETF, HYMB, also saw a record daily outflow on June 3…

“While we’re working through this dual threat of new worries around trade and the re-rating at the front end of the curve, you want to be cautious for credit assets,” Rob Waldner, chief fixed income strategist at Invesco Ltd. said on Bloomberg TV Tuesday.

And where are those de-risked assets seeking safe-havens? Gold!

GLD – the Gold ETF – saw its biggest single-day asset inflow since Brexit yesterday.

end

* * *

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9087/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9286 /shanghai bourse CLOSED DOWN 27.80 POINTS OR 0.96%

HANG SANG CLOSED DOWN 132.34 POINTS OR 0.49%

2. Nikkei closed DOWN 2.34 POINTS OR 0.01%

3. Europe stocks OPENED GREEN /

USA dollar index FALLS TO 97.09/Euro RISES TO 1.1261

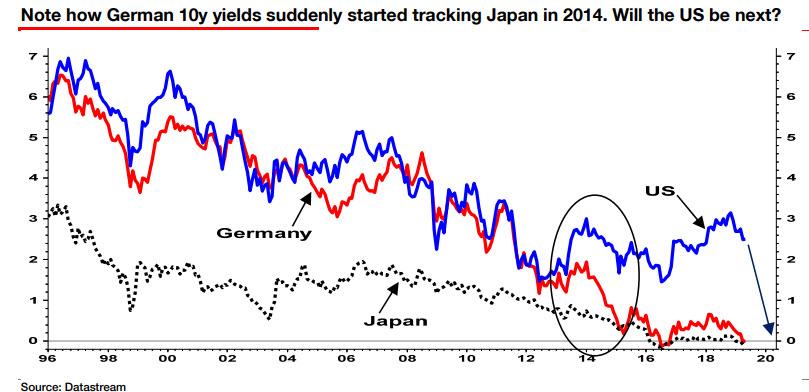

3b Japan 10 year bond yield: FALLS TO. –.10/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.93/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.49 and Brent: 60,38

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.22%/Italian 10 yr bond yield DOWN to 2.49% /SPAIN 10 YR BOND YIELD DOWN TO 0.65%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.71: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.93

3k Gold at $1325.90 silver at: 14.73 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 5/100 in roubles/dollar) 65.24

3m oil into the 52 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.93 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9926 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1176 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.22%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.10% early this morning. Thirty year rate at 2.56%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8161..

Stocks, Futures, Yields Rebound As Selling Pauses

Global stocks rebounded from Monday’s hammering even as worries about a regulatory crackdown on the world’s internet and social media giants compounded mounting global trade and recession jitters, while interest rates remained just shy of multi-year lows as Treasuries dipped for the first time in a week while the dollar was unchanaged.

Europe’s STOXX 600 index recovered from a weak start, reversing earlier losses of as much as 0.7% led by gains in autos and chemicals shares, but tech stocks remained more than 1% lower after reports the US government was gearing up to investigate whether Amazon, Apple, Facebook and Google misused their market power. The Stoxx 600 Automobiles & Parts Index is best-performing as RBC says that it has a more positive bias on the region’s carmakers. BASF (+3%) and Linde (+1.3%) lead gains in chemical stocks.

Earlier, Asian shares dropped as the broadest index of Asia-Pacific shares outside Japan had ended down 0.3%, catching down to the US tech rout, as communications stocks fell while materials shares gained. Most markets in the region were down. The Shanghai Composite Index fell 1%, while Hong Kong’s Hang Seng Index declined for a fifth day in its longest losing streak since April. India’s S&P BSE Sensex Index retreated after reaching a fresh record ahead of the central bank’s rate decision later this week. Emerging-market stocks fell for the first time in three days .

On Monday a combined $85 billion was wiped off Facebook and Google parent Alphabet’s market caps, in the worst rout for the FANG sector in two years…

…which in turn dragged the Nasdaq into correction territory, having lost 10% over the last month.

“That (U.S. investigation) is currently weighing on stocks, but more importantly the market is increasingly pricing in the risk of recession,” said Rabobank senior macro strategist Teeuwe Mevissen. “Sentiment is significantly suppressed.”

Meanwhile, global monetary policy remains in focus this week as the hostile trade rhetoric between the U.S. and China continues. Fed ratesetter James Bullard said on Monday lowering U.S. rates “may be warranted soon”.

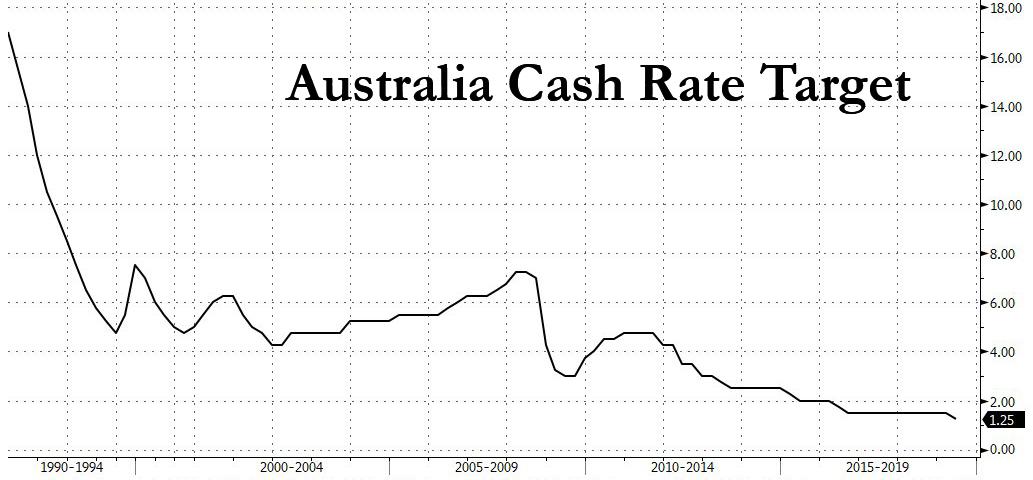

Sure enough, after nearly 3 years of resisting any change to its monetary policy, Australia’s central bank cut rates to a record low and on Thursday the European Central Bank is set to detail a fresh dump of cheap money. India is expected to lower its rates too.

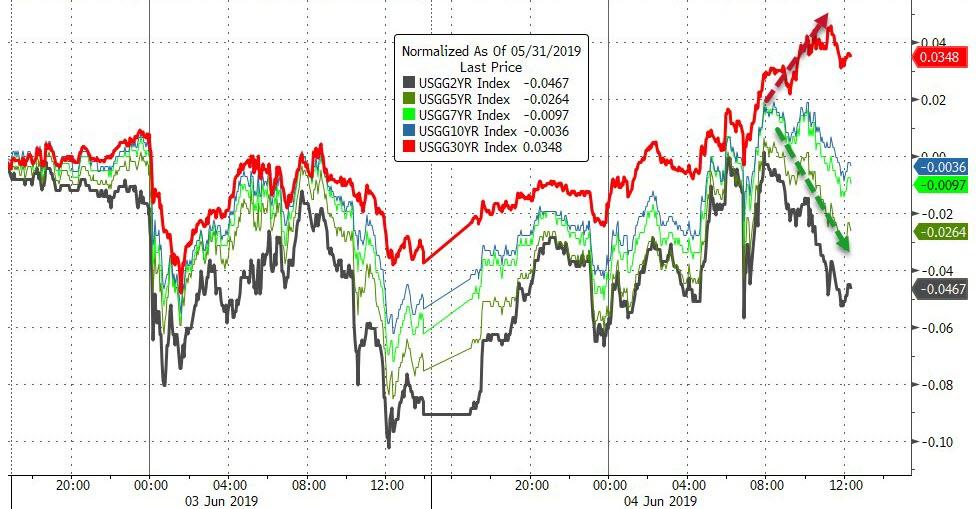

After a furious plunge on Monday in a move that left many rates traders shocked, US Treasury yields also rose but remained near recent lows. U.S. 10-year notes yielded 2.0968% after touching 2.06, the lowest since September 2017. All this underlined the scramble to re-price Fed policy and the biggest two-day drop in U.S. two-year Treasury yields since the 2008 crash. The yield curve between three-month and 10-year debt has inverted by as much as 27 basis points, historically a recession signal. More shockingly, the curve between the 3 month and 2 year was the most inverted since the financial crisis.

In FX, the dollar halted a three-day decline and Treasury yields rose as traders awaited clues on monetary policy when Federal Reserve Chairman Jerome Powell speaks later Tuesday. The euro touched its highest level in seven weeks against the dollar before erasing gains after regional inflation data fell slightly short of expectations even as unemployment dropped more than expected. The pound fluctuated after data showed U.K. retail sales in May declined by the most on record.

The AUD/USD advanced briefly after the RBA lowered the cash rate by a quarter-point to 1.25%, citing a need to boost employment and spur inflation. It however surrendered the gain as traders interpreted a move by the Australia & New Zealand Banking Group Ltd. to reduce its mortgage rate as a signal that the central bank may need to cut rates further to achieve its desired impact on the economy. Additionally, Australia’s central bank chief strongly suggested he could follow up Tuesday’s interest- rate cut with another reduction as he seeks to drive down unemployment and revive inflation.

EM currencies, however, extended gains to a fourth day, the longest rally since March, as the dollar remained subdued while traders await further developments on the trade front. South Africa’s rand fell by more than 1% after reporting the biggest first-quarter GDP contraction since 2009. The Thai baht, Hungarian forint and Mexico’s peso led the charge higher as MSCI’s Emerging Markets Currency Index climbed to a three-week high. The yuan and India’s rupee were outliers on the day. “Markets continued to digest the implications of a potential tariff on Mexican exports to the U.S.,” Guillaume Tresca, a Montrouge, France-based strategist at Credit Agricole SA, said in a note to clients. “The timeline for dialogue and resolution is pretty tight. Depending on the outcome, FX and rates markets could go through another round of correction.”

Finally, the Turkish lira initially dropped, then rebounded even after Turkish President Erdogan repeated that Turkey will not take a step back from the Russian S-400 missile deal.

“Risk aversion has also been seen with the yen carry trade unwinding as the markets comprehend that the U.S. technology containment strategy towards China is unlikely to reverse,” analysts at Jefferies said in a note. “In the short term, positioning has become so bearish that ‘a ceasefire’ could spark a risk rally,” they said.

In overnight geopolitical news, China issued a warning against travelling to the US; subsequently, China’s Foreign Ministry says it is clear that every set-back in US trade talks was due to the US breaking consensus, have resolve and ability to defend their interests and rights. Elsewhere, Commerce Secretary Ross reiterated President Trump’s message that Mexico needs to do more on illegal immigration in a meeting with Mexico’s Economic Minister, while Mexico said without its efforts a further 500k migrants would reach US this year and that they could take several paths if the US goes ahead with the tariffs including asking for help from WTO or implementing its own tariffs on US goods. This is as the WaPo reported that US Congressional Republicans are discussing moves to stop Trump’s tariffs on Mexico.

Finally, oil fell and was hovering on the edge of a bear market after the Wall Street banks raised the specter of a recession, while Saudi Arabia tried to assure investors that OPEC will avert a supply glut. Brent crude futures are now testing $60 per barrel for the first time in four months. It was last down 0.6% at $60.92 per barrel and U.S. crude was down 0.4% at $53.02. In contrast, safe-have gold was up 0.1% at $1,326.47 per ounce, near three-month highs.

Expected data include factory orders and durable goods orders. Tiffany and Salesforce are among companies reporting earnings.

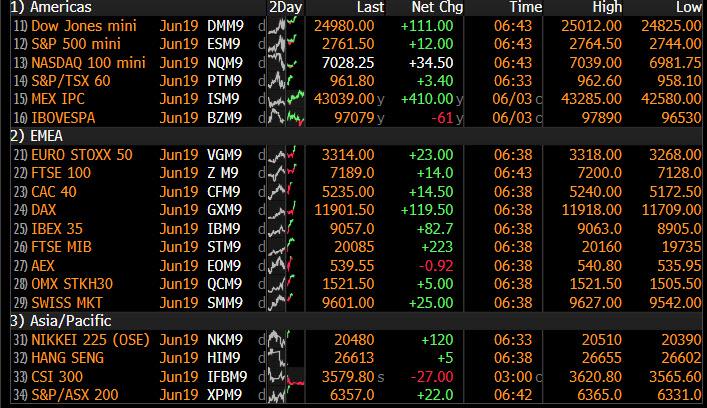

Market Snapshot

- S&P 500 futures up 0.5% to 2,763.00

- STOXX Europe 600 down 0.2% to 369.69

- MXAP down 0.1% to 152.41

- MXAPJ down 0.3% to 499.82

- Nikkei down 0.01% to 20,408.54

- Topix up 0.01% to 1,499.09

- Hang Seng Index down 0.5% to 26,761.52

- Shanghai Composite down 1% to 2,862.28

- Sensex down 0.1% to 40,218.55

- Australia S&P/ASX 200 up 0.2% to 6,332.36

- Kospi down 0.04% to 2,066.97

- German 10Y yield fell 0.7 bps to -0.208%

- Euro up 0.2% to $1.1259

- Italian 10Y yield fell 10.8 bps to 2.189%

- Spanish 10Y yield fell 1.5 bps to 0.677%

- Brent futures down 0.3% to $61.10/bbl

- Gold spot down 0.2% to $1,323.23

- U.S. Dollar Index up 0.1% to 97.24

Top Overnight News from Bloomberg

- Investors are plowing into Treasuries, favoring shorter maturities in particular, on growing conviction the Federal Reserve will cut interest rates this year to contain the fallout from trade tensions. Two-year yields sank to their lowest level since December 2017 and have tumbled by more than a quarter- point since the middle of last week

- The Federal Reserve may need to cut interest rates soon to prop up inflation and counter downside economic risks from an escalating trade war, St. Louis Fed President James Bullard said

- Yuan watchers arguing that China shouldn’t be scared of the currency breaking 7 a dollar are being emboldened by a former central bank official’s support for their thesis

- Germany’s Chancellor Angela Merkel won her rattled government some time as her junior coalition partner agreed to remain on board for a while longer despite the turbulent resignation of its chief.

- Italian Prime Minister Giuseppe Conte threatened to resign if the partners in his populist coalition don’t stop posturing, demanding they get to work on new policies to help the country

- Oil edged closer to a bear market collapse as Wall Street banks raised the specter of a recession, while Saudi Arabia tried to assure investors that OPEC will avert a supply glut

- There is no fundamental change in the view that Japan’s economy is gradually recovering, says Taro Aso, assessing the economic outlook in the runup to a planned sales tax hike in October.

- China issued a travel advisory on the U.S. through the end of the year, amid spiraling trade tensions between the two countries

- Donald Trump is expected to wade further into the U.K.’s fraught politics on a visit to London, having already dangled the promise of a trade deal if his hosts push on with Brexit

- Australia’s central bank chief strongly suggested he could follow up Tuesday’s interest- rate cut with another reduction as he seeks to drive down unemployment and revive inflation

Asian equity markets traded subdued after the headwinds from Wall St where tech underperformed and the Nasdaq slipped into a correction as FAANG stocks were hit on reports of the US launching antitrust and business practice probes into the large tech names. ASX 200 (+0.2%) and Nikkei 225 (U/C) were indecisive as strength in mining names and a widely anticipated RBA rate cut helped offset the tech losses in Australia, while trade in Tokyo was relatively uneventful with exporter sentiment dampened by further unfavourable currency flows. Hang Seng (-0.5%) and Shanghai Comp. (-1.0%) weakened as trade tensions persisted as the US accused China of misrepresenting trade talks and placed the blame on Chinese negotiators back-peddling on issues, while the PBoC’s liquidity efforts resulted to a daily net drain of CNY 90bln. Finally, 10yr JGBs were higher and the 10yr yield dropped to the lowest since August 2016 of below -0.10% amid the risk averse tone and as prices tracked the moves in T-notes following the comments from Fed’s Bullard, while 10yr JGB auction results showed higher accepted prices.

Top Asian News

- China to Audit Sanofi, Bristol-Myers in Drugmaker Accounts Probe

- Australia Cuts Key Rate to Record Low, Ending Near 3-Year Pause

Major European indices are now firmer [Euro Stoxx 50 +0.6%] and diverting from the negative overnight session as tech suffered with FAANG stocks underperforming on Wall St. due to reports that the US is launching an antitrust and business practice probe into tech names. While tech names still lag, the sectors has come off of lows as equities have been grinding higher this morning with no significant fundamental drivers behind the move. EU sectors are mixed, with the aforementioned tech sector underperforming on the potential probes into tech names; sector heavyweight SAP (-1.5%) is the notable negative tech stock as it comprises a 27.6% sector weighting, and has over a 10% weighting in the DAX (+0.8%). Elsewhere, other notable movers this morning include Hargreaves Lansdown (-4.2%) at the bottom of both the Stoxx 600 and FTSE 100 (+0.2%), following concern over customer backlash as the Co. had promoted the Woodford fund extensively in-spite of its underperformance, the Co. finally removed the fund from their recommendation list on Monday. Towards the top of the Stoxx 600 rests Telecom Italia (+3.3%) after a filing showed the Co’s CFO purchased 150k ordinary shares. Separately, much of the sessions positive stock activity has been driven by broker moves with the likes of Lagadere (+2.2%), Royal Mail (+3.3%), BMW (+1.9%) and Volkswagen (+2.2%) supported by broker moves.

Top European News

- U.K. Construction Declines at Sharpest Pace in More Than a Year

- ECB Pressured as Euro-Area Inflation Slows More Than Forecast

- Billionaire-Backed Coloplast Said to Mull Urology Asset Sale

- European Tech Stocks Plunge as U.S. Antitrust Sell-Off Spreads

In FX, the Dollar is trying to recover after another bout of post-Bullard selling pressure pushed the DXY through 97.000, albeit marginally and briefly, with the index back above the big figure and now probing fresh highs within a 97.265-96.987 range as certain G10 counterparts succumb to independent bearish impulses. However, Buck bulls and bears will now be focusing on a raft of Fed speakers to see if other members turn more dovish, and in particular Chair Powell.

- AUD/EUR – Both holding up relatively well in the face of seemingly negative factors as RBA Governor Lowe flags further policy easing and a potentially lower than previously forecast OCR by the end of 2019 (was 1% vs the current 1.25% after last night’s 25 bp cut), while Eurozone inflation missed already considerably softer consensus forecasts. Aud/Usd remains firmly above 0.6950 around 0.6975 between 0.6955-93 trading parameters, and Eur/Usd is pivoting 1.1250 where the top of a band of option expiries reside (1 bn from 1.1235), but capped at the 100 DMA (1.1278).

- GBP/CAD/JPY – All a fraction firmer against the Greenback, as Cable straddles 1.2650 and shrugs off another poor UK PMI, but the Pound underperforms vs the Euro on political/Brexit grounds (cross hovering just below 0.8900). Meanwhile, the Loonie is also displaying a degree of resilience in the face of weak crude prices and testing offers/resistance ahead of 1.3400 in a 1.3450-20 band and the Yen extended safe-haven gains through 108.00 to 107.85 before losing some momentum.

- CHF/NZD – The major ‘laggards’ with the Franc stalling ahead of 0.9900 and Kiwi also finding it tough to breach a round number at 0.6600 vs its US rival as the Aud/Nzd cross rebounds from pre-RBA levels amidst general Aussie short covering and profit taking.

- EM – Contrasting fortunes for the Lira and Rand, as Usd/Try retreats further from 6.0000 towards 5.8100 in spite of more talk from Turkish President Erdogan about the merits of Russia’s S-400 system over the US F-35 alternative that could trigger sanctions. However, Usd/Zar has rallied over 1% to just shy of 14.6500 in wake of significantly weaker than expected SA GDP data.

In FX, the energy market continues to be pressured as the ongoing trade concerns dampens global demand output, with WTI (-0.6%) and Brent (-0.6%) on the backfoot in early European trade following on from a lacklustre Asia-Pac session. News-flow this morning has largely been from the OPEC front in which a letter showed that Iran opposes delaying the OPEC meeting to July, whilst Algeria and Kazakhstan have also told OPEC that the early July dates are unsuitable. This comes amid split views as to whether the OPEC/OPEC+ meeting should be at the end of June or in early July (touted dates July 3rd/4th), which Russia is in favour for. Furthermore, sources stated that Russian production this month fell to 10.87mln, down from the prior month’s 11.11mln BPD which was reported via the Energy Ministry. Finally, traders will be eyeing tonight’s API data for any signs of a short-term catalyst, with the street looking for headline inventories to draw by around 1.8mln BPD. Elsewhere, gold (Unch) is choppy and largely unchanged intraday as the yellow metal gave up its gains as the Buck recovered. Meanwhile, copper is little changed as the weaker Dollar countered the soured risk sentiment. Finally, Zinc prices dropped to six-month lows overnight amid a deterioration of the global outlook, with the recent China PMIs pointing to growth of just 4.5%-5%, according to CapEco.

US Event Calendar

- 10am: Factory Orders, est. -0.95%, prior 1.9%; Factory Orders Ex Trans, prior 0.8%

- 10am: Durable Goods Orders, prior -2.1%; Durables Ex Transportation, prior 0.0%

- 10am: Cap Goods Orders Nondef Ex Air, prior -0.9%; Cap Goods Ship Nondef Ex Air, prior 0.0%

DB’s Jim Reid concludes the overnight wrap

It looked like we were going to get an up day to start the week yesterday but the rally stalled in the US session as large-cap names dragged down the major indices. The S&P 500 ended -0.29%, despite the fact that 72% of companies in the index advanced on the day, only the eighth day this year where the index ended lower despite the majority of names rallying. The -7.51% and -6.11% moves for Facebook and Alphabet outweighed their smaller peers (a mere $85bn of lost market cap between the two), as the Federal Trade Commission and Justice Department reportedly opened investigations into the two companies respectively. The NASDAQ and NYFANG indexes accordingly fell -1.61% and -3.54% to their lowest levels since February and January, respectively, though the Philly semiconductor index outperformed tech peers by advancing +0.33%.

Meanwhile, in rates, treasuries continued their seemingly relentless rally, boosted by softer data and Fedspeak which raised the expectations for near-term policy easing. Ten-year yields fell another -4.7bps (but up +3.4bps this morning) while 2-year yields dropped -8.0bps (up +5.9bps this morning), taking their two-session move to -22.1bps and their 5-day move to -32.4bps. Both are the sharpest such drops since 2008. Futures markets last night priced a fairly startling 68bps of cuts this year. The front-end rally also continued to support the yield curve, with the 2y10y curve steepening +3.4bps to 23.4bps (+21.3bps this morning) – so that’s one silver lining to this whole episode. In Europe, Bunds did hit an intraday low of -0.221% before ending at 0.201% while the euro was a little bit stronger at $1.1242. Elsewhere HY credit spreads were +12bps wider in the US while oil prices fell -1.21%.

The data was the main talking point yesterday following the final PMI revisions in Europe and then the ISM manufacturing in the US. We’ll touch on the details further down but in short there wasn’t a great deal of change in Europe but in the US we saw a 31-month low for the ISM which was slightly tempered by better under-the-hood component details. That in itself causes some problems for markets though as it creates a bit more of a headache for the Fed as they battle with increasingly aggressive market pricing which has completely shifted towards more than two rate cuts this year and almost four over the next 12 months.

Turning to yesterday’s Fedspeak, the highlight was a series of comments from St. Louis Fed President Bullard, who is a voter this year, who said that “a downward policy adjustment may be warranted soon.” That’s the first time this year that an official has directly called for a rate cut. Bullard noted that “the direct effects of trade restrictions on the US economy are relatively small, but the effects through global financial markets may be larger.” He also conspicuously used the word “now” with regards to policy easing, which raises the odds that he votes for a rate cut as soon as this month’s meeting. Separately, Richmond Fed President Barkin also referenced tariff uncertainty as a potential headwind, though he stopped short of talking about interest rate cuts.

Overnight, the US Secretary of State Mike Pompeo condemned China’s human rights record as we hit the 30th anniversary of the Tiananmen Square incident. He said “We urge the Chinese government to make a full public accounting of those killed or missing to give comfort to the many victims of this dark chapter of history,” in a statement issued at 12.01am Beijing time. Elsewhere, negative rhetoric around the US-China trade war continued with the US Treasury Department and the Trade Representative office saying that its ‘disappointed’ that China is misrepresenting trade talks while saying that the US positions in negotiations have been ‘consistent’ while China ‘back-pedaled’. The joint statement also added that the Chinese have used the ‘White Paper’ and recent public statements to “pursue a blame game misrepresenting the nature and history of trade negotiations between the two countries.” Meanwhile, Bloomberg reported (citing sources) that the Congressional Republicans, worried about the possible economic fallout from President Trump’s plan to impose a tariff on Mexico, are considering whether to revive a resolution of disapproval over the national emergency declaration that underpins Trump’s justification for the tariffs. The action would also stop the president from spending billions on a border wall without congressional approval.

This morning in Asia markets are largely heading lower with the Shanghai Comp (-0.84%) and Hang Seng (-0.33%) trading down while the Nikkei (-0.01%) and Kospi (+0.02%) are trading flattish after erasing earlier losses. Elsewhere, futures on the S&P 500 are up +0.14% though. WTI oil prices are down -0.17% this morning, bringing the four day decline to -10.11%, despite Saudi Energy Minister Khalid Al-Falih saying yesterday that he was committed to doing whatever it takes to stabilize markets.

In other news, President Trump yesterday called on the UK to throw off the “shackles” of European Union membership and strike a free-trade deal with the US. Trump tweeted, “Big Trade Deal is possible once UK gets rid of the shackles,” and “Already starting to talk!” Elsewhere, French President Emmanuel Macron reinforced his hardline stance on Brexit, saying Brexit must happen at the end of October and there should be no more extensions. Meanwhile, the UK’s former foreign secretary Boris Johnson launched his leadership campaign yesterday, saying the U.K. must leave the bloc in October, with or without a deal.

Back to the details of yesterday’s data, where the May ISM manufacturing in the US hit a new 31-month low of 52.1 (vs. 53.0 expected) – down -0.7pts from April. The good news was that both the new orders (+1.0pt to 52.7) and employment (+1.3pts to 53.7) components improved. Even the prices paid component bounced +3.2pts to 53.2. How much of the latest tariff escalation is in the data however remains to be seen. In the meantime a quick refresh of our equities versus ISM regression shows that the US equities are around 5% ‘cheap’ given that markets have fallen more than the data has. Indeed the equity market-implied ISM is actually now below 50 at 49.8. However for this to be a buying opportunity you have to believe the ISM will settle at these levels over the summer in the face of rising trade tensions. That data followed a small -0.1pt downward revision to the rival Markit PMI release to 50.5 while elsewhere construction spending was flat, versus expectations for a slight rise, though the prior month was revised higher leaving the overall trend roughly neutral.

In Europe, the final manufacturing PMI for the Euro Area was unrevised at 47.7 which means it is -0.2pts down from April and 0.2pts higher than the March lows. Our economists did highlight that there were some green shoots of optimism in the details with the new orders subindex up more than +2pts in the past two months (albeit still at a lowly 46.6) while there were similar moves in both output and the new export order series.They also noted that new orders-to-inventories difference, which tends to lead the headline and output indices, is back to August/September 2018 levels – still negative but signalling that we are perhaps past the trough in the manufacturing PMI. The question though is whether a genuine recovery of the manufacturing sector can be expected especially now the trade war has been reignited. Meanwhile, at a country level Germany and France were unrevised at 44.3 and 50.6 respectively while a big drop for Spain (-1.7pts to 50.1) was partly offset by a +0.6pt advance for Italy to 49.7. Greece (-2.2pts to 54.2) was another country that deteriorated however it is only behind Hungary (57.9) at the top of the EU ranks now. Our regression of European equities versus PMIs now has the STOXX fairly valued but equity markets in France, Italy and Spain all slightly cheap. Only Germany appears expensive on this measure due to how low the German PMI is relative to history. However these are a very broad guide and work best for general market valuations especially when there are big outliers. It’s hard to say there are at the moment. On our measure most global equity markets price in high 40s on the manufacturing PMIs/ISM, and in the US we are still above this and therefore cheap, whilst in Europe we are generally at that level or a bit lower.

Here in the UK, the latest PMI reading of 49.4 was a little worrying, printing -2.6pts lower than expectations and also -3.7pts below the April level. It’s worth flagging that rising stockpiles had been behind some of the recent manufacturing resilience in the UK so it isn’t a huge surprise to now see this filter out and therefore the UK start to catch down to the rest of Europe. It’s worth noting also that the last time the UK PMI went sub-50 was in 2016 and when the BoE last cut rates. One ray of positivity came from Sweden’s manufacturing PMI which came in +2.7pts better than expected at 53.1. Sweden, as a highly cyclical economy, has tended to lead the rest of Europe, so its bounce could be cause for optimism moving forward.

In other news, our economists in Germany published their views on the surprising weekend resignation of SPD party leader and chief whip Andrea Nahles over the weekend. They note that the implications are clearly negative, and go as far as saying that it is hard to see how the Groko might still be in place at the end of the year given the current dynamics in the SPD. They highlight that if the SPD pull out of the coalition, then snap elections are most likely as the Greens rejected joining the government on the basis of the 2017 election results. The Greens currently score around 20% in the polls giving them a much stronger weight in a possible future conservative-green government. See more in our colleagues’ report here .

To the day ahead now, which this morning includes the advanced May CPI report for the Euro Area where the consensus expects a +0.9% yoy core reading compared to +1.3% in April. We’ll also receive the April unemployment rate while data in the US this afternoon includes final durable and capital goods orders revisions for April, as well as April factory orders data. Away from that the Fed’s Williams is due to speak just after lunch before the two-day Fed conference gets underway including opening remarks from Powell at 2.55 pm BST.

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 27.80 POINTS OR 0.96% //Hang Sang CLOSED DOWN 132.34 POINTS OR 0.49% /The Nikkei closed DOWN 2.34 POINTS OR 0.01%//Australia’s all ordinaires CLOSED UP .01%

/Chinese yuan (ONSHORE) closed DOWN at 6.9087 /Oil DOWN TO 52.49 dollars per barrel for WTI and 60.38 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED UP // LAST AT 6.9087 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9287 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China

In a new report, we find out how China is circumventing the tariffs by exporting to nations not subject to tariffs and then this is re imported back into the USA without the tariffs implemented.

(courtesy zerohedge)

Shocking New Report Exposes How Chinese Companies Are Dodging US Tariffs

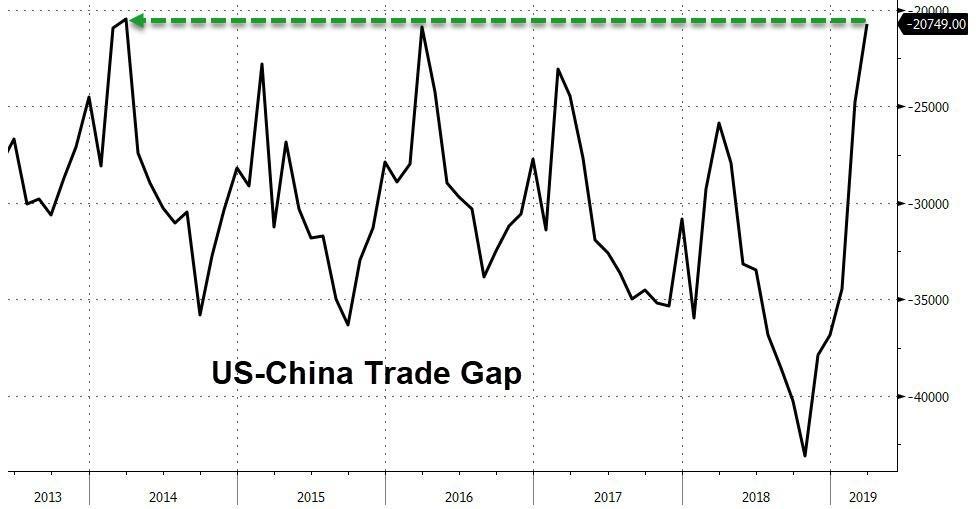

While the US trade deficit declined only marginally in March, we posited that the unexpectedly large decline in the US-China bilateral trade deficit might be of greater interest to both the Trump Administration and the general investing public because – as both Zero Hedge and Bloomberg argued – it is an unequivocal sign that President Trump is, in at least one respect, “winning” the trade war.

In March (the most recent month for which data are available), the bilateral trade gap shrank to just $20.75 billion, the lowest level since March 2014.

All told, official US data showed that official Chinese exports to the US tumbled by $15.2 billion, or 12%, in the late January-March quarter of 2019 on an annualized basis.

Since these data were collected before President Trump raised tariffs on $200 billion in Chinese goods in the latest round of trade-war escalation, the conventional wisdom would dictate that the bilateral deficit will probably continue to improve, as US companies source their goods from other foreign markets, or – as President Trump would undoubtedly prefer – opt to manufacture them in the US.

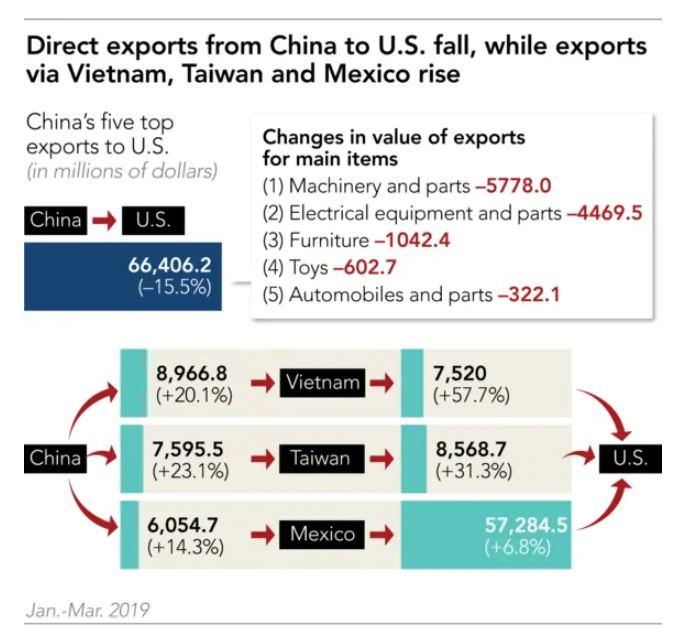

And while that may or may not turn out to be true, Nikkei Asia Review raised questions about whether these data accurately reflect the impact of the tariffs on Chinese exporters – and, by extension, the Chinese economy – with an explosive report published Monday describing how Chinese exporters are using intermediaries to get around the tariffs.

In an analysis of data from the US International Trade Commission and the International Trade Center, Nikkei revealed that while exports of machinery, electrical equipment and some other products impacted by tariffs have reflected particularly sharp declines, shipments of these goods from China to the US via Vietnam, Taiwan and Mexico actually rose during this period, a sign that exporters are rejiggering their supply chains to compensate for the US tariffs.

Of course, Chinese companies have other ways of compensating for American tariffs. President Trump railed against China’s “subsidizing” of goods to keep them competitive in American markets. Washington has repeatedly criticized Beijing for unfairly subsidizing state-backed companies, and although the Treasury once again declined to name China a currency manipulator, the weakness in the Chinese yuan has also elicited criticism.

Donald J. Trump

✔@realDonaldTrump

China is subsidizing its product in order that it can continue to be sold in the USA. Many firms are leaving China for other countries, including the United States, in order to avoid paying the Tariffs. No visible increase in costs or inflation, but U.S. is taking Billions!

But Nikkei’s calculations suggest that the tariffs are being offset, at least in part, by exports to Vietnam, Mexico and Taiwan, much of which are then routed to the US.

Five key items which have suffered the biggest declines were analyzed: machinery and parts; electrical equipment and parts; furniture; toys; and automotive equipment and parts.

In the case when China’s exports to the U.S. are classified in accordance with customs codes, the volume of products including machinery and parts, and electrical equipment and parts, slumped conspicuously.

In the first quarter of this year, exports of machinery and parts plunged by $5.77 billion from a year earlier, while exports of electrical equipment and parts plummeted by $4.46 billion year-on-year.

With the exception of toys, four of these five items have become subject to three rounds of punitive import tariffs imposed by the administration of U.S. President Donald Trump.

While exports of the five items from China to the U.S. between January and March declined by 16%, equivalent to a value of $12.2 billion, exports from China to developing countries and from developing countries to the U.S. have generally climbed. Exports via Vietnam, Taiwan and Mexico have increased particularly steeply.

In January-March 2019, exports of the five items from China to Vietnam rose by $1.5 billion, or 20%, while exports of the five items from Vietnam to the U.S. surged by $2.7 billion, or 58%.

In the same three-month period, exports of the five items from China to Taiwan increased by $1.4 billion, or 23%, while such exports from Taiwan to the U.S. expanded by $2.0 billion, or 31%.

Exports from China to the U.S. via Mexico also increased. Mexico’s exports to the U.S. surpassed those of China to become the biggest source in March.

Here’s a breakdown of the chart: