GOLD: $1330.00 UP $6.00 (COMEX TO COMEX CLOSING)

Silver: $14.83 UP 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1330.00

silver: $14.83

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 6/52

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,323.400000000 USD

INTENT DATE: 06/04/2019 DELIVERY DATE: 06/06/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 30

357 C WEDBUSH 1

657 C MORGAN STANLEY 1

661 C JP MORGAN 8

686 C INTL FCSTONE 22 6

690 C ABN AMRO 1

737 C ADVANTAGE 19 4

800 C MAREX SPEC 7 1

905 C ADM 3 1

____________________________________________________________________________________________

TOTAL: 52 52

MONTH TO DATE: 500

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 52 NOTICE(S) FOR 5200 OZ (0.1617 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 500 NOTICES FOR 50000 OZ (1.555 TONNES)

SILVER

FOR JUNE

0 NOTICE(S) FILED TODAY FOR NIL OZ/

total number of notices filed so far this month: 262 for 1310,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 7856 UP 168

Bitcoin: FINAL EVENING TRADE: $ 7650 DOWN 545

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A CONSIDERABLE SIZED 2644 CONTRACTS FROM 213,481 UP TO 216,145 DESPITE THE TINY 1 CENT GAIN IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER AND IT STOPPED FOR GOLD AS WELL. WE WILL WITNESS A RISE IN THE SPREADERS IN SILVER ONCE WE START TRADING IN JUNE… READY FOR THE FIRST DAY NOTICE JULY CONTRACT.) TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A LARGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 2475 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2475 CONTRACTS. WITH THE TRANSFER OF 2475 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2475 EFP CONTRACTS TRANSLATES INTO 12.38 MILLION OZ ACCOMPANYING:

1.THE 1 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.330 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

8998 CONTRACTS (FOR 3 TRADING DAYS TOTAL 8998 CONTRACTS) OR 44.990 MILLION OZ: (AVERAGE PER DAY: 2966 CONTRACTS OR 14.83 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 44.99 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.41% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 933.70 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2664 WITH THE 1 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A VERY HUGE SIZED EFP ISSUANCE OF 2475 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED AN ATMOSPHERIC SIZED: 5139 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2475 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 2664 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A TINY 1 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.79 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.067 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL, OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.330 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE PROBABLY HAD GOOD ACTIVITY OF THE SPREADING ACCUMULATION IN SILVER TODAY//

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG SIZED 4791 CONTRACTS, TO 481,495 DESPITE THE TINY $0.85 PRICE GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// YESTERDAY/THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADING FELLOWS WILL MORPH INTO SILVER ONCE JUNE GETS UNDERWAY. THE GAIN IN OI GOLD CONTRACTS IS REAL AND NOT PUMPED UP BY SPREADING.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 14,486 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 14,486 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 481,495. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 19,277 CONTRACTS: 4791 OI CONTRACTS INCREASED AT THE COMEX AND 14,486 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 19,277 CONTRACTS OR 1,927,700 OZ OR 59.95 TONNES. YESTERDAY WE HAD A TINY GAIN OF $0.85 IN GOLD TRADING….AND WITH THAT GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 59.95 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 41,971 CONTRACTS OR 4,197,100 OR 130.54 TONNES (3 TRADING DAYS AND THUS AVERAGING: 13,990 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAYS IN TONNES: 130.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 130.54/3550 x 100% TONNES =3.67% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2408.46 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 4791 DESPITE THE TINY PRICING GAIN THAT GOLD UNDERTOOK ON YESTERDAY($0.85)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 14,486 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 14,486 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC SIZED GAIN OF 19,277 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

14,486 CONTRACTS MOVE TO LONDON AND 4791 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 59.95 TONNES). ..AND THIS GAIN OF DEMAND OCCURRED WITH THE RISE IN PRICE OF $0.85 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 52 notice(s) filed upon for 5,200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $6.00 TODAY// MY GOODNESS IS THIS STRANGE:

???A WITHDRAWAL OF 2.06 TONNES OF GOLD FROM THE GLD…IT LOOKS LIKE THE CROOKS FOUND SOME PHYSICAL TO SENT OFF TO LONDON

INVENTORY RESTS AT 757.59 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 1 CENT TODAY:

A HUGE CHANGES IN SILVER INVENTORY AT THE SLV:

AN ADDITION (DEPOSIT) OF 2.396 MILLION OZ OF PAPER SILVER ADDED TO THE GLD.

/INVENTORY RESTS AT 314.434 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 2664 CONTRACTS from 213.481 UP TO 216,145 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER AND GOLD FOR NOW BUT WILL NOW MORPH INTO SILVER AS THE COMEX SILVER MONTH OF JUNE COMMENCES IN EARNEST..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 2475 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2475 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2644 CONTRACTS TO THE 2475 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC GAIN OF 5139 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 26.87MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 1.330 MILLION OZ FOR JUNE.

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 1 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A HUGE SIZED 2475 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 0.86 POINTS OR 0.03% //Hang Sang CLOSED UP 133.92 POINTS OR 1.80% /The Nikkei closed UP 367.56 POINTS OR 1.80%//Australia’s all ordinaires CLOSED UP .42%

/Chinese yuan (ONSHORE) closed DOWN at 6.9091 /Oil DOWN TO 52.49 dollars per barrel for WTI and 60.38 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.9091 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9206 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China

The USA braces for Chinese retaliation as they scramble to find alternative to rare earth suppliers. China supplies 80% of the rare earths

( zerohedge)

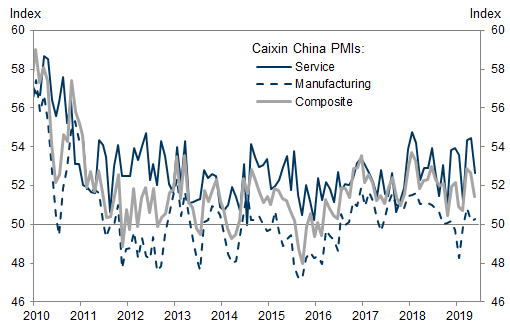

ii)Awful PMI numbers coming out of China last night as both the Mfg PMI which went into contraction and the Service PMI close to contraction!!

( zerohedge)

iv)China/Russia

( zerohedge)

4/EUROPEAN AFFAIRS

i) ITALY

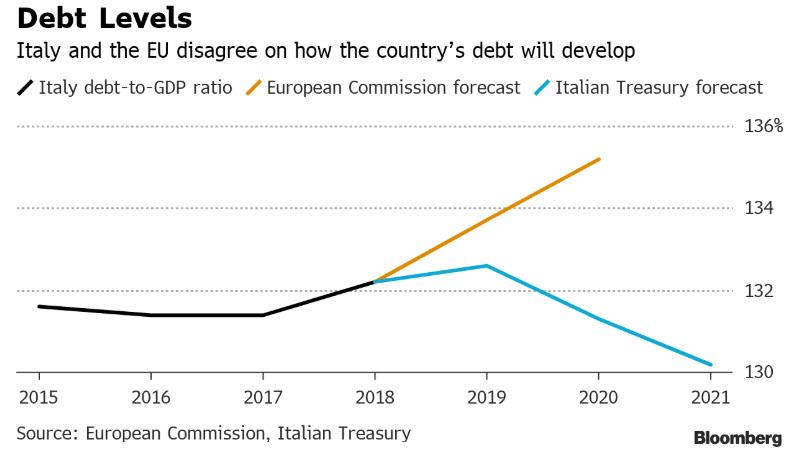

This is big!! Italian stocks and bonds slide after the EU officially triggers disciplinary action over |Italy;s large Debt which now stands at 132% /GDP heading towards 135% due to the high 2.5% deficit in this years spending. Strangely Brussels is now going to sanction Italy 3.5 billion euros for being consistently offside. Expect a full war between Italy and Brussels and this may be the signal that Salvini wishes for as he really wants to leave the Euro and then that will collapse all the European banks

( zeorhedge)

ii)The atomic blast has just been delivered. Italy is now poised to issue a Euro parallel currency called a Mini bot. You can say that it is the forerunner to a newly introduced Lira.

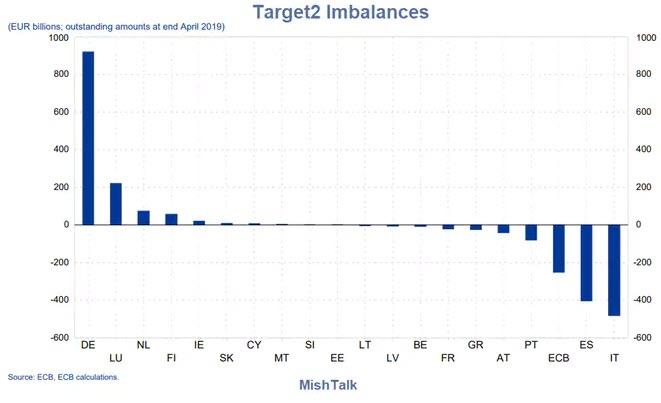

I have been telling you for the past several years the problem facing the ECB and Germany with respect to the Target 2 imbalances. Germany is owed 1 trillion euros from the likes of Italy and Spain (also Portugal). If Italy walks and forms the Lira then the rest of the EU must share according to their GDP percentages part of the debt including Italy at 17% and surely they will not pay. Also Greece and Portugal and Spain will not pay. Then the only solution is for the ECB to print 1 trillion euros and pay Germany. That will cause gold and silver to skyrocket and send the euro tumbling to nothing.

Italy points out that France is in worse shape than Italy and they have been having constant deficits since the start of the Euro scheme.

I would say that Italy that the upper hand.

(courtesy Mish Shedlock)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

i)THE GLOBE/AIR CARGO

A strong indicator that global growth is plunging

( zerohedge)

ii)Mexico

iii)Australia

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

( Bloomberg/GATA)

ii)Deutsche bank gets it keep the 20 tonnes of gold received through a swap with Venezuela. Deutsche bank is so off side with its precious metals derivatives the small sum of 20 tonnes will not help them one bit.

(bloomberg/GATA)

iii)China is not looking at European investments as it departs dollar investments

(Reuters/GATA)

iv)Craig comments on the Fed Chairman Powell’s announcement that interest rates will now revert southbound as the economy is now moribund..expect the dollar to plummet, gold and silver to skyrocket…

( Craig Hemke/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading/early morning/

ii)Market data

a)Wow! this was a surprise. The ADP report is always bullish and rarely do we see a miss..except today. They report only a tiny gain of 27,000 jobs on expectations of 185,000

(zerohedge)

b)This is not good!! Services is by far the bigger part of USA GDP. Now we see that growth is the weakest since over 3 years.

(courtesy zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

a)What a riot..CNN ratings plunge again

( zerohedge)

b)USA/China

( zerohedge)

c)Hong Kong’s major newspaper, the South China Morning Post comments and warns USA farmers that they will lose the Chinese market for good if Trump continues with his tariffs. They state that the tariff impact in China on an increase of Chinese tariffs on USA goods will not be a big factor

( South China Morning Post)

d)Bill Blain’s open letter to Powell highlighting the folly of the Fed

SWAMP STORIES

Let us head over to the comex:

Gold withdrawals;

i) We had 1 withdrawal:

out of BRINKS: 4983.405 oz

.

Gold Hi

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Russia states that it consider exporting more gold only after purchasing gold at a discount from market prices. From the data received so far this year, the official gold that Russia is reporting is basically the gold produced from within Russia

(courtesy Bloomberg)

Russian banks consider exporting more gold

Submitted by cpowell on Wed, 2019-06-05 00:53. Section: Daily Dispatches

By Elena Mazneva and Yuliya Fedorinova

Bloomberg News

Tuesday, June 4, 2019

Russian banks are considering increasing gold exports after the central bank said it would buy gold only at a discount, a move that could pressure global bullion prices.

The Bank of Russia made the change to its pricing policy this year, saying it would buy from dealers at a level slightly below the benchmark London gold price. It’s part of a broader policy push to stimulate growth in the market for gold as a financial investment, namely bars and coins, rather than foreign currencies or assets priced in U.S. dollars.

…

However, gold as an investment option in Russia doesn’t have the same cachet as in other countries, like China or the United States, and demand for the metal has been stagnant. Given the new discount, some dealers may be reluctant to sell to the central bank, said Oleg Petropavlovskiy, a BCS Global Market analyst. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-06-04/russian-banks-mull-ex…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

Deutsche bank gets it keep the 20 tonnes of gold received through a swap with Venezuela. Deutsche bank is so off side with its precious metals derivatives the small sum of 20 tonnes will not help them one bit.

(bloomberg/GATA)

Deutsche Bank gets to keep gold swapped by Venezuela

Submitted by cpowell on Wed, 2019-06-05 00:59. Section: Daily Dispatches

Venezuela Defaults on Gold Swap with Deutsche Bank

By Patricia Laya

Bloomberg News

Tuesday, June 4, 2019

Venezuela has defaulted on a gold swap agreement valued at $750 million with Deutsche Bank AG, prompting the lender to take control of the precious metal which was used as collateral and close out the contract, according to two people with direct knowledge of the matter.

As part of a financing agreement signed in 2016, Venezuela received a cash loan from Deutsche Bank and put up 20 tons of gold as collateral. The agreement, which was set to expire in 2021, was settled early due to missed interest payments, said the people, who asked not to be named speaking about a private matter.

In the meantime, opposition leader Juan Guaido’s parallel government has asked the bank to deposit $120 million into an account outside President Nicolas Maduro’s reach, which represents the difference in price from when the gold was acquired to current levels. As part of efforts to unseat Maduro, the U.S. and more than 50 countries have recognized Guaido as the legitimate leader of Venezuela even though he still doesn’t control key institutions at home, including the central bank.

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-06-04/venezuela-is-said-to-…

end

China is not looking at European investments as it departs dollar investments

(Reuters/GATA)

China looks beyond U.S. Treasuries for dollar investments

Submitted by cpowell on Wed, 2019-06-05 01:09. Section: Daily Dispatches

By Abhinav Ramnarayan, Virginia Furness

Reuters

Tuesday, June 4, 2019

LONDON — China may be expanding its investments beyond U.S. Treasuries into debt issued by top-rated European and other government agencies, allowing it to keep its money in dollar assets while picking up some extra yield, bankers with knowledge of the matter say.

At least four investment banking officials who deal with public-sector debt report a spike in interest from China in government-linked borrowers, who can offer an alternative to U.S. Treasuries.

…

Prominent among these are the European Investment Bank, a development bank backed by European Union countries, KfW, a German government-guaranteed institution, and AIIB, a Beijing-based pan-Asian development bank that issued its first ever bond last month. …

… For the remainder of the report:

https://www.reuters.com/article/china-treasuries/china-looks-beyond-u-s-…

end

Craig comments on the Fed Chairman Powell’s announcement that interest rates will now revert southbound as the economy is now moribund..expect the dollar to plummet, gold and silver to skyrocket…

(courtesy Craig Hemke/GATA)

Craig Hemke at Sprott Money: Fed policy reversal is imminent

Submitted by cpowell on Wed, 2019-06-05 01:22. Section: Daily Dispatches

9:21p ET Tuesday, June 4, 2019

Dear Friend of GATA and Gold:

The Federal Reserve, the TF Metals Report’s Craig Hemke writes today at Sprott Money, is trapped and cannot raise interest rates and “normalize” its balance sheet without worsening the turmoil already underway in financial markets. Fed policy, Hemke writes, will soon revert to interest rates cuts and “quantitative easing,” monetary devaluation that should be good for the monetary metals.

Hemke’s analysis is headlined “Fed Policy Reversal Now Imminent” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/fed-policy-reversal-now-imminent-craig-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

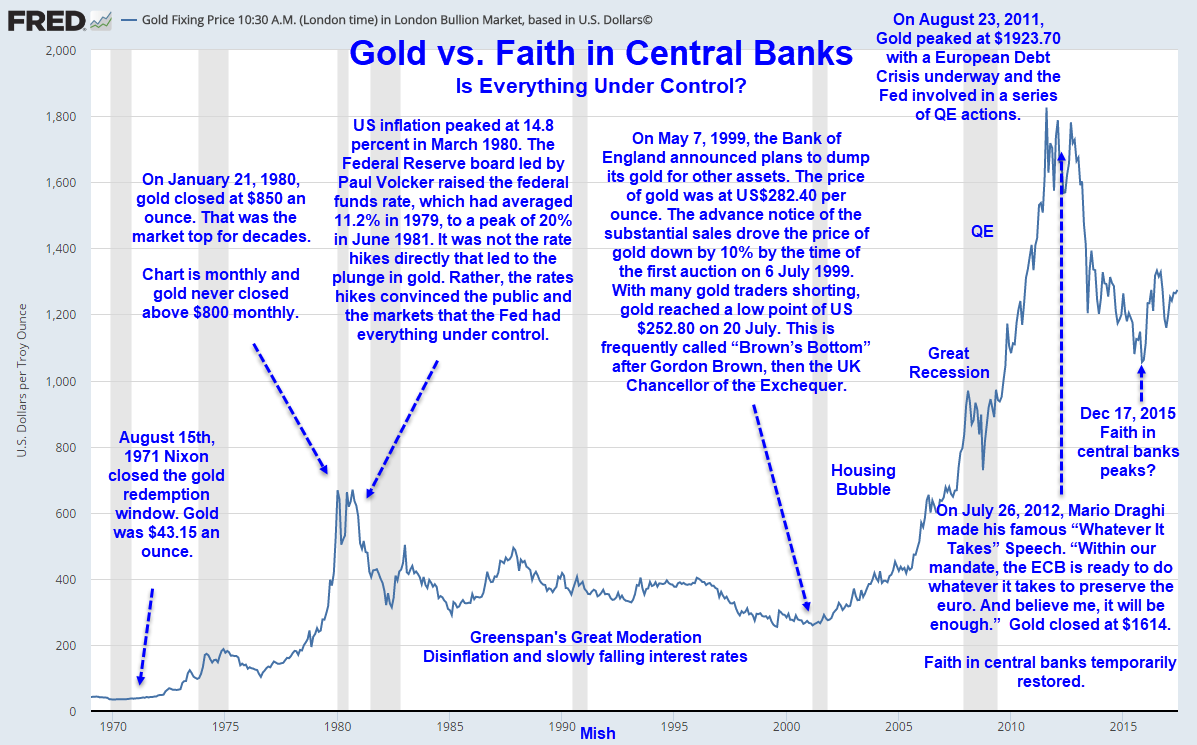

Mish: Gold Gains As Faith In Central Banks Is About To Be Tested Again

Authored by Mike Shedlock via MishTalk,

Gold put in a strong performance with the St. Louis Fed president presenting a case for cutting rates.

St. Louis Fed president James Bullard helped light a fire under gold today, Yapping About Too Little Inflation and the Need for Rate Cuts.

Technically speaking, the $1350 to $1370 area has been one tough nut for gold to crack.

On a weekly chart, gold has failed in this area five or six times, depending on how one counts.

Gold a Hedge, But Against What?

Some view gold as an inflation hedge.

It isn’t.

Gold is a hedge against the notion that the Fed has things under control.

Gold fell from $850 an ounce in 1980 to $262 an ounce in in 1999 with inflation every step of the way.

People believed Greenspan, the great “maestro” had everything under control. It was an illusion.

Faith in central banks is about to be tested again.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

end

* * *

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9071/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9206 /shanghai bourse CLOSED DOWN 0.86 POINTS OR 0.03%

HANG SANG CLOSED UP 133.92 POINTS OR 0.50%

2. Nikkei closed UP 367.56 POINTS OR 1.80%

3. Europe stocks OPENED GREEN EXCEPT ITALY /

USA dollar index FALLS TO 97.08/Euro RISES TO 1.1264

3b Japan 10 year bond yield: FALLS TO. –.12/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.31/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.10 and Brent: 61.76

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.22%/Italian 10 yr bond yield UP to 2.61% /SPAIN 10 YR BOND YIELD DOWN TO 0.65%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.83: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.96

3k Gold at $1335.10silver at: 14.85 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 1/100 in roubles/dollar) 65.09

3m oil into the 53 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.31 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9917 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1166 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.22%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.12% early this morning. Thirty year rate at 2.62%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7031..

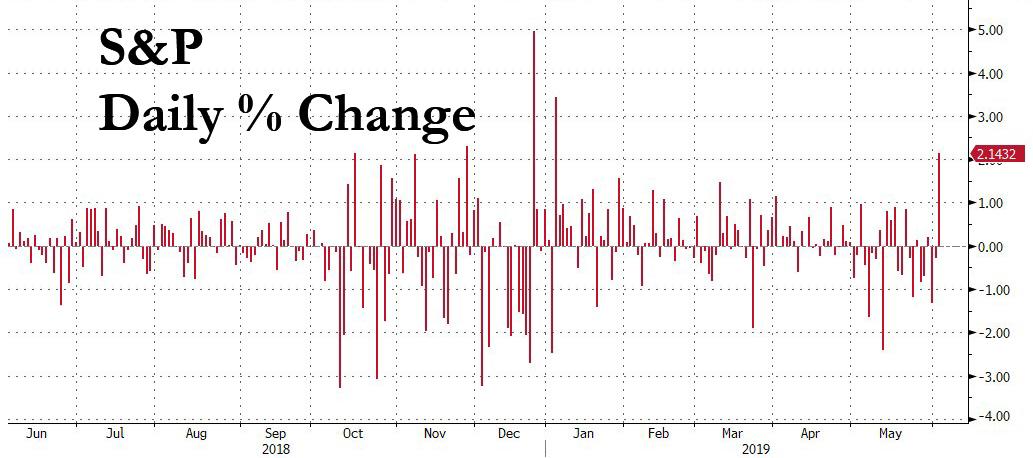

Global Markets Roar Higher After Powell Spikes The Koolaid

After the second best day for the S&P in 2019, which saw the US stock market surge by 2.14%…

… global stocks gained for a third straight day on Wednesday, paradoxically bolstered by growing hopes that the global economy is deteriorating fast enough so that the Fed will cut interest rates this year – perhaps as soon as this month – to avert a recession, while the dollar languished near seven-week lows.

“The market is sending out invitations for a rate cut party, and waiting for the Fed to turn-up,” said Greg Gibbs, director and founder of Amplifying Global FX. Powell “gave just enough hint that he might turn up, but he is still reluctant to acknowledge that risks to growth have increased.”

And while Powell made ‘terrible news great again’, as observed late last night when the China Caixin Services PMI dropped again by 1.8 to 52.7 in May, below consensus expectations (the sub-indexes suggest slow down in the growth of services exports orders, new business and employment, though inflationary pressures were reduced slightly in the services sector)…

… in turn sending futures even higher, the overnight rally has cooled somewhat amid lingering trade-war concerns.

Global equities, and US index futures advanced and the yen fell after Fed Chairman Jerome Powell said the central bank is monitoring the trade war’s impact and would act appropriately to sustain the U.S. expansion, opening the door to possible interest-rate cuts. Powell’s comments come a day after St. Louis Federal Reserve President James Bullard said in a speech that a rate cut may be needed “soon.”

Stock markets responded positively to Powell’s comments, with U.S. stocks registering their biggest one-day gains in five months. The optimism rolled over into markets on Wednesday, with the MSCI All-Country World Index up 0.4% after the start of European trading, adding further to a 1.4% gain on Tuesday.

“Whilst the markets are giddy on central bank support, the effects could be short-lived,” said London Capital Group’s Jasper Lawler. “Let’s not forget the other half of the equation is the escalating trade war on multiple fronts. Today the markets are happy to focus on Fed support, but with the U.S. Commerce Department promising retaliation in the event of China’s rare earth’s threat, this trade war looks set to get worse before it gets better.”

Technology shares led the advance in Europe’s Stoxx 600 index as software companies including SAP and Micro Focus jumped after a positive sales forecast by U.S. peer Salesforce.com. Sectors are somewhat mixed, with the Tech sector the notable outperformer, despite yesterday’s FAANG driven underperformance in tech names; where the sector lagged heavily for much of the session. Separately, TSMC Chairman Liu stated that the US’s move to ban US companies from doing business with Huawei is to have a short-term impact on TSMC, though the Co’s outlook remains unchanged, which may have provided some impetus to the European IT names.

Asian stocks gained, led by industrials and IT sectors. Japan and Hong Kong led the rally, while markets in Singapore, India, Philippines, Malaysia and Indonesia were shut today for public holidays. Japan’s Topix Index closed 2.1% higher. Hong Kong’s Hang Seng Index snapped its five-day losing streak, with Techtronic Industries Co. and WH Group Ltd. contributing most of the gains. Australia’s S&P/ASX 200 Index rose 0.4% after its central bank chief strongly suggested he could follow up Tuesday’s interest-rate cut with another reduction.

Overnight, the IMF cut its 2019 economic growth forecast for China to 6.2% on heightened uncertainty around trade frictions, saying that more monetary policy easing would be warranted if the Sino-U.S. trade war escalates.

Ten-year Treasuries were little changed and EU government bonds were mixed, while the euro strengthened to a seven-week high. Italy’s yields rose after the EU started a disciplinary process against the country over its debt. Germany’s 10-year bond yield reached a record low and Italian debt held on to this week’s gains as investors ramped up their bets on a generous loan package for banks in the euro zone as well as a U.S. rate cut. Germany’s 10-year bond yield reached a record low, following a spike in Japanese bonds which surged on speculation of more easing from the BOJ.

In FX, the dollar steadied after a four-day decline on short-term positioning as Treasuries edged up alongside most euro-area bonds. Global equities advanced and the yen fell after Fed Chairman Jerome Powell opened the door to possible interest-rate cuts. The kiwi led gains in Group-of-10 currencies after RBNZ’s Christian Hawkesby surprised traders with relatively hawkish comments. The euro climbed for a fourth day. The loonie and the Norwegian krone extended recent gains as oil prices consolidated, while sterling advanced on stronger-than-expected U.K. services data, and as Theresa May prepared to step down on Friday.

“Given the extent of the dovish re-pricing of the Fed outlook and the collapse in U.S. treasury yields in recent weeks, the dollar losses appear fairly muted in this context,” said Chris Turner, head of FX strategy at ING in London.

In the escalating feud between the US and Mexico, Trump stated that US Senate Minority leader Schumer gave Mexico bad advice in his suggestion that the tariffs on Mexico is a bluff, while Trump added it is ‘no bluff!’. Elsewhere, US Senate Majority leader McConnell said there is “not much support” from Republicans for tariffs on Mexico and hopes they can be avoided via talks with the Mexican delegation, while a US administration official said US-Mexico talks will be held at the White House later today.

In the latest Brexit news, former UK Foreign Secretary Boris Johnson warned Conservative MPs that a Brexit delay means defeat and that the Conservative Party faces “extinction” if Britain is not out of the EU by October 31st. Meanwhile, Trump backtracked regarding the NHS being part of a future US-UK trade deal and stated that he doesn’t see it being on the table as the health service was something that would not be consider part of trade, which was in contrast to a prior suggestion of including the NHS in trade discussions.

In commodity markets, oil prices resumed their slide, dragged down by a surprise gain in U.S. inventories and comments from the head of Russian state oil producer Rosneft questioning the point of a deal with OPEC to withhold supplies. In European trade, U.S. crude retreated 0.85% to $53.03 a barrel and Brent crude futures dropped 0.6% to $61.58 per barrel.[

Expected data include mortgage applications and employment change. Brown-Forman and Campbell Soup are among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.4% to 2,816.00

- STOXX Europe 600 up 0.5% to 374.39

- MXAP up 1% to 153.95

- MXAPJ up 0.4% to 502.83

- Nikkei up 1.8% to 20,776.10

- Topix up 2.1% to 1,530.08

- Hang Seng Index up 0.5% to 26,895.44

- Shanghai Composite down 0.03% to 2,861.42

- Sensex down 0.5% to 40,083.54

- Australia S&P/ASX 200 up 0.4% to 6,358.52

- Kospi up 0.1% to 2,069.11

- German 10Y yield unchanged at -0.206%

- Euro up 0.2% to $1.1273

- Italian 10Y yield fell 4.4 bps to 2.145%

- Spanish 10Y yield fell 2.6 bps to 0.639%

- Brent futures down 0.2% to $61.83/bbl

- Gold spot up 0.8% to $1,336.43

- U.S. Dollar Index down 0.2% to 96.93

Top Overnight News from Bloomberg

- In separate comments Tuesday, Fed Chair Jerome Powell and his No. 2, Richard Clarida, reassured nervous investors they’re watching closely for signs that disputes between the U.S. and its trading partners are denting the outlook for the world’s largest economy

- Treasury Secretary Steven Mnuchin will meet with the People’s Bank of China chief during the Group of 20 gathering of finance ministers and central bankers in Japan over the weekend, the Treasury Department said on Tuesday

- Democratic presidential candidate Elizabeth Warren called for “actively managing” the dollar to bolster U.S. jobs and growth, a move that would break from a longstanding currency policy agreement among the world’s 20 major economies

- Boris Johnson, the front-runner to replace Theresa May as U.K. prime minister, warned Conservative Party colleagues that they face “extinction” if they don’t deliver Brexit by the current deadline of Oct. 31

- The U.K. economy was ‘close to stagnation’ according to IHS Markit. Stronger-than-expected growth in Britain’s dominant services sector isn’t enough to make up for a poor performance in the rest of the economy, with data showing contractions in construction and manufacturing

- Strength among service providers helped economic activity in the euro area expand at a modest pace in May, though signs of a broader rebound continue to be elusive. A composite Purchasing Managers’ Index came in at 51.8, above the 51.6 initial estimate and higher than April’s reading

- It’s Japanese government bonds’ turn to take the lead in the global fixed-income melt-up as bets climb for the Bank of Japan to add to its stimulus. Japan’s two- year yield is on course for its biggest daily drop since January and swaps indicate that traders have priced in a full 10-basis point reduction in rates by next April

- Central banks are resuming their first-responder role as the world economy runs into trouble. Traders are betting the Fed will lower rates before year-end, Australia’s central bank cut rates Tuesday and India’s may follow this week while the ECB is bound to stay dovish

- Australia’s economy expanded slightly slower than forecast in the first three months of the year, as a housing downturn continued to weigh on growth

- Oil resumed declines as an industry report signaling a surprise jump in U.S. crude inventories stirred fears of a supply glut at a time when trade wars are jeopardizing the global demand outlook

Asian equity markets were higher as the region took impetus from the strength in the US where sentiment was buoyed after comments from Fed Chair Powell spurred hopes of a rate cut. This saw Wall St notch its biggest gain since early-January with the Nasdaq the frontrunner as tech outperformed, while all sectors in the S&P 500 closed in the green and the DJIA rallied by over 500 points. ASX 200 (+0.4%) gained in which tech led the upside and with risk appetite supported by the recent rate cut by the RBA, as well its openness to further reductions. Nikkei 225 (+1.8%) surged as Japanese exporters cheered a weaker currency and with SoftBank shares boosted as it expects to book a profit of around JPY 1.2tln on the partial sale of its Alibaba stake. Hang Seng (+0.5%) and Shanghai Comp. (U/C) conformed to the positive global risk tone but with gains capped by disappointing Chinese Caixin PMI data and a substantial liquidity drain of CNY 210bln by the PBoC, while trade concerns lingered after China issued a warning against travelling to the US and held a meeting on rare earths where experts recommended greater controls on exports of the metals. Finally, 10yr JGBs were higher with prices underpinned on the back of Fed Chair Powell’s dovishness and as Japanese 10yr yields slipped to their lowest in around 3 years.

Top Asian News

- Chinese Auto Group Calls for Stimulus to Help Spur Car Sales

- Diokno Says Rate Cut Inevitable as Faster May CPI Isn’t a Trend

- China Nominates Occupy-Era Hong Kong Police Chief for UN Post

- IMF Cuts China Growth Forecast, Citing Downside Trade War Risks

Major European indices [Euro Stoxx 50 +0.2%] are firmer, although somewhat more subdued than their Asia-Pac counterparts,which were boosted by Wall Street printing its largest daily gain since early-January. Sectors are somewhat mixed, with the Tech sector the notable outperformer, despite yesterday’s FAANG driven underperformance in tech names; where the sector lagged heavily for much of the session. Separately, but potentially of note for Tech names; TSMC Chairman Liu stated that the US’s move to ban US companies from doing business with Huawei is to have a short-term impact on TSMC, though the Co’s outlook remains unchanged, which may have provided some impetus to the European IT names. This morning’s most notable move is Provident Financial (+16.4%) on the back of Non-Standard Finance (-2.7%) stating that they are not going ahead with the hostile takeover. Also, in the green and towards the top of the Stoxx 600 are Norsk Hydro (+3.6%) after posting stronger than expected earnings; however, the Co. state that they expect to see payments relating to the cyber-attack in their Q3 earnings. Meanwhile, Saipem (+4.8%) shares spiked higher after announcing a new EPC contract for Anadarko Mozambique project, in which the Co. will have a share of around USD 6bln. Finally, Hikma Pharmaceuticals (-0.8%) are in negative territory as they are set to be removed from the FTSE 100.

Top European News

- Italy Commits to EU3.5b Annual Savings in Response to EU: Stampa

- Deutsche Bank’s DWS to Focus on Costs as Deals Prove Difficult

- Euro-Area Economy Extends Modest Growth With Help From Services

- Romanian Central Bank Mulls New Tools Amid Fastest EU Inflation

In FX, some divergence down under as RBNZ Deputy Governor Hawkesby intimates that rates may remain on hold for a while if not considerably longer in contrast to RBA Governor Lowe who inferred that more easing could be in the offing in addition to Tuesday’s 25 bp OCR cut. Hence, the Aud/Nzd cross has recoiled further from circa 1.0600 and through 1.0550, while the Kiwi is leading G10 gains vs a soggy Greenback after Fed chair Powell promised to support the US economy against a more pronounced slowdown yesterday. Nzd/Usd has tested resistance and offers around 0.6950, as Aud/Usd continues its rebound from pre-RBA lows to just over 0.7000 and into a heavy option expiry zone spanning 0.7005 to 0.7025 (1.7 bn). Note also, the Aussie needs to clear Fib resistance at 0.6995 convincingly and faces congested technical resistance between 0.7033-35 in the form of the 55 DMA and another Fib.

- USD – The aforementioned Dollar weakness has pushed the DXY back down below 97.000 and sub-the 100 DMA at 96.980 to a fresh 96.915 low amidst widespread losses vs major currency counterparts and EMs, bar the Yen and Rand. Technically, 96.745 is the next support level and fundamentally the focus switches to ADP ahead of Friday’s NFP, services surveys (Markit PMI and ISM) and more Fed speak.

- EUR/GBP/CAD/CHF – As noted above, all beneficiaries of the Buck’s demise, but with the single currency and Pound also gleaning some traction via better than expected services PMIs, on balance. Indeed, Eur/Usd has now surpassed the 100 DMA (1.1276) having narrowly missed the equivalent level on Tuesday and is eyeing 1.1300, while Cable seems more assured on the 1.2700 handle, albeit still lagging in Eur/Gbp cross terms within a 0.8855-80 range. Elsewhere, the Loonie has overcome 1.3400 and is filling hefty buying interest layered from 1.3370 to 1.3360, with the 100 DMA sitting just under 1.3350 at 1.3348, and the Franc has rebounded towards 0.9900 but underperforming vs the Euro in broad 1.1300-1.1250 parameters.

- JPY – In contrast to its major peers, the Yen has been undermined by the ongoing recovery in broad risk sentiment and is retesting recent 108.30+ lows vs the Dollar with decent expiries also within close proximity at 108.20-30 (1 bn) and 108.50-55 (1.1 bn).

- EM – While most of the region takes advantage of the Dollar’s downturn, more downbeat SA macro developments have hit the Rand and propped up Usd/Zar within 14.8240-6260 boundaries. The bad news kicked off with a sub-50 services PMI and continued via weaker business sentiment, while the ANC party’s ally has joined forces to back a wider SARB policy mandate prompting a dismissive response from the Bank itself.

In commodities, WTI (-0.7%) and Brent (-0.6%) prices are back on the decline as a surprise build in last night’s API exacerbated the recent downside seen amidst demand concerns. Stockpiles last week increased by 3.5mln barrels vs. an expected decline of 800k barrels. On the OPEC front, Russian Energy Minister Novak will be meeting his Saudi counterpart, Al-Falih, on June 10th to potentially discuss a date for the OPEC/OPEC+ meeting with no confirmation as of yet to whether it will take place at the end of June or early July. News-flow has been light for the complex thus far, with traders now eyeing the release of the weekly DoE crude stocks data in which the headline is expected to draw by 849k barrels. Elsewhere, Gold (+0.9%) is holding onto a bulk of its recent gains amid the weaker post-Powell USD whilst copper is set to notch a third straight day of gains on the back of a receding Buck, whilst alumina prices declined due to a demand halt as traders paused on spot purchases amid high prices.

US Event Calendar

- 8:15am: ADP Employment Change, est. 185,000, prior 275,000

- 9:45am: Markit US Services PMI, est. 50.9, prior 50.9; Composite PMI, prior 50.9

- 10am: ISM Non-Manufacturing Index, est. 55.4, prior 55.5

- 2pm: U.S. Federal Reserve Releases Beige Book

DB’s Jim Reid concludes the overnight wrap

I am still trying to get over the powerful conclusion to “Chernobyl” that aired in the UK last night. I’ve no idea if your country has the rights to it but if not move to somewhere that does. TV drama doesn’t get much better. It’s ironic that this great show ended the day after the new series of “Love Island” started. If your country hasn’t had an international version count yourself lucky! Back to Chernobyl and the only thing left to do is spend some time reading up on how much of it was true and how much of it was a dramatised version. I did this for the excellent “The Crown” and walked away feeling slightly cheated when I realised not all of it happened so it’s always a danger with stories based on real life.

How much truth there was in the big rally for markets yesterday and how much was dramatised is open for question. Indeed, the last 24 hours has seen a marked change in sentiment and although it’s hard to completely attribute the move to Powell’s comments at the Fed conference yesterday, the fact that the Chair seemingly didn’t push back on very dovish market pricing did at least fill investors with a bit more confidence. Indeed the +2.14% return for the S&P 500 was in fact the biggest since January while the recently battered NASDAQ rose +2.65% and FANGS +3.92% which at least helped to plaster over some of the recent damage to the sector.

In truth Powell didn’t provide a huge amount for the market to feed off however he did say in relation to “trade negotiations and other matters” that “we are closely monitoring the implications of these developments for the US economic outlook and, as always, we will act as appropriate to sustain the expansion, with a strong labour market and inflation near our symmetric 2% objective”. The reference to being prepared to “act as appropriate” was probably the most significant insofar as not pushing back on market pricing. The rest of Powell’s speech focused on longer term issues which our US economists summarised as being balanced in the assessment of ‘make-up’ inflation policies. He did not talk about new policy tools, e.g. negative rates, and he downplayed the significance of the dot plots.

Treasury yields were already higher prior to Powell speaking and finished the day slightly higher still, despite a brief knee-jerk drop lower as his comments hit the wires. Ten-year yields ended at 2.131% and +5.9bps on the day. At the short-end, 2y yields sold off +5.2bps and the most since April 1, making the 2s10s curve marginally steeper. It’s a bit puzzling that front-end rates rose despite the dovish tilt to Powell’s comments, but after parsing the price action, it turns out that the market is now pricing even higher odds of a cut by September, now at 93%. Powell’s willingness not to push back against this pricing and his dovish comments have likely raised expectations that the Fed will act promptly, which perversely lowers the odds that they need to cut rates even more steeply later in 2020. So two-year yields rising in this case may actually be completely consistent with the market’s perception of Powell being dovish. Well that’s the only way we can explain the price action and the narrative together.

The USD (-0.07%) was little changed despite the Fed noise and some new political headlines, which goes to show how much is already priced in. Democratic Presidential Candidate Elizabeth Warren released a plan aimed at “more actively managing our currency value” in an effort to boost American manufacturing. This drew some attention, but did not move markets given the early stage of the primary campaign. Still, it seems like the political consensus for a weaker dollar is growing in a bipartisan way.

In Europe Bund yields stubbornly failed to take part in the bond sell-off with 10y yields actually edging -0.7bps lower in yield to a fresh closing low (-0.210%) covering all of human existence and probably through the lives of the dinosaurs and beyond too. Indeed the divergence in moves between treasuries and bunds was its sharpest of the year, for both 10- and 30-year paper. Elsewhere in Europe, BTPs rallied -4.4bps as risk-on dominated, with sentiment also boosted by constructive comments from Deputy PM Di Maio, who downplayed the recent stories about disagreements within the coalition by saying he is open to the Northern League’s proposed flat tax and devolution measures. Staying with Italy, the risk of the Commission recommending an Excessive Deficit Procedure as soon as today has increased significantly of late but our economists continue to believe it is more likely in Q4 after the 2020 draft budget, as they highlight in their report here . In any case it’s one to watch.

Back to the risk-on. It wasn’t just Powell’s comments yesterday which seemed to help. Mexico’s Foreign Minister said that there’s an 80% chance that Mexico and the USA will find common ground – which helped the Mexican Peso to strengthen +1.08% – while the Senate leadership from both parties pushed back against the tariffs. Majority Leader McConnell said that there is “not much support” for the new duties among Republican lawmakers, and Democratic Leader Schumer added that Trump “likely won’t follow through.” Auto stocks led gains in both Europe and the US, rallying +3.09% and +4.65%, respectively. Overnight, however, President Trump doubled down, saying his plan was “no bluff,” which caused the peso to give back about 0.35% of its gains. In addition, China’s Commerce Ministry put out a statement saying that China hopes the US will meet China halfway. As always with these headlines it’s hard to know how much weight was behind them but it at least acted as a temporary circuit breaker, especially given that China had also issued a warning to citizens travelling to the US which wasn’t a good sign.

Staying with trade, overnight the US Treasury Department confirmed that Treasury Secretary Mnuchin will meet Chinese central bank Governor Yi Gang during a gathering of G-20 finance ministers from this Friday to Sunday in Japan, which should add as the next focal point for markets. This comes as reports also hit that China has fined Ford’s main China venture for antitrust violations. Elsewhere, Chinese President Xi Jinping gave a reasonably good assessment of the country’s economy in an interview with Russian media including Tass saying, while the global economy and trade have slowed down, China’s economy has stayed in a reasonable range in 2019, with stable growth, increasing employment, rising incomes and stable prices. He also said, China has “sufficient conditions, ability and confidence” to cope with various risks.

Markets in Asia are following Wall Street’s lead this morning with the Nikkei (+1.76%), Hang Seng (+0.72%), Shanghai Comp (+0.63%) and Kospi (+0.31%) all up. The more modest gains in China however may partly reflect the Caixin services PMI which printed at 52.7 (vs. 54.0 expected) and the lowest since February 2019. As you’ll see in the day ahead the remaining global services PMIs are due out today.

Moving on. Prior to Powell, the Chicago Fed’s Evans had sounded fairly balanced, saying that the economy is “doing well” and “the consumer is solid” but also that he was “nervous” about “inflation underrunning 2%”. On the current very dovish market pricing, Evans also responded by saying that “it suggests the market sees something that I haven’t yet seen in the national data”. So no endorsing of cutting rates yet but suggesting that he will need to see the impact in the data to lean towards justifying easing. After Powell, Vice Chair Clarida largely repeated the same message, saying the economy is in a good place but that tariff uncertainty will need to be taken into account. He said that if the Fed senses growth slowing, they will respond appropriately and cited the 1995 and 1998 “insurance cut” episodes as a possible roadmap. He also responded to a question about the yield curve by saying “if the yield curve inverts as it has and if it persists for some time, that’s obviously something I would definitely take seriously.”

It’s worth making the point that there is still a fairly steady stream of Fed speakers this week – including Clarida again today – however that will be the final chance for the market to digest officials’ latest views before the Fed hits their blackout period from next week before the Fed meeting outcome on the 19th.

Meanwhile in Europe there was more disappointment in the latest inflation data which showed that May core CPI was 0.8% yoy, and one-tenth below consensus. Our economists forecast core CPI to hover around 0.8-0.9% for the next few months before rising back towards 1.0% at the end of the summer. Finally in the UK the May construction PMI followed the manufacturing reading in slumping last month, to 48.6 (vs. 50.6 expected) and nearly 2pts lower than April. That puts both readings in contractionary territory and puts the focus on today’s services reading.

Finally, in other news, the World Bank cut its global growth forecast to 2.6% this year (vs. 2.9% previously) and 2.7% next year. The World Bank President David Malpass said in a call with reporters that “there’s been a tumble in business confidence, a deepening slowdown in global trade and sluggish investment in emerging and developing economies,” while adding, “momentum remains fragile.”

Looking at the day ahead, this morning the focus will be on those remaining services and composite PMIs in Europe with a first look also at the data for the non-core and UK. Not long after we get the April PPI and retail sales reports for the Euro Area. This afternoon in the US we’ve got the May ADP employment change reading, PMIs and May non-manufacturing ISM. The Fed’s Beige Book is also due out tonight while the scheduled Fed speakers include Clarida, Bowman and Bosic. The BoE’s Ramsden is also due to speak this morning. Away from that China’s Xi Jinping departs for a two-day visit to Russia while President Trump is due to meet Irish PM Varadkar.

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 0.86 POINTS OR 0.03% //Hang Sang CLOSED UP 133.92 POINTS OR 1.80% /The Nikkei closed UP 367.56 POINTS OR 1.80%//Australia’s all ordinaires CLOSED UP .42%

/Chinese yuan (ONSHORE) closed DOWN at 6.9091 /Oil DOWN TO 52.49 dollars per barrel for WTI and 60.38 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.9091 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9206 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China

The USA braces for Chinese retaliation as they scramble to find alternative to rare earth suppliers. China supplies 80% of the rare earths

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i) ITALY

This is big!! Italian stocks and bonds slide after the EU officially triggers disciplinary action over |Italy;s large Debt which now stands at 132% /GDP heading towards 135% due to the high 2.5% deficit in this years spending. Strangely Brussels is now going to sanction Italy 3.5 billion euros for being consistently offside. Expect a full war between Italy and Brussels and this may be the signal that Salvini wishes for as he really wants to leave the Euro and then that will collapse all the European banks

(courtesy zeorhedge)

Italian Stocks, Bonds Slide After EU Triggers Disciplinary Process Over Public Debt

It’s not just the trade war of 2018 that is back: as of moments ago, the feud between Italy and EU over the Mediterranean country’s soaring debt (and spending) which sent Italian bond yields soaring last year, only to fade away as Brussels conceded to vague promises from Rome, is now officially back and moments ago Italian stocks, bonds and the Euro all slumped after the EU’s executive arm formally took the first step toward “disciplining” Italy over its failure to rein in its debt, setting up a clash with the government in Rome and paving the way for an initial penalty of as much as €3.5 billion.

In a report published Wednesday, the European Commission said Italy hasn’t made sufficient progress in reducing its mountain of debt in line with the bloc’s fiscal rules, and now expects Italy’s debt ratio to rise in both 2019 and 2020, up to over 135%, due to a large debt-increasing “snowball” effect, and that a disciplinary process is “warranted”.

“Italy’s public debt remains a major source of vulnerability for the economy,” the commission said in its report. The ratio of the nation’s debt to gross domestic product will “rise in both 2019 and 2020, up to over 135%, due to a large debt-increasing ‘snowball’ effect, a declining primary surplus, and underachieved privatization proceeds,” according to the report. “While refinancing risks remain limited in the short term, the high public debt remains a source of vulnerability for Italy’s economy,” the commission added.

Additionally, in its damning report, the commission says that Italy made only limited progress in tackling tax evasion and improving market-based access to finance. “There has been no progress in shifting taxation away from productive factors, in reducing the share of old-age pensions in public spending (and indeed there has even been some backtracking in that field), in reducing trial length in civil justice, and in addressing restrictions on competition,” the commission said.

The step marks an escalation of the country’s budget tussle that roiled markets at the end of 2018 and is a warning for Italy’s populist leaders, particularly Deputy Premier Matteo Salvini who has vowed to change EU budget rules.

As Bloomberg notes, the commission’s move is just one step in a complicated process, which requires EU governments to weigh in several times, and while any fine would be relatively small, an official reprimand from the bloc could spell further trouble for Italy, “which is already buffeted by financial markets and plagued by tensions between the anti-establishment Five Star Movement and the anti-migration League, which are in a tenuous ruling coalition.”

EU finance chiefs would also have to say whether they agree with the commission’s proposal, most likely at their next gathering in early July.

What happens then is a paradox: after being punished for having too much debt, the EU will fine Italy several billions in euros, forcing Rome to incur even more debt! Specifically, at that point the commission will have 20 days to say whether a “non-interest bearing deposit” of up to 0.2% of gross domestic product — around 3.5 billion euros — should be demanded from Italy. If Italy fails to comply with the EU’s recommendations on reducing its debt – which it will – it could face even higher sanctions.

While the EU has started such procedures for other countries, it has never done so on the basis of excessive debt. It has also never actually fined any country, opting to set other sanctions for countries breaching fiscal rules at zero.

Even if Italy eventually evades a financial penalty, the stigma of the disciplinary process casts a shadow over its engagement with EU business and may reduce the Italian government’s leverage in everything from the scramble for European Central Bank board seats to its ability to negotiate politically thorny issues in Brussels.

Besides the purely monetary considerations, the Brussels escalation sets up a dilemma for Salvini and his fellow-Deputy Premier Luigi Di Maio. Salvini and Di Maio will have to establish how far to go in defying Brussels over the 2020 budget, which must be drafted in the fall. It’s also likely to exacerbate tensions in the coalition. Salvini insisted on renegotiating EU rules after Prime Minister Giuseppe Conte – who threatened Monday to resign if Salvini and Di Maio don’t stop electioneering – said that the rules “remain in force until we manage to change them.”

Italy’s debt ratio rose to 132.2% in 2018, and under Rome’s current plan is expected to reach 133.7% of GDP this year and 135.2% in 2020, according to the commission’s forecasts, which predict a higher debt-to-GDP ratio than the Italian government’s projections.

In what will likely be a self-fulfilling prophecy, the commission’s report warned that Italy is exposed to sudden increases in “financial market risk aversion due to still large rollover needs (around 17% of GDP in 2019) related to its large public debt” which can “lead to high volatility in sovereign bond markets and substantially higher debt servicing costs, with the subsequent risk of negative spillovers to the banking sector and to financing conditions for firms and households.”

And while Italy’s deficit is well within the 3% limit, the commission has demanded smaller gaps for the country to bring down its debt load, which at more than 130% of GDP is second only to Greece within Europe. Under EU rules, no country should have a budget deficit larger than 3% of gross domestic product or debt above 60% of output; any country outside of those limits must set annual targets to show they’re moving in the right direction.

Finally, for those asking if the move is objective and justified or purely political, here is the answer:

- EU SAYS FRENCH SPENDING DOESN’T WARRANT DISCIPLINARY ACTION

In kneejerk response, the news sent Italian yields higher…

the Euro lower, and Italian stocks plunging like a rock.

end

The atomic blast has just been delivered. Italy is now poised to issue a Euro parallel currency called a Mini bot. You can say that it is the forerunner to a newly introduced Lira.

I have been telling you for the past several years the problem facing the ECB and Germany with respect to the Target 2 imbalances. Germany is owed 1 trillion euros from the likes of Italy and Spain (also Portugal). If Italy walks and forms the Lira then the rest of the EU must share according to their GDP percentages part of the debt including Italy at 17% and surely they will not pay. Also Greece and Portugal and Spain will not pay. Then the only solution is for the ECB to print 1 trillion euros and pay Germany. That will cause gold and silver to skyrocket and send the euro tumbling to nothing.

Italy points out that France is in worse shape than Italy and they have been having constant deficits since the start of the Euro scheme.

I would say that Italy that the upper hand.

(courtesy Mish Shedlock)

Brace For Impact: Italy Poised To Launch Euro Parallel Currency

Authored by Mike Shedlock via MishTalk,

Italy faces an “Excessive Deficit” ruling, the first in EU history. Italy’s response is to revive a parallel currency proposal.

A euro crisis has been brewing for years.

Eurozone officials and the ECB have long held the upper hand vs individual countries like Greece and Portugal.

However, Italy now has the upper hand, if it chooses to wage war.

Let’s backup and start from the beginning to tie this story together.

Excessive Debt

Please consider EU Could Slap 3 Billion Euro Fine on Italy for Excessive Debt.

The European Commission could impose a 3 billion euro fine on Italy for breaking EU rules due to its rising debt and structural deficit levels, the country’s Deputy Prime Minister Matteo Salvini said on Tuesday.

Salvini, whose far-right League party triumphed in European elections on Sunday, said he would use “all my energies” to fight what he said were outdated and unfair European fiscal rules.

“Let’s see if we get this letter where they give us a fine for debt accumulated over the past and tell us to pay 3 billion euros,” Salvini said in an interview with RTL radio.

What About France?

Daniel Lacalle

✔@dlacalle_IA

While everyone is talking about Italy and its budget deficit, France has not had a balanced budget since the late 70s,

France vs Italy Key Points

- The current debate is over excessive debt, not deficits.

- Italy is in defiance of debt, not deficit rules, but its proposed budget will violate both.

- France violates both sets of numbers already, but not by as much.

- In essence, there is one set of rules for France and Germany and another set of rules for everyone else.

Parallel Currency Proposal

Please consider Italy to Activate its ‘Parallel Currency’ in Defiant Riposte to EU Ultimatum.

“I don’t govern a country on its knees,” said Matteo Salvini after sweeping the European elections even more emphatically than the Brexit party. Note the majestic ‘I’. He is already master of Rome.

The Lega strongman can no longer be contained, even by Italy’s ever-ingenious mandarin class. His party commands 40pc of the country together with eurosceptic confederates from the Brothers of Italy. It has erupted like a volcano in the Bourbon territories of the Mezzogiorno, now on the front line of migrant flows and left to fend for itself by Europe. Salvini can force a snap-election at any time.

By some maniacal reflex the dying Commission of Jean-Claude Juncker has chosen this moment to draw up the first indictment letter of the revamped debt and deficits regime. Italy faces €3.5bn of fines for failure to tighten its belt. It has 48 hours to respond.